Exhibit 99.1

Company Overview

May 2013

Safe Harbor Language

This presentation includes forward-looking statements. Quiksilver, Inc. (“Quiksilver” or the “Company”) cautions that these statements are qualified by important factors that could cause actual results to differ materially from those presented or implied in the forward-looking statements. These statements are based on Quiksilver’s current plans and expectations and involve risks and uncertainties that could cause future activities and results of operations to be materially different from those set forth in or implied by the forward-looking statements. For the factors that could cause actual results to differ materially from expectations, please refer to the Company’s filings with the Securities and Exchange Commission (“SEC”) and specifically the sections titled “Risk Factors,” “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and “Forward-Looking Statements” in the Company’s Forms 10-K and 10-Q. The Company cautions that any forward-looking statements included in this presentation are made as of the date of this presentation, and the Company does not undertake to update any forward-looking statements. This presentation also includes certain non-GAAP financial measures including Pro Forma Adjusted EBITDA (“EBITDA”). The reconciliation of such non-GAAP financial measures to the nearest GAAP equivalent can be found in the Company’s earnings press releases and Forms 10-K and 10-Q, which are filed with the SEC and can also be found on the Company’s website at www.quiksilverinc.com.

2

Agenda

Company

Inflection Point

Profit Improvement Plan

Financial Performance

3

Who We Are

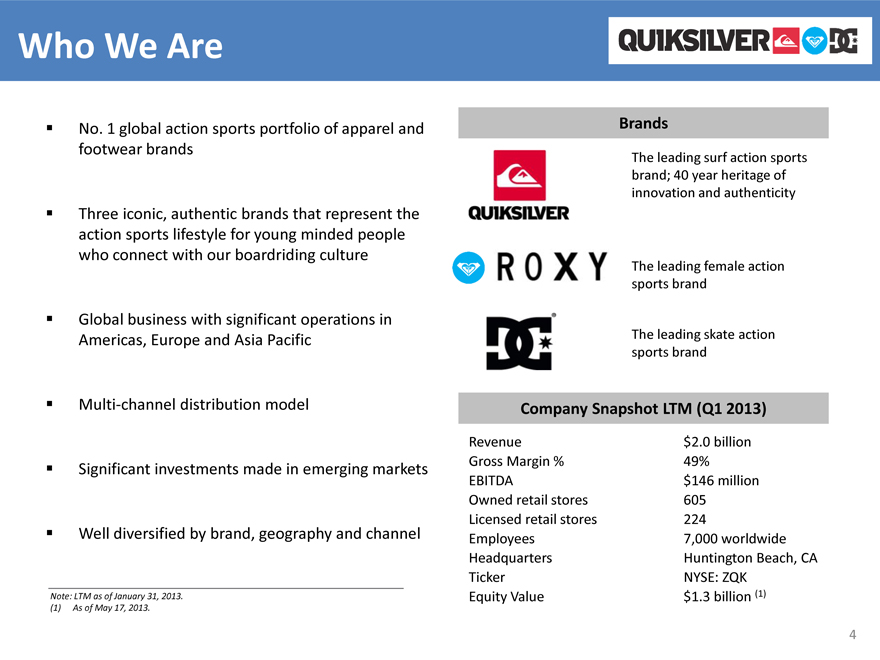

No. 1 global action sports portfolio of apparel and footwear brands

Three iconic, authentic brands that represent the action sports lifestyle for young minded people who connect with our boardriding culture

Global business with significant operations in Americas, Europe and Asia Pacific

Multi-channel distribution model

Significant investments made in emerging markets

Well diversified by brand, geography and channel

Brands

The leading surf action sports brand; 40 year heritage of innovation and authenticity

The leading female action sports brand

The leading skate action sports brand

Company Snapshot LTM (Q1 2013)

Revenue $2.0 billion

Gross Margin % 49%

EBITDA $146 million

Owned retail stores 605

Licensed retail stores 224

Employees 7,000 worldwide

Headquarters Huntington Beach, CA

Ticker NYSE: ZQK

Equity Value $1.3 billion (1)

Note: LTM as of January 31, 2013.

(1) As of May 17, 2013.

4

History and Milestones

1969 1998 2000 2002 2004 2006 2008 2010 2013

1969-1991

Founded, Australia

IP0 (1986)

Acquired Quiksilver Europe

Roxy launched

1998-2002

Quiksilver listed on NYSE as ‘ZQK’

Acquired Quiksilver Asia/Pacific

Acquired international trademarks

Revenues top $500M (2000)

2003-2004

Acquired DC Shoes (2004)

Revenues top $1B (2004)

2005-2008

Issued $400M Senior Notes (2005)

Acquired Rossignol (2005)

Global Credit Crisis

Divested Rossignol (2008)

2009-2010

Initial Rhone investment (2009)

Debt for equity exchange (2010)

Issued €200M Senior Notes (2010)

2011-2013

Revenues of $2B

New management team (2013)

Profit Improvement Plan (2013)

5

Flagship Brands

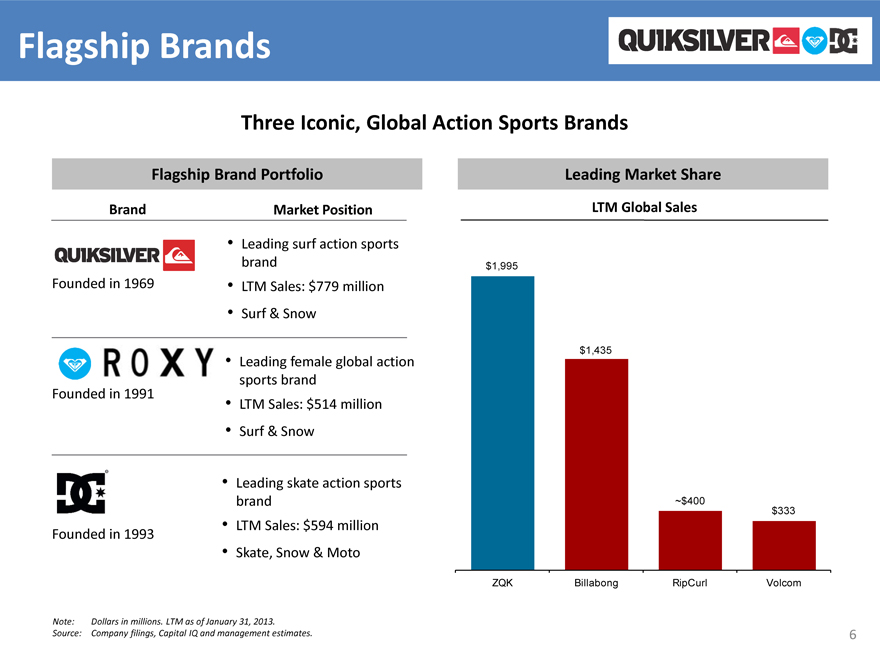

Three Iconic, Global Action Sports Brands

Flagship Brand Portfolio

Brand

Market Position

Founded in 1969

Leading surf action sports brand

LTM Sales: $779 million

Surf & Snow

Founded in 1991

Leading female global action sports brand

LTM Sales: $514 million

Surf & Snow

Founded in 1993

Leading skate action sports brand

LTM Sales: $594 million

Skate, Snow & Moto

Leading Market Share

LTM Global Sales

$1,995

$1,435

~$400

$333

ZQK Billabong RipCurl Volcom

Note: Dollars in millions. LTM as of January 31, 2013.

Source: Company filings, Capital IQ and management estimates.

6

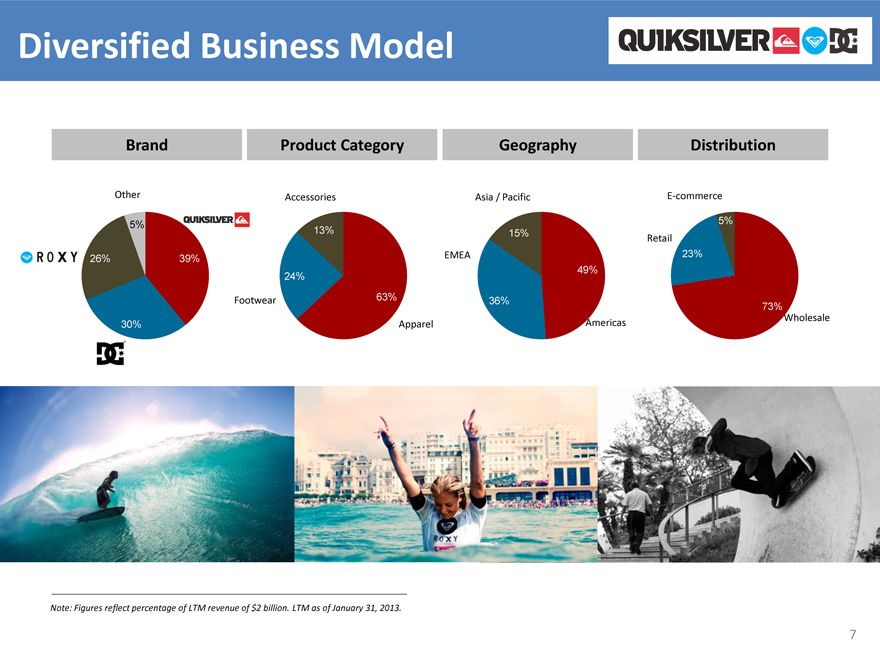

Diversified Business Model

Brand

Product Category

Geography

Distribution

Other

5%

26%

39%

30%

Accessories

13%

24%

63%

Footwear

Apparel

Asia / Pacific

EMEA

15%

36%

49%

Americas

E-commerce

Retail

5%

23%

73%

Wholesale

Note: Figures reflect percentage of LTM revenue of $2 billion. LTM as of January 31, 2013.

7

Three Fundamental Strategies

BRAND STRENGTH

Build global consumer awareness and appreciation of our flagship brands.

REVENUE GROWTH

Drive sales of our core brands with new products, new markets, new sales channels and new consumers.

OPERATING EFFICIENCY

Relentless global focus to improve efficiency via process re-design, team upgrading, workload prioritization, automation, different business models, and divestitures.

8

Highlights

3 global iconic brands Diversified business model New management team in place

Execution commenced on Profit Improvement Plan

Significant opportunity to improve profitability and free cash flow

9

Agenda

Company

Inflection Point

Profit Improvement Plan

Financial Performance

10

New Leadership Team

Name Title Start Date Previous Experience

Andy Mooney President & CEO 2013 Nike 20 years; Disney 10 years

Tom Hartge Global Head of Footwear 2013 Nike 24 years; Patagonia 2 years

Pierre Agnes Global Head of Apparel 1988 Quiksilver 25 years

Gap 2 years; Levi’s 13 years;

Kasey Mazzone Global Head of Supply Chain 2013

American Eagle 2 years

Nick Drake Chief Marketing Officer 2013 TBWA/Chiat/Day 4 years; adidas 6 years

Steve Finney Head of Retail / Ecomm N.A. 2013 Disney 21 years

Pam Lifford Global Licensing 2013 Disney 11 years

Charlie Exon General Counsel and CAO 2000 Quiksilver 13 years

Carol Scherman Global EVP Human Resources 2006 Quiksilver 7 years

Richard Shields Chief Financial Officer 2012 Oakley 7 years; AST 9 years.

Newly formed management team has substantial expertise and experience in successful global apparel companies.

11

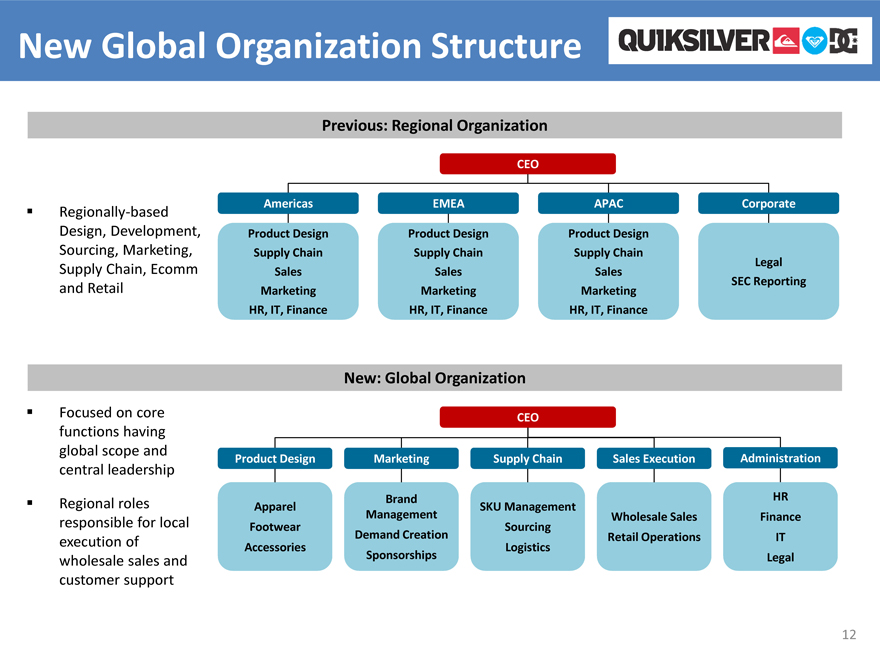

New Global Organization Structure

Previous: Regional Organization

Regionally-based Design, Development, Sourcing, Marketing, Supply Chain, Ecomm and Retail

CEO

Americas EMEA APAC Corporate

Product Design Supply Chain Sales Marketing HR, IT, Finance

Product Design Supply Chain Sales Marketing HR, IT, Finance

Product Design Supply Chain Sales Marketing HR, IT, Finance

Legal SEC Reporting

New: Global Organization

Focused on core functions having global scope and central leadership

Regional roles responsible for local execution of wholesale sales and customer support

Product Design Marketing Supply Chain Sales Execution Administration

Apparel Footwear Accessories

Brand Management Demand Creation Sponsorships

SKU Management Sourcing Logistics

Wholesale Sales Retail Operations

HR Finance IT Legal

12

Agenda

Company

Inflection Point

Profit Improvement Plan

Financial Performance

13

Profit Improvement Plan Summary

BRAND STRENGTH

Focus on core brands Clarify positioning of each core brand Reallocate marketing from athletes and events to social media and print

REVENUE GROWTH

Increase demand creation investment Continued investments in emerging markets Improve sales execution

OPERATING EFFICIENCY

Centralize Supply Chain Product design process

G&A reductions SAP automation Retail

Licensing

14

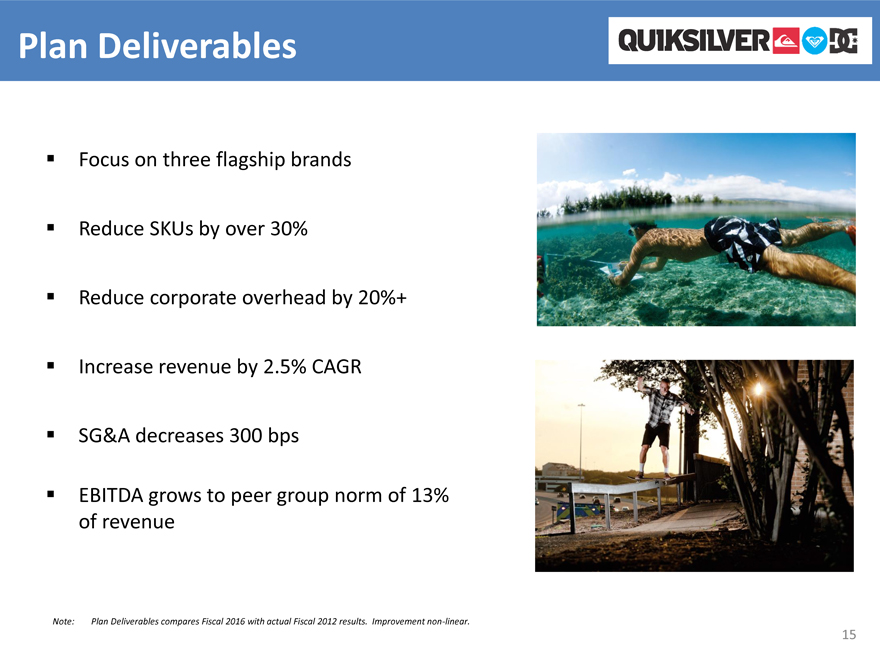

Plan Deliverables

Focus on three flagship brands Reduce SKUs by over 30% Reduce corporate overhead by 20%+ Increase revenue by 2.5% CAGR SG&A decreases 300 bps

EBITDA grows to peer group norm of 13% of revenue

Note: Plan Deliverables compares Fiscal 2016 with actual Fiscal 2012 results. Improvement non-linear.

15

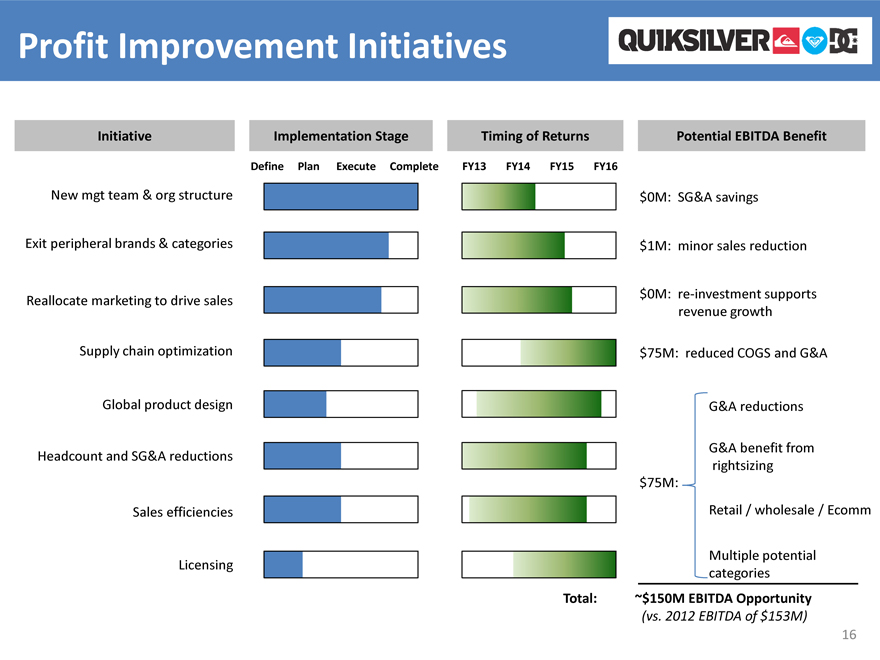

Profit Improvement Initiatives

Initiative Implementation Stage Timing of Returns Potential EBITDA Benefit

Define Plan Execute Complete FY13 FY14 FY15 FY16

New mgt team & org structure

Exit peripheral brands & categories

Reallocate marketing to drive sales

Supply chain optimization

Global product design

Headcount and SG&A reductions

Sales efficiencies

Licensing

$0M: SG&A savings

$1M: minor sales reduction

$0M: re-investment supports revenue growth

$75M: reduced COGS and G&A

$75M:

G&A reductions

G&A benefit from rightsizing

Retail / wholesale / Ecomm

Multiple potential categories

Total:

~$150M EBITDA Opportunity

(vs. 2012 EBITDA of $153M)

16

Mission Statement

Build Authentic, Active brands into

Significant Sustainable successes.

17

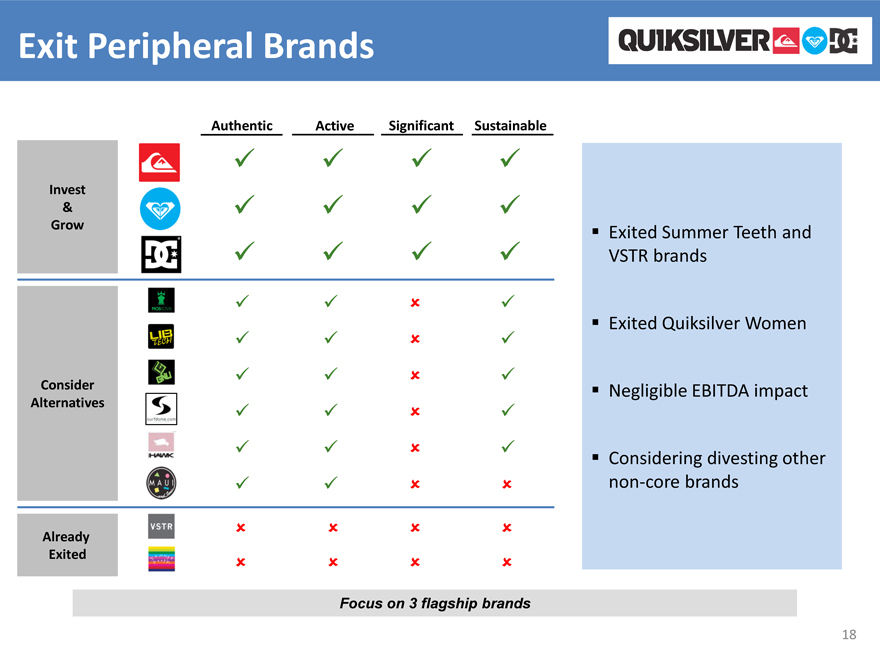

Exit Peripheral Brands

Authentic Active Significant Sustainable

Invest & Grow

Consider Alternatives

Already Exited

Exited Summer Teeth and VSTR brands

Exited Quiksilver Women

Negligible EBITDA impact

Considering divesting other non-core brands

Focus on 3 flagship brands

18

Reallocate Marketing

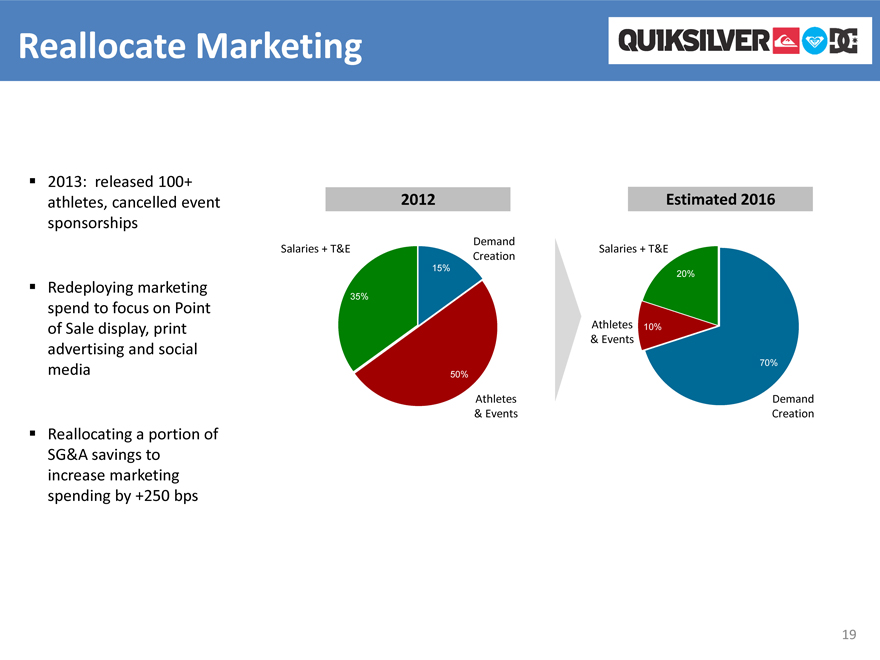

2013: released 100+ athletes, cancelled event sponsorships

Redeploying marketing spend to focus on Point of Sale display, print advertising and social media

Reallocating a portion of SG&A savings to increase marketing spending by +250 bps

2012

Salaries + T&E

35%

15%

50%

Athletes & Events

Demand Creation

Estimated 2016

Salaries + T&E

Athletes

& Events

20%

10%

70%

Demand Creation

19

Supply Chain Optimization

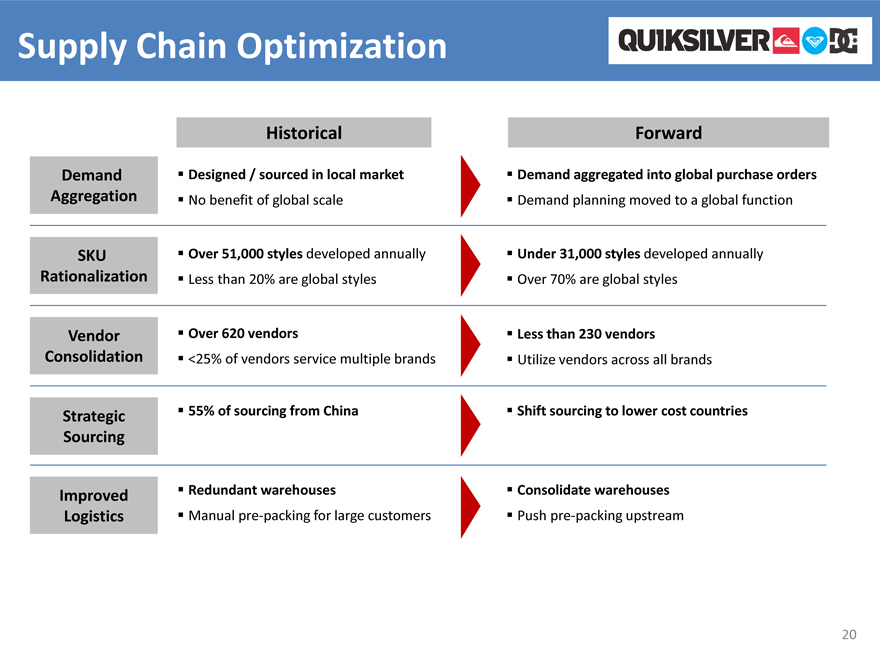

Historical

Demand Aggregation

SKU Rationalization

Vendor Consolidation

Strategic Sourcing

Improved Logistics

Designed / sourced in local market

No benefit of global scale

Over 51,000 styles developed annually

Less than 20% are global styles

Over 620 vendors

<25% of vendors service multiple brands

55% of sourcing from China

Redundant warehouses

Manual pre-packing for large customers

Forward

Demand aggregated into global purchase orders

Demand planning moved to a global function

Under 31,000 styles developed annually

Over 70% are global styles

Less than 230 vendors

Utilize vendors across all brands

Shift sourcing to lower cost countries

Consolidate warehouses

Push pre-packing upstream

20

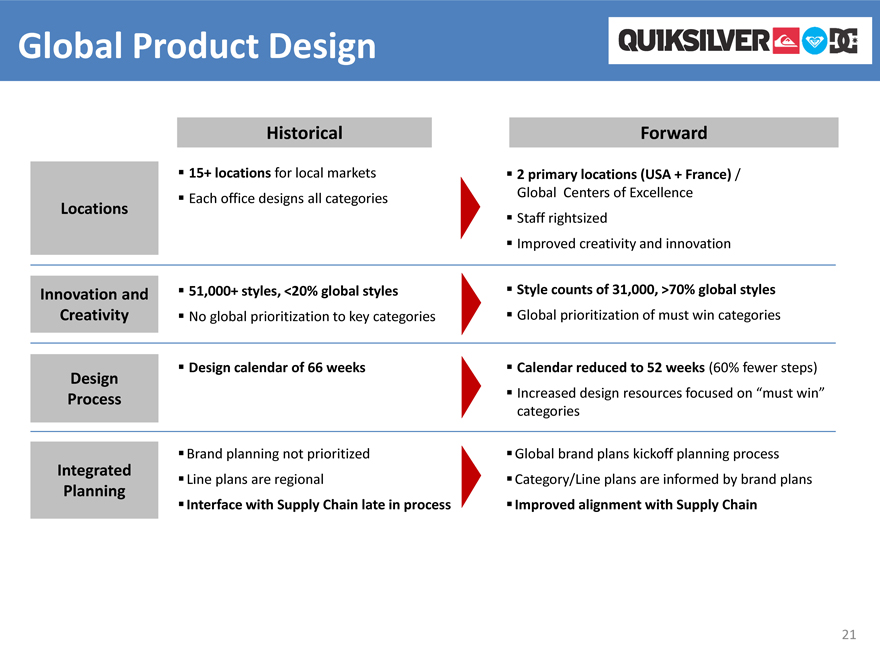

Global Product Design

Historical

Locations

Innovation and Creativity

Design Process

Integrated Planning

15+ locations for local markets

Each office designs all categories

51,000+ styles, <20% global styles

No global prioritization to key categories

Design calendar of 66 weeks

Brand planning not prioritized

Line plans are regional

Interface with Supply Chain late in process

Forward

2 primary locations (USA + France) /

Global Centers of Excellence Staff rightsized

Improved creativity and innovation

Style counts of 31,000, >70% global styles

Global prioritization of must win categories

Calendar reduced to 52 weeks (60% fewer steps)

Increased design resources focused on “must win” categories

Global brand plans kickoff planning process

Category/Line plans are informed by brand plans

Improved alignment with Supply Chain

21

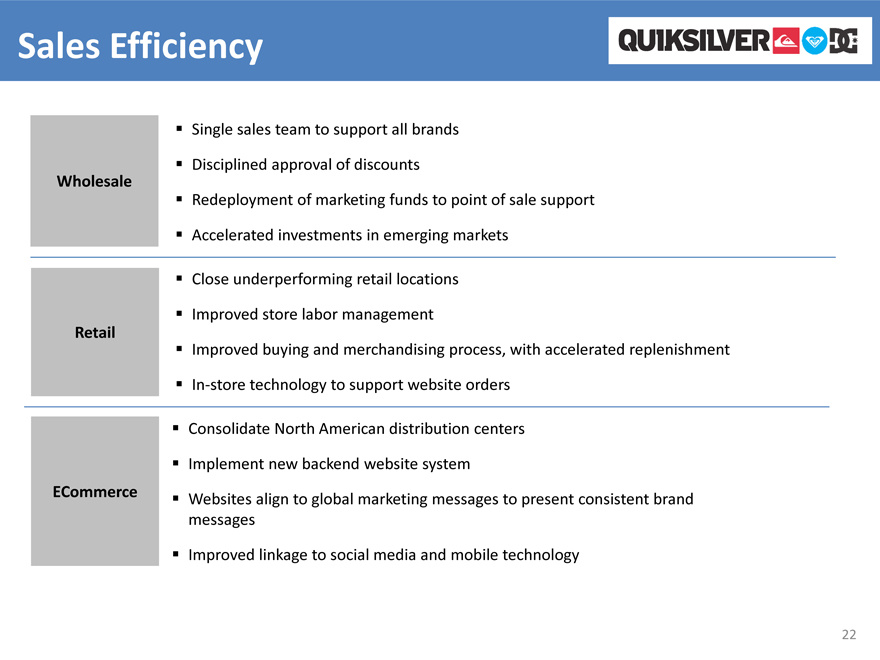

Sales Efficiency

Wholesale

Single sales team to support all brands

Disciplined approval of discounts

Redeployment of marketing funds to point of sale support

Accelerated investments in emerging markets

Retail

Close underperforming retail locations

Improved store labor management

Improved buying and merchandising process, with accelerated replenishment

In-store technology to support website orders

ECommerce

Consolidate North American distribution centers

Implement new backend website system

Websites align to global marketing messages to present consistent brand messages

Improved linkage to social media and mobile technology

22

Agenda

Company

Inflection Point

Profit Improvement Plan

Financial Performance

23

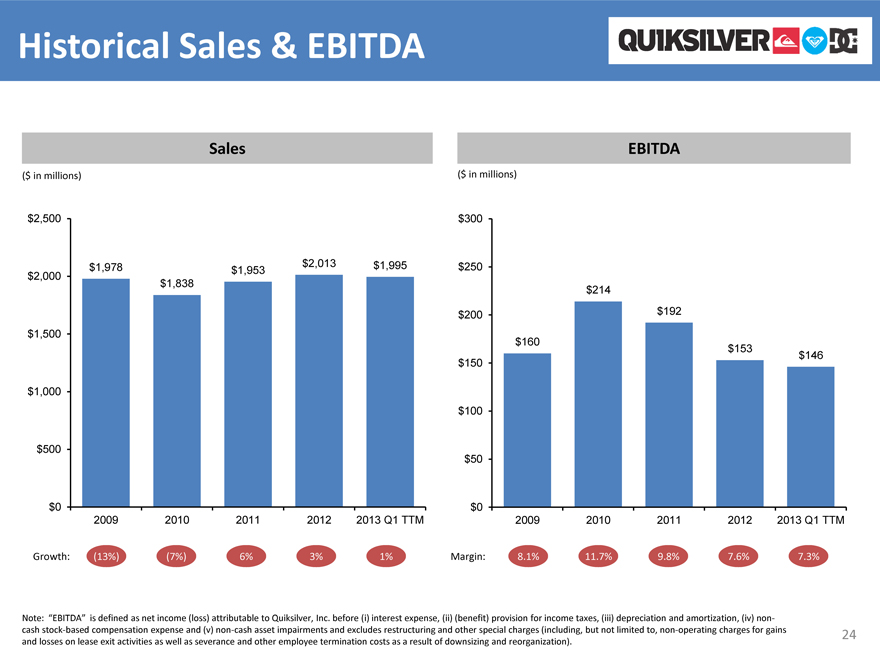

Historical Sales & EBITDA

Sales

($ in millions)

$2,500

$2,000

$1,500

$1,000

$500

$0

$1,978

$1,838

$1,953

$2,013

$1,995

2009 2010 2011 2012 2013 Q1 TTM

EBITDA

($ in millions)

$300

$250

$200

$150

$100

$50

$0

$160

$214

$192

$153

$146

2009 2010 2011 2012 2013 Q1 TTM

Growth: (13%) (7%) 6% 3% 1%

Margin: 8.1% 11.7% 9.8% 7.6% 7.3%

Note: “EBITDA” is defined as net income (loss) attributable to Quiksilver, Inc. before (i) interest expense, (ii) (benefit) provision for income taxes, (iii) depreciation and amortization, (iv) non-cash stock-based compensation expense and (v) non-cash asset impairments and excludes restructuring and other special charges (including, but not limited to, non-operating charges for gains and losses on lease exit activities as well as severance and other employee termination costs as a result of downsizing and reorganization).

24

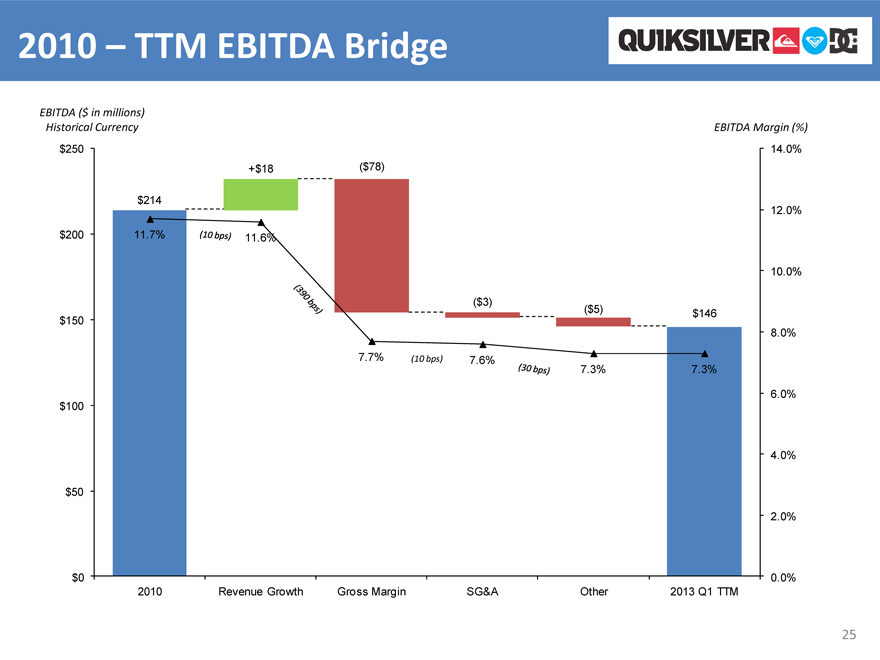

2010 – TTM EBITDA Bridge

EBITDA ($ in millions) Historical Currency

$250

$200

$150

$100

$50

$0

$214

+$18

($78)

($3)

($5)

$146

11.7%

(10bps)

11.6%

(390 bps)

7.7%

(10 bps)

7.6%

(30bps)

7.3%

7.3%

EBITDA Margin (%)

14.0%

12.0%

10.0%

8.0%

6.0%

4.0%

2.0%

0.0%

2010 Revenue Growth Gross Margin SG&A Other 2013 Q1 TTM

25

www.quiksilverinc.com