Exhibit 99.2

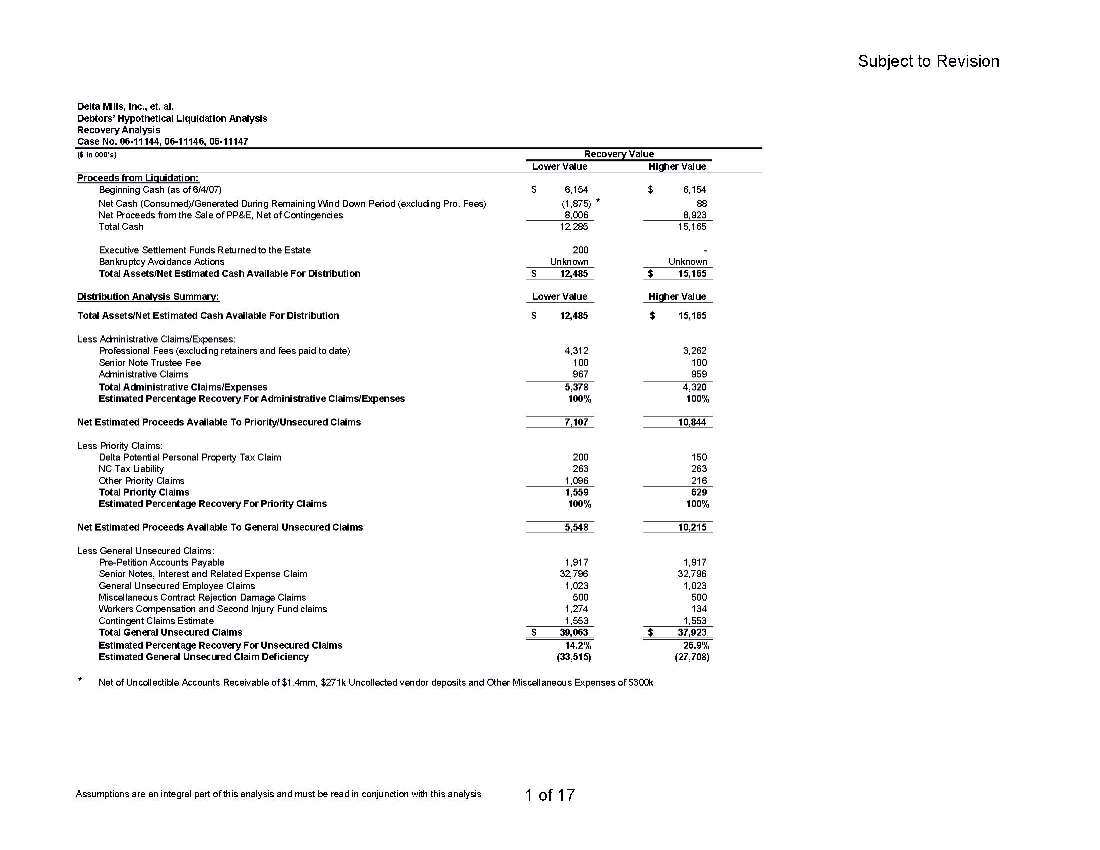

Delta Mills, Inc., et. al. Debtors’ Hypothetical Liquidation Analysis Recovery Analysis Case No. 06-11144, 06-11146, 06-11147 ($ in 000's) Lower Value Higher Value Proceeds from Liquidation: Beginning Cash (as of 6/4/07) 6,154 $ 6,154 $ Net Cash (Consumed)/Generated During Remaining Wind Down Period (excluding Pro. Fees) (1,875) * 88 Net Proceeds from the Sale of PP&E, Net of Contingencies 8,006 8,923 Total Cash 12,285 15,165 Executive Settlement Funds Returned to the Estate 200 - Bankruptcy Avoidance Actions Unknown Unknown Total Assets/Net Estimated Cash Available For Distribution 12,485 $ 15,165 $ Distribution Analysis Summary: Lower Value Higher Value Total Assets/Net Estimated Cash Available For Distribution 12,485 $ $ 15,165 Less Administrative Claims/Expenses: Professional Fees (excluding retainers and fees paid to date) 4,312 3,262 Senior Note Trustee Fee 100 100 Administrative Claims 967 959 Total Administrative Claims/Expenses 5,378 4,320 Estimated Percentage Recovery For Administrative Claims/Expenses 100% 100% Net Estimated Proceeds Available To Priority/Unsecured Claims 7,107 10,844 Less Priority Claims: Delta Potential Personal Property Tax Claim 200 150 NC Tax Liability 263 263 Other Priority Claims 1,096 216 Total Priority Claims 1,559 629 Estimated Percentage Recovery For Priority Claims 100% 100% Net Estimated Proceeds Available To General Unsecured Claims 5,548 10,215 Less General Unsecured Claims: Pre-Petition Accounts Payable 1,917 1,917 Senior Notes, Interest and Related Expense Claim 32,796 32,796 General Unsecured Employee Claims 1,023 1,023 Miscellaneous Contract Rejection Damage Claims 500 500 Workers Compensation and Second Injury Fund claims 1,274 134 Contingent Claims Estimate 1,553 1,553 Total General Unsecured Claims 39,063 $ 37,923 $ Estimated Percentage Recovery For Unsecured Claims 14.2% 26.9% Estimated General Unsecured Claim Deficiency (33,515) (27,708) * Net of Uncollectible Accounts Receivable of $1.4mm, $271k Uncollected vendor deposits and Other Miscellaneous Expenses of $300k Recovery Value Assumptions are an integral part of this analysis and must be read in conjunction with this analysis Subject to Revision 1 of 17

Delta Mills, et al Debtors’ Hypothetical Liquidation Analysis Summary of Critical Assumptions I. Introduction The Hypothetical Chapter 11 Liquidation Analysis and accompanying footnotes (the “Analysis”) have been prepared by Management for inclusion with the Disclosure Statement Regarding the Joint Plan of Liquidation (the “Plan”) Proposed by the Boards of Directors and Management of Delta Mills, et al. The Analysis will be attached to the Disclosure Statement as Exhibit B. The Analysis has been prepared on a consolidated basis and, consistent with the proposed Plan, intercompany claims have been eliminated. The Analysis has not been examined or reviewed by independent accountants. The Analysis is limited to the sole use of parties considering voting for acceptance or rejection of the Plan and is not to be used for any other purposes whatsoever. New information and outcomes of events are constantly changing. Although Management does not intend to update this Analysis, Management reserves the right to change or update this Analysis as new information becomes available if deemed warranted. These changes could be material. The Analysis was prepared based on assumed treatment of various issues that are subject to considerable uncertainty, including but not limited to, the sales price of the Pamplico facility; the realization on a large unpaid account receivable which is due from a certain foreign customer, which Management believes has not made payment due to financial considerations; the outcome of settlement negotiations with certain claimholders including, but not limited to, GMAC; the eventual total cost to the estate of professional fees; the ultimate amount of post-confirmation expenses incurred in administering the wind-down; collection of remaining accounts receivable; and the treatment of claims for workers compensation and several other significant claimants. The eventual outcome of these issues is uncertain and could be different than the assumed treatment in the Analysis and such differences could be material. Each of these issues are covered further later in the footnotes. Additionally, the Analysis was prepared based on an assumed treatment of various issues by the US Bankruptcy Court (the “Court”), including but not limited to the following: • Reclamation rights of certain vendors • Governmental or tax claims • Contingent and/or executory contract claims • Merger • Administrative claims of certain vendors • Health insurance/group insurance • Professional fees • Realization of receivables, the Debtors’ rights under the GMAC financing and factoring agreements and associated costs Subject to Revision 2 of 17

Delta Mills, et al Debtors’ Hypothetical Liquidation Analysis Summary of Critical Assumptions Actual treatment of these issues by the Court could be materially different than the assumptions made in the Analysis. Additionally, these issues could be the subject of substantial litigation by the various parties-in-interest to the Estate. Such litigation could cause the professional fees incurred to greatly exceed the amounts estimated in the Analysis and delay the timing of distributions to creditors. Any such litigation would likely increase the length of time necessary for the Debtors to remain under bankruptcy protection and the time needed to effectuate the liquidation which would increase costs and fees; such increased costs and fees could materially reduce the distributions to creditors. No representation is made regarding the length of time required to resolve any possible disputes, legal or otherwise, in order to distribute money to creditors. The Analysis was prepared utilizing nominal dollars. No discounting of future values or other similar adjustments has been made to reflect the passage of time and the time value of money. Although no formal tax analysis has been prepared, Management believes that any tax effect of the transactions contemplated herein would not result in any tax liability to the Debtors based upon current and past operating deficits. The Debtors also do not believe that they are due any material tax refund. Any potential state, local, transfer or other taxes are thought to be immaterial in nature and amount with the possible exception of personal property taxes. Management estimates approximately $34mm in Federal Net Operating Losses at Delta Mills, Inc. and $21mm in Federal Net Operating Losses at Delta Woodside, Inc. (in addition to the Delta Mills, Inc. Federal Net Operating losses) currently outstanding. In addition, this Analysis makes certain assumptions regarding key issues including, but not limited to, the following: 1) Timing and realization of certain sales of real property; 2) Timing and realization of the collection of accounts receivable; 3) Timing and amount of remaining sales of fabric and miscellaneous assets; 4) Wind-down expenses and other expenses of the Debtors’ Estate; 5) Amount and timing of professional fees; and 6) The amount and order of priority of claims. There will usually be differences between actual and estimated results because events and circumstances frequently do not occur as expected and these differences may be material. It should be noted that the ranges of potential outcomes are based upon estimates and assumptions, some of which may ultimately be materially different than the actual outcome. Some risk factors are not quantifiable and, thus, are not reflected herein. Further, the occurrence of unforeseen circumstances could materially change the outcomes, and the outcomes could be materially lower. Subject to Revision 3 of 17

Delta Mills, et al Debtors’ Hypothetical Liquidation Analysis Summary of Critical Assumptions In connection with the preparation and development of the Plan, the Analysis, which utilizes various assumptions based on historical facts and anticipated changes in the Debtors’ business, was prepared in June 2007 by the Debtors’ Management. The Analysis was updated to reflect the June 29, 2007 Court Order authorizing the sale of the Beattie Plant to Gibbs International. No other updates have been made to the Analysis since June 2007. The Analysis assumes that the Plan will be confirmed and will be implemented in accordance with its terms. The estimates and assumptions underlying the Analysis are inherently uncertain and, though considered reasonable by the Debtors’ Management as of the date hereof, are subject to significant business, economic and competitive uncertainties. Accordingly, the Analysis and such estimates and assumptions are not necessarily indicative of current values or future performance, which may be significantly less favorable than is presently projected. The Analysis included herein should not be regarded as a representation by the Debtors, the Debtors’ Management, the Debtors’ advisors or any other person that these projected results will be achieved. Background On October 13, 2006, Delta Woodside Industries, Inc. ("Delta Woodside"), Delta Mills, Inc. ("Delta Mills"), a wholly-owned subsidiary of Delta Woodside, and Delta Mills Marketing, Inc. ("Marketing"), the wholly owned subsidiary of Delta Mills (collectively referred to as the "Companies," the “Debtors” or the “Estate”), filed voluntary petitions for bankruptcy protection under Chapter 11 of the United States Bankruptcy Code (the "Bankruptcy Code") in the United States Bankruptcy Court for the District of Delaware (the "Bankruptcy Court"). The Companies proceeded after the filing of the bankruptcy petition with a Court approved orderly wind-down of the operations of the Companies designed to result in a liquidation and distribution to creditors. As part of this orderly wind-down process, Delta Mills has filled substantially all accepted orders from its customers and has discontinued operations at both its Beattie plant and its Delta 3 finishing plant. The Companies have sold substantially all equipment at both plants, and all real property at the Delta 2 and 3 facilities. The Companies’ Beattie facility is under contract to be sold within five days of July 31, 2007. The Companies’ remaining facility, known as Pamplico, remains available for sale. Subject to Revision 4 of 17

Delta Mills, et al Debtors’ Hypothetical Liquidation Analysis Summary of Critical Assumptions Assumptions and Footnotes to the Analysis: II. The Analysis The Liquidation Analysis consists of two primary supporting schedules. 1. The Wind-Down Budget – Weekly cash flow forecast for the period June 4, 2007 through the end of the wind-down period, currently assumed to be June 30, 2008 2. The Recovery Analysis – Analysis of cash available for distribution and forecasted claims of the Estate The Wind-Down Budget Methodology The wind-down budget was developed by Management to plan the cash receipts and disbursements related to the orderly wind-down process for the period June 4, 2007 to June 30, 2008. There is no certainty that the wind-down process can be completed prior to June 30, 2008. If the wind-down process extends beyond June 30, 2008 then recoveries may be reduced and additional liquidation costs will be incurred. Beginning balances in the Analysis are based on preliminary numbers from the Company’s May Monthly Operating Report (“MOR”), balances of accounts receivable (“AR”) and cash as provided by relevant reports from GMAC’s systems. These amounts have not been subjected to any review or auditing procedures. These amounts could be subject to revision and such differences could be material. The Analysis has not been adjusted for June activity. The descriptions of the wind-down receipts and disbursements shown herein reflect Management’s current assessment of likely outcomes. However, as these outcomes are uncertain, certain risk adjustments are assessed and described further in Section III of this summary; “Recovery Analysis.” The cash receipts associated with the sale of Property, Plant, and Equipment have been excluded from the wind-down budget and are shown as part of the Recovery Analysis in Section III. Subject to Revision 5 of 17

Delta Mills, et al Debtors’ Hypothetical Liquidation Analysis Summary of Critical Assumptions Sales All “normal course” finished goods sales were completed as of the week of May 5, 2007. Miscellaneous Inventory Sales All remaining Raw Materials and Work in Process inventory that cannot be sold in the normal course are assumed to be sold to liquidators or others. Management anticipates selling any remaining such inventory that can be sold by the end of July 2007 for approximately $0.2mm. All other remaining inventory is assumed to be disposed of by the Debtors for an estimated cost of $25k ($75k in the “Lower” scenario covered later in the footnotes). Management believes they have contracted with a third party to purchase approximately $150k of the remaining inventory. However if this third party does not perform on this contract and purchase the yarn, the Debtors’ may be required to take legal action against this third party in order to ensure performance on the contract. If the Debtors are unable to enforce the contract, Management estimates this yarn could then be sold at the market prevailing price which is likely to be less than the contract price. No such price reduction has been included in this Analysis. Receipts Delta Mills has factored nearly all of its AR with GMAC Commercial Finance (“GMAC”) on a non-recourse basis. Collections during the wind-down period are assumed to be approximately $2.3mm. The beginning AR balance is based on the Debtors’ AR aging report as of June 4, 2007. This report showed approximately $1.2mm outstanding. In addition to this amount the Analysis also includes approximately $1.4mm in AR owing from one foreign customer which Management believes has not made payment due to financial considerations. Collections are assumed to be net of client risk, disputes, deductions, and other miscellaneous offsets. No value has been attributed to client risk accounts receivable, disputes, deductions or other miscellaneous offset amounts except for the foreign customer which Management believes has not made payment due to financial considerations. Treatment of this customer is addressed later in the footnotes. The Analysis assumes $300k of uncollected AR; $100k of this balance is due to potential credits. The remaining $200k of uncollected AR are considered to be losses due to customer disputes, allowances, quality related issues, or any possible insurance shortfalls. Generally, losses arising from customer credit issues are assumed borne by GMAC. The Analysis also assumes approximately $400k of AR credits outstanding. The Analysis assumes that approximately $100k of these credits relate to post-petition AR and the remaining approximately $300k of credits are assumed to relate to pre-petition AR. Subject to Revision 6 of 17

Delta Mills, et al Debtors’ Hypothetical Liquidation Analysis Summary of Critical Assumptions All miscellaneous asset and yarn sales are assumed to be on cash terms and not factored with GMAC. The Analysis assumes no maturity based (ADDA) payments. Standard Company terms are 60-days; however, the Analysis assumes equal weekly payments of remaining outstanding AR over eight weeks. Actual timing of these collections will likely vary from this assumption. One foreign customer, which Management believes has not made payment due to financial considerations, has been addressed later in the footnotes. Management’s assessment of the collectibility of AR is based primarily on past payment patterns and the factoring agreement entered into between the Company and GMAC (as successor corporation to BancBoston Financial) dated March 31, 1993 and amended as of May 30, 2006. Under this agreement, GMAC accepts the credit risk for all domestic and foreign accounts receivable that have been approved by GMAC. As it relates to foreign accounts receivable, GMAC generally accepts 90% of the credit risk of any approved foreign receivables. It is Management’s belief that GMAC insures this credit risk with a third party insurer. As mentioned above, there is one foreign customer which Management believes has not made payment due to financial considerations. At this time the Company is in discussions with GMAC regarding responsibility for the payment of this receivable. GMAC and the insurer have indicated that they will not accept responsibility for this receivable. The Debtors are disputing this position. The Debtors do not currently have sufficient information to predict the outcome of this matter. This Analysis assumes that 90% of accounts outstanding for this customer (net of credits) are collected in the “Higher” case. It is Management’s intent to aggressively pursue the collection of this receivable from the customer, GMAC, and/or the insurance company as necessary. These matters and other matters relating to GMAC are or may be put before the Court for resolution. Currently GMAC is withholding approximately $1.9mm as of June 13, 2007 from the Estate that is due to the Company under the factoring agreement. It is possible that GMAC may continue to withhold these or other funds from the Estate in the future. This Analysis treats these funds as if GMAC were to not transfer any funds to the Estate until an undetermined time after the confirmation of the Plan. Further, the Analysis assumes that GMAC has already deducted termination fees aggregating $600k from the funds of the Estate that it is holding and that the Estate pays certain of GMAC’s costs relating to the case including professional fees and related charges. GMAC has continued to credit interest on balances withheld at a rate of 3.0% below prime. In a letter to the Debtors dated May 15, 2007 GMAC notified the Debtors that GMAC has terminated the Financing Agreements and the Factoring Agreements. In addition, GMAC has claimed $600k in fees over the Debtors’ objections (these funds have been deducted from the Estate’s account with GMAC). For purposes of this Analysis, it is assumed that GMAC would ultimately prevail in the receipt of these fees; however this treatment in the Analysis in no way constitutes the Debtors conceding that GMAC is entitled to Subject to Revision 7 of 17

Delta Mills, et al Debtors’ Hypothetical Liquidation Analysis Summary of Critical Assumptions these fees at the present time. The aforementioned letter further indicated that they will, in their capacity as factor, continue to fulfill their obligations under and as set forth in the Factoring Agreement with respect to all AR outstanding as of the date of the letter. Operating Disbursements Operating Disbursements are expenses incurred by the Debtors in the remaining wind-down period. The Analysis assumes a gradual reduction of employees until August 25, 2007 at which point a staff of one full time accounting employee, one full time plant engineer at the Pamplico facility (until that facility is sold), and three part time senior Company executives are assumed to work half time through December 29, 2007 and quarter time through June 30, 2008 to wrap up any remaining affairs of the Estate. In addition to these employees, the Debtors have negotiated consulting arrangements with certain former employees who are able to provide necessary services to the Estate on an hourly rate basis as needed. Estimates for the cost of these consulting arrangements are included in the Analysis. These arrangements are terminable at will by the Debtors. All employment for the Estate is assumed to end as of June 30, 2008. These same three senior Company executives have negotiated a settlement agreement with the Unsecured Creditors Committee’s (“UCC”). This agreement requires that these executives forgo receipt of $200k that would otherwise be payable to them under a court approved incentive plan. This money can then be earned back if the return to the general unsecured creditors meets certain thresholds upon the terms and conditions described in the Disclosure Statement. The settlement agreement gives these three executives two options. a. Option One: Each Executive may elect to add the amount he individually waived, as mentioned in the paragraph above, to his respective unsecured claim against the Debtors’ estates for unpaid severance. Any of the three executives who chooses Option One shall not be required to provide “no cost” employment services to the Debtors’ estates at any time. b. Option Two: Alternatively, each of the three executives may elect to earn-back the amount he individually waived, as mentioned in the paragraph above, on the basis of a sliding scale depending on the ultimate percentage yield to unsecured creditors. Any Executive who chooses Option Two will not be entitled to add any portion of the amount waived to his respective unsecured claim against the Debtors’ estates for unpaid severance, whether or not such waived amount is earned back. Earn-back amounts will be paid by Delta Mills, Inc. in increments consistent with the sliding Subject to Revision 8 of 17

Delta Mills, et al Debtors’ Hypothetical Liquidation Analysis Summary of Critical Assumptions scale. Any of the three executives who chooses Option Two will provide consulting services to Delta Mills, Inc. from and after the effective date of the Plan for an aggregate of sixty (60) hours at no cost to the Debtors’ estates. Generally, under either option, the three executives have the option to resign with ten business days notice. However, should the executives choose Option Two, they will be required to provide the 60 hours of consulting services to the Estate. The Analysis assumes the economics of Option Two and furthermore assumes that these executives continue to be engaged in day-today aspects of the wind-down through June 30, 2008. Critical items in the operating disbursements budget include holding costs for the facilities, administrative expenses, travel, and insurance. The wind-down budget also includes approximately $0.9mm in other currently unidentified costs. Included in the wind-down budget are holding costs for the Beattie facility including power (Duke Power), security, maintenance, taxes and miscellaneous items through the approximate end of the month of July 2007, at which time it is anticipated that the Beattie facility will be sold. For every month beyond July 31, 2007 the holding costs of the Beattie facility are estimated to be approximately $40k. Also included in the wind-down budget are the assumed holding costs of the Pamplico facility including power (Progress Energy), security, maintenance, taxes, and miscellaneous through December 29, 2007, at which time it is anticipated that the Pamplico facility will be sold. For each month beyond December 29, 2007 the holding costs of the Pamplico facility are estimated to be approximately $27k per month. Other (Sources) / Uses • Progress Energy/Duke Power Refund – On November 2, 2006 the Debtors provided an approximate $209k deposit to utility providers Progress Energy and Duke Energy as adequate assurance for payment of post-petition electricity at the Delta and Pamplico facilities. Approximately $162k of this deposit is attributable to the Delta facility and is to be returned to the Debtors in two amounts. Approximately $42k of this amount was returned during the week ended May 5, 2007. In the “Higher” scenario the remaining $120k is assumed to be returned in July 2007. Approximately $29k of this deposit is attributable to the Pamplico facility and is assumed, in the “Higher” scenario, to be returned to the Debtors during the week ended December 29, 2007. Approximately $18k of this amount is attributable to the Beattie facility and is assumed to be returned to the Debtors, in Subject to Revision 9 of 17

Delta Mills, et al Debtors’ Hypothetical Liquidation Analysis Summary of Critical Assumptions the “Higher” scenario, during July 2007. Note that in the “Lower” scenario the amounts that are currently outstanding are assumed not to be returned to the Estate. • Record Storage Prepayment – Record retention requirements are assumed beyond the wind-down period of the case and it is assumed that these requirements would be met through prepayment to a record storage specialist. The Debtor estimates storage costs for five years would be approximately $100k. • NC Tax Liability – Delta Woodside continues paying the monthly installments to the North Carolina Department of Revenue (“NCDOR”) in accordance with the settlement agreement reached with NCDOR in May 2006. The Analysis assumes that any amounts left outstanding at confirmation are paid as priority claim amounts. • Professional Fees – Professional Fees used in the wind-down Budget assume that the Plan is confirmed on or about September 5, 2007. It is further assumed that the majority of pre-confirmation Professional Fees in the case would be incurred prior to this date. The Analysis assumes that total professional fees (excluding professionals representing GMAC) are approximately $5.4mm (after adjusting for retainers paid to certain professionals pre-petition). Each month after August 4, 2007 that the confirmation is delayed could add $200k to $400k to the total of these fees. Such amounts are not included in the Analysis. o The Analysis assumes that the Companies incur an additional approximate $900k of professional fees postconfirmation. Approximately $650k of these fees are assumed to be incurred by legal counsel to the post-confirmation entity. Approximately $50k of these fees are assumed to be incurred by the Debtors’ tax accountants for the filing of tax returns. o The analysis assumes approximately $205k in professional fees for Mesirow Financial Consulting (“Mesirow”) for post-effective date financial advisory and liquidation services. This amount may increase or decrease depending upon, among other things, the extent to which current management continues to assist in the wind-down. Mesirow and Management have estimated that their combined post-effective date costs will approximate $500k, with the allocation of these costs to be determined as the wind-down progresses. Additional employee and consulting costs of approximately $100k are also included in the budget. o Mesirow has estimated that, should Management choose not to participate in the wind-down, the wind-down budget could increase by as much as $125k. This additional amount has not been included in the Analysis. • Trustee Fees – Payments to the US Trustee are assumed to be paid quarterly through June 2008. • Workers’ Comp L/C – The Debtors were self insured for workers’ compensation liability insurance. As security for future workers’ compensation obligations or “tail” coverage they had delivered a standby letter of credit (“L/C”) payable to the South Carolina Workers’ Compensation Commission (the “Commission”) in the amount of $0.75mm which has been drawn upon in Subject to Revision 10 of 17

Delta Mills, et al Debtors’ Hypothetical Liquidation Analysis Summary of Critical Assumptions full and is assumed to be used by the Commission or the South Carolina Second Injury Fund “SIF” to cover outstanding claims. However, additional claims have been made upon the Estate for Workers’ Compensation related claims. These claims are covered later in the Analysis. Directors and Officers Insurance Tail Coverage – Most, if not all, current and former officers and directors of the Debtors have filed contingent claims for indemnification under applicable state law and corporate organizational documents. The Analysis includes an estimated expense for the purchase of an extension of the run-off period under the Debtors’ Directors and Officers liability insurance for $350k and no claims by current or former officers or directors for indemnification are assumed to be allowed. Severance & Incentive Payments – Severance to non-executive employees (other than non-executive members of the wind-down team) was paid in the amount of approximately $1.5mm evenly over twelve weeks ending on April 21, 2007. This amount represents approximately 65 of what these employees would be entitled to according to the Debtors’ employment policies. The remaining 35 is assumed to result in an automatic general unsecured claim (further detailed in Section III) Severance to non-executive employees who are members of the wind-down team are assumed to be paid after these employees complete their employment with the Debtors. Incentive payments to executive employees were contingent on the Debtors meeting certain predetermined goals.The first of those predetermined goals was met during the week of February 10, 2007 at which point the first payment of 21 weekly payments equal to 50 of executive incentive payments was made.The second of those predetermined goals was met during the week of March 3, 2007 at which point, the first of 18 weekly installment payments of the remaining 50 of executive incentive was begun (ending on June 30, 2007). As mentioned previously in the Analysis, three senior executives have negotiated a settlement agreement with the UCC relating to incentive compensation. The financial impact of this agreement to the Estate is covered elsewhere in the footnotes. Employee Vacation Payouts – Employees are paid any remaining accrued vacation after they have completed their required employment term with the Debtors. The vacation payments are made at the employees’ normal bi-weekly pay rates until all accrued vacation owing to these employees is paid. The Debtors’ vacation policy is that employees earn all of their vacation from the previous year as of the first day of the following year. As such, employees remaining with the Debtors as of January 1, 2007 earned their vacation for 2006 and will be paid this vacation once their service with the Debtors is terminated. Any employees remaining after June 30, 2007, are assumed to have their vacation paid out in a lump sum in July 2007. Subject to Revision 11 of 17

Delta Mills, et al Debtors’ Hypothetical Liquidation Analysis Summary of Critical Assumptions • Group Health Insurance - The Analysis assumes no additional disbursements or claims due to Group Health Insurance. All payments have been made in accordance with the orders of the Bankruptcy Court. Amounts are currently on deposit with Blue Cross Blue Shield, the Debtors’ healthcare claims administrator, and no additional payments are assumed to be made. The Analysis does assume in the “Higher” case only that all Group Health Insurance claims have been satisfied and therefore Blue Cross Blue Shield returns approximately $100k of remaining held funds to the Estate. • Factoring Fee, Bank Interest, and Termination Related Fees – o All obligations under the credit agreement have been paid in full and the Debtors are assumed not to re-borrow under the credit agreement. o Termination Fees are assumed to cost the Estate $0.6mm. GMAC has notified the Debtors that they have terminated the agreement and claimed $600k in fees over the Debtors’ objections. The Analysis assumes GMAC would ultimately prevail in the receipt of these fees; however this treatment in the Analysis in no way constitutes the Debtors conceding that GMAC is entitled to these fees at the present time. o Bank/Money Market Interest on Cash Deposits – Any cash on hand in excess of the $100k minimum deposit held at Wachovia is assumed to earn interest at a 3% annual rate of return paid weekly. As of July 2007, actual interest rate being paid by Wachovia was 4.16%. Currently GMAC is withholding approximately $1.9mm as of June 13, 2007 from the Estate that is due to the Company under the factoring agreement. It is possible that GMAC may continue to withhold these or other funds from the Estate in the future. This Analysis treats these funds as if GMAC were to not transfer any funds to the Estate until an undetermined time after the confirmation of the Plan. Further, the Analysis assumes that GMAC has already deducted termination fees aggregating $600k from the funds of the Estate that it is holding and that the Estate pays certain of GMAC’s costs relating to the case including professional fees and related charges. GMAC has continued to credit interest on balances withheld at a rate of 3.0% below prime. These matters and other matters relating to GMAC are or may be put before the Court for resolution. Subject to Revision 12 of 17

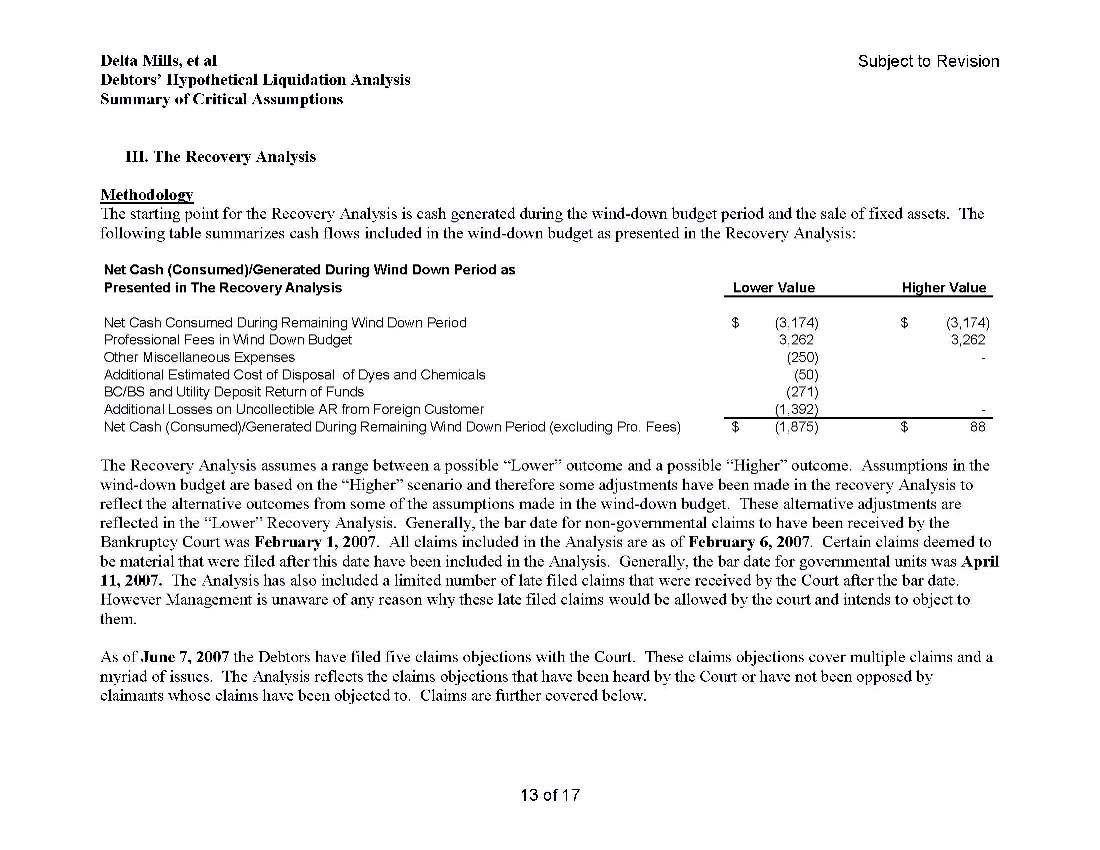

Delta Mills, et al Debtors’ Hypothetical Liquidation Analysis Summary of Critical Assumptions III. The Recovery Analysis Methodology The starting point for the Recovery Analysis is cash generated during the wind-down budget period and the sale of fixed assets. The following table summarizes cash flows included in the wind-down budget as presented in the Recovery Analysis: Net Cash (Consumed)/Generated During Wind Down Period as Presented in The Recovery Analysis Lower Value Higher Value Net Cash Consumed During Remaining Wind Down Period (3,174) $ (3,174) $ Professional Fees in Wind Down Budget 3,262 3,262 Other Miscellaneous Expenses (250) - Additional Estimated Cost of Disposal of Dyes and Chemicals (50) BC/BS and Utility Deposit Return of Funds (271) Additional Losses on Uncollectible AR from Foreign Customer (1,392) - Net Cash (Consumed)/Generated During Remaining Wind Down Period (excluding Pro. Fees) (1,875) $ 88 $ The Recovery Analysis assumes a range between a possible “Lower” outcome and a possible “Higher” outcome. Assumptions in the wind-down budget are based on the “Higher” scenario and therefore some adjustments have been made in the recovery Analysis to reflect the alternative outcomes from some of the assumptions made in the wind-down budget. These alternative adjustments are reflected in the “Lower” Recovery Analysis. Generally, the bar date for non-governmental claims to have been received by the Bankruptcy Court was February 1, 2007. All claims included in the Analysis are as of February 6, 2007. Certain claims deemed to be material that were filed after this date have been included in the Analysis. Generally, the bar date for governmental units was April 11, 2007. The Analysis has also included a limited number of late filed claims that were received by the Court after the bar date. However Management is unaware of any reason why these late filed claims would be allowed by the court and intends to object to them. As of June 7, 2007 the Debtors have filed five claims objections with the Court. These claims objections cover multiple claims and a myriad of issues. The Analysis reflects the claims objections that have been heard by the Court or have not been opposed by claimants whose claims have been objected to. Claims are further covered below. Subject to Revision 13 of 17

Delta Mills, et al Debtors’ Hypothetical Liquidation Analysis Summary of Critical Assumptions Proceeds from Liquidation • Reduction in Assumed AR Collections – For purposes of the Analysis AR collections in the “Lower” scenario have been reduced by approximately $1.7mm to reflect possible uncollectible AR. Approximately $1.4mm of this amount relates to one foreign customer which Management believes has not made payment due to financial considerations. At this time, the Company is in discussions with GMAC to determine responsibility for this foreign receivable. GMAC and the insurer (mentioned above) have indicated that they will not accept responsibility for this receivable. The Debtors are disputing this position. The Debtors do not currently have sufficient information to predict the outcome of this matter. It is Management’s intent to aggressively pursue the collection of this receivable from the customer, GMAC, and/or the insurance company as necessary. As mentioned previously in the footnotes, in the “Higher” scenario uncollected AR is assumed to be approximately $300k. • Proceeds from the Sale of PP&E – o Proceeds from the sale of the Delta 2 and 3 facility, and machinery and equipment at both the Delta 3 facility and the Beattie facility were based on information provided in the closing statements for the sales of these assets as of the closing on February 13, 2007. o Proceeds from the sale of the Beattie Plant were based on an order authorizing the sale of the Beattie Plant to Gibbs International, Inc. dated as of June 29, 2007. The closing of the Beattie Plant sale is under contract to occur within five days of July 31, 2007. o Proceeds from the sale of the Pamplico facility were based on Management assumptions, feedback from potential buyers to individuals handling the asset sale efforts, as well as an appraisal of the Pamplico facility from March 2007. The appraised value at that time was approximately $2.7mm. Despite marketing efforts to date, no bona fide offers for the Pamplico facility have been received. As such the ultimate realization of value from this asset is subject to uncertainty. Accordingly, the Debtors have assessed a subjective contingency against the appraised value in the Analysis to address this uncertainty. • Commissions were based on closing statements and/or contracts with or proposals from professionals handling the asset sale efforts as appropriate. Sales commissions on Pamplico facility are assumed to be 3.5% unless sales price exceeds $2.2mm. • Amounts required to exit the FILOT arrangement and receive saleable title to all PP&E were paid out of the proceeds from the February 13, 2007 sale of fixed assets. Any real property taxes to be paid for tax year 2007 (some of which having been prepaid by the Debtors) would be pro-rated with the purchaser. • 2007 Property taxes for the Pamplico facility are assumed to accrue at a rate of $4k per month and are assumed to be pro-rated with the purchaser. Subject to Revision 14 of 17

Delta Mills, et al Debtors’ Hypothetical Liquidation Analysis Summary of Critical Assumptions • 2007 Property taxes for the Beattie facility are assumed to be offset by amounts prepaid as part of the payments made to exit the Company’s FILOT arrangement. • The Estate may be assessed taxes for personal property at the Delta facility. While this property has already been sold, it is Management’s understanding that the state of South Carolina assesses property taxes on personal property in arrears. At the present time, the required property tax returns for this property have not been filed and therefore no property tax has been assessed. Additionally, there may be legal precedent for the Estate to possibly negotiate a lower tax assessment. For purposes of the Analysis, Management has assumed property tax expenses of between $150k and $200k to cover this potential assessment. • Timing of Asset Sales is assumed as follows: o Delta 2 and 3 facility was sold February 13, 2007 o Machinery and Equipment at both Delta 3 and Beattie were sold February 13, 2007 o Pamplico facility is assumed sold December 29, 2007 o Beattie facility is assumed sold within five days of July 31, 2007 Distribution Analysis Summary Administrative Claims: • Professional Fees – In the “Lower” outcome of the Analysis additional costs of professionals have been included to reflect the case remaining in bankruptcy significantly longer than anticipated in the “Higher” case. Professional fees (excluding fees charged by GMAC professionals) are assumed to increase by $1.1mm. Should this occur total professional fees would approximate $6.5mm including retainers and professional fees paid to date. • Senior Note Trustee Fee – The Analysis assumes that the fees charged by the Trustee for the Senior Notes of approximately $100k are paid by the Estate and are not netted out of the Senior Notes’ general unsecured claims. • 20 Day Administrative Vendor Claims – These are based primarily on administrative proofs of claims filed with the Bankruptcy Court. However, some vendors sent the Debtors reclamation demands but did not file proofs of claims for administrative status or possibly at all. o Claimants who filed neither a reclamation demand nor an administrative proof of claim were treated as unsecured creditors even if their goods were received within 20 days of the petition date. o Claimants who filed reclamation demand letters but filed general unsecured proofs of claims were considered to have general unsecured claims. Subject to Revision 15 of 17

>Delta Mills, et al Debtors’ Hypothetical Liquidation Analysis Summary of Critical Assumptions o Claimants who filed valid administrative proofs of claim, and whose goods were received by the Debtor within 20 days of the petition, were considered to have administrative status in both the “Higher” and “Lower” scenarios. Priority Claims • NC Tax Liability – The negotiated settlement with the NCDOR is assumed to be a priority tax claim against the Estate for amounts remaining after monthly installments are no longer made. • Reclamation Demand Claims – These claims were based upon the approximate 16 reclamation demands sent by vendors to the Debtors. It should be noted that 2 of these reclamation demands were sent after the 20 day time limit prescribed in the Bankruptcy Code. All 16 reclamation claim demands were objected to by the Debtors. The Court has ruled in the Debtors’ favor with respect to each of these reclamation claims except with respect to the claims of certain vendors which are the subject of settlement discussions between the Debtors and these claimants. • Other Priority Claims – Included in these claims are the claims of certain vendors with which the Debtors are actively in settlement negotiations. The treatment of these claims in the Analysis in no way constitutes the Debtors conceding that the claims of these vendors are entitled to any specific treatment by the Court. General Unsecured Claims • Pre-petition accounts payable – These claims were estimated based upon Schedule F of the Statement of Assets and Liabilities for each of the Debtors and/or proofs of claims filed with the court. Amounts were reduced by intercompany claims, Senior Notes, Pre-petition Senior Note Interest, and any amounts considered as having been paid as administrative or priority claims or if these amounts were assumed to have been paid as part of the wind-down budget. • Senior Notes – These claims were estimated based upon the proof of claim filed by the senior note trustee. Approximately $100k in Senior Note Trustee Fees are assumed to be paid as an administrative expense. • General Unsecured Employee Claims – Represents the remaining 35% of severance that is not to be paid out as part of the wind-down budget. • Miscellaneous Contract Rejection Claims – $0.5mm estimate of possible contract rejection claims. It is possible that these claims could be filed after the February 1st bar date. The Debtors are unaware of the existence of any such claims at the present time and would object to any asserted claims. • Workers Compensation Claims – This amount represents ten claims filed against the Estate by former employees for workers’ compensation benefits totaling approximately $1.1mm and an approximate $134k claim filed against the Estate by the SIF. The Court has allowed the SIF claim as an unsecured claim. All workers compensation claims are being administered Subject to Revision 16 of 17

>Delta Mills, et al Debtors’ Hypothetical Liquidation Analysis Summary of Critical Assumptions by the Debtors’ third party administrator, the Commission or the SIF. As mentioned above, the Debtors have paid the Commission or the SIF $0.75mm through the draw of a letter of credit issued to the benefit of the Commission. These funds are to be used to cover any outstanding liabilities related to workers compensation. The Debtors believe that these amounts should be sufficient to cover the majority of outstanding workers’ compensation claims and therefore these claims would be liquidated for less than their claimed amounts and only after all amounts available from the letter of credit proceeds are exhausted. For purposes of the Analysis, approximately $1.3mm in workers’ compensation and SIF claims have been included in the “Lower” scenario and approximately $134k, representing the SIF’s claim, have been included in the “Higher” scenario. • Contingent Claims Estimate – There could be the possibility of contingent claims arising from the case for a myriad of issues. The Debtors are unaware of the existence of any such claims at the present time and would likely object to any asserted claims. However, it is possible that such claims could be filed after the bar dates. As such, the Analysis includes $1.6mm for potential claims in the “Lower” and “Higher” scenarios. Subject to Revision 17 of 17