Filed Pursuant to Rule 433

Registration No: 333-134553

FX Basket-Linked Note

Final Terms and Conditions

“High Yield Digital Plus Basket”

June 29, 2007

Contact: + 1 212 526 2237

Lehman Brothers Holdings Inc. has filed a registration statement (including a prospectus) with the U.S. Securities and Exchange Commission (SEC) for this offering. Before you invest, you should read the prospectus dated May 30, 2006, the prospectus supplement dated May 30, 2006 for its Medium Term Notes, Series I, and other documents Lehman Brothers Holdings Inc. has filed with the SEC for more complete information about Lehman Brothers Holdings Inc. and this offering. Buyers should rely upon the prospectus, prospectus supplement and any relevant free writing prospectus for complete details. You may get these documents and other documents Lehman Brothers Holdings Inc. has filed for free by searching the SEC online database (EDGAR®) at www.sec.gov with “Lehman Brothers Holdings Inc.” as a search term. You may also access the prospectus and Series I MTN prospectus supplement on the SEC web site as follows:

Series I MTN prospectus supplement dated May 30, 2006:

http://www.sec.gov/Archives/edgar/data/806085/000104746906007785/a2170815z424b2.htm

Prospectus dated May 30, 2006:

http://www.sec.gov/Archives/edgar/data/806085/000104746906007771/a2165526zs-3asr.htm

Alternatively, Lehman Brothers Inc. will arrange to send you the prospectus, Series I MTN prospectus supplement and final pricing supplement (when completed) if you request it by calling your Lehman Brothers sales representative or 1-888-603-5847.

Summary Description

This note allows an investor to hold via a single basket a long position in the Brazilian Real (BRL), Indian Rupee (INR), Mexican Peso (MXN) and Turkish Lira (TRY), in each case relative to the U.S. Dollar (USD). If the Basket Return, which is linked to the performance of the long currencies vs. the USD, is greater than zero but less than 0.0575 on the Valuation Date (that is, the Basket Return has increased by up to 5.75%), the investor will receive a single payment at maturity equal to the principal amount of the notes plus an Additional Amount of 11.50% multiplied by that principal amount. If the Basket Return is greater than or equal to 0.0575 on the Valuation Date (that is, the Basket Return has increased by 5.75% or more), the investor will receive a single payment at maturity equal to the principal amount of the notes plus an Additional Amount equal to the principal amount of the notes multiplied the product of 200% (the Leverage) and the Basket Return (that is, the amount by which the Basket Return exceeds zero). If the Basket Return on the Valuation Date is less than zero, then the investor will receive at maturity only the principal amount of the notes, with no additional return. The notes do not bear interest and are 100% principal protected if held to maturity.

|

|

|

|

|

|

Issuer |

| Lehman Brothers Holdings Inc. (A1, A+, A+) |

|

|

|

|

|

|

Issue Size |

| USD 500,000 (re-opening to become fungible with the outstanding $4,500,000 FX Basket-Linked Notes due June 30, 2008, issued on June 28, 2007 so that the aggregate principal amount outstanding after the issue of these notes will be $5,000,000) |

|

|

|

|

|

|

Issue Price |

| 100% |

|

|

|

|

|

|

Principal Protection |

| 100% |

|

|

|

|

|

|

Trade Date of Re-Opening |

| June 29, 2007 |

|

|

|

|

|

|

Original Trade Date |

| June 21, 2007 |

|

|

|

|

|

|

Issue Date |

| July 2, 2007 |

|

|

|

|

|

|

|

| |||||||||

|

|

| ||||||||

Valuation Date |

| June 20, 2008, provided that, upon the occurrence of a Disruption Event, the Valuation Date may be postponed (as described under “Disruption Events” below) | ||||||||

|

|

| ||||||||

|

|

| ||||||||

Maturity Date |

| June 30, 2008 | ||||||||

|

|

| ||||||||

|

|

| ||||||||

Reference Currencies |

| Brazilian Real (BRL), Indian Rupee (INR), Mexican Peso (MXN), and Turkish Lira (TRY) | ||||||||

|

|

| ||||||||

|

|

| ||||||||

Reference Exchange Rate |

| The spot exchange rate for each of the Reference Currencies quoted against the U.S. dollar expressed as number of units of the Reference Currency per USD 1. | ||||||||

|

|

| ||||||||

|

|

| ||||||||

Settlement Rate |

| For each Reference Currency, the Reference Exchange Rate on the Valuation Date, determined in accordance with the applicable Settlement Rate Option (subject to the occurrence of a Disruption Event). | ||||||||

|

|

| ||||||||

|

|

| ||||||||

Leverage |

| 200% | ||||||||

|

|

| ||||||||

|

|

| ||||||||

Redemption Amount |

| A single U.S. dollar payment on the Maturity Date equal to the principal amount of each note plus the Additional Amount | ||||||||

|

|

| ||||||||

|

|

| ||||||||

Additional Amount |

| A single USD payment on the Maturity Date equal to the principal amount of each note multiplied by: | ||||||||

|

|

| ||||||||

|

| 0.0% |

| If the Basket Return is less than or equal to 0.0 | ||||||

|

|

|

|

| ||||||

|

| 11.5% |

| if the Basket Return is greater than 0.0 but less than 0.0575; or | ||||||

|

|

|

|

| ||||||

|

| Leverage * Basket Return |

| if the Basket Return is greater than or equal to 0.0575 | ||||||

|

|

| ||||||||

|

|

| ||||||||

Basket Return |

| The sum of the Weighted Currency Returns. | ||||||||

|

|

| ||||||||

|

|

| ||||||||

Weighted Currency |

| For each Reference Currency: | ||||||||

Returns |

|

| ||||||||

|

| Weighting * | { | Initial Reference Currency Rate – Settlement Rate | } | |||||

|

|

|

| Initial Reference Currency Rate |

| |||||

|

|

| ||||||||

|

|

| ||||||||

Weightings and Initial |

| The Initial Currency Amount for the USD and each Reference Currency is as set forth below: | ||||||||

Reference Currency |

|

| ||||||||

Rates |

| Reference Currency |

| Weighting |

| Initial Reference Currency Rates | ||||

|

| BRL |

| 25% |

| 1.9190 | ||||

|

| INR |

| 25% |

| 40.72 | ||||

|

| MXN |

| 25% |

| 10.8376 | ||||

|

| TRY |

| 25% |

| 1.3085 | ||||

|

|

| ||||||||

|

| The Initial Currency Rate for each Reference Currency is the Reference Exchange Rate for that Reference Currency determined by the Calculation Agent on the Original Trade Date. | ||||||||

|

|

| ||||||||

|

|

| ||||||||

|

| |||||||

|

|

| ||||||

Settlement Rate Option and Valuation Business |

| For each Reference Currency as set forth below: | ||||||

Day |

| Reference Currency |

| Screen Reference |

| Valuation Business Day | ||

|

| Brazilian Real |

| BRFR |

| Brazilia, Rio de Janiero or São Paulo; and New York | ||

|

|

|

|

|

|

| ||

|

| Indian Rupee |

| RBIB |

| Mumbai and New York | ||

|

|

|

|

|

|

| ||

|

| Mexican Peso |

| USDMXNFIX= |

| Mexico City and New York | ||

|

|

|

|

|

|

| ||

|

| Turkish Lira |

| The TRY/EUR fixing rate on ECB37 divided by the USD/EUR fixing rate on ECB37 |

| TARGET and New York | ||

|

|

| ||||||

|

| For further information concerning the Settlement Rate Option and Valuation Business Day, see “Description of the Notes—Currency-Indexed Notes” in, and Appendix A to, the prospectus supplement dated May 30, 2006 for the issuer’s Medium Term Notes, Series I.The spot exchange rate for each of the Reference Currencies quoted against the U.S. dollar expressed as number of units of the Reference Currency per USD 1. | ||||||

|

|

| ||||||

|

|

| ||||||

Business Day |

| New York | ||||||

|

|

| ||||||

|

|

| ||||||

Business Day Convention |

| Following | ||||||

|

|

| ||||||

|

|

| ||||||

Disruption Events |

| If a Disruption Event relating to one or more Reference Currencies is in effect on the scheduled Valuation Date, the Calculation Agent will calculate the Basket Return using: | ||||||

|

|

|

|

| ||||

|

| · |

| for each Reference Currency that did not suffer a Disruption Event on the scheduled Valuation Date, the Settlement Rate on the scheduled Valuation Date, and | ||||

|

|

|

|

| ||||

|

| · |

| for each Reference Currency that did suffer a Disruption Event on the scheduled Valuation Date, the Settlement Rate on the immediately succeeding scheduled Valuation Business Day for such Reference Currency on which no Disruption Event occurs or is continuing with respect to such Reference Currency; | ||||

|

|

|

|

| ||||

|

| provided however that if a Disruption Event has occurred or is continuing with respect to a Reference Currency on each of the three scheduled Valuation Business Days following the scheduled Valuation Date, then (a) such third scheduled Valuation Business Day shall be deemed the Valuation Date for the affected Reference Currency; and (b) the Calculation Agent will determine the Settlement Rate for the affected Reference Currency on such day in accordance with “Fallback Rate Observation Methodology” (as defined under “Description of the Notes—Currency-Indexed Notes” in the prospectus supplement dated May 30, 2006, for the issuer’s Medium Term Notes, Series I). | ||||||

|

|

|

|

| ||||

|

| A “Disruption Event” means any of the following events with respect to a Reference Currency, as determined in good faith by the Calculation Agent: | ||||||

|

|

|

|

| ||||

|

| (A) |

| the occurrence and/or existence of an event on any day that has the effect of preventing or making impossible (x) the delivery of USD from accounts inside the Reference Currency Jurisdiction for that Reference Currency to accounts outside that Reference Currency Jurisdiction; or (y) for MXN and TRY only, the conversion of the Reference Currency into USD through customary legal channels; | ||||

|

|

|

|

| ||||

|

| (B) |

| the occurrence of any event causing the Reference Exchange Rate for the Reference Currency to be split into dual or multiple currency exchange rates; or | ||||

|

|

|

|

| ||||

|

| (C) |

| the Settlement Rate being unavailable for the Reference Currency, or the occurrence of an | ||||

|

|

| event (i) in the Reference Currency Jurisdiction for that Reference Currency that materially disrupts the market for the Reference Currency or (ii) that generally makes it impossible to obtain the Settlement Rate for the Reference Currency, on the Valuation Date. | |

|

|

| ||

|

| For purposes of the above, “scheduled Valuation Business Day” means a day that is or, in the judgment of the Calculation Agent, should have been, a Valuation Business Day for the affected Reference Currency. | ||

|

|

| ||

|

| For further information concerning the Settlement Rate Option and Valuation Business Day, see “Description of the Notes—Currency-Indexed Notes” in, and Appendix A to, the prospectus supplement dated May 30, 2006 for the issuer’s Medium Term Notes, Series I. | ||

|

|

| ||

|

|

| ||

Calculation Agent |

| Lehman Brothers Inc. | ||

|

|

| ||

|

|

| ||

Underwriter |

| Lehman Brothers Inc. | ||

|

|

| ||

|

|

| ||

Identifier |

| CUSIP: 52517P3K5 | ||

|

|

| ||

|

| ISIN: US52517P3K51 | ||

|

|

| ||

|

|

| ||

Settlement System |

| DTC | ||

|

|

| ||

|

|

| ||

Denominations |

| USD 1,000 and whole multiples of USD 1,000 | ||

|

|

| ||

|

|

| ||

Issue Type |

| US MTN | ||

|

|

| ||

|

|

| ||

United States Federal Income Tax Treatment

Lehman Brothers Holdings Inc. intends to treat the notes as contingent payment debt instruments, as described under “Supplemental United States Federal Income Tax Consequences—Contingent Payment Debt Instruments” in the prospectus supplement dated May 30, 2006.

Historical Exchange Rates

The following charts show the spot exchange rates for each Reference Currency at the end of each week in the period from the week ending June 13, 2004 through the week ending June 24, 2007 using historical data obtained from Reuters; neither Lehman Brothers Inc. nor Lehman Brothers Holdings Inc. makes any representation or warranty as to the accuracy or completeness of this data. The spot exchange rates are expressed as the amount of U.S. dollars per Reference Currency to show the appreciation or depreciation, as the case may be, of the Reference Currency against the U.S. dollar. The spot exchange rates used to calculate the Basket Return are expressed as the amount of Reference Currency per U.S. dollar, which are the inverse of the spot exchange rates presented in the following charts. The historical data on each Reference Currency is not necessarily indicative of the future performance of the Reference Currencies, the Basket Return or what the Value of the notes may be. Fluctuations in exchange rates make it difficult to predict whether the Additional Amount will be payable at maturity, or what that Additional Amount, if any, may be. Historical exchange rate fluctuations may be greater or lesser than those experienced by the holders of the notes.

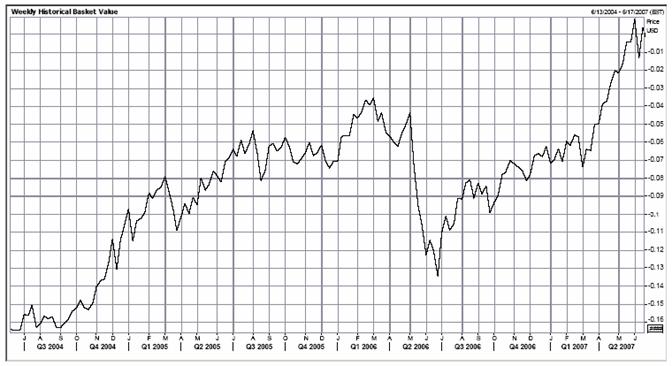

Hypothetical Historical Basket Return

The following chart shows the hypothetical Basket Return at the end of each week in the period from the week ending June 13, 2004 through the week ending June 24, 2007, based on the hypothetical composite performance of the Reference Currencies using data obtained from Reuters; neither Lehman Brothers Inc. nor Lehman Brothers Holdings Inc. makes any representation or warranty as to the accuracy or completeness of this data. The Basket Return was indexed to a level of 0.0 based upon the Reference Exchange Rates determined on June 18, 2007, based upon Initial Reference Currency Rates determined on that day. The composite value of the Reference Currencies on any prior day was obtained by using the calculation of the Basket Return described above. Spot exchange rates used in this determination are expressed as the number of units of Reference Currency per U.S. dollar. For purposes of the notes and the determination of the Additional Amount, the Basket Return will be indexed to 0.0 on the Original Trade Date.

Hypothetical Redemption Amount Payment Examples

The following payment examples for this note shows scenarios for the Redemption Amount payable at maturity of the notes, including scenarios under which an Additional Amount will or will not be payable, based on the Initial Currency Rates for the Reference Currencies (which were determined on the Original Trade Date) and hypothetical values for the Settlement Rates (which will be determined on the Valuation Date), and consequently of the Basket Return.

The Settlement Rate values for the Reference Currencies have been chosen arbitrarily for the purpose of these examples, are not associated with Lehman Brothers Research forecasts for any Reference Currency/USD exchange rates and should not be taken as indicative of the future performance of any Reference Currency/USD exchange rate.

Example 1: BRL, INR, TRY and MXN each appreciate relative to their Initial Currency Rates, resulting in a Basket Return of 0.0735, which is greater than 0.0575. Therefore, the Additional Amount is 14.70%, and the Redemption Amount is equal to 114.70% times the principal amount of the notes.

Because the Basket Return is 0.0735, which is greater than zero, the Redemption Amount payable at maturity is equal to $1,147.00 per $1,000 note (reflecting an Additional Amount of 14.70% per note), calculated as follows:

Redemption Amount = $1,000 + ($1,000 * 200% * 0.0735) = $1,147.00 The table below illustrates how the Basket Return in the above example was calculated:

Basket |

| Initial Reference |

| Weighting |

| Hypothetical |

| Weighted Currency |

BRL |

| 1.9190 |

| 25% |

| 1.8218 |

| 0.0127 |

INR |

| 40.7200 |

| 25% |

| 37.685 |

| 0.0186 |

TRY |

| 1.3085 |

| 25% |

| 1.237 |

| 0.0137 |

MXN |

| 10.8376 |

| 25% |

| 9.5984 |

| 0.0286 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Basket Return = |

| 0.0735 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Leverage = |

| 200% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Additional Amount = |

| 14.70% |

|

|

|

|

|

| Redemption Amount = |

| 114.70% |

|

|

|

|

|

|

|

|

|

Example 2: BRL, INR, TRY and MXN each appreciate relative to their Initial Currency Rates, resulting in a Basket Return of 0.0402, which is greater than zero but less than 0.0575. Therefore, the Additional Amount is 11.5%, and the Redemption Amount is equal to 111.5% times the principal amount of the notes.

The table below illustrates how the Basket Return in the above example was calculated:

Basket |

| Initial Reference |

| Weighting |

| Hypothetical |

| Weighted Currency |

BRL |

| 1.9190 |

| 25% |

| 1.8218 |

| 0.0061 |

INR |

| 40.7200 |

| 25% |

| 38.685 |

| 0.0125 |

TRY |

| 1.3085 |

| 25% |

| 1.297 |

| 0.0022 |

MXN |

| 10.8376 |

| 25% |

| 9.9984 |

| 0.0194 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Basket Return = |

| 0.0402 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Leverage = |

| 200% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Additional Amount = |

| 11.50% |

|

|

|

|

|

| Redemption Amount = |

| 111.50% |

|

|

|

|

|

|

|

|

|

Example 3: BRL, INR, TRY and MXN each depreciate relative to their Initial Currency Rates, resulting in a Basket Return of

–0.0723; because the Basket Return is less then zero, the Additional Amount is zero, and the Redemption Amount is equal to 100% times the principal amount of the notes.

Because the Basket Return is –0.0723, which is less than zero, the Redemption Amount payable at maturity is equal to $1,000.00 per $1,000 note (reflecting an Additional Amount of 0% per note).

The table below illustrates how the Basket Return in the above example was calculated:

Basket |

| Initial Reference |

| Weighting |

| Hypothetical |

| Weighted Currency |

BRL |

| 1.9190 |

| 25% |

| 2.1018 |

| –0.0238 |

INR |

| 40.7200 |

| 25% |

| 41.485 |

| –0.0047 |

TRY |

| 1.3085 |

| 25% |

| 1.3975 |

| –0.0170 |

MXN |

| 10.8376 |

| 25% |

| 11.9982 |

| –0.0268 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Basket Return = |

| 0.0723 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Additional Amount = |

| 0% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Redemption Amount = |

| 100% |

|

|

|

|

|

|

|

|

|

Example 4: BRL, INR each depreciate relative to their Initial Currency Rates while TRY and MXN each appreciate relative to their Initial Currency Rates, resulting in a Basket Return of 0.0808, which is greater than 0.0575. Therefore, the Additional Amount is 16.16%, and the Redemption Amount is equal to 116.16% times the principal amount of the notes.

Because the Basket Return is 0.0808, which is greater than zero, the Redemption Amount payable at maturity is equal to $1,161.60 per $1,000 note (reflecting an Additional Amount of 16.16% per note), calculated as follows:

Redemption Amount = $1,000 + ($1,000 * 200% * 0.0808) = $1,161.60

The table below illustrates how the Basket Return in the above example was calculated:

Basket |

| Initial Reference |

| Weighting |

| Hypothetical |

| Weighted Currency |

BRL |

| 1.9190 |

| 25% |

| 2.0218 |

| –0.0134 |

INR |

| 40.7200 |

| 25% |

| 41.685 |

| –0.0059 |

TRY |

| 1.3085 |

| 25% |

| 0.934 |

| 0.0716 |

MXN |

| 10.8376 |

| 25% |

| 9.5984 |

| 0.0286 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Basket Return = |

| 0.0808 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Leverage = |

| 200% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Additional Amount = |

| 16.16% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Redemption Amount = |

| 116.16% |

|

|

|

|

|

|

|

|

|

Example 5: MXN, INR each depreciate relative to their Initial Currency Rates while TRY and BRL each appreciate relative to their Initial Currency Rates, resulting in a Basket Return of 0.0179, which is greater than zero but less than 0.0575. Therefore, the Additional Amount is 11.5%, and the Redemption Amount is equal to 111.5% times the principal amount of the notes.

The table below illustrates how the Basket Return in the above example was calculated:

Basket |

| Initial Reference |

| Weighting |

| Hypothetical |

| Weighted Currency |

BRL |

| 1.9190 |

| 25% |

| 1.8218 |

| 0.0127 |

INR |

| 40.7200 |

| 25% |

| 41.685 |

| –0.0059 |

TRY |

| 1.3085 |

| 25% |

| 1.184 |

| 0.0238 |

MXN |

| 10.8376 |

| 25% |

| 11.384 |

| –0.0126 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Basket Return = |

| 0.0179 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Additional Amount = |

| 11.5% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Redemption Amount = |

| 111.5% |

|

|

|

|

|

|

|

|

|

Example 6: MXN, BRL each depreciate relative to their Initial Currency Rates while TRY and INR each appreciate relative to their Initial Currency Rates, resulting in a Basket Return of –0.0489, which is less than zero. Therefore, the Additional Amount is 0%, and the Redemption Amount is equal to 100% times the principal amount of the notes.

Because the Basket Return is –0.0489, which is less than zero, the Redemption Amount payable at maturity is equal to $1,000.00 per $1,000 note (reflecting an Additional Amount of 0% per note).

The table below illustrates how the Basket Return in the above example was calculated:

Basket |

| Initial Reference |

| Weighting |

| Hypothetical |

| Weighted Currency |

BRL |

| 1.9190 |

| 25% |

| 2.1218 |

| –0.0264 |

INR |

| 40.7200 |

| 25% |

| 38.685 |

| 0.0125 |

TRY |

| 1.3085 |

| 25% |

| 1.184 |

| 0.0238 |

MXN |

| 10.8376 |

| 25% |

| 13.384 |

| –0.0587 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Basket Return = |

| –0.0489 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Additional Amount = |

| 0% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Redemption Amount = |

| 100% |

|

|

|

|

|

|

|

|

|