| Private and Confidential AN AFFILIATE OF PROJECT INSTRUMENT BOARD DISCUSSION MATERIALS DECEMBER 17, 2024 Exhibit (c)(v) |

| 11 Private and Confidential TABLE OF CONTENTS SECTION I EXECUTIVE SUMMARY SECTION II VIOLIN MARKET DATA SECTION III VIOLIN FINANCIAL OVERVIEW SECTION IV VALUATION |

| 22 Private and Confidential DISCLAIMER The following pages contain materials provided to the Transaction Committee (the “Committee") of VOXX International Corporation (the "Company") by Solomon Partners Securities, LLC (“Solomon”) in connection with Project Instrument. These materials were prepared on a confidential basis in connection with an oral presentation to the Committee and not with a view to public disclosure or toward complying with the disclosure standards under state or federal securities laws or other laws, rules or regulations. These materials are for use by the Committee in its evaluation of the proposed transaction and may not be used or relied upon for any other purpose or disclosed to any third party or circulated or referred to publicly without Solomon's prior written consent. The information contained in this presentation was based solely on publicly available information or historical financial information, forecasts and other information furnished to Solomon, and approved for its use, by the Committee. Solomon has relied, without independent investigation or verification, on the accuracy, completeness and fair presentation of all such information and the conclusions contained herein are conditioned upon such information (whether written or oral) being accurate, complete and fairly presented in all respects. This presentation includes certain statements, estimates and projections provided by the Company with respect to the historical and anticipated future performance of the Company. Such statements, estimates and projections contain or are based on significant assumptions and subjective judgments made by the Company’s management. None of Solomon, its affiliates or its or their respective employees, directors, officers, contractors, advisors, members, successors or agents makes any representation or warranty in respect of the accuracy, completeness or fair presentation of any information, projections or any conclusion contained herein. Solomon, its affiliates and its and their respective employees, directors, officers, contractors, advisors, members, successors and agents shall have no liability with respect to any information, projections or matter contained herein, or any oral information provided herewith or data any of them generates. The information contained herein should not be assumed to have been updated at any time subsequent to date shown on the first page of the presentation and the delivery of the presentation does not constitute a representation by Solomon that such information will be updated at any time after the date of the presentation. Solomon has not assumed any responsibility for or performed any independent valuation or appraisal of the assets or liabilities of the Company, the potential effects of volatility in the credit, financial and stock markets on the Company or any other party to the transaction, or the impact of the proposed transaction on the solvency or viability of the Company or any other party to the transaction, and the information herein does not necessarily reflect the prices at which businesses or securities actually may be sold. Neither Solomon nor any of its affiliates is an advisor as to legal, tax, accounting or regulatory matters in any jurisdiction. The Committee acknowledges that Solomon is an affiliate of Natixis, a global full service commercial and investment bank. These materials are not and should not be construed as a fairness opinion. The information herein does not constitute a recommendation to the Committee, any security holder of the Company or any other person as to how to vote or act with respect to the proposed transaction or any other matter. The information herein, including this disclaimer, is subject to, and governed by, any written agreement between the Company and the Committee, on the one hand, and Solomon, on the other hand. |

| SECTION I – EXECUTIVE SUMMARY |

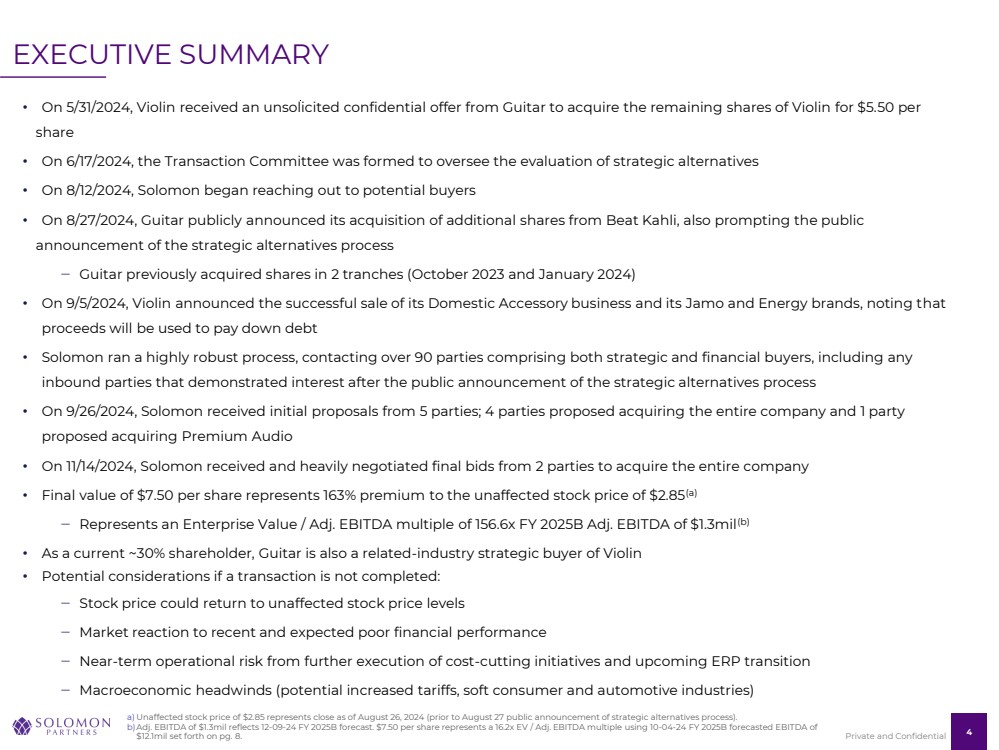

| 44 Private and Confidential • On 5/31/2024, Violin received an unsolicited confidential offer from Guitar to acquire the remaining shares of Violin for $5.50 per share • On 6/17/2024, the Transaction Committee was formed to oversee the evaluation of strategic alternatives • On 8/12/2024, Solomon began reaching out to potential buyers • On 8/27/2024, Guitar publicly announced its acquisition of additional shares from Beat Kahli, also prompting the public announcement of the strategic alternatives process ‒ Guitar previously acquired shares in 2 tranches (October 2023 and January 2024) • On 9/5/2024, Violin announced the successful sale of its Domestic Accessory business and its Jamo and Energy brands, noting that proceeds will be used to pay down debt • Solomon ran a highly robust process, contacting over 90 parties comprising both strategic and financial buyers, including any inbound parties that demonstrated interest after the public announcement of the strategic alternatives process • On 9/26/2024, Solomon received initial proposals from 5 parties; 4 parties proposed acquiring the entire company and 1 party proposed acquiring Premium Audio • On 11/14/2024, Solomon received and heavily negotiated final bids from 2 parties to acquire the entire company • Final value of $7.50 per share represents 163% premium to the unaffected stock price of $2.85(a) ‒ Represents an Enterprise Value / Adj. EBITDA multiple of 156.6x FY 2025B Adj. EBITDA of $1.3mil(b) • As a current ~30% shareholder, Guitar is also a related-industry strategic buyer of Violin • Potential considerations if a transaction is not completed: ‒ Stock price could return to unaffected stock price levels ‒ Market reaction to recent and expected poor financial performance ‒ Near-term operational risk from further execution of cost-cutting initiatives and upcoming ERP transition ‒ Macroeconomic headwinds (potential increased tariffs, soft consumer and automotive industries) EXECUTIVE SUMMARY a) Unaffected stock price of $2.85 represents close as of August 26, 2024 (prior to August 27 public announcement of strategic alternatives process). b)Adj. EBITDA of $1.3mil reflects 12-09-24 FY 2025B forecast. $7.50 per share represents a 16.2x EV / Adj. EBITDA multiple using 10-04-24 FY 2025B forecasted EBITDA of $12.1mil set forth on pg. 8. |

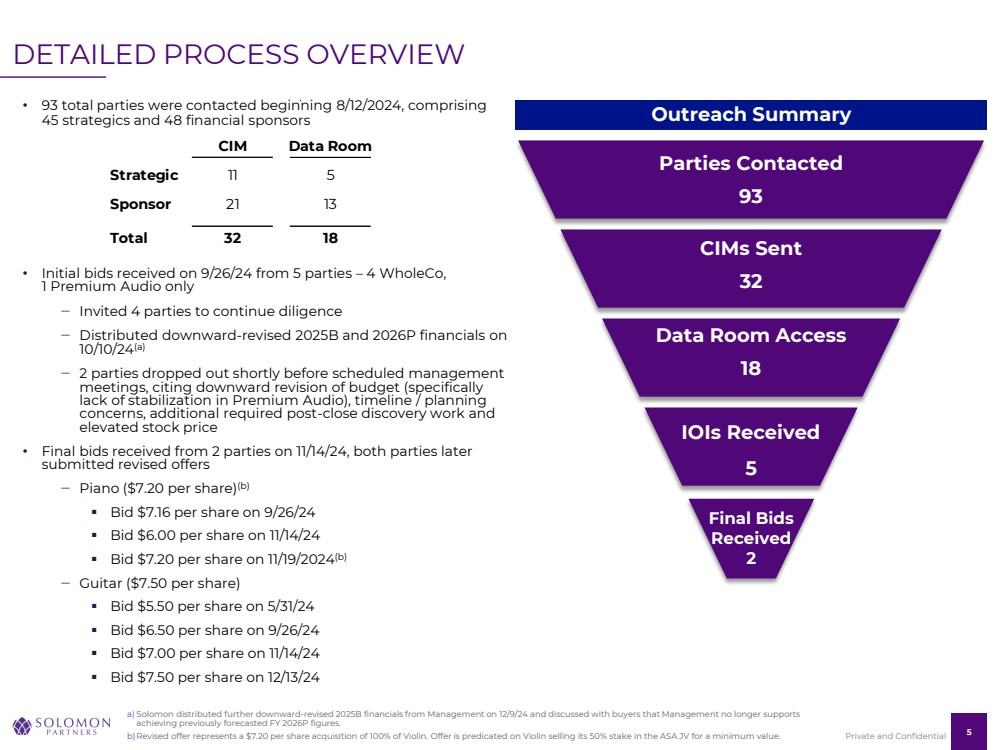

| 55 Private and Confidential • 93 total parties were contacted beginning 8/12/2024, comprising 45 strategics and 48 financial sponsors • Initial bids received on 9/26/24 from 5 parties – 4 WholeCo, 1 Premium Audio only ‒ Invited 4 parties to continue diligence ‒ Distributed downward-revised 2025B and 2026P financials on 10/10/24(a) ‒ 2 parties dropped out shortly before scheduled management meetings, citing downward revision of budget (specifically lack of stabilization in Premium Audio), timeline / planning concerns, additional required post-close discovery work and elevated stock price • Final bids received from 2 parties on 11/14/24, both parties later submitted revised offers ‒ Piano ($7.20 per share)(b) ▪ Bid $7.16 per share on 9/26/24 ▪ Bid $6.00 per share on 11/14/24 ▪ Bid $7.20 per share on 11/19/2024(b) ‒ Guitar ($7.50 per share) ▪ Bid $5.50 per share on 5/31/24 ▪ Bid $6.50 per share on 9/26/24 ▪ Bid $7.00 per share on 11/14/24 ▪ Bid $7.50 per share on 12/13/24 DETAILED PROCESS OVERVIEW a) Solomon distributed further downward-revised 2025B financials from Management on 12/9/24 and discussed with buyers that Management no longer supports achieving previously forecasted FY 2026P figures. b)Revised offer represents a $7.20 per share acquisition of 100% of Violin. Offer is predicated on Violin selling its 50% stake in the ASA JV for a minimum value. Outreach Summary 32 CIMs Sent Parties Contacted 93 18 Data Room Access Bids 5 IOIs Received Final Bids Received 2 CIM Data Room Strategic 11 5 Sponsor 21 13 Total 32 18 |

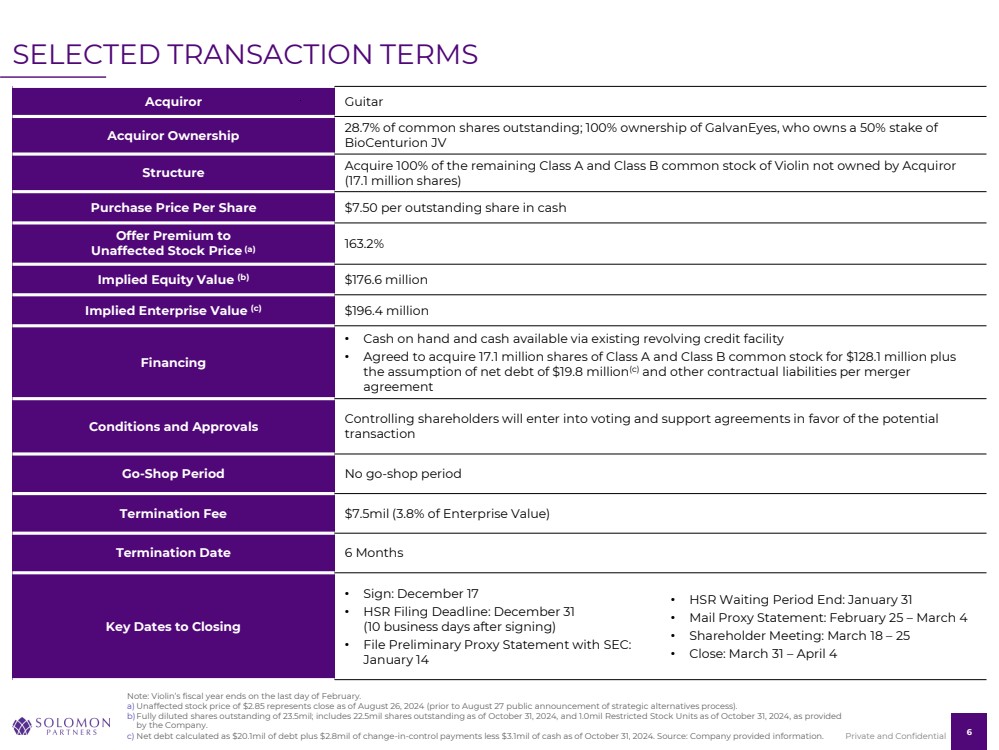

| 66 Private and Confidential SELECTED TRANSACTION TERMS Note: Violin’s fiscal year ends on the last day of February. a) Unaffected stock price of $2.85 represents close as of August 26, 2024 (prior to August 27 public announcement of strategic alternatives process). b)Fully diluted shares outstanding of 23.5mil; includes 22.5mil shares outstanding as of October 31, 2024, and 1.0mil Restricted Stock Units as of October 31, 2024, as provided by the Company. c) Net debt calculated as $20.1mil of debt plus $2.8mil of change-in-control payments less $3.1mil of cash as of October 31, 2024. Source: Company provided information. Acquiror Guitar Acquiror Ownership 28.7% of common shares outstanding; 100% ownership of GalvanEyes, who owns a 50% stake of BioCenturion JV Structure Acquire 100% of the remaining Class A and Class B common stock of Violin not owned by Acquiror (17.1 million shares) Purchase Price Per Share $7.50 per outstanding share in cash Offer Premium to Unaffected Stock Price (a) 163.2% Implied Equity Value (b) $176.6 million Implied Enterprise Value (c) $196.4 million Financing • Cash on hand and cash available via existing revolving credit facility • Agreed to acquire 17.1 million shares of Class A and Class B common stock for $128.1 million plus the assumption of net debt of $19.8 million(c) and other contractual liabilities per merger agreement Conditions and Approvals Controlling shareholders will enter into voting and support agreements in favor of the potential transaction Go-Shop Period No go-shop period Termination Fee $7.5mil (3.8% of Enterprise Value) Termination Date 6 Months Key Dates to Closing • Sign: December 17 • HSR Filing Deadline: December 31 (10 business days after signing) • File Preliminary Proxy Statement with SEC: January 14 • HSR Waiting Period End: January 31 • Mail Proxy Statement: February 25 – March 4 • Shareholder Meeting: March 18 – 25 • Close: March 31 – April 4 |

| 77 Private and Confidential TRANSACTION PRICE ANALYSIS Source: Capital IQ and Management provided information as of December 16, 2024; totals may not foot due to rounding. Note: Violin’s fiscal year ends on the last day of February. a) Unaffected stock price represents stock price on 8/26/2024, the day before 8/27/2024 public announcement of strategic alternatives process. All financials included in enterprise value calculation represent financials as of May 31, 2024 as represented in the FY Q1 2025 10-Q. Does not include negative non-controlling interest of ($39.4mil) as of May 31, 2024. b)Shares outstanding as of October 31, 2024. Class A shares are entitled to one vote per share. Source: Company provided information. c) Shares outstanding as of October 31, 2024. Class B shares are entitled to ten votes per share. Class B shares are entirely owned by Violin’s founder, John Shalam, and his family. Source: Company provided information. d)As of October 31, 2024. Source: Company provided information. e) Does not include negative non-controlling interest of ($40.6mil) as of August 31, 2024. Comprises ($4.0mil) of redeemable non-controlling interest related to Onkyo acquisition and ($36.6mil) of non-controlling interest related to EyeLock. f) Represents payments due upon a change-in-control. Source: Company provided information. g)Source: Capital IQ as of December 16, 2024. Volume-weighted average closing price for the 90 most recent trading days from August 9, 2024 to December 16, 2024. h)Source: “FY 2021-2025 Historical and Projected Quarterly PL (Excl. Domestic Accessory, EyeLock and BioCenturion)(Updated FY25_12.09.24) as provided to Solomon Partners on December 9, 2024, and approved for its use by the Committee. Financials include actual figures through October 31, 2024 and actual sales for November 2024. i) Note: Excludes ~($0.4mil) of negative equity income in BioCenturion JV in FY 2025B. BioCenturion JV is a 50/50 partnership between EyeLock, a majority-owned subsidiary of Violin, and GalvanEyes. (Amounts in Millions USD, Except Per Share Data) Unaffected Proposed Stock Price (a) Offer Price Stock Price $2.85 $7.50 Class A Shares Outstanding 20.2 20.3 (b) Class B Shares Outstanding 2.3 2.3 (c) Restricted Stock Units -- 1.0 (d) Diluted Shares Outstanding 22.5 23.5 Total Equity Value $64.1 $176.6 Plus: Debt $67.8 $20.1 (d) Less: Cash (4.2) (3.1) (d) Plus: Non-controlling Interest -- -- (e) Plus: Change-in-Control Payments -- 2.8 (f) Total Enterprise Value $127.7 $196.4 Premium / (Discount) to: Close On 12/16/2024 $8.00 (64.4) % (6.3) % Unaffected Stock Price (a) 2.85 -- 163.2 Guitar Original Offer On 5/31/2024 5.50 (48.2) 36.4 90 Trading Day VWAP (g) 4.95 (42.5) 51.4 1-Year Median 6.92 (58.8) 8.4 1-Year High 11.45 (75.1) (34.5) 1-Year Low 2.32 22.8 223.3 Enterprise Value as a Multiple of: Adjusted EBITDA - Management (h)(i) FY 2025B $1.3 156.6 x |

| 88 Private and Confidential $17.1 $12.1 $1.3 08-15-24 Forecast (a) 10-04-24 Forecast (b) 12-09-24 Forecast (c) $408.9 $405.1 $375.9 08-15-24 Forecast (a) 10-04-24 Forecast (b) 12-09-24 Forecast (c) CHANGES TO MANAGEMENT FY 2025 BUDGET OVER TIME Note: Violin’s fiscal year ends on the last day of February. a) Source: "FY 2021-2026 Historical and Projected P&L (Excl. Domestic Accessory, EyeLock and BioCenturion)", as provided to Solomon Partners on August 15, 2024, and approved for its use by the Committee. Financials include actual figures through June 30, 2024 and actual sales figures for July 2024. b)Source: "FY 2021-2026 Historical and Projected P&L (Excl. Domestic Accessory, EyeLock and BioCenturion)(as of 8.31.24)", as provided to Solomon Partners on October 4, 2024, and approved for its use by the Committee. Financials include actual figures through August 31, 2024. c) Source: “FY 2021-2025 Historical and Projected Quarterly PL (Excl. Domestic Accessory, EyeLock and BioCenturion)(Updated FY25_12.09.24)”, as provided to Solomon Partners on December 9, 2024, and approved for its use by the Committee. Financials include actual figures through October 31, 2024 and actual sales figures for November 2024. NET SALES ADJUSTED EBITDA ($33.0) (8.1%) ($15.8) (92.7%) (Amounts in Millions USD) |

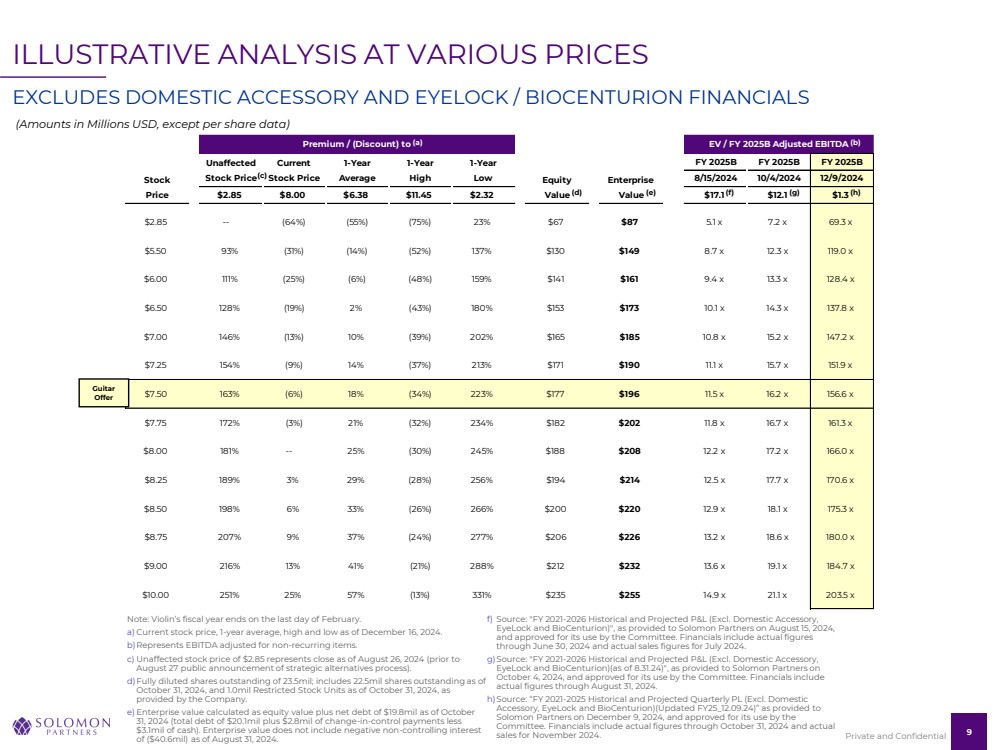

| 99 Private and Confidential Premium / (Discount) to EV / FY 2025B Adjusted EBITDA EV / Adjusted EBITDA Unaffected Current 1-Year 1-Year 1-Year FY 2025B FY 2025B FY 2025B Stock Stock Price Stock Price Average High Low Equity Enterprise 8/15/2024 10/4/2024 12/9/2024 Price $2.85 $8.00 $6.38 $11.45 $2.32 Value Value $17.1 $12.1 $1.3 $2.85 -- (64%) (55%) (75%) 23% $67 $87 5.1 x 7.2 x 69.3 x $5.50 93% (31%) (14%) (52%) 137% $130 $149 8.7 x 12.3 x 119.0 x $6.00 111% (25%) (6%) (48%) 159% $141 $161 9.4 x 13.3 x 128.4 x $6.50 128% (19%) 2 % (43%) 180% $153 $173 10.1 x 14.3 x 137.8 x $7.00 146% (13%) 10% (39%) 202% $165 $185 10.8 x 15.2 x 147.2 x $7.25 154% (9%) 14% (37%) 213% $171 $190 11.1 x 15.7 x 151.9 x $7.50 163% (6%) 18% (34%) 223% $177 $196 11.5 x 16.2 x 156.6 x $7.75 172% (3%) 21% (32%) 234% $182 $202 11.8 x 16.7 x 161.3 x $8.00 181% -- 25% (30%) 245% $188 $208 12.2 x 17.2 x 166.0 x $8.25 189% 3% 29% (28%) 256% $194 $214 12.5 x 17.7 x 170.6 x $8.50 198% 6% 33% (26%) 266% $200 $220 12.9 x 18.1 x 175.3 x $8.75 207% 9% 37% (24%) 277% $206 $226 13.2 x 18.6 x 180.0 x $9.00 216% 13% 41% (21%) 288% $212 $232 13.6 x 19.1 x 184.7 x $10.00 251% 25% 57% (13%) 331% $235 $255 14.9 x 21.1 x 203.5 x Note: Violin’s fiscal year ends on the last day of February. a) Current stock price, 1-year average, high and low as of December 16, 2024. b)Represents EBITDA adjusted for non-recurring items. c) Unaffected stock price of $2.85 represents close as of August 26, 2024 (prior to August 27 public announcement of strategic alternatives process). d)Fully diluted shares outstanding of 23.5mil; includes 22.5mil shares outstanding as of October 31, 2024, and 1.0mil Restricted Stock Units as of October 31, 2024, as provided by the Company. e) Enterprise value calculated as equity value plus net debt of $19.8mil as of October 31, 2024 (total debt of $20.1mil plus $2.8mil of change-in-control payments less $3.1mil of cash). Enterprise value does not include negative non-controlling interest of ($40.6mil) as of August 31, 2024. f) Source: "FY 2021-2026 Historical and Projected P&L (Excl. Domestic Accessory, EyeLock and BioCenturion)", as provided to Solomon Partners on August 15, 2024, and approved for its use by the Committee. Financials include actual figures through June 30, 2024 and actual sales figures for July 2024. g)Source: "FY 2021-2026 Historical and Projected P&L (Excl. Domestic Accessory, EyeLock and BioCenturion)(as of 8.31.24)", as provided to Solomon Partners on October 4, 2024, and approved for its use by the Committee. Financials include actual figures through August 31, 2024. h)Source: “FY 2021-2025 Historical and Projected Quarterly PL (Excl. Domestic Accessory, EyeLock and BioCenturion)(Updated FY25_12.09.24)” as provided to Solomon Partners on December 9, 2024, and approved for its use by the Committee. Financials include actual figures through October 31, 2024 and actual sales for November 2024. ILLUSTRATIVE ANALYSIS AT VARIOUS PRICES (Amounts in Millions USD, except per share data) EXCLUDES DOMESTIC ACCESSORY AND EYELOCK / BIOCENTURION FINANCIALS Guitar Offer (d) (c) (e) (a) (b) (f) (g) (h) |

| SECTION II – VIOLIN MARKET DATA |

| 1111 Private and Confidential -- $5.00 $10.00 $15.00 $20.00 $25.00 $30.00 Dec-19 Jun-20 Dec-20 Jun-21 Dec-21 Jun-22 Dec-22 Jun-23 Dec-23 Jun-24 Dec-24 -- $2.00 $4.00 $6.00 $8.00 $10.00 $12.00 Jan-24 Feb-24 Mar-24 Apr-24 May-24 Jun-24 Jul-24 Aug-24 Sep-24 Oct-24 Nov-24 Dec-24 5/14/24: Violin reported declining YoY full-year financial results Affected Stock Price(b) Affected Stock Price(b) YEAR-TO-DATE LAST 5 YEARS VIOLIN STOCK PRICE PERFORMANCE Source: Capital IQ as of December 16, 2024. Note: Stock price Highs, Medians, and Lows calculated using daily close prices. a) Stock price on 8/26/2024, the day before 8/27/2024 public announcement of strategic alternatives. b)Represents trading after Violin’s announcement of strategic alternatives on 8/27/24. c) Represents inflated trading range from March 2020 to July 2021 due to improved financial performance driven by COVID-related macroeconomic tailwinds. 5-Yr Median: $9.07 3-Yr Median: $8.78 1-Yr Median: $6.92 YTD Median: $6.72 Unaffected: $2.85(a) 8/27/24: Violin announced evaluation of strategic alternatives Offer: $7.50 5/31/24: Guitar confidentially submitted offer to the Board of $5.50 per share to acquire 100% of Violin Price Date High $10.85 1/9/2024 Low $2.32 8/5/2024 6-Mo Median: $5.98 Offer: $7.50 Price Date High $27.18 2/17/2021 Low $1.83 3/20/2020 Unaffected: $2.85(a) 5/14/24: Violin reported declining YoY full-year financial results COVID–Affected Trading(c) 1/9/24: Violin reported declining YoY Q3 financial results and settlement of Seaguard arbitration for $42mil |

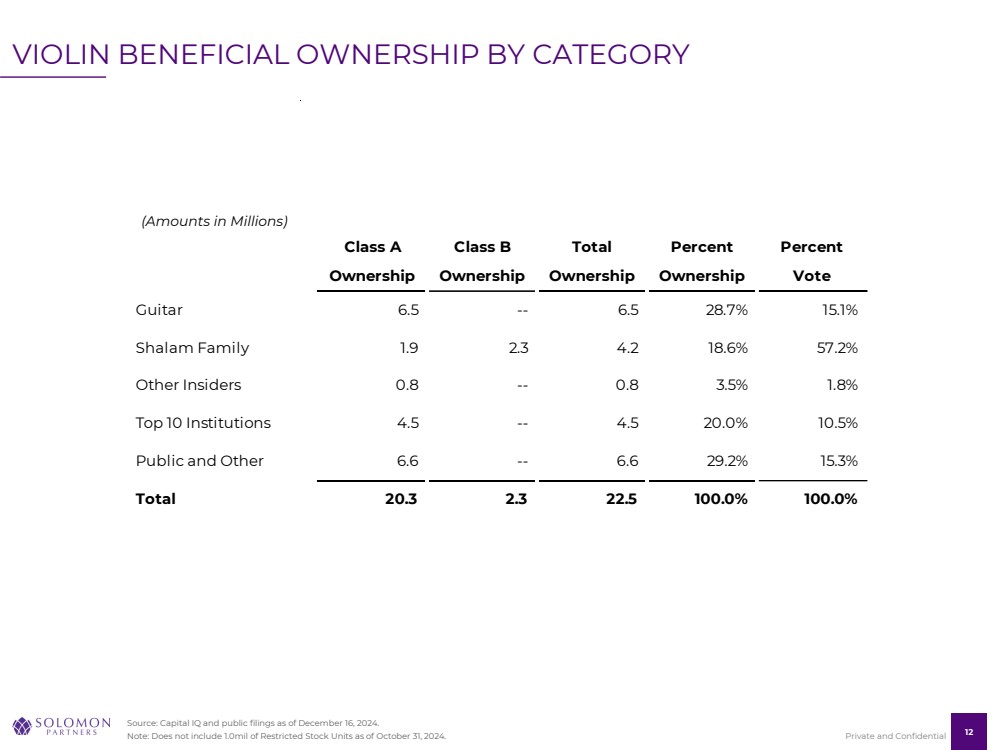

| 1212 Private and Confidential VIOLIN BENEFICIAL OWNERSHIP BY CATEGORY Source: Capital IQ and public filings as of December 16, 2024. Note: Does not include 1.0mil of Restricted Stock Units as of October 31, 2024. Class A Class B Total Percent Percent Ownership Ownership Ownership Ownership Vote Guitar 6.5 -- 6.5 28.7% 15.1% Shalam Family 1.9 2.3 4.2 18.6% 57.2% Other Insiders 0.8 -- 0.8 3.5% 1.8% Top 10 Institutions 4.5 -- 4.5 20.0% 10.5% Public and Other 6.6 -- 6.6 29.2% 15.3% Total 20.3 2.3 22.5 100.0% 100.0% (Amounts in Millions) |

| SECTION III – VIOLIN FINANCIAL OVERVIEW |

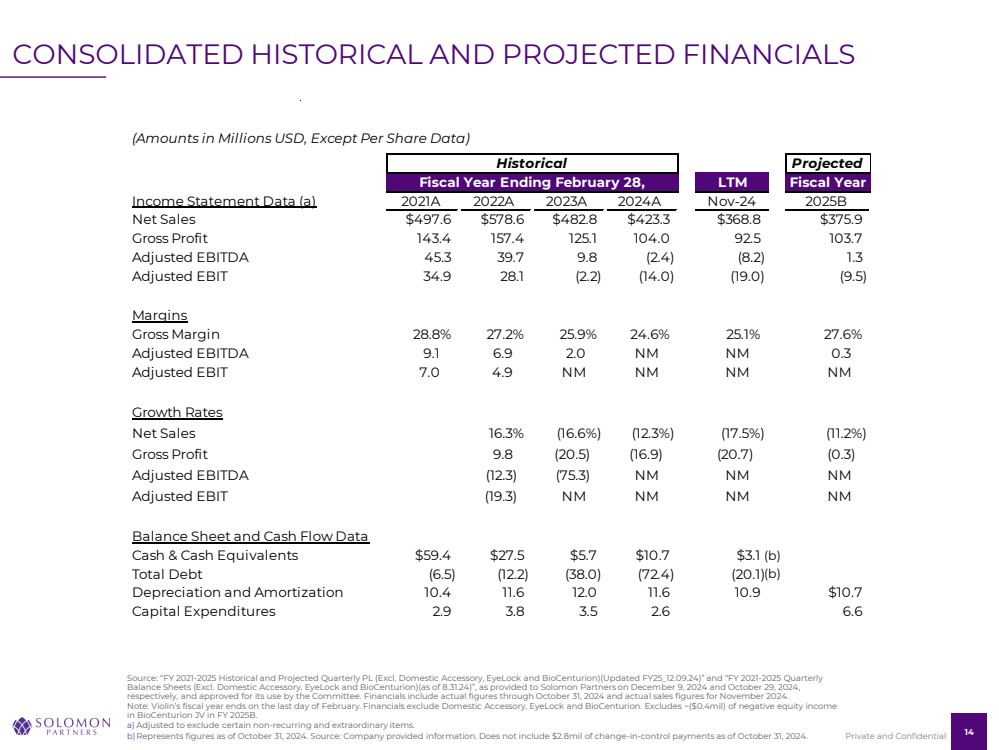

| 1414 Private and Confidential (Amounts in Millions USD, Except Per Share Data) Historical Projected Fiscal Year Ending February 28, LTM Fiscal Year Income Statement Data (a) 2021A 2022A 2023A 2024A Nov-24 2025B Net Sales $497.6 $578.6 $482.8 $423.3 $368.8 $375.9 Gross Profit 143.4 157.4 125.1 104.0 92.5 103.7 Adjusted EBITDA 45.3 39.7 9.8 (2.4) (8.2) 1.3 Adjusted EBIT 34.9 28.1 (2.2) (14.0) (19.0) (9.5) Margins Gross Margin 28.8% 27.2% 25.9% 24.6% 25.1% 27.6% Adjusted EBITDA 9.1 6.9 2.0 N M N M 0.3 Adjusted EBIT 7.0 4.9 N M N M N M N M Growth Rates Net Sales 16.3% (16.6%) (12.3%) (17.5%) (11.2%) Gross Profit 9.8 (20.5) (16.9) (20.7) (0.3) Adjusted EBITDA (12.3) (75.3) N M N M N M Adjusted EBIT (19.3) N M N M N M N M Balance Sheet and Cash Flow Data Cash & Cash Equivalents $59.4 $27.5 $5.7 $10.7 $3.1 Total Debt (6.5) (12.2) (38.0) (72.4) (20.1) Depreciation and Amortization 10.4 11.6 12.0 11.6 10.9 $10.7 Capital Expenditures 2.9 3.8 3.5 2.6 6.6 CONSOLIDATED HISTORICAL AND PROJECTED FINANCIALS Source: “FY 2021-2025 Historical and Projected Quarterly PL (Excl. Domestic Accessory, EyeLock and BioCenturion)(Updated FY25_12.09.24)” and “FY 2021-2025 Quarterly Balance Sheets (Excl. Domestic Accessory, EyeLock and BioCenturion)(as of 8.31.24)”, as provided to Solomon Partners on December 9, 2024 and October 29, 2024, respectively, and approved for its use by the Committee. Financials include actual figures through October 31, 2024 and actual sales figures for November 2024. Note: Violin’s fiscal year ends on the last day of February. Financials exclude Domestic Accessory, EyeLock and BioCenturion. Excludes ~($0.4mil) of negative equity income in BioCenturion JV in FY 2025B. a) Adjusted to exclude certain non-recurring and extraordinary items. b)Represents figures as of October 31, 2024. Source: Company provided information. Does not include $2.8mil of change-in-control payments as of October 31, 2024. (b) (b) |

| 1515 Private and Confidential HISTORICAL AND PROJECTED FINANCIALS BY SEGMENT Source: “FY 2021-2025 Historical and Projected Quarterly PL (Excl. Domestic Accessory, EyeLock and BioCenturion)(Updated FY25_12.09.24)” as provided to Solomon Partners on December 9, 2024, and approved for its use by the Committee. Financials include actual figures through October 31, 2024 and actual sales figures for November 2024. Note: Violin’s fiscal year ends on the last day of February. Financials exclude Domestic Accessory, EyeLock and BioCenturion. Excludes ~($0.4mil) of negative equity income in BioCenturion JV in FY 2025B. a) Adjusted to exclude certain non-recurring and extraordinary items. (a) (Amounts in Millions USD) Historical Budget CAGR FY 2021A FY 2022A FY 2023A FY 2024A FY 2025B FY '21-FY '25 Premium Audio $299.9 $344.0 $274.5 $237.9 $221.1 (5.9%) Automotive Aftermarket 117.7 135.6 101.8 84.1 74.8 (8.7%) Automotive OEM 46.2 65.0 73.0 58.3 46.1 (0.0%) European Accessory 33.1 33.5 33.1 43.6 33.7 0.4% Corporate 0.7 0.5 0.4 (0.6) 0.3 Total Revenue $497.6 $578.6 $482.8 $423.3 $375.9 (5.5%) Growth 16.3% (16.6%) (12.3%) (11.2%) Premium Audio $92.2 $98.0 $72.0 $60.4 $62.7 (7.4%) Automotive Aftermarket 33.5 43.7 36.6 31.0 27.0 (4.2%) Automotive OEM 5.8 3.6 5.8 (1.0) 3.6 (9.2%) European Accessory 10.9 11.3 10.0 12.9 10.0 (1.8%) Corporate 0.9 0.8 0.6 0.7 0.4 Total Gross Profit $143.4 $157.4 $125.1 $104.0 $103.7 (6.3%) Margin 28.8% 27.2% 25.9% 24.6% 27.6% Premium Audio $49.1 $42.2 $12.9 $8.9 $16.6 (19.5%) Automotive Aftermarket 12.4 16.4 12.1 8.2 5.0 (16.5%) Automotive OEM (5.6) (11.2) (7.5) (13.0) (7.8) NM European Accessory 2.0 1.9 1.5 3.5 0.9 (14.6%) Corporate (12.6) (9.6) (9.2) (9.9) (13.5) Total Adjusted EBITDA $45.3 $39.7 $9.8 ($2.4) $1.3 (51.2%) Growth (12.3%) (75.3%) NM NM Margin 9.1% 6.9% 2.0% NM 0.3% |

| SECTION IV – VALUATION |

| 1717 Private and Confidential $3 $7 $121 $74 $6 $15 $212 $289 $0 $50 $100 $150 $200 $250 $300 Selected Public Companies (EV / FY 2025B Adj. EBITDA) (c) Selected Precedent Transactions (EV / FY 2025B Adj. EBITDA) (d) Sum-of-the-Parts Break-Up Sale Analysis (e) 52-Week Trading Range SUMMARY VALUATION OVERVIEW Source: Company provided information. Note: “NM” (Not Meaningful) data points reflect negative implied equity values per share. a) Unaffected stock price represents close as of August 26, 2024 (prior to August 27 public announcement of strategic alternatives process). b)Net debt calculated as $20.1mil of debt plus $2.8mil of change-in-control payments less $3.1mil of cash as of October 31, 2024. Source: Company provided information. c) Violin FY 2025B Adj. EBITDA used to represent CY 2024E EBITDA, as Violin’s fiscal year ends on the last day of February. Assumes FY 2025B Adj. EBITDA multiple of 2.6x – 5.0x. Implied equity value per share is NM due to net debt of $19.8mil exceeding implied enterprise value. Using now-superseded 10-04-24 Forecast set forth on pg. 8 (which was subsequently lowered by Management on 12-09-24), implied equity value per share range would have been $0.52 to $1.74. d)Violin FY 2025B Adj. EBITDA used to represent LTM EBITDA, as Violin’s LTM EBITDA is negative. Assumes FY 2025B Adj. EBITDA multiple of 5.5x – 11.8x. Implied equity value per share is NM due to net debt of $19.8mil exceeding implied enterprise value. Using now-superseded 10-04-24 Forecast set forth on pg. 8 (which was subsequently lowered by Management on 12-09-24), implied equity value per share range would have been $1.99 to $5.26. e) See pg. 22 for further detail; reflects fully diluted shares outstanding of 23.5mil; includes 22.5mil shares outstanding as of October 31, 2024, and 1.0mil Restricted Stock Units as of October 31, 2024, as provided by the Company. f) Represents trading range between Violin’s release of declining FY 2024 financial results on May 14, 2024 and Violin’s public announcement of the strategic alternatives process on August 27, 2024. Offer Price $7.50 Unaffected Stock Price(a) $2.85 (Amounts in Millions USD, Except Per Share Data) Implied Enterprise Value Implied Equity Value Per Share Legend Implied Equity Value Per Share: $0.00 $1.28 $3.41 $5.53 $7.65 $9.78 $11.90 Implied Enterprise Value: $19.8 $4.29 $8.18 $2.32 $11.45 NM NM NM NM Net Debt(b) $4.53 $126 Trading Range (5/15/24-8/26/24)(f) |

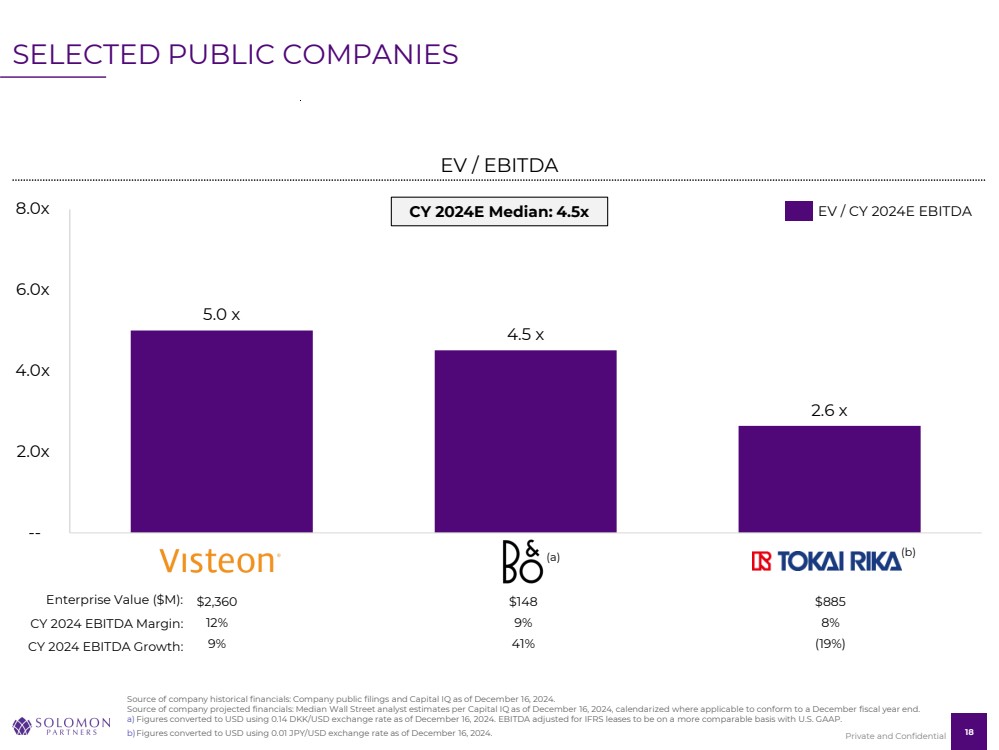

| 1818 Private and Confidential 5.0 x 4.5 x 2.6 x -- 2.0x 4.0x 6.0x 8.0x Visteon B&O Tokai Rika $2,360 $148 $885 12% 9% 8% 9% 41% (19%) EV / EBITDA SELECTED PUBLIC COMPANIES Source of company historical financials: Company public filings and Capital IQ as of December 16, 2024. Source of company projected financials: Median Wall Street analyst estimates per Capital IQ as of December 16, 2024, calendarized where applicable to conform to a December fiscal year end. a) Figures converted to USD using 0.14 DKK/USD exchange rate as of December 16, 2024. EBITDA adjusted for IFRS leases to be on a more comparable basis with U.S. GAAP. b)Figures converted to USD using 0.01 JPY/USD exchange rate as of December 16, 2024. CY 2024E Median: 4.5x Enterprise Value ($M): CY 2024 EBITDA Margin: (a) EV / CY 2024E EBITDA CY 2024 EBITDA Growth: (b) |

| 1919 Private and Confidential SUMMARY VALUATION BASED ON SELECTED PUBLIC COMPANIES Note: Violin’s fiscal year ends on the last day of February. a) Net debt calculated as $20.1mil of debt plus $2.8mil of change-in-control payments less $3.1mil of cash as of October 31, 2024. Source: Company provided information. b)Fully diluted shares outstanding of 23.5mil; includes 22.5mil shares outstanding as of October 31, 2024, and 1.0mil Restricted Stock Units as of October 31, 2024, as provided by the Company. c) Source: “FY 2021-2025 Historical and Projected Quarterly PL (Excl. Domestic Accessory, EyeLock and BioCenturion)(Updated FY25_12.09.24)” as provided to Solomon Partners on December 9, 2024, and approved for its use by the Committee. Financials include actual figures through October 31, 2024 and actual sales for November 2024. d)Violin FY 2025B figures represent CY 2024E figures, as Violin’s fiscal year ends on the last day of February. Multiples are on a calendar-year basis. (Amounts in Millions USD, Except Per Share Data) Valuation Implied Less: Implied Implied Per Multiples Enterprise Value Net Debt (a) Equity Value Share Value (b) FY 2025B Adj. EBITDA (c) (d) $1.3 2.6 x - 5.0 x $3.3 - $6.3 ($19.8) NM NM NM NM |

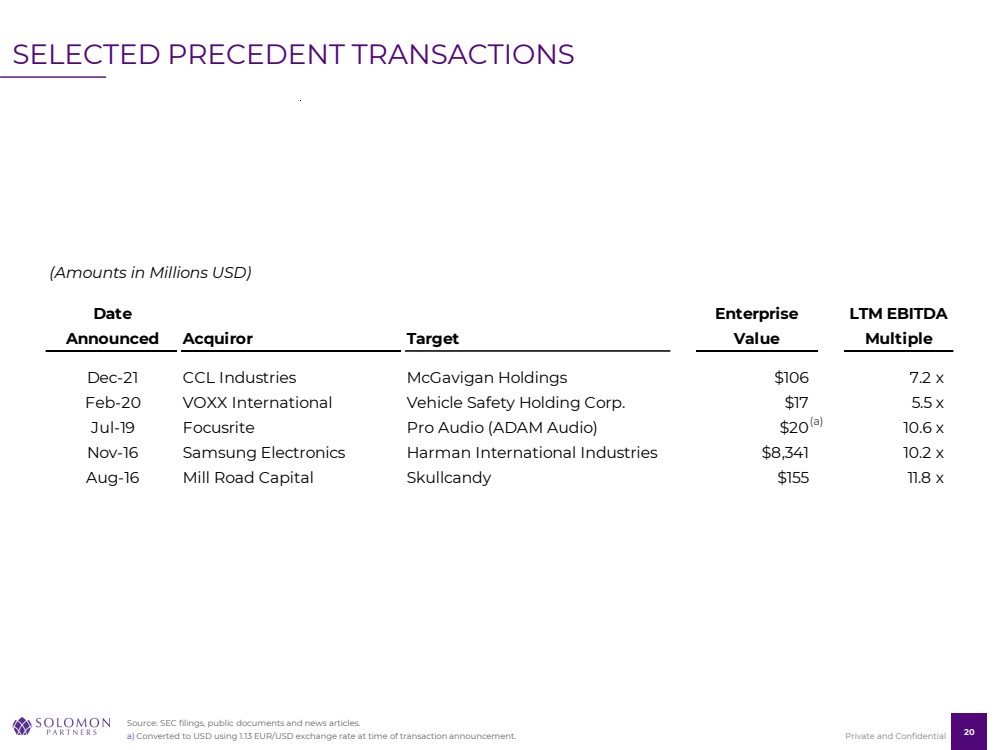

| 2020 Private and Confidential Source: SEC filings, public documents and news articles. a) Converted to USD using 1.13 EUR/USD exchange rate at time of transaction announcement. SELECTED PRECEDENT TRANSACTIONS (a) (Amounts in Millions USD) Date Announced Acquiror Target Enterprise Value LTM EBITDA Multiple Dec-21 CCL Industries McGavigan Holdings $106 7.2 x Feb-20 VOXX International Vehicle Safety Holding Corp. $17 5.5 x Jul-19 Focusrite Pro Audio (ADAM Audio) $20 10.6 x Nov-16 Samsung Electronics Harman International Industries $8,341 10.2 x Aug-16 Mill Road Capital Skullcandy $155 11.8 x |

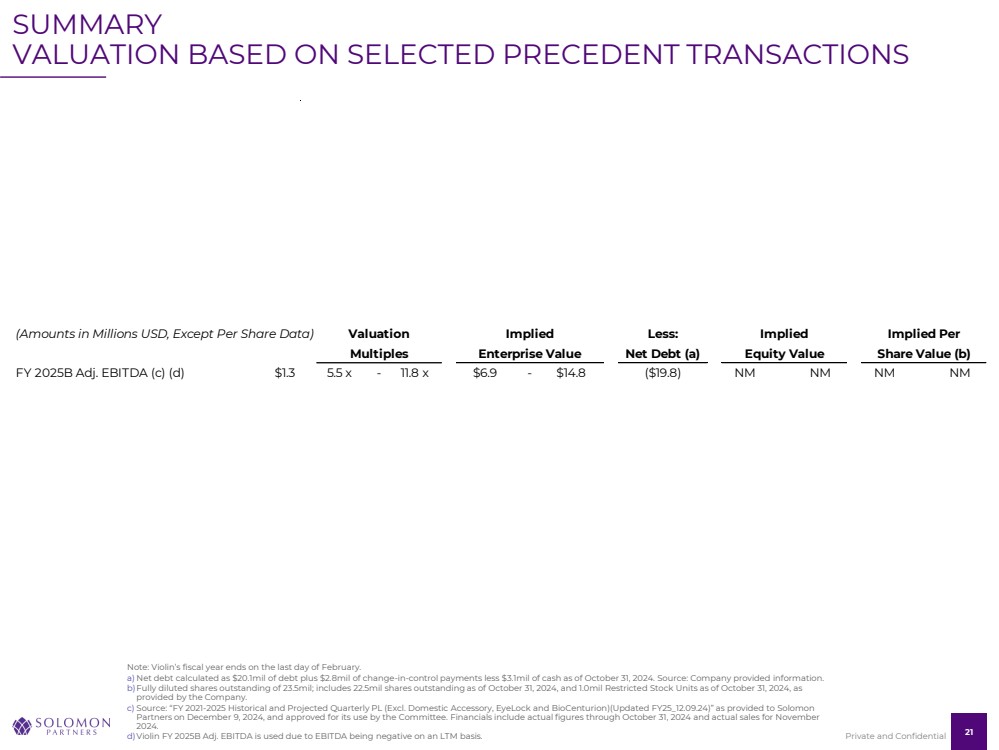

| 2121 Private and Confidential SUMMARY VALUATION BASED ON SELECTED PRECEDENT TRANSACTIONS Note: Violin’s fiscal year ends on the last day of February. a) Net debt calculated as $20.1mil of debt plus $2.8mil of change-in-control payments less $3.1mil of cash as of October 31, 2024. Source: Company provided information. b)Fully diluted shares outstanding of 23.5mil; includes 22.5mil shares outstanding as of October 31, 2024, and 1.0mil Restricted Stock Units as of October 31, 2024, as provided by the Company. c) Source: “FY 2021-2025 Historical and Projected Quarterly PL (Excl. Domestic Accessory, EyeLock and BioCenturion)(Updated FY25_12.09.24)” as provided to Solomon Partners on December 9, 2024, and approved for its use by the Committee. Financials include actual figures through October 31, 2024 and actual sales for November 2024. d)Violin FY 2025B Adj. EBITDA is used due to EBITDA being negative on an LTM basis. (Amounts in Millions USD, Except Per Share Data) Valuation Implied Less: Implied Implied Per Multiples Enterprise Value Net Debt (a) Equity Value Share Value (b) FY 2025B Adj. EBITDA (c) (d) $1.3 5.5 x - 11.8 x $6.9 - $14.8 ($19.8) NM NM NM NM |

| 2222 Private and Confidential Source: “FY 2021-2025 Historical and Projected Quarterly PL (Excl. Domestic Accessory, EyeLock and BioCenturion)(Updated FY25_12.09.24)”, as provided to Solomon Partners on December 9, 2024, and approved for its use by the Committee, and other Company provided information. a) Low-end of valuation multiples based on EV / CY2024E EBITDA multiple of comparable company, Bang and Olufsen (as detailed on pg. 18). Mid- to high-end of valuation multiples based on market tests and discussions with Management and reflects the judgement and experience of Solomon Partners. b)Comprises Automotive OEM, Automotive Aftermarket and German Accessories segments. Valuation range based on market tests and discussions with Management and reflects the judgement and experience of Solomon Partners. c) Represents Corporate EBITDA burden excluding the $3.5mil of equity income received from ASA JV. Multiple of 2.0x is a proxy for illustrative severance and transition / wind down costs. Assumes NY Headquarters would be sold with the elimination of Corporate / Shared Services and net proceeds would reduce illustrative severance and transition / wind down costs. NY Headquarters valuation range of $8mil to $12mil based on JLL appraisal values. d)Represents sale of 50% equity interest in ASA Electronics joint venture. EBITDA represents $3.5mil of equity income received from ASA JV, which is included within the Corporate EBITDA burden on a consolidated basis. Valuation multiples based on offers, market tests and discussions with Management and reflects the judgement and experience of Solomon Partners. Valuation range calculated as equity income multiplied by EV / EBITDA multiples plus 50% of the $20mil in excess cash on ASA’s balance sheet. e) Excludes ~($0.4mil) of negative equity income in BioCenturion JV in FY 2025B. BioCenturion JV is a 50/50 partnership between EyeLock, a majority-owned subsidiary of Violin, and GalvanEyes. Guitar purchased 100% of GalvanEyes equity in BioCenturion on 8/27/2024 in the form of a 10- year earnout with a maximum total payment of $8mil. There is an additional potential total earnout of $7mil in the 5 years proceeding the 10-year period, if the $8mil earnout is achieved within the 10-year period. Valuation range based on 50% of the maximum total earnout of $8mil in the 10-year period and reflects the judgement and experience of Solomon Partners. f) Net debt assumes $20.1mil of debt, $3.1mil of cash and $2.8mil of change-in-control payments as of October 31, 2024. Source: Company provided information. g)Does not include negative non-controlling interest of ($40.6mil) as of August 31, 2024. Comprises ($4.0mil) of redeemable non-controlling interest related to Onkyo acquisition and ($36.6mil) of non-controlling interest related to EyeLock. h)Fully diluted shares outstanding of 23.5mil; includes 22.5mil shares outstanding as of October 31, 2024, and 1.0mil Restricted Stock Units as of October 31, 2024, as provided by the Company. SUM-OF-THE-PARTS BREAK-UP SALE ANALYSIS Execution, timing, stranded costs, financial performance, buyer landscape, market sentiment, public disclosure, tax leakage Potential Risks Does not reflect any analysis of potential tax impacts (Amounts in Millions USD, except per share data) Sum-of-the-Parts Break-Up Sale Analysis (EV / FY 2025B Adjusted EBITDA) FY 2025B Multiple (TEV / Adj. EBITDA) Valuation Segment Adj. EBITDA Low - Mid - High Low - Mid - High Premium Audio (a) $16.6 5.0 x - 6.5 x - 8.0 x $82.8 - $107.7 - $132.5 Automotive OEM / Aftermarket and German Accessories (b) (1.8) N M N M N M 40.0 - 50.0 - 60.0 Total Segment-Level $14.7 8.3 x - 10.7 x - 13.1 x $122.8 - $157.7 - $192.5 Less: Corporate Expenses (incl. Net Proceeds from Sale of NY Headquarters) (c) ($16.9) 2.0 x 2.0 x 2.0 x ($25.9) - ($23.9) - ($21.9) Total Whole Co. ($2.2) N M N M N M $97.0 - $133.8 - $170.7 Equity in ASA Electronics Joint Venture (d) $3.5 4.0 x - 6.0 x - 8.0 x $23.8 - $30.7 - $37.6 Equity in BioCenturion Joint Venture (e) N M N M N M N M -- - 2.0 - 4.0 Total Whole Co. (incl. ASA and BioCenturion) $1.3 96.3 x - 132.8 x - 169.3 x $120.8 - 166.6 - $212.3 Less: Debt (f) ($20.1) ($20.1) ($20.1) Plus: Cash (f) 3.1 3.1 3.1 Less: Change-in-Control Payments (f) (2.8) (2.8) (2.8) Plus: Non-Controlling Interest (g) -- -- -- Equity Value $101.0 - $146.8 - $192.5 Fully Diluted Shares Outstanding (h) 23.5 23.5 23.5 Implied Share Price $4.29 - $6.23 - $8.18 Offer Price $7.50 $7.50 $7.50 % Premium / (Discount) of Offer Price to Implied Share Price 74.8% - 20.3% - (8.3%) |