Exhibit 99.2

THIS DISCLOSURE STATEMENT HAS

NOT YET BEEN APPROVED BY THE COURT

This proposed Disclosure Statement is not a solicitation of acceptance or rejection of the Plan of Reorganization. Acceptances or rejections may not be solicited until the Bankruptcy Court has approved this Disclosure Statement under section 1125 of the Bankruptcy Code. This proposed Disclosure Statement is being submitted for approval only, and has not yet been approved by the Bankruptcy Court.

IN THE UNITED STATES BANKRUPTCY COURT

FOR THE DISTRICT OF DELAWARE

| - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - | x | |||

| : | ||||

| In re: | : | Chapter 11 | ||

| : | ||||

| QUIKSILVER, INC., et al., | : | Case No. 15-11880 (BLS) | ||

| : | ||||

| Debtors.1 | : | Jointly Administered | ||

| : | ||||

| - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - | x |

DISCLOSURE STATEMENT WITH RESPECT TO

THE JOINT CHAPTER 11 PLAN OF REORGANIZATION OF QUIKSILVER, INC.

AND ITS AFFILIATED DEBTORS AND DEBTORS IN POSSESSION

| SKADDEN, ARPS, SLATE, MEAGHER & FLOM LLP | ||||

Van C. Durrer, II (I.D. No. 3827) Annie Z. Li 300 South Grand Avenue, Suite 3400 Los Angeles, CA 90071 Telephone: (213) 687-5000 Fax: (213) 687-5600 | Mark S. Chehi (I.D. No. 2855) One Rodney Square P.O. Box 636 Wilmington, DE 19899 Telephone: (302) 651-3000 Fax: (302) 651-3001 | John K. Lyons Jessica Kumar 155 N. Wacker Dr. Chicago, IL 60606 Telephone: (312) 407-0700 Fax: (312) 407-0411 | ||

| Counsel for Debtors and Debtors in Possession | ||||

Dated: Wilmington, Delaware

October 30, 2015

| 1 | The Debtors and the last four digits of their respective taxpayer identification numbers are as follows: Quiksilver, Inc. (9426), QS Wholesale, Inc. (8795), DC Direct, Inc. (8364), DC Shoes, Inc. (0965), Fidra, Inc. (8945), Hawk Designs, Inc. (1121), Mt. Waimea, Inc. (5846), Q.S. Optics, Inc. (2493), QS Retail, Inc. (0505), Quiksilver Entertainment, Inc. (9667), and Quiksilver Wetsuits, Inc. (9599). The address of the Debtors’ corporate headquarters is 5600 Argosy Circle, Huntington Beach, California 92649. |

DISCLAIMER

THE DISCLOSURE STATEMENT CONTAINS SUMMARIES OF CERTAIN PROVISIONS OF THE DEBTORS’ PLAN AND CERTAIN OTHER DOCUMENTS AND FINANCIAL INFORMATION. THE INFORMATION INCLUDED IN THE DISCLOSURE STATEMENT IS PROVIDED FOR THE PURPOSES OF SOLICITING ACCEPTANCES OF THE PLAN AND PROVIDING INFORMATION REGARDING RELATED TRANSACTIONS AND SHOULD NOT BE RELIED UPON FOR ANY PURPOSES OTHER THAN TO DETERMINE WHETHER AND HOW TO VOTE ON THE PLAN AND WHETHER TO PARTICIPATE IN RELATED TRANSACTIONS. THE DEBTORS BELIEVE THAT THESE SUMMARIES ARE FAIR AND ACCURATE. THE SUMMARIES OF THE FINANCIAL INFORMATION AND THE DOCUMENTS WHICH ARE ATTACHED TO, OR INCORPORATED BY REFERENCE IN, THE DISCLOSURE STATEMENT ARE QUALIFIED IN THEIR ENTIRETY BY REFERENCE TO SUCH INFORMATION AND DOCUMENTS. IN THE EVENT OF ANY INCONSISTENCY OR DISCREPANCY BETWEEN A DESCRIPTION IN THE DISCLOSURE STATEMENT AND THE TERMS AND PROVISIONS OF THE PLAN OR THE OTHER DOCUMENTS AND FINANCIAL INFORMATION INCORPORATED IN THE DISCLOSURE STATEMENT BY REFERENCE, THE PLAN OR THE OTHER DOCUMENTS AND FINANCIAL INFORMATION, AS THE CASE MAY BE, SHALL GOVERN FOR ALL PURPOSES.

THE STATEMENTS AND FINANCIAL INFORMATION CONTAINED IN THE DISCLOSURE STATEMENT HAVE BEEN MADE AS OF THE DATE OF THE DISCLOSURE STATEMENT UNLESS OTHERWISE SPECIFIED. HOLDERS OF CLAIMS AND INTERESTS REVIEWING THE DISCLOSURE STATEMENT SHOULD NOT ASSUME AT THE TIME OF SUCH REVIEW THAT THERE HAVE BEEN NO CHANGES IN THE FACTS SET FORTH IN THE DISCLOSURE STATEMENT SINCE THE DATE OF THE DISCLOSURE STATEMENT.

EACH HOLDER OF A CLAIM ENTITLED TO VOTE ON THE PLAN SHOULD CAREFULLY REVIEW THE PLAN AND THE DISCLOSURE STATEMENT IN THEIR ENTIRETIES BEFORE CASTING A BALLOT. THE DISCLOSURE STATEMENT DOES NOT CONSTITUTE LEGAL, BUSINESS, FINANCIAL, OR TAX ADVICE. ANY ENTITIES DESIRING ANY SUCH ADVICE SHOULD CONSULT WITH THEIR OWN ADVISORS.

NO REPRESENTATIONS CONCERNING THE DEBTORS OR THE VALUE OF THEIR PROPERTY HAVE BEEN AUTHORIZED BY THE DEBTORS OTHER THAN AS SET FORTH IN THE DISCLOSURE STATEMENT AND THE DOCUMENTS ATTACHED TO THE DISCLOSURE STATEMENT. ANY INFORMATION, REPRESENTATIONS, OR INDUCEMENTS MADE TO OBTAIN AN ACCEPTANCE OF THE PLAN WHICH ARE OTHER THAN AS SET FORTH, OR INCONSISTENT WITH, THE INFORMATION CONTAINED IN THE DISCLOSURE STATEMENT, THE DOCUMENTS ATTACHED TO THE DISCLOSURE STATEMENT, AND THE PLAN SHOULD NOT BE RELIED UPON BY ANY HOLDER OF A CLAIM OR INTEREST.

WITH RESPECT TO CONTESTED MATTERS, ADVERSARY PROCEEDINGS, AND OTHER PENDING, THREATENED, OR POTENTIAL LITIGATION OR OTHER

ii

ACTIONS, THE DISCLOSURE STATEMENT DOES NOT CONSTITUTE, AND MAY NOT BE CONSTRUED AS, AN ADMISSION OF FACT, LIABILITY, STIPULATION, OR WAIVER, BUT RATHER AS A STATEMENT MADE IN THE CONTEXT OF SETTLEMENT NEGOTIATIONS PURSUANT TO RULE 408 OF THE FEDERAL RULES OF EVIDENCE.

THE SECURITIES DESCRIBED IN THE DISCLOSURE STATEMENT TO BE ISSUED PURSUANT TO THE PLAN WILL BE ISSUED WITHOUT REGISTRATION UNDER THE SECURITIES ACT, AS AMENDED, OR ANY SIMILAR FEDERAL, STATE, OR LOCAL LAW, GENERALLY, IN RELIANCE ON THE EXEMPTIONS SET FORTH IN SECTION 1145 OF THE BANKRUPTCY CODE AND SECTION 4(a)(2) OF THE SECURITIES ACT, AS APPLICABLE.

THE DISCLOSURE STATEMENT HAS NOT BEEN APPROVED OR DISAPPROVED BY THE UNITED STATES SECURITIES AND EXCHANGE COMMISSION, NOR HAS THE COMMISSION COMMENTED UPON THE ACCURACY OR ADEQUACY OF THE STATEMENTS CONTAINED IN THE DISCLOSURE STATEMENT.

THE FINANCIAL INFORMATION CONTAINED IN OR INCORPORATED BY REFERENCE INTO THE DISCLOSURE STATEMENT HAS NOT BEEN AUDITED, UNLESS SPECIFICALLY INDICATED OTHERWISE.

THE FINANCIAL PROJECTIONS, ATTACHED HERETO ASEXHIBIT B AND DESCRIBED IN THE DISCLOSURE STATEMENT, HAVE BEEN PREPARED BY THE DEBTORS’ MANAGEMENT TOGETHER WITH THEIR ADVISORS. THE FINANCIAL PROJECTIONS, WHILE PRESENTED WITH NUMERICAL SPECIFICITY, ARE NECESSARILY BASED ON A VARIETY OF ESTIMATES AND ASSUMPTIONS WHICH, THOUGH CONSIDERED REASONABLE BY THE DEBTORS’ MANAGEMENT AND ITS ADVISORS, MAY NOT ULTIMATELY BE REALIZED, AND ARE INHERENTLY SUBJECT TO SIGNIFICANT BUSINESS, ECONOMIC, COMPETITIVE, INDUSTRY, REGULATORY, MARKET, AND FINANCIAL UNCERTAINTIES AND CONTINGENCIES, MANY OF WHICH ARE BEYOND THE DEBTORS’ CONTROL. THE DEBTORS CAUTION THAT NO REPRESENTATIONS CAN BE MADE AS TO THE ACCURACY OF THESE PROJECTIONS OR TO THE ABILITY TO ACHIEVE THE PROJECTED RESULTS. SOME ASSUMPTIONS INEVITABLY WILL NOT MATERIALIZE. FURTHER, EVENTS AND CIRCUMSTANCES OCCURRING SUBSEQUENT TO THE DATE ON WHICH THE FINANCIAL PROJECTIONS WERE PREPARED MAY BE DIFFERENT FROM THOSE ASSUMED OR, ALTERNATIVELY, MAY HAVE BEEN UNANTICIPATED, AND, THUS, THE OCCURRENCE OF THESE EVENTS MAY AFFECT FINANCIAL RESULTS IN A MATERIALLY ADVERSE OR MATERIALLY BENEFICIAL MANNER. THEREFORE, THE FINANCIAL PROJECTIONS MAY NOT BE RELIED UPON AS A GUARANTEE OR OTHER ASSURANCE OF THE ACTUAL RESULTS THAT WILL OCCUR. EXCEPT WHERE SPECIFICALLY NOTED, THE FINANCIAL INFORMATION CONTAINED HEREIN HAS NOT BEEN AUDITED BY A CERTIFIED PUBLIC ACCOUNTANT AND MAY NOT HAVE BEEN PREPARED IN ACCORDANCE WITH GENERALLY ACCEPTED ACCOUNTING PRINCIPLES (“GAAP”).

iii

PLEASE REFER TO ARTICLE VIII OF THE DISCLOSURE STATEMENT, ENTITLED “PLAN-RELATED RISK FACTORS AND ALTERNATIVES TO CONFIRMATION AND CONSUMMATION OF THE PLAN” FOR A DISCUSSION OF CERTAIN FACTORS THAT A CREDITOR VOTING ON THE PLAN SHOULD CONSIDER.

FOR A VOTE ON THE PLAN TO BE COUNTED, THE BALLOT INDICATING ACCEPTANCE OR REJECTION OF THE PLAN MUST BE RECEIVED BY KURTZMAN CARSON CONSULTANTS LLC, THE DEBTORS’ CLAIMS AND SOLICITATION AGENT, NO LATER THAN 4:00 P.M. PREVAILING EASTERN TIME, ON JANUARY 14, 2016. SUCH BALLOTS SHOULD BE CAST IN ACCORDANCE WITH THE SOLICITATION PROCEDURES DESCRIBED IN FURTHER DETAIL IN ARTICLE III OF THE DISCLOSURE STATEMENT. ANY BALLOT RECEIVED AFTER THE VOTING DEADLINE SHALL NOT BE COUNTED UNLESS OTHERWISE DETERMINED BY THE DEBTORS IN THEIR SOLE AND ABSOLUTE DISCRETION.

THE CONFIRMATION HEARING WILL COMMENCE ON [JANUARY ●], 2016 AT [●] PREVAILING EASTERN TIME, BEFORE THE HONORABLE BRENDON L. SHANNON, CHIEF UNITED STATES BANKRUPTCY JUDGE, IN THE UNITED STATES BANKRUPTCY COURT FOR THE DISTRICT OF DELAWARE, 824 NORTH MARKET STREET, WILMINGTON, DELAWARE 19801. THE DEBTORS MAY CONTINUE THE CONFIRMATION HEARING FROM TIME TO TIME WITHOUT FURTHER NOTICE OTHER THAN AN ADJOURNMENT ANNOUNCED IN OPEN COURT OR A NOTICE OF ADJOURNMENT FILED WITH THE BANKRUPTCY COURT AND SERVED ON THE MASTER SERVICE LIST AND THE ENTITIES WHO HAVE FILED AN OBJECTION TO THE PLAN. THE BANKRUPTCY COURT, IN ITS DISCRETION AND BEFORE THE CONFIRMATION HEARING, MAY PUT IN PLACE ADDITIONAL PROCEDURES GOVERNING THE CONFIRMATION HEARING. THE PLAN MAY BE MODIFIED, IF NECESSARY, PRIOR TO, DURING, OR AS A RESULT OF THE CONFIRMATION HEARING, WITHOUT FURTHER NOTICE TO PARTIES IN INTEREST.

THE PLAN OBJECTION DEADLINE IS JANUARY 14, 2016 AT 4:00 P.M. PREVAILING EASTERN TIME. ALL PLAN OBJECTIONS MUST BE FILED WITH THE BANKRUPTCY COURT AND SERVED ON THE DEBTORS AND CERTAIN OTHER PARTIES IN INTEREST IN ACCORDANCE WITH THE DISCLOSURE STATEMENT ORDER SO THAT THEY ARE RECEIVED ON OR BEFORE THE PLAN OBJECTION DEADLINE.

THE PLAN, THE DISCLOSURE STATEMENT, THE PLAN SUPPLEMENT AND EXHIBITS, ONCE FILED, AND OTHER DOCUMENTS AND MATERIALS RELATED THERETO MAY BE OBTAINED BY: (A) ACCESSING THE DEBTORS’ RESTRUCTURING WEBSITE AT http://www.kccllc.net/quiksilver, (B) EMAILING QuiksilverInfo@kccllc.com, (C) CALLING THE DEBTORS’ RESTRUCTURING HOTLINE at (877) 709-4757, WITHIN THE UNITED STATES OR CANADA, OR (424) 236-7235, OUTSIDE OF THE UNITED STATES OR CANADA, OR (D) ACCESSING THE COURT’S WEBSITE AT http://www.deb.uscourts.gov. COPIES OF SUCH DOCUMENTS AND MATERIALS MAY ALSO BE EXAMINED BETWEEN THE HOURS OF 8:00 AM AND 4:00 PM, MONDAY THROUGH FRIDAY, EXCLUDING FEDERAL HOLIDAYS, AT THE OFFICE OF THE CLERK OF THE COURT, 824 N. MARKET ST., 3RD FLOOR, WILMINGTON, DELAWARE 19801.

iv

EXECUTIVE SUMMARY

Quiksilver, Inc. QS Wholesale, Inc., DC Direct, Inc., DC Shoes, Inc., Fidra, Inc., Hawk Designs, Inc., Mt. Waimea, Inc., Q.S. Optics, Inc., QS Retail, Inc., Quiksilver Entertainment, Inc., and Quiksilver Wetsuits, Inc., the debtors and debtors-in-possession in the above-captioned cases (collectively, the “Debtors”), together with their direct and indirect non-debtor subsidiaries (collectively, with the Debtors, the “Company”), operate in more than 115 countries and comprise one of the world’s leading outdoor sports lifestyle companies.

The Debtors’ proposal for the reorganization of their business is set forth in theJoint Chapter 11 Plan of Reorganization of Quiksilver, Inc. and its affiliated Debtors and Debtors in Possession (the “Plan”) [Docket No. 292], a copy of which is attached hereto asExhibit A. As described below, the Plan is supported and sponsored by certain funds managed by affiliates of Oaktree Capital Management (collectively, “Oaktree”), as Plan Sponsor,2 under the Plan Sponsor Agreement, and Backstop Parties, under the Backstop Commitment Letter.

This Disclosure Statement contains, among other things, descriptions and summaries of provisions of the Debtors’ proposed Plan, as filed on the date hereof with the United States Bankruptcy Court for the District of Delaware. Certain provisions of the Plan, and thus the description and summaries contained herein, may be the subject of continuing negotiations among the Debtors and various parties. Accordingly, the Debtors reserve the right to modify the Plan consistent with section 1127 of the Bankruptcy Code, Federal Rule of Bankruptcy Procedure 3019, and Article 13.3 of the Plan.

The Plan provides for an equitable distribution of recoveries to the Debtors’ creditors, preserves the value of the Debtors’ business as a going concern, and preserves the jobs of employees. The Debtors and the Plan Sponsor believe that any alternative to confirmation of the Plan, such as liquidation or attempts by another party in interest to file a plan, could result in significant delays, litigation and costs, the loss of jobs by the Debtors’ employees, and/or impaired recoveries. Moreover, the Debtors and the Plan Sponsor believe that the Debtors’ creditors will receive greater and earlier recoveries under the Plan than those that would be achieved in liquidation or under an alternative plan.For these reasons, the Debtors and the Plan Sponsor urge you to return your ballot accepting the Plan.

| 2 | Capitalized terms not otherwise defined in this Disclosure Statement shall have the meanings ascribed to them in the Plan. |

v

Plan Overview and Summary of Distributions

The following summary3 is a general overview only and is qualified in its entirety by, and should be read in conjunction with, the more detailed discussions, information, and financial statements and notes thereto appearing elsewhere in this Disclosure Statement with respect to the Plan and the Plan itself.

| A. | Overview and Funding of the Plan |

The Plan is supported and sponsored by Oaktree, as Plan Sponsor, under the Plan Sponsor Agreement, and Backstop Parties, under the Backstop Commitment Letter. The Plan provides for the following key economic terms and mechanics:

| • | Issuance of New Quiksilver Common Stock: On the Effective Date, Reorganized Quiksilver will authorize and issue the New Quiksilver Common Stock. Shares of New Quiksilver Common Stock will be allocated as follows: (a) first, to holders of Allowed Secured Notes Claims; (b) second, up to [●]% of New Quiksilver Common Stock to Rights Offering Participants under the Rights Offerings, which, for the avoidance of doubt, shall dilute subpart (a); and (c) third, any New Quiksilver Common Stock issued to the Backstop Parties under the Backstop Commitment Letter, which, for the avoidance of doubt, shall dilute subparts (a) and (b). |

| • | Cancellation of Old Quiksilver Securities and Agreements: The Euro Notes Guaranty Claims shall be Reinstated and the Holders of such Claims shall be Unimpaired. Except with respect to the Euro Notes Guaranty Claims or as otherwise provided in the Plan, on the Effective Date, the Old Quiksilver Securities, which includes the Secured Notes, the Unsecured Notes, and the Old Quiksilver Common Stock, along with any other note, bond, indenture, Certificate, or other instrument or document evidencing or creating any indebtedness or obligation of or ownership interest in the Debtors (including the Indentures), shall be cancelled, and any obligations of, Claims against, and/or Interests in the Debtors under, relating, or pertaining to the foregoing, other than the Euro Notes, shall be released and discharged and cancelled. |

| • | Exit Financing: On the Effective Date, the Reorganized Debtors, as borrowers, will enter into the Exit Facility, an asset-based revolving credit facility in the principal amount of up to $[120] million pursuant to a new credit agreement with the Exit Lenders, which may include the DIP Lenders. The proceeds of the Exit Financing will fund (1) first, distributions under the Plan on account of the DIP ABL Facility Claims and (2) second, distributions under the Plan on account of DIP Term Facility Claims. |

| • | Exit Rights Offering: Each Eligible Holder of an Allowed Secured Notes Claim, or its affiliated Eligible Affiliate, will have the right to exercise subscription rights for the |

| 3 | These summaries below are qualified in their entirety by reference to the provisions of the Plan. For a more detailed description of the terms and provisions of the Plan, see Article VI below. |

vi

purchase of up to $122.5 million of New Quiksilver Common Stock. The proceeds of the Exit Rights Offering will be used to fund (1) first, distributions under the Plan on account of DIP Term Loan Facility Claims, (2) second, the Unsecured Cash Consideration of $7.5 million, and (3) third, any payments required on the Effective Date under the Plan. The Exit Rights Offering will run concurrently with solicitation on the Plan and will be consummated on the Effective Date. The Exit Rights Offering is backstopped by the Backstop Parties to the extent set forth in the Backstop Commitment Letter. |

| • | Unsecured Cash Consideration: The proceeds of the Exit Rights Offering will be used, in part, to fund the Unsecured Cash Consideration of $7.5 million pursuant to the Plan Sponsor Agreement. The Unsecured Cash Consideration will fund recoveries to Holders of Allowed Unsecured Notes Claims and Allowed General Unsecured Claims. |

| • | Euro Notes Exchange Offer: The Company will proffer an exchange offer to holders of Euro Notes, the terms and conditions of which will be set forth in a document contained in the Plan Supplement. The Euro Notes Exchange Offer will be consummated on the Effective Date to the extent the conditions precedent to such exchange offer are met. |

| • | Euro Notes Rights Offering: Each Eligible Holder of an Allowed Secured Notes Claim, or its affiliated Eligible Affiliate, will have the right to exercise subscription rights for the purchase of up to €50.0 million of New Quiksilver Common Stock, the proceeds of which will be used to consummate the Euro Notes Exchange Offer. The Euro Notes Rights Offering be consummated on the Effective Date. The Euro Notes Rights Offering is backstopped by the Backstop Parties to the extent set forth in the Backstop Commitment Letter. |

| • | Backstop of the Rights Offerings: Pursuant to the Backstop Commitment Letter, on or before the Effective Date, the Backstop Parties will backstop the Rights Offerings by providing up to $122.5 million for the Exit Rights Offering and up to €50 million for the Euro Notes Rights Offering. |

The Reorganized Debtors’ debt at emergence shall comprise of the following: (i) the Exit Facility of up to $[120] million, (ii) an estimated €150 million of Euro Notes,4 and (iii) $32 million of European lines of credit and other borrowing facilities. At emergence, the Reorganized Debtors will have liquidity of approximately $[●] due to a combination of cash-on-hand and availability under the Exit Facility.

| 4 | The Reorganized Debtors’ debt at emergence with respect to the Euro Notes is an estimate subject to the consummation of, and participation rates with respect to, the Euro Notes Exchange Offer. |

vii

The Reorganized Debtors’ capital structure at emergence will consist of the following:

| Debt | ||||

Exit Facility | $ | [120] million | ||

Euro Notes | € | 150 million | 5 | |

Eurofactor Agreement and Unsecured Lines of Credit | $ | 32 million | ||

| Equity | ||||

New Quiksilver Common Stock | $ | [●] | ||

| B. | Summary of Treatment of Claims and Interests under the Plan. |

The Plan contains separate classes for Holders of Claims and Interests. Pursuant to section 1122 of the Bankruptcy Code, set forth below is a designation of classes of Claims and Interests. A Claim or Interest is placed in a particular Class for the purposes of voting on the Plan and of receiving distributions pursuant to the Plan only to the extent that such Claim or Interest is an Allowed Claim or an Allowed Interest in that Class and such Claim or Interest has not been paid, released, or otherwise settled prior to the Effective Date. In accordance with section 1123(a)(1) of the Bankruptcy Code, Administrative Claims, Professional Claims, DIP ABL Facility Claims, DIP Term Facility Claims, and Priority Tax Claims have not been classified. The treatment of all such unclassified claims is set forth in Article II of the Plan.

The table below summarizes the classification and treatment of Claims and Interests under the Plan. These summaries are qualified in their entirety by reference to the provisions of the Plan. For a more detailed description of the terms and provisions of the Plan, see Article VI below. The tables below also set forth the estimated percentage recovery for Holders of Claims and Interests in each Class, and the Debtors’ estimates of the amount of Claims that will ultimately become Allowed in each Class based upon (a) review by the Debtors of their books and records, (b) all Claims scheduled by the Debtors, and (c) consideration of the provisions of the Plan that affect the allowance of certain Claims.6 The aggregate Claim amounts in each Class and the estimated percentage recoveries in the table below are set forth for the Debtors on a consolidated basis.

| 5 | The Reorganized Debtors’ debt at emergence with respect to the Euro Notes is an estimate subject to the consummation of, and participation rates with respect to, the Euro Notes Exchange Offer. |

| 6 | Although the Debtors believe that the estimated recoveries are reasonable, there is no assurance that the actual amounts of Allowed Claims in each Class will not materially exceed the estimated aggregate amounts shown in the table above. The actual recoveries under the Plan will depend upon a variety of factors, including: i) the reconciliation of asserted claims, ii) cure amounts, iii) whether, and in what amount and with what priority, contingent Claims against the Debtors become non-contingent and fixed; and iv) whether, and to what extent, Disputed Claims are resolved in favor of the Debtors. Accordingly, no representation can be or is being made with respect to whether each estimated recovery amount shown in the table above will be realized. |

viii

Class Description | Status | Proposed Treatment | ||

Unclassified Claims | ||||

DIP ABL Facility Claims

Estimated Recovery: 100% Estimated Amount: $60.0 million | Unclassified | DIP ABL Facility Claims consist of Claims of each of the Debtors arising under, derived from, based upon, or as a result of the DIP ABL Facility. Except to the extent that a Holder of a DIP ABL Facility Claim agrees to a less favorable treatment, in full and final satisfaction, settlement, release, and discharge of and in exchange for each and every DIP ABL Facility Claim, Holders of DIP ABL Facility Claim shall be paid in full in Cash from the proceeds of the Exit Facility on the Effective Date, such payments to be distributed to the DIP ABL Agent for the ratable benefit of the Holders of DIP ABL Facility Claim. To the extent that any Letter of Credit remains undrawn as of the Effective Date, the Debtors, with the Plan Sponsor’s consent, shall (i) cause that Letter of Credit to be replaced with a letter of credit issued under the Exit Facility, [(ii) collateralize that Letter of Credit with Cash in an amount equal to 105% of its Face Amount,] (iii) provide a back-to-back letter of credit to the Letter of Credit Issuer on terms and from a financial institution reasonably acceptable to the Letter of Credit Issuer, or (iv) provide such other treatment as the Letter of Credit Issuer shall agree in its sole discretion.

| ||

DIP Term Loan Facility Claims

Estimated Recovery: 100% Estimated Amount: $115.0 million | Unclassified | DIP Term Loan Facility Claims consist of Claims of each of the Debtors arising under, derived from, based upon, or as a result of the DIP Term Loan Facility.

Except to the extent that a Holder of a DIP Term Loan Facility Claim agrees to a less favorable treatment, in full and final |

ix

Class Description | Status | Proposed Treatment | ||

satisfaction, settlement, release, and discharge of and in exchange for each and every DIP Term Loan Facility Claim, Holders of DIP Term Loan Facility Claims shall be paid in full in Cash from the proceeds of the Exit Facility (after satisfying the DIP ABL Facility Claims) and the Exit Rights Offering on the Effective Date, such payments to be distributed to the DIP Term Loan Agent for the ratable benefit of the Holders of DIP Term Loan Facility Claims.

| ||||

Administrative Claims

Estimated Recovery: 100% Estimated Amount: $7.0 million | Unclassified | Administrative Claims consist of the Administrative Claims of each of the Debtors.

Except to the extent that the Debtors, with the consent of the Plan Sponsor, or the Reorganized Debtors, as applicable, and a Holder of an Allowed Administrative Claim agree to a less favorable treatment, a Holder of an Allowed Administrative Claim (other than a DIP Claim, which shall be subject to Article 2.2 of the Plan, or a Professional Claim, which shall be subject to Article 2.3 of the Plan) shall receive, in full satisfaction, settlement, release, and discharge of, and in exchange for, such Administrative Claim, Cash equal to the unpaid portion of such Allowed Administrative Claim either (a) on the later of (x) the Initial Distribution Date; or (y) the first Periodic Distribution Date occurring after the later of (i) 30 days after the date when an Administrative Claim becomes an Allowed Administrative Claim or (ii) 30 days after the date when an Administrative Claim becomes payable pursuant to any agreement between the Debtors (or the Reorganized Debtors) and the Holder of such Administrative Claim; or (b) if the Allowed Administrative Claim is based on liabilities incurred by |

x

Class Description | Status | Proposed Treatment | ||

| the Debtors in the ordinary course of their business after the Petition Date, in the ordinary course of business in accordance with the terms and conditions of the particular transaction giving rise to such Allowed Administrative Claims, without any further action by the Holders of such Allowed Administrative Claims; provided, however, that other than Holders of (i) a DIP Facility Claim, (ii) a Professional Claim, (iii) an Administrative Claim Allowed by an order of the Bankruptcy Court on or before the Effective Date, or (iv) an Administrative Claim that is not Disputed and arose in the ordinary course of business and was paid or is to be paid in accordance with the terms and conditions of the particular transaction giving rise to such Administrative Claim, the Holder of any Administrative Claim shall have filed a proof of Claim form no later than the Administrative Claims Bar Date and such Claim shall have become an Allowed Claim. | ||||

Priority Tax Claims

Estimated Recovery: 100% Estimated Amount: $2.5 million | Unclassified | Priority Tax Claims consist of the Priority Tax Claims of each of the Debtors.

On the later of (a) the Initial Distribution Date or (b) the first Periodic Distribution Date occurring after the later of, (i) 30 days after the date when a Priority Tax Claim becomes an Allowed Priority Tax Claim or (ii) 30 days after the date when a Priority Tax Claim becomes payable pursuant to any agreement between the Debtors (or the Reorganized Debtors) and the Holder of such Priority Tax Claim, except to the extent that the Debtors (or Reorganized Debtors) and a Holder of an Allowed Priority Tax Claim agree to a less favorable treatment, each Holder of an Allowed Priority Tax Claim due and payable on or before the Effective Date shall receive one of the following |

xi

Class Description | Status | Proposed Treatment | ||

treatments on account of such Claim: (a) Cash in an amount equal to the amount of such Allowed Priority Tax Claim, (b) Cash in an amount agreed to by the Debtors (or the Reorganized Debtors) and such Holder, provided, however, that such parties may further agree for the payment of such Allowed Priority Tax Claim to occur at a later date, or (c) at the sole option of the Debtors, Cash in the aggregate amount of such Allowed Priority Tax Claim payable in installment payments over a period of not more than five (5) years after the Petition Date pursuant to section 1129(a)(9)(C) of the Bankruptcy Code. To the extent any Allowed Priority Tax Claim is not due and owing on the Effective Date, such Claim shall be paid in full in Cash in accordance with the terms of any agreement between the Debtors and the Holder of such Claim, or as may be due and payable under applicable non-bankruptcy law or in the ordinary course of business.

| ||||

Classified Claims | ||||

Class 1: Other Priority Claims

Estimated Recovery: 100% Estimated Amount: $1.0 million | Unimpaired | Class 1 consists of the Other Priority Claims of each of the Debtors.

Except as otherwise provided in and subject to Article 9.5 of the Plan, and except to the extent that a Holder of an Allowed Class 1 Claim agrees to a less favorable treatment, in full and final satisfaction, settlement, release, and discharge of and in exchange for each and every Allowed Class 1 Claim, each such Holder of an Allowed Class 1 Claim shall be paid in full in Cash on the later of (a) the Initial Distribution Date or (b) the first Periodic Distribution Date occurring after the later of (i) 30 days after the date when a Class 1 Claim becomes an Allowed Class 1 Claim or (ii) 30 days |

xii

Class Description | Status | Proposed Treatment | ||

after the date when a Class 1 Claim becomes payable pursuant to any agreement between the Debtors (or the Reorganized Debtors) and the Holder of such Class 1 Claim; provided, however, that Other Priority Claims that arise in the ordinary course of the Debtors’ business and which are not due and payable on or before the Effective Date shall be paid in the ordinary course of business in accordance with the terms thereof.

| ||||

Class 2: Other Secured Claims

Estimated Recovery: 100% Estimated Amount: $2.5 million | Unimpaired | Class 2 consists of the Other Secured Claims of each of the Debtors.

Except as otherwise provided in and subject to Article 9.5 of the Plan, and except to the extent that a Holder of an Allowed Class 2 Claim agrees to a less favorable treatment, in full and final satisfaction, settlement, release and discharge of and in exchange for each and every Allowed Class 2 Claim, each such Holder of an Allowed Class 2 Claim shall, at the sole election of the Debtors or the Reorganized Debtors, with the consent of the Plan Sponsor, as applicable:

(i) have its Allowed Class 2 Claim Reinstated and rendered Unimpaired on the Effective Date in accordance with section 1124(2) of the Bankruptcy Code, notwithstanding any contractual provision or applicable non-bankruptcy law that entitles the Holder of an Allowed Class 2 Claim to demand or receive payment of such Allowed Class 2 Claim prior to the stated maturity of such Allowed Class 2 Claim from and after the occurrence of a default; or

(ii) be paid in full in Cash in an amount equal to such Allowed Class 2 Claim, including postpetition interest, if any, on such Allowed Class 2 Claim required to be paid pursuant to section 506 of the Bankruptcy Code, on the later of (a) the |

xiii

Class Description | Status | Proposed Treatment | ||

Initial Distribution Date or (b) the first Periodic Distribution Date occurring after the later of (i) 30 days after the date when a Class 2 Claim becomes an Allowed Class 2 Claim or (ii) 30 days after the date when a Class 2 Claim becomes payable pursuant to any agreement between the Debtors (or the Reorganized Debtors) and the Holder of such Class 2 Claim.

| ||||

Class 3: Euro Notes Guaranty Claims

Estimated Recovery: 100% Estimated Amount: $227.7 million | Unimpaired | Class 3 consists of the Euro Notes Guaranty Claims of each of the Debtors.

Except to the extent that a Holder of an Allowed Class 3 Claim agrees to a less favorable treatment, in full and final satisfaction, settlement, release and discharge of and in exchange for each and every Allowed Class 3 Claim, each such Holder of an Allowed Class 3 Claim shall have its Allowed Class 3 Claim Reinstated and rendered Unimpaired in accordance with section 1124(2) of the Bankruptcy Code, notwithstanding any contractual provision or applicable non-bankruptcy law that entitles the Holder of an Allowed Class 3 Claim to demand or receive payment of such Allowed Class 3 Claim prior to the stated maturity of such Allowed Class 3 Claim from and after the occurrence of a default.

| ||

Class 4: Secured Notes Claims

Estimated Recovery: [●]% Estimated Amount: $282.3 million7 | Impaired | Class 4 consists of the Secured Notes Claims of each of the Debtors.

The Secured Notes Claims are applicable as to certain of the Debtors, including Quiksilver, Inc., QS Wholesale, Inc., DC Shoes, Inc., Hawk Designs, Inc., and QS Retail, Inc. |

| 7 | The Estimated Amount for the Secured Notes Claims set forth in this Disclosure Statement is an estimate based on outstanding principal and prepetition interest (accrued from August 1, 2015 through September 8, 2015) on the Secured Notes. |

xiv

Class Description | Status | Proposed Treatment | ||

Except to the extent that a Holder of an Allowed Class 4 Claim agrees to a less favorable treatment, in full and final satisfaction, settlement, release, and discharge of and in exchange for each and every Allowed Class 4 Claim, on the Effective Date, each Holder of an Allowed Class 4 Claim shall receive on account of such Holder’s Secured Notes Claims its Pro Rata share, based on the aggregate amount of Allowed Class 4 Claims, of the New Quiksilver Common Stock, subject to dilution in accordance with the New Quiksilver Common Stock Allocation.

| ||||

Class 5-A: Unsecured Notes Claims

Estimated Recovery: [●]% Estimated Amount: $227.4 million | Impaired | Class 5-A consists of the Unsecured Notes Claims of each of the Debtors.

The Unecured Notes Claims are applicable as to certain of the Debtors, including Quiksilver, Inc., QS Wholesale, Inc., DC Shoes, Inc., Hawk Designs, Inc., and QS Retail, Inc.

Except to the extent that a Holder of an Allowed Class 5-A Claim agrees to a less favorable treatment, in full and final satisfaction, settlement, release, and discharge of and in exchange for each and every Allowed Class 5-A Claim, on the Initial Distribution Date, each Holder of an Allowed Class 5-A Claim shall receive its Pro Rata share, based on the aggregate amount of Allowed Class 5-A Claims, of the Notes Cash Consideration.

| ||

Class 5-B: General Unsecured Claims

Estimated Recovery: [●]% Estimated Amount: $49.0 million | Impaired | Class 5-B consists of the General Unsecured Claims of each of the Debtors. Except as otherwise provided in and subject to Article 9.5 of the Plan, and except to the extent that a Holder of an Allowed Class 5-B Claim agrees to a less favorable treatment, in full and final |

xv

Class Description | Status | Proposed Treatment | ||

satisfaction, settlement, release, and discharge of and in exchange for each and every Allowed Class 5-B Claim, each Holder of an Allowed Class 5-B Claim shall receive its Pro Rata share, based on the aggregate amount of Allowed Class 5-B Claims, of the GUC Cash Consideration on the later of (a) the Initial Distribution Date or (b) the first Periodic Distribution Date occurring after the later of, (i) 30 days after the date when a Class 5-B Claim becomes an Allowed Class 5-B Claim or (ii) 30 days after the date when a Class 5-B Claim becomes payable pursuant to any agreement between the Debtors (or the Reorganized Debtors) and the Holder of such Class 5-B Claim.

General Unsecured Claims are only applicable as to certain Debtors. Those Debtors, along with the corresponding Estimated Amount of General Unsecured Claims, are listed below:

1. Quiksilver, Inc.: $6.0 million

2. QS Wholesale, Inc.: $20.0 million

3. DC Shoes, Inc.: $6.0 million

4. QS Retail, Inc. $17.0 million

| ||||

Class 6: Intercompany Claims

Estimated Recovery: 0-100% Estimated Amount: $[●] | Unimpaired | Class 6 consists of the Intercompany Claims of each of the Debtors.

On the Effective Date, all net Allowed Class 6 Claims (taking into account any setoffs of Intercompany Claims) held by the Debtors between and among the Debtors and/or any Affiliates of the Debtors shall, at the election of the Debtors, with the consent of the Plan Sponsor, or the Reorganized Debtors, as applicable, be either (i) Reinstated, or (ii) released, waived, and discharged.

| ||

| Class 7: Intercompany Interests | Unimpaired | Class 7 consists of the Intercompany Interests of each of the Debtors. |

xvi

Class Description | Status | Proposed Treatment | ||

| Estimated Recovery: 0-100% | On the Effective Date, all Class 7 Interests held by the Debtors shall, at the election of the Debtors, with the consent of the Plan Sponsor, or the Reorganized Debtors, as applicable, be either (i) Reinstated, or (ii) deemed automatically cancelled, released, and extinguished. For the avoidance of doubt, any Interest in any non-Debtor subsidiary owned by a Debtor shall continue to be owned by the applicable Reorganized Debtor.

| |||

Class 8: Subordinated Claims

Estimated Recovery: 0% Estimated Amount: $0 | Impaired | Class 8 consists of the Subordinated Claims of each of the Debtors.

Holders of Allowed Class 8 Claims shall not receive any distributions on account of such Allowed Class 8 Claims, and on the Effective Date, all Allowed Class 8 Claims shall be released, waived, and discharged.

| ||

Class 9: Interests in Quiksilver

Estimated Recovery: 0% | Impaired | Class 9 consists of the Interests in Quiksilver.

On the Effective Date, Allowed Class 9 Interests shall be deemed automatically cancelled, released, and extinguished without further action by the Debtors or the Reorganized Debtors and the obligations of the Debtors and the Reorganized Debtors thereunder shall be discharged. |

THE DEBTORS AND THE PLAN SPONSOR BELIEVE THAT THE PLAN PROVIDES THE BEST RECOVERIES POSSIBLE FOR THE HOLDERS OF CLAIMS. THE DEBTORS AND THE PLAN SPONSORSTRONGLY RECOMMEND THAT YOU VOTE TOACCEPT THE PLAN.

A VOTE TO ACCEPT THE PLAN OR A DECISION TO ABSTAIN FROM VOTING ON THE PLAN CONSTITUTES YOUR CONSENT TO THE RELEASE SET FORTH IN ARTICLE X OF THE PLAN OF THE PARTIES SPECIFIED IN ARTICLE X OF THE PLAN UNLESS YOU OPT OUT OF SUCH RELEASE IN ACCORDANCE WITH THE PROCEDURES SET FORTH IN YOUR BALLOT.

xvii

TABLE OF CONTENTS

ARTICLE I. INTRODUCTION | 1 | |||||

A. | Rules of Interpretation | 2 | ||||

ARTICLE II. OVERVIEW OF THE PLAN | 2 | |||||

A. | Summary of the Plan | 2 | ||||

B. | Unclassified Claims | 4 | ||||

C. | Treatment of Claims and Interests Under the Plan | 4 | ||||

D. | Liquidation and Valuation Analyses | 5 | ||||

ARTICLE III. VOTING PROCEDURES | 5 | |||||

A. | Classes Entitled to Vote | 5 | ||||

B. | Voting Procedures | 6 | ||||

C. | Rights Offering Procedures | 7 | ||||

ARTICLE IV. GENERAL INFORMATION | 9 | |||||

A. | Overview of the Company’s Business | 9 | ||||

B. | The Company’s Corporate Structure | 11 | ||||

C. | The Company’s Board of Directors | 11 | ||||

D. | Executive Officers and Senior Management of the Debtors | 13 | ||||

E. | The Debtors’ Workforce | 14 | ||||

F. | Employee Benefit Plans | 15 | ||||

G. | The Company’s Prepetition Capital Structure | 16 | ||||

ARTICLE V. THE CHAPTER 11 CASES | 21 | |||||

A. | Events Leading to the Commencement of the Chapter 11 Cases | 21 | ||||

B. | Summary of Material Prepetition Legal Proceedings | 26 | ||||

C. | Stabilization of Operations/First Day Relief | 27 | ||||

D. | Appointment of the Creditors’ Committee | 30 | ||||

E. | Postpetition Financing | 30 | ||||

F. | Plan Sponsor Agreement | 32 | ||||

G. | Store Closing and Similar Sales | 32 | ||||

H. | Schedules and Statements | 33 | ||||

I. | Backstop Commitment Letter | 33 | ||||

J. | Analyzing Executory Contracts and Unexpired Leases | 34 | ||||

K. | Management Incentive Compensation Plan | 34 | ||||

L. | Analysis and Resolution of Claims | 34 | ||||

ARTICLE VI. PLAN SUMMARY | 35 | |||||

A. | Overview of Chapter 11 | 35 | ||||

B. | Overall Structure of the Plan | 37 | ||||

C. | Classification, Treatment, and Voting of Claims and Interests | 40 | ||||

D. | Acceptance | 45 | ||||

E. | Means for Implementation of the Plan | 46 | ||||

F. | Unexpired Leases and Executory Contracts | 54 | ||||

G. | Procedures for Resolving Disputed Claims and Interests | 59 | ||||

xviii

H. | Provisions Governing Distributions | 62 | ||||

I. | Effect of the Plan on Claims and Interests | 68 | ||||

J. | Conditions Precedent | 72 | ||||

K. | Retention of Jurisdiction | 74 | ||||

L. | Miscellaneous Provisions | 76 | ||||

ARTICLE VII. STATUTORY REQUIREMENTS FOR CONFIRMATION OF THE PLAN | 80 | |||||

A. | The Confirmation Hearing | 80 | ||||

B. | Confirmation Standards | 80 | ||||

C. | Liquidation Analysis | 82 | ||||

D. | Valuation Analysis | 83 | ||||

E. | Financial Feasibility | 83 | ||||

F. | Acceptance by Impaired Classes | 83 | ||||

G. | Confirmation Without Acceptance by All Impaired Classes | 83 | ||||

ARTICLE VIII. PLAN-RELATED RISK FACTORS AND ALTERNATIVES TO CONFIRMATION AND CONSUMMATION OF THE PLAN | 85 | |||||

A. | General | 85 | ||||

B. | Certain Bankruptcy Considerations | 85 | ||||

C. | Claims Estimations | 86 | ||||

D. | Risk Factors That May Affect the Value of the Securities to Be Issued Under the Plan | 86 | ||||

E. | Bankruptcy-Specific Risk Factors That Could Negatively Impact the Debtors’ Business | 88 | ||||

F. | Additional Risk Factors That Could Negatively Impact the Company’s Business | 94 | ||||

G. | Risks Associated with Forward-Looking Statements | 105 | ||||

H. | Disclosure Statement Disclaimer | 106 | ||||

I. | Liquidation Under Chapter 7 | 108 | ||||

ARTICLE IX. EXEMPTIONS FROM SECURITIES ACT REGISTRATION | 108 | |||||

A. | Securities Issued in Reliance on Section 1145 of the Bankruptcy Code and Section 4(A)(2) of the Securities Act | 108 | ||||

B. | Restricted Securities | 110 | ||||

ARTICLE X. CERTAIN UNITED STATES FEDERAL INCOME TAX CONSEQUENCES | 110 | |||||

A. | Certain United States Federal Income Tax Consequences to the Debtors | 112 | ||||

B. | Certain United States Federal Income Tax Consequences to Holders of Claims | 113 | ||||

C. | Importance of Obtaining Professional Tax Advice | 120 | ||||

ARTICLE XI. ALTERNATIVES TO CONFIRMATION AND CONSUMMATION OF THE PLAN | 120 | |||||

A. | Continuation of the Bankruptcy Cases | 120 | ||||

B. | Alternative Plans of Reorganization | 121 | ||||

xix

ARTICLE XII. RECOMMENDATION | 121 | |||||

A. | Hearing on and Objections to Confirmation | 121 | ||||

B. | Recommendation | 121 | ||||

xx

EXHIBITS

| Exhibit A | Plan of Reorganization Pursuant to Chapter 11 Of the Bankruptcy Code Proposed by the Debtors | |

| Exhibit B | [Financial Projections] | |

| Exhibit C | [Liquidation Analysis] | |

| Exhibit D | Corporate Structure Chart | |

| Exhibit E | Proposed Disclosure Statement Approval Order | |

xxi

ARTICLE I.

INTRODUCTION

The Debtors, together with their direct and indirect subsidiaries, operate in more than 115 countries and comprise one of the world’s leading outdoor sports lifestyle companies.

On September 9, 2015, the Debtors filed voluntary petitions for relief under the Bankruptcy Code and commenced the Chapter 11 Cases. The Debtors’ cases are pending in the Bankruptcy Court and are jointly administered under Case No. 15-11880. No trustee has been appointed in the Chapter 11 Cases. On September 22, 2015, the United States Trustee appointed the Creditors’ Committee pursuant to section 1102 of the Bankruptcy Code.

The Debtors submit this Disclosure Statement pursuant to section 1125 of the Bankruptcy Code for purposes of soliciting votes to accept or reject the Plan, a copy of which is attached to the Disclosure Statement asExhibit A.

This Disclosure Statement sets forth certain information regarding the Debtors’ prepetition operations and financial history, their reasons for seeking protection under chapter 11, and significant events that have occurred during the Chapter 11 Cases. This Disclosure Statement also describes certain terms and provisions of the Plan, certain effects of confirmation of the Plan, certain risk factors associated with the Plan and the securities to be issued under the Plan, and the manner in which distributions will be made under the Plan. In addition, this Disclosure Statement discusses the requirements for confirmation of the Plan and the voting procedures that Holders of Claims entitled to vote on the Plan must follow for their votes to be counted. All capitalized terms used and not otherwise defined in this Disclosure Statement shall have the meanings ascribed to such terms in the Plan.

FOR A DESCRIPTION OF THE PLAN AND THE VARIOUS RISKS AND OTHER FACTORS PERTAINING TO THE PLAN AS IT RELATES TO HOLDERS OF CLAIMS AND INTERESTS, PLEASE SEEARTICLES VIII ANDX HEREIN.

THIS DISCLOSURE STATEMENT CONTAINS SUMMARIES OF CERTAIN PROVISIONS OF THE PLAN, CERTAIN STATUTORY PROVISIONS, CERTAIN DOCUMENTS RELATED TO THE PLAN, CERTAIN EVENTS IN THE CHAPTER 11 CASE, AND CERTAIN FINANCIAL INFORMATION. TO THE EXTENT ANY PORTION OF THIS DISCLOSURE STATEMENT CONFLICTS WITH THE PLAN, THE PLAN SHALL GOVERN. ALTHOUGH THE DEBTORS BELIEVE THAT THE SUMMARIES CONTAINED HEREIN ARE FAIR AND ACCURATE, SUCH SUMMARIES ARE QUALIFIED TO THE EXTENT THAT THEY DO NOT SET FORTH THE ENTIRE TEXT OF THE DOCUMENTS OR STATUTORY PROVISIONS THEY ARE SUMMARIZING. THE DEBTORS’ MANAGEMENT HAS PROVIDED FACTUAL INFORMATION CONTAINED IN THIS DISCLOSURE STATEMENT, EXCEPT WHERE OTHERWISE SPECIFICALLY NOTED. THE DEBTORS DO NOT WARRANT OR REPRESENT THAT THE INFORMATION CONTAINED HEREIN, INCLUDING FINANCIAL INFORMATION, IS WITHOUT ANY MATERIAL INACCURACY OR OMISSION.

| A. | Rules of Interpretation |

For purposes of the Plan, unless otherwise provided in the Plan: (a) whenever from the context it is appropriate, each term, whether stated in the singular or the plural, shall include both the singular and the plural; (b) each pronoun stated in the masculine, feminine, or neuter includes the masculine, feminine, and neuter; (c) any reference in the Plan to an existing document or schedule filed or to be filed means such document or schedule, as it may have been or may be amended, modified, or supplemented; (d) any reference to an entity as a Holder of a Claim or Interest includes that entity’s successors and assigns; (e) all references in the Plan to Sections, Articles, and Exhibits are references to Sections, Articles, and Exhibits of or to the Plan; (f) the words “herein,” “hereunder,” and “hereto” refer to the Plan in its entirety rather than to a particular portion of the Plan; (g) captions and headings to Articles and Sections are inserted for convenience of reference only and are not intended to be a part of or to affect the interpretation of the Plan; (h) the rules of construction set forth in section 102 of the Bankruptcy Code shall apply; (i) to the extent the Disclosure Statement is inconsistent with the terms of the Plan, the Plan shall control; (j) to the extent the Plan is inconsistent with the Confirmation Order, the Confirmation Order shall control; and (k) any immaterial effectuating provision may be interpreted by the Reorganized Debtor in a manner that is consistent with the overall purpose and intent of the Plan without further Final Order of the Bankruptcy Court.

The Plan and the Disclosure Statement are the product of extensive discussions and negotiations between and among the Debtors and the Plan Sponsor. Each of the foregoing was represented by counsel, who either (a) participated in the formulation and documentation of, or (b) was afforded the opportunity to review and provide comments on, the Plan, the Disclosure Statement, and the documents ancillary thereto. Accordingly, the general rule of contract construction known as “contra proferentem” shall not apply to the construction or interpretation of any provision of the Plan, the Disclosure Statement, or any contract, instrument, release, indenture, exhibit, or other agreement or document generated in connection herewith.

ARTICLE II.

OVERVIEW OF THE PLAN

| A. | Summary of the Plan |

The Plan is supported and sponsored by Oaktree as Plan Sponsor under the Plan Sponsor Agreement and the Backstop Parties, under the Backstop Commitment Letter. The Plan provides for the following key economic terms and mechanics:8

| • | Issuance of New Quiksilver Common Stock: On the Effective Date, Reorganized Quiksilver will authorize and issue the New Quiksilver Common Stock. Shares of New Quiksilver Common Stock will be allocated as follows: (a) first, to holders of Allowed Secured Notes Claims; (b) second, up to [●]% of New Quiksilver Common |

| 8 | Any summaries or descriptions of the Plan are qualified in their entirety by reference to the provisions of the Plan. For a more detailed description of the terms and provisions of the Plan, see Article VI below. |

2

Stock to Rights Offering Participants under the Rights Offerings, which, for the avoidance of doubt, shall dilute subpart (a); and (c) third, any New Quiksilver Common Stock issued to the Backstop Parties under the Backstop Commitment Letter, which, for the avoidance of doubt, shall dilute subparts (a) and (b). |

| • | Cancellation of Old Quiksilver Securities and Agreements: The Euro Notes Guaranty Claims shall be Reinstated and the Holders of such Claims shall be Unimpaired. Except with respect to the Euro Notes Guaranty Claims or as otherwise provided in the Plan, on the Effective Date, the Old Quiksilver Securities, which includes the Secured Notes, the Unsecured Notes, and the Old Quiksilver Common Stock, along with any other note, bond, indenture, Certificate, or other instrument or document evidencing or creating any indebtedness or obligation of or ownership interest in the Debtors (including the Indentures), shall be cancelled, and any obligations of, Claims against, and/or Interests in the Debtors under, relating, or pertaining to the foregoing, other than the Euro Notes, shall be released and discharged and cancelled. |

| • | Exit Financing: On the Effective Date, the Reorganized Debtors, as borrowers, will enter into the Exit Facility, an asset-based revolving credit facility in the principal amount of up to $[120] million pursuant to a new credit agreement with the Exit Lenders, which may include the DIP Lenders. The proceeds of the Exit Financing will fund (1) first, distributions under the Plan on account of the DIP ABL Facility Claims and (2) second, distributions under the Plan on account of DIP Term Facility Claims. |

| • | Exit Rights Offering: Each Eligible Holder of an Allowed Secured Notes Claim, or its affiliated Eligible Affiliate, will have the right to exercise subscription rights for the purchase of up to $122.5 million of New Quiksilver Common Stock. The proceeds of the Exit Rights Offering will be used to fund (1) first, distributions under the Plan on account of DIP Term Loan Facility Claims, (2) second, the Unsecured Cash Consideration of $7.5 million, and (3) third, any payments required on the Effective Date under the Plan. The Exit Rights Offering will run concurrently with solicitation on the Plan and will be consummated on the Effective Date. The Exit Rights Offering is backstopped by the Backstop Parties to the extent set forth in the Backstop Commitment Letter. |

| • | Unsecured Cash Consideration: The proceeds of the Exit Rights Offering will be used, in part, to fund the Unsecured Cash Consideration of $7.5 million pursuant to the Plan Sponsor Agreement. The Unsecured Cash Consideration will fund recoveries to Holders of Allowed Unsecured Notes Claims and Allowed General Unsecured Claims. |

| • | Euro Notes Exchange Offer: The Company will proffer an exchange offer to holders of Euro Notes, the terms and conditions of which will be set forth in a document contained in the Plan Supplement. The Euro Notes Exchange Offer will be consummated on the Effective Date to the extent the conditions precedent to such exchange offer are met. |

3

| • | Euro Notes Rights Offering: Each Eligible Holder of an Allowed Secured Notes Claim, or its affiliated Eligible Affiliate, will have the right to exercise subscription rights for the purchase of up to €50.0 million of New Quiksilver Common Stock, the proceeds of which will be used to consummate the Euro Notes Exchange Offer. The Euro Notes Rights Offering will be consummated on the Effective Date. The Euro Notes Rights Offering is backstopped by the Backstop Parties to the extent set forth in the Backstop Commitment Letter. |

| • | Backstop of the Rights Offerings: Pursuant to the Backstop Commitment Letter, on or before the Effective Date, the Backstop Parties will backstop the Rights Offerings by providing up to $122.5 million for the Exit Rights Offering and up to €50 million for the Euro Notes Rights Offering. |

| B. | Unclassified Claims. |

In accordance with section 1123(a)(1) of the Bankruptcy Code, the Plan does not classify Administrative Claims, Professional Claims, DIP ABL Facility Claims, DIP Term Facility Claims, and Priority Tax Claims. These Claims are therefore excluded from the Classes of Claims set forth in Article II of the Plan. The projected percentage of recoveries provided below are projected as of [●], 2015.

Claim | Plan Treatment | Projected Recovery Under the Plan | ||

| Administrative and Professional Claims | Paid in full in Cash. | 100% | ||

| DIP ABL Facility Claims | Paid in full in Cash. | 100% | ||

| DIP Term Loan Facility Claims | Paid in full in Cash. | 100% | ||

| Priority Tax Claims | Paid in full in Cash. | 100% |

| C. | Treatment of Claims and Interests Under the Plan |

The table below summarizes the classification, treatment, and estimated percentage recoveries of the Claims and Interests under the Plan. Estimated percentage recoveries have been calculated based upon a number of assumptions. For certain Classes of Claims, the actual percentage recovery is contingent upon a number of factors, including, but not limited to, Claims that are subject to liquidation pursuant to litigation.

Class | Type of Claim or Equity Interest | Treatment of Claim/Interest | Estimated % Recovery Under the Plan | |||

1 | Other Priority Claims | Unimpaired | 100% | |||

2 | Other Secured Claims | Unimpaired | 100% | |||

3 | Euro Notes Guaranty Claims | Unimpaired | 100% | |||

4 | Secured Notes Claims | Impaired | [●]% | |||

5-A | Unsecured Notes Claims | Impaired | [●]% | |||

5-B | General Unsecured Claims | Impaired | [●]% | |||

6 | Intercompany Claims | Unimpaired | 0-100% | |||

7 | Intercompany Interests | Unimpaired | 0-100% | |||

| 8 | Subordinated Claims | Impaired | 0% | |||

| 9 | Existing Equity Interests | Impaired | 0% |

4

| D. | Liquidation and Valuation Analyses |

[●]

ARTICLE III.

VOTING PROCEDURES

The following Classes are the only Classes entitled to vote to accept or reject the Plan:

| Class | Claim or Interest | Status | ||

| 4 | Secured Notes Claims | Impaired | ||

| 5-A | Unsecured Notes Claims | Impaired | ||

| 5-B | General Unsecured Claims | Impaired |

If your Claim or Interest is not included in any of these Classes, you are not entitled to vote and you will not receive a Solicitation Package (as defined below).

| A. | Classes Entitled to Vote |

Under the Bankruptcy Code, acceptance of a plan of reorganization by a Class of Claims is determined by calculating the number and the amount of Claims voting to accept, based on the actual total Allowed Claims voting on the Plan. Acceptance by a Class requires more than one-half of the number of total Allowed Claims in the Class to vote in favor of the Plan and at least two-thirds in dollar amount of the total Allowed Claims in the Class to vote in favor of the Plan. In addition, under the Bankruptcy Code, creditors are not entitled to vote if their contractual rights are Unimpaired by the Plan or if they will receive no distribution of property under the Plan. The following table sets forth which Classes of Claims will or will not be entitled to vote on the Plan:

Class | Claim or Interest | Status | Voting Rights | |||

1 | Other Priority Claims | Unimpaired | Presumed to Accept | |||

2 | Other Secured Claims | Unimpaired | Presumed to Accept | |||

3 | Euro Notes Guaranty Claims | Unimpaired | Presumed to Accept | |||

4 | Secured Notes Claims | Impaired | Entitled to Vote | |||

5-A | Unsecured Notes Claims | Impaired | Entitled to Vote | |||

5-B | General Unsecured Claims | Impaired | Entitled to Vote | |||

6 | Intercompany Claims | Unimpaired | Presumed to Accept | |||

7 | Intercompany Interests | Unimpaired | Presumed to Accept | |||

8 | Subordinated Claims | Impaired | Deemed to Reject | |||

9 | Existing Equity Interests | Impaired | Deemed to Reject |

5

| B. | Voting Procedures |

The Debtors retained Kurtzman Carson Consultants, LLC (“KCC”) to, among other things, act as Claims and Solicitation Agent in connection with the solicitation of votes to accept or reject the Plan.

The Voting Record Date (as defined in the Solicitation Motion)9 is December 1, 2015. The Voting Record Date is the date for determining (1) which Holders of Claims are entitled to vote to accept or reject the Plan and receive the Solicitation Package in accordance with the Solicitation Procedures (as defined in the Solicitation Motion) and (2) whether Claims have been properly assigned or transferred to an assignee pursuant to Bankruptcy Rule 3001(e) such that the assignee can vote as the Holder of a Claim. The Voting Record Date and all of the Debtors’ solicitation and voting procedures shall apply to all of the Debtors’ creditors and other parties in interest.

Under the Plan, Holders of Claims in the Voting Classes are entitled to vote to accept or reject the Plan. In order for the Holder of a Claim in the Voting Classes to have such Holder’s Ballot (as defined in the Solicitation Motion) counted as a vote to accept or reject the Plan, such Holder’s Ballot or Master Ballot (as defined in the Solicitation Motion), as applicable, must be properly completed, executed, and delivered in accordance with the instructions included in the Ballot by: (1) first class mail; (2) courier; or (3) personal delivery to the Claims and Solicitation Agent, so that such Holder’s Ballot or Master Ballot, as applicable, isactually received by the Claims and Solicitation Agent prior to4:00 p.m. prevailing Eastern Time on January 14, 2016 (the “Voting Deadline”). It is important that the Holder of a Claim in the Voting Classes follow the specific instructions provided on such Holder’s Ballot and the accompanying instructions.

IF A BALLOT IS RECEIVED AFTER THE VOTING DEADLINE, IT WILL NOT BE COUNTED UNLESS THE DEBTORS DETERMINE OTHERWISE IN THEIR SOLE AND ABSOLUTE DISCRETION.

ANY BALLOT THAT IS PROPERLY EXECUTED BY THE HOLDER OF A CLAIM BUT THAT DOES NOT CLEARLY INDICATE AN ACCEPTANCE OR REJECTION OF THE PLAN OR ANY BALLOT THAT INDICATES BOTH AN ACCEPTANCE AND A REJECTION OF THE PLAN WILL NOT BE COUNTED FOR PURPOSES OF ACCEPTING OR REJECTING THE PLAN.10

| 9 | As used herein, the “Solicitation Motion” refers to the Debtors’ Motion for Entry of an Order (A) Approving the Adequacy of the Debtors’ Disclosure Statement; (B) Approving Solicitation and Notice Procedures With Respect to Confirmation of the Debtors’ Proposed Plan of Reorganization; (C) Approving the Form of Various Ballots and Notices in Connection Therewith; and (D) Scheduling Certain Dates with Respect Thereto, filed substantially concurrently with this Disclosure Statement. |

| 10 | Holders who return Ballots that do not indicate a vote to accept or reject the Plan may still opt-out of the third party release provisions set forth in the Plan. |

6

EACH HOLDER OF A CLAIM MUST VOTE ALL OF ITS CLAIMS WITHIN A PARTICULAR CLASS EITHER TO ACCEPT OR REJECT THE PLAN AND MAY NOT SPLIT SUCH VOTES. BY SIGNING AND RETURNING A BALLOT, EACH HOLDER OF A CLAIM WILL CERTIFY TO THE BANKRUPTCY COURT AND THE DEBTORS THAT NO OTHER BALLOTS WITH RESPECT TO SUCH CLAIM HAVE BEEN CAST.

IT IS IMPORTANT TO FOLLOW THE SPECIFIC INSTRUCTIONS PROVIDED ON EACH BALLOT, AS APPROPRIATE, WHEN SUBMITTING A VOTE.

IF YOU ARE A HOLDER OF A CLAIM ENTITLED TO VOTE ON THE PLAN AND YOU DID NOT RECEIVE A BALLOT, YOU RECEIVED A DAMAGED BALLOT, OR YOU LOST YOUR BALLOT, OR IF YOU HAVE ANY QUESTIONS CONCERNING THE DISCLOSURE STATEMENT, THE PLAN, OR PROCEDURES FOR VOTING ON THE PLAN, PLEASE CONTACT THE VOTING AGENT KURTZMAN CARSON CONSULTANTS LLC, AT (877) 709-4757, WITHIN THE UNITED STATES OR CANADA, OR (424) 236-7235, OUTSIDE OF THE UNITED STATES OR CANADA, OR AT QUIKSILVERINFO@KCCLLC.COM.

| C. | Rights Offering Procedures |

The Debtors and the Backstop Parties, which includes the Plan Sponsor, will implement and conduct the Exit Rights Offering and the Euro Notes Rights Offering in accordance with the Backstop Commitment Letter and the Rights Offering Procedures. Each Eligible Holder of an Allowed Secured Notes Claim, or its affiliated Eligible Affiliate, will have the right to exercise subscription rights for the purchase of up to $122.5 million of New Quiksilver Common Stock, the proceeds of which will be used to fund distributions under the Plan and to provide working capital to the Debtors. The Exit Rights Offering will be consummated on the Effective Date. In addition, each Eligible Holder of an Allowed Secured Notes Claims, or its affiliated Eligible Affiliate, will have the right to exercise subscription rights for the purchase of up to €50.0 million of New Quiksilver Common Stock, the proceeds of which will be used to effectuate the Euro Notes Exchange Offer. The Euro Notes Rights Offering will be consummated on the Effective Date.

The Backstop Parties will backstop up to $122.5 million of the Exit Rights Offering and up to €50 million of the Euro Notes Rights Offering, in accordance with the Backstop Commitment Letter.

The Rights Offering Procedures provide for a two-step process whereby holders of Secured Notes or their affiliates must first certify that they are Eligible Holders or Eligible Affiliates (together, the “Eligible Offerees”), respectively, by returning, via the bank, brokerage

7

house, or other financial institution holding the notes underlying the Holder’s Secured Notes Claim (the “Nominee”), the eligibility form sent to that Holder (the “Secured Notes Eligibility Certificate”), which must be submitted by December 28, 2015 or such later time as determined by the Debtors with the consent of the Backstop Parties (the “Secured Notes Eligibility Certificate Deadline”). KCC, as subscription agent for the Rights Offerings (the “Subscription Agent”) will mail the Secured Notes Eligibility Certificates to the Nominees by no later than December 7, 2015, providing parties with approximately 21 days to return their Secured Notes Eligibility Certificates to their Nominees, which must complete the confirmation of ownership section and return the certificates to the Subscription Agent. To expedite the process, Secured Notes Eligibility Certificates may be returned to the Subscription Agent by mail or by email. Holders of Secured Notes who obtain their notes after the commencement of the Rights Offerings but before the Secured Notes Eligibility Certificate Deadline (as defined in the Rights Offering Procedures, the “Transferee Holders”) must also submit, along with their Secured Notes Eligibility Certificate, a notice notifying the Subscription Agent of the transfer of the Allowed Secured Notes Claim.

Those holders (including Transferee Holders) and their affiliates which return a properly completed Secured Notes Eligibility Certificate – will then receive a Subscription Form,11 whereby they can subscribe for the exercise of some or all of their rights under the Rights Offerings. The Subscription Form and the purchase price for rights acquired by the participant, as calculated in accordance with the Subscription Form, must be returned to the Subscription Agent by the subscription deadline of January 14, 2016, approximately 17 days after the Secured Notes Eligibility Certificate Deadline. Instructions with respect to completing each of the forms shall accompany such form.

In addition to compliance with the Rights Offering Procedures, it is a condition precedent to participation in the Rights Offerings that the holder of the Secured Notes Claims for which Rights are being exercised properly submit a ballot (i) to accept the Plan and (ii) not opting out of the releases included in Article 10.5 of the Plan.

The Rights Offering process will run parallel to, but independently of, the solicitation process – commencing on the date of mailing of solicitation materials and concluding on the deadline for submitting ballots voting on the Plan. To assist the holders of Secured Notes with making a decision with respect to whether to participate in the Rights Offerings, the Rights Offering Procedures and this Disclosure Statement, both of which shall be made available to holders of Secured Notes upon commencement of the Rights Offerings, shall contain further detail regarding the Rights Offerings and the Reorganized Debtors. Further, the Rights Offering Materials will contain warnings urging holders to review this Disclosure Statement and Plan prior to making a decision with respect to the exercise of their Rights.

| 11 | As used herein, the “Subscription Form” refers to the subscription form(s) and applicable instructions sent to each Eligible Offeree on which such Eligible Offeree may exercise its rights, substantially in the form attached as Annex A to the Rights Offering Procedures. |

8

ARTICLE IV.

GENERAL INFORMATION

| A. | Overview of the Company’s Business |

The Company is one of the world’s leading outdoor sports lifestyle companies. The Company designs, develops and distributes branded apparel, footwear, accessories and related products. The Company’s business is rooted in the strong heritage and authenticity of its core, iconic brands, Quiksilver, Roxy, and DC (shown below), each of which caters to the casual, outdoor lifestyle associated with surfing, skateboarding, snowboarding, and motocross, among other activities:

The Company’s products are sold in over 115 countries through a wide range of distribution points, including wholesale accounts (surf shops, skate shops, snow shops, sporting goods stores, discount centers, specialty stores, select department stores, and licensed stores), Company-owned retail stores, and its e-commerce websites.

The Company has four operating segments: the Americas (consisting of United States, Mexico, Brazil, and Canada), EMEA (consisting of Europe, the Middle East, and Africa), APAC (consisting of Australia, New Zealand, and the Pacific Rim, and headquartered in Torquay, Australia), and Corporate Operations. The Debtors, including the Company’s ultimate parent, Quiksilver, as well as a number of its domestic subsidiaries, are corporations based solely in the United States and operating in the Americas segment. The Non-Debtor Affiliates are foreign direct and indirect subsidiaries of Quiksilver operating solely outside of the United States; however, the Company’s operations as well as its supply chain are highly integrated across the four operating segments.

The Company’s operations can be divided into three segments – product design and development, production, and distribution channels.

| 1. | Product Design and Development |

The Company’s footwear is created by its design and merchandising teams based in Huntington Beach, California, and its apparel and accessories are created by design and merchandising teams based in Saint-Jean-De-Luz, France. The design centers monitor local, regional, and global fashion trends to develop specific product categories for each of the Company’s brands. The design centers share inspiration, design concepts, merchandising themes, graphics, and style viewpoints that are globally consistent while reflecting local adaptations to account for differences in geography, culture, and taste.

9

| 2. | Production |

The Company uses a direct-sourcing model to import its products from a variety of suppliers principally located in China, South Korea, Indonesia, India, Vietnam, and other parts of Asia. Once the products are imported, some require embellishments such as screen printing, dyeing, washing or embroidery. The Company generally does not enter into supply agreements with its vendors, and relies instead on individual purchase orders.

In addition to its direct sourcing model, the Company retains independent buying agents and employs staff to assist in the sourcing and manufacturing process. The buying agents are located primarily in China and Vietnam and assist in selecting and overseeing the majority of the Company’s independent third-party manufacturing and sourcing of finished goods, fabrics, and other products. The agents monitor trade regulations and perform some quality control functions. The Company’s staff, located in China, Vietnam, Indonesia, and other countries, are involved in sourcing and quality control functions that aid the Company in monitoring and coordinating overseas production. The employees help to ensure compliance with the Company’s standards of manufacturing practices, including adherence with a code of conduct related to factory working conditions and the treatment of workers involved in the manufacturing process.

| 3. | Distribution Channels |

Once produced, the Company’s products are sold in over 115 countries through wholesale customers, retail stores, and its e-commerce websites.

| (a) | Wholesale Customers |

Wholesale customers accounted for approximately 67% of the Company’s net revenues in fiscal year 2014. Wholesale accounts include surf shops, skate shops, snow shops, sporting goods stores, discount centers, specialty stores, online retailers, licensee shops, and select department stores. The Company’s products are distributed through active lifestyle specialty chains in the United States such as Zumiez, Tilly’s, Famous Footwear, and Journeys, chains in Europe such as Go Sport, Intersport, and Sport 2000, and chains in the Asia/Pacific region such as City Beach and Murasaki Sports. Department stores such as Macy’s in the United States, Galeries Lafayette in France, and El Corte Inglés in Spain distribute limited collections of the Company’s products. In the wholesale channel, the Company’s products are sold in major markets by over 300 independent sales representatives and an employee sales staff, and in smaller markets by over 150 local distributors. The Company also employs retail merchandise coordinators who travel between retail locations of wholesale customers to further improve the presentation of the Company’s product and build its brand image at the retail level.

| (b) | Retail Stores |

Sales at Company retail stores accounted for approximately 28% of Company revenue during fiscal year 2014. The Company’s retail shops include full-price stores, factory outlet stores, and “shop-in-shops.”12 At the end of the fiscal year 2014, the Company had

| 12 | The Company operates “shop-in-shops” –Quiksilver andRoxy shops primarily within larger department stores. As compared to a typical retail store, the shop-in-shops require a much smaller initial investment and are typically smaller than a traditional retail store, though they have many of the same operational characteristics. As of the end of the fiscal year 2014, the Company had approximately 270 shop-in-shops, all of which are located outside of the United States. |

10

approximately 266 full-price core brand stores, of which 75 are located in the United States. These full-price stores include a combination of its proprietary, multi-brand Boardriders stores, as well asQuiksilver,Roxy, andDC brand stores that feature a broad selection of products from its core brands, and, at times, a limited selection of products from other brands. The proprietary design of the stores demonstrates the Company’s history, authenticity, and commitment to surfing, skating and other board-riding sports. In addition to the core brand stores, the Company operates factory outlet stores in which it offers products specifically designed for the factory outlets, along with products from prior seasons. As of the end of fiscal year 2014, the Company had 147 factory outlet stores, of which 47 are located in the United States.

| (c) | E-Commerce Websites |

The Company operates several e-commerce websites that sell its products throughout the world and provide online content for its customers regarding its brands, athletes, events and the lifestyle associated with the Company’s brands. Sales on e-commerce websites accounted for approximately 5% of Company net revenue in fiscal year 2014.

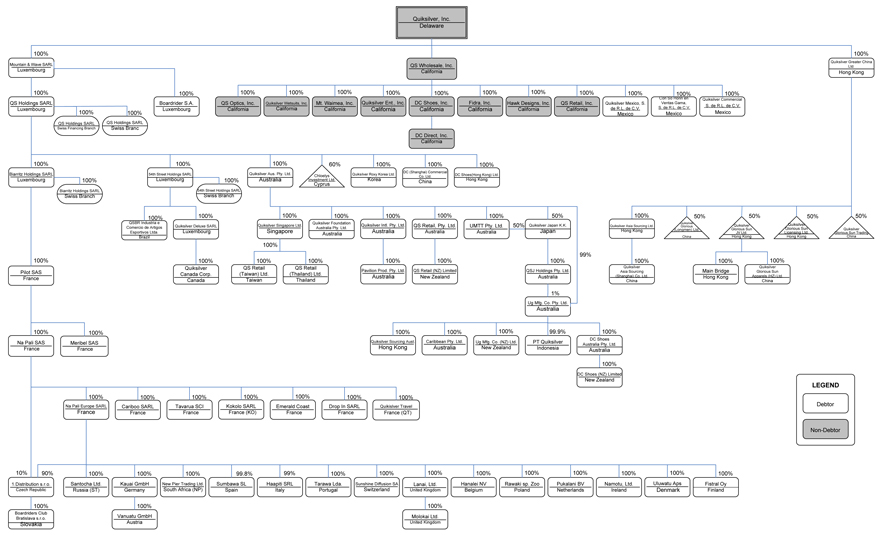

| B. | The Company’s Corporate Structure |

The Debtors in the Chapter 11 Cases are Quiksilver, Inc. (“Quiksilver”), QS Wholesale, Inc. (“QS Wholesale”), DC Direct, Inc., DC Shoes, Inc., Fidra, Inc., Hawk Designs, Inc., Mt. Waimea, Inc., Q.S. Optics, Inc., QS Retail, Inc., Quiksilver Entertainment, Inc., and Quiksilver Wetsuits, Inc. Quiksilver is the direct parent of QS Wholesale, which is in turn the direct parent of each of the remaining Debtors. Quiksilver is also the direct and indirect parent of several wholly-owned, non-Debtor foreign subsidiaries. The corporate structure chart attached asExhibit D sets forth the Company’s corporate structure.

The Company’s financial reporting for ZQK (on a consolidated basis) and for each of the Company’s segments is provided in the Company’s annual and quarterly reports. The Company’s annual and quarterly reports, along with its proxy statements, for the last five (5) years are available at the Company’s restructuring website at http://www.kccllc.net/quiksilver/document/noticelist/5.

| C. | The Company’s Board of Directors |

The following persons comprise the board of directors of Quiksilver (the “Board of Directors”):

Name | Position | |

Robert B. McKnight, Jr. | Director, Chairman of the Board | |

Pierre Agnes | Director | |

William M. Barnum, Jr. | Director |

11

Name | Position | |

Joseph F. Berardino | Director | |

Michael A. Clarke | Director | |

M. Steven Langman | Director | |

Andrew W. Sweet | Director |

Mr. Robert B. McKnight, Jr. has been Chairman of the Company’s Board since August 1991 and has provided consulting and strategic advisory services to the Company on an as-requested basis since October 2014. Mr. McKnight is also a co-founder of the Company. He previously served as the Company’s Executive Chairman from January 2013 to October 2014. In that capacity, he reported to the Company’s Board, and, among other things, provided guidance and support for the Company’s business, representing the Company at industry and public functions, and establishing and maintaining relationships with sponsored athletes and other endorsers of the Company’s products and services. He also served as the Company’s Chief Executive Officer from 1991 until January 2013, and President from 1979 until July 1991 and again from February 2008 until January 2013.

Mr. Pierre Agnes has been a member of the Company’s Board and its Chief Executive Officer since March 2015. Mr. Agnes previously served as the Company’s President since October 2014, Global Head of Apparel since March 2013, and President of Quiksilver Europe since June 2005. Prior to that, he served as Managing Director of Quiksilver Europe since December 2003. Between 1992 and 2002, Mr. Agnes founded and operated Omareef Europe, a licensee of the Company for wetsuits and eyewear that the Company purchased in November 2002. Mr. Agnes originally joined the Company in 1988, first as team manager, and later in various capacities throughout the Company’s European marketing operations.

Mr. William M. Barnum, Jr. has been a member of the Company’s Board since 1991. Mr. Barnum currently serves as a director of Zoe’s Kitchen, Inc., which is listed on the New York Stock Exchange, as well as several private companies, and has been a Managing Member of Brentwood Associates, a Los Angeles based venture capital and private equity investment firm since 1986. Prior to that, Mr. Barnum held several positions at Morgan Stanley & Co. Mr. Barnum graduated from Stanford University in 1976 with a B.A. in Economics and from the Stanford Graduate School of Business and Stanford Law School in 1981 with an M.B.A. and J.D.

Mr. Joseph F. Berardino has been a member of the Company’s Board since May 2011. Mr. Berardino currently serves as a Managing Director at Alvarez & Marsal, a global professional services firm. Prior to joining Alvarez & Marsal in October 2008, Mr. Berardino was Chairman of the Board of Profectus BioSciences, a biotechnology company, from 2004 until September 2008, and served as its Chief Executive Officer from October 2005 until January 2008. He previously served as Vice-Chairman of Sciens Capital Management, a New York-based alternative asset management firm from 2004 to September 2005 and prior to his tenure at Sciens, he served as Chief Executive Officer of Andersen Worldwide, a global accounting and consulting firm. Mr. Berardino graduated from Fairfield University with a B.S. in Accounting and has been a Certified Public Accountant since 1975 (inactive).

12

Mr. Michael A. Clarke has been a member of the Company’s Board since April 2013. Mr. Clarke currently serves as managing director and chief executive officer of Treasury Wine Estates, an Australian wine producer and distributor. Prior to joining Treasury Wine Estates in March 2014, Mr. Clarke served as chief executive officer of Premier Foods Plc., a branded food company in the United Kingdom from August 2011 until February 2013. He has also served as President of Kraft Foods Europe from January 2009 until August 2011 and held several positions with The Coca-Cola Company from 1996 to 2008, including President-Northwest Europe from 2005 to 2008, President-South Pacific & Korea from 2000 to 2005 and Senior Vice President-Minute Maid International from 1996 to 2000. Mr. Clarke also has held a variety of positions with Reebok International Ltd. (1991 to 1996), served in senior financial roles with Acer Consulting (Far East) Ltd., consulting engineers, and as a chartered accountant with Deloitte. Mr. Clarke graduated from the University of Cape Town with a Bachelor of Commerce.