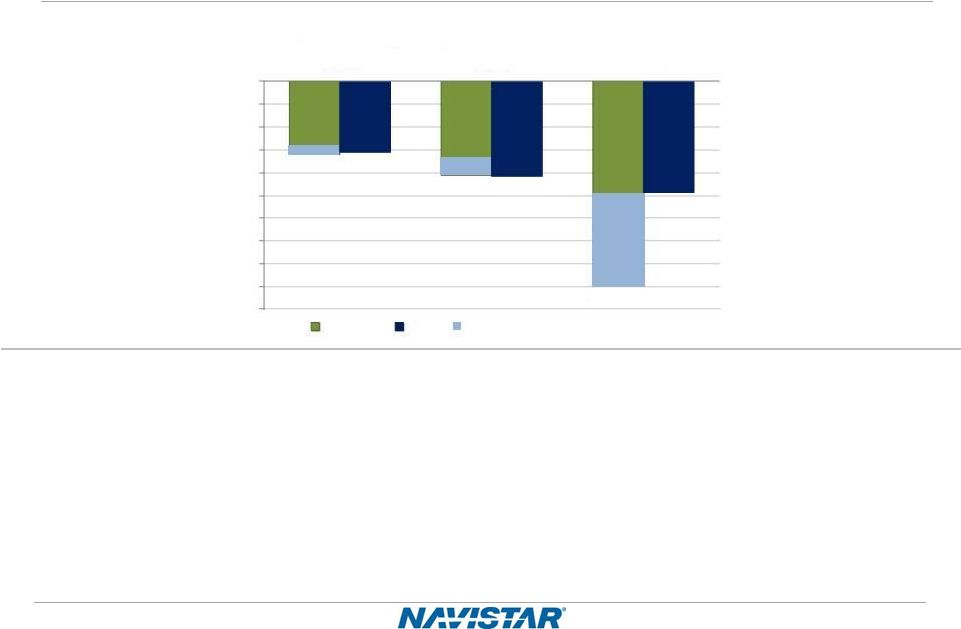

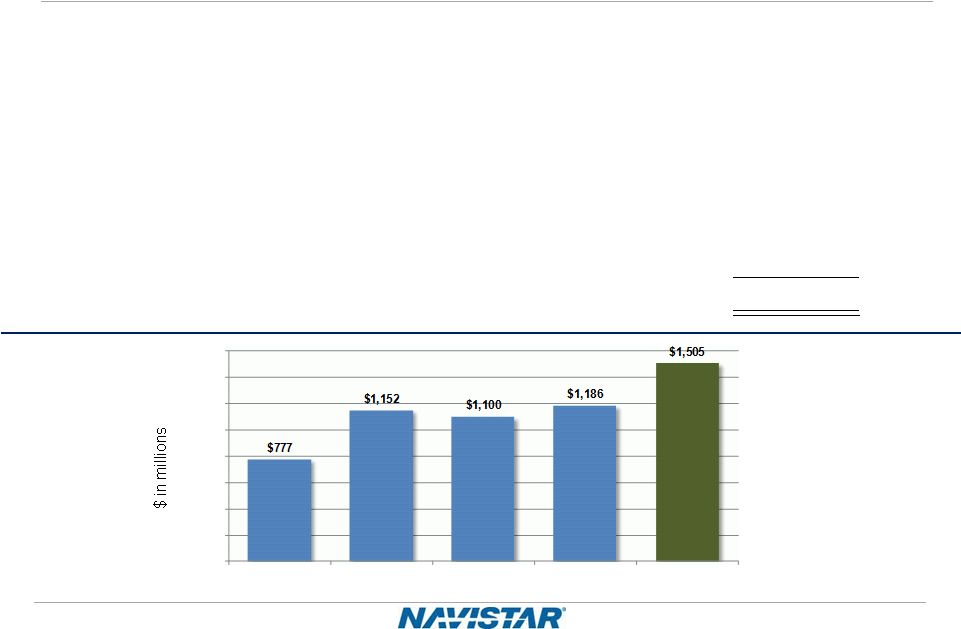

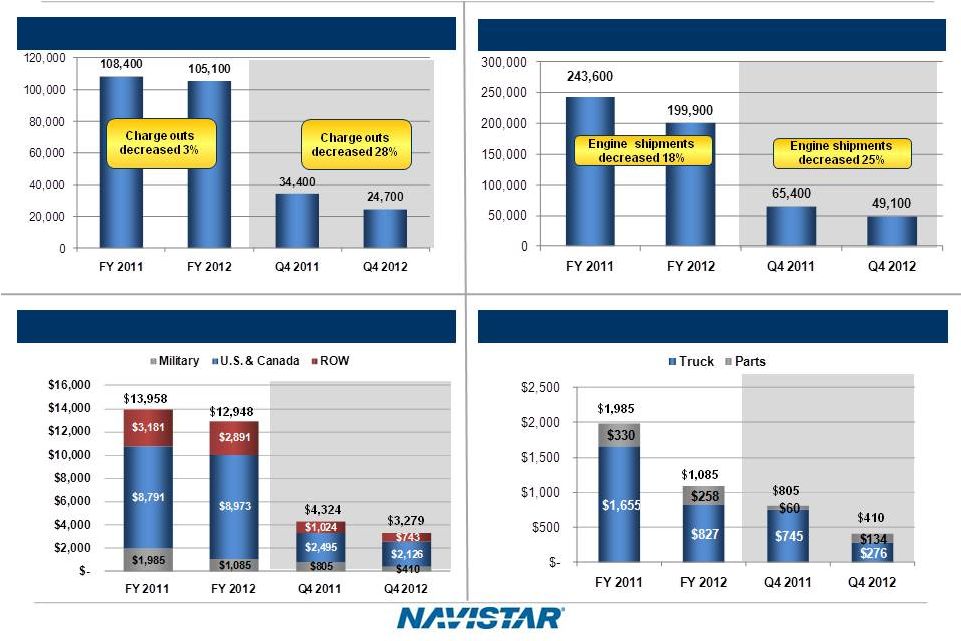

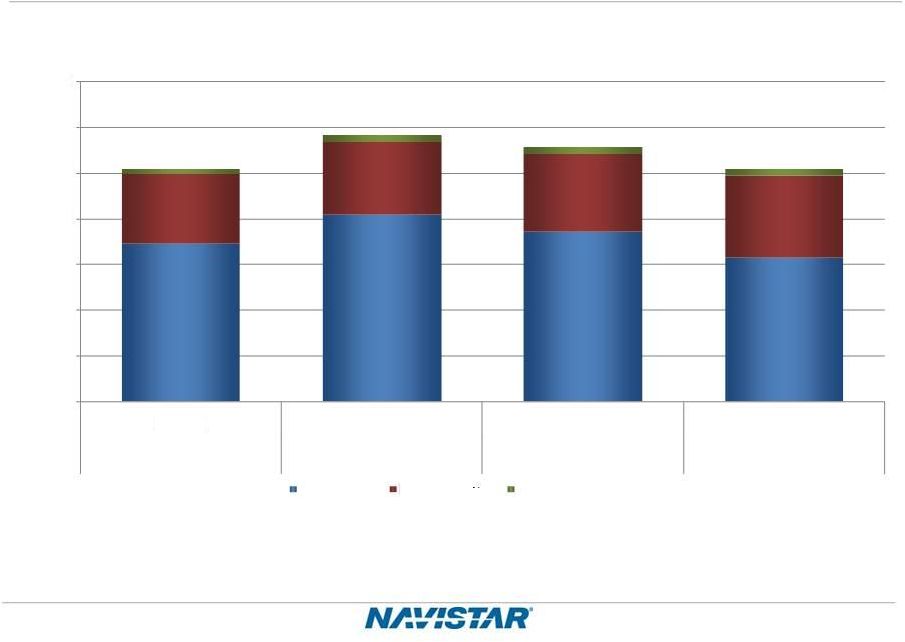

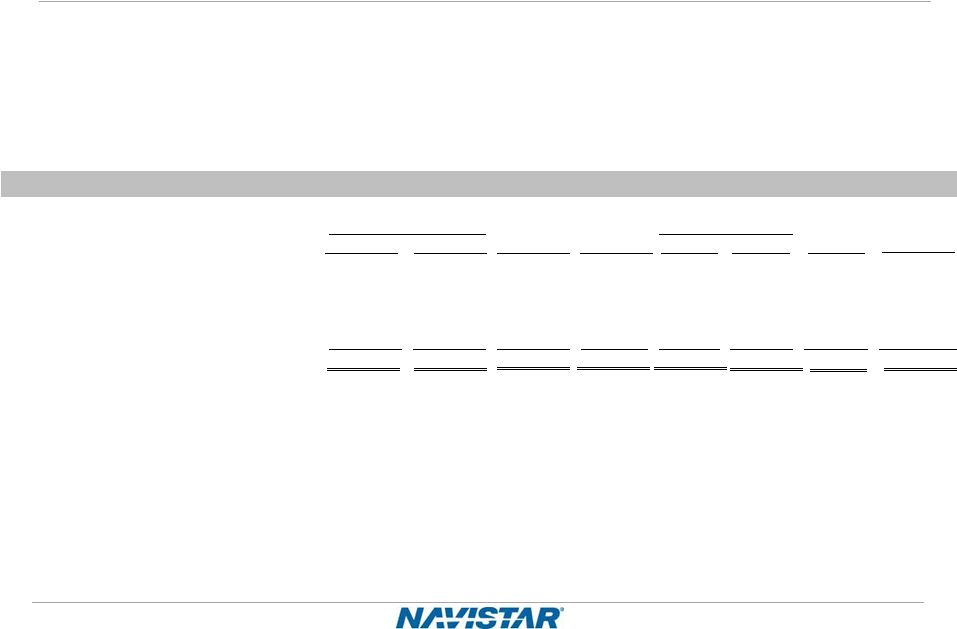

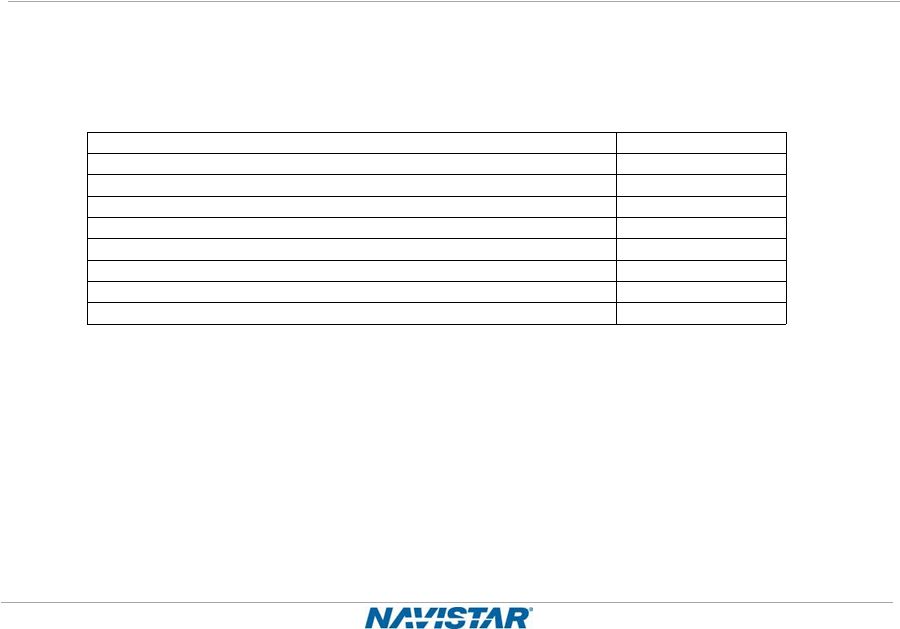

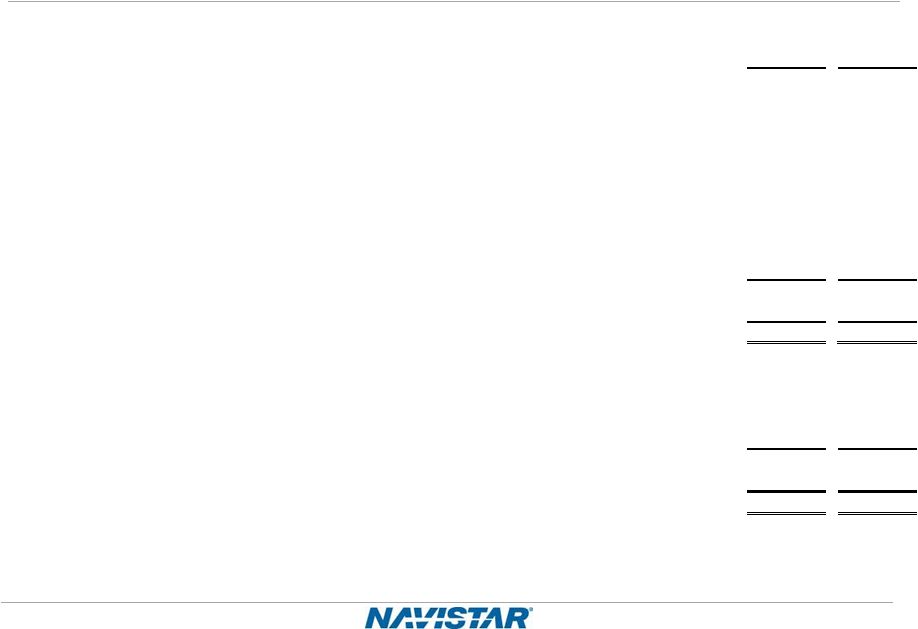

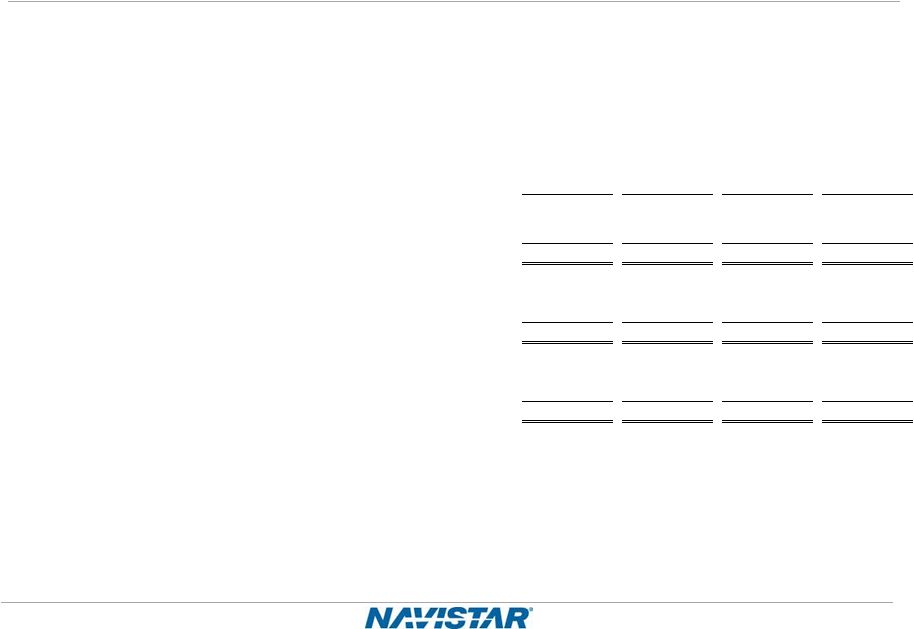

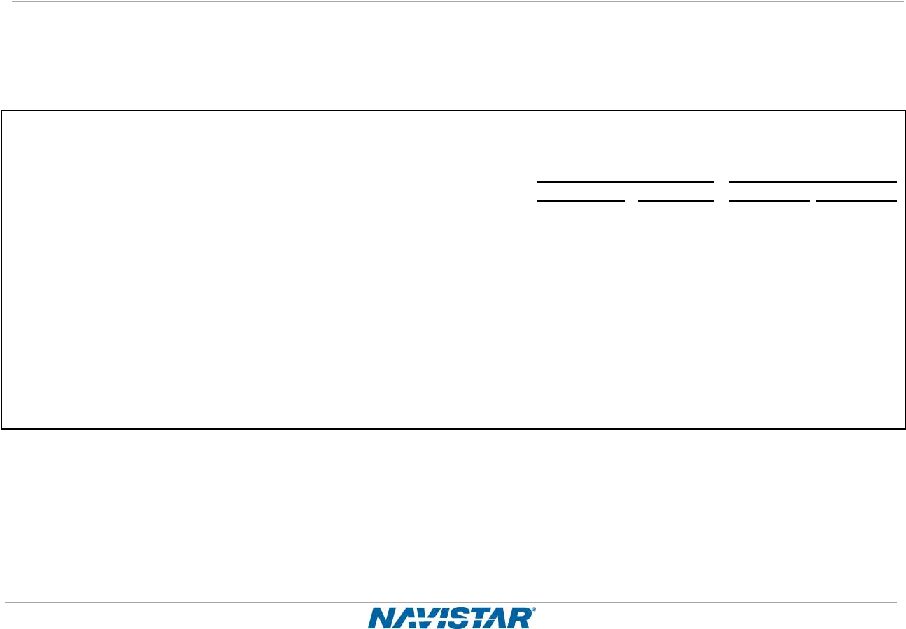

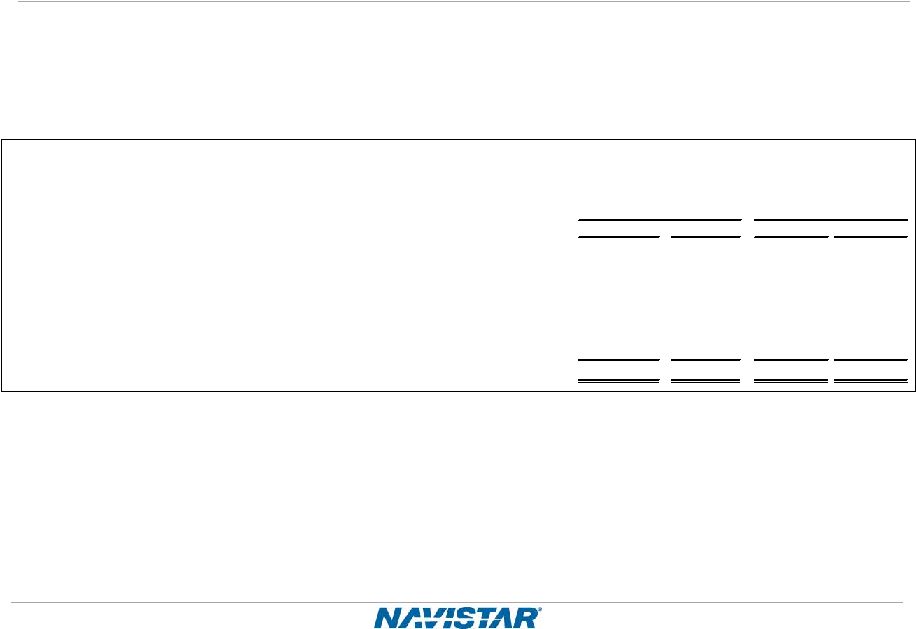

41 NYSE: NAV 4Q 2012 Earnings – 12/19/2012 Worldwide Truck Chargeouts We define our “traditional” markets to include U.S. and Canada School bus and Class 6 through 8 medium and heavy truck. We classify militarized commercial vehicles sold to the U.S. and Canadian militaries as Class 8 severe service within our “traditional” markets. Our “traditional” markets include CAT- branded units sold to Caterpillar under our North America supply agreement. FISCAL YEAR 2010 Q1 Q2 Q3 Q4 FULL YEAR BUS 3,100 3,000 2,400 3,900 12,400 MEDIUM 3,900 5,300 3,900 5,400 18,500 HEAVY 5,200 4,600 6,400 5,400 21,600 SEVERE 3,900 3,800 2,200 4,100 14,000 TOTAL 16,100 16,700 14,900 18,800 66,500 NON-TRADITIONAL MILITARY 100 200 1,000 100 1,400 EXPANSIONARY 3,900 4,500 4,700 6,000 19,100 WORLDWIDE TRUCK 20,100 21,400 20,600 24,900 87,000 FISCAL YEAR 2011 Q1 Q2 Q3 Q4 FULL YEAR BUS 2,100 2,000 2,200 2,900 9,200 MEDIUM 4,600 7,200 7,400 7,900 27,100 HEAVY 4,700 5,200 6,800 9,000 25,700 SEVERE 2,700 3,200 3,700 3,700 13,300 TOTAL 14,100 17,600 20,100 23,500 75,300 NON-TRADITIONAL MILITARY 100 400 200 700 1,400 EXPANSIONARY 5,300 7,600 8,600 10,200 31,700 WORLDWIDE TRUCK 19,500 25,600 28,900 34,400 108,400 FISCAL YEAR 2012 Q1 Q2 Q3 Q4 FULL YEAR BUS 1,700 2,600 2,900 2,500 9,700 MEDIUM 4,300 7,100 5,800 4,700 21,900 HEAVY 8,000 7,200 6,300 5,600 27,100 SEVERE 3,300 3,600 3,600 3,100 13,600 TOTAL 17,300 20,500 18,600 15,900 72,300 NON-TRADITIONAL MILITARY 200 400 500 500 1,600 EXPANSIONARY 7,400 7,500 8,000 8,300 31,200 WORLDWIDE TRUCK 24,900 28,400 27,100 24,700 105,100 |