NAREIT Institutional Investor Conference

June 2004

Why ANL Today?

• Both a value and a growth company

– Visibility of organic growth over 3-5 year horizon

• Demographic focus on 55+

• Growth through internal build-out; plus future acquisition strategy

• Focus on active adult market – rent securitized by high value homes and growth of customer base

2

Manufactured Housing Today In ANL Portfolio

• Community designs that value “residential appearance”:

– Curvilinear road patterns

– Larger lots/lower density

– Sidewalks and street lights

– Lots “with a view”

• Quality homes

– Average sales price >$ 100,000

– 3 bedroom models

– Garages replacing carports

3

Quality Homes Made Affordable Through Manufacturing

4

Communities & Subdivisions –Not Trailer Parks

Riverside Club Savanna Club

5

Amenitized Communities

• Clubhouse focus

• Golf courses

• Marinas

• Fitness/Social Center

• Curvilinear streets

• Landscaping

• Quality homes provide visibility on quality of future residents

6

The Manufactured Housing Sector Model

• Leasing land for residential use to tenants who have an investment in improvements to the land

• Provides a form of common interest development while maintaining single family home format

• Land lease community owners benefit from:

– Diversity of tenant base

– Lower recurring capital requirements as compared to other residential asset classes

– Lower tenant turnover as compared to other residential asset classes

7

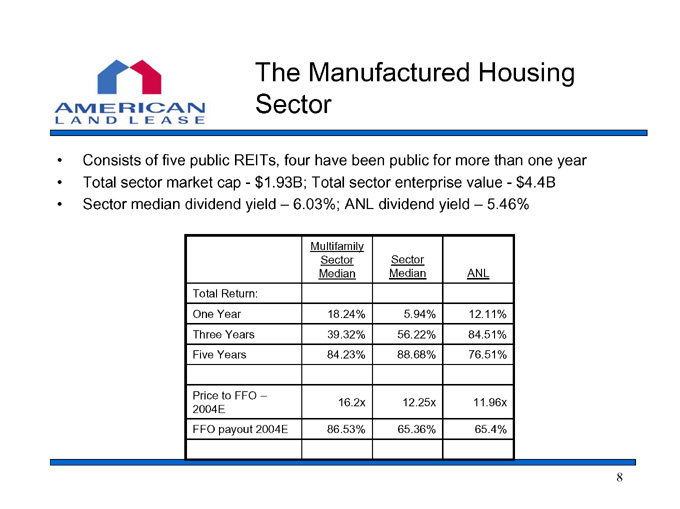

The Manufactured Housing Sector

• Consists of five public REITs, four have been public for more than one year

• Total sector market cap—$1.93B; Total sector enterprise value—$4.4B

• Sector median dividend yield – 6.03%; ANL dividend yield – 5.46%

Multifamily

Sector Sector

Median Median ANL

Total Return:

One Year 18.24% 5.94% 12.11%

Three Years 39.32% 56.22% 84.51%

Five Years 84.23% 88.68% 76.51%

Price to FFO –

16.2x 12.25x 11.96x

2004E

FFO payout 2004E 86.53% 65.36% 65.4%

8

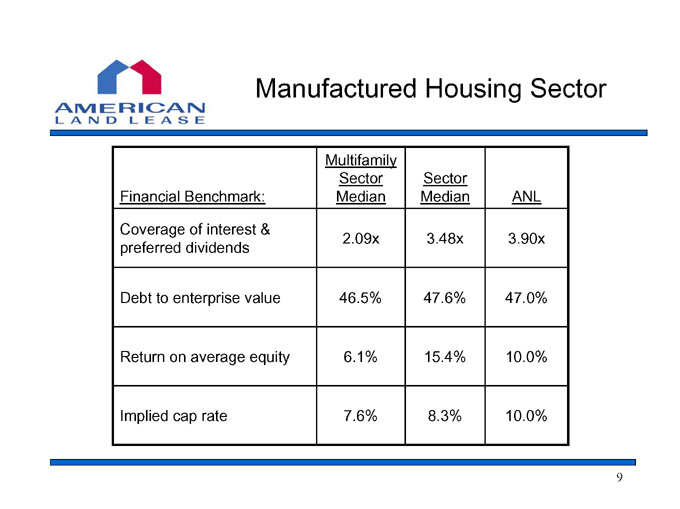

Manufactured Housing Sector

Multifamily

Sector Sector

Financial Benchmark: Median Median ANL

Coverage of interest &

2.09x 3.48x 3.90x

preferred dividends

Debt to enterprise value 46.5% 47.6% 47.0%

Return on average equity 6.1% 15.4% 10.0%

Implied cap rate 7.6% 8.3% 10.0%

9

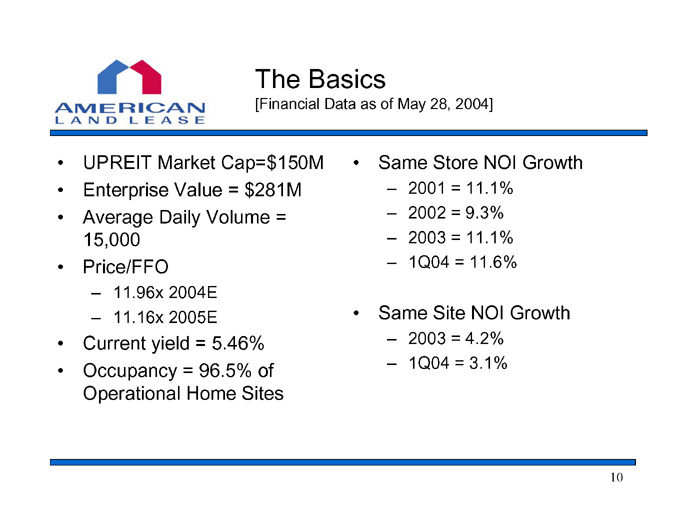

The Basics

[Financial Data as of May 28, 2004]

• UPREIT Market Cap=$150M

• Enterprise Value = $281M

• Average Daily Volume = 15,000

• Price/FFO

– 11.96x 2004E

– 11.16x 2005E

• Current yield = 5.46%

• Occupancy = 96.5% of Operational Home Sites

• Same Store NOI Growth

– 2001 = 11.1%

– 2002 = 9.3%

– 2003 = 11.1%

– 1Q04 = 11.6%

• Same Site NOI Growth

– 2003 = 4.2%

– 1Q04 = 3.1%

10

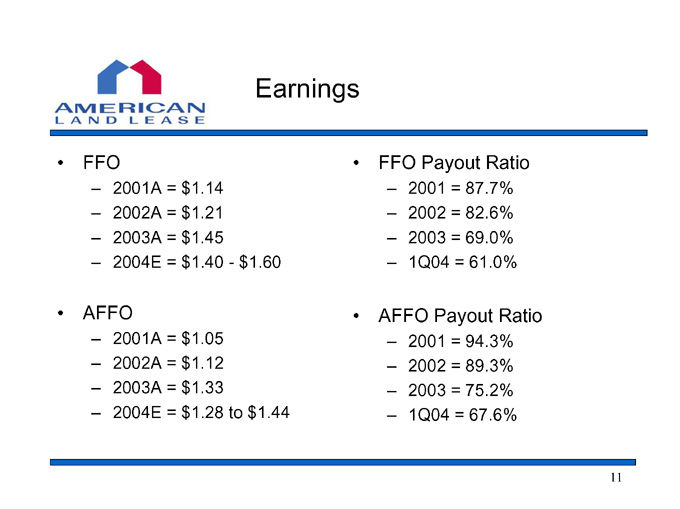

Earnings

• FFO

– 2001A = $1.14

– 2002A = $1.21

– 2003A = $1.45

– 2004E = $1.40—$1.60

• AFFO

– 2001A = $1.05

– 2002A = $1.12

– 2003A = $1.33

– 2004E = $1.28 to $1.44

• FFO Payout Ratio

– 2001 = 87.7%

– 2002 = 82.6%

– 2003 = 69.0%

– 1Q04 = 61.0%

• AFFO Payout Ratio

– 2001 = 94.3%

– 2002 = 89.3%

– 2003 = 75.2%

– 1Q04 = 67.6%

11

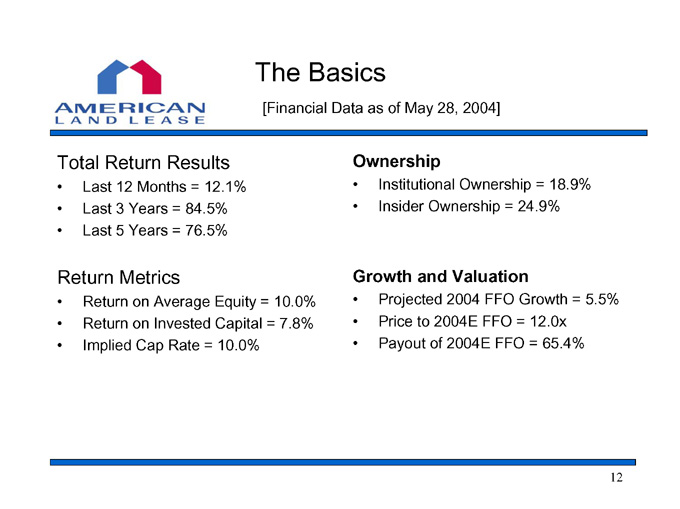

The Basics

[Financial Data as of May 28, 2004]

Total Return Results

• Last 12 Months = 12.1%

• Last 3 Years = 84.5%

• Last 5 Years = 76.5%

Return Metrics

• Return on Average Equity = 10.0%

• Return on Invested Capital = 7.8%

• Implied Cap Rate = 10.0%

Ownership

• Institutional Ownership = 18.9%

• Insider Ownership = 24.9%

Growth and Valuation

• Projected 2004 FFO Growth = 5.5%

• Price to 2004E FFO = 12.0x

• Payout of 2004E FFO = 65.4%

12

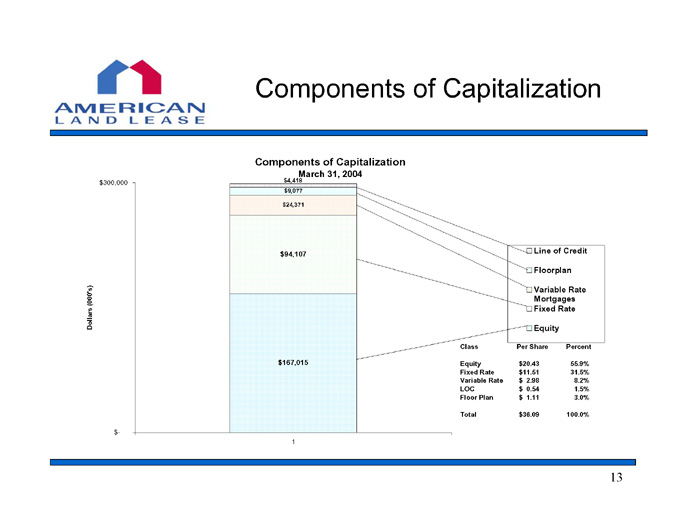

Components of Capitalization

Components of Capitalization

March 31, 2004

$4,418 Line of Credit

$9,077 Floorplan

$24,371 Variable Rate Mortgages

$94,107 Fixed Rate

$167,015 Equity

Class Per Share Percent

Equity $ 20.43 55.9%

Fixed Rate $ 11.51 31.5%

Variable Rate $ 2.98 8.2%

LOC $ 0.54 1.5%

Floor Plan $ 1.11 3.0%

Total $ 36.09 100.0%

13

Strength Behind the Balance Sheet

• Company led by Terry Considine – CEO/Chairman of ANL and AIV

• Strong “same store” results from core operating properties

• Beneficiary of “recession resistant” property class

• Financing using primarily fully amortizing mortgages:

– NAV increase through principal reduction

– Minimize interest rate risk

• Demographic support of asset class

• Quality asset locations

14

Value & Growth Company

Value Company:

• Sustaining community operations

• Increasing NOI growth through rental increases and expense control

• Tax efficient dividend yield

• Quality Core portfolio

Growth Company:

• Ability to grow the company 50% through internal assets

• Demonstrated competency in land development and home sale operations

• Maximize operating leverage gained through community expansion

15

Four Elements of the ANL Business

1. Land Lease Operations

2. Home Sales Operations

3. Land Development Operations

4. Investment Operations

16

Property Management Strategy

• Improve operating results from property management business.

– Centralized financial control and uniform operating procedures.

– Localized property management decision-making and market knowledge.

Operations are supervised by three Regional Managers – Two in Florida and one in Arizona.

Large development projects have high quality, full time, on-site Project Managers.

17

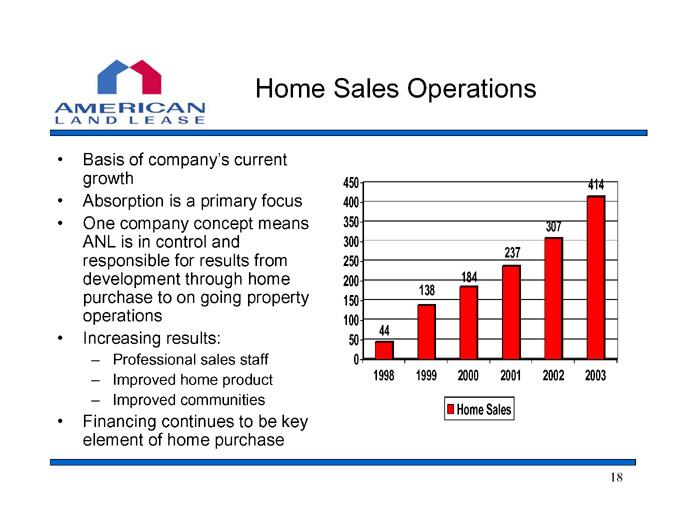

Home Sales Operations

• Basis of company’s current growth

• Absorption is a primary focus

• One company concept means

ANL is in control and responsible for results from development through home

purchase to on going property operations

• Increasing results:

– Professional sales staff

– Improved home product

– Improved communities

• Financing continues to be key element of home purchase

44 1998

138 1999

184 2000

237 2001

307 2002

414 2003

Home Sales

18

Land Development

• Turning land into income

• Expanding communities where the value and quality is known

• Development as a core competency

• Creation of value and increased NAV through execution of development plans

• Adding one high quality home community annually

Riverside Club

19

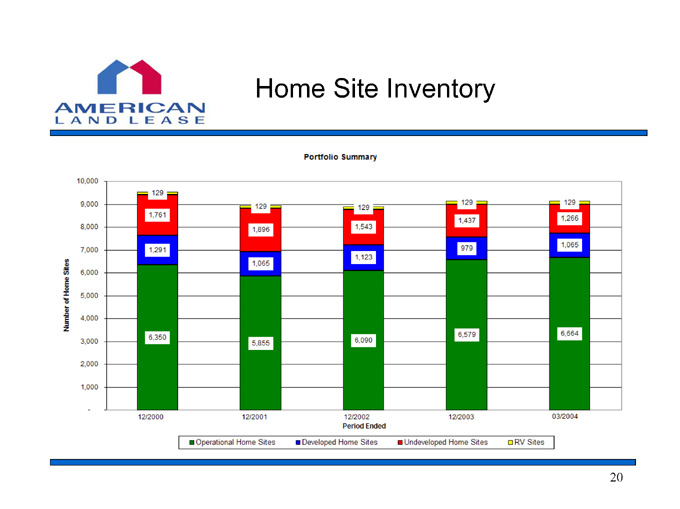

Home Site Inventory

20

Investment Operations

• Current focus is on investment into development of currently held property assets

• Additional focus has been on company restructuring –investment in future operating performance and expansion ability

• Evaluate property financing and seek to use effectively to expand available funds

• High quality properties available for sale are few and far between – even fewer at good prices

• Continue to look towards discipline to “buy right”

21

Building NAV

• Consistent NOI growth within stabilized communities

• Increasing absorption through focused home sales efforts

• Development of land assets

• Scheduled maturities of long term debt

• Accretive acquisition strategy

• Disposition of under performing assets and deployment of capital to development and acquisition activities

22

Points of Contact

Bob Blatz

President and Chief Operating Officer Shannon Smith Chief Financial Officer 29399 US Hwy 19N, Ste 320 Clearwater, FL 33761

Phone: (727) 726-8868 – Bob ext 116/Shannon ext 124 Fax: (727) 726-6788 Email: robert.blatz@americanlandlease.com shannon.smith@americanlandlease.com

23