Forward-Looking Statement 2 EXHIBIT 99 Certain of the matters discussed in this report about our and our subsidiaries' future performance, including, without limitation, future revenues, earnings, strategies, prospects, consequences and all other statements that are not purely historical constitute “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995. Such forward-looking statements are subject to risks and uncertainties, which could cause actual results to differ materially from those anticipated. Such statements are based on management's beliefs as well as assumptions made by and information currently available to management. When used herein, the words “anticipate,” “intend,” “estimate,” “believe,” “expect,” “plan,” “should,” “hypothetical,” “potential,” “forecast,” “project,” variations of such words and similar expressions are intended to identify forward-looking statements. Factors that may cause actual results to differ are often presented with the forward- looking statements themselves. Other factors that could cause actual results to differ materially from those contemplated in any forward-looking statements made by us herein are discussed in filings we make with the United States Securities and Exchange Commission (SEC), including our Annual Report on Form 10-K and subsequent reports on Form 10-Q and Form 8-K and available on our website: http://www.pseg.com. These factors include, but are not limited to: adverse changes in the demand for or the price of the capacity and energy that we sell into wholesale electricity markets, adverse changes in energy industry law, policies and regulation, including market structures and transmission planning, any inability of our transmission and distribution businesses to obtain adequate and timely rate relief and regulatory approvals from federal and state regulators, changes in federal and state environmental regulations and enforcement that could increase our costs or limit our operations, changes in nuclear regulation and/or general developments in the nuclear power industry, including various impacts from any accidents or incidents experienced at our facilities or by others in the industry, that could limit operations of our nuclear generating units, actions or activities at one of our nuclear units located on a multi-unit site that might adversely affect our ability to continue to operate that unit or other units located at the same site, any inability to manage our energy obligations, available supply and risks, adverse outcomes of any legal, regulatory or other proceeding, settlement, investigation or claim applicable to us and/or the energy industry, any deterioration in our credit quality or the credit quality of our counterparties, availability of capital and credit at commercially reasonable terms and conditions and our ability to meet cash needs, changes in the cost of, or interruption in the supply of, fuel and other commodities necessary to the operation of our generating units, delays in receipt of necessary permits and approvals for our construction and development activities, delays or unforeseen cost escalations in our construction and development activities, any inability to achieve, or continue to sustain, our expected levels of operating performance, any equipment failures, accidents, severe weather events or other incidents that impact our ability to provide safe and reliable service to our customers, and any inability to obtain sufficient insurance coverage or recover proceeds of insurance with respect to such events, acts of terrorism, cybersecurity attacks or intrusions that could adversely impact our businesses, increases in competition in energy supply markets as well as for transmission projects, any inability to realize anticipated tax benefits or retain tax credits, challenges associated with recruitment and/or retention of a qualified workforce, adverse performance of our decommissioning and defined benefit plan trust fund investments and changes in funding requirements, changes in technology, such as distributed generation and micro grids, and greater reliance on these technologies, and changes in customer behaviors, including increases in energy efficiency, net-metering and demand response. All of the forward-looking statements made in this report are qualified by these cautionary statements and we cannot assure you that the results or developments anticipated by management will be realized or even if realized, will have the expected consequences to, or effects on, us or our business prospects, financial condition or results of operations. Readers are cautioned not to place undue reliance on these forward-looking statements in making any investment decision. Forward-looking statements made in this report apply only as of the date of this report. While we may elect to update forward-looking statements from time to time, we specifically disclaim any obligation to do so, even if internal estimates change, unless otherwise required by applicable securities laws. The forward-looking statements contained in this report are intended to qualify for the safe harbor provisions of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended. |

GAAP Disclaimer These materials and other financial releases can be found on the pseg.com website under the investor tab, or at http://investor.pseg.com/ PSEG presents Operating Earnings and Adjusted Earnings Before Interest, Taxes, Depreciation and Amortization (EBITDA) in addition to its Income from Continuing Operations/Net Income reported in accordance with accounting principles generally accepted in the United States (GAAP). Operating Earnings and Adjusted EBITDA are non-GAAP financial measures that differ from Income from Continuing Operations/Net Income. Operating Earnings exclude gains or losses associated with Nuclear Decommissioning Trust (NDT), Mark-to-Market (MTM) accounting, and other material one-time items. PSEG presents Operating Earnings because management believes that it is appropriate for investors to consider results excluding these items in addition to the results reported in accordance with GAAP. PSEG believes that the non-GAAP financial measure of Operating Earnings provides a consistent and comparable measure of performance of its businesses to help shareholders understand performance trends. PSEG is presenting Adjusted EBITDA because it provides investors with additional information to compare our business performance to other companies and understand performance trends. Adjusted EBITDA excludes the same items as our Operating Earnings measure as well as income tax expense, interest expense, depreciation and amortization and major maintenance expense costs at Power’s fossil generation facilities. This information is not intended to be viewed as an alternative to GAAP information. The last three slides in this presentation (Slides A, B and C) include a list of items excluded from Income from Continuing Operations/Net Income to reconcile to Operating Earnings and Adjusted EBITDA with a reference to that slide included on each of the slides where the non-GAAP information appears. 3 |

** ** Operating Earnings Disciplined investment program and focus on operational excellence have supported growth Power’s diverse fuel mix and dispatch flexibility continue to generate strong earnings and free cash flow in low price environment PSE&G’s investment program has driven double digit compound annual earnings growth since 2010 Operating Earnings* Contribution by Subsidiary *SEE SLIDE A FOR ITEMS EXCLUDED FROM INCOME FROM CONTINUING OPERATIONS/ NET INCOME TO RECONCILE TO OPERATING EARNINGS. E=ESTIMATE ** 2015 PERCENTS USE MIDPOINT OF EARNINGS GUIDANCE. 8 |

• NJ Capital Infrastructure Program 1 (CIP 1) – 2009 • NJ Capital Infrastructure Program 2 (CIP 2) – 2011 • Energy Strong – 2014 • Carbon Abatement – 2008 • Demand Response – 2009 • Energy Efficiency (EE) – 2009 • EE Extension – 2011 • EE Extension II – 2015 • Solar Loan I – 2008 • Solar Loan II – 2009 • Solar 4 All – 2009 • Solar Loan III – 2013 • Solar 4 All Ext – 2013 PSE&G has successfully worked with regulators to develop multiple solutions for New Jersey’s energy and economic development goals 30 RENEWABLES creative solutions to install solar generation ENERGY EFFICIENCY assisting customers with controlling energy usage DISTRIBUTION improving electric and gas delivery infrastructure |

Extension of PSE&G’s award winning Energy Efficiency program • Energy Efficiency Extension II approved by the BPU in April 2015 will extend the investment and time frame for three previously approved programs already in the marketplace, allowing PSE&G to factor in lessons learned and balance policy issues • $95M of rate base investment approved at an ROE of 9.75% • Extends existing programs, two of which have sizable waiting lists: • Hospitals • Multifamily • Direct install – government, non-profit, and small business • Would allow PSE&G to leverage past investments in people, capabilities, systems and processes 33 |

PSE&G’s 2015 operating earnings expected to benefit from increased investment in Transmission *SEE SLIDE A FOR ITEMS EXCLUDED FROM NET INCOME TO RECONCILE TO OPERATING EARNINGS. E =ESTIMATE. DATA AS OF MARCH 2, 2015. 37 |

Shasta A & B California (4 MW) COD March 2014 Polycrystalline - single axis Investment $13 million 20 year PPAs with PG&E Hackettstown (Mars) New Jersey (2 MW) COD September 2009 Thin film panels – fixed tilt Investment $13 million 15 year PPA with Mars, Inc. Wyandot Ohio (12 MW) COD May 2010 Thin film panels – fixed tilt Investment $44 million 20 year PPA with AEP JEA Florida (15 MW) COD September 2010 Thin film panels – fixed tilt Investment $59 million 30 year PPA with JEA Queen Creek Arizona (25 MW) COD October 2012 Polycrystalline - single axis Investment $75 million 20 year PPA with SRP Milford Delaware (15 MW) COD December 2012 Polycrystalline - fixed tilt Investment $47 million 20 year PPA with DEMEC Badger I Arizona (19 MW) COD November 2013 Polycrystalline - single axis Investment $48 million 30 year PPA with APS PSEG Solar Source owns ~123 MW of solar facilities * with long term contracted revenues Newman Texas (13 MW) COD December 2014 Polycrystalline - single axis Investment $22 million 30 year PPA with El Paso Elec. Whitcomb Vermont (4 MW) COD October 2014 Polycrystalline – fixed tilt Investment $10 million 25 year PPA with VT Electric Power Producers, Inc. *PROJECT SIZE IN MEGAWATTS SHOWN IN DC (DIRECT CURRENT), AC EQUIVALENT IS 96 MEGAWATTS. E=ESTIMATE. In Construction – Rockfish Maryland (13 MW) COD - June 2015E Polycrystalline - single axis 20 year PPA with SMECO 61 |

Power’s 2015 operating earnings maintain solid performance Power Operating Earnings* ($ Millions) 2015 Observations • 75-80% hedged at $52/MWh • Increase in average hedge price for energy helps mitigate reset in capacity price and volume * SEE SLIDE A FOR ITEMS EXCLUDED FROM NET INCOME TO RECONCILE TO OPERATING EARNINGS. E = ESTIMATE. 66 |

Market Review: Winter Z6 gas prices retain seasonal volatility; spark spreads have continued to be robust in PJM FORWARDS AS OF APRIL 30, 2015 2015 YTD Z6 PJM West vs. PS Zone Spark Spreads (2013-2018) 2015-2018 Z6 70 |

Regulatory Framework: Significant reforms already implemented and new rules being promulgated to improve energy and capacity market designs ISSUE /POLICY OUTCOME PJM CAPACITY • Higher payments for enhanced reliability (Capacity Performance) DEMAND RESPONSE RULES • Stricter rules for eligibility and deployment ENERGY PRICE FORMATION • PJM and FERC forcing improvements to energy price formation; higher caps ISO-NE CAPACITY • Higher prices in recent auction better reflect tight supply conditions • Implementation of sloping demand curve in FCA 9 • Zonal demand curves expected in FCA 10 ENERGY • Demand response required to participate in Day Ahead markets • Implemented hourly offers/real time reoffers • Reserve market prices better reflect scarcity prices • 5 minute interval LMP settlements expected Q1 2016 NYISO CAPACITY • New Capacity Zone (LHV) leads to more accurate price signals ENERGY • Improvement in price formation during reserve shortage conditions FEDERAL DEMAND RESPONSE • EPSA VS. FERC and national implications; US Supreme Court will hear case ENVIRONMENTAL REGULATIONS • HEDD, CPP, HAPS/MACT will lead to tightening of supply in 2015+ timeframe 73 |

PJM Capacity Performance Proposal: aims to increase electric supply reliability • Capacity performance (CP) proposal places emphasis on reliability, given observed outages during times of extreme weather stress and anticipated retirements; Imposition of higher penalty structure and enhanced opportunities for cost recovery to encourage reliability • Elimination of 2.5% holdback offsetting weak demand growth, making all capacity resources annual products in end state, net CONE bidding safe harbor, and the change in the demand curve (VRR) support price formation and improve resource adequacy • Generator performance/flexibility is key objective for units with secure fuel supply capable of meeting more stringent operating standards 74 |

HEDGE PERCENTAGES AND PRICES AS OF MARCH 31, 2015. REVENUES OF FULL REQUIREMENT LOAD DEALS BASED ON CONTRACT PRICE, INCLUDING RENEWABLE ENERGY CREDITS, ANCILLARY, AND TRANSMISSION COMPONENTS BUT EXCLUDING CAPACITY. HEDGES INCLUDE POSITIONS WITH MTM ACCOUNTING TREATMENT AND OPTIONS. EXCLUDES SOLAR AND KALAELOA. Apr-Dec 2015 2016 2017 Volume TWh 26 37 37 Base Load % Hedged 100% 80-85% 40-45% (Nuclear and Base Load Coal) Price $/MWh $52 $51 $52 Volume TWh 17 20 20 Intermediate Coal, Combined % Hedged 30-35% 0% 0% Cycle, Peaking Price $/MWh $52 -- -- Volume TWh 41-43 55-57 55-57 Total % Hedged 70-75% 50-55% 25-30% Price $/MWh $52 $51 $52 Hedging strategy: designed to protect gross margin while leveraging the portfolio 80 |

PSEG 2015 Guidance for Operating Income – by Subsidiary and PSEG Power Adjusted EBITDA PSEG Power Adjusted EBITDA** $ millions (except EPS) 2015E 2014 PSEG Power $1,545 - $1,645 $1,584 * SEE SLIDE A FOR ITEMS EXCLUDED FROM NET INCOME TO RECONCILE TO OPERATING EARNINGS; INCLUDES THE FINANCIAL IMPACT FROM MARK-TO-MARKET POSITIONS WITH FORWARD DELIVERY MONTHS. ** SEE SLIDE B FOR A RECONCILIATION OF ADJUSTED EBITDA TO OPERATING EARNINGS AND NET INCOME. E = ESTIMATE. 96 |

PSEG Summary • Our 2014 earnings of $2.76 exceeded our revised operating earnings guidance of $2.60 - $2.75 per share • Continued third year of anticipated positive earnings trend in 2015 with operating earnings guidance of $2.75 to $2.95 per share • Continued 5 th straight year of expected double digit, 5 year growth in rate base • Anticipated high single digit earnings growth at PSE&G on three-year basis from 2014 to 2017, driven by transmission investments and planned programs • Power’s continued focus on operational excellence, market expertise and financial strength delivers value in current price environment • Strong Balance Sheet and Cash Flow support full capital program and new potential opportunities without the need for equity • Our $0.08 per share dividend increase is consistent with our long history of returning cash to the shareholder through the common dividend, with potential for consistent and sustainable growth 99 |

March 31, 2015 $ Billions PSEG PSE&G Power Cash and Cash Equivalents $1.0 $0.3 $0.0 Short Term Debt $0.0 $0.0 N/A Long Term Debt (1) 8.9 6.3 2.5 Common Equity 12.5 7.0 5.7 Total Capitalization $21.4 $13.3 $8.2 Total Debt / Capitalization 41% 47% 31% PSE&G Regulated Equity Ratio (2) 52.3% Our balance sheet remains strong (1)INCLUDES L-T DEBT DUE WITHIN 1 YEAR; EXCLUDES SECURITIZATION DEBT OF $201 MILLION AND NON-RECOURSE DEBT OF $16 MILLION. (2)REGULATED EQUITY RATIO INCLUDES CUSTOMER DEPOSITS OF ~$98 MILLION AND EXCLUDES SHORT-TERM DEBT. 111 |

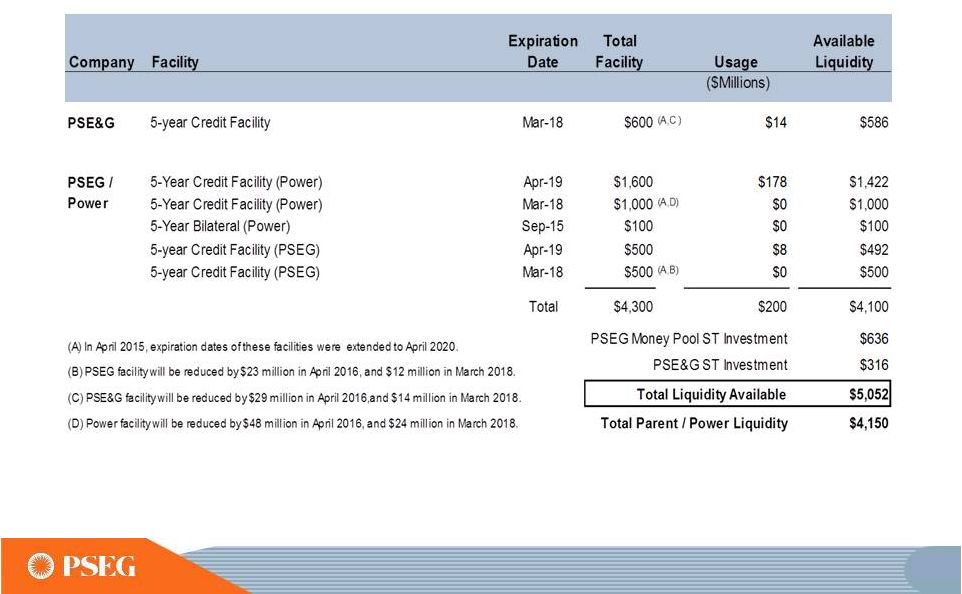

PSEG Liquidity as of March 31, 2015 115 |

PSEG Energy Holdings Investment Portfolio Equipment Investment Balance* at 3/31/15 ($Millions) Merchant Energy Leases NRG REMA Keystone, Conemaugh & Shawville (PA) 3 coal-fired plants (1,162 equity MW) 355 NRG Energy, Inc./Midwest Gen** Powerton & Joliet Generating Stations (IL) 2 coal-fired generating facilities (1,640 equity MW) 218 Regulated Energy Leases Merrill Creek Reservoir in NJ (PECO, MetEd, Delmarva Power & Light) 148 Grand Gulf Nuclear station in Mississippi (175 equity MW) 28 Real Estate Leveraged Leases GM Renaissance Center; Wal-Marts; E-D (shopping) Centers 62 Real Estate Operating Leases Office Towers, Shopping Centers - 28 properties 40 Generation Legacy Assets GWF (in wind down stage), GSOE 2 Other Land 5 Total Holdings Investments $858 * BOOK BALANCE EXCLUDING DEFERRED TAX ACCOUNTS. **EME WAS ACQUIRED BY NRG ON APRIL 1 2014. 116 |

Items Excluded from Income from Continuing Operations/Net Income to Reconcile to Operating Earnings PLEASE SEE PAGE 3 FOR AN EXPLANATION OF PSEG’S USE OF OPERATING EARNINGS AS A NON-GAAP FINANCIAL MEASURE AND HOW IT DIFFERS FROM NET INCOME. 2014 2013 2012 2011 2010 2009 Earnings Impact ($ Millions) Operating Earnings 1,400 $ 1,309 $ 1,236 $ 1,389 $ 1,584 $ 1,567 $ Gain (Loss) on Nuclear Decommissioning Trust (NDT) Fund Related Activity (PSEG Power) 68 40 52 50 46 9 Gain (Loss) on Mark-to-Market (MTM) (PSEG Power) 66 (74) (10) 107 (1) (11) Lease Transaction Activity (PSEG Enterprise/Other) - - 36 (173) - 29 Storm O&M (PSEG Power) (16) (32) (39) - - - Market Transition Charge Refund (PSE&G) - - - - (72) - Gain (Loss) on Asset Sales and Impairments (PSEG Enterprise/Other) - - - 34 - - Income from Continuing Operations 1,518 $ 1,243 $ 1,275 $ 1,407 $ 1,557 $ 1,594 $ Discontinued Operations - - - 96 7 (2) Net Income 1,518 $ 1,243 $ 1,275 $ 1,503 $ 1,564 $ 1,592 $ Fully Diluted Average Shares Outstanding (in Millions) 508 508 507 507 507 507 Per Share Impact (Diluted) Operating Earnings 2.76 $ 2.58 $ 2.44 $ 2.74 $ 3.12 $ 3.09 $ Gain (Loss) on NDT Fund Related Activity (PSEG Power) 0.13 0.08 0.10 0.10 0.09 0.02 Gain (Loss) on MTM (PSEG Power) 0.13 (0.14) (0.02) 0.21 - (0.02) Lease Transaction Activity (PSEG Enterprise/Other) - - 0.07 (0.34) - 0.05 Storm O&M (PSEG Power) (0.03) (0.07) (0.08) - - - Market Transition Charge Refund (PSE&G) - - - - (0.14) - Gain (Loss) on Asset Sales and Impairments (PSEG Enterprise/Other) - - - 0.06 - - Income from Continuing Operations 2.99 $ 2.45 $ 2.51 $ 2.77 $ 3.07 $ 3.14 $ Discontinued Operations - - - 0.19 0.01 - Net Income 2.99 $ 2.45 $ 2.51 $ 2.96 $ 3.08 $ 3.14 $ (Unaudited) For the Year Ended December 31, PUBLIC SERVICE ENTERPRISE GROUP INCORPORATED Reconciling Items, net of tax (a) Includes the financial impact from positions with forward delivery months. A (a) (a) |

Items Excluded from Net Income to Reconcile to Operating Earnings and Adjusted EBITDA PLEASE SEE PAGE 3 FOR AN EXPLANATION OF PSEG’S USE OF OPERATING EARNINGS AND ADJUSTED EBITDA AS NON-GAAP FINANCIAL MEASURES AND HOW THEY DIFFER FROM NET INCOME. B 2015 2014 Adjusted EBITDA 626 $ 651 $ 1,584 $ Fossil Major Maintenance, pre-tax (49) (58) (144) Depreciation and Amortization, pre-tax (b) (77) (73) (291) Interest Expense, pre-tax (b) (31) (31) (120) Income Taxes (b) (191) (196) (387) Operating Earnings 278 $ 293 $ 642 $ Gain (Loss) on NDT Fund Related Activity, pre-tax 7 19 138 Gain (Loss) on MTM, pre-tax (a) (34) (223) 111 Storm O&M, net of insurance recoveries, pre-tax 127 (10) (27) Income Taxes related to Operating Earnings reconciling items (43) 85 (104) Net Income 335 $ 164 $ 760 $ (a) Includes the financial impact from positions with forward delivery months. (b) Excludes amounts related to Operating Earnings reconciling items ($ Millions, Unaudited) PSEG Power Adjusted EBITDA Reconcilation Year Ended December 31, 2014 Reconciling Items Three Months Ended March 31, |

Items Excluded from Income from Continuing Operations/Net Income to Reconcile to Operating Earnings PLEASE SEE PAGE 3 FOR AN EXPLANATION OF PSEG’S USE OF OPERATING EARNINGS AS A NON-GAAP FINANCIAL MEASURE AND HOW IT DIFFERS FROM NET INCOME. 2015 2014 Earnings Impact ($ Millions) Operating Earnings 529 $ 515 $ Gain (Loss) on Nuclear Decommissioning Trust (NDT) Fund Related Activity (PSEG Power) 2 9 Gain (Loss) on Mark-to-Market (MTM) (PSEG Power) (20) (132) Lease Transaction Activity (PSEG Enterprise/Other) - - Storm O&M (PSEG Power) 75 (6) Market Transition Charge Refund (PSE&G) - - Gain (Loss) on Asset Sales and Impairments (PSEG Enterprise/Other) - - Income from Continuing Operations 586 $ 386 $ Discontinued Operations - - Net Income 586 $ 386 $ Fully Diluted Average Shares Outstanding (in Millions) 508 508 Per Share Impact (Diluted) Operating Earnings 1.04 $ 1.01 $ Gain (Loss) on NDT Fund Related Activity (PSEG Power) - 0.02 Gain (Loss) on MTM (PSEG Power) (0.04) (0.26) Lease Transaction Activity (PSEG Enterprise/Other) - - Storm O&M (PSEG Power) 0.15 (0.01) Market Transition Charge Refund (PSE&G) - - Gain (Loss) on Asset Sales and Impairments (PSEG Enterprise/Other) - - Income from Continuing Operations 1.15 $ 0.76 $ Discontinued Operations - - Net Income 1.15 $ 0.76 $ Reconciling Items, net of tax PUBLIC SERVICE ENTERPRISE GROUP INCORPORATED Three Months Ended March 31, (Unaudited) (a) Includes the financial impact from positions with forward delivery months. C (a) (a) |