UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 |

| |

| FORM 10-K |

| (Mark One) |

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| | For the fiscal year ended December 31, 2011 |

| | Or |

| o | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| | For the transition period from _________________ to _______________________ |

| | |

| Commission file number: 000-50571 |

| |

| RESPONSE BIOMEDICAL CORPORATION |

| (Exact name of registrant as specified in its charter) |

| |

| Vancouver, British Columbia, Canada | 98 -1042523 |

(State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification Number) |

1781 - 75th Avenue W. Vancouver, British Columbia, Canada | V6P 6P2 |

| (Address of principal executive offices) | (Zip Code) |

| | |

| Registrant's telephone number, including area code: (604) 456-6010 |

Securities registered pursuant to Section 12(b) of the Act: NONE Securities registered pursuant to Section 12(g) of the Act: COMMON STOCK WITHOUT PAR VALUE |

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes o No x |

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes o No x |

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No o |

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No o |

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of the registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. x |

| Indicate by check mark whether the Registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of "large accelerated filer," "accelerated filer" and "smaller reporting company" in Rule 12b-2 of the Exchange Act. |

Large accelerated filer o | Accelerated filer o | Non-accelerated filer o (Do not check if a smaller reporting company) | Smaller reporting company x |

Indicate by check mark if the Registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes o No x |

| The aggregate market value of the voting common stock held by non-affiliates of the Registrant (assuming officers, directors and 10% stockholders are affiliates), based on the last sale price for such stock on June 30, 2011: $14,136,998. The Registrant has no non-voting common stock. |

As of March 23, 2012, there were 129,078,166 shares of the Registrant's common stock outstanding. |

|

DOCUMENTS INCORPORATED BY REFERENCE |

Portions of the Registrant's Proxy Statement for the 2012 Annual Meeting of Stockholders of the Registrant to be held on June 19, 2012 are incorporated by reference into Part III of this Form 10-K. The Registrant makes available free of charge on or through its website (http://www.responsebio.com) its Annual Report on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K and any amendments to those reports filed or furnished pursuant to Section 13(a) or 15(d) of the Securities Exchange Act of 1934. The material is made available through the Registrant's website as soon as reasonably practicable after the material is electronically filed with or furnished to the U.S. Securities and Exchange Commission, or SEC. All of the Registrant's filings may be read or copied at the SEC's Public Reference Room at 100 F Street, N.E., Room 1580, Washington D.C. 20549. Information on the hours of operation of the SEC's Public Reference Room can be obtained by calling the SEC at 1-800-SEC-0330. The SEC maintains a website (http://www.sec.gov) that contains reports and proxy and information statements of issuers that file electronically. |

| |

RESPONSE BIOMEDICAL CORPORATION

Form 10-K – ANNUAL REPORT

For the Fiscal Year Ended December 31, 2011

Table of Contents

| | | Page |

| | | |

| PART I |

| |

| Item 1. | Business | 2 |

| Item 1A. | Risk Factors | 18 |

| Item 2. | Properties | 32 |

| Item 3. | Legal Proceedings | 32 |

| Item 4. | Mine Safety Disclosures | 32 |

| | | |

| PART II |

| | | |

| Item 5. | Market for Registrant's Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities | 33 |

| Item 6. | Selected Financial Data | 34 |

| Item 7. | Management's Discussion and Analysis of Financial Condition and Results of Operations | 35 |

| Item 7A. | Quantitative and Qualitative Disclosures about Market Risk | 45 |

| Item 8. | Financial Statements and Supplementary Data | 46 |

| Item 9. | Changes in and Disagreements With Accountants on Accounting and Financial Disclosure | 74 |

| Item 9A. | Controls and Procedures | 74 |

| Item 9B. | Other Information | 76 |

| | | |

| PART III |

| | | |

| Item 10. | Directors, Executive Officers and Corporate Governance | 76 |

| Item 11. | Executive Compensation | 76 |

| Item 12. | Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters | 76 |

| Item 13. | Certain Relationships and Related Transactions, and Director Independence. | 76 |

| Item 14. | Principal Accountant Fees and Services | 77 |

| | | |

| PART IV |

| | | |

| Item 15. | Exhibits and Financial Statement Schedules | 78 |

PART I

SPECIAL NOTE REGARDING FORWARD LOOKING STATEMENTS

This Annual Report on Form 10-K contains forward-looking statements relating to future events and our future performance within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended. In some cases, you can identify forward-looking statements by terms such as "may", "will", "should", "could", "would", "hope", "expects", "plans", "intends", "anticipates", "believes", "estimates", "projects", "predicts", "potential" and similar expressions intended to identify forward-looking statements. These forward-looking statements include, without limitation, statements relating to future events, future results, and future economic conditions in general and statements about:

| · | The development of new products, regulatory approvals of new and existing products and the expansion of the market for our current products; |

| · | Implementing aspects of our business plan and strategies; |

| · | Our financing goals and plans; |

| · | Our existing working capital and cash flows and whether and how long these funds will be sufficient to fund our operations; and |

| · | Our raising of additional capital through future equity and debt financings. |

These statements involve known and unknown risks, uncertainties and other factors, including the risks described in Part I, Item 1A. of this Annual Report on Form 10-K, which may cause our actual results, performance or achievements to be materially different from any future results, performances, time frames or achievements expressed or implied by the forward-looking statements. Given these risks, uncertainties and other factors, you should not place undue reliance on these forward-looking statements. Information regarding market and industry statistics contained in this Annual Report on Form 10-K is included based on information available to us that we believe is accurate. It is generally based on academic and other publications that are not produced for purposes of securities offerings or economic analysis. We have not reviewed or included data from all sources and cannot assure you of the accuracy of the market and industry data we have included.

Corporate Information

ITEM 1. Business

General

Response Biomedical Corporation (“Response”, “us”, or “we”) develops, manufactures and markets rapid on-site diagnostic tests for use with our RAMP® platform for clinical and environmental applications. RAMP represents a paradigm in diagnostics that provides high sensitivity and reliable information in minutes. It is ideally suited to both point of care testing and laboratory use. Response was incorporated in British Columbia in August 1980. Our principal offices are located at 1781 – 75th Avenue West, Vancouver, British Columbia, Canada. Our common stock is traded on the Toronto Stock Exchange (TSX) under the trading symbol “RBM” and quoted on the OTC markets under the symbol “RPBIF”. Our results by segment are included in our financial statements, which are included under Item 8 to this Annual Report on Form 10-K.

Our Technology – The RAMP® System

The RAMP® system is a proprietary platform technology that combines a sensitive, portable fluorescence detection system with simple lateral flow immunoassays. Although lateral flow immunoassay technology has been available for over 25 years, the market for early generation rapid immunoassays has been limited by their inability to provide the accurate, quantitative results required by the majority of test situations.

RAMP® maintains key positive attributes of lateral flow immunoassays - simplicity, specificity, reliability and rapid results – but includes a method to overcome the performance limitations of early generation immunoassays that suffer from relatively poor sensitivity and precision. By introducing a population of known antibodies that are impacted by the same conditions as the test antibodies, the ratio of a measurement of the signal from the two sets of antibodies effectively factors out uncontrolled variability, thereby providing an accurate result. Furthermore, the use of a fluorescent label in the cartridge combined with a custom optical scanner in the RAMP® Reader, or Reader, results in a reliable and sensitive detection system. The RAMP® System has demonstrated its capability to detect and quantify a wide variety of analytes with sensitivity and accuracy comparable to centralized lab systems, including multiple analytes simultaneously.

Minimal training is required to use the RAMP® System. A test is performed by adding a sample (e.g., blood, urine, saliva, water, or unknown powders) containing the analyte of interest (e.g., Myoglobin, anthrax spores) mixed with a proprietary buffer and labeled antibodies to the sample well of a cartridge. The cartridge is then inserted into the Reader, which scans the test strip and provides the result in 20 minutes or less, depending on the assay. In the absence of rapid on-site and point-of-care (POC) test results like the RAMP® test, health care providers and first responders may be forced to wait up to three days for a confirmatory result from a government- or hospital -run lab.

The RAMP® system consists of a reader and single-use disposable test cartridges, and has the potential to be adapted to more than 250 medical and non-medical tests currently performed in laboratories.

Our Markets

We develop, manufacture and sell the RAMP® system for the medical point of care market including cardiovascular tests and infectious disease tests, and the on-site environmental testing market including biodefense and vector infectious disease testing.

Medical Point-of-Care (POC) Clinical Diagnostics

Cardiovascular Testing

A major focus of our development programs in cardiovascular testing has been clinical tests for the quantification of cardiac markers. Cardiac markers are biochemical substances that are released by the heart after it has been damaged or stressed. Elevated levels of these markers can be indicative of a heart attack or congestive heart failure. There are three primary markers for the detection of a heart attack: Myoglobin, CK-MB, and Troponin I. The primary markers for congestive heart failure are B-type natriuretic peptide, or BNP, and NT-proBNP. Response has developed POC tests for each of these markers, where NT-proBNP is various countries by our international distributor network except for Japan, where BNP is sold solely.

Heart Attack/Myocardial Infarction (MI) Testing

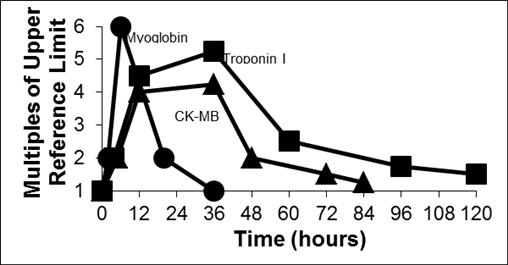

Serial measurement of biochemical markers is now universally accepted as an important determinant in the diagnosis of a heart attack. The ideal cardiac marker is one that has high clinical sensitivity and specificity, appears soon after the onset of a heart attack, remains elevated for several days following a heart attack, and can be assayed with a rapid turnaround time.1 Today, there is no single marker that meets all of these criteria, thus necessitating testing for multiple cardiac markers. The biochemical markers that are commonly used by physicians to aid in the diagnosis of a heart attack are Myoglobin, CK-MB, Troponin I, and Troponin T. As seen in the figure below, cardiac markers follow a specific, predictable pattern of release kinetics following a coronary event. The differences in the time that it takes each marker to reach peak concentration has made it common practice for clinicians to make use of at least two different markers in tandem, an early marker such as Myoglobin and a later one such as Troponin I. More recently, international guidelines recommend the use of serial Troponin assays for definitive diagnosis of heart attacks.

Release of Cardiac Markers into the Bloodstream Following a Heart Attack2

The turn-around times for results from a hospital lab can vary from as little as thirty minutes to more than two hours due to the necessity of test ordering and specimen collection, specimen transport, sample preparation, test completion and reporting. In rural settings and physicians’ offices, the turn-around time can be many hours or even days. Evidence-based clinical practice guidelines recommend that the results from cardiac marker testing be available within 60 minutes of patient presentation and ideally within thirty minutes. POC testing with products such as RAMP® could provide doctors with the information they need to diagnose and treat heart attack patients in a much shorter timeframe (e.g., less than 20 minutes from blood draw to result). In most cases, this is more likely to be within the critical window of time to minimize irreversible heart damage or death. The RAMP® System is expected to aid in the diagnosis of heart attack by enabling physicians to easily and frequently monitor changes in the levels of a patient’s cardiac markers. Early access to this information enables physicians to use accelerated care protocols, which are intended to drive earlier and better treatment decisions. According to statistics published by the U.S. Centers for Disease Control and Prevention, or CDC, approximately 6 million people visit U.S. hospital emergency departments each year with complaints of chest pain, a primary symptom of heart attack.

1 Adams JE, III, Clin Chem Acta, 1999.

2 Wu AHB, Introduction to Coronary Artery Disease (CAD) and Biochemical Markers, 1998.

Congestive Heart Failure (CHF) testing

Congestive heart failure, or CHF, is a chronic, progressive disease in which the heart muscle weakens and becomes impaired, thus impeding the heart's ability to pump enough blood to support the body's metabolic demands. CHF is the only cardiovascular disorder to show a marked increase in incidence in the past 40 years and it is expected to continue rising due in part to the aging population and better survival prospects of patients with other cardiovascular diseases.3 Many patients hospitalized with acute CHF will be re-admitted to the hospital with repeat incidence of the disease.

Previous methods for the diagnosis and assessment of CHF, which include physical examinations and chest x-rays, are not usually conclusive, making accurate diagnoses difficult. The introduction of testing for BNP and NT-proBNP dramatically changed the ability of physicians to make a qualified diagnosis and monitor the success of treatment because the level of these molecules is elevated in the blood when the heart is forced to work harder. These tests have proven to be more accurate than any other single physical or laboratory gauge of heart failure.4 Both BNP and NT-proBNP are fragments of proBNP, a neurohormone that is released by the heart in response to increased blood pressure and volume overload causing stretching of the ventricular muscle of the heart during heart failure. Both of these markers are elevated in the blood during heart failure and are sensitive and specific indicators of congestive heart failure.

Infectious Disease Testing

Influenza viruses cause seasonal epidemics associated with high morbidity and mortality, especially affecting those with underlying medical conditions and the elderly.5 Influenza is characterized by rapid start of high fever, chills, myalgia, headache, sore throat, and cough. However, even during periods of large outbreak, clinical diagnosis can be difficult due to the presence of other respiratory viruses.6 The rapid and accurate diagnosis of Influenza is important for determining appropriate treatment strategies and decreasing unnecessary use of antibiotics.7 The laboratory diagnosis of Influenza infections is based on either detection of the Influenza virus directly or isolation of the virus in cell culture, or detection of nucleic acid by polymerase chain reaction, each of which can take several hours to days before results become available.

With the recent development of different treatments for Influenza A and B and the need to begin therapy within the first 48 hours of infection8, the demand for rapid and accurate Influenza tests has grown. Being able to rapidly identify patients with Influenza at the clinic or hospital allows sites to reduce infections occurring in hospitals and reduces the amount of unnecessary or incorrect treatment and administration.

Most of the rapid Influenza tests on the market are qualitative strip tests that produce a change in color if the Influenza virus is present in sufficient quantities. Several independent evaluations demonstrate the limited clinical sensitivity or ability to detect small amounts of the Influenza virus, of the current, commercially available rapid Influenza tests.9,10,11,14 While the specificity, or ability to detect the Influenza correctly, if in sufficient quantity, of these rapid tests is generally high (median 90–95%), their limited sensitivity and false negative results remain a major concern.

3 McCullough, PA, Nowak, RM, McCord J, et al. B-type natriuretic peptide and clinical judgment in emergency diagnosis of heart failure. Clin Inv Rep. 2002;106:416-422.

4 http://www.stjohnsmercy.org/healthinfo/newsletters/heart/Aug02.asp

5 Nicholson KG, Wood JM, Zambon M (2003) Influenza. Lancet 362:1733– 1745.

6 http://www.cdc.gov/flu/about/qa/disease.htm.

7 http://www.cdc.gov/flu/professionals/treatment/0506antiviralguide.htm.

8 http://www.cdc.gov/flu/keyfacts.htm.

9 Fader RC. Comparison of the BinaxNOW Flu A Enzyme Immunochromatographic Assay and R-mix Shell Vial Culture for the 2003-2004 Influenza Season. Journal of Clinical Microbiology, December 2005; 43(12), 6133-6135.

10 Landry ML, Cohen S, Ferguson D. Comparison of BinaxNOW and Directigen for rapid detection of influenza A and B. Journal of Clinical Virology. 2004, 31, 113-115.

11 Weinberg A, Walker ML. Evaluation of Three Immunoassay Kites for Rapid Detection of Influenza Virus A and B. Clinical and Diagnostic Laboratory Immunology. March 2005, 367-370.

Respiratory Syncytial Virus (RSV)

Respiratory syncytial virus, or RSV, is a respiratory virus that infects the lungs and breathing passages. Most otherwise healthy people recover from RSV infection in 1- 2 weeks. However, infection can be severe in some people, such as certain infants, young children, and older adults. In fact, RSV is the most common cause of bronchiolitis (inflammation of the small airways in the lung) and pneumonia in children under one year of age in the United States. In addition, RSV is more often being recognized as an important cause of respiratory illness in older adults.13

On- Site Environmental Testing

Environmental tests are generally considered to be products and services used to detect and quantify substances and microbes in the environment that have potentially harmful effects to humans. We participate in two distinct areas of the environmental market. The first is biodefense, where RAMP® products are used for the detection and identification of threatening biological agents, and the second is the vector infectious diseases testing market, where a RAMP® product is used to test samples from mosquito pools for West Nile Virus to monitor the threat to humans.

We have developed and are selling RAMP® tests for the rapid detection and identification of anthrax, ricin, botulinum toxin and orthopox viruses (including smallpox). Our target market for our RAMP® Biodefense tests is primarily public safety institutions, or first responders, such as fire and police departments, military installations, emergency response teams and hazardous materials (HAZMAT) units. Government agencies and corporations that handle mail are also candidates for an on-site test for anthrax. The rapid detection and identification of biological agents is an important capability affecting the management of a bioterrorism event, forming the basis of emergency response, medical treatment and consequence management. In addition, the rapid identification of biological agents facilitates the quick dismissal of hoaxes and panic-based reports, thereby reducing the logistical burden on first responders who will be required to maintain a higher level of preparedness than in the past. In the aftermath of the terrorist attacks on September 11, 2001, there was an increased desire to be prepared for potential terrorist attacks, particularly on the part of the U.S. government, as evidenced by numerous initiatives, including the creation of the U.S. Department of Homeland Security, or DHS. The first priority of the DHS is to protect the United States against further terrorist attacks. Component agencies analyze threats and intelligence, guard borders and airports, protect critical infrastructure, and coordinate the response of the U.S. for future emergencies.

Following use of anthrax as a weapon for terrorist attacks in the United States in October 2001, we saw an opportunity to adapt the RAMP® technology for the rapid detection and identification of agents used in acts of bioterrorism and initiated development of a test for the rapid, on-site detection of Bacillus anthracis, the causative agent for anthrax, referred to as the Anthrax Test. Development of the Anthrax Test was substantially completed in April 2002 following successful initial validation by the Maryland State Department of Health where testing confirmed that the RAMP® Anthrax Test could reliably detect anthrax spores at levels lower than an infectious dose of 10,000 spores. These results were supported by further independent testing conducted by Defense Research and Development Canada in Suffield. The Anthrax Test was launched commercially in May 2002. In September 2006, our RAMP® Anthrax Test was the first and only biodetection technology approved for field use by first responders in the United States for the detection of anthrax in an independent testing program conducted by AOAC and sponsored by the U.S. Department of Homeland Security. Since the commercial launch of the Anthrax Test in May 2002, we have commercialized tests for ricin, botulinum toxin and orthopox (including smallpox), three priority bio-threat agents. Commercial sales of the ricin test and the botulinum toxin test commenced in November 2002 and the orthopox test was launched in May 2003.

12 Storch GA. Rapid diagnostic tests for influenza. Current Opinion in Pediatrics 2003, 15:77-84.

13 Centers for Disease Control & Prevention – http://www.cdc.gov/RSV/

Vector Infectious Disease Testing

West Nile Virus is an arbovirus that can cause a fatal neurological disease in humans and is commonly found in North America, Europe, Africa, the Middle East, and West Asia. Since its establishment in 1999 into the USA, the virus has spread and is now widely established from Canada to Venezuela. In the US alone, over the last five years (2007 to 2011) the CDC has reported 7417 total human WNV disease cases and a total of 300 deaths. The virus is mainly transmitted to people through the bites of infected mosquitoes, thus mosquito surveillance programs for WNV have been successfully implemented in the USA to mitigate the spread of the virus.

In North America, West Nile Virus prevalence is dependent on climate and has a specific season, beginning in May and ending in September, when the temperature drops, and the mosquito population drops.

Our Products

Cardiovascular Testing Products

Our RAMP® cardiovascular tests are intended for use primarily in hospital emergency rooms, laboratories and walk-in clinics around the world. We have obtained clearance to market these tests in the U.S., Canada, the European Union, China and other regulated jurisdictions.

In China, we sell a co-branded RAMP® Reader, RAMP®200 reader, Myoglobin, CK-MB, Troponin I and NT-proBNP products through O&D Biotech Co., Ltd. (“O&D”), who serves as our exclusive distributor and service agent, with the exception of Hong Kong Special Administrative Region and Macau Special Administrative Region. In addition, Wondfo Biotech Co. Ltd (“Wondfo”) is our exclusive distributor for the marketing and sale of the cardiac reader, assays and controls under private label OEM products bearing the Wondfo name, brand, logo and trademark in those same markets

In Japan our distributor Shionogi& Co., Ltd. (“Shionogi”) sells a rapid quantitative test for BNP under its own brand name.

In the United States, from 2009 through September 2011, Roche Diagnostics Ltd. (“Roche Diagnostics”) had served as our exclusive distributor for sale of cardiovascular products; however our agreement with Roche Diagnostics terminated effective September 30, 2011. Since that time we have resumed selling our products directly to US customers.

In addition to the above, we have agreements with regional distributors that sell our RAMP® cardiovascular products in various countries in Asia, Latin America, Europe, the Middle East and Africa.

Infectious Disease Testing Products

Influenza A/B

In 2008, our partner 3M Company (“3M”) launched their Rapid Detection Flu A+B test. This test provides hospital and physician office laboratories reliable and objective electronic results in approximately 15 minutes. For our flu tests, we were granted a Special 510(k) clearance by the U.S. Food and Drug Administration, or FDA, for an update to our RAMP® Influenza A/B Assay Package Insert to include analytical reactivity information for a strain of the 2009 H1N1 virus cultured from positive respiratory specimens. Although the RAMP® Influenza A/B Assay has been shown to detect the 2009 influenza A (H1N1) virus in cultured isolates, the performance characteristics of this device with clinical specimens that are positive for the 2009 influenza A (H1N1) virus have not been established. The RAMP® Influenza A/B Assay can distinguish between influenza A and B viruses, but it cannot differentiate influenza subtypes.

RSV

In collaboration with 3M, we began development of a RAMP® test for rapid detection of RSV, which infects virtually all children by the age of two. This product was launched in October 2009 and product sales are ongoing through our distributor, 3M.

On-Site Environmental Testing Products

Environmental tests are generally considered to be products and services used to detect and quantify substances and microbes in the environment that have potentially harmful effects to humans. We participate in two distinct areas of the environmental market. The first is biodefense, where RAMP® products are used for the detection and identification of threatening biological agents, and the second is the vector infectious diseases testing market, where a RAMP® product is used to test samples from mosquito pools for West Nile Virus to monitor the threat to humans.

Biodefense Testing Products

We market and sell our biodefense products through a network of regional distributors in the United States, and country-specific national distributors in certain other countries. These efforts are supplemented by direct sales in some geographical territories. Since October 2002, RAMP® biodefense systems have been sold in Canada, the United States, Saipan, Guam, Japan, Italy, Australia, Ireland, Israel, Korea, China, Singapore and the United Arab Emirates. Customers include UNMOVIC, the United States Air Force, the United States Army, Canadian Department of Defense, Health Canada, and the Royal Canadian Mounted Police. RAMP® Systems are being used in major U.S. markets including Chicago, Orlando, Philadelphia, Los Angeles, West Palm Beach, Atlanta, and Houston.

Vector Infectious Diseases Testing Products

The market for our West Nile Virus Test is comprised of the following end users: state public health/veterinary labs; mosquito control districts; and universities. U.S. state government testing figures for 2002 – 2003 indicated that the average state tested approximately 3,500 mosquito pools and 1,000 birds. It is estimated that approximately 279,000 tests are performed throughout North America each year to screen for West Nile Virus. We launched our WNV Test expecting that initial sales would be derived from a mixture of both direct sales and sales generated via distribution partners. On December 1, 2003, we entered into a sole distribution agreement with ADAPCO Inc., the largest distributor of mosquito control products in the United States.

Key Manufacturing, Development, Sales and Distribution Agreements

O&D Biotech, LTD. China

In February 2011, we signed an agreement with O&D that replaces an earlier agreement signed in April 2007, as the exclusive distributor of RAMP co-branded cardiovascular products in the People’s Republic of China, exclusive of Hong Kong and Macau Special Administrative Region. Under the agreement O&D is subject to certain minimum purchase levels. In the event O&D does not meet those levels, we have the option to terminate the agreement.

Wondfo Biotech Co., Ltd

In December 2009 we signed a private label OEM agreement with Wondfo which names Wondfo the exclusive distributor for the marketing and sale of private label OEM cardiac testing products in the People’s Republic of China, excluding Hong Kong and Macau. This agreement is subject to certain minimum purchase requirements by Wondfo. Should they fail to meet the minimum purchase requirements under the agreement, we may at our discretion either convert this to a non-exclusive OEM agreement or immediately terminate the agreement.

Shionogi & Co., Ltd.

In May 2006, we signed an agreement with Shionogi to market and sell our BNP tests in Japan. Under the terms of the agreement, we agreed to become the exclusive manufacturer of BNP assay kit on an OEM basis. The agreement is subject to minimum purchase levels by Shionogi. In the event Shionogi fails to meet these minimum purchase levels, it is required to pay us a percentage of the unit price for each unit that represents the shortfall. The initial term of the agreement ran for three years; however, the agreement is automatically renewed for successive periods of one year under the same terms and conditions (except for price and minimum order quantity). The agreement may be terminated by either party with twelve months notice, should either party be in breach under the terms of the agreement, or under certain other conditions.

3M Company

In September 2004 we signed a Joint Development Agreement (JDA) with 3M. This agreement was amended in November 2006 for development of tests and related reader for detection of infectious diseases.

In November 2006, we entered into a Manufacturing and Supply Agreement with 3M that was subsequently amended in November 2009 and June 2010. The agreement and related amendments set the specific products, prices and terms for the products to be provided by us to 3M. The agreement grants 3M a worldwide, royalty bearing license to all products under the agreement and requires 3M to purchase all tests, readers and related equipment under the agreement exclusively from us. Currently the supply agreement covers the Flu A/B cartridges, RSV cartridges, and the 3M branded Rapid Detection Reader.

In March 2010, we entered into a Distribution Agreement with 3M granting us a right to sell products covered under the Manufacturing and Supply Agreement in China, Hong Kong, Australia, New Zealand, Canada, Japan, Korea, Thailand and Iran. Under the terms of this agreement, we are to pay 3M a royalty on net sales of our Flu A/B cartridges, RSV cartridges and readers under ours or a third party’s brand. The initial term of this agreement is for five years, after which the parties can mutually agree to extend the agreement for another two years.

Adapco, Inc.

In April 2008 we entered into a Distribution Agreement with Adapco, which replaced an earlier agreement signed in March 2006. The initial term of the agreement was for one year, and is automatically renewed on an annual basis. This agreement appoints Adapco the exclusive distributor of tests and readers for detection of West Nile Virus in the United States; however the agreement gives us the right to sell these products directly should we choose.

Roche Diagnostics GmbH and Roche Diagnostics Ltd.

In July 2005, we secured a license from Roche Diagnostics GmbH to develop, manufacture and sell POC tests for the detection of NT pro-BNP in markets where we do not sell BNP tests.

In June 2008, we entered into a Sales and Distribution Agreement with Roche Diagnostics. That agreement granted Roche Diagnostics the rights to market our line of cardiovascular POC tests worldwide with the exception of Japan. This agreement was revised in February 2010 to limit the licensed territory to the US.

On September 2, 2011, we received notification from Roche Diagnostics that they have terminated the sales and distribution agreement between Roche and Response effective September 30, 2011. Roche Diagnostics terminated the agreement because we have not obtained the necessary approvals from the FDA to permit Roche Diagnostics to market the Response’s cardiovascular POC tests in the United States using the RAMP® 200 Reader.

Competition

Medical Point-of- Care Market

The medical POC test market is comprised of five basic segments: clinical chemistry, hematology, immunoassay, blood glucose and urinalysis, plus miscellaneous other tests. Dozens of companies sell qualitative POC tests in these segments. Few companies however, participate in the quantitative POC immunoassay market. The following table summarizes our key known competitors in the POC testing market.

| | Test Market Segment |

| Company | Cardiac Markers | CHF Marker | Drugs of Abuse | Flu and Infectious Disease | Pregnancy / Ovulation | Blood Gases/ Electrolytes | Coagulation |

| Response Biomedical Corporation | Ö | Ö | | Ö | | | |

| Abbott Point of Care Inc. | Ö(1) | Ö | | | | Ö | Ö |

Becton Dickinson Corporation (4) | | | | Ö | | | |

| Dade Behring | Ö | Ö | | | | | |

| Alere Inc. | Ö | Ö | Ö | Ö | Ö | Ö | Ö |

Mitsubishi Chemical Medience Corporation (3) | Ö | Ö | | | | | |

Roche Diagnostics (2) | Ö | Ö | Ö | | | Ö | Ö |

Quidel Corporation (4) | | | | Ö | Ö | | |

| (1) | Only Troponin I, CK-MB and BNP cardiac tests at this time. |

| (2) | The Cardiac Reader measures Troponin T rather than TnI and does not measure CK-MB. This platform uses semi-quantitative technology. This limits the upper end of their NT-proBNP assay to only 20% of the entire clinical range. |

| (3) | Mitsubishi Pathfast weighs 33kg, which for some would not be considered a POC system but rather a small laboratory analyzer. |

| (4) | These companies sell rapid Influenza tests that are visually read, require precise timing and do not require an instrument. |

Certain of the competitors listed in the table above have stated their intention to broaden their category offerings. In addition to the key competitors listed above, we believe that each of the major diagnostics companies has an active interest in POC testing and, as well as being potential competitors, are also potential business partners.

Alere Inc. (formerly Inverness Medical Innovations Inc.), or Alere, has sold a three-in-one quantitative immunoassay and reader system for cardiac markers (CK-MB, Troponin I and Myoglobin) since 1999 and is currently one of the leading participants in quantitative POC cardiovascular testing on the basis of market share, revenues and technology. They also sell a “shortness of breath” panel cartridge, which includes Myoglobin, CK-MB, Troponin I, BNP and D-Dimer. While BNP is available as a stand-alone cartridge, this system can only perform Troponin I tests as part of a panel. In 2007, Biosite Incorporated, or Biosite, was acquired by Inverness Medical Innovations in a transaction valued at $1.68 billion. Based on published list prices for the Biosite products and data from the completed multi-site clinical study entitled “Evaluation of a point-of-care assay for cardiac markers for patients suspected of acute myocardial infarction”14, we believe that RAMP® has several advantages over the competing Biosite products including product performance and menu flexibility. These results were recently replicated in an unpublished trial.

14 Munjal I, Gialanella P, Goss C, McKitrick JC, Avner JR, Quiulu Pan, Litman C, Levi ML, J Clin Micro 2011Mar 49(3):1151-3.

Since 2003, Abbott Point of Care Inc., (formerly iStat Corporation) has sold a 10-minute Troponin I test for use on the i-STAT Portable Clinical Analyzer, a biosensor based technology. In 2005, Abbott Point of Care launched a CK-MB test and in 2006, launched a POC BNP test. In addition, Abbott Point of Care offers several tests for other markers in whole blood, predominantly electrolytes and blood gases. We believe the requirement for different sample types for the i-STAT markers for heart attack (TnI and CK-MB) and congestive heart failure (BNP) is a significant disadvantage as compared to the RAMP® system.

Quidel Corporation has sold rapid, qualitative tests for the detection of RSV and Influenza A and B since 2001 as the QuickVue® Influenza A+B test and the QuickVue RSV test. Based on data published in March 2011, we believe that the RAMP® RSV test branded under 3M has superior performance than the QuickVue RSV test. Binax, Inc., a division of Alere, has been selling Influenza A, Influenza B and RSV tests under the BinaxNOW® brand since 2002 and a combined Influenza A + B test since 2004. Both of these tests have received Clinical Laboratory Improvement Amendments of 1988, or CLIA, waived status, which allows for their use in physician office laboratories. Other tests available include Becton-Dickinson and Thermo Electron Corp., which produce rapid Influenza A+B tests that are not currently CLIA waived.

Other technologies that may compete against RAMP® in the future by delivering highly sensitive, quantitative results, for some POC tests include immunosensors or biosensors and nanotechnology-based approaches. Biosensor methods use specific binding molecules such as antibodies to generate a measurable signal as a direct result of binding to their target molecule (or analyte). These technologies are extremely complex and have been under development for many years with limited commercial success to date. Immunobiosensors, to date, have limited sensitivity and are not competitive with RAMP®. Although methods of testing using biosensors and nanotechnology can be fast, they generally suffer from a significant lack of accuracy, repeatability and reliability, and can be expensive to produce. Biosensors are now in limited use for selected diagnostic applications, most notably for blood glucose monitoring using non-immunoassay methods. Nanotechnology is a relatively new and growing field that deals with the use of inert micro-etched wafers, or chips, to provide templates for chemical, biochemical, and biological processes.

Much of the research effort for recent diagnostic testing has been directed toward the development of DNA hybridization probe tests. These tests identify specific gene sequences that can be associated with certain genetically based disorders, infectious diseases and the prediction of predisposition to certain medical conditions such as cancer. Several companies, such as Becton-Dickinson and Gen-Probe Inc. are now marketing specific probe tests for infectious diseases such as tuberculosis, hepatitis, Legionnaires disease and vaginitis. DNA probe technology is useful for gene markers that have been shown to be associated with specific disease states or clinical conditions. Although more useful gene sequences are being discovered all the time, we believe they will not displace the need for high-sensitivity immunoassays; there is, for instance, no genetic change when a person has a heart attack. In addition, the RAMP® format may be applicable to hybridization probe methods if a need is found for these tests to be quantitative and at the POC.

The following table summarizes our known competitors in the rapid on-site environmental biodefense testing market (note that this table may not include all biological agents for which these companies may have tests):

| Company | Biological Agent |

| Anthrax | Ricin | Botulinum Toxin | Orthopox | Brucella | Plague | Tularemia | SEB |

| Response Biomedical Corporation | Ö | Ö | Ö | Ö | | | | |

Alexeter Technologies LLC (1) | Ö | Ö | Ö | Ö | Ö | Ö | Ö | Ö |

| New Horizons Diagnostics | Ö | Ö | Ö | | | Ö | Ö | Ö |

| ADVNT Inc. | Ö | Ö | Ö | | | Ö | | Ö |

Idaho Technology Inc. (2) | Ö | Ö | Ö | Ö | Ö | Ö | Ö | |

| Tetracore, Inc. | Ö | Ö | Ö | Ö | Ö | Ö | Ö | Ö |

Smiths Detection BioSeeq Plus (3) | Ö | | | Ö | | Ö | Ö | |

| QTL/MSA | Ö | Ö | | | | | | Ö |

| (1) | Product includes a portable reader based on reflectance technology. |

| (2) | Product includes a portable reader based on polymerase chain reaction technology. |

| (3) | Product includes a portable reader based on polymerase chain reaction technology. |

A number of independent studies have been conducted on biodefense tests. The RAMP® Anthrax Test has been evaluated at four sites in the United States and Canada: DRDC Suffield,15 a division of the Canadian Department of National Defense; the Maryland State Department of Health;16 Intertox Inc.,17 a Seattle-based public and occupational health firm; and, Edgewood Chemical Biological Center, part of the U.S. Army's Aberdeen proving ground, and more recently the AOAC testing.18 Data from these four evaluations show that the RAMP® Anthrax Test meets or exceeds its product claims of reliably detecting less than 4,000 live spores, with 99 percent confidence in specificity. The CDC defines a lethal dose of anthrax as 10,000 spores.

In November 2004, the RAMP® System was the only commercially available rapid on-site anthrax detection system of those tested that met the new performance standards introduced by AOAC for rapid immunoassay-based anthrax detection systems and to receive the AOAC Official Methods Certificate 070403 stating that the RAMP® Anthrax Test performed as we claimed and that we are authorized to display the AOAC Performance Tested certification mark. All other commercially available rapid on-site anthrax detection systems tested failed to meet the AOAC’s performance standard. A further intensive, independent field testing program conducted by AOAC and sponsored by the DHS, culminated in the announcement in September 2006 that our RAMP® Anthrax Test is the first and only biodetection product approved for field use by first responders in the United States for the detection of anthrax. To date, RAMP® remains the only product with this designation by the AOAC.

Since the initial RAMP® product launch, many competitors have launched competitive products into the market place, including Alexeter Biotechnologies and ADVNT Inc., both of whom also market rapid detection tests in the US for Anthrax, Ricin and Botulinum, in addition to SEB, Y. pestis (plague) and others. Internationally, Smith Detection maintains a strong market share. We also believe that a number of diagnostics companies have an active interest in rapid on-site biodefense testing and have the potential to become either competitors or business affiliates.

We currently have approximately 346 RAMP® biodefense systems in field use by our customers (see “On-Site Environmental Testing Market, Industry Trends” and “Risk Factors”).

15 Defence Research and Development Canada, July, 2002.

16 Maryland State Department of Health, March 2002.

17Intertox Inc., July 2002.

18 The U.S. Army Aberdeen Proving Ground, November 2004.

Vector Infectious Diseases Market

Our main competitor in the rapid on-site environmental vector infectious disease testing market is VecTest, currently distributed by Thermo Scientific. VecTest is a qualitative test strip, available in multiplex format, used to detect WNV, SLE, EEE and WEE. While a study by the CDC in 2006 confirmed that RAMP® outperforms VecTest19, VecTest continues to occupy a market share due to its qualitative nature as no instrument is required to perform the testing.

Emerging competition in the detection of West Nile Virus in the US market is from RT-PCR systems, as more labs are investing in PCR technology in lieu of rapid detection.

Operations and Manufacturing

A RAMP® System consists of a Reader and kits, or Kits, of applicable RAMP® tests. Manufacturing of the Readers is currently outsourced to an electronics manufacturer that we have qualified, located in British Columbia. We manufacture all Kits in-house in order to maximize return on investment, protect proprietary technology, and ensure compliance with government and internal quality standards. Kit manufacturing includes reagent and component production, cartridge assembly and final packaging with the exception of our Chinese customers where bulk components are shipped to our distributors in China for final packaging.

In advance of expected growth of our products, we invested significantly, since 2007, to increase automation, quality and capacity of our manufacturing operations. In March 2008, we moved into our current corporate headquarters, a leased, multi-use, 46,000 square foot facility in Vancouver, British Columbia where we coordinate all support operations including customer support, technical and instrument service, production planning, shipping and receiving. The facility houses all of our operations and will allow us to achieve our projected manufacturing capacity targets during the term of the agreement. Our manufacturing scale up is ongoing, and our test production capacity has increased from approximately 500,000 tests per shift per year to approximately 2 million tests per shift per year. The initial term of the lease agreement is 15 years with two 5-year renewal options.

Where possible, we require distribution and marketing partners to provide a twelve-month rolling forecast in order to ensure timely and adequate product supply and to allow efficient production, materials, shipping and inventory planning, see “Risk Factors". We plan to meet cost and quality targets through strict scale-up validation procedures and by negotiating supplier agreements for key materials. Final packaging, inventory storage and product distribution to marketing partners will be managed in accordance with individual partner agreements.

The primary raw materials for a test cartridge consist of: antibody reagents, nitrocellulose membrane and injection molded plastic parts to act as housing for the cartridge assembly. There are several different components required to perform the test that are included with the Kit. These are a sample transfer device, a solution for diluting the test sample and reagent-containing tips (for placing the sample being tested into the cartridge). Response purchases these primary raw materials from unaffiliated domestic and international suppliers, some of which are sole suppliers. Interruptions in the delivery of these materials or services could adversely impact the Company.

Patents and Proprietary Rights

We rely on a combination of patents, trademarks, confidential procedures, contractual provisions and similar measures to protect our proprietary information. To develop and maintain our competitive position, we also rely upon continuing invention, trade secrets and technical know-how.

It has been our practice to periodically file for patent and trademark protection in the U.S. and other countries with significant markets, such as Canada, Western European countries, Japan and China. No assurance can be given that patents or trademarks will be issued to us pursuant to our applications or that our patent portfolio will provide us with a meaningful level of commercial protection. We file patent applications on our own behalf as assignee and, when appropriate, have filed and expect to continue to file, applications jointly with our collaborators. Our ability to obtain and enforce patents is uncertain and we cannot guarantee that any patents will issue from any pending or future patent applications owned by or licensed to us, see “Risk Factors”.

19 Burkhalter et al, 2006

We hold exclusive ownership to technology that originated from the University of British Columbia, which has resulted in three issued U.S. patents, one issued Canadian patent and four active foreign patents. Our key patent is also pending in China and Hong Kong. In addition Response holds an additional two patents in the U.S. These patents have expiration dates ranging from 2020 to 2028. We have pending applications for 3 additional U.S. patents and numerous foreign counterparts as well as one pending patent application filed in both the US and Europe, with joint inventorship and assignment with one of our partners. We also have two granted Design Patents related to the Ramp® 200 reader. We have four registered trademarks.

We seek to protect our trade secrets and technology by entering into confidentiality agreements with employees and third parties (such as potential licensees, customers, strategic partners and consultants). In addition, we have implemented certain security measures in our laboratories and offices. Despite such efforts, no assurance can be given that the confidentiality of our proprietary information can be maintained. Also, to the extent that consultants or contracting parties apply technical or scientific information independently developed by them to our projects, disputes may arise as to the proprietary rights to such data.

Government Regulation

Regulatory Approval

Point of Care Diagnostics

The FDA, Health Canada and comparable agencies in foreign countries impose substantial requirements upon the development, manufacturing and marketing of drugs and medical devices through the regulation of laboratory and clinical testing procedures, manufacturing, marketing and distribution by requiring labeling, registration, notification, clearance or approval, record keeping and reporting, see “Risk Factors”.

In China, clearance to market drugs and medical devices must be granted by the State Food & Drug Administration (“SFDA”). In May 2004 and November 2004, O&D received regulatory clearance from the SFDA to market the RAMP® Reader and three RAMP® cardiac marker tests in China. In November 2007, they received clearance to market the RAMP® NT-proBNP Assay and in December 2010 the clearance to market the RAMP®200 Reader was received.

As of December 7, 2003, all medical devices sold in the countries of the European Union, or the EU, are required to be compliant with the EU In-Vitro Diagnostic Directive. All new in-vitro diagnostic devices must bear a mark, called the CE Mark, to be registered and legally marketed in the EU after that date. The regulatory requirements for marketing are based on the classification of the individual products and EU member countries are not allowed to impose any additional requirements on medical device manufacturers other than the language used in product labeling. In April 2003, we fulfilled the requirements of the EU In-Vitro Diagnostic Directive Essential Requirements for the three RAMP® cardiac tests and Reader; in December 2006, we registered the NT-proBNP test as well as the RAMP® liquid cardiac marker controls used by laboratories to verify Kit performance and user technique; in May 2009, we registered the RAMP® 200 reader and in December 2009, we registered the Influenza A/B Test. Through the EC Declaration of Conformity, we are entitled to apply the CE Mark to these products. As with the FDA, future RAMP® tests may have different classifications which would require ISO 13485 registration as well as a technical file review by a registration organization, known as a Notified Body, prior to authorization to apply the CE Mark.

Prior to sale in the United States, RAMP® clinical products will typically require pre-marketing clearance through a filing with the FDA called a 510(k) submission. A 510(k) submission claims substantial equivalence to an accepted reference method or a similar, previously cleared product known as a “predicate device” and minimally takes about 100 days for approval once a submission is made. Some RAMP® tests may detect analytes or have applications, intended uses for which there are no equivalent products on the market. In such cases, the test will require pre-market approval, a process that requires clinical trials to demonstrate clinical utility, as well as safety and efficacy of the product. Including clinical trials, the pre-market approval process can take approximately two years.

Marketing clearance for the RAMP® Myoglobin Assay and RAMP® Reader was received in 2002. Marketing clearances for the RAMP® CK-MB Assay and the RAMP® Troponin I Assay on the RAMP® Reader were received in May 2004. The marketing clearance for the RAMP® Influenza A/B Assay and the RAMP® 200 Reader was received in April 2008. The marketing clearance for the RAMP® NT-proBNP Assay on the RAMP® Reader was received in July 2008. The marketing clearance for the RAMP® RSV Assay on the RAMP® 200 was received in July 2009.

As of March 23, 2012, we have received the FDA premarket clearance for Myoglobin, CK-MB, Troponin I and NT-proBNP on the RAMP® Reader, Flu and RSV on the RAMP®200 reader. We are currently developing additional tests that we will have to clear with the FDA through the 510(k) notification procedures. These new test products are crucial for our continued success in the human medical market. If we do not receive 510(k) clearance for a particular product, we will not be able to market that product in the United States until we provide additional information to the FDA and gain premarket clearance. The inability to market a new product during this time could harm our future sales in the US.

For our products to be sold in the physicians’ office lab market in the U.S., we will need to obtain waiver status under the CLIA. A CLIA-waived test is a test that employs methodologies that are so simple and accurate as to render the likelihood of erroneous results negligible and/or pose no reasonable risk of harm to the patient if the test is performed incorrectly. CLIA-waived tests are designed to be performed by less experienced and untrained personnel. The current CLIA regulations divide laboratory tests into three categories: “waived,” “moderately complex” and “highly complex.” Many of the tests performed using the RAMP system is in the “moderately complex” category. Moderately complex tests can only be performed in laboratories fulfilling certain criteria, which are fulfilled by a minority of physician office laboratories in the U.S.

In Canada, in vitro diagnostics are regulated by the Therapeutic Products Directorate of Health Canada, referred to as the TPD, and are licensed for sale through submission to the TPD. The timeline for approval is similar to that of the FDA’s 510(k) process. As of January 2003, all new and existing class II, III and IV Medical Device Licenses, or MDLs, in Canada also require a valid International Organization for Standardization, or ISO, 13485 or ISO 13488 Quality System Certificate from a registrar recognized by the Canadian Medical Devices Conformity Assessment System (“CMDCAS”). We achieved registration to the ISO 13485:2003 standard in April 2004. An MDL was issued for the Myoglobin Assay and Reader in 2002. MDLs were received for the RAMP® CK-MB Assay and RAMP® Troponin I Assay in August 2004; for the RAMP® NT-proBNP Assay in June 2007, and for RAMP® liquid cardiac marker controls used by laboratories to verify Kit performance and user technique. These controls are manufactured for Response by a U.S. company who holds the 510(k) clearance with the FDA. An MDL was received for the RAMP® Influenza A/B Assay and RAMP® 200 reader in May 2009. An MDL was received for the RAMP® RSV Assay in May 2010.

In other parts of the world, the regulatory process varies greatly and is subject to rapid change. Many developing countries only require an import permit from their own government agency or proof of approval from the regulatory agency in the manufacturer’s country of origin. We require our marketing and distribution partners to ensure that all regulatory requirements are met in order to sell RAMP® tests in their respective territories.

Clinical consultants are used to support in-house resources where necessary to develop protocols and prepare regulatory submissions for government agencies such as the FDA and the TPD. We completed multi-center clinical trials for the RAMP® Myoglobin Assay and the RAMP® Reader in 2001, for the RAMP® CK-MB Assay and the RAMP® Troponin I Assay in November 2003, for the RAMP® NT-proBNP Assay in November 2006 and for the Flu A/B Assay and the RAMP® 200 reader in May 2007, and for the RAMP® RSV Assay in November 2008.

ON-SITE ENVIRONMENTAL TESTING

Biodefense Testing

There are currently no regulatory approvals or clearances required to market on-site environmental biodefense tests in North America. There appears to be some support from the market for regulatory oversight of such testing, and regulatory agencies such as the Department of Homeland Security may in the future impose substantial requirements upon the development, manufacturing and marketing of devices through the regulation of laboratory and clinical testing procedures, manufacturing, marketing and distribution by requiring labeling, registration, pre-market notification, clearance or approval, record keeping and reporting. While additional regulatory requirements will make it more difficult for poorly performing products to participate in the market, they could also significantly increase the time and cost for companies to bring new tests to market, creating a barrier to entry.

The lack of regulatory oversight in the biodefense industry means there is virtually no independent data available for a customer to verify a manufacturer’s product claims. Since launching our Anthrax Test, we have received third party validation of the product’s performance; see “On-Site Environmental Testing Market, Competition”. Currently, however, companies do not require any form of regulatory clearance to market handheld assays for the detection of biodefense threats such as anthrax, see “Risk Factors”.

The performance and field-testing programs conducted by the AOAC in 2004 through 2006 were developed in collaboration with and funded by the DHS. One of the goals of the testing programs was to develop industry performance standards. The final form and substance of these possible standards and the impact on the industry is currently unclear.

Vector Infectious Diseases Testing

There is no regulatory clearance required for our RAMP® West Nile Virus Test because it is only used for testing mosquitoes. If we develop a Flu A or H5N1 screening test for birds, it will require regulatory clearance in some countries, such as the United States, where such tests are regulated by the Center for Veterinary Biologics division of the Department of Agriculture.

Manufacturing Regulations and Various Federal, State, Local and International Regulations

The 1976 Medical Device Amendment also requires us to manufacture our RAMP products in accordance with Good Manufacturing Practices guidelines. Current Good Manufacturing Practice requirements are set forth in the 21CFR 820 Quality System Regulation. These requirements regulate the methods used in, and the facilities and controls used for the design, manufacture, packaging, storage, installation and servicing of our medical devices intended for human use. Our manufacturing facility is subject to periodic inspections. In addition, various state regulatory agencies may regulate the manufacture of our products.

Federal, state, local and international regulations regarding the manufacture and sale of health care products and diagnostic devices may change. In addition, as we continue to sell in foreign markets, we may have to obtain additional governmental clearances in those markets.

To date, we have complied with the following federal, state, local and international regulatory requirements:

| · | United States Food and Drug Administration: In August 2007, the FDA conducted a facility inspection and verified our compliance with the 21 CFR 820 Regulation. |

| · | Health Canada Therapeutic Products Directorate: In 2004, the TPD granted our manufacturing facility Medical Device Licenses, based on the Medical Device Regulations (SOR/98-282), Section 36, for the manufacture of our medical devices . |

| · | International Organization for Standardization: In July 2004, we received our ISO 9001 certification, expanding our compliance with international quality standards. In April 2004, we received ISO 13485 Quality System certification as required by the 2003 European In Vitro Device Directive. This certified our quality system specifically to medical devices. In April 2004, we received the Canadian Medical Device Conformity Assessment System stamp on our ISO 13485 certificate to signify compliance with Health Canada regulations. In June 2010, we received our recertification to the ISO 13485:2003 Quality System Standard for medical devices. |

Research and Development Expenditure

Research and development activities relate to development of new tests and test methods, clinical trials, product improvements and optimization and enhancement of existing products. Our research and development expenses, which consist of personnel costs, facilities, materials and supplies, regulatory activities and other related expenses were $2.9 million, $4.1 million, and $5.6 million for the years ended December 31, 2011, 2010, and 2009, respectively.

Seasonal Variations in Business

Our operating results may fluctuate from quarter to quarter due to many seasonal factors. Many of our end-users are government related organizations at a federal, state/provincial or municipal level. Consequently, our sales may be tied to government budget and purchasing cycles. Sales may also be slower in the traditional vacation months, could be accelerated in the first or fourth calendar quarters by customers whose annual budgets are about to expire (especially affecting purchases of our fluorescent Readers), may be distorted by unusually large Reader shipments from time to time, or may be affected by the timing of customer cartridge ordering patterns.

Backlog

Because we ship our products shortly after we receive the orders from our customers, we generally operate with a limited order backlog. As a result, our product sales in any quarter are generally dependent on orders that we receive and ship in that quarter. As a result, any such revenue shortfall would immediately materially and adversely impact our operating results and financial condition. The sales cycle for our products can fluctuate, which may cause revenue and operating results to vary significantly from period to period. We believe this fluctuation is primarily due (i) to seasonal patterns in the decision making processes by our independent distributors and direct customers, (ii) to inventory or timing considerations by our distributors and (iii) to the purchasing requirements by various international governments to acquire our products.

Risks Attendant to Foreign Operations and Dependence

We sell in China through an exclusive distributor for RAMP branded products, O&D Biotech Co. Ltd., China (O&D), and an exclusive distributor for private labeled OEM products, Wondfo Biotech Co. Ltd. (Wondfo). Sales to O&D accounted for 44% of our total product sales in the year ended December 31, 2011. If O&D underperforms we may not be able to generate alternative distribution channels rapidly enough to prevent a significant disruption in sales generated in China, which would have an adverse impact on our business performance.

Financial Information about Industry Segments

The Company operates primarily in one business segment, the research, development, commercialization and distribution of diagnostic technologies, with primarily all of its assets and operations located in Canada. The Company’s revenues are generated from product sales primarily in China, the United States, Europe, Asia and Canada. Expenses are primarily incurred from purchases made from suppliers in Canada and the United States.

Product sales by customer location were as follows:

| | | 2011 | | | 2010 | | | 2009 | |

| | | | $ | | | $ | | | $ | |

| China | | | 5,281,063 | | | | 3,576,935 | | | | 2,273,055 | |

| United States | | | 1,551,444 | | | | 1,003,297 | | | | 3,752,552 | |

| Asia (excluding China) | | | 794,667 | | | | 844,633 | | | | 774,676 | |

| Europe | | | 654,649 | | | | 812,328 | | | | 801,629 | |

| Canada | | | 59,148 | | | | 52,872 | | | | 76,484 | |

| Other | | | 683,112 | | | | 502,065 | | | | 474,653 | |

| Total | | | 9,024,083 | | | | 6,792,130 | | | | 8,153,049 | |

Product sales by type of product were as follows:

| | | 2011 | | | 2010 | | | 2009 | |

| | | $ | | | $ | | | $ | |

| Cardiovascular | | | 7,295,501 | | | | 5,969,672 | | | | 5,984,267 | |

| Infectious Diseases | | | 587,040 | | | | 67,472 | | | | 844,384 | |

| | | 659,463 | | | | 444,895 | | | | 517,981 | |

Vector Infectious Diseases | | | 482,080 | | | | 310,090 | | | | 806,417 | |

| Total | | | 9,024,083 | | | | 6,792,130 | | | | 8,153,049 | |

For further information, please see Item 6 (“Selected Financial Data”).

Working Capital

Please see Item 6 (“Selected Financial Data”) and Item 7 (“Management's Discussion and Analysis of Financial Condition and Results of Operations").

Employees

On December 31, 2011, we had 67 full-time employees.

Available Information

Our corporate Internet address is www.responsebio.com. At the "Investors" section of this website, we make available free of charge our Annual Report on Form 10-K, our Annual Proxy statement, our quarterly reports on Form 10-Q, any Current Reports on Form 8-K, and any amendments to these reports, as soon as reasonably practicable after we electronically file them with, or furnish them to, the Securities and Exchange Commission, or the SEC, as well as our previously filed reports on Forms 20-F and 6-K. The information found on our website is not part of this Annual Report on Form 10-K. In addition to our website, the Securities and Exchange Commission, or the SEC, maintains an Internet site at www.sec.gov that contains reports, proxy and information statements, and other information regarding us and other issuers that file electronically with the SEC.

Our future performance is subject to a number of risks. If any of the following risks actually occur, our business could be harmed and the trading price of our common stock could decline. In evaluating our business, you should carefully consider the following risks in addition to the other information in this Annual Report on Form 10-K. We note these factors for investors as permitted by the Private Securities Litigation Reform Act of 1995. It is not possible to predict or identify all such factors and, therefore, you should not consider the following risks to be a complete statement of all the potential risks or uncertainties that we face.

Risks Related to Our Company

We may need to raise additional capital to fund operations. If we are unsuccessful in attracting capital to our Company, we will not be able to continue operations or will be forced to sell assets to do so. Alternatively, capital may not be available to our Company on favorable terms, or at all. If available, financing terms may lead to significant dilution to the shareholders' equity in our Company.

We are not profitable and have negative cash flow from operations. Based on our current cash resources, expected cash burn, and anticipated revenues, we expect that we can maintain operations through the fourth quarter of 2012. We may need to raise additional capital to fund our operations. We have relied primarily on debt and equity financings to fund our operations and commercialize our products. Additional capital may not be available, at such times or in amounts as needed by us. Even if capital is available, it might be on adverse terms. Any additional equity financing will be dilutive to our shareholders. If access to sufficient capital is not available as and when needed, our business will be materially impaired and we may be required to cease operations, curtail one or more product development programs, attempt to obtain funds through collaborative partners or others that may require us to relinquish rights to certain technologies or product candidates, or we may be required to significantly reduce expenses, sell assets, seek a merger or joint venture partner, file for protection from creditors or liquidate all our assets.

Our inability to generate sufficient cash flows may result in our Company not being able to continue as a going concern.

We have incurred significant losses to date. As at December 31, 2011, we had an accumulated deficit of $106,890,091 and had not generated positive cash flow from operations. Accordingly, there is substantial doubt about our ability to continue as a going concern. We may need to seek additional financing to support our continued operation; however, there are no assurances that any such financing can be obtained on favorable terms, if at all. In view of these conditions, our ability to continue as a going concern is dependent upon our ability to obtain such financing and, ultimately, on achieving profitable operations. The outcome of these matters cannot be predicted at this time. The consolidated financial statements for the year ended December 31, 2011 do not include any adjustments to the amounts and classification of assets and liabilities that might be necessary should we be unable to continue in business. Such adjustments could be substantial.

We have incurred substantial operating losses to date. We expect these losses to continue for the near future. If we are unable to generate sufficient revenue, positive cash flow or earnings, or raise sufficient capital to maintain operations, we may not be able to continue operating our business and be forced to sell our Company or liquidate our assets.

We have evolved from a pure development company to a commercial enterprise but to date have realized minimal operating revenues from product sales. As of December 31, 2011, we have incurred cumulative losses since inception of $106,890,091. For the fiscal years ending December 31, 2011, 2010, and 2009, we incurred losses of $5,371,312, $10,081,911, and $9,543,531, respectively. We currently are not profitable and expect operating losses to continue. Generating revenues and profits will depend significantly on our ability to successfully develop, commercialize, manufacture and market our products. The time necessary to achieve market success for any individual product is uncertain. No assurance can be given that product development efforts will be successful, that required regulatory approvals can be obtained on a timely basis, if at all, or that approved products can be successfully manufactured or marketed. Consequently, we cannot assure that we will ever generate significant revenue or achieve or sustain profitability. As well, there can be no assurance that the costs and time required to complete commercialization will not exceed current estimates. We may also encounter difficulties or problems relating to research, development, manufacturing, distribution and marketing of our products. In the event that we are unable to generate adequate revenues, cash flow or earnings, to support our operations, or we are unable to raise sufficient capital to do so, we may be forced to cease operations and either sell our business or liquidate our assets.

Current and future conditions in the global economy may have a material adverse effect on our business prospects, financial condition and results of operations.

During the second half of fiscal year 2008, the global financial crisis, particularly affecting the credit and equity markets, accelerated and the global recession deepened, with an exceptionally weak global economy in 2009 and 2010 followed by a mixed economic performance during 2011. Though we cannot predict the extent, timing or ramifications of the global financial crisis and the economic outlook in different economies, we believe that the current downturn in the world's major economies and the constraints in the credit markets have heightened or could heighten a number of material risks to our business, results of operations, cash flows and financial condition, as well as our future prospects, including the following:

| · | Credit availability and access to equity markets — Continued issues involving liquidity and capital adequacy affecting lenders could affect our ability to fully obtain credit facilities or additional debt and could affect the ability of any lenders to meet their funding requirements when we need to borrow. Further, the high level of volatility in the equity markets and the decline in our stock price may make it difficult for us to access the equity markets for additional capital at attractive prices, if at all. If we are unable to obtain credit, or access the capital markets, where required, our business could be negatively impacted. |

| · | Credit availability to our customers — We believe that many of our customers are reliant on liquidity from global credit markets and, in some cases, require external financing to fund their operations. As a consequence, if our customers lack liquidity, it would likely negatively impact their ability to pay amounts due to us. |

| · | Commitments from our customers — There is a greater risk that customers may be slower to make purchase commitments during the current economic downturn, which may negatively impact the sales of our new and existing products. |

| · | Supplier difficulties — If one or more of our suppliers experiences difficulties that result in a reduction or interruption in supplies or services to us, or they fail to meet any of our manufacturing requirements, our business could be adversely impacted until we are able to secure alternative sources, if any. |

Many of these and other factors affecting the diagnostic technology industry are inherently unpredictable and beyond our control.

We are not able to predict sales in future quarters and a number of factors affect our periodic results, which makes our quarterly operating results less predictable.

We are not able to accurately predict our sales in future quarters. A significant portion of our product sales is made through distributors, including strategic alliance partners, both domestically and internationally. As a result, our financial results, quarterly product sales, trends and comparisons are affected by seasonal factors and fluctuations in the buying patterns of end-user customers, our distributors, and by the changes in inventory levels of our products held by these distributors. For example, higher utilization rates of our BNP and NT-proBNP tests may be due to a higher number of emergency department visits by patients exhibiting shortness of breath, a symptom of heart failure and of influenza. However, higher utilization may also result from greater awareness, education and acceptance of the uses of our tests, as well as from additional users within the hospitals. Accordingly, our sales in any one quarter or period are not indicative of our sales in any future period.

We generally operate with a limited order backlog, because we ship our products shortly after we receive the orders from our customers. As a result, our product sales in any quarter are generally dependent on orders that we receive and ship in that quarter. As a result, any such revenue shortfall would immediately materially and adversely impact our operating results and financial condition. The sales cycle for our products can fluctuate, which may cause revenue and operating results to vary significantly from period to period. We believe this fluctuation is primarily due (i) to seasonal patterns in the decision making processes by our independent distributors and direct customers, (ii) to inventory or timing considerations by our distributors and (iii) to the purchasing requirements by various international governments to acquire our products.