Exhibit 99.1

Public Service Enterprise Group

PSEG Earnings Conference Call

2nd Quarter 2008

August 1, 2008

Forward-Looking Statement

Readers are cautioned that statements contained in this presentation about our and our subsidiaries’ future performance, including future

revenues, earnings, strategies, prospects and all other statements that are not purely historical, are forward-looking statements for purposes of

the safe harbor provisions under The Private Securities Litigation Reform Act of 1995. Although we believe that our expectations are based on

reasonable assumptions, we can give no assurance they will be achieved. The results or events predicted in these statements may differ

materially from actual results or events. Factors which could cause results or events to differ from current expectations include, but are not

limited to:

Adverse Changes in energy industry, policies and regulation, including market rules that may adversely affect our operating results.

Any inability of our energy transmission and distribution businesses to obtain adequate and timely rate relief and/or regulatory approvals from

federal and/or state regulators.

Changes in federal and/or state environmental regulations that could increase our costs or limit operations of our generating units.

Changes in nuclear regulation and/or developments in the nuclear power industry generally, that could limit operations of our nuclear generating

units.

Actions or activities at one of our nuclear units that might adversely affect our ability to continue to operate that unit or other units at the same

site.

Any inability to balance successfully our energy obligations, available supply and trading risks.

Any deterioration in our credit quality.

Any inability to realize anticipated tax benefits or retain tax credits.

Increases in the cost of or interruption in the supply of fuel and other commodities necessary to the operation of our generating units.

Delays or cost escalations in our construction and development activities.

Adverse capital market performance of our decommissioning and defined benefit plan trust funds.

Changes in technology and/or increased customer conservation.

For further information, please refer to our Annual Report on Form 10-K, including Item 1A. Risk Factors, and subsequent reports on Form 10-Q

and Form 8-K filed with the Securities and Exchange Commission. These documents address in further detail our business, industry issues and

other factors that could cause actual results to differ materially from those indicated in this presentation. In addition, any forward-looking

statements included herein represent our estimates only as of today and should not be relied upon as representing our estimates as of any

subsequent date. While we may elect to update forward-looking statements from time to time, we specifically disclaim any obligation to do so, even if our estimates change, unless otherwise required by applicable securities laws.

1

GAAP Disclaimer

PSEG presents Operating Earnings in addition to its Net Income reported

in accordance with accounting principles generally accepted in the United

States (GAAP). Operating Earnings is a non-GAAP financial measure that

differs from Net Income because it excludes the impact of the sale of

certain non-core domestic and international assets and material

impairments and lease-transaction-related charges. PSEG presents

Operating Earnings because management believes that it is appropriate

for investors to consider results excluding these items in addition to the

results reported in accordance with GAAP. PSEG believes that the non-

GAAP financial measure of Operating Earnings provides a consistent and

comparable measure of performance of its businesses to help

shareholders understand performance trends. This information is

not intended to be viewed as an alternative to GAAP information. The last

slide in this presentation includes a list of items excluded from Net Income

to reconcile to Operating Earnings, with a reference to that slide included

on each of the slides where the non-GAAP information appears.

2

PSEG

2008 Q2 Review

Tom O’Flynn

Executive Vice President and Chief Financial Officer

PSEG – Q2 2008 Highlights

Solid earnings growth:

Maintaining guidance of $2.80 - - $3.05 per share.

Steady and consistently solid operations.

Strong energy markets.

Improved risk profile:

SAESA sale closed.

Lease transaction reserve:

Substantial book reserves recognized for potential tax risk.

Litigation option preserved.

Ratings outlook for PSEG, PSE&G and Holdings moved to Stable from Negative.

Pursuing regulatory recovery for major transmission investments.

Discretionary cash position remains strong.

$750 million share repurchase program approved.

4

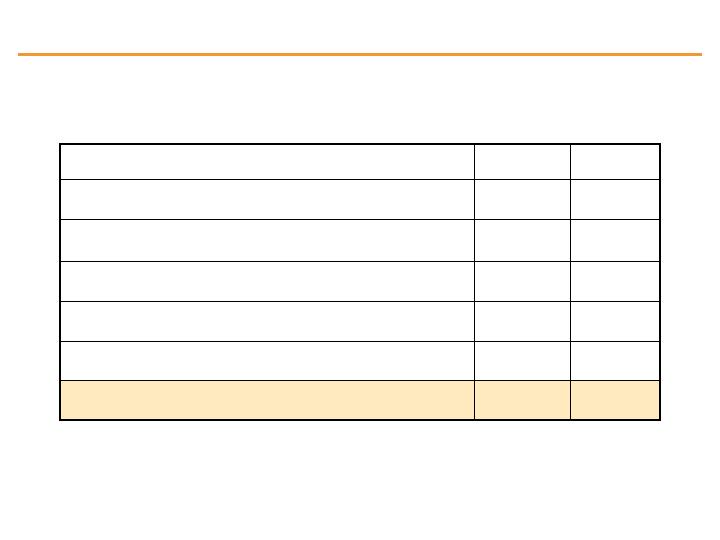

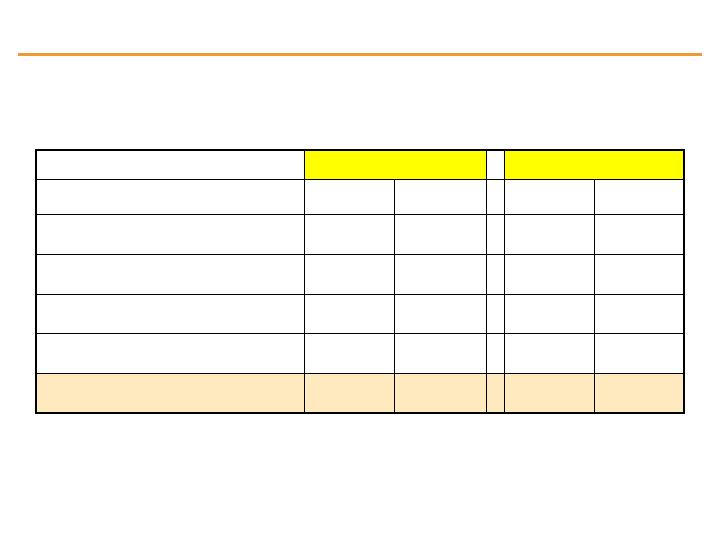

Q2 2008 Earnings Summary

(6)

16

Discontinued Operations

$ 0.55

$ 0.64

EPS from Operating Earnings

275

(150)

Net Income / (Loss)

281

(166)

Income / (Loss) from Continuing Operations

—

(490)

Lease Transaction Reserves

$ 281

$ 324

Operating Earnings

2007

2008

$ millions (except EPS)

Quarter ended June 30,

5

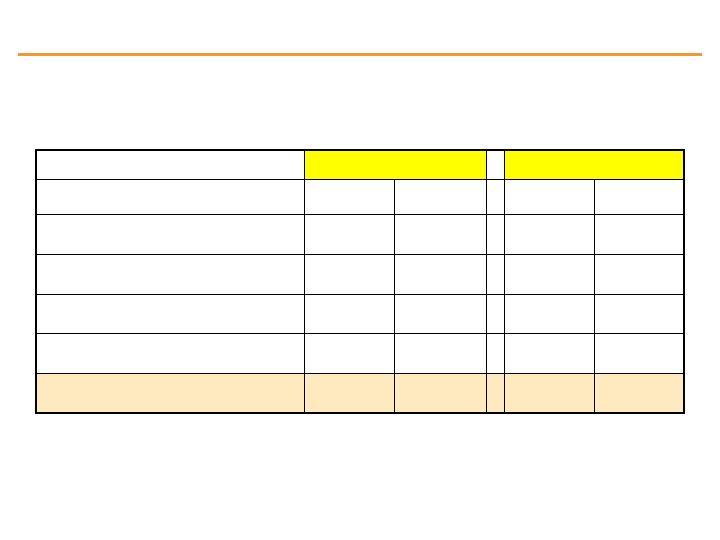

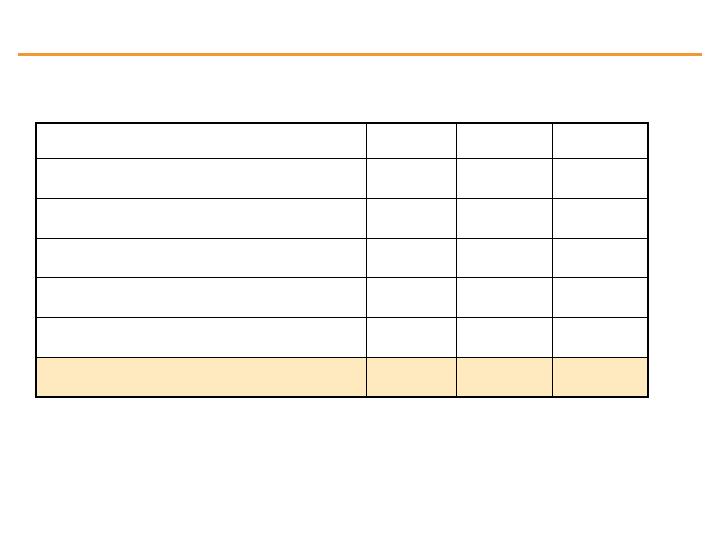

YTD Earnings Summary

—

(490)

Lease Transaction Reserves

2

30

Discontinued Operations, net of tax

$ 1.19

$ 1.49

EPS from Operating Earnings

604

298

Net Income

602

268

Income from Continuing Operations

—

(1)

Premium on Bond Redemption, net of tax

$ 602

$ 759

Operating Earnings

2007

2008

$ millions (except EPS)

Six months ended June 30,

6

PSEG

2008 Q2 Operating Company Review

Q2 Operating Earnings by Subsidiary

$ 281

(15)

47

62

$ 187

2007

$ 324

(4)

37

51

$ 240

2008

Operating Earnings

Earnings per Share

(0.03)

(0.01)

Enterprise

$ 0.55

$ 0.64

Operating Earnings

0.09

0.08

PSEG Energy Holdings

0.12

0.10

PSE&G

$ 0.37

$ 0.47

PSEG Power

2007

2008

$ Millions (except EPS)

Quarter ended June 30,

8

YTD Operating Earnings by Subsidiary

$ 602

(33)

36

193

$ 406

2007

$ 759

(9)

66

187

$ 515

2008

Operating Earnings

Earnings per Share

(0.06)

(0.02)

Enterprise

$ 1.19

$ 1.49

Operating Earnings

0.07

0.13

PSEG Energy Holdings

0.38

0.37

PSE&G

$ 0.80

$ 1.01

PSEG Power

2007

2008

$ Millions (except EPS)

Six months ended June 30,

9

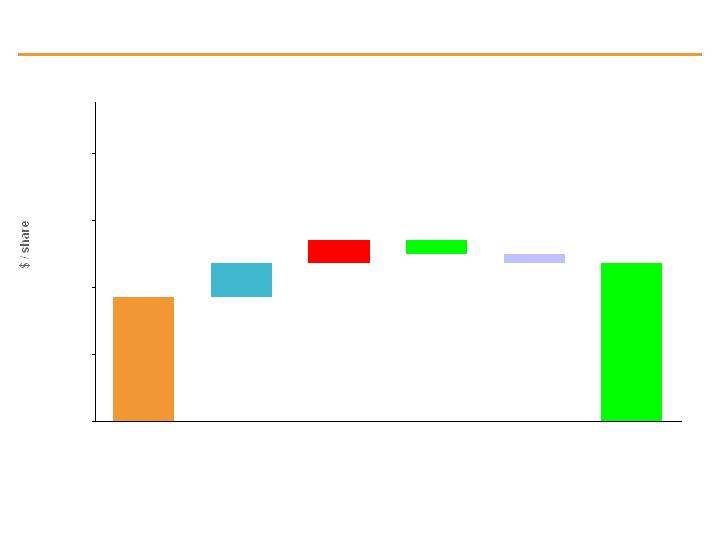

$0.55

.10

(.02)

(.01)

.02

$0.64

0.00

0.25

0.50

0.75

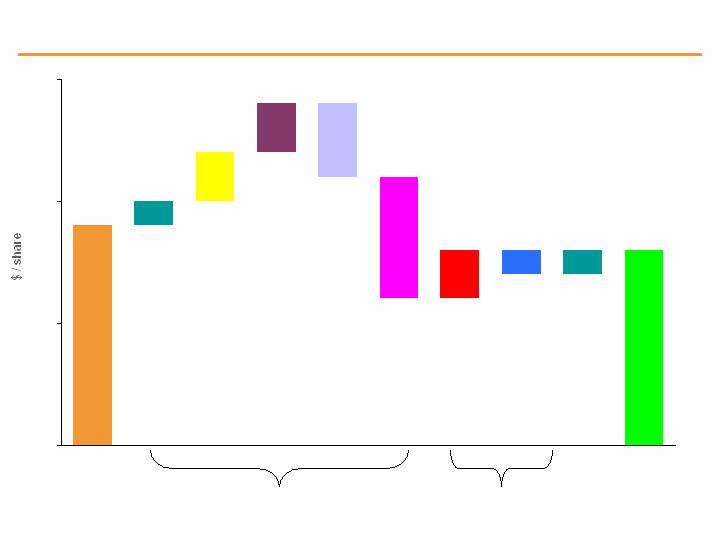

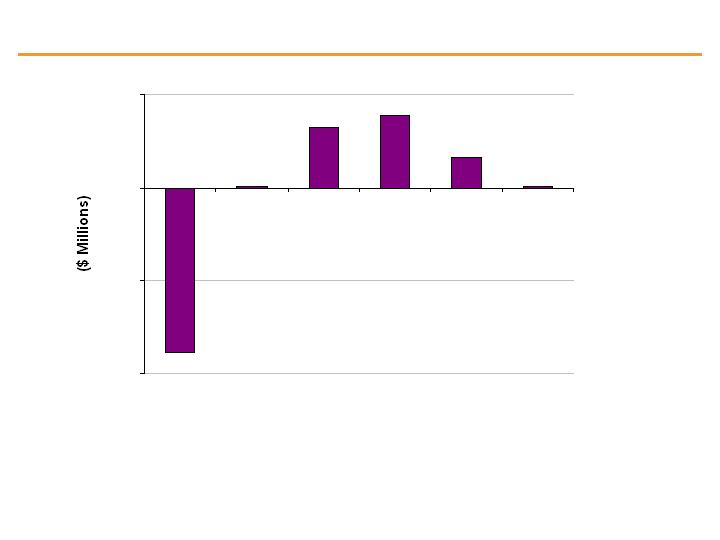

PSEG EPS Reconciliation – Q2 2007 versus Q2 2008

Q2 2008

operating

earnings

Q2 2007

operating

earnings

Interest .02

Recontracting

and strong

markets .10

MTM .08

O&M (.04)

Depreciation,

interest & NDT

(.03)

BGSS (.01)

PSEG Power

Transmission (.01)

Gas (.01)

O&M (.01)

Depreciation, taxes

& other .01

PSE&G

PSEG Energy

Holdings

Enterprise

Global:

Texas – MTM (.05)

Operations .06

Bioenergie .02

Interest expense .02

Effective tax rate

(.03)

Chilquinta/LDS (.03)

Other (.02)

Resources:

Effective tax rate .02

Lease income (.01)

Holdings Parent .01

10

$1.19

.21

(.01)

.06

.04

$1.49

1.00

1.50

PSEG EPS Reconciliation – YTD 2007 versus YTD 2008

Six months

ended 6/30/2008

operating

earnings

Six months

ended 6/30/2007

operating

earnings

Interest .04

Recontracting and

strong markets .24

MTM .09

Depreciation,

interest & NDT (.07)

O&M (.04)

BGSS (.01)

PSEG Power

Effective tax rate .06

Weather – Gas (.02)

O&M (.02)

Transmission (.01)

Gas (.01)

Depreciation (.01)

PSE&G

PSEG Energy

Holdings

Enterprise

Global:

Texas – MTM (.01)

Operations .06

Interest expense .04

Effective tax rate .03

Bioenergie .02

Chilquinta/LDS (.05)

Other (.04)

Resources:

Effective tax rate .03

Lease income (.01)

2007 CBO

Settlement (.01)

11

PSEG Power

2008 Q2 Review

PSEG Power – Q2 2008 EPS Summary

$ 318

$ 1,305

$ 1,623

Operating Revenues

$ 0.10

$ 0.37

$ 0.47

EPS from Operating Earnings

56

184

240

Net Income

3

(3)

—

Discontinued Operations

53

187

240

Income from Continuing Operations

53

187

240

Operating Earnings

Variance

Q2 2007

Q2 2008

$ millions (except EPS)

13

$0.37

.10

.07

(.04)

(.03)

$0.47

0.00

0.20

0.40

0.60

0.80

Recontracting

and strong

markets

PSEG Power EPS Reconciliation – Q2 2008 versus Q2 2007

Q2 2008

operating

earnings

Q2 2007

operating

earnings

MTM .08

BGSS (.01)

Depreciation, Interest

& NDT (.03)

O&M

14

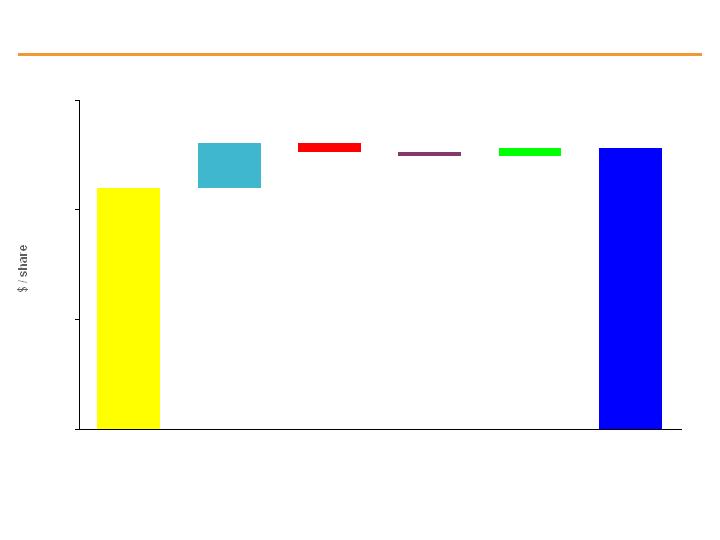

PSEG Power – Generation Measures

6,958

7,032

2,977

2,889

2,681

3,648

0

5,000

10,000

15,000

2007

2008

Quarter ended June 30,

Total Nuclear

Total Coal*

Total Oil &

Natural Gas

* Includes figures for Pumped Storage

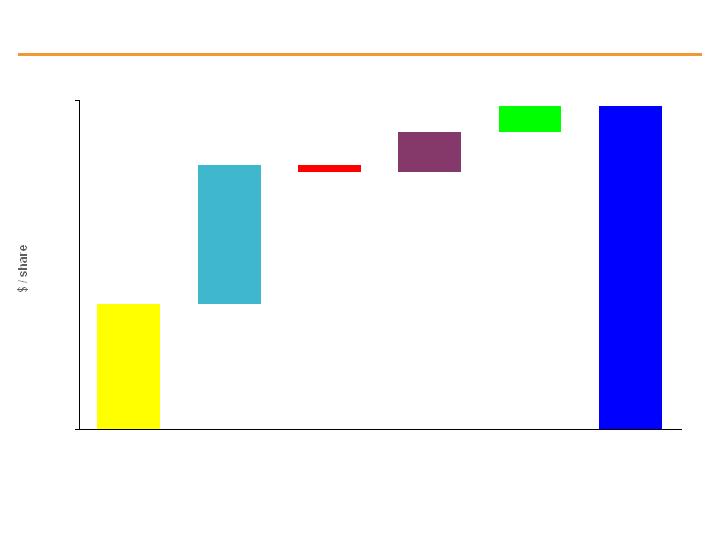

PSEG Power – Generation (GWh)

12,616

13,569

14,414

14,296

6,119

6,546

4,993

6,426

0

10,000

20,000

30,000

2007

2008

Six months ended June 30,

25,526

27,268

15

$0

$20

$40

$60

2007

2008

Strong Pricing Supports Margin Improvement

$0

$20

$40

$60

2007

2008

PSEG Power Gross Margin* ($/MWh)

$47

$54

$0

$20

$40

$60

2007

2008E

Quarter ended June 30,

Six months ended June 30,

Twelve months ended

December 31,

$46

$53

$50

* Includes MTM

16

PSEG Power – Q2 Operating Highlights

Output increased 7.6%.

Nuclear fleet capacity factor improved slightly to 90.5%.

Salem No. 2 steam generator replacement completed in 58 days – second fastest in industry.

Hope Creek extended power uprate of 125MW; Salem No. 2 capacity expansion of 11MW.

Significant progress with coal plant capital improvement program.

Operations

Regulatory and Market Environment

Financial

Benefiting from roll-off of below-market contracts; high natural gas prices.

Clean Air Interstate Rule (CAIR) regulating NOx and SO2 was vacated in July 2008 by D.C.

Circuit Court of Appeals. Although PJM West prices declined subsequent to this decision, it

is difficult to predict the long-term impact on the market.

PSEG Power foresees no change in its response to controlling NOx and SO

2.

Brattle report on RPM offers constructive recommendations to improve effectiveness.

Second quarter EBITDA of $481 million versus $370 million bringing EBITDA for six months

ended June 30, 2008 to $1.028 billion versus $793 million.

Open EBITDA of $2.6 - $2.8 billion.

17

PSE&G

2008 Q2 Review

PSE&G – Q2 2008 Earnings Summary

($ 0.02)

$ 0.12

$ 0.10

EPS from Operating Earnings

(11)

62

51

Income from Continuing Operations/

Net Income

(11)

62

51

Operating Earnings

$ 110

$ 1,748

$ 1,858

Operating Revenues

Variance

Q2 2007

Q2 2008

$ millions (except EPS)

19

$0.12

(.02)

.00

$0.10

0.00

0.05

0.10

0.15

0.20

PSE&G EPS Reconciliation – Q2 2008 versus Q2 2007

Q2 2008

operating

earnings

Q2 2007

operating

earnings

Margin:

Transmission (.01)

Gas (.01)

O&M (.01)

Depreciation, Taxes

& Other .01

20

PSE&G – Q2 Operating Highlights

Petitioned FERC in July for cost of service formula rates for existing and future

transmission investments to be effective October 1, 2008.

In May, filed in NJ for 20% increase in base prices for Gas commodity supply.

New solar program ~40% subscribed; AMI pilot program (17,500 customers)

approved.

Solid and improving operating cash flow.

Moody’s outlook revised to Stable.

Operations

Regulatory and Market Environment

Financial

O&M growth remains below inflation.

Accounts receivable balance and aging stable as a result of customer outreach

programs.

Construction programs on time, on budget.

21

PSEG Energy Holdings

2008 Q2 Review

PSEG Energy Holdings – Q2 2008 Earnings Summary

(490)

—

(490)

Lease Transaction Reserves

(500)

47

(453)

Income / (Loss) from Continuing Operations

($0.01)

$ 0.09

$ 0.08

EPS from Operating Earnings

(481)

44

(437)

Net Income / (Loss)

19

(3)

16

Discontinued Operations

($ 10)

$ 47

$ 37

Operating Earnings

Variance

Q2 2007

Q2 2008

$ millions (except EPS)

23

.02

(.05)

$0.08

(.03)

.02

.02

.01

$0.09

(.01)

.01

0.00

0.05

0.10

0.15

PSEG Energy Holdings EPS Reconciliation – Q2 2008 versus

Q2 2007

Q2 2008

operating

earnings

Q2 2007

operating

earnings

Effective tax

rate

Interest

expense

Texas -

Operations .06

MTM (.05)

Effective

tax rate

GLOBAL

RESOURCES

Bioenergie

Earnings on

Chilquinta/

LDS (.03)

Other (.02)

Lease

income

Holdings -

Parent

24

PSEG Energy Holdings – Q2 Operating Highlights

PSEG Global is continuing to explore options for its remaining $122 million of international

investments in Italy, Venezuela and India.

Texas assets benefiting from strong pricing.

Closed on sale of SAESA.

Recognized substantial book reserves related to IRS challenge of certain leveraged

leases in Resources’ portfolio.

Operations

Regulatory and Market Environment

Financial

Texas – integrated into PSEG Power gas fleet management

1,000MW gas-fired Odessa plant dispatch affected by significant wind resources in west Texas.

1,000MW gas fired Guadalupe plant operating better than expected given normal weather, spark

spreads and increased dispatch in southeast Texas.

Italy

Biomass facilities running well versus year-ago period when one of the facilities was closed in first

half of 2007.

25

PSEG

Market

28 - 30

19.04

19.42

16.52

$11.97

Spark

Spread

125 - 145

43 - 45%

14%

10.00

2008 Forecast

104

48.7%

15%

6.76

2007

130

54.4%

16%

10.82

2006

93

54.6%

17%

6.34

2005

$48

50.4%

25%

$5.42

2004

EBITDA

($M)

Capacity

Factors

Reserve

Margin

Natural Gas

NYMEX

Texas Market Update

26

Impact of Lease Transaction Reserves

2Q 2008 results include a charge of $490 million:

$135 million after-tax increase to the interest reserve recorded in

Income Tax Expense.

$355 million after-tax charge reflecting a change in assumptions

relating to the amount paid and timing of cash flow for certain leases

in the portfolio. This charge will be recognized in income over the

remaining terms of the affected leases.

Reserves represent our view of most of the book exposure

related to the leases under challenge. In addition, our forecast of

cash available includes potential cash outflows of $900 - $950

million over 2 – 3 years.

Based on status of discussions with IRS, PSEG anticipates that it

will pay in 2008, the taxes, interest and penalties claimed by the

IRS for 1997-2000 audit cycle ($300 - $350 million) and

subsequently commence litigation to recover a refund.

27

Income Recognition – $355 Million Charge

(400)

(200)

0

200

06/30/08

2009-

2013

2014-

2018

2019-

2023

2024-

2028

2029-

2034

Assumes issue is resolved with the IRS at current reserve levels

involving $900 - $950 million cash outflow in or by 2010.

$355

28

Review of Discretionary Cash/Liquidity

Discretionary Cash / Liquidity

$2.5 billion forecast of discretionary cash for 2008 – 2011

versus prior forecast of $3.0 billion.

Revised figure reflects a higher than originally forecast

payment of $900 - $950 million for taxes on our leveraged

lease position over a period of several years, as well as

higher proceeds from asset sales.

Major drivers that can influence our forecast of

discretionary cash include changes in commodity prices

and capital spending.

Collateral postings have declined by $1.3 billion to $800

million since the end of June 2008 with the decline in

commodity prices.

30

PSEG – Share Repurchase Authorized

Board authorized the repurchase of up to $750 million of

common stock during an 18 month period.

Improved risk profile:

Sale of most of international assets completed.

Recognition of substantial book reserves for leases.

Credit ratings in line with objectives.

Represents commitment to making investments that

provide best available return to shareholders.

Maintains financial flexibility to pursue higher value

opportunities to grow the business, when available.

31

Maintaining 2008 Operating Earnings Guidance

$2.80 - $3.05

$1,420 - $1,560

(15) – (10)

45 - 60

350 - 370

$1,040 - $1,140

Current

Enterprise

Earnings per Share

Operating Earnings

PSEG Energy Holdings

PSE&G

PSEG Power

$ millions (except EPS)

32