Free-Writing Prospectus

Filed pursuant to Rule 433

Registration Statement No. 333-134553

| Contacts | ||

Neuberger Berman Clients: For immediate assistance or questions on any of the product offerings, please contact your Neuberger Berman Internal Sales Associate at 877-628-2583, option 2.

Also, please feel free to call 212-526-1330 or emailstructuredinvestments@lehman.com with any questions relating to these calendar offerings or any other structured investment.

If you would like to direct a question to a specific asset group or if you wish to consider a customized offering, please feel free to contact our asset class teams at the following numbers:

| Commodities: | 212-528-1009 | |

| Equities: | 212-526-0905 | |

| FX: | 212-526-5641 | |

| Rates: | 212-528-6428 |

| 1 | |||

| Introduction | ||

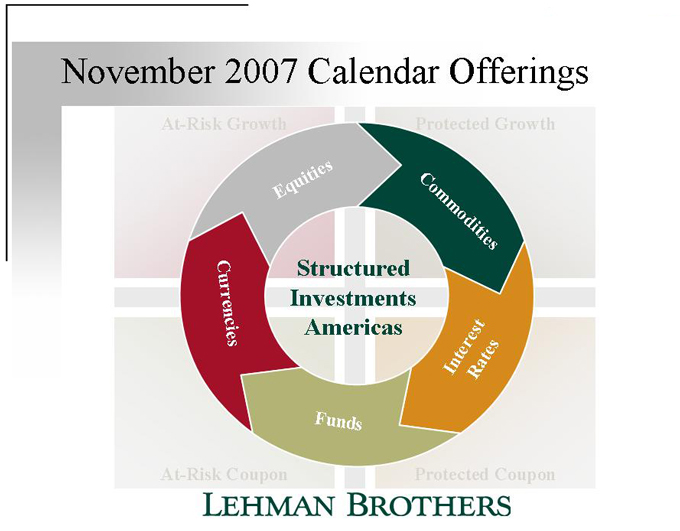

Structured Investments Offerings Calendar

| ¨ | Lehman Brothers has developed a systematic framework for presenting new product offerings |

| ¨ | Structured investments can accommodate any of the following investment profiles: |

| – | At-risk growth |

| – | Protected growth |

| – | At-risk coupon |

| – | Protected coupon |

| ¨ | Each calendar features multiple asset classes across |

| a wide range of structured investment offerings |

| ¨ | The calendar is released monthly |

| I. | Summary of Offerings | page 6 | ||

| II. | Commodity | page 7 | ||

| III. | Equity | page 8 | ||

| IV. | FX | page 9 | ||

| V. | Rates | page 10 | ||

| 2 | |||

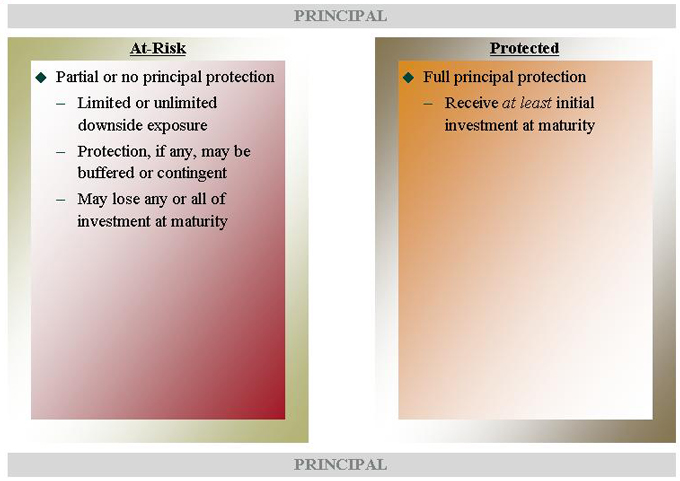

Principal Risk Profiles

| ||

Investors can choose between full, partial or no protection of their principal investment, at maturity

| 3 | |||

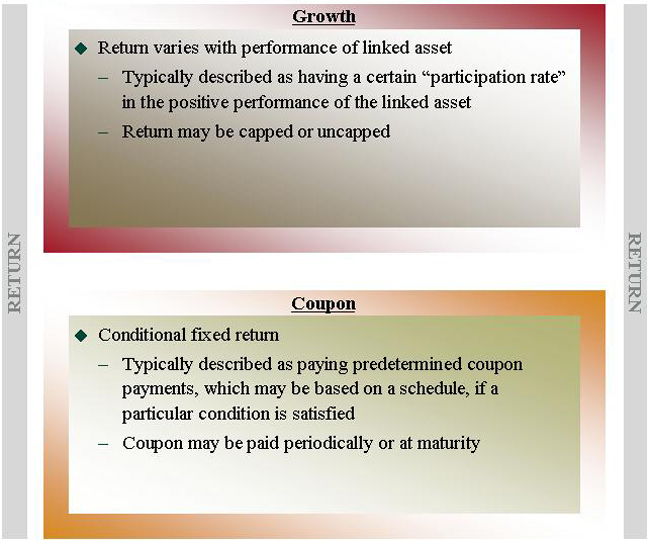

| Return Profiles | ||

Investors can also choose a return profile which is either growth or coupon driven, or a combination thereof

| 4 | |||

| Structured Investments Cross-Asset Offerings | ||

November 2007 Offerings

| 5 | |||

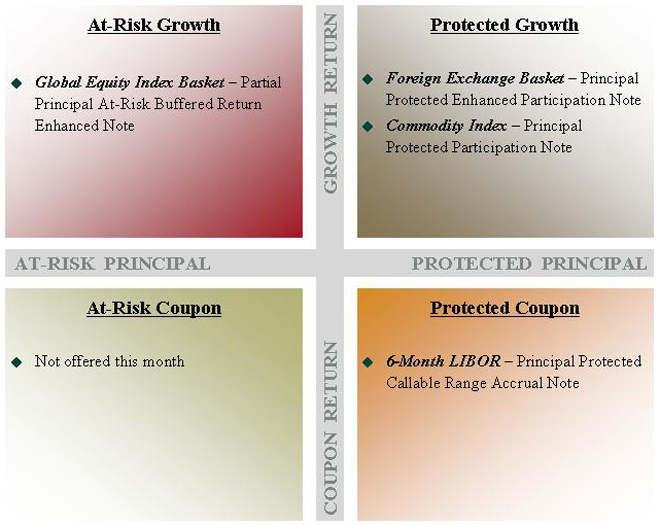

| Summary of November Offerings | ||

|  |  |  |  | ||||||||||||||||

| ¨ |

Lehman Brothers Commodity Index Excess Return (LBCIER) | ¨ |

Basket of equity indices: – Dow Jones EURO STOXX 50® Index (SX5E) – Nikkei 225SM Index (NKY) – S&P 500® Index (SPX) | ¨ |

Basket of BRIC currencies: – Brazilian Real (BRL) – Russian Ruble (RUB) – Indian Rupee (INR) – Chinese Renminbi (CNY) | ¨ |

6-Month LIBOR, observed daily | ||||||||

| ¨ |

Low to negative correlation to stocks and bonds | ¨ |

Diversification using global equities |

¨ |

Medium term bullish view of BRIC currency markets with diversified exposure and enhanced risk/returns |

¨ |

View that 6-month LIBOR will stay below 6.0% | ||||||||

¨ |

Commodities can be positively correlated to inflation and may act as an inflation hedge |

¨ |

Enhanced exposure with uncapped appreciation potential |

¨ |

Positive correlation between 6-Month LIBOR and the Fed Funds rate | |||||||||||

| ¨

| 3 years

| ¨

| 4 years

| ¨

| 2 years

| ¨

| 10 years

| ||||||||

|

¨ |

Not callable |

¨ |

Not callable |

¨ |

Not callable |

¨ |

Callable semi-annually after May 30, 2008 | ||||||||

|

¨ |

100% participation in index return up to a maximum return of [50% – 60%] |

¨ |

Leveraged participation of [115% – 125%] of equity basket return |

¨ |

Leveraged participation of [280%] in upside of FX basket return |

¨ |

Accrues [8% – 9%] p.a. coupon, payable semi-annually, for every day that 6-month LIBOR remains between 0.0% and 6.0% | ||||||||

|

¨ |

Full principal protection if held to maturity

|

¨ |

20% downside buffer; 80% loss potential |

¨ |

Full principal protection if held to maturity

|

¨ | Full principal protection if held to maturity

| ||||||||

|

¨

| 52517P4D0

|

¨

|

52517P7E5

|

¨

|

52517P3G4

|

¨

|

5252M0AA5

| ||||||||

|

¨ |

|

¨ |

|

¨ |

|

¨ |

|

| 6 | The terms described above are a summary only and are not complete. This description should be read in conjunction with, and for complete details purchasers should rely only on, the termsheet for the offering and the other documents referenced herein. The termsheet for the offering is available through the link above. |

| Protected Growth Offering –Commodity |  | |||

An investor who seeks a return linked to the performance of the Lehman Brothers Commodity Index in a principal protected format, up to a cap of [50% – 60%].

| Summary Offering Terms | ||

Issuer |

Lehman Brothers Holdings Inc. (A1, A+, AA-)† | |||||

Linked Asset |

LBCI Excess Return (LBCIER) | |||||

Term |

3 years | |||||

Maturity Date |

November 30, 2010 | |||||

Upside Participation Rate |

100% | |||||

Principal Protection |

100%, if held to maturity | |||||

Return Cap |

[50% – 60%], will be set on pricing date | |||||

CUSIP |

52517P4D0 |

| Hypothetical Examples – Payments at Maturity |

| 1) | Index increases but percentage appreciation is less than Return Cap

| |||||||

| – | Return Calculation:$1,000 +($1,000 x Index Return)

| |||||||

| – | Hypothetical Example: Index appreciates 15%, the investor receives a payment at maturity of $1,150 per $1,000 invested, calculated as follows:

| |||||||

$1,000 + ($1,000 x 15%)

| ||||||||

| 2) | Index declines by any amount

| |||||||

| – | Return at maturity is original principal only

| |||||||

| – | Hypothetical Example: Index declines by 25% (or by any amount), the investor receives a payment at maturity of $1,000 per $1,000 invested

| |||||||

| 3) | Index increases and percentage appreciation is greater than Return Cap

| |||||||

| – | Return Calculation:$1,000 + ($1,000 x Return Cap)

| |||||||

| – | Hypothetical Example: Assume the Return Cap is 55% and the index appreciates 80%. Since the index appreciation is greater than the 55% Return Cap, the investor return is capped at 55% and receives a payment at maturity of $1,550 per $1,000 invested, calculated as follows:

| |||||||

| $1,000 + ($1,000 x 55%) | ||||||||

| Investment Rationale | ||

| ¨ | Selected Benefits

| |||||||

| – | Full principal protection – The notes have 100% principal protection, if held to maturity.

| |||||||

| – | Allocation benefits – Investing in the note provides easy access and broad exposure to commodities.

| |||||||

| – | Low correlation to other asset classes - Commodities show low to negative correlation to stocks and bonds, therefore an investor can potentially diversify an investment portfolio by adding commodity exposure.

| |||||||

| – | Potential inflation hedge – Commodities tend to be positively correlated to inflation and therefore may act as an inflation hedge.

| |||||||

| ¨ | Selected Risks

| |||||||

| – | Return is capped – Investor will have 100% participation in the appreciation of the index up to a [50% – 60%] cap. As a result, investors will not participate in any increase greater than the Return Cap.

| |||||||

| – | Commodity price and volatility risk – Commodity prices change unpredictably and can be highly volatile.

| |||||||

The termsheet for this offering is available through the following link:

http://www.sec.gov/Archives/edgar/data/806085/000110465907078231/a07-25006_81fwp.htm

|

| † | Lehman Brothers Holdings Inc. is rated A+ by Standard & Poor’s, Al by Moody’s and AA- by Fitch. A credit rating reflects the creditworthiness of Lehman Brothers Holdings Inc. and is not a recommendation to buy, sell or hold securities, and it may be subject to revision or withdrawal at any time by the assigning rating organization. Each rating should be evaluated independently of any other rating. The creditworthiness of the issuer does not affect or enhance the likely performance of the investment other than the ability of the issuer to meet its obligations. |

| 7 | In reaching a determination as to the appropriateness of any proposed transaction, clients should undertake a thorough independent review of the legal, regulatory, credit, tax, accounting and economic consequences of such transaction in relation to their particular circumstances. |

| At-Risk Growth Offering –Equity |  | |||

An investor who seeks an uncapped return and enhanced participation between [115% and 125%] in the appreciation of a diversified global equities basket with partial principal protection.

| Summary Offering Terms | ||

Issuer |

Lehman Brothers Holdings Inc. (A1, A+, AA-)† | |||||

Linked Assets |

Equally weighted global stock basket: Dow Jones EURO STOXX Index, Nikkei 225 Index and S&P 500 | |||||

Term |

4 years | |||||

Maturity Date |

November 30, 2011 | |||||

Upside Participation Rate |

[115% – 125%], will be set on pricing date | |||||

Buffer Protection |

20% | |||||

Return Cap |

None | |||||

CUSIP |

52517P7E5 |

| Hypothetical Examples – Payments at Maturity |

| 1) | Linked equity basket increases by any amount

| |||||||

| – | Return Calculation:$1,000 + ($1,000 x Basket Return x Participation Rate)

| |||||||

| – | Hypothetical Example: Assume participation rate, which will be set on pricing date is 120%. If the basket appreciates 15%, the investor receives a payment at maturity of $1,180 per $1,000 invested, calculated as follows:

| |||||||

$1,000 + ($1,000 x 15% x 120%)

| ||||||||

| 2) | Linked equity basket declines but not by more than 20% buffer level

| |||||||

| – | Return at maturity is original principal

| |||||||

| – | Hypothetical Example: Index declines by 15%, the investor receives a payment at maturity of $1,000 per $1,000 invested

| |||||||

| 3) | Linked equity basket declines greater than buffer level

| |||||||

| – | Return Calculation:$1,000 + [$1,000 x (Basket Return + Buffer Level)]

| |||||||

| – | Hypothetical Example: Basket declines by 25%, the investor receives a payment at maturity of $950 per $1,000 invested, calculated as follows:

| |||||||

| $1,000 + [$1,000 x (-25% +20%)] | ||||||||

| Investment Rationale | ||

| ¨ | Selected Benefits

| |||||||

| – | Diversification – The investment provides global diversification in equities, linked to a basket consisting of the Dow Jones EURO STOXX 50® Index, the Nikkei 225SM Index and the S&P 500 Index®.

| |||||||

| – | Enhanced equity returns – The return of the underlying basket will be enhanced by the participation rate, which will be between 115% and 125% times the basket appreciation.

| |||||||

| – | Uncapped appreciation potential – The notes are not subject to a predetermined appreciation cap and upside potential is not limited.

| |||||||

| – | Partial principal protection – If the underlying basket declines at maturity, but not by more than the 20% buffer amount, investor will receive full return of principal.

| |||||||

| ¨ | Selected Risks

| |||||||

| – | Substantial loss potential – Investment does not have full principal protection and investors will participate in the decline of the basket on a 1-for-1 basis beyond the 20% buffer amount.

| |||||||

The termsheet for this offering is available through the following link:

http://sec.gov/Archives/edgar/data/806085/000119312507232617/dfwp.htm

|

| † | Lehman Brothers Holdings Inc. is rated A+ by Standard & Poor’s, Al by Moody’s and AA- by Fitch. A credit rating reflects the creditworthiness of Lehman Brothers Holdings Inc. and is not a recommendation to buy, sell or hold securities, and it may be subject to revision or withdrawal at any time by the assigning rating organization. Each rating should be evaluated independently of any other rating. The creditworthiness of the issuer does not affect or enhance the likely performance of the investment other than the ability of the issuer to meet its obligations. |

| 8 | In reaching a determination as to the appropriateness of any proposed transaction, clients should undertake a thorough independent review of the legal, regulatory, credit, tax, accounting and economic consequences of such transaction in relation to their particular circumstances. |

| Protected Growth Offering –FX |  | |||

An investor who seeks an uncapped return of [280%] the appreciation of a diversified basket of BRIC market currencies in a principal protected format.

| Summary Offering Terms | ||

Issuer |

Lehman Brothers Holdings Inc. (A1, A+, AA-)† | |||||

Linked Assets |

Equally weighted BRIC emerging market currency basket: Brazilian Real, Russian Ruble, Indian Rupee and Chinese Renminbi | |||||

Term |

2 years | |||||

Maturity Date |

November 30, 2009 | |||||

Upside Participation Rate |

[280%], will be set on pricing date | |||||

Principal Protection |

100%, if held to maturity | |||||

Return Cap |

None | |||||

CUSIP |

52517P3G4 |

| Hypothetical Examples – Payments at Maturity |

| 1) | Value of linked currency basket increases by any amount

| |||||||

| – | Return Calculation: $1,000 + ($1,000 x Basket Return x Participation Rate)

| |||||||

| – | Hypothetical Example: Assume participation rate, which will be set on pricing date, is 280%. If the basket value appreciates 15%, the investor receives a payment at maturity of $1,420 per $1,000 invested, calculated as follows:

| |||||||

$1,000 + ($1,000 x 15% x 280%) | ||||||||

| 2) | Value of linked currency basket declines by any amount

| |||||||

| – | Return at maturity is original principal only

| |||||||

| – | Hypothetical Example: Basket value declines by 25%, the investor receives a payment at maturity of $1,000 per $1,000 invested | |||||||

| Investment Rationale | ||

| ¨ | Selected Benefits

| |||||||

| – | Foreign currency portfolio allocation – The basket provides exposure to leading emerging economies of Brazil, Russia, India and China.

| |||||||

| – | Enhance participation rate – The note will have a participation rate of [280%] times the basket appreciation.

| |||||||

| – | Uncapped appreciation potential – The notes are not subject to a predetermined appreciation cap and upside potential is not limited.

| |||||||

| – | Diversification – The investment provides a level of global currency diversification that can shield an investor against continued US dollar depreciation. | |||||||

| – | Full principal protection – The notes have 100% principal protection, if held to maturity.

| |||||||

| ¨ | Selected Risks

| |||||||

| – | Currency risk – The value of a reference currency relative to the US dollar will be influenced by complex factors, including: global and regional events, political landscapes, economic and financial growth and stability. These factors can affect the currency markets on which a reference currency is traded.

| |||||||

| – | Interest rate risk – US monetary policy could affect US dollar performance against this basket of foreign currencies. Alternatively, actions on monetary policy on behalf of Central Banks in Brazil, Russia, India and China could also affect the performance of their respective currencies versus the US dollar.

| |||||||

The termsheet for this offering is available through the following link:

http://www.sec.gov/Archives/edgar/data/806085/000110465907078387/a07-25006_82fwp.htm

|

| † | Lehman Brothers Holdings Inc. is rated A+ by Standard & Poor’s, Al by Moody’s and AA- by Fitch. A credit rating reflects the creditworthiness of Lehman Brothers Holdings Inc. and is not a recommendation to buy, sell or hold securities, and it may be subject to revision or withdrawal at any time by the assigning rating organization. Each rating should be evaluated independently of any other rating. The creditworthiness of the issuer does not affect or enhance the likely performance of the investment other than the ability of the issuer to meet its obligations. |

| 9 | In reaching a determination as to the appropriateness of any proposed transaction, clients should undertake a thorough independent review of the legal, regulatory, credit, tax, accounting and economic consequences of such transaction in relation to their particular circumstances. |

| Protected Coupon Offering –Rates |  | |||

An investor who has a view that 6-Month LIBOR will remain below 6% over the next ten years can receive a coupon up to [8 – 9%] per annum and principal protection at maturity.

| Summary Offering Terms | ||

Issuer |

Lehman Brothers Holdings Inc. (A1, A+, AA-)† | |||||

Linked Asset |

6-Month LIBOR, observed daily | |||||

Term |

10 years | |||||

Maturity Date |

November 30, 2017 | |||||

Principal Protection |

100%, if held to maturity | |||||

Coupon |

[8% – 9%] p.a.; coupon accrues for every day that 6-Month LIBOR remains within specified range | |||||

Specified Range for 6-Month LIBOR |

Greater than 0.00% and less than or equal to 6.00% | |||||

Coupon payment |

Semi-annual | |||||

Callable |

Semi-annually after May 30, 2008 | |||||

CUSIP |

5252M0AA5 |

| Hypothetical Examples – Payments at Maturity |

| 1) | 6-Month LIBOR is within range on one or more observation dates

| |||||||

| – | Semi-annual Coupon Calculation: ($1,000 x (n/N) x Annual Coupon Rate) • n is the number of days that 6-Month LIBOR was within range • N is the total number of days in the observation period

| |||||||

| – | Hypothetical Example: 6-Month LIBOR is below 6% for 160 days during the 6-month period. Assume an 8.5% annual coupon, investor receives a semi-annual coupon of $37.78 per $1,000 invested, calculated as follows: ($1,000 x 160/360 (days) x 8.5%), using 30/360 day count.

| |||||||

| 2) | 6-Month LIBOR is above 6.00% on all the observation dates

| |||||||

| – | Semi-annual coupon payment is 0.00% or $0.00.

| |||||||

| 3) | Note is called | |||||||

| – | Return on called note is original principal only (plus accrued interest, if any). | |||||||

| Investment Rationale | ||

| ¨ | Selected Benefits

| |||||||

| – | Attractive return potential – The note could potentially pay a higher coupon than a vanilla fixed-rate bond with similar credit, maturity and call features.

| |||||||

| – | Coupon payments – This note allows investors to earn a coupon of up to [8% – 9%] p.a., paid semi-annually for a 10 year period, if note is not called.

| |||||||

| – | Investment positioning – 6-Month LIBOR could respond to changes in economic fundamentals and to policy actions by the Federal Reserve Board. Investing in this note allows the investor to express the view that the 6-Month LIBOR will remain below 6% over the next 10 years.

| |||||||

| – | Positive correlation – Historically(1) the Fed Funds Rate and 6-Month LIBOR have been positively correlated. | |||||||

| – | Full principal protection – The notes have 100% principal protection, if held to maturity.

| |||||||

| ¨ | Selected Risks

| |||||||

| – | Interest rate risk – Adverse interest rate fluctuations can cause the coupon to become unpredictable. If 6-Month LIBOR exceeds 6% on one or more observation dates during any semi-annual interest period, the coupon payable for that interest period will be less than the maximum coupon of [8% – 9%] p.a.

| |||||||

| – | Call risk – The notes are callable at par after the first 6 months. If the notes are called, the investor may have to reinvest at less favorable rates.

| |||||||

The termsheet for this offering is available through the following link:

http://www.sec.gov/Archives/edgar/data/806085/000110465907077458/a07-25006_72fwp.htm

|

| _______________________ |

| 1. | Represents data for last 15 years. Historical results are not indicative of future performance, and there is no guarantee that any historical correlation will continue to be observable in the future. |

| † | Lehman Brothers Holdings Inc. is rated A+ by Standard & Poor’s, A1 by Moody’s and AA- by Fitch. A credit rating reflects the creditworthiness of Lehman Brothers Holdings Inc. and is not a recommendation to buy, sell or hold securities, and it may be subject to revision or withdrawal at any time by the assigning rating organization. Each rating should be evaluated independently of any other rating. The creditworthiness of the issuer does not affect or enhance the likely performance of the investment other than the ability of the issuer to meet its obligations. |

| . |

| 10 | In reaching a determination as to the appropriateness of any proposed transaction, clients should undertake a thorough independent review of the legal, regulatory, credit, tax, accounting and economic consequences of such transaction in relation to their particular circumstances. |

| Select Other Risk Factors | ||

An investment in any of the securities mentioned herein involves significant risks. Some of those risks are summarized here, but we urge you to read the more detailed explanation of risks relating to the specific securities in the relevant offering materials. We also urge you to consult your investment, legal, tax, accounting and other advisers before you consider investing in any such securities.

No Interest or Dividend Payments or Voting Rights: As a holder of the equity-linked notes, you will not receive interest payments, and you will not have voting rights or rights to receive cash dividends or other distributions or other rights that holders of stocks included in the indices would have.

Lack of Liquidity: The notes will not be listed on any securities exchange. Lehman Brothers Inc. intends to make a secondary market in the notes but is not required to do so. Even if there is a secondary market, it may not provide enough liquidity to allow you to trade or sell the notes easily. Because other dealers are not likely to make a secondary market for the notes, the price at which you may be able to trade your notes is likely to depend on the price, if any, at which Lehman Brothers Inc. is willing to buy the notes. If you are an employee of Lehman Brothers Holdings Inc. or one of our affiliates, you may not be able to purchase the notes from us and your ability to sell or trade the notes in the secondary market may be limited.

Market Risk: The notes are designed to be held to maturity and are not designed to be short-term trading instruments. The price at which you will be able to sell your notes prior to maturity may be at a substantial discount from the principal amount of the notes, even in cases where the linked asset has appreciated since the date of the issuance of the notes. The potential returns described in the respective pricing supplements or free writing prospectuses, as applicable, assume that the notes are held to maturity.

Uncertain Tax Treatment: Significant aspects of the tax treatment of the notes are uncertain. You should consult your own tax advisor about your own tax situation before investing in the notes.

Many Economic and Market Factors Will Impact the Value of the Notes: In addition to the level or value of the linked asset on any day, the value of the notes will be affected by a number of economic and market factors that may either offset or magnify each other and which are set out in more detail in the respective pricing supplements or free writing prospectuses, as applicable. | Credit of Issuer: An investment in the notes will be subject to the credit risk of Lehman Brothers Holdings Inc., and the actual and perceived creditworthiness of Lehman Brothers Holdings Inc. may affect the market value of the notes.

Potential Conflicts: We and our affiliates play a variety of roles in connection with the issuance of the notes, including acting as calculation agent and hedging our obligations under the notes. In performing these duties, the economic interests of the calculation agent and other affiliates of ours are potentially adverse to your interests as an investor in the notes.

Certain Built-in Costs are Likely to Adversely Affect the Value of the Notes Prior to Maturity: While the payments described in the term sheet are based on the full principal amount of your notes, the original issue price of the notes includes the agent’s commission and the cost of hedging our obligations under the notes through one or more of our affiliates, which includes our affiliates’ expected cost of providing such hedge as well as the profit our affiliates expect to realize in consideration for assuming the risks inherent in providing such hedge. As a result, the price, if any, at which Lehman Brothers Inc. will be willing to purchase notes from you in secondary market transactions, if at all, will likely be lower than the original issue price and any sale prior to the maturity date could result in a substantial loss to you.

We and our Affiliates and Agents May Publish Research, Express Opinions or Provide Recommendations that are Inconsistent with Investing in or Holding the Respective Notes. Any Such Research, Opinions or Recommendations Could Affect the Levels or Prices of the Linked Asset or the Value of the Respective Notes: We, our affiliates and agents publish research from time to time on financial markets and other matters that may influence the value of the respective notes, or express opinions or provide recommendations that are inconsistent with purchasing or holding the respective notes. We, our affiliates and agents may have published research or other opinions that are inconsistent with the investment view implicit in the respective notes. Any research, opinions or recommendations expressed by us, our affiliates or agents may not be consistent with each other and may be modified from time to time without notice. Investors should make their own independent investigation of the merits of investing in the respective notes which are linked to the asset. |

| 11 | In reaching a determination as to the appropriateness of any proposed transaction, clients should undertake a thorough independent review of the legal, regulatory, credit, tax, accounting and economic consequences of such transaction in relation to their particular circumstances. | ||

| Disclosure | ||

Lehman Brothers Holdings Inc. has filed a registration statement (including a prospectus) with the U.S. Securities and Exchange Commission (SEC) for this offering. Before you invest, you should read the prospectus dated May 30, 2006, the prospectus supplement dated May 30, 2006 for its Medium Term Notes, Series I, and other documents Lehman Brothers Holdings Inc. has filed with the SEC for more complete information about Lehman Brothers Holdings Inc. and this offering. Buyers should rely upon the prospectus, prospectus supplement and any relevant free writing prospectus for complete details. You may get these documents and other documents Lehman Brothers Holdings Inc. has filed for free by searching the SEC online database (EDGAR®) atwww.sec.gov with “Lehman Brothers Holdings Inc.” as a search term. You may also access the prospectus and Series I MTN prospectus supplement on the SEC web site as follows:

• Series I MTN prospectus supplement dated May 30, 2006:

http://www.sec.gov/Archives/edgar/data/806085/000104746906007785/a2170815z424b2.htm

• Prospectus dated May 30, 2006:

http://www.sec.gov/Archives/edgar/data/806085/000104746906007771/a2165526zs-3asr.htm

Alternatively, Lehman Brothers Inc. will arrange to send you the prospectus, Series I MTN prospectus supplement and final pricing supplement (when completed) if you request it by calling your Lehman Brothers sales representative or 1-888-603-5847. |

| 12 | |||