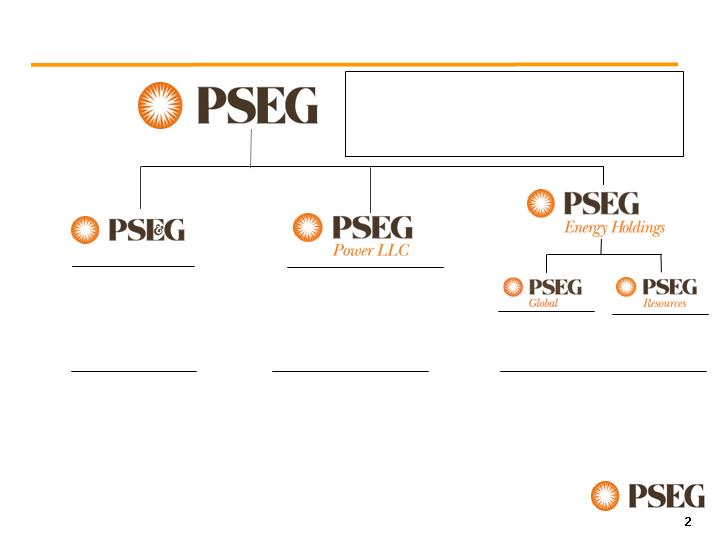

PSEG Overview

Electric Customers: 2.1M

Gas Customers: 1.7M

Nuclear Capacity: 3,500 MW

Total Capacity: 13,600 MW*

Traditional T&D

Leveraged

Leases

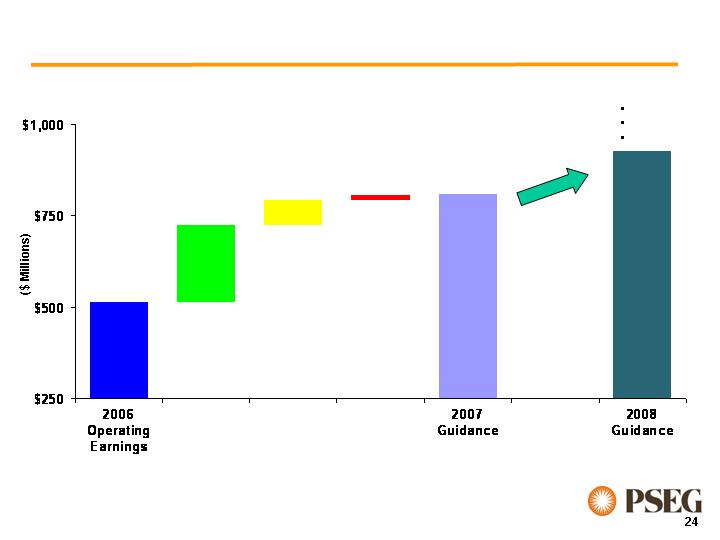

2007E Operating Earnings(4) : $1,170M - $1,295M

2007 EPS Guidance(4) : $4.60 - $5.00

Assets (as of 12/31/06): $28.6B

Market Capitalization (as of 2/23/07): $18.9B

Domestic/Int’l

Energy

Regional

Wholesale Energy

Operating Earnings = Earnings Available and Excludes:

(1) Merger Costs of $1M

(2) Loss from Discontinued Operations of $239M

(3) Loss on Sale of RGE of $178M and Income from Discontinued Operations of $226M

Includes Operating Earnings from Global of $166M, Resources of $63M and Energy Holdings of ($2M)

(4) Includes the parent impact of $(50-60)M

*After sale of Lawrenceburg

2006 Operating Earnings: $262M(1) $515M(2) $227M(3)

2007 Guidance: $330M - $350M $770M - $850M $130M - $145M

Operations

PSE&G consistently demonstrates top reliability performance

Significant improvement in nuclear operations

Regulatory

PSE&G settlement demonstrates return to constructive environment

Environmental – achieved NJ coal settlement

Energy Markets

Power benefiting from higher prices and lower risk through forward hedges

Utility customers benefit from staggered BGS – another auction complete

Financial

International – reduced exposure, improved stability

Improving cash flows and credit measures

Strong earnings growth in 2007 and 2008

We have made steady progress across a variety of areas.

Our objective is to build on these results to make a

strong company even stronger.

Much has been accomplished since the termination of

the merger…

September 2006

October

November

December

January 2007

9/14 – Merger

Termination

Announced

11/16–

PSE&G named

America’s Most

Reliable Electric

Utility

11/9 –

PSE&G Rate

Settlements

12/20– PSEG resumes direct

management of Nuclear stations

and Exelon’s senior management

team joins PSEG.

11/30- PSEG

Power Consent

Decree

1/31 - Operating Earnings at

upper end of guidance;

Confirmed strong ’07-’08

outlook; Improved Balance

Sheet

9/25 –

CEO

Succession

Announced

Regulatory

Operations

Management

Financial /

Asset

Rationalization

12/7 –

New Senior Team

Announced

1/16 –

Dividend

Increase

Organizational Design

& Staffing in progress

12/31 – Achieved

96% annual

nuclear capacity

factor

February

1/2 – Sale of

Lawrenceburg

announced

2/22 –

Election of

Chairman

and CEO

Power

Re-contracting &

Higher Margins

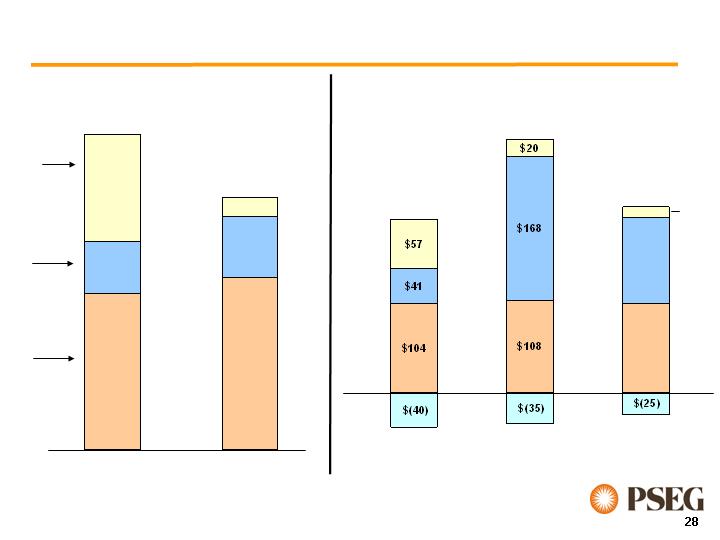

$.22

Depreciation,

Interest & Other

$.06

O&M $.03

Nuclear Operations

$.02

BGSS ($.11)

Turbine Impairment

($.10)

New Assets ($.06)

NDT ($.05)

MTM ($.05)

Shares O/S ($.01)

PSE&G

O&M & Other

$.02

Transmission

$.02

Demand $.02

Effective Tax

Rate $.02

Weather ($.06)

Expiration of

Depreciation

Credit ($.03)

4Q 2006

Operating

Earnings**

4Q 2005

Operating

Earnings*

*Excludes Merger Costs ($.02), Cumulative Effect of a Change in Accounting Principle ($.07) and Discontinued Operations ($.02)

**Excludes Discontinued Operations ($.87)

Holdings

Lower taxes $.08

Lower Interest &

Other $.04

Gain on sale of

Seminole lease in

2005 ($.18)

TIE – MTM &

Operations ($.08)

RGE Sale ($.04)

Turboven

Impairment ($.02)

Enterprise

Interest

Savings $.01

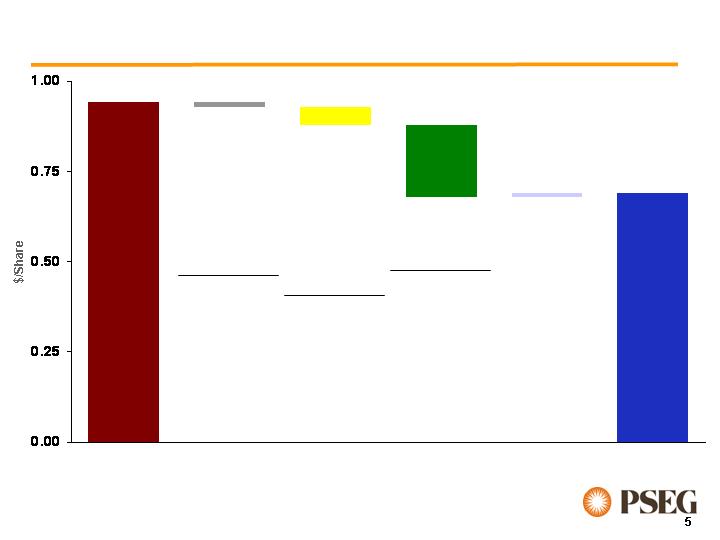

4Q 2006 Results - Earnings Variance

$0.94

(.01)

(.05)

(.20)

.01

$0.69

2006 Results - Earnings Variance

Power

Re-contracting &

Higher Margins

$.84

Nuclear

Operations $.20

Depreciation,

Interest & Other

$.04

New Assets ($.23)

BGSS ($.22)

NDT ($.13)

Turbine

Impairment ($.10)

Shares O/S ($.07)

Environmental

Reserve ($.06)

O&M ($.06)

PSE&G

Transmission

$.06

Other $.01

Weather ($.19)

Expiration of

Depreciation

Credit ($.15)

O&M ($.04)

Depr./Amort.

($.04)

Shares O/S

($.03)

2006

Operating

Earnings**

2005

Operating

Earnings*

Holdings

Texas Ops $.21,

including MTM of

$.13

Lower Interest &

Taxes $.18

2005 UAL Write-

off $.05

FX Gains/Losses

$.03

Prior Year Gains:

Eagle Point,

Seminole,

SEGS, MPC

($.31)

RGE Sale ($.06)

Turboven

Impairment

($.02)

Enterprise

Interest

Savings $.03

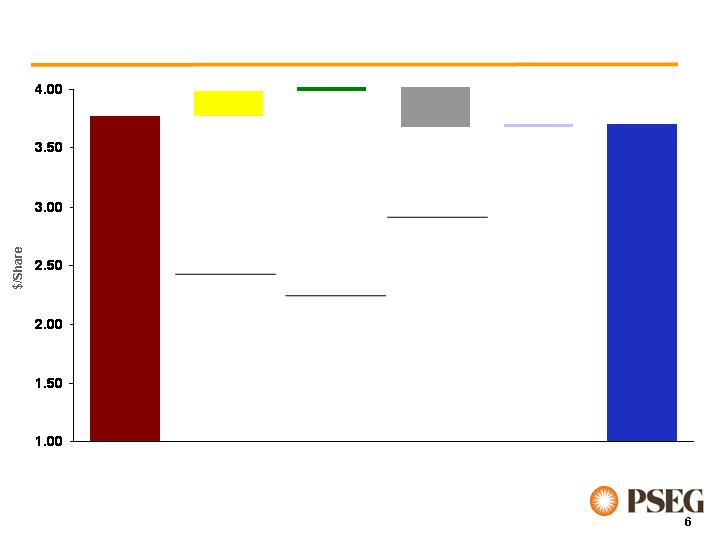

.21

.08

(.38)

.03

$3.77

$3.71

*Excludes Merger Costs ($.14), Cumulative Effect of a Change in Accounting Principle ($.07) and Discontinued Operations ($.85) &nb sp;

**Excludes Merger Costs ($.03), Loss on Sale of RGE ($.70) and Discontinued Operations ($.05)

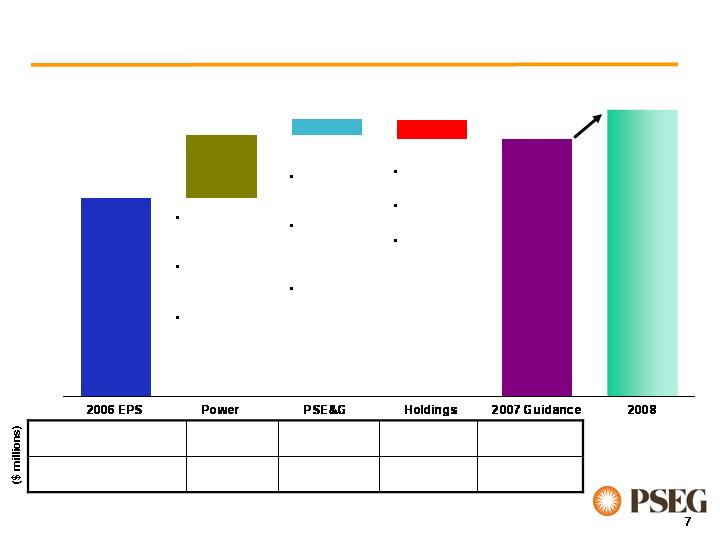

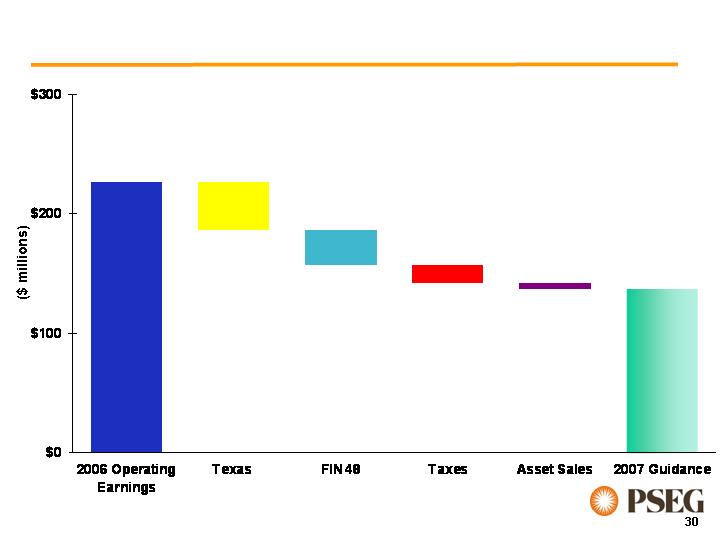

PSEG 2007 Earnings Outlook & Drivers

$3.71

Excess of

10% Growth

Forward

Hedging

Re-contracting

- PJM/NE

Capacity

Market Design

Gas Rate

Case

Electric

Financial

Review

Weather

Texas

Asset Sales

New

Accounting

Standard

Increase/(Decrease) vs.

2006 Operating Earnings

2007 Forecast Operating

Earnings Ranges

$232 - $357

($97) – ($82)

$68 - $88

$255 - $335

$1170 - $1295

$130 - $145

$330 - $350

$770 - $850

$4.60 - $5.00

2006

Operating

Earnings:

$938M*

*Excludes Loss on Sale of RGE of $178M ($.70 per share), Merger Costs of $8M ($.03 per share) and Loss from Discontinued

Operations of $13M ($.05 per share)

PSE&G

PSE&G Overview

2.1M electric customers

1.7M gas customers

2,600 sq miles in service territory

Electric

Distribution

$3.2B

Gas

Distribution

$2.1B

Electric

Transmission

$0.7B

Rate Base

(As of December 31, 2006)

Capital Structure

(As of December 31, 2006)

Total Long-

term Debt*

49%

Total

Common

Equity

50%

*Excludes Securitization Debt

Preferred

Stock

1%

Fair outcome on recent gas and electric cases will

help ensure…

Settlement agreement with BPU staff, Public Advocate, and other parties

Gas Base Rate case provides for $79M of gas margin

$40M increase in rates

$39M decrease in non-cash expenses

Electric Distribution financial review provides $47M of additional annual

revenues

Base rates remain effective at least until November 2009

New Jersey regulatory climate providing a fair return to investors

Opportunity to earn a ROE of 10%

…our continued ability to provide safe, reliable service

to customers and fair returns to shareholders.

Rate relief and normal weather…

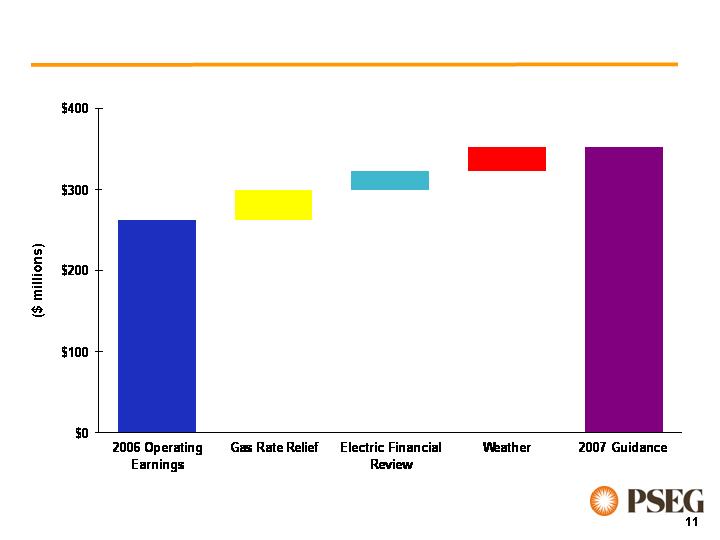

$262M

$30M - $40M

$20M - $25M

$330M

to

$350M

$20M - $30M

… provide opportunity to earn allowed returns.

*

*Excludes $1M of Merger Costs

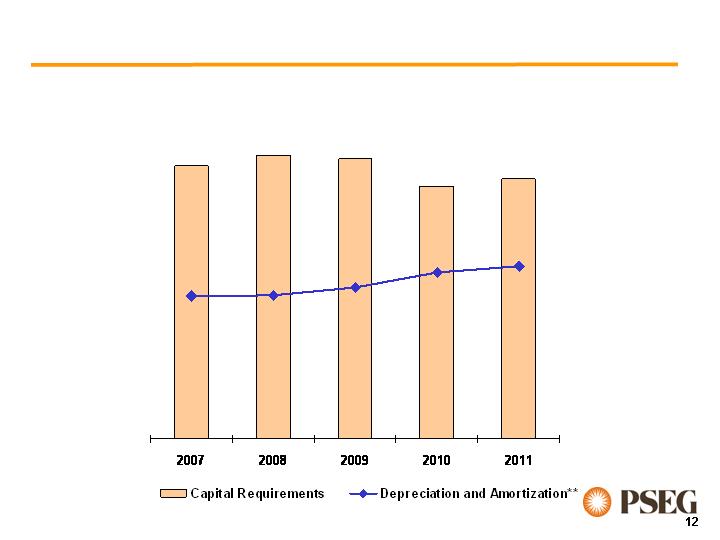

$605

$628

$631

$560

$575

PSE&G Capital Requirements*

(2007 – 2011)

($ Millions)

*Excludes impact of NJ Energy Master Plan; Reflects completion of infrastructure improvement projects by 2010

**Excludes Securitization

PSE&G’s capital program supports current plans

Looking Forward PSE&G…

Is committed to meeting customer needs and expectations

Continues to invest in its assets for the future

Distribution System Reinforcements

Transmission Investments

Customer Service

Supports NJ’s Energy Master Plan process, which may

create opportunities for additional investments

Advanced Metering, Solar Installations/other renewables and Energy

Efficiency

Endeavors to maintain constructive regulatory relations

PSEG Power

PSEG Power Overview

Diverse asset mix mitigates risk

and provides strong returns

13,600* MW of nuclear, coal, gas,

oil and hydro facilities

Low-cost portfolio

Strong cash generator

Regional focus with demonstrated

BGS success

Assets favorably located

Many units east of PJM constraint

Southern NEPOOL/Connecticut

constraint

Near customers/load centers

Integrated generation and portfolio

management optimizes asset-

based revenues

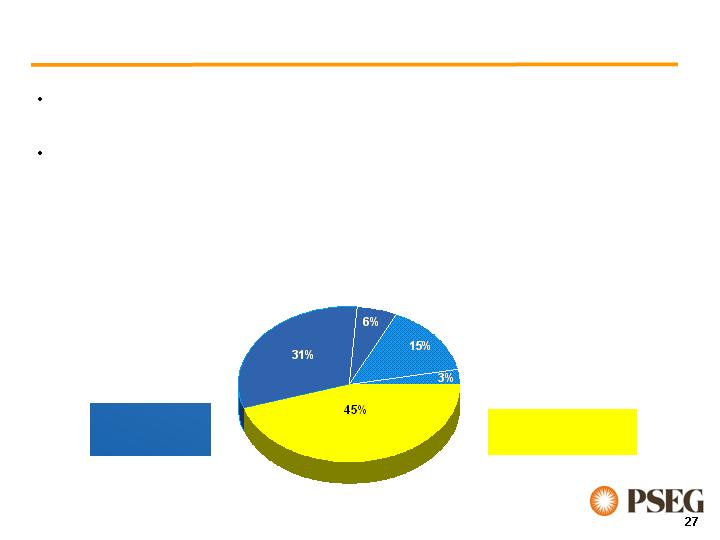

18%

47 %

8 %

26 %

Fuel Diversity – 2007*

Coal

Gas

Oil

Nuclear

Pumped

Storage

1%

(MWs)

* After sale of Lawrenceburg

Energy Produced - 2006

(MWhrs)

55%

27%

16%

Oil 1%

Pumped

Storage

1%

Nuclear

Coal

Gas

Total MWhrs: 53,617

*Uprate of 127MW scheduled for Fall 2007

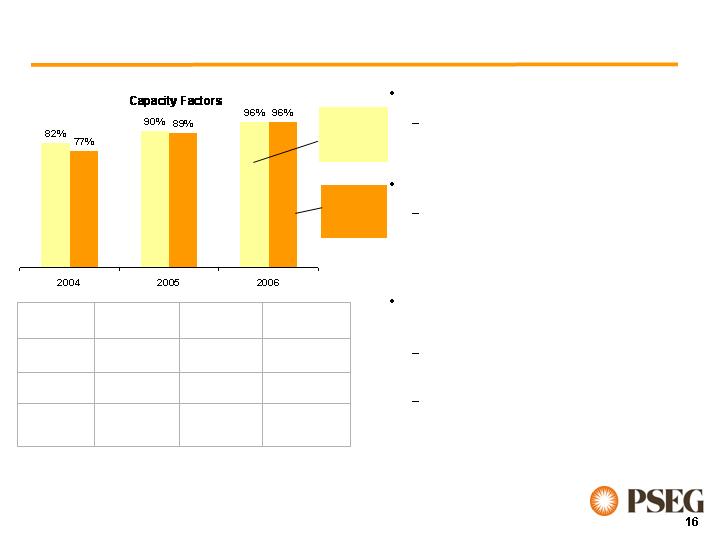

Strong operational performance

Capacity factors: Year-end ~96%

Summer ~100%

Outage management

Site records achieved, including most

recent 21 day refueling outage at

Salem 2

Nuclear Operating Services

Agreement (NOSA)

PSEG resuming direct management of

Salem and Hope Creek

Exelon’s senior management team has

joined PSEG

Hope Creek*

Salem

1 & 2

Peach Bottom

2 & 3

PSEG MW

Owned

1,061 MW*

1,323 MW

1,112 MW

Ownership

PSEG Owned

Jointly Owned

Jointly Owned

Operations

PSEG

Operated

(NOSA)

PSEG

Operated

(NOSA)

Exelon

Operated

Total

Fleet:

3,496 MW

Strong Nuclear Operations

NJ Fleet:

2,384 MW

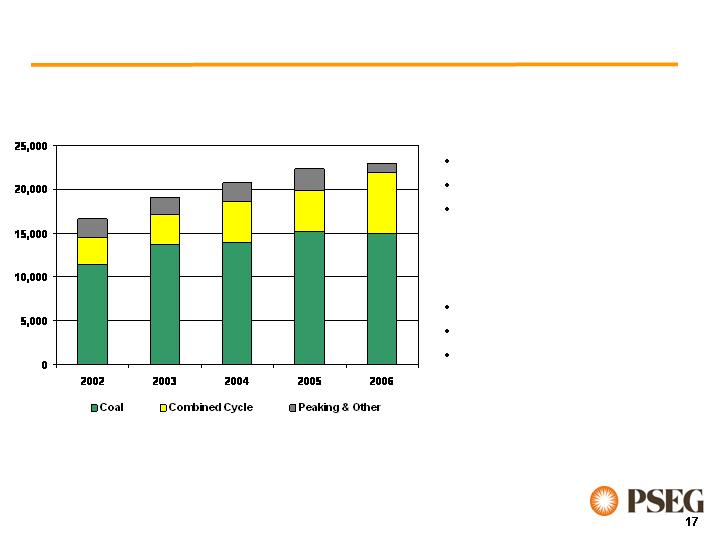

Strong Fossil Operations round out a diverse portfolio…

Total Fossil Output (Gwh)

A Diverse 10,000 MW Fleet

2,400 MW coal

3,200 MW combined cycle

4,400 MW peaking and other

Strong Performance

Continued growth in output

Improved fleet performance

Achieved resolution regarding

Hudson / Mercer

…in which over 80% of fleet output is from low cost coal

and nuclear facilities.

Our Environmental Strategy…

$451

$703

2007 – 2010

Total

2010

$83

$110

$132

$126

Mercer

2010

$263

$229

$143

$68

Hudson Unit 2

Completion

Date

2010

2009

2008

2007

PSEG Power Environmental Capital Requirements

($ Millions)

*PSEG Fossil to notify USEPA and NJDEP by end of 2007 on decision to install emissions controls at Hudson Unit 2

…will help preserve the availability of our fossil fleet.

Emissions Control Technology Projects

- NOx control – SCR

- SO2 control – Scrubber

- Hg and particulate matter control - Baghouse

Hudson Unit 2* (608 MW)

NOx control – SCR installation complete

SO2 control – Scrubbers

Hg and particulate matter control – Baghouse

Mercer (648 MW) – Units 1&2

Strengthening of capacity market design…

PSEG Power

PJM

NY

NE

Total Capacity 13,600MW*

(1,500 MW under RMR)

…provides meaningful market signals, and enhances expected

margin for Power’s generating fleet.

January 2008

2010 – 2011

October 2007

2009 – 2010

July 2007

2008 – 2009

April 2007

2007 – 2008

Auction Date

Planning Year

New England

Forward Capacity Market (FCM) began 12/1/06

Transition period prices have been established

Grows from $37/kw-yr to $49/kw-yr through 2010

First auction scheduled in 2008 for June 2010 delivery

PJM

FERC Approved 12/22/06

Locational pricing

4 zones initially, 23 in 2010

Anticipated implementation 6/1/07

Auction schedule:

*After sale of Lawrenceburg

The 1st RPM-year spans June 2007 through May 2008, and will

cover similar one year (BGS) intervals thereafter. Recent market

activity has shown considerable price increases for the

2007/2008 year.

PJM’s Reliability Pricing Model

RPM reflects a change in

market design

- More structured, forward-

looking, transparent pricing model

- Gives prospective investors in

new generating facilities more

clarity on future value of capacity

- Sends pricing signal to

encourage expansion of capacity

where needed for future market

demands

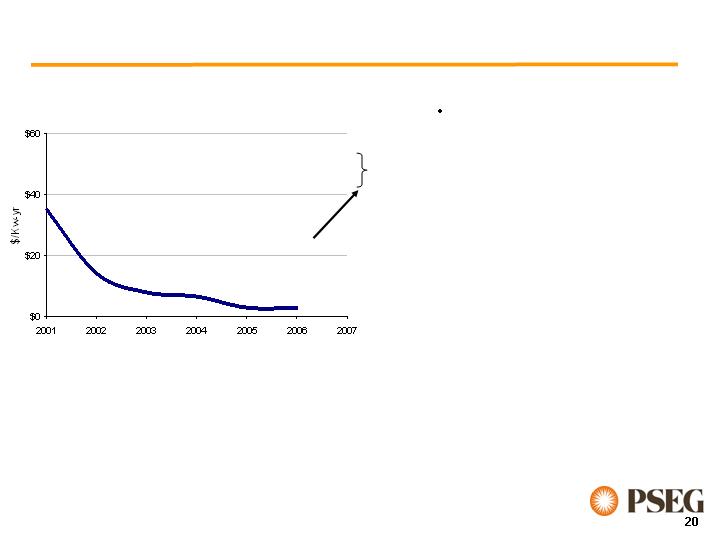

Capacity revenues, driven by RPM, provide a meaningful increase in

Power’s expected margin - $100 - $150 million for 2007 - and is anticipated

to increase in future years due to full year PJM impact and as more capacity

comes off existing contracts.

Capacity Prices

2007

Range

Fall 2006

Increase of

recent prices

for ’07 – ’08

year

20,000

4,000

8,000

12,000

16,000

2002

2003

2004

2005

2006

2007

2008

2002 FP

Auction

1 Year

170

Tranches

2003 FP

Auction

10

months

104

Tranches

2003 FP Auction

34 months

51 Tranches

2004 FP

Auction - 1 Yr.

50 Tranches

2004 FP Auction - 3 Years

51 Tranches

2006 FP Auction Load

54 Tranches

2005 FP Auction Load

50 Tranches

2007 FP Auction Load

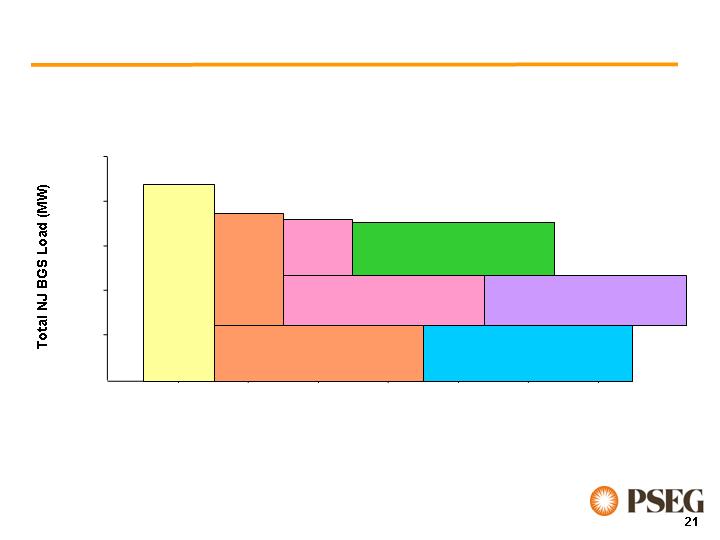

New Jersey BGS Auction Structure

The BGS structure in New Jersey successfully mitigates

risk for both suppliers and for customers.

51 Tranches

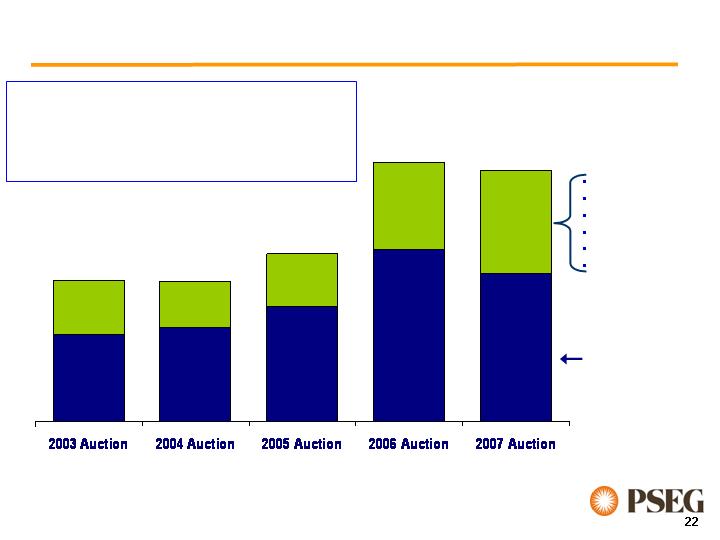

Market Viewpoint - BGS Auction Results

Capacity

Load shape

Transmission

Congestion

Ancillary services

Risk premium

Full Requirements

Round the Clock

PJM West

Forward Energy

Price

$33 - $34

$36 - $37

$55.59

$55.05

$65.91

$44 - $46

~ $21

~ $18

~ $21

$102.21

$67 - $70

~ $32

Increase in Full Requirements Component Due to:

Increased Congestion (East/West Basis)

Increase in Capacity Markets/RPM

Volatility in Market Increases Risk Premium

$98.88

~ $41

$58-$60

Power has been a successful participant in each BGS auction.

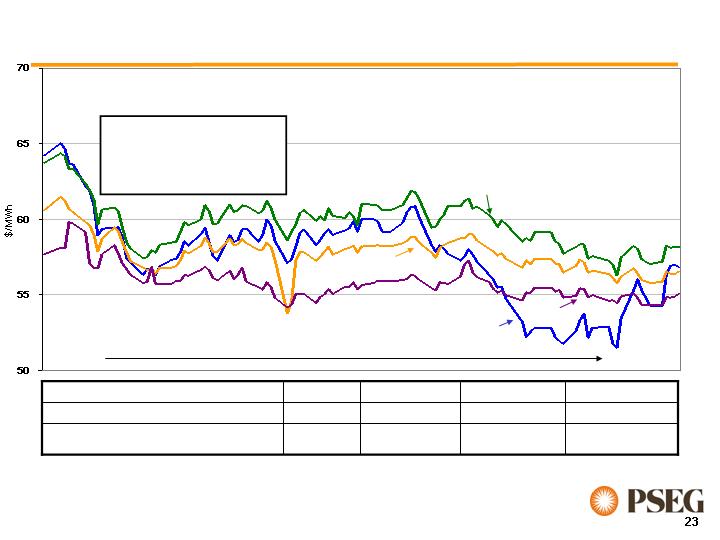

Strong electric prices support growth in margins…

…as Power secures a stable revenue stream through a

strategy of forward hedging

Average PJM West RTC Price

2006 = $50/MWh

2005 = $60/MWh

2004 = $42/MWh

2003 = $38/MWh

Sep ‘06

Feb ‘07

2007

2008

2009

2010

Calendar Forward Prices - PJM West RTC

$0.85 - $1.20

$0.45 - $0.80

$0.01 - $0.10

Estimated impact of $10/MWh PJM West RTC

price change*

0 – 20%

35 – 50%

90 – 100%

~100%

Percent of coal and nuclear energy output hedged

2010

2009

2008

2007

*Assuming normal market dynamics

The year over year improvements…

Energy

Capacity

Other

…drive growth in PSEG’s 2007 earnings guidance

with further improvements in 2008.

$515M*

Power drives 2008 earnings

guidance in excess of 10%

Full year of capacity pricing

Recontracting of BGS

Hope Creek uprate

$200M - $240M

$50M - $80M

$770M

to

$850M

$5M - $15M

* Excludes Loss from Discontinued Operations of $239M

Looking Forward PSEG Power…

Transitions its New Jersey nuclear plants to independent

operations

Moves forward to enhance environmental profile through

Consent Decree compliance

Anticipates energy markets to provide attractive growth

Energy hedges roll with increased margin

Capacity markets increasing – RPM auctions will provide visibility

Positions balance sheet for growth

PSEG Energy Holdings

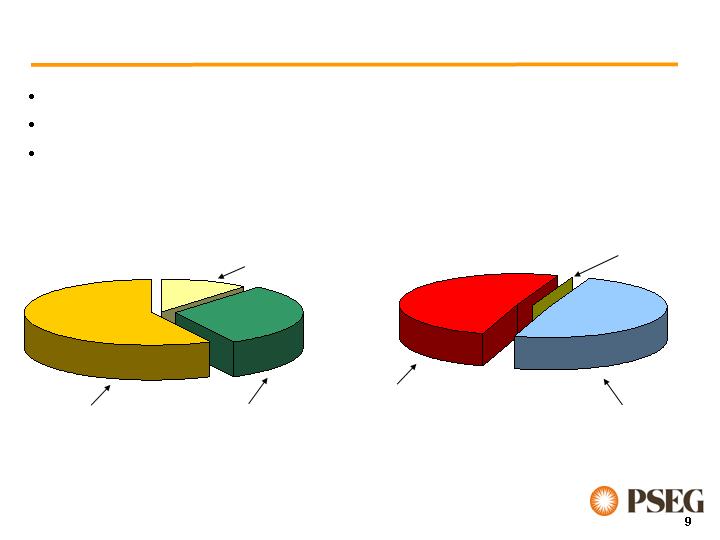

PSEG Energy Holdings Overview

Other Resources Investments

TOTAL ASSETS $6.2 B – 12/31/06

PSEG Global

Domestic

Generation

PSEG Resources

Leveraged Leases

Other International Generation

Chile & Peru

Distribution and

Generation

Two businesses with redirected strategy to maximize value of existing

investments

Balance and diversity: over 60 total investments; no single investment

more than 11% of Holdings assets

Improved risk profile by opportunistically reducing

capital invested in non-strategic assets…

…while increasing returns and sharpening focus on G&A.

2004

2006

$2.6B

$2.0B

Chile & Peru

US

Other

$900M

$400M

$1.3B

$160M

$500M

$1.4B

34%

16%

50%

8%

24%

68%

$296M**

48%

45%

2004

2006

2007 Est.

$202M**

$210M-$230M**

Composition of Global’s Pre-tax

Contribution by Region*

G&A

Chile

& Peru

US

Other

28%

20%

51%

6%

57%

37%

7%

Global’s Invested Capital

*Includes both consolidated and unconsolidated investments

**Excludes interest, taxes, G&A and other corporate items to arrive at Global’s Operating Earnings

Holdings has provided meaningful earnings and

cash flow…

…which has supported debt reduction and return

of capital to PSEG.

Asset

Sales

Cash Ops/

Cash on

Hand

Reduced

Debt

Return

Capital/

Dividends

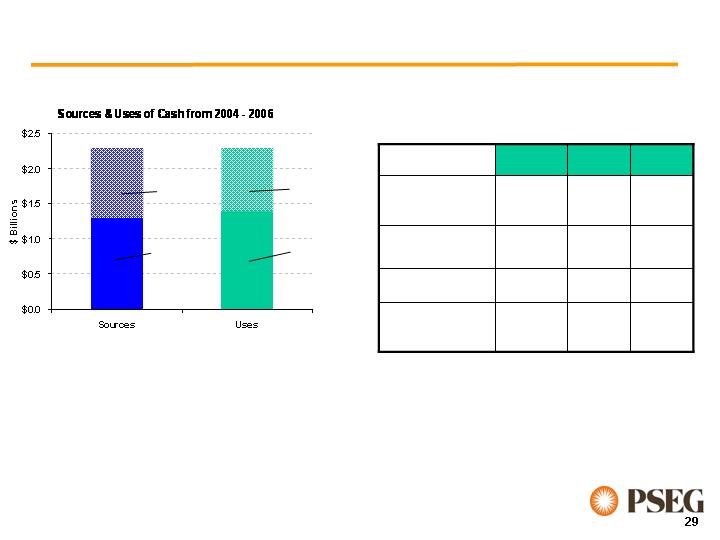

Significant de-capitalization

totaling $2.3B from 2004 -

2006

$609M

-

$311M

Net Debt

Reduction

47%

3.4x

$491M

2004

36%

41%

Recourse

Debt/Capital

4.5x

2.5x

FFO/Interest

$520M

$412M

Dividends & ROC

2006

2005

Debt Reduction & Dividends from 2004 - 2006

PSEG Energy Holdings – 2007 Drivers

$227M

$25M - $35M

$10M - $20M

$130M

to

$145M

$5M - $10M

$35M - $45M

*Excludes Loss on Sale of RGE of $178M and Income from Discontinued Operations of $226M

*

Looking Forward Energy Holdings…

Global’s Portfolio – Allocation of Invested Capital

Improved risk profile

Chile - Investment Grade; Peru - approaching

US – Texas is merchant; others are contracted

Stable earnings and cash distributions

Continue opportunistic monetization of non-strategic assets

Optimizes returns on Global’s current portfolio

Attractive market opportunities for Texas assets

Continue to seek increased returns in Chile and Peru

Other opportunities (eg. G&A)

Monitors Resources’ lease portfolio

Lessee credit risks exist, but have subsided

Current weighted average rating: A-/A3

Adoption of FIN 48 decreases earnings

Continue to monitor tax issues

Looking Forward PSEG…

Financial

Strength

We will focus on the basics of operational excellence...

…to produce financial strength that will be deployed

through disciplined investment.

Operational

Excellence

Disciplined

Investment

Strong earnings and cash flows will be used to

further de-lever the balance sheet.

Improving our credit profile will enable us to maximize

growth opportunities.

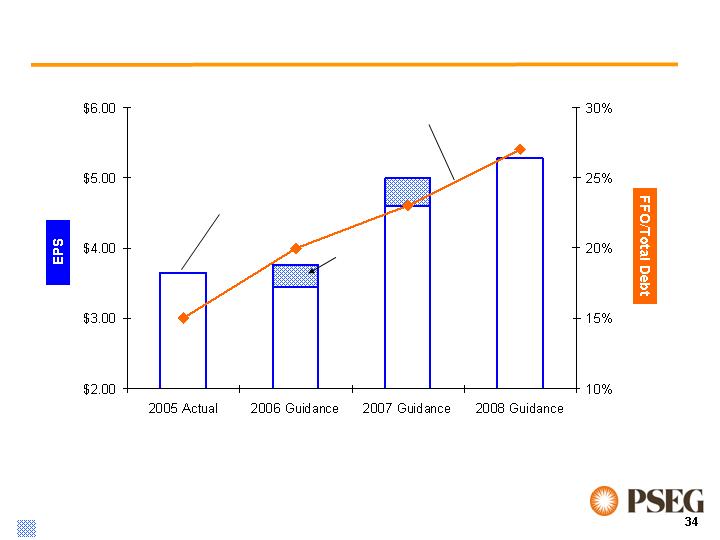

Excess

of 10%

Growth

FFO/

Total Debt

EPS

YE ‘06

EPS**:

$3.71

Guidance range: ’06: $3.45 - $3.75

’07: $4.60 - $5.00

YE ‘05

EPS*:

$3.77

*Excludes Merger Costs ($.14), Cumulative Effect of a Change in Accounting Principle ($.07) and Discontinued Operations ($.85) &nbs p;

**Excludes Merger Costs ($.03), Loss on Sale of RGE ($.70) and Discontinued Operations ($.05)

…and capitalize on multiple alternatives to grow the generation

and delivery business.

From a position of financial strength, we will make

disciplined investments…

Near-term:

Capitalize on opportunities for rate base growth

Distribution, transmission, customer service

Optimize our existing generation portfolio

Environmental improvements at NJ coal stations

Nuclear uprate

Continue to review Global’s portfolio

Focus on international investments

Longer-term:

Flexibility to pursue growth in core businesses and regions

PSE&G integrating with NJ Energy Master Plan initiatives

Advanced metering

Renewables

Demand side management

Power well positioned for growth in attractive Northeast markets

Strong and improving operations

Site expansion capability

Attractive cash flow

Consider a range of strategic alternatives

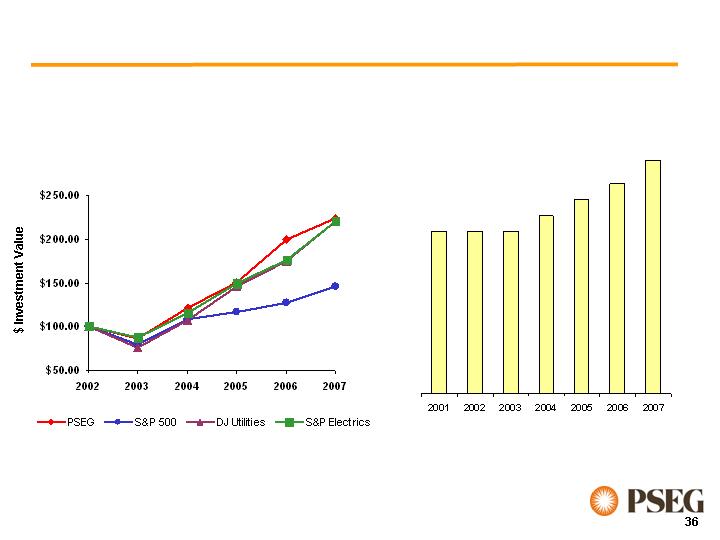

Creating Shareholder Value

5-Year Cumulative

Total Comparative Returns

(as of February 23, 2007)

Focused on producing superior shareholder return

Growing, Stable Dividends

(Annualized Quarterly Dividends)

$2.16

$2.20

$2.24

$2.28

$2.16

$2.16

$2.34