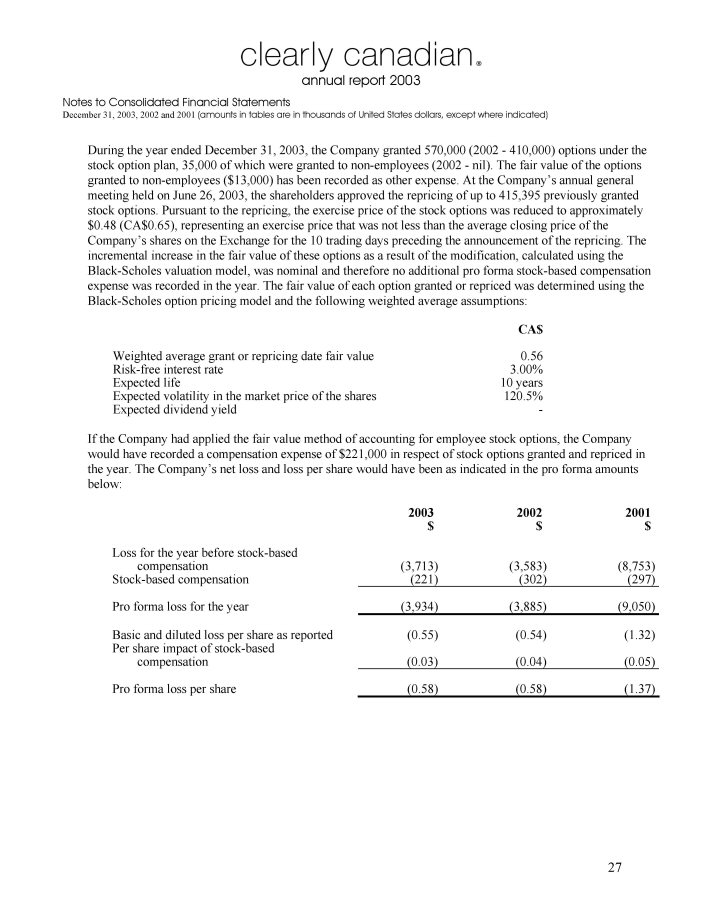

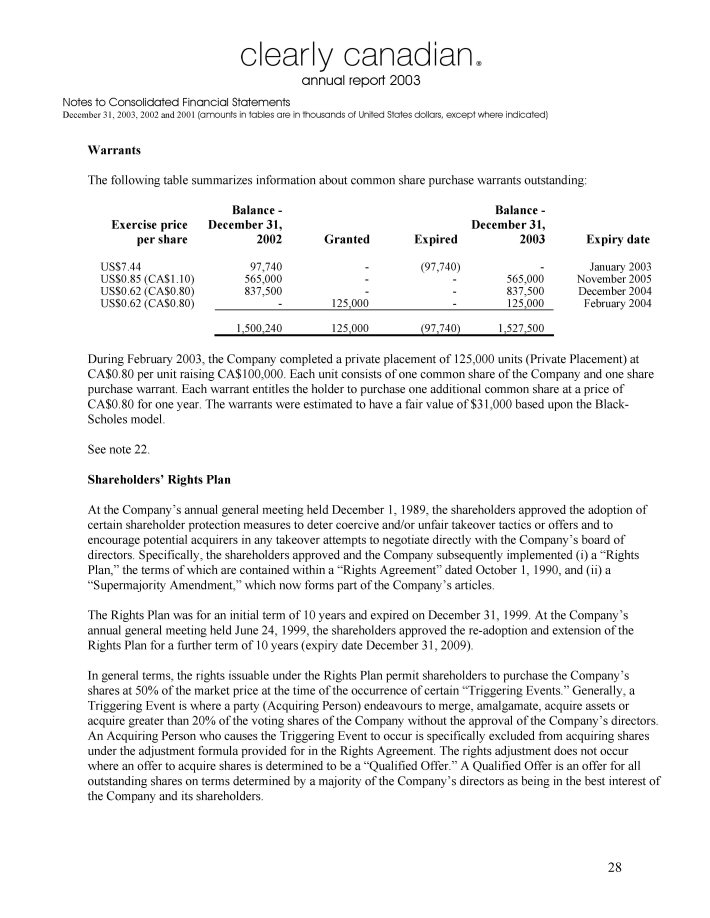

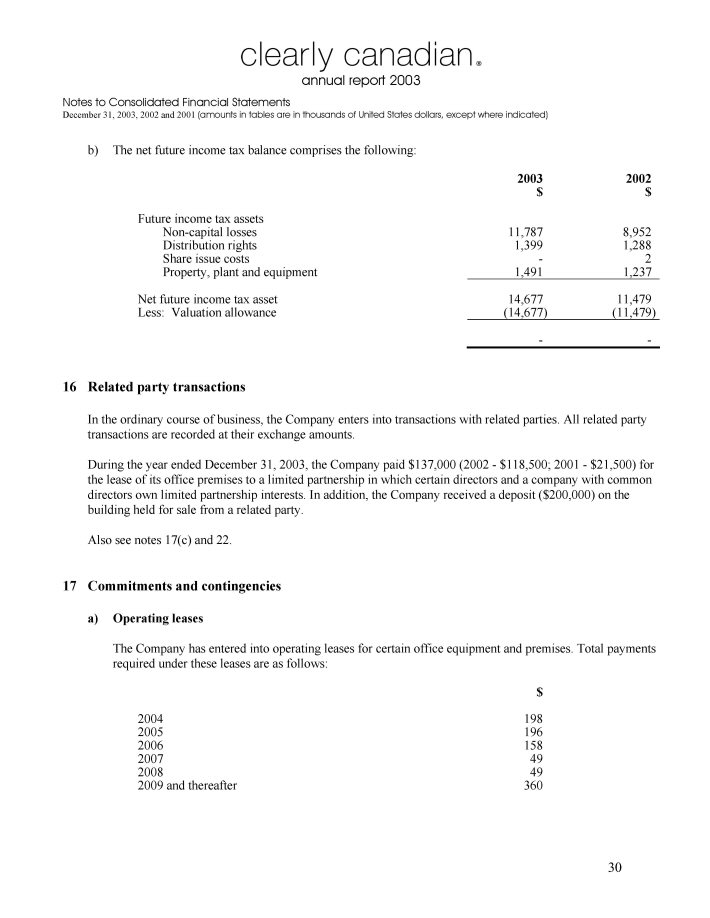

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form 20-F

(Mark One)

| [_] | REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR (g) OF THE SECURITIES EXCHANGE ACT OF 1934 |

OR

| [X] | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| For the fiscal year endedDecember 31, 2003 |

OR

| [_] | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from _______________________ to _______________________

Commission file number 0-15276

CLEARLY CANADIAN

BEVERAGE CORPORATION

(exact name of Registrant as specified in its charter)

Incorporated in the Province of British Columbia, Canada

(Jurisdiction of incorporation or organization)

2489 Bellevue Avenue, West Vancouver, British Columbia, Canada V7V 1E1

(Address of principal executive offices)

Securities registered or to be registered pursuant to Section 12(b) of the Act.

| Title of each class N/A N/A | Name of each exchange on which registered |

Securities registered or to be registered pursuant to Section 12(g) of the Act.

Common Shares With No Par Value

(Title of Class)

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act.

None

(Title of Class)

Indicate the number of outstanding shares of each of the issuer’s classes of capital or common stock as of December 31, 2003

7,168,682 Common Shares with no par value

Indicate by check mark whether the Registrant (1) has filed all reports required to be filed by section 13 or 15(d) of theSecurities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the Registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Yes [X] No

Indicate by check mark which financial statement item the Registrant has elected to follow.

Item 17 Item 18 [X]

TABLE OF CONTENTS

| 1. Identity of Directors, Senior Management and Advisors | 2 | ||

| 2. Offer Statistics and Expected Timetable | 2 | ||

| 3. Key Information | 2 | ||

| Selected Financial Data | 2 | ||

| Currency Translations | 4 | ||

| Risk Factors | 5 | ||

| Estimates Related to Critical Accounting Policies | 9 | ||

| 4. Information on the Company | 10 | ||

| History and Development of the Company | 10 | ||

| Business Overview | 11 | ||

| Sale of Certain Business Assets | 11 | ||

| The New Age Beverage Industry | 12 | ||

| Products | 13 | ||

| Seasonal Nature of the Business | 15 | ||

| Competition | 15 | ||

| Proprietary Protection | 15 | ||

| Operations and Distribution | 16 | ||

| Product and Distribution Initiatives and Objectives | 18 | ||

| Insurance | 19 | ||

| Government Regulation | 19 | ||

| The Company's Properties | 19 | ||

| Employees | 20 | ||

| 5. Operating and Financial Review and Prospects | 20 | ||

| Overall Performance for the Year Ended December 31, 2003 | 20 | ||

| Application of Critical Accounting Policies | 21 | ||

| Results of Operations | 23 | ||

| Liquidity and Capital Resources | 25 | ||

| Trends | 28 | ||

| Legal Proceedings | 28 | ||

| Dividends and Dividend Policy | 29 | ||

| 6. Directors, Senior Management and Employees | 29 | ||

| Directors and Senior Management | 29 | ||

| Executive Compensation | 32 | ||

| Options and Stock Appreciation Rights (SARs) | 33 | ||

| Options and SAR Repricings | 36 | ||

| Employment, Management and Consulting Agreements | 37 | ||

| Composition of the Compensation Committee | 37 | ||

| Report on Executive Compensation | 38 | ||

| Compensation of Directors | 39 | ||

| Committees of the Board of Directors | 39 | ||

| Employees | 39 | ||

| 7. Major Shareholders and Related Party Transactions | 40 | ||

| Major shareholders | 40 | ||

| Related Party Transactions | 40 | ||

| 8. Financial Information | 42 | ||

| 9. The Offer and Listing | 42 | ||

| 10. Additional Information | 44 | ||

| Memorandum and Articles | 44 | ||

| Shareholder Protection Provisions | 45 | ||

| Material Contracts | 46 | ||

| Exchange Controls | 47 | ||

| Taxation | 47 | ||

| Scope of this Disclosure | 49 | ||

| U.S. Federal Income Tax Consequences of the Acquisition, Ownership, and Disposition of Common Shares | 50 | ||

| Documents on display | 54 | ||

| 11. Quantitative and Qualitative Disclosures about Market Risk | 54 | ||

| 12. Description of Securities other than Equity Securities | 54 | ||

| 13. Defaults, Dividend Arrearages and Delinquencies | 54 | ||

| 14. Material Modifications to the Rights of Security Holders and Use of Proceeds | 55 | ||

| 15. Controls and Procedures | 55 | ||

| 16A. Audit Committee Financial Expert | 55 | ||

| 16B. Code of Ethics | 55 | ||

| 16C. Principal Accountant Fees and Services | 56 | ||

| Audit Committee's Pre-Approval Policies and Procedures | 56 | ||

| 16D. Exemptions From the Listing Standards for Audit Committees | 56 | ||

| 16E. Purchases of Equity Securities by the Issuer and Affiliated Purchasers | 57 | ||

| 17. Financial Statements | 57 | ||

| 18. Financial Statements | 57 | ||

| 19. Exhibits | 92 | ||

DISCLOSURE NOTICE

NOTE REGARDING FORWARD-LOOKING STATEMENTS

This report contains forward-looking statements within the meaning of the United States Private Securities Litigation Reform Act of 1995 concerning the Company’s business strategies, market conditions, outlook and other matters. These statements relate to analyses and other information that are based on forecasts of future results, estimates of amounts not yet determinable and assumptions of management including, but not limited to, certain statements and projections concerning the Company’s or management’s plans, intentions, strategies, expectations, predictions, financial projections, assumptions and estimates related to accounting policies, concerning the Company’s future activities and results of operations and other future events or conditions. Any statements that express or involve discussions with respect to predictions, expectations, beliefs, plans, projections, objectives, assumptions or future events or performance (often, but not always, using words or phrases such as “expects” or “does not expect”, “is expected”, “anticipates” or “does not anticipate”, “plans”, “estimates” or “intends”, or stating that certain actions, events or results “may”, “could”, “would”, “might” or “will” be taken, occur or be achieved) are not statements of historical fact and may be “forward-looking statements.” Forward-looking statements contained in this report are based on current facts and analyses and include, but are not limited to, the following:

| • | the Company’s expectations regarding the merits of the Company’s recent divestiture of certain business assets (see “Item 4. Information on the Company – History and Development of the Company”); |

| • | the effect of certain transactions, including marketing arrangements and product distribution system changes, on the Company’s revenues and results of operations in future periods; |

| • | the Company's discussions with potential new customers and the status of these discussions; |

| • | the Company's ability to secure additional financing and improve operating cash flow to allow it to continue as a going concern |

| • | the Company's application of critical accounting policies and the effect of recent accounting pronouncements on the Company's results of operations; |

| • | the Company’s focus on key long-term objectives, including diversifying its new age beverage product lines, maintaining and expanding current market share, and improving its network of distributors; |

| • | the sufficiency and availability of the Company’s supply of raw materials and water, distribution network, contract bottling supplier facilities and property, plant and equipment related to the Company’s operations; and |

| • | other statements related to the Company's business and results of operations. |

Such statements involve known and unknown risks, uncertainties and other factors that may cause the actual results, performance or achievements of the Company or industry results to be materially different from any future results, performance or achievements expressed or implied by such forward-looking statements. Such factors with respect to the Company include, but are not limited to, general economic conditions, the Company’s ability to generate sufficient cash flows to support capital expansion plans and general operating activities; changing beverage consumption trends of consumers; competition; pricing and availability of raw materials; the ability of the Company to maintain the current and future retail listings for its beverages and to maintain favourable supply arrangements and relationships and procure timely and/or adequate production of all or any of the Company’s products; laws and regulations and changes thereto that may affect the way the Company’s products are manufactured, distributed and sold; and political and economic uncertainties including exchange controls, currency fluctuations, taxation and other laws or governmental economic, fiscal, monetary or political policies of Canada, the United States and foreign countries affecting foreign trade, investment and taxation and other factors beyond the reasonable control of the Company, which, in turn, could affect the Company’s current or future operations. See “Key Information – Risk Factors”. Should one or more of these risks and uncertainties materialize, or should underlying assumptions prove incorrect, actual results may vary materially from those described in forward-looking statements. Forward looking statements are made based on management’s beliefs, estimates and opinions on the date the statements are made and the Company undertakes no obligation to update forward-looking statements if these beliefs, estimates and opinions or other circumstances should change. Investors are cautioned against attributing undue certainty to forward-looking statements.

-2-

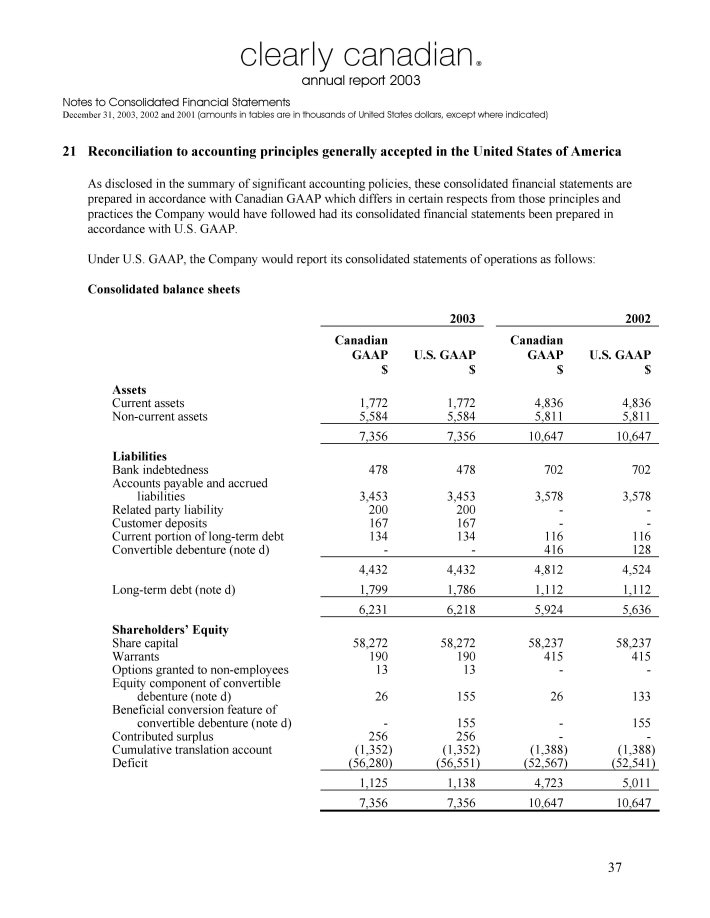

The Company’s consolidated financial statements which form part of the annual report are presented in U.S. dollars and are prepared in accordance with accounting principles generally accepted in Canada (“Canadian GAAP”) which differ in certain respects from accounting principles generally accepted in the United States (“U.S. GAAP”). The differences between Canadian GAAP and U.S. GAAP, as it relates to the Company, are explained in the notes to the Company’s consolidated financial statements.

In view of the consolidated nature of the Company’s operations and corporate structure, the term “Company”, as used herein, is sometimes used to refer to the Company and all of its affiliated companies and subsidiaries collectively, and where the context or specific transactions require, the term Company is sometimes used to refer to certain of the affiliated companies individually.

ITEM 1. IDENTITY OF DIRECTORS, SENIOR MANAGEMENT AND ADVISERS

Not applicable.

ITEM 2. OFFER STATISTICS AND EXPECTED TIMETABLE

Not applicable.

ITEM 3. KEY INFORMATION

Selected Financial Data

Annual Information

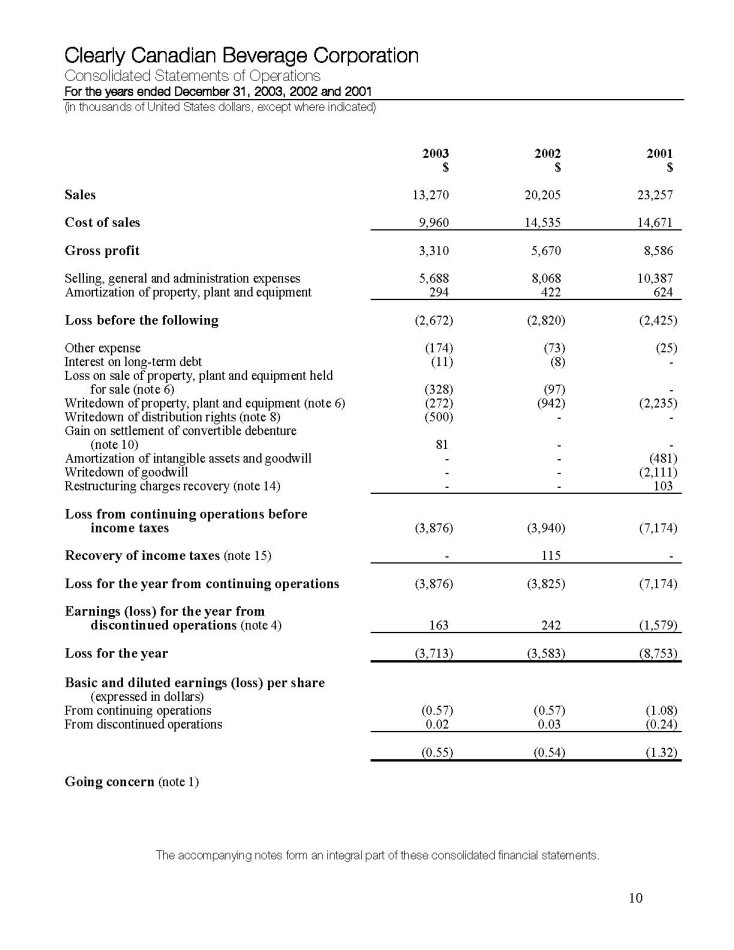

The following summary of financial information of Clearly Canadian Beverage Corporation (the “Company”) for the five years ended December 31, 2003 is qualified in its entirety by reference to and should be read in conjunction with “Item 5. Operating and Financial Review and Prospects” and the consolidated financial statements of the Company and related notes included therein, as well as the risk factors set out in this annual report.The results are presented in U.S. dollars, unless otherwise indicated.

During the year ended December 31, 2001, the Company’s wholly owned U.S. subsidiary, CC Beverage (U.S.) Corporation, (“CC Beverage”) entered into agreements to sell certain of its business assets (see “Item 4. Information on the Company – History and Development of the Company”). The divestiture related to two business segments: its home and office five-gallon water business (which sale completed in April 2001) and its private label co-pack bottling business, Cascade Clear business and related production assets (which sale completed in February 2002). For reporting purposes, as summarized below, the results and financial position of the Company reflect the results of the “continuing operations” only, whereas the results and financial position of the “discontinued operations” are shown separately. Accordingly, prior year figures have been restated to reflect this change. The following financial statement data has been derived from the consolidated financial statements of the Company which have been prepared in accordance with Canadian GAAP.

| Amounts in Accordance with Canadian GAAP (in US dollars, except number of shares data) | |||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| Year Ended | |||||||||||

| December 31 2003 | December 31 2002 | December 31 2001 | December 31 2000 | December 31 1999 | |||||||

| Statement of Operations Data: | |||||||||||

| Total revenues | $ 13,270,000 | $ 20,205,000 | $ 23,257,000 | $ 23,247,000 | $ 31,418,000 | ||||||

| Gross profit | 3,310,000 | 5,670,000 | 8,586,000 | 8,225,000 | 10,033,000 | ||||||

| Loss before the following(4) | (2,672,000 | ) | (2,820,000 | ) | (2,425,000 | ) | (3,479,000 | ) | (3,511,000 | ) | |

-3-

| Amounts in Accordance with Canadian GAAP (in US dollars, except number of shares data) | |||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| Year Ended | |||||||||||

| December 31 2003 | December 31 2002 | December 31 2001 | December 31 2000 | December 31 1999 | |||||||

| Net income (loss) from continuing | |||||||||||

| operations | (3,876,000 | ) | (3,825,000 | ) | (7,174,000 | ) | (4,228,000 | ) | (8,978,000 | ) | |

| Net Income (loss) from discontinued | |||||||||||

| operations(3) | 163,000 | 242,000 | (1,579,000 | ) | (2,221,000 | ) | (967,000 | ) | |||

| Net income (loss) | (3,713,000 | ) | (3,583,000 | ) | (8,753,000 | ) | (6,449,000 | ) | (9,945,000 | ) | |

| Net income (loss) per share (basic) | |||||||||||

| from continued operations | (0.57 | ) | (0.57 | ) | (1.08 | ) | (0.69 | ) | (1.40 | ) | |

| Net income (loss) per share | |||||||||||

| (diluted) from continued operations | (0.57 | ) | (0.57 | ) | (1.08 | ) | (0.69 | ) | (1.40 | ) | |

| Net income (loss) per share | |||||||||||

| (basic)from discontinued operations | 0.02 | 0.03 | (0.24 | ) | (0.37 | ) | (0.15 | ) | |||

| Net income (loss) per share | |||||||||||

| (diluted) from discontinued | |||||||||||

| operations | 0.02 | 0.03 | (0.24 | ) | (0.37 | ) | (0.15 | ) | |||

| Net income (loss) per share (basic) | (0.55 | ) | (0.54 | ) | (1.32 | ) | (1.06 | ) | (1.55 | ) | |

| Net income (loss) per share | |||||||||||

| (diluted) (1)(2) | (0.55 | ) | (0.54 | ) | (1.32 | ) | (1.06 | ) | (1.55 | ) | |

| Amounts in Accordance with Canadian GAAP (in US dollars, except number of shares data) | |||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| Year Ended | |||||||||||

| December 31 2003 | December 31 2002 | December 31 2001 | December 31 2000 | December 31 1999 | |||||||

| Balance Sheet Data: | |||||||||||

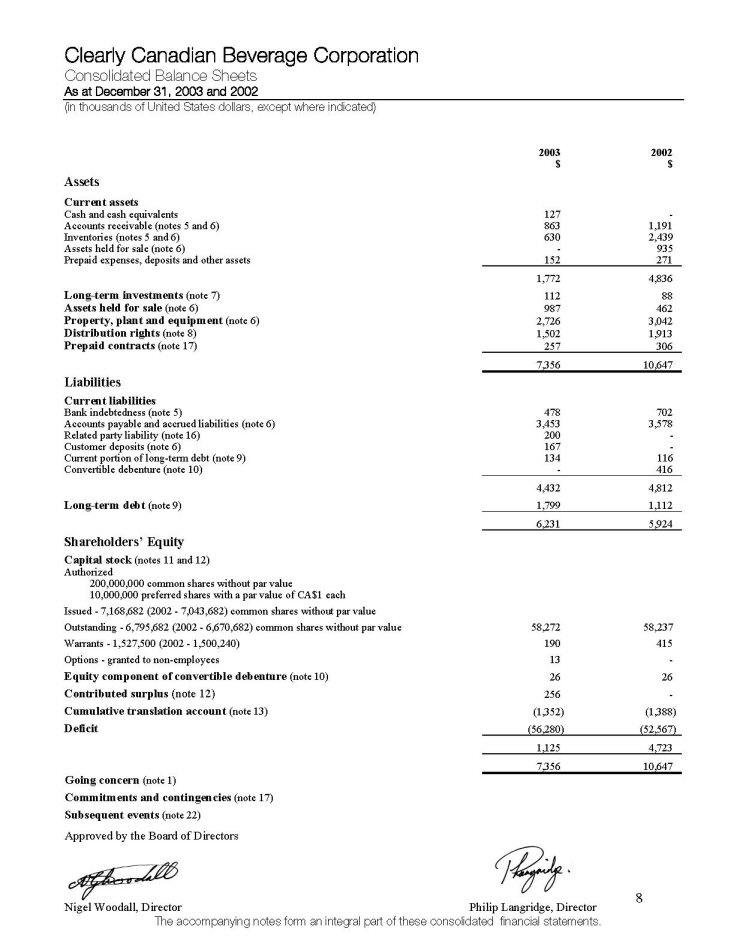

| Total assets | $ 7,356,000 | $10,647,000 | $17,018,000 | $27,943,000 | $33,847,000 | ||||||

| Long term liabilities | 1,799,000 | 1,112,000 | 3,252,000 | 5,466,000 | 4,599,000 | ||||||

| Shareholders' Equity: | |||||||||||

| Shareholders' Equity | 1,125,000 | 4,723,000 | 8,289,000 | 17,080,000 | 23,680,000 | ||||||

| Capital Stock | 58,757,000 | 58,678,000 | 58,631,000 | 58,631,000 | 58,427,000 | ||||||

| Number of shares issued(2) | 7,168,682 | 7,043,682 | 7,013,682 | 7,013,682 | 6,418,682 | ||||||

| Number of shares outstanding(2) | 6,795,682 | 6,670,682 | 6,640,682 | 6,640,682 | 6,173,982 | ||||||

| Cash dividends declared per share | nil | nil | nil | nil | nil | ||||||

| U.S. GAAP Information (in US dollars) | |||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| Year Ended | |||||||||||

| December 31 2003 | December 31 2002 | December 31 2001 | December 31 2000 | December 31 1999 | |||||||

| Statement of Operations Data: | |||||||||||

| Net income (loss) under US GAAP | $(4,046,000 | ) | $(3,578,000 | ) | $(8,753,000 | ) | $(6,440,000 | ) | $(9,906,000 | ) | |

-4-

| U.S. GAAP Information (in US dollars) | |||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| Year Ended | |||||||||||

| December 31 2003 | December 31 2002 | December 31 2001 | December 31 2000 | December 31 1999 | |||||||

| Net income (loss) per share (basic)(2)(3) | (0.60 | ) | (0.54 | ) | (1.31 | ) | (1.06 | ) | (1.55 | ) | |

| Net income (loss) per share | |||||||||||

| (diluted)(2)(3) | (0.60 | ) | (0.54 | ) | (1.31 | ) | (1.06 | ) | (1.55 | ) | |

| Balance Sheet Data: | |||||||||||

| Total assets | 7,356,000 | 10,647,000 | 16,945,000 | 27,653,000 | 32,701,000 | ||||||

| Long term liabilities | 1,786,000 | 1,112,000 | 3,252,000 | 5,466,000 | 4,599,000 | ||||||

| Shareholders' Equity: | |||||||||||

| Net Equity | 1,138,000 | 5,011,000 | 8,216,000 | 16,246,000 | 21,990,000 | ||||||

| Capital Stock | 59,041,000 | 58,940,000 | 58,606,000 | 58,351,000 | 58,138,000 | ||||||

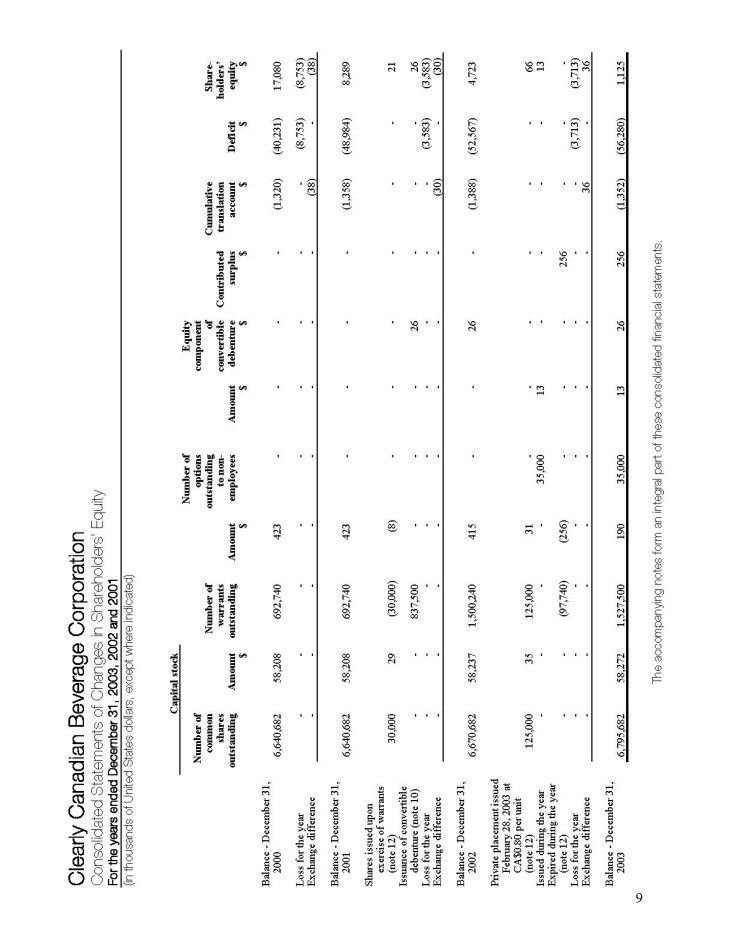

| (1) | Based on weighted average shares outstanding. For accounting purposes, there were 6,795,682 shares of the Company outstanding as of December 31, 2003 (not including 373,000 shares owned by the Company, as previously acquired under normal course issuer bids). |

| (2) | On February 18, 1999, the common shares of the Company were consolidated on the basis of 4.25 old for 1 new common share. Income per share data is presented on a post-consolidation basis as are the numbers of shares outstanding at each year-end. |

| (3) | During the year ended December 31, 2001, the Company disposed of its home and office five gallon water business and also entered into an agreement to dispose of its private label co-pack bottling business and related assets. For reporting purposes, the results and the assets and liabilities of these two business segments have been presented as discontinued operations. Accordingly, prior year figures have been restated to reflect this change. See the consolidated financial statements of the Company for the year ended December 31, 2003 at note 4, "Discontinued Operations". |

| (4) | Loss before other expense, interest on long-term debt, sale of property plant and equipment held for sale, writedown of property, plant and equipment, writedown of distribution rights, gain on settlement of convertible debentures, amortization of intangible assets and goodwill, writedown of goodwill, restructuring charges and recovery. |

Currency Translations

Effective December 31, 1997, the Company adopted the U.S. dollar as its reporting currency. The following table sets out the exchange rates for the conversion of one Canadian dollar (“Cdn$”) into United States dollars (“$”) in effect at the end of the following periods, and the average exchange rates (based on the average of the exchange rates on the last day of each month in such periods) and the range of high and low exchange rates for such periods.

| At Year End December 31 | 2003 | 2002 | 2001 | 2000 | 1999 | ||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| End ($) | 0 | .77 | 0 | .63 | 0 | .62 | 0 | .66 | 0 | .6929 | |

| Average ($) | 0 | .71 | 0 | .63 | 0 | .64 | 0 | .67 | 0 | .6730 | |

| High ($) | 0 | .77 | 0 | .66 | 0 | .66 | 0 | .69 | 0 | .6929 | |

| Low ($) | 0 | .63 | 0 | .61 | 0 | .62 | 0 | .64 | 0 | .6537 | |

The following table sets forth the high and low exchange rates for the conversion of Canadian dollars into United States dollars for each of the last 6 months.

| April 2004 | March 2004 | February 2004 | January 2004 | December 2003 | November 2003 | ||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| High for the month ($) | 0.7275 | 0.7448 | 0.7450 | 0.7519 | 0.7478 | 0.7471 | |||||||

| Low for the month ($) | 0.7651 | 0.7652 | 0.7631 | 0.7867 | 0.7726 | 0.7698 | |||||||

-5-

Exchange rates are based upon the noon buying rate in New York City for cable transfers in foreign currencies as certified for customs purposes by the Federal Reserve Bank of New York. The noon rate of exchange on May 7, 2004 as reported by the Federal Reserve Bank of New York for the conversion of Canadian dollars into United States dollars was $0.7216 ($1.00 = Cdn$1.3858).Unless otherwise indicated, all references herein are toUnited States Dollars.

Risk Factors

The Company’s business is subject to the following risks. These risks could cause actual results to differ materially from results projected in any forward-looking statement in this report.

History of Losses

The Company incurred net losses from continuing operations during the year ended December 31, 2003 of $3,876,000 (including a writedown of property, plant and equipment of $272,000 and a writedown of distribution rights of $500,000) and $3,825,000 (including a writedown of property, plant and equipment of $942,000) during the year ended December 31, 2002. Losses before expenses not related to selling, general and administrative and amortization of tangible assets were $2,672,000during the year ended December 31, 2003 and $2,820,000 during the year ended December 31, 2002. The Company may incur additional losses during the year ending December 31, 2004. The Company believes that to operate at a profit it must significantly increase the sales volume for its products, achieve and maintain efficiencies in operations, maintain fixed costs at or near current levels and avoid significant increases in variable costs relating to production, marketing and distribution. The Company’s ability to significantly increase sales from current levels will depend primarily on success in maintaining and/or increasing market share and availability for its Clearly Canadian® sparkling flavoured water and expanding distribution of its other beverage product lines into new geographic distribution areas, particularly in the United States and Canada. The Company’s ability to successfully enter new distribution areas will, in turn, depend on various factors, many of which are beyond its control, including, but not limited to, the continued demand for its current brands and products in target markets, the ability to price its products at levels competitive with competing products, the ability to establish and maintain relationships with distributors in each geographic area of distribution and the ability in the future to create, develop and successfully introduce new brands and products.

Going Concern

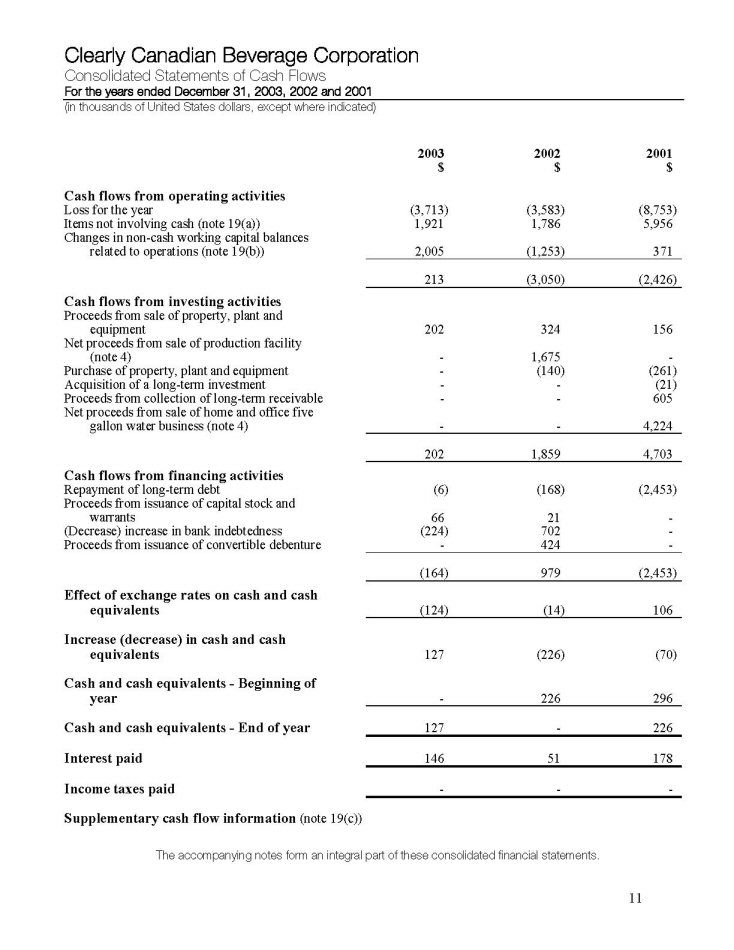

The Company had a working capital deficit of $2,660,000 at December 31, 2003 compared to a working capital surplus of $24,000 at December 31, 2002. The Company’s financial statements were prepared assuming that the Company will continue as a going concern. The Company’s financial statements do not reflect adjustments to carrying value of assets and liabilities, the reported revenues and expenses and balance sheet clarifications used that would be necessary if the going concern assumption were not appropriate. Such adjustments could be material. Due to the Company’s recurring losses from operations, net deficit and lack of working capital for the Company’s planned business activities (see attached consolidated financial statements), there is substantial doubt as to the Company’s ability to continue as a going concern. In April 2001, the Company sold its home and office water business assets for $4.8 million and in February 2002 the Company completed the sale of certain bottling plant and production facility assets for $4.3 million in order to pay down certain debts and improve the Company’s working capital position. Additionally, in October 2003, the Company sold certain surplus water source properties located in British Columbia for Cdn$275,000. The Company will require additional capital during the year ending December 31, 2004 to meet its on-going capital requirements and, in connection therewith, the Company has listed for sale its office building in Burlington, Washington and certain land and water rights in Canada, which properties are not currently required in the Company’s day-to-day operations In view of the Company’s history of losses, it may be difficult for the Company to obtain debt financing. The Company may raise such additional capital through equity or debt financing, dispositions of non-material assets, or through joint ventures or other strategic relationships. There can be no assurance that the Company will successfully raise additional financing or enter into any strategic relationships on acceptable terms, if at all. If the Company is unable to meet its on-going obligations, it may have to consolidate operations, reduce operating expenditures, sell assets, suspend marketing efforts or terminate its operations.

Declining Revenue Trend

The Company has experienced a declining revenue trend since 1998 and earlier. During the year ended December 31, 2003, the Company had sales revenues of $13,270,000, compared to revenues of $20,205,000 in

-6-

2002, $23,257,000 in 2001, $23,247,000 in 2000 and $31,418,000 in 1999. This declining revenue trend occurred while the industry for the new age beverage category, according to Beverage Marketing Corporation of New York, has grown in market size in the United States from $3.8 billion in wholesale dollar sales in 1992 to $13.3 billion in 2002 (on volumes of 4.6 billion gallons). Competition has intensified in the new age beverage category and the Company competes for market share against some companies with substantially greater marketing, personnel, distribution and production resources. In an effort to compete, the Company has spent substantial resources marketing and repositioning its Clearly Canadian® sparkling flavoured water brand and introducing new brands, including Clearly Canadian O+2® and Tré Limone® beverage products. There can be no assurance that the Company will successfully reverse the declining revenue trend or that it will generate sufficient revenues from sales to return to profitability.

Uncertainty of Future Operating Results

The Company’s future operating results are subject to a number of uncertainties, including the ability of the Company to market its beverage products and to develop and introduce new products, the Company’s ability to penetrate new markets, the marketing efforts of distributors and/or retailers of the Company’s products, most of which distribute and/or sell products that are competitive with the products of the Company, the number, quantity and marketing forces behind products introduced by competitors and laws and regulations and/or any changes thereto, especially those that may affect the way in which the Company’s products are marketed and/or produced, as well as laws or regulations that are enforceable by such regulatory authorities as the Food and Drug Administration.

Loss of Market Share

The beverage consumption trends of consumers are subject to constant change. There is no assurance that consumers will continue to purchase the Company’s products in the future. Additionally, many of the Company’s products are marketed as premium products at premium prices. In a recessionary environment it is possible that consumers will not perceive the current pricing of these products as affordable. To maintain market share during recessionary periods, the Company may have to reduce profit margins which would adversely affect the Company’s prospects and results of operations. There can be no assurance that the Company will not encounter difficulties in retaining its current market share due to a variety of factors such as market acceptance, costs of manufacturing and marketing, and competition in the beverage industry, all of which factors are largely beyond the Company’s ability to reasonably predict, much less control.

Increased Competition and Product Lifecycle

The Company’s products compete with a number of established brands and new products that target the same market for the Company’s products. The Company competes against major manufacturers of both traditional and new age beverages (See “Item 4. Information on the Company — Products”), many with substantially greater marketing, cash, distribution, production, technical and other resources than the Company. Although the size of the new age beverage market has grown, the competition and number of brands has also increased. There can be no assurance that future growth of the new age beverage market will result in increased demand for the Company’s products. The Company’s market distribution and penetration may be limited as competition increases. Based on industry information, the product lifecycle for beverage brands and products may be limited to a few years in a geographic distribution area before consumers’ taste preferences change. The development of new products requires a significant investment of capital and there can be no assurance that such new products, when introduced, will be accepted by consumers. The Company’s current products are in varying stages of their lifecycles. The Company expects that these lifecycles will vary from product to product, and there can be no assurance that such products will either become or remain profitable for the Company. A failure or inability to introduce new brands, products or product extensions into the marketplace as existing products mature would likely prevent the Company from achieving long-term profitability.

Seasonal Variations in Demand

Sales of the Company’s beverage products are subject to seasonal variations in demand. For example, consumers in North America typically consume fewer beverage products in the late fall, winter and early spring months. As a result, the Company’s results of operations vary seasonally and such variations may be significant.

-7-

Dependence on Third Party Services

The Company relies, to a significant extent, on the distribution services of independent distributors in order to distribute and sell its beverage products to retailers and consumers. Over recent years, the Company has observed an increased consolidation of distribution services within the new age beverage industry. Traditional soft drink companies, which also own or operate distribution companies that provide distribution services to new age beverage companies, have acquired and/or developed new age beverage products. As a result of these developments, distribution companies that previously operated independently from the traditional soft drink companies are less willing to distribute and sell other companies’ new age beverage products, especially if such products compete with the products that the traditional soft drink companies now have within their portfolio of beverages. In view of these developments, the Company has attempted to align itself with distribution companies that are not restricting their distribution services to beverage products which they own or are otherwise connected with.

Potential Fluctuations in Quarterly Operating Results

The Company’s results of operations have fluctuated in the past and are likely to continue to fluctuate from period to period depending on a number of factors, including the timing and receipt of significant product orders, increased cost in the completion of product orders, increased competition, regulatory and other developments in the Company’s markets, changes in the demand for the Company’s products, the cancellation of product orders, difficulties in collection of receivables, the timing of new product introductions, changes in pricing policies by the Company and its competitors, delays in the introduction of products by the Company, expenses associated with the acquisition of production resources and raw materials from third parties, the mix of sales of the Company’s products, seasonality of customer purchases, personnel changes, political and economic uncertainty, the mix of international and North American revenue, tax policies, foreign currency exchange rates and general economic and political conditions.

The Company believes that economic developments and trends have adversely affected and may continue to affect levels of consumer spending in the markets that the Company serves. The Company believes that these and other factors have adversely affected demand for products offered by the Company. While the Company believes that economic conditions in certain of its markets show signs of improvement, the Company believes that economic conditions and general trends are likely to continue to affect demand for premium priced beverage products such as the Company produces and sells. Such factors may also increase the amount of doubtful accounts or adversely affect the likelihood of collection of such accounts with third parties, such as distributors and retailers, that the Company sells its products to.

Because the Company is unable to forecast with certainty the receipt of orders for its products and the Company’s expense levels are relatively fixed and are based, in part, upon its expectation of future revenue, if revenue levels fall below expectations, operating results are likely to be adversely affected. As a result, net income may be disproportionately affected because a relatively small amount of the Company’s expenses vary with its revenue.

Based on all of the foregoing factors, the Company believes that its quarterly revenue, direct expenses and operating results are likely to vary significantly in the future, that period-to-period comparisons of the results of operations may not necessarily be meaningful and that such comparisons should not be relied upon as an indication of future performance.

Dependence on Management

The Company’s business is dependent upon the continued support of existing senior management. The loss of any key members of the Company’s existing management could adversely affect the Company’s prospects.

Uncertainty Related to Regulatory Proceedings Involving Douglas Mason

On October 30, 2000, the British Columbia Securities Commission (the “Commission”) issued a Notice of Hearing with respect to regulatory proceedings against Douglas Mason, the President, Chief Executive Officer and a director of the Company. The Notice of Hearing alleges that Mr. Mason failed to comply with insider reporting and control person reporting requirements with respect to certain trades in shares of the Company and other companies, and that Mr. Mason engaged or participated in improper trading of shares of certain companies other than the Company. Mr. Mason has denied the allegations contained in the Notice of Hearing and has indicated that he will vigorously defend his position. A Commission hearing with respect to the allegations was initially scheduled for January 14,

-8-

2002, however, was subsequently adjourned pending a judicial determination by the British Columbia Court of Appeal of whether the Commission had failed to disclose relevant documentation. Specifically, Mr. Mason appealed to the British Columbia Court of Appeal the decision by the Commission to dismiss Mr. Mason’s application for disclosure of further documentation in the possession of the Commission. On June 13, 2003, the British Columbia Court of Appeal decided in favour of Mr. Mason and ruled that the Commission’s approach to disclosure did not meet the requirements of procedural fairness, and accordingly, referred the matter back to the Commission with specific instructions on disclosure requirements. In order to address the Commission’s additional

disclosure requirements, the Commission hearing has been adjourned to October 25, 2004. If the Commission determines that some or all of the allegations contained in the Notice of Hearing are true, Mr. Mason could be ordered to resign from the offices he currently holds with the Company and prohibited from acting as a director or officer of the Company. Douglas Mason is one of the founders of the Company’s business and is a core member of the management team that is responsible for the success of the Company’s business to date. Losing the services of Mr. Mason could have a material adverse effect on the Company’s business, prospects and results of operations.

Regulatory Compliance

The production and marketing of the Company’s unique beverages, including contents, labels, caps and containers, are subject to the rules and regulations of various federal, provincial, state and local health agencies. If a regulatory authority finds that a current or future product or production run is not in compliance with any of these regulations, the Company may be fined, or production may be stopped, thus adversely affecting the Company’s financial condition and operations. Similarly, any adverse publicity associated with any non-compliance may damage the Company’s reputation and its ability to successfully market its products. Furthermore, the rules and regulations are subject to change from time to time and while the Company closely monitors developments in this area, it has no way of anticipating whether changes in these rules and regulations will impact its business adversely.

Change in Control Restrictions

The Company has a shareholder’s rights plan and super majority approval requirements, each of which may prevent or delay a change of control of the Company. See “Item 10. Additional Information — Shareholder Protections Provisions”.

Douglas Mason, a member of the board of directors, President and Chief Executive Officer of the Company, beneficially owns or controls, in the aggregate, 241,546 (3.08%) of the outstanding common shares of the Company. In addition to these shareholdings, Mr. Mason has agreed to purchase an additional 660,000 shares of the Company from Quest Capital Corp. on July 6, 2004. See “Item 7. Major Shareholders and Related Party Transactions”. If this purchase is completed, Mr. Mason would beneficially own an aggregate of 901,546 (11.5%) of the issued and outstanding shares of the Company.

In addition to Mr. Mason’s shareholdings, Waterfront Capital Corporation (“Waterfront”) owns 422,100 (5.4%) of the outstanding common shares of the Company. Mr. Mason is a director, officer and shareholder of Waterfront. Through his holdings, Mr. Mason could possibly influence matters requiring shareholder approval, including the election of directors. Such control could have the effect of delaying, deferring or preventing a change of control of the Company.

Share Price Volatility

The Company’s common share price has experienced significant price volatility, with trading prices on the OTC Bulletin Board ranging from US$0.51 (high) to US$0.20 (low) during the year ended December 31, 2003, and from US$0.35 (high) to US$0.26 (low) during the first four months ended April 30, 2004. Announcements of developments related to the Company’s business, fluctuations in operating results, failure to meet investor expectations, general conditions in the beverage industry and the worldwide economy, announcements of innovations, new products or product enhancements by the Company or its competitors, acquisitions and divestitures, changes in governmental regulations, developments in licensing arrangements and changes in relationships with trade partners and suppliers could cause the price of the Company’s common shares to fluctuate substantially. In addition, in recent years the stock market in general, and the market for small capitalization stocks in particular, has experienced extreme price fluctuations which have often been unrelated to the operating performance of affected companies. Such fluctuations could adversely affect the market price of the Company’s common shares.

-9-

Foreign Operations

The Company’s operations are carried out primarily in Canada and in the U.S., with less significant operations in other countries. Such operations and the associated capital investments could be adversely affected by exchange controls, currency fluctuations, taxation laws and other laws or policies of Canada, the United States and other countries affecting foreign trade, investment and taxation, which, in turn, could affect the Company’s current or future foreign operations.

Conflicts of Interest

Certain of the directors, officers, promoters and other members of management of the Company serve as directors, officers, promoters and members of management of other companies and therefore it is possible that a conflict may arise between their duties as a director, officer, promoter or member of management of the Company and their duties as a director, officer, promoter or member of management of such other companies.

The directors and officers of the Company are aware of the existence of laws governing accountability of directors and officers for corporate opportunity and requiring disclosures by directors of conflicts of interest and the Company will rely upon such laws in respect of any directors’ and officers’ conflicts of interest or in respect of any breaches of duty by any of its directors or officers. All such conflicts will be disclosed in accordance with the provisions of applicable corporate legislation and directors or officers will govern themselves in respect thereof to the best of their ability in accordance with the obligations imposed upon them by law.

Potential Dilution

The Company has reserved 1,750,000 common shares for issuance upon exercise of options under an incentive stock option plan. As of April 30, 2004, the Company has granted options exercisable to acquire 1,704,336 common shares under the plan at exercise prices ranging from Cdn$0.65 to Cdn$1.35 per share. In addition, the Company has issued warrants exercisable to acquire up to an aggregate of 1,652,500common shares as follows: warrants exercisable to acquire 565,000 common shares at an exercise price of Cdn$1.10 per share; warrants exercisable to acquire 837,500 common shares at an exercise price of Cdn$0.80 per share; and warrants exercisable to acquire 250,000 common shares at an exercise price of Cdn$0.34. Also, the Company has issued Cdn$670,000 in convertible debentures, which if converted at Cdn$0.80 per share, would result in the issuance of 837,500 common shares. See “Item 6. Directors, Senior Management and Employees — Options and Stock Appreciation Rights (SARs)” and “Item 7. Major Shareholders and Related Party Transactions”.

Holders of such options, warrants and debentures may exercise them when, in all likelihood, the Company could obtain additional capital on terms more favourable than those provided by the options, debentures and warrants. The exercise of options, debentures and/or warrants could result in dilution to the Company’s existing shareholders. Further, while these options, warrants and debentures are outstanding, the Company’s ability to obtain additional financing on favourable terms may be adversely affected.

Estimates Related to Critical Accounting Policies

In the ordinary course of business, the Company has made a number of estimates and assumptions relating to the reporting of results of operations and financial position in the preparation of its financial statements in conformity with accounting principles generally accepted in Canada (“Canadian GAAP”). Actual results could differ significantly from anticipated results should such estimates and/or assumptions prove to be materially incorrect or inaccurate. The Company believes that the information herein (see “Item 5. Operating and Financial Review and Prospects — Application of Critical Accounting Policies”) addresses the Company’s most critical accounting policies, which are those that are most important to the portrayal of the Company’s financial condition and results of operations and require management’s most difficult, subjective and complex judgments, often as a result of the need to make estimates about the effect of matters that are inherently uncertain and beyond the Company’s control.

-10-

ITEM 4. INFORMATION ON THE COMPANY

History and Development of the Company

Name and Incorporation

The Company was incorporated under theCompany Act (British Columbia) by registration of its memorandum and articles under the name of Cambridge Development Corporation on March 18, 1981. The Company subsequently changed its name to Bridgewest Development Corporation on October 28, 1983, to BDC Industries Corp. on November 15, 1984 and to The Jolt Beverage Company, Ltd. on September 3, 1986. On December 14, 1987, The Jolt Beverage Company, Ltd. amalgamated with Interbev Packaging Corp. and Brewmaster Systems Ltd. and on May 13, 1988 changed its name to The International Beverage Corporation. The Company adopted its current name on May 14, 1990. The Company is now governed by theBusiness Corporations Act (British Columbia).

The Company’s corporate head office is presently located at 2489 Bellevue Avenue, West Vancouver, British Columbia, Canada, V7V 1E1 (telephone no: (604) 922-8100) and its registered and records offices are located at 1100 — 888 Dunsmuir Street, Vancouver, British Columbia, V6C 3K4.

Intercorporate Relationships

The Company has four wholly-owned subsidiaries: (i) CC Beverage (U.S.) Corporation, (ii) Clearly Canadian Beverage (International) Corporation, (iii) 546274 Alberta Limited; and (iv) Blue Mountain Springs Ltd.

-------------------------------------------

Clearly Canadian

Beverage Corporation

(British Columbia)

-------------------------------------------

- ------------------------------------------------------------------------------

100% | 100% | 100% | 100% |

- ------------------ ----------------- ----------------- -----------------

CC Beverage Clearly 546274 Alberta Blue Mountain

(U.S.) Canadian Limited Springs Ltd.

Corporation Beverage (Alberta) (Ontario)

(Washington) (International)

Corporation

(Barbados)

- ------------------ ----------------- ----------------- -----------------

CC Beverage (U.S.) Corporation (“CC Beverage”) was formed on December 31, 1998 through the merger of the Company’s two U.S. subsidiaries, namely, Clearly Canadian Beverage (U.S.) Corporation (a Wyoming State corporation established in 1994) and Cascade Clear Water Co. (a Washington State corporation established in 1990). Cascade Clear Water Co. was formed through the merger on January 29, 1998 of Clearly Acquisition Corp. (a wholly-owned Washington State subsidiary of the Company) and Cascade Clear Water Co., an existing Washington State corporation, pursuant to the laws of the State of Washington. As a result of these mergers, CC Beverage handles the Company’s operational business in the United States, which includes the distribution and sale of Clearly Canadian® beverages.

Clearly Canadian Beverage (International) Corporation (“Clearly International”) was incorporated on April 7, 1987 pursuant to the laws of Barbados. In 1988, Clearly International acquired the distribution rights for the Company’s beverage products for all countries other than Canada, the United States and the Caribbean. In 1999, Clearly International assigned certain of its international distribution rights and responsibilities to CC Beverage.

546274 Alberta Limited, which was incorporated on November 12, 1992 pursuant to the laws of Alberta, previously held certain short-term investments for the Company.

Blue Mountain Springs Ltd., which the Company acquired on September 24, 1996, owns certain property interests in Ontario which may be a potential future source of water for the Company and its products.

-11-

Business Overview

The Company, together with its affiliated companies, produces, distributes and markets beverage products including, Clearly Canadian® flavoured sparkling beverages, Clearly Canadian O+2® and Tré Limone®. All of the Company’s products are distributed in the United States and Canada and certain of its products are distributed in Denmark, Norway, Sweden, Finland, Netherlands, the Middle East, the Caribbean, Turkey, Korea, Malaysia, People’s Republic of China, Hong Kong, Taiwan and other countries. The Company’s largest markets for its products are presently the United States (approximately 77.6% of the Company’s total 2003 sales) and Canada (approximately 16.5% of the Company’s total 2003 sales).

Over the last three financial years, the Company has focused on creating new premium beverage brands, developing product extensions and reformulations for existing brands and strengthening its distribution network for its products. In so doing, the Company has attempted to expand the availability of its existing products and to diversify its new age beverage product line offerings.

Since the Company’s acquisition of CC Beverage in January 1998 and up until the end of its most recent financial year, the Company did not effect any significant acquisitions. Rather, during this period, the Company focussed on a variety of brand development and product licensing initiatives. In particular, during 1999 and 2000 the Company redesigned and relaunched its principal beverage product line (Clearly Canadian® sparkling flavoured water) and, as a result, acquired additional numerous new retail listings for this product line. During the last five financial years, the Company also developed and launched two new beverage product lines, namely, Clearly Canadian O+2® in 1998 and Tré Limone® in 2000. The Company also conducted product development work with Reebok International Ltd. (“Reebok”), which resulted in Reebok and the Company entering into a License Agreement in February 2001. Under this License Agreement, the Company manufactured, marketed and distributed certain Reebok branded beverage products until December 31, 2003 when this License Agreement terminated due the inability of the Company to meet the minimum net sales requirements for 2003. As a result, the Company is considering development of its own line of fitness water beverage products and/or formulating such a product line for other potential customers. Since early 2004, the Company has been in discussions with two significant potential new customers. One of these potential customers is interested in a licensed product incorporating their own branding for an enhanced water beverage developed by the Company. Another potential customer is a retailer considering the use of enhanced water beverages developed by the Company in a private label offering across their retail network. Additionally, during the last three financial years, the Company has continually attempted to improve its network of distributors, and a number of key appointments have enhanced the distribution system for the Company’s beverage product lines in certain regions within the U.S. and Canada.

Sale of Certain Business Assets

In August 2000, the Company appointed The Tullius Company of Portland, Oregon, to act as its agent to investigate the potential sale of CC Beverage’s home and office water business. To this end, on April 30, 2001, CC Beverage sold the assets associated with its home and office water business to Cullyspring Water Co., Inc., a Washington corporation affiliated with Sparkling Spring Water Group (“Sparkling Spring”). The purchase price paid by Sparkling Spring was $4.8 million ($4.5 million in cash and with Sparkling Spring assuming approximately $320,000 in liabilities). The proceeds from the sale to Sparkling Springs were used to pay down certain debt obligations and improve the Company’s working capital position. Upon completing the sale of the home and water business to Sparkling Spring, the Company concluded its engagement of The Tullius Company.

On February 22, 2002, CC Beverage concluded the sale of certain production facility assets and a bottling plant lease located in Burlington, Washington, and the sale of its “Cascade Clear” water business and its private label co-pack bottling business to Advanced H2O, Inc. of Bellevue, Washington (“AH2O”). AH2O acquired CC Beverage’s production facility assets and bottling plant lease for a total of $4,348,600, which purchase price included $2,130,000 in cash, the assumption of long-term indebtedness of approximately $2,155,000 and the assumption of certain capital equipment leases of approximately $63,600. In addition to the purchase of the production facility and lease, AH2O purchased CC Beverage’s “Cascade Clear” water business for an aggregate of $2,000,000, which purchase price is payable to CC Beverage based on a percentage of the gross sales earned by AH2O over time, subject to a minimum payment of $100,000 per year commencing December 31, 2002. At December 31, 2005, if CC Beverage has received less than $500,000, then AH2O must make an additional lump sum payment to increase the proceeds to $800,000 if AH2O wishes to keep the “Cascade Clear” brand. At the end of each year, AH2O has the option to not make the minimum payment and, if not paid, CC Beverage can elect to repurchase the Cascade Clear brand for $1.00. Also, CC Beverage sold its private label co-pack (bottling) business to AH2O. For such

-12-

business AH2O will pay CC Beverage a percentage of the gross profits received by AH2O from the private label business over the next five years (up to a maximum payment of $125,000 per year and a minimum payment of $62,500 per year). Additionally, AH2O agreed to provide CC Beverage with “at cost” co-packing (bottling) services for ten years (five year initial term and five year renewal term) for up to 1,500,000 cases per year of carbonated beverages and 250,000 cases per year of non-carbonated beverages. The proceeds from the sales of the various assets to AH2O were used for general working capital purposes, to reduce debt and to provide additional funding for the marketing and distribution of the Company’s beverages. Upon completing the sale of assets to AH2O, the Company concluded its engagement of McDonald Investments, Inc., which was appointed as the Company’s investment banker and financial advisor in November 2000 to evaluate various strategic options, including possible divestiture of certain assets as well as acquisition opportunities.

On October 24, 2003, the Company completed the sale of its water source properties located in British Columbia for a purchase price of Cdn$275,000. In connection with such sale, the Company has retained an eight year license which entitles the Company to draw up to 1,750,000 gallons of water per year at no cost during the first four years of the license and at a price of Cdn$0.01 per gallon in the last four years of the license.

The New Age Beverage Industry

The Company’s products are considered “new age” beverages, a category which became identifiable in the mid-1980‘s. New age beverages are distinguishable from traditional soft drinks in that they generally contain natural ingredients, less sugar, and less, or no, carbonation. New age beverages are traditionally seen as healthful, premium-priced, distinctively packaged and distributed primarily through cold channels represented by convenience stores, delis and specialty stores. The new age beverage category is now generally recognized in the beverage industry to include the following eleven major beverage market segments: “single-serve water”, “premium sodas”, “single-serve fruit beverages”, “sparkling waters”, “sports beverages”, “ready-to-drink coffees”, “ready-to-drink teas”, “energy drinks”, “vegetable/fruit juice blends”, “new age dairy products” and “other nutrient enhanced” beverages.

The new age beverage category, according to Beverage Marketing Corporation of New York (“Beverage Marketing”), has grown in market size in the United States from US$3.8 billion in wholesale dollar sales in 1992 to $13.3 billion in 2002 (on volumes of 4.6 billion gallons). In 2002, for the fifth straight year, the new age beverage market achieved double digit growth in terms of both wholesale dollar sale and volume (i.e. gallons consumed). While 1998 and 1999 saw growth in the 14% to 15% range and volume growth even higher than that, 2000 experienced a slight deceleration (wholesale dollar sales grew by 11% and volume increased by 11%). In 2001 wholesale dollar sales grew by 14.2% and volume consumed increased by 14.7% and in 2002 sales increased by 12% over 2001 and volume consumed increased by 13.2%. (Source: New Age Beverages in the U.S., 2003 Edition (August 2003), Beverage Marketing Corporation of New York).

While Beverage Marketing projects a compound annual growth rate of 8.7% for the New Age beverage market for the period from 2002 to 2007, the projected growth over the next five years is slower than the growth over the previous five years (1997 to 2002), when the market grew by a compound annual rate of 12.9%. According to Beverage Marketing, the slower growth rate is indicative of the market’s maturation, however, the New Age beverage market is expected to reach overall wholesale sales of $20.2 billion in 2007, an increase of $6.7 billion over 2002, which outpaces the $6.2 billion incremental growth for the 1997 to 2002 period. (Source: New Age Beverages in the U.S., 2003 Edition (August 2003), Beverage Marketing Corporation of New York).

In 1998 the premium soda segment of the new age beverage market category accounted for $260 million in wholesale dollar sales. In 1999, sales of premium sodas increased by $10 million, or 3.8%, to $270 million and in 2000 sales increased by $20 million or 7.4%, to $290 million. In 2001, sales of premium sodas reached $305 million, an increase of 5.2% over 2000. In 2002, sales of premium sodas finished at $318.7 million, an increase of 4.5% over 2001. The premium soda segment had a 5.7% compound annual growth rate during the last five years. According to Beverage Marketing, the premium soda segment is expected to grow by 2.5% annually between 2002 and 2007. Notwithstanding the expected 2.5% five-year compound annual growth rate, the premium soda segment is still expected to lose some market share within the overall new age beverage category, going from 2.4% of wholesale dollar sales in 2002 to 1.8% in 2007 (Source: New Age Beverages in the U.S., 2003 Edition (August 2003), Beverage Marketing Corporation of New York).

With respect to the sports beverages segment of the new age beverage category, in 1998 the segment accounted for $1.587 billion wholesale dollar sales and in 1999 sales of sports beverages increased to $1.757 billion. In 2000, the

-13-

sports beverage segment achieved sales of $2.067 billion. In 2001, sales of sports beverages reached $2.182 billion and in 2002 such sales reached $2.41 billion (a 10.1% annual growth rate). According to Beverage Marketing, sports beverages have lost market share over the last five years, however, still retain a solid lock on the third position among new age beverage categories. Beverage Marketing predicts that the sports beverages segment will grow at a 6.8% compound annual growth rate from 2002 to 2007. Based on such expected growth, the sports beverages segment will have a 16.5% market share in 2007, down by 1.5% from 2002 (Source: New Age Beverages in the U.S., 2002 Edition (August 2003), Beverage Marketing Corporation of New York). With respect to information concerning the single-serve water segment of the new age beverage category, in which Clearly Canadian O+2® also competes, see “Cascade ClearTM Bottled Water” below.

In 2002 Beverage Marketing added a new grouping to the new age marketplace. Specifically, the single-serve water segment is now comprised of the retail PET water sub-segment and the new enhanced water sub-segment. Retail PET water is the largest new age beverage category in terms of wholesale dollar sales. In 1998 wholesale dollar sales of retail PET waters were $1.534 billion and reached $2.120 billion in 1999. In 2000, sales of retail PET waters reached $2.674 billion (an increase of 26.2% over 1999 sales). The wholesale dollar sales for retail PET waters in 2001 was $3.449 billion and in 2002 such sales reached $4 billion (a 19.9% annual growth rate). This market segment now has a 30% market share of the total new age beverage market. Similarly, the volume consumed of retail PET waters increased from 809.6 million gallons in 1998 to 1,094.9 million gallons in 1999 and 1,361.5 million gallons in 2000. The volume for 2001 was 1,675 million gallons and the volume for 2002 was 2,042 million gallons, which represents a 20.5% increase over 2001. According to Beverage Marketing, the retail PET water segment grew at a 29.6% average rate between 1997 and 2002 and over the next five years is still expected to grow at a compound annual growth rate of 15.7%. As a result, by 2007, retail PET water is estimated to account for 43% of all new age beverage market sales with estimated wholesale dollar sales of $8.785 billion, up from 30% in 2002 and 16.5% in 1997 (Source: New Age Beverages in the U.S., 2003 Edition (August 2003), Beverage Marketing Corporation of New York).

Products

Principal Beverage Products

Clearly Canadian® Flavoured Sparkling Water

In 1988 the Company introduced its flavoured sparkling water to the beverage marketplace. This product line, which is referred to as the Company’s “core brand”, competes in the “premium soda” segment of the new age beverage market as a premium brand product with distinctive flavours and packaging. A premium soda is a carbonated beverage containing a sugar concentrate base, which often carries a unique and sophisticated imagery and a premium price tag. This segment also includes all natural sodas, which, for the most part, contains all natural ingredients, including no artificial colours, flavours or preservatives. The Company currently offers eight natural fruit flavoured sparkling beverages: Blackberry, Cherry, Strawberry Melon, Grape, Peach, Raspberry Cream, Orange Pineapple and Lemonade. The Company has developed and owns the formulae for its flavourings. The flavours for these products are produced under contract by concentrate suppliers. In the second quarter of 2004, the Company introduced a reformulated version of Clearly Canadian® flavoured sparking beverages which has approximately one-half of the calories (approximately 45 calories per 8 fl. oz. serving), approximately one-half the carbohydrates (approximately 10 grams per 8 fl. oz. serving) with no preservatives and without compromising the products’ premium taste profile. Based on the Company’s discussions with certain of its major distributors and retailers and from its own analysis, the Company anticipates that the new formula for Clearly Canadian® flavoured sparkling beverages will be well received by the consuming public and especially from those more health conscious consumers that have a greater awareness of the health related issues associated with increased levels of sugar intake and obesity. This product line is available in 414 ml (14 fl. oz.) glass bottles with shrink-sleeve labels that are in vivid colours in abstract patterns and cover the entire bottle.

In 2003 and 2002, the Company’s core brand products sales represented approximately 77% and 66%, respectively, of total product sales revenues. As a result of the projected growth rates in other segments of the new age beverage market, the Company has diversified, and intends to continue to diversify, its beverage product lines.

Clearly Canadian O+2®

In 1998 the Company developed a new oxygen enhanced beverage called "Clearly Canadian O+2(R)" which was launched and marketed in U.S. and Canadian markets through 1999 and 2000. In its unflavoured form, Clearly

-14-

Canadian O+2® is produced with up to ten times the normal concentration of oxygen naturally found in water. Additionally, Clearly Canadian O+2® also comes in two flavours (Fruit-Citrus and Berry-Citrus) which are produced with up to five times the normal concentration of oxygen. Clearly Canadian O+2® features an innovative, sleek, blue bottle, which is designed to prolong the retention of oxygen levels. This product line has been designed to compete in the “single-serve water” and “sports beverages” segments and the new enhanced water sub-segment of the new age beverage category.

Cascade ClearTMBottled Water

In February 2002, the Company’s subsidiary, CC Beverage, concluded the sale of certain production facility assets to Advanced H2O, Inc. (“AH2O”) of Bellevue, Washington. (See “Business of the Company”). As part of the sale to AH2O, CC Beverage sold its “Cascade Clear” bottled water business for an aggregate of $2 million, which purchase price is being paid to CC beverage as a royalty based on a percentage of the gross sales earned by AH2O over time, subject to a minimum payment of $100,000 per year. As such, CC Beverage has a continuing interest in Cascade Clear unflavoured bottled water, which is sold by AH2O in a variety of single-serve bottled water sizes. Cascade Clear bottled water competes in the retail PET water sub-segment of the single-serve water segment of the new age beverage category, being non-sparkling water in 1.5 litres or less “PET bottles” (PET is short for polyethylene terephthalate and is often interchangeably used with the term plastic).

Other Beverage Products

Tré Limone®

In 1999 the Company developed a new product line for the North American market. The product, Tré Limone®, is a dry, sparkling lemon-ginger drink and was launched on a roll-out basis in 2000. This product line has also subsequently been distributed in certain international markets.

Tré Limone® competes in the premium soda segment of the new age beverage category (See “Clearly Canadian® Flavoured Sparkling Water” above for information concerning the “premium soda” segment). The Tré Limone® product line is packaged in a 414 ml (14 fl oz.) glass bottle with a distinctive shrink-sleeve label.

Reebok Fitness Water Beverages

The Company conducted product development work with Reebok International Ltd. (“Reebok”), which resulted in Reebok and the Company entering into a license agreement in February 2001. Under this license agreement, the Company manufactured, marketed and distributed certain Reebok branded beverage products, until December 31, 2003 when this license agreement terminated due the inability of the Company to meet certain minimum net sales requirements for 2003. In 2003 and 2002, the sales of Reebok represented approximately 10.4% and 23.1%, respectively, of total product sales revenues. The Company no longer markets or distributes Reebok branded beverage products.

Co-Packing

The Company currently bottles a private label bottled water, utilizing the Company’s licensed oxygenation technology, for a private label customer.

Other Products

The Company also plans to continue in negotiations with various parties in relation to the development of additional co-packing opportunities in private label businesses and licensing opportunities in enhanced beverage manufacturing that utilize technologies and expertise developed by the Company.

Since early 2004, the Company has engaged in discussions with two significant potential new customers. One of these potential customers is interested in the development of a licensed enhanced water beverage that would incorporate their own branding. Another potential customer is a retailer considering the use of enhanced water beverages developed by the Company in a private label offering across their retail network.

-15-

Other Sales

The Company from time to time will sell bulk water from its wellsites (and other materials or ingredients which have been deemed surplus to its core businesses).

Seasonal Nature of the Business

Sales of the Company’s beverage products are subject to seasonal variations in demand. For example, consumers in North America typically consume fewer beverage products in the late fall, winter and early spring months. As a result, the Company’s results of operations vary seasonally and such variations may be significant. See “Risk Factors”.

Competition

The Company’s products compete broadly with all beverages available to consumers. The beverage market is highly competitive, and includes international, national, regional and local producers and distributors, many of whom have greater resources than the Company. The Company believes that its direct competitors in the new age beverage market include: Cadbury Schweppes, which purchased Snapple Beverage Group from Triarc Beverage Companies Inc. in September 2000, producers of “Snapple”, “Mistic” and “Stewart’s Soda”; Coca-Cola Company, producers of “Fruitopia”, “Nestea”, “Powerade” and “Dasani”; PepsiCo, producers of “Lipton Teas”, “Acquafina”, “SoBe” (ie. acquired by PepsiCo through an acquisition of a 90% interest in South Beach Beverages in January 2001), and “Gatorade” (acquired by PepsiCo through merger with Quaker Oats which was approved in August 2001); Nestlé Waters North America, Inc., producers of “Perrier”, “Poland Springs”, “Arrowhead”, “Aberfoyle Springs” and other water beverages; Danone Waters of North America, Inc., producers of “Evian” and “Dannon”; Hansen Natural Corp., producers of various natural sodas, smoothies, functional drinks, juices and iced teas; and Ferolito, Vultaggio & Sons, producers of “Arizona Iced Teas”. While the Company believes that it competes favourably on factors such as quality, merchandising, range of flavours, brand name recognition and loyalty, the Company and its product lines will continue to experience increasing competitive pressures from both traditional and new age beverage companies, many of whom have substantially greater marketing, cash, distribution, technical and other resources than the Company.

Proprietary Protection

Trademarks

The Company has numerous trademark registrations in the United States, Canada and in other countries worldwide in connection with its Clearly Canadian®, Clearly Canadian O+2®, Tré Limone®, and other beverage product lines. The Company’s trademark registrations are valid for varying periods of time, but are renewable before expiry.

Copyright

The Company retains copyright to any work created by its employees during the course of their employment and, where necessary, acquires copyright by assignment from independent contractors who prepare artistic work for the Company’s products and promotional materials.

Reliance on Intellectual Property Rights

The Company regards its trademarks, copyrights, trade secrets and similar intellectual property as critical to its success and attempts to protect such property with registered and common law trademarks and copyrights, restrictions on disclosure and other actions to forestall infringement. The Company relies on a combination of trademark and trade secrecy laws, confidentiality procedures and contractual provisions to protect its intellectual property rights. The Company has in the past, and it expects that it may in the future, license elements of its distinctive trademarks, trade dress and similar proprietary rights to third parties. While the Company attempts to ensure that the quality of its brand is maintained by such licensees, no assurances can be given that such licensees will not take actions that might materially and adversely affect the value of the Company’s proprietary rights or the reputation of its products, either of which could have a material adverse effect on the Company’s business. Product package and merchandising design and artwork are important to the success of the Company and it intends to take action to protect against imitation of its products and packages and to protect its trademarks, patents and copyrights

-16-

as necessary. However, there can be no assurance that other third parties will not infringe or misappropriate the Company’s trademarks, trade dress and similar proprietary rights. In addition, despite the Company’s precautions, some or all of the trade secrets and other know-how that the Company considers proprietary could be independently developed, could otherwise become known by others or could be deemed to be in the public domain.

Operations and Distribution

Well Sites

The Company’s first well site, which is leased, is situated on five acres of land located in Thornton, Ontario (the “Thornton Well Site”). In Ontario, the Company must obtain a commercial licence to draw quantities of water from its property. The Company is presently licensed to draw approximately 104 million gallons of water per year from its two wells on the Thornton Well Site, and is presently drawing water from this site.

The Company’s second well site is located near the Village of Formosa, Ontario (the “Formosa Well Site”) and consists of approximately seven acres with an artesian well which is approximately 950 feet deep. The Company owns the Formosa Well Site and the water-taking permit allowing up to approximately 238,000 gallons per day to be drawn from the property, and is presently drawing water from this site.

Also, the Company previously owned a well site property which is located near Vernon, British Columbia, consisting of approximately 16.9 acres of land on which five wells are drilled (the “B.C. Well Site”). On October 24, 2003, the Company completed the sale of the BC Well Site for a purchase price of Cdn$275,000. In connection with such sale, the Company has retained an eight year license which entitles the Company to draw up to 1,750,000 gallons of water per year at no cost during the first four years of the license and at a price of Cdn$0.01 per gallon in the last four years of the license. Water from this site has previously been used for the Company’s flavoured beverage products, however the Company is not presently drawing water from this site.

The water used in the Company’s “core brand” product line, Clearly Canadian® sparkling flavoured sparkling beverages and its Tré Limone® product line, presently comes from water sources located in Canada, which are on properties owned or leased by the Company, or subject to a water supply contract with a third party. This water is transported from the well sites to bottling facilities in dedicated stainless steel tankers (ie. dedicated for water uses only) and placed in dedicated stainless steel storage tanks. The transport trucks then return with empty sealed tankers to ensure no contamination. The water used in the Company’s Clearly Canadian O+2® product line is supplied by Advanced H2O, Inc. from a water supply source located in the Cascade Mountain area near the town of Concrete, Washington.

On an on-going basis, the Company reviews the sources of the water used in its products and may make changes to the sourcing of its water in the future.

In March 1993, the Company purchased approximately 300 acres of land in Piney, Manitoba. This site may be developed as a future water source. Also, in September 1996, the Company acquired Blue Mountain Springs Ltd., which company has certain property interests in Ontario which may be a potential future spring water source for the Company and its products.

Based upon the present flow capacities of the Company’s own well sites and contracted water sources, the Company believes that it has an adequate supply of water to meet their present and anticipated future water requirements.

Bottling

The Company’s and CC Beverage’s bottles are currently supplied from one glass bottle manufacturer and two plastic (PET) bottle manufacturers. Based on the Company’s knowledge of the capacities of its suppliers, the Company expects to have a sufficient supply of bottles to enable it to meet its anticipated future requirements.

Frequent and regular testing of product and packaging quality parameters is conducted at the bottling plants by trained personnel. Additionally, a sampling submission program tests samples from each and every production run and such samples are sent to the Company’s quality control facilities. In addition to this testing program, the Company reviews daily production and quality control records from each bottling facility which are forwarded to the Company every production day. All analytical data is summarized and trend results are utilized in conjunction

-17-

with regular plant inspections to monitor the success of the overall quality assurance program. The Company’s quality assurance personnel continuously review standards with both suppliers and production operations. The Company also utilizes independent testing labs on a regular basis.

The Company uses contract bottling facilities (being independent bottling companies under contract with the Company or its subsidiaries). Currently the Company utilizes the following contract bottling facilities for producing products:

Advanced H2O, Inc. of Bellevue, Washington produces product (Clearly Canadian® flavoured sparkling beverages and Clearly Canadian® oxygenated beverages) primarily for distribution to western Canada and to western U.S. Advanced H2O, Inc. also produces for the Company other branded oxygenated water that the Company sells to certain co-pack customers. The Company is currently in discussions with Advanced H2O, Inc that may result in the sub-contracting the bottling of Clearly Canadian® flavoured sparkling beverages to an alternative bottling facility also located in Washington State.

Delta Beverages of Woodbridge, Ontario produces product (Clearly Canadian® flavoured beverages) primarily for distribution in Canada and the U.S.

Ameripec, Inc. of Buena Park, California has produced Reebok beverage products in the past and may be utilized for other new product initiatives in the future.

Quality Control