Exhibit 99.1

Investor Presentation NASDAQ: CVLY As of September 30, 2021

Safe Harbor Notice Regarding Forward Looking Statements This presentation contains forward - looking statements about Codorus Valley Bancorp, Inc . that are intended to be covered by the safe harbor for forward - looking statements provided by the Private Securities Litigation Reform Act of 1995 . Forward - looking statements are not historical facts . These statements can be identified by the use of forward - looking terminology such as “believe,” “expect,” “may,” “will,” “should,” “project,” “plan,” “seek,” “intend,” “anticipate” or similar terminology . Such forward - looking statements include, but are not limited to, discussions of strategy, financial projections and estimates and their underlying assumptions ; statements regarding plans, objectives, goals, expectations or consequences ; and statements about future performance, operations, products and services of Codorus Valley Bancorp, Inc . and its subsidiaries . Note that many factors, some of which are discussed elsewhere in this presentation could affect the future financial results of the Codorus Valley Bancorp, Inc . and its subsidiaries, both individually and collectively, and could cause those results to differ materially from those expressed in the forward - looking statements contained or incorporated by reference in this presentation . In addition to the foregoing, the effect of COVID - 19 and related events, including those described above and those not yet known or knowable, could have a negative effect on the Corporation's business prospects, financial condition and results of operations, as a result of quarantines ; market volatility ; market downturns ; changes in consumer behavior ; business closures ; deterioration in the credit quality of borrowers or the inability of borrowers to satisfy their obligations (and any related forbearances or restructurings that may be implemented) ; changes in the value of collateral securing outstanding loans ; changes in the value of the investment securities portfolio ; effects on key employees, including operational management personnel and those charged with preparing, monitoring and evaluating the Corporation's financial reporting and internal controls ; declines in the demand for loans and other banking services and products ; declines in demand resulting from adverse impacts of the disease on businesses deemed to be "non - essential" by governments ; and Financial Center or office closures and business interruptions . Additional factors that may affect forward - looking statements made in this presentation can be found in Codorus Valley Bancorp, Inc . ’s Quarterly Reports on Forms 10 - Q and its Annual Report on Form 10 - K, as filed with the Securities and Exchange Commission and available on the Corporation’s website at www . peoplesbanknet . com and on the Securities and Exchange Commission’s website at www . sec . gov . We include web addresses here as inactive textual references only . Information on these websites is not part of this presentation . Forward - looking statements in this presentation speak only as of the date of this presentation and Codorus Valley Bancorp, Inc . makes no commitment to revise or update such statements to reflect changes that occur after the date the forward - looking statement was made . 2

3

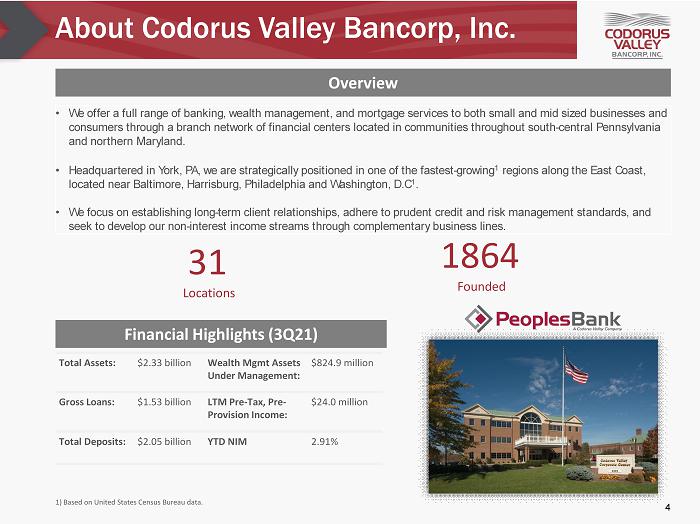

About Codorus Valley Bancorp, Inc. Overview • We offer a full range of banking, wealth management, and mortgage services to both small and mid sized businesses and consumers through a branch network of financial centers located in communities throughout south - central Pennsylvania and northern Maryland. • Headquartered in York, PA, we are strategically positioned in one of the fastest - growing 1 regions along the East Coast, located near Baltimore, Harrisburg, Philadelphia and Washington, D.C 1 . • We focus on establishing long - term client relationships, adhere to prudent credit and risk management standards, and seek to develop our non - interest income streams through complementary business lines. 1) Based on United States Census Bureau data. Total Assets: $2.33 billion Wealth Mgmt Assets Under Management: $824.9 million Gross Loans: $1.53 billion LTM Pre - Tax, Pre - Provision Income: $24.0 million Total Deposits: $2.05 billion YTD NIM 2.91% Financial Highlights (3Q21) 31 Locations 1864 Founded 4

Attractive Footprint & Market Share Source: FDIC Summary of Deposits. Deposit data as of June 30, 2021. 1) Based on United States Census Bureau data. • #2 market position by deposits in York County, PA, with a 14.5% market share (out of 15 banks that report deposit data); #1 market position for banks under $100 billion in assets. • Strategic focus is on maximizing presence in our existing market area while expanding into adjacent and contiguous markets where we can differentiate ourselves from competitors and grow market share. Deposit Market Share by County: June 30, 2021 Market County Share (%) Pennsylvania York 14.5 Lancaster 0.6 Cumberland 0.2 Maryland Baltimore City 0.1 Baltimore County 0.9 Harford 1.7 5

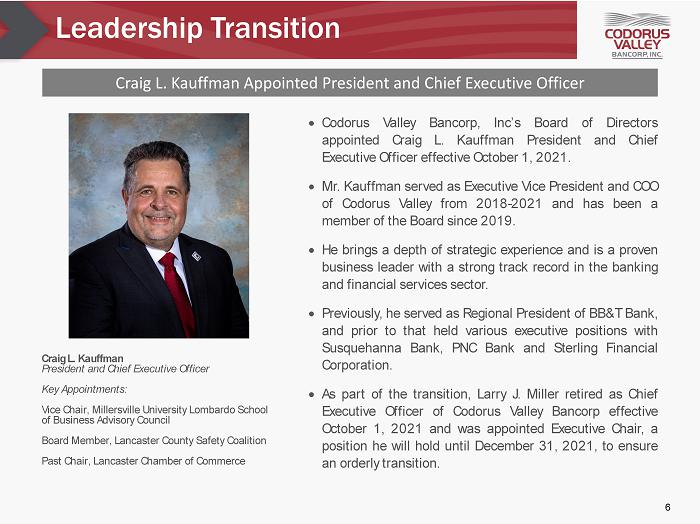

Leadership Transition Codorus Valley Bancorp, Inc’s Board of Directors appointed Craig L . Kauffman President and Chief Executive Officer effective October 1 , 2021 . Mr . Kauffman served as Executive Vice President and COO of Codorus Valley from 2018 - 2021 and has been a member of the Board since 2019 . He brings a depth of strategic experience and is a proven business leader with a strong track record in the banking and financial services sector . Previously, he served as Regional President of BB&T Bank, and prior to that held various executive positions with Susquehanna Bank, PNC Bank and Sterling Financial Corporation . As part of the transition, Larry J . Miller retired as Chief Executive Officer of Codorus Valley Bancorp effective October 1 , 2021 and was appointed Executive Chair, a position he will hold until December 31 , 2021 , to ensure an orderly transition . Craig L . Kauffman President and Chief Executive Officer Key Appointments : Vice Chair, Millersville University Lombardo School of Business Advisory Council Board Member, Lancaster County Safety Coalition Past Chair, Lancaster Chamber of Commerce Craig L. Kauffman Appointed President and Chief Executive Officer 6

Recent Developments • In September 2021, recognized as 2021 Readers’ Choice for Best Mortgage Lender by readers of Hanover Evening Sun. • In September 2021, PeoplesBank received the Outstanding Community Service Award by The Salvation Army York Citadel. • In July 2021, Wealth Management Division recognized as Pohl Consulting and Training, Inc. Top Performer. • In May 2021, r ecognized as 2021 Best of the Best in two categories Best Bank and Best Mortgage Lender by readers of York Daily Record. • In January 2021, r eceived 2020 Laserfiche Run Smarter® Award. • In September 2020, Connections Center was recognized winner in URC’s 6th Annual Unsurpassed Award Winners Competition. 7

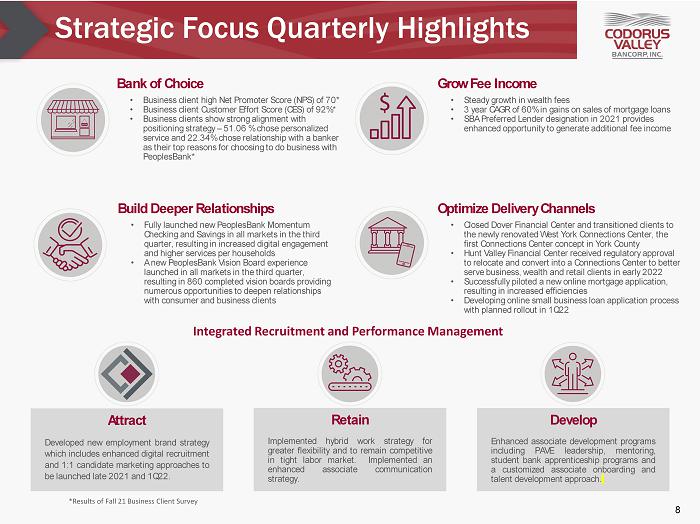

Strategic Focus Quarterly Highlights Attract Developed new employment brand strategy which includes enhanced digital recruitment and 1 : 1 candidate marketing approaches to be launched late 2021 and 1 Q 22 . Retain Implemented hybrid work strategy for greater flexibility and to remain competitive in tight labor market . Implemented an enhanced associate communication strategy . Develop Enhanced associate development programs including PAVE leadership, mentoring, student bank apprenticeship programs and a customized associate onboarding and talent development approach . Build Deeper Relationships • Fully launched new PeoplesBank Momentum Checking and Savings in all markets in the third quarter, resulting in increased digital engagement and higher services per households • A new PeoplesBank Vision Board experience launched in all markets in the third quarter, resulting in 860 completed vision boards providing numerous opportunities to deepen relationships with consumer and business clients Grow Fee Income • Steady growth in wealth fees • 3 year CAGR of 60% in gains on sales of mortgage loans • SBA Preferred Lender designation in 2021 provides enhanced opportunity to generate additional fee income Optimize Delivery Channels • Closed Dover Financial Center and transitioned clients to the newly renovated West York Connections Center, the first Connections Center concept in York County • Hunt Valley Financial Center received regulatory approval to relocate and convert into a Connections Center to better serve business, wealth and retail clients in early 2022 • Successfully piloted a new online mortgage application, resulting in increased efficiencies • Developing online small business loan application process with planned rollout in 1Q22 8 Integrated Recruitment and Performance Management Bank of Choice • Business client high Net Promoter Score (NPS) of 70* • Business client Customer Effort Score (CES) of 92%* • Business clients show strong alignment with positioning strategy -- 51.06 % chose personalized service and 22.34% chose relationship with a banker as their top reasons for choosing to do business with PeoplesBank * *Results of Fall 21 Business Client S urvey

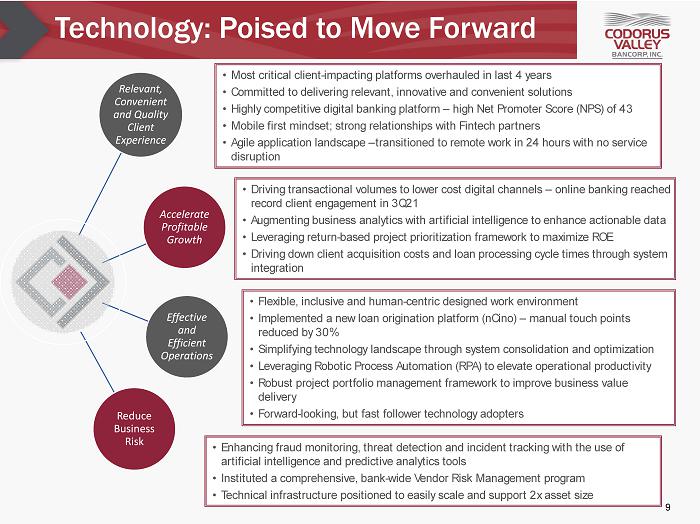

9 Technology: Poised to Move Forward • Most critical client - impacting platforms overhauled in last 4 years • Committed to delivering relevant, innovative and convenient solutions • Highly competitive digital banking platform – high Net Promoter Score (NPS) of 43 • Mobile first mindset; strong relationships with Fintech partners • Agile application landscape – transitioned to remote work in 24 hours with no service disruption • Driving transactional volumes to lower cost digital channels – online banking reached record client engagement in 3Q21 • Augmenting business analytics with artificial intelligence to enhance actionable data • Leveraging return - based project prioritization framework to maximize ROE • Driving down client acquisition costs and loan processing cycle times through system integration • Flexible, inclusive and human - centric designed work environment • Implemented a new loan origination platform ( nCino ) – manual touch points reduced by 30% • Simplifying technology landscape through system consolidation and optimization • Leveraging Robotic Process Automation (RPA) to elevate operational productivity • Robust project portfolio management framework to improve business value delivery • Forward - looking, but fast follower technology adopters • Enhancing fraud monitoring, threat detection and incident tracking with the use of artificial intelligence and predictive analytics tools • Instituted a comprehensive, bank - wide Vendor Risk Management program • Technical infrastructure positioned to easily scale and support 2x asset size Relevant, Convenient and Quality Client Experience Accelerate Profitable Growth Effective and Efficient Operations Reduce Business Risk

Key Technology Partners 10

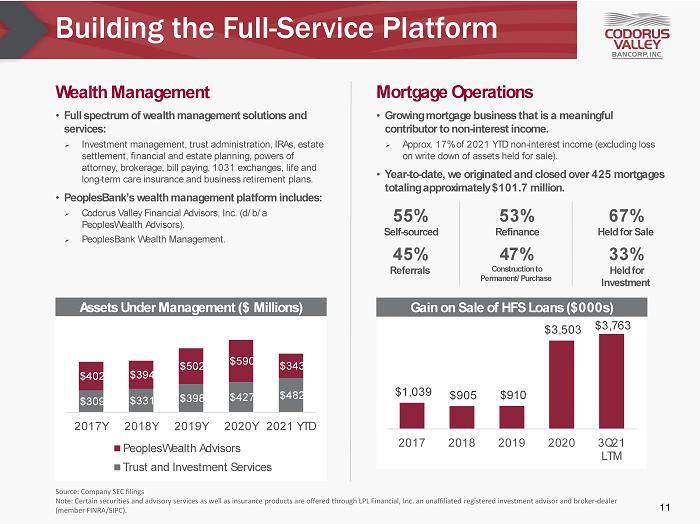

• Full spectrum of wealth management solutions and services: » Investment management, trust administration, IRAs, estate settlement, financial and estate planning, powers of attorney, brokerage, bill paying, 1031 exchanges, life and long - term care insurance and business retirement plans. • PeoplesBank’s wealth management platform includes: » Codorus Valley Financial Advisors, Inc. (d/b/a PeoplesWealth Advisors). » PeoplesBank Wealth Management. Building the Full - Service Platform Assets Under Management ($ Millions) Source: Company SEC filings Note: Certain securities and advisory services as well as insurance products are offered through LPL Financial, Inc. an unaff ili ated registered investment advisor and broker - dealer (member FINRA/SIPC). Gain on Sale of HFS Loans ($000s) • Growing mortgage business that is a meaningful contributor to non - interest income. » Approx. 17% of 2021 YTD non - interest income (excluding loss on write down of assets held for sale). • Year - to - date, we originated and closed over 425 mortgages totaling approximately $101.7 million. Wealth Management Mortgage Operations 11 55% Self - sourced 45% Referrals 47% Construction to Permanent/Purchase 53% Refinance 33% Held for Investment 67% Held for Sale $1,039 $905 $910 $3,503 $3,763 2017 2018 2019 2020 3Q21 LTM $309 $331 $398 $427 $482 $402 $394 $502 $590 $343 2017Y 2018Y 2019Y 2020Y 2021 YTD PeoplesWealth Advisors Trust and Investment Services

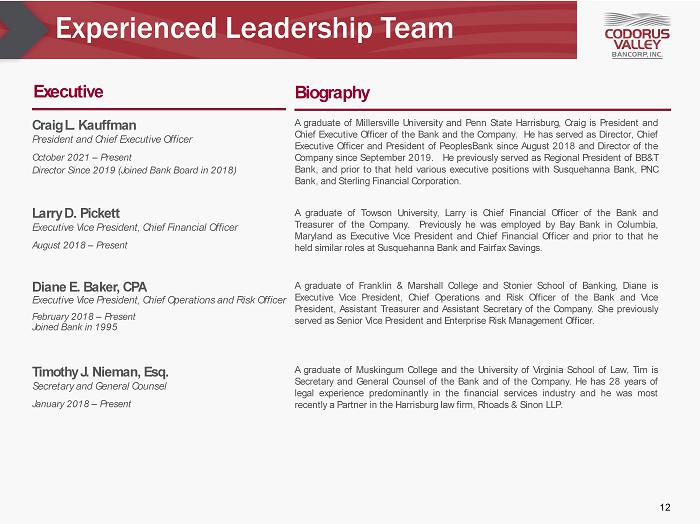

Experienced Leadership Team Craig L . Kauffman President and Chief Executive Officer October 2021 – Present Director Since 2019 (Joined Bank Board in 2018 ) Larry D. Pickett Executive Vice President, Chief Financial Officer August 2018 – Present Diane E. Baker, CPA Executive Vice President, Chief Operations and Risk Officer February 2018 – Present Joined Bank in 1995 Executive Biography Timothy J . Nieman, Esq . Secretary and General Counsel January 2018 – Present 12 A graduate of Millersville University and Penn State Harrisburg, Craig is President and Chief Executive Officer of the Bank and the Company . He has served as Director, Chief Executive Officer and President of PeoplesBank since August 2018 and Director of the Company since September 2019 . He previously served as Regional President of BB&T Bank, and prior to that held various executive positions with Susquehanna Bank, PNC Bank, and Sterling Financial Corporation . A graduate of Towson University, Larry is Chief Financial Officer of the Bank and Treasurer of the Company . Previously he was employed by Bay Bank in Columbia, Maryland as Executive Vice President and Chief Financial Officer and prior to that he held similar roles at Susquehanna Bank and Fairfax Savings . A graduate of Franklin & Marshall College and Stonier School of Banking, Diane is Executive Vice President, Chief Operations and Risk Officer of the Bank and Vice President, Assistant Treasurer and Assistant Secretary of the Company . She previously served as Senior Vice President and Enterprise Risk Management Officer . A graduate of Muskingum College and the University of Virginia School of Law, Tim is Secretary and General Counsel of the Bank and of the Company . He has 28 years of legal experience predominantly in the financial services industry and he was most recently a Partner in the Harrisburg law firm, Rhoads & Sinon LLP .

Experienced Board of Directors Larry J . Miller Executive Chairman of the Board • Will continue in his role as a Director and as Executive Chair of the Bank and the Company until December 31 , 2021 . • President and Chief Executive Officer of the Company from 1986 to October 2021 and Chief Executive Officer of the Bank from 1980 to 2016 . Cynthia A. Dotzel, CPA Vice Chairman and Lead Director – Since 2021 • Practicing CPA with Dotzel & Company, Inc . Chair of The York Water Company (NASDAQ : YORW) board . Former board member of Waypoint Financial Corp . , Waypoint Bank, York Financial Corp . and York Federal Savings & Loan . Brian D. Brunner Director – Since 2015 • Division President of Account and Item Processing Sales for Fiserv, Inc . , a leading provider of financial services technology and one of FORTUNE magazine’s World’s Most Admired Companies . • Former President and Chief Executive Officer of The York Water Company . Member of The York Water Company board (retired 2021 ) . Jeffrey R . Hines, P . E . Director – Since 2011 • President and Chief Executive Officer of Keller - Brown Insurance Services, a fifth generation, family owned insurance agency located in York County, Pennsylvania . Joined Bank Board in 2019 . Sarah M. Brown Director – Since 2020 John W. Giambalvo, Esq. Director – Since 2017 • President and Chief Executive Officer of Jack Giambalvo Motor Co . with over 20 years of experience in the auto industry . John Rodney Messick Director – Since 2020 • Chief Executive Officer of Homesale Realty Service Group, Inc . , headquartered in Lancaster, Pennsylvania and servicing clients in the Baltimore, South Central Pennsylvania and Southeastern Pennsylvania areas . Joined Bank Board in 2019 . Executive Team Biography 13 Craig L. Kauffman Director – Since 2019 • Appointed President and Chief Executive Officer of the Company effective October 1 , 2021 . • Joined Bank Board in 2018 . Independent Directors Biography

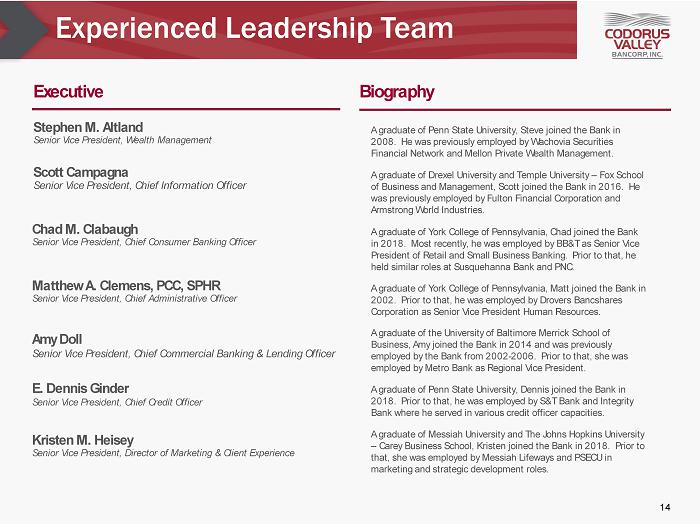

Experienced Leadership Team Amy Doll Senior Vice President, Chief Commercial Banking & Lending Officer Stephen M. Altland Senior Vice President, Wealth Management Matthew A. Clemens, PCC, SPHR Senior Vice President, Chief Administrative Officer Executive Biography E . Dennis Ginder Senior Vice President, Chief Credit Officer Chad M. Clabaugh Senior Vice President, Chief Consumer Banking Officer 14 Kristen M. Heisey Senior Vice President, Director of Marketing & Client Experience Scott Campagna Senior Vice President, Chief Information Officer A graduate of Penn State University, Steve joined the Bank in 2008. He was previously employed by Wachovia Securities Financial Network and Mellon Private Wealth Management. A graduate of Drexel University and Temple University – Fox School of Business and Management, Scott joined the Bank in 2016. He was previously employed by Fulton Financial Corporation and Armstrong World Industries. A graduate of York College of Pennsylvania, Chad joined the Bank in 2018. Most recently, he was employed by BB&T as Senior Vice President of Retail and Small Business Banking. Prior to that, he held similar roles at Susquehanna Bank and PNC. A graduate of York College of Pennsylvania, Matt joined the Bank in 2002. Prior to that, he was employed by Drovers Bancshares Corporation as Senior Vice President Human Resources. A graduate of the University of Baltimore Merrick School of Business, Amy joined the Bank in 2014 and was previously employed by the Bank from 2002 - 2006. Prior to that, she was employed by Metro Bank as Regional Vice President. A graduate of Penn State University, Dennis joined the Bank in 2018. Prior to that, he was employed by S&T Bank and Integrity Bank where he served in various credit officer capacities. A graduate of Messiah University and The Johns Hopkins University – Carey Business School, Kristen joined the Bank in 2018. Prior to that, she was employed by Messiah Lifeways and PSECU in marketing and strategic development roles.

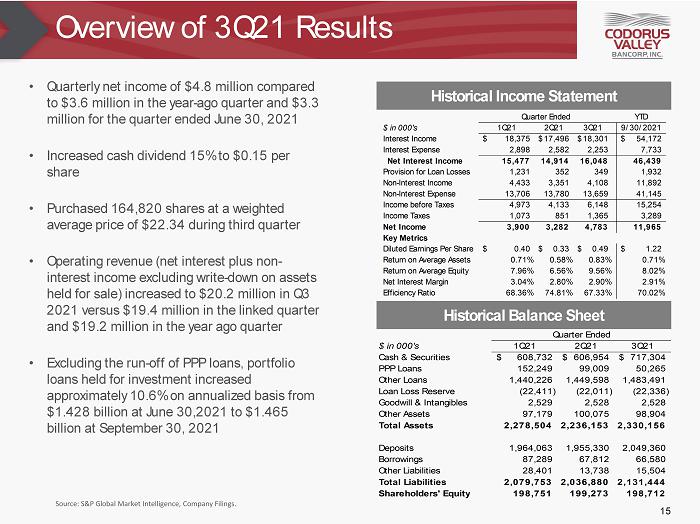

Overview of 3Q21 Results • Quarterly net income of $4.8 million compared to $3.6 million in the year - ago quarter and $3.3 million for the quarter ended June 30, 2021 • Increased cash dividend 15% to $0.15 per share • Purchased 164,820 shares at a weighted average price of $22.34 during third quarter • Operating revenue (net interest plus non - interest income excluding write - down on assets held for sale) increased to $20.2 million in Q3 2021 versus $19.4 million in the linked quarter and $19.2 million in the year ago quarter • Excluding the run - off of PPP loans, portfolio loans held for investment increased approximately 10.6% on annualized basis from $1.428 billion at June 30,2021 to $1.465 billion at September 30, 2021 Source: S&P Global Market Intelligence, Company Filings . Historical Income Statement 15 Historical Balance Sheet YTD $ in 000's 1Q21 2Q21 3Q21 9/30/2021 Interest Income 18,375$ 17,496$ 18,301$ 54,172$ Interest Expense 2,898 2,582 2,253 7,733 Net Interest Income 15,477 14,914 16,048 46,439 Provision for Loan Losses 1,231 352 349 1,932 Non-Interest Income 4,433 3,351 4,108 11,892 Non-Interest Expense 13,706 13,780 13,659 41,145 Income before Taxes 4,973 4,133 6,148 15,254 Income Taxes 1,073 851 1,365 3,289 Net Income 3,900 3,282 4,783 11,965 Key Metrics Diluted Earnings Per Share 0.40$ 0.33$ 0.49$ 1.22$ Return on Average Assets 0.71% 0.58% 0.83% 0.71% Return on Average Equity 7.96% 6.56% 9.56% 8.02% Net Interest Margin 3.04% 2.80% 2.90% 2.91% Efficiency Ratio 68.36% 74.81% 67.33% 70.02% Quarter Ended $ in 000's 1Q21 2Q21 3Q21 Cash & Securities 608,732$ 606,954$ 717,304$ PPP Loans 152,249 99,009 50,265 Other Loans 1,440,226 1,449,598 1,483,491 Loan Loss Reserve (22,411) (22,011) (22,336) Goodwill & Intangibles 2,529 2,528 2,528 Other Assets 97,179 100,075 98,904 Total Assets 2,278,504 2,236,153 2,330,156 Deposits 1,964,063 1,955,330 2,049,360 Borrowings 87,289 67,812 66,580 Other Liabilities 28,401 13,738 15,504 Total Liabilities 2,079,753 2,036,880 2,131,444 Shareholders' Equity 198,751 199,273 198,712 Quarter Ended

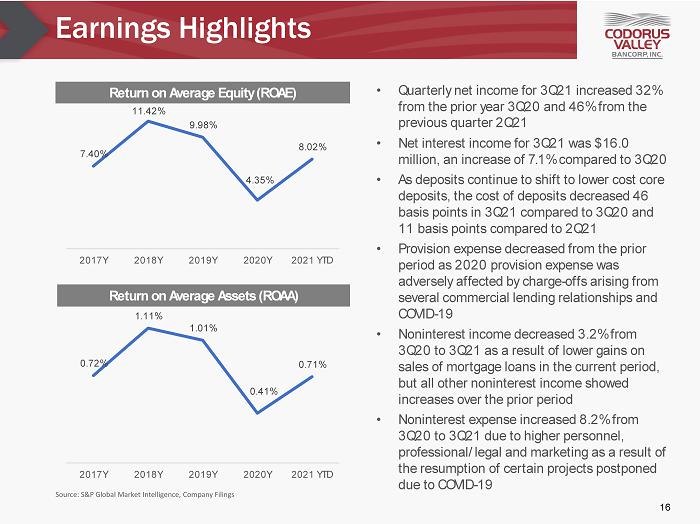

Earnings Highlights Source: S&P Global Market Intelligence, Company Filings • Quarterly net income for 3Q21 increased 32% from the prior year 3Q20 and 46% from the previous quarter 2Q21 • Net interest income for 3Q21 was $16.0 million, an increase of 7.1% compared to 3Q20 • As deposits continue to shift to lower cost core deposits, the cost of deposits decreased 46 basis points in 3Q21 compared to 3Q20 and 11 basis points compared to 2Q21 • Provision expense decreased from the prior period as 2020 provision expense was adversely affected by charge - offs arising from several commercial lending relationships and COVID - 19 • Noninterest income decreased 3.2% from 3Q20 to 3Q21 as a result of lower gains on sales of mortgage loans in the current period, but all other noninterest income showed increases over the prior period • Noninterest expense increased 8.2% from 3Q20 to 3Q21 due to higher personnel, professional/legal and marketing as a result of the resumption of certain projects postponed due to COVID - 19 Return on Average Equity (ROAE) Return on Average Assets (ROAA) 16 7.40% 11.42% 9.98% 4.35% 8.02% 2017Y 2018Y 2019Y 2020Y 2021 YTD 0.72% 1.11% 1.01% 0.41% 0.71% 2017Y 2018Y 2019Y 2020Y 2021 YTD

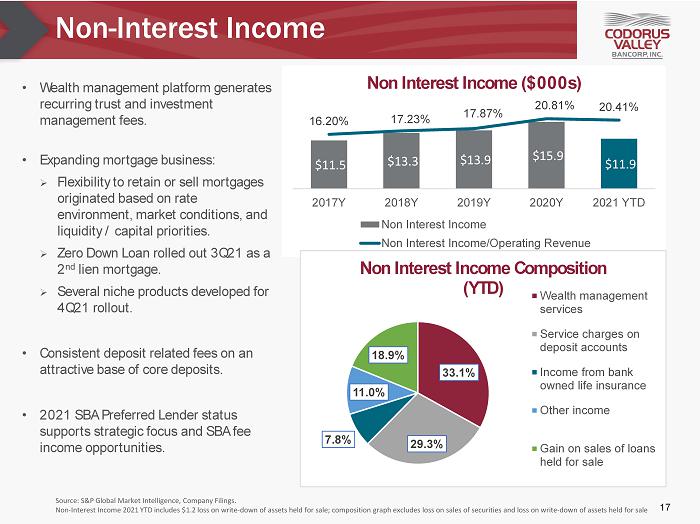

Non - Interest Income • Wealth management platform generates recurring trust and investment management fees. • Expanding mortgage business: » Flexibility to retain or sell mortgages originated based on rate environment, market conditions, and liquidity / capital priorities. » Zero Down Loan rolled out 3Q21 as a 2 nd lien mortgage. » Several niche products developed for 4Q21 rollout. • Consistent deposit related fees on an attractive base of core deposits. • 2021 SBA Preferred Lender status supports strategic focus and SBA fee income opportunities. Source: S&P Global Market Intelligence, Company Filings. Non - Interest Income 2021 YTD includes $1.2 loss on write - down of assets held for sale; composition graph excludes loss on sales of securities and loss on write - down of assets held for sale 17 $11.5 $13.3 $13.9 $15.9 $11.9 16.20% 17.23% 17.87% 20.81% 20.41% 2017Y 2018Y 2019Y 2020Y 2021 YTD Non Interest Income ($000s) Non Interest Income Non Interest Income/Operating Revenue 33.1% 29.3% 7.8% 11.0% 18.9% Non Interest Income Composition (YTD) Wealth management services Service charges on deposit accounts Income from bank owned life insurance Other income Gain on sales of loans held for sale

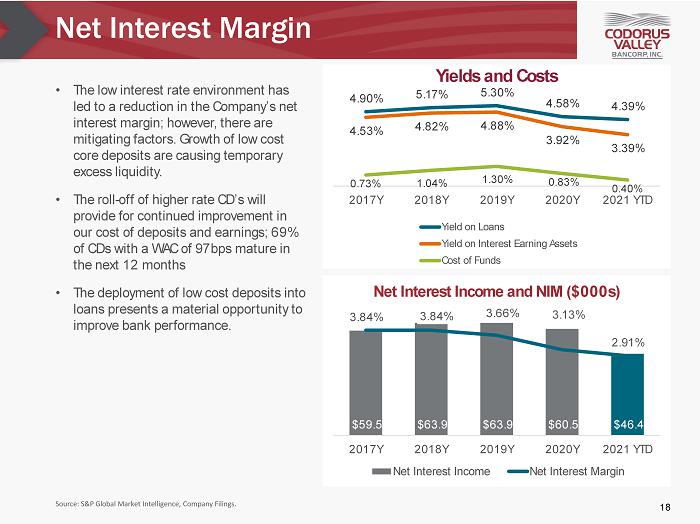

Net Interest Margin Source: S&P Global Market Intelligence, Company Filings. • The low interest rate environment has led to a reduction in the Company’s net interest margin; however, there are mitigating factors. Growth of low cost core deposits are causing temporary excess liquidity. • The roll - off of higher rate CD’s will provide for continued improvement in our cost of deposits and earnings; 69% of CDs with a WAC of 97bps mature in the next 12 months • The deployment of low cost deposits into loans presents a material opportunity to improve bank performance. 18 $59.5 $63.9 $63.9 $60.5 $46.4 3.84% 3.84% 3.66% 3.13% 2.91% 2017Y 2018Y 2019Y 2020Y 2021 YTD Net Interest Income and NIM ($000s) Net Interest Income Net Interest Margin 4.90% 5.17% 5.30% 4.58% 4.39% 4.53% 4.82% 4.88% 3.92% 3.39% 0.73% 1.04% 1.30% 0.83% 0.40% 2017Y 2018Y 2019Y 2020Y 2021 YTD Yields and Costs Yield on Loans Yield on Interest Earning Assets Cost of Funds

CD Repricing Opportunities Source: Company Filings. • Approximately 69% of CDs will reprice within the next 12 months. » This repricing benefits the Bank’s cost of deposits in the low interest - rate environment. • The total weighted - average rate on certificate of deposits at September 30, 2021 is 0.99%. • Average rates based on maturity date as are follows: » Maturing within the next 3 months: 1.27% » Maturing within 3 to 12 months: 0.83% » Maturing between 1 and 5 years: 0.76% Certificate of Deposit Repricing Timeline ($000s): Remaining Months Until Maturity 19 $100,408 $212,189 $176,149 $480 < 3 Months 3 - 12 Months 1 - 5 Years > 5 Years

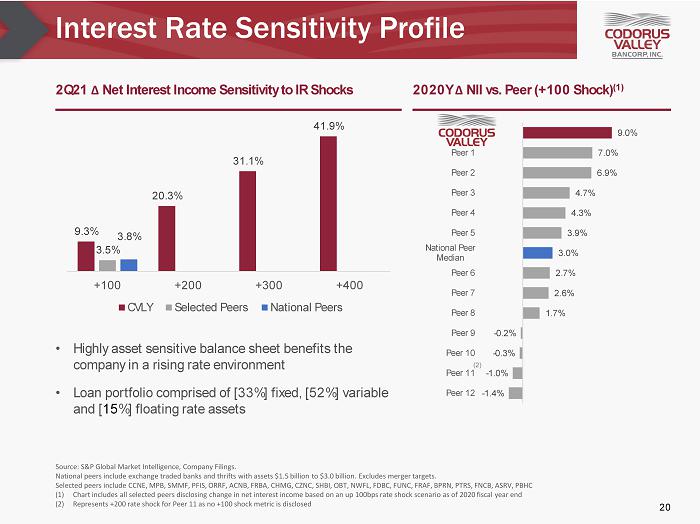

Interest Rate Sensitivity Profile 2Q21 ∆ Net Interest Income Sensitivity to IR Shocks 2020Y ∆ NII vs. Peer (+100 Shock) (1) 9.3% 20.3% 31.1% 41.9% 3.5% 3.8% +100 +200 +300 +400 CVLY Selected Peers National Peers Source: S&P Global Market Intelligence, Company Filings. National peers include exchange traded banks and thrifts with assets $1.5 billion to $3.0 billion. Excludes merger targets. Selected peers include CCNE, MPB, SMMF, PFIS, ORRF, ACNB, FRBA, CHMG, CZNC, SHBI, OBT, NWFL, FDBC, FUNC, FRAF, BPRN, PTRS, FN CB, ASRV, PBHC (1) Chart includes all selected peers disclosing change in net interest income based on an up 100bps rate shock scenario as of 20 20 fiscal year end (2) Represents +200 rate shock for Peer 11 as no +100 shock metric is disclosed 9.0% 7.0% 6.9% 4.7% 4.3% 3.9% 3.0% 2.7% 2.6% 1.7% - 0.2% - 0.3% - 1.0% - 1.4% CVLY Peer 1 Peer 2 Peer 3 Peer 4 Peer 5 National Peer Median Peer 6 Peer 7 Peer 8 Peer 9 Peer 10 Peer 11 Peer 12 (2) • Highly asset sensitive balance sheet benefits the company in a rising rate environment • Loan portfolio comprised of [33%] fixed, [52%] variable and [ 15 %] floating rate assets 20

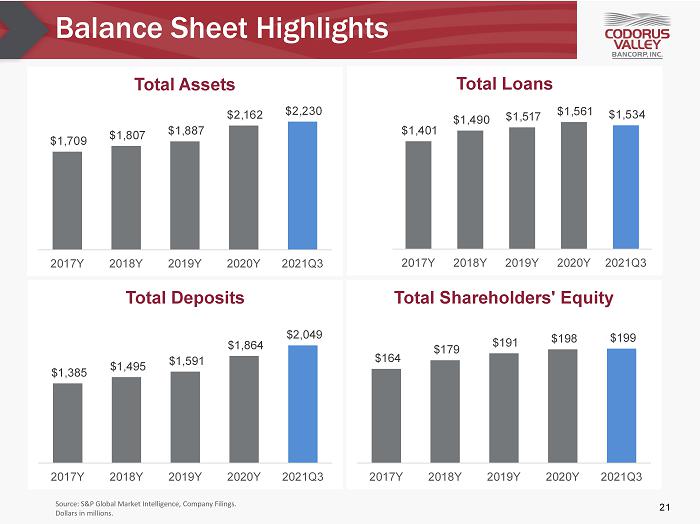

Balance Sheet Highlights Source: S&P Global Market Intelligence, Company Filings. Dollars in millions. 21 $1,709 $1,807 $1,887 $2,162 $2,230 2017Y 2018Y 2019Y 2020Y 2021Q3 Total Assets $1,401 $1,490 $1,517 $1,561 $1,534 $500 $700 $900 $1,100 $1,300 $1,500 $1,700 2017Y 2018Y 2019Y 2020Y 2021Q3 Total Loans $1,385 $1,495 $1,591 $1,864 $2,049 2017Y 2018Y 2019Y 2020Y 2021Q3 Total Deposits $164 $179 $191 $198 $199 2017Y 2018Y 2019Y 2020Y 2021Q3 Total Shareholders' Equity

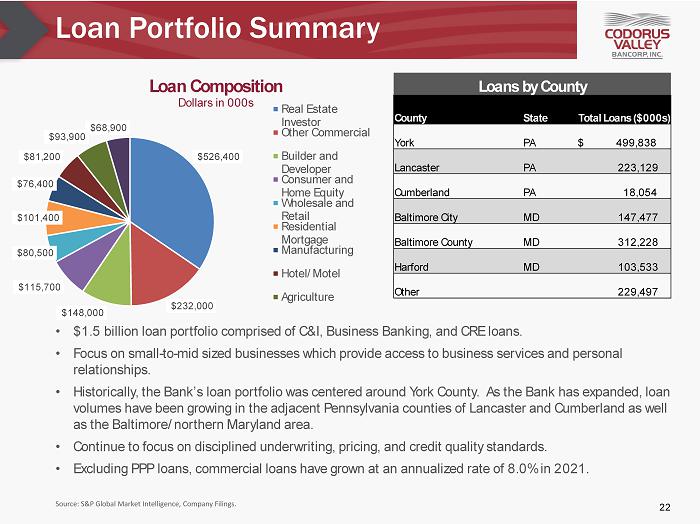

Loan Portfolio Summary • $1.5 billion loan portfolio comprised of C&I, Business Banking, and CRE loans. • Focus on small - to - mid sized businesses which provide access to business services and personal relationships. • Historically, the Bank’s loan portfolio was centered around York County. As the Bank has expanded, loan volumes have been growing in the adjacent Pennsylvania counties of Lancaster and Cumberland as well as the Baltimore/northern Maryland area. • Continue to focus on disciplined underwriting, pricing, and credit quality standards. • Excluding PPP loans, commercial loans have grown at an annualized rate of 8.0% in 2021. Source: S&P Global Market Intelligence, Company Filings. 22 $526,400 $232,000 $148,000 $115,700 $80,500 $101,400 $76,400 $81,200 $93,900 $68,900 Loan Composition Dollars in 000s Real Estate Investor Other Commercial Builder and Developer Consumer and Home Equity Wholesale and Retail Residential Mortgage Manufacturing Hotel/Motel Agriculture Loans by County County State Total Loans ($000s) York PA $ 499,838 Lancaster PA 223,129 Cumberland PA 18,054 Baltimore City MD 147,477 Baltimore County MD 312,228 Harford MD 103,533 Other 229,497

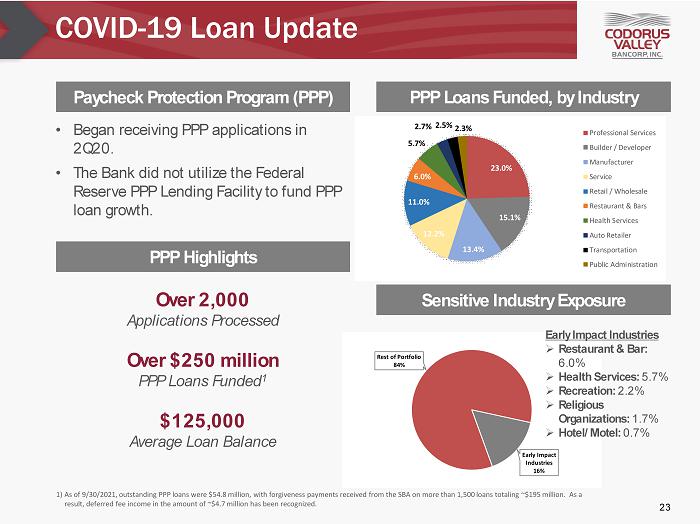

COVID - 19 Loan Update • Began receiving PPP applications in 2Q20. • The Bank did not utilize the Federal Reserve PPP Lending Facility to fund PPP loan growth. Paycheck Protection Program (PPP) PPP Loans Funded, by Industry 23.0% 15.1% 13.4% 12.2% 11.0% 6.0% 5.7% 2.7% 2.5% 2.3% Professional Services Builder / Developer Manufacturer Service Retail / Wholesale Restaurant & Bars Health Services Auto Retailer Transportation Public Administration Rest of Portfolio 84% Early Impact Industries 16% Early Impact Industries » Restaurant & Bar: 6.0% » Health Services: 5.7% » Recreation: 2.2% » Religious Organizations: 1.7% » Hotel/Motel: 0.7% 1) As of 9/30/2021, outstanding PPP loans were $54.8 million, with forgiveness payments received from the SBA on more than 1,500 lo ans totaling ~$195 million. As a result, deferred fee income in the amount of ~$4.7 million has been recognized. Sensitive Industry Exposure PPP Highlights Over 2,000 Applications Processed Over $250 million PPP Loans Funded 1 $125,000 Average Loan Balance 23

Loan Modification Update COVID Modifications in Effect as of September 30, 2021 24 Industry # of Loans $000s % Hotel 2 19,885 49.5% Recreation 1 19,000 47.3% Restaurant 1 38 0.1% Services 1 1,213 3.0% Total 5 40,136 100.0%

Allowance for Loan Losses Source: S&P Global Market Intelligence and Company Filings. • The Company’s allowance for loan losses was 1.47% of gross loans as of September 30, 2021. » Excluding $45.8 million in PPP loans, the allowance for loan losses totaled 1.52% of gross loans. • Reserve levels reflect the expectation of continued economic uncertainty. • The Company has conservatively classified commercial loans, provided appropriate specific reserves when necessary and has made proactive efforts to identify and mitigate problem credits. 25 $1,404 $1,489 $1,509 $1,551 $1,529 1.19% 1.29% 1.40% 1.38% 1.47% 2017Y 2018Y 2019Y 2020Y 2021 YTD ALLL (%) and Gross Loans ($millions) Gross Loans ALLL (%) 1.7 11.0 4.7 1.0 2.2 2017Y 2018Y 2019Y 2020Y 2021 YTD Provision to Charge Offs

Non - Performing Asset Summary Source: S&P Global Market Intelligence and Company Filings. Selected peers include CCNE, MPB, SMMF, PFIS, ORRF, ACNB, FRBA, C HMG , CZNC, SHBI, OBT, NWFL, FDBC, FUNC, FRAF, BPRN, PTRS, FNCB, ASRV, PBHC (1) Adjusted net charge - off ratio of 0.43%. Adjusted net charge - offs exclude loss from one borrower recognized in 1Q20 and has s ince been fully written off. Net Charge - Offs / Average Loans Non - Performing Assets / Loans + OREO 0.16% 0.10% 0.05% 0.19% 0.06% 0.18% 0.02% 0.04% 0.07% 2012 2013 2014 2015 2016 2017 2018 2019 2020 YTD CVLY Selected Peer Median 2.09% 2.63% 1.43% 0.89% 0.74% 0.61% 1.73% 1.79% 2.54% 2.75% 2012 2013 2014 2015 2016 2017 2018 2019 2020 YTD CVLY Selected Peer Median 0.93% (1) • Conservative credit culture • Credit performance has exceeded peer metrics for the majority of the last decade plus low Great Recession net charge - off rates • Focused on credit quality metrics with dedicated team for asset recovery 26

Deposit Composition Source: S&P Global Market Intelligence and Company Filings . • Deposit mix reflects the Company’s relationship - based business model. • The Company had core (non - time) deposits of $1.6 billion at 3Q21, representing 76% of total deposits. • Non - interest bearing deposits totaled $461 million at 3Q21, representing approximately 22% of total deposits and a 16% YTD increase in 2021. • Cost of interest bearing deposits at 3Q21 was 0.53%, compared to 0.97% in 2020. 27 $247 $253 $274 $397 $461 $158 $157 $174 $225 $254 $447 $536 $514 $598 $702 $86 $85 $86 $111 $143 $446 $465 $543 $532 $489 2017Y 2018Y 2019Y 2020Y 2021 YTD Deposit Composition ($ Millions) Noninterest bearing demand Interest bearing demand Money market Savings Time deposits 0.74% 1.15% 1.47% 0.97% 0.53% 2017Y 2018Y 2019Y 2020Y 2021 YTD Cost of Interest Bearing Deposits

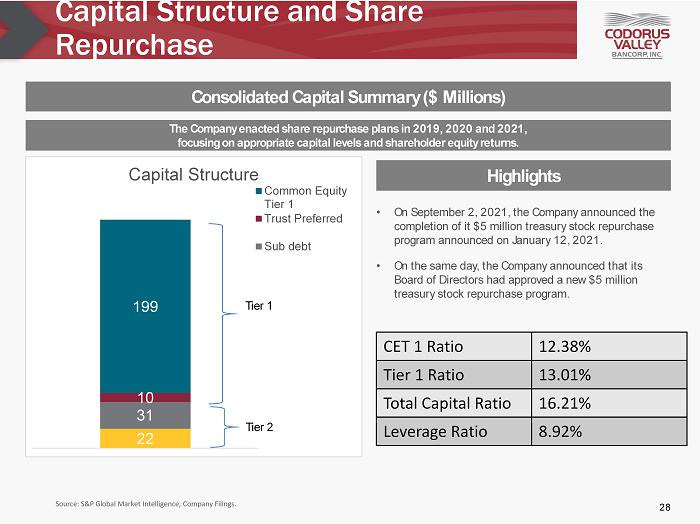

Capital Structure and Share Repurchase Consolidated Capital Summary ($ Millions) Source: S&P Global Market Intelligence, Company Filings. The Company enacted share repurchase plans in 2019, 2020 and 2021, focusing on appropriate capital levels and shareholder equity returns. • On September 2, 2021, the Company announced the completion of it $5 million treasury stock repurchase program announced on January 12, 2021. • On the same day, the Company announced that its Board of Directors had approved a new $5 million treasury stock repurchase program. Highlights 28 CET 1 Ratio 12.38% Tier 1 Ratio 13.01% Total Capital Ratio 16.21% Leverage Ratio 8.92% 22 31 10 199 Capital Structure Common Equity Tier 1 Trust Preferred Sub debt Tier 1 Tier 2

Appendix

COVID - 19 Response Employees Facilities Customers and Credit • PeoplesBank processed over 800 second round PPP loans totaling $77 million. • A significant majority of these loans supported small businesses, with the average outstanding loan balance below $150,000 and supported 9,800 jobs. • PeoplesBank offered several free PPP Forgiveness webinars in 3Q20, tailored specifically for PPP borrowers and to provide an overview of the PPP forgiveness process. • The process of returning associates to the office in a phased and hybrid approach was completed in August. • A long - term remote work policy was recently adopted allowing a portion of positions to work remotely on an ad hoc, part - time or full - time basis. This new employment strategy provides more work flexibility, broadens the employment geographic markets, allows for the redeployment of office space and ensures that PeoplesBank remains competitive in a tightening labor market. • All financial centers are now operating with normal drive - thru hours and lobby hours. • All retirement community office lobbies also remain open by appointment only with several modifications to ensure the safety of clients and associates. Three loan production offices remain closed; however, staff are working remotely. 30

Non - GAAP Disclosure Tangible common equity and tangible book value per common share are non - GAAP financial measures calculated using GAAP figures . Tangible common equity is calculated by excluding the balance of goodwill and intangibles from stockholder's equity . Tangible book value per share is calculated by dividing tangible common equity by the number of common shares outstanding . The Company has presented these non - GAAP financial measures because it believes that these measures provide useful and comparative information to assess trends in the Company’s financial condition and results of operations) . Because not all companies use the same calculations for tangible common equity, this presentation may not be comparable to other similarly titled measures calculated by other companies . These non - GAAP financial measures should not be considered a substitute for GAAP basis measures, and the Company encourages a review of its consolidated financial statements in their entirety . Following are reconciliations of these non - GAAP financial measures to the most directly comparable GAAP measure . 31 Tangible Common Equity As of and for the year ending December 31, Dollars in thousands, except per share data 2017 2018 2019 2020 3Q21 Common Equity $ 164,219 $ 178,746 $ 191,168 $ 197,960 $ 198,712 Intangibles 2,321 2,633 2,547 2,308 2,306 Tangible Common Equity 161,898 176,113 188,621 195,652 196,406 Common Shares Outstanding 9,819,000 9,924,000 9,756,000 9,821,000 9,592,000 Book Value per Common Share $ 16.72 $ 18.01 $ 19.59 $ 20.16 $ 20.72 Tangible Book Value per Common Share $ 16.49 $ 17.75 $ 19.33 $ 19.93 $ 20.48

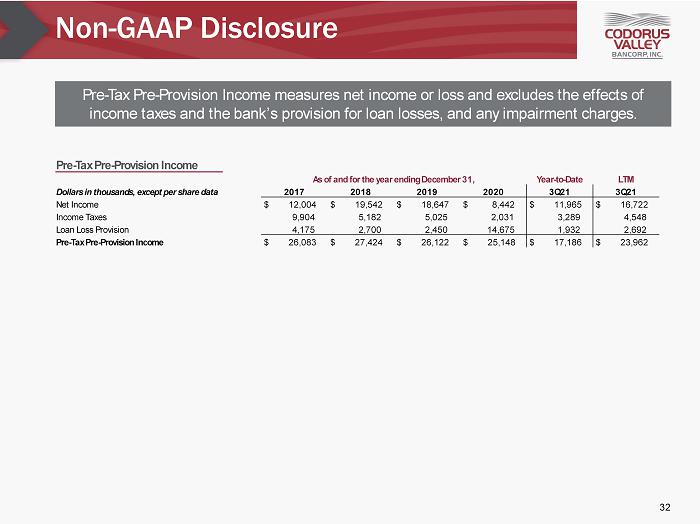

Non - GAAP Disclosure Pre - Tax Pre - Provision Income measures net income or loss and excludes the effects of income taxes and the bank’s provision for loan losses, and any impairment charges. 32 Pre - Tax Pre - Provision Income As of and for the year ending December 31, Year - to - Date LTM Dollars in thousands, except per share data 2017 2018 2019 2020 3Q21 3Q21 Net Income $ 12,004 $ 19,542 $ 18,647 $ 8,442 $ 11,965 $ 16,722 Income Taxes 9,904 5,182 5,025 2,031 3,289 4,548 Loan Loss Provision 4,175 2,700 2,450 14,675 1,932 2,692 Pre - Tax Pre - Provision Income $ 26,083 $ 27,424 $ 26,122 $ 25,148 $ 17,186 $ 23,962

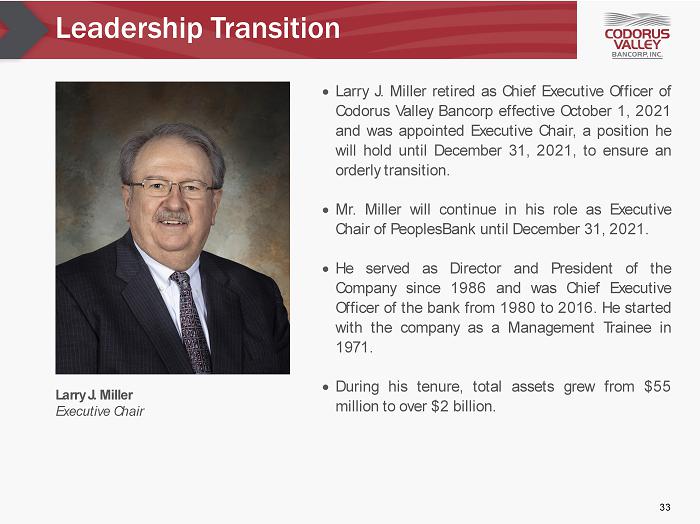

Leadership Transition Larry J . Miller retired as Chief Executive Officer of Codorus Valley Bancorp effective October 1 , 2021 and was appointed Executive Chair, a position he will hold until December 31 , 2021 , to ensure an orderly transition . Mr . Miller will continue in his role as Executive Chair of PeoplesBank until December 31 , 2021 . He served as Director and President of the Company since 1986 and was Chief Executive Officer of the bank from 1980 to 2016 . He started with the company as a Management Trainee in 1971 . During his tenure, total assets grew from $ 55 million to over $ 2 billion . Larry J . Miller Executive Chair 33