Filed Pursuant to Rule 433

Registration Statement No. 333-134553

Structured Investments

Structures at a Glance

at lehman Brothers Structured Investments,

we build well-crafted investment solutions

that enable you to optimize the approach you

use to manage your investment strategies.

every investment we construct incorporates

the knowledge, creativity, expertise, and wealth

management insights of lehman Brothers, a

leader in the global capital markets.

Common Terms And Definitions

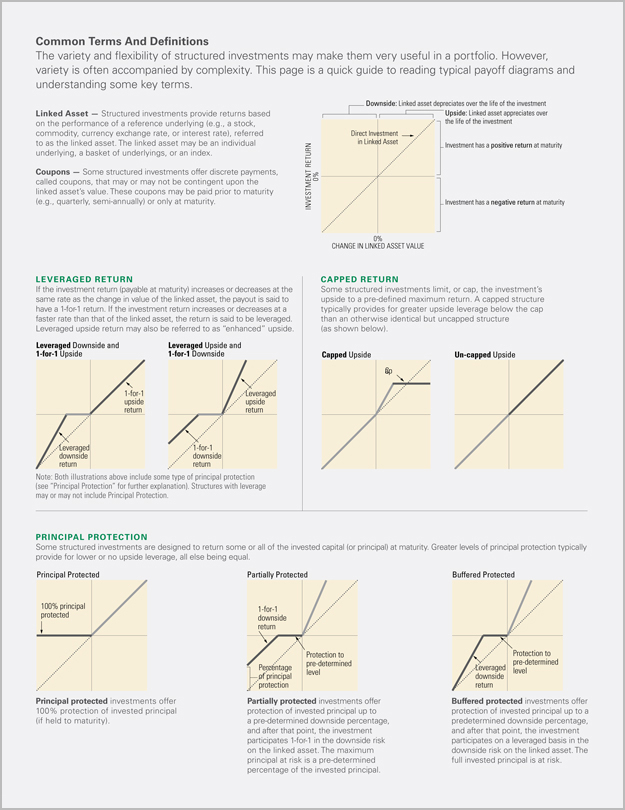

The variety and flexibility of structured investments may make them very useful in a portfolio. However, variety is often accompanied by complexity. This page is a quick guide to reading typical payoff diagrams and understanding some key terms.

Linked Asset — Structured investments provide returns based on the performance of a reference underlying (e.g., a stock, commodity, currency exchange rate, or interest rate), referred to as the linked asset. The linked asset may be an individual underlying, a basket of underlyings, or an index.

Coupons — Some structured investments offer discrete payments, called coupons, that may or may not be contingent upon the linked asset’s value. These coupons may be paid prior to maturity (e.g., quarterly, semi-annually) or only at maturity.

Downside: Linked asset depreciates over the life of the investment Upside: Linked asset appreciates over the life of the investment Direct Investment in Linked Asset Investment has a positive return at maturity RETURN

INVESTMENT0%

Investment has a negative return at maturity

0%

CHANGE IN LINKED ASSET VALUE

LEVERAGED RETURN

If the investment return (payable at maturity) increases or decreases at the same rate as the change in value of the linked asset, the payout is said to have a 1-for-1 return. If the investment return increases or decreases at a faster rate than that of the linked asset, the return is said to be leveraged. Leveraged upside return may also be referred to as “enhanced” upside.

Leveraged Downside and Leveraged Upside and 1-for-1 Upside 1-for-1 Downside

1-for-1 Leveraged upside upside return return

Leveraged 1-for-1 downside downside return return

Note: Both illustrations above include some type of principal protection (see “Principal Protection” for further explanation). Structures with leverage may or may not include Principal Protection.

CAPPED RETURN

Some structured investments limit, or cap, the investment’s upside to a pre-defined maximum return. A capped structure typically provides for greater upside leverage below the cap than an otherwise identical but uncapped structure (as shown below).

Capped Upside Un-capped Upside

Cap

PRINCIPAL PROTECTION

Some structured investments are designed to return some or all of the invested capital (or principal) at maturity. Greater levels of principal protection typically provide for lower or no upside leverage, all else being equal.

Principal Protected

100% principal protected

Principal protected investments offer 100% protection of invested principal (if held to maturity).

Partially Protected

1-for-1 downside return

Protection to pre-determined Percentage level of principal protection

Partially protected investments offer protection of invested principal up to a pre-determined downside percentage, and after that point, the investment participates 1-for-1 in the downside risk on the linked asset. The maximum principal at risk is a pre-determined percentage of the invested principal.

Buffered Protected

Protection to pre-determined Leveraged level downside return

Buffered protected investments offer protection of invested principal up to a predetermined downside percentage, and after that point, the investment participates on a leveraged basis in the downside risk on the linked asset. The full invested principal is at risk.

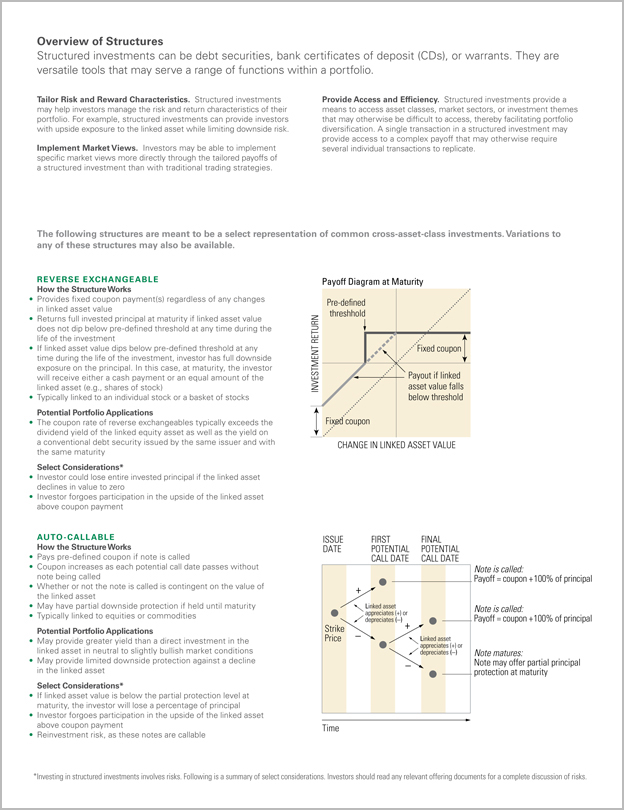

Overview of Structures

Structured investments can be debt securities, bank certificates of deposit (CDs), or warrants. They are

versatile tools that may serve a range of functions within a portfolio.

Tailor Risk and Reward Characteristics. Structured investments

may help investors manage the risk and return characteristics of their

portfolio. For example, structured investments can provide investors

with upside exposure to the linked asset while limiting downside risk.

Implement Market Views. Investors may be able to implement

specific market views more directly through the tailored payoffs of

a structured investment than with traditional trading strategies.

Provide Access and Efficiency. Structured investments provide a

means to access asset classes, market sectors, or investment themes

that may otherwise be difficult to access, thereby facilitating portfolio

diversification. A single transaction in a structured investment may

provide access to a complex payoff that may otherwise require

several individual transactions to replicate.

The following structures are meant to be a select representation of common cross-asset-class investments. Variations to

any of these structures may also be available.

REVERSE exchangeaBLE

How the Structure Works

Provides fixed coupon payment(s) regardless of any changes

in linked asset value

• Returns full invested principal at maturity if linked asset value

does not dip below pre-defined threshold at any time during the

life of the investment

• If linked asset value dips below pre-defined threshold at any

time during the life of the investment, investor has full downside

exposure on the principal. In this case, at maturity, the investor

will receive either a cash payment or an equal amount of the

linked asset (e.g., shares of stock)

• Typically linked to an individual stock or a basket of stocks

Potential Portfolio Applications

• The coupon rate of reverse exchangeables typically exceeds the

dividend yield of the linked equity asset as well as the yield on

a conventional debt security issued by the same issuer and with

the same maturity

Select Considerations*

• Investor could lose entire invested principal if the linked asset

declines in value to zero

• Investor forgoes participation in the upside of the linked asset

above coupon payment

Payoff Diagram at Maturity

Payout if linked

asset value falls

below threshold

Fixed coupon

Pre-defined

threshhold

Fixed coupon

INVESTMENT RETURN

CHANGE IN LINKED ASSET VALUE

Auto-Callable

How the Structure Works

• Pays pre-defined coupon if note is called

• Coupon increases as each potential call date passes without

note being called

• Whether or not the note is called is contingent on the value of

the linked asset

• May have partial downside protection if held until maturity

• Typically linked to equities or commodities

Potential Portfolio Applications

• May provide greater yield than a direct investment in the

linked asset in neutral to slightly bullish market conditions

• May provide limited downside protection against a decline

in the linked asset

Select Considerations*

• If linked asset value is below the partial protection level at

maturity, the investor will lose a percentage of principal

• Investor forgoes participation in the upside of the linked asset

above coupon payment

• Reinvestment risk, as these notes are callable

ISSUE

DATE

FIRST

POTENTIAL

CALL DATE

FINAL

POTENTIAL

CALL DATE

Strike

Price

Note is called:

Payoff = coupon + 100% of principal

Note is called:

Payoff = coupon + 100% of principal

–

–

+

+

Note matures:

Note may offer partial principal

protection at maturity

Linked asset

appreciates (+) or

depreciates (–)

Linked asset

appreciates (+) or

depreciates (–)

Time

* Investing in structured investments involves risks. Following is a summary of select considerations. Investors should read any relevant offering documents for a complete discussion of risks.

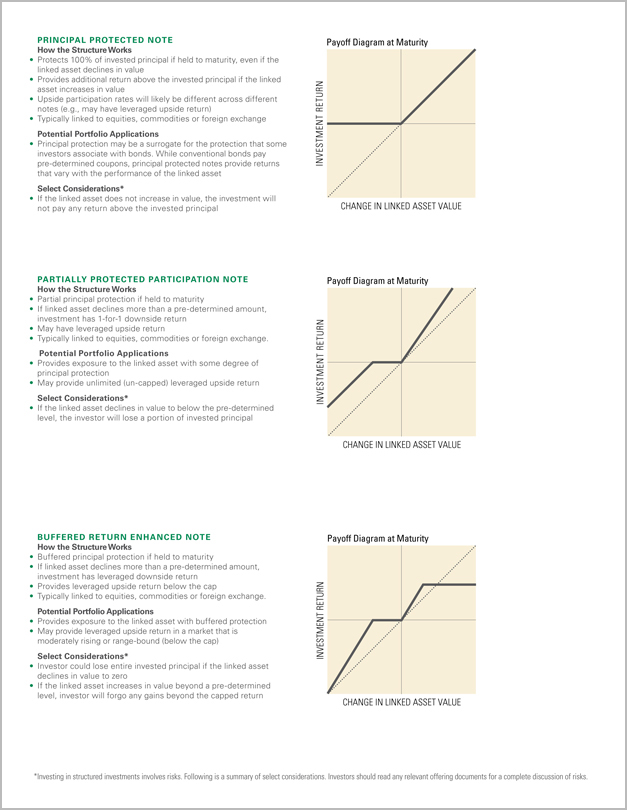

Principal Protected Note

How the Structure Works

• Protects 100% of invested principal if held to maturity, even if the

linked asset declines in value

• Provides additional return above the invested principal if the linked

asset increases in value

• Upside participation rates will likely be different across different

notes (e.g., may have leveraged upside return)

• Typically linked to equities, commodities or foreign exchange

Potential Portfolio Applications

• Principal protection may be a surrogate for the protection that some

investors associate with bonds. While conventional bonds pay

pre-determined coupons, principal protected notes provide returns

that vary with the performance of the linked asset

Select Considerations*

• If the linked asset does not increase in value, the investment will

not pay any return above the invested principal

Payoff Diagram at Maturity

CHANGE IN LINKED ASSET VALUE

INVESTMENT RETURN

Partially Protected Participation Note

How the Structure Works

• Partial principal protection if held to maturity

• If linked asset declines more than a pre-determined amount,

investment has 1-for-1 downside return

• May have leveraged upside return

• Typically linked to equities, commodities or foreign exchange.

Potential Portfolio Applications

• Provides exposure to the linked asset with some degree of

principal protection

• May provide unlimited (un-capped) leveraged upside return

Select Considerations*

• If the linked asset declines in value to below the pre-determined

level, the investor will lose a portion of invested principal

Payoff Diagram at Maturity

CHANGE IN LINKED ASSET VALUE

INVESTMENT RETURN

Buffered Return Enhanced Note Payoff Diagram at Maturity

How the Structure Works

• Buffered principal protection if held to maturity

• If linked asset declines more than a pre-determined amount,

investment has leveraged downside return

• Provides leveraged upside return below the cap

• Typically linked to equities, commodities or foreign exchange.

Potential Portfolio Applications

• Provides exposure to the linked asset with buffered protection

• May provide leveraged upside return in a market that is

moderately rising or range-bound (below the cap)

Select Considerations*

• Investor could lose entire invested principal if the linked asset

declines in value to zero

• If the linked asset increases in value beyond a pre-determined

level, investor will forgo any gains beyond the capped return

INVESTMENT RETURN

CHANGE IN LINKED ASSET VALUE

*Investing in structured investments involves risks. Following is a summary of select considerations. Investors should read any relevant offering documents for a complete discussion of risks.

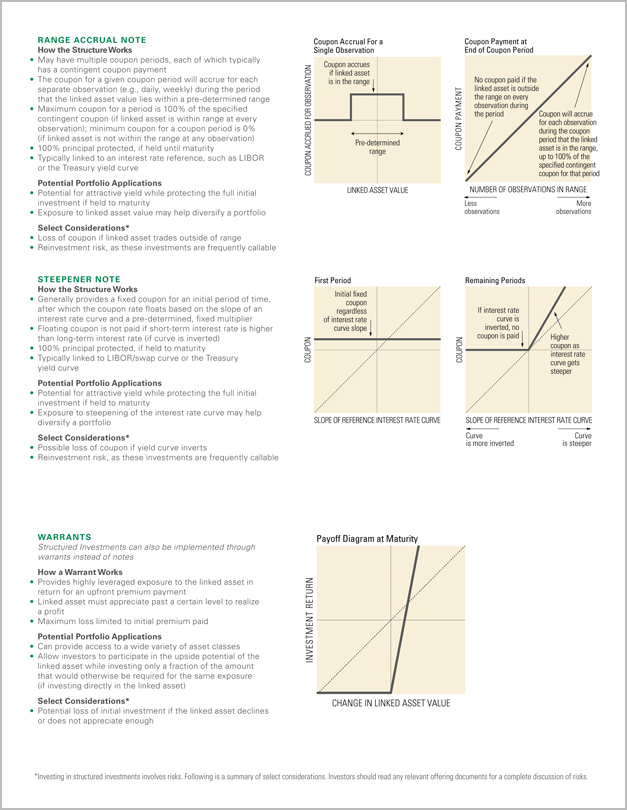

Range accrual Note

How the Structure Works

• May have multiple coupon periods, each of which typically

has a contingent coupon payment

• The coupon for a given coupon period will accrue for each

separate observation (e.g., daily, weekly) during the period

that the linked asset value lies within a pre-determined range

• Maximum coupon for a period is 100% of the specified

contingent coupon (if linked asset is within range at every

observation); minimum coupon for a coupon period is 0%

(if linked asset is not within the range at any observation)

• 100% principal protected, if held until maturity

• Typically linked to an interest rate reference, such as LIBOR

or the Treasury yield curve

Potential Portfolio Applications

• Potential for attractive yield while protecting the full initial

investment if held to maturity

• Exposure to linked asset value may help diversify a portfolio

Select Considerations*

• Loss of coupon if linked asset trades outside of range

• Reinvestment risk, as these investments are frequently callable

Coupon Accrual For a

Single Observation

Coupon accrues

if linked asset

is in the range

Pre-determined

range

LINKED ASSET VALUE

COUPON ACCRUED FOR OBSERVATION

Coupon Payment at

End of Coupon Period

No coupon paid if the

linked asset is outside

the range on every

observation during

the period

Coupon will accrue

for each observation

during the coupon

period that the linked

asset is in the range,

up to 100% of the

specified contingent

coupon for that period

NUMBER OF OBSERVATIONS IN RANGE

Less

observations

More

observations

in range

COUPON PAYMENT

Steepener Note

How the Structure Works

• Generally provides a fixed coupon for an initial period of time,

after which the coupon rate floats based on the slope of an

interest rate curve and a pre-determined, fixed multiplier

• Floating coupon is not paid if short-term interest rate is higher

than long-term interest rate (if curve is inverted)

• 100% principal protected, if held to maturity

• Typically linked to LIBOR/swap curve or the Treasury

yield curve

Potential Portfolio Applications

• Potential for attractive yield while protecting the full initial

investment if held to maturity

• Exposure to steepening of the interest rate curve may help

diversify a portfolio

Select Considerations*

• Possible loss of coupon if yield curve inverts

• Reinvestment risk, as these investments are frequently callable

First Period

Initial fixed

coupon

regardless

of interest rate

curve slope

SLOPE OF REFERENCE INTEREST RATE CURVE

COUPON

First Period

Remaining Periods

If interest rate

curve is

inverted, no

coupon is paid

Higher

coupon as

interest rate

curve gets

steeper

Curve

is more inverted

Curve

is steeper

SLOPE OF REFERENCE INTEREST RATE CURVE

COUPON

Warrants Structured Investments can also be implemented through

warrants instead of notes

How a Warrant Works

• Provides highly leveraged exposure to the linked asset in

return for an upfront premium payment

• Linked asset must appreciate past a certain level to realize

a profit

• Maximum loss limited to initial premium paid

Potential Portfolio Applications

• Can provide access to a wide variety of asset classes

• Allow investors to participate in the upside potential of the

linked asset while investing only a fraction of the amount

that would otherwise be required for the same exposure

(if investing directly in the linked asset)

Select Considerations*

• Potential loss of initial investment if the linked asset declines

or does not appreciate enough

Payoff Diagram at Maturity

INVESTMENT RETURN

INVESTMENT RETURN

* Investing in structured investments involves risks. Following is a summary of select considerations. Investors should read any relevant offering documents for a complete discussion of risks.

Select Risk Considerations*

Principal Risk

If the structured investment does not include principal protection, the

investor may be exposed to all or a portion of the potential downside

risk of the linked asset.

• A principal protected investment does not provide protection on the

invested principal prior to maturity.

Liquidity Risk

• A liquid market for a particular structured investment may not exist

or develop.

• The issuer and underwriter of structured investments are not obligated

to commence or continue any secondary market-making activity and,

if started, may discontinue such activity at any time.

• A lack of liquidity may cause the investor to experience a loss if the

investment is not held to maturity.

Credit Risk

• All payments associated with the structured investment are obligations

of the issuer.

• An investor should be aware of the issuer’s credit rating before

purchasing a structured investment. To the extent that structured

investments are debt of the issuer, investors will be exposed to the

credit of the issuer.

Structure Complexity

• Structured investments may include multiple derivative instruments.

Investors should be aware of all the instruments involved in the structure.

• If you are an advisor, you should be aware of the behavior of each

instrument inherent in a structure and be able to determine if the

structure as a whole is suitable for any particular client.

Price Volatility

• The value of a structured investment at maturity depends on the value

of the linked asset, which may be highly volatile.

• Leverage may magnify the volatility of structured investments and

cause the performance of certain structured investments to experience

more volatility than the linked asset.

Opportunity Cost

• Investors will lose access to invested principal for the term of the

investment.

• Investors may also forgo the return that could have been achieved had

the principal been invested in other fixed income securities.

Tax Considerations

• Tax considerations will vary depending on the type of structured investment.

• Investors should consult their own tax advisor regarding the tax treatment

of structured investments.

For any questions or comments please contact us.

Lehman Brothers Structured Investments

1.212.526.0905

Structured_Investments@lehman.com

* Investing in structured investments involves risks. Above is a summary of select considerations. Investors should read any relevant offering documents for a complete discussion of risks.

Lehman Brothers Holdings Inc. has filed a registration statement (including a prospectus) with the SEC for the offerings to which this communication relates. Before you invest, you

should read the prospectus in that registration statement and other documents Lehman Brothers Holdings Inc. has filed with the SEC for more complete information about the issuer

and these offerings. You may get these documents and other documents Lehman Brothers Holdings Inc. has filed for free by searching the SEC online database (EDGAR®) at www.sec.gov,

with “Lehman Brothers Holdings Inc.” as a search term or by calling Lehman Brothers Inc. toll-free at 1.888.603.5847.

©2008 Lehman Brothers Inc. All rights reserved. Member SIPC. LB17619c5