UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form 10-K

(Mark One)

x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended September 30, 2014

OR

¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

Commission File Number 001-12488

Powell Industries, Inc.

(Exact name of registrant as specified in its charter)

Delaware | | 88-0106100 |

(State or other jurisdiction of incorporation or organization) | | (I.R.S. Employer Identification No.) |

8550 Mosley Road Houston, Texas | | 77075-1180 |

(Address of principal executive offices) | | (Zip Code) |

Registrant’s telephone number, including area code:

(713) 944-6900

Securities registered pursuant to section 12(b) of the Act:

Common Stock, par value $.01 per share

Securities registered pursuant to Section 12(g) of Act:

None

Indicate by check mark whether the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. ¨ Yes x No

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. ¨ Yes x No

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. x Yes ¨ No

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Date File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). x Yes ¨ No

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§232.405 of this chapter) is not contained herein and will not be contained, to the best of the registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

¨ Large accelerated filer | | x Accelerated filer | | ¨ Non-accelerated filer | | ¨ Smaller reporting company |

| | (Do not check if a smaller reporting company) |

Indicate by check mark whether the registrant is a shell company (as defined in Exchange Act Rule 12b-2). ¨ Yes x No

The aggregate market value of the common stock held by non-affiliates of the registrant was approximately $375 million as of March 31, 2014, based upon the closing price on the NASDAQ Global Market on that date. For purposes of the calculation above only, all directors, executive officers and beneficial owners of 5% or more are considered to be “affiliates.”

At November 28, 2014, there were 12,031,243 outstanding shares of the registrant’s common stock, par value $0.01 per share.

Documents Incorporated By Reference

Portions of the registrant’s definitive Proxy Statement for the 2015 annual meeting of stockholders to be filed not later than 120 days after September 30, 2014, are incorporated by reference into Part III of this Form 10-K.

POWELL INDUSTRIES, INC.

TABLE OF CONTENTS

2

CAUTIONARY STATEMENT REGARDING FORWARD-LOOKING STATEMENTS;

RISK FACTORS

Unless otherwise indicated, all references to “we,” “us,” “our,” “Powell” or “the Company” include Powell Industries, Inc. and its consolidated subsidiaries.

Forward-Looking Statements

This Annual Report on Form 10-K (Annual Report) includes forward-looking statements based on our current expectations, which are subject to risks and uncertainties. Forward-looking statements include information concerning future results of operations and financial condition. Statements that contain words such as “believes,” “expects,” “anticipates,” “intends,” “estimates,” “continue,” “should,” “could,” “may,” “plan,” “project,” “predict,” “will” or similar expressions may be forward-looking statements. These forward-looking statements are subject to risks and uncertainties, and many factors could affect the future financial results and condition of the Company. Factors that may have a material effect on our revenues, expenses and operating results include adverse business or market conditions, our ability to meet our customers’ scheduling requirements, our customers’ financial conditions and their ability to secure financing to support current and future projects, the availability and cost of materials from suppliers, availability of skilled labor force, adverse competitive developments and changes in customer requirements as well as those circumstances discussed under “Item 1A. Risk Factors,” below. Accordingly, actual results may differ materially from those expressed or implied by the forward-looking statements contained in this Annual Report. Any forward-looking statements made by or on our behalf are made pursuant to the safe harbor provisions of the Private Securities Litigation Reform Act of 1995.

The forward-looking statements contained in this Annual Report are based on current assumptions that we will continue to develop, market, manufacture and ship products and provide services on a competitive and timely basis; that competitive conditions in our markets will not change in a materially adverse way; that we will accurately identify and meet customer needs for products and services; that we will be able to hire and retain skilled laborers and key employees; that our products and capabilities will remain competitive; that the financial markets and banking systems will remain stable and availability of credit will continue; that risks related to shifts in customer demand are minimized and that there will be no material adverse change in the operations or business of the Company. Assumptions relating to these factors involve judgments that are based on available information, which may not be complete, and are subject to changes in many factors beyond the Company’s control that can materially affect results. Because of these and other factors that affect our operating results, past financial performance should not be considered an indicator of future performance, and investors should not use historical trends to anticipate results or trends in future periods.

3

PART I

Item 1. Business

Overview

Powell Industries, Inc. was incorporated in the state of Delaware in 2004 as a successor to a Nevada company incorporated in 1968. The Nevada corporation was the successor to a company founded by William E. Powell in 1947, which merged into the Company in 1977. We are headquartered in Houston, Texas, and our major subsidiaries, all of which are wholly owned, include: Powell Electrical Systems, Inc.; Powell (UK) Limited (formerly Switchgear & Instrumentation Limited); Powell Canada Inc. and Powell Industries International, B.V.

Our website is powellind.com. We make available, free of charge on or through our website, copies of our Annual Reports on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K and amendments to those reports filed or furnished pursuant to Section 13(a) or 15(d) of the Securities Exchange Act of 1934 as soon as reasonable after we electronically file such material with, or furnish it to, the Securities and Exchange Commission (SEC).

We develop, design, manufacture and service custom-engineered equipment and systems for the distribution, control and monitoring of electrical energy designed to (1) distribute, monitor and control the flow of electrical energy and (2) provide protection to motors, transformers and other electrically powered equipment. Our principal products include integrated power control room substations (PCRs®), custom-engineered modules, electrical houses (E-Houses), traditional and arc-resistant distribution switchgear and control gear, medium-voltage circuit breakers, monitoring and control communications systems, motor control centers and bus duct systems. These products are designed for application voltages ranging from 480 volts to 38,000 volts and are used in oil and gas refining, offshore oil and gas production, petrochemical, pipeline, terminal, pulp and paper, mining and metals, light rail traction power, electric utility and other heavy industrial markets. Our product scope includes designs tested to meet both U.S. standards (ANSI) and international standards (IEC). We assist customers by providing value-added services such as spare parts, field service inspection, installation, commissioning, modification and repair, retrofit and retrofill components for existing systems and replacement circuit breakers for switchgear that is obsolete or that is no longer produced by the original manufacturer. We seek to establish long-term relationships with the end users of our systems as well as the design and construction engineering firms contracted by those end users.

References to Fiscal 2014, Fiscal 2013 and Fiscal 2012 used throughout this Annual Report on Form 10-K relate to our fiscal years ended September 30, 2014, 2013 and 2012, respectively.

Revenues from customers located in the United States of America (U.S.) accounted for approximately 56%, 58% and 56% of our consolidated revenues for Fiscal 2014, 2013 and 2012, respectively. Revenues from customers located in Canada accounted for approximately 21%, 18% and 13% of consolidated revenues for Fiscal 2014, 2013 and 2012, respectively. Approximately 64% of our long-lived assets were located in the U.S. at September 30, 2014, with the remaining long-lived assets located primarily in the United Kingdom (U.K.) and Canada. Detailed geographic information is included in Note L of the Notes to Consolidated Financial Statements included elsewhere in this Annual Report.

We previously reported two business segments: Electrical Power Products and Process Control Systems. In January 2014, we sold our wholly owned subsidiary Transdyn Inc. (Transdyn) which was reported in our Process Controls business segment. We reclassified the assets and liabilities of Transdyn as held for sale within the accompanying consolidated balance sheet as of September 30, 2013, and presented the results of these operations as income from discontinued operations, net of tax, for each of the accompanying consolidated statements of operations. While this sale did not result in a material disposition of assets or material reduction to income before income taxes relative to our consolidated financial statements, the revenues, gross profit, income before income taxes and assets of Transdyn comprised a significant majority of those respective amounts previously reported in our Process Control Systems business segment. As we previously reported only two business segments, Electrical Power Products and Process Control Systems, we have removed the presentation of business segments in this Annual Report. Additionally, all current and historical financial information presented in this Annual Report excludes the financial information for Transdyn or presents it as discontinued operations where applicable. For more information about this disposition, see Note N of the Notes to Consolidated Financial Statements included elsewhere in this Annual Report.

Customers and Markets

Our principal customers are sophisticated users of large amounts of electrical energy that typically require a complex combination of electrical components and systems. These customers and their industries include oil and gas refining, offshore oil and gas production, petrochemical, pipeline, terminal, pulp and paper, mining and metals, light rail traction power and electric utility customers.

4

Products and services are principally sold directly to the end user or to an engineering, procurement and construction (EPC) firm on behalf of the end user. Each project is specifically engineered and manufactured to meet the exact specifications and requirements of the individual customer. Powell’s expertise is in the design and engineering, manufacturing, project management and integration of the various systems into a single deliverable (custom-engineered). We market and sell our products and services, which are typically awarded in competitive bid situations, to a wide variety of customers, governmental agencies, markets and geographic regions. Contracts often represent large-scale and complex projects with an individual customer. By their nature, these projects are typically nonrecurring. Thus, multiple and/or continuous projects of similar magnitude with the same customer may vary. As such, the timing of large project awards may cause material fluctuations in revenues and gross margins.

Due to the nature and timing of large projects, a significant percentage of revenues in a given period may result from one specific contract or customer. Although we could be adversely impacted by a significant reduction in business volume from a particular industry, we do not believe the loss of any specific customer would have a material adverse effect on our business. No customer accounted for more than 10% of our revenues in Fiscal 2014, Fiscal 2013 or Fiscal 2012.

Competition

We strive to be the supplier of choice for custom-engineered system solutions and services to a variety of customers and markets. Our activities are predominantly in the oil and gas and the electric utility industries, but also include other markets where customers need to manage, monitor and control large amounts of electrical energy. The majority of our business is in support of capital investment projects that are highly complex and competitively bid. Our customized systems are designed to meet the specifications of our customers. Each system is designed, engineered and manufactured to the specific requirements of the particular application. We consider our engineering, project management, systems integration and technical support capabilities vital to the success of our business.

We believe our products and services, turn-key integration capabilities, technical and project management strengths, application expertise and specialty contracting experience, together with our responsiveness and flexibility to the needs of our customers and financial strength, give us a sustainable competitive advantage in our markets. We compete with a small number of multinational competitors that sell to a broad industrial and geographic market and with smaller, regional competitors that typically have limited capabilities and scope of supply. Our principal competitors include ABB, Eaton, General Electric Company, Schneider and Siemens. The competitive factors used during bid evaluation by our customers vary from project to project and may include technical support and application expertise, engineering and manufacturing capabilities, equipment rating, delivered value, scheduling and price. While projects are typically non-recurring, a significant portion of our business is from repeat customers and many times involves third-party EPC firms hired by the end user and with which we also have long and established relationships. Ultimately, our competitive position is dependent upon our ability to provide quality custom-engineered products, services and systems on a timely basis at a competitive price.

Backlog

Backlog represents the dollar amount of revenue that we expect to realize from work to be performed on uncompleted contracts, including new contractual agreements on which work has not begun. Our methodology for determining backlog may not be comparable to the methodology used by other companies. Orders included in our backlog are represented by customer purchase orders and contracts, which we believe to be firm. Our backlog at September 30, 2014 totaled $507.1 million compared to $437.9 million at September 30, 2013. We anticipate that approximately $415 million of Fiscal 2014 ending backlog will be fulfilled during our fiscal year ending September 30, 2015. Projects may be delayed or cancelled for various reasons; accordingly, backlog may not be indicative of future operating results as orders in our backlog may be cancelled or modified by our customers.

Raw Materials and Suppliers

The principal raw materials used in our operations include steel, copper and aluminum and various electrical components. Material costs represented 48% of revenues in Fiscal 2014 compared to 46% in Fiscal 2013. Unanticipated increases in material requirements, disruptions in supplies or price increases could increase production costs and adversely affect our results of operations.

We purchase certain key electrical components on a sole-sourced basis and maintain a qualification and performance monitoring program to control risk associated with sole-sourced items. Changes in our design to accommodate similar components from other suppliers could be implemented to resolve a supply problem related to a sole-sourced component. In this circumstance, supply problems could result in delays in our ability to meet commitments to our customers. We believe that sources of supply for raw materials and components are generally sufficient, and we do not believe a shortage of materials will cause any significant adverse impact in the future. While we are not dependent on any one supplier for the majority of our raw materials, we are highly dependent on our suppliers in order to meet commitments to our customers. We have not experienced significant or unusual issues in the purchase of key raw materials or components in the past three fiscal years.

5

Our business is subject to the effects of changing material prices. During the last three fiscal years, we have not experienced significant price volatility for raw materials or component parts used in the production of our products. While the cost outlook for commodities used in the production of our products is not certain, we believe we can manage this volatility through contract pricing adjustments, with material-cost predictive estimating and by actively pursuing internal cost reduction efforts. We did not enter into any derivative contracts to hedge our exposure to commodity price changes in Fiscal 2014, 2013 or 2012.

Employees

At September 30, 2014, we had 2,940 full-time employees located primarily in the United States, the United Kingdom and Canada. Our employees are not represented by unions, and we believe that our relationship with our employees is good.

Intellectual Property

While we are the holder of various patents, trademarks, servicemarks, copyrights and licenses, we do not consider any individual intellectual property to be material to our consolidated business operations.

Item 1A. Risk Factors

Our business is subject to a variety of risks and uncertainties, including, but not limited to, the most significant risks and uncertainties described below. Additional risks and uncertainties not known to us or not described below may also impair our business operations. If any of the following risks actually occur, our business, financial condition, cash flows and results of operations could be harmed and we may not be able to achieve our goals. This Annual Report also includes statements reflecting assumptions, expectations, projections, intentions or beliefs about future events that are intended as “forward-looking statements” under the Private Securities Litigation Reform Act of 1995 and should be read in conjunction with the discussion under “Forward-Looking Statements,” above.

Economic uncertainty and financial market conditions may impact our customer base, suppliers and backlog.

Various factors drive demand for our products and services, including the price and demand for oil and gas, capital expenditures, economic forecasts and financial markets. Uncertainty regarding these factors could impact our customers and severely impact the demand for projects and orders for our products and services. If one or more of our suppliers or subcontractors experiences difficulties that result in a reduction or interruption in supply to us, or they fail to meet our manufacturing requirements, our business could be adversely impacted until we are able to secure alternative sources. Furthermore, our ability to expand our business would be limited in the future if we are unable to increase our bonding capacity or our credit facility on favorable terms or at all. These disruptions could lead to reduced demand for our products and services, could materially impact our business, financial condition, cash flows and results of operations and could potentially impact the trading price of our common stock.

Our backlog is subject to unexpected adjustments and cancellations and, therefore, may not be a reliable indicator of our future earnings.

We have a backlog of uncompleted contracts. Backlog represents the dollar amount of revenue that we expect to realize from work to be performed on uncompleted contracts, including new contractual agreements on which work has not begun. From time to time, projects are cancelled that appeared to have a high certainty of going forward at the time they were recorded as new business taken. In the event of a project cancellation, we may be reimbursed for certain costs but typically have no contractual right to the total revenue reflected in our backlog. In addition to our being unable to recover certain direct costs, cancelled projects may also result in additional unrecoverable costs due to underutilization of our assets.

The use of percentage-of-completion accounting on our fixed-price contracts could result in volatility in our results of operations.

As discussed in “Management’s Discussion and Analysis of Financial Condition and Results of Operations — Critical Accounting Policies and Estimates” and in the Notes to Consolidated Financial Statements included elsewhere in this Annual Report, the majority of our revenues are recognized on the percentage-of-completion method of accounting. Under the percentage-of-completion method of accounting, revenues are recognized as work is performed. The estimated completion to date is calculated by multiplying the total contract price by the percentage of performance to date, which is based on total costs or total labor dollars incurred to date compared to the total estimated costs or total labor dollars estimated at completion. The method used to determine the percentage of completion is typically the cost method, unless the labor method is a more accurate method of measuring the progress of the project. Application of the percentage-of-completion method of accounting requires the use of estimates of costs to be incurred for the performance of the contract. The cost estimation process is based upon the professional knowledge and experience of our engineers, project managers and financial professionals. Contract losses are recognized in full when determined, and estimates of revenue and cost to complete are adjusted based on ongoing reviews of estimated contract performance. Previously recorded estimates are adjusted as the project

6

progresses. In certain circumstances, it is possible that such adjustments could have a significant impact on our operating results for any fiscal quarter or year.

A portion of our contracts contain terms with penalty provisions.

Some of our contracts contain penalty provisions for the failure to meet specified contractual provisions. These contractual provisions define the conditions under which our customers may make claims against us.

Fluctuations in the price and supply of materials used to manufacture our products may reduce our profits and could materially impact our ability to meet commitments to our customers.

Our material costs represented 48% of our consolidated revenues for Fiscal 2014. We purchase a wide variety of materials and component parts to manufacture our products, including steel, aluminum, copper and various electrical components. Unanticipated increases in raw material requirements, changes in supplier availability or price increases could increase production costs and adversely affect profitability. Our ability to meet customer commitments could be negatively impacted due to the time and effort associated with the selection and qualification of a new supplier. Additionally, we rely on certain competitors for key materials used in our products. This could put us at risk if the relationships change or become adversarial.

Our industry is highly competitive.

Some of our competitors are significantly larger and have substantially greater resources. Competition in the industry depends on a number of factors, including technical ability, production capacity and price. Certain of our competitors may have lower cost structures and may, therefore, be able to provide their products or services at lower prices than we are able to provide. Similarly, we cannot be certain that we will be able to maintain or enhance our competitive position within our industry, maintain our customer base at current levels or increase our customer base.

Our operations could be adversely impacted by the effects of government regulations.

Changes in policy, laws or regulations regarding oil and gas exploration and development activities and decisions by customers and other industry participants could reduce demand for our services, which would have a negative impact on our operations. Various regulations have been implemented around the world related to safety and certification requirements applicable to oil and gas drilling and production activities and we cannot predict whether operators will be able to satisfy these requirements. Further, we cannot predict future changes in any country in which we operate and how those changes may affect our ability to perform projects in those regions.

Changes in tax laws and regulations may change our effective tax rate and could have a material effect on our financial results.

We are subject to income taxes in the United States and numerous foreign jurisdictions. A change in tax laws, deductions or credits, treaties or regulations, or their interpretation, in the countries in which we operate could result in a higher tax rate on our pre-tax income, which could have a material impact on our net income and cash flows from operations. We are regularly under audit by tax authorities, and our tax estimates and tax positions could be materially affected by many factors including the final outcome of tax audits and related litigation, the introduction of new tax accounting standards, legislation, regulations and related interpretations, our global mix of earnings, the realizability of deferred tax assets and changes in uncertain tax positions. A significant increase in our tax rate could have a material effect on our profitability.

In Fiscal 2013, we released a valuation allowance of $7 million recorded against our Canadian deferred tax assets. We believed it was more likely than not these deferred tax assets would be realized in future periods as taxable income is generated in Canada. Although in Fiscal 2014 our Canadian operations reported a loss, we still believe these deferred tax assets will be realized in the future periods. A valuation allowance, with a corresponding increase to deferred tax expense and thus a reduction in net income, may be required to be recorded against the deferred tax assets in the future if we do not generate income in Canada. The recognition of deferred tax assets requires estimates related to future income and other assumptions regarding timing and future profitability. Estimates may change as new events occur, additional information becomes available or operating environments change. If we were to record this valuation allowance in the future, it would have a material adverse effect on our profitability.

Our international operations expose us to risks that are different from, or possibly greater than, the risks we are exposed to domestically and may adversely affect our operations.

Revenues with customers located outside of the U.S., including sales from our operations in the United Kingdom and Canada, accounted for approximately 44% of our consolidated revenues in Fiscal 2014. While our manufacturing facilities are in developed

7

countries with historically stable operating and fiscal environments, our consolidated results of operations, cash flows and financial condition could be adversely affected by a number of factors, including: political and economic instability; social unrest, acts of terrorism, force majeure, war or other armed conflict; inflation; currency fluctuations, devaluations and conversion restrictions; governmental activities that limit or disrupt markets, restrict payments or limit the movement of funds and trade restrictions or economic embargoes imposed by the U.S. or other countries. Additionally, the compliance with foreign and domestic import and export regulations and anti-corruption laws, such as the U.S. Foreign Corrupt Practices Act, or similar laws of other jurisdictions outside the United States, could adversely impact our ability to compete for contracts in such jurisdictions. Moreover, the violation of such laws or regulations could result in severe penalties including monetary fines, criminal proceedings and suspension of export privileges.

Acquisitions involve a number of risks.

Our strategy has been to pursue growth and product diversification through the acquisition of companies or assets that will enable us to expand our product and service offerings. We routinely review potential acquisitions however we may be unable to implement this strategy. Acquisitions involve certain risks, including difficulties in the integration of operations and systems; failure to realize cost savings; the termination of relationships by key personnel and customers of the acquired company and a failure to add additional employees to handle the increased volume of business. Additionally, financial and accounting challenges and complexities in areas such as valuation, tax planning, treasury management and financial reporting from our acquisitions pose risks to our strategy. Due diligence may not reveal all risks and challenges associated with our acquisitions. It is possible that impairment charges resulting from the overpayment for an acquisition may negatively impact our results of operations. Financing for acquisitions may require us to obtain additional equity or debt financing, which, if available, may not be available on attractive terms.

Our operating results may vary significantly from quarter to quarter.

Our quarterly results may be materially and adversely affected by a number of factors including: changes in estimated costs or revenues under fixed-price contracts; the timing and volume of work under new agreements; general economic conditions; the spending patterns of customers; variations in the margins of projects performed during any particular quarter; losses experienced in our operations not otherwise covered by insurance; a change in the demand or production of our products and our services caused by severe weather conditions; a change in the mix of our customers, contracts and business; increases in design and manufacturing costs; the ability of customers to pay their invoices owed to us and disagreements with customers related to project performance on delivery. Accordingly, our operating results in any particular quarter may not be indicative of future results.

The departure of key personnel could disrupt our business.

We depend on the continued efforts of our executive officers, senior management and other key professionals. We cannot be certain that any individual will continue in such capacity for any particular period of time. The loss of key personnel, or the inability to hire and retain qualified employees, could negatively impact our ability to manage our business.

Our business requires skilled labor and we may be unable to attract and retain qualified employees.

Our ability to maintain our productivity and profitability will be limited by our ability to employ, train and retain personnel necessary to meet our requirements. We may experience shortages of qualified personnel such as engineers, project managers and select skilled trades. We cannot be certain that we will be able to maintain an adequate skilled labor force necessary to operate efficiently and to support our growth strategy and ramp of operations or that our labor expenses will not increase as a result of a shortage in the supply of skilled personnel. Labor shortages or increased labor costs could impair our ability to maintain our business, meet customer commitments or grow our revenues, and may adversely impact our results of operations.

Actual and potential claims, lawsuits and proceedings could ultimately reduce our profitability and liquidity and weaken our financial condition.

We could be named as a defendant in future legal proceedings that claim damages in connection with the operation of our business. Most of the actions against us arise out of the normal course of our performing services or manufacturing equipment. From time to time, we may be a plaintiff in legal proceedings against customers in which we seek to recover payment of contractual amounts due to us, as well as claims for increased costs incurred by us. When appropriate, we establish provisions against certain legal exposures, and we adjust such provisions from time to time according to ongoing developments related to each exposure. If in the future our assumptions and estimates related to such exposures prove to be inadequate or wrong, or our insurance coverage is insufficient, our consolidated results of operations, cash flows and financial condition could be adversely affected. In addition, claims, lawsuits and proceedings may harm our reputation or divert management resources away from operating our business.

8

Unforeseen difficulties with our enterprise resource planning (ERP), engineering and manufacturing process systems (Business Systems) could adversely affect our internal controls and our business.

The efficient execution of our business is dependent upon the proper functioning of our Business Systems that support our production, engineering, human resources, estimating, financial, project management and customer systems. Any significant failure or malfunction of our Business Systems may result in disruption of our operations. These systems may be susceptible to outages due to natural disaster, power loss, telecommunications failures, break-ins and similar events. Despite the implementation of network security measures, our systems may be vulnerable to security breaches such as computer viruses and similar disruptions from unauthorized tampering. The occurrence of these or other events could disrupt or damage our Business Systems and adversely affect our business or results of operations.

In Fiscal 2014, we re-implemented our existing ERP system and added a suite of new software tools to expand our Business Systems. These upgrades and enhancements were designed to standardize best process practices, drive efficiency and increase productivity across our organization. There can be no certainty that these Business Systems will deliver the expected benefits and the inability to do so may impact our ability to deliver on our commitment to our customers which could negatively impact our operations and may adversely impact our results of operations.

We carry insurance against many potential liabilities, but our management of risk may leave us exposed to unidentified or unanticipated risks.

Although we maintain insurance policies with respect to our related exposures, including certain casualty, property, business interruption, self-insured medical and dental programs, these policies contain deductibles, self-insured retentions and limits of coverage. We estimate our liabilities for known claims and unpaid claims and expenses based on information available as well as projections for claims incurred but not reported. However, insurance liabilities, some of which are self-insured, are difficult to estimate due to various factors. If any of our insurance policies or programs are not effective in mitigating our risks, we may incur losses that are not covered by our insurance policies, subject to deductibles, or that exceed our accruals or our coverage limits and could adversely impact our consolidated results of operations, cash flows and financial position.

Technological innovations by competitors may make existing products and production methods obsolete.

All of the products manufactured and sold by Powell depend upon the best available technology for success in the marketplace. This competitive environment is highly sensitive to technological innovation. It is possible for competitors (both domestic and international) to develop products or production methods that will make current products or methods obsolete or at least hasten their obsolescence; therefore, we cannot be certain that our competitors will not develop the expertise, experience and resources to provide products and services that are superior in both price and quality.

Catastrophic events could disrupt our business.

The occurrence of catastrophic events, ranging from natural disasters such as hurricanes, to health epidemics, to acts of war and terrorism, could disrupt or delay our ability to complete projects for our customers and could potentially expose us to third-party liability claims. Such events may or may not be fully covered by our various insurance policies or may be subject to deductibles or exceed coverage limits. In addition, such events could impact our customers and suppliers, resulting in temporary or long-term delays and/or cancellations of orders for raw materials used in normal business operations. These situations are outside our control and could have a significant adverse impact on our consolidated results of operations, cash flows and financial position.

Unforeseen difficulties with expansions or relocation of our existing facilities could adversely affect our operations.

From time to time we may decide to build additional facilities, expand our existing facilities or relocate or consolidate one or more of our operations. Challenges arising from the staffing, relocation or expansion of our facilities could adversely affect our operations and may adversely impact our profitability.

Due to the cyclical nature of the oil and gas industry, our business may be adversely impacted by extended periods of low oil or natural gas prices or unsuccessful exploration efforts which may decrease our customers’ spending and therefore our results in the future.

Oil and natural gas prices have been, and are expected to, remain volatile. This volatility causes oil and natural gas companies to change their strategies, delay or cancel projects. The price for oil and natural gas can be influenced by many factors, including global economic growth, inventory levels and supply and demand for these commodities. These factors could cause the oil and natural gas prices to decrease which could result in a decrease in projects with our customers that would adversely impact our business and our

9

results. No assurances can be given that extended periods of reduced oil and natural gas prices will not negatively impact our business and our consolidated results of operations and cash flows.

Item 1B. Unresolved Staff Comments

None.

10

Item 2. Properties

We own or lease manufacturing facilities, warehouse space, sales offices, field offices and repair centers located throughout the United States, Canada and the United Kingdom. Our facilities are generally located in areas that are readily accessible to materials and labor pools and are maintained in good condition. These facilities, together with recent expansions, are expected to meet our needs for the foreseeable future.

Our principal locations as of September 30, 2014, are as follows:

| | | | | | | Approximate

Square Footage | |

Location | Description | | | Acres | | | Owned | | | Leased | |

Houston, TX | Corporate office and manufacturing facility | | | | 21.4 | | | | 428,515 | | | | — | |

Houston, TX | Office and manufacturing facility | | | | 53.4 | | | | 290,554 | | | | — | |

Houston, TX | Office, fabrication facility and yard | | | | 63.3 | | | | 82,320 | | | | — | |

North Canton, OH | Office and manufacturing facility | | | | 8.0 | | | | 115,200 | | | | — | |

Northlake, IL | Office and manufacturing facility | | | | 10.0 | | | | 103,500 | | | | — | |

Bradford, United Kingdom | Office and manufacturing facility | | | | 7.9 | | | | 129,200 | | | | — | |

Acheson, Alberta, Canada | Office and manufacturing facility | | | | 20.1 | | | | 163,000 | | | | — | |

Acheson, Alberta, Canada | Office and service shop | | | | 3.5 | | | | — | | | | 44,248 | |

Edmonton, Alberta, Canada | Office and service shop | | | | 1.0 | | | | — | | | | 28,000 | |

Calgary, Alberta, Canada | Office and manufacturing facility | | | | — | | | | — | | | | 8,200 | |

All leased properties are subject to long-term leases. We do not anticipate experiencing significant difficulty in retaining occupancy of any of our leased facilities through lease renewals prior to expiration or through month-to-month occupancy, or in replacing them with equivalent facilities.

In Fiscal 2012, we acquired land in Houston, Texas, and in Acheson, Alberta, Canada, and began construction of two facilities to allow us to expand our operations. The construction of these two facilities was substantially completed in September 2013 and we relocated our operations and personnel from their existing leased facilities. We are in the process of expanding our manufacturing facility in Acheson, Alberta, Canada. The expansion is expected to cost approximately $33 million and will increase that facility by approximately 158,000 square feet. We expect the expansion of our Canadian facility to be completed in early Fiscal 2015. Such costs are expected to be funded from our existing cash and cash equivalents and future cash flows from operations.

Item 3. Legal Proceedings

We are involved in various legal proceedings, claims and other disputes arising in the ordinary course of business which, in general, are subject to uncertainties and in which the outcomes are not predictable. We do not believe that the ultimate conclusion of these disputes could materially affect our results of operations, cash flow and financial position.

Item 4. Mine Safety Disclosures

Not applicable.

11

PART II

Item 5. Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities

Price Range of Common Stock

Our common stock trades on the NASDAQ Global Market (NASDAQ) under the symbol “POWL.” The following table sets forth, for the periods indicated, the high and low sales prices per share as reported on the NASDAQ for our common stock.

| High | | | Low | |

Fiscal 2013: | | | | | | | |

First Quarter | $ | 43.95 | | | $ | 37.00 | |

Second Quarter | | 59.89 | | | | 41.45 | |

Third Quarter | | 53.02 | | | | 44.94 | |

Fourth Quarter | | 61.29 | | | | 49.20 | |

Fiscal 2014: | | | | | | | |

First Quarter | $ | 68.86 | | | $ | 60.87 | |

Second Quarter | | 69.50 | | | | 59.17 | |

Third Quarter | | 65.40 | | | | 60.20 | |

Fourth Quarter | | 67.65 | | | | 40.86 | |

As of November 28, 2014, the last reported sales price of our common stock on the NASDAQ was $42.55 per share. As of November 28, 2014, there were 443 stockholders of record of our common stock. All common stock held in street names are recorded in the Company’s stock register as being held by one stockholder.

See “Part III, Item 12. Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters” of this Annual Report for information regarding securities authorized for issuance under our equity compensation plans.

Dividend Policy

In November 2013, our Board of Directors (the Board) elected to begin the payments of quarterly cash dividends. In Fiscal 2014, we paid $12.0 million in dividends. In November 2014, the Board elected to increase our quarterly cash dividend by 4% to $0.26 per share from $0.25 per share. This increase will be effective beginning with the first quarter of Fiscal 2015. The Board anticipates declaring cash dividends in future quarters; however, there is no assurance as to future dividends or their amounts because they depend on future earnings, capital requirements and financial condition.

12

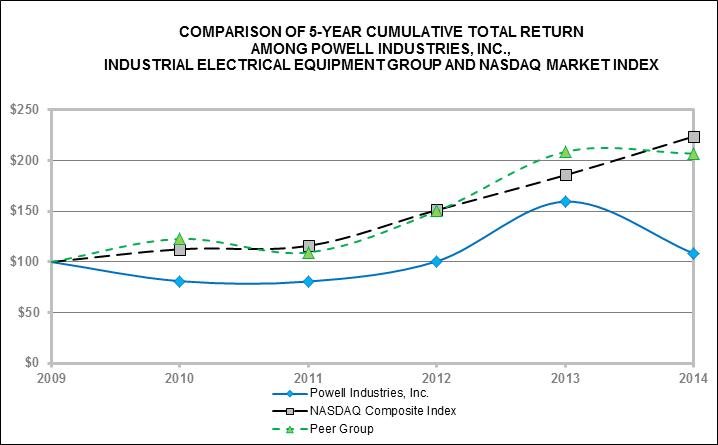

Performance Graph

The following Performance Graph and related information shall not be deemed “soliciting material” or to be “filed” with the Securities and Exchange Commission, nor shall such information be incorporated by reference into any future filing under the Securities Act of 1933 or Securities Act of 1934, each as amended, except to the extent that we specifically incorporate it by reference into such filing.

The following graph compares, for the period from October 1, 2009 to September 30, 2014, the cumulative stockholder return on our common stock with the cumulative total return on the NASDAQ Market Index and the Industrial Electrical Equipment Group (a select group of peer companies – Altra Holdings Inc.; Ameresco, Inc.; AZZ Inc.; Belden Inc.; Coleman Cable, Inc.; Daktronics Inc./SD; Electro Scientific Industries, Inc.; EnerSys; Franklin Electric Co, Inc.; GrafTech International Ltd; Littelfuse Inc./DE; LSI Industries Inc.; Preformed Line Products; A O Smith Corporation and Woodward, Inc.). The comparison assumes that $100 was invested on October 1, 2009, in our common stock, the NASDAQ Market Index and the Industrial Electrical Equipment Group, and that all dividends were re-invested. The stock price performance reflected on the following graph is not necessarily indicative of future stock price performance.

13

Item 6. Selected Financial Data

The selected financial data shown below for the past five years was derived from our audited financial statements, adjusted for discontinuing operations. The historical results are not necessarily indicative of the operating results to be expected in the future. The selected financial data should be read in conjunction with “Part II, Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations” and the consolidated financial statements and related notes included elsewhere in this Annual Report.

| Years ended September 30, | |

| 2014 | | | 2013 | | | 2012 | | | 2011 | | | 2010 | |

Statement of Operations: | (In thousands, except per share data) | |

Revenues | $ | 647,814 | | | $ | 640,867 | | | $ | 690,741 | | | $ | 536,623 | | | $ | 524,237 | |

Cost of goods sold | | 522,340 | | | | 502,375 | | | | 557,938 | | | | 444,861 | | | | 390,459 | |

Gross profit | | 125,474 | | | | 138,492 | | | | 132,803 | | | | 91,762 | | | | 133,778 | |

Selling, general and administrative expenses | | 87,756 | | | | 79,707 | | | | 76,961 | | | | 71,934 | | | | 71,655 | |

Research and development expenses | | 7,608 | | | | 7,615 | | | | 6,286 | | | | 6,435 | | | | 6,110 | |

Amortization of intangible assets | | 779 | | | | 1,659 | | | | 2,599 | | | | 4,752 | | | | 4,477 | |

Restructuring and relocation expenses | | — | | | | 3,927 | | | | — | | | | — | | | | — | |

Impairments | | — | | | | — | | | | — | | | | 7,158 | | | | 7,452 | |

Operating income | | 29,331 | | | | 45,584 | | | | 46,957 | | | | 1,483 | | | | 44,084 | |

Gain on sale of investment | | — | | | | — | | | | — | | | | (1,229 | ) | | | — | |

Gain on settlement | | — | | | | (1,709 | ) | | | — | | | | — | | | | — | |

Other income | | (1,522 | ) | | | — | | | | — | | | | — | | | | — | |

Interest expense (net) | | 165 | | | | 167 | | | | 158 | | | | 194 | | | | 610 | |

Income from continuing operations before income taxes | | 30,688 | | | | 47,126 | | | | 46,799 | | | | 2,518 | | | | 43,474 | |

Income tax provision (1) | | 11,068 | | | | 7,387 | | | | 18,056 | | | | 6,190 | | | | 19,306 | |

Income (loss) from continuing operations before non-controlling interest | | 19,620 | | | | 39,739 | | | | 28,743 | | | | (3,672 | ) | | | 24,168 | |

Non-controlling interest | | — | | | | — | | | | — | | | | — | | | | (159 | ) |

Income (loss) from continuing operations | | 19,620 | | | | 39,739 | | | | 28,743 | | | | (3,672 | ) | | | 24,009 | |

Income from discontinued operations, net of tax | | 9,604 | | | | 2,337 | | | | 914 | | | | 957 | | | | 999 | |

Net income (loss) | $ | 29,224 | | | $ | 42,076 | | | $ | 29,657 | | | $ | (2,715 | ) | | $ | 25,008 | |

| | | | | | | | | | | | | | | | | | | |

Earnings per share: | | | | | | | | | | | | | | | | | | | |

Continuing operations | $ | 1.63 | | | $ | 3.32 | | | $ | 2.43 | | | $ | (0.31 | ) | | $ | 2.08 | |

Discontinued operations | | 0.80 | | | | 0.20 | | | | 0.07 | | | | 0.08 | | | | 0.09 | |

Basic earnings per share | $ | 2.43 | | | $ | 3.52 | | | $ | 2.50 | | | $ | (0.23 | ) | | $ | 2.17 | |

| | | | | | | | | | | | | | | | | | | |

Continuing operations | $ | 1.62 | | | $ | 3.32 | | | $ | 2.41 | | | $ | (0.31 | ) | | $ | 2.05 | |

Discontinued operations | | 0.80 | | | | 0.19 | | | | 0.08 | | | | 0.08 | | | | 0.09 | |

Diluted earnings per share | $ | 2.42 | | | $ | 3.51 | | | $ | 2.49 | | | $ | (0.23 | ) | | $ | 2.14 | |

| | | | | | | | | | | | | | | | | | | |

(1) For an explanation of the effective tax rate for the last three fiscal years, see Note H of the Notes to Consolidated Financial | |

Statements included elsewhere in this Annual Report. | |

| | |

| Years ended September 30, | |

| 2014 | | | 2013 | | | 2012 | | | 2011 | | | 2010 | |

Balance Sheet Data: | (In thousands) | |

Cash and cash equivalents | $ | 103,118 | | | $ | 107,411 | | | $ | 89,669 | | | $ | 123,161 | | | $ | 115,061 | |

Property, plant and equipment, net | | 156,896 | | | | 144,495 | | | | 78,489 | | | | 59,416 | | | | 63,370 | |

Total assets | | 541,443 | | | | 530,903 | | | | 448,312 | | | | 421,676 | | | | 400,712 | |

Long-term debt and capital lease obligations, including current maturities | | 3,200 | | | | 3,616 | | | | 4,355 | | | | 5,441 | | | | 6,885 | |

Total stockholders' equity | | 371,097 | | | | 355,226 | | | | 310,103 | | | | 275,343 | | | | 277,303 | |

Total liabilities and stockholders' equity | | 541,443 | | | | 530,903 | | | | 448,312 | | | | 421,676 | | | | 400,712 | |

Dividends paid on common stock | | 11,998 | | | | — | | | | — | | | | — | | | | — | |

14

Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations

The following discussion should be read in conjunction with the accompanying consolidated financial statements and related notes. Any forward-looking statements made by or on our behalf are made pursuant to the safe-harbor provisions of the Private Securities Litigation Reform Act of 1995. Readers are cautioned that such forward-looking statements involve risks and uncertainties in that the actual results may differ materially from those projected in the forward-looking statements. For a description of the risks and uncertainties, please see “Cautionary Statement Regarding Forward-Looking Statements; Risk Factors” and “Item 1A. Risk Factors” included elsewhere in this Annual Report.

Overview

We develop, design, manufacture and service custom-engineered equipment and systems for the management and control of electrical energy and other critical processes. Headquartered in Houston, Texas, we serve the oil and gas refining, offshore oil and gas production, petrochemical, pipeline, terminal, pulp and paper, mining and metals, light rail traction power, and electric utility markets. Revenues and costs are primarily related to custom engineered-to-order equipment and systems and accounted for under percentage of completion accounting which precludes us from providing detailed price and volume information.

The markets in which we participate are capital intensive and cyclical in nature. Cyclicality is predominantly driven by customer demand, global economic conditions and anticipated environmental or regulatory changes which affect the manner in which our customers proceed with capital investments. Our customers analyze various factors including the demand for oil, gas and electrical energy, the overall financial environment, governmental budgets, regulatory actions and environmental concerns. These factors influence the release of new capital projects by our customers, which are traditionally awarded in competitive bid situations. Scheduling is matched to the customer requirements and projects may take a number of months to produce; schedules also may change during the course of any particular project. Our operating results can be impacted by factors outside of our control. For example, many of our projects have contracting arrangements where the approval of engineering and design specifications may affect the timing of the project execution thus impacting the recognition of revenue and costs. In the second half of Fiscal 2014, we experienced schedule changes on various U.S. projects which negatively impacted our results as the revenues have been pushed into subsequent quarters.

As of September 30, 2014, our order backlog strengthened to $507.1 million, an increase of approximately $69.2 million over the beginning of this fiscal year. Our backlog includes various projects, some of which are petrochemical, oil and gas construction and transportation infrastructure projects which take a number of months to produce.

The strength in the western Canadian oil and gas markets continued to be a major contributor to our increase in revenue in Fiscal 2014. We completed the construction of our new Canadian facility and relocated operations from our previous facility in the fall of 2013. The production ramp of our Canadian operations has presented challenges resulting in inefficiencies that have led to extended project delivery times, higher operating costs, gross margin deterioration and project revenues being pushed into Fiscal 2015. We continue to take actions to mitigate the risks associated with these challenges.

On January 15, 2014, we sold Transdyn to a global provider of electronic toll collection systems, headquartered in Vienna, Austria. The purchase price from the sale of this subsidiary totaled $16.0 million, of which we received cash of $14.4 million. The remaining $1.6 million was placed into an escrow account until April 2015, to be released subject to certain contingent obligations, and was recorded to other assets. We received additional cash of $0.4 million after the final working capital adjustment was calculated in March 2014. We recorded a gain on this transaction of $8.6 million, net of tax, which has been included in income from discontinued operations in Fiscal 2014 in the accompanying consolidated statements of operations. We reclassified the assets and liabilities of Transdyn as held for sale within the accompanying consolidated balance sheets as of September 30, 2013 and presented the results of these operations as income from discontinued operations, net of tax, for each of the accompanying consolidated statements of operations. Accordingly, we have removed Transdyn from the Results of Operations discussions below. For more information about this disposition, see Note N of the Notes to Consolidated Financial Statements included elsewhere in this Annual Report.

In the fourth quarter of Fiscal 2013, we recovered approximately $5.1 million related to one large project at Powell Canada, of which approximately $3.8 million was recorded as revenue and the remaining $1.3 million was related to amounts recorded to other assets in prior periods. This recovery related to cost overruns on a large project with execution challenges which negatively impacted revenue and gross profit in Fiscal 2012.

15

Results of Operations

Twelve Months Ended September 30, 2014 Compared to Twelve Months Ended September 30, 2013

Revenue and Gross Profit

Revenues increased 1.1% or $6.9 million, to $647.8 million in Fiscal 2014. Domestic revenues decreased 2.5%, or $9.3 million, to $365.1 million in Fiscal 2014 primarily due to the mix of projects and international revenues increased 6.1%, or $16.3 million, to $282.7 million in Fiscal 2014. The expansion of our Canadian operations contributed to the increase in international revenues. Revenues from industrial customers increased $18.8 million to $474.4 million in Fiscal 2014. Revenues from public and private utilities decreased $11.6 million to $127.0 million in Fiscal 2014. Revenues from municipal and transit projects decreased $0.3 million to $46.3 million in Fiscal 2014. Additionally, revenues in Fiscal 2013 were favorably impacted by the recovery of $3.8 million related to cost overruns from a previous year on a large industrial project.

Gross profit decreased 9.4%, or $13.0 million, to $125.5 million in Fiscal 2014. Gross profit as a percentage of revenues decreased to 19.4% in Fiscal 2014, compared to 21.6% in Fiscal 2013 primarily due to higher costs resulting from the efficiency and utilization challenges associated with the ramp of our Canadian operations. Additionally, we incurred higher operating costs associated with inefficiencies from the re-implementation of our existing ERP system and added a suite of new software tools to expand our Business Systems. These higher costs were partially offset by various supply chain and productivity initiatives. Gross profit for Fiscal 2013 was favorably impacted by the $3.8 million recovery from the project discussed above.

Selling, General and Administrative Expenses

Selling, general and administrative expenses increased by $8.0 million to $87.8 million in Fiscal 2014, compared to Fiscal 2013, primarily due to increased personnel costs, travel and administrative expenses and bad debts. Selling, general and administrative expenses, as a percentage of revenues, increased to 13.5% in Fiscal 2014, compared to 12.4% in Fiscal 2013. This increase in selling, general and administrative expense was partially offset by a decrease in depreciation expense as our existing Business Systems became fully depreciated in December 2012 and the favorable impact of the capitalization of certain personnel costs associated with the development and implementation of our new Business Systems, which went live in May 2014. However, going forward, the favorable impact of depreciation expense and capitalization of certain personnel costs will no longer be realized.

Amortization of Intangible Assets

Amortization of intangible assets decreased to $0.8 million in Fiscal 2014 compared to $1.7 million in Fiscal 2013 primarily due to the amendment to the supply agreement which is discussed in Note E of the Notes to Consolidated Financial Statements included elsewhere in this Annual Report.

Other Income

We recorded other income of $1.5 million in Fiscal 2014 which represents the amortization of the deferred gain from the amendment to the supply agreement discussed above. We did not record other income in Fiscal 2013.

Income Tax Provision

Our provision for income taxes for continuing operations was $11.1 million in Fiscal 2014, compared to $7.4 million in Fiscal 2013. The effective tax rate in Fiscal 2014 was 36.1%, which approximates the combined U.S. federal and state statutory rates as the majority of our income is attributable to the U.S. Additionally, the Federal Research and Development Tax Credit (R&D Credit) expired December 31, 2013. The effective tax rate for Fiscal 2013 was 15.7% and was favorably impacted by the release of the $7 million valuation allowance recorded as an offset to the prior years’ Canadian pre-tax losses and the R&D Credit as well as the utilization of certain foreign tax credits. For further information on the effective tax rate for Fiscal 2013, see Note H of the Notes to Consolidated Financial Statements included elsewhere in this Annual Report.

Income from Continuing Operations

In Fiscal 2014, we recorded income from continuing operations of $19.6 million, or $1.62 per diluted share, compared to $39.7 million, or $3.32 per diluted share, in Fiscal 2013. This decrease in income from continuing operations was primarily due to efficiency and utilization challenges associated with the ramp of our Canadian operations, higher operating costs associated with inefficiencies from the re-implementation of our existing ERP system and the mix of projects in process at our domestic operations.

16

Income from Discontinued Operations

In Fiscal 2014, we recorded $9.6 million, or $0.80 per diluted share, of income from discontinued operations compared to $2.3 million, or $0.19 per diluted share, in Fiscal 2013 as the current fiscal year includes the gain on the sale. For additional information about this disposition, see Note N of the Notes to Consolidated Financial Statements included elsewhere in this Annual Report.

Backlog

The order backlog at September 30, 2014 was $507.1 million, compared to $437.9 million at September 30, 2013. New orders placed in Fiscal 2014 totaled $725.8 million compared to $715.7 million in Fiscal 2013. The year over year increase in new orders was primarily due to the continued strength in oil and gas production and petrochemical and pipeline projects.

Twelve Months Ended September 30, 2013 Compared to Twelve Months Ended September 30, 2012

Revenue and Gross Profit

Revenues decreased 7.2%, or $49.9 million, to $640.9 million in Fiscal 2013 compared to Fiscal 2012. Domestic revenues decreased by 3.7%, or $14.6 million, to $374.4 million in Fiscal 2013 and international revenues decreased 11.7%, or $35.3 million, to $266.5 million in Fiscal 2013. Revenues decreased primarily due to the completion of certain complex domestic and international petrochemical and oil and gas construction projects that were in process during Fiscal 2012. However, revenues in Fiscal 2013 were favorably impacted by the recovery of $3.8 million related to cost overruns on a large industrial project at Powell Canada. This Canadian project experienced execution challenges in the first half of Fiscal 2012, which negatively impacted revenue and gross profit in Fiscal 2012. Revenues from public and private utilities increased $22.8 million to $138.6 million in Fiscal 2013. Revenues from industrial customers decreased $70.7 million to $455.6 million in Fiscal 2013. Revenues from municipal and transit projects decreased $2.0 million to $46.6 million in Fiscal 2013.

Gross profit increased 4.3%, or $5.7 million, to $138.5 million in Fiscal 2013. Gross profit as a percentage of revenues increased to 21.6% in Fiscal 2013, compared to 19.2% in Fiscal 2012. These increases were primarily driven by the recovery from the Canadian contract settlement discussed above, the margins associated with the mix of projects in process during Fiscal 2012 and 2013, as well as the increased focus on cost reduction activities.

Selling, General and Administrative Expenses

Selling, general and administrative expenses increased $2.7 million to $79.7 million in Fiscal 2013. Selling, general and administrative expenses, as a percentage of revenues, increased to 12.4% in Fiscal 2013 from 11.1% in Fiscal 2012. This increase was primarily related to increased personnel costs and increased long-term incentive compensation resulting from higher levels of operating performance over the three-year performance cycle. This increase in selling, general and administrative expenses was offset by a decrease in depreciation expense as our Business Systems became fully depreciated in December 2012. Additionally, selling, general and administrative costs for Fiscal 2013 were favorably impacted by the capitalization of certain personnel costs in Fiscal 2013 associated with the development and implementation of our new Business Systems. However, the favorable impact of depreciation expense and capitalization of certain personnel costs will no longer be realized as the Business Systems were implemented in Fiscal 2014.

Amortization of Intangible Assets

Amortization of intangible assets decreased to $1.7 million in Fiscal 2013, compared to $2.6 million in Fiscal 2012, as certain intangible assets became fully amortized.

Restructuring and Relocation Costs

During Fiscal 2013, we recorded restructuring and relocation charges totaling $3.9 million. We incurred approximately $2.8 million in Fiscal 2013 related to relocation efforts in connection with the construction of our new facility in Houston, Texas and our new facility in Acheson, Alberta, Canada. These costs were primarily related to the relocation of our operations, the loss on the sublease, and the abandonment of leasehold improvements on the previously occupied facilities in the second half of Fiscal 2013. The construction of our two new facilities was substantially completed in September 2013 and we relocated the majority of our operations and personnel from their previously leased facilities.

In the third quarter of Fiscal 2013, we recorded and paid $1.1 million related to severance at our United Kingdom operations. These operations were negatively impacted by market conditions and competitive pressures in the international markets in which they operate; therefore, we exited certain non-core operations and eliminated certain positions to better align our workforce with current market conditions.

17

Gain on Settlement

In March 2013, we settled a lawsuit we had filed against the previous owners of Powell Canada in the amount of $1.7 million, which was received in April 2013. There was no gain on settlement in Fiscal 2012.

Income Tax Provision

Our provision for income taxes reflected an effective tax rate on earnings before income taxes of 15.7% in Fiscal 2013 compared to 38.6% in Fiscal 2012. The effective tax rate for Fiscal 2013 was favorably impacted by the release of the $7 million valuation allowance recorded as an offset to the prior years’ Canadian pre-tax losses. We believe that it is more likely than not that the market conditions and our operating results going forward will allow us to realize the deferred tax assets associated with the prior year losses in Canada. The rate for Fiscal 2013 was also favorably impacted by the Federal Research and Development Tax Credit and the utilization of certain foreign tax credits. The effective tax rate for Fiscal 2012 was negatively impacted by our inability to record a tax benefit related to pre-tax losses in Canada. For further information on the effective tax rate for Fiscal 2013, see Note H of the Notes to Consolidated Financial Statements included elsewhere in this Annual Report.

Income from Continuing Operations

In Fiscal 2013, we recorded income from continuing operations of $39.7 million, or $3.32 per diluted share, compared to $28.7 million, or $2.41 per diluted share, in Fiscal 2012. Income from continuing operations in Fiscal 2013 was positively impacted by the recovery of $3.8 million from the Canadian contract settlement and the favorable tax benefits discussed above.

Income from Discontinued Operations

In Fiscal 2013, we recorded $2.3 million, or $0.19 per diluted share, of income from discontinued operations compared to $0.9 million, or $0.08 per diluted share, in Fiscal 2012. For additional information about this disposition, see Note N of the Notes to Consolidated Financial Statements.

Backlog

The order backlog at September 30, 2013, was $437.9 million, compared to $365.9 million at September 30, 2012. New orders placed during Fiscal 2013 totaled $715.7 million compared to $659.9 million in Fiscal 2012. The backlog for Fiscal 2013 increased primarily due to continued strength in oil and gas production projects, refining projects and transportation markets.

Liquidity and Capital Resources

Cash and cash equivalents decreased to $103.1 million at September 30, 2014, compared to $107.4 million at September 30, 2013. As of September 30, 2014, current assets exceeded current liabilities by 2.3 times and our debt to total capitalization ratio was 0.85%.

We have a $75.0 million revolving credit facility in the U.S., which expires in December 2016. As of September 30, 2014, there were no amounts borrowed under this line of credit. We also have a $9.0 million revolving credit facility in Canada. At September 30, 2014, there was no balance outstanding under the Canadian revolving credit facility. Total long-term debt and capital lease obligations, including current maturities, totaled $3.2 million at September 30, 2014, compared to $3.6 million at September 30, 2013. Total letters of credit outstanding were $21.5 million and $20.1 million at September 30, 2014 and 2013, respectively, which reduce our availability under our U.S. credit facility and our Canadian revolving credit facility. Amounts available at September 30, 2014 under the U.S. and Canadian revolving credit facilities were $53.5 million and $9.0 million, respectively. For further information regarding our debt, see Notes F and G of the Notes to Consolidated Financial Statements included elsewhere in this Annual Report.

Approximately $5.9 million of our cash at September 30, 2014 was held outside of the United States for international operations. It is our intention to indefinitely reinvest all current and future foreign earnings internationally in order to ensure sufficient working capital and support and expand these international operations. In the event that we elect to repatriate some or all of the foreign earnings that were previously deemed to be indefinitely reinvested outside the U.S., under current tax laws we would incur additional tax expense upon such repatriation.

We believe that cash available and borrowing capacity under our existing credit facilities should be sufficient to finance anticipated operating activities, capital improvements and expansions, as well as debt repayments, for the foreseeable future. We continue to monitor the factors that drive our markets and strive to maintain our leadership and competitive advantage in the markets we serve while aligning our cost structures with market conditions.

18

Operating Activities

During Fiscal 2014, net cash provided by operating activities was $9.1 million. During Fiscal 2013, net cash provided by operating activities was $91.4 million and in Fiscal 2012, net cash used in operating activities was $6.0 million. Cash flow from operations is primarily influenced by demand for our products and services and is impacted as our progress payment terms with our customers are matched with the payment terms with our suppliers. During Fiscal 2014, our cash from operations decreased over Fiscal 2013, primarily due to the timing of billing and collection of contracts receivable based on the progress billing milestones, an increase in inventories and a decrease in accounts payable and income taxes payable. The increase in inventories resulted in part from supply chain inefficiencies resulting from the re-implementation of our Business Systems. These uses of cash were partially offset by the $10.0 million received from the amended supply agreement. For further information regarding the amended supply agreement, see Note E of the Notes to Consolidated Financial Statements included elsewhere in this Annual Report. Additionally in Fiscal 2013, we received $6.8 million in contract settlements related to Fiscal 2012 matters. During Fiscal 2012, the cash used in operations of $6.0 million was primarily the result of increased unbilled contract receivables based on progress billing milestones.

Investing Activities

Purchases of property, plant and equipment during Fiscal 2014 totaled $16.5 million compared to $74.4 million and $29.1 million in Fiscal 2013 and 2012, respectively. A significant portion of the investments in Fiscal 2012 and 2013 were to acquire land and build facilities in the United States and Canada to support our continued expansion in our key markets, including the oil and gas markets and Canadian oil sands region. Costs related to the re-implementation and additional software added to our Business Systems were incurred during Fiscal 2013 and were placed into service in the third quarter of Fiscal 2014.

Financing Activities

Net cash used in financing activities was $12.5 million in Fiscal 2014 and $0.5 million in Fiscal 2013. Net cash provided by financing activities was $1.3 million during Fiscal 2012 due to cash being received from the exercise of stock options. The increase in the use of cash in Fiscal 2014 was primarily driven by the payment of $12.0 million in cash dividends.

Contractual and Other Obligations

At September 30, 2014, our long-term contractual obligations were limited to debt and leases. The table below details our commitments by type of obligation, including interest if applicable, and the period that the payment will become due (in thousands).

As of September 30, 2014, Payments Due by Period: | Long‑Term

Debt

Obligations | | | | Operating

Lease

Obligations | | | Total | |

Less than 1 year | $ | 406 | | | | $ | 4,155 | | | $ | 4,561 | |

1 to 3 years | | 809 | | | | | 5,490 | | | | 6,299 | |

3 to 5 years | | 806 | | | | | 3,036 | | | | 3,842 | |

More than 5 years | | 1,202 | | | | | 5,586 | | | | 6,788 | |

Total long-term contractual obligations | $ | 3,223 | | | | $ | 18,267 | | | $ | 21,490 | |

The lease on our previously occupied Canadian facility does not expire until July 2023; however, we have sublet that facility through July 2019.

As of September 30, 2014, the total unrecognized tax benefit related to uncertain tax positions was $4.0 million. We estimate that none of this will be paid within the next 12 months. However, we believe that it is reasonably possible that within the next 12 months, the total unrecognized tax benefits will decrease by approximately 1% due to the expiration of certain statutes of limitations in various state and local jurisdictions. We are unable to make reasonably reliable estimates regarding the timing of future cash outflows, if any, associated with the remaining unrecognized tax benefits.

Other Commercial Commitments

We are contingently liable for secured and unsecured letters of credit of $24.2 million as of September 30, 2014, of which $21.5 million reduces our borrowing capacity.

19

The following table reflects potential cash outflows that may result in the event that we are unable to perform under our contracts (in thousands):

As of September 30, 2014, Payments Due by Period: | | Letters of

Credit | |

Less than 1 year | | $ | 12,939 | |

1 to 3 years | | | 8,340 | |

More than 3 years | | | 2,893 | |

Total long-term commercial obligations | | $ | 24,172 | |

We also had performance and maintenance bonds totaling $298.7 million that were outstanding at September 30, 2014. Performance and maintenance bonds are primarily used to guarantee our contract performance to our customers.

Outlook

The markets in which we participate are capital-intensive and cyclical in nature. Cyclicality is predominantly driven by customer demand, global economic conditions and anticipated environmental or regulatory changes which affect the manner in which our customers proceed with capital investments. Our customers analyze various factors including the demand for oil, gas and electrical energy, the overall financial environment, governmental budgets, regulatory actions and environmental concerns. These factors influence the release of new capital projects by our customers, which are traditionally awarded in competitive bid situations. Scheduling is matched to the customer requirements; and projects may take a number of months to produce; schedules also may change during the course of any particular project.

Growth in demand for energy is expected to continue over the long term. This, when coupled with the need for replacement of existing infrastructure that is nearing the end of its life cycle, demonstrates a continued need for products and services produced by us. Our orders over the past year have been solid, driven primarily by the relative stability in the oil and gas industry overall, along with the specific demand associated with Canadian oil sands related projects. We continue to experience timing challenges in the near-term related to the awarding of large projects due to various global market conditions and industry constraints. However, the long-term outlook for continued opportunities for our products and services remains positive; even though the timing and pricing of many of these projects are difficult to predict.

Our operating results are frequently impacted by the timing and resolution of change orders and project close-out which could cause gross margins to improve or deteriorate during the period in which these items are approved and finalized with customers. Our operating results are also impacted by factors outside of our control, such as our projects that have contract arrangements where the approval of engineering and design specifications may affect the timing of the project execution.