Term sheet no. 1 to

Prospectus dated May 30, 2006

Prospectus supplement dated May 30, 2006

Product supplement no. 1140-I dated May [ ], 2008

Underlying Supplement no. 100 dated January 28, 2008

Registration Statement no. 333-134553

Dated May [ ], 2008

Rule 433

ISSUER FREE WRITING PROSPECTUS Filed Pursuant to Rule 433 Registration Statement No. 333-134553 Dated May 30, 2008

|  |

100% Principal Protection Absolute Return Barrier Notes

Investment Strategies for Uncertain Markets

Lehman Brothers Holdings Inc. Notes Linked to the S&P 500® Index due June 29, 2009

Lehman Brothers Holdings Inc. Notes Linked to the S&P 500® Index due June 29, 2009

(Asymmetric Barriers)

Investment Description

This term sheet relates to two separate issuances of 100% Principal Protection Absolute Return Barrier Notes Linked to the S&P 500® Index (each, a “Note” and collectively, the “Notes”). The Notes provide an opportunity to potentially hedge your exposure to equity securities as represented by the S&P 500® Index (the “Index”), while benefiting from moderately positive or negative returns of the Index. If the Index never closes above the applicable Upper Index Barrier or below the applicable Lower Index Barrier on any trading day during the Observation Period, at maturity you will receive your principal plus a return equal to the absolute value of the applicable Index Return. Otherwise, at maturity you will receive only your principal.

Features

q | Hedging Opportunity—You have the potential to hedge your exposure to the S&P 500® Index while benefiting from moderately positive or negative returns over the 1 year term of the Notes. |

| q | Potential for Equity-Linked Performance—If the Index never closes above the applicable Upper Index Barrier or below the applicable Lower Index Barrier on any trading day during the Observation Period, you will receive an equity-based return that may exceed the return you could receive on traditional fixed income investments. |

| q | Preservation of Capital—At maturity, you will receive a cash payment equal to at least 100% of your principal. |

Key Dates1

Trade Date | June 25, 2008 | |

Settlement Date | June 30, 2008 | |

Final Valuation Date | June 24, 2009 | |

Maturity Date | June 29, 2009 |

1 | The Notes are expected to trade on or about June 25, 2008 and settle on or about June 30, 2008. In the event we make any change to the expected Trade Date and Settlement Date, the Final Valuation Date and the Maturity Date will be changed so that the stated term of the Notes remains the same. |

Security Offerings

We are offering two separate issuances of 100% Principal Protection Absolute Return Barrier Notes linked to the S&P 500® Index. You may participate in one or both of the issuances. Each issuance of Notes is linked to the S&P 500® Index with a specified Upper Index Barrier and Lower Index Barrier. The actual Upper Index Barrier and Lower Index Barrier applicable to both issuances of Notes will be determined on the Trade Date.The performance of each issuance of Notes will not depend on the performance of the other issuance of Notes.Each Note is offered at a minimum investment of $1,000 in denominations of $10 and integral multiples of $10 in excess thereof.

| Underlying Index | Index Ticker | Upper Index Barrier* | Lower Index Barrier* | Index Starting Level* | CUSIP | ISIN | ||||||

S&P 500® Index | SPX | Index Starting Level × (1 + [14.50% - 16.50%]) | Index Starting Level × (1 - [14.50% - 16.50%]) | TBD | 52523J248 | US52523J2481 | ||||||

S&P 500® Index (Asymmetric Barriers) | SPX | Index Starting Level × (1+ [17.50% - 19.50%]) | Index Starting Level × (1-10%) | TBD | 52523J255 | US52523J2556 |

| * | The actual Upper Index Barrier, Lower Index Barrier and Index Starting Level applicable to both issuances of Notes will be determined on the Trade Date. |

See “Additional Information about Lehman Brothers Holdings Inc. and the Notes” on page 2. The Notes offered will have the terms specified in the base prospectus dated May 30, 2006, the MTN prospectus supplement dated May 30, 2006, product supplement no. 1140-I dated May 23, 2008, underlying supplement no. 100 dated January 28, 2008 and this term sheet. See “Key Risks” on page 6, the more detailed “Risk Factors” beginning on page SS-1 of product supplement no. 1140-I for risks related to an investment in the Notes and “Risk Factors” beginning on page US-1 of underlying supplement no. 100 for risks related to the Index.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of the Notes or passed upon the accuracy or the adequacy of this term sheet, the accompanying base prospectus, MTN prospectus supplement, product supplement no. 1140-I, underlying supplement no. 100 or any other related prospectus supplements, or any other relevant terms supplement. Any representation to the contrary is a criminal offense. The Notes are not deposit liabilities of Lehman Brothers Holdings Inc. and are not FDIC-insured.

| Price to Public | Underwriting Discount | Proceeds to Us | ||||||||||

| Offering of Notes | Per Note | Total | Per Note | Total | Per Note | Total | ||||||

S&P 500® Index | $10.00 | $0.125 | $9.875 | |||||||||

S&P 500® Index (Asymmetric Barriers) | $10.00 | $0.125 | $9.875 | |||||||||

UBS Financial Services Inc. | Lehman Brothers Inc. |

Lehman Brothers Holdings Inc. has filed a registration statement (including a base prospectus) with the U.S. Securities and Exchange Commission, or SEC, for this offering. Before you invest, you should read this term sheet together with the base prospectus, as supplemented by the MTN prospectus supplement relating to our Series I medium-term notes of which the Notes are a part, and the more detailed information contained in product supplement no. 1140-I (which supplements the description of the general terms of the Notes) and underlying supplement no. 100 (which describes the Index, including risk factors specific to it). Buyers should rely upon the base prospectus, the MTN prospectus supplement, product supplement no. 1140-I, underlying supplement no. 100, this term sheet, any other relevant terms supplement and any other relevant free writing prospectus for complete details. To the extent that there are any inconsistencies among the documents listed below, this term sheet shall supersede product supplement no. 1140-I, which shall, likewise, supersede the base prospectus and the MTN prospectus supplement. You should carefully consider, among other things, the matters set forth in “Risk Factors” in the accompanying product supplement no. 1140-I and “Risk Factors” in the accompanying underlying supplement no. 100, as the Notes involve risks not associated with conventional debt securities. We urge you to consult your investment, legal, tax, accounting and other advisors before you invest in the Notes. You may get these documents and other documents Lehman Brothers Holdings Inc. has filed for free by searching the SEC online database (EDGAR®) atwww.sec.gov, with “Lehman Brothers Holdings Inc.” as a search term or through the links below, or by calling UBS Financial Services Inc. toll-free at 1-877-827-2010 or Lehman Brothers Inc. toll-free at 1-888-603-5847.

You may access these documents on the SEC website at www.sec.gov as follows (or if such address has changed, by reviewing our filings for the relevant date on the SEC website):

| ¨ | Product supplement no. 1140-I dated May 23, 2008:http://www.sec.gov/Archives/edgar/data/806085/000119312508121284/d424b2.htm |

| ¨ | Underlying supplement no. 100 dated January 28, 2008:http://www.sec.gov/Archives/edgar/data/806085/000119312508013371/d424b2.htm |

| ¨ | MTN Prospectus supplement dated May 30, 2006:http://www.sec.gov/Archives/edgar/data/806085/000104746906007785/a2170815z424b2.htm |

| ¨ | Base Prospectus dated May 30, 2006:http://www.sec.gov/Archives/edgar/data/806085/000104746906007771/a2165526zs-3asr.htm |

References to “Lehman Brothers,” “we,” “our” and “us” refer only to Lehman Brothers Holdings Inc. and not to its consolidated subsidiaries. In this document, “Notes” refers collectively to the two separate issuances of the 100% Principal Protection Absolute Return Barrier Notes Linked to the S&P 500® Index that are offered hereby, unless the context otherwise requires.

Investor Suitability

The Notes may be suitable for you if, among other considerations:

| ¨ | You seek an investment that offers 100% principal protection when the Notes are held to maturity |

| ¨ | You believe that the Index will appreciate or depreciate over the Observation Period and that any appreciation or depreciation is unlikely to exceed the applicable Upper Index Barrier or the applicable Lower Index Barrier on any trading day during the Observation Period |

| ¨ | You are willing to hold the Notes to maturity |

| ¨ | You do not seek current income from this investment |

| ¨ | You are willing to invest in securities for which there may be little or no secondary market |

| ¨ | You are willing to forgo dividends paid on the stocks included in the Index |

The Notes may not be suitable for you if, among other considerations:

| ¨ | You believe the Index is likely to appreciate or depreciate over the Observation Period and that any appreciation or depreciation is likely to exceed the applicable Upper Index Barrier or the applicable Lower Index Barrier on any trading day during the Observation Period |

| ¨ | You are unable or unwilling to hold the Notes to maturity |

| ¨ | You prefer the lower risk, and therefore accept the potentially lower returns, of fixed income investments with comparable maturities and credit ratings |

| ¨ | You seek current income from your investments |

| ¨ | You seek an investment for which there will be an active secondary market |

The suitability considerations identified above are not exhaustive. Whether or not the Notes are a suitable investment for you will depend on your individual circumstances, and you should reach an investment decision only after you and your investment, legal, tax, accounting and other advisors have carefully considered the suitability of an investment in the Notes in light of your particular circumstances. You should also review carefully the “Key Risks” on page 5, “Risk Factors” in product supplement no. 1140-I, underlying supplement no. 100 and the MTN prospectus supplement for risks related to an investment in the Notes.

2

Common Terms for Each Offering of the Notes

Issuer | Lehman Brothers Holdings Inc. (A+/A1/AA-)1 | |

Issue Price | $10 per Note | |

Term | 1 year | |

Index | The S&P 500® Index (Ticker: SPX) | |

Principal Protection | 100% if held to maturity | |

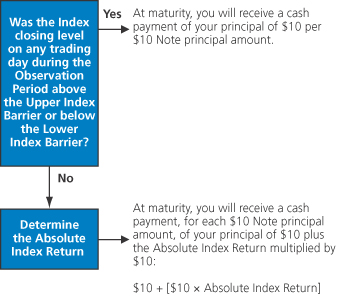

Payment at Maturity (per $10 Note principal amount) | If the Index closing level on any trading day during the Observation Period is not above the Upper Index Barrier or below the Lower Index Barrier, you will receive a cash payment, for each $10 Note principal amount, equal to: | |

$10 + [$10 × Absolute Index Return] | ||

If the Index closing level on any trading day during the Observation Period is above the Upper Index Barrier or below the Lower Index Barrier, you will receive a cash payment of $10 for each $10 Note principal amount. | ||

Absolute Index Return | Absolute value of: Index Ending Level – Index Starting Level | |

Index Starting Level | ||

Index Starting Level | The closing level of the Index on the Trade Date. | |

Index Ending Level | The closing level of the Index on the Final Valuation Date. | |

Observation Period | The period starting on (but excluding) the Trade Date and ending on (and including) the Final Valuation Date. | |

Upper Index Barrier | See Specific Terms for Each Offering of Notes. | |

Lower Index Barrier | See Specific Terms for Each Offering of Notes. | |

Determining Payment at Maturity |

Specific Terms for Each Offering of Notes

| Offering of Notes | Upper Index Barrier* | Lower Index Barrier* | ||

| S&P 500® Index | Index Starting Level × (1 + [14.50% - 16.50%]) | Index Starting Level × (1 - [14.50% - 16.50%]) | ||

| S&P 500® Index (Asymmetric Barriers) | Index Starting Level × (1+ [17.50% - 19.50%]) | Index Starting Level × (1 - 10.00%) | ||

| * | The actual Upper Index Barrier, Lower Index Barrier and Index Starting Level applicable to both issuances of Notes will be determined on the Trade Date. |

1 | Lehman Brothers Holdings Inc. is rated A+ by Standard & Poor’s, A1 by Moody’s and AA- by Fitch. A credit rating reflects the creditworthiness of Lehman Brothers Holdings Inc. and is not a recommendation to buy, sell or hold securities, and it may be subject to revision or withdrawal at any time by the assigning rating organization. Each rating should be evaluated independently of any other rating. The creditworthiness of the issuer does not affect or enhance the likely performance of the investment other than the ability of the issuer to meet its obligations. |

3

Scenario Analysis and Examples at Maturity for the Absolute Return Barrier Notes

The following examples and table illustrate the Payment at Maturity for a $10 Note on a hypothetical offering of the Notes, with the following assumptions:

| Principal Amount: | $10.00 | |

| Index Starting Level: | 1,425.35* | |

| Principal Protection: | 100% at maturity | |

| Term: | 1 year | |

| Upper Index Barrier: | 1,646.28, which is 15.50% (the midpoint of the range of 14.50% and 16.50%) above the Index Starting Level* | |

| Lower Index Barrier: | 1,204.42, which is 15.50% (the midpoint of the range of 14.50% and 16.50%) below the Index Starting Level* | |

| Observation Period: | The period starting on, but excluding, the Trade Date and ending on, and including, the Final Valuation Date. |

| * | The actual Index Starting Level, Upper Index Barrier and Lower Index Barrier will be set on the Trade Date. |

Hypothetical Index Ending Level | Hypothetical Index Return | Hypothetical Performance of the Notes | ||||||||||||

| The Index Never Closes Outside Absolute Return Barrier* | The Index Closes Outside Absolute Return Barrier** | |||||||||||||

| Additional Amount at Maturity ($) | Payment at Maturity ($) | Return on Note (%) | Additional Amount at Maturity ($) | Payment at Maturity ($) | Return on Note (%) | |||||||||

| 2,850.70 | 100.00% | N/A | N/A | N/A | $0.00 | $10.00 | 0.00% | |||||||

| 2,565.63 | 80.00% | N/A | N/A | N/A | $0.00 | $10.00 | 0.00% | |||||||

| 2,280.56 | 60.00% | N/A | N/A | N/A | $0.00 | $10.00 | 0.00% | |||||||

| 1,995.49 | 40.00% | N/A | N/A | N/A | $0.00 | $10.00 | 0.00% | |||||||

| 1,710.42 | 20.00% | N/A | N/A | N/A | $0.00 | $10.00 | 0.00% | |||||||

| 1,646.28 | 15.50% | $1.55 | $11.55 | 15.50% | $0.00 | $10.00 | 0.00% | |||||||

| 1,567.89 | 10.00% | $1.00 | $11.00 | 10.00% | $0.00 | $10.00 | 0.00% | |||||||

| 1,425.35 | 0.00% | $0.00 | $10.00 | 0.00% | $0.00 | $10.00 | 0.00% | |||||||

| 1,282.82 | -10.00% | $1.00 | $11.00 | 10.00% | $0.00 | $10.00 | 0.00% | |||||||

| 1,204.42 | -15.50% | $1.55 | $11.55 | 15.50% | $0.00 | $10.00 | 0.00% | |||||||

| 1,140.28 | -20.00% | N/A | N/A | N/A | $0.00 | $10.00 | 0.00% | |||||||

| 855.21 | -40.00% | N/A | N/A | N/A | $0.00 | $10.00 | 0.00% | |||||||

| 570.14 | -60.00% | N/A | N/A | N/A | $0.00 | $10.00 | 0.00% | |||||||

| 285.07 | -80.00% | N/A | N/A | N/A | $0.00 | $10.00 | 0.00% | |||||||

| 0.00 | -100.00% | N/A | N/A | N/A | $0.00 | $10.00 | 0.00% | |||||||

| * | Calculation assumes that the Index never closes above the Upper Index Barrier or below the Lower Index Barrier on any single trading day during the Observation Period |

| ** | Calculation assumes that the Index closes above the Upper Index Barrier or below the Lower Index Barrier on at least one trading day during the Observation Period |

Example 1: On a trading day during the Observation Period, the Index closes at 1,710.42, which is 20% above the Index Starting Level, and the Index Ending Level is 10% above the Index Starting Level.Since the Index closed at a level above the Upper Index Barrier, you will receive a Payment at Maturity of $10.00 per $10 Note principal amount (a zero return).

Example 2: During the Observation Period, the Index never closes above the Upper Index Barrier or below the Lower Index Barrier and the Index Ending Level is 1,567.89. The Absolute Index Return is 10%, calculated as follows:

The Absolute Value of: (1,567.89 – 1,425.35)/ 1,425.35 = 10%

You will receive a Payment at Maturity of $11.00 per $10 Note principal amount calculated as follows:

$10 + ($10 × 10%) = $11.00

Example 3: On a trading day during the Observation Period, the Index closes at 1,140.28, which is 20% below the Index Starting Level, and the Index Ending Level is 10% below the Index Starting Level. Since the Index closed at a level below the Lower Index Barrier, you will receive a Payment at Maturity of $10.00 per $10 Note principal amount (a zero return).

Example 4: During the Observation Period, the Index never closes above the Upper Index Barrier or below the Lower Index Barrier and the Index Ending Level is 10% below the Index Starting Level 1,282.82.The Absolute Index Return is 10%, calculated as follows:

The Absolute Value of: (1,282.82 – 1,425.35)/ 1,425.35 = -10%

You will receive a Payment at Maturity of $11.00 per $10 Note principal amount calculated as follows:

$10 + ($10 × 10%) = $11.00

4

Scenario Analysis and Examples at Maturity for the Absolute Return (Asymmetric Barriers)

The following examples and table illustrate the Payment at Maturity for a $10 Note on a hypothetical offering of the Notes, with the following assumptions:

| Principal Amount: | $10.00 | |

| Index Starting Level: | 1,425.35* | |

| Principal Protection: | 100% at maturity | |

| Term: | 1 year | |

| Upper Index Barrier: | 1,689.04, which is 18.50% (the midpoint of the range of 17.50% and 19.50%) above the Index Starting Level* | |

| Lower Index Barrier: | 1,282.82, which is 10.00% below the Index Starting Level | |

| Observation Period: | The period starting on, but excluding, the Trade Date and ending on, and including, the Final Valuation Date. |

| * | The actual Index Starting Level, Upper Index Barrier and Lower Index Barrier will be set on the Trade Date. |

Hypothetical Ending Level | Hypothetical Index Return | Hypothetical Performance of the Notes | ||||||||||||

| The Index Never Closes Outside Absolute Return Barrier* | The Index Closes Outside Absolute Return Barrier** | |||||||||||||

| Additional Amount at Maturity ($) | Payment at Maturity ($) | Return on Note (%) | Additional Amount at Maturity ($) | Payment at Maturity ($) | Return on Note (%) | |||||||||

| 2,850.70 | 100.00% | N/A | N/A | 0.00% | $0.00 | $10.00 | 0.00% | |||||||

| 2,565.63 | 80.00% | N/A | N/A | 0.00% | $0.00 | $10.00 | 0.00% | |||||||

| 2,280.56 | 60.00% | N/A | N/A | 0.00% | $0.00 | $10.00 | 0.00% | |||||||

| 1,995.49 | 40.00% | N/A | N/A | 0.00% | $0.00 | $10.00 | 0.00% | |||||||

| 1,852.96 | 30.00% | N/A | N/A | 0.00% | $0.00 | $10.00 | 0.00% | |||||||

| 1,710.42 | 20.00% | N/A | N/A | 0.00% | $0.00 | $10.00 | 0.00% | |||||||

| 1,689.04 | 18.50% | $1.85 | $11.85 | 18.50% | $0.00 | $10.00 | 0.00% | |||||||

| 1,567.89 | 10.00% | $1.00 | $11.00 | 10.00% | $0.00 | $10.00 | 0.00% | |||||||

| 1,496.62 | 5.00% | $0.50 | $10.50 | 5.00% | $0.00 | $10.00 | 0.00% | |||||||

| 1,425.35 | 0.00% | $0.00 | $10.00 | 0.00% | $0.00 | $10.00 | 0.00% | |||||||

| 1,354.08 | -5.00% | $0.50 | $10.50 | 5.00% | $0.00 | $10.00 | 0.00% | |||||||

| 1,282.82 | -10.00% | $1.00 | $11.00 | 10.00% | $0.00 | $10.00 | 0.00% | |||||||

| 1,140.28 | -20.00% | N/A | N/A | 0.00% | $0.00 | $10.00 | 0.00% | |||||||

| 997.75 | -30.00% | N/A | N/A | 0.00% | $0.00 | $10.00 | 0.00% | |||||||

| 855.21 | -40.00% | N/A | N/A | 0.00% | $0.00 | $10.00 | 0.00% | |||||||

| 684.17 | -52.00% | N/A | N/A | 0.00% | $0.00 | $10.00 | 0.00% | |||||||

| * | Calculation assumes that the Index never closes above the Upper Index Barrier or below the Lower Index Barrier on any single trading day during the Observation Period |

| ** | Calculation assumes that the Index closes above the Upper Index Barrier or below the Lower Index Barrier on at least one trading day during the Observation Period |

Example 1: On a trading day during the Observation Period, the Index closes at 1,710.42 which is 20% above the Index Starting Level, and the Index Ending Level is 10% above the Index Starting Level.Since the Index closed at a level above the Upper Index Barrier, you will receive a Payment at Maturity of $10.00 per $10 Note principal amount (a zero return).

Example 2: During the Observation Period, the Index never closes above the Upper Index Barrier or below the Lower Index Barrier and the Index Ending Level is 1,567.89.The Absolute Index Return is 10.00%, calculated as follows:

The Absolute Value of: (1,567.89 – 1,425.35)/ 1,425.35 = 10%

You will receive a Payment at Maturity of $11.00 per $10 Note principal amount calculated as follows:

$10 + ($10 × 10%) = $11.00

Example 3: On a trading day during the Observation Period, the Index closes at 1,140.28, which is 20% below the Index Starting Level, and the Index Ending Level is 10% below the Index Starting Level. Since the Index closed at a level below the Lower Index Barrier, you will receive a Payment at Maturity of $10.00 per $10 Note principal amount (a zero return).

Example 4: During the Observation Period, the Index never closes above the Upper Index Barrier or below the Lower Index Barrier and the Index Ending Level is 1,354.08.The Absolute Index Return is 5% calculated as follows:

The Absolute Value of: (1,354.08 – 1,425.35)/ 1,425.35 = -5%

You will receive a Payment at Maturity of $10.50 per $10 Note principal amount calculated as follows:

$10 + ($10 × 5%) = $10.50

5

Key Risks

An investment in the Notes involves significant risks not associated with an investment in conventional floating rate or fixed rate medium-term notes. Some of these risks are summarized below and are explained in more detail in the “Risk Factors” section of the accompanying product supplement no. 1140-I and in the “Risk Factors” section of the accompanying underlying supplement no. 100, which you are urged to read. You should reach an investment decision only after you have carefully considered with your advisors the suitability of an investment in the Notes in light of your particular circumstances. Investing in the Notes is not equivalent to investing directly in any of the stocks included in the Index.

| ¨ | No Principal Protection Unless You Hold the Notes To Maturity: The Notes are not designed to be short-term trading instruments. You will receive at least the minimum payment of 100% of the principal amount of your Notes if you hold your Notes to maturity. If you sell your Notes in the secondary market prior to maturity, you will not receive principal protection. YOU SHOULD BE WILLING TO HOLD YOUR NOTES TO MATURITY. |

| ¨ | Market Risk: Amounts payable on the Notes and their market value will depend on the performance of the Index and will depend on where the Index closes on any single trading day during the Observation Period. YOU WILL RECEIVE NO MORE THAN THE FULL PRINCIPAL AMOUNT OF YOUR NOTES AT MATURITY IF THE INDEX CLOSES EITHER ABOVE THE APPLICABLE UPPER INDEX BARRIER OR BELOW THE APPLICABLE LOWER INDEX BARRIER DURING THE OBSERVATION PERIOD. |

| ¨ | The Notes Might Not Pay More Than the Principal Amount: You may receive a lower Payment at Maturity than you would have received if you had invested in any of the stocks underlying the Index or contracts related to the Index. If the Index Ending Level is above the Index Starting Level but the Index closes above the applicable Upper Index Barrier or below the applicable Lower Index Barrier on any trading day during the Observation Period, you will receive only the principal amount of your Notes. |

| ¨ | The Upper Index Barrier and Lower Index Barrier Limit Your Potential Return: The appreciation potential of the Notes is limited to the applicable Upper Index Barrier, if the Index appreciates, and to the applicable Lower Index Barrier, if the Index depreciates, regardless of the performance of the Index. |

| ¨ | No Interest or Dividend Payments or Voting Rights: As a holder of the Notes, you will not receive interest payments, and you will not have voting rights or rights to receive cash dividends or other distributions or other rights that holders of stocks underlying the Index would have. |

| ¨ | Certain Built-in Costs are Likely to Adversely Affect the Value of the Notes Prior to Maturity: While the Payment at Maturity described in this term sheet is based on the full principal amount of your Notes, the original issue price of the Notes includes the agents’ commission and the cost of hedging our obligations under the Notes through one or more of our affiliates, which includes our affiliates’ expected cost of providing such hedge as well as the profit our affiliates expect to realize in consideration for assuming the risks inherent in providing such hedge. As a result, the price, at which Lehman Brothers Inc. will be willing to purchase Notes from you in secondary market transactions, if at all, will likely be lower than the original issue price and any sale prior to the Maturity Date could result in a substantial loss to you. The Notes are not designed to be short-term trading instruments. YOU SHOULD BE WILLING TO HOLD YOUR NOTES TO MATURITY. |

| ¨ | Dealer Incentives: We, our affiliates and agents, and UBS Financial Services Inc. and its affiliates, act in various capacities with respect to the Notes. Lehman Brothers Inc. and other of our affiliates may act as principals, agents or dealers in connection with the Notes. Such affiliates, including the sales representatives, will derive compensation from the distribution of the Notes and such compensation may serve as an incentive to sell the Notes instead of other investments. We will pay compensation of $0.125 per $10 Note principal amount to the principals, agents and dealers in connection with the distribution of the Notes. |

| ¨ | Lack of Liquidity: The Notes will not be listed on any securities exchange. Lehman Brothers Inc. intends to offer to purchase the Notes in the secondary market but is not required to do so and may cease any such market making activities at any time. Even if there is a secondary market, it may not provide enough liquidity to allow you to trade or sell the Notes easily. Because other dealers are not likely to make a secondary market for the Notes, the price at which you may be able to trade your Notes is likely to depend on the price, if any, at which Lehman Brothers Inc. is willing to buy the Notes. If you are an employee of Lehman Brothers Holdings Inc. or one of our affiliates, you may not be able to purchase the Notes from us and your ability to sell or trade the Notes in the secondary market may be limited. |

| ¨ | Potential Conflicts: We and our affiliates play a variety of roles in connection with the issuance of the Notes, including acting as calculation agent and hedging our obligations under the Notes. In performing these duties, the economic interests of the calculation agent and other affiliates of ours are potentially adverse to your interests as an investor in the Notes. |

¨ | We are One of the Companies that Make up the S&P 500® Index: We are one of the companies that make up the S&P 500® Index. We will not have any obligation to consider your interests as a holder of the Notes in taking any corporate action that might affect the level of the S&P 500® Index and the value of the Notes. |

| ¨ | We and Our Affiliates and Agents May Publish Research, Express Opinions or Provide Recommendations that are Inconsistent with Investing in or Holding the Notes. Any Such Research, Opinions or Recommendations Could Affect the Level of the Index or the Value of the Notes: We, our affiliates and agents publish research from time to time on financial markets and other matters that may influence the value of the Notes, or express opinions or provide recommendations that are inconsistent with purchasing or holding the Notes. We, our affiliates and agents may publish or may have published research or other opinions that are inconsistent with the investment view implicit in the Notes. Any research, opinions or recommendations expressed by us, our affiliates or agents may not be consistent with each other and may be modified from time to time without notice. Additionally, UBS Financial Services Inc. and its affiliates may publish, or may have published, research or other opinions that are inconsistent with purchasing or holding the Notes. You should make your own independent investigation of the merits of investing in the Notes. |

| ¨ | Many Economic and Market Factors Will Impact the Value of the Notes: In addition to the level of the Index on any day, the value of the Notes will be affected by a number of economic and market factors over which we have no control and that cannot |

6

readily be foreseen. These factors may include, but are not limited to, economic events, changes in monetary policy, inflation, interest rate volatility, supply and demand for the Notes, market expectations, political, legislative, accounting, tax and other regulatory events, and financial events may either offset or magnify each other and which are described in more detail in product supplement no. 1140-I. |

| ¨ | Uncertain Tax Treatment: Significant aspects of the tax treatment of the Notes are uncertain. You should consult your own tax advisor about your own tax situation before investing in the Notes. |

| ¨ | Credit of Issuer: An investment in the Notes will be subject to the credit risk of Lehman Brothers Holdings Inc., and the actual and perceived creditworthiness of Lehman Brothers Holdings Inc. may affect the market value of the Notes. |

What are the tax consequences of the Notes?

Lehman Brothers Holdings Inc. intends to treat, and by purchasing a Note, for all tax purposes, you agree to treat, a Note as a debt instrument that is a “short-term obligation” for U.S. federal income tax purposes. Subject to certain limitations, and based on certain factual representations received from us, in the opinion of Sidley AustinLLP, the Notes will be treated for U.S. federal income tax purposes as debt instruments that constitute “short-term obligations” for U.S. federal income tax purposes.

No statutory, judicial or administrative authority directly addresses the treatment of the Notes or instruments similar thereto for U.S. federal income tax purposes and no ruling will be requested from the Internal Revenue Service with respect to the Notes. As a result, certain aspects of the U.S. federal income tax consequences of an investment in the Notes are uncertain. Any differing treatment could affect the amount, timing and character of income with respect to the Notes.

In general, pursuant to the short-term debt rules, you will be taxed on discount on the Notes. Individuals and certain other cash method holders of the Notes generally are not required to include accrued discount in their income currently unless they elect to do so. Holders that report income for U.S. federal income tax purposes on the accrual method and certain other holders are generally required to accrue discount on the Notes (as ordinary income) on a straight-line basis, unless an election is made to accrue the discount according to a constant yield method based on daily compounding. If a holder is not required, and does not elect, to include discount in income currently, any gain a holder realizes on the sale, exchange or retirement of a Note will generally be ordinary income to the extent of the discount accrued by the holder through the date of sale, exchange or retirement.

Because the amount payable upon maturity of the Notes is not fixed, it is not clear to what extent holders generally required to accrue discount under the short-term debt rules would be required to accrue income with respect to the Notes or the extent to which any gain realized by holders on the sale, exchange or maturity of the Notes would be treated as capital gain or ordinary interest income. Gain realized by a holder who has held the Notes during their entire term to maturity is likely to be treated as ordinary interest income. Any loss realized by such holder upon maturity would likely be treated as capital loss, except possibly to the extent of amounts, if any, previously included in income. You should consult your tax advisors regarding the proper treatment of amounts paid in respect of the Notes.

If you do not elect to currently include accrued discount in income you may be required to defer deductions for a portion of your interest expense with respect to any indebtedness attributable to the Notes.

See “Certain U.S. Federal Income Tax Consequences” in the accompanying product supplement no. 1140-I.

The S&P 500® Index

The S&P 500® Index is published by Standard & Poor’s (“S&P”), a division of The McGraw-Hill Companies, Inc. As discussed more fully in underlying supplement no. 100 under the heading “The S&P 500® Index”, the S&P 500® Index is intended to provide a performance benchmark for the U.S. equity markets. The calculation of the value of the S&P 500® Index is based on the relative value of the aggregate market value of the common stocks of 500 companies as of a particular time compared to the aggregate average market value of the common stocks of 500 similar companies during the base period of the years 1941 through 1943. Ten main groups of companies comprising the S&P 500® Index, along with the number of companies included in each group as of April 30, 2008 are indicated below: Consumer Discretionary (86); Consumer Staples (40); Energy (36); Financials (92); Health Care (51); Industrials (56); Information Technology (71); Materials (28); Telecommunications Services (9); and Utilities (31).

You can obtain the level of the S&P 500® Index at any time from the Bloomberg Financial Markets page “SPX <Index> <GO>“ or from the S&P website at www.standardandpoors.com.

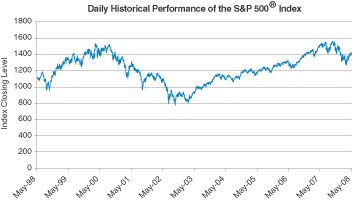

The graph below illustrates the daily performance of the S&P 500® Index from May 15, 1998 to May 16, 2008. The historical levels of the S&P 500® Index should not be taken as an indication of future performance.

Source: Bloomberg L.P.

The S&P 500® Index closing level on May 16, 2008 was 1,425.35.

The information on the S&P 500® Index provided in this document should be read together with the discussion under the heading “The S&P 500® Index” beginning on page US-3 of underlying supplement no. 100. Information contained in the S&P website referenced above is not incorporated by reference in, and should not be considered a part of, this term sheet.

7

Supplemental Plan of Distribution

We will agree to sell to UBS Financial Services Inc. and Lehman Brothers Inc. (together, the “Agents”), and the Agents will agree to purchase, all of the Notes at the price indicated on the cover of the pricing supplement, the document that will be filed pursuant to Rule 424(b) and will contain the final pricing terms of the Notes. UBS Financial Services Inc. may allow a concession not in excess of the underwriting discount set forth on the cover of the pricing supplement to its affiliates.

We have agreed to indemnify the Agents against liabilities, including liabilities under the Securities Act of 1933, as amended, or to contribute to payments that the Agents may be required to make relating to these liabilities as described in the MTN prospectus supplement and the base prospectus. We have agreed that UBS Financial Services Inc. may sell all or a part of the Notes that it purchases from us to its affiliates at the price that will be indicated on the cover of the pricing supplement that will be available in connection with the sales of the Notes.

Subject to regulatory constraints, Lehman Brothers Inc. has agreed to use reasonable efforts to make a market in the Notes for so long as the Notes are outstanding.

We or our affiliate will enter into swap agreements or related hedge transactions with one of our other affiliates or unaffiliated counterparties in connection with the sale of the Notes, and the Agents and/or an affiliate may earn additional income as a result of payments pursuant to the swap or related hedge transactions.

8