Lehman Brothers Holdings Inc Plan Trust (LEHMQ)

Filed: 5 Feb 08, 12:00am

ISSUER FREE WRITING PROSPECTUS Filed Pursuant to Rule 433 Registration Statement No. 333-134553 Dated February 4, 2008 |  |

Performance Securities

Linked to an Asian Currency Basket

Strategic Alternatives to Indexing

Lehman Brothers Holdings Inc. $· Notes Linked to an Asian Currency Basket due February 26, 2010

Investment Description

These Performance Securities Linked to an Asian Currency Basket (the “Notes”) provide potentially enhanced returns based on the positive performance of a basket composed of four currencies (the “Basket”) relative to the U.S. dollar (USD). The Basket includes the Malaysian Ringgit (MYR), the Indonesian Rupiah (IDR), the Indian Rupee (INR) and the Philippine Peso (PHP). The Notes are not subject to a maximum gain and, accordingly, any return at maturity will be determined by the appreciation of the Basket.Investing in the Notes is subject to significant risks, including a potential loss of up to 100% of principal.

Features

| q | Potential enhanced returns linked to the appreciation of the Basket relative to the USD, with one for one downside exposure |

| q | Exposure to the currencies of Malaysia, Indonesia, India and the Philippines relative to the U.S. dollar |

| q | [325-375%] Participation Rate (the actual Participation Rate will be determined on the Trade Date) |

Key Dates1

Trade Date | February 26, 2008 | |

Settlement Date | February 29, 2008 | |

Valuation Date2 | February 23, 2010 | |

Maturity Date | February 26, 2010 |

1 | Expected. In the event we make any change to the expected Trade Date and Settlement Date, the Valuation Date and the Maturity Date will be changed so that the stated term of the Notes remains the same. |

2 | Upon the occurrence of a Disruption Event with respect to a Basket Currency, the Valuation Date for the affected Basket Currency may be postponed (as described in “Disruption Events” in “Additional Specific Terms of the Notes” below). |

Security Offerings

We are offering Performance Securities Linked to an Asian Currency Basket. The Notes do not bear interest and, accordingly, any return at maturity will be determined by the appreciation or depreciation of the Basket relative to the USD. If the Basket Return, which is linked to the performance of the Basket relative to the USD, is greater than zero on the Valuation Date, the investor will receive a single payment at maturity equal to the principal amount of the Notes plus an additional amount equal to the principal amount of the Notes multiplied by the product of [325- 375%] (the Participation Rate) and the appreciation of the Basket (that is, the amount by which the Basket Return exceeds zero). If the Basket Return on the Valuation Date is less than or equal to zero, then the investor will receive at maturity the principal amount of the Notes minus an amount equal to the principal amount of the Notes multiplied by the depreciation of the Basket (that is, the amount by which the Basket Return is below zero).Since the Notes are not principal protected even if held to maturity, investors may lose their entire investment in the Notes. The Notes do not bear interest. The Notes are offered at a minimum investment of $1,000. The CUSIP for the Notes is 52522L632 and the ISIN is US52522L6323.

See “Additional Information about Lehman Brothers Holdings Inc. and the Notes” on page 2, “Indicative Terms” on page 3 and “Additional Specific Terms of the Notes” on page 5. The Notes offered will have the terms specified in the base prospectus dated May 30, 2006, the prospectus supplement dated May 30, 2006 for the Issuer’s Medium term Notes, Series I (the “MTN Prospectus Supplement”), and this Term Sheet. See “Key Risks” on page 6 and “Risk Factors” generally, and “Risk Factors—Risks Relating to Currency Indexed Notes” in particular, in the MTN Prospectus Supplement for risks related to an investment in the Notes.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of the Notes or passed upon the accuracy or the adequacy of this term sheet, the accompanying base prospectus, the MTN Prospectus Supplement or any other relevant terms or pricing supplement. Any representation to the contrary is a criminal offense. The Notes are not deposit liabilities of Lehman Brothers Holdings Inc. and are not FDIC-insured.

| Price to Public | Underwriting Discount | Proceeds to Us | ||||

Per Note | $10.00 | $0.20 | $9.80 | |||

Total |

UBS Financial Services Inc. | Lehman Brothers Inc. |

Additional Information about Lehman Brothers Holdings Inc. and the Notes

Lehman Brothers Holdings Inc. has filed a registration statement (including a prospectus) with the U.S. Securities and Exchange Commission (SEC) for this offering. Before you invest, you should read the prospectus dated May 30, 2006, the MTN Prospectus Supplement and other documents Lehman Brothers Holdings Inc. has filed with the SEC for more complete information about Lehman Brothers Holdings Inc. and this offering. Buyers should rely upon the prospectus, MTN Prospectus Supplement, this term sheet and any relevant free writing prospectus for complete details. You may get these documents and other documents Lehman Brothers Holdings Inc. has filed for free by searching the SEC online database (EDGAR®) atwww.sec.gov, with “Lehman Brothers Holdings Inc.” as a search term or through the links below, or by calling UBS Financial Services Inc. toll-free at 1-877-827-2010 or Lehman Brothers Inc. toll-free at 1-888-603-5847.

You may access these documents on the SEC web site at www.sec.gov as follows:

| ¨ | MTN Prospectus Supplement dated May 30, 2006 |

http://www.sec.gov/Archives/edgar/data/806085/000104746906007785/a2170815z424b2.htm

| ¨ | Base Prospectus dated May 30, 2006 |

http://www.sec.gov/Archives/edgar/data/806085/000104746906007771/a2165526zs-3asr.htm

| ¨ | Prospectus Addendum dated December 12, 2007: |

http://www.sec.gov/Archives/edgar/data/806085/000119312507263735/d424b2.htm

We urge you to consult your investment, legal, tax, accounting and other advisors before you invest in the Notes. You should reach an investment decision only after you and your advisors have carefully considered the suitability of an investment in the Notes in light of your particular circumstances.

References to “Lehman Brothers,” “we,” “our” and “us” refer only to Lehman Brothers Holdings Inc. and not to its consolidated subsidiaries. In this document, “Notes” refers to the Non-Principal Protected Notes Linked to an Asian Currency Basket that are offered hereby, unless the context otherwise requires.

Investor Suitability

The Notes may be suitable for you if, among other considerations:

| ¨ | You seek an investment with a return linked to the performance of the currencies of Malaysia, Indonesia, India and the Philippines relative to the U.S. dollar |

| ¨ | You believe the currencies in the Basket will appreciate relative to the U.S. dollar over the term of the Notes |

| ¨ | You are willing to invest in notes that offer no principal protection, and are willing to risk losing up to 100% of your investment |

| ¨ | You do not seek current income from this investment |

| ¨ | You are willing to hold the Notes to maturity, and are aware that there may be little or no secondary market for the Notes |

| ¨ | You are willing to invest in the Notes based on the range indicated for the Participation Rate (the actual Participation Rate will be determined on the Trade Date) |

The Notes may not be suitable for you if, among other considerations:

| ¨ | You do not seek an investment with exposure to the currencies of Malaysia, Indonesia, India and the Philippines relative to the U.S. dollar |

| ¨ | You seek an investment that is 100% principal protected |

| ¨ | You prefer the lower risk, and therefore accept the potentially lower returns, of fixed income investments with comparable maturities and credit ratings |

| ¨ | You seek current income from your investments |

| ¨ | You seek an investment for which there will be an active secondary market, or are unable or unwilling to hold the Notes to maturity |

The suitability considerations identified above are not exhaustive. Whether or not the Notes are a suitable investment for you will depend on your individual circumstances, and you should reach an investment decision only after you and your investment, legal, tax, accounting and other advisors have carefully considered the suitability of an investment in the Notes in light of your particular circumstances. You should also review carefully the “Key Risks” on page 6, and “Risk Factors” generally, and “Risk Factors—Risks Relating to Currency Indexed Notes” in particular, in the MTN Prospectus Supplement for risks related to an investment in the Notes.

2

Indicative Terms

Issuer | Lehman Brothers Holdings Inc. (A+/A1/AA-)1 | |||

Issue Size | $ TBD | |||

Issue Price | $10 per Note | |||

Term | 2 years | |||

Basket | The Malaysian Ringgit (MYR), the Indonesian Rupiah (IDR), the Indian Rupee (INR) and the Philippine Peso (PHP) (each a “Basket Currency” and collectively the “Basket Currencies”)2 The performance of the Basket will be measured relative to the U.S. dollar | |||

Basket Currency Weighting | For each Basket Currency, as set forth below: | |||

MYR | 25% | |||

IDR | 25% | |||

INR | 25% | |||

PHP | 25% | |||

Protection Percentage | None | |||

Participation Rate | 325% to 375%. The actual Participation Rate will be determined on the Trade Date. | |||

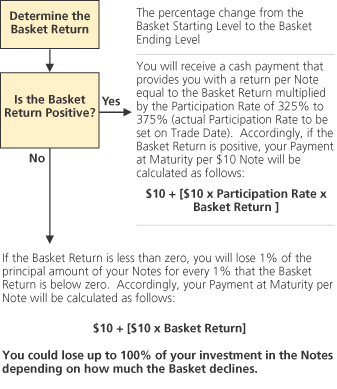

Payment at Maturity | If the Basket Return is greater than zero, you will receive a cash payment, for each Note, equal to:

$10 + [$10 x Participation Rate x Basket Return]

If the Basket Return is equal to or less than zero, you will lose 1% of the principal amount of your Notes for every 1% that the Basket Return is below zero. Accordingly, you will receive a cash payment, for each Note, equal to:

$10 + [$10 x Basket Return] | |||

Basket Return | A percentage equal to: | |||

Basket Ending Level – Basket Starting Level Basket Starting Level | ||||

Basket Starting Level | Set to 100 on the Trade Date | |||

Basket Ending Level | The Basket closing level on the Valuation Date, equal to 100 x (1 plus the sum of the Weighted Currency Returns) | |||

Weighted Currency Return | For each Basket Currency: Currency Return x Basket Currency Weighting | |||

Currency Return | For each Basket Currency: | |||

Initial Spot Rate – Final Spot Rate Initial Spot Rate | ||||

Final Spot Rate2: | For each Basket Currency, the Reference Exchange Rate for that Basket Currency on the Valuation Date, determined by the Calculation Agent in accordance with the Spot Rate Source2 (subject to the occurrence of a Disruption Event). | |||

Initial Spot Rate | For each Basket Currency, the Reference Exchange Rate for that Basket Currency determined by the Calculation Agent on the Trade Date, as set forth below: | |||

MYR | TBD | |||

IDR | TBD | |||

INR | TBD | |||

PHP | TBD | |||

Determining Payment at Maturity

1 | Lehman Brothers Holdings Inc. is rated A+ by Standard & Poor’s, A1 by Moody’s and AA- by Fitch. A credit rating reflects the creditworthiness of Lehman Brothers Holdings Inc. and is not a recommendation to buy, sell or hold securities, and may be subject to revision or withdrawal at any time by the assigning rating organization. Each rating should be evaluated independently of any other rating. The creditworthiness of the issuer does not affect or enhance the likely performance of the investment other than the ability of the issuer to meet its obligations. |

2 | As used herein, the term “Final Spot Rate” has the meaning assigned to the term “Settlement Rate” in the MTN Prospectus Supplement and the term “Spot Rate Source” has the meaning assigned to the term “Settlement Rate Option” in the MTN Prospectus Supplement, and the term “Basket Currency” has the meaning assigned to the term “reference currency” in the MTN Prospectus Supplement. |

3

Scenario Analysis and Examples at Maturity

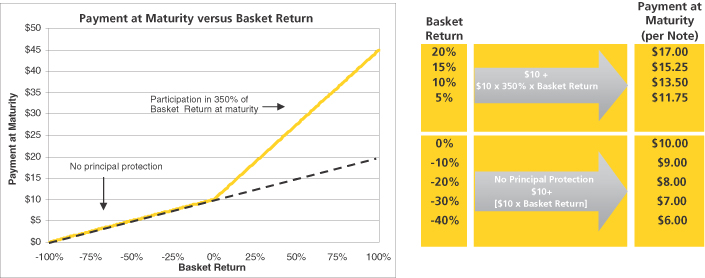

The following examples for the Notes show scenarios for the Payment at Maturity for the Notes, assuming a Participation Rate of 350% and a range of hypothetical Basket Returns from +100% to –100%. The actual Participation Rate will be set on the Trade Date.

Example A— The level of the Basket increases from a Basket Starting Level of 100 to a Basket Ending Level of 110.Because the Basket Ending Level is 110 and the Basket Starting Level is 100, the Basket Return is 10%, calculated as follows:

(110 - 100)/100 = 10%

Because the Basket Return is equal to 10%, the Payment at Maturity is equal to $13.50 per $10 Note (a return of 35% or $3.50 per $10 Note), calculated as follows:

$10 + ($10 x 350% x 10%) = $13.50

Example B— The level of the Basket decreases from a Basket Starting Level of 100 to a Basket Ending Level of 90.Because the Basket Ending Level is 90 and the Basket Starting Level is 100, the Basket Return is –10%, calculated as follows:

(90 - 100)/100 = –10%

Because the Basket Return is equal to –10%, the Payment at Maturity is equal to $9 per $10 Note (a loss of $1 in principal per $10 Note), calculated as follows:

$10 + ( $10 x –10%) = $9

For additional payment examples for the Notes showing scenarios for the Payment at Maturity of the Notes, showing Basket Ending Levels above and below the Basket Starting Level and the resulting positive and negative Basket Ending Levels and Basket Returns (based on either correlated or offsetting appreciation and depreciation in the different Basket Currencies), see “Additional Payment at Maturity Examples” below.

4

Additional Specific Terms of the Notes

Valuation Date | February 23, 2010; provided that, upon the occurrence of a Disruption Event with respect to a Basket Currency, the Valuation Date for the affected Basket Currency may be postponed (as described in “Disruption Events” below). | |||||

Reference Exchange Rates | The spot exchange rates for each of the Basket Currencies quoted against the U.S. dollar, expressed as the number of units of the Basket Currency per one USD. | |||||

Spot Rate Source and Valuation Business Day: | The Spot Rate Source and Valuation Business Day for each Basket Currency is as set forth below: | |||||

| Basket Currency | Screen Reference | Valuation Business Day | ||||

| MYR | ABSIRFIX01 | Singapore | ||||

| IDR | ABSIRFIX01 | Singapore | ||||

| INR | RBIB | Mumbai | ||||

| PHP | PDSPESO (as successor to PHPESO) | Manila | ||||

For further information concerning the Spot Rate Source and Valuation Business Day, see “Description of the Notes—Currency-Indexed Notes” in, and Appendix A to, the MTN Prospectus Supplement | ||||||

Disruption Events | If a Disruption Event relating to one or more Basket Currencies is in effect on the scheduled Valuation Date, the Calculation Agent will calculate the Basket Return using: | |||||

¨ for each Basket Currency that did not suffer a Disruption Event on the scheduled Valuation Date, the Final Spot Rate on the scheduled Valuation Date, and

¨ for each Basket Currency that did suffer a Disruption Event on the scheduled Valuation Date, the Final Spot Rate on the immediately succeeding scheduled Valuation Business Day for such Basket Currency on which no Disruption Event occurs or is continuing with respect to such Basket Currency;

provided however that if a Disruption Event has occurred or is continuing with respect to a Basket Currency on each of the three scheduled Valuation Business Days following the scheduled Valuation Date, then (a) such third scheduled Valuation Business Day shall be deemed the Valuation Date for the affected Basket Currency; and (b) the Calculation Agent will determine the Final Spot Rate for the affected Basket Currency on such day in accordance with "Fallback Rate Observation Methodology” (as defined under “Description of the Notes—Currency-Indexed Notes” in the MTN Prospectus Supplement).

A “Disruption Event” means any of the following events with respect to a Basket Currency, as determined in good faith by the Calculation Agent:

(A) the occurrence and/or existence of an event on any day that has the effect of preventing or making impossible the delivery of USD from accounts inside the Basket Currency Jurisdiction3 for that Basket Currency to accounts outside that Basket Currency Jurisdiction;

(B) the occurrence of any event causing the Reference Exchange Rate for the Basket Currency to be split into dual or multiple currency exchange rates; or

(C) the Final Spot Rate being unavailable for the Basket Currency, or the occurrence of an event (i) in the Basket Currency Jurisdiction for that Basket Currency that materially disrupts the market for the Basket Currency or (ii) that generally makes it impossible to obtain the Final Spot Rate for the Basket Currency, on the Valuation Date.

For purposes of the above, “scheduled Valuation Business Day” means a day that is or, in the judgment of the Calculation Agent, should have been, a Valuation Business Day for the affected Basket Currency | ||||||

Business Day | New York | |||||

Business Day Convention | Following | |||||

Calculation Agent: | Lehman Brothers Inc. | |||||

Identifier | CUSIP: 52522L632 | ISIN: US52522L6323 | ||||

Denominations | $10 and whole multiples of $10 | |||||

3 | As used herein, the term “Basket Currency Jurisdiction” has the meaning assigned to the term “Reference Currency Jurisdiction” in the MTN Prospectus Supplement. |

5

What are the tax consequences of the Notes?

Lehman Brothers Holdings Inc. intends to treat the Notes as financial contracts subject to the Foreign Currency Rules, as described under “Supplemental United States Federal Income Tax Consequences—Financial Contracts” in the MTN Prospectus Supplement. However, no statutory, judicial or administrative authority directly addresses the treatment of the Notes. The characterization and the tax treatment of the Notes is uncertain and some of the discussion under “Supplemental United States Federal Income Tax Consequences—Financial Contracts” in the MTN Prospectus Supplement could be inapplicable. Any differing treatment could affect the amount, timing, and character of income with respect to the Notes. For example, the IRS recently issued a Revenue Ruling treating certain foreign currency-linked instruments as indebtedness. Although the terms of the Notes are distinguishable from those of the Revenue Ruling, there can be no assurance that the IRS will not seek to apply the Revenue Ruling to the Notes or otherwise recharacterize the Notes as indebtedness. The Notes are subject to complex tax rules and investors should consult their own tax advisors regarding the tax treatment of the Notes.

Assuming the Notes are characterized as financial contracts, gain or loss upon a sale, exchange or other disposition of the Notes will generally be treated as ordinary gain or loss unless you make a valid election before the close of the day on which you purchase the Notes to treat such gain or loss as capital gain or loss. To make this election, you must, in accordance with the detailed procedures set forth in the regulations under section 988 of the Code, either (a) clearly identify the transaction on your books and records on the date you acquire your Notes as being subject to such an election and file the relevant statement verifying such election with your federal income tax return, or (b) otherwise obtain independent verification. It is unclear whether the Notes qualify for such an election, and you should consult your own advisors in that regard. In addition, the Notes may be subject to the “mark-to-market” rules of section 1256 of the Code, and you could incur federal tax liability on an annual basis in respect of an increase in the value of the Notes without a corresponding receipt of cash. If you have made a valid election as described above, the “mark-to-market” rules would treat 60% of any capital gain or loss recognized on the sale, exchange, settlement or other disposition as long-term capital gain or loss, and 40% of any such gain or loss as short-term capital gain or loss. You should consult your advisors with respect to the character of gain or loss with respect to the sale, exchange, settlement or other disposition of the Notes. See “Supplemental United States Federal Income Tax Consequences-Financial Contracts-Foreign Currency Rules” in the MTN Prospectus Supplement.

On December 7, 2007, the IRS released a Notice indicating that the IRS and the Treasury Department are considering and seeking comments as to whether holders of instruments similar to the Notes should be required to accrue income on a current basis over the term of the Notes, regardless of whether any payments are made prior to maturity. In addition, the Notice provides that the IRS and the Treasury Department are considering related issues, including, among other things, whether gain or loss from such instruments should be treated as ordinary or capital, whether foreign holders of such instruments should be subject to withholding tax, whether the tax treatment of such instruments should vary depending upon the nature of the underlying asset, and whether such instruments should be subject to the special “constructive ownership rules” contained in section 1260 of the Code. It is not possible to predict what changes, if any, will be adopted, or when they will take effect. Any such changes could affect the amount, timing and character of income, gain or loss in respect of the notes, possibly with retroactive effect. Holders are urged to consult their tax advisors concerning the impact of the Notice on their investment in the Notes.

Subject to future developments with respect to the foregoing, Lehman Brothers Holdings Inc. intends to continue to treat the Notes for U.S. federal income tax purposes in accordance with the treatment described above.

6

Key Risks

An investment in the Notes entails certain risks not associated with an investment in conventional floating rate or fixed rate medium-term notes. You should read the risks summarized below in conjunction with, and the risks summarized below are qualified by reference to, the risks described in “Risk Factors” generally, and “Risk Factors—Risks Relating to Currency Indexed Notes” in particular, in the MTN Prospectus Supplement. We urge you to consult your investment, legal, tax, accounting and other advisors before you invest in the Notes. You should reach an investment decision only after you and your advisors have carefully considered the suitability of an investment in the Notes in light of your particular circumstances.

| ¨ | No principal protection; your investment in the Notes may result in a loss—The return on the Notes at maturity is dependent on the Basket Return, which in turn depends on the aggregate Weighted Currency Returns of the Basket Currencies Because the Notes are not principal protected even if held to maturity, if the Basket Return is negative (that is, the Final Basket Level is less than the Initial Basket Level), you will lose 1% of the principal amount of your Notes for every 1% that the Basket Return is below zero, andyou will be exposed to a loss of up to 100% of the principal you invest in the Notes, or a potential loss of $10 on each $10 Note. In addition, the trading value of the Notes will be affected by factors that interrelate in complex ways, including (but not limited to) the prevailing exchange rates of the Basket Currencies relative to the U.S. dollar from time to time (as discussed under “Foreign Exchange Rate Risk” below). Selling this or any fixed income security prior to maturity may result in a dollar price less than 100% of the applicable principal amount of Notes sold. |

| ¨ | No interest payments—The terms of the Notes differ from those of ordinary debt securities in that the Issuer will not pay interest on the Notes. The return on the Notes at maturity is entirely dependent on the aggregate performance of the Basket Currencies, and if the Basket Return is zero or less than zero, you will be exposed to a loss of up 100% of the principal amount invested in the Notes. |

| ¨ | Foreign exchange rate risk—An investment in the Notes may not be suitable for an investor unfamiliar with the exchange rates of the Basket Currencies relative to the U.S. dollar or the factors that affect movements in such exchange rates. The exchange rates for the Basket Currencies relative to the U.S. dollar will be influenced by the complex and interrelated global and regional political, economic, financial and other factors that can affect the currency markets on which a Basket Currency is traded. Changes in the exchange rates for the Basket Currencies result over time from the interaction of many factors directly or indirectly affecting economic and political conditions in the United States and the countries in which the Basket Currencies are circulated as legal tender, particularly relative rates of inflation, interest rate levels, the balance of payments and the extent of governmental surpluses or deficits in those countries. |

Foreign exchange rates can either be fixed by the sovereign government, allowed to float within a range of exchange rates set by the government, or left to float freely. Governments, including those issuing the Basket Currencies, use a variety of techniques, such as intervention by their central bank or imposition of regulatory controls or taxes, to affect the exchange rates of their respective currencies. They may also issue a new currency to replace an existing currency or alter the exchange rate or relative exchange characteristics by devaluation or revaluation of a currency. Thus, a special risk in purchasing the Notes is that their liquidity, trading value and amount payable could be affected by the actions of sovereign governments that could change or interfere with previously freely determined currency valuations, fluctuations in response to other market forces and the movement of currencies across borders. There will be no offsetting adjustment or change made during the term of the Notes in the event that the exchange rates should become fixed (or in the case of certain currencies, become floating), or in the event of any devaluation or revaluation or imposition of exchange or other regulatory controls or taxes or in the event of other developments affecting a Basket Currency, the U.S. dollar, or any other currency.

In addition, investments in or related to the currencies of emerging markets such as Malaysia, India, Indonesia and the Philippines are also subject to greater risks than those investments in more developed currencies of other markets, as discussed below. The information below is taken from and based on publicly available information.

Malaysia.The value of the Malaysian ringgit is heavily influenced by the actions of the central bank of Malaysia, Bank Negara Malaysia (“BNM”). The Malaysian ringgit was heavily impacted by the Asian financial crisis of 1997/1998. In the wake of the market driven devaluation, the Malaysian government announced that it would peg the Malaysian ringgit to the U.S. dollar. This peg remained in place until July 2005 when, following a similar announcement by the government of China related to the renminbi, the Malaysian government announced it was removing the peg and would allow the Malaysian ringgit to operate in a managed float. The BNM monitors the exchange rate for the Malaysian ringgit against a basket of currencies. The components of the basket are not disclosed. Factors that might affect the Malaysian government’s policy with respect to the Malaysian ringgit include the extent of Malaysia’s foreign currency reserves, the monetary policy of neighboring regional powers such as China, the balance of payments, the extent of governmental surpluses and deficits, the size of Malaysia’s debt service burden relative to the economy as a whole, regional hostilities, terrorist attacks or social unrest, and political constraints to which Malaysia may be subject.

The Republic of India.The Indian government has pursued policies of economic liberalization and deregulation, but the government’s role in the economy has remained significant. The Indian government allows the exchange rate to float freely, without a fixed target or band, but may intervene when it deems necessary to preserve stability. It also has the ability to restrict the conversion of rupees into foreign currencies, and, under certain circumstances, investors that seek to convert rupees into foreign currency must obtain the approval of the Reserve Bank of India. If the Indian government prevents the Indian rupee from floating freely in order to preserve stability, or if the Indian government, with the approval of the Reserve Bank of India, restricts the conversion of rupees into foreign currencies, the exchange rate of the Indian rupee relative to the U.S. dollar may be adversely impacted.

Indonesia. From 1977 to 1997, the Indonesian government maintained a managed floating exchange rate system under which the Indonesian rupiah was linked to a basket of currencies. In 1997, the Indonesian rupiah depreciated significantly during the Asian currency crisis and the Indonesian government subsequently abandoned its trading band policy and permitted the Indonesian rupiah to float without an announced level at which the government would intervene. The Indonesian government continues to intervene in the foreign exchange market and to impose restrictions on certain foreign exchange transactions and dealings. Factors that might affect the Indonesian government’s policy with respect to the Indonesian rupiah include the extent of Indonesia’s

7

foreign currency reserves, the balance of payments, the extent of governmental surpluses and deficits, the size of Indonesia’s debt service burden relative to the economy as a whole, regional hostilities, terrorist attacks or social unrest, and political constraints to which Indonesia may be subject.

Philippines.The Philippine peso has been a floating currency since the mid-1960s. Between 1996 and 2001, the Philippine peso depreciated significantly during and following the Asian financial crisis, and beginning in 2000, the Philippine Central Bank (the Bangko Sentral) began implementing a series of measures to curb foreign exchange speculation and foreign exchange volatility, including requiring a minimum holding period for foreign investments in peso time deposits and establishing documentary requirements for foreign exchange forward and swap transactions. The current administration has also continued to experience domestic political instability, including terrorist activity and attempted coups. Factors that might affect the Philippine government’s policy with respect to the Philippine peso include the extent of the Philippine’s foreign currency reserves, the balance of payments, the extent of governmental surpluses and deficits, the size of Philippine’s debt service burden relative to the economy as a whole, regional hostilities, terrorist attacks or social unrest, and political constraints to which the Philippines may be subject.

| ¨ | Volatility of currency markets—The values of the Basket Currencies relative to the U.S. dollar have in the past been, and may continue to be, volatile and may vary based on a number of interrelated factors, including economic, financial and political events that Lehman Brothers Holdings Inc. cannot control. |

| ¨ | Changes in the value of the Basket Currencies may offset each other—The Basket Return will be based on the aggregate appreciation or depreciation of the Basket Currencies as a whole. Movements in the exchange rates of the Basket Currencies may not correlate with each other, and an increase in the values of some but not all of the Basket Currencies relative to the U.S. dollar may be substantially or entirely offset by decreases in the values of the other Basket Currencies relative to the U.S. dollar. Therefore, in calculating the Basket Return, increases in the value of one or more of the Basket Currencies may be moderated, or wholly offset, by declines or lesser increases in the value of one or more of the other Basket Currencies. |

| ¨ | Exchange rates for the Basket Currencies prior to the Valuation Date will not factor into the calculation of the Basket Return—Because the Payment at Maturity will be based on the Basket Return, which in turn is calculated based on the Final Spot Rate for each Basket Currency on the Valuation Date, a single day near the end of the term of the Notes, the exchange rates for the Basket Currencies at other times during the term of the Notes or at the Maturity Date may have appreciated more (or depreciated less) than the Final Spot Rates for the Basket Currencies on the Valuation Date. |

| ¨ | Even though currency trades around-the-clock, the Notes may not—The interbank market in foreign currencies is a global, around-the-clock market. The hours of trading for the Notes may not conform to the hours during which the Basket Currencies and the U.S. dollar are traded. Significant price and rate movements may take place in the underlying foreign exchange markets that will not be reflected immediately in the market price of the Notes. |

| ¨ | The market for the Notes may be illiquid—The Notes will not be listed on any securities exchange, and as a result, there may be little or no secondary market for the Notes. Subject to regulatory constraints, Lehman Brothers Inc. has agreed to use reasonable efforts to make a market in the Notes for so long as the Notes are outstanding. Even if there is a secondary market, it may not provide enough liquidity to allow you to sell the Notes easily, and if at any time Lehman Brothers Inc. were to cease acting as market maker, it is likely that there would be no secondary market for the Notes. |

| ¨ | Credit of Lehman Brothers Holdings Inc.—An investment in the Notes is subject to the creditworthiness of Lehman Brothers Holdings Inc. as issuer of the Notes, and the actual and perceived creditworthiness of Lehman Brothers Holdings Inc. may affect the market value of the Notes. |

| ¨ | Potential conflicts of interest—Lehman Brothers Inc. and other affiliates of Lehman Brothers Holdings Inc. play a variety of roles in connection with the issuance of the Notes, including acting as Calculation Agent and hedging Lehman Brothers Holdings Inc.’s obligations under the Notes. In performing these duties, the economic interests of the Calculation Agent and other affiliates of Lehman Brothers Holdings Inc. are potentially adverse to your interests as an investor in the Notes. |

| ¨ | Commissions and Hedging Costs—The original issue price of the Notes includes the underwriting commissions and fees and Lehman Brothers Holdings Inc.’s cost of hedging its obligations under the Notes through one or more of its affiliates. Such cost includes such affiliates’ expected cost of providing this hedge, as well as the profit these affiliates expect to realize in consideration for assuming the risks inherent in providing such hedge. As a result, assuming no change in market conditions or any other relevant factors, the price, if any, at which you are able to sell Notes in secondary market transactions, if at all, will likely be lower than the original issue price. |

| ¨ | Suspension or disruption of market trading in the Basket Currencies—Certain events, including events involving the suspension or disruption of market trading in the Basket Currencies, constitute Disruption Events under the terms of the Notes. To the extent any of these events occurs with respect to a Basket Currency and remains in effect on the Valuation Date, the Valuation Date for the affected Basket Currency may be postponed until the Disruption Event ceases to be in effect or, if the Disruption Event remains in effect for three scheduled Valuation Business Days, the exchange rate for the affected Basket Currency will be determined by the Calculation Agent in good faith based on quotations from dealers in the market for the relevant Basket Currency or, in certain circumstances, in the Calculation Agent’s discretion. In the event that the Valuation Date for one or more Basket Currencies is postponed, the Basket Return may be lower, and could result in the Payment at Maturity being lower, than what you may have anticipated based on the last available exchange rate for any affected Basket Currency as of the scheduled Valuation Date. For further information, see “Disruption Events” above. |

| ¨ | You must rely on your own evaluation of the merits of an investment linked to the Basket Currencies—In the ordinary course of their businesses, Lehman Brothers Holdings Inc., Lehman Brothers Inc., UBS Financial Services Inc. or their respective affiliates may from time to time express views on expected movements in the exchange rates of the Basket Currencies or other currencies. These views are sometimes communicated to clients who participate in the markets for the Basket Currencies and other currencies. However, these views, depending upon worldwide economic, political and other developments, may vary over differing time horizons and are subject to change. In connection with your purchase of the Notes, you should investigate the Basket Currencies and the markets in which they trade and not rely on views which may be expressed by Lehman Brothers Holdings Inc., Lehman Brothers Inc., UBS Financial Services Inc. or their respective affiliates in the ordinary course of their businesses with respect to future Basket Currency or other currency price movements. |

8

| ¨ | Historical information about the exchange rates for the Basket Currencies may not be indicative of future values—Historical information on the exchange rates of the Basket Currencies relative to the U.S. dollar, and hypothetical historical information concerning the composite Basket performance, furnished herein is provided as a matter of information only, and you should not regard the information as indicative of the range of, or trends in, future fluctuations in the exchange rates for the Basket Currencies relative to the U.S. dollar, the future performance of the Basket, the Basket Return or what the value of the Notes may be. Fluctuations in exchange rates make it difficult to predict whether the return on the Notes will be positive or negative, or what the Payment at Maturity may be. Historical exchange rate fluctuations may be greater or lesser than those experienced by the holders of the Notes. |

| ¨ | Certain activities by Lehman Brothers Holdings Inc., Lehman Brothers Inc, UBS Financial Services Inc. and their respective affiliates may adversely affect the value of the Notes—Lehman Brothers Holdings Inc. or one or more of its affiliates may hedge its obligations under the Notes by purchasing or selling the Basket Currencies, options or futures on the Basket Currencies or other instruments linked to the Basket Currencies, and may adjust the hedge by, among other things, purchasing or selling any of the foregoing, at any time and from time to time, and by unwinding the hedge by selling any of the foregoing. Lehman Brothers Holdings Inc. or one or more of its affiliates also may enter into, adjust and unwind hedging transactions relating to other notes whose returns are linked to the same Basket Currencies. Lehman Brothers Inc., UBS Financial Services Inc. and their respective affiliates may engage in trading in the Basket Currencies, or instruments whose returns are linked to the Basket Currencies, either for their proprietary accounts, for other accounts under their management or to facilitate transactions on behalf of customers. Any of these activities may adversely affect the market values or levels of the Basket Currencies and therefore the market value of the Notes. It is possible that Lehman Brothers Holdings Inc., Lehman Brothers Inc., UBS Financial Services Inc. or their respective affiliates could receive positive returns with respect to these activities while the value of the Notes may decline. |

Lehman Brothers Holdings Inc. or its affiliates also have issued and in the future may issue, and Lehman Brothers Inc., UBS Financial Services Inc. and their respective affiliates also have underwritten on behalf of other issuers and in the future may underwrite, other securities or financial or derivative instruments with returns linked to changes in the level of the Basket Currencies or other currencies. By introducing competing products into the marketplace in this manner, Lehman Brothers Holdings Inc., Lehman Brothers Inc., UBS Financial Services Inc. and their respective affiliates could adversely affect the value of the Notes and the amount payable on the Notes.

| ¨ | The trading value of the Notes may reflect a time premium or discount—As a result of a “time premium or discount,” the Notes may trade at a value above or below that which would be expected based on the level of interest rates and the values of the Basket Currencies relative to the U.S. dollar. A “time premium or discount” results from expectations regarding the value of one or more Basket Currencies relative to the U.S. dollar during the period prior to the Maturity Date. However, as the time remaining to the Maturity Date decreases, this time premium or discount may diminish, thereby decreasing or increasing the market value of the Notes. |

| ¨ | The Notes are not foreign currencies, and holders of the Notes will have no rights to receive the Basket Currencies—The Notes are linked to the composite value of the Basket Currencies relative to the U.S. dollar, but are not themselves the basket Currencies. The Payment at Maturity on the Notes will be made in U.S. dollars, and investing in the Notes will not entitle holders of the notes to receive the Basket Currencies. |

9

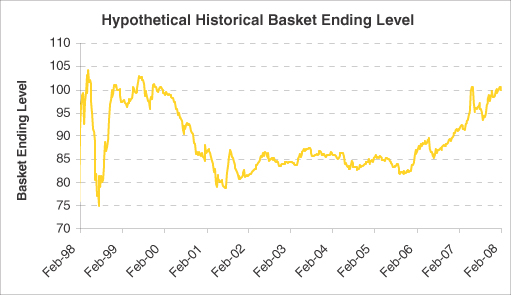

Hypothetical Historical Basket Performance

The following chart shows the hypothetical Basket Ending Level at the end of each week in the period from the week February 1, 1998 through the week ending February 3, 2008, using a Basket Ending Level indexed to 100 on February 3, 2008, based upon Initial Spot Rates determined on that day. The Basket Ending Level for any prior day was obtained by using the formula for the calculation of the Basket Ending Level described above. For purposes of the Notes and the determination of the Payment at Maturity, the Basket Starting Level will be indexed to 100 on the Trade Date.

Source: Lehman Brothers Inc.

The hypothetical historical Basket Ending Level chart above was prepared using historical weekly data for the Basket Currencies obtained from Reuters; none of UBS Financial Services Inc., Lehman Brothers Inc. or Lehman Brothers Holdings Inc. makes any representation or warranty as to the accuracy or completeness of this data. The hypothetical historical Basket Return is not necessarily indicative of the future performance of the Basket, the actual Basket Ending Level, the Basket Return or what the value of the Notes may be. Fluctuations in exchange rates make it difficult to predict the Payment at Maturity, or whether there will be a positive return on the Notes or a loss of principal. Historical exchange rate fluctuations may be greater or lesser than those experienced by the holders of the Notes.

10

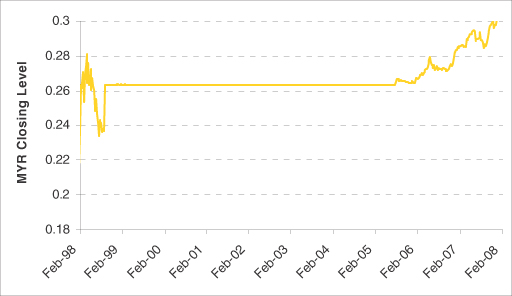

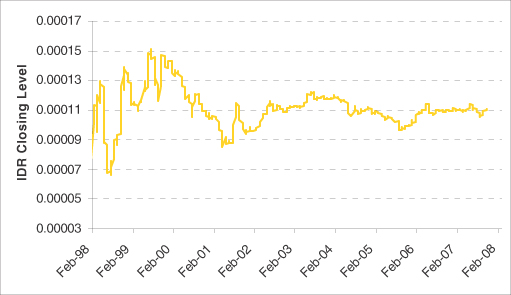

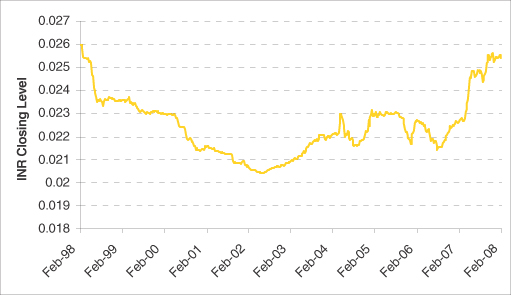

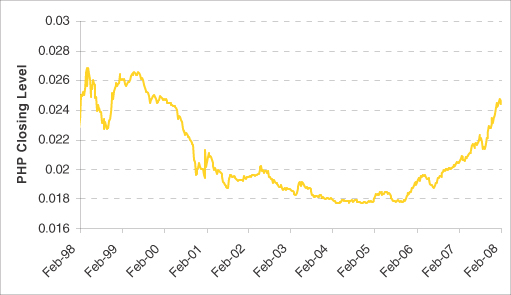

Historical Exchange Rates

The following charts show the spot exchange rates for each Basket Currency at the end of each week in the period from the week ending February 1, 1998 through the week ending February 3, 2008. The spot exchange rates are expressed as the amount of U.S. dollars per Basket Currency to show the appreciation or depreciation, as the case may be, of the Basket Currency against the U.S. dollar. The spot exchange rates used to calculate the Basket Return are expressed as the amount of Basket Currency per U.S. dollar, which are the inverse of the spot exchange rates presented in the following charts.

11

The historical exchange rates presented in the charts above were prepared using historical data obtained from Reuters; none of UBS Financial Services Inc., Lehman Brothers Inc. or Lehman Brothers Holdings Inc. makes any representation or warranty as to the accuracy or completeness of this data. The historical data on each Basket Currency is not necessarily indicative of the future performance of the Basket Currencies, the Basket Ending Level, the Basket Return or what the value of the Notes may be. Fluctuations in exchange rates make it difficult to predict the Payment at Maturity, or whether there will be a positive return on the Notes or a loss of principal. Historical exchange rate fluctuations may be greater or lesser than those experienced by the holders of the Notes.

12

Additional Payment at Maturity Examples

The following additional payment examples for the Notes shows scenarios for the Payment at Maturity of the Notes, illustrating Basket Ending Levels above and below the Basket Starting Level, and resulting positive and negative Basket Returns, reflecting either correlated or offsetting appreciation and depreciation in the different Basket Currencies. The following examples are, like the examples under “Scenario Analysis and Examples at Maturity” above, based on a hypothetical Participation Rate of 350% and hypothetical Initial Spot Rates for the Basket Currencies (each of which will be determined on the Trade Date), as well as hypothetical Final Spot Rates for the Basket Currencies (which will be determined on the Valuation Date), and the resulting Basket Ending Levels and Basket Returns. The hypothetical Initial Spot Rate and Final Spot Rate values for the Basket Currencies have been chosen arbitrarily for the purpose of these examples, are not associated with Lehman Brothers Research forecasts for any Basket Currency/USD exchange rates and should not be taken as indicative of the future performance of any Basket Currency/USD exchange rate.

Example A: MYR, IDR, INR and PHP each appreciate relative to their Initial Spot Rates, resulting in a Basket Ending Level of 107.75 and a Basket Return of 7.75%, and therefore a Payment at Maturity of $12.71 per $10 Note.

Because the Basket Return is 7.75%, which is greater than zero, the Payment at Maturity is equal to $12.71, per $10 Note (a return of 27.10% or $2.71 per $10 Note), calculated as follows:

$10 + ($10 x 350% x 7.75%) = $12.71

The table below illustrates how the Basket Ending Level in the above example was calculated:

Basket Currency | Initial Spot Rate | Final Spot Rate | Currency Return | Basket Currency | Weighted Currency | |||||

| MYR | 3.3256 | 3.0606 | 0.0600 | 25% | 0.0150 | |||||

| IDR | 9425 | 8577 | 0.0900 | 25% | 0.0225 | |||||

| INR | 39.26 | 34.55 | 0.1200 | 25% | 0.0300 | |||||

| PHP | 40.28 | 38.67 | 0.0400 | 25% | 0.0100 | |||||

| Sum of Weighted Currency Returns = | 0.0775 | |||||||||

| Basket Ending Level = 100 x (1 + Sum of Weighted Currency Returns) = | 107.75 | |||||||||

Example B: MYR, IDR, INR and PHP each depreciate relative to their Initial Spot Rates, resulting in a Basket Ending Level of 95.25 and a Basket Return of –4.75%, and therefore a Payment at Maturity of $9.53 per $10 Note.

Because the Basket Return is –4.75%, which is less than zero, the Payment at Maturity is equal to $9.53, per $10 Note (a loss of $0.47 in principal per $10 Note), calculated as follows:

$10 + ($10 x [–4.75%]) = $9.53

The table below illustrates how the Basket Ending Level in the above example was calculated:

Basket Currency | Initial Spot Rate | Final Spot Rate | Currency Return | Basket Currency | Weighted Currency | |||||

| MYR | 3.3256 | 3.3862 | –0.0400 | 25% | –0.0100 | |||||

| IDR | 9425 | 9708 | –0.0300 | 25% | –0.0075 | |||||

| INR | 39.26 | 41.22 | –0.0500 | 25% | –0.0125 | |||||

| PHP | 40.28 | 43.10 | –0.0700 | 25% | –0.0175 | |||||

| Sum of Weighted Currency Returns = | –0.0475 | |||||||||

| Basket Ending Level = 100 x (1 + Sum of Weighted Currency Returns) = | 95.25 | |||||||||

Example C: MYR and IDR each appreciate relative to their Initial Spot Rates, while INR and PHP each depreciate relative to their Initial Spot Rates, resulting in a Basket Ending Level of 100.63 and a Basket Return of 0.63%, and therefore a Payment at Maturity of $10.22 per $10 Note.

Because the Basket Return is 0.63%, which is greater than zero, the Payment at Maturity is equal to $10.22, per $10 Note (a return of 2.2% or $0.22 per $10 Note), calculated as follows:

$10 + ($10 x 350% x 0.63%) = $10.22

The table below illustrates how the Basket Ending Level in the above example was calculated:

Basket Currency | Initial Spot Rate | Final Spot Rate | Currency Return | Basket Currency | Weighted Currency | |||||

| MYR | 3.3256 | 2.8490 | 0.1250 | 25% | 0.0313 | |||||

| IDR | 9425 | 8388 | 0.1100 | 25% | 0.0275 | |||||

| INR | 39.26 | 44.76 | –0.1400 | 25% | –0.0350 | |||||

| PHP | 40.28 | 43.10 | –0.0700 | 25% | –0.0175 | |||||

| Sum of Weighted Currency Returns = | 0.0063 | |||||||||

| Basket Ending Level = 100 x (1 + Sum of Weighted Currency Returns) = | 100.63 | |||||||||

13

Example D: INR and PHP appreciate relative to their Initial Spot Rates, while MYR and IDR depreciate relative to their Initial Spot Rates, resulting in a Basket Ending Level of 97.24 and a Basket Return of –2.76%, and therefore a Payment at Maturity of $9.72 per $10 Note.

Because the Basket Return is –2.76%, which is less than zero, the Payment at Maturity is equal to $9.72, per $10 Note (a loss of $0.28 in principal per $10 Note) , calculated as follows:

$10 + ( $10 x [–2.76%]) = $9.72

The table below illustrates how the Basket Ending Level in the above example was calculated:

Basket Currency | Initial Spot Rate | Final Spot Rate | Currency Return | Basket Currency | Weighted Currency | |||||

| MYR | 3.3256 | 3.7118 | –0.1400 | 25% | –0.0350 | |||||

| IDR | 9425 | 10840 | –0.1501 | 25% | –0.0375 | |||||

| INR | 39.26 | 37.69 | 0.0399 | 25% | 0.0100 | |||||

| PHP | 40.28 | 34.64 | 0.1399 | 25% | 0.0350 | |||||

| Sum of Weighted Currency Returns = | –0.0276 | |||||||||

| Basket Ending Level = 100 x (1 + Sum of Weighted Currency Returns) = | 97.24 | |||||||||

14

Supplemental Plan of Distribution

We will agree to sell to UBS Financial Services Inc. and Lehman Brothers Inc. (together, the “Agents”), and the Agents will agree to purchase, all of the Notes at the price indicated on the cover of the pricing supplement, the document that will be filed pursuant to Rule 424(b) containing the final pricing terms of the Notes.

We have agreed to indemnify the Agents against liabilities, including liabilities under the Securities Act of 1933, as amended, or to contribute to payments that the Agents may be required to make relating to these liabilities as described in the MTN prospectus supplement and the base prospectus.

Subject to regulatory constraints, Lehman Brothers Inc. has agreed to use reasonable efforts to make a market in the Notes for so long as the Notes are outstanding.

We or our affiliate will enter into swap agreements or related hedge transactions with one of our other affiliates or unaffiliated counterparties in connection with the sale of the Notes, and the Agents and/or an affiliate may earn additional income as a result of payments pursuant to the swap or related hedge transactions.

15