| | |

OMB APPROVAL |

OMB Number: | | 3235 - 0570 |

Expires: | | January 31, 2014 |

Estimated average burden |

hours per response . . . | | 20.6 |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

| | |

Investment Company Act file number: 811-5032 | | |

BARON INVESTMENT FUNDS TRUST f/k/a

BARON ASSET FUND

|

| (Exact name of registrant as specified in charter) |

| | |

| 767 Fifth Avenue, 49th Floor | | New York, NY 10153 |

| (Address of Principal Executive Offices) | | (Zip Code) |

Patrick M. Patalino, Esq.

c/o Baron Investment Funds Trust

767 Fifth Avenue, 49th Floor

New York, NY 10153

|

| (Name and Address of Agent for Service) |

Registrant’s Telephone Number, including Area Code: 212-583-2000

Date of fiscal year end: September 30

Date of reporting period: March 31, 2011

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17CRF 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget (“OMB”) control number. Please direct comments concerning the accuracy of the information collection burden estimate and suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 450 5th Street, NW, Washington, D.C. 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. Section 3507.

Persons who are to respond to the collection of information contained in this form are not required to respond unless the form displays a currently valid OMB control number.

SEC 2569 (5-07)

Item 1. Reports to Stockholders.

Baron Investment Funds Trust Semi-Annual Report for the period ended March 31, 2011.

Baron Asset Fund

Baron Growth Fund

Baron Small Cap Fund

Baron Opportunity Fund

Baron Fifth Avenue Growth Fund

March 31, 2011

Baron Funds®

Semi-Annual Financial Report

DEAR BARON FUNDS SHAREHOLDER:

In this report you will find unaudited financial statements for Baron Asset Fund, Baron Growth Fund, Baron Small Cap Fund, Baron Opportunity Fund and Baron Fifth Avenue Growth Fund (the “Funds”) for the six months ended March 31, 2011. The Securities and Exchange Commission (the “SEC”) requires mutual funds to furnish these statements semi-annually to their shareholders. We hope you find these statements informative and useful.

We thank you for choosing to join us as fellow shareholders in Baron Funds. We will continue to work hard to justify your confidence.

Sincerely,

| | | | |

| |  | |  |

Ronald Baron Chief Executive Officer and Chief Investment Officer May 20, 2011 | | Linda S. Martinson Chairman, President and Chief Operating Officer May 20, 2011 | | Peggy Wong Treasurer and Chief Financial Officer May 20, 2011 |

This Semi-Annual Financial Report is for the Baron Investment Funds Trust, which currently has five series: Baron Asset Fund, Baron Growth Fund, Baron Small Cap Fund, Baron Opportunity Fund and Baron Fifth Avenue Growth Fund. If you are interested in the Baron Select Funds, which contains the Baron Partners Fund, Baron Focused Growth Fund, Baron International Growth Fund, Baron Real Estate Fund and Baron Emerging Markets Fund series, please visit the Funds’ website at www.BaronFunds.com or contact us at 1-800-99BARON.

A description of the Funds’ proxy voting policies and procedures is available without charge on the Funds’ website, www.BaronFunds.com, or by calling 1-800-99BARON and on the SEC’s website at www.sec.gov. The Funds’ most current proxy voting record, Form N-PX, is also available on the Funds’ website and on the SEC’s website.

The Funds file their complete schedules of portfolio holdings with the SEC for the first and third quarters of each fiscal year on Form N-Q. The Funds’ Forms N-Q are available on the SEC’s website at www.sec.gov. The Funds’ Forms N-Q may also be reviewed and copied at the SEC’s Public Reference Room in Washington, DC; information on the operation of the SEC’s Public Reference Room may be obtained by calling 1-202-551-8090. A copy of the Funds’ Forms N-Q may also be obtained upon request by calling 1-800-99BARON. Schedules of portfolio holdings current to the most recent quarter are also available on the Funds’ website.

Some of the comments are based on current management expectations and are considered “forward-looking statements.” Actual future results, however, may prove to be different from our expectations. You can identify forward-looking statements by words such as “estimate,” “may,” “expect,” “should,” “could,” “believe,” “plan” and other similar terms. We cannot promise future returns and our opinions are a reflection of our best judgment at the time this report is compiled.

The views expressed in this report reflect those of the BAMCO, Inc. (“BAMCO” or the “Adviser”) only through the end of the period stated in this report. The views are not intended as recommendations or investment advice to any person reading this report and are subject to change at any time without notice based on market and other conditions.

Past performance is no guarantee of future results. The investment return and principal value of an investment will fluctuate; an investor’s shares, when redeemed, may be worth more or less than their original cost. For more complete information about Baron Funds, including charges and expenses, call or write for a prospectus. Read it carefully before you invest or send money. This report is not authorized for use as an offer of sale or a solicitation of an offer to buy shares of Baron Funds, unless accompanied or preceded by the Funds’ current prospectus.

767 Fifth Avenue

NY, NY 10153

212-583-2100

| | |

| Baron Asset Fund | | March 31, 2011 |

| | | | | | | | |

Baron Asset Fund | | | | | | | | |

| | |

Ticker Symbols: | | | | | | | | |

Retail Shares: BARAX | | | | | | | | |

Institutional Shares: BARIX | | | | | | | | |

Performance | | | 2 | | | | | |

Top Ten Holdings | | | 3 | | | | | |

Sector Breakdown | | | 3 | | | | | |

Management’s Discussion of Fund Performance | | | 3 | | | | | |

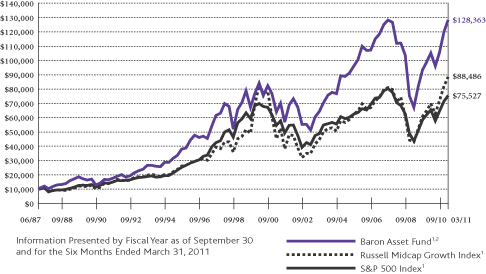

COMPARISONOFTHECHANGEIN VALUEOF $10,000INVESTMENTIN BARON ASSET FUND†INRELATIONTOTHE RUSSELL MIDCAP GROWTH INDEXANDTHE S&P 500 INDEX

AVERAGE ANNUAL TOTAL RETURNSFORTHEPERIODSENDED MARCH 31, 2011

| | | | | | | | | | | | | | | | | | | | | | | | |

| | | Six

Months* | | | One

Year | | | Three

Years | | | Five

Years | | | Ten

Years | | | Since

Inception

(June 12,

1987) | |

Baron Asset Fund — Retail Shares1,2 | | | 21.64% | | | | 22.09% | | | | 4.68% | | | | 3.17% | | | | 7.20% | | | | 11.32% | |

Baron Asset Fund — Institutional Shares1,2,4 | | | 21.81% | | | | 22.43% | | | | 4.84% | | | | 3.26% | | | | 7.25% | | | | 11.34% | |

Russell Midcap Growth Index1 | | | 22.96% | | | | 26.60% | | | | 7.63% | | | | 4.93% | | | | 6.94% | | | | 9.61% | 3 |

S&P 500 Index1 | | | 17.31% | | | | 15.65% | | | | 2.35% | | | | 2.62% | | | | 3.29% | | | | 8.87% | |

| 1 | The Russell Midcap Growth Index and the S&P 500 Index are unmanaged indexes. The Russell Midcap Growth Index measures the performance of mid-sized companies that are classified as growth. The S&P 500 Index measures the performance of larger cap equities in the stock market in general. The indexes and the Baron Asset Fund are with dividends, which positively impact the performance results. |

| 2 | Past performance is not predictive of future performance. The performance data in the table does not reflect the deduction of taxes that a shareholder would pay on dividends, capital gain distributions, or redemption of Fund shares. |

| 3 | For the period June 30, 1987 to March 31, 2011. |

| 4 | Performance for the Institutional Shares prior to May 29, 2009 is based on the performance of the Retail Shares, which have a distribution fee. The Institutional Shares do not have a distribution fee. If the annual returns prior to May 29, 2009 did not reflect this fee, the returns would be higher. |

| † | Performance information reflects results of the Retail Shares. |

1.800.99.BARON

www.BaronFunds.com

©2011 All Rights Reserved

2

| | |

| March 31, 2011 | | Baron Asset Fund |

TOP TEN HOLDINGSASOF MARCH 31, 2011

| | | | |

| Baron Asset Fund | | % of Net

Assets | |

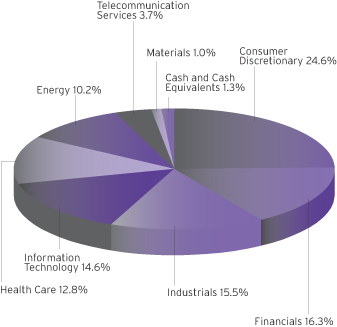

Gartner, Inc. | | | 4.0% | |

Charles Schwab Corp. | | | 3.6% | |

IDEXX Laboratories, Inc. | | | 3.4% | |

Polo Ralph Lauren Corp. | | | 3.2% | |

FactSet Research Systems, Inc. | | | 3.2% | |

Vail Resorts, Inc. | | | 3.0% | |

Fastenal Co. | | | 3.0% | |

C. H. Robinson Worldwide, Inc. | | | 2.7% | |

DeVry, Inc. | | | 2.5% | |

Mettler-Toledo International, Inc. | | | 2.3% | |

| | | | 30.9% | |

SECTOR BREAKDOWNASOF MARCH 31, 20112

(as a percentage of net assets)

MANAGEMENT’S DISCUSSIONOF FUND PERFORMANCE

For the six-month period ended March 31, 2011, Baron Asset Fund (Retail Shares) gained 21.64%, the Russell Midcap Growth Index gained 22.96% and the S&P 500 Index was up 17.31%.

Baron Asset Fund invests primarily in medium-sized growth companies for the long term while using value-oriented purchase and sell disciplines.1 The Fund purchases companies that the Adviser believes have sustainable competitive advantages and strong financial characteristics, operating in industries with favorable macroeconomic trends led by strong management.

The economy has demonstrated steady improvement over the past six months as evidenced by growing corporate profits. Certain risks remain, including continuing high unemployment, depressed home prices, budget deficits and the threat of inflation. New risks have surfaced as well, stemming from the disaster in Japan and civil unrest that has engulfed the Middle East and North Africa. Nonetheless, investors showed increasing confidence throughout the period as they continued to focus on corporate profits, increased market stability, improved credit quality and the Federal Reserve’s attention to providing increased liquidity.

One area the Fund continues to favor is the information services businesses, a term we use to describe companies spanning several industry sectors. These include companies that possess proprietary information-related assets, which are generally sold through annual subscriptions to customers in areas including investment management, insurance, and information technology.

Gartner, Inc., the leading independent provider of research and analysis on the information technology industry, was the single largest contributor to Fund performance in the period. The company has continued to generate record bookings in its research business. We expect the company to show continued sales momentum throughout 2011 and beyond as it adds to its sales force, raises prices, and leverages its global sales network to distribute research from recent acquisitions of AMR and Burton.

Equinix, Inc., a network neutral operator of state-of-the-art data centers across North America, Europe and Asia-Pacific, was the leading detractor from Fund performance in the period. The company’s shares experienced a sharp sell-off last Fall following disclosure that it would miss revenue expectations while making pricing concessions to certain large customers. We continue to believe Equinix represents significant growth potential over the long term.

The Adviser expects to continue to invest in companies that, in our opinion, are undervalued relative to their long-term growth prospects and have the ability to sustain superior levels of profitability. We intend to continue to identify superior quality companies through independent research efforts. We expect the Fund will remain diversified not only by industry and investment theme, but also by external factors we believe could affect company performance.

| 1 | Prior to February 15, 2007, the Fund’s strategy was also to invest primarily in small- and mid-sized growth companies. |

| 2 | Industry sector levels are derived from the Global Industry Classification Standard (“GICS”), developed and exclusively owned by MSCI, Inc. and Standard & Poor’s Financial Services LLC, unless otherwise stated that they have been reclassified or classified by the Adviser. All GICS data is provided “as is” with no warranties. |

3

| | |

| Baron Growth Fund | | March 31, 2011 |

| | | | | | | | |

Baron Growth Fund | | | | | | | | |

| | |

Ticker Symbols: | | | | | | | | |

Retail Shares: BGRFX | | | | | | | | |

Institutional Shares: BGRIX | | | | | | | | |

Performance | | | 4 | | | | | |

Top Ten Holdings | | | 5 | | | | | |

Sector Breakdown | | | 5 | | | | | |

Management’s Discussion of

Fund Performance | | | 5 | | | | | |

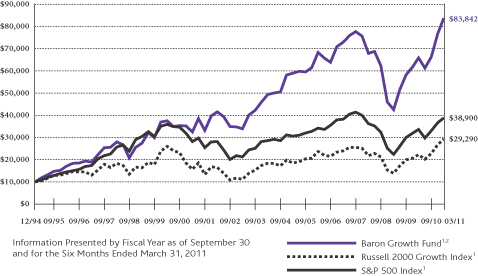

COMPARISONOFTHECHANGEIN VALUEOF $10,000INVESTMENTIN BARON GROWTH FUND†INRELATIONTOTHE RUSSELL 2000 GROWTH INDEXANDTHE S&P 500 INDEX

AVERAGE ANNUAL TOTAL RETURNSFORTHEPERIODSENDED MARCH 31, 2011

| | | | | | | | | | | | | | | | | | | | | | | | |

| | | Six

Months* | | | One

Year | | | Three

Years | | | Five

Years | | | Ten

Years | | | Since

Inception

(December 31,

1994) | |

Baron Growth Fund — Retail Shares1,2 | | | 26.28% | | | | 27.23% | | | | 7.29% | | | | 4.15% | | | | 9.92% | | | | 13.98% | |

Baron Growth Fund — Institutional Shares1,2,3 | | | 26.44% | | | | 27.55% | | | | 7.46% | | | | 4.25% | | | | 9.97% | | | | 14.01% | |

Russell 2000 Growth Index1 | | | 27.93% | | | | 31.04% | | | | 10.16% | | | | 4.34% | | | | 6.44% | | | | 6.84% | |

S&P 500 Index1 | | | 17.31% | | | | 15.65% | | | | 2.35% | | | | 2.62% | | | | 3.29% | | | | 8.72% | |

| 1 | The Russell 2000 Growth Index and S&P 500 Index are unmanaged indexes. The Russell 2000 Growth Index measures the performance of 2,000 small U.S. companies classified as growth. The S&P 500 Index measures the performance of larger cap equities in the stock market in general. These indexes and the Baron Growth Fund are with dividends, which positively impact the performance results. |

| 2 | Past performance is not predictive of future performance. The performance data in the table does not reflect the deduction of taxes that a shareholder would pay on dividends, capital gain distributions, or redemption of Fund shares. |

| 3 | Performance for the Institutional Shares prior to May 29, 2009 is based on the performance of the Retail Shares, which have a distribution fee. The Institutional Shares do not have a distribution fee. If the annual returns prior to May 29, 2009 did not reflect this fee, the returns would be higher. |

| † | Performance information reflects results of the Retail Shares. |

1.800.99 BARON

www.BaronFunds.com

©2011 All Rights Reserved

4

| | |

| March 31, 2011 | | Baron Growth Fund |

TOP TEN HOLDINGSASOF MARCH 31, 2011

| | | | |

| Baron Growth Fund | | % of Net

Assets | |

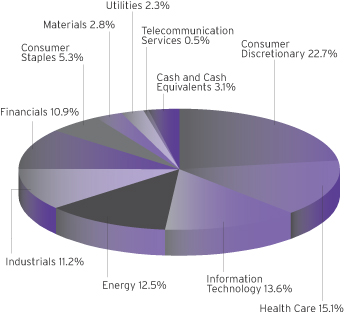

Edwards Lifesciences Corp. | | | 3.3% | |

Dick's Sporting Goods, Inc. | | | 2.9% | |

DeVry, Inc. | | | 2.9% | |

Molycorp, Inc. | | | 2.5% | |

Mettler-Toledo International, Inc. | | | 2.5% | |

FactSet Research Systems, Inc. | | | 2.5% | |

AMERIGROUP Corp. | | | 2.3% | |

ITC Holdings Corp. | | | 2.3% | |

MSCI, Inc., Cl A | | | 2.3% | |

Community Health Systems, Inc. | | | 2.1% | |

| | | | 25.6% | |

SECTOR BREAKDOWNASOF MARCH 31, 20111

(as a percentage of net assets)

MANAGEMENT’S DISCUSSIONOF FUND PERFORMANCE

Baron Growth Fund (Retail Shares) gained 26.28% for the six months ended March 31, 2011, while the Russell 2000 Growth Index gained 27.93% and the S&P 500 Index gained 17.31%.

Baron Growth Fund is a long-term investor primarily in small-sized growth companies. The Adviser, through its independent research of companies, utilizes an investment approach that it believes allows it to look beyond the current market environment and invest based upon the potential profitability of a business, and therefore its value in the future.

The economy has demonstrated steady improvement over the past six months as evidenced by growing corporate profits. Certain risks remain, including continuing high unemployment, depressed home prices, budget deficits and the threat of inflation. New risks have surfaced as well, stemming from the disaster in Japan and civil unrest that has engulfed the Middle East and North Africa. Nonetheless, investors showed increasing confidence throughout the period as they continued to focus on corporate profits, increased market stability, improved credit quality and the Federal Reserve’s attention to providing increased liquidity.

Molycorp, Inc., the leading producer of rare earths outside of China, was the largest contributor to Fund performance during the period. Stricter environmental standards, higher taxes, and increased vigilance on illegal mining could increase the supply/demand gap in the near term. Molycorp says it has already “sold-out” of its 2011 production. To supply growing demand, Molycorp plans to double its potential capacity from 20,000 tons to 40,000 tons by 2014.

Strayer Education, Inc., an education services holding company, was the Fund’s leading detractor from performance in the period. Strayer’s shares declined principally on regulatory uncertainty, possible Pell-grant cuts and heightened competition for quality students. We are confident that management will adapt its model as necessary and thrive again. In our view, Strayer retains its long-term growth potential.

We believe that our investment process, with its focus on research and long-term investing, will enable the Fund to take advantage of opportunities as they arise throughout the economic recovery. We intend to continue to invest in small businesses that we believe have the potential to grow substantially in the years ahead. We expect the Fund will remain diversified not only by industry and investment theme, but also by external factors we believe could affect company performance.

| 1 | Industry sector levels are derived from the Global Industry Classification Standard (“GICS”), developed and exclusively owned by MSCI, Inc. and Standard & Poor’s Financial Services LLC, unless otherwise stated that they have been reclassified or classified by the Adviser. All GICS data is provided “as is” with no warranties. |

5

| | |

| Baron Small Cap Fund | | March 31, 2011 |

| | | | | | | | |

Baron Small Cap Fund | | | | | | | | |

| | |

Ticker Symbols: | | | | | | | | |

Retail Shares: BSCFX | | | | | | | | |

Institutional Shares: BSFIX | | | | | | | | |

Performance | | | 6 | | | | | |

Top Ten Holdings | | | 7 | | | | | |

Sector Breakdown | | | 7 | | | | | |

Management’s Discussion of Fund Performance | | | 7 | | | | | |

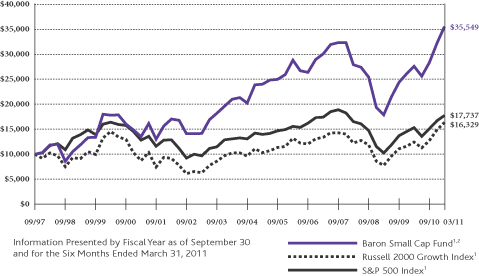

COMPARISONOFTHECHANGEIN VALUEOF $10,000INVESTMENTIN BARON SMALL CAP FUND†INRELATIONTOTHE RUSSELL 2000 GROWTH INDEXANDTHE S&P 500 INDEX

AVERAGE ANNUAL TOTAL RETURNSFORTHEPERIODSENDED MARCH 31, 2011

| | | | | | | | | | | | | | | | | | | | | | | | |

| | | Six

Months* | | | One

Year | | | Three

Years | | | Five

Years | | | Ten

Years | | | Since Inception

(September 30,

1997) | |

Baron Small Cap Fund — Retail Shares1,2 | | | 25.22% | | | | 28.92% | | | | 8.34% | | | | 4.27% | | | | 10.13% | | | | 9.85% | |

Baron Small Cap Fund — Institutional Shares1,2,3 | | | 25.37% | | | | 29.25% | | | | 8.51% | | | | 4.36% | | | | 10.18% | | | | 9.89% | |

Russell 2000 Growth Index1 | | | 27.93% | | | | 31.04% | | | | 10.16% | | | | 4.34% | | | | 6.44% | | | | 3.70% | |

S&P 500 Index1 | | | 17.31% | | | | 15.65% | | | | 2.35% | | | | 2.62% | | | | 3.29% | | | | 4.34% | |

| 1 | The Russell 2000 Growth Index and S&P 500 Index are unmanaged indexes. The Russell 2000 Growth Index measures the performance of 2,000 small U.S. companies classified as growth. The S&P 500 Index measures the performance of larger cap equities in the stock market in general. These indexes and the Baron Small Cap Fund are with dividends, which positively impact the performance results. |

| 2 | Past performance is not predictive of future performance. The performance data in the table does not reflect the deduction of taxes that a shareholder would pay on dividends, capital gain distributions, or redemption of Fund shares. |

| 3 | Performance for the Institutional Shares prior to May 29, 2009 is based on the performance of the Retail Shares, which have a distribution fee. The Institutional Shares do not have a distribution fee. If the annual returns prior to May 29, 2009 did not reflect this fee, the returns would be higher. |

| † | Performance information reflects results of the Retail Shares. |

1.800.99 BARON

www.BaronFunds.com

©2011 All Rights Reserved

6

| | |

March 31, 2011 | | Baron Small Cap Fund |

TOP TEN HOLDINGSASOF MARCH 31, 2011

| | | | |

| Baron Small Cap Fund | | % of Net

Assets | |

Penn National Gaming, Inc. | | | 2.7% | |

TransDigm Group, Inc. | | | 2.7% | |

Liberty Media Corp. | | | 2.6% | |

SBA Communications Corp., Cl. A | | | 2.6% | |

Brookdale Senior Living, Inc. | | | 2.4% | |

Gartner, Inc. | | | 2.2% | |

Waste Connections, Inc. | | | 2.0% | |

Mettler-Toledo International, Inc. | | | 2.0% | |

Fossil, Inc. | | | 2.0% | |

Clean Harbors, Inc. | | | 2.0% | |

| | | | 23.2% | |

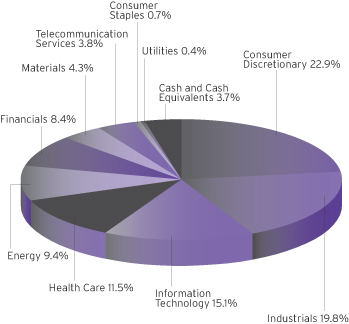

SECTOR BREAKDOWNASOF MARCH 31, 20111

(as a percentage of net assets)

MANAGEMENT’S DISCUSSIONOF FUND PERFORMANCE

Baron Small Cap Fund (Retail Shares) performed well for the six months ended March 31, 2011. The Fund gained 25.22%, compared to 27.93% for the Russell 2000 Growth Index and 17.31% for the S&P 500 Index.

Baron Small Cap Fund invests primarily in small-cap growth companies. The Fund is a long-term investor in what we believe are well-run small-cap growth businesses that can be purchased

at prices that represent a significant discount to our assessment of true value.

The equity markets have now retraced much of the ground they lost since the end of 2008. We believe that the first stage of the market recovery was led by outsized performance in more speculative, leveraged companies. We believe that the market is now beginning to reward higher-quality companies that have the ability to generate sustainable earnings growth over an extended economic cycle.

When the market has increased as it has over the past six months, we look for fallen angels and special situations. This past quarter we found two unique businesses — one is a turnaround of a shoe retailer, and the other is a diversified manufacturer and supplier of commercial vehicle components that came out of bankruptcy late last year.

Energy-related stock prices rose during the period along with commodity prices, outperforming the broader market. As a consequence of the recent events in North Africa, the Middle East, and Japan, more attention is being put on U.S. domestic energy policy, exploration, and development. We believe these recent developments will benefit our energy-related investments over the long term.

We expect multiples to expand as investors move back into equities and M&A activity returns to more normal levels. 2011 is off to a positive start and we are committed to keeping the Fund well positioned by investing in special small-cap companies that can thrive in this environment.

Brookdale Senior Living, Inc., the owner and operator of 550 senior living communities throughout the U.S., was the leading contributor to Fund performance during the period. Pent-up demand, a stabilizing economy and little new supply supported improving fundamentals. Through the remainder of the year, we see continued slow and steady improvements in rate, occupancy and margins. We expect Brookdale to become an increasingly active acquirer.

Strayer Education, Inc., an education services holding company, was the Fund’s leading detractor from performance in the period. Strayer’s shares declined principally on regulatory uncertainty, possible Pell-grant cuts and heightened competition for quality students. We are confident that management will adapt its model as necessary and thrive again. In our view, Strayer retains its long-term growth potential.

Baron Small Cap’s investments fall into three categories: Growth Stocks, Fallen Angels and Special Situations. The Fund intends to continue to invest in “Growth Stocks” that we believe have significant long-term growth prospects and can be purchased at what we believe are attractive prices because their prospects have not yet been appreciated by investors. “Fallen Angels” are companies that we believe have strong long-term franchises but have disappointed investors with short-term results, creating what we believe is a buying opportunity. “Special Situations” include spin-offs and recapitalizations, where lack of investor awareness creates opportunities to purchase what we believe are strong businesses at attractive prices.

| 1 | Industry sector levels are derived from the Global Industry Classification Standard (“GICS”), developed and exclusively owned by MSCI, Inc. and Standard & Poor’s Financial Services LLC, unless otherwise stated that they have been reclassified or classified by the Adviser. All GICS data is provided “as is” with no warranties. |

7

| | |

| Baron Opportunity Fund | | March 31, 2011 |

| | | | | | | | |

Baron Opportunity Fund | | | | | | | | |

| | |

Ticker Symbols: | | | | | | | | |

Retail Shares: BIOPX | | | | | | | | |

Institutional Shares: BIOIX | | | | | | | | |

Performance | | | 8 | | | | | |

Top Ten Holdings | | | 9 | | | | | |

Sector Breakdown | | | 9 | | | | | |

Management’s Discussion of Fund Performance | | | 9 | | | | | |

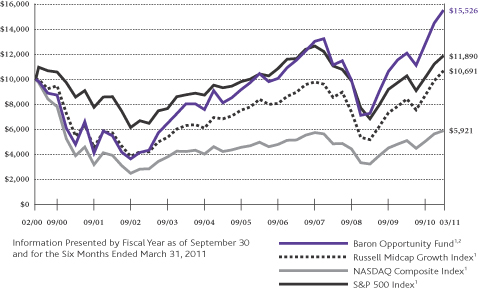

COMPARISONOFTHECHANGEIN VALUEOF $10,000INVESTMENTIN BARON OPPORTUNITY FUND†INRELATIONTOTHE RUSSELL MIDCAP GROWTH INDEX,THE NASDAQ COMPOSITE INDEX,ANDTHE S&P 500 INDEX

AVERAGE ANNUAL TOTAL RETURNS FOR THE PERIODS ENDED MARCH 31, 2011

| | | | | | | | | | | | | | | | | | | | | | | | |

| | | Six

Months* | | | One

Year | | | Three

Years | | | Five

Years | | | Ten

Years | | | Since

Inception

(February 29,

2000) | |

Baron Opportunity Fund — Retail Shares1,2 | | | 21.24% | | | | 28.28% | | | | 11.63% | | | | 8.18% | | | | 12.46% | | | | 4.05% | |

Baron Opportunity Fund — Institutional Shares1,2,3 | | | 21.48% | | | | 28.62% | | | | 11.83% | | | | 8.29% | | | | 12.52% | | | | 4.10% | |

Russell Midcap Growth Index1 | | | 22.96% | | | | 26.60% | | | | 7.63% | | | | 4.93% | | | | 6.94% | | | | 0.61% | |

NASDAQ Composite Index1 | | | 17.41% | | | | 15.98% | | | | 6.86% | | | | 3.52% | | | | 4.22% | | | | –4.62% | |

S&P 500 Index1 | | | 17.31% | | | | 15.65% | | | | 2.35% | | | | 2.62% | | | | 3.29% | | | | 1.57% | |

| 1 | The Russell Midcap Growth Index has replaced the NASDAQ Composite Index as the primary broad-based index for the Fund because the Adviser believes that the Russell Midcap Growth Index is more representative of the Fund’s investment strategy. The NASDAQ Composite Index remains in the table above for comparison purposes. The Russell Midcap Growth Index, the NASDAQ Composite Index and the S&P 500 Index are unmanaged indexes. The Russell Midcap Growth Index measures the performance of mid-sized companies that are classified as growth. The NASDAQ Composite Index tracks the performance of market-value weighted common stocks listed on NASDAQ. The S&P 500 Index measures the performance of larger cap equities in the stock market in general. The NASDAQ Composite Index is without dividends. The S&P 500 Index, the Russell Midcap Growth Index and the Baron Opportunity Fund are with dividends, which positively impact the performance results. |

| 2 | Past performance is not predictive of future performance. The performance data in the table does not reflect the deduction of taxes that a shareholder would pay on dividends, capital gain distributions, or redemption of Fund shares. |

| 3 | Performance for the Institutional Shares prior to May 29, 2009 is based on the performance of the Retail Shares, which have a distribution fee. The Institutional Shares do not have a distribution fee. If the annual returns prior to May 29, 2009 did not reflect this fee, the returns would be higher. |

| † | Performance information reflects results of the Retail Shares. |

1.800.99.BARON

www.BaronFunds.com

©2011 All Rights Reserved

8

| | |

| March 31, 2011 | | Baron Opportunity Fund |

TOP TEN HOLDINGSASOF MARCH 31, 2011

| | | | |

| Baron Opportunity Fund | | % of Net

Assets | |

Gartner, Inc. | | | 3.9% | |

Equinix, Inc. | | | 3.7% | |

SBA Communications Corp., Cl A | | | 3.6% | |

NII Holdings, Inc. | | | 3.5% | |

CARBO Ceramics, Inc. | | | 2.9% | |

Apple, Inc. | | | 2.8% | |

MSCI, Inc., Cl A | | | 2.6% | |

Polypore International, Inc. | | | 2.5% | |

ANSYS, Inc. | | | 2.5% | |

Polycom, Inc. | | | 2.5% | |

| | | | 30.5% | |

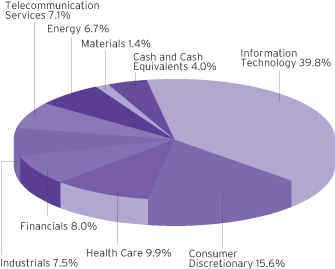

SECTOR BREAKDOWNASOF MARCH 31, 20111

(as a percentage of net assets)

MANAGEMENT’S DISCUSSIONOF FUND PERFORMANCE

Baron Opportunity Fund (Retail Shares) performed well for the six months ended March 31, 2011. The Fund gained 21.24%, compared to 22.96% for the Russell Midcap Growth Index and 17.31% for the S&P 500 Index.

Baron Opportunity Fund, like the other Baron Funds, utilizes value purchase disciplines while investing in growth companies that the Adviser believes are driving or benefiting from innovation through development of pioneering, transformative or technologically advanced products and services.

The economy has demonstrated steady improvement over the past six months as evidenced by growing corporate profits. Certain risks remain, including continuing high unemployment, depressed home prices, budget deficits and the threat of inflation. New risks have surfaced as well, stemming from the disaster in Japan and civil unrest that has engulfed the Middle East and North Africa. Nonetheless, investors showed increasing confidence throughout the period as they continued to focus on corporate profits, increased market stability, improved credit quality and the Federal Reserve’s attention to providing increased liquidity.

In the current environment, two innovative industries that appear particularly attractive are wireless data services and health care. We believe growth in wireless data services is coming from the increasing usage of smartphones and other advanced data devices. The appeal of these devices and the need for increased bandwidth has created opportunities for innovation that we believe will continue to benefit this industry.

In health care, we have invested in companies that are saving lives, saving money, and changing the way medical professionals care for patients. Real-time diagnostics, for example, is having a profound and positive impact on health care. In one major U.S. hospital, blood transfusions dropped dramatically since it started using a device that fits on a patient’s fingertip. This small device uses light technology and provides doctors and nurses vital statistics about a patient’s blood without needles or lab tests.

Today many large technology and health care companies are struggling for growth because they cut R & D spending during the downturn and stopped innovating. Many of these companies are sitting on large hoards of cash, and have been forced to make expensive acquisitions to keep pace with the competition and find growth. This dynamic has been a big benefit to the innovative companies and their investors, and we believe it will continue going forward.

CARBO Ceramics, Inc., the world’s largest supplier of ceramic proppant, used to enhance production from oil and gas wells, was the leading contributor to Fund performance in the period. We continue to see growing demand for fracturing as more wells drilled in North America are employing this technology. We think CARBO is expanding its product offering in a way that brings significant incremental earnings potential, and we continue to like the stock.

Equinix, Inc., a network neutral operator of state-of-the-art data centers across North America, Europe and Asia-Pacific, was the leading detractor from Fund performance in the period. The company’s shares experienced a sharp sell-off in the Fall following disclosure that it would miss revenue expectations while making pricing concessions to certain large customers. We continue to believe Equinix represents significant growth potential over the long term.

We believe that our investment process, with its focus on research and long-term investing, will enable the Fund to continue taking advantage of opportunities as they arise throughout the economic recovery. We expect to continue to invest in high-growth businesses of all market capitalizations in any sector or industry that we believe will benefit from innovations and advances in technology.

| 1 | Industry sector levels are derived from the Global Industry Classification Standard (“GICS”), developed and exclusively owned by MSCI, Inc. and Standard & Poor’s Financial Services LLC, unless otherwise stated that they have been reclassified or classified by the Adviser. All GICS data is provided “as is” with no warranties. |

9

| | |

| Baron Fifth Avenue Growth Fund | | March 31, 2011 |

| | | | | | | | |

Baron Fifth Avenue Growth Fund | | | | | |

| | |

Ticker Symbols: | | | | | | | | |

Retail Shares: BFTHX | | | | | | | | |

Institutional Shares: BFTIX | | | | | | | | |

Performance | | | 10 | | | | | |

Top Ten Holdings | | | 11 | | | | | |

Sector Breakdown | | | 11 | | | | | |

Management’s Discussion of Fund Performance | | | 11 | | | | | |

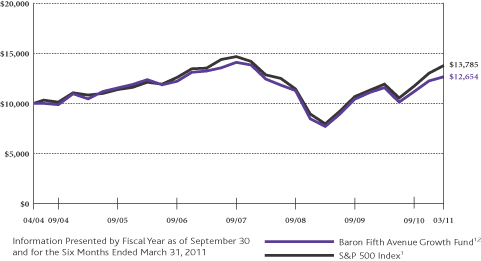

COMPARISONOFTHECHANGEIN VALUEOF $10,000INVESTMENTIN BARON FIFTH AVENUE GROWTH FUND†INRELATIONTOTHE S&P 500 INDEX

AVERAGE ANNUAL TOTAL RETURNSFORTHEPERIODSENDED MARCH 31, 2011

| | | | | | | | | | | | | | | | | | | | |

| | | Six

Months* | | | One

Year | | | Three

Years | | | Five

Years | | | Since

Inception

(April 30,

2004) | |

Baron Fifth Avenue Growth Fund — Retail Shares1,2 | | | 13.03% | | | | 9.29% | | | | 0.59% | | | | 0.42% | | | | 3.46% | |

Baron Fifth Avenue Growth Fund — Institutional Shares1,2,3 | | | 13.25% | | | | 9.62% | | | | 0.75% | | | | 0.52% | | | | 3.54% | |

S&P 500 Index1 | | | 17.31% | | | | 15.65% | | | | 2.35% | | | | 2.62% | | | | 4.75% | |

| 1 | The S&P 500 Index is an unmanaged index. The S&P 500 Index measures the performance of larger cap equities in the stock market in general. The index and the Baron Fifth Avenue Growth Fund are with dividends, which positively impact the performance results. |

| 2 | Past performance is not predictive of future performance. The performance data in the table does not reflect the deduction of taxes that a shareholder would pay on dividends, capital gain distributions, or redemption of Fund shares. |

| 3 | Performance for the Institutional Shares prior to May 29, 2009 is based on the performance of the Retail Shares, which have a distribution fee. The Institutional Shares do not have a distribution fee. If the annual returns prior to May 29, 2009 did not reflect this fee, the returns would be higher. |

| † | Performance information reflects results of the Retail Shares. |

1.800.99 BARON

www.BaronFunds.com

©2011 All Rights Reserved

10

| | |

| March 31, 2011 | | Baron Fifth Avenue Growth Fund |

TOP TEN HOLDINGSASOF MARCH 31, 2011

| | | | |

| Baron Fifth Avenue Growth Fund | | % of Net

Assets | |

Halliburton Co. | | | 3.6% | |

Occidental Petroleum Corp. | | | 3.6% | |

Apple, Inc. | | | 3.5% | |

Potash Corp. of Saskatchewan, Inc. | | | 3.4% | |

FedEx Corp. | | | 3.3% | |

Ford Motor Co. | | | 3.3% | |

Intuitive Surgical, Inc. | | | 3.3% | |

Liberty Media Corp. | | | 3.2% | |

American Tower Corp., Cl A | | | 3.0% | |

Carnival Corp. | | | 2.9% | |

| | | | 33.1% | |

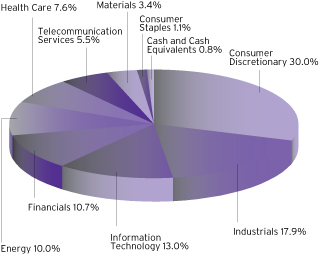

SECTOR BREAKDOWNASOF MARCH 31, 20111

(as a percentage of net assets)

MANAGEMENT’S DISCUSSIONOF FUND PERFORMANCE

Baron Fifth Avenue Growth Fund (Retail Shares) gained 13.03% for the six months ended March 31, 2011, underperforming the S&P 500 Index, which gained 17.31%.

Baron Fifth Avenue Growth Fund focuses on the long-term fundamental prospects of the businesses in which it invests. This contrasts with other investors’ focus on historical operating results or current earnings expectations. The Adviser believes that historical results and the outlook for near-term earnings are often not indicative of superior longer-term prospects that can be identified through research efforts.

The economy has demonstrated steady improvement over the past six months as evidenced by growing corporate profits. Certain risks remain, including continuing high unemployment, depressed home prices, budget deficits and the threat of inflation. New risks have surfaced as well, stemming from the disaster in Japan and civil unrest that has engulfed the Middle East and North Africa. Nonetheless, investors showed increasing confidence throughout the period as they continued to focus on corporate profits, increased market stability, improved credit quality and the Federal Reserve’s attention to providing increased liquidity.

Energy-related stock prices rose during the period, outperforming the broader market. As a consequence of Middle East unrest, and Japan’s nuclear disaster, more attention is being put on U.S. domestic energy policy, exploration, and development. Various countries are also reconsidering their nuclear programs. We believe these recent developments will benefit our energy-related investments over the long term.

Improvement in the economy and the new health care legislation, in our opinion, is making the Health Care sector increasingly attractive. We invest in medical device companies that develop and sell innovative products used in a variety of medical and surgical procedures that make surgery less invasive, shorten hospitalizations, and generate cost savings. If the economy continues to improve, we expect utilization trends to accelerate.

Last quarter we observed a pullback in some consumer-oriented and transportation-related stocks based on what we believe to be a short-term reaction to rising oil prices. We continue to find unique large-cap businesses that we believe are poised for significant growth over a multi-year time horizon. We believe the portfolio is well positioned for the current economic and stock market environment.

Haliburton Co. was the leading contributor to Fund performance in the period. The company is the leader in providing technology and services for the development of unconventional oil and gas resources. It also has strong positions in deepwater exploration and development and operates in over 80 countries. Despite poor weather in a number of key markets and political unrest in the Middle East, which had a negative impact on first-quarter earnings, the combination of higher oil prices and better-than-expected rig activity drove shares higher.

Equinix, Inc., a network neutral operator of state-of-the-art data centers across North America, Europe and Asia-Pacific, was the leading detractor from Fund performance in the period. The company’s shares experienced a sharp sell-off in the Fall following disclosure that it would miss revenue expectations while making pricing concessions to certain large customers. We continue to believe Equinix represents significant growth potential over the long term.

The Adviser invests in what we believe are some of the best companies in America. The Fund is positioned, in our view, in blue-chip, best-of-breed growth companies with a strong emphasis on quality to reduce risk. We believe the key to long-term stock appreciation is consistent earnings growth. We invest in those companies that are market share leaders who dominate their industry, companies with strong franchises and a strong brand name, avoiding fads and other short-term, unsustainable trends. We target companies that are the low-cost operators in their industry with, in our view, high barriers to entry. We also try to invest in growth companies that are positioned in industries that are themselves growing as opposed to industries that are stagnant or structurally challenged.

| 1 | Industry sector levels are derived from the Global Industry Classification Standard (“GICS”), developed and exclusively owned by MSCI, Inc. and Standard & Poor’s Financial Services LLC, unless otherwise stated that they have been reclassified or classified by the Adviser. All GICS data is provided “as is” with no warranties. |

11

| | |

| Baron Asset Fund | | March 31, 2011 |

STATEMENT OF NET ASSETS (UNAUDITED)

MARCH 31, 2011

| | | | | | | | | | | | |

| Shares | | | | | Cost | | | Value | |

| Common Stocks (97.45%) | | | | | | | | |

| Consumer Discretionary (24.26%) | | | | | | | | |

| | | | Advertising (1.27%) | | | | | | | | |

| | 1,025,000 | | | Lamar Advertising Co., Cl A1 | | $ | 53,133,779 | | | $ | 37,863,500 | |

| | | |

| | | | Apparel Retail (1.00%) | | | | | | | | |

| | 1,000,000 | | | Urban Outfitters, Inc.1 | | | 17,391,964 | | | | 29,830,000 | |

| | | |

| | | | Apparel, Accessories & Luxury Goods (3.22%) | | | | | | | | |

| | 775,000 | | | Polo Ralph Lauren Corp., Cl A | | | 14,925,404 | | | | 95,828,750 | |

| | | |

| | | | Auto Parts & Equipment (0.71%) | | | | | | | | |

| | 75,000 | | | BorgWarner, Inc.1 | | | 4,227,642 | | | | 5,976,750 | |

| | 500,000 | | | Gentex Corp. | | | 14,728,771 | | | | 15,125,000 | |

| | | | | | | | | | | | |

| | | | | | | 18,956,413 | | | | 21,101,750 | |

| | | |

| | | | Automotive Retail (0.54%) | | | | | | | | |

| | 500,000 | | | CarMax, Inc.1 | | | 5,701,415 | | | | 16,050,000 | |

| | | |

| | | | Broadcasting (1.48%) | | | | | | | | |

| | 1,100,000 | | | Discovery Communications, Inc., Cl A1 | | | 29,767,574 | | | | 43,890,000 | |

| | | |

| | | | Casinos & Gaming (2.14%) | | | | | | | | |

| | 500,000 | | | Wynn Resorts, Ltd. | | | 1,660,930 | | | | 63,625,000 | |

| | | |

| | | | Education Services (2.50%) | | | | | | | | |

| | 1,350,000 | | | DeVry, Inc. | | | 10,721,692 | | | | 74,344,500 | |

| | | |

| | | | Hotels, Resorts & Cruise Lines (2.34%) | | | | | | | | |

| | 850,000 | | | Choice Hotels International, Inc. | | | 4,185,563 | | | | 33,022,500 | |

| | 850,000 | | | Hyatt Hotels Corp., Cl A1 | | | 24,084,647 | | | | 36,584,000 | |

| | | | | | | | | | | | |

| | | | | | | 28,270,210 | | | | 69,606,500 | |

| | | |

| | | | Household Appliances (0.58%) | | | | | | | | |

| | 225,000 | | | Stanley Black & Decker, Inc. | | | 13,421,708 | | | | 17,235,000 | |

| | | |

| | | | Internet Retail (1.88%) | | | | | | | | |

| | 110,000 | | | priceline.com, Inc.1 | | | 17,910,917 | | | | 55,708,400 | |

| | | |

| | | | Leisure Facilities (2.95%) | | | | | | | | |

| | 1,799,200 | | | Vail Resorts, Inc.1 | | | 35,613,087 | | | | 87,728,992 | |

| | | |

| | | | Specialty Stores (3.65%) | | | | | | | | |

| | 1,250,000 | | | Dick’s Sporting Goods, Inc.1 | | | 35,113,986 | | | | 49,975,000 | |

| | 950,000 | | | Tiffany & Co. | | | 30,239,344 | | | | 58,368,000 | |

| | | | | | | | | | | | |

| | | | | | | 65,353,330 | | | | 108,343,000 | |

| | | | | | | | | | | | |

| Total Consumer Discretionary | | | 312,828,423 | | | | 721,155,392 | |

| | | | | | | | | | | | |

| | |

| Energy (10.24%) | | | | | | | | |

| | | | Oil & Gas Drilling (1.79%) | | | | | | | | |

| | 775,000 | | | Helmerich & Payne, Inc. | | | 23,964,498 | | | | 53,234,750 | |

| | | |

| | | | Oil & Gas Equipment & Services (2.29%) | | | | | | | | |

| | 440,000 | | | Core Laboratories N.V.2 | | | 30,622,516 | | | | 44,954,800 | |

| | 250,000 | | | SEACOR Holdings, Inc.1 | | | 7,030,773 | | | | 23,115,000 | |

| | | | | | | | | | | | |

| | | | | | | 37,653,289 | | | | 68,069,800 | |

| | | |

| | | | Oil & Gas Exploration & Production (4.52%) | | | | | | | | |

| | 489,500 | | | Concho Resources, Inc.1 | | | 22,879,901 | | | | 52,523,350 | |

| | 360,000 | | | SM Energy Co. | | | 21,209,164 | | | | 26,708,400 | |

| | 750,000 | | | Whiting Petroleum Corp.1 | | | 26,220,923 | | | | 55,087,500 | |

| | | | | | | | | | | | |

| | | | | | | 70,309,988 | | | | 134,319,250 | |

| | | |

| | | | Oil & Gas Storage & Transportation (1.64%) | | | | | | | | |

| | 1,700,000 | | | Southern Union Co. | | | 20,450,150 | | | | 48,654,000 | |

| | | | | | | | | | | | |

| Total Energy | | | 152,377,925 | | | | 304,277,800 | |

| | | | | | | | | | | | |

| | | | | | | | | | | | |

| Shares | | | | | Cost | | | Value | |

| Common Stocks (continued) | | | | | | | | |

| Financials (15.43%) | | | | | | | | |

| | | | Asset Management & Custody Banks (3.17%) | | | | | | | | |

| | 1,175,000 | | | Eaton Vance Corp. | | $ | 25,858,501 | | | $ | 37,882,000 | |

| | 850,000 | | | T. Rowe Price Group, Inc. | | | 23,450,029 | | | | 56,457,000 | |

| | | | | | | | | | | | |

| | | | | | | 49,308,530 | | | | 94,339,000 | |

| | | |

| | | | Insurance Brokers (0.54%) | | | | | | | | |

| | 625,000 | | | Brown & Brown, Inc. | | | 11,088,023 | | | | 16,125,000 | |

| | | |

| | | | Investment Banking & Brokerage (3.64%) | | | | | | | | |

| | 6,000,000 | | | Charles Schwab Corp. | | | 11,701,340 | | | | 108,180,000 | |

| | | |

| | | | Office REITs (1.83%) | | | | | | | | |

| | 133,500 | | | Alexander’s, Inc.4 | | | 7,221,750 | | | | 54,327,825 | |

| | | |

| | | | Real Estate Services (1.17%) | | | | | | | | |

| | 1,300,000 | | | CB Richard Ellis Group, Inc., Cl A1 | | | 14,831,561 | | | | 34,710,000 | |

| | | |

| | | | Regional Banks (0.47%) | | | | | | | | |

| | 450,000 | | | First Republic Bank1 | | | 11,878,902 | | | | 13,909,500 | |

| | | |

| | | | Reinsurance (2.09%) | | | | | | | | |

| | 625,000 | | | Arch Capital Group, Ltd.1,2 | | | 20,620,935 | | | | 61,993,750 | |

| | | |

| | | | Specialized Finance (2.52%) | | | | | | | | |

| | 90,000 | | | CME Group, Inc., Cl A | | | 6,209,144 | | | | 27,139,500 | |

| | 1,300,000 | | | MSCI, Inc., Cl A1 | | | 39,123,416 | | | | 47,866,000 | |

| | | | | | | | | | | | |

| | | | | | | 45,332,560 | | | | 75,005,500 | |

| | | | | | | | | | | | |

| Total Financials | | | 171,983,601 | | | | 458,590,575 | |

| | | | | | | | | | | | |

| | |

| Health Care (12.79%) | | | | | | | | |

| | | | Health Care Distributors (1.42%) | | | | | | | | |

| | 600,000 | | | Henry Schein, Inc.1 | | | 16,675,146 | | | | 42,102,000 | |

| | | |

| | | | Health Care Equipment (4.33%) | | | | | | | | |

| | 1,300,000 | | | IDEXX Laboratories, Inc.1 | | | 53,002,192 | | | | 100,386,000 | |

| | 85,000 | | | Intuitive Surgical, Inc.1 | | | 12,819,285 | | | | 28,344,100 | |

| | | | | | | | | | | | |

| | | | | | | 65,821,477 | | | | 128,730,100 | |

| | | |

| | | | Health Care Facilities (2.05%) | | | | | | | | |

| | 600,000 | | | Brookdale Senior Living, Inc.1 | | | 15,940,319 | | | | 16,800,000 | |

| | 1,100,000 | | | Community Health Systems, Inc.1 | | | 30,985,486 | | | | 43,989,000 | |

| | | | | | | | | | | | |

| | | | | | | 46,925,805 | | | | 60,789,000 | |

| | | |

| | | | Health Care Supplies (0.50%) | | | | | | | | |

| | 225,000 | | | Gen-Probe, Inc.1,4 | | | 9,743,640 | | | | 14,928,750 | |

| | | |

| | | | Health Care Technology (0.65%) | | | | | | | | |

| | 175,000 | | | Cerner Corp.1 | | | 15,678,453 | | | | 19,460,000 | |

| | | |

| | | | Life Sciences Tools & Services (3.21%) | | | | | | | | |

| | 325,000 | | | Life Technologies Corp.1 | | | 16,407,788 | | | | 17,036,500 | |

| | 400,000 | | | Mettler-Toledo International, Inc.1 | | | 26,298,876 | | | | 68,800,000 | |

| | 175,000 | | | Thermo Fisher Scientific, Inc.1 | | | 4,853,514 | | | | 9,721,250 | |

| | | | | | | | | | | | |

| | | | | | | 47,560,178 | | | | 95,557,750 | |

| | | |

| | | | Pharmaceuticals (0.63%) | | | | | | | | |

| | 235,000 | | | Perrigo Co. | | | 17,121,784 | | | | 18,687,200 | |

| | | | | | | | | | | | |

| Total Health Care | | | 219,526,483 | | | | 380,254,800 | |

| | | | | | | | | | | | |

| | |

| Industrials (15.55%) | | | | | | | | |

| | | | Air Freight & Logistics (4.52%) | | | | | | | | |

| | 1,100,000 | | | C. H. Robinson Worldwide, Inc. | | | 20,241,548 | | | | 81,543,000 | |

| | 1,050,000 | | | Expeditors International of Washington, Inc. | | | 26,285,873 | | | | 52,647,000 | |

| | | | | | | | | | | | |

| | | | | | | 46,527,421 | | | | 134,190,000 | |

| | |

| 12 | | See Notes to Financial Statements. |

| | |

| March 31, 2011 | | Baron Asset Fund |

STATEMENT OF NET ASSETS (UNAUDITED) (Continued)

MARCH 31, 2011

| | | | | | | | | | | | |

| Shares | | | | | Cost | | | Value | |

| Common Stocks (continued) | | | | | | | | |

| Industrials (continued) | | | | | | | | |

| | | | Diversified Support Services (1.47%) | | | | | | | | |

| | 1,550,000 | | | Ritchie Bros. Auctioneers, Inc.2 | | $ | 38,130,924 | | | $ | 43,632,500 | |

| | | |

| | | | Electrical Components & Equipment (0.51%) | | | | | | | | |

| | 175,000 | | | Roper Industries, Inc. | | | 14,045,821 | | | | 15,130,500 | |

| | | |

| | | | Environmental & Facilities Services (2.16%) | | | | | | | | |

| | 725,000 | | | Stericycle, Inc.1 | | | 21,068,310 | | | | 64,285,750 | |

| | | |

| | | | Human Resource & Employment Services (0.88%) | | | | | | | | |

| | 850,000 | | | Robert Half International, Inc. | | | 776,403 | | | | 26,010,000 | |

| | | |

| | | | Research & Consulting Services (3.07%) | | | | | | | | |

| | 50,000 | | | Dun & Bradstreet Corp. | | | 3,708,791 | | | | 4,012,000 | |

| | 1,400,000 | | | Nielsen Holdings NV1,2 | | | 34,671,114 | | | | 38,234,000 | |

| | 1,500,000 | | | Verisk Analytics, Inc., Cl A1 | | | 39,224,920 | | | | 49,140,000 | |

| | | | | | | | | | | | |

| | | | | | | 77,604,825 | | | | 91,386,000 | |

| | | |

| | | | Trading Companies & Distributors (2.94%) | | | | | | | | |

| | 1,350,000 | | | Fastenal Co. | | | 53,631,828 | | | | 87,520,500 | |

| | | | | | | | | | | | |

| Total Industrials | | | 251,785,532 | | | | 462,155,250 | |

| | | | | | | | | | | | |

| | |

| Information Technology (14.56%) | | | | | | | | |

| | | | Application Software (5.49%) | | | | | | | | |

| | 800,000 | | | ANSYS, Inc.1 | | | 26,291,691 | | | | 43,352,000 | |

| | 350,000 | | | Citrix Systems, Inc.1 | | | 13,746,569 | | | | 25,711,000 | |

| | 900,000 | | | FactSet Research Systems, Inc. | | | 52,246,929 | | | | 94,257,000 | |

| | | | | | | | | | | | |

| | | | | | | 92,285,189 | | | | 163,320,000 | |

| | | |

| | | | Communications Equipment (1.05%) | | | | | | | | |

| | 600,000 | | | Polycom, Inc.1 | | | 24,637,221 | | | | 31,110,000 | |

| | | |

| | | | Data Processing & Outsourced Services (0.58%) | | | | | | | | |

| | 150,000 | | | FleetCor Technologies, Inc.1 | | | 4,856,202 | | | | 4,899,000 | |

| | 600,000 | | | Western Union Co. | | | 11,184,906 | | | | 12,462,000 | |

| | | | | | | | | | | | |

| | | | | | | 16,041,108 | | | | 17,361,000 | |

| | | |

| | | | Electronic Equipment & Instruments (0.93%) | | | | | | | | |

| | 800,000 | | | FLIR Systems, Inc. | | | 17,739,772 | | | | 27,688,000 | |

| | | |

| | | | Internet Software & Services (0.09%) | | | | | | | | |

| | 50,000 | | | WebMD Health Corp., Cl A1 | | | 2,665,125 | | | | 2,671,000 | |

| | | |

| | | | IT Consulting & Other Services (6.18%) | | | | | | | | |

| | 700,000 | | | Equinix, Inc.1,4 | | | 56,983,955 | | | | 63,770,000 | |

| | 2,875,000 | | | Gartner, Inc.1 | | | 68,065,780 | | | | 119,801,250 | |

| | | | | | | | | | | | |

| | | | | | | 125,049,735 | | | | 183,571,250 | |

| | | |

| | | | Systems Software (0.24%) | | | | | | | | |

| | 375,000 | | | TOTVS SA (Brazil)2 | | | 6,655,067 | | | | 7,200,717 | |

| | | | | | | | | | | | |

| Total Information Technology | | | 285,073,217 | | | | 432,921,967 | |

| | | | | | | | | | | | |

| | |

| Materials (0.95%) | | | | | | | | |

| | | | Diversified Metals & Mining (0.45%) | | | | | | | | |

| | 225,000 | | | Molycorp, Inc.1 | | | 11,522,309 | | | | 13,504,500 | |

| | | |

| | | | Specialty Chemicals (0.50%) | | | | | | | | |

| | 300,000 | | | Rockwood Holdings, Inc.1 | | | 14,132,562 | | | | 14,766,000 | |

| | | | | | | | | | | | |

| Total Materials | | | 25,654,871 | | | | 28,270,500 | |

| | | | | | | | | | | | |

| | | | | | | | | | |

| Shares | | | | Cost | | | Value | |

Common Stocks (continued) | | | | | | | | |

Telecommunication Services (3.67%) | | | | | | | | |

| | Wireless Telecommunication Services (3.67%) | | | | | | | | |

| 1,025,000 | | NII Holdings, Inc.1 | | $ | 39,262,199 | | | $ | 42,711,750 | |

| 1,675,000 | | SBA Communications Corp., Cl A1 | | | 55,336,595 | | | | 66,464,000 | |

| | | | | | | | | | |

Total Telecommunication Services | | | 94,598,794 | | | | 109,175,750 | |

| | | | | | | | | | |

Total Common Stocks | | | 1,513,828,846 | | | | 2,896,802,034 | |

| | | | | | | | | | |

| | | | | | | | | | |

Private Equity Investments (1.26%) | | | | | | | | |

Consumer Discretionary (0.35%) | | | | | | | | |

| | Hotels, Resorts & Cruise Lines (0.35%) | | | | | | | | |

| 5,200,000 | | Kerzner International Holdings, Ltd., Cl A1,2,3,4,6 | | | 52,000,000 | | | | 10,400,000 | |

| | | | | | | | | | |

| | |

Financials (0.91%) | | | | | | | | |

| | Asset Management & Custody Banks (0.91%) | | | | | | | | |

| 6,532,691 | | Windy City Investments Holdings LLC1,3,4,6 | | | 33,639,547 | | | | 25,085,533 | |

| 523,532 | | Windy City Investments Holdings LLC1,3,4,6 | | | 942,357 | | | | 1,910,891 | |

| | | | | | | | | | |

Total Financials | | | 34,581,904 | | | | 26,996,424 | |

| | | | | | | | | | |

Total Private Equity Investments | | | 86,581,904 | | | | 37,396,424 | |

| | | | | | | | | | |

| | | | | | | | | | |

Principal

Amount | | | | | | |

Short Term Investments (0.90%) | | | | | | | | |

| $26,780,086 | | Repurchase Agreement with Fixed Income Clearing Corp., dated 03/31/2011, 0.01% due 04/01/2011; Proceeds at maturity - $26,780,094; (Fully collateralized by U.S. Treasury Note, 3.50% due 05/15/2020; Market value - $28,122,675)5 | | | 26,780,086 | | | | 26,780,086 | |

| | | | | | | | | | |

Total Investments (99.61%) | | $ | 1,627,190,836 | | | | 2,960,978,544 | |

| | | | | | | | | | |

Cash and Other Assets Less Liabilities (0.39%) | | | | 11,673,116 | |

| | | | | | | | | | |

Net Assets | | | | | | $ | 2,972,651,660 | |

| | | | | | | | | | |

Retail Shares (Equivalent to $59.11 per share based on 44,491,071 shares outstanding) | | | $ | 2,629,692,538 | |

| | | | | | | | | | |

Institutional Shares (Equivalent to $59.38 per share

based on 5,775,270 shares outstanding) | | | $ | 342,959,122 | |

| | | | | | | | | | |

| % | Represents percentage of net assets. |

| 1 | Non-income producing securities. |

| 3 | At March 31, 2011, the market value of restricted and fair valued securities amounted to $37,396,424 or 1.26% of net assets. None of these securities are deemed liquid. See Note 6 regarding Restricted Securities. |

| 4 | The Adviser has reclassified/classified certain securities in or out of this sub-industry. Such reclassifications/classifications are not supported by S&P or MSCI. |

| 5 | Level 2 security. See Note 7 regarding Fair Value Measurements. |

| 6 | Level 3 security. See Note 7 regarding Fair Value Measurements. |

| | |

| See Notes to Financial Statements. | | 13 |

| | |

| Baron Growth Fund | | March 31, 2011 |

STATEMENT OF NET ASSETS (UNAUDITED)

MARCH 31, 2011

| | | | | | | | | | | | |

| Shares | | | | | Cost | | | Value | |

| Common Stocks (96.58%) | | | | | |

| Consumer Discretionary (22.47%) | | | | | |

| | | | Apparel Retail (0.39%) | | | | | | | | |

| | 1,464,900 | | | Companhia Hering SA (Brazil)2 | | $ | 21,638,953 | | | $ | 26,917,588 | |

| | | |

| | | | Apparel, Accessories & Luxury Goods (1.43%) | | | | | | | | |

| | 1,450,000 | | | Under Armour, Inc., Cl A1 | | | 47,233,672 | | | | 98,672,500 | |

| | | |

| | | | Automotive Retail (0.34%) | | | | | | | | |

| | 200,000 | | | CarMax, Inc.1 | | | 1,895,337 | | | | 6,420,000 | |

| | 850,000 | | | Penske Automotive Group, Inc.1 | | | 14,931,776 | | | | 17,017,000 | |

| | | | | | | | | | | | |

| | | | | | | 16,827,113 | | | | 23,437,000 | |

| | | |

| | | | Casinos & Gaming (1.45%) | | | | | | | | |

| | 2,700,000 | | | Penn National Gaming, Inc.1 | | | 75,975,993 | | | | 100,062,000 | |

| | | |

| | | | Distributors (1.52%) | | | | | | | | |

| | 4,350,000 | | | LKQ Corp.1 | | | 57,463,126 | | | | 104,835,000 | |

| | | |

| | | | Education Services (5.82%) | | | | | | | | |

| | 4,667,005 | | | Anhanguera Educacional Participacoes SA (Brazil)2 | | | 61,955,342 | | | | 114,284,666 | |

| | 3,625,000 | | | DeVry, Inc.4 | | | 60,704,873 | | | | 199,628,750 | |

| | 675,000 | | | Strayer Education, Inc.4 | | | 55,103,824 | | | | 88,080,750 | |

| | | | | | | | | | | | |

| | | | | | | 177,764,039 | | | | 401,994,166 | |

| | | |

| | | | Home Improvement Retail (0.37%) | | | | | | | | |

| | 1,032,729 | | | Lumber Liquidators Holdings, Inc.1 | | | 25,756,399 | | | | 25,807,897 | |

| | | |

| | | | Hotels, Resorts & Cruise Lines (1.69%) | | | | | | | | |

| | 3,000,000 | | | Choice Hotels International, Inc.4 | | | 74,119,736 | | | | 116,550,000 | |

| | | |

| | | | Internet Retail (0.78%) | | | | | | | | |

| | 1,000,000 | | | Blue Nile, Inc.1,4 | | | 32,886,089 | | | | 53,990,000 | |

| | | |

| | | | Leisure Facilities (1.42%) | | | | | | | | |

| | 1,900,000 | | | Vail Resorts, Inc.1,4 | | | 51,691,238 | | | | 92,644,000 | |

| | 430,600 | | | Whistler Blackcomb Holdings, Inc. (Canada)2 | | | 5,253,307 | | | | 5,218,721 | |

| | | | | | | | | | | | |

| | | | | | | 56,944,545 | | | | 97,862,721 | |

| | | |

| | | | Publishing (2.28%) | | | | | | | | |

| | 2,154,552 | | | Morningstar, Inc. | | | 62,871,270 | | | | 125,782,746 | |

| | 3,350,000 | | | The New York Times Co., Cl A1 | | | 32,346,583 | | | | 31,724,500 | |

| | | | | | | | | | | | |

| | | | | | | 95,217,853 | | | | 157,507,246 | |

| | | |

| | | | Restaurants (2.08%) | | | | | | | | |

| | 825,000 | | | Panera Bread Co., Cl A1 | | | 32,060,440 | | | | 104,775,000 | |

| | 800,000 | | | Peet’s Coffee & Tea, Inc.1,4 | | | 18,562,773 | | | | 38,472,000 | |

| | | | | | | | | | | | |

| | | | | | | 50,623,213 | | | | 143,247,000 | |

| | | |

| | | | Specialty Stores (2.90%) | | | | | | | | |

| | 5,000,000 | | | Dick’s Sporting Goods, Inc.1 | | | 86,074,246 | | | | 199,900,000 | |

| | | | | | | | | | | | |

| Total Consumer Discretionary | | | 818,524,977 | | | | 1,550,783,118 | |

| | | | | | | | | | | | |

| | |

| Consumer Staples (5.26%) | | | | | | | | |

| | | | Food Distributors (0.50%) | | | | | | | | |

| | 768,401 | | | United Natural Foods, Inc.1 | | | 30,490,705 | | | | 34,439,733 | |

| | | |

| | | | Household Products (0.92%) | | | | | | | | |

| | 800,000 | | | Church & Dwight Co., Inc. | | | 29,177,096 | | | | 63,472,000 | |

| | | |

| | | | Packaged Foods & Meats (3.84%) | | | | | | | | |

| | 1,064,823 | | | Diamond Foods, Inc. | | | 38,931,996 | | | | 59,417,123 | |

| | 4,000,000 | | | Dole Food Co., Inc.1 | | | 48,959,106 | | | | 54,520,000 | |

| | 1,107,649 | | | Ralcorp Holdings, Inc.1 | | | 40,376,485 | | | | 75,796,421 | |

| | 200,000 | | | Seneca Foods Corp., Cl A1 | | | 4,400,000 | | | | 5,974,000 | |

| | 1,225,000 | | | TreeHouse Foods, Inc.1 | | | 47,319,599 | | | | 69,665,750 | |

| | | | | | | | | | | | |

| | | | | | | 179,987,186 | | | | 265,373,294 | |

| | | | | | | | | | | | |

| Total Consumer Staples | | | 239,654,987 | | | | 363,285,027 | |

| | | | | | | | | | | | |

| | | | | | | | | | | | |

| Shares | | | | | Cost | | | Value | |

| Common Stocks (continued) | | | | | | | | |

| Energy (12.49%) | | | | | | | | |

| | | | Oil & Gas Drilling (1.00%) | | | | | | | | |

| | 1,000,000 | | | Helmerich & Payne, Inc. | | $ | 22,564,231 | | | $ | 68,690,000 | |

| | | |

| | | | Oil & Gas Equipment & Services (5.19%) | | | | | | | | |

| | 875,764 | | | CARBO Ceramics, Inc. | | | 59,006,928 | | | | 123,587,816 | |

| | 1,388,272 | | | Core Laboratories N.V.2 | | | 43,036,240 | | | | 141,839,750 | |

| | 1,000,000 | | | SEACOR Holdings, Inc. 1 | | | 69,798,678 | | | | 92,460,000 | |

| | | | | | | | | | | | |

| | | | | | | 171,841,846 | | | | 357,887,566 | |

| | | |

| | | | Oil & Gas Exploration & Production (4.38%) | | | | | | | | |

| | 1,600,000 | | | Brigham Exploration Co.1 | | | 24,210,346 | | | | 59,488,000 | |

| | 700,000 | | | Concho Resources, Inc.1 | | | 20,053,293 | | | | 75,110,000 | |

| | 2,000,000 | | | Denbury Resources, Inc.1 | | | 11,237,573 | | | | 48,800,000 | |

| | 247,191 | | | Oasis Petroleum, Inc.1 | | | 3,460,674 | | | | 7,816,180 | |

| | 1,500,000 | | | SM Energy Co. | | | 52,961,473 | | | | 111,285,000 | |

| | | | | | | | | | | | |

| | | | | | | 111,923,359 | | | | 302,499,180 | |

| | | |

| | | | Oil & Gas Storage & Transportation (1.92%) | | | | | | | | |

| | 3,600,000 | | | Southern Union Co. | | | 48,544,865 | | | | 103,032,000 | |

| | 814,751 | | | Targa Resources Corp. | | | 22,236,065 | | | | 29,526,576 | |

| | | | | | | | | | | | |

| | | | | | | 70,780,930 | | | | 132,558,576 | |

| | | | | | | | | | | | |

| Total Energy | | | 377,110,366 | | | | 861,635,322 | |

| | | | | | | | | | | | |

| | |

| Financials (10.72%) | | | | | | | | |

| | | | Asset Management & Custody Banks (1.29%) | | | | | | | | |

| | 500,000 | | | Cohen & Steers, Inc. | | | 6,508,018 | | | | 14,840,000 | |

| | 1,500,000 | | | Eaton Vance Corp. | | | 26,667,458 | | | | 48,360,000 | |

| | 925,000 | | | Financial Engines, Inc.1 | | | 13,840,204 | | | | 25,493,000 | |

| | | | | | | | | | | | |

| | | | | | | 47,015,680 | | | | 88,693,000 | |

| | | |

| | | | Consumer Finance (0.49%) | | | | | | | | |

| | 450,000 | | | Green Dot Corp., Cl A1 | | | 24,088,302 | | | | 19,309,500 | |

| | 1,385,188 | | | NetSpend Holdings, Inc.1 | | | 16,889,173 | | | | 14,572,178 | |

| | | | | | | | | | | | |

| | | | | | | 40,977,475 | | | | 33,881,678 | |

| | | |

| | | | Diversified REITs (0.14%) | | | | | | | | |

| | 470,000 | | | American Assets Trust, Inc. | | | 9,735,710 | | | | 9,996,900 | |

| | | |

| | | | Investment Banking & Brokerage (0.36%) | | | | | | | | |

| | 1,000,000 | | | Jefferies Group, Inc. | | | 9,859,745 | | | | 24,940,000 | |

| | | |

| | | | Life & Health Insurance (0.78%) | | | | | | | | |

| | 2,100,000 | | | Primerica, Inc. | | | 46,453,115 | | | | 53,571,000 | |

| | | |

| | | | Office REITs (1.72%) | | | | | | | | |

| | 135,500 | | | Alexander’s, Inc.5 | | | 28,639,990 | | | | 55,141,725 | |

| | 3,400,000 | | | Douglas Emmett, Inc. | | | 47,518,561 | | | | 63,750,000 | |

| | | | | | | | | | | | |

| | | | | | | 76,158,551 | | | | 118,891,725 | |

| | | |

| | | | Regional Banks (0.36%) | | | | | | | | |

| | 1,250,000 | | | SJB Escrow Corp., Cl A, 144A1,5,6 | | | 25,000,000 | | | | 24,750,000 | |

| | | |

| | | | Reinsurance (2.01%) | | | | | | | | |

| | 1,400,000 | | | Arch Capital Group, Ltd.1,2 | | | 41,487,457 | | | | 138,866,000 | |

| | | |

| | | | Residential REITs (0.29%) | | | | | | | | |

| | 600,000 | | | American Campus Communities, Inc. | | | 16,235,192 | | | | 19,800,000 | |

| | | |

| | | | Specialized Finance (2.25%) | | | | | | | | |

| | 4,222,433 | | | MSCI, Inc., Cl A1 | | | 96,041,636 | | | | 155,469,983 | |

| | | |

| | | | Specialized REITs (1.03%) | | | | | | | | |

| | 775,000 | | | Alexandria Real Estate Equities, Inc.5 | | | 29,669,521 | | | | 60,426,750 | |

| | 400,000 | | | LaSalle Hotel Properties | | | 8,565,042 | | | | 10,800,000 | |

| | | | | | | | | | | | |

| | | | | | | 38,234,563 | | | | 71,226,750 | |

| | | | | | | | | | | | |

| Total Financials | | | 447,199,124 | | | | 740,087,036 | |

| | | | | | | | | | | | |

| | |

| 14 | | See Notes to Financial Statements. |

| | |

| March 31, 2011 | | Baron Growth Fund |

STATEMENT OF NET ASSETS (UNAUDITED) (Continued)

MARCH 31, 2011

| | | | | | | | | | | | |

| Shares | | | | | Cost | | | Value | |

| Common Stocks (continued) | | | | | | | | |

| Health Care (15.10%) | | | | | | | | |

| | | | Health Care Equipment (4.56%) | | | | | | | | |

| | 2,600,000 | | | Edwards Lifesciences Corp.1 | | $ | 36,868,520 | | | $ | 226,200,000 | |

| | 1,150,000 | | | IDEXX Laboratories, Inc.1 | | | 38,825,384 | | | | 88,803,000 | |

| | | | | | | | | | | | |

| | | | | | | 75,693,904 | | | | 315,003,000 | |

| | | |

| | | | Health Care Facilities (2.58%) | | | | | | | | |

| | 3,625,000 | | | Community Health Systems, Inc.1 | | | 71,473,442 | | | | 144,963,750 | |

| | 1,300,000 | | | VCA Antech, Inc.1 | | | 34,889,375 | | | | 32,734,000 | |

| | | | | | | | | | | | |

| | | | | | | 106,362,817 | | | | 177,697,750 | |

| | | |

| | | | Health Care Services (0.66%) | | | | | | | | |

| | 600,000 | | | Chemed Corp. | | | 21,302,479 | | | | 39,966,000 | |

| | 125,000 | | | IPC The Hospitalist Co., Inc.1 | | | 2,062,500 | | | | 5,676,250 | |

| | | | | | | | | | | | |

| | | | | | | 23,364,979 | | | | 45,642,250 | |

| | | |

| | | | Health Care Supplies (1.26%) | | | | | | | | |

| | 1,200,000 | | | Gen-Probe, Inc.1,5 | | | 49,959,009 | | | | 79,620,000 | |

| | 175,000 | | | Neogen Corp.1 | | | 3,887,774 | | | | 7,241,500 | |

| | | | | | | | | | | | |

| | | | | | | 53,846,783 | | | | 86,861,500 | |

| | | |

| | | | Health Care Technology (0.30%) | | | | | | | | |

| | 1,000,000 | | | Allscripts Healthcare Solutions, Inc.1 | | | 16,782,598 | | | | 20,990,000 | |

| | | |

| | | | Life Sciences Tools & Services (3.41%) | | | | | | | | |

| | 1,000,000 | | | Mettler-Toledo International, Inc.1 | | | 58,852,435 | | | | 172,000,000 | |

| | 880,943 | | | Techne Corp. | | | 46,631,249 | | | | 63,075,519 | |

| | | | | | | | | | | | |

| | | | | | | 105,483,684 | | | | 235,075,519 | |

| | | |

| | | | Managed Health Care (2.33%) | | | | | | | | |

| | 2,500,000 | | | AMERIGROUP Corp.1,4 | | | 42,959,676 | | | | 160,625,000 | |

| | | | | | | | | | | | |

| Total Health Care | | | 424,494,441 | | | | 1,041,895,019 | |

| | | | | | | | | | | | |

| | |

| Industrials (11.24%) | | | | | | | | |

| | | | Construction &

Engineering (1.20%) | | | | | | | | |

| | 3,000,000 | | | AECOM Technology Corp.1 | | | 65,871,334 | | | | 83,190,000 | |

| | | |

| | | | Diversified Support

Services (2.49%) | | | | | | | | |

| | 2,075,000 | | | Copart, Inc.1 | | | 51,478,764 | | | | 89,909,750 | |

| | 2,900,000 | | | Ritchie Bros. Auctioneers, Inc.2 | | | 66,712,065 | | | | 81,635,000 | |

| | | | | | | | | | | | |

| | | | | | | 118,190,829 | | | | 171,544,750 | |

| | | |

| | | | Electrical Components & Equipment (0.95%) | | | | | | | | |

| | 3,243,578 | | | Generac Holdings, Inc.1 | | | 43,195,908 | | | | 65,812,198 | |

| | | |

| | | | Environmental & Facilities Services (1.02%) | | | | | | | | |

| | 2,850,000 | | | Tetra Tech, Inc.1 | | | 71,178,894 | | | | 70,366,500 | |

| | | |

| | | | Industrial Machinery (1.56%) | | | | | | | | |

| | 704,000 | | | Middleby Corp.1 | | | 62,120,615 | | | | 65,626,880 | |

| | 400,000 | | | Valmont Industries, Inc. | | | 32,589,034 | | | | 41,748,000 | |

| | | | | | | | | | | | |

| | | | | | | 94,709,649 | | | | 107,374,880 | |

| | | |

| | | | Railroads (1.69%) | | | | | | | | |

| | 2,000,000 | | | Genesee & Wyoming, Inc., Cl A1 | | | 32,221,169 | | | | 116,400,000 | |

| | | |

| | | | Research & Consulting Services (1.52%) | | | | | | | | |

| | 939,811 | | | CoStar Group, Inc.1 | | | 40,526,096 | | | | 58,907,353 | |

| | 400,000 | | | IHS, Inc., Cl A1 | | | 16,387,387 | | | | 35,500,000 | |

| | 600,000 | | | Mistras Group, Inc.1 | | | 7,563,468 | | | | 10,326,000 | |

| | | | | | | | | | | | |

| | | | | | | 64,476,951 | | | | 104,733,353 | |

| | | |

| | | | Trading Companies & Distributors (0.50%) | | | | | | | | |

| | 500,000 | | | MSC Industrial Direct Co., Inc., Cl A | | | 17,821,237 | | | | 34,235,000 | |

| | | | | | | | | | | | |

| Shares | | | | | Cost | | | Value | |

| Common Stocks (continued) | | | | | | | | |

| Industrials (continued) | | | | | | | | |

| | | | Trucking (0.31%) | | | | | | | | |

| | 475,000 | | | Landstar System, Inc. | | $ | 11,073,375 | | | $ | 21,698,000 | |

| | | | | | | | | | | | |

| Total Industrials | | | 518,739,346 | | | | 775,354,681 | |

| | | | | | | | | | | | |

| | |

| Information Technology (13.65%) | | | | | | | | |

| | | | Application Software (7.58%) | | | | | | | | |

| | 1,400,000 | | | Advent Software, Inc.1 | | | 26,532,888 | | | | 40,138,000 | |

| | 2,250,000 | | | ANSYS, Inc.1 | | | 54,764,730 | | | | 121,927,500 | |

| | 183,452 | | | Blackboard, Inc.1 | | | 6,927,498 | | | | 6,648,300 | |

| | 1,000,000 | | | Concur Technologies, Inc.1 | | | 22,319,863 | | | | 55,450,000 | |

| | 1,635,000 | | | FactSet Research Systems, Inc. | | | 82,436,633 | | | | 171,233,550 | |

| | 1,550,000 | | | Pegasystems, Inc. | | | 47,512,692 | | | | 58,807,000 | |

| | 535,038 | | | RealPage, Inc.1 | | | 13,417,979 | | | | 14,836,604 | |

| | 2,423,656 | | | SS&C Technologies Holdings, Inc.1 | | | 40,675,932 | | | | 49,491,056 | |

| | 140,107 | | | Synchronoss Technologies, Inc.1 | | | 4,625,396 | | | | 4,868,718 | |

| | | | | | | | | | | | |

| | | | | | | 299,213,611 | | | | 523,400,728 | |

| | | |

| | | | Internet Software & Services (1.16%) | | | | | | | | |

| | 1,500,000 | | | WebMD Health Corp., Cl A1 | | | 44,434,390 | | | | 80,130,000 | |

| | | |

| | | | IT Consulting & Other Services (3.68%) | | | | | | | | |

| | 372,572 | | | Booz Allen Hamilton Holding Corp.1 | | | 6,504,476 | | | | 6,710,021 | |

| | 925,000 | | | Equinix, Inc.1,5 | | | 29,378,111 | | | | 84,267,500 | |

| | 3,000,000 | | | Gartner, Inc.1 | | | 49,076,692 | | | | 125,010,000 | |

| | 465,734 | | | MAXIMUS, Inc. | | | 34,793,690 | | | | 37,803,629 | |

| | | | | | | | | | | | |

| | | | | | | 119,752,969 | | | | 253,791,150 | |

| | | |

| | | | Systems Software (1.23%) | | | | | | | | |

| | 4,418,000 | | | TOTVS SA (Brazil)2 | | | 60,197,679 | | | | 84,834,043 | |

| | | | | | | | | | | | |

| Total Information Technology | | | 523,598,649 | | | | 942,155,921 | |

| | | | | | | | | | | | |

| | |

| Materials (2.85%) | | | | | | | | |

| | | | Diversified Metals & Mining (2.55%) | | | | | | | | |

| | 2,929,426 | | | Molycorp, Inc.1 | | | 76,925,262 | | | | 175,824,149 | |

| | | |

| | | | Fertilizers & Agricultural Chemicals (0.30%) | | | | | | | | |

| | 601,920 | | | Intrepid Potash, Inc.1 | | | 19,321,732 | | | | 20,958,854 | |

| | | | | | | | | | | | |

| Total Materials | | | 96,246,994 | | | | 196,783,003 | |

| | | | | | | | | | | | |

| |

| Telecommunication Services (0.52%) | | | | | |

| | | | Wireless Telecommunication Services (0.52%) | | | | | | | | |

| | 900,000 | | | SBA Communications Corp., Cl A1 | | | 3,361,183 | | | | 35,712,000 | |

| | | | | | | | | | | | |

| | |

| Utilities (2.28%) | | | | | | | | |

| | | | Electric Utilities (2.28%) | | | | | | | | |

| | 2,250,000 | | | ITC Holdings Corp. | | | 69,934,399 | | | | 157,275,000 | |

| | | | | | | | | | | | |

| Total Common Stocks | | | 3,518,864,466 | | | | 6,664,966,127 | |

| | | | | | | | | | | | |

| | | | | | | | | | | | |

| Private Equity Investments (0.35%) | | | | | |

| Consumer Discretionary (0.22%) | | | | | | | | |

| | | | Hotels, Resorts & Cruise Lines (0.22%) | | | | | | | | |

| | 7,400,000 | | | Kerzner International Holdings, Ltd., Cl A1,2,3,5,7 | | | 74,000,000 | | | | 14,800,000 | |

| | | | | | | | | | | | |

| | |

| See Notes to Financial Statements. | | 15 |

| | |

| Baron Growth Fund | | March 31, 2011 |

STATEMENT OF NET ASSETS (UNAUDITED) (Continued)

MARCH 31, 2011

| | | | | | | | | | |

| Shares | | | | Cost | | | Value | |

Private Equity Investments (continued) | | | | | |

Financials (0.13%) | | | | | | | | |

| | Asset Management & Custody Banks (0.13%) | | | | | | | | |

| 176,224 | | Windy City Investments Holdings LLC1,3,5,7 | | $ | 317,203 | | | $ | 643,217 | |

| 2,198,950 | | Windy City Investments Holdings LLC1,3,5,7 | | | 8,313,795 | | | | 8,443,967 | |

| | | | | | | | | | |

Total Financials | | | 8,630,998 | | | | 9,087,184 | |

| | | | | | | | | | |

Total Private Equity Investments | | | 82,630,998 | | | | 23,887,184 | |

| | | | | | | | | | |

| | | | | | | | | | |

Warrants (0.01%) | | | | | | | | |

Financials (0.01%) | | | | | | | | |

| | Regional Banks (0.01%) | | | | | | | | |

| 75,000 | | SJB Escrow Corp. Warrants, Exp 02/16/20171,5,6 | | | 0 | | | | 489,187 | |

| | | | | | | | | | |

| | | | | | | | | | |

Principal

Amount | | | | | | |

Short Term Investments (2.71%) | | | | | | | | |

| $186,957,745 | | Repurchase Agreement with Fixed Income Clearing Corp., dated 03/31/2011, 0.01% due 04/01/2011; Proceeds at maturity - $186,957,797; (Fully collateralized by U.S. Treasury Note, 3.50% due 05/15/2020; Market value - $184,559,550 and U.S. Treasury Note, 1.875% due 06/30/2015; Market value - $11,748,450)6 | | | 186,957,745 | | | | 186,957,745 | |

| | | | | | | | | | |

Total Investments (99.65%) | | $ | 3,788,453,209 | | | | 6,876,300,243 | |

| | | | | | | | | | |

Cash and Other Assets Less Liabilities (0.35%) | | | | | | | 24,234,376 | |

| | | | | | | | | | |

Net Assets | | | | | | $ | 6,900,534,619 | |

| | | | | | | | | | |

Retail Shares (Equivalent to $56.03 per share based on

99,891,741 shares outstanding) | | | $ | 5,596,701,625 | |

| | | | | | | | | | |

Institutional Shares (Equivalent to $56.29 per share

based on 23,162,844 shares outstanding) | | | $ | 1,303,832,994 | |

| | | | | | | | | | |

| % | Represents percentage of net assets. |

| 1 | Non-income producing securities. |

| 3 | At March 31, 2011, the market value of restricted and fair valued securities amounted to $23,887,184 or 0.35% of net assets. None of these securities are deemed liquid. See Note 6 regarding Restricted Securities. |

| 4 | See Note 9 regarding “Affiliated” companies. |

| 5 | The Adviser has reclassified/classified certain securities in or out of this sub-industry. Such reclassifications/classifications are not supported by S&P or MSCI. |

| 6 | Level 2 security. See Note 7 regarding Fair Value Measurements. |

| 7 | Level 3 security. See Note 7 regarding Fair Value Measurements. |