Lehman Brothers Holdings Inc Plan Trust (LEHMQ)

Filed: 30 Jan 08, 12:00am

Calculation of the Registration Fee

Title of Each Class of Securities |

| Maximum Aggregate Offering |

| Amount of Registration Fee(1)(2) |

|

Notes |

| $875,000 |

| $34.39 |

|

(1) Calculated in accordance with Rule 457(r) of the Securities Act of 1933.

(2) Pursuant to Rule 457(p) under the Securities Act of 1933, filing fees have already been paid with respect to unsold securities that were previously registered pursuant to a Registration Statement on Form S-3 (No. 333-134553) filed by Lehman Brothers Holdings Inc. and the other Registrants thereto on May 30, 2006, and have been carried forward, of which $34.39 is offset against the registration fee due for this offering and of which $1,272,720.46 remains available for future registration fees. No additional registration fee has been paid with respect to this offering.

Filed Pursuant to Rule 424(b)(2)

Registration No. 333-134553

PRICING SUPPLEMENT NO. 618

(To prospectus dated May 30, 2006 and prospectus supplement dated May 30, 2006)

U.S.$875,000

LEHMAN BROTHERS HOLDINGS INC.

MEDIUM-TERM NOTES, SERIES I

FX Basket-Linked Notes

Due January 31, 2011

Because these notes are part of a series of Lehman Brothers Holdings’ debt securities called Medium-Term Notes, Series I, this pricing supplement should also be read with the accompanying prospectus supplement, dated May 30, 2006 (the “MTN prospectus supplement”) and the accompanying prospectus dated May 30, 2006 (the “base prospectus”). Terms used here have the meanings given to them in the MTN prospectus supplement or the base prospectus, unless the context requires otherwise.

General: |

| · Additional Amount: A single U.S. dollar amount equal to the principal amount of the notes multiplied by the product of the Upside Leverage times the Basket Return, if the Basket Return is greater than zero, and the Downside Return Rate times the product of -1 times the Basket Return, if the Basket Return is less than or equal to zero; provided that the minimum Additional Amount payable on the notes shall be zero.

· Settlement Rate: For each Reference Currency, the Reference Exchange Rate on the Valuation Date determined in accordance with the applicable Settlement Rate Option (as defined in “Description of the Notes” below) subject to the occurrence of a Disruption Event (as defined in “Description of the Notes” below).

· Upside Leverage: 100%

· Downside Return Rate: 60%

· Reference Exchange Rates: For each Reference Currency, the spot exchange rate for that Reference Currency quoted against the U.S. dollar expressed as number of units of the Reference Currency per one USD.

· Basket Return: The sum of the Weighted Currency Returns for the Reference Currencies.

· Weighted Currency Returns: For each Reference Currency, the product of the Weighting for such Reference Currency times a quotient, the numerator of which is the difference of the Initial Reference Currency Rate for such Reference Currency minus the Settlement Rate for such Reference Currency and the denominator of which is the Initial Reference Currency Rate for such Reference Currency.

· Initial Reference Currency Rates: |

| ||

· Senior unsecured obligations of Lehman Brothers Holdings Inc.

· CUSIP: 52517P6E6

· ISIN: US52517P6E64

· The notes are designed for investors who wish to hold simultaneously a long and short position in a basket of currencies relative to the U.S. dollar.

· Reference Currency: Each of the Brazilian Real (BRL), Russian Ruble (RUB), Indian Rupee (INR), Chinese Renminbi (CNY) and South Korean Won (KRW) (collectively, the “Reference Currencies”).

· Basket: The Basket will be comprised of the five Reference Currencies. Each of the BRL, RUB, INR, CNY and KRW makes up a portion of the Basket with a weighting (the “Weighting”), on the date of this pricing supplement, of 20%.

· Maturity Date: January 31, 2011

· Valuation Date: January 26, 2011; provided that, upon the occurrence of a Disruption Event (as defined in “Description of the Notes” below) with respect to a Reference Currency, the Valuation Date for the affected Reference Currency may be postponed (as described in “Description of the Notes” below).

· The notes are 100% principal protected if held to maturity.

· Denominations: U.S.$1,000 and whole multiples of U.S.$1,000 in excess thereof. |

| ||||

|

|

|

|

|

|

Payments: · No interest payments during the term of the notes.

· Each note will receive a single U.S. dollar payment on the Maturity Date equal to the principal amount of the notes plus the Additional Amount, if any, which payment is linked to the Basket Return. |

| Reference |

| Initial Reference Currency |

|

BRL |

| 1.7906 |

| ||

RUB |

| 24.5408 |

| ||

INR |

| 39.47 |

| ||

CNY |

| 7.1996 |

| ||

KRW |

| 946.60 |

| ||

|

|

|

| ||

Investing in the notes involves risks. Risk Factors begin on page S-4 of the MTN prospectus supplement.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or determined if this pricing supplement or any accompanying prospectus supplement or prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

|

| Per Note |

| Total |

|

Public offering price(1) |

| 100.00 | % | U.S.$875,000.00 |

|

Underwriting discount(2) |

| 2.50 | % | U.S.$21,875.00 |

|

Proceeds to Lehman Brothers Holdings Inc. |

| 97.50 | % | U.S.$853,125.00 |

|

(1) The price to public includes the cost of hedging the Issuer’s obligations under the notes through one or more of the Issuer’s affiliates, which includes the Issuer’s affiliates expected cost of providing such hedge as well as the profit the Issuer’s affiliates expect to realize in consideration for assuming the risks inherent in providing such hedge.

(2) Lehman Brothers Inc. will receive commissions equal to $25.00 per $1,000 principal amount, or 2.50%, and may use all or a portion of these commissions to pay selling concessions or fees to other dealers. Lehman Brothers Inc. and/or an affiliate may earn additional income as a result of payments pursuant to any hedges.

The notes are expected to be ready for delivery in book-entry form only through The Depository Trust Company on or about January 31, 2008.

Lehman Brothers Inc., a wholly owned subsidiary of Lehman Brothers Holdings, makes a market in Lehman Brothers Holdings’ securities. It may act as principal or agent in, and this pricing supplement may be used in connection with, those transactions. Any such sales will be made at varying prices related to prevailing market prices at the time of sale.

LEHMAN BROTHERS

January 28, 2008

SUMMARY INFORMATION — Q&A

This summary highlights selected information from this pricing supplement, the MTN prospectus supplement and the base prospectus to help you understand the notes. You should carefully read this pricing supplement, the MTN prospectus supplement and the base prospectus to understand fully the terms of the notes and the tax and other considerations that are important to you in making a decision about whether to invest in the notes. You should pay special attention to the “Risk Factors” section on page S-4 of the MTN prospectus supplement to determine whether an investment in the notes is appropriate for you.

What are the notes?

The notes will be a series of our senior debt that are linked to a basket (the “Basket”) that measures the performance of the Brazilian Real (BRL), Russian Ruble (RUB), Indian Rupee (INR), Chinese Renminbi (CNY) and South Korean Won (KRW), , relative to the U.S. dollar (USD). We refer to BRL, RUB, INR, CNY and KRW as the Reference Currencies. Each of the BRL, RUB, INR, CNY and KRW makes up a portion of the Basket, with a Weighting of 20%.

The notes will rank equally with all other unsecured debt of Lehman Brothers Holdings Inc., except subordinated debt, and will mature on January 31, 2011 (or if such day is not a New York business day, the next succeeding New York business day).

What payments will I receive on the notes before maturity?

None. Unlike ordinary debt securities, the notes do not pay interest before maturity.

What will I receive if I hold the notes until the stated maturity date?

We have designed this type of note for investors who want to protect their investment by receiving at least the principal amount of their investment at maturity and who also want to participate in a possible change in the value of the U.S. dollar relative to the Reference Currencies. At maturity, you will receive a payment equal to the sum of:

· the principal amount of the notes; and

· the Additional Amount, if any.

As a result, if you hold the notes until maturity, you will not receive less than the principal amount.

How will the Additional Amount be calculated?

The Additional Amount is a single U.S. dollar amount equal to the principal amount of the notes multiplied by the product of the Upside Leverage times the Basket Return, if the Basket Return is greater than zero, and the Downside Return Rate times the product of –1 times the Basket Return, if the Basket Return is less than or equal to zero; provided that the minimum Additional Amount payable on the notes shall be zero.

The Upside Leverage is 100%.

The Downside Return Rate is 60%.

The Basket Return is the sum of the Weighted Currency Returns. For each Reference Currency, this equals the product of the Weighting for such Reference Currency times a quotient, the numerator of which is the difference of the Initial Reference Currency Rate for such Reference Currency minus the Settlement Rate for such Reference Currency and the denominator of which is the Initial Reference Currency Rate for such Reference Currency.

The Initial Reference Currency Rate for each Reference Currency is as follows:

Reference |

| Initial Reference Currency |

|

BRL |

| 1.7906 |

|

RUB |

| 24.5408 |

|

INR |

| 39.47 |

|

CNY |

| 7.1996 |

|

KRW |

| 946.60 |

|

The Settlement Rate for each Reference Currency is the Reference Exchange Rate on the Valuation Date observed in accordance with the applicable Settlement Rate Option (as defined in “Description of the Notes” below), subject to the occurrence of a Disruption Event (as defined in “Description of the Notes” below).

The Valuation Date is January 26, 2011; provided that, upon the occurrence of a Disruption Event with respect to a Reference Currency, the Valuation Date for the affected Reference Currency may be postponed (as described in “Description of the Notes” below).

The Reference Exchange Rates are, for each Reference Currency, the spot exchange rate for that Reference Currency quoted against the U.S. dollar, expressed as the number of units of the Reference Currency per one USD.

PS-1

For further information concerning the calculation of the Additional Amount, see “Description of the Notes” below. You can review hypothetical Redemption Amount payment examples under “Description of the Notes—Hypothetical Redemption Amount Payment Examples” below.

How will I be able to find the Basket Return at any point in time?

You can obtain the Basket Return at any time by calling your Lehman Brothers sales representative.

You can review the historical performance of the Reference Currencies under “Historical Exchange Rates” below.

Are there any risks associated with my investment?

Yes, the notes will be subject to a number of risks. See “Risk Factors” beginning on page S-4 of the MTN prospectus supplement.

What about taxes?

We intend to treat the notes as contingent payment debt instruments as described under “Certain United States Federal Income Tax Consequences” below and “Supplemental United States Federal Income Tax Consequences—Contingent Payment Debt Instruments” in the MTN prospectus supplement.

What happens in the event of a Disruption Event?

If the Calculation Agent determines that a Disruption Event (as defined in “Description of the Notes” below) relating to one or more of the Reference Currencies is in effect on the scheduled Valuation Date, the Calculation Agent will determine the Basket Return using:

· for each Reference Currency that did not suffer a Disruption Event on the scheduled Valuation Date, the Settlement Rate on the scheduled Valuation Date, and

· for each Reference Currency that did suffer a Disruption Event on the scheduled Valuation Date, the Settlement Rate on the immediately succeeding scheduled Valuation Business Day for such Reference Currency on which no Disruption Event occurs or is continuing with respect to such Reference Currency;

provided however that if a Disruption Event has occurred or is continuing with respect to a Reference Currency on each of the three scheduled Valuation Business Days following the scheduled Valuation Date, then (a) such third scheduled Valuation Business Day shall be deemed the Valuation Date for the affected Reference Currency; and (b) the Calculation Agent will determine the Settlement Rate for the affected Reference Currency on such day in accordance with the Fallback Rate Observation Methodology, as defined under “Description of the Notes—Currency-Indexed Notes” in the MTN prospectus supplement.

Who is Lehman Brothers Holdings?

Lehman Brothers Holdings Inc. and its subsidiaries (collectively “Lehman Brothers Holdings”) an innovator in global finance, serves the financial needs of corporations, governments and municipalities, institutional clients and high-net-worth clients worldwide. Lehman Brothers Holdings’ worldwide headquarters in New York and regional headquarters in London and Tokyo are complemented by offices in additional locations in North America, Europe, the Middle East, Latin America and the Asia Pacific region. See “Prospectus Summary – Lehman Brothers Holdings Inc.” and “Where You Can Find More Information” on pages 1 and 58, respectively, of the base prospectus.

You may request a copy of any document Lehman Brothers Holdings files with the Securities and Exchange Commission, or the SEC, pursuant to the Securities and Exchange Act of 1934, at no cost, by writing or telephoning Lehman Brothers Holdings at the address set forth under the caption “Where You Can Find More Information” in the base prospectus.

What is the role of Lehman Brothers Inc.?

Lehman Brothers Inc., one of our subsidiaries, will be the agent and the calculation agent for purposes of determining whether the Additional Amount is payable on the Maturity Date as well as determining whether a Disruption Event has occurred. Potential conflicts of interest may exist between Lehman Brothers Inc. and you as a beneficial owner of the notes. See “Risk Factors—An affiliate of ours may act as calculation agent on the notes, creating a potential conflict of interest between you and us” in the MTN prospectus supplement and “Description of the Notes” below.

Can you tell me more about the effect of hedging activity by Lehman Brothers Holdings?

We expect to hedge our obligations under the notes through one or more of our affiliates. This hedging activity will likely involve trading in the Reference Currencies or in other instruments, such as options, swaps or futures, based on the Reference Currencies. This hedging activity could adversely affect the price at which your notes will trade in the secondary market. Moreover, this hedging activity may result in

PS-2

us or our affiliates receiving a profit, even if the market value of the notes declines.

In what form will the notes be issued?

The notes of each series will be represented by one or more global securities that will be deposited with and registered in the name of The Depository Trust Company or its nominee. Except in very limited circumstances you will not receive a certificate for your notes.

Will the notes be listed on a stock exchange?

No, the notes will not be listed on a stock exchange.

After the initial offering of the notes, Lehman Brothers Inc. intends to make a market in the notes and may stabilize or maintain the market price of the notes during the initial distribution of the notes. However, Lehman Brothers Inc. will not be obligated to engage in any of these market activities or to continue them once they are begun. No assurance can be given as to the liquidity of the trading market for the notes.

PS-3

RISK FACTORS

An investment in the notes entails certain risks not associated with an investment in conventional floating rate or fixed rate medium-term notes. See “Risk Factors” generally, and “Risk Factors—Risks Relating to Currency-Indexed Notes” specifically, in the MTN prospectus supplement.

DESCRIPTION OF THE NOTES

The U.S.$875,000 aggregate principal amount of FX Basket-Linked Notes Due January 31, 2011 offered hereby are Medium-Term Notes, Series I, of Lehman Brothers Holdings Inc. The CUSIP number for the notes is 52517P6E6 and the ISIN number is US52517P6E64. The notes will be issued in book-entry form only, and will be eligible for transfer through the facilities of DTC or any successor depository. See “Book-Entry Procedures and Settlement” in the base prospectus.

The notes will be issued in minimum denominations of U.S.$1,000 and in integral multiples of U.S.$1,000 in excess thereof, and will have a stated “Maturity Date” of January 31, 2011 or if such day is not a New York business day, the next succeeding New York business day.

The notes allow you to hold via a single basket a long and short position simultaneously in the Brazilian Real (BRL), Russian Ruble (RUB), Indian Rupee (INR), Chinese Renminbi (CNY) and South Korean Won (KRW), relative to the U.S. dollar (USD). Each of the BRL, RUB, INR, CNY and KRW (each a “Reference Currency” and, collectively, the “Reference Currencies”) makes up a portion of the “Basket” with a weighting, on the date of this pricing supplement, of 20%.

If held to the Maturity Date, holders of the notes will receive on the Maturity Date a single payment in U.S. dollars in an amount equal to the Redemption Amount as described below. No interest will accrue during the term of the notes and no interest will be payable on the Maturity Date except in the event that the Redemption Amount is not paid when due, as described below.

The “Reference Exchange Rates” are, for each Reference Currency, the spot exchange rate for that Reference Currency quoted against the U.S. dollar, expressed as the number of units of the Reference Currency per one USD.

The “Settlement Rate” for each Reference Currency is the Reference Exchange Rate on the Valuation Date, determined in accordance with the applicable Settlement Rate Option (subject to the occurrence of a Disruption Event).

The “Upside Leverage” is 100%.

The “Downside Return Rate” is 60%.

The “Redemption Amount” for each note will be an amount equal to the sum of the principal amount of each note plus the Additional Amount, if any. The Additional Amount is linked to the Basket Return, which in turn is based on whether the USD has appreciated or depreciated, in aggregate, relative to the Reference Currencies on the Valuation Date. Holders of the notes will receive on the Maturity Date an amount equal to not less than the principal amount of each note.

The “Additional Amount” is a single U.S. dollar amount equal to the principal amount of the notes multiplied by the product of the Upside Leverage times the Basket Return, if the Basket Return is greater than zero, and the Downside Return Rate times the product of –1 times the Basket Return, if the Basket Return is less than or equal to zero; provided that the minimum Additional Amount payable on the notes shall be zero.

The “Basket Return” is the sum of the Weighted Currency Returns for each Reference Currency. The “Weighted Currency Return” for each Reference Currency is the product of the Weighting for such Reference Currency times a quotient, the numerator of which is the difference of the Initial Reference Currency Rate for such Reference Currency minus the Settlement Rate for such Reference Currency and the denominator of which is the Initial Reference Currency Rate for such Reference Currency.

The “Initial Reference Currency Rate” for each Reference Currency is the Reference Exchange Rate for that Reference Currency on the Trade Date, determined in accordance with the applicable Settlement Rate Option, as follows:

Reference |

| Weighting |

| Initial Reference |

|

BRL |

| 20% |

| 1.7906 |

|

RUB |

| 20% |

| 24.5408 |

|

INR |

| 20% |

| 39.47 |

|

CNY |

| 20% |

| 7.1996 |

|

KRW |

| 20% |

| 946.60 |

|

PS-4

The “Valuation Date” is January 26, 2011; provided that, upon the occurrence of a Disruption Event with respect to a Reference Currency, the Valuation Date for the affected Reference Currency may be postponed (as described below).

The “Trade Date” is the date hereof.

The “Issue Date” is January 31, 2008.

The “Settlement Rate Option” and “Valuation Business Day” for each Reference Currency are as follows:

Reference |

| Screen Reference |

| Valuation |

|

BRL |

| BRFR |

| Brazilia, Rio de Janiero or |

|

RUB |

| EMTA |

| Moscow |

|

INR |

| RBIB |

| Mumbai |

|

CNY |

| SAEC |

| Beijing |

|

KRW |

| KFTC18 |

| Seoul |

|

For further information concerning the Settlement Rate Option and Valuation Business Day, see “Description of the Notes—Currency-Indexed Notes” in, and Appendix A to, the MTN prospectus supplement.

If a Disruption Event relating to one or more of the Reference Currencies is in effect on the scheduled Valuation Date, the Calculation Agent will determine the Basket Return using:

· for each Reference Currency that did not suffer a Disruption Event on the scheduled Valuation Date, the Settlement Rate on the scheduled Valuation Date, and

· for each Reference Currency that did suffer a Disruption Event on the scheduled Valuation Date, the Settlement Rate on the immediately succeeding scheduled Valuation Business Day for such Reference Currency on which no Disruption Event occurs or is continuing with respect to such Reference Currency;

provided however that if a Disruption Event has occurred or is continuing with respect to a Reference Currency on each of the three scheduled Valuation Business Days following the scheduled Valuation Date, then (a) such third scheduled Valuation Business Day shall be deemed the Valuation Date for the affected Reference Currency; and (b) the Calculation Agent will determine the Settlement Rate for the affected Reference Currency on such day in accordance with the Fallback Rate Observation Methodology, as defined under “Description of the Notes—Currency-Indexed Notes” in the MTN prospectus supplement.

A “Disruption Event” means any of the following events as determined in good faith by the Calculation Agent:

(A) the occurrence and/or existence of an event on any day that has the effect of preventing or making impossible the delivery of USD from accounts inside the Reference Currency Jurisdiction for that Reference Currency to accounts outside that Reference Currency Jurisdiction;

(B) the occurrence of any event causing the Reference Exchange Rate for the Reference Currency to be split into dual or multiple currency exchange rates; or

(C) the Settlement Rate being unavailable for the Reference Currency, or the occurrence of an event (i) in the Reference Currency Jurisdiction for that Reference Currency that materially disrupts the market for the Reference Currency or (ii) that generally makes it impossible to obtain the Settlement Rate for the Reference Currency, on the Valuation Date.

For purposes of the above, “scheduled Valuation Business Day” means a day that is or, in the judgment of the Calculation Agent, should have been, a Valuation Business Day for the affected Reference Currency.

The notes are not subject to redemption at our option or to repayment at the option of the Holders of the notes prior to the Maturity Date.

In case an event of default (as described in the base prospectus) with respect to any note shall have occurred and be continuing, the amount that may be declared due and payable upon any acceleration of the notes will be determined by the Calculation Agent for the period from and including the Issue Date to but excluding the date of early repayment and will equal, for each note, the Redemption Amount, calculated as though the date of early repayment were the Maturity Date. If a bankruptcy proceeding is commenced in respect of Lehman Brothers Holdings, the claim of the beneficial owner of a note for the period from and including the Issue Date to but excluding the date of early repayment will be capped at the Redemption Amount, calculated as though the

PS-5

date of the commencement of the proceeding were the Maturity Date.

Any overdue payment in respect of any note will bear interest until the date upon which all sums due in respect of such note are received by or on behalf of the relevant Holder, at the rate per annum that is the rate for deposits in U.S. dollars for a period of six months that appears on the Reuters Screen LIBOR page as of 11:00 a.m. (London time) on the first London business day following such failure to pay. Such rate will be determined by the Calculation Agent. If interest in respect of overdue amounts is calculated for a period of less than one year, it will be calculated on the basis of a 360-day year consisting of 12 months of 30 days each, and, in the case of an incomplete month, the number of days elapsed.

The “Calculation Agent” means Lehman Brothers Inc.

PS-6

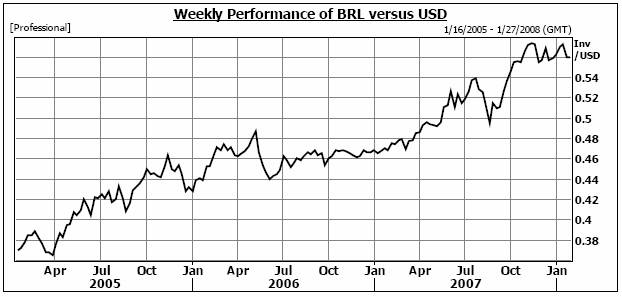

HISTORICAL EXCHANGE RATES

General

The notes allow you to hold via a single basket a long and short position simultaneously in the Reference Currencies relative to the U.S. dollar.

Historical Data on the Reference Currencies

The following charts show the spot exchange rates for each Reference Currency at the end of each week in the period from the week ending January 16, 2005, through the week ending January 27, 2008, using historical data obtained from Reuters; neither Lehman Brothers Inc. nor Lehman Brothers Holdings Inc. makes any representation or warranty as to the accuracy or completeness of this data. The spot exchange rates are expressed as the amount of Reference Currency per U.S. dollar to show the appreciation or depreciation, as the case may be, of the U.S. dollar relative to the Reference Currency. The spot exchange rates used to calculate the Basket Return are expressed as the amount of Reference Currency per U.S. dollar, which are the inverse of the spot exchange rates presented in the following charts. The historical data on each Reference Currency is not necessarily indicative of the future performance of the Reference Currencies, the Basket Return or what the value of the notes may be. Fluctuations in exchange rates make it difficult to predict whether the Basket Return will be greater than, less than or equal to zero and, consequently, the Additional Amount payable at maturity. Historical exchange rate fluctuations may be greater or lesser than those experienced by the holders of the notes.

PS-7

PS-8

PS-9

Hypothetical Historical Basket Return

The following charts show the hypothetical Basket Return at the end of each week in the period from the week ending January 16, 2005, through the week ending January 27, 2008, and on the Trade Date, based on the hypothetical composite performance of the Reference Currencies using data obtained from Reuters; neither Lehman Brothers Inc. nor Lehman Brothers Holdings Inc. makes any representation or warranty as to the accuracy or completeness of this data. The Basket Return was indexed to a level of 0.0 on the Trade Date, based upon the Reference Exchange Rates determined on that day. The composite value of the Reference Currencies on any prior day was obtained by using the calculation of the Basket Return described above. Spot exchange rates used in this determination are expressed as the number of units of Reference Currency per U.S. dollar. For purposes of the notes and the determination of the Additional Amount, the Basket Return was indexed to 0.0 on the Trade Date.

PS-10

Hypothetical Redemption Amount Payment Examples

The following payment examples for this note shows scenarios for the Redemption Amount payable at maturity of the notes, including scenarios for the Additional Amounts payable if the Basket Return is greater or less than zero, based on the an Upside Leverage of 100%, a Downside Return Rate of 60% and the Initial Reference Currency Rates (each of which were determined on the Trade Date), as well hypothetical values for the Settlement Rates (which will be determined on the Valuation Date), and the resulting Basket Return.

The Settlement Rate values for the Reference Currencies have been chosen arbitrarily for the purpose of these examples, are not associated with Lehman Brothers Research forecasts for any Reference Currency/USD exchange rates and should not be taken as indicative of the future performance of any Reference Currency/USD exchange rate.

Example 1: BRL, RUB, INR, CNY and KRW appreciate relative to their respective Initial Reference Currency Rates, resulting in a Basket Return of 0.0720. The Additional Amount is therefore equal to $72.00 or 7.20%, and the Redemption Amount is equal to the product of 107.20% times the principal amount of the notes.

Because the Basket Return is 0.0720, the Redemption Amount payable at maturity is equal to $1,072.00 per $1,000 note (reflecting an Additional Amount of $72.00 per $1,000 note), calculated as follows:

Redemption Amount = $1,000 + ($1,000 * 100% * 0.0720) = $1,072.00

The table below illustrates how the Basket Return in the above example was calculated:

Reference |

| Initial Reference |

| Weighting |

| Hypothetical |

| Weighted Currency |

|

BRL |

| 1.7906 |

| 20% |

| 1.6653 |

| 0.0140 |

|

RUB |

| 24.5408 |

| 20% |

| 22.5775 |

| 0.0160 |

|

INR |

| 39.47 |

| 20% |

| 35.13 |

| 0.0220 |

|

CNY |

| 7.1996 |

| 20% |

| 6.7676 |

| 0.0120 |

|

KRW |

| 946.60 |

| 20% |

| 908.74 |

| 0.0080 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Basket Return = |

| 0.0720 |

|

PS-11

Example 2: BRL, RUB, INR, CNY and KRW depreciate relative to their respective Initial Reference Currency Rates, resulting in a Basket Return of –0.0456. Because the Basket Return is less than zero, the Additional Amount is equal to $27.36 or 2.736%, and the Redemption Amount is equal to 102.736%, times the principal amount of the notes.

Because the Basket Return is –0.0456, the Redemption Amount payable at maturity is equal to $1,027.36 per $1,000 note (reflecting an Additional Amount of $27.36 per $1,000 note), calculated as follows:

Redemption Amount = $1,000 + ($1,000 * 60% * [ –1 * –0.0456] ) = $1,027.36

The table below illustrates how the Basket Return in the above example was calculated:

Reference |

| Initial Reference |

| Weighting |

| Hypothetical |

| Weighted Currency |

|

BRL |

| 1.7906 |

| 20% |

| 1.8658 |

| –0.0084 |

|

RUB |

| 24.5408 |

| 20% |

| 25.0562 |

| –0.0042 |

|

INR |

| 39.47 |

| 20% |

| 41.68 |

| –0.0112 |

|

CNY |

| 7.1996 |

| 20% |

| 7.7684 |

| –0.0158 |

|

KRW |

| 946.60 |

| 20% |

| 975.00 |

| –0.0060 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Basket Return = |

| –0.0456 |

|

Example 3: BRL, RUB and KRW appreciate relative to their respective Initial Reference Currency Rates, while INR and CNY depreciate relative to their respective Initial Currency Rates, resulting in a Basket Return of 0.0310. The Additional Amount is therefore $31.00 or 3.10%, and the Redemption Amount is equal to the product of 103.10% times the principal amount of the notes.

Because the Basket Return is 0.0310, the Redemption Amount payable at maturity is equal to $1,031.00 per $1,000 note (reflecting an Additional Amount of $31.00 per $1,000 note), calculated as follows:

Redemption Amount = $1,000 + ($1,000 * 100% * 0.0310) = $1,031.00

The table below illustrates how the Basket Return in the above example was calculated:

Reference |

| Initial Reference |

| Weighting |

| Hypothetical |

| Weighted Currency |

|

BRL |

| 1.7906 |

| 20% |

| 1.6080 |

| 0.0204 |

|

RUB |

| 24.5408 |

| 20% |

| 22.4794 |

| 0.0168 |

|

INR |

| 39.47 |

| 20% |

| 40.42 |

| –0.0048 |

|

CNY |

| 7.1996 |

| 20% |

| 7.4660 |

| –0.0074 |

|

KRW |

| 946.60 |

| 20% |

| 918.20 |

| 0.0060 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Basket Return = |

| 0.0310 |

|

PS-12

Example 4: BRL, INR and KRW depreciate relative to their respective Initial Reference Currency Rates, while RUB and CNY appreciate relative to their respective Initial Reference Currency Rates, resulting in a Basket Return of –0.0272. The Additional Amount is therefore equal to $16.32 or 1.632%, and the Redemption Amount is equal to the product of 101.632% times the principal amount of the notes.

Because the Basket Return is –0.0272, the Redemption Amount payable at maturity is equal to $1,016.32 per $1,000 note (reflecting an Additional Amount of $16.32 per $1,000 note), calculated as follows:

Redemption Amount = $1,000 + ($1,000 * 60% * [ –1* –0.0272] ) = $1,016.32

The table below illustrates how the Basket Return in the above example was calculated:

Reference |

| Initial Reference |

| Weighting |

| Hypothetical |

| Weighted Currency |

|

BRL |

| 1.7906 |

| 20% |

| 2.0467 |

| –0.0286 |

|

RUB |

| 24.5408 |

| 20% |

| 23.7555 |

| 0.0064 |

|

INR |

| 39.47 |

| 20% |

| 45.51 |

| –0.0306 |

|

CNY |

| 7.1996 |

| 20% |

| 6.0621 |

| 0.0316 |

|

KRW |

| 946.60 |

| 20% |

| 975.00 |

| –0.0060 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Basket Return = |

| –0.0272 |

|

PS-13

CERTAIN UNITED STATES FEDERAL INCOME TAX CONSEQUENCES

We intend to treat the notes as contingent payment debt instruments, as described under “Supplemental United States Federal Income Tax Consequences—Contingent Payment Debt Instruments” in the MTN prospectus supplement.

PS-14

SUPPLEMENTAL PLAN OF DISTRIBUTION

We have agreed to sell to Lehman Brothers Inc. (the “Agent”), and the Agent has agreed to purchase from us, the principal amount of the notes at the price specified on the cover of this pricing supplement. The Agent is committed to take and pay for all of the notes, if any are taken.

The Agent proposes to offer the notes initially at a public offering price equal to the public offering price on the cover of this pricing supplement and to certain dealers at a discount not to exceed 2.50%. After the initial public offering, the public offering price and the selling terms may from time to time be varied by the Agent.

It is expected that delivery of the notes will be made against payment therefor more than three business days following the date of this pricing supplement. Trades in the secondary market generally are required to settle in three business days unless the parties to any such trade expressly agree otherwise. Accordingly, purchasers who wish to trade the securities on any day prior to the third business day before the settlement date will be required to specify an alternative settlement cycle at the time of any such trade to prevent failed settlement.

If the notes are sold in a market-making transaction after their initial sale, information about the purchase price and the date of the sale wil l be provided in a separate confirmation of sale.

PS-15

U.S.$875,000

LEHMAN BROTHERS HOLDINGS INC.

MEDIUM-TERM NOTES, SERIES I

FX BASKET-LINKED NOTES

DUE JANUARY 31, 2011

PRICING SUPPLEMENT

JANUARY 28, 2008

(INCLUDING PROSPECTUS SUPPLEMENT

DATED MAY 30, 2006 AND

PROSPECTUS

DATED MAY 30, 2006)

LEHMAN BROTHERS