The information in this combined proxy statement and prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This combined proxy statement and prospectus is not an offer to sell these securities and is not soliciting an offer to buy these securities in any state where the offer or sale is not permitted.

COMBINED PROXY STATEMENT AND PROSPECTUS

For the Reorganization of

Sound Point Floating Rate Income Fund

a series of Trust for Advised Portfolios

615 East Michigan Street

Milwaukee, Wisconsin 53202

626-914-7220

Into

American Beacon Sound Point Floating Rate Income Fund

a series of American Beacon Funds

220 East Las Colinas Boulevard, Suite 1200

Irving, Texas 75039

(800) 658-5811

TRUST FOR ADVISED PORTFOLIOS

Sound Point Floating Rate Income Fund

615 East Michigan Street

Milwaukee, Wisconsin 53202

[ ], 2015

To the Shareholders:

We are pleased to announce that the Sound Point Floating Rate Income Fund (the “Sound Point Fund”), a series of Trust for Advised Portfolios (the “Trust”), is proposing to reorganize into the American Beacon Sound Point Floating Rate Income Fund (the “AB Fund”), a newly created series of American Beacon Funds (the “AB Trust”). The AB Fund is designed to be substantially identical from an investment perspective to the Sound Point Fund.

A Special Meeting of Shareholders of the Sound Point Fund is to be held at [ ] p.m. Central Time on December 7, 2015, at 615 East Michigan Street, Milwaukee, Wisconsin 53202, where you will be asked to vote on the proposal to reorganize the Sound Point Fund into the AB Fund. A Combined Proxy Statement and Prospectus (the “Proxy Statement”) regarding the meeting, a proxy card for your vote at the meeting and a postage-prepaid envelope in which to return your proxy card are enclosed. You may also submit your vote via telephone or the internet.

The primary purpose of the reorganization transaction (the “Reorganization”) is to move the Sound Point Fund to the American Beacon Family of Funds. The Reorganization will shift management oversight responsibility for the Sound Point Fund to American Beacon Advisors, Inc. (the “Manager”) while retaining Sound Point Capital Management, L.P., the investment adviser of the Sound Point Fund, as the sub-advisor to the AB Fund (“Sound Point Capital” or the “Sub-Advisor”). In this capacity, Sound Point Capital will continue to make day-to-day investment decisions for the AB Fund. The Manager is an experienced provider of investment advisory services to institutional and retail investors, with approximately $[ ] billion in mutual fund and $[ ] billion in overall assets under management as of September 30, 2015. Since 1986, the Manager has offered a variety of services and products, including corporate cash management, separate account management, and mutual funds. The Reorganization has the potential to expand the Sound Point Fund’s presence in more distribution channels, increase its asset base and lower operating expenses as a percentage of assets.

By engaging Sound Point Capital as the Sub-Advisor to the AB Fund, the AB Fund will be advised by the same portfolio management team at Sound Point Capital that currently advises the Sound Point Fund. In particular, the portfolio managers of the Sub-Advisor who are primarily responsible for the day-to-day portfolio management of the Sound Point Fund will remain the same.

If Sound Point Fund shareholders approve the Reorganization, it is expected to take effect on or about December 11, 2015. At that time, the Sound Point Fund Investor Class shares or Institutional Class shares you currently own would, in effect, be exchanged on a tax-free basis for SP Class shares or Institutional Class shares, respectively, of the AB Fund equal in number and value, as follows:

| Sound Point Floating Rate Income Fund | à | American Beacon Sound Point Floating Rate Income Fund |

| Investor Class shares | à | SP Class shares |

| Institutional Class shares | à | Institutional Class shares |

No sales loads, commissions or other transactional fees will be imposed on shareholders in connection with the tax-free exchange of their shares.

The AB Fund’s advisory fees will be lower than the advisory fee currently paid by the Sound Point Fund. The Sound Point Fund assesses no front-end sales charge, contingent deferred sales charge, redemption fees or exchange fees on its Investor Class or Institutional Class shares, and no such fees will be assessed by the AB Fund on its SP Class or Institutional Class shares. The AB Fund's SP Class will have a Rule 12b-1 distribution and service fee of 0.25% while the Sound Point Fund's Investor Class does not. Neither the AB Fund's Institutional Class nor the Sound Poibnt Fund's Institutional Class has a Rule 12b-1 fee.

The net annual operating expense ratio of the AB Fund’s SP Class shares is not expected to be materially different than that of the Sound Point Fund’s Investor Class shares for the first two years after the Reorganization. Although the gross annual operating expense ratio of the AB Fund’s SP Class shares is expected to be higher than that of the Sound Point Fund’s Investor Class shares, shareholders will not be affected by the increase for the first two years after the Reorganization and for so long thereafter as the Manager agrees to maintain the net annual operating expense ratio of the AB Fund’s SP Class shares at the current expense cap level.

The net annual operating expense ratio of the AB Fund’s Institutional Class shares is expected to be lower than that of the Sound Point Fund’s Institutional Class shares for the first two years after the Reorganization. The gross annual operating expense ratio of the AB Fund’s Institutional Class also is expected to be lower than that of the Sound Point’s Institutional Class shares.

The Board of Trustees of the Trust unanimously recommends that the shareholders of the Sound Point Fund vote in favor of the proposed Reorganization.

Detailed information about the proposal is contained in the enclosed materials. Whether or not you plan to attend the meeting in person, we need your vote. Once you have decided how you will vote, please promptly complete, sign, date and return the enclosed proxy card in the postage-prepaid envelope or you may submit your vote via telephone or the internet. If you have any questions regarding the proposal to be voted on, please do not hesitate to call our proxy solicitor, [ ] toll free at [ ].

Your vote is very important to us. Thank you for your response and for your continued investment in the Sound Point Floating Rate Income Fund.

Respectfully,

Stephen Ketchum

Managing Partner

Sound Point Capital Management, L.P.

TRUST FOR ADVISED PORTFOLIOS

Sound Point Floating Rate Income Fund

615 East Michigan Street

Milwaukee, Wisconsin 53202

NOTICE OF SPECIAL MEETING OF SHAREHOLDERS

TO BE HELD DECEMBER 7, 2015.

To the Shareholders of the Sound Point Floating Rate Income Fund:

NOTICE IS HEREBY GIVEN that a Special Meeting of Shareholders (the “Special Meeting”) of the Sound Point Floating Rate Income Fund (the “Sound Point Fund”), a series of Trust for Advised Portfolios, is to be held at [ ] p.m. Central Time on December 7, 2015, at 615 East Michigan Street, Milwaukee, Wisconsin 53202.

The Special Meeting is being held to consider an Agreement and Plan of Reorganization and Termination (the “Plan”) providing for the transfer of all of the assets of the Sound Point Fund to the American Beacon Sound Point Floating Rate Income Fund (the “AB Fund”), a newly created series of American Beacon Funds. The transfer effectively would be (a) an exchange of your Investor Class shares of the Sound Point Fund for SP Class shares of the AB Fund and an exchange of your Institutional Class shares of the Sound Point Fund for Institutional Class shares of the AB Fund, which would be distributed pro rata by the Sound Point Fund to the holders of its shares in complete liquidation of the Sound Point Fund, and (b) the AB Fund’s assumption of all of the liabilities of the Sound Point Fund, as follows:

| Sound Point Floating Rate Income Fund | à | American Beacon Sound Point Floating Rate Income Fund |

| Investor Class shares | à | SP Class shares |

| Institutional Class shares | à | Institutional Class shares |

Those present and the appointed proxies also will transact such other business, if any, as may properly come before the Special Meeting or any adjournments or postponements thereof.

Holders of record of the shares of beneficial interest in the Sound Point Fund as of the close of business on October 23, 2015, are entitled to vote at the Special Meeting or any adjournments or postponements thereof.

If the necessary quorum to transact business or the vote required to approve any proposal is not obtained at the Special Meeting or if a quorum is obtained but sufficient votes required to approve the Plan are not obtained, the persons named as proxies on the enclosed proxy card may propose one or more adjournments of the Special Meeting to permit, in accordance with applicable law, further solicitation of proxies with respect to the proposal. Any such adjournment would require the affirmative vote of a majority of the shares voted in person or by proxy. The persons designated as proxies may use their discretionary authority to vote on questions of adjournment and on any other proposals raised at the Special Meeting to the extent permitted by the proxy rules of the Securities and Exchange Commission (the “SEC”), including proposals for which timely notice was not received, as set forth in the SEC’s proxy rules.

Important Notice Regarding the Availability of Proxy Materials for the Special Meeting of Shareholders to be Held on Monday, December 7, 2015, or any adjournment or postponement thereof. This Notice and the attached Combined Proxy Statement and Prospectus are available on the internet at [ ]. On this webpage, you will be able to access the Notice, the Combined Proxy

Statement and Prospectus, any accompanying materials and any amendments or supplements to the foregoing material that are required to be furnished to shareholders. We encourage you to access and review all of the important information contained in the proxy materials before voting.

By order of the Board of Trustees,

Eric W. Pinciss, Secretary

[ ], 2015

YOUR VOTE IS IMPORTANT

NO MATTER HOW MANY SHARES YOU OWN

We urge you to vote your shares. Your prompt vote may save the Sound Point Fund the necessity of further solicitations to ensure a quorum at the Special Meeting. Shareholders may cast their vote by telephone, by mail, by the internet and by automated touchtone as set forth below:

| Phone: | To cast your vote by phone with a proxy voting representative, call the toll-free number found on the enclosed proxy card. You will be required to provide your control number found on the reverse side of your proxy card. |

| | |

| | |

| Mail: | To vote your proxy by mail, check the appropriate voting box on the reverse side of your proxy card, sign and date the card and return it in the enclosed postage-prepaid envelope. If you sign, date and return the proxy card but give no voting instructions, the proxies will vote FOR the proposal. |

| | |

| | |

| The options below are available 24 hours a day/7 days a week. |

| | |

| | |

| Internet: | The web address and instructions for voting online can be found on the enclosed proxy card. You will be required to provide your control number found on the reverse side of your proxy card. |

| | |

| | |

| Automated Touchtone: | The toll-free number for automated touchtone telephone voting can be found on the enclosed proxy card. You must have the control number found on the reverse side of your proxy card. |

If you have any questions regarding the proposal, the proxy card or need assistance voting your shares, please contact [ ], the Sound Point Fund’s proxy solicitor, toll-free at [ ]. If the Sound Point Fund does not receive your voting instructions after our original mailing, you may be contacted by us or by [ ], in either case, to remind you to vote.

If you can attend the Special Meeting and wish to vote your shares in person at that time, you will be able to do so. If you hold your shares in “street name” through a broker, bank or other nominee, you should contact your nominee about voting in person at the Special Meeting.

TRUST FOR ADVISED PORTFOLIOS

Sound Point Floating Rate Income Fund

615 East Michigan Street

Milwaukee, Wisconsin 53202

QUESTIONS AND ANSWERS

YOUR VOTE IS VERY IMPORTANT!

Dated: [ ], 2015

Question: What is this document and why did you send it to me?

Answer: The attached Combined Proxy Statement and Prospectus is a proxy statement for the Sound Point Floating Rate Income Fund (the “Sound Point Fund”), a series of Trust for Advised Portfolios (the “Trust”), and a prospectus for the SP Class shares and Institutional Class shares of a newly created series of American Beacon Funds (the “AB Trust”), the American Beacon Sound Point Floating Rate Income Fund (the “AB Fund”) (collectively, the “Proxy Statement”). The purposes of the Proxy Statement are to (1) solicit votes from shareholders of the Sound Point Fund to approve the proposed reorganization of the Sound Point Fund into the AB Fund (the “Reorganization”), as described in the Agreement and Plan of Reorganization and Termination between the Trust and the AB Trust (the “Plan”), the form of which is attached to the Proxy Statement as Appendix A, and (2) provide information regarding the SP Class shares and Institutional Class shares of the AB Fund.

The Proxy Statement contains information that shareholders of the Sound Point Fund should know before voting on the Reorganization. The Proxy Statement should be retained for future reference.

Question: What is the purpose of the Reorganization?

Answer: The primary purpose of the Reorganization is to move the Sound Point Fund to the American Beacon Family of Funds. Reconstituting the Sound Point Fund as a series of the AB Trust has the potential to (1) expand the Sound Point Fund’s presence in more distribution channels, (2) increase its asset base, and (3) lower operating expenses as a percentage of assets. Sound Point Capital Management, L.P. (“Sound Point Capital”), the current adviser to the Sound Point Fund, recommends that the Sound Point Fund be reorganized as a series of the AB Trust.

Question: How will the Reorganization work?

Answer: In order to reconstitute the Sound Point Fund as a series of the AB Trust, a fund using substantially identical principal investment strategies and portfolio management techniques, referred to as the “AB Fund,” has been created as a new series of the AB Trust. If shareholders of the Sound Point Fund approve the Plan, the Sound Point Fund will transfer all of its assets to the AB Fund in return for shares of the AB Fund and the AB Fund’s assumption of the Sound Point Fund’s liabilities. The Sound Point Fund will then distribute the shares it receives from the AB Fund to shareholders. Existing shareholders of the Sound Point Fund’s Investor Class shares and Institutional Class shares will become shareholders of the AB Fund’s SP Class shares and Institutional Class shares, respectively, and

immediately after the Reorganization each shareholder will hold SP Class shares or Institutional Class shares, as the case may be, of the AB Fund, equal in number and value to the Sound Point Fund’s Investor Class shares or Institutional Class shares, as the case may be, that the shareholder held immediately prior to the Reorganization. Subsequently, the Sound Point Fund will be liquidated.

Please refer to the Proxy Statement for a detailed explanation of the proposal. If the Plan is approved by shareholders of the Sound Point Fund at the Special Meeting of Shareholders (the “Special Meeting”), the Reorganization is expected to be effective on or about December 11, 2015.

Question: How will the Reorganization affect me as a shareholder?

Answer: You will become a shareholder of the AB Fund. If you hold Investor Class shares of the Sound Point Fund, you will receive SP Class shares of the AB Fund. If you hold Institutional Class shares of the Sound Point Fund, you will receive Institutional Class shares of the AB Fund. The shares of the AB Fund that you receive will have a total net asset value equal to the total net asset value of the shares you hold in the Sound Point Fund as of the closing date of the Reorganization. The Reorganization will not affect the value of your investment at the time of the Reorganization. The Reorganization is expected to be tax-free to the Sound Point Fund and its shareholders.

The Reorganization will shift management oversight responsibility for the Sound Point Fund from Sound Point Capital to American Beacon Advisors, Inc. (the “Manager”). By engaging Sound Point Capital, the current advisor to the Sound Point Fund, as the sub-advisor to the AB Fund (the “Sub-Advisor”), the AB Fund will be advised by the same portfolio management team at Sound Point Capital that currently advises the Sound Point Fund. In particular, the portfolio managers of the Sub-Advisor who are primarily responsible for the day-to-day portfolio management of the Sound Point Fund will remain the same. The investment objective of the AB Fund will be identical, and the investment strategies of the AB Fund will be substantially identical, to those of the Sound Point Fund. The AB Fund’s investment limitations are substantially identical to those of the Sound Point Fund; however, the investment limitations have been updated by the AB Fund to align with the limitations applicable to other funds in the American Beacon Family of Funds.

The Reorganization will affect other services currently provided to the Sound Point Fund. Foreside Fund Services, LLC (“Foreside”) will be the distributor and principal underwriter of the AB Fund’s shares; Quasar Distributors, LLC currently serves as the distributor and principal underwriter of the Sound Point Fund’s shares. Additionally, the Manager will engage Foreside to provide sub-administrative services in connection with the marketing and distribution of shares of the AB Fund. The AB Fund will engage State Street Bank and Trust Company (“State Street”) as the AB Fund’s custodian and accounting agent; U.S. Bank National Association (“U.S. Bank”), currently serves as the custodian for the Sound Point Fund. U.S. Bancorp Fund Services, LLC (“USBFS”), a U.S. Bank affiliate, currently serves as the Sound Point Fund’s administrator, transfer agent and fund accountant. The AB Fund will engage Boston Financial Data Services, a State Street affiliate, as the AB Fund’s transfer agent, and the Manager will provide administration services for the AB Fund.

The Reorganization will move the assets of the Sound Point Fund from the Trust, which is a Delaware statutory trust, to the AB Fund, a series of the AB Trust, which is a Massachusetts business trust. As a result of the Reorganization, the AB Fund will operate under the supervision of the AB Trust’s Board of Trustees. Please refer to the section in the Proxy Statement entitled “Comparison of Forms of Organization and Shareholder Rights” for more information about the differences between the Trust and the AB Trust.

Question: Who will manage the AB Fund?

Answer: The Manager will be responsible for overseeing the management of the AB Fund, and the portfolio managers of the Sub-Advisor who are primarily responsible for the day-to-day portfolio management of the Sound Point Fund will continue to manage the portfolio of the AB Fund. In addition to overseeing the management of the AB Fund by the Sub-Advisor, the Manager may invest the portion of the AB Fund’s assets that the Sub-Advisor determines to be allocated to short-term investments.

The Manager is an experienced provider of investment advisory services to institutional and retail investors, with approximately $[ ] billion in mutual fund and $[ ] billion in overall assets under management as of September 30, 2015. Since 1986, the Manager has offered a variety of services and products, including corporate cash management, separate account management, and mutual funds. The Manager serves retail clients as well as defined benefit plans, defined contribution plans, foundations, endowments, corporations, and other institutional investors. There are currently over 30 series of the AB Trust, including the AB Fund. The American Beacon Family of Funds advised by the Manager currently includes international and domestic equity portfolios spanning a variety of longer-range investment strategies through balanced portfolios, as well as short-term investment options such as bond funds and money market funds.

The Sub-Advisor is a Delaware limited partnership that has been registered as an investment adviser with the SEC since July 2011 and has managed the affairs of the Sound Point Fund since its inception. The Sub-Advisor had approximately $[ ] billion under management as of September 30, 2015.

Question: How will the Reorganization affect the fees and expenses I pay as a shareholder of the Sound Point Fund?

Answer: The AB Fund’s advisory fees will be lower than the advisory fee currently paid by the Sound Point Fund. The AB Fund will pay advisory fees at an annual rate of 0.40% of its average daily net assets while the Sound Point Fund pays an advisory fee at an annual rate of 0.65% of its average daily net assets. The Sound Point Fund assesses no front-end sales charge, contingent deferred sales charge, redemption fees or exchange fees on its Investor Class or Institutional Class shares, and no such fees will be assessed by the AB Fund on its SP Class or Institutional Class shares. The AB Fund's SP Class will have a Rule 12b-1 distribution and service fee of 0.25% while the Sound Point Fund's Investor Class does not. Neither the AB Fund's Institutional Class nor the Sound Point Fund's Institutional Class has a Rule 12b-1 fee.

The net annual operating expense ratio of the AB Fund’s SP Class shares is not expected to be materially different from that of the Sound Point Fund’s Investor Class shares for the first two years after the Reorganization. The net annual operating expense ratio of the Sound Point Fund’s Investor Class shares for the annual period ended August 31, 2014 was 1.15% of that Fund’s average daily net assets while the projected net annual operating expense ratio for the AB Fund’s SP Class shares based on the same asset level is 1.16% of that Fund’s average daily net assets. The net annual operating expense ratio of the AB Fund’s Institutional Class shares is expected to be lower than that of the Sound Point Fund’s Institutional Class shares for the first two years after the Reorganization. The net annual operating expense ratio of the Sound Point Fund’s Institutional Class shares for the annual period ended August 31, 2014 was 0.90% of that Fund’s average daily net assets while the projected net annual operating expense ratio for the AB Fund’s Institutional Class shares based on the same asset levels is 0.85% of that Fund’s average daily net assets.

Although the gross annual operating expense ratio of the AB Fund’s SP Class shares is expected to be higher than that of the Sound Point Fund’s Investor Class shares, shareholders will not be affected by the increase for the first two years after the Reorganization and for so long thereafter as the Manager agrees to maintain the net expense ratio of the AB Fund’s SP Class shares at the current expense cap

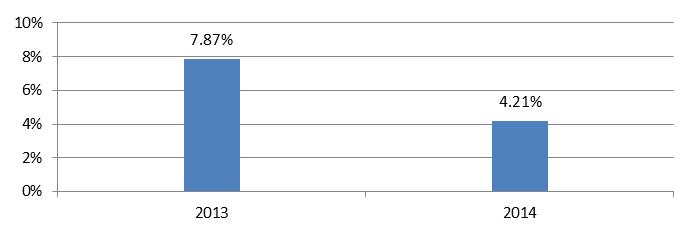

level. The gross annual operating expense ratio of the Sound Point Fund’s Investor Class shares based on its annual period ended August 31, 2014 was 1.95% of that Fund’s average daily net assets before the limitation on expenses. The projected gross annual operating operating expenses for the AB Fund’s SP Class shares based on the same asset level is 2.15% of that Fund’s average daily net assets before the limitation on expenses.

The gross annual operating expense ratio of the AB Fund’s Institutional Class is expected to be lower than that of the Sound Point’s Institutional Class shares. The gross annual operating expense ratio of the Sound Point Fund’s Institutional Class shares for the annual period ended August 31, 2014 was 2.37% of that Fund’s average daily net assets before the limitation on expenses. The projected gross annual operating expense ratio for the AB Fund’s Institutional Class shares based on the same asset levels is 1.90% of that Fund’s average daily net assets before the limitation on expenses.

The Manager has contractually agreed to waive fees and/or reimburse expenses, excluding taxes, interest, brokerage commissions, acquired fund fees and expenses, securities lending fees, expenses associated with securities sold short, litigation, and other extraordinary expenses, in order to limit net annual fund operating expenses through December 31, 2017 to 1.15% for the AB Fund’s SP Class shares and 0.84% for the Institutional Class shares. However, the net expenses of the AB Fund’s SP Class shares and Institutional Class shares would increase after December 31, 2017, and for so long thereafter, if the Manager does not continue to reduce and/or reimburse expenses at these levels (unless the assets of the AB Fund increased enough to result in a sufficient decrease in the AB Fund’s gross expenses). After the initial term, the AB Trust Board intends to consider the continuation of the expense caps on the SP Class and Institutional Class shares on an annual basis. Sound Point Capital has contractually agreed to waive fees and/or reimburse expenses, excluding acquired fund fees and expenses, interest, taxes, interest and dividend expense on securities sold short and extraordinary expenses, in order to limit net annual fund operating expenses through December 31, 2015 to 1.15% for the Sound Point Fund’s Investor Class shares and 0.90% for the Institutional Class shares.

Question: Will the Reorganization result in any taxes?

Answer: We expect that neither the Sound Point Fund nor its shareholders will recognize any gain or loss for federal income tax purposes as a direct result of the Reorganization, and the Trust and the AB Trust expect to receive a tax opinion confirming this position. Shareholders should consult their own tax advisers about possible state and local tax consequences of the Reorganization, if any, because the information about tax consequences in this document relates only to the federal income tax consequences of the Reorganization.

Question: Will I be charged a sales charge or contingent deferred sales charge (CDSC) as a result of the Reorganization?

Answer: No sales loads, commissions or other transactional fees will be imposed on shareholders in connection with the Reorganization.

Question: Why do I need to vote?

Answer: Your vote is needed to ensure that a quorum and sufficient votes are present at the Special Meeting so that the proposal can be acted upon. Your immediate response on the enclosed Proxy Card will help prevent the need for any further solicitations for a shareholder vote. Your vote is very important to us regardless of the number of shares you own.

Question: How does the Trust’s Board of Trustees recommend that I vote?

Answer: After careful consideration and upon recommendation of Sound Point Capital, the Trust’s Board of Trustees unanimously recommends that shareholders vote “FOR” the Plan.

Question: Who is paying for expenses related to the Special Meeting and the Reorganization?

Answer: The Manager and Sound Point Capital will pay all direct costs relating to the Reorganization, including the costs relating to the Special Meeting and the Proxy Statement. The Sound Point Fund and its shareholders will not incur any expenses in connection with the Reorganization. Expenses relating to the Reorganization are estimated to be approximately $[ ].

Question: What will happen if the Plan is not approved by shareholders?

Answer: If shareholders of the Sound Point Fund do not approve the Plan, the Sound Point Fund will not be reorganized into the AB Fund.

Question: How do I vote my shares?

Answer: You can vote your shares by telephone, by mail, by the internet and by automated touchtone as set forth below:

| | Phone: | To cast your vote by phone with a proxy voting representative, call the toll-free number found on the enclosed proxy card. You will be required to provide your control number found on the reverse side of your proxy card. |

| | | |

| | Mail: | To vote your proxy by mail, check the appropriate voting box on the reverse side of your proxy card, sign and date the card and return it in the enclosed postage-prepaid envelope. If you sign, date and return the proxy card but give no voting instructions, the proxies will vote FOR the proposal. |

| | | |

| | The options below are available 24 hours a day/7 days a week. |

| | | |

| | Internet: | The web address and instructions for voting online can be found on the enclosed proxy card. You will be required to provide your control number found on the reverse side of your proxy card. |

| | | |

| | Automated Touchtone: | The toll-free number for automated touchtone telephone voting can be found on the enclosed proxy card. You must have the control number found on the reverse side of your proxy card. |

Question: Who do I call if I have questions?

Answer: If you have any questions regarding the proposal, the proxy card or need assistance voting your shares, please contact [ ], the Sound Point Fund’s proxy solicitor, toll-free at [ ].

COMBINED PROXY STATEMENT AND PROSPECTUS

[ ], 2015

For the Reorganization of

Sound Point Floating Rate Income Fund

a series of Trust for Advised Portfolios

615 East Michigan Street

Milwaukee, Wisconsin 53202

626-914-7220

Into

American Beacon Sound Point Floating Rate Income Fund,

a series of American Beacon Funds

220 East Las Colinas Boulevard, Suite 1200

Irving, Texas 75039

(800) 658-5811

_________________________________________

This Combined Proxy Statement and Prospectus (the “Proxy Statement”) is being sent to you in connection with the solicitation of proxies by the Board of Trustees (the “Board”) of Trust for Advised Portfolios (the “Trust”) for use at a Special Meeting of Shareholders (the “Special Meeting”) of the Sound Point Floating Rate Income Fund, a series of the Trust (the “Sound Point Fund”), managed by Sound Point Capital Management, L.P. (“Sound Point Capital”), at the principal executive offices of the Trust located at 615 East Michigan Street, Milwaukee, Wisconsin 53202 on Monday, December 7, 2015, at [ ] p.m. Central Time. At the Special Meeting, shareholders of the Sound Point Fund will be asked:

1. To approve the Agreement and Plan of Reorganization and Termination (the “Plan”) adopted by the Trust’s Board of Trustees, which provides for the reorganization of the Sound Point Fund into the American Beacon Sound Point Floating Rate Income Fund (the “AB Fund”), a newly created series of American Beacon Funds (the “AB Trust”).

The Plan provides for the transfer of all of the assets of the Sound Point Fund to the AB Fund in exchange for:

(a) SP Class shares and Institutional Class shares of the AB Fund equal in number and value to the Sound Point Fund’s Investor Class shares and Institutional Class shares, respectively, which will be distributed pro rata by the Sound Point Fund to the holders of its shares in complete liquidation of the Sound Point Fund as follows:

| Sound Point Floating Rate Income Fund | à | American Beacon Sound Point Floating Rate Income Fund |

| Investor Class shares | à | SP Class shares |

| Institutional Class shares | à | Institutional Class shares |

and

(b) the AB Fund’s assumption of all of the liabilities of the Sound Point Fund (collectively, the “Reorganization”); and

2. To transact any other business as may properly come before the Special Meeting or any adjournments or postponements thereof.

The Sound Point Fund is a series of the Trust, an open-end management investment company registered with the Securities and Exchange Commission (the “SEC”) and organized as a Delaware statutory trust. The AB Fund is a newly created series of the AB Trust, an open-end management investment company registered with the SEC and organized as a Massachusetts business trust.

This Proxy Statement sets forth the basic information you should know before voting on the proposal. You should read it and keep it for future reference. Additional information relating to the AB Fund and this Proxy Statement is set forth in the Statement of Additional Information to this Proxy Statement dated [ ], 2015, which is incorporated by reference into this Proxy Statement. Additional information about the AB Fund has been filed with the SEC and is available upon request and without charge by writing to the AB Fund or by calling 1-800-658-5811. The Sound Point Fund expects that this Proxy Statement will be mailed to shareholders on or about [ ], 2015.

The following documents have been filed with the SEC and are incorporated by reference into this Proxy Statement, which means that these documents are considered legally to be part of this Proxy Statement:

| · | Statement of Additional Information to this Proxy Statement, dated [ ], 2015; |

| · | Prospectus and Statement of Additional Information of the Sound Point Fund, each dated December 29, 2014; and; |

| · | Annual Report to Shareholders of the Sound Point Fund for the fiscal year ended August 31, 2014, as supplemented; and |

| · | Semi-Annual Report to Shareholders of the Sound Point Fund for the semi-annual period ended February 28, 2015. |

A copy of the Statement of Additional Information to this Proxy Statement is available upon request and without charge by writing to the AB Trust or by calling (toll-free) at 1-800-658-5811. Copies of the other documents are available upon request and without charge by writing to the Trust, through the internet at www.[ ].com, or by calling (toll-free) at [ ].

Because the AB Fund has not yet commenced operations as of the date of this Proxy Statement, no annual or semi-annual report is available for the AB Fund at this time.

THE SEC HAS NOT APPROVED OR DISAPPROVED THESE SECURITIES NOR HAS IT PASSED ON THE ACCURACY OR ADEQUACY OF THIS PROXY STATEMENT. ANY REPRESENTATION TO THE CONTRARY IS A CRIMINAL OFFENSE.

The shares offered by this Proxy Statement are not deposits or obligations of any bank, and are not insured or guaranteed by the Federal Deposit Insurance Company or any other government agency. An investment in the AB Fund involves investment risk, including the possible loss of principal.

TABLE OF CONTENTS

| I. | PROPOSAL – TO APPROVE THE AGREEMENT AND PLAN OF REORGANIZATION AND TERMINATION | 1 |

| | A. | OVERVIEW | 1 |

| | B. | REASONS FOR THE REORGANIZATION | 1 |

| | C. | BOARD CONSIDERATIONS | 3 |

| | D. | COMPARISON OF PRINCIPAL INVESTMENT OBJECTIVES, STRATEGIES AND POLICIES OF THE FUNDS | 6 |

| | E. | COMPARISON OF PRINCIPAL RISKS | 10 |

| | F. | COMPARISON OF THE FUNDS’ INVESTMENT RESTRICTIONS AND LIMITATIONS | 17 |

| | G. | COMPARISON OF FEES AND EXPENSES | 22 |

| | H. | PERFORMANCE INFORMATION | 25 |

| | I. | COMPARISON OF DISTRIBUTION AND PURCHASE, REDEMPTION AND EXCHANGE PROCEDURES | 27 |

| | J. | KEY INFORMATION ABOUT THE PROPOSAL | 28 |

| | | 1. | SUMMARY OF THE PROPOSED REORGANIZATION | 28 |

| | | 2. | DESCRIPTION OF THE AB FUND’S SP CLASS SHARES AND INSTITUTIONAL CLASS SHARES | 30 |

| | | 3. | FEDERAL INCOME TAX CONSEQUENCES | 30 |

| | | 4. | COMPARISON OF FORMS OF ORGANIZATION AND SHAREHOLDER RIGHTS | 31 |

| | | 5. | CAPITALIZATION | 34 |

| | K. | ADDITIONAL INFORMATION ABOUT THE AB FUND | 34 |

| | | 1. | MANAGER AND SUB-ADVISOR | 34 |

| | | 2. | OTHER SERVICE PROVIDERS | 36 |

| | | 3. | TAX CONSIDERATIONS | 36 |

| | | 4. | PAYMENTS TO BROKER-DEALERS AND OTHER FINANCIAL INTERMEDIARIES | 37 |

| II. | VOTING INFORMATION | 37 |

| | A. | RECORD DATE, VOTING RIGHTS AND VOTE REQUIRED | 37 |

| | B. | HOW TO VOTE | 37 |

| | C. | PROXIES | 38 |

| | D. | QUORUM AND ADJOURNMENTS | 38 |

| | E. | EFFECT OF ABSTENTIONS AND BROKER “NON-VOTES” | 38 |

| | F. | SOLICITATION OF PROXIES | 39 |

| III. | OTHER INFORMATION | 39 |

| | A. | OTHER BUSINESS | 39 |

| | B. | NEXT MEETING OF SHAREHOLDERS | 39 |

| | C. | LEGAL MATTERS | 39 |

| | D. | INFORMATION FILED WITH THE SEC | 39 |

| APPENDIX A − FORM OF AGREEMENT AND PLAN OF REORGANIZATION AND TERMINATION | A-1 |

| APPENDIX B − OWNERSHIP OF SHARES OF THE SOUND POINT FUND | B-1 |

| APPENDIX C − VALUATION, PURCHASE, REDEMPTION AND TAX INFORMATION FOR THE AB FUND | C-1 |

| APPENDIX D − FINANCIAL HIGHLIGHTS OF THE SOUND POINT FUND | D-1 |

I. PROPOSAL – TO APPROVE THE AGREEMENT AND

PLAN OF REORGANIZATION AND TERMINATION

The Board, including all the Trustees who are not “interested persons,” as that term is defined in the Investment Company Act of 1940, as amended (the “1940 Act”), of the Trust, proposes that the Sound Point Fund reorganize into the AB Fund and that each Sound Point Fund shareholder become a shareholder of the AB Fund, pursuant to the Plan, the form of which is attached to this Proxy Statement as Appendix A. The Board considered the Reorganization at a meeting held on September 30, 2015. The Board believes that the Reorganization is in the best interests of the Sound Point Fund and its shareholders.

In order to reorganize the Sound Point Fund into a series of the AB Trust, a substantially identical fund, referred to as the “AB Fund,” has been created as a new series of the AB Trust. If the shareholders of the Sound Point Fund approve the Plan, the Reorganization will have three primary steps:

* First, the Sound Point Fund will transfer all of its assets to the AB Fund in exchange solely for SP Class shares and Institutional Class shares of the AB Fund and the AB Fund’s assumption of all of the Sound Point Fund’s liabilities;

* Second, each holder of Sound Point Fund Investor Class shares will receive a pro rata distribution of the AB Fund’s SP Class shares and each holder of Sound Point Fund Institutional Class shares will receive a pro rata distribution of the AB Fund’s Institutional Class shares; and

* Third, the Sound Point Fund will be liquidated.

Approval of the Plan will constitute approval of the transfer of the Sound Point Fund’s assets, the assumption of its liabilities, the distribution of the AB Fund’s SP Class shares and Institutional Class shares, and liquidation of the Sound Point Fund. The SP Class shares and Institutional Class shares issued in connection with the Reorganization will have an aggregate net asset value (“NAV”) equal to the value of the assets that the Sound Point Fund transferred to the AB Fund, less the Sound Point Fund’s liabilities that the AB Fund assumes. Existing shareholders of the Sound Point Fund’s Investor Class shares will become shareholders of the AB Fund’s SP Class shares and existing shareholders of the Sound Point Fund’s Institutional Class shares will become shareholders of the AB Fund’s Institutional Class shares, and immediately after the Reorganization, each shareholder will hold SP Class shares or Institutional Class shares of the AB Fund, as the case may be, equal in number and value to the Sound Point Fund’s Investor Class shares or Institutional Class shares that the shareholder held immediately prior to the Reorganization. No sales charge or fee of any kind will be charged to the Sound Point Fund’s shareholders in connection with the Reorganization.

The Trust believes that the Reorganization will constitute a tax-free transaction for federal income tax purposes. Therefore, shareholders should not recognize any gain or loss on their Sound Point Fund shares for federal income tax purposes as a direct result of the Reorganization. The Trust and the AB Trust will receive an opinion from tax counsel to the AB Trust confirming such tax treatment.

| B. | REASONS FOR THE REORGANIZATION |

The primary purpose of the Reorganization is to move the investment portfolio and shareholders presently associated with Sound Point Fund to the American Beacon Family of Funds. Reconstituting the

Sound Point Fund as a series of the AB Trust has the potential to expand the distribution network and increase the Sound Point Fund’s assets, as the AB Trust has access to greater resources and distribution channels than does the Trust.

The Reorganization will shift management oversight responsibility for the Sound Point Fund from Sound Point Capital to American Beacon Advisors, Inc. (the “Manager”). By engaging Sound Point Capital, the current advisor to the Sound Point Fund, as the sub-advisor to the AB Fund (the “Sub-Advisor”), the AB Fund will be advised by the same portfolio management team at Sound Point Capital that currently advises the Sound Point Fund. In particular, the portfolio managers of the Sub-Advisor who are primarily responsible for the day-to-day portfolio management of the Sound Point Fund will remain the same. The investment objective of the AB Fund will be identical, and the investment strategies of the AB Fund will be substantially identical, to those of the Sound Point Fund. The AB Fund’s material investment limitations are substantially identical to those of the Sound Point Fund; however, the investment limitations have been updated by the AB Fund to align with the limitations applicable to other funds in the American Beacon Family of Funds.

The Reorganization will affect other services currently provided to the Sound Point Fund. Foreside Fund Services, LLC (“Foreside”) will be the distributor and principal underwriter of the AB Fund’s shares; Quasar Distributors, LLC currently serves as the distributor and principal underwriter of the Sound Point Fund’s shares. Additionally, the Manager will engage Foreside to provide sub-administrative services in connection with the marketing and distribution of shares of the AB Fund. The AB Trust will engage State Street Bank and Trust Company (“State Street”) as the AB Fund’s custodian and accounting agent; U.S. Bank National Association (“U.S. Bank”) currently serves as the custodian for the Sound Point Fund. U.S. Bancorp Fund Services, LLC (“USBFS”), a U.S. Bank affiliate, currently serves as the Sound Point Fund’s administrator, transfer agent and fund accountant. The AB Trust will engage Boston Financial Data Services, a State Street affiliate, as the AB Fund’s transfer agent, and the Manager will provide administration services for the AB Fund.

The Reorganization will move the assets of the Sound Point Fund from the Trust, which is a Delaware statutory trust, to the AB Fund, a series of the AB Trust, which is a Massachusetts business trust. As a result of the Reorganization, the AB Fund will operate under the supervision of the AB Trust’s Board of Trustees. Please refer to the section in the Proxy Statement entitled “Comparison of Forms of Organization and Shareholder Rights” for more information about the differences between the Trust and the AB Trust.

The AB Fund’s advisory fees will be lower than the advisory fee currently paid by the Sound Point Fund. The AB Fund will pay advisory fees at an annual rate of 0.40% of its average daily net assets while the Sound Point Fund pays an advisory fee at an annual rate of 0.65% of its average daily net assets. The Sound Point Fund assesses no front-end sales charge, contingent deferred sales charge, redemption fees or exchange fees on its Investor Class or Institutional Class shares, and no such fees will be assessed by the AB Fund on its SP Class or Institutional Class shares. The AB Fund's SP Class will hae a Rule 12b-1 distribution and service fee of 0.25% while the Sound Point Fund's Investor class does not. Neither the AB Fund's Institutional Class nor the Sound Point Fund's Institutional Class has a Rule 12b-1 fee.

The net annual operating expense ratio of the AB Fund’s SP Class shares is not expected to be materially different from that of the Sound Point Fund’s Investor Class shares for the first two years after the Reorganization. The net annual operating expense ratio of the Sound Point Fund’s Investor Class shares for the annual period ended August 31, 2014 was 1.15% of that Fund’s average daily net assets while the projected net annual operating expense ratio for the AB Fund’s SP Class shares based on the same asset level is 1.16% of that Fund’s average daily net assets. The net annual operating expense ratio of the AB Fund’s Institutional Class shares is expected to be lower than that of the Sound Point Fund’s Institutional Class shares for the first two years after the Reorganization. The net annual operating

expense ratio of the Sound Point Fund’s Institutional Class shares for the annual period ended August 31, 2014 was 0.90% of that Fund’s average daily net assets while the projected net annual operating expense ratio for the AB Fund’s Institutional Class shares based on the same asset levels is 0.85% of that Fund’s average daily net assets.

Although the gross annual operating expense ratio of the AB Fund’s SP Class shares is expected to be higher than that of the Sound Point Fund’s Investor Class shares, shareholders will not be affected by the increase for the first two years after the Reorganization and for so long thereafter as the Manager agrees to maintain the net expense ratio of the AB Fund’s SP Class shares at the current expense cap level. The gross annual operating expense ratio of the Sound Point Fund’s Investor Class shares based on its annual period ended August 31, 2014 was 1.95% of that Fund’s average daily net assets before the limitation on expenses. The projected gross annual operating expenses for the AB Fund’s SP Class shares based on the same asset level is 2.15% of that Fund’s average daily net assets before the limitation on expenses.

The gross annual operating expense ratio of the AB Fund’s Institutional Class is expected to be lower than that of the Sound Point’s Institutional Class shares. The gross annual operating expense ratio of the Sound Point Fund’s Institutional Class shares for the annual period ended August 31, 2014 was 2.37% of that Fund’s average daily net assets before the limitation on expenses. The projected gross annual operating expense ratio for the AB Fund’s Institutional Class shares based on the same asset levels is 1.90% of that Fund’s average daily net assets before the limitation on expenses.

The Manager has contractually agreed to waive fees and/or reimburse expenses, excluding taxes, interest, brokerage commissions, acquired fund fees and expenses, securities lending fees, expenses associated with securities sold short, litigation, and other extraordinary expenses, in order to limit net annual fund operating expenses through December 31, 2017 to 1.15% for the AB Fund’s SP Class shares and 0.84% for the Institutional Class shares. However, the net expenses of the AB Fund’s SP Class shares and Institutional Class shares would increase after December 31, 2017, and for so long thereafter, if the Manager does not continue to reduce and/or reimburse expenses at these levels (unless the assets of the AB Fund increased enough to result in a sufficient decrease in the AB Fund’s gross expenses). After the initial term, the AB Trust Board intends to consider the continuation of the expense caps on the SP Class and Institutional Class shares on an annual basis. Sound Point Capital has contractually agreed to waive fees and/or reimburse expenses, excluding acquired fund fees and expenses, interest, taxes, interest and dividend expense on securities sold short and extraordinary expenses, in order to limit net annual fund operating expenses through December 31, 2015 to 1.15% for the Sound Point Fund’s Investor Class shares and 0.90% for the Institutional Class shares.

Sound Point Capital proposed, and the Board considered (with the advice and assistance of independent legal counsel), the Reorganization at a meeting held on September 30, 2015. Based upon the recommendation of Sound Point Capital, the Board’s evaluation of the relevant information prepared by the Manager and presented to the Board in advance of the meeting, and in light of its fiduciary duties under federal and state law, the Board, including all trustees who are not “interested persons” of the Trust under the 1940 Act, determined that the Reorganization is in the best interests of the Sound Point Fund and its shareholders and that the interests of existing Sound Point Fund shareholders will not be diluted as a result of the Reorganization.

In approving the Reorganization as proposed by Sound Point Capital, the Board noted that the Sound Point Fund assets have not achieved economies of scale despite significant sales efforts by Sound

Point Capital. The Board noted further Sound Point Capital’s belief that, as a result, the Sound Point Fund may not be able to achieve economies of scale unless it can be combined with another fund. The Board considered the terms of the Reorganization and determined that the Reorganization would provide shareholders with the options of (1) transferring their investment to a substantially identical fund on a tax-free basis in the Reorganization or (2) redeeming their investment in the Sound Point Fund, which might have tax consequences for them.

The Board considered the following additional matters, among others, in approving the Reorganization:

The Terms and Conditions of the Reorganization. The Board considered the terms of the Plan, and, in particular, that the transfer of the assets of the Sound Point Fund will be in exchange for SP Class shares and Institutional Class shares of the AB Fund and the AB Fund’s assumption of all liabilities of the Sound Point Fund. The Board also took note of the fact that no sales charges would be imposed in connection with the Reorganization. In addition, the Board noted that pursuant to the Plan, each Sound Point Fund shareholder’s account will be credited with the number of full and fractional AB Fund Shares equal to the number of full and fractional Sound Point Fund shares that each shareholder holds immediately prior to the Reorganization and that the aggregate net asset value of AB Fund shares to be credited to each Sound Point Fund shareholder’s account will equal the aggregate net asset value of the Sound Point Fund shares that each shareholder holds immediately prior to the Reorganization. As a result, the Board noted that the interests of Sound Point Fund shareholders would not be diluted as a result of the Reorganization. The Board also noted that the Reorganization would be submitted to the Sound Point Fund’s shareholders for approval.

Substantially Identical Investment Objectives, Policies and Limitations and Continuity of Sub-Advisor. The Board considered that the investment objective of the AB Fund will be identical, and the investment strategies of the AB Fund will be substantially identical, to those of the Sound Point Fund. The Board noted that the investment limitations of the AB Fund are slightly different from those of the Sound Point Fund in order for the AB Fund to conform its limitations to those applicable to other funds in the American Beacon Family of Funds. In particular, the Board considered that the substantially identical investment strategy, together with the fact that Sound Point Capital would serve as Sub-Advisor to the AB Fund would provide continuation of portfolio management expertise to the shareholders of the Sound Point Fund.

Expenses Relating to Reorganization. The Board also considered that the Sound Point Fund and Sound Point Fund shareholders will not incur any expenses in connection with the Reorganization. The Board considered that, except for costs associated with a special meeting of the AB Trust Board which will be borne solely by Manager, the Manager and Sound Point Capital will each bear 50% of the direct costs associated with the Reorganization, Special Meeting, and solicitation of proxies, including the expenses associated with preparing and filing the registration statement that includes this Proxy Statement and the cost of copying, printing and mailing proxy materials.

Consideration Paid to Sound Point Capital. The Board considered that the Manager had agreed to pay Sound Point Capital a fee, which is contemplated to be paid in three annual installments commencing with the closing of the Reorganization, based on the average daily net assets of the Sound Point Fund for the 30 calendar days up to and including the closing date of the Reorganization. The Board noted that this fee is payable by the Manager and not by either the Sound Point Fund or AB Fund.

Relative Expense Ratios and Continuation of Limitation on Expenses. The Board first reviewed information concerning advisory fees and considered that the advisory fees payable by the AB Fund would be less than the advisory fee paid by the Sound Point Fund. The Board then reviewed information regarding comparative expense ratios (current and pro forma expense ratios are set forth in the “Comparison of Fees and Expenses” section below), which indicated that gross annual operating expense ratio for SP Class shares of the AB Fund would be higher than the gross annual operating expense ratio of Investor Class shares of the Sound Point Fund and that the gross annual operating expense ratio for Institutional Class shares of the AB Fund would be lower than the gross annual operating expense ratio of Institutional Class shares of the Sound Point Fund. The Board considered, however that, excluding acquired fund fees and expenses of 0.01%, the net total annual operating expense ratio for SP Class shares of the AB Fund through December 31, 2017 would be the same as the net total annual operating expense ratio of Investor Class shares of the Sound Point Fund, and that net total annual operating expense ratio for Institutional Class shares of the AB Fund through December 31, 2017 would be lower than the net total annual operating expense ratio of Institutional Class shares of the Sound Point Fund. In this regard, the Board recognized that the Manager would contractually agree to reduce and/or reimburse expenses payable by the AB Fund through at least December 31, 2017, to the extent that the total annual operating expense ratio of SP Class shares exceeds 1.15% of average daily net assets and Institutional Class shares exceeds 0.84% of average daily net assets, which expense limits are the same as Sound Point Fund’s expense limits for Investor Class shares and lower than the Sound Point Fund’s expense limits for Institutional Class shares. The Board also considered the exclusions from the expense limitation arrangement applicable to the AB Fund as compared to the Sound Point Fund. The Board also considered that the Sound Point Fund’s expense cap was scheduled to expire on December 31, 2015 and that the Manager had agreed to a contractual two-year expense cap as described above. The Board noted that, after the initial term, the AB Trust Board intends to consider the continuation of the expense caps on the SP Class and Institutional Class shares on an annual basis.

Economies of Scale. The Board considered the potential of the AB Fund to experience economies of scale as a result of its being a series of the AB Trust (which has over 30 series and $[ ] billion in assets as of September 30, 2015) because certain fixed costs, such as legal, accounting, shareholder services and trustee expenses, would be spread over a larger fund complex. The Board concluded that the structure may benefit shareholders as the AB Fund grows.

Distribution and Service Fees. The Board considered the fund distribution capabilities of the Manager and its affiliates and their commitment to distribute the AB Fund. The Board further considered that while the Investor Class of the Sound Point Fund currently does not have a Rule 12b-1 distribution and service fee, it previously did have a 0.25% Rule 12b-1 distribution and service fee like that of the SP Class of the AB Fund, and that having one again would benefit shareholders by enhancing distribution. The Board also considered that, despite the 0.25% difference in expenses between the two classes, the net total annual operating expense ratio for SP Class shares of the AB Fund through December 31, 2017 would be the same as the net total annual operating expense ratio of Investor Class shares of the Sound Point Fund. With respect to the Institutional Class of the Sound Point Fund, the Board noted that like the Sound Point Fund's Institutional Class the Institutional Class shares of the AB Fund will not pay a Rule 12b-1 distribution or service fee.

The Experience and Expertise of the Manager and Sub-Advisor. The Board considered the following information that was provided to it regarding the Manager: (1) the Manager is an experienced provider of investment advisory services to institutional and retail markets, with approximately $[ ] billion in mutual fund and $[ ] billion in overall assets under management as of September 30, 2015; (2) since 1986, the Manager has offered a variety of services and products, including corporate cash management, separate account management, and mutual funds; and (3) the Manager serves retail clients as well as defined benefit plans, defined contribution plans, foundations, endowments, corporations, and other institutional investors. The Board also considered that there are currently over 30 series of the AB Trust.

The Board considered that Sound Point Capital, a Delaware limited liability company and the current advisor to the Sound Point Fund, would provide sub-advisory services to the AB Fund. The Board noted that the Sub-Advisor’s principals have significant investment experience related to the investment management of the Sound Point Fund and the accounts of institutional and individual clients, private investment companies and mutual funds.

Tax Consequences. The Board considered that the Reorganization is expected to be free from adverse federal income tax consequences.

Based on the information presented to the Board by Sound Point Capital, the Board determined that the Reorganization as proposed by Sound Point Capital is in the best interests of the Sound Point Fund and its shareholders. The Board approved the Reorganization, subject to approval by shareholders of the Sound Point Fund and the solicitation of the shareholders of the Sound Point Fund to vote “FOR” the approval of the Plan, the form of which is attached to this Proxy Statement in Appendix A.

| D. | COMPARISON OF PRINCIPAL INVESTMENT OBJECTIVES, STRATEGIES AND POLICIES OF THE FUNDS |

The Sound Point Fund and the AB Fund (each sometimes referred to herein as a “Fund”) have identical investment objectives and substantially identical strategies, which are presented in the table below.

The AB Fund has been created as a shell series of the AB Trust solely for the purpose of acquiring the Sound Point Fund’s assets and continuing its business, and will not conduct any investment operations until after the closing of the Reorganization. The Manager has reviewed the Sound Point Fund’s current portfolio holdings and determined that those holdings are compatible with the AB Fund’s investment objectives and policies. As a result, the Manager believes that, if the Reorganization is approved, all or substantially all of the Sound Point Fund’s assets will be transferred to and held by the AB Fund.

| Sound Point Fund | AB Fund |

| Investment Objective | |

The Sound Point Fund seeks to provide a high level of current income consistent with strong risk-adjusted returns. The Sound Point Fund’s investment objective is a non-fundamental policy that may be changed by its Board without shareholder approval. | The AB Fund will have the same investment objective. The AB Fund’s investment objective also will be a non-fundamental policy that may be changed by its Board without shareholder approval. |

| Principal Investment Strategies | |

| Under normal circumstances, the Sound Point Fund invests at least 80% of its net assets (plus any borrowings for investment purposes) in income producing floating rate loans and other floating rate debt securities, which may include bonds, notes | Under normal circumstances, the AB Fund invests at least 80% of its net assets (plus any borrowings for investment purposes) in income producing floating rate loans and other floating rate debt securities, which may include bonds, notes and |

and debentures issued by corporations, debt securities issued or guaranteed by the U.S. government or one of its agencies or instrumentalities, and commercial paper. The Sound Point Fund invests primarily in senior floating rate loans (“Floating Rate Loans”) which are made by banks and other large financial institutions to various companies and are senior in the borrowing companies’ capital structure. Floating Rate Loans typically are of below investment grade quality and have below investment grade credit ratings, which ratings are associated with securities having high risk, speculative characteristics (sometimes referred to as “high yield” or “junk”).

Sound Point Capital utilizes a fundamental, research intensive approach to achieve its objective by identifying fundamentally attractive floating rate loans or variable-rate investments, which it considers under-valued, which pay interest at variable-rates and are determined periodically, on the basis of a floating base lending rate, such as the London Interbank Offered Rate (“LIBOR”), with or without a floor plus a fixed spread and other investments, including senior secured and unsecured bonds, and by creating a portfolio with an optimal blend of these assets. In managing the Sound Point Fund, Sound Point Capital seeks to invest in a portfolio of Floating Rate Loans that it believes will be less volatile over time than the general loan market. Preservation of capital is considered when consistent with the Sound Point Fund’s objective. The Fund invests in securities without regard to maturity or duration.

Sound Point Capital manages the Sound Point Fund using a bottom-up, fundamental approach and focuses on relative value across industries, within industries and within individual capital structures. Given the focus on relative value, the Sound Point Fund has a target investment lifecycle of 3 to 12 months and does not employ a “buy-and-hold to maturity” strategy. Sound Point Capital generally sells a security when it believes its projected future return becomes unattractive relative to the rest of the portfolio or the investable universe. | debentures issued by corporations, debt securities issued or guaranteed by the U.S. government or one of its agencies or instrumentalities, and commercial paper. The AB Fund invests primarily in senior floating rate loans (“Floating Rate Loans”) which are made by banks and other large financial institutions to various companies and are senior in the borrowing companies’ capital structure. Floating Rate Loans typically are of below investment grade quality (sometimes referred to as “high yield” or “junk” bonds) and have below investment grade credit ratings, which ratings are associated with securities having high risk, speculative characteristics, or are unrated but deemed by Sound Point Capital to be of equivalent quality.

Sound Point Capital utilizes a bottom-up, fundamental, research intensive approach to achieve its objective by identifying fundamentally attractive floating rate loans or variable-rate investments, which it considers under-valued, which pay interest at variable-rates and are determined periodically, on the basis of a floating base lending rate, such as the London Interbank Offered Rate (“LIBOR”), with or without a floor plus a fixed spread and other investments, including senior secured and unsecured bonds, and by creating a portfolio with an optimal blend of these assets. In managing the AB Fund, Sound Point Capital seeks to invest in a portfolio of Floating Rate Loans that it believes will be less volatile over time than the general loan market. Sound Point Capital considers preservation of capital when consistent with the AB Fund’s investment objective. The AB Fund invests in securities without regard to maturity or duration.

Sound Point Capital focuses on relative value across industries, within industries and within individual capital structures. Given the focus on relative value, the AB Fund has a target investment lifecycle of 3 to 12 months and does not employ a “buy-and-hold to maturity” strategy. Therefore, the AB Fund may have high portfolio turnover Sound Point Capital generally sells a security when it believes its projected future return becomes unattractive relative to the rest of the portfolio or the investable universe. |

| Interest Rates and Portfolio Maturity. The Floating Rate Loans in which the Sound Point Fund invests typically have multiple reset periods during the year with each reset period applicable to a designated portion of the loan. As short-term interest rates decline, interest payable to the Sound Point Fund should decrease. The amount of time that will pass before the Sound Point Fund experiences the effects of changing short-term interest rates will depend on the dollar weighted average time until the next interest rate adjustment on the Sound Point Fund’s portfolio of loans. Loans usually have mandatory and optional prepayment provisions. Because of prepayments, the actual remaining maturity of a loan may be considerably less than its stated maturity. If a loan is prepaid, the Sound Point Fund will have to reinvest the proceeds in other loans or securities, which may have a lower fixed spread over its base rate. In such a case, the amount of interest paid to the Sound Point Fund would likely decrease. The Sound Point Fund is non-diversified and therefore is allowed to focus its investments in fewer companies than a fund that is required to diversify its portfolio. | The Floating Rate Loans in which the AB Fund invests typically have multiple reset periods during the year with each reset period applicable to a designated portion of the loan. As short-term interest rates decline, interest payable to the AB Fund should decrease. The amount of time that will pass before the AB Fund experiences the effects of changing short-term interest rates will depend on the dollar-weighted average time until the next interest rate adjustment on the AB Fund’s portfolio of loans. Loans usually have mandatory and optional prepayment provisions. Because of prepayments, the actual remaining maturity of a loan may be considerably less than its stated maturity. If a loan is prepaid, the AB Fund will have to reinvest the proceeds in other loans or securities, which may have a lower fixed spread over its base rate. In such a case, the amount of interest paid to the AB Fund would likely decrease.

The AB Fund is non-diversified, which means that it may invest a high percentage of its assets in a limited number of issuers.

|

| Cash Management Investments |

| The Sound Point Fund may invest a portion of its assets in high quality fixed-income securities, money market instruments, and money market mutual funds, or hold cash or cash equivalents in such amounts as Sound Point Capital deems appropriate under the circumstances, including when Sound Point Capital believes the Sound Point Fund needs to retain cash. Money market instruments or short-term debt securities held by the Sound Point Fund for cash management or defensive investing purposes can fluctuate in value. To the extent that the Sound Point Fund uses a money market fund or an exchange-traded fund for its cash position, there will be some duplication of expenses because the Fund would bear its pro rata portion of such money market fund’s or exchange-traded fund’s management fees and operational expenses. | The AB Fund may invest cash balances in money market funds that are registered as investment companies under the 1940 Act, including money market funds that are advised by the Manager or a sub-advisor. If the AB Fund invests in money market funds, shareholders will bear their proportionate share of the expenses, including, for example, advisory and administrative fees, of the money market funds in which the AB Fund invests, such as advisory fees charged by the Manager to any applicable money market funds advised by the Manager. Shareholders also would be exposed to the risks associated with money market funds and the portfolio investments of such money market funds, including that a money market fund’s yield will be lower than the return that the AB Fund would have derived from other investments that would provide liquidity. |

| Temporary Defensive Strategy | |

| Please see “−Cash Management Investments” above. | The AB Fund may depart from its principal investment strategy by taking temporary defensive positions in response to adverse market, economic, political or other conditions. During these times, the AB Fund may not achieve its investment objective. When the AB Fund takes a defensive or interim position, its investments can include (i) obligations issued or guaranteed by the U.S. Government, its agents or instrumentalities; (ii) commercial paper rated in the highest short term category by a rating organization; (iii) domestic, Yankee and Eurodollar certificates of deposit or bankers’ acceptances of banks rated in the highest short term category by a rating organization; (iv) any of the foregoing securities that mature in one year or less (generally known as “cash equivalents”); (v) other short-term corporate debt obligations; (vi) repurchase agreements; or (vii) shares of money market funds, including money market funds advised by the Manager a sub-advisor. |

| | |

| Investment Advisor | |

| Sound Point Capital Management, L.P. | American Beacon Advisors, Inc. |

| Investment Sub-Advisor | |

| None | Sound Point Capital Management, L.P. |

Portfolio Managers

The following portfolio managers are jointly and primarily responsible for the day-to-day management of the Funds. |

| Stephen Ketchum is a Portfolio Manager and the Managing Partner and principal owner of Sound Point Capital, which he founded in 2008. Mr. Ketchum is a co-portfolio manager of the Sound Point Fund and was a co-portfolio manager of the Predecessor Fund. Prior to founding Sound Point Capital, Mr. Ketchum was Global Head of Media Investment and Corporate Banking for Banc of America Securities where he was a member of the Global Investment Banking Leadership Team. As Global Head of Media Banking, Mr. Ketchum was | Same. |

| responsible, together with a risk partner, for a multi-billion dollar portfolio of corporate loans and bonds, which was used to support investment banking activities. Prior to joining Banc of America Securities, he was a Managing Director at UBS in the TMT Investment Banking Group. Mr. Ketchum earned his B.A., magna cum laude, from New England College in 1983 and an M.B.A. from the Harvard Business School in 1990. Mr. Richert has been at Sound Point Capital since May 2011, and is co-portfolio manager for the Fund. He was a co-portfolio manager of the Predecessor Fund. Prior to joining Sound Point Capital, Mr. Richert was a Principal in the collateralized loan obligation (“CLO”) group at American Capital where for four years, he served as a senior member of a team managing $725 million in bank loan assets. His primary role was managing the cash flow CLO and directly covered over 40 names in the Aerospace & Defense, Building Materials, Chemical, Electronics, Metals & Mining and Oil & Gas industries. Prior to American Capital, Mr. Richert was a Senior Credit Analyst at Sanno Point Capital Management, a credit-focused hedge fund, where he covered Home Builders, Metals & Mining, TMT, and Drug Store Retailers. Mr. Richert earned his M.B.A. in Finance from the University of Michigan and his B.B.A in Accounting from Southern College. Mr. Richert is a Chartered Financial Analyst charterholder and is a Certified Public Accountant. | |

| E. | COMPARISON OF PRINCIPAL RISKS |

Risk is the chance that you will lose money on your investment or that it will not earn as much as you expect. In general, the greater the risk, the more money your investment can earn for you and the more you can lose. Like other investment companies, the value of each Fund’s shares may be affected by its investment objectives, principal investment strategies and particular risk factors. The principal risks of investing in the Funds are discussed below. However, other factors may also affect each Fund’s NAV. There is no guarantee that a Fund will achieve its investment objectives or that it will not lose principal value.

The main risks of investing in the Funds are similar, as their investment objectives are identical and the investment strategies of the Funds are substantially identical. However, the AB Fund has included certain additional risk disclosures and eliminated or revised other risk disclosures in its registration statement to clarify for shareholders the principal risks of investing in the AB Fund. The additional risks included in the AB Fund prospectus include callable securities risk, floating rate securities risk, liquidity risk, loan interests risk, investment risk, issuer risk, redemption risk, sector risk, U.S. Government securities

and government sponsored enterprises risk and unrated securities risk. The AB Fund prospectus also discloses the risks associated with investments in investment companies, including money market funds. The AB Fund prospectus does not disclose inflation risk and lender liability and equitable subordination risks, which are discussed in the Sound Point Fund’s prospectus. The risks of the AB Fund, as described in the AB Fund’s prospectus, are described below:

Callable Securities Risk

The AB Fund may invest in fixed-income securities with call features. A call feature allows the issuer of the security to redeem or call the security prior to its stated maturity date. In periods of falling interest rates, issuers may be more likely to call in securities that are paying higher coupon rates than prevailing interest rates. In the event of a call, the AB Fund would lose the income that would have been earned to maturity on that security, and the proceeds received by the Fund may be invested in securities paying lower coupon rates. Thus, the AB Fund’s income could be reduced as a result of a call. In addition, the market value of a callable security may decrease if it is perceived by the market as likely to be called, which could have a negative impact on the AB Fund’s total return.

Credit Risk

The AB Fund is subject to the risk that the issuer or guarantor of a debt security or the counterparty to a derivatives contract or a loan will fail to make timely payment of interest or principal or otherwise honor its obligations or default completely. The strategies utilized by the Sub-Advisor require accurate and detailed credit analysis of issuers and there can be no assurance that its analysis will be accurate or complete. The AB Fund may be subject to substantial losses in the event of credit deterioration or bankruptcy of one or more issuers in its portfolio. Financial strength and solvency of an issuer are the primary factors influencing credit risk. In addition, inadequacy of collateral or credit enhancement for a debt instrument may affect its credit risk. Credit risk may change over the life of an instrument and debt obligations which are rated by rating agencies may be subject to downgrade. The credit ratings of debt instruments and investments represent the rating agencies’ opinions regarding their credit quality and are not a guarantee of future credit performance of such securities. Rating agencies attempt to evaluate the safety of the timely payment of principal and interest (or preferred dividends) and do not evaluate the risks of fluctuations in market value. The ratings assigned to securities by rating agencies do not purport to fully reflect the true risks of an investment. Further, in recent years many highly rated structured securities have been subject to substantial losses as the economic assumptions on which their ratings were based proved to be materially inaccurate. A decline in the credit rating of an individual security held by the AB Fund may have an adverse impact on its price and make it difficult for the AB Fund to sell it. Rating agencies might not always change their credit rating on an issuer or security in a timely manner to reflect events that could affect the issuer’s ability to make timely payments on its obligations. Credit risk is typically greater for securities with ratings that are below investment grade. Since the AB Fund can invest significantly in lower-quality investments considered speculative in nature, this risk will be substantial.

Floating Rate Securities Risk

The interest rates payable on certain fixed income securities in which the AB Fund may invest are not fixed and may fluctuate based upon changes in market rates. The interest rate on a floating rate security is a variable rate which is tied to another interest rate, such as a money-market index or Treasury bill rate. Additionally, such securities are subject to interest rate risk and may fluctuate in value in response to interest rate changes if there is a delay between changes in market interest rates and the interest reset date

for the obligation, or for other reasons. Floating rate securities are less effective at locking in a particular yield and are subject to credit risk.

High Portfolio Turnover Risk