Public Service Enterprise Group

American Gas Association Financial Forum

Orlando, FL

April 30, 2007

Forward-Looking Statement

The statements contained in this communication about our and our subsidiaries’ future performance, including, without limitation, future revenues, earnings, strategies, prospects and all other statements that are not purely historical, are forward-looking statements for purposes of the safe harbor provisions under The Private Securities Litigation Reform Act of 1995. Although we believe that our expectations are based on information currently available and on reasonable assumptions, we can give no assurance they will be achieved. There are a number of risks and uncertainties that could cause actual results to differ materially from the forward-looking statements made herein. A discussion of some of these risks and uncertainties is contained in our Annual Report on Form 10-K and subsequent reports on Form 10-Q and Form 8-K filed with the Securities and Exchange Commission (SEC), and available on our website: http://www.pseg.com These documents address in further detail our business, industry issues and other factors that could cause actual results to differ materially from those indicated in this communication. In addition, any forward-looking statements included herein represent our estimates only as of today and should not be relied upon as representing our estimates as of any subsequent date. While we may elect to update forward-looking statements from time to time, we specifically disclaim any obligation to do so, even if our estimates change, unless otherwise required by applicable securities laws.

1

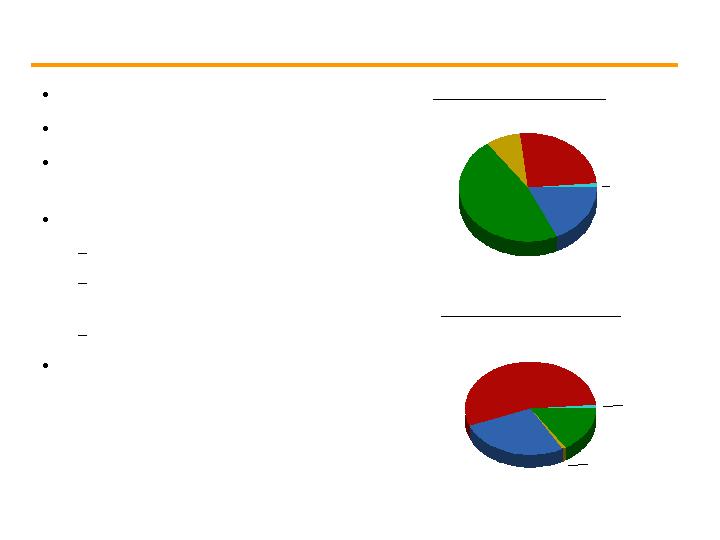

PSEG’s family of businesses combine the right set of

assets …

Domestic Generation

Regulated Transmission &

Distribution

- Domestic / International

T&D and Generation

- Leveraged Leases

… providing opportunity for growth in their respective markets.

2

The current business environment …

Convergence of market forces and policy

creates the need to address:

Critical infrastructure requirements

Environmental requirements

Capacity requirements in constrained markets

… creates opportunities for PSEG’s long-term growth.

3

Carbon Reduction – A common focus …

International directives

- More support globally since adoption of Kyoto Agreement in 1997 for

reduction in greenhouse gas

On the national level

Multiple carbon legislative proposals are currently under

consideration by Congress

Legislation probable by 2008

Regional Greenhouse Gas Initiative (RGGI)

A nine state collaborative calling for a 10% reduction in carbon from

2000 – 2004 levels by 2019

In New Jersey, Governor Corzine has signed Executive Order

No. 54 and the Legislature has introduced multi-sector carbon

legislation with aggressive reduction targets.

… an issue we support and an opportunity for investment

4

NJ Energy Master Plan …

Identifies the same issues as those at the international and national

levels

Provides PSEG the opportunity to:

Meet environmental goals that we have long supported

Expand PSE&G through broader investment opportunities

Support growth in the State’s urban areas through investment in the “Smart

Growth Initiative” program

Expand Power through carbon-free generation

Shape the debate, find the solution and implement the plan

PSEG has pledged its full support to the effort launched by Governor

Corzine

PSEG expects to implement several proposals during 2007 to support

the Energy Master Plan, consistent with PSEG’s business interests

… an Intersection of Energy – the Environment – PSEG

5

PSE&G – A consistent, strong performer …

Continued top quartile/top decile performance

National ReliabilityOne Award winner – two years running

American Customer Satisfaction Index (ACSI) Customer Satisfaction

Survey

Regulatory agreements provide opportunity to earn reasonable

returns over 2007-2009

Energy Master Plan initiatives fuel long-term growth

New customer information system investment (2007 - 2009)

Advanced Metering technology investment (2008 - 2012)

Renewables and energy efficiency enhanced by utility

participation (2008 – 2020)

… providing stability and multiple platforms for growth.

6

PSEG Power – Solidly positioned …

Nuclear and fossil fleet operating at historically high

levels with opportunity for improvement

Near-term growth fueled by strong markets and roll-off

of below market contracts

Long-term growth influenced by

Tightening reserve margins

Expansion capability at existing sites

Carbon advantaged portfolio

Debate on energy policy will influence investment

Environmental compliance driving current investment

Meeting EMP objectives may require a look at new nuclear

investment

… to provide strong growth for PSEG.

7

PSEG Energy Holdings - Improving returns and reducing

risk …

Diverse asset base with improved stability

Stable Latin American distribution assets in stable economies

Gas-fired combined cycle generation in Texas

A source of capital

Asset sales have reduced risk and contributed to an improved

balance sheet at PSEG

A source of growth

Texas generating assets benefit from location, low cost

structure and opportunity for expansion

… to create opportunities to redeploy capital.

8

Growth opportunities …

Achieve Credit Targets

Sustainable and Growing Dividend Increases

Operational Excellence Builds Financial Strength

… Near-Term, Long-Term, with Manageable Risk.

Manageable Risk

Strong Earnings from Existing Assets and Base Capital Plan

Share Repurchases and New Investment

Annual Excess Cash $500M

~

~

9

Improving returns on existing investments

Texas assets benefit from location and cost

Reasonable regulated returns

New Customer System

Transmission & Distribution expansion

NJ Smart Growth Initiative

Strong energy markets and contract repricing

Implementing capacity market mechanisms

Nuclear uprates

Environmental improvements preserve availability of

NJ coal stations

“Growth Opportunities Near-Term” are contributing to

earnings improvements …

… resulting in expected increases of 37% in 2007 and 15% in

2008.

10

Opportunity to leverage Texas position for new

acquisition / build.

Redeploy capital to Enterprise

EMP initiatives (energy efficiency, advanced

metering, renewables)

Generation value improvement (upward pressure on

capacity prices / heat rate expansion / carbon)

Growing markets (PJM, NY, NEPOOL)

Expansion capability at existing sites

Preliminary consideration of nuclear expansion

“Growth Opportunities Long-Term” are available to the

PSEG Family of Companies …

… to address infrastructure, environmental, and capacity

requirements.

11

Reshaped portfolio through asset sales

Continuing to evaluate capital invested internationally

Solid regulatory relations

Appropriate regulatory incentives for EMP investments

Established markets and mechanisms

Hedging strategy adds stability

Capacity auctions increases visibility of earnings

“Growth Opportunities with Manageable Risk” …

… adds stability to strong earnings and cash flow.

12

Right set of assets…

Large, diverse mix of low-cost, base-load, load-following generating assets

Reliable electric and gas distribution and transmission systems

Stable portfolio of investments in domestic generation, international distribution and leases

Right markets…

Generation assets operate in tightly constrained and growing markets

Nuclear and coal base-load capacity operate in markets where the price for power is set by

gas

Transmission and distribution assets provide service in a modest growth market with

reasonable regulation

At the right time…

Mid-Atlantic, New England and Texas recognizing the value of capacity in constrained areas

A move to control carbon benefits our nuclear-based fleet

Power has opportunity for brownfield development at existing sites

Values are improving for international assets

T&D set to benefit from implementing state’s energy plan

PSEG – Excellent position for today …

… ready for tomorrow

13

PSE&G

Review and Outlook

Positioned for growth in 2007 and beyond

Strong

Operations

Constructive

Regulatory and

Business

Environment

Positive Market

Fundamentals

Growth

Opportunities…

with Manageable

Risk

At or approaching top decile

performance in key operating measures

Reasonable rate case outcome

Valued partner on State policy

Constructive State policies with reasonable

prices to customers

Baseline capital growth of 4-5% in near-term

with State energy policy providing potential

for longer-term growth

15

PSE&G is favorably located …

Attractive market (NJ is ranked 3rd

nationally in personal income per capita)

National ReliabilityOne Award winner -

two years running

Solid regulatory relationships on

traditional utility matters

Reasonable returns and strong cash flow

3,169 M Therms

43,678 GWh

Electric Sales and

Gas Sold and

Transported

1.4%

1.7 Million

Gas

1.2%

2.1 Million

Electric

Projected Annual

Load Growth

2007 - 2011

Customers

11,108

Billing Peak (MW)

1,408

Network Circuit Miles

1.1%

Projected Annual

Load Growth

2007 - 2011

Electric and Gas Distribution Statistics (12/31/06)

Transmission Statistics (12/31/06)

… and is the largest transmission operator in “classic” PJM and the 11th

largest electric and gas distribution company in the nation (by customers).

N

E

W

S

N

E

W

S

COMBINED ELECTRIC &

ELECTRIC TERRITORY

KEY

:

COMBINED ELECTRIC &

GAS TERRITORIES

ELECTRIC TERRITORY

GAS TERRITORY

KEY

:

16

Fair outcome on recent gas and electric cases will help

ensure …

Settlement agreement with BPU staff, Public Advocate, and other

parties within weeks of merger failure

Gas Base Rate case provides for $79M of gas margin:

- $40M increase in rate

- $39M decrease in non-cash expenses

Electric Distribution financial review provides $47M of additional

annual revenues

Base rates remain effective at least until November 2009

New Jersey regulatory climate providing a fair return to investors

Opportunity to earn a ROE of 10%

… our continued ability to provide safe, reliable service to

customers and fair returns to shareholders.

17

Regulated electric transmission, electric and gas distribution system

Characteristics

FERC regulation for electric transmission; NJ BPU regulation for electric

and gas distribution

Electric and Gas distribution rates frozen through November 2009

PSE&G’s base investment plan …

Gas

Distribution

36%

Electric

Transmission

14%

Electric

Distribution

50%

Gas

Distribution

35%

Electric

Transmission

11%

Electric

Distribution

54%

2006 Actual

Rate Base = $6.0 B

2011 Base Plan

Rate Base = $7.5 B

Equity Ratio ~ 48%

… coupled with fair regulatory treatment provides a solid base

for future earnings growth.

PSE&G Rate Base

18

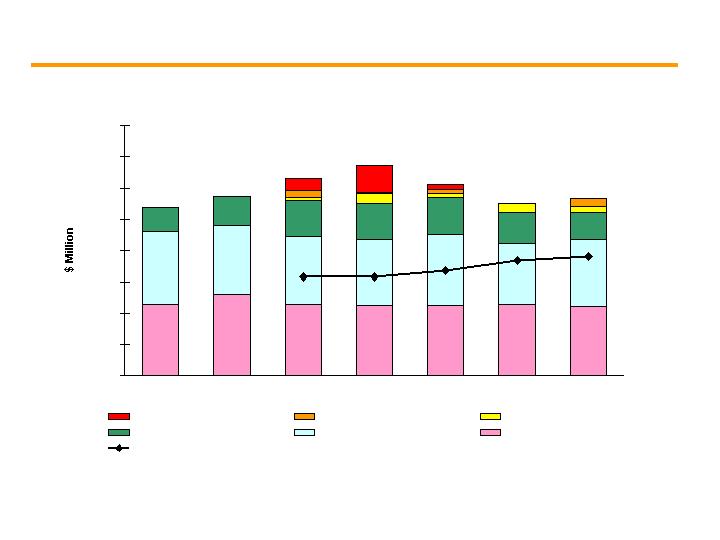

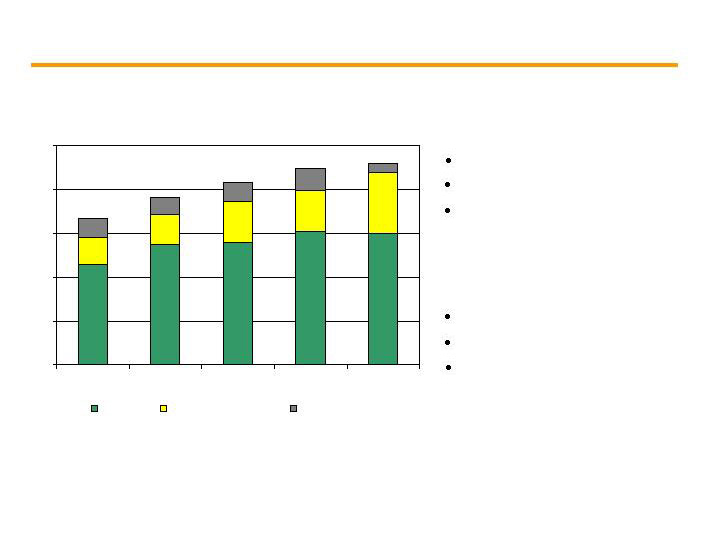

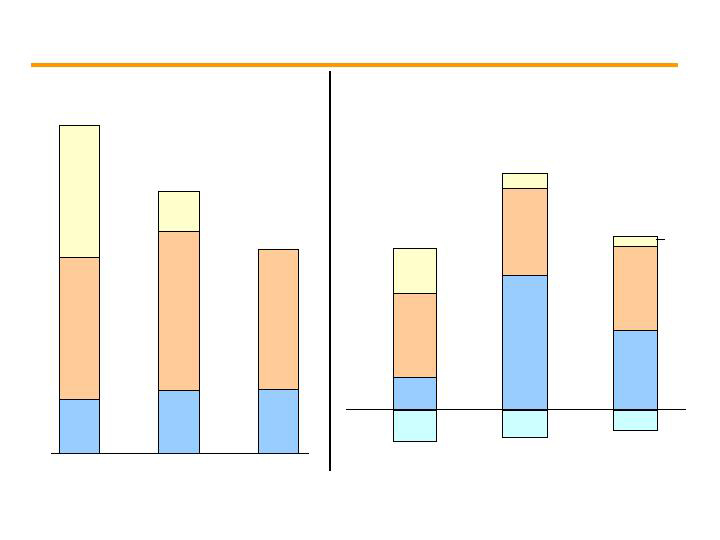

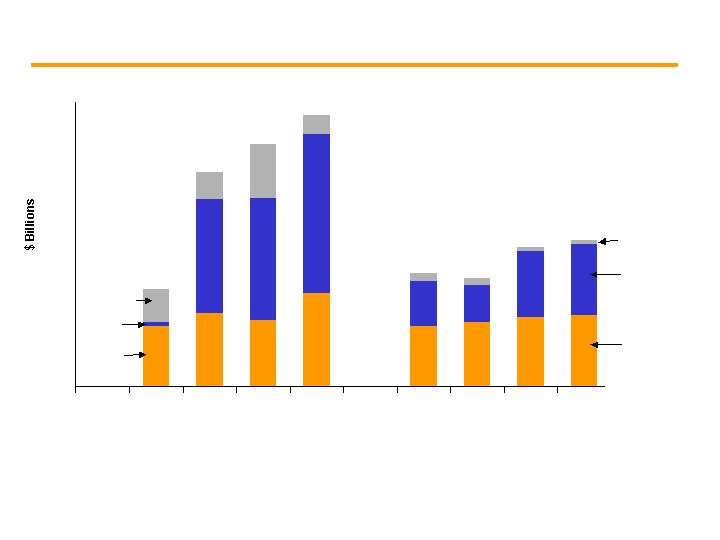

PSE&G’s capital program is supported by internally

generated cash …

PSE&G Base Capital Requirements*

(2005 – 2011)

*Excludes impact of NJ Energy Master Plan; Reflects completion of infrastructure improvement projects by 2010. Base CapEx is consistent with 10-K but includes adjusted amounts for ICSP project.

**Excludes Securitization

… and supports a payout ratio of more than 75% in the forecasted

period.

$630

$673

$611

$568

$538

$572

$551

$0

$100

$200

$300

$400

$500

$600

$700

$800

2005

2006

2007

2008

2009

2010

2011

ICSP

RTEP

Dist Reinforcement

Transmission

Gas

Electric

Depreciation & Amortization**

19

Three areas of additional potential growth for PSE&G …

T&D Expansion

Opportunities

PJM backbone transmission

and RTEP projects

Distribution System

Reinforcements

PSEG EMP Strategies

Renewables/Emissions

Strategies

Solar initiative

Greenhouse Gas Offset

Demand-Side Strategies

Advanced Metering

Infrastructure

Residential Energy Efficiency

Commercial and Industrial

Energy Efficiency

PSE&G Facility and System

Efficiency

Integrated Customer

System Platform (ICSP)

Leveraging State of the Art

Technology – SAP CCS

Improving capabilities to

implement strategic

functionality

Enabling GPS technology to

improve dispatching

Creating new opportunities

through web-based

empowerment

Moving to a platform with full

AMI capability

… have preliminary annual earnings impacts in the $25M-$150M

range by 2015.

Potential Range of Capital Spending:

$150M - $1.5B

$140M - $150M

$500M - $1.5B

Aggregate $500M - $3.0B

20

PSE&G’s Solar Initiative Plan filed with BPU on 4/19/07…

PSE&G would invest $100M over 2008-2009 to help finance installation of 30MW

of solar photovoltaic systems on homes, businesses and municipal buildings.

The solar initiative is designed to fulfill 50% of the renewable portfolio standard

(RPS) requirements over this two year period.

Program will provide loans to developers to cover 40-50% of the cost of solar

installation project. The remaining cost of the project will be funded by an equity

partner (or host customer) who would also own the solar panels.

PSE&G will be repaid the principal plus interest over 15 year period in the form of

credits called Solar Renewable Energy Certificates (SREC’s) in cash. PSE&G will

allocate SRECS to Load Serving Entities (LSE) which will lower their renewable

portfolio compliance cost standards over time.

PSE&G would earn a return for the full cost of capital plus an incentive for

spurring the solar market.

… first step to meeting Energy Master Plan requirements

21

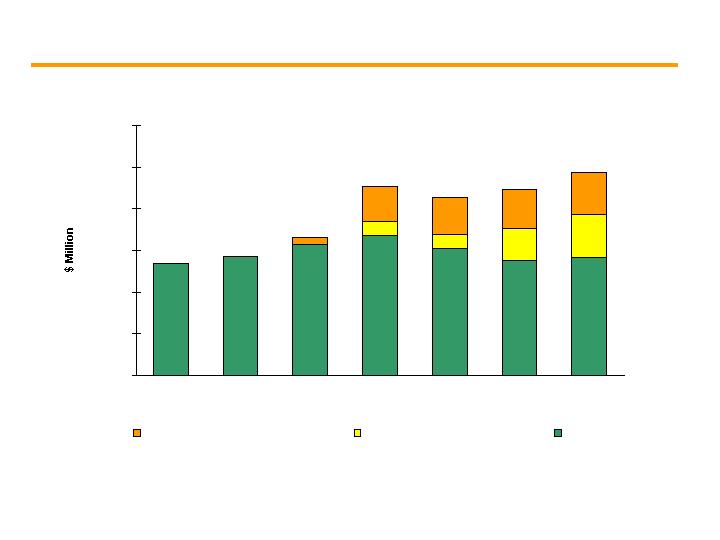

EMP and additional T&D investments …

$0

$200

$400

$600

$800

$1,000

$1,200

2005

2006

2007

2008

2009

2010

2011

Representative Potential EMP

Potential Incremental T&D

Base CapEx

Potential PSE&G Capital Requirements

(2005 – 2011)

… provide additional upside growth potential to our base plan.

22

In the near-term, rate relief and normal weather …

$0

$100

$200

$300

$400

2005 Operating

Earnings

2006 Operating

Earnings

Gas Rate Relief

Electric

Financial

Review

Weather/Other

2007

Guidance

2008

Expectations

$262M*

$30M - $40M

$20M - $25M

$340M

to

$360M

$28M - $33M

… provide opportunity to earn allowed returns.

*Excludes $3M and $1M of Merger costs in 2005 and 2006, respectively

ROE Range: 10.5% - 11.5%

Consistent

with 2007

Modest

Sales

Growth

Offset by

O&M

Increases

$347M*

23

Positioned for growth in 2007 and beyond …

Strong

Operations

Constructive

Regulatory and

Business

Environment

Positive Market

Fundamentals

Growth

Opportunities…

with Manageable

Risk

Approaching Top Decile Performance in Key Operating

Measures: CAIDI, SAIFI and Leak Response

National ReliabilityOne Award winner – two years

running

Rate Case result reasonable and received within weeks

of the merger failure

Attractive Market

Constructive state policies

Electricity and gas prices better than average of region

and less than 1990 levels on a “real” basis creating

superior value for customers.

Near Term Growth

RTEP

Distribution Reinforcement

ICSP

Long Term Growth

Incremental RTEP

Distribution Reinforcements

EMP and AMI

Manageable Risks

Regulatory Recovery at FERC and BPU

Competing Proposals in EMP

Proper Regulatory Incentives for EMP Investments

24

PSEG Power

Review and Outlook

Record production

Liquid markets structure and

stable NJ BGS model

Favorable energy and capacity

outlook

Strong

Operations

Constructive

Regulatory and

Business

Environment

Positive Market

Fundamentals

Growth

Opportunities…

with Manageable

Risk

Tightening reserve margin and site

expansion opportunities

Positioned for growth in 2007 and beyond …

26

Low-cost portfolio

Strong cash generator

Regional focus with demonstrated

BGS success

Assets favorably located

Many units east of PJM constraint

Southern NEPOOL/ Connecticut

constraint

Near customers/load centers

Integrated generation and portfolio

management optimizes asset-

based revenues

* After sale of Lawrenceburg

… which provides for risk mitigation and strong returns.

Power’s assets reflect a diverse blend of fuels and

technologies …

18%

47 %

8 %

26 %

Fuel Diversity – 2007*

Coal

Gas

Oil

Nuclear

Pumped

Storage

1%

Energy Produced - 2006

55%

27%

16%

Oil 1%

Pumped

Storage

1%

Nuclear

Coal

Gas

Total GWh: 53,617

Total MW: 13,600*

27

Operated by PSEG Nuclear

PSEG Ownership: 100%

Technology:

Boiling Water Reactor

Total Capacity: 1,061MW*

Owned Capacity: 1,061MW

License Expiration: 2026

Operated by PSEG Nuclear

Ownership: PSEG - 57%,

Exelon – 43%

Technology:

Pressurized Water Reactor

Total Capacity: 2,304MW

Owned Capacity: 1,323MW

License Expiration: 2016 and

2020

Operated by Exelon

PSEG Ownership: 50%

Technology:

Boiling Water Reactor

Total Capacity: 2,224MW

Owned Capacity: 1,112MW

License Expiration: 2033

and 2034

Hope Creek

Salem Units 1 and 2

Peach Bottom Units 2 and 3

Our five-unit nuclear fleet …

… is a critical element of Power’s success.

*Uprate of 125MW scheduled for fall 2007

28

82.3%

65.6%

92.0%

82.8%

92.6%

97.2%

50%

60%

70%

80%

90%

100%

Salem

Hope Creek

Capacity Factor

6.5%

20.2%

0.9%

7.6%

0.7%

0.4%

0%

6%

12%

18%

24%

Salem

Hope Creek

Forced Loss Rate

81.0

64.8

95.2

65.0

99.2

91.4

60

70

80

90

100

Salem

Hope Creek

INPO Index

80.2%

97.4%

84.7%

99.9%

99.8%

100.0%

50%

60%

70%

80%

90%

100%

Salem

Hope Creek

Summer Capacity Factor

… and corresponds directly with improved regulatory relations and

financial outcomes.

Improvement in nuclear performance can be seen in

numerous measures of operations ...

2004

2005

2006

29

0

5,000

10,000

15,000

20,000

25,000

2002

2003

2004

2005

2006

Coal

Combined Cycle

Peaking & Other

Total Fossil Output (GWh)

A Diverse 10,000 MW Fleet

2,400 MW coal

3,200 MW combined cycle

4,400 MW peaking and other

Strong Performance

Continued growth in output

Improved fleet performance

Achieved resolution regarding

Hudson / Mercer

… contribute to a low-cost fossil portfolio in which two-thirds of

fleet output is from coal facilities.

Strong Fossil operations …

30

-

1,000

2,000

3,000

4,000

5,000

6,000

2007

2008

2009

2010

Nuclear / Pumped Storage

Coal

CC

Steam / CT

Existing Load + Hedges + Future BGS

Existing Load + Hedges

Existing Hedges

2007

2008

2009

2010

… while preserving market growth opportunities.

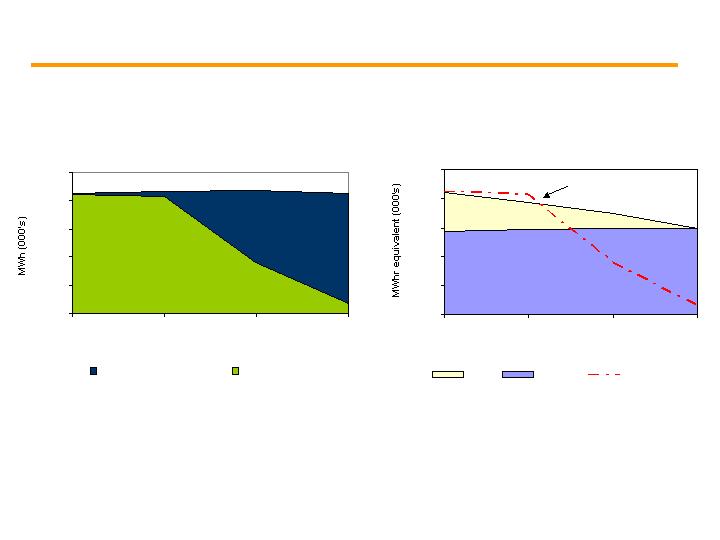

Power’s hedging strategy aims to balance stable

earnings …

0 – 20%

35 – 50%

90 – 100%

~100%

Percent of Power’s coal and nuclear energy output

hedged (total portfolio)

2010

2009

2008

2007

PJM RTC (GWh)

31

-

10,000

20,000

30,000

40,000

50,000

2007

2008

2009

2010

Year

Coal

Uranium

Contracted sales

… is aligned with its low-cost generating output and our hedging

strategies.

Power has contracted for 100% of its nuclear uranium fuel through 2011 and

approximately 70% of its coal needs through 2009.

Coal and Nuclear Fuel

Power’s hedging of coal and nuclear fuel …

Gas supply secured

based on sales of output

Coal and Nuclear Output

-

10,000

20,000

30,000

40,000

50,000

2007

2008

2009

2010

Year

Nuclear and Coal output

Contracted sales

32

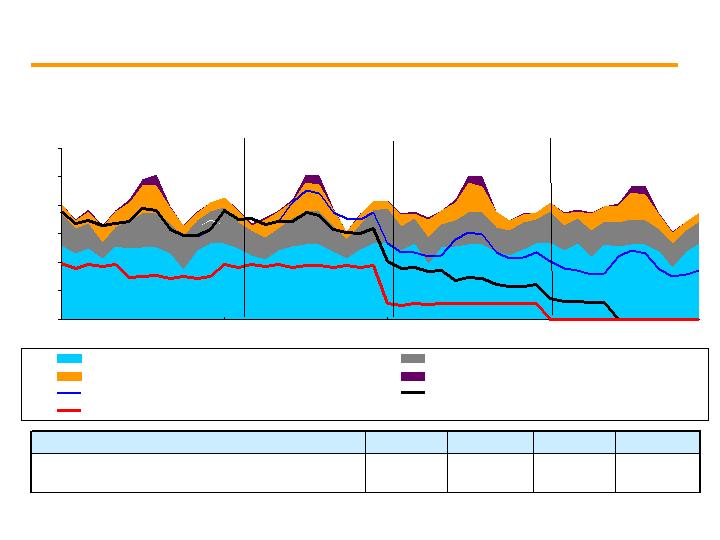

The New Jersey BGS auction successfully mitigates risk

for both suppliers and customers …

… and is a critical component to Power’s hedging strategy.

20,000

4,000

8,000

12,000

16,000

2002

2003

2004

2005

2006

2007

2008

2002 FP

Auction

1 Year

170

Tranches

2003 FP

Auction

10

months

104

Tranches

2003 FP Auction

34 months

51 Tranches

2004 FP

Auction - 1 Yr.

50 Tranches

2004 FP Auction - 3 Years

51 Tranches

2006 FP Auction Load

54 Tranches

2005 FP Auction Load

50 Tranches

2007 FP Auction Load

51 Tranches

New Jersey BGS - FP Auction

2009 2010

Note: 1 Tranche = ~100MW Peak

33

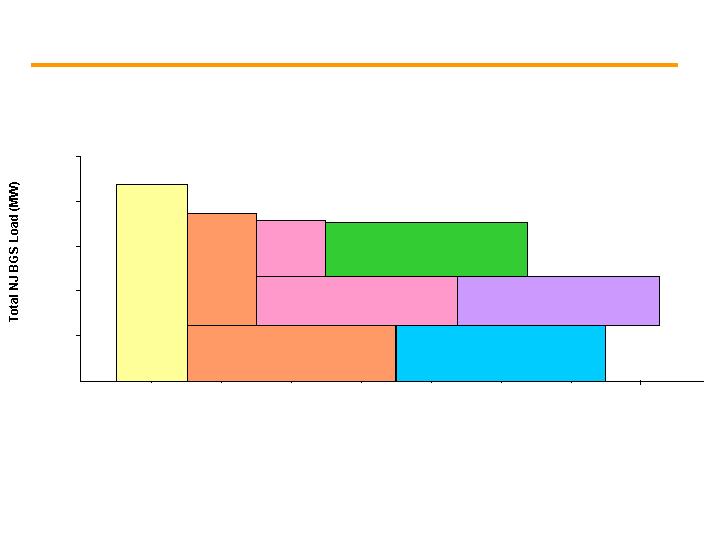

2003 Auction

2004 Auction

2005 Auction

2006 Auction

2007 Auction

Capacity

Load shape

Transmission

Congestion

Ancillary services

Risk premium

Full Requirements

Round the Clock

PJM West

Forward Energy

Price

$33 - $34

$36 - $37

$55

$55

$66

$44 - $46

~ $21

~ $18

~ $21

$102

$67 - $70

~ $32

Increase in Full Requirements Component Due to:

Increased Congestion (East/West Basis)

Increase in Capacity Markets/RPM

Volatility in Market Increases Risk Premium

$99

~ $41

$58-$60

Market Perspective – BGS Auction Results

… has enabled successful participation in each BGS auction.

Power’s fleet diversity and location ...

34

More structured, forward-

looking, transparent pricing

model

Gives prospective

investors in new

generating facilities more

clarity on future value of

capacity

Sends locational pricing

signal to encourage

expansion of capacity

where needed for future

market demands

… in which longer-term price signals are provided.

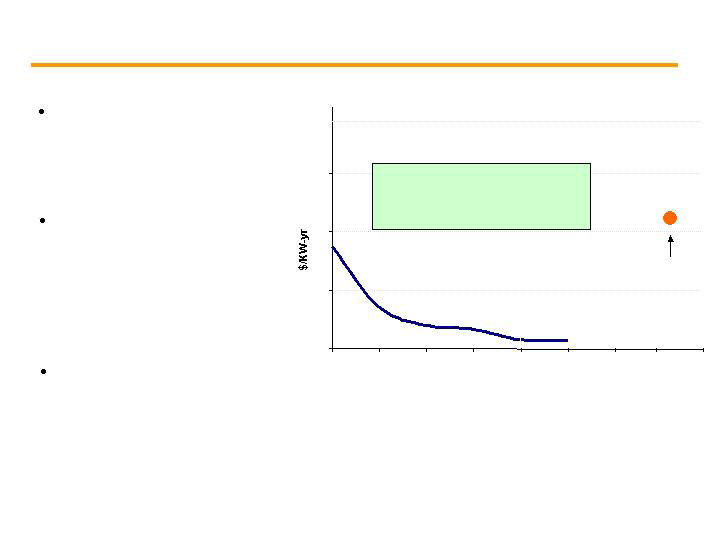

PJM’s Reliability Pricing Model (RPM) reflects a change

in market design …

$0

$20

$40

$60

2001

2002

2003

2004

2005

2006

2007

$80

2008

2009

Settled @ $72

’08 – ’09 Market

Trading

@ $40 -$45

’07 – ’08 Auction

Capacity Prices

$45/KW-yr = $123/MW-day

@ 50% load factor ~ $10/MWh

~

35

RPM Capacity Auction – April Results and Schedule

2007- 2008 Capacity Auction Results

($/ MW-day)

N/A

N/A

$40.80

Rest of

Pool

$48.38

$140.16

$188.54

Southwest

MAAC

$20.16

$177.51

$197.67

Eastern

MAAC

CTR

Value*

Load

Price

Unit

Price

PJM released results on April 13 from its

first capacity auction under the Reliability

Pricing Model (RPM) for the 2007-2008

delivery year.

Pricing in initial auction for Eastern MAAC

reflected “Cost of New Entry”: standard

simple cycle gas turbine adjusted for

location.

Future auction pricing could be influenced

by changes in demand and capacity

availability including transmission capability

between zones.

Market prices support our forecast year-

over-year improvement in capacity margin

of $125M - $175M in 2007 with further

improvement in 2008.

Auctions are scheduled throughout the

year to provide transition through the 2010-

2011 delivery year.

*CTR Value: Capacity Transfer Rights

Allocated to Load Serving Entities (LSE) in constrained zones to provide them with

access to supply from outside the zone.

May 2008

2011 – 2012

January 2008

2010 – 2011

Annual base auction in May of each subsequent year

October 2007

2009 – 2010

July 2007

2008 – 2009

Auction Date

Planning Year

(6/1 to 5/31)

Auction Schedule

36

… drive the increase in PSEG’s 2007 earnings guidance.

* Excludes Merger costs of $12M in 2005, Cumulative Effect of a Change in Accounting Principle of $16M in 2005 and Loss from Discontinued

Operations of $226M and $239M in 2005 and 2006, respectively

2005 Operating

Earnings

2006 Operating

Earnings

Energy

Capacity

Other

2007 Guidance

$515M*

$446M*

$825M to

$905M

$15M - $25M

$220M - $260M

$75M - $105M

Improvements across the portfolio …

37

2007 Guidance

Energy

Capacity

Other

2008

Expectations

2009

… drive PSEG’s earnings expectation for 2008 and beyond.

Drivers of 2009 Earnings

Recontracting

Operational excellence

Free cash flow

Growth opportunities

Further improvements at Power…

$825M to

$905M

38

Highest output ever from Nuclear

Highest output ever from Fossil

Balanced hedging strategy at ER&T

Strong, liquid markets

Sustainable BGS auction structure

Consent decree resolution

Rising energy prices

Favorable capacity market design

Diverse assets in constrained zones

Strong

Operations

Constructive

Regulatory and

Business

Environment

Positive Market

Fundamentals

Growth

Opportunities…

with Manageable

Risk

Near term – Hope Creek Uprate, RPM auctions

Longer term –

Tightening reserve margins

CO2 benefit to nuclear

Site expansion opportunities

Surrounding market opportunities

New nuclear investment potential

Manageable risk –

Enhanced operations

Balanced hedging strategy

Existing sites

Increasingly stable earnings base through

capacity market design

Positioned for growth in 2007 and beyond

39

PSEG Energy Holdings

Review and Outlook

Reducing risk in 2007 and beyond …

Strong

Operations

Constructive

Regulatory and

Business

Environment

Positive

Market

Fundamentals

Growth

Opportunities…

with

Manageable

Risk

Global

Resources

International Distribution

Domestic Generation

Improving valuations

and debt capacity could

present opportunity to

redeploy capital

Opportunities for:

Expansion, Hedging

and Debt capacity

Residual

value

upside

Stable F/X rates and

sovereign spreads

Tightening reserve

margins, gas-driven

market

Tax issues

monitored

closely

Reasonable rate case

outcomes

ERCOT – liquid and

transparent

Credit

ratings

Focus on Safety,

Reliability and line

losses

Forced outage

rates;

Heat rates

… opportunity for growth

41

Holdings’ Portfolio has …

Two businesses focused on maximizing value of existing investments

Represents 10% of PSEG’s total earnings

70% of earnings from Global (50% US Generation, 50% Chile & Peru Distribution)

30% from Resources

… a diverse asset base with improved stability.

PSEG

Resources

Chile & Peru

Distribution

Texas Merchant

Generation

(2,000 MW)

International

Generation

Other fully

contracted

US Generation

Two 1,000MW CCGT 7FA plants with record

2006 results in an attractive market

395MW owned primarily in California and

Hawaii fully contracted with utilities / state

agencies

1.9M customers served

by 3 company groups

Very modest

contributor in a sector

with decreased

investment

2006 Earnings Contribution

86% of the Resources

portfolio is in energy-related

leveraged leases

2007 Earnings Contribution

42

2006 benefited from open position

Open position sensitivity to market (Calendar 2008):

Natural Gas: +/- $1/MMBtu = +/- $13 M

Heat Rate: +/- 500 Btu/KWh = +/- $25 M

Potential growth opportunities:

Potential opportunity for reasonable return at appropriate valuations

Current debt levels offer additional leverage capacity

The Texas Market has shown significant improvement …

$100

~19

15%

6.90

2007

$130

19.42

16%

10.82

2006

$93

16.50

17%

6.34

2005

$48

11.97

25%

5.42

2004

EBITDA

($M)

Spark

Spread

Reserve

Margin

NYMEX

Gas Prices and reserve margins have driven spark spreads higher, generating strong results:

… and with strong demand growth and uncertain future capacity

additions, reserve margins may be pressured, presenting

opportunities.

NYMEX = Forward curve at year-end

Reserve margin c/o ERCOT (both

actuals and June 06 report for

projections)

Spark Spread and EBITDA = actual

amount achieved and projected

(including ancillary revenues, but

excluding MTM gains)

43

$41

$168

$104

$108

$57

$20

$(40)

$(35)

$(25)

Reshaped Portfolio - Improved risk profile by reducing

capital invested in non-strategic assets …

… while increasing returns and sharpening focus on G&A.

2004

2006

$2.6B

$2.0B

Chile &

Peru

US

Other

$900M

$400M

$1.3B

$150M

$500M

$1.4B

42%

16%

42%

15%

60%

25%

$296M**

48%

45%

2004

2006

2007

Projected

$202M**

$210M-$230M**

Composition of Global’s Pre-tax

Contribution by Region*

G&A

Chile &

Peru

US

Other

29%

51%

20%

8%

35%

57%

7%

Global’s Invested Capital

$500M

~$1 B

12/31/07

Projected

$1.6B

69%

31%

*Includes both consolidated and unconsolidated investments after project debt, before allocation of parent debt

**Excludes interest, taxes, G&A and other corporate items to arrive at Global’s Operating Earnings

44

Holdings has generated substantial operating cash

flow and monetized non-strategic assets …

… which has supported debt reduction and return of capital to

PSEG over the past three years.

36%

4.5x

$520

$609

$740

$159

2006

$1,423

$920

$1,617

$835

Total

$273

$403

Operating Cash

Flows

$435

$442

Asset Sale

Proceeds

41%

47%

Recourse

Debt / Capital

2.5x

3.4x

FFO/Interest

$412

$491

Dividends / Return

on Capital

-

$311

Net Recourse Debt

Reduction

2005

2004

Net after-tax gain of over

$50M on major asset sales

Improved returns on

recourse capital from 6% to

over 10% (using Operating

Earnings) from 2004 – 2006

Improved credit metrics

Improved risk profile of remaining portfolio - Global’s portfolio now comprised of:

$500M US generation companies in TX, CA and HI

$1.4B in distribution and generation companies in Chile & Peru

$150M in other international generation

45

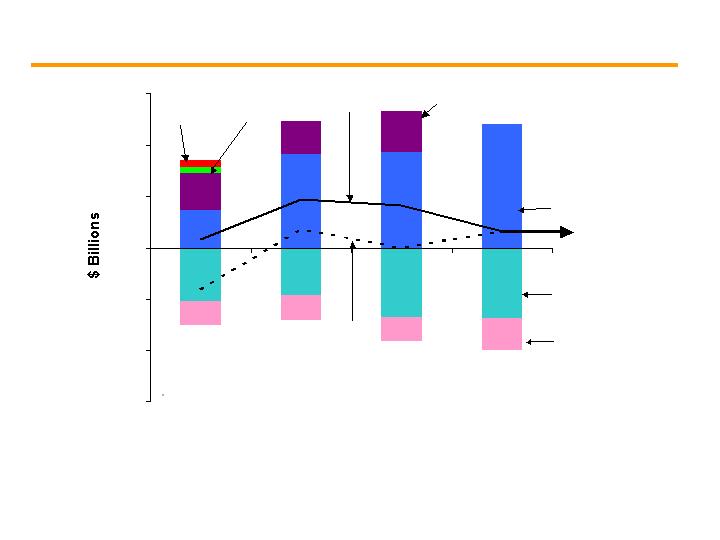

PSEG Energy Holdings – 2007 Drivers

$0

$100

$200

$300

2005

Operating

Earnings

2006

Operating

Earnings

Texas

FIN 48 /

FSP 13-2

Taxes

Asset Sales

2007

Guidance

2008

Expectations

$227M*

$25M - $35M

$10M - $20M

$5M - $10M

$35M - $45M

*Excludes Loss on Sale of RGE of $178M in 2006 and Income from Discontinued Operations of $18M and $226M in 2005 and 2006, respectively

Underlying project results are stable, but Operating Earnings are lower driven by

absence of MTM gain on Texas contract and adoption of new accounting rule.

Consistent with

2007

Modest

increase due to

organic growth

at Distribution

Companies

$130M to

$145M

$196M*

46

Positioned for growth in 2007 and beyond

Strong

Operations

Constructive

Regulatory and

Business

Environment

Positive

Market

Fundamentals

Growth

Opportunities…

with

Manageable

Risk

Global

Resources

International Distribution

Domestic Generation

Improving valuations and

stable F/X allow opportunity

to monetize / refinance and

reallocate capital

Opportunity to leverage

position for acquisitions/

new build

Medium term hedges

Opportunity to relever

Upside to residual

value of leases –

particularly

merchant energy

sector.

Strong energy demand

growth

Improved and stable F/X

rates and sovereign spreads

Tightening reserve

margins, improved spark

spread

Tax issues

monitored closely

Reasonable rate case

outcomes

Successful supply auctions

(pass-through)

ERCOT – Continues to

become more liquid and

transparent

Improved lessee

credit ratings

Chilquinta & LDS – strong

reliability

SAESA – improved reliability,

improving line losses

Low Forced outage rates

Competitive heat rates in

TX

47

PSEG

Financial Review and Outlook

196

227

347

262

446

515

130-145

130-145

340-360

330-350

825-905

770-850

(71)

(66)

(50)-(40)

(60)-(50)

2005

2006

2007 (Initial)

2007 (Revised)

2008

$5.60 - $6.10

Strong earnings growth in 2007 resulting in …

… a 37% increase over 2006 and an additional 15% in 2008.

$3.77*

$3.71**

$4.60 - $5.00

$4.90 - $5.30

Holdings

PSE&G

Power

Parent

Operating Earnings by Subsidiary

37%

15%

68%

~ 0

~

*Excludes ($.14) Merger Costs, ($.07) Cumulative Effect of an Accounting Change and ($.85) Discontinued Operations

**Excludes ($.03) Merger Costs, ($.70) Loss on Sale of RGE and ($.05) Discontinued Operations

49

Holdings

$0.0

$0.5

$1.0

$1.5

$2.0

$2.5

2005

2006

2007

2008

2005

2006

2007

2008

Strong earnings generate Cash from Operations…

…exceeding our capital requirements.

Holdings

PSE&G

Power

$1.0B

$1.3B

$1.3B

Capital Expenditures (2)

Cash from Operations (1)

$1.8B

$2.1B

$2.4B

Power

PSE&G

(1) Non-GAAP view: excludes revenues collected for securitization

principal payment & taxes associated with asset sales.

(2) Excludes nuclear fuel & includes cost of removal

$1.0B

$0.7B

50

($3.0)

($2.0)

($1.0)

$0.0

$1.0

$2.0

$3.0

2005

2006

2007

2008

Represents a Non-GAAP view excluding revenues

collected for securitization principal repayments

Excess

Cash

Available

Asset Sales/

Return of Capital

Excess

Cash

Ops

Cash from

Ops

Net Dividends

Investment

incl. Nuclear

Fuel

…beginning in mid-2008, expect annual excess cash of

approximately $500M to be available for new investments and/or

repurchasing shares.

We are currently using excess cash to reduce debt

and...

BGS

Securitization

Offshore

Cash

Repatriation

51

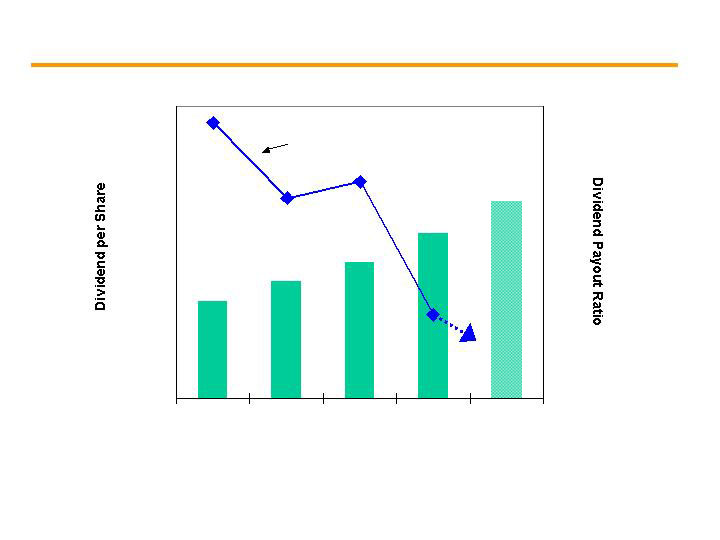

$2.20

$2.24

$2.28

$2.34 *

$2.00

$2.10

$2.20

$2.30

$2.40

$2.50

$2.60

2004

2005

2006

2007

2008

35

40

45

50

55

60

65

70

Improved earnings causes our dividend payout ratio to

quickly decline below 50% ...

… providing us the flexibility to raise our dividend at a rate

higher than prior increases.

Payout

Ratio

?

*Indicated annual dividend rate

52

… enabling excess cash to be used for share repurchases and/or

new investments beginning in mid-2008.

During 2007/2008, PSEG expects to achieve key target

credit measures …

2006

Target

Achieved

PSEG Consolidated

Total Debt / Total Capitalization

52%

~ 50%

~

2007

PSEG excl. EH

FFO/Total Debt

18%

Mid-20’s

2008

POWER

FFO/Total Debt

25%

Mid-30’s

2007

PSE&G

Debt/Total Capitalization

50%

~ 50%

~

Ö

HOLDINGS

FFO Coverage

4.5

3.0x - 4.0x

Ö

53

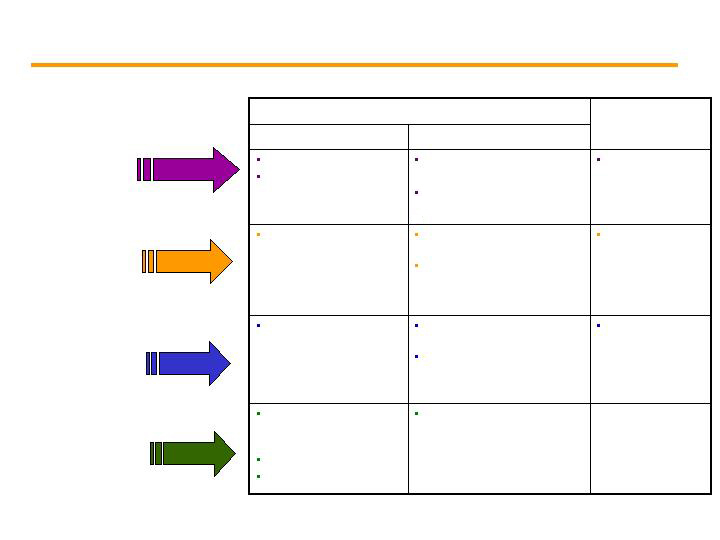

Growth opportunities …

Achieve Credit Targets

Sustainable and Growing Dividend Increases

Operational Excellence Builds Financial Strength

… Near-Term, Long-Term, with Manageable Risk.

Power

PSE&G

Holdings

Manageable Risk

Hedging strategy adds stablility and capacity auctions increases visibility of earnings

Solid regulatory relations and appropriate regulatory incentives for EMP investments

Reshaped portfolio and continuing to evaluate capital invested internationally

PSEG

Growing markets (PJM / NY / NEPOOL)

PSE&G

Holdings

Strong Earnings from Existing Assets and Base Capital Plan

Customer growth and network investment -->

Improving returns on existing investments and Texas assets benefit from low cost -->

Power

Attractive energy markets and recontracting

Generation value improvement (upward pressure on

capacity prices / heat rate expansion / carbon)

Guidance reflects strong growth

Implementing capacity market mechanisms

Annual Excess Cash ~ $500M

~

PSE&G

Holdings

Share Repurchases and New Investments

Power

Expansion capability at existing sites

Preliminary consideration of nuclear expansion

EMP Initiatives (new CIS, advanced metering, renewables)

Opportunity to leverage Texas position for new acquisition / build

54

Summary

Positioned for growth in 2007 and beyond

Strong

Operations

Constructive

Regulatory and

Business

Environment

Positive Market

Fundamentals

Growth

Opportunities…

with Manageable

Risk

PSE&G named America’s most reliable electric utility for second consecutive year

Generating fleet operating at record levels

NJ BPU approved rate changes providing

opportunity to earn authorized return

Natural gas setting price for generation

Capacity values recognized in tight markets

Potential for development at existing sites

Value for international assets improving

Free cash flow of $1.5B – $2.0B over

2007 – 2011 powers growth of incumbent

utility and generation businesses

56

Summary

Operating strength - foundation of our performance

Strong markets and improved regulated returns

propelling expected earnings growth of 15-20% per

year over 2005-2008

Financial targets for leverage and coverage ratios will

be met in 2008

Policy and market forces converging to provide

investment options across our asset base

An Intersection of Energy -- the Environment -- PSEG

57

Public Service Enterprise Group

APPENDIX

PSEG Overview

Electric Customers: 2.1M

Gas Customers: 1.7M

Nuclear Capacity: 3,500 MW

Total Capacity: 13,600 MW*

Traditional T&D

Leveraged

Leases

2007E Operating Earnings(4): $1,245M - $1,370M

2007 EPS Guidance(4) : $4.90 - $5.30

Assets (as of 12/31/06): $28.6B

Market Capitalization (as of 4/25/07): $22.8B

Domestic/Int’l

Energy

Regional

Wholesale Energy

Operating Earnings = Earnings Available and Excludes:

(1) Merger Costs of $1M

(2) Loss from Discontinued Operations of $239M

(3) Loss on Sale of RGE of $178M and Income from Discontinued Operations of $226M

Includes Operating Earnings from Global of $166M, Resources of $63M and Energy Holdings of ($2M)

(4) Includes the parent impact of $(50)M –$(40)M

*After sale of Lawrenceburg

2006 Operating Earnings: $262M(1) $515M(2) $227M(3)

2007 Guidance: $340M - $360M $825M - $905M $130M - $145M

60

-

10,000

20,000

30,000

40,000

50,000

2007

2008

2009

2010

A significant portion of Power’s low-cost coal and nuclear

output has been sold at increasingly attractive rates …

… with remaining output available to capture future market opportunities.

2007

$63-65/MWh

2008

$65-67/MWh

2009

$72-75/MWh

Power’s Generation Output

Other output

Contracted coal & nuclear output

Open coal & nuclear output

Contracted Prices

Estimated impact of $10/MWh

PJM West RTC price change*

$0.01 - $0.10

$0.45 - $0.80

*Assuming normal market dynamics

Includes roll off of 4 year,

500MW RTC contract ($100M+)

and other recontracting

61

0%

20%

40%

60%

80%

100%

2007

2008

2009

2010

Power will realize increasing margin improvement …

… through the repricing of capacity at market prices.

2007

$20-24/KW-yr

2008

$30-34/KW-yr

2009

$39-43/KW-yr

Total Capacity

Contracted Capacity

Open Capacity

Contracted Prices

Estimated impact of $10/KW-yr

capacity price change

$0.05 - $0.10

$0.10 - $0.20

62

$0

$10

$20

$30

$40

$50

$60

$70

2005

2006

2007 Est

2008 Est

2009 Est

… are expected to drive significant increases in Power’s gross

margin.

Operational improvements and recontracting in

current markets …

Realized Gross Margin ($/MWh)

Energy

Capacity

(Energy prices based on recent forward markets;

Illustrative capacity prices based on recent market for 2007/2008 in all years)

63

Energy Holdings’ Adjusted EBITDA

Adjusted EBITDA

2006

Global

465

$

Resources

147

Other

13

Total Energy Holdings

625

$

Debt Information

Holdings’ Senior Notes

1,149

$

Global Project Debt

1,034

Resources Project Debt

40

EGDC Project Debt

19

Holdings Total Debt

2,242

$

2006 Global EBITDA Detail

Adj EBITDA**

Project Debt

PSEG Share

PSEG Share

Texas *

174

$

375

$

SAESA

73

178

Electroandes

36

105

Prisma

14

3

Chilquinta

47

162

Luz del Sur

51

77

GWF - QF

33

0

GWF - Energy

19

72

Kalaeloa

28

62

Other, including G&A

(10)

-

Total Global

465

$

1,034

$

* Texas EBITDA includes mark to market gains of $44 million.

**EBITDA is adjusted for Global’s share of depreciation, interest and other items

so as to include those investments accounted for under the equity method.

64