Public Service Enterprise Group

European Investor Meetings

June 29, 2009 – July 2, 2009

Forward-Looking Statement

Readers are cautioned that statements contained in this presentation about our and our subsidiaries’ future performance, including future

revenues, earnings, strategies, prospects and all other statements that are not purely historical, are forward-looking statements for

purposes of the safe harbor provisions under The Private Securities Litigation Reform Act of 1995. Although we believe that our

expectations are based on reasonable assumptions, we can give no assurance they will be achieved. The results or events predicted in

these statements may differ materially from actual results or events. Factors which could cause results or events to differ from current

expectations include, but are not limited to:

Adverse changes in energy industry, policies and regulation, including market structures and rules.

New energy legislation.

Any inability of our energy transmission and distribution businesses to obtain adequate and timely rate relief and regulatory approvals from

federal and state regulators.

Changes in federal and state environmental regulations that could increase our costs or limit operations of our generating units.

Changes in nuclear regulation and/or developments in the nuclear power industry generally, that could limit operations of our nuclear

generating units.

Actions or activities at one of our nuclear units that might adversely affect our ability to continue to operate that unit or other units at the

same site.

Any inability to balance our energy obligations, available supply and trading risks.

Any deterioration in our credit quality.

Availability of capital and credit at reasonable pricing terms and our ability to meet cash needs.

Any inability to realize anticipated tax benefits or retain tax credits.

Increases in the cost of or interruption in the supply of fuel and other commodities necessary to the operation of our generating units.

Delays or cost escalations in our construction and development activities.

Adverse investment performance of our decommissioning and defined benefit plan trust funds, and changes in discount rates and funding

requirements.

Changes in technology and increased customer conservation.

For further information, please refer to our Annual Report on Form 10-K, including Item 1A. Risk Factors, and subsequent reports on Form

10-Q and Form 8-K filed with the Securities and Exchange Commission. These documents address in further detail our business, industry

issues and other factors that could cause actual results to differ materially from those indicated in this presentation. In addition, any

forward-looking statements included herein represent our estimates only as of today and should not be relied upon as representing our

estimates as of any subsequent date. While we may elect to update forward-looking statements from time to time, we specifically disclaim

any obligation to do so, even if our internal estimates change, unless otherwise required by applicable securities laws.

Delivering Value: Today and Tomorrow 2

GAAP Disclaimer

PSEG presents Operating Earnings in addition to its Net Income reported

in accordance with accounting principles generally accepted in the United

States (GAAP). Operating Earnings is a non-GAAP financial measure that

differs from Net Income because it excludes the impact of the sale of

certain non-core domestic and international assets and material

impairments and lease-transaction-related charges. PSEG presents

Operating Earnings because management believes that it is appropriate

for investors to consider results excluding these items in addition to the

results reported in accordance with GAAP. PSEG believes that the non-

GAAP financial measure of Operating Earnings provides a consistent and

comparable measure of performance of its businesses to help

shareholders understand performance trends. This information is

not intended to be viewed as an alternative to GAAP information. The last

slide in this presentation includes a list of items excluded from Net Income

to reconcile to Operating Earnings, with a reference to that slide included

on each of the slides where the non-GAAP information appears.

Delivering Value: Today and Tomorrow 3

PSEG establishing a policy leadership position …

Electric and Gas

Delivery

Leveraged Leases and

Renewable Investments

Regional

Wholesale Energy

… in promoting a sustainable energy future.

PSE&G positioned to meet

NJ’s energy policy and

economic growth objectives

with $1.7 billion investment

program.

PSEG Power’s low-cost

baseload nuclear fleet well-

positioned in carbon

constrained environment.

PSEG Energy Holdings

positioned to pursue attractive

renewable generation

opportunities.

Compressed Air Energy

Storage (CAES)

Solar

Offshore wind

Delivering Value: Today and Tomorrow 4

Public Service Enterprise Group …

… an energy provider

meeting the needs of customers

and shareholders.

Meeting

Commitments

Delivering

Value Today

Positioned for

the Future

Delivering Value: Today and Tomorrow 5

PSEG: Establishing a foundation…

Meeting Commitments

Achieved 2008 earnings targets

Operational excellence drove results

Sharpened business focus; international assets

sold

Balance sheet strengthened; credit outlook

improved

Attractive dividend growth rate

… and building a record that sets us apart.

Delivering Value: Today and Tomorrow 6

Making decisions and achieving results…

… to strengthen operational and financial position.

Delivering Value Today

2009 earnings guidance represents continued

growth

Operational excellence improving results

Core business investments providing attractive

returns

Dividend increased – 6th consecutive year; 102nd

year of paying an annual dividend

Strong financial position – credit metrics, liquidity

Delivering Value: Today and Tomorrow 7

2007 Operating Earnings Per Share*

2008 Operating Earnings Per Share*

2009 Guidance

$2.68

$3.00 - $3.25

PSEG – 2009: Meeting the Challenge

$3.03

* See page 64 for Items excluded from Income from Continuing Operations to reconcile to Operating Earnings.

Delivering Value: Today and Tomorrow 8

Strong operations and risk controls…

… position us to meet challenges of today’s market.

Asset optimization yielding

results

7th successful BGS auction validates

hedging strategy

RPM capacity auction supports asset

values in constrained areas

Power’s dispatch profile provides

operating flexibility

PSE&G focused on reliability and

meeting energy goals

On track to achieve

earnings growth in 2009.

Guidance maintained at

$3.00 - $3.25.

Investment focus on projects

with attractive risk-adjusted

returns

iPower

Infrastructure

Energy Efficiency

Solar

Delivering Value: Today and Tomorrow 9

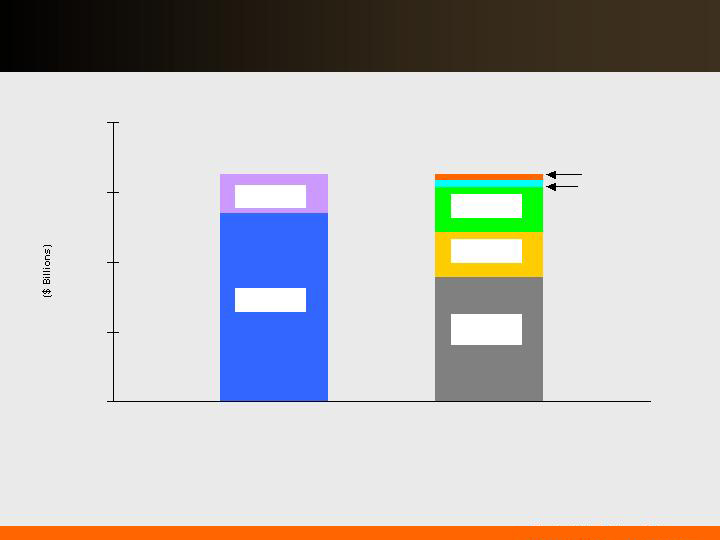

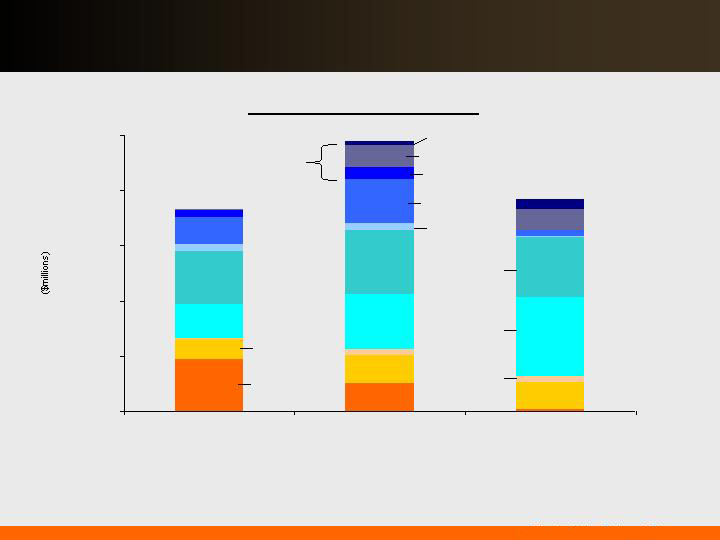

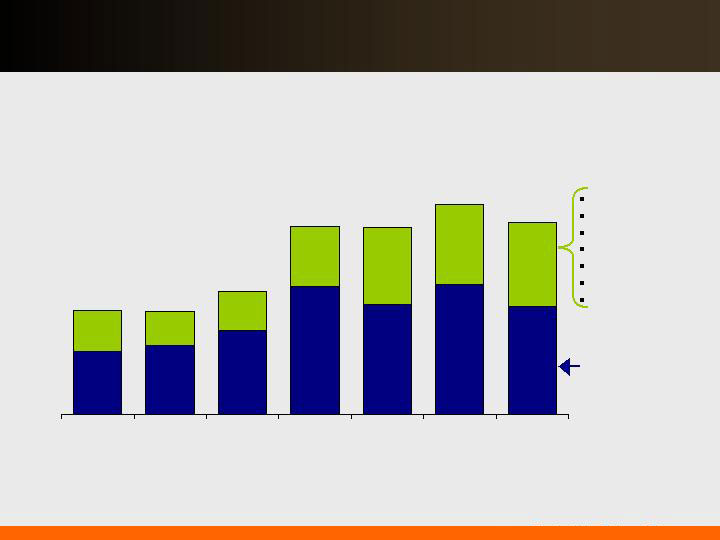

PSEG Consolidated

2008 Sources and Uses

Proceeds from asset sales provided further support for debt

reduction.

$0.0

$1.0

$2.0

$3.0

$4.0

Sources

Uses

Share Repurchases

Cash Ops*

(Non-GAAP)

Shareholder

Dividend

Investment

(includes

Nuclear Fuel)

Debt

Reduction

Net Asset

Sales

Internally generated cash in 2008 exceeded investment needs.

* Cash Ops (Non-GAAP) represents Cash Ops adjusted for securitization principal repayment, taxes associated with asset sales, and IRS deposits.

IRS Deposit

Delivering Value: Today and Tomorrow 10

Consolidated

PSE&G

Power

Holdings

Net Short Term Debt / (Investments)

(0.2)

(0.0)

-

-

Total Long-Term Debt

7.2

3.5

2.9

0.5

Preferred Stock

0.1

0.1

-

-

Common Equity

7.8

3.6

3.9

1.1

Total Capitalization

14.9

7.2

6.8

1.6

2008 Year-End Capital Structure*

$ Billions

45%

50%

55%

2007

2008

48%

50%

47%

50%

53%

2007

2008

PSE&G

Regulatory Equity Ratio

PSEG Consolidated

Total Debt to Total Capitalization

Our balance sheet has been strengthened …

… which provides us substantial financial flexibility.

*Excludes securitization and non-recourse debt

~$525M reduction in Net Debt

excluding PSE&G

~

~

Delivering Value: Today and Tomorrow 11

35%

40%

45%

50%

55%

2007

2008

2009

20%

25%

30%

35%

2007

2008

2009

PSEG

Funds from Operations / Total Debt

PSEG Power

Funds from Operations / Total Debt

Target Mid-20’s

~

~

Target Mid-30’s

~

~

We are meeting or exceeding key credit measures …

… maximizing financial flexibility in uncertain credit markets.

Delivering Value: Today and Tomorrow 12

… continues 102-year history of paying common dividends.

70%

44%

Payout

Ratio

41% - 44%

43%

66%

63%

$1.10

$1.12

$1.33*

$1.17

$1.29

$1.14

2004

2005

2006

2007

2008

2009E

*Indicated annual dividend rate

Dividends per Share

Sixth consecutive annual increase in common dividend …

Delivering Value: Today and Tomorrow 13

Operational excellence, financial strength and disciplined investment …

Positioned for the Future

… support shareholder value.

Balanced business mix

BGS: A demonstrated mechanism for meeting customer

supply at market prices for multi-year period

Federal and State policies provide opportunities for

growth – Leadership position in energy policy

T&D investments providing growth with minimal rate

impact

Strong financial position and cash flow provide flexibility

in volatile markets – No need to issue equity

Delivering Value: Today and Tomorrow 14

PSE&G’s investments in Energy Efficiency, Stimulus and Solar are

conditioned upon receiving reasonable rate treatment.

Future investments are weighted towards PSE&G and growth.

2009 - 2011 Capital Expenditures

$0

$500

$1,000

$1,500

$2,000

$2,500

2009

2010

2011

Power –

Sustainability

PSE&G -

Distribution

Infrastructure

Power – BET

Environmental

PSE&G -

Transmission

PSE&G - Other

Solar 4 All

Pending

Approval

Energy Efficiency

Solar II

Power –

Growth

Delivering Value: Today and Tomorrow 15

PSEG leadership recognized

Named one of the Most

Admired Companies,

2007 & 2008

One of 125 companies

named to DJSI North

America and one of only

10 U.S. electric

companies included

Corporation of the year 2007

One of the 400 best

big companies, 2008

PSE&G named America’s Most

Reliable Utility

Mid-Atlantic Region

winner for the 7th straight year

PSEG Chairman

Ralph Izzo named

CEO of the year

Carbon Disclosure

Leadership Index 2008

2008 Balanced Scorecard

Achievement Award

Delivering Value: Today and Tomorrow

16

Operational excellence, financial strength and disciplined investment…

… position us well in today’s market.

Low payout ratio and strong balance sheet provide support

Is dividend secure?

Strong balance sheet, credit metrics and liquidity

What is the impact of

credit market stress?

Strong cash flow well in excess of PSE&G’s equity

requirements

Do you need equity?

Carbon friendly

Federal and State Policy initiatives support capital plans

How is PSEG affected

by policy changes?

Multi-year hedging profile supported by core assets

Asset balance dampens relative fuel price volatility

Capacity markets provide stability

What’s the impact of

commodity volatility?

PSE&G current/pending rate needs equal 2-4% impact

BGS supply generally priced at market

What is impact on

customer from capital

programs?

PSEG Position

Market’s Questions

Delivering Value: Today and Tomorrow

17

PSEG – Delivering Value: Today and Tomorrow

Delivering

Value Today

Positioned for

the Future

Achieved 2008 earnings

targets

Operational excellence

drove results

Sharpened business focus;

international assets sold

Balance sheet

strengthened; credit

outlook improved

Attractive dividend growth

rate

2009 earnings guidance

represents continued

growth

Operational excellence

improving results

Core business

investments providing

attractive returns

Dividend increased – 6th

consecutive year; 102nd

year of paying an annual

dividend

Strong financial position

– credit metrics, liquidity

Balanced business mix

BGS: A demonstrated

mechanism for meeting

customer supply at market

prices for multi-year period

Federal and State policies

provide opportunities for

growth – Leadership position

in energy policy

T&D investments providing

growth with minimal rate

impact

Strong financial position and

cash flow provide flexibility in

volatile markets – No need to

issue equity

Meeting

Commitments

Delivering Value: Today and Tomorrow

18

PSEG Power – Overview

Delivering

Value Today

Positioned for

the Future

Meeting

Commitments

Achieved 2008 earnings

targets

Improved operating

performance of generation

fleet

Environmental

commitments met

$1 Billion capital expense

on budget, met specs

Disciplined hedging

strategies have managed

earnings volatility and

reduced risk

On target to meet 2009

earnings guidance of

$1,210M to $1,285M

Continued Operational

Excellence Model (OEM)

implementation with

demonstrated

improvements at Fossil

Sustained, strong nuclear

performance

Successful multi-year

hedging strategy

supported by BGS, RPM in

liquid markets

Effective management of

costs and capital programs

to drive value

Low-cost, baseload

nuclear fleet benefits in

carbon constrained world

BET installation improves

operating capability of coal

fleet and enables a wide

variety of coals

Expansion opportunities

through existing

experience and

infrastructure, including

peaker bids

Strong free cash flow

PSEG Power - Delivering Value: Today and Tomorrow

Delivering Value: Today and Tomorrow

20

Low-cost portfolio

Regional focus in competitive, liquid

markets

Assets favorably located near

customers/load centers

Many units east of PJM

constraints

Southern NEPOOL/ Connecticut

Market knowledge and experience

to maximize the value of our assets

… with low cost plants, in good locations, within solid markets.

Power’s assets support commitments in a dynamic environment…

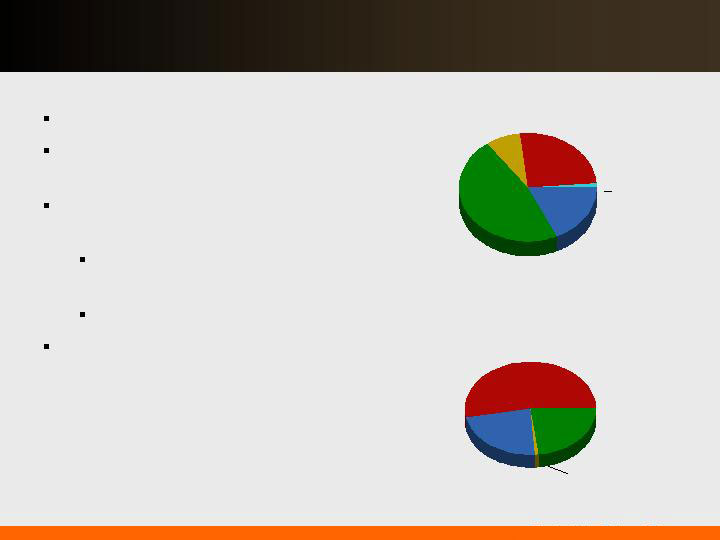

18%

45 %

9 %

27 %

Fuel Diversity

Coal

Gas

Oil

Nuclear

Pumped

Storage

1%

Energy Produced – 2008

53%

23%

23%

Pumped Storage

& Oil 1%

Nuclear

Coal

Gas

Total GWh: 55,300

Total MW: 13,576

Delivering Value: Today and Tomorrow

21

… of serving full requirement load contracts, while maintaining

optionality under a variety of conditions.

Power’s assets along the dispatch curve reduce the risk…

X

X

Ancillary Revenue

X

X

X

X

Capacity Revenue

X

X

Energy Revenue

X

X

Dual Fuel

Baseload units

Load following units

Peaking units

Illustrative

Salem

Hope

Creek

Keystone

Conemaugh

Hudson 2

Linden 1,2

Burlington 8-9-11

Edison 1-2-3

Essex 10-11-12

Bergen 1

Sewaren 1-4

Hudson 1

Mercer1, 2

Bergen 2

Sewaren 6

Mercer 3

Kearny 10-11

Linden 5-8 / Essex 9

Burlington 12 / Kearny 12

Peach

Bottom

Bridgeport

New

Haven

Nuclear

Coal

Combined Cycle

Steam

Peaking

BEC

Yards

Creek

National Park

Delivering Value: Today and Tomorrow

22

2003

2004

2005

2006

2007

2008

2009

Increase in Full Requirements

Component Due to:

Increased Congestion (East/West Basis)

Increase in Capacity Markets/RPM

Volatility in Market Increases Risk

Premium

The recent successful completion of the seventh BGS auction...

Market Perspective – BGS Auction Results

… cushions the impact of volatile markets on customers.

Note: BGS prices reflect PSE&G Zone

Full Requirements

3 Year Average

Round the Clock

PJM West

Forward Energy

Price

$55.05

$65.41

~ $18

~ $21

$102.51

~ $32

$98.88

~ $41

~ $43

$111.50

~ $47

$103.72

$55.59

~ $21

Capacity

Load shape

Transmission

Congestion

Ancillary services

Risk premium

Green

$33 - $34

$36 - $37

$44 - $46

$67 - $70

$58-$60

$68 - $71

$56 - $58

*

*2009 RTC price was ~ $50/MWh at time of auction

Delivering Value: Today and Tomorrow

23

-

2,000

4,000

6,000

8,000

10,000

12,000

-

2,000

4,000

6,000

8,000

10,000

12,000

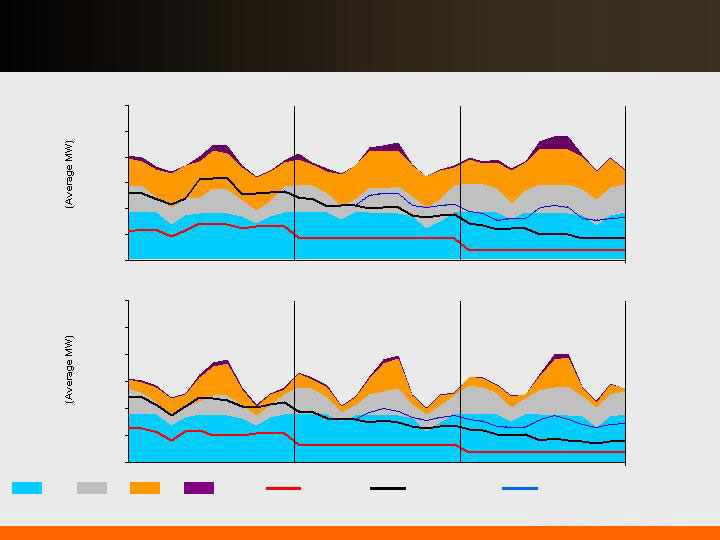

Power’s output is sold forward…

… through full requirement contracts and other hedging transactions.

2009 2010 2011

2009 2010 2011

Nuclear

Coal

CC

Steam / Pk

Existing Hedges

Existing Loads+ Hedges

Existing Loads+ Hedges + Potential Future BGS

Total Fleet On-Peak Average MW

Total Fleet Off-Peak Average MW

Delivering Value: Today and Tomorrow

24

$0

$20

$40

$60

$80

$100

2004

2005

2006

2007

2008

2009

Fwd *

2010

Fwd

2011

Fwd

Commodity prices have been volatile…

*Average of 6 historical months and 6 forward months

… but Power’s diverse asset portfolio and hedging strategy has

mitigated the effect of volatility, providing strong results.

Henry Hub NYMEX

($/MMBTU)

Western Hub RTC

($/MWh)

West Hub On Peak

($/MWh)

Central Appalachian Coal

($/Ton)

Note: Forward prices as of 6/18/09

$0

$20

$40

$60

$80

$100

$120

2004

2005

2006

2007

2008

2009

Fwd *

2010

Fwd

2011

Fwd

$0

$2

$4

$6

$8

$10

2004

2005

2006

2007

2008

2009

Fwd *

2010

Fwd

2011

Fwd

$0

$20

$40

$60

$80

$100

2004

2005

2006

2007

2008

2009

Fwd *

2010

Fwd

2011

Fwd

Delivering Value: Today and Tomorrow

25

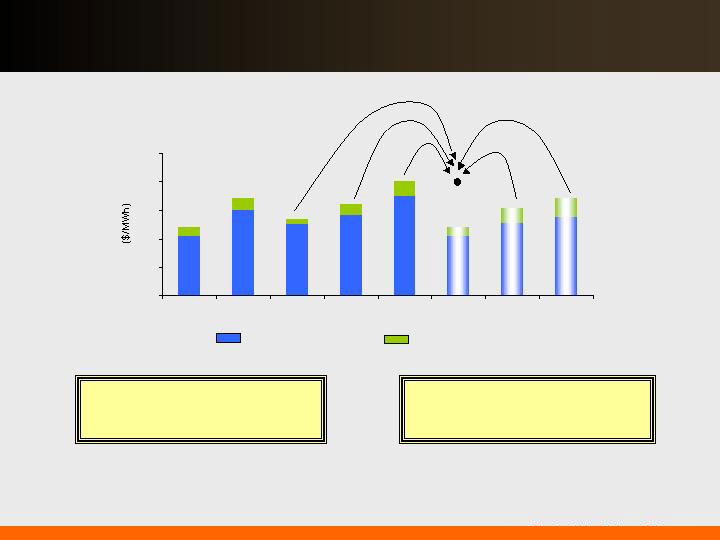

The effect of our hedging/forward sales strategy…

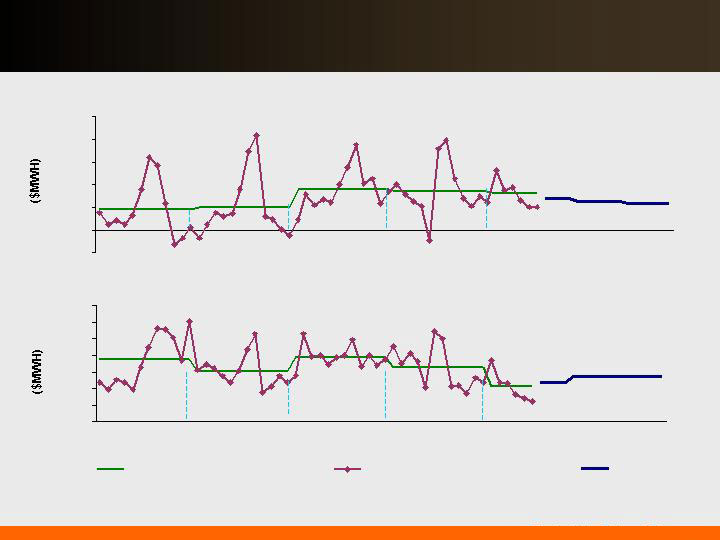

Power’s hedging strategy

secures pricing over a 2 - 3 year

future time horizon.

The 3 year BGS Auction period

has the effect of pulling forward

prices back.

… is to create a realized price that is a blend of prior and future pricing,

moderating volatility.

*PJM West Average of 6 historical months and 6 forward months

$0

$20

$40

$60

$80

$100

2004

2005

2006

2007

2008

2009 Fwd

2010 Fwd

2011 Fwd

PJM West

PS Zone vs PJM West Basis

2009 realized

price

*

Delivering Value: Today and Tomorrow

26

-$10

$0

$10

$20

$30

$40

$50

2005

2006

2007

2008

2009

2010

2011

$0

$10

$20

$30

$40

$50

$60

$70

2005

2006

2007

2008

2009

2010

2011

Annual Average

Historical Monthly

Forecast

Note: Forward prices as of 06/18/09

Spark spreads are in line with rising historical averages…

PJM Western Hub Spark Spread (On-Peak – Henry Hub * 7.5 Heat Rate)

PJM Western Hub Dark Spread (RTC – Central Appalachian Coal * 10 Heat Rate)

… but near term dark spreads have declined in response to weak demand.

Delivering Value: Today and Tomorrow

27

0%

25%

50%

75%

100%

2009

2010

2011

$40

$50

$60

$70

$80

$90

0%

25%

50%

75%

100%

2009

2010

2011

$0

$50

$100

$150

Power’s hedging program provides near-term stability from

market volatility…

… while remaining open to long-term market forces.

Estimated EPS impact of

$10/MWh PJM West around

the clock price change*

(~$2/mmbtu gas change)

Contracted Capacity

Estimated EPS impact of

$30/MW-day capacity

price change*

Price

(right

scale)

*As of June 2009; Assuming normal market commodity correlations

Power has

contracted at

attractive prices,

which includes

locational basis

and load shaping

premium.

The pricing for

most of Power’s

capacity has been

fixed through May

2013, with the

completion of

auctions in PJM

and NE.

% sold

(left

scale)

$0.25 - $0.45

$0.10 - $0.20

$0.01 - $0.02

$0.00 - $0.01

$0.00 - $0.01

$0.00 - $0.01

Contracted Energy

Price

(right

scale)

% sold

(left

scale)

Delivering Value: Today and Tomorrow

28

2012 / 2013 RPM Auction Results

PSEG Power’s assets are in

constrained zones, which

cleared at higher prices.

Power’s offer for 178MW of new

capacity was accepted by PJM.

Auction results reflect impact of

new transmission capability.

Delivering Value: Today and Tomorrow

29

… Power expects to see continued strong margins from PJM’s

Reliability Pricing Model.

Through the new capacity construct, and pricing at auction

prices…

$185.00

PSEG North Zone

$16.46

$110.00

$174.29

$102.04

$111.92

$40.80

Rest of Pool

$133.37

$110.00

$174.29

191.32

MAAC

$139.73

$110.00

$174.29

$191.32

$148.80

$197.67

Eastern MAAC

2012 / 2013

2011 / 2012

2010 / 2011

2009 / 2010

2008 / 2009

2007 / 2008

PJM Zones

With nearly 1/3 of its capacity in PS North and nearly 2/3 of its capacity in

MAAC and EMAAC, Power’s assets in congested locations received higher

pricing in the 2012/2013 RPM Auction.

PJM Capacity Available to Receive Auction Pricing

0

2,000

4,000

6,000

8,000

10,000

12,000

07/08

08/09

09/10

10/11

11/12

12/13

Delivering Value: Today and Tomorrow

30

Power’s coal hedging strategy is matched up with generation…

…with hedged coal pricing aligned with coal output sold.

$0

$10

$20

$30

$40

$50

2008

2009

2010

2011

Anticipated Coal Cost

(Cost/MWh)

Hedged

Open

Mid $20’s

Mid $20’s

Low $40’s

High $40’s/$50

To

High $30’s

High $40’s/$50

Indicative

Pricing

($/MWh)

Prices lower,

moderating

Northern

Appalachian

Conemaugh

Prices lower,

moderating

Northern

Appalachian

Keystone

More limited

segment of

coal market

Metallurgical

Mercer

Flexibility after

BET in 2010

Adaro /

Domestic

Hudson

Higher price,

lower BTU,

enviro coal

Adaro

Bridgeport

Harbor

Comments

Coal Type

Station

Delivering Value: Today and Tomorrow 31

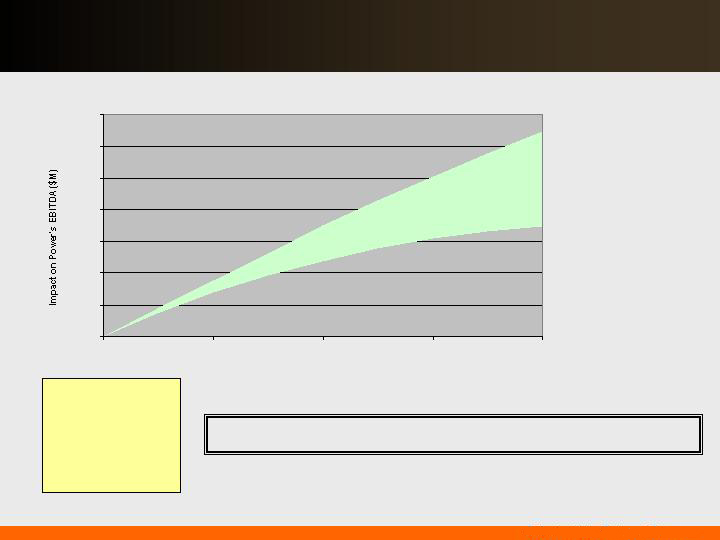

As national carbon regulation looks increasingly likely…

… Power should benefit based on its low carbon fleet.

The diversity of the portfolio makes Power well positioned to capture value in a

wide range of potential regulatory outcomes.

CO2 $/Ton Impact on PJM Prices and Power’s EBITDA

Illustration at $20 CO2:

(2008 Data)

55 TWh

x ~ $12 to $14/MWh

~ $660 – $770 M revenue

20M tons

x $20/ton

~ $400 M expense

The impact on electric

prices moderates at

higher CO2 prices as:

- the fleet dispatch

changes, and

- the CO2 intensity of

the grid goes down.

$0

$100

$200

$300

$400

$500

$600

$700

$0

$10

$20

$30

$40

CO2 Price ($/ton)

Delivering Value: Today and Tomorrow 32

2008 Operating

Earnings*

Energy

Capacity

Other Margin

Cost

2009 Guidance

… with visible sources of value to achieve this result.

Power’s commitment in 2009 reflects continued earnings

growth…

$1,107M

$1,210 -

$1,285M

$90 – 100M

($25 – 15M)

$88 – 133M

O&M (pension)

Depreciation

Other

($50 – 40M)

Power’s 2008 Operating Earnings vs 2009 Guidance

Operations

Uprates

BGS

Recontracting

Fuel

More capacity

open to auction

BGSS

Other

$2,170M EBITDA $2,350 - $2,450M

* See page 64 for Items excluded from Income from Continuing Operations to reconcile to Operating Earnings.

Delivering Value: Today and Tomorrow 33

… including market and operational factors.

Power’s earnings for 2010 will be subject to many influences…

$1,210 – $1,285M

Revenue/Margin

Nuclear output largely contracted

Dark Spread change of $5/MWh at market – impact

of $0.05-$0.10/share

Spark Spread change of $5/MWh at market –

impact of $0.05-$0.10/share

Capacity change of $30/MW-day – impact of $0.00-

$0.01/share

Operations

Operational excellence – 1% change in nuclear

capacity factor – impact of $0.01-$0.03/share

O&M 1% change – impact of ~$0.01/share

Depreciation increase of ~$0.03/share due to capital

in service

2009 Guidance

2010+ Drivers

Delivering Value: Today and Tomorrow 34

PSE&G - Review and Outlook

2008 earnings targets met

Transmission formula rate

treatment received from

FERC

Strong O&M control

Reduced Distribution capital

expenditures

National ReliabilityOne Award

winner

Earnings on track to meet

2009 guidance

Distribution base rate case

filed mid-2009

Transmission investment

increasing

New customer information

system implemented at end of

1st quarter

Active participant in shaping

State energy policy

Prepared to meet NJ’s

stimulus and energy goals

Resolve Distribution base rate

case by mid-2010

Investment program

responsive to NJ’s economic

and energy-related goals

Transmission formula rates

provide current return on

invested capital

Earnings growth in line with

capital investment

Continue to lead the nation in

electric reliability

PSE&G – Delivering Value: Today and Tomorrow

Delivering

Value Today

Positioned for

the Future

Meeting

Commitments

Delivering Value: Today and Tomorrow 36

PSE&G regulatory strategy…

Earn authorized returns

Minimize regulatory lag

Support state energy goals

Maintain/enhance local relationships

…designed to support customer and shareholder requirements.

Delivering Value: Today and Tomorrow 37

New Jersey Electric & Gas Rate Case*

Filed: May 29, 2009

Test Year: 2009**

51.2%

Equity Ratio

11.5%

Return on Equity

*New Jersey BPU decision anticipated within 9-12 months.

**Test year can be updated for known changes.

$2.4 billion

$3.8 billion

Rate Base

$96.9 million

$133.7 million

Increase

Gas

Electric

Request

Delivering Value: Today and Tomorrow 38

PSE&G’s current investment plan including the

recently approved state capital stimulus …

34%

51%

15%

0%

31%

1%

19%

49%

33%

17%

1%

49%

… now provides for growth in rate base of 11%.

PSE&G Rate Base

29%

23%

1%

47%

Electric Transmission

Electric Distribution

Gas Distribution

Energy Master Plan

2008

Rate Base $6.9B

Equity Ratio ~ 50%

2009

Rate Base $7.6B

Equity Ratio ~ 51%*

2010

Rate Base $8.6B

Equity Ratio ~ 51%*

2011

Rate Base $9.4B

Equity Ratio ~ 51%*

*Pending regulatory approval

Delivering Value: Today and Tomorrow

39

$0

$100

$200

$300

$400

2009

2010

2011

Energy Efficiency Stimulus

Solar II

Solar 4 All

… would result in rate base growth of 12%.

PSE&G Annual Potential Capital Investments

Rate Base Including Potential Investments

31%

4%

18%

47%

28%

22%

5%

45%

Electric Transmission

Electric Distribution

Gas Distribution

Energy Master Plan

$9.8B

$8.8B

2011

2010

An additional ~$0.7B of

investments to be added

2009-2011 if appropriate

regulatory treatment is

received

Filed positions:

• 10.3% ROE

• 51% Equity Ratio

PSE&G’s additional investment proposals …

Delivering Value: Today and Tomorrow

40

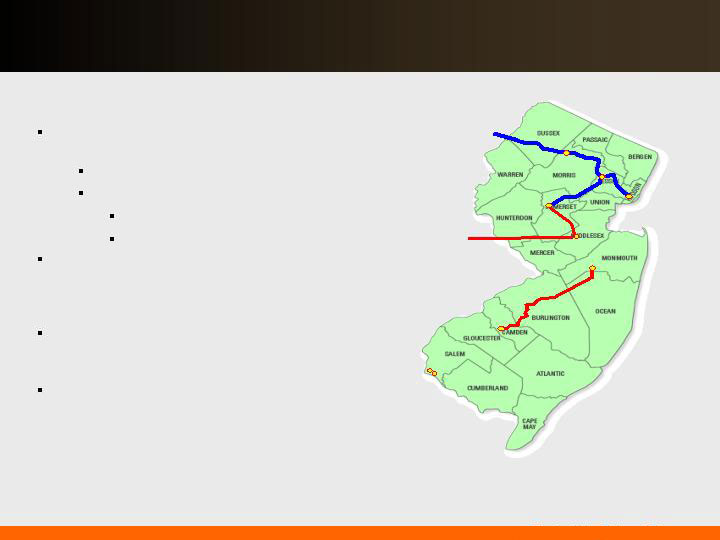

Transmission Growth

PJM approved the $750M Susquehanna to

Roseland line in October 2007

Siting and permitting process underway

Incentives approved by FERC:

ROE: 12.93% (125 basis point adder)

100% CWIP in Rate Base

FERC approval of Sub-Transmission to

Transmission system reliability investments

represents about $340M through 2011, post-2011

~$60M per year

Other approved RTEP projects ~$250M also

contribute meaningfully to improved reliability and

earnings growth

PJM approved the Branchburg-Roseland-Hudson

line in November 2008. Additional 500 kV

investments brings potential capital expenditures to

approximately $1.0 -1.5B

These opportunities will require substantial deployment of capital with siting and

permitting as the major challenges.

Branchburg

Roseland

Jefferson

New Freedom

Smithburg

Deans

MAPP

Hope Creek

Salem

Project

I-765

Interstate

Project

PSE&G implemented fully-forecasted formula rates with an 11.68%

base ROE, which provides attractive current return on investments.

Delivering Value: Today and Tomorrow

41

2008 Regulatory Activities

A.

Solar Loan Program

($105M)

Approved April 2008

Up to 30MW

B.

Demand Response

($63M)

Filed August 2008. Decision

pending

Reduce demand by residential

and small commercial

customers by 150MW

C.

Carbon Abatement

Program ($47M)

Approved December 2008

Provides energy efficiency

programs

A

C

B

2009 Regulatory Activities

D.

Capital Economic Stimulus Infrastructure Investment

Program ($694M)

Filed January 2009, approved April 2009; 10.0% ROE

Accelerate capital investments to promote economic stimulus and

promote job growth in NJ

E.

Solar Loan Program – Phase II

Filed March 2009

F.

Electric and Gas Distribution base

rate case

Filed May 2009

G.

Energy Efficiency Economic Stimulus Program

($200M)

Filed January 2009, expected BPU decision by mid-year 2009

Promote job growth and stimulate NJ economy via energy

efficiency expenditures

H.

Solar 4 All ($800M)

Filed February 2009, expected BPU decision by August 2009

120MW of utility-owned solar generation

D

E

G

H

I

2010 Regulatory Activities

I.

Resolve Electric and

Gas Distribution

base rate case

Normal BPU schedule would

have resolution of rate

proceeding by mid-2010

2011 will be first full year of

rate relief

2008

2009

2010

May

Dec

Dec

Jan

Jan

Jun

F

… with a manageable rate increase of 2% - 4% to customers.

$215M Filed

PSE&G is well positioned to respond to NJ’s needs…

Delivering Value: Today and Tomorrow

42

18.5

0

2

4

6

8

10

12

14

16

18

20

PSE&G

Average

2011

Based on tariff rates in effect in Nov 2008, does not include effects of the BGSS decreases effective Jan 1, 2009 and March 1, 2009.

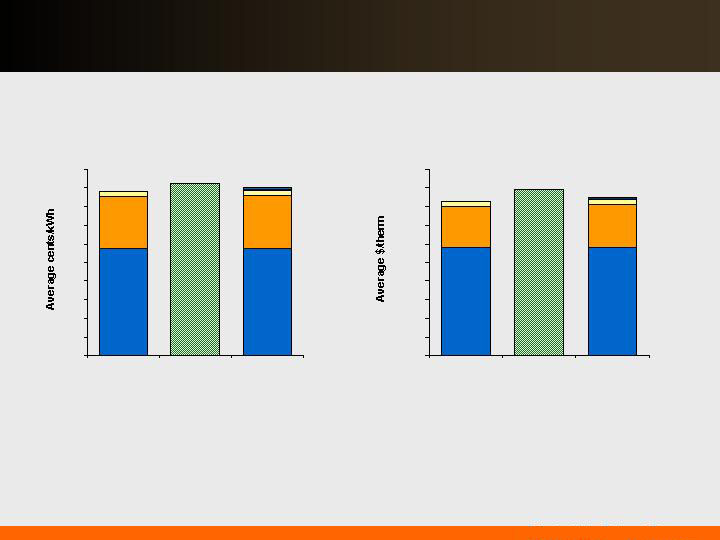

… produces superior value to our electric and gas customers.

Electricity

(500kWh/month bill)

BGS

Delivery

Clauses

17.7

1.79

0.00

0.20

0.40

0.60

0.80

1.00

1.20

1.40

1.60

1.80

2.00

PSE&G

Average

2011

Gas

(100 therm/month bill)

BGSS

Delivery

Clauses

1.65

Source: Rates from PSE&G, NYPSC and PAPUC

1.70

BGSS

Delivery *

Clauses

BGS***

Delivery *

Clauses

Potential

Investments**

18.1

* Includes base rate increases

** Includes NJ stimulus filing (Capital and EEE), Solar 4 All and Solar II

Potential

Investments**

*** Assumes BGS/BGSS pricing remains constant

Combining operational excellence with prices comparable to

regional competitors …

Delivering Value: Today and Tomorrow 43

2008 Operating

Earnings*

Weather

Transmission

Pension

Depreciation,

Interest and Other

2009 Guidance

$360M

$5 - 10M

$320 –

$345M

$10 - 15M

… increasing pension, depreciation and interest costs.

($40 - 35M)

($15 - 5M)

In 2009, controlling O&M will mitigate the effects of…

*See page 64 for Items excluded from Income from Continuing Operations to reconcile to Operating Earnings

Delivering Value: Today and Tomorrow 44

PSE&G – Business Drivers

Operational excellence and effective cost

management

Distribution rate case should improve 2009 ROE’s

of 8.0% - 8.8% to 9.0% - 9.5%

Addresses capital investment, O&M and sales

losses

1% change in Distribution rate case ROE for

2010 = ~$21M change in earnings

Transmission Investment under formula rates. ROE

~ 11.7%

Capital Stimulus could provide an additional 25 – 50

basis points to ROE

Energy Master Plan investments for Energy

Efficiency and Renewables could provide an

additional 5 – 10 basis points to ROE if approved as

planned.

A ±1% deviation in sales would result in a ±$15M

change to margin revenues

$320 – $345M

2009 Guidance

2010+ Drivers

Delivering Value: Today and Tomorrow 45

PSEG Energy Holdings -

Review and Outlook

PSEG Energy Holdings – Delivering Value: Today and Tomorrow

Exceeded 2008 earnings

targets

Strong 2008 Texas

performance well above

expectations

Stable earnings from

US contracted

generation assets

Sale of international assets

yielded $1.5B over 2007-

2008

Proactively reserved for

potential LILO/SILO liability

Earnings on track to meet

2009 guidance

Achieving predictable

performance from

contracted US generation

assets

Improving Texas

operations via asset

management agreement

with PSEG Power

Redeemed approximately

$280M of Texas project

debt in the first quarter of

2009

Managing risk by limiting

growth in lease tax liability

Sufficient liquidity and credit

strength to fund potential

LILO/SILO liability through

cash, asset value and debt

capacity

Exploring opportunities to

optimize other U.S. assets

Pursuing attractive

renewable generation

opportunities

Compressed Air Energy

Storage (CAES)

Solar

Offshore Wind

Meeting

Commitments

Delivering

Value Today

Positioned for

the Future

Delivering Value: Today and Tomorrow 47

By reducing its investment in international assets …

… Holdings has decreased its risk profile and improved its

business focus.

$0.4

$0.5

$0.5

$0.8

$2.2

$1.4

$0.1

2004

2006

2008

2009 Projected*

PSEG Global Invested Capital

($ Billions)

$2.6B

$1.9B

$0.6B

$0.8B

*Investment Includes redemption of Texas debt in February 2009

International

Domestic

Delivering Value: Today and Tomorrow 48

Texas assets are the major driver of PSEG Global’s business

results…

…PSEG Texas projected EBITDA reflects higher maintenance costs and

market uncertainty.

Strong 2008 performance from favorable market in Spring 2008

Looking ahead to 2009:

Uncertainty on gross margin impact from new wind additions

Operations and maintenance costs approximately $20M higher in 2009 than 2007 as

plants enter periods of major maintenance

Longer-term:

Continued uncertainty from wind

Positive impact from transmission build-up and potential unit mothballing by other

generators

70 – 80

35 – 45%

135 – 145

16%

4.0 - 5.0

2009

PSEG

Market

214

162

$186

Gross

Margin ($M)

147

47.9%

14%

9.0

2008

104

48.7%

15%

6.9

2007

$130

54.4%

16%

$6.7

2006

EBITDA*

($M)

Capacity

Factors

Reserve

Margin

Nat. Gas

Henry Hub Spot

($/mmBtu)

*Excluding Mark-to-Market Accounting effects

Delivering Value: Today and Tomorrow 49

Holdings is focused on managing its current investment

portfolio.

Net Investment in lease portfolio of $0.3B*.

Book investment of $2.3B less deferred taxes of $2.0B

Assuming 100% litigation loss, the lease portfolio would generate

$2.1B* of after-tax cash over the remaining life of the portfolio.

Net present value of after tax cash flow using 8% discount rate

would be approximately $800M.

Reached agreement on termination of several international leases

reducing portfolio by $76M.

Redeemed $280M of non-recourse debt at Texas facilities;

repurchased $10M of Energy Holdings senior notes.

Projected earnings for 2009 reflect reduced LILO/SILO lease income

pending IRS resolution.

* As of 12/31/08

Delivering Value: Today and Tomorrow 50

2008 Operating

Earnings*

Texas Margin

and Major

Maintenance

Texas Project

Financing Paid

Off

Interest & Other

Global Taxes

Resources

Lease Income &

LILO/SILO

Interest

Resources

Interest, G&A,

Other & Taxes

2009 Guidance

PSEG Energy Holdings – 2009 Earnings Drivers

$99M

$0 – 20M

($50 - 40M)

($4 - 2M)

$17M

($20 - 16M)

($31 - 29M)

($11 - 9M)

Holdings 2008 Operating Earnings vs 2009 Guidance

* See page 64 for Items excluded from Income from Continuing Operations to reconcile to Operating Earnings.

Delivering Value: Today and Tomorrow 51

PSEG Energy Holdings – Business Drivers

$0 – 20M

2009 Guidance

2010+ Drivers

Sale of remaining international assets

(Book value $9M)

Continued defense of LILO/SILO lease

position with improved return post-

resolution

Focused management of domestic

contracted generation portfolio

Support of 2009 joint venture Energy

Storage & Power in efforts to license CAES

2 technology

Pursuit of renewable development with

focus on Solar and Offshore Wind

Texas Spark Spread change of ±$5/MWh at

market – impact of approximately

$0.03/share

Delivering Value: Today and Tomorrow 52

Appendix

Q1 2009 Earnings Summary

13

-

Discontinued Operations, Net of Tax

$ 0.86

$ 0.95

EPS from Operating Earnings*

448

444

Net Income

435

444

Income from Continuing Operations

(3)

(38)

Reconciling Items, Net of Tax

$ 438

$ 482

Operating Earnings

2008

2009

$ millions (except EPS)

Quarter ended March 31,

* See page 64 for Items excluded from Income from Continuing Operations to reconcile to Operating Earnings.

Delivering Value: Today and Tomorrow

54

Q1 Operating Earnings by Subsidiary

$ 438

(5)

28

136

$ 279

2008

$ 482

(4)

4

123

$ 359

2009

Operating Earnings

Earnings per Share

(0.01)

(0.01)

Enterprise

$ 0.86

$ 0.95

Operating Earnings*

0.06

0.01

PSEG Energy Holdings

0.26

0.24

PSE&G

$ 0.55

$ 0.71

PSEG Power

2008

2009

$ millions (except EPS)

Quarter ended March 31,

* See page 64 for Items excluded from Income from Continuing Operations to reconcile to Operating Earnings.

Delivering Value: Today and Tomorrow

55

PSEG Power’s asset mix and dispatch profile …

7,265

7,817

3,659

2,679

2,776

2,621

0

5,000

10,000

15,000

2008

2009

Quarter ended March 31,

Total Nuclear

Total Coal*

Total Oil &

Natural Gas

PSEG Power – Generation (GWh)

13,700

13,117

Generation declined 4.3%.

Nuclear fleet capacity factors:

NJ fleet operated at 99.3% in

Q1 2009 vs 91.0% in Q1

2008.

Nuclear fleet capacity factor

of 97.8% in Q1 2009 vs

94.1% in Q1 2008.

Nuclear generation increase

of 7.6% supported by

uprates in capacity at Hope

Creek and Salem.

Gas units displaced coal in Q1

2009 with decline in gas prices

and higher than expected

demand in January.

… supported Q1’s strong results.

* Includes figures for Pumped Storage

Delivering Value: Today and Tomorrow

56

$30.60

55,300

$1,693

129

$1,564

1,141

423

2008

$24.50

53,197

$1,305

122

$1,183

847

336

2007

Year ended December 31,

$ / MWh

Total Generation

(GWhr)

Total Fuel Cost

Nuclear

Total Fossil

Oil & Gas

Coal

($ millions)

174

242

94

115

$23.20

$28.30

13,117

13,700

$304

$388

36

31

$268

$357

2009

2008

Quarter ended March 31,

PSEG Power – Fuel Costs

Q1 2009 fuel costs reflect:

Dispatch flexibility

Decline in gas prices

Increase in nuclear generation

Delivering Value: Today and Tomorrow 57

Operated by PSEG Nuclear

PSEG Ownership: 100%

Technology:

Boiling Water Reactor

Total Capacity: 1,211MW

Owned Capacity: 1,211MW

License Expiration: 2026

Operated by PSEG Nuclear

Ownership: PSEG - 57%,

Exelon – 43%

Technology:

Pressurized Water Reactor

Total Capacity: 2,345MW

Owned Capacity: 1,346MW

License Expiration: 2016 and

2020

Operated by Exelon

PSEG Ownership: 50%

Technology:

Boiling Water Reactor

Total Capacity: 2,224MW

Owned Capacity: 1,112MW

License Expiration: 2033

and 2034

Hope Creek

Salem Units 1 and 2

Peach Bottom Units 2 and 3

Our five unit nuclear fleet …

… is a critical element of Power’s success.

Delivering Value: Today and Tomorrow 58

The implementation of carbon will address the critical issue of global

warming…

~$12.00 - ~$14.00

100%

Total

$0.00

$0.00

0%

Nuclear

$4.80 - $3.60

$8.00

60%- 45%

Gas CC

$1.20 - $0.60

$12.00

10% - 5%

CTs

$6.00 - $10.00

$20.00

30% - 50%

Coal

Impact

$/MWh

On margin

(approximate)

Dispatch curve implication @ $20/ton*

By Fuel Type

$12.0

$18.0

$30.0

@$30

$8.0

$12.0

$20.0

@$20

$4.0

$6.0

$10.0

@$10

Price ($/MWh)

0.4

0.6

1.0

Carbon tons/MWh

CC

CTs

Coal

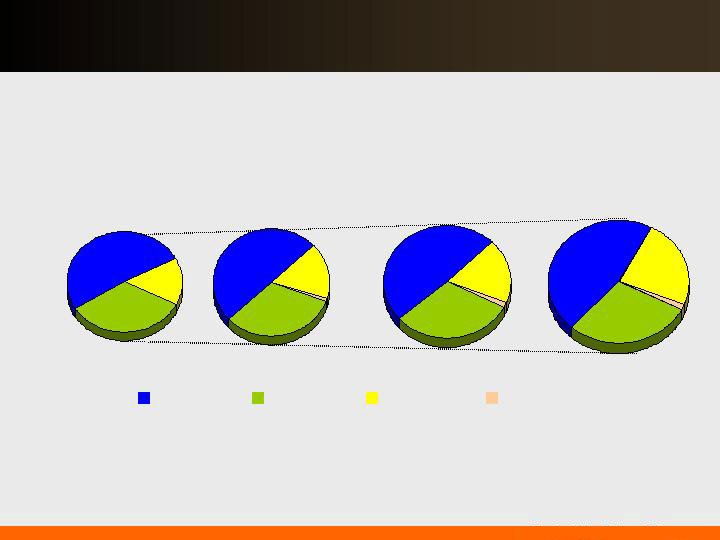

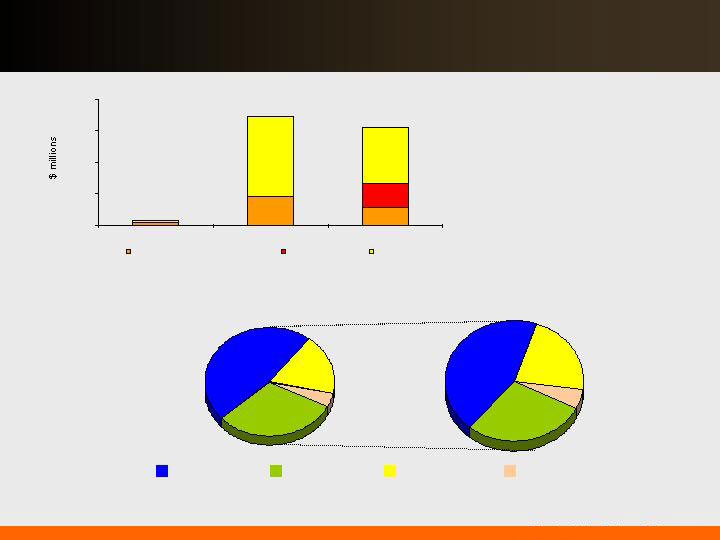

PSEG Power Generation by Fuel

… and activity continues in the direction of a national program.

*For illustration purposes – potential impact of CO2 on power prices with current dispatch – not an indication of net effect on income.

Energy Produced – 2008

53%

23%

23%

Nuclear

Coal

Gas

Total GWh: 55,300

Pumped Storage

& Oil 1%

Delivering Value: Today and Tomorrow 59

The RGGI cap on CO2 emission shows that headroom exists …

… compared to historical emission levels.

Affected Sources

Fossil-fired electric generating

units with a capacity of 25MW

and larger

Targets and Timing

Three-year compliance periods

with the first running from 2009-

2011

Stabilization of CO2 emissions at

recent levels through 2015

(~188 million tons per year)

Achieve a 10% reduction of CO2

emissions below recent levels by

2019

This translates into ~13%

reduction below 1990 levels or

~35% reduction from Business

as Usual (BAU) levels by 2020

CO

2

Emissions vs. RGGI Cap

(Actuals through 2007)

130

140

150

160

170

180

190

200

2000

2002

2004

2006

2008

2010

2012

2014

2016

2018

RGGI Cap

Projected

Actual &

Forecast CO

2

Actual

Delivering Value: Today and Tomorrow 60

Proposed energy efficiency investment and savings

Investment Timeline

2009 – 2011 (18 months)

Delivering Value: Today and Tomorrow 61

Category

Investment

Annual

Lifetime

Annual

Lifetime

Jobs

Residential

($ millions)

Whole House

$25

5,428

86,847

27,587

551,744

120

Multi-Family

25

5,428

86,847

27,587

551,744

60

10,856

173,694

55,174

1,103,488

180

Industrial & Commercial

Small Business

20

35,897

538,462

74,359

1,115,385

80

Muni/Local/State Government

35

49,595

743,927

82,186

1,232,794

143

Hospital Efficiency

35

73,200

1,098,000

748,466

11,226,994

140

Data Center

12

38,400

576,000

147,239

2,208,589

50

Tech Demo Sub-Program

12

18,947

284,210

192,000

2,880,000

50

Building

2

3,750

56,250

38,462

576,923

8

219,789

3,296,849

1,282,712

19,240,685

471

Admin Sales, Training, Evaluation, IT

24

TOTAL

$190

230,645

3,470,543

1,337,886

20,344,173

651

Savings (MWh)

Savings (Dtherms)

Rate Mechanism

PSE&G proposes to recover the costs of the program through

an annual adjustment to electric and gas rates which would

not exceed 1%.

The cost of capital would be based on a capital structure

consisting of 51.2% common equity with a return on common

equity of 10.3%--consistent with the return allowed NJNG in

its December 2008 base rate case decision.

The Energy Efficiency Program revenue requirements would

include the recovery of lost distribution margin.

Delivering Value: Today and Tomorrow 62

PSE&G Solar 4 All Proposal

Neighborhood Solar (40 megawatts) - $264M investment

Solar panels on utility poles and street lights in neighborhoods throughout

PSE&G’s service territory.

Local Government Solar (43 megawatts) - $273M investment

Solar, owned and operated by PSE&G, on municipal and public school district

facilities. Local governments will receive a credit on their utility bill equal to the

amount of energy generated by the system.

Centralized Solar (35 megawatts) – $221M investment

Solar systems on PSE&G land/buildings.

Solar energy farms on brownfields, non-profit-owned real estate, and

underdeveloped real estate

HMFA/Affordable Housing Solar (2 megawatts) - $15M investment

Solar on New Jersey Housing and Mortgage Finance Agency (HMFA)-financed

or other affordable housing communities

PSE&G is seeking a 10.3% ROE on its equity capital invested (51.2% common equity

in its capital structure). Customer rate impact mitigated by benefits associated with ITC

and the value of electricity and Solar Renewable Energy Certificates (SRECs)

generated by the projects

NJ BPU has 180 days to respond.

Delivering Value: Today and Tomorrow 63

Items Excluded from Income from Continuing Operations

to Reconcile to Operating Earnings

Please see Slide 3 for an explanation of PSEG’s use of Operating Earnings as a non-GAAP financial measure and how

it differs from Net Income.

Pro-forma Adjustments, net of tax

2009

2008

2008

2007

Earnings Impact (in Millions)

Impairment of PPN

-

$

-

$

(9)

$

(2)

$

Impairment of Turboven

-

-

(4)

(7)

Loss on Sale of Chilquinta and Luz del Sur

-

-

-

(23)

Nuclear Decommissioning Trust (NDT) Fund Related Activity

(23)

(7)

(71)

12

Mark-to-Market (MTM)

(15)

5

16

10

Premium on Bond Redemption

-

(1)

(1)

(28)

Lease Reserves

-

-

(490)

-

Total Pro-forma to Operating Earnings

(38)

$

(3)

$

(559)

$

(38)

$

Fully Diluted Average Shares Outstanding (in Millions)

507

510

508

509

Per Share Impact (Diluted)

Impairment of PPN

-

$

-

$

(0.02)

$

-

$

Impairment of Turboven

-

-

(0.01)

(0.01)

Loss on Sale of Chilquinta and Luz del Sur

-

-

-

(0.05)

Nuclear Decommissioning Trust (NDT) Fund Related Activity

(0.04)

(0.02)

(0.14)

0.02

Mark-to-Market (MTM)

(0.03)

0.01

0.03

0.02

Premium on Bond Redemption

-

-

-

(0.06)

Lease Reserves

-

-

(0.96)

-

Total Pro-forma to Operating Earnings

(0.07)

$

(0.01)

$

(1.10)

$

(0.08)

$

December 31,

For the Quarters Ended

March 31,

PUBLIC SERVICE ENTERPRISE GROUP INCORPORATED

Reconciling Items Excluded from Continuing Operations to Compute Operating Earnings

(Unaudited)

For the Twelve Months Ended

Delivering Value: Today and Tomorrow

64