UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number: 811-04920

WASATCH FUNDS TRUST

(Exact name of registrant as specified in charter)

505 Wakara Way,

3rd Floor

Salt Lake City, UT 84108

(Address of principal executive offices)(Zip code)

| | |

| (Name and Address of Agent for Service) | | Copy to: |

| |

Samuel S. Stewart, Jr. Wasatch Advisors, Inc. 505 Wakara Way, Suite 300 Salt Lake City, UT 84108 | | Eric F. Fess, Esq. Chapman & Cutler LLP 111 West Monroe Street Chicago, IL 60603 |

Registrant’s telephone number, including area code: (801) 533-0777

Date of fiscal year end: September 30

Date of reporting period: March 31, 2014

| Item 1: | Report to Shareholders. |

Wasatch Funds

Salt Lake City, Utah

www.WasatchFunds.com

800.551.1700

This material must be accompanied or preceded by a prospectus.

Please read the prospectus carefully before you invest.

Wasatch Funds are distributed by ALPS Distributors, Inc.

1

| | | | |

LETTERTO SHAREHOLDERS — THREE YARDSANDA CLOUDOF DUST | | |

| |

| | |

| | |

| | |

Samuel S. Stewart, Jr. PhD, CFA President of

Wasatch Funds | | DEAR FELLOW SHAREHOLDERS: Former Ohio State football coach Woody Hayes was well-known for his conservative offense. He was often quoted as saying, “There are only three things that can happen when you pass, and two of them are bad.” The two bad outcomes are either an incompletion or an interception. Instead, Hayes favored a methodical, grind-it-out approach, running the ball directly into the line. Described as “three yards and a cloud of dust,” what Hayes’ style of play may have lacked in pizazz, it more than made up for in results. As head coach of the Buckeyes, Hayes compiled an impressive 205-61-10 win-lose-tie record. ECONOMY The U.S. economy today is following a similar offensive playbook, but with less satisfying results. Unlike other post-recession recoveries that featured at least one or two quarters of rapid growth — the economic equivalent of a 60-yard pass play — the current recovery has been characterized by quarter after quarter of slow, grind-it-out gains. The good news is that the economy is inching ahead, rather than slipping back into recession. The bad news is that the progress is modest and unlikely to put much of a dent in unemployment. |

The U.S. economy’s slow march forward is reflected in most of the leading indicators that I have found useful over the years. In addition, gross domestic product (GDP), which is a coincident indicator, has continued to make very small gains. A graph of U.S. GDP since 1947 (which is readily available from the Federal Reserve Bank of St. Louis) shows a remarkably smooth trend overall. But in years marked by recession and recovery, we see some significant quarterly fluctuations in GDP’s rate of change. In recession years, GDP sometimes fell by over 5% on an annualized basis. Those declines were often offset in recovery years by gains approaching or exceeding 10% on an annualized basis.

The economy has performed differently during the period that included the global financial crisis and the subsequent recovery. In 2008, GDP dropped by an annualized 8.3%, which was painful and on par with some of the worst downturns since 1947. Since the economic low in 2009, annualized GDP growth has averaged only 2.4%. This 2.4% average is certainly not what we’d expect during a “recovery,” considering that the overall average GDP growth rate since 1947 has been 3.2%. Because our current growth rate is below not only past recoveries but also below the long-term trend, you can see why I’ve dubbed this recovery as “the tortoise economy.”

GDP growth in the fourth quarter of 2013 fell to 2.6% from 4.1% for the third quarter. This trend may have weakened even further in the quarter ended March 31, 2014, partly due to the harsh winter most of the country experienced. For the entire year of 2014, I expect the overall growth rate to stay below 3%. So, like Woody Hayes’ offense, I expect our recovery to continue grinding forward. But as businesspeople and investors, we should also be aware that we’re operating within the tortoise economy.

MARKETS

Stock prices have certainly gone up a lot since the global financial crisis. For example, U.S. small-cap stocks, as represented by the Russell 2000® Index, have risen more than three-fold since the market’s bottom in 2009. Based on the dramatic rise in stock prices and my overall economic concerns, I have been cautioning investors that the market may experience periodic “air pockets,” much like an airplane that hits turbulence, drops precipitously and then recovers.

In January of 2014, my caution seemed warranted as the S&P 500® Index fell 3.46% and the Russell 2000 Index fell 2.77% for the month. But gains of 4.57% and 4.71%, respectively, in February brought both indices back into positive territory for the year-to-date. While March was bumpy, both indices remained positive for the quarter with the S&P 500 returning 1.81% and the Russell 2000 returning 1.12%.

For bonds, the ride was considerably smoother during the first quarter. The intermediate-term Barclays Capital U.S. Aggregate Bond Index rose 1.84% and the long-term Barclays U.S. 20+ Year Treasury Bond Index rose 7.73%. But at current prices, I believe that U.S. government bonds are more expensive than at almost any time in over 50 years. I continue to warn investors that if interest rates rise substantially, the declines in bond prices — particularly in long-term bond prices — could be devastating.

While I concede that the economy is sluggish, that overall stock valuations are relatively high, and that some indicators are pointing down, I remain cautiously bullish for two primary reasons. First, I believe that all market indicators must be taken with a grain of salt because the level of monetary stimulus by the Federal Reserve and other central banks has been massive, unprecedented and beyond any investor’s experience. We’re in uncharted territory, so I wouldn’t automatically assume that any indicator, positive or negative, is necessarily predictive in the current environment. Second, while the market as a whole seems overvalued, we at Wasatch invest in individual companies that we believe are unique and we take into account their valuations.

In the portfolios I manage, I’m maintaining a relatively high amount of cash, “dry powder” that I can use as I find companies with more reasonable valuations over time. Other than that, I’m sticking to the basics — like Woody Hayes — in an attempt to reduce risk. I’m operating under the philosophy of, “When in doubt, throw it out.” That means I’m pruning holdings with stock prices that seem to have gotten ahead of company fundamentals. I want my portfolios to only hold companies in which I’m comfortable with the valuations. I’m focused on companies that are growing their earnings, while at the same time maintaining or increasing their market share. This investment discipline causes me to stay away from social-media companies, for example, which may be increasing their market share, but are generally light on earnings.

2

| | |

| | MARCH 31, 2014 (UNAUDITED) |

|

|

|

Aggressive investing may have its place during a more normal economic recovery, with lower overall stock valuations and typical monetary policies in place. Today’s environment is much different. We’ve never been down this road before, and now is not the time to put the pedal to the metal. But, for the reasons discussed here, I don’t think it makes sense to abandon stocks, either. I’m simply proceeding with caution.

Despite the challenges and uncertainties we face, I’m optimistic about the future. And this optimism extends well beyond the United States. I recently returned from a trip to Southeast Asia and France. While traveling, I couldn’t help but notice the increased diversity of the other tourists I encountered. In Myanmar, for example, there were some Americans and Europeans, but also Chinese, Thais and others. This increased diversity is clear evidence of the prosperous middle class that’s spreading around the globe. While the rise of the middle class is gratifying to see because it means that overall living conditions are improving, it’s also a good sign for investors in companies that are serving the growing demands of middle-class consumers all over the world.

WASATCH

I’m pleased to announce that two Wasatch funds received a total of three 2014 Lipper Awards, which recognize mutual funds that deliver consistently strong risk-adjusted performance relative to peers.

The Wasatch World Innovators Fund (WAGTX) was honored as #1 for both the three-year and five-year periods ended December 31, 2013 among 163 and 112 global multi-cap growth funds, respectively. I manage the Fund with Josh Stewart. We focus on finding innovative companies across industries and around the globe. These companies often benefit from “creative destruction,” in which they set new standards, outmaneuver competitors, and increase market share. We also seek to invest in these companies at reasonable valuations.

The Wasatch Emerging Markets Small Cap Fund (WAEMX) was honored as #1 for the five-year period ended December 31, 2013 among 266 emerging markets funds. Portfolio Managers Roger Edgley and Laura Geritz, and Associate Portfolio Manager Andrey Kutuzov invest in small companies, many of which are meeting home-country consumer needs in emerging markets. The Fund is closed to new investors, though existing direct shareholders and intermediaries with established positions continue to have access to the Fund.

All of us at Wasatch Advisors are very proud of these awards and the performance results they represent.

With sincere thanks for your continued investment and for your trust,

Sam Stewart

President of Wasatch Funds

Information in this document regarding market or economic trends or the factors influencing historical or future performance reflects the opinions of management as of the date of this document. These statements should not be relied upon for any other purpose. Past performance is no guarantee of future results, and there is no guarantee that the market forecasts discussed will be realized.

CFA® is a trademark owned by CFA Institute.

Wasatch Advisors is the investment advisor to Wasatch Funds.

The Lipper Fund Awards program honors funds that have excelled in delivering consistently strong risk-adjusted performance relative to peers. Lipper designates award-winning funds in most individual classifications for the three-, five- and 10-year periods. Lipper Award designations are not intended to constitute investment advice or predict future results, and Lipper does not guarantee the accuracy of this information. In addition to periods of positive returns, the Wasatch Funds that received Lipper Awards experienced some periods of negative returns during the award time frames. Past performance is not indicative of future results.

The Lipper Fund Awards are part of the Thomson Reuters Awards for Excellence, a global family of awards that celebrate exceptional performance throughout the professional investment community. The Thomson Reuters Awards for Excellence recognize the world’s top funds, fund management firms, sell-side firms, research analysts, and investor relations teams. The Thomson Reuters Awards for Excellence also include the Extel Survey Awards, the StarMine Analyst Awards, and the StarMine Broker Rankings. For more information, please contact markets.awards@thomsonreuters.com or visit http://excellence.thomsonreuters.com/.

The Wasatch World Innovators Fund and the Wasatch Emerging Markets Small Cap Fund seek to provide long-term growth of capital.

Someone who is “bullish” or “a bull” is optimistic with regard to the stock market’s prospects.

Gross domestic product (GDP) is a basic measure of a country’s economic performance and is the market value of all final goods and services made within the borders of a country in a year.

Valuation is the process of determining the current worth of an asset or company.

The Russell 2000 Index is an unmanaged total return index of the smallest 2,000 companies in the Russell 3000 Index, as ranked by total market capitalization. The Russell 2000 is widely used in the industry to measure the performance of small company stocks.

The S&P 500 Index includes 500 of the United States’ largest stocks from a broad variety of industries. The Index is unmanaged but is a commonly used measure of common stock total return performance.

The Barclays Capital U.S. Aggregate Bond Index covers the U.S. investment grade fixed rate bond market, including government and corporate securities, agency mortgage pass-through securities, and asset-backed securities.

The Barclays U.S. 20+ Year Treasury Bond Index measures the performance of U.S. Treasury securities that have remaining maturities of 20 or more years.

You cannot invest directly in these or any indices.

3

| | |

| WASATCH CORE GROWTH FUND (WGROX / WIGRX) — Management Discussion | | MARCH 31, 2014 (UNAUDITED) |

|

|

|

The Wasatch Core Growth Fund is managed by a team of Wasatch portfolio managers led by JB Taylor and Paul Lambert.

| | | | |

JB Taylor Lead Portfolio Manager | |

Paul Lambert Portfolio Manager | | OVERVIEW In the quarter ended March 31, 2014, the Wasatch Core Growth Fund — Investor Class returned -1.10% and underperformed its benchmark, the Russell 2000 Index, which |

returned 1.12%. Over the same period, the Russell 2000 Growth Index returned 0.48%. When compared to the tremendous gains of 2013, returns so far in 2014 seem relatively boring. However, the period-end results don’t illustrate the “tug-of-war” that seems to have started between momentum-oriented investors and investors focused on fundamentals and reasonable valuations. We remain steadfastly in the second camp. This hurt the Fund’s returns relative to the Russell 2000 in 2013.

We take underperformance in any type of market seriously. While we aren’t content with our underperformance over the last 18 months, we recognize that a Fed-fueled, liquidity-driven market like the one we’ve experienced is not optimal for our investment approach. We remain focused on companies with sustainable competitive advantages, high returns on capital and reasonable valuations. We would welcome a market that is driven by long-term fundamentals and appropriately priced risks. There are signs this may be occurring. From the beginning of March, stocks with nosebleed valuations such as those in the biotechnology industry have been selling off and the Fund has outperformed since.

Until the recent pivot, lower-quality stocks had also been some of the market’s strongest performers. This type of performance is unusual so late in a market cycle. Typically, we’ll see the lowest-quality companies do better right off a deep market bottom, but not several years into a recovery.

DETAILSOFTHE QUARTER

One of the Fund’s top contributors for the quarter was Spirit Airlines, a low-cost, low-frills airline. The stock was up over 30% and has increased over 130% since our first purchases in April of last year. Spirit had a phenomenal quarter, growing revenues 28% and earnings over 100% as the company benefited from a growing route network and a good pricing environment.

ICON and MEDNAX were health-care holdings that contributed positively to results during the quarter. ICON provides outsourced services for managing clinical trials in the pharmaceutical, biotechnology and medical-device industries. ICON is our “picks and shovels” play on the biotech boom. While not every highly valued biotech company will deliver the FDA-approved products their investors are hoping for, most of them need the services of a company like ICON. Clinical trials are costly, are highly

specialized, and increasingly require a global reach to run effectively. ICON continues to benefit from this trend. The management team at MEDNAX continues to execute its time-tested business plan with great results. MEDNAX partners with physicians, mostly neonatologists and pediatric sub-specialists, to help manage their businesses so the doctors can focus on better clinical care. This model has worked for decades in neonatology, and now MEDNAX is expanding its business in anesthesiology.

Nu Skin Enterprises was our worst performer during the quarter. Nu Skin is a global direct seller of premium-quality personal-care products and vitamins. We purchased Nu Skin last year and the stock turned out to be one of our strongest contributors in 2013. Our original thesis, that Nu Skin’s sales in China would continue to drive exceptionally high growth rates, was proving out. This momentum was derailed in January, when an enforcement agency of the Chinese government opened an inquiry into Nu Skin’s selling practices. The company has operated in China for over a decade, and we believe Nu Skin has done everything possible to operate within the local laws. This confidence seemed well-founded in March, when the same enforcement agency closed its inquiry and fined Nu Skin a relatively paltry sum of $540,000.

IPC The Hospitalist was another detractor for the quarter. The company is the market leader in the hospitalist industry. IPC’s physicians provide more efficient care of patients and allow hospitals to better manage resources in an increasingly complex and competitive health-care environment. IPC is an example of a well-run company growing in the mid-teens that has underperformed the market.

OUTLOOK

In navigating the current market, we are sticking to our time-tested approach. We continue to focus on what we consider to be high-quality growth companies with business models demonstrating real competitive advantages. In the recently reported quarter, our current portfolio companies generated earnings growth of 19% on revenue growth of 13%. This compares well to the average Russell 2000 company, which grew earnings 8% on revenue growth of 5%. Furthermore, the average Russell 2000 company is not seeing an acceleration in revenue or earnings growth. This is another reason the market’s buoyancy over the last year has been surprising.

While stock prices are up broadly, we are not paying unrealistic prices for our companies. When looking at the average price-to-earnings ratio on expected 2014 calendar-year earnings, the Fund’s holdings trade at a modest discount to the Russell 2000. We believe this combination of above-average growth rates, below average P/E multiples, and strong business models is a good balance for navigating what could be a choppier market environment going forward.

Thank you for the opportunity to manage your assets and for your trust.

| Current | and future holdings are subject to risk. |

4

| | |

| WASATCH CORE GROWTH FUND (WGROX / WIGRX) — Portfolio Summary | | MARCH 31, 2014 (UNAUDITED) |

|

|

|

AVERAGE ANNUAL TOTAL RETURNS

| | | | | | | | | | | | | | | | |

| | | SIX MONTHS* | | | 1 YEAR | | | 5 YEARS | | | 10 YEARS | |

Core Growth (WGROX) — Investor | | | 5.71% | | | | 19.67% | | | | 26.13% | | | | 7.85% | |

Core Growth (WIGRX) — Institutional | | | 5.74% | | | | 19.75% | | | | 26.17% | | | | 7.87% | |

Russell 2000® Index | | | 9.94% | | | | 24.90% | | | | 24.31% | | | | 8.53% | |

Russell 2000® Growth Index | | | 8.69% | | | | 27.19% | | | | 25.24% | | | | 8.87% | |

Data shows past performance, which is not indicative of future performance. Current performance may be lower or higher than the performance quoted. To obtain the most recent month-end performance data available, please visit www.WasatchFunds.com. The Advisor may absorb certain Fund expenses, without which total return would have been lower. Investment returns and principal value will fluctuate and shares, when redeemed, may be worth more or less than their original cost.

As of the January 31, 2014 prospectus, the Total Annual Fund Operating Expenses for the Wasatch Core Growth Fund — Investor Class: 1.21% / Institutional Class: 1.32%, Net: 1.12%. The expense ratio shown elsewhere in this report may be different. Net expenses are based on Fund expenses, net of waivers and reimbursements. See the prospectus for additional information regarding Fund expenses.

Wasatch Funds will deduct a 2.00% redemption proceeds fee on Fund shares held 60 days or less. Performance data does not reflect the deduction of fees, including sales charges, or the taxes you would pay on fund distributions or the redemption of fund shares. Fees and taxes, if reflected, would reduce the performance quoted. Wasatch does not charge any sales fees. For more complete information including charges, risks and expenses, read the prospectus carefully.

Performance for the Institutional Class prior to 1/31/2012 is based on the performance of the Investor Class. Performance of the Fund’s Institutional Class prior to 1/31/2012 uses the actual expenses of the Fund’s Investor Class without any adjustments. For any such period of time, the performance of the Fund’s Institutional Class would have been substantially similar to, yet higher than, the performance of the Fund’s Investor Class, because the shares of both classes are invested in the same portfolio of securities, but the classes bear different expenses.

Investing in small cap funds will be more volatile and loss of principal could be greater than investing in large cap or more diversified funds. Investing in foreign securities, especially in emerging markets, entails special risks, such as currency fluctuations and political uncertainties, which are described in more detail in the prospectus.

TOP 10 EQUITY HOLDINGS**

| | | | |

| Company | | % of Net

Assets | |

| Copart, Inc. | | | 6.0% | |

| Life Time Fitness, Inc. | | | 3.6% | |

| MEDNAX, Inc. | | | 3.2% | |

| IDEX Corp. | | | 3.0% | |

| Allegiant Travel Co. | | | 2.8% | |

| | | | |

| Company | | % of Net

Assets | |

| Alliance Data Systems Corp. | | | 2.7% | |

| Waste Connections, Inc. | | | 2.7% | |

| MSC Industrial Direct Co., Inc., Class A | | | 2.4% | |

| Ensign Group, Inc. (The) | | | 2.4% | |

| Credit Acceptance Corp. | | | 2.4% | |

| ** | As of March 31, 2014, there were 66 holdings in the Fund. Foreign currency contracts, written options and repurchase agreements, if any, are not included in the number of holdings. Portfolio holdings are subject to change at any time. References to specific securities should not be construed as recommendations by the Funds or their Advisor. Current and future holdings are subject to risk. |

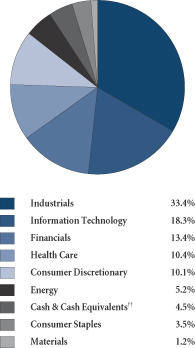

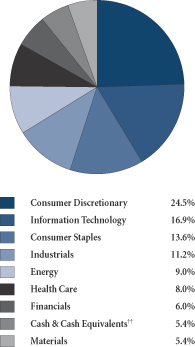

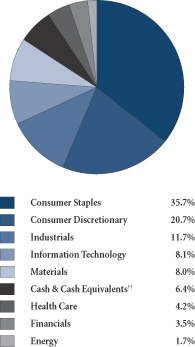

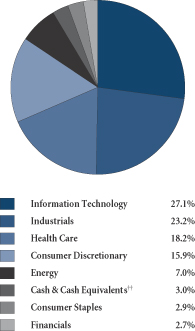

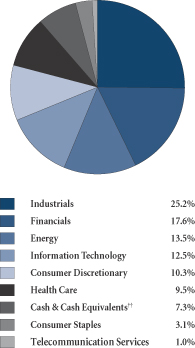

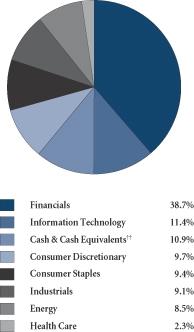

SECTOR BREAKDOWN†

| † | Excludes securities sold short and options written, if any. |

| †† | Also includes Other Assets & Liabilities. |

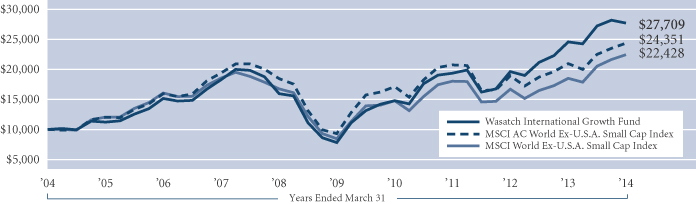

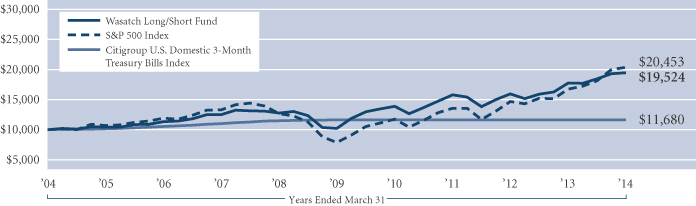

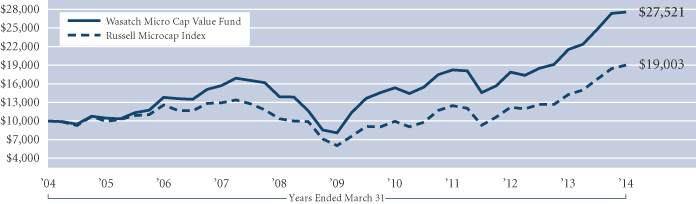

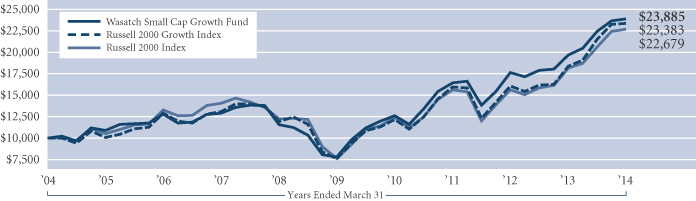

GROWTHOFA HYPOTHETICAL $10,000 INVESTMENT

Past performance does not predict future performance. The graph above does not reflect the deduction of fees, sales charges, or taxes that you would pay on fund distributions or the redemption of fund shares. Wasatch does not charge any sales fees. The Russell 2000 Index is an unmanaged total return index of the smallest 2,000 companies in the Russell 3000 Index, as ranked by total market capitalization. The Russell 2000 Index is widely regarded in the industry as accurately capturing the universe of small company stocks. The Russell 2000 Growth Index is an unmanaged total return index that measures the performance of those Russell 2000 Index companies with higher price-to-book ratios and higher forecasted growth values. You cannot invest directly in these or any indices.

5

| | |

| WASATCH EMERGING INDIA FUND (WAINX) — Management Discussion | | MARCH 31, 2014 (UNAUDITED) |

|

|

|

The Wasatch Emerging India Fund is managed by a team of Wasatch portfolio managers led by Ajay Krishnan.

| | |

Ajay Krishnan, CFA Lead Portfolio Manager | | OVERVIEW For the quarter ended March 31, 2014, the Wasatch Emerging India Fund gained 7.39% in what was a strong period for the Indian equity market. The Fund’s benchmark, the MSCI India Investable Market Index (IMI), rose 8.49%. Optimism surrounding the upcoming national elections pushed India’s major stock indices to new all-time highs. The S&P Bombay Stock |

Exchange Sensitive Index (the SENSEX) crossed the previously unseen level of 22,000, while the CNX Nifty (the Nifty) closed above 6,700 for the first time on the final trading day of the quarter. Driving the euphoria was the expectation that Narendra Modi, leader of the Bharatiya Janata Party (BJP), will become prime minister. Investors hope that Mr. Modi will be able to bring to India the same expansions in infrastructure investment and economic growth he achieved as chief minister of the state of Gujarat.

Expectations for a new cycle of infrastructure and corporate investment helped make industrials the top-performing sector of both the MSCI India IMI and the Fund. Our industrial stocks outperformed the benchmark’s industrials, and the Fund’s overweight position in this sector also helped its performance. However, our stocks rose less than the benchmark’s holdings in the financials and the consumer-staples sectors, which were the Fund’s main sources of underperformance relative to the benchmark.

We were not surprised the Fund modestly trailed its benchmark in such an aggressive market like the one we observed for most of the quarter. During sentiment-driven rallies, investors do not place as much emphasis on fundamentals, and in that circumstance, our favored stocks typically would be expected to underperform.

DETAILSOFTHE QUARTER

Our strongest contributor to performance for the quarter was MakeMyTrip, the largest online travel agency in India. Additional capacity in the Indian airline industry is benefiting the company by making air travel more affordable. Other positives for MakeMyTrip include continued strong earnings from its hotel bookings and the growing popularity of making travel reservations on the Internet. Additionally, the company’s successful completion of a secondary stock offering appears to have encouraged investors by eliminating a source of uncertainty.

Page Industries was our second-best contributor. The company makes and sells undergarments and other apparel under the Jockey brand in India, Sri Lanka, Bangladesh, Nepal and the United Arab Emirates. Earnings have been strong as major brands such as Jockey continue to gain market share at the expense of local competitors. Page also is benefiting from good distribution for its products and from its management team’s solid execution.

Our greatest detractor from performance for the quarter was India’s largest non-banking finance company, Mahindra & Mahindra Financial Services. Through its network of branches, Mahindra finances purchases of tractors, utility vehicles, cars and homes, primarily in rural India. In its most-recently reported quarter, the company’s loan provisions and write-offs increased 43% compared to the previous quarter and 121% year-over-year. As a result, earnings fell 18% versus the year-ago period, and the stock declined. However, we think at least some of the shortfall in loan collections will be made up when crops are harvested. We remain positive on the company’s long-term prospects and continue to hold the stock in the Fund.

Jubilant Foodworks operates Domino’s Pizza and Dunkin’ Donuts franchises in India. Earnings declined 10.9% year-over-year in the company’s most-recently reported quarter on higher costs for raw materials, combined with higher spending on advertising and promotion, new-product launches and new-restaurant openings. In addition, same-store sales at Jubilant’s Domino’s Pizza franchises fell 2.6% versus the year-ago period as consumers turned increasingly cautious. While disappointing, the decline in same-store sales was less than at similar chains. For example, at the KFC and Pizza Hut stores operated by YUM Restaurants India,* same-store sales fell 4%. Although Jubilant was our second-largest detractor from performance for the quarter, we believe it remains an attractive long-term holding for the Fund.

OUTLOOK

Recent data suggest the fundamentals in India are improving. In the quarter ended December 31, 2013, the current-account deficit narrowed to 0.9% of gross domestic product (GDP), its lowest level since 2010. The smaller shortfall helped support India’s currency, the rupee, which as of March 31, 2014 had risen nearly 15% since reaching an all-time low on August 28, 2013. From that low, the Fund gained 44.4% versus the benchmark’s 41.8% through March 31, 2014. The strong bounce-back illustrates the importance of patience and a long-term horizon, especially when investing in emerging markets.

Foreign investors, encouraged by improving fundamentals and the firmer rupee, have been helping fuel the gains in India’s stock market as they seek to put money to work ahead of the elections. Together with interest-rate hikes from the Reserve Bank of India, the inflows of foreign funds have contributed to the rupee’s rise.

While the BJP is likely to emerge from the elections as the largest party in India, it may fall short of a majority in parliament. Even with a strong mandate for Mr. Modi, optimism surrounding the elections may fade as the realities of governing a country the size of India become apparent.

To the extent that India’s equity market remains driven by sentiment rather than fundamentals, we would expect the Fund to lag its benchmark. Over the long term, however, we believe the strong fundamentals of our companies will enable them to outperform.

Thank you for the opportunity to manage your assets.

| * | As of March 31, 2014, the Wasatch Emerging India Fund did not hold YUM! Brands, Inc., the parent of YUM Restaurants India. |

| Current | and future holdings are subject to risk. |

6

| | |

| WASATCH EMERGING INDIA FUND (WAINX) — Portfolio Summary | | MARCH 31, 2014 (UNAUDITED) |

|

|

|

AVERAGE ANNUAL TOTAL RETURNS

| | | | | | | | | | |

| | | SIX MONTHS* | | 1 YEAR | | 5 YEARS | | SINCE INCEPTION 4/26/11 | |

Emerging India | | 22.47% | | 11.22% | | N/A | | | 3.31% | |

MSCI India IMI | | 21.02% | | 7.09% | | N/A | | | -5.71% | |

Data shows past performance, which is not indicative of future performance. Current performance may be lower or higher than the performance quoted. To obtain the most recent month-end performance data available, please visit www.WasatchFunds.com. The Advisor may absorb certain Fund expenses, without which total return would have been lower. Investment returns and principal value will fluctuate and shares, when redeemed, may be worth more or less than their original cost.

As of the January 31, 2014 prospectus, the Total Annual Fund Operating Expenses for the Wasatch Emerging India Fund are 2.99%. The Net Expenses are 1.95%. The expense ratio shown elsewhere in this report may be different. Net Expenses are based on Fund expenses, net of waivers and reimbursements. See the prospectus for additional information regarding Fund expenses.

Wasatch Funds will deduct a 2.00% redemption proceeds fee on Fund shares held 60 days or less. Performance data does not reflect the deduction of fees, including sales charges, or the taxes you would pay on fund distributions or the redemption of fund shares. Fees and taxes, if reflected, would reduce the performance quoted. Wasatch does not charge any sales fees. For more complete information including charges, risks and expenses, read the prospectus carefully.

Investing in small cap funds will be more volatile and loss of principal could be greater than investing in large cap or more diversified funds. Investing in foreign securities, especially in emerging markets, entails special risks, such as currency fluctuations and political uncertainties, which are described in more detail in the prospectus. Being non-diversified, the Fund can invest a larger portion of its assets in the stocks of a limited number of companies than a diversified fund. Non-diversification increases the risk of loss to the Fund if the values of these securities decline.

TOP 10 EQUITY HOLDINGS**

| | | | |

| Company | | % of Net

Assets | |

Cognizant Technology Solutions Corp., Class A | | | 3.3% | |

MakeMyTrip Ltd. (India) | | | 3.3% | |

Lupin Ltd. (India) | | | 3.2% | |

Gruh Finance Ltd. (India) | | | 2.8% | |

Mahindra & Mahindra Financial Services Ltd. (India) | | | 2.8% | |

| | | | |

| Company | | % of Net

Assets | |

IPCA Laboratories Ltd. (India) | | | 2.7% | |

Eicher Motors Ltd. (India) | | | 2.5% | |

HCL Technologies Ltd. (India) | | | 2.3% | |

Page Industries Ltd. (India) | | | 2.2% | |

Glenmark Pharmaceuticals Ltd. (India) | | | 2.1% | |

| ** | As of March 31, 2014, there were 63 holdings in the Fund. Foreign currency contracts, written options and repurchase agreements, if any, are not included in the number of holdings. Portfolio holdings are subject to change at any time. References to specific securities should not be construed as recommendations by the Funds or their Advisor. Current and future holdings are subject to risk. |

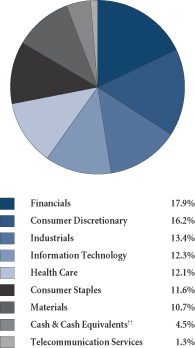

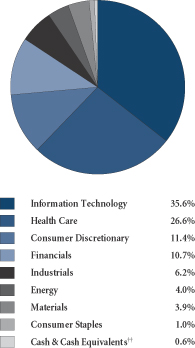

SECTOR BREAKDOWN†

| † | Excludes securities sold short and options written, if any. |

| †† | Also includes Other Assets & Liabilities. |

GROWTHOFA HYPOTHETICAL $10,000 INVESTMENT

Past performance does not predict future performance. The graph above does not reflect the deduction of fees, sales charges, or taxes that you would pay on fund distributions or the redemption of fund shares. Wasatch does not charge any sales fees. ‡Inception: April 26, 2011. The MSCI India IMI (Investable Market Index) covers all investable large, mid and small cap securities across India, targeting approximately 99% of the Indian market’s free-float adjusted market capitalization. You cannot invest directly in this or any index.

7

| | |

| WASATCH EMERGING MARKETS SELECT FUND (WAESX/WIESX) — Management Discussion | | MARCH 31, 2014 (UNAUDITED) |

|

|

|

The Wasatch Emerging Markets Select Fund is managed by a team of Wasatch portfolio managers led by Ajay Krishnan and Roger Edgley.

| | | | |

Ajay Krishnan, CFA Lead Portfolio Manager | |

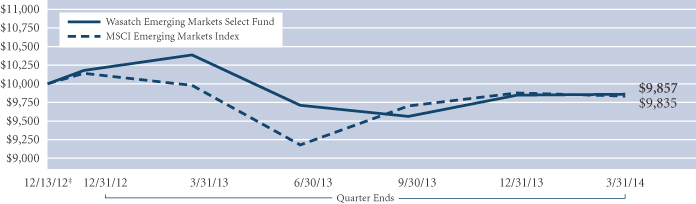

Roger Edgley, CFA Portfolio Manager | | OVERVIEW The quarter ended March 31, 2014 was a volatile period for emerging markets. The Wasatch Emerging Markets Select Fund — Investor Class returned 0.10% for the quarter and |

outperformed its benchmark, the MSCI Emerging Markets Index, which fell 0.43%.

Indonesia was the best-performing country in the Index. The policies of new central-bank governor Agus Martowardogo have helped Indonesia reduce its current-account deficit, stabilize its currency and reassure foreign investors. Also fueling recent gains in the country’s stock market has been optimism about the candidacy of Jakarta governor and presidential frontrunner Joko Widodo. While our Indonesian stocks rose less than those in the Index, that underperformance was more than offset by the Fund’s overweight position in Indonesia compared to its benchmark. As the quarter progressed, we sold two of the Fund’s three Indonesian stocks because we believed the long-term fundamentals did not support their higher prices.

Other countries in which the Fund’s overweight positions helped its performance included India and Thailand. As in Indonesia, the local currencies in India and Thailand strengthened during the quarter in response to political optimism and improving current accounts. Our stocks performed roughly in line with the benchmark’s holdings in India and outperformed in Thailand.

Geopolitical tensions impacted equity prices in Russia, making it the worst-performing country in the Index. Slowing growth in China helped make that country another of the Index’s poor performers. Although we were underweight in China and reduced the Fund’s holdings in Russia during the quarter, in both countries our stocks fell more than those in the Index and hurt the Fund’s performance relative to its benchmark.

DETAILSOFTHE QUARTER

Brazilian drug-store chain Raia Drogasil was our strongest contributor to performance for the quarter after having been our greatest detractor the previous quarter. Higher costs had been frustrating Raia Drogasil’s efforts to realize the benefits of the merger of Raia, S.A. and Drogasil, S.A. that formed the company in 2011. The merger now appears to be paying off. Adjusted net income at Raia Drogasil rose 38.2% year-over-year on 17.5% sales growth in its most-recently reported quarter. Same-store sales during the period increased 6% for mature stores and 11.9% overall as the company closed four of its less-profitable stores and opened 41 new ones.

Promotora y Operadora de Infraestructura (PINFRA) operates toll-road concessions in Mexico under contracts with the government. PINFRA continues to benefit from its strong balance sheet, solid execution and leading position in an industry serving Mexico’s significant infrastructure needs. Earnings before interest, taxes, depreciation and amortization (EBITDA) grew 20.3% in the company’s most-recently reported quarter on revenue growth of 28.5%. Investors reacted positively, and the stock was one of our best contributors during the quarter.

Russia’s annexation of Crimea from Ukraine resulted in a repricing of risk for Russian stocks and for companies with significant exposure to Russia. Two of those, Yandex and O’Key Group, were our greatest detractors for the quarter.

Although the geopolitical risk is very high, the fundamental long-term growth prospects for both companies remain favorable in our view. Yandex, based in the Netherlands, operates Russia’s main Internet search engine. The company also has a strong search presence in Belarus, Kazakhstan, Turkey and Ukraine. O’Key operates a retail chain of hypermarkets and supermarkets in Russia. The company focuses on major metropolitan areas, where we think it is well-positioned to continue taking market share from informal retail-food distributors.

Another of the Fund’s weaker stocks was SouFun Holdings, which operates the leading real-estate Internet portal in China. Concerns about a potential bubble in Chinese real-estate prices weighed on the stock. While we believe weakness in Chinese real estate may pose significant risks for the country’s shadow-banking system, we think SouFun may be relatively insulated. We are cautiously maintaining the Fund’s position as we continue to monitor the situation.

OUTLOOK

Over the next several quarters, China will be a critical country to watch. China’s importance extends well beyond its own borders to its role as an engine of growth throughout Asia. Recently, that engine has been sputtering, as reports on trade, industrial production and investment have been disappointing. Slower growth in China impacts nearby countries dependent upon Chinese imports of their raw materials and finished goods. While the U.S. and Europe appear to be on solid footing, their ability to counteract flagging Chinese demand for Asian exports may be limited. Fiscal and monetary stimulus from the Chinese government may offer the best hope for a reacceleration of growth in the region.

Hope for political change drove rallies in the equity markets of several countries with recent or upcoming elections. Although we believe the gains may be justified in countries where the fundamentals are improving, in other countries the situation is less certain.

As a result of recent sales, the Fund currently holds approximately 11% of its assets in cash. If emerging markets should come under additional stress, we believe that cash could prove to be a valuable strategic asset for capitalizing on the unique opportunities we continue to find.

Thank you for the opportunity to manage your assets.

| Current | and future holdings are subject to risk. |

8

| | |

| WASATCH EMERGING MARKETS SELECT FUND (WAESX/WIESX) — Portfolio Summary | | MARCH 31, 2014 (UNAUDITED) |

|

|

|

AVERAGE ANNUAL TOTAL RETURNS

| | | | | | | | | | | | | | | | |

| | | SIX MONTHS* | | | 1 YEAR | | | 5 YEARS | | | SINCE INCEPTION 12/13/12 | |

Emerging Markets Select (WAESX) — Investor | | | 3.10% | | | | -5.13% | | | | N/A | | | | -1.11% | |

Emerging Markets Select (WIESX) — Institutional | | | 3.34% | | | | -4.51% | | | | N/A | | | | -0.53% | |

MSCI Emerging Markets Index | | | 1.39% | | | | -1.43% | | | | N/A | | | | -1.28% | |

Data shows past performance, which is not indicative of future performance. Current performance may be lower or higher than the performance quoted. To obtain the most recent month-end performance data available, please visit www.WasatchFunds.com. The Advisor may absorb certain Fund expenses, without which total return would have been lower. Investment returns and principal value will fluctuate and shares, when redeemed, may be worth more or less than their original cost.

As of the January 31, 2014 prospectus, the Total Annual Fund Operating Expenses for the Wasatch Emerging Markets Select Fund are Investor Class — Gross: 2.40%, Net: 1.69% / Institutional Class — Gross: 2.21%, Net: 1.50%. The expense ratio shown elsewhere in this report may be different. Net Expenses are based on Fund expenses, net of waivers and reimbursements. See the prospectus for additional information regarding Fund expenses.

Wasatch Funds will deduct a 2.00% redemption proceeds fee on Fund shares held 60 days or less. Performance data does not reflect the deduction of fees, including sales charges, or the taxes you would pay on fund distributions or the redemption of fund shares. Fees and taxes, if reflected, would reduce the performance quoted. Wasatch does not charge any sales fees. For more complete information including charges, risks and expenses, read the prospectus carefully.

Investing in foreign securities, especially in emerging markets, entails special risks, such as currency fluctuations and political uncertainties, which are described in more detail in the prospectus. Investing in small cap funds will be more volatile and loss of principal could be greater than investing in large cap or more diversified funds. Being non-diversified, the Fund can invest a larger portion of its assets in the securities of a limited number of companies than a diversified fund. Non-diversification increases the risk of loss to the Fund if the values of these securities decline.

TOP 10 EQUITY HOLDINGS**

| | | | |

| Company | | % of Net

Assets | |

| Galaxy Entertainment Group Ltd. (Hong Kong) | | | 4.5% | |

| Lupin Ltd. (India) | | | 4.0% | |

| International Container Terminal Services, Inc. (Philippines) | | | 3.7% | |

| Promotora y Operadora de Infraestructura S.A.B. de C.V. (Mexico) | | | 3.5% | |

| | | | |

| Company | | % of Net

Assets | |

| Sino Biopharmaceutical Ltd. (China) | | | 3.5% | |

| SJM Holdings Ltd. (Hong Kong) | | | 3.2% | |

| Coca-Cola Icecek A.S. (Turkey) | | | 3.2% | |

| Sanlam Ltd. (South Africa) | | | 3.2% | |

| Cemex Latam Holdings S.A. (Colombia) | | | 3.2% | |

| Raia Drogasil S.A. (Brazil) | | | 3.1% | |

| ** | As of March 31, 2014, there were 34 holdings in the Fund. Foreign currency contracts, written options and repurchase agreements, if any, are not included in the number of holdings. Portfolio holdings are subject to change at any time. References to specific securities should not be construed as recommendations by the Funds or their Advisor. Current and future holdings are subject to risk. |

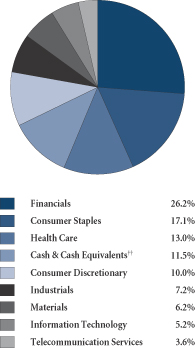

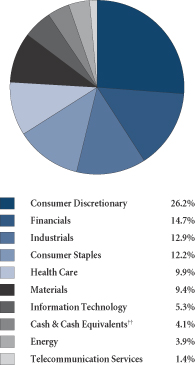

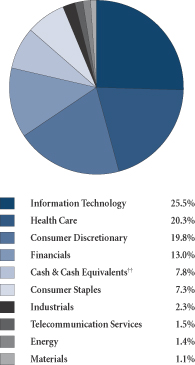

SECTOR BREAKDOWN†

| † | Excludes securities sold short and options written, if any. |

| †† | Also includes Other Assets & Liabilities. |

GROWTHOFA HYPOTHETICAL $10,000 INVESTMENT

Past performance does not predict future performance. The graph above does not reflect the deduction of fees, sales charges, or taxes that you would pay on fund distributions or the redemption of fund shares. Wasatch does not charge any sales fees. ‡Inception: December 13, 2012. The MSCI Emerging Markets Index is a free float-adjusted market capitalization index designed to measure equity market performance of emerging markets. You cannot invest directly in this or any index.

9

| | |

| WASATCH EMERGING MARKETS SMALL CAP FUND (WAEMX) — Management Discussion | | MARCH 31, 2014 (UNAUDITED) |

|

|

|

The Wasatch Emerging Markets Small Cap Fund is managed by a team of Wasatch portfolio managers led by Roger Edgley, Laura Geritz and Andrey Kutuzov.

| | | | |

Roger Edgley, CFA Lead Portfolio Manager | |

Laura Geritz, CFA Portfolio Manager | |

Andrey Kutuzov, CFA Associate Portfolio Manager |

OVERVIEW

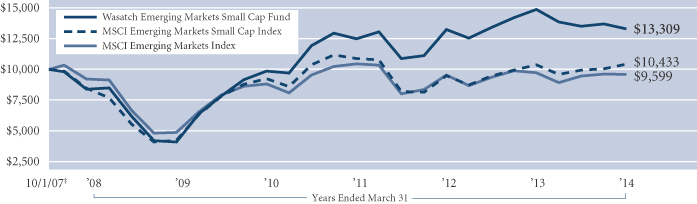

The Wasatch Emerging Markets Small Cap Fund returned -3.02% for the quarter ended March 31, 2014 and underperformed the MSCI Emerging Markets Small Cap Index, which returned 3.54%. Performance in emerging market equities was volatile during the quarter. In late January into the first part of February, stocks slid as weak U.S. data raised concerns over the ability of emerging market economies to withstand higher U.S. interest rates on top of softer demand from China. Entering March, geopolitics moved to the forefront, as tensions between Russia and Ukraine rose sharply, culminating in Russia’s annexation of Crimea. Stocks were volatile but mostly traded within a band throughout March.

DETAILSOFTHE QUARTER

The performance of the Fund’s Russian holdings reflected the challenging macro environment. TCS Group, Russia’s leading provider of online retail financial services; M Video, Russia’s largest electronic retail chain; O’Key Group, a fast growing food retailer; MD Medical Group, the leading provider of pre-natal health care; and Global Ports, a leading regional container port operator, were all down in March and detracted from performance for the quarter.

While hopes of stimulus measures to support China’s economy emerged toward the end of the quarter, the Fund’s Chinese stocks were generally down. The Fund continues to be structurally underweight in China and we continue to be highly selective of Chinese companies, as we believe there are real long-term issues that will be difficult to address. Biostime International, a pediatric nutrition and baby care products provider, and Sa Sa International, the largest specialty cosmetics retailer in Hong Kong, were among the Fund’s largest detractors from performance in the quarter.

Student protests in Taiwan continued to delay the passing of a trade pact with China and our Taiwanese stocks were generally weak. The Fund is structurally underweight versus the benchmark in Taiwan at nearly 16% versus the benchmark at approximately 21%. Several of the Fund’s holdings provided solid performance during the quarter, including Airtac International, a pneumatic equipment company with substantial business in China. Other stocks were down, including St. Shine Optical, a contact lens manufacturer.

The Fund’s holdings in India also detracted from absolute and relative performance. The Fund is structurally overweight in India. We have been able to find what we believe are high quality companies with strong corporate governance that fit our investment profile broadly across sectors. A notable detractor was Mahindra & Mahindra Financial Services. Mahindra is a vehicle financier focused on the rural economy of India. The stock has been weak as there were questions surrounding the asset quality in some of the Southern Indian states. Some of these concerns appear to be a matter of timing (collection of payments) and we continue to be constructive on the company’s long-term growth prospects.

The Fund’s holdings in Korea significantly outperformed, up approximately 15% versus the benchmark, which was up about 5%. The Fund is underweight in Korea. We see real opportunities in small cap companies in Korea and have been adding to the Fund’s weight. Some of the attractive main themes we see are in tourism, the Internet and technology companies. We are also seeing the emergence of entrepreneurial, founder-owned, non-chaebol, next-generation companies that have know-how and technology. Hotel Shilla, a hotel and leisure company, was the portfolio’s top contributor, as the stock rose over 27% during the quarter. Paradise, a gaming company, and Hanssem, a manufacturer of kitchen and bath cabinetry, were also among the Fund’s top 10 contributors.

OUTLOOK

One of the trends we are seeing unfold is increasing geopolitical risk globally. The impact is going to be felt throughout the world, whether in developed, emerging or frontier markets as rising geopolitical agitation tends to lead to slowing economic growth and rising risk premiums across the globe. While we are not, nor do we claim to be, experts on geopolitics, we are certainly cognizant of the impact conflict, real or perceived, could have on our companies. We are usually very careful about where we invest and the geopolitical flare-up between Russia and Ukraine caught us by surprise.

Overall, conditions for the companies held by the Fund remain benign. While emerging world growth is slowing, compounded by increasing cost of capital as central banks in emerging markets hike interest rates to offset currency weakness, our companies generally have been able to maintain rock-solid balance sheets and industry-leading margins. While in good times the rising tide lifts all boats, in challenging times like these our companies have been able to gain market share and continue to invest in products and innovation, even as the competition pulls back. As a result, we believe our companies will be well-positioned to take advantage of the new up-cycle in stronger form.

Thank you for your trust and the opportunity to manage your assets.

| Current | and future holdings are subject to risk. |

10

| | |

| WASATCH EMERGING MARKETS SMALL CAP FUND (WAEMX) — Portfolio Summary | | MARCH 31, 2014 (UNAUDITED) |

|

|

|

AVERAGE ANNUAL TOTAL RETURNS

| | | | | | | | | | | | | | | | |

| | | SIX MONTHS* | | | 1 YEAR | | | 5 YEARS | | | SINCE INCEPTION 10/1/07 | |

Emerging Markets Small Cap | | | -1.61% | | | | -10.64% | | | | 26.47% | | | | 4.50% | |

MSCI Emerging Markets Small Cap Index | | | 4.84% | | | | 0.40% | | | | 19.70% | | | | 0.65% | |

MSCI Emerging Markets Index | | | 1.39% | | | | -1.43% | | | | 14.48% | | | | -0.63% | |

Data shows past performance, which is not indicative of future performance. Current performance may be lower or higher than the performance quoted. To obtain the most recent month-end performance data available, please visit www.WasatchFunds.com. The Advisor may absorb certain Fund expenses, without which total return would have been lower. Investment returns and principal value will fluctuate and shares, when redeemed, may be worth more or less than their original cost.

As of the January 31, 2014 prospectus, the Total Annual Fund Operating Expenses for the Wasatch Emerging Markets Small Cap Fund are 2.06%. The Net Expenses are 1.95%. The expense ratio shown elsewhere in this report may be different. Net Expenses are based on Fund expenses, net of waivers and reimbursements. See the prospectus for additional information regarding Fund expenses.

Wasatch Funds will deduct a 2.00% redemption proceeds fee on Fund shares held 60 days or less. Performance data does not reflect the deduction of fees, including sales charges, or the taxes you would pay on fund distributions or the redemption of fund shares. Fees and taxes, if reflected, would reduce the performance quoted. Wasatch does not charge any sales fees. For more complete information including charges, risks and expenses, read the prospectus carefully.

Investing in foreign securities, especially in emerging markets, entails special risks, such as currency fluctuations and political uncertainties, which are described in more detail in the prospectus. Investing in small cap funds will be more volatile and loss of principal could be greater than investing in large cap or more diversified funds.

TOP 10 EQUITY HOLDINGS**

| | | | |

| Company | | % of Net

Assets | |

Hotel Shilla Co. Ltd. (Korea) | | | 2.0% | |

Merida Industry Co. Ltd. (Taiwan) | | | 2.0% | |

Paradise Co. Ltd. (Korea) | | | 1.9% | |

Grand Korea Leisure Co. Ltd. (Korea) | | | 1.8% | |

International Container Terminal Services, Inc. (Philippines) | | | 1.8% | |

| | | | |

| Company | | % of Net

Assets | |

St. Shine Optical Co. Ltd. (Taiwan) | | | 1.8% | |

Promotora y Operadora de Infraestructura S.A.B. de C.V. (Mexico) | | | 1.8% | |

Ulker Biskuvi Sanayi A.S. (Turkey) | | | 1.7% | |

Chailease Holding Co. Ltd. (Taiwan) | | | 1.7% | |

Pidilite Industries Ltd. (India) | | | 1.7% | |

| ** | As of March 31, 2014, there were 96 holdings in the Fund. Foreign currency contracts, written options and repurchase agreements, if any, are not included in the number of holdings. Portfolio holdings are subject to change at any time. References to specific securities should not be construed as recommendations by the Funds or their Advisor. Current and future holdings are subject to risk. |

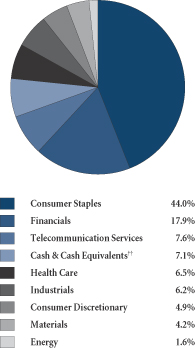

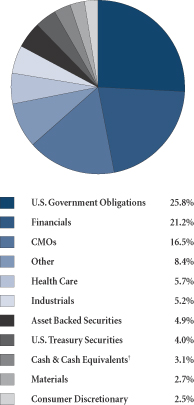

SECTOR BREAKDOWN†

| † | Excludes securities sold short and options written, if any. |

| †† | Also includes Other Assets & Liabilities. |

GROWTHOFA HYPOTHETICAL $10,000 INVESTMENT

Past performance does not predict future performance. The graph above does not reflect the deduction of fees, sales charges, or taxes that you would pay on fund distributions or the redemption of fund shares. Wasatch does not charge any sales fees. ‡Inception: October 1, 2007. The MSCI Emerging Markets and Emerging Markets Small Cap indices are free float-adjusted market capitalization indices designed to measure the equity market performance of emerging markets. You cannot invest directly in these or any indices.

11

| | |

| WASATCH FRONTIER EMERGING SMALL COUNTRIES FUND (WAFMX) — Management Discussion | | MARCH 31, 2014 (UNAUDITED) |

|

|

|

The Wasatch Frontier Emerging Small Countries Fund is managed by a team of Wasatch portfolio managers led by Laura Geritz.

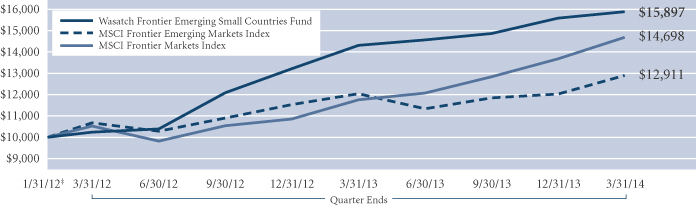

| | |

Laura Geritz, CFA Lead Portfolio Manager | | OVERVIEW The Wasatch Frontier Emerging Small Countries Fund returned 1.93% for the quarter ended March 31, 2014, underperforming its primary benchmark, the MSCI Frontier Emerging Markets Index, and the MSCI Frontier Markets Index, which gained 7.28% and 7.41%, respectively. Frontier markets finished the quarter well ahead of their emerging and developed market peers with some of the best performance coming from |

the Middle East in the United Arab Emirates (U.A.E.), Qatar and Kuwait — countries where the Fund is underweight relative to the benchmark. It appears these markets are being driven by two different but intertwined catalysts. The first is the upgrade of the U.A.E. and Qatar from frontier to emerging market status with their placement in the MSCI Emerging Markets Index. The second is Kuwait being left behind in the Frontier Emerging Markets Index but with a much larger position. The upgrade announcement was made in June of 2013 with the index changes becoming effective in May of this year. It was at the approximate time of this announcement that the Fund started to underperform relative to the Index.

We recognized that some of these markets in the Middle East had low valuations. We sought to invest in quality companies when we discovered them on fundamental research trips, but we saw a risk to the Fund’s short-term performance relative to the Index if valuation bounced up. We were also unable to find enough names that we thought were high enough quality to have the Fund’s weight match that of the benchmark in the Middle East. The stock prices of a number of inexpensive, cyclical companies in the Middle East have risen significantly. In addition, lower-quality companies, including a handful of cyclical property companies, led the rally in markets like the U.A.E. and our names, which we consider to be higher-quality, just didn’t keep up. When reviewing the companies that have led the rally, their stocks no longer seem inexpensive, and we do not believe market rallies driven by low-quality, cyclical companies are sustainable. In contrast, we feel we have a broadly positioned portfolio of high-quality stocks that should do well when this low-quality surge ends.

DETAILSOFTHE QUARTER

Looking at results for the quarter, the Fund had strong performance due to stock-picking and an overweight position in Bangladesh. A number of our best contributing stocks came from this market, including Square Pharmaceuticals, British American Tobacco Bangladesh and Olympic Industries. Saudi Arabia, a country we consider to be a frontier market, also added a number of top contributors including Abdullah Al Othaim Markets and Jarir Marketing. Our team was on the ground in Saudi Arabia during the quarter.

While the outlook for growth is still good, we are watching valuations carefully — the Saudi market has had a big move.

Our worst contributing market was Nigeria. Our stocks declined slightly more than those in the Index and our overweight hurt. Names like Zenith Bank, Nestlé Foods Nigeria, Guinness Nigeria and Cadbury Nigeria all contracted during the quarter. The good news is that valuations in Nigeria look attractive, and since quarter-end, we have been seeing a strong recovery in a number of our names.

I’m often asked the question, “Have frontier markets come too far too fast?” Frontier markets have enjoyed a sustained period of outperformance…their salad days. Investors have been attracted to the asset class on hopes of better growth than they are seeing in either the emerging or the developed world and on prospects of better diversification benefits. What’s curious to me is that markets that have had higher correlation to the developed world (e.g., those in the Middle East) have been driving recent performance. There are signs of a momentum trade gone too far — of valuations in some parts of the world that are rising too quickly. We are not chasing these investments.

OUTLOOK

The Fund is not positioned to keep up with the movements in the current market environment. Shareholder money should be treated dearly. When markets get too hot, we are willing to step back, stay diversified, and focus on quality. In other words, we are willing to lose a short-term battle in order to retain the potential to deliver good consistent returns over the long term. The U.S. economy is seeing some benefit in the short run, and this is helping other regions of the world, the Middle East and Frontier Europe, to cyclical recoveries. I’m worried that equity markets have gotten too hot in some regions of the world. It might simply be the shifting of the sands — the graduation of the U.A.E. and Qatar from frontier to emerging and the increasing weight of Kuwait in the frontier index. When these regions of the world are stripped away, frontier valuations look reasonable.

While I’m cognizant of a run up of stock prices in the Middle East, I’m optimistic about the portfolio we’ve constructed. I believe it is positioned to hold up well if the market pulls back, which we believe is possible given this stage of the rally. The Fund is composed of a unique and differentiated set of frontier market countries and companies. We believe our companies have outstanding potential for long-term growth and valuations look reasonable. However, we are always aware of where our countries sit in relation to the rest of the world.

Thank you for your investment.

| Current | and future holdings are subject to risk. |

12

| | |

| WASATCH FRONTIER EMERGING SMALL COUNTRIES FUND (WAFMX) — Portfolio Summary | | MARCH 31, 2014 (UNAUDITED) |

|

|

|

AVERAGE ANNUAL TOTAL RETURNS

| | | | | | | | | | | | | | |

| | | SIX MONTHS* | | | 1 YEAR | | | 5 YEARS | | SINCE INCEPTION 1/31/12 | |

Frontier Emerging Small Countries | | | 6.92% | | | | 11.03% | | | N/A

| | | 23.88% | |

MSCI Frontier Emerging Markets Index | | | 8.94% | | | | 7.17% | | | N/A | | | 12.52% | |

MSCI Frontier Markets Index | |

| 14.44%

|

| | | 24.99% | | | N/A | | | 19.46% | |

Data shows past performance, which is not indicative of future performance. Current performance may be lower or higher than the performance quoted. To obtain the most recent month-end performance data available, please visit www.WasatchFunds.com. The Advisor may absorb certain Fund expenses, without which total return would have been lower. Investment returns and principal value will fluctuate and shares, when redeemed, may be worth more or less than their original cost.

As of the January 31, 2014 prospectus, the Total Annual Fund Operating Expenses for the Wasatch Frontier Emerging Small Countries Fund are 2.43%. The Net Expenses are 2.25%. The expense ratio shown elsewhere in this report may be different. Net Expenses are based on Fund expenses, net of waivers and reimbursements. See the prospectus for additional information regarding Fund expenses.

Wasatch Funds will deduct a 2.00% redemption proceeds fee on Fund shares held 60 days or less. Performance data does not reflect the deduction of fees, including sales charges, or the taxes you would pay on fund distributions or the redemption of fund shares. Fees and taxes, if reflected, would reduce the performance quoted. Wasatch does not charge any sales fees. For more complete information including charges, risks and expenses, read the prospectus carefully.

Investing in small cap funds will be more volatile and loss of principal could be greater than investing in large cap or more diversified funds. Investing in foreign securities, especially in frontier and emerging markets, entails special risks, such as currency fluctuations and political uncertainties, which are described in more detail in the prospectus. Being non-diversified, the Fund can invest a larger portion of its assets in the stocks of a limited number of companies than a diversified fund. Non-diversification increases the risk of loss to the Fund if the values of these securities decline.

TOP 10 EQUITY HOLDINGS**

| | | | |

| Company | | % of Net

Assets | |

| Safaricom Ltd. (Kenya) | | | 3.3% | |

| Viet Nam Dairy Products JSC (Vietnam) | | | 3.0% | |

| MTN Group Ltd. (South Africa) | | | 2.9% | |

| Universal Robina Corp. (Philippines) | | | 2.8% | |

| Nestlé Nigeria plc (Nigeria) | | | 2.8% | |

| | | | |

| Company | | % of Net

Assets | |

| East African Breweries Ltd. (Kenya) | | | 2.4% | |

| Square Pharmaceuticals Ltd. (Bangladesh) | | | 2.4% | |

| Qatar National Bank (Qatar) | | | 2.2% | |

| Nigerian Breweries plc (Nigeria) | | | 2.0% | |

| Brasseries Maroc (Morocco) | | | 1.9% | |

| ** | As of March 31, 2014, there were 126 holdings in the Fund. Foreign currency contracts, written options and repurchase agreements, if any, are not included in the number of holdings. Portfolio holdings are subject to change at any time. References to specific securities should not be construed as recommendations by the Funds or their Advisor. Current and future holdings are subject to risk. |

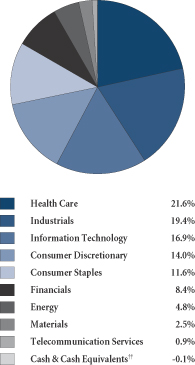

SECTOR BREAKDOWN†

| † | Excludes securities sold short and options written, if any. |

| †† | Also includes Other Assets & Liabilities. |

GROWTHOFA HYPOTHETICAL $10,000 INVESTMENT

Past performance does not predict future performance. The graph above does not reflect the deduction of fees, sales charges, or taxes that you would pay on fund distributions or the redemption of fund shares. Wasatch does not charge any sales fees. ‡Inception: January 31, 2012. The MSCI Frontier Emerging Markets and MSCI Frontier Markets indices are free float-adjusted market capitalization indices designed to measure the equity market performance of the global frontier and emerging markets. You cannot invest directly in these or any indices.

13

| | |

| WASATCH GLOBAL OPPORTUNITIES FUND (WAGOX) — Management Discussion | | MARCH 31, 2014 (UNAUDITED) |

|

|

|

The Wasatch Global Opportunities Fund is managed by a team of Wasatch portfolio managers led by JB Taylor and Ajay Krishnan.

| | | | |

JB Taylor Lead Portfolio Manager | |

Ajay Krishnan, CFA Lead Portfolio Manager | | OVERVIEW In general, small cap equities began 2014 on a positive note. The MSCI AC World Small Cap Index gained 2.90% in the quarter ended March 31, 2014, and the Wasatch Global Opportunities Fund returned -2.06%. |

International small cap markets rose 3.47%, as measured by the MSCI AC World Ex-U.S.A. Small Cap Index. European equities performed especially well, as the euro zone recovery that began last spring showed signs of strengthening. Markets in Portugal, Italy, Spain and France posted double-digit gains for the quarter. Emerging markets rallied strongly in February and March after several countries took steps to narrow their current account deficits and support their currencies.

In the United States, small caps rose 2.39% for the quarter, as measured by the MSCI U.S.A. Small Cap Index. The market was volatile — the Index was down almost 5% through early February and then up almost 5% by early March. We believe the volatility was a function of investors trying to determine if continued gains in U.S. small caps were justified on the heels of last year’s exceptional returns. Their indecision was driven by several factors, including new leadership at the Federal Reserve, signs the housing recovery was losing momentum and conflicting reports on the health of the job market.

DETAILSOFTHE QUARTER

Our international holdings, which on average during the quarter represented about 60% of the Fund, lost more than 3% in the quarter, trailing the 3.47% gain in the MSCI AC World Ex-U.S.A. Small Cap Index. In developed markets, the Fund benefited from good stock selection in Japan and Norway where MonotaRO (Japan) and TGS-NOPEC Geophysical (Norway) were strong performers. Conversely, stock selection in Italy and the United Kingdom detracted. In emerging markets, being overweight in India and Indonesia added nearly 1.5% to relative performance, and stock selection in Brazil was a plus. However, these and other positive effects were overshadowed by the Fund’s positioning in Russia and China.

Two of the worst-performing stocks in the portfolio were Eurasia Drilling, a provider of oilfield services, and TCS Group, an online financial services firm. Both of these Russian stocks fell sharply in response to the unforeseen events in Ukraine, which led the United States and European Union to impose economic sanctions on Russia. We believe the fundamentals of Eurasia Drilling and TCS are sound but are reviewing these positions in light of the political crisis.

The Fund’s U.S. stocks, which accounted for about 38% of the portfolio, rose just over 1%, a result that trailed the 2.39% gain in the MSCI U.S.A. Small Cap Index. Strong stock selection in the health care and industrial sectors was offset by weakness elsewhere, most notably in some of our financial and consumer holdings.

Our U.S. health care stocks gained more than 9% overall, and Covance was one of our top-contributing stocks in the sector. Covance is a long-time holding and one of the bigger cap names in the Fund. The contract research organization (CRO) runs clinical trials for drug manufacturers and biotech firms. Increasingly, to have a really robust clinical trial, it has to be conducted globally. As a result, more business is being awarded to CROs like Covance, whose global reach allows them to access patients from around the world.

Knight Transportation was the top U.S. contributor in the Fund. We have owned Knight for a while and have always believed that it is the best-run trucking company in the country. That said, this was one of the stock’s first quarters of significant outperformance in about two years. The confounding part of this story is that the economy had been gaining momentum throughout this time, but the operating results of trucking companies were not improving. If anything, the industry was still losing capacity as truckers continued to go out of business following the 2008 - 2009 recession. The overcapacity that existed seems to have finally been weeded out and, with volumes still growing, trucking companies are finally starting to have pricing power.

Hibbett Sports was one of our weaker U.S. stocks. Hibbett operates a chain of stores that sell everyday sporting apparel and equipment, mainly in small towns across the United States. Because it doesn’t focus on trendier merchandise, which goes in and out of fashion, the company’s business has generally been very steady. However, the stock was impacted by the current perception that, if a retailer isn’t Internet retail, it can’t be that interesting. The price-to-earnings (P/E) ratio of predominately “brick-and-mortar” Hibbett has come down as a result. While sentiment may have taken a turn for the worse, Hibbett’s management team continues to execute well, and we remain positive on the stock.

OUTLOOK

Given the positive dynamics at work in many emerging countries, we believe our relatively high exposure to these markets has the potential to benefit the Fund in the months ahead. Additionally, we are starting to see signs that market leadership in the United States may be shifting from speculative and lower-quality, cyclical stocks to quality growth stocks. This also bodes well for the Fund.

Thank you for the opportunity to manage your assets.

| Current | and future holdings are subject to risk. |

14

| | |

| WASATCH GLOBAL OPPORTUNITIES FUND (WAGOX) — Portfolio Summary | | MARCH 31, 2014 (UNAUDITED) |

|

|

|

AVERAGE ANNUAL TOTAL RETURNS

| | | | | | | | | | | | | | | | | | | | |

| | | SIX MONTHS* | | 1 YEAR | | 5 YEARS | | SINCE INCEPTION 11/17/08 |

Global Opportunities | | | | 3.94% | | | | | 13.35% | | | 23.72% | | | | 24.10% | |

MSCI AC World Small Cap Index | | | | 9.91% | | | | | 20.74% | | | 23.77% | | | | 21.46% | |

Data shows past performance, which is not indicative of future performance. Current performance may be lower or higher than the performance quoted. To obtain the most recent month-end performance data available, please visit www.WasatchFunds.com. The Advisor may absorb certain Fund expenses, without which total return would have been lower. Investment returns and principal value will fluctuate and shares, when redeemed, may be worth more or less than their original cost.

As of the January 31, 2014 prospectus, the Total Annual Fund Operating Expenses for the Wasatch Global Opportunities Fund are 1.80%. The expense ratio shown elsewhere in this report may be different. See the prospectus for additional information regarding Fund expenses.

Wasatch Funds will deduct a 2.00% redemption proceeds fee on Fund shares held 60 days or less. Performance data does not reflect the deduction of fees, including sales charges, or the taxes you would pay on fund distributions or the redemption of fund shares. Fees and taxes, if reflected, would reduce the performance quoted. Wasatch does not charge any sales fees. For more complete information including charges, risks and expenses, read the prospectus carefully.

Investing in small and micro cap funds will be more volatile and loss of principal could be greater than investing in large cap or more diversified funds. Investing in foreign securities, especially in emerging markets, entails special risks, such as currency fluctuations and political uncertainties, which are described in more detail in the prospectus.

TOP 10 EQUITY HOLDINGS**

| | | | |

| Company | | % of Net

Assets | |

| Lupin Ltd. (India) | | | 2.9% | |

| MakeMyTrip Ltd. (India) | | | 2.4% | |

| Wirecard AG (Germany) | | | 2.4% | |

| IPCA Laboratories Ltd. (India) | | | 2.1% | |

| Promotora y Operadora de Infraestructura S.A.B. de C.V. (Mexico) | | | 1.9% | |

| | | | |

| Company | | % of Net

Assets | |

| Covance, Inc. | | | 1.9% | |

| International Container Terminal Services, Inc. (Philippines) | | | 1.8% | |

| SouFun Holdings Ltd. ADR (China) | | | 1.8% | |

| Coca-Cola Icecek A.S. (Turkey) | | | 1.8% | |

| Qualicorp S.A. (Brazil) | | | 1.7% | |

| ** | As of March 31, 2014, there were 82 holdings in the Fund. Foreign currency contracts, written options and repurchase agreements, if any, are not included in the number of holdings. Portfolio holdings are subject to change at any time. References to specific securities should not be construed as recommendations by the Funds or their Advisor. Current and future holdings are subject to risk. |

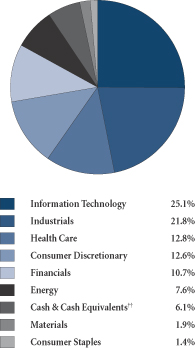

SECTOR BREAKDOWN†

| † | Excludes securities sold short and options written, if any. |

| †† | Also includes Other Assets & Liabilities. |

GROWTHOFA HYPOTHETICAL $10,000 INVESTMENT

Past performance does not predict future performance. The graph above does not reflect the deduction of fees, sales charges, or taxes that you would pay on fund distributions or the redemption of fund shares. Wasatch does not charge any sales fees. ‡Inception: November 17, 2008. The MSCI AC (All Country) World Small Cap Index is an unmanaged index and includes reinvestment of all dividends of issuers located in countries throughout the world representing developed and emerging markets. This index is a free float-adjusted market capitalization index designed to measure the performance of small capitalization securities. You cannot invest directly in this or any index.

15

| | |

| WASATCH HERITAGE GROWTH FUND (WAHGX) — Management Discussion | | MARCH 31, 2014 (UNAUDITED) |

|

|

|

The Wasatch Heritage Growth Fund is managed by a team of Wasatch portfolio managers led by Chris Bowen.

| | |

Chris Bowen Lead Portfolio Manager | | OVERVIEW In comparison with the gains of recent quarters, the stock market tempered during the three months ended March 31, 2014 but still finished in positive territory. The Wasatch Heritage Growth Fund gained 1.25% and slightly underperformed its primary benchmark, the Russell Midcap Growth Index, which was up 2.04%. The U.S. markets essentially shrugged off the Federal Reserve’s continuing withdrawal of its asset purchase program |

under new Fed chair Janet Yellen, as well as strained international relations caused by Russia’s annexation of Crimea.

The Fund benefited from stellar stock performance from a number of holdings, including Spirit Airlines and a pair of energy-related companies, Ultra Petroleum and CARBO Ceramics. Unfortunately, a large portion of the positive result was offset by disappointing declines in LKQ and Nu Skin. We continue to hold these stocks. We believe that there was no fundamental reason for the pullback in the stock price of LKQ. Nu Skin was impacted by some negative developments in its rapidly growing Chinese business.

DETAILSOFTHE QUARTER

In our search for quality companies, we spend a great deal of time researching management teams because we believe it is a crucial element for investing success. We look for those with demonstrated success in an industry, a focus on prudent spending and long-term, sustainable plans for growing their businesses. This naturally aligns with our philosophy of investing for the long run. Of course, our assessment of quality goes beyond the management teams and ultimately hinges on the results the companies are able to produce. Relative to the benchmark, on average, the Fund’s holdings have better return on capital metrics, use less financial leverage, and have comparable growth metrics.

Spirit Airlines has many of the attributes we seek and has been an outstanding investment since we purchased the stock less than a year ago. Spirit was the largest contributor to the Fund’s performance for the quarter. The ultra-discount, no frills airline continues to grow by entering new markets as a low-cost alternative to the big carriers. It would be easy for an airline like Spirit to try to grow faster by spending more, but the management team appears to be sticking to its plan. We are keeping a close eye on Spirit’s valuation with the stock up over 130% since our initial purchase.

Ultra Petroleum, an oil and natural gas exploration and production company, was able to capitalize on a steep increase in natural gas prices. It has also made some property acquisitions, which we feel will benefit the company in the coming years.

CARBO Ceramics, a provider of proppants that are used in oil and gas “fracking,” has staged a strong rebound.

Competition — especially from cheaper, but lower quality imported proppants — seems to be easing. We believe that CARBO has a technologically superior product that will benefit as energy companies continue to look for ways to improve their returns from drilling.

The downward pressure on the stock price of LKQ seemed to have been caused primarily by short sellers. We have examined in depth the contentions of those betting against the company and we don’t think anything has fundamentally changed for LKQ’s prospects. We believe LKQ will continue to consolidate a very fragmented industry that supplies replacement non-OEM and salvage parts to auto and body shops. Management has been adept at adding complementary businesses, making LKQ a one-stop shop for everything that a repair shop needs. LKQ’s valuation also remains attractive to us.