Term sheet no. 1 to

Prospectus dated May 30, 2006

Prospectus supplement dated May 30, 2006

Product supplement no. 890-I dated December 7, 2007

Underlying supplement no. 1080 dated December 7, 2007

Registration Statement no. 333-134553

Dated December 7, 2007

Rule 433

| Preliminary Terms and Conditions, December 7, 2007 | Telephone: +1 212 526 0905 |

15.80% Reverse Exchangeable Notes Linked to the Least Performing Index Fund in a

Basket of Index Funds

Lehman Brothers Holdings Inc. has filed a registration statement (including a base prospectus) with the U.S. Securities and Exchange Commission, or SEC, for this offering. Before you invest, you should read the base prospectus dated May 30, 2006, the MTN prospectus supplement dated May 30, 2006, product supplement no. 890-I dated December 7, 2007, underlying supplement no. 1080 dated December 7, 2007 and other documents that Lehman Brothers Holdings Inc. has filed with the SEC for more complete information about Lehman Brothers Holdings Inc. and this offering. Buyers should rely upon the base prospectus, MTN prospectus supplement, product supplement no. 890-I, underlying supplement no. 1080, this term sheet and any other relevant terms supplement and any relevant free writing prospectus for complete details. You may get these documents and other documents Lehman Brothers Holdings Inc. has filed for free by searching the SEC online database (EDGAR®) at www.sec.gov, with “Lehman Brothers Holdings Inc.” as a search term. Alternatively, Lehman Brothers Inc., or any other dealer participating in the offering will arrange to send you the base prospectus, the MTN prospectus supplement, product supplement no. 890-I, underlying supplement no. 1080, this term sheet and any other relevant terms supplement and the final pricing supplement (when completed) if you request it by calling your Lehman Brothers sales representative, such other dealer or 1-888-603-5847.

Summary Description

The notes are designed for investors who seek a higher coupon rate than the current yield on the Index Funds or the yield that we believe would be payable on a conventional debt security with the same maturity issued by us or an issuer with a comparable credit rating. Investors should be willing to forgo the potential to participate in appreciation in the Index Funds, be willing to accept the risks of owning interests in exchange traded funds in general and the Least Performing Index Fund in particular, and be willing to lose some or all of their principal.

The notes do not guarantee any return of principal at maturity. Instead, the Payment at Maturity will be based on the Final Share Price of the Least Performing Index Fund if the closing price of any Index Fund is below such Index Fund’s Trigger Price during the Monitoring Period, as described below. You may lose some or all of your investment.

Issuer: | Lehman Brothers Holdings Inc. (A+/A1/AA-)† | |

Issue Size: | $[TBD] | |

Pricing Date: | December 21, 2007‡ | |

Settlement Date: | December 31, 2007‡ | |

Observation Date: | March 24, 2008ࠠ | |

Maturity Date: | March 31, 2008ࠠ | |

Term: | 3 months | |

Basket: | The basket (the “Basket”) will be composed of the iShares® MSCI Brazil Index Fund (NYSE: EWZ) and the iShares® FTSE/Xinhua China 25 Index Fund (NYSE: FXI) (each, an “Index Fund”). Either Index Fund issuer may be changed in certain circumstances. See “Description of Notes—[Alternative Calculation of Price and Closing Price]” in the accompanying product supplement no. 890-I for further information. | |

Underlying Indices: | With respect to the iShares® MSCI Brazil Index Fund, the MSCI Brazil IndexSMand with respect to the iShares® FTSE/Xinhua China 25 Index Fund, the FTSE/Xinhua China 25 IndexTM. | |

Coupon Rate: | 15.80% per annum, paid monthly and calculated on a 30/360 basis. | |

Coupon Payment Date: | Monthly, on the last day of each month, starting on January 31, 2007, to, and including, the Maturity Date. If any Coupon Payment Date falls on a day that is not a business day, then any payment required to be made on such Coupon Payment Date will instead be made on the first preceding day that is a business day;provided, however, that the final coupon payment will be made with the Payment at Maturity. | |

Payment at Maturity: | The payment at maturity, in addition to accrued and unpaid coupon payments, is based on the performance of each of the Index Funds individually. You will receive $1,000 for each $1,000 principal amount note plus any accrued and unpaid coupon payments at maturity,unless: | |

(i) the Final Share Price of any Index Fund is less than its Initial Share Price;and | ||

(ii) a Trigger Event has occurred. | ||

| If the conditions described in (i) and (ii) are both satisfied, at maturity you will receive, instead of the principal amount of your notes, a cash payment per $1,000 principal amount note equal to the Cash Value, |

| plus any accrued and unpaid coupon payments.The Cash Value will be less than the principal amount of your notes and may be zero. Accordingly, you may lose some or all of your principal if you invest in the notes. | ||

Cash Value: | The amount in cash equal to the product of (1) $1,000 divided by the Initial Share Price of the Least Performing Index Fund and (2) the Final Share Price of the Least Performing Index Fund. | |

Trigger Event: | A Trigger Event occurs if, on any trading day during the Monitoring Period, the closing price of a share of any Index Fund is below such Index Fund’s Trigger Price. | |

Monitoring Period: | The period from, but excluding, the Pricing Date to, and including, the Observation Date. | |

Initial Share Price: | For each Index Fund, the closing price of one share of such Index Fund on the Pricing Date, divided by the Share Adjustment Factor. See “The Index Funds—Initial Share Prices and Trigger Prices.” | |

Trigger Price: | For each Index Fund, a dollar amount that represents 60% of the applicable Initial Share Price of such Index Fund in effect on such trading day. See “The Index Funds—Initial Share Prices and Trigger Prices.” | |

| Least Performing Index Fund: | The Index Fund with the lower value of the two Index Funds included in the Basket, with value calculated as the product of (i) $1,000 divided by the Initial Share Price for such Index Fund times (ii) the Final Share Price for such Index Fund. | |

Final Share Price: | For each Index Fund, the closing price of one share of such Index Fund on the Observation Date. | |

Share Adjustment Factor: | For each Index Fund, 1.0 on the Pricing Date, subject to adjustment under certain circumstances. See “Description of Notes—Anti-dilution Adjustments” in the accompanying product supplement no. 890-I for further information about these adjustments. | |

CUSIP: | 5249083T5 | |

ISIN: | US5249083T52 |

| ‡ | Expected. In the event that we make any change to the expected Pricing Date and Settlement Date, the Observation Date and Maturity Date will be changed so that the stated term of the notes remains the same. |

| † | Lehman Brothers Holdings Inc. is rated A+ by Standard & Poor’s, A1 by Moody’s and AA- by Fitch. A credit rating reflects the creditworthiness of Lehman Brothers Holdings Inc. and is not a recommendation to buy, sell or hold securities, and it may be subject to revision or withdrawal at any time by the assigning rating organization. Each rating should be evaluated independently of any other rating. The creditworthiness of the issuer does not affect or enhance the likely performance of the investment other than the ability of the issuer to meet its obligations. |

| †† | Subject to postponement in the event of a market disruption event, as described under “Description of Notes—Payment at Maturity” in the accompanying product supplement no. 890-I. |

Investing in the Reverse Exchangeable Notes Linked to the Least Performing Index Fund in a Basket of Index Funds involves a number of risks. See “Risk Factors” beginning on page SS-1 of the accompanying product supplement no. 890- I, “Risk Factors” beginning on page US-1 of the accompanying underlying supplement no. 1080 and “Selected Risk Factors” beginning on page TS-2 of this term sheet.

You may revoke your offer to purchase the notes at any time prior to the time at which we accept such offer by notifying the applicable agent. We reserve the right to change the terms of, or reject any offer to purchase the notes prior to their issuance. In the event of any changes to the terms of the notes, we will notify you and you will be asked to accept such changes in connection with your purchase. You may also choose to reject such changes, in which case we may reject your offer to purchase.

Neither the SEC nor any state securities commission has approved or disapproved of the notes or passed upon the accuracy or the adequacy of this term sheet, the accompanying base prospectus, MTN prospectus supplement, product supplement no. 890-I, underlying supplement no. 1080, or any other relevant terms supplement. Any representation to the contrary is a criminal offense.

| Price to Public (1) | Fees (2) | Proceeds to Us | ||||

Per note | $1,000.00 | $18.00 | $982.00 | |||

Total | $ | $ | $ |

(1) | The price to the public includes the cost of hedging our obligations under the notes through one or more of our affiliates, which includes our affiliates’ expected cost of providing such hedge as well as the profit our affiliates expect to realize in consideration for assuming the risks inherent in providing such hedge. |

(2) | If the notes priced today Lehman Brothers Inc. would receive a fee of approximately 1.80% of the principal amount of the notes. Lehman Brothers Inc. would use those fees to allow selling concessions to one or more brokers and/or dealers. The actual fees received by Lehman Brothers Inc. per $1,000 principal amount may be more or less than the fees listed above and will depend on market conditions on the Pricing Date. In no event will the fees received by Lehman Brothers Inc. per $1,000 principal amount, which include the concessions to be paid to one or more brokers and/or dealers, exceed 5.00% of the principal amount of the notes. Lehman Brothers Inc. and/or an affiliate may earn additional income as a result of payments pursuant to the hedges. |

LEHMAN BROTHERS

December 7, 2007

ADDITIONAL TERMS SPECIFIC TO THE NOTES

Lehman Brothers Holdings Inc. has filed a registration statement (including a base prospectus) with the U.S. Securities and Exchange Commission, or SEC, for this offering. Before you invest, you should read this term sheet together with the base prospectus, as supplemented by the MTN prospectus supplement relating to our Series I medium-term notes of which these notes are a part, and the more detailed information contained in product supplement no. 890-I (which supplements the description of the general terms of the notes) and underlying supplement no. 1080 (which describes each of the Index Funds, as defined herein, including risk factors specific to each). Buyers should rely upon the base prospectus, the MTN prospectus supplement, product supplement no. 890-I, underlying supplement no. 1080, this term sheet and any other relevant terms supplement for complete details. This term sheet, together with the documents listed below, contains the terms of the notes and supersedes all prior or contemporaneous communications concerning the notes. To the extent that there are any inconsistencies among the documents listed below, this term sheet shall supersede product supplement no. 890-I, which shall, likewise, supersede the base prospectus and the MTN prospectus supplement. You should carefully consider, among other things, the matters set forth in “Risk Factors” in the accompanying product supplement no. 890-I and “Risk Factors” in the accompanying underlying supplement no. 1080, as the notes involve risks not associated with conventional debt securities. We urge you to consult your investment, legal, tax, accounting and other advisors before you invest in the notes. You may get these documents and other documents Lehman Brothers Holdings Inc. has filed for free by searching the SEC online database (EDGAR®) atwww.sec.gov, with “Lehman Brothers Holdings Inc.” as a search term or through the links below, or by calling Lehman Brothers Inc. toll-free at 1-888-603-5847.

You may access these documents on the SEC website atwww.sec.govas follows (or if such address has changed, by reviewing our filings for the relevant date on the SEC website):

| • | Product supplement no. 890-I dated December 7, 2007: |

http://www.sec.gov/Archives/edgar/data/806085/000119312507261375/d424b2.htm

| • | Underlying supplement no. 1080 dated December 7, 2007: |

http://www.sec.gov/Archives/edgar/data/806085/000119312507261478/d424b2.htm

| • | MTN prospectus supplement May 30, 2006: |

http://www.sec.gov/Archives/edgar/data/806085/000104746906007785/a2170815z424b2.htm

| • | Base prospectus dated May 30, 2006: |

http://www.sec.gov/Archives/edgar/data/806085/000104746906007771/a2165526zs-3asr.htm

As used in this term sheet, the “Company,” “we,” “us,” or “our” refers to Lehman Brothers Holdings Inc.

Selected Purchase Considerations

| • | The Notes Offer a Higher Coupon Rate Than the Current Yield on the Index Funds or the Yield We Believe Would be Payable on Conventional Debt Securities With the Same Maturity Issued by Us or an Issuer with a Comparable Credit Rating: The notes will pay coupon payments at 15.80% per year, which is higher than the current yield on the Index Funds or the yield that we believe would be payable on conventional debt securities of the same maturity issued by us or an issuer with a comparable credit rating. Because the notes are our senior unsecured obligations, any coupon payment or any other payment at maturity is subject to our ability to pay our obligations as they become due. |

• | Index Funds: The return on the notes is linked to the performance of the Index Funds. Each Index Fund seeks investment results that correspond generally to the price and yield performance, before fees and expenses, of the related Underlying Index. The FTSE/Xinhua China 25 IndexTM measures a free-float-adjusted total market Hong Kong dollar value of all its constituent equity securities that is designed to represent the performance of the mainland Chinese market and that is available to the international investors. The MSCI Brazil IndexSM is a free-float-adjusted and capitalization-weighted index designed to measure equity market performance in Brazil by aiming to capture 85% of the publicly available total market capitalization in Brazil. For additional information about the Index Funds and the Underlying Indices, see “The iShares® MSCI Brazil Index Fund,” the “FTSE/Xinhua China 25 IndexTM,” “The iShares® FTSE/Xinhua China 25 Index Fund” and the “MSCI Brazil IndexSM” in the accompanying underlying supplement no. 1080. |

| • | Your Return at Maturity May Be Based on an Index Fund Whose Share Price During the Term of the Notes Has Never Been Below Such Index Fund’s Trigger Price: Your return at maturity may not necessarily be based on an Index Fund whose share price is, if at all, below its Trigger Price during the Monitoring Period. For example, if a Trigger Event occurs with respect to an Index Fund that experiences a significant closing price increase on the Observation Date such that its Final Share Price exceeds its Initial Share Price, your return on the notes will not be based on the performance of that Index Fund. Under these circumstances, if on the Observation Date the Final Share Price of the other Index Fund is below its respective Initial Share Price, your return on the notes will be based on the performance of that Index Fund and not on the performance of the Index Fund with respect to which a Trigger Event has occurred. Accordingly, you could lose a portion of your principal amount even if the Least Performing Index Fund was at no time during the Monitoring Period below its Trigger Price. |

| • | Certain U.S. Federal Income Tax Consequences: There is no statutory, judicial or administrative authority that directly addresses the proper U.S. federal income tax characterization and treatment of securities similar to the notes. No ruling is being sought from the Internal Revenue Service as to the proper U.S. federal income tax characterization and treatment of the notes. You should also be aware that our special tax counsel, Sidley Austin LLP, has not provided us with an opinion regarding the proper characterization of the notes for U.S. federal income tax purposes. Therefore, the proper U.S. federal income tax characterization and treatment of the notes is uncertain. Notwithstanding the foregoing, Lehman Brothers Holdings Inc. intends to treat, and by purchasing a note, for all tax purposes, you agree to treat, a note as a cash-settled financial contract, rather than as a debt instrument. See “Certain U.S. Federal Income Tax Consequences” in the accompanying product supplement no. 890-I. |

TS-1

An investment in the notes involves significant risks. Investing in the notes is not equivalent to investing directly in one or both of the Index Funds, any of the equity securities held by the Index Funds or any of the equity securities included in the Underlying Indices. These risks are explained in more detail in the “Risk Factors” section of the accompanying product supplement no. 890-I and in the “Risk Factors” section of the accompanying underlying supplement no. 1080. You should reach an investment decision only after you have carefully considered with your advisors the suitability of an investment in the notes in light of your particular circumstances.

| • | Your Investment in the Notes May Result in a Significant Loss: The notes do not guarantee any return of principal. The Payment at Maturity will be based on the Final Share Price of the Least Performing Index Fund if the closing price of a share of any Index Fund is below such Index Fund’s Trigger Price on any trading day during the Monitoring Period. Under certain circumstances, you will receive at maturity the Cash Value instead of the principal amount of your notes. The Cash Value will be less than the principal amount of each note and may be zero. In addition, on the Pricing Date, stock prices generally in the market and share prices for the Index Funds may be significantly higher than historical averages, which could increase the likelihood of subsequent declines in stock prices and of a Trigger Event with respect to either or both Index Funds. Accordingly, you could lose some or all of the principal amount of your notes. |

| • | The Notes Will Not Pay More Than the Principal Amount at Maturity, Plus Accrued and Unpaid Coupons, and Principal Protection is Under Limited Circumstances: Your return of principal at maturity is protected so long as a Trigger Event does not occur or if the Final Share Price of each Index Fund is not below its respective Initial Share Price. However, if the Final Share Price of any Index Fund is below the applicable Initial Share Price and a Trigger Event has occurred, you could lose the entire principal amount of your notes. |

| • | You Are Exposed to the Closing Price Risk of Each Index Fund: Your return on the notes and your payment at maturity, if any, is not linked to a basket consisting of the Index Funds. Rather, you will receive set coupon payments at a rate of 15.80% per annum and your payment at maturity is contingent upon the performance of each individual Index Fund such that you will be equally exposed to the risks related toboth of the Index Funds. Poor performance by either of the Index Funds over the term of the notes may negatively affect your payment at maturity and will not be offset or mitigated by positive performance by the other Index Fund. The performance of the individual Index Funds, and your payment at maturity, should not be expected to match the performance of the two Index Funds as a basket. |

| • | Your Return on the Notes is Limited to the Principal Amount Plus Accrued Coupon Payments, Regardless of Any Appreciation in the Value of Any Index Fund: Unless (i) the Final Share Price of any Index Fund is less than its Initial Share Price and (ii) on any trading day during the Monitoring Period, the closing price of a share of any Index Fund is below such Index Fund’s Trigger Price, for each $1,000 principal amount note, you will receive $1,000 at maturity plus accrued and unpaid coupon payments, regardless of any appreciation in the value of any Index Fund, which may be significant. Accordingly, the return on the notes may be significantly less than the return on a direct investment in the shares of one or more of the Index Funds, the equity securities held by the Index Funds, the common stocks included in the Underlying Indices or contracts relating to the Underlying Indices for which there is an active secondary market during the term of the notes. |

| • | Your Payment at Maturity May Be Determined By the Least Performing Index Fund: If a Trigger Event occurs, you will lose some or all of your investment in the notes if the Final Share Price of either Index Fund is below its Initial Share Price. This will be true even if (i) the Final Share Price of the other Index Fund is above its Initial Share Price and/or (ii) the sole Index Fund with a Final Share Price that is below its Initial Share Price was not the same Index Fund that was below its Trigger Price during the Monitoring Period. |

| • | No Ownership Rights in the Index Funds: As a holder of the notes, you will not have any ownership interest or rights in the Index Funds or in the equity securities held by the Index Funds or in the stocks included in the Underlying Indices, such as voting rights, dividend payments or other distributions. |

| • | Differences Between the Index Funds and their Respective Underlying Indices:The Index Funds do not fully replicate their respective Underlying Indices, may hold securities not included in such Underlying Indices and will reflect transaction costs and fees that are not included in the calculation of such Underlying Indices, all of which may lead to a lack of correlation between the Index Funds and their respective Underlying Indices. In addition, because the shares of the Index Funds are traded on the New York Stock Exchange and are subject to market supply and investor demand, the market price per share of the Index Funds may differ from the net asset value per share of the Index Funds. |

| • | We Cannot Control Actions by the Companies Whose Stocks or Other Equity Securities are Represented in the Underlying Indices: We are not affiliated with any of the companies whose stocks are represented in the Underlying Indices. As a result, we will have no ability to control the actions of such companies, including actions that could affect the value of the stocks underlying the Underlying Indices or your notes. None of the money you pay us will go to any of the companies represented in the Underlying Indices, and none of those companies will be involved in the offering of the notes in any way. Neither those companies nor we will have any obligation to consider your interests as a holder of the notes in taking any corporate actions that might affect the value of your notes. |

| • | The Index Funds are Subject to Management Risk: The Index Funds are subject to the risk that the investment strategy of Barclays Global Fund Advisors, which we refer to as BGFA, which is the investment adviser to both of the Index Funds, may not produce the intended results. Pursuant to its investment strategy or otherwise, BGFA may add, delete or substitute the equity securities held by the Index Funds. Any of these actions could adversely affect the price of the shares of the Index Funds and consequently the value of the notes. |

| • | Our Affiliates’ Compensation May Serve as an Incentive to Sell You These Notes: We and our affiliates act in various capacities with respect to the notes. Lehman Brothers Inc. and other of our affiliates may act as a principal, agent or dealer in connection with the notes. Such affiliates, including the sales representatives, may derive compensation from the distribution of the notes and such compensation may serve as an incentive to sell these notes instead of other investments. |

TS-2

| • | Certain Built-in Costs Are Likely to Adversely Affect the Value of the Notes Prior to Maturity: While the Payment at Maturity described in this term sheet is based on the full principal amount of your notes, the original issue price of the notes includes the agent’s commission and the cost of hedging our obligations under the notes through one or more of our affiliates, which includes our affiliates’ expected cost of providing such hedge as well as the profit our affiliates expect to realize in consideration for assuming the risks inherent in providing such hedge. As a result, the price, if any, at which Lehman Brothers Inc. will be willing to purchase notes from you in secondary market transactions, if at all, will likely be lower than the original issue price and any sale prior to maturity could result in a substantial loss to you. The notes are not designed to be short-term trading instruments. YOU SHOULD BE WILLING TO HOLD YOUR NOTES TO MATURITY. |

| • | An Investment in the Notes is Subject to Risks Associated with Non-U.S. Securities Markets:The stocks that constitute the Underlying Index of each Index Fund have been issued by non-U.S. companies. Investments in securities linked to the value of such non-U.S. equity securities involve risks associated with the securities markets in those countries, including risks of volatility in those markets, governmental intervention in those markets and cross shareholdings in companies in certain countries. Also, there is generally less publicly available information about companies in some of these jurisdictions than about U.S. companies that are subject to the reporting requirements of the Securities and Exchange Commission, and generally non-U.S. companies are subject to accounting, auditing and financial reporting standards and requirements and securities trading rules different from those applicable to U.S. reporting companies. |

The prices of securities in non-U.S. jurisdictions may be affected by political, economic, financial and social factors in such markets, including changes in a country’s government, economic and fiscal policies, currency exchange laws or other foreign laws or restrictions. Moreover, the economies in such countries may differ favorably or unfavorably from the economy of the United States in such respects as growth of gross national product, rate of inflation, capital reinvestment, resources and self sufficiency. Such countries may be subject to different and, in some cases, more adverse economic environments.

The securities markets on which the stocks of the companies included in the MSCI Brazil IndexSM are traded are not as large as the U.S. securities markets and have substantially less trading volume, which may result in a lack of liquidity and high price volatility relative to the U.S. securities markets. There is also a high concentration of market capitalization and trading volume in a small number of issuers representing a limited number of industries, as well as a high concentration of certain types of investors (including investment funds and other institutional investors) in these securities markets. As a result, the securities markets on which the stocks of the companies included in the MSCI Brazil IndexSM are traded may be subject to significantly greater risk and price volatility than the U.S. securities markets.

• | The Basket Return Will Not Be Adjusted for Changes in Exchange Rates Relative to the U.S. Dollar that Might Affect the MSCI Brazil IndexSM or the FTSE/Xinhua China 25 IndexTM: The value of your notes will not be adjusted for exchange rate fluctuations between the U.S. dollar and the currencies in which the stocks included in the MSCI Brazil IndexSM and the FTSE/Xinhua China 25 IndexTM are based. Therefore, if the applicable currencies appreciate or depreciate relative to the U.S. dollar over the term of the notes, you will not receive any additional payment or incur any reduction in your Payment at Maturity. |

| • | Lack of Liquidity: The notes will not be listed on any securities exchange. Lehman Brothers Inc. intends to offer to purchase the notes in the secondary market but is not required to do so. Even if there is a secondary market, it may not provide enough liquidity to allow you to trade or sell the notes easily. Because other dealers are not likely to make a secondary market for the notes, the price at which you may be able to trade your notes is likely to depend on the price, if any, at which Lehman Brothers Inc. is willing to buy the notes. If you are an employee of Lehman Brothers Holdings Inc. or one of our affiliates, you may not be able to purchase the notes from us and your ability to sell or trade the notes in the secondary market may be limited. |

| • | Potential Conflicts: We and our affiliates play a variety of roles in connection with the issuance of the notes, including acting as calculation agent and hedging our obligations under the notes. In performing these duties, the economic interests of the calculation agent and other affiliates of ours are potentially adverse to your interests as an investor in the notes. |

| • | We and our Affiliates and Agents May Publish Research, Express Opinions or Provide Recommendations that are Inconsistent with Investing in or Holding the Notes. Any Such Research, Opinions or Recommendations Could Affect the Index Funds or the Value of the Notes: We, our affiliates and agents publish research from time to time on financial markets and other matters that may influence the value of the notes, or express opinions or provide recommendations that are inconsistent with purchasing or holding the notes. We, our affiliates and agents may have published research or other opinions that are inconsistent with the investment view implicit in the notes. Any research, opinions or recommendations expressed by us, our affiliates or agents may not be consistent with each other and may be modified from time to time without notice. Investors should make their own independent investigation of the merits of investing in securities (like the notes) that which are linked to the Index Funds. |

| • | Many Economic and Market Factors Will Influence the Value of the Notes: In addition to the value of the Index Funds and interest rates on any trading day, the value of the notes will be affected by a number of economic and market factors that may either offset or magnify each other and which are set out in more detail in the accompanying product supplement no. 890-I and the accompanying underlying supplement no. 1080. |

| • | Anti-Dilution Protection is Limited: The calculation agent will make adjustments to the Share Adjustment Factor for certain adjustment events affecting the Index Funds. However, the calculation agent will not make an adjustment in response to all events that could affect the Index Funds. If an event occurs that does not require the calculation agent to make an adjustment, the value of the notes may be materially and adversely affected. |

| • | Credit of Issuer: An investment in the notes will be subject to the credit risk of Lehman Brothers Holdings Inc., and the actual and perceived creditworthiness of Lehman Brothers Holdings Inc. may affect the market value of the notes. |

TS-3

Examples of Hypothetical Payment at Maturity for Each $1,000 Principal Amount Note

The following table illustrates hypothetical payments at maturity on a $1,000 investment in the notes, based on a range of hypothetical Final Share Prices of the Least Performing Index Fund and assuming that the closing price per share of each Index Fund is not below such Index Fund’s Trigger Price on any trading day from the Pricing Date to, and including, the Observation Date, except as indicated in the column titled “Hypothetical lowest closing price per share of iShares® MSCI Brazil Index Fund during the Monitoring Period.” The following table assumes that the Least Performing Index Fund will be the iShares® MSCI Brazil Index Fund and that the iShares® MSCI Brazil Index Fund will be the least performing Index Fund at all times during the term of the notes. We make no representation or warranty as to which of the Index Funds will be the Least Performing Index Fund for the purposes of calculating your actual Payment at Maturity. For more information see “Selected Purchase Considerations—Your Return at Maturity May Be Based on an Index Fund Whose Share Price Has Never Been Below Such Index Fund’s Trigger Price.”

For this table of hypothetical payments at maturity, we have also assumed the following:

| • | Initial Share Price: $79.88 |

| • | Trigger Price: $47.928 |

| • | Coupon: 15.80% |

Hypothetical lowest closing price per share of the iShares® MSCI Brazil Index Fund during the Monitoring Period | Hypothetical Final Share Price of the Least Performing Index Fund (the iShares® MSCI Brazil Index Fund) | Payment at Maturity* | ||

$79.88 | $111.83 | $1,000.00 | ||

$79.88 | $95.86 | $1,000.00 | ||

$79.88 | $79.88 | $1,000.00 | ||

$63.90 | $63.90 | $1,000.00 | ||

$43.93 | $83.87 | $1,000.00 | ||

$39.94 | $67.90 | $850.00 | ||

$39.94 | $55.92 | $700.00 | ||

$39.94 | $39.94 | $500.00 | ||

$0.00 | $0.00 | $0.00 |

| * | Note that you will receive at maturity any accrued and unpaid coupon payments, in addition to the Cash Value or the principal amount of your note in cash, as applicable. |

The following examples illustrate how the total value of payments received at maturity set forth in the table above are calculated.

Example 1: During the Monitoring Period, none of the Index Funds closes at a price below its respective Trigger Price. Because a Trigger Event has not occurred and none of the Final Share Prices of the Index Funds is below the Initial Share Prices of the Index Funds, you will receive a Payment at Maturity of $1,000 per $1,000 principal amount note.

Example 2: During the Monitoring Period, the iShares® MSCI Brazil Index Fund closed below its Trigger Price. However, on the Observation Date, none of the Final Share Prices of the Index Funds is below the Initial Share Prices of the Index Funds. Because none of the Final Share Prices of the Index Funds is below the Initial Share Prices of the Index Funds, you will receive $1,000 per $1,000 principal amount note at maturity even though a Trigger Event occurred.

TS-4

Example 3: During the Monitoring Period, the iShares® MSCI Brazil Index Fund closed below its Trigger Price. On the Observation Date, the Final Share Price of the iShares® MSCI Brazil Index Fund, the Least Performing Index Fund, is $67.90, which is below its Initial Share Price. Because at least one of the Index Funds had a closing price that was below its Trigger Price, and because the Final Share Price of the Least Performing Index Fund is below its Initial Share Price, you will receive the Cash Value at maturity. Because the Final Share Price of the Least Performing Index Fund is $67.90, the total value of your final Payment at Maturity is $850.00.

Regardless of the other payment you receive at maturity, you will have received coupon payments, for each $1,000 principal amount note, in the aggregate amount of approximately $39.50 over the term of the notes.

The actual Cash Value you would receive at maturity (if a Trigger Event occurs and the Final Share Price of one or more of the Index Funds is below its respective Initial Share Price) and the actual Trigger Price may be more or less than the amounts displayed in the hypothetical examples and the chart above and will depend in part on the closing price of the shares of each Index Fund on the Pricing Date.

The Index Funds

Initial Share Prices and Trigger Prices

The Index Funds are the iShares® MSCI Brazil Index Fund (NYSE: EWZ) and the iShares® FTSE/Xinhua China 25 Index Fund (NYSE: FXI). The table below sets forth the ticker symbol for each Index Fund and the U.S. exchange on which each Index Fund is listed. The Index Funds may be modified in the case of certain corporate events. See “Description of Notes — Anti-dilution Adjustments” in the accompanying product supplement no. 890-I.

The table below indicates the Initial Share Price and Trigger Price for each Index Fund, subject to adjustments.

Index Fund | Ticker Symbol | Exchange | Initial Share Price | Trigger Price | ||||

iShares® MSCI Brazil Index Fund | EWZ | NYSE | $[TBD] | $[TBD] | ||||

iShares® FTSE/Xinhua China 25 Index Fund | FXI | NYSE | $[TBD] | $[TBD] |

Historical Information on the iShares® MSCI Brazil Index Fund

The following graph sets forth the historical performance of the shares of the iShares® MSCI Brazil Index Fund based on the daily closing price per share of the iShares® MSCI Brazil Index Fund from December 4, 2002 through December 4, 2007. The closing price per share of the iShares® MSCI Brazil Index Fund on December 4, 2007 was $79.88. We obtained the closing prices below from Bloomberg Financial Markets, without independent verification. We make no representation or warranty as to the accuracy or completeness of the information obtained from Bloomberg Financial Markets.

The historical performance of the iShares® MSCI Brazil Index Fund should not be taken as an indication of future performance, and no assurance can be given as to the closing prices of the iShares® MSCI Brazil Index Fund during the term of the notes. We cannot give you assurance that the performance of the iShares® MSCI Brazil Index Fund will result in the return of any of your initial investment.

TS-5

Historical Information on the iShares® FTSE/Xinhua China 25 Index Fund

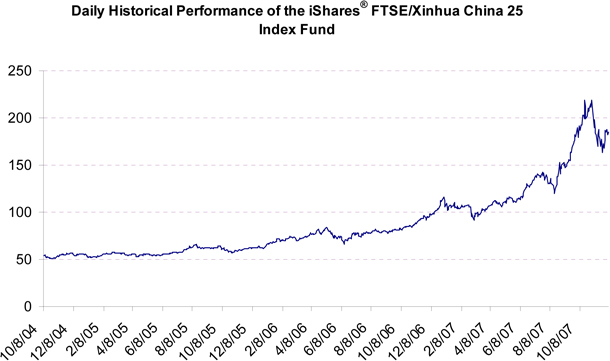

The following graph sets forth the historical performance of the shares of the iShares® FTSE/Xinhua China 25 Index Fund based on the daily closing price per share of the iShares® FTSE/Xinhua China 25 Index Fund from October 8, 2004 (the day the iShares® FTSE/Xinhua China 25 Index Fund began trading) through December 4, 2007. The closing price per share of the iShares® FTSE/Xinhua China 25 Index Fund on December 4, 2007 was $184.80. We obtained the closing prices below from Bloomberg Financial Markets, without independent verification. We make no representation or warranty as to the accuracy or completeness of the information obtained from Bloomberg Financial Markets.

The historical performance of the iShares® FTSE/Xinhua China 25 Index Fund should not be taken as an indication of future performance, and no assurance can be given as to the closing prices of the iShares® FTSE/Xinhua China 25 Index Fund during the term of the notes. We cannot give you assurance that the performance of the iShares® FTSE/Xinhua China 25 Index Fund will result in the return of any of your initial investment.

TS-6

Supplemental Plan of Distribution

We have agreed to sell to Lehman Brothers Inc., and Lehman Brothers Inc. has agreed to purchase, all of the notes at the price indicated on the cover of the pricing supplement that will contain the final pricing terms of the notes.

We have agreed to indemnify Lehman Brothers Inc. against liabilities, including liabilities under the Securities Act of 1933, as amended, or to contribute to payments that Lehman Brothers Inc. may be required to make relating to these liabilities as described in the MTN prospectus supplement and the base prospectus.

Lehman Brothers Inc. will offer the notes initially at a public offering price equal to the issue price set forth on the cover of the pricing supplement. After the initial public offering, the public offering price may from time to time be varied by Lehman Brothers Inc.

We expect to deliver the notes against payment on or about December 31, 2007, which is the fifth business day following the Pricing Date. Under Rule 15c6-1 of the Exchange Act, trades in the secondary market generally are required to settle in three business days, unless the parties to any such trade expressly agree otherwise. Accordingly, if any purchaser wishes to trade the notes on the Pricing Date, it will be required, by virtue of the fact that the notes initially will settle on the fifth business day following the Pricing Date, to specify an alternative settlement cycle at the time of any such trade to prevent a failed settlement.

We or our affiliate may enter into swap agreements or related hedge transactions with one of our other affiliates or unaffiliated counterparties in connection with the sale of the notes, and Lehman Brothers Inc. and/or an affiliate may earn additional income as a result of payments pursuant to the swap or related hedge transactions.

TS-7