Lehman Brothers Holdings Inc Plan Trust (LEHMQ)

Filed: 7 Mar 08, 12:00am

Calculation of the Registration Fee

Title of Each Class of |

| Maximum Aggregate Offering |

| Amount of Registration |

Notes |

| $100,000 |

| $3.93 |

(1) Calculated in accordance with Rule 457(r) of the Securities Act of 1933.

(2) Pursuant to Rule 457(p) under the Securities Act of 1933, filing fees have already been paid with respect to unsold securities that were previously registered pursuant to a Registration Statement on Form S-3 (No. 333-134553) filed by Lehman Brothers Holdings Inc. and the other Registrants thereto on May 30, 2006, and have been carried forward, of which $3.93 is offset against the registration fee due for this offering and of which $1,126,302.29 remains available for future registration fees. No additional registration fee has been paid with respect to this offering.

Filed Pursuant to Rule 424(b)(2)

Registration No. 333-134553

PRICING SUPPLEMENT NO. 733, dated March 5, 2008

(To prospectus dated May 30, 2006 and prospectus supplement dated May 30, 2006)

China Bull Notes

100% Principal Protected at Maturity

Because these notes are part of a series of Lehman Brothers Holdings’ debt securities called Medium-Term Notes, Series I, this pricing supplement should also be read with the accompanying prospectus supplement, dated May 30, 2006 (the “Series I MTN prospectus supplement”) and the accompanying prospectus dated May 30, 2006 (the “base prospectus”). Terms used here have the meanings given to them in the Series I MTN prospectus supplement or the base prospectus, unless the context requires otherwise.

Investing in the notes involves risks. See Risk Factors beginning on page 8 and on page S-4 of the Series I MTN prospectus supplement.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of the Notes or passed upon the accuracy or the adequacy of this pricing supplement, the base prospectus, the Series I MTN prospectus supplement or any other relevant terms. Any representation to the contrary is a criminal offense.

Lehman Brothers Inc., a wholly owned subsidiary of Lehman Brothers Holdings, makes a market in Lehman Brothers Holdings’ securities. It may act as principal or agent in, and this pricing supplement may be used in connection with, those transactions. Any such sales will be made at varying prices related to prevailing market prices at the time of sale.

BASIC TERMS |

|

|

Issuer: |

| Lehman Brothers Holdings Inc. |

Ratings: |

| (A+/A1/AA–)(1) |

Principal Amount: |

| $100,000 |

CUSIP: |

| 5252M0DF1 |

Re-Opening Trade Date: |

| March 5, 2008 |

Original Trade Date: |

| February 25, 2008 |

Issue Date: |

| March 10, 2008 |

Valuation Date: |

| February 21, 2012, or if such day is not a Valuation Business Day, the immediately preceding Valuation Business Day; provided that, upon the occurrence of a Disruption Event with respect to a Basket Component, the Valuation Date for the affected Basket Component may be postponed (as described below under “Disruption Events” below) |

Maturity Date: |

| February 28, 2012, or if such date is not a Business Day, the immediately succeeding Business Day |

Issue Price: |

| 100% |

Interest: |

| The notes do not bear interest. |

(1) Lehman Brothers Holdings Inc. is rated A+ by Standard & Poor’s, A1 by Moody’s and AA- by Fitch. A credit rating reflects the creditworthiness of Lehman Brothers Holdings Inc. and is not a recommendation to buy, sell or hold securities, and it may be subject to revision or withdrawal at any time by the assigning rating organization. Each rating should be evaluated independently of any other rating.

1

Redemption Amount: |

| A single U.S. dollar (“USD”) payment on the Maturity Date equal to the principal amount of each note plus the Additional Amount, if any. | |||||

Additional Amount: |

| A single USD amount equal to the principal amount of each note multiplied by: | |||||

|

| 60.0% | If the Basket Return is greater than or equal to 60.0% | ||||

|

| Basket Return | If the Basket Return is greater than zero, but less than 60.0% | ||||

|

| 0.0% | If the Basket Return is less than or equal to zero | ||||

Basket Return: |

| Weighted Index Return + Weighted Currency Return + Weighted Copper Return + Weighted Crude Oil Return | |||||

TERMS RELATING TO THE WEIGHTED INDEX RETURN: | |||||||

Reference Index: |

| Hang Seng® Index (“Hang Seng Index”) | |||||

Index Level: |

| The daily closing level of the Reference Index, as determined and published by the Index Sponsor (subject to the occurrence of a Disruption Event). | |||||

Initial Index Level: |

| 23,269.14, which is the Index Level on the Original Trade Date | |||||

Final Index Level: |

| The Index Level on the Valuation Date (subject to the occurrence of a Disruption Event) | |||||

Index Sponsor: |

| Hang Seng Indexes Company Limited, a wholly owned subsidiary of the Hang Seng® Bank | |||||

Weighted Index Return: |

| Index Weight * Index Return | |||||

Index Weight: |

| 33.34% | |||||

Index Return: |

|

| Final Index Level – Initial Index Level |

| |||

|

|

| Initial Index Level |

| |||

|

| expressed as a percentage | |||||

TERMS RELATING TO THE WEIGHTED CURRENCY RETURN: | |||||||

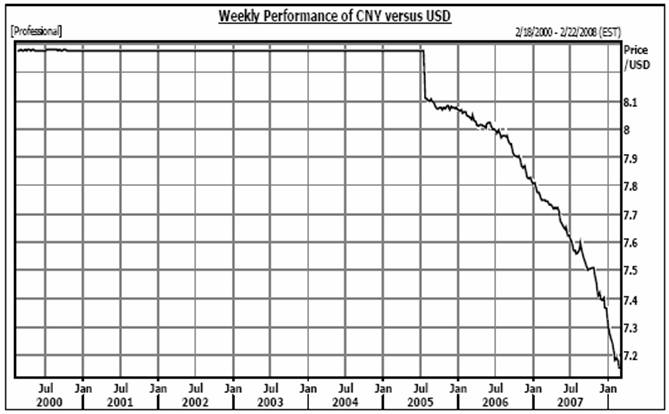

Reference Currency: |

| Chinese Renminbi (“CNY”) | |||||

Reference Exchange Rate: |

| The spot exchange rate for the Reference Currency quoted against the U.S. dollar expressed as number of units of the Reference Currency per one USD. | |||||

Initial Currency Rate: |

| 7.146, which is the Reference Exchange Rate on the Original Trade Date, observed in accordance with the Settlement Rate Option. | |||||

Settlement Rate: |

| The Reference Exchange Rate on the Valuation Date, observed in accordance with the Settlement Rate Option (subject to the occurrence of a Disruption Event). | |||||

Weighted Currency Return: |

| Currency Weight * Currency Return | |||||

Currency Weight: |

| 33.34% | |||||

Currency Return: |

|

| Initial Currency Rate – Settlement Rate |

| |||

|

|

| Initial Currency Rate |

| |||

2

|

| expressed as a percentage | |||

Settlement Rate Option: |

| The CNY/USD official Beijing fixing rate, expressed as the amount of CNY per one USD, for settlement in two Beijing and New York business days reported by The State Administration of Foreign Exchange of the People’s Republic of China, Beijing, which appears on the Reuters Screen SAEC Page opposite the symbol “USDCNY=” at approximately 5:00 p.m., Beijing time, on the relevant day. | |||

TERMS RELATING TO THE WEIGHTED COPPER RETURN: | |||||

Copper: |

| Copper – Grade A | |||

Copper Price: |

| The official settlement price of Copper for cash delivery, expressed as the U.S. dollar price per metric ton, as made public by the Relevant Commodity Exchange for Copper (subject to the occurrence of a Disruption Event). | |||

Initial Copper Price: |

| $8,247, which is the Copper Price on the Original Trade Date | |||

Final Copper Price: |

| The Copper Price on the Valuation Date. | |||

Weighted Copper Return: |

| (Copper Weight * Copper Return) | |||

Copper Weight: |

| 16.66% | |||

Copper Return: |

|

| Final Copper Price – Initial Copper Price |

| |

|

|

| Initial Crude Oil Price |

| |

|

| expressed as a percentage | |||

TERMS RELATING TO THE WEIGHTED CRUDE OIL RETURN: | |||||

Crude Oil: |

| Light sweet crude oil | |||

|

| (Crude Oil and Copper together, the “Reference Commodities” and each a “Reference Commodity”) | |||

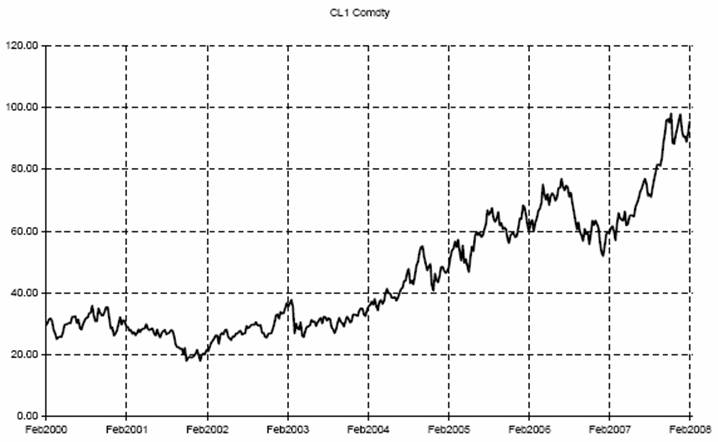

Crude Oil Price: |

| The official settlement price of the first nearby month futures contract (or, in the case of the last trading day of the first nearby month contract, the second nearby month contract) for Crude Oil, expressed as the U.S. dollar price per barrel, as made public by the Relevant Commodity Exchange for Crude Oil (subject to the occurrence of a Disruption Event). | |||

Initial Crude Oil Price: |

| $99.23, which is the Crude Oil Price on the Original Trade Date | |||

Final Crude Oil Price: |

| The Crude Oil Price on the Valuation Date. | |||

Weighted Crude Oil Return: |

| (Crude Oil Weight * Crude Oil Return) | |||

Crude Oil Weight: |

| 16.66% | |||

Crude Oil Return: |

|

| Final Crude Oil Price – Initial Crude Oil Price |

| |

|

|

| Initial Crude Oil Price |

| |

|

| expressed as a percentage | |||

ADDITIONAL TERMS: |

|

| |||

Relevant Commodity |

| For each Reference Commodity, the exchange set forth opposite such Reference Commodity below, or its successor, or if the exchange set forth below is no longer the principal exchange | |||

3

Exchange: |

| or trading market for a Reference Commodity or options or futures contracts for such Reference Commodity, such other exchange or principal trading market for the relevant Reference Commodity as determined in good faith by the Calculation Agent which serves as the source of prices for that Reference Commodity, and any principal exchanges where options or futures contracts on that Reference Commodity are traded. | ||

|

| Reference Commodity |

| Relevant Commodity Exchange |

|

| Copper |

| London Metal Exchange (“LME”) |

|

| Crude Oil |

| The NYMEX Division, or its successor, of the |

Disruption Events: |

| If a Disruption Event relating to one or more of the Reference Index, the Reference Currency or the Reference Commodities (with respect to a Commodity Disruption Event identified in clauses (A), (B) or (C) below) is in effect on the scheduled Valuation Date, the Calculation Agent will calculate the Basket Return using:

· If the Reference Index, the Reference Currency or a Reference Commodity did not suffer a Disruption Event on the scheduled Valuation Date, the Final Index Level, the Settlement Rate, the Final Copper Price or the Final Crude Oil Price, as applicable, on the scheduled Valuation Date, and

· If any or all of the Reference Index, the Reference Currency or a Reference Commodity did suffer a Disruption Event on the scheduled Valuation Date, the Final Index Level, the Settlement Rate, the Final Copper Price and/or the Final Crude Oil Price, as the case may be, on the immediately succeeding Scheduled Index Trading Day, scheduled Currency Business Day or scheduled Commodity Trading Day, as applicable, on which no Disruption Event occurs or is continuing with respect to the affected Reference Index, Reference Currency or Reference Commodity;

provided however that if a Disruption Event with respect to one or more of the Reference Index, the Reference Currency or a Reference Commodity has occurred or is continuing on each of the three Scheduled Index Trading Days, scheduled Currency Business Days or scheduled Commodity Trading Days, as applicable, following the scheduled Valuation Date, then (a) such third Scheduled Index Trading Day, scheduled Currency Business Day or scheduled Commodity Trading Day, as applicable, shall be deemed the Valuation Date for the affected Reference Index, Reference Currency or Reference Commodity, respectively; and (b) the Calculation Agent will determine, on such day, (i) in the case of the Reference Index, its good faith estimate of the Final Index Level, based on the last available Index Level and any other information that in good faith it deems relevant, (ii) in the Case of the Reference Currency, the Settlement Rate in accordance with the “Fallback Rate Observation Methodology” (as defined under “Description of the Notes—Currency-Indexed Notes” in the Series I MTN prospectus supplement), or (iii) in the case of a Reference Commodity, the Final Copper Price or the Final Crude Oil Price, as applicable, for the affected Reference Commodity in its sole and absolute discretion, taking into account the latest available quotation for the Final Copper Price or the Final Crude Oil Price, as the case may be, for the affected Reference Commodity and any other information that in good faith it deems relevant.

If a Commodity Disruption Event identified in clauses (D) or (E) below relating to one or both of the Reference Commodities is in effect on the Valuation Date, the Calculation Agent will determine the Final Copper Price or the Final Crude Oil Price, as applicable, for the affected Reference Commodity on the scheduled Valuation Date in its sole and absolute discretion, taking into account the latest available quotation for the Copper Price and/or the Crude Oil Price, as the case may be, for the affected Reference Commodity and any other information that in good faith it deems relevant.

A “Disruption Event” means, for the Reference Index, an Index Disruption Event, for the Reference Currency, a Currency Disruption Event and for the Reference Commodities, a Commodity Disruption Event.

An “Index Disruption Event” means any of the following events, as determined in good faith by the Calculation Agent:

(A) A material suspension of or limitation imposed on trading relating to the securities that then comprise 20% or more of the level of the Reference Index (or the successor index) by the Relevant Equity Exchanges (as defined below) on which those securities are traded, at any time during the one hour period that ends at the close of trading on | ||

4

|

| such day, whether by reason of movements in price exceeding limits permitted by that Relevant Equity Exchange or otherwise;

(B) A material suspension of or limitation imposed on trading in futures or options contracts related to the Reference Index (or the successor index) by the primary exchange or quotation system on which those futures or options contracts are traded at any time during the one hour period that ends at the close of trading on such day, whether by reason of movements in price exceeding limits permitted by the exchanges or otherwise;

(C) Any event, other than an early closure, that disrupts or impairs the ability of market participants in general to effect transactions in, or obtain market values for the securities that then comprise 20% or more of the Reference Index (or the successor index) on the Relevant Equity Exchanges on which those securities are traded, at any time during the one hour period that ends at the close of trading on that day;

(D) Any event, other than an early closure, that disrupts or impairs the ability of market participants in general to effect transactions in, or obtain market values for, the futures or options contracts relating to the Reference Index (or the successor index) on the primary exchange or quotation system on which those futures or options contracts are traded at any time during the one hour period that ends at the close of trading on such day;

(E) The closure of the Relevant Equity Exchanges on which the securities that then comprise 20% or more of the Reference Index (or the successor index) are traded or on which futures or options contracts relating to the Reference Index (or the successor index) are traded prior to its scheduled closing time unless the earlier closing time is announced by the Relevant Equity Exchanges at least one hour prior to the earlier of (1) the actual closing time for the regular trading session on the Relevant Equity Exchanges and (2) the submission deadline for orders to be entered into the Relevant Equity Exchanges for execution at the close of trading on such day.

For the purpose of determining whether an Index Disruption Event exists at any time:

(1) the relevant percentage contribution of a security to the level of the Reference Index (or the successor index) will be based on a comparison of (x) the portion of the level of the Reference Index (or the successor index) attributable to that security and (y) the overall level of the Reference Index (or the successor index), in each case immediately before the occurrence of the Index Disruption Event;

(2) “close of trading” means in respect of any Relevant Equity Exchange, the scheduled weekday closing time on a day on which the Relevant Equity Exchange is scheduled to be open for trading for its respective regular trading session, without regard to after hours or any other trading outside of the regular trading session hours; and

(3) limitations pursuant to the rules of any Relevant Equity Exchange similar to NYSE Rule 80A (or any applicable rule or regulation enacted or promulgated by any other self-regulatory organization or any government agency of scope similar to NYSE Rule 80A as determined by the Calculation Agent) on trading during significant market fluctuations will constitute a suspension, absence or material limitation of trading.

For purposes of the above, “Relevant Equity Exchange” means the primary organized exchange or market of trading for any security (or any combination thereof) then included in the Reference Index or any successor index.

A “Currency Disruption Event” means any of the following events, as determined in good faith by the Calculation Agent:

(A) the occurrence and/or existence of an event on any day that has the effect of preventing or making impossible (x) the delivery of USD from accounts inside the country for which the Reference Currency is the lawful currency (such jurisdiction with respect to such Reference Currency, the “Reference Currency Jurisdiction”) to accounts outside that Reference Currency Jurisdiction or (y) the conversion of the Reference Currency into USD through customary legal channels;

(B) the occurrence of any event causing the Reference Exchange Rate for the Reference Currency to be split into dual or multiple currency exchange rates; or |

5

|

| (C) the Settlement Rate being unavailable for the Reference Currency, or the occurrence of an event (i) in the Reference Currency Jurisdiction for that Reference Currency that materially disrupts the market for the Reference Currency or (ii) that generally makes it impossible to obtain the Settlement Rate for the Reference Currency, on the Valuation Date.

For purposes of the above, “scheduled Currency Business Day” means a day that is or, in the judgment of the Calculation Agent, should have been, a Currency Business Day.

A “Commodity Disruption Event” with respect to a Reference Commodity means any of the following events, as determined in good faith by the Calculation Agent:

(A) the suspension of or material limitation on trading in the Reference Commodity or futures contracts or options related to the Reference Commodity, on the Relevant Commodity Exchange for that Reference Commodity;

(B) either (i) the failure of trading to commence, or permanent discontinuance of trading, in the Reference Commodity, or futures contracts or options related to the Reference Commodity, on the Relevant Commodity Exchange for that Reference Commodity, or (ii) the disappearance of, or of trading in, the Reference Commodity;

(C) the failure of the Relevant Commodity Exchange for the Reference Commodity to publish the official daily settlement price of the Reference Commodity for that day (or the information necessary for determining the settlement price);

(D) the occurrence since the Original Trade Date of a material change in the content, composition, or constitution of the Reference Commodity; or

(E) the occurrence since the Original Trade Date of a material change in the formula for or the method of calculating the settlement price of the Reference Commodity.

For the purpose of determining whether a Commodity Disruption Event for a Reference Commodity has occurred:

(1) a limitation on the hours in a trading day and/or number of days of trading will not constitute a Commodity Disruption Event if it results from an announced change in the regular business hours of the Relevant Commodity Exchange for the Reference Commodity;

(2) a suspension in trading in a Reference Commodity on the Relevant Commodity Exchange for that Reference Commodity (without taking into account any extended or after-hours trading session), by reason of a price change reflecting the maximum permitted price change from the previous trading day’s settlement price will constitute a Commodity Disruption Event; and

(3) a suspension of or material limitation on trading on a Relevant Commodity Exchange for a Reference Commodity will not include any time when the Relevant Commodity Exchange for that Reference Commodity is closed for trading under ordinary circumstances.

For purposes of the above, “scheduled Commodity Trading Day” means a day, as determined in good faith by the Calculation Agent, on which trading is generally conducted on the Relevant Commodity Exchange applicable to the affected Reference Commodity. |

Index Discontinuation / Alteration |

| For provisions governing modifications to the Reference Index or the Index Level in the event the Reference Index is discontinued or the method of its calculation is modified, see “The Hang Seng® Index—Discontinuation of the Hang Seng® Index; Alteration of Method of Calculation” below. |

Valuation Business Day: |

| Any day that is each of (a) a Scheduled Index Trading Day for the Reference Index. (b) a Currency Business Day for the Reference Currency, and (c) a Commodity Business Day for the Reference Commodities. |

Scheduled Index Trading Day: |

| Any day on which the Hang Seng (or any successor index) is published by the Sponsor (or the publisher of such successor index) or otherwise determined by the Calculation Agent. |

Currency Business Day: |

| Any day that is not a Saturday, a Sunday or a day on which banking institutions generally are authorized or obligated by law or executive order to be closed (including for dealings in foreign exchange in accordance with the market practice of the foreign exchange market) in Beijing. |

6

Commodity Business Day: |

| A day, as determined in good faith by the Calculation Agent, on which the Relevant Commodity Exchange for each Reference Commodity is scheduled to be (or, but for the occurrence of a Commodity Disruption Event, would have been) open for trading during its regular trading session (notwithstanding the Relevant Commodity Exchange closing prior to its scheduled closing time). | |||||||||

Business Days: |

| New York | |||||||||

Underwriter: |

| Lehman Brothers Inc. | |||||||||

Calculation Agent |

| Lehman Brothers Inc. | |||||||||

Denomination: |

| US$1,000 and integral multiples of US$1,000 | |||||||||

Issue Type: |

| US MTN | |||||||||

Fees: |

|

|

| Price to Public (1) |

| Fees (2) |

| Proceeds to the Issuer | |||

|

| Per note |

| $ | 1,000 |

| $ | 20.00 |

| $ | 980.00 |

|

| Total (3) |

| $ | 100,000 |

| $ | 2,000 |

| $ | 98,000 |

|

| (1) The price to public includes Lehman Brothers Holdings Inc.’s cost of hedging its obligations under the notes through one or more of its affiliates, which includes such affiliates expected cost of providing such hedge as well as the profit the such affiliates expect to realize in consideration for assuming the risks inherent in providing such hedge.

(2) Lehman Brothers Inc. will receive commissions of $20.00 per $1,000.00 principal amount, or 2.00%, and may use all or a portion of these commissions to pay selling concessions or fees to other dealers. Lehman Brothers Inc. and/or an affiliate may earn additional income as a result of payments pursuant to any hedges.

(3) The notes will be issued in an aggregate principal amount of $100,000 and will be a further issuance of, and will form a single tranche with, the $3,260,000 aggregate principal amount of Medium-Term Notes, Series I, due February 28, 2012, that Lehman Brothers Holdings issued on February 28, 2008 and the $285,000 aggregate principal amount of Medium-Term Notes, Series I, due February 28, 2012, that Lehman Brothers Holdings issued on March 4, 2008. The notes will have the same CUSIP and ISIN numbers as the other notes of this tranche and are expected to settle on March 10, 2008. The notes will trade interchangeably with the other notes of this tranche. The issuance of the notes will increase the aggregate principal amount of the outstanding notes of this tranche to $3,645,000. | |||||||||

7

Risk Factors

An investment in the notes entails certain risks not associated with an investment in conventional floating rate or fixed rate medium term notes. See “Risk Factors” generally in the Series I MTN prospectus supplement. For particular risks relating to an investment related to the Reference Currency, see “Risk Factors—Risks Relating to Currency-Indexed Notes” in the Series I MTN prospectus supplement. In addition, the notes are subject to the further specific risks discussed below.

Risks Related to the Notes

The notes do not bear interest and your return on the notes at maturity is dependent on the Basket Return

The notes do not bear interest, and the return on the notes at maturity is dependent on the Basket Return, which in turn depends on the combined performance of the Reference Index, the Reference Currency and the Reference Commodities. Because the notes do not bear interest, if the Basket Return is equal to or less than zero, the Additional Amount will be zero, and you will receive at maturity only the return of your principal invested, with no additional return. In addition, if the Basket Return is greater than or equal to 60%, the Additional Amount will be capped at an amount equal to the principal amount of each note multiplied by 60%. The Additional Amount you receive will not be greater than this capped amount.

The inclusion in the original issue price of the broker’s fee and Lehman Brothers Holdings Inc.’s cost of hedging its obligations under the notes through one or more of its affiliates is likely to adversely affect the value of the notes prior to maturity.

The original issue price of the notes includes the broker’s fee and Lehman Brothers Holdings Inc.’s cost of hedging its obligations under the notes through one or more of its affiliates. Such cost includes such affiliates’ expected cost of providing a hedge, as well as the profit these affiliates expect to realize in consideration for assuming the risks inherent in providing such hedge. As a result, assuming no change in market conditions or any other relevant factors, the price, if any, at which a broker will be willing to purchase notes from you in secondary market transactions, if at all, will likely be lower than the original issue price. In addition, any such prices may differ from values determined by pricing models used by a broker, as a result of such compensation or other transaction costs.

The return on your notes may not reflect all developments in the Reference Index, the Reference Currency or the Reference Commodities.

The Additional Amount payable on the notes is dependent on the Basket Return, which in turn depends on the combined performance of the Reference Index, the Reference Currency and the Reference Commodities on the Valuation Date, a single Valuation Business Day near the end of the term of the notes. As a result, the Index Level, the Reference Exchange Rate, the Copper Price and the Crude Oil Price at other times during the term of the notes or at the Maturity Date could be higher than the Final Index Level, the Settlement Rate, the Final Copper Price and the Final Crude Oil Price, respectively. This difference could be particularly large if there is a significant decrease in the Index Level, the Reference Exchange Rate, the Copper Price and/or the Crude Oil Price during the latter portion of the term of the notes or if there is significant volatility in the Reference Index, the Reference Currency and/or the Reference Commodities during the term of the notes, especially on dates near the Valuation Date.

Many factors affect the market value of the notes; these factors interrelate in complex ways and the effect of any one factor may offset or magnify the effect of another factor.

The market value of the notes will be affected by factors that interrelate in complex ways. The effect of one factor may offset the increase in the market value of the notes caused by another factor and the effect of one factor may exacerbate the decrease in the market value of the notes caused by another factor. For example, the market value of the notes will be affected by changes in the level of interest rates, the time to maturity of the notes (and any associated “time premium”) and the credit ratings of Lehman Brothers Holdings Inc. In addition, the market value of the notes will also be affected by certain specific factors, which are described in the following paragraphs (along with the expected impact on the market value of the notes given a change in that specific factor, assuming all other conditions remain constant).

The Index Level, the Reference Exchange Rate and the prices of the Reference Commodities will affect the market value of the notes. It is expected that the market value of the notes will depend on the combined performance of the Reference Index, the Reference Currency and the Reference Commodities. If you choose to sell your notes when the Index Level is at or below the Initial Index Level, the Reference Exchange Rate is at or below the Initial Currency Rate, the Copper Price is at or below the Initial Copper Price, and/or the Crude Oil Price is at or below the Initial Crude Oil Price, or when the market perceives an increased risk of this occurring, the trading price of the notes may be adversely affected.

The forward prices of the Reference Commodities may be lower than spot prices, which imply a decline in spot prices over time. Your return on the notes depends, in part, on the Final Crude Oil Price being greater than the Initial Crude Oil Price and/or the Final Copper Price being greater than the Initial Copper Price, which in turn depends on the prices for Copper and Crude Oil appreciating relative to the Initial Copper Price and Initial Crude Oil Price, respectively. However, the prices for the Component Commodities are currently in “backwardation”, meaning that the forward prices are currently lower than the spot prices, and which implies that the prices of the Component Commodities are expected to decrease in the future..

8

Changes in the volatility of the Reference Index, the Reference Currency and the Reference Commodities are expected to affect the market value of the notes. Volatility is the term used to describe the size and frequency of price and/or market fluctuations. If the volatility of the Reference Index, the Reference Currency or the Reference Currencies increases or decreases, the market value of the notes may be adversely affected. The volatility of the Reference Index, the Reference Currency and the Reference Commodities are affected by a variety of factors, including governmental programs and policies, national and international political and economic events (including terrorist attacks and wars), changes in interest and exchange rates and trading activity in the Reference Index, the Reference Currency or the Reference Commodities and options, futures, forwards or other derivatives on the Reference Index, the Reference Currency or the Reference Commodities.

Suspension or disruptions of market trading in the commodity markets may adversely affect the value of the notes. The commodity markets are subject to temporary distortions or other disruptions due to various factors, including the lack of liquidity in the markets, the participation of speculators and government regulation and intervention. These circumstances could adversely affect the prices of one or more of the Reference Commodities and, therefore, the value of your notes.

Active trading in options, futures contracts, options on futures contracts and underlying commodities may adversely affect the value of the notes. Lehman Brothers Commodity Services Inc. and certain other affiliates of Lehman Brothers Holdings Inc. actively trade the Reference Commodities, futures contracts on the Reference Commodities on a spot and forward basis and other contracts and products in or related to the Reference Commodities and other derivative products (including futures contracts, options on futures contracts and options and swaps on the Reference Commodities). Lehman Brothers Holdings Inc., Lehman Brothers Inc. or their affiliates may also issue or underwrite other financial instruments with returns indexed to one or more of the Reference Commodities or futures contracts on the Reference Commodities and derivative commodities. These trading and underwriting activities by Lehman Brothers Holdings Inc., Lehman Brothers Inc., Lehman Brothers Commodity Services Inc. or their affiliates, or by unaffiliated third parties, could adversely affect the prices of the Reference Commodities, which could in turn affect the return on and the value of the notes.

As a result of factors that impact the market value of the notes, selling the notes (or any fixed income investment) prior to maturity may result in a loss of principal invested.

You must rely on your own evaluation of the merits of an investment linked to the Reference Index, the Reference Currency and the Reference Commodities.

In the ordinary course of their businesses, affiliates of Lehman Brothers Holdings Inc. may from time to time express views on expected movements in the Index Level (or the equity securities that comprise the Reference Index), the Reference Exchange Rate and the price of the Reference Commodities. These views are sometimes communicated to clients who participate in the markets for the Reference Index (or the equity securities that comprise the Reference Index), the Reference Currency and the Reference Commodities. However, these views, depending upon worldwide economic, political and other developments, may vary over differing time horizons and are subject to change. Moreover, other professionals who deal in the markets for the Reference Index (or the equity securities that comprise the Reference Index), the Reference Currency and the Reference Commodities and other sectors may at any time have significantly different views from those of Lehman Brothers Holdings Inc. or its affiliates. In connection with your purchase of the notes, you should investigate the Reference Index, the Reference Currency and the Reference Commodities and not rely on views which may be expressed by Lehman Brothers Holdings Inc. or its affiliates in the ordinary course of their businesses with respect to future movements of the Index Level (or the equity securities that comprise the Reference Index), the Reference Exchange Rate and the prices of the Reference Commodities.

You should make such investigation as you deem appropriate as to the merits of an investment linked to the Reference Index, the Reference Currency and the Reference Commodities. Neither the offering of the notes nor any views which may from time to time be expressed by Lehman Brothers Holdings Inc. or its affiliates in the ordinary course of their businesses with respect to future movements of the Index Level (or the equity securities that comprise the Reference Index), the Reference Exchange Rate and the prices of the Reference Commodities constitutes a recommendation as to the merits of an investment in your notes.

Certain events may require a postponement in the Valuation Date for one or more of the Reference Index, the Reference Currency and/or the Reference Commodities and may adversely affect the value of the notes.

Certain events constitute Disruption Events under the terms of the notes. For further information on these events, see “Disruption Events” above. To the extent any of these events occurs with respect to one or more of the Reference Index, the Reference Currency and/or the Reference Commodities and remains in effect on the scheduled Valuation Date for the notes, the Valuation Date for the Reference Index, the Reference Currency and/or the Reference Commodities, as the case may be, may be postponed. In the event the Valuation Date is delayed, the Basket Return, and therefore the Additional Amount (and related Redemption Amount ), may be lower, than what you may have anticipated based on the last available Index Level, Reference Exchange Rate and/or prices of the Reference Commodities, as the case may be, as of the scheduled Valuation Date.

9

Risks Related to the Reference Index

The Index Sponsor may adjust the Reference Index in a way that affects its level and adversely affects the value of the notes; the Index Sponsor has no obligation to consider your interests.

The Index Sponsor is responsible for calculating and maintaining the Reference Index. Lehman Brothers Holdings Inc. is not affiliated with the Index Sponsor in any way (except for the licensing arrangement discussed below under “The Hang Seng® Index”) and has no way to control or predict the Index Sponsor’s actions, including any errors in or discontinuation of disclosure regarding its methods or policies relating to the calculation of the Reference Index.

The Index Sponsor can add, delete or substitute the stocks underlying the Reference Index or make other methodological changes that could change the level of the Reference Index. You should realize that the changing of companies included in the Reference Index may affect the level of the Reference Index, and in turn the Basket Return, as a newly added company may perform significantly better or worse than the company or companies it replaces. Additionally, the Index Sponsor may alter, discontinue or suspend calculation or dissemination of the Reference Index. Any of these actions could affect the Basket Return and adversely affect the value of your notes. The Index Sponsor has no obligation to consider your interests in calculating or revising the Reference Index. See “The Hang Seng® Index.”

Neither Lehman Brothers Holdings Inc. nor any of its affiliates assumes any responsibility for the adequacy or accuracy of the information about the Reference Index or the Index Sponsor in this pricing supplement. You, as an investor in the notes, should make your own investigation into the Reference Index and the Index Sponsor.

The Additional Amount and Redemption Amount will not be adjusted for changes in exchange rates that might affect the Reference Index.

Although the stocks composing the Reference Index are traded in currencies other than U.S. dollars, and the notes, which are linked in part to the Reference Index are denominated in U.S. dollars, the Additional Amount and Redemption Amount payable at maturity will not be adjusted for changes in the exchange rate between the U.S. dollar and each of the currencies in which the stocks composing the Reference Index are denominated. Changes in exchange rates, however, may reflect changes in various non-U.S. economies that in turn may affect the Additional Amount (and related Redemption Amount). The Additional Amount (if any) and Redemption Amount Lehman Brothers Holdings Inc. will pay in respect of the notes on the maturity date will be determined solely in accordance with the terms described above under “Redemption Amount.”

Lehman Brothers Holdings Inc. cannot control actions by the companies whose stocks or other equity securities are represented in the Reference Index.

Lehman Brothers Holdings Inc. is not affiliated with any of the other companies whose stock is represented in the Reference Index. As a result, Lehman Brothers Holdings Inc. will have no ability to control the actions of such companies, including actions that could affect the value of the stocks underlying the Reference Index or your notes. None of the Index Sponsor or any of the companies represented in the Reference Index will be involved in the offering of notes in any way. Neither those companies nor the Reference Index will have any obligation to consider your interests as a holder of the notes in taking any corporate actions that might affect the value of your notes.

You will have no shareholder rights in issuers of stocks underlying the Reference Index.

Investing in the notes is not equivalent to investing in the securities underlying the Reference Index. As a holder of the notes, you will not have voting rights or rights to receive dividends or other distributions or other rights that holders of the securities comprising the Reference Index would have.

Certain of Lehman Brothers Inc.’s, or its affiliates’, activities may adversely affect the value of your notes.

Lehman Brothers Inc. and/or certain of its affiliates trade the stocks underlying the Reference Index, and other financial instruments related to the Reference Index and its component stocks on a regular basis, for their accounts and for other accounts under their management and such trading could affect the value of the notes. Lehman Brothers Inc. and these affiliates may also issue or underwrite or assist unaffiliated entities in the issuance or underwriting of other securities or financial instruments linked to the Reference Index. To the extent that Lehman Brothers Inc. or one of its affiliates serves as issuer, agent or underwriter for such securities or financial instruments, Lehman Brothers Inc.’s or their interests with respect to such products may be adverse to those of the holders of the notes. Any of these trading activities could potentially affect the level of the Reference Index and, accordingly, could affect the value of the notes and the amount, if any, payable to you at maturity.

Lehman Brothers Inc. and/or certain of its affiliates may currently or from time to time engage in business with companies whose stocks are included in the Reference Index, including extending loans to, or making equity investments in, or providing advisory services to them, including merger and acquisition advisory services. In the course of this business, Lehman Brothers Inc. and/or certain of its affiliates may acquire non-public information about the companies, and Lehman Brothers Inc. or such affiliates will not disclose any such information to you.

In addition, Lehman Brothers Inc. and/or certain of its affiliates may serve as issuer, agent or underwriter for additional issuances of notes with returns linked or related to changes in the level of the Reference Index or the stocks that compose the Reference Index. By introducing competing products into the marketplace in this manner, Lehman Brothers Inc. and/or certain of its affiliates could adversely affect the value of the notes.

10

An investment in the notes is subject to risks associated with non-U.S. securities markets.

The stocks that constitute the Reference Index have been issued by non-U.S. companies. Investments in securities indexed to the value of such non-U.S. equity securities involve risks associated with the securities markets in China and Hong Kong, including risks of volatility in the Chinese and Hong Kong markets, governmental intervention in that market and cross shareholdings in companies in China and Hong Kong. Also, there is generally less publicly available information about companies in China and Hong Kong than about U.S. companies that are subject to the reporting requirements of the Securities and Exchange Commission, and generally non-U.S. companies are subject to accounting, auditing and financial reporting standards and requirements and securities trading rules different from those applicable to U.S. reporting companies.

The prices of securities in China and Hong Kong may be affected by political, economic, financial and social factors in China and Hong Kong, including changes in government, economic and fiscal policies, currency exchange laws or other laws or restrictions. Moreover, the economies in China and Hong Kong may differ favorably or unfavorably from the economy of the United States in such respects as growth of gross national product, rate of inflation, capital reinvestment, resources and self sufficiency. Each of China and Hong Kong may be subjected to different and, in some cases, more adverse economic environments.

Your return on the notes, if any, generally will not reflect dividends on the common stocks or other equity securities of the companies in the Reference Index.

Your return on the notes, if any, will not reflect the return you would realize if you actually owned the stocks of the companies included in the Reference Index and received the dividends paid on those stocks. Rather, the Calculation Agent will calculate the Additional Amount (and related Redemption Amount) payable to you at maturity of the notes by reference, in part, to the Final Index Level, which reflects the prices of the stocks as calculated in the Reference Index without taking into consideration the value of dividends paid on those stocks.

Time differences between Hong Kong and New York City may create discrepancies in trading levels.

As a result of the time difference between Hong Kong, where the securities underlying the Reference Index trade, and New York City (where the notes may trade), there may be discrepancies between the level of the Reference Index and the trading prices of the notes. In addition, there may be periods when the foreign securities markets are closed for trading (for example during holidays in Hong Kong), as a result of which the level of the Reference Index remain unchanged for multiple trading days in New York City.

Risks Related to the Reference Commodities

An investment in the notes is subject to risks associated with the performance of the Reference Commodities

The Additional Amount payable on the notes is dependent on the Basket Return, which in turn depends in part on the performance of the Reference Commodities. The prices of the Reference Commodities are primarily affected by the global demand for and supply of such Reference Commodities (including certain specific factors discussed below), but from time to time may also be significantly affected by speculative actions or currency exchange rates. Demand for the Reference Commodities is significantly linked to the level of global economic activity, but is also influenced by other factors such as government regulations (including environmental or consumption policies) and growth in industrial production and gross domestic policy in emerging market countries, such as China, that have become oversized users of commodities. In addition to general economic activity and demand, prices for a Reference Commodity can be influenced by political events and trade policies, as well as labor activity and supply disruptions in regions of the world that are major producers of the relevant Reference Commodity, all of which will tend to affect worldwide prices of a Reference Commodity, regardless of the location of the event. It is impossible to predict what effect these factors will have on the value of any of the Reference Commodities and thus, the return on the notes.

In the event of sudden disruptions in the supplies of a Reference Commodity, such as those caused by war, natural events, or accidents, prices of a Reference Commodity and futures contracts on a Reference Commodity could become extremely volatile and unpredictable. Also, sudden and dramatic changes in the futures market may occur, for example, upon the introduction of new or previously withheld supplies of the Reference Commodities into the market or the introduction of substitute products or commodities.

In addition, the Reference Commodities are also subject to certain specific risks.

Specific factors affecting the price of Crude Oil. The price of crude oil is primarily affected by the global demand for and supply of crude oil. Demand for refined petroleum products by consumers, as well as the agricultural, manufacturing and transportation industries, affects the price of crude oil. Crude oil’s end-use as a refined product is often as transport fuel, industrial fuel and in-home heating fuel. Potential for substitution in most areas exists, although considerations including relative cost often limit substitution levels. Because the precursors of demand for petroleum products are linked to economic activity, demand will tend to reflect economic conditions. Demand is also influenced by government regulations, such as environmental or consumption policies. In addition to general economic activity and demand, prices for crude oil are affected by political events, labor activity and, in particular, direct government intervention (such as embargos) or supply disruptions in major oil producing regions of the world. Such events tend to affect oil prices worldwide, regardless of the location of the event. Supply for crude oil may increase or decrease depending on many factors. These include production decisions by the Organization of Oil and Petroleum Exporting Countries and other crude oil producers. In the event of sudden disruptions in the supplies of oil, such as those caused by war, natural events,

11

accidents or acts of terrorism, prices of oil futures contracts could become extremely volatile and unpredictable. Also, sudden and dramatic changes in the futures market may occur, for example, upon a cessation of hostilities that may exist in countries producing oil, the introduction of new or previously withheld supplies into the market or the introduction of substitute products or commodities. A decrease in the price of any of these commodities may have a material adverse effect on the price of crude oil and the return on an investment in the notes.

Specific factors affecting the price of Copper. The price of copper is primarily affected by the global demand for and supply of copper. Copper is a conductor of electricity, and one of the most significant applications for copper is the production of cable, wire and electrical products for both the electrical and building industries. Construction is another principal industrial application for copper, which is used in pipes for plumbing, heating, ventilation, and air conditioning, along with masonry wiring and sheet metal facing. Demand for copper products in recent years has been supported by strong consumption from newly industrializing countries due to their copper-intensive economic growth and infrastructure development. Apart from the United States, Canada and Australia, the majority of copper concentrate supply (the raw material) comes from outside the Organization for Economic Cooperation and Development countries. In previous years, copper supply has been affected by strikes, financial problems and terrorist activity.

The notes are not regulated by the CFTC or any other commodities regulatory authority.

The notes are debt securities that are direct obligations of Lehman Brothers Holdings Inc. The net proceeds to be received by Lehman Brothers Holdings Inc. from the sale of the notes will not be used to purchase or sell the Reference Commodities, or futures contracts on the Reference Commodities on the Relevant Commodity Exchanges, for the benefit of holders of the notes. The notes are not themselves futures contracts, and an investment in the notes does not constitute either an investment in the Reference Commodities or futures contracts on Reference Commodities or in a collective investment vehicle that trades in the Reference Commodities or futures contracts on the Reference Commodities.

Unlike an investment in the notes, an investment in a collective investment vehicle that invests in commodities on behalf of its participants may be regulated as a commodity pool and its operator may be required to be registered with and regulated by the Commodity Futures Trading Commission (“CFTC”) as a “commodity pool operator” (“CPO”). Because the notes are not interests in a commodity pool, the notes will not be regulated by the CFTC as a commodity pool, Lehman Brothers Holdings Inc. will not be registered with the CFTC as a CPO, and you will not benefit from the CFTC’s or any non-U.S. regulatory authority’s regulatory protections afforded to persons who trade in commodities or who invest in regulated commodity pools.

The notes do not constitute investments by you in futures contracts traded on regulated futures exchanges. Accordingly, you will not benefit from the CFTC’s or any other regulatory authority’s regulatory protections afforded to persons who trade in futures contracts on a regulated futures exchange.

There are specific risks you should consider relating to the trading of Copper on the London Metal Exchange.

The price of Copper will be determined by reference to the official cash delivery settlement price of the copper contract traded on the London Metal Exchange (the “LME”). The LME is a principals’ market which operates in a manner more closely analogous to the over-the-counter physical commodity markets than regulated futures markets, and certain features of regulated futures markets are not present in the context of LME trading. For example, there are no daily price limits on the LME, which would otherwise restrict the extent of daily fluctuations in the prices of LME contracts. In a declining market, therefore, it is possible that prices would continue to decline without limitation within a trading day or over a period of trading days. In addition, a contract may be entered into on the LME calling for delivery on any day from one day to three months following the date of such contract, weekly from three months to six months, and monthly thereafter up to 63, 27 and 15 months forward depending on the commodity (63 months forward for Copper), in contrast to trading on futures exchanges, which call for delivery in stated delivery months. As a result, there may be a greater risk of a concentration of positions in LME contracts on particular delivery dates, which in turn could cause temporary aberrations in the prices of LME contracts for certain delivery dates. If such aberrations are occurring on the Valuation Date, the Final Copper Price and, therefore, the Basket Return and Redemption Amount, could be adversely affected.

Risks Related to the Reference Currency

As discussed above, please see “Risk Factors—Risks Relating to Currency-Indexed Notes” in the Series I MTN prospectus supplement for particular risks relating to an investment related to the Reference Currency.

UNITED STATES FEDERAL INCOME TAX TREATMENT

Lehman Brothers Holdings Inc. intends to treat the notes as contingent payment debt instruments, as described under “Supplemental United States Federal Income Tax Consequences—Contingent Payment Debt Instruments” in the Series I MTN prospectus supplement.

12

THE HANG SENG® INDEX

Lehman Brothers Holdings Inc. has derived all information regarding the Reference Index, including, without limitation, its make-up, method of calculation and changes in its components, from publicly available information. Such information reflects the policies of, and is subject to change by, Hang Seng Indexes Company Limited. The Reference Index is offered and maintained by Hang Seng Indexes Company Limited. Lehman Brothers Holdings Inc. has not independently verified such information. Lehman Brothers Holdings Inc. makes no representation or warranty as to the accuracy or completeness of such information.

Additional information concerning the Reference Index, including the country and industrial sector weightings of the securities included in the Reference Index, may be obtained at the Hang Seng Indexes Company Limited web site (www.hsi.com.hk). Information contained in the Hang Seng Indexes Company Limited website is not incorporated by reference in, and should not be considered a part of, this terms sheet or any related pricing supplement.

You can obtain the level of the Reference Index at any time from the Bloomberg Financial Markets page “HSI <Index> <GO>“ or from the Hang Seng Indexes Company Limited website at www.hsi.com.hk.

Hang Seng® Index Composition and Maintenance

The Reference Index is compiled, published and managed by Hang Seng Indexes Company Limited, a wholly owned subsidiary of the Hang Seng® Bank, and was first calculated and published on November 24, 1969. The Reference Index is a market capitalization weighted stock market index of the Stock Exchange of Hong Kong (the “SEHK”). As of February 25, 2008 it consisted of 43 stocks listed on the SEHK that are grouped under Finance, Utilities, Properties and Commerce and Industry sub-indices.

Only companies with a primary listing on the main board of the SEHK are eligible as constituents of the Reference Index. Mainland China enterprises that have an H-share listing in Hong Kong are eligible for inclusion in the Reference Index when any one of the following conditions is met:

(1) |

| the H-share company has 100% of its ordinary share capital in the form of H-shares which are listed on the SEHK; |

|

|

|

(2) |

| the H-share company has completed the process of share reform, with the result that there is no unlisted share capital in the country; or |

|

|

|

(3) |

| for new H-share initial public offerings, the company has no unlisted share capital. |

To be eligible for selection in the Reference Index, a company:

(1) |

| must be among those that constitute the top 90% of the total market value of all primary shares listed on the SEHK (market value is expressed as an average of the past 12 months); |

|

|

|

(2) |

| must be among those that constitute the top 90% of the total turnover of all primary listed shares on the SEHK (turnover is aggregated and individually assessed for eight quarterly sub-periods for the past 24 months); and |

|

|

|

(3) |

| should normally have a listing history of 24 months, or meet the requirements set out in the following guidelines: |

For a newly listed large-cap stock, in order to be eligible for selection in the Index, the minimum listing time is required:

Average Market Level Rank at the Time of Review |

| Minimum Listing History |

|

Top 5 |

| 3 Months |

|

6-15 |

| 6 Months |

|

16-20 |

| 12 Months |

|

21-25 |

| 18 Months |

|

Below 25 |

| 24 Months |

|

From the eligible candidates, final selections are based on the following:

(1) the market value and turnover rankings of the companies;

(2) the representation of the sub-sectors within the Reference Index directly reflecting that of the market; and

(3) the financial performance of the companies.

Hang Seng® Index Calculation

As of February 2008, the Reference Index uses a freefloat-adjusted market capitalization weighting calculation methodology. Under this calculation methodology, the following shareholdings are viewed as strategic in nature and excluded for calculation: (1) shares held by strategic shareholders who individually or collectively control more than 30% of the shareholdings; (2) shares held by directors who individually control more than 5% of the shareholdings; (3) shares held by a Hong Kong-listed company which controls more than 5% of the shareholdings as investments; and (4) shares held by shareholders who individually or collectively represent more than 5% of the shareholdings in the company and with a publicly disclosed lock-up arrangement.

13

A Freefloat – Adjusted Factor, representing the proportion of shares that are free floated as a percentage of the issued shares, is rounded up to the nearest multiple of 5% for the calculation of the Reference Index and is updated half-yearly.

A Cap Factor of 15% on individual stock weightings is applied. A re-capping is conducted semi-annually to coincide with the regular update of the Freefloat - Adjusted Factor. Additional re-capping is performed upon constituent changes.

Discontinuation of the Hang Seng® Index; Alteration of Method of Calculation

Hang Seng Indexes Company Limited has no obligation to continue to publish the Reference Index, and may discontinue publication of the Reference Index at any time in its sole discretion. If Hang Seng Indexes Company Limited discontinues publication of the Reference Index and Hang Seng Indexes Company Limited or another entity publishes a successor or substitute index that the calculation agent determines, in its sole discretion, to be comparable to the discontinued Reference Index (such index being referred to herein as a “Hang Seng® Successor Index”), then any Index closing level will be determined by reference to the level of such Hang Seng® Successor Index at the close of trading on the relevant exchange or market for the Hang Seng® Successor Index on each relevant Valuation Date or other relevant date or dates as set forth in the relevant terms supplement.

Upon any selection by the calculation agent of a Hang Seng® Successor Index, the calculation agent will cause written notice thereof to be promptly furnished to the trustee, to us and to the holders of the notes.

If Hang Seng Indexes Company Limited discontinues publication of the Reference Index prior to, and such discontinuance is continuing on, a Valuation Date or other relevant date or dates as set forth in the relevant terms supplement and the calculation agent determines, in its sole discretion, that no Hang Seng® Successor Index is available at such time, or the calculation agent has previously selected a Hang Seng® Successor Index and publication of such Hang Seng® Successor Index is discontinued prior to, and such discontinuation is continuing on, such Valuation Date or other relevant date, or if Hang Seng Indexes Company Limited (or the publisher of any Hang Seng® Successor Index) fails to calculate and publish a closing level for the Reference Index (or any Hang Seng® Successor Index) on any date when it would ordinarily do so in accordance with its customary practice, then the calculation agent will determine the Index closing level for such date. The Index closing level will be computed by the calculation agent in accordance with the formula for and method of calculating the Reference Index or Hang Seng® Successor Index, as applicable, last in effect prior to such discontinuation or failure to calculate or publish a closing level for the index, using the closing price (or, if trading in the relevant securities has been materially suspended or materially limited, its good faith estimate of the closing price that would have prevailed but for such suspension or limitation) at the close of the principal trading session on such date of each security most recently comprising the Reference Index or Hang Seng® Successor Index, as applicable. Notwithstanding these alternative arrangements, discontinuation of the publication or failure to calculate or publish the closing level of the Reference Index may adversely affect the value of the notes.

As used herein, “closing price” of a security, on any particular day, means the last reported sales price for that security on the relevant exchange at the scheduled weekday closing time of the regular trading session of the relevant exchange. If, however, the security is not listed or traded on a bulletin board, then the closing price of the security will be determined using the average execution price per share that an affiliate of Lehman Brothers Holdings Inc. pays or receives upon the purchase or sale of the security used to hedge Lehman Brothers Holdings Inc.’s obligations under the notes. The “relevant exchange” for any security (or any combination thereof then underlying the Reference Index or any Hang Seng® Successor Index) means the primary exchange, quotation system (which includes bulletin board services) or other market of trading for such security.

If at any time the method of calculating the Reference Index or a Hang Seng® Successor Index, or the level thereof, is changed in a material respect, or if the Reference Index or a Hang Seng® Successor Index is in any other way modified so that the Reference Index or such Hang Seng® Successor Index does not, in the opinion of the calculation agent, fairly represent the level of the Reference Index or such Hang Seng® Successor Index had such changes or modifications not been made, then the calculation agent will, at the close of business in New York City on each date on which the Reference Index closing level is to be determined, make such calculations and adjustments as, in the good faith judgment of the calculation agent, may be necessary in order to arrive at a level of a stock index comparable to the Reference Index or such Hang Seng® Successor Index, as the case may be, as if such changes or modifications had not been made, and the calculation agent will calculate the Index closing level with reference to the Reference Index or such Hang Seng® Successor Index, as adjusted. Accordingly, if the method of calculating the Reference Index or a Hang Seng® Successor Index is modified so that the level of the Reference Index or such Hang Seng® Successor Index is a fraction of what it would have been if there had been no such modification (e.g., due to a split in the Reference Index), then the calculation agent will adjust its calculation of the Reference Index or such Hang Seng® Successor Index in order to arrive at a level of the Reference Index or such Hang Seng® Successor Index as if there had been no such modification (e.g., as if such split had not occurred).

License Agreement with Hang Seng Indexes Company Limited

Lehman Brothers Holdings Inc. will enter into a non-exclusive license agreement with Hang Seng Indexes Company Limited and Hang Seng Data Services Limited providing for the license to Lehman Brothers Holdings Inc., in exchange for a fee, of the right to use certain indices calculated by Hang Seng Indexes Company Limited in connection with the issuance and marketing of securities, including the Notes.

The Hang Seng® Index is published and compiled by Hang Seng Indexes Company Limited pursuant to a license from Hang Seng Data Services Limited. The mark(s) and name(s) of the Hang Seng® Index are proprietary to Hang Seng Data Services Limited. Hang Seng Indexes Company Limited and Hang Seng Data Services Limited have agreed to the use of, and reference

14

to, the Hang Seng® Index by Lehman Brothers Holdings Inc. in connection with the Securities, BUT NEITHER HSI SERVICES LIMITED NOR HANG SENG DATA SERVICES LIMITED WARRANTS OR REPRESENTS OR GUARANTEES TO ANY BROKER OR HOLDER OF THE SECURITIES OR ANY OTHER PERSON (i) THE ACCURACY OR COMPLETENESS OF ANY OF THE HANG SENG® INDEX AND ITS COMPUTATION OR ANY INFORMATION RELATED THERETO; OR (ii) THE FITNESS OR SUITABILITY FOR ANY PURPOSE OF ANY OF THE HANG SENG® INDEX OR ANY COMPONENT OR DATA COMPRISED IN IT; OR (iii) THE RESULTS WHICH MAY BE OBTAINED BY ANY PERSON FROM THE USE OF ANY OF THE HANG SENG® INDEX OR ANY COMPONENT OR DATA COMPRISED IN IT FOR ANY PURPOSE, AND NO WARRANTY OR REPRESENTATION OR GUARANTEE OF ANY KIND WHATSOEVER RELATING TO ANY OF THE HANG SENG® INDEX IS GIVEN OR MAY BE IMPLIED. The process and basis of computation and compilation of any of the Hang Seng® Index and any of the related formula or formulae, constituent stocks and factors may at any time be changed or altered by Hang Seng Indexes Company Limited without notice. TO THE EXTENT PERMITTED BY APPLICABLE LAW, NO RESPONSIBILITY OR LIABILITY IS ACCEPTED BY HSI SERVICES LIMITED OR HANG SENG DATA SERVICES LIMITED (i) IN RESPECT OF THE USE OF AND/OR REFERENCE TO ANY OF THE HANG SENG® INDEX BY LEHMAN BROTHERS HOLDINGS INC. IN CONNECTION WITH THE SECURITIES; OR (ii) FOR ANY INACCURACIES, OMISSIONS, MISTAKES OR ERRORS OF HSI SERVICES LIMITED IN THE COMPUTATION OF ANY OF THE HANG SENG® INDEX; OR (iii) FOR ANY INACCURACIES, OMISSIONS, MISTAKES, ERRORS OR INCOMPLETENESS OF ANY INFORMATION USED IN CONNECTION WITH THE COMPUTATION OF ANY OF THE HANG SENG® INDEX WHICH IS SUPPLIED BY ANY OTHER PERSON; OR (iv) FOR ANY ECONOMIC OR OTHER LOSS WHICH MAY BE DIRECTLY OR INDIRECTLY SUSTAINED BY ANY BROKER OR HOLDER OF THE SECURITIES OR ANY OTHER PERSON DEALING WITH THE SECURITIES AS A RESULT OF ANY OF THE AFORESAID, AND NO CLAIMS, ACTIONS OR LEGAL PROCEEDINGS MAY BE BROUGHT AGAINST HSI SERVICES LIMITED AND/OR HANG SENG DATA SERVICES LIMITED in connection with the Securities in any manner whatsoever by any broker, holder or other person dealing with the Securities. Any broker, holder or other person dealing with the Securities does so therefore in full knowledge of this disclaimer and can place no reliance whatsoever on Hang Seng Indexes Company Limited and Hang Seng Data Services Limited. For the avoidance of doubt, this disclaimer does not create any contractual or quasi-contractual relationship between any broker, holder or other person and Hang Seng Indexes Company Limited and/or Hang Seng Data Services Limited and must not be construed to have created such relationship.

15

INFORMATION ON COPPER, CRUDE OIL AND THE RELEVANT COMMODITY EXCHANGES

Lehman Brothers Holdings Inc. has derived all information regarding the commodities futures markets, the LME and the NYMEX from publicly available sources. Information concerning the LME and Copper trading on the LME reflects the policies of, and is subject to change without notice by, the LME. Information concerning the NYMEX and Crude Oil trading on the NYMEX reflects the policies of, and is subject to change without notice by, the NYMEX. Neither Lehman Brothers Holdings Inc. nor Lehman Brothers Inc. makes any representation or warranty as to the accuracy or completeness of such information.

The Copper Price is published on Bloomberg page “LOCADY” and on Reuters page MTLE.

The Crude Oil Price is published on Bloomberg page “CL1” and on Reuters page 0#2CL.

The Commodity Futures Markets

An exchange-traded futures contract is a bi-lateral contract that provides for the future purchase and sale of a specified type and quantity of a commodity for a fixed price. The contract provides for a specified settlement month in which the commodity is to be delivered by the seller. Rather than settlement by physical delivery of the commodity, futures contracts may be settled for the cash value of the right to receive or sell the specified commodity on the specified date.

Futures contracts are traded on organized exchanges, known as “contract markets”, through the facilities of a centralized clearing house and a brokerage firm which is a member of the clearing house. The clearing house guarantees the performance of each clearing member which is a party to a futures contract by, in effect, taking the opposite side of the transaction. U.S. futures markets, as well as brokers and market participants, are subject to regulation by the CFTC. Futures markets outside the United States are generally subject to regulation by comparable regulatory authorities (such as the Financial Services Authority (FSA) in the United Kingdom). Because the notes do not constitute futures contracts or commodity options, noteholders will not benefit from the aforementioned clearing house guarantees or the regulatory protections of the CFTC, the FSA or any other non-U.S. regulatory authority.

Information on Copper Trading on the LME

According to publicly available information, the LME was established in 1877 and is the principal metal exchange in the world on which contracts for delivery of copper — as well as nickel, zinc, lead, tin, aluminum and aluminum alloy — are traded. In contrast to U.S. futures exchanges, the LME operates as a principals’ market for the trading of forward contracts, and is therefore more closely analogous to over-the-counter physical commodity markets than futures markets. As a result, members of the LME trade with each other as principals and not as agents for customers, although such members may enter into offsetting “back-to-back” contracts with their customers. Further, the LME does not require client orders to be exposed to the market via LME Select, inter-office dealing or the floor of the exchange trading, and LME members may, at their option (unless they have specific client instructions to the contrary) cross the order against their own book or that of another customer, rather than expose it to the market. As a result price discovery will take place against LME members’ net exposures during the relevant LME second ring (as discussed below).

In addition, while futures exchanges permit trading to be conducted in contracts for monthly delivery in stated delivery months, LME contracts are be established for delivery on any day (referred to as a “prompt date”) from one day to three months following the date of contract, weekly from three months to six months, and monthly thereafter up to 63, 27 and 15 months forward (depending on the commodity). Further, there are no price limits applicable to LME contracts, and prices could decline without limitation over a period of time. Trading is conducted on the basis of warrants that cover physical material held in listed warehouses.

The trading on the LME is transacted through open-outcry sessions on the LME floor, electronically on LME Select (the LME’s official electronic trading platform) and through inter-office dealing, which allows the LME to operate as a 24-hour market. Trading on the floor takes place in two sessions daily, from 11:45 am to 1:05 pm and from 2:55 to 4:15 pm, London time. The two sessions are each broken down into two rings made up of five minutes’ trading in each contract. After the second ring of the first session the official prices for the day are announced. Contracts may be settled by offset or delivery and can be cleared in U.S. dollars, pounds sterling, Japanese yen and euros.

The LME is not a cash-cleared market. Both inter-office and floor trading are cleared and guaranteed by a system run by the London Clearing House, whose role is to act as a central counterparty to trades executed between clearing members and thereby reduce risk and settlement costs. The LME is subject to regulation by the FSA.

The Copper Price is the official settlement price of copper for cash delivery, expressed as the U.S. dollar price per metric ton of copper, as made public by the LME.

Copper has traded on the LME since its establishment. The Copper contract traded on the LME was upgraded to High Grade Copper in November 1981 and again to the current Copper – Grade A contract in June 1986. Copper trades on the LME in units of 25 metric tons and the settlement price of Copper for cash delivery is the price for the contract, expressed as U.S. dollars per metric ton, scheduled for same-day settlement. Copper contracts on the LME may be established for delivery daily from one day (cash delivery) to three months, weekly on each Wednesday from three months to six months, and monthly on every third Wednesday from seven months to 63 months.

16

Information on Crude Oil Trading on the NYMEX

According to publicly available information, the NYMEX was established in 1872 as the Butter and Cheese Exchange of New York, and has since traded a variety of commodity products. It is now the largest exchange in the world for the trading of energy futures and options contracts, including contracts for Crude Oil, RBOB Gasoline, Heating Oil and Natural Gas. It is also a leading North American exchange for the trading of platinum group metals and other precious metals contracts. The NYMEX conducts trading in its futures contracts through an open-outcry trading floor during the trading day and after hours through an internet-based electronic platform. The establishment of energy futures on the NYMEX occurred in 1979, with the introduction of heating oil futures contracts. The NYMEX opened trading in leaded gasoline futures in 1981, followed by the crude oil futures contract in 1983 and unleaded gasoline futures in 1984.

The Crude Oil Price is the U.S. dollar cash buyer settlement price per barrel of the “first nearby month” contract traded on NYMEX. The “first nearby month” contract is, at any given time, the contract next scheduled for settlement. For example, in February 2008, prior to the termination of trading in a given commodity contract, the first nearby month futures contract for a given commodity will be the March 2008 futures contract, which is the contract for delivery of the commodity in March 2008. After the contract terminates trading in that month, the first nearby contract will be the April 2008 futures contract, which is the contract for delivery of the commodity in April 2008. See below for the dates in any given month in which trading terminates in the Crude Oil contract.

The Crude Oil contract trades on NYMEX in units of 1,000 barrels and the delivery point is Cushing, Oklahoma. The Crude Oil Contract provides for delivery of several grades of domestic and internationally traded foreign crude oils. It may be settled by delivery of West Texas Intermediate, Low Sweet Mix, New Mexican Sweet, North Texas Sweet, Oklahoma Sweet or South Texas Sweet. Trading in the Crude Oil contract terminates at the close of business on the third business day prior to the 25th calendar day of the month preceding the delivery month (or if the 25th calendar day of the month is a non-business day, on the third business day prior to the business day preceding the 25th calendar day).

17

HISTORICAL INFORMATION