Exhibit 99.6

GOVERNMENT OF ALBERTA

2024-25 Second

Quarter Fiscal

Update and

Economic Statement

Table of Contents

2024-25 Second Quarter Fiscal Plan Highlights | 3 | |||

Revenue Highlights | 4 | |||

Expense Highlights | 6 | |||

Fiscal Framework | 7 | |||

Assets and Liabilities | 9 | |||

Capital Plan Highlights | 11 | |||

Fiscal Update and Economic Statement | 12 | |||

2024-25 Second Quarter Fiscal Update Tables | 19 | |||

Reporting Methodology and Legislative Compliance | 27 | |||

Note: Amounts presented in tables may not add to totals due to rounding.

Note on restatements and accounting policy changes:

| • | 2023-24 Actual and 2024-25 Budget numbers have been restated to reflect the revised government structure under the Government Organization Act (Order in Council 157/2023, June 9, 2023, Order in Council 29/2024, February 16, 2024 and Order in Council 234/2024, August 28, 2024). |

| • | Effective April 1, 2023, the Province adopted the Public Private Partnerships (P3) standard. This standard provides guidance on how to account for public private partnerships between public and private sector entities, where the public sector entity procures infrastructure using a private sector partner. The Province used prospective application to adopt this standard, except for P3 contracts entered prior to April 1, 2023, of which retroactive application is used without restating prior year comparatives. As a result, the reported opening net book value of tangible capital assets decreased by $415 million and opening P3 liabilities decreased by $353 million. Effective April 1, 2024, associated debt servicing costs were increased by $24 million. |

| • | Effective April 1, 2023, the Province adopted the Revenue standard. This standard provides guidance on how to account for and report revenue, and specifically differentiates between revenue arising from exchange and non-exchange transactions. The Province used prospective application to adopt this standard. As a result, 2023 comparatives are not restated. |

| • | Effective April 1, 2023, the Province adopted the Purchased Intangibles guideline. The Province used prospective application to adopt this guideline. As a result, 2023 comparatives are not restated. |

| • | Effective September 1, 2024, Recovery Alberta has been transferred from the Ministry of Health to the Ministry of Mental Health and Addiction through amendments to Alberta’s Provincial Health Agencies Act (Act). The Act established the acute care, primary care, continuing care and mental health and addiction health services sectors (Ministerial Order 803/2024, August 28, 2024). |

Treasury Board and Finance, Government of Alberta

November, 2024

2024–25 Second Quarter Fiscal Update and Economic Statement,

Additional copies of this report may be obtained by visiting our website at:

www.alberta.ca/budget-documents.aspx

| 2 | 2024-25 Second Quarter Fiscal Update and Economic Statement | |

2024-25 Second Quarter Fiscal Plan Highlights

The 2024-25 surplus is now forecast to be $4.6 billion at second quarter, up $1.7 billion from the estimated first quarter forecast and $4.2 billion more than Budget 2024. While the fiscal situation has improved in 2024-25, uncertainty about global economic conditions and their impact on Alberta’s economy as well as government revenues and expenses present risks in the near and medium term. The economic forecast has been revised lower for both 2024 and 2025, compared to first quarter, reflecting weaker-than-expected domestic demand arising from a slowing employment growth and lower investment in industries outside the oil and gas sector in 2024, while a lower population forecast has dampened the outlook for 2025.

The government’s revenue is highly sensitive to changes in oil prices. Potential downward pressure on oil prices coupled with spending pressures mainly as a result of population growth and compensation negotiations, pose

risks to the forecast for Budget 2025. The government is monitoring its fiscal situation and is committed to the efficient delivery of core programs and services and key government priorities.

The 2024-25 second quarter forecast is prepared in accordance with Alberta’s fiscal rules and Alberta’s government is on track to allocate surplus cash to debt repayment and the Alberta Fund.

Total revenue in 2024-25 is forecast at $77.9 billion, $4.4 billion more than budget, mainly due to higher-than-expected non-renewable resource and personal income tax revenues.

Total expense is forecast at $73.3 billion, up $0.1 billion from budget. Operating expense is up by $1.2 billion, mainly for physician compensation, AHS service activities, income support program delivery costs, and to address enrolment growth in K-12 education. Disaster and emergency assistance, primarily for wildfire fighting, is estimated at $0.8 billion. This

$0.8 billion increase is offset by $0.1 billion in dedicated revenue and $0.7 billion is preliminarily allocated from the contingency. Capital grants, amortization, inventory consumption, pension provision, loss on disposal, and debt servicing costs increased by a net of $0.2 billion.

The 2024-25 Capital Plan is now forecast at $8.3 billion, which is close to budget. The forecast aligns with the progress of completion and project scheduling, ensuring projects continue to be delivered as committed in Budget 2024.

Taxpayer-supported debt is forecast at $84 billion on March 31, 2025, an increase of $2.2 billion from 2024, due to additional borrowing required in 2024-25 for pre-funding of large upcoming debt maturities. At March 31, 2025, net debt to GDP is forecast at 8.2 per cent.

Fiscal Plan Summary

(millions of dollars)

| Fiscal Year | Change

from

Budget | |||||||||||||||

| 2023-24 | 2024-25 | |||||||||||||||

| Actual | Budget | Forecast | ||||||||||||||

Revenue | ||||||||||||||||

Tax revenue | 26,747 | 28,645 | 29,867 | 1,222 | ||||||||||||

Non-renewable resource revenue | 19,287 | 17,315 | 20,295 | 2,980 | ||||||||||||

Federal transfers | 12,336 | 12,640 | 12,753 | 113 | ||||||||||||

Investment income | 4,581 | 3,267 | 3,723 | 456 | ||||||||||||

Other revenue | 11,781 | 11,670 | 11,249 | (421 | ) | |||||||||||

Total Revenue | 74,732 | 73,537 | 77,887 | 4,350 | ||||||||||||

Expense | ||||||||||||||||

Operating expense | 58,143 | 60,124 | 61,292 | 1,168 | ||||||||||||

Capital grants | 2,103 | 3,469 | 3,523 | 54 | ||||||||||||

Amortization / inventory consumption / loss on disposals | 4,399 | 4,564 | 4,574 | 10 | ||||||||||||

Debt servicing costs | 3,149 | 3,389 | 3,173 | (216 | ) | |||||||||||

Pension provisions | (372 | ) | (364 | ) | (364 | ) | - | |||||||||

Disaster and emergency assistance | 3,025 | - | 847 | 847 | ||||||||||||

Expense before contingency | 70,447 | 71,182 | 73,045 | 1,863 | ||||||||||||

Contingency (forecast un-allocated) | - | 2,000 | 279 | (1,721 | ) | |||||||||||

Total Expense | 70,447 | 73,182 | 73,324 | 143 | ||||||||||||

Surplus / (Deficit) | 4,285 | 355 | 4,563 | 4,208 | ||||||||||||

Capital Plan | ||||||||||||||||

Capital grants | 2,103 | 3,469 | 3,523 | 54 | ||||||||||||

Capital investment | 4,197 | 4,830 | 4,742 | (88 | ) | |||||||||||

Total Capital Plan | 6,300 | 8,299 | 8,265 | (34 | ) | |||||||||||

| 2024-25 Second Quarter Fiscal Update and Economic Statement | 3 | |

Revenue Highlights

Total Revenue is forecast at $77.9 billion in 2024-25, $4.4 billion higher than Budget 2024, and $1.7 billion more than the first quarter forecast. This change is mainly due to higher resource and income tax revenue.

| • | Resource revenue is forecast to be $20.3 billion, an increase of $3 billion from Budget 2024, primarily driven by higher bitumen royalties. Compared to 2023-24, non-renewable resource revenue (NRR) is up $1.0 billion, largely due to the narrower light-heavy oil price differential. |

| • | The West Texas Intermediate oil price is forecast to average US$74 per barrel in 2024-25, aligning with the Budget 2024 estimate but down from first quarter, mainly due to persistent global economic weakness dampening crude oil demand expectations. The light-heavy differential is expected to average US$14/bbl for 2024-25, $2/bbl narrower than budgeted and $3/bbl narrower than the prior year. This is due to higher global demand for heavier crude grades overall and the Trans Mountain pipeline expansion project (TMX) coming online, providing additional egress capacity. |

| • | The US-Canadian dollar exchange rate is forecast to average 73.30 US¢/Cdn$ for the fiscal year, falling below the budget rate of 75.90 US¢/Cdn$. |

| • | Bitumen royalties are forecast at $15.6 billion, exceeding Budget 2024 projections by $3.1 billion. This increase is primarily due to a narrower light-heavy differential and a weaker Canadian dollar. |

| • | Natural gas and by-product royalties are expected to be approximately $1.2 billion, $288 million lower than Budget 2024. This decrease is due to lower natural gas prices driven by strong production, higher storage inventories, and weaker demand, partially offset by a lower exchange rate and higher butane and propane production. |

| • | Personal income tax revenue is forecast at $16.6 billion, up $948 million from budget, mainly due to stronger 2023 tax assessments and an upward revision of personal incomes for 2024, on the heels of strong population growth and employment gains. |

| • | Corporate income tax revenue is forecast at $7.3 billion, up $300 million from budget due to stronger-than-expected corporate profits. |

| • | Other tax revenue is forecast at $6 billion, a $26 million decrease from budget due to a decline in the tobacco tax revenue, and the policy change in car insurance premiums’ growth rates for good drivers, partially offset by higher revenues from fuel and cannabis taxes. |

| • | Federal transfers are forecast at $12.8 billion for 2024-25, $113 million higher than estimated in Budget 2024. Increases include $80 million for Federal Rare Disease Strategy, $58 million for the Jasper wildfire under the Disaster Financial Assistance Arrangements, $36 million for reprofiling Investing in Canada Infrastructure Program grants from 2023-24, and $10 million for gender based violence initiatives. A $71 million decrease in the labour market agreements following the elimination of the one-time top-up revenue to provinces and territories offset by other increases, mainly from reprofiled infrastructure projects. |

| • | Total revenue from other sources is forecast at $15 billion, $35 million higher than budget. |

| - | Investment income is forecast to increase $456 million from budget with Heritage Fund net income up $167 million and endowment funds up by $111 million due to higher than anticipated equity earnings. |

| - | Net income from government business enterprises is forecast at $2 billion, $82 million lower than budget, primarily due to Alberta Petroleum Marketing Commission’s operating loss. |

| - | Premiums, fees, and licences revenue of $5.5 billion is forecast for 2024-25, $70 million higher than budget, mainly due to higher Alberta Health Services’ revenue collected from increases in out-of-country and out-of-province patients. |

| - | Other revenue of $3.8 billion is down $409 million from budget. This is mainly due to a decrease in Technology Innovation and Emissions Reduction Fund (TIER) revenue related to lower-than-expected compliance payments accrued in 2023-24, and assumptions that facilities will minimize their costs by using credits up to the legislated limit to meet their compliance obligations. There is also a decrease in other sources, primarily for the Renewable Electricity Program (REP). The REP is a cost-for-differences initiative to provide economic stability that promoted renewable electricity projects, and the current electricity prices results in lower than budgeted revenues from this program. |

| 4 | 2024-25 Second Quarter Fiscal Update and Economic Statement | |

Revenue

(millions of dollars)

| Fiscal Year | Change

| |||||||||||||||

| 2023-24 | 2024-25 | from

| ||||||||||||||

| Actual | Budget | Forecast | Budget | |||||||||||||

Income Taxes | ||||||||||||||||

Personal income tax | 15,160 | 15,604 | 16,552 | 948 | ||||||||||||

Corporate income tax | 7,044 | 7,028 | 7,328 | 300 | ||||||||||||

| 22,204 | 22,632 | 23,880 | 1,248 | |||||||||||||

Other Taxes | ||||||||||||||||

Education property tax | 2,526 | 2,733 | 2,732 | (1 | ) | |||||||||||

Fuel tax / electric vehicle tax | 269 | 1,398 | 1,425 | 27 | ||||||||||||

Tobacco / vaping taxes | 439 | 473 | 439 | (34 | ) | |||||||||||

Insurance taxes | 858 | 918 | 896 | (22 | ) | |||||||||||

Cannabis tax | 210 | 196 | 210 | 14 | ||||||||||||

Tourism levy | 116 | 118 | 117 | (1 | ) | |||||||||||

Freehold mineral rights tax | 125 | 100 | 91 | (9 | ) | |||||||||||

Land titles registration levy | - | 77 | 78 | 1 | ||||||||||||

| 4,543 | 6,013 | 5,988 | (26 | ) | ||||||||||||

Non-Renewable Resource Revenue | ||||||||||||||||

Bitumen royalty | 14,518 | 12,538 | 15,628 | 3,090 | ||||||||||||

Crude oil royalty | 2,972 | 2,779 | 2,957 | 178 | ||||||||||||

Natural gas and by-products royalty | 1,058 | 1,468 | 1,180 | (288 | ) | |||||||||||

Bonuses and sales of Crown leases | 499 | 321 | 370 | 49 | ||||||||||||

Rentals and fees / coal royalty | 242 | 209 | 160 | (49 | ) | |||||||||||

| 19,287 | 17,315 | 20,295 | 2,980 | |||||||||||||

Transfers from Government of Canada | ||||||||||||||||

Canada Health Transfer | 5,964 | 6,164 | 6,156 | (8 | ) | |||||||||||

Canada Social Transfer | 1,908 | 2,001 | 1,993 | (8 | ) | |||||||||||

Direct transfers to SUCH sector / Alberta Innovates Corporation | 608 | 633 | 630 | (3 | ) | |||||||||||

Infrastructure support | 715 | 840 | 876 | 36 | ||||||||||||

Agriculture support programs | 615 | 537 | 541 | 4 | ||||||||||||

Labour market agreements | 322 | 317 | 253 | (64 | ) | |||||||||||

Early learning child care agreements | 881 | 1,139 | 1,139 | - | ||||||||||||

Other (includes Fiscal Stabilization payment in 2023-24) | 1,323 | 1,008 | 1,164 | 156 | ||||||||||||

| 12,336 | 12,640 | 12,753 | 113 | |||||||||||||

Investment Income | ||||||||||||||||

Alberta Heritage Savings Trust Fund | 2,065 | 1,042 | 1,209 | 167 | ||||||||||||

Endowment funds | 527 | 291 | 402 | 111 | ||||||||||||

Income from local authority loans | 802 | 758 | 731 | (27 | ) | |||||||||||

Agriculture Financial Services Corporation | 93 | 148 | 148 | - | ||||||||||||

Other (includes SUCH sector) | 1,095 | 1,027 | 1,233 | 206 | ||||||||||||

| 4,581 | 3,267 | 3,723 | 456 | |||||||||||||

Net Income from Government Business Enterprises | ||||||||||||||||

AGLC – Gaming / lottery | 1,569 | 1,487 | 1,493 | 6 | ||||||||||||

AGLC – Liquor | 791 | 808 | 791 | (17 | ) | |||||||||||

AGLC – Cannabis | 11 | 7 | 8 | 1 | ||||||||||||

ATB Financial | 337 | 266 | 254 | (12 | ) | |||||||||||

Balancing Pool | 160 | 65 | 72 | 7 | ||||||||||||

Other (CUDGCo / APMC / PSIs) | (1,630 | ) | (509 | ) | (577 | ) | (68 | ) | ||||||||

| 1,237 | 2,123 | 2,041 | (82 | ) | ||||||||||||

Premiums, Fees and Licences | ||||||||||||||||

Post-secondary institution tuition fees | 1,836 | 1,999 | 1,999 | - | ||||||||||||

Health / school board fees and charges | 818 | 845 | 911 | 66 | ||||||||||||

Motor vehicle licences | 969 | 594 | 598 | 4 | ||||||||||||

Crop, hail and livestock insurance premiums | 619 | 695 | 695 | - | ||||||||||||

Energy industry levies | 400 | 394 | 394 | - | ||||||||||||

Other | 924 | 856 | 856 | - | ||||||||||||

| 5,565 | 5,384 | 5,453 | 70 | |||||||||||||

Other | ||||||||||||||||

SUCH sector sales, rentals and services | 1,123 | 947 | 941 | (6 | ) | |||||||||||

SUCH sector fundraising, donations, gifts and contributions | 788 | 784 | 796 | 12 | ||||||||||||

AIMCo investment management charges | 860 | 936 | 1,012 | 76 | ||||||||||||

Fines and penalties | 174 | 203 | 203 | - | ||||||||||||

Refunds of expense | 431 | 138 | 146 | 8 | ||||||||||||

Technology Innovation and Emissions Reduction Fund | 907 | 539 | 140 | (399 | ) | |||||||||||

Miscellaneous | 696 | 618 | 518 | (100 | ) | |||||||||||

| 4,979 | 4,164 | 3,755 | (409 | ) | ||||||||||||

Total Revenue | 74,732 | 73,537 | 77,887 | 4,350 | ||||||||||||

| 2024-25 Second Quarter Fiscal Update and Economic Statement | 5 | |

Expense Highlights

Total Expense is forecast at $73.3 billion in 2024-25, close to the first quarter forecast, a $0.3 billion increase from 2023-24 and $0.1 billion from Budget 2024.

| • | Operating expense is forecast at $61.3 billion, a $1.2 billion increase from budget, mainly from: |

| - | $716 million increase in Health service activities. Population growth, the aging population requiring a higher level of care, and more fee-for-service billings resulted in additional pressure on physician services. An increase of $451 million will support the rise in the number of patients seen and their complex needs. The remaining $265 million increase is due to activity growth in Alberta Health Services including lab tests, urgent care visits, and expanding access to family health services. |

| - | $240 million increase in Seniors, Community and Social Services, mainly for additional program costs related to Income Support, due to population growth and higher unemployment levels, Assured Income for the Severely Handicapped, Disability Services, Ukrainian Emergency Evacuees Financial Support and Benefits, and Homeless initiatives. |

| - | $125 million increase in Education, primarily to address enrolment growth pressures as school authorities experience an increase in student numbers - more than 33,000 new students in the 2024/25 school year. |

| - | $91 million increase in Treasury Board and Finance, primarily for internal and external management fees. |

| - | $34 million increase in Energy and Minerals for the cost of selling oil, driven by the higher oil prices and volume of Crude Oil Royalty-in-Kind barrels marketed by the APMC. |

| - | A net $18 million increase in Advanced Education from higher post-secondary institutions’ expense funding from accumulated operating reserves, offset by reductions in Labour Market Transfer Agreement and Workforce Development Agreement expense. |

| - | $16 million increase in Mental Health and Addiction mostly due to unrealized savings from the core review and costs pressure, offset by reprioritizing one-time department grant reductions. |

| - | $30 million net increase in other ministries for various other initiatives. |

These increases are partially offset by decreases as follows:

| - | $80 million net decrease in Environment and Protected Areas mainly as a result of the decrease in TIER revenue, while still continuing to invest in strategic initiatives that reduce emissions. |

| - | $22 million net decrease in other ministries for various initiatives. |

| • | Capital Grants of $3.5 billion are forecast, up $54 million from budget, primarily from re-profiling 2023-24 projects, including Investing in Canada Infrastructure Program projects and other capital grant projects and programs, offset by slower-than-expected progress on municipal transit projects. |

| • | Debt servicing costs are forecast to decrease $216 million from budget, due mainly due to a reduction in required borrowing as a result of the improved surplus. |

| • | Disaster and emergency assistance of $847 million is forecast, primarily due to an active wildfire season. This includes: |

| - | $647 million for wildfire presuppression and response disaster and emergency assistance, and for the Wildfire Reclamation Program which includes reforesting areas that were burned in the 2023 wildfire season. |

| - | $163 million for Jasper Wildfire Disaster Recovery Program (DRP), Mackenzie County DRP extension, and Wood Buffalo and Peace and Grande Prairie DRPs. |

| - | $20 million for emergency evacuation payments and other disaster reliefsupport for Albertans displaced during recent wildfires. |

| - | $12 million for donation matching with the Canadian Red Cross. |

| - | $5 million in Jasper municipal support. |

| • | A Contingency of $2.0 billion was included in Budget 2024, as legislated through the in-year expense limitation under the legislated fiscal framework. Increases in expense not offset by dedicated revenue are included in the preliminary contingency allocation of $1.7 billion. The government continues to monitor the impact of the sudden and unexpected surge in population growth and other pressures on programs and services. The $0.3 billion remaining in contingency is available to address impacts as required. |

| 6 | 2024-25 Second Quarter Fiscal Update and Economic Statement | |

Fiscal Framework

In Budget 2023, the government introduced a new fiscal framework to guide decision-making and help manage the Alberta’s unique economic and revenue volatility.

The framework is contained in the Sustainable Fiscal Planning and Reporting Act, which requires the government to balance the budget. The government is forecasting a surplus of $4.6 billion in 2024-25.

The framework also limits in-year expense increases, adjusted to exclude expense that is directly offset by a related increase to revenue and non-cash, non-recurring adjustments, to the voted, budgeted contingency. In 2024-25, the contingency was set at $2 billion.

In 2024-25, expense is forecast to increase by $1.9 billion. Of this increase, $143 million is directly offset by revenue and is excluded from the in-year expense limit calculation. The remaining $1.7 billion is forecast to be allocated from the contingency, leaving $279 million unallocated.

Expense increases offset by dedicated revenue include allocations for Alberta Health Services expense funded by increased revenue for services provided to non-Alberta patients, capital grants partially funded by the federal government, costs related to selling oil offset by increased resource revenue, and other minor adjustments.

2024-25 Contingency

(millions of dollars)

| 2,000 | ||||||||

Expense increases: | ||||||||

Emergency / disaster assistance | 847 | |||||||

Other | 1,016 | |||||||

Total expense increases | 1,863 | |||||||

Less dedicated revenue / expense | (143) | |||||||

Preliminary contingency allocation | 1,721 | (1,721 | ) | |||||

Contingency - unallocated | 279 | |||||||

Debt Repayment and Alberta Fund Allocation

The framework also sets policies for the allocation of surplus cash available from fiscal results with the first 50 per cent used to repay debt maturing and the remaining 50 per cent allocated to the Alberta Fund.

Surplus cash available for allocation to debt repayment and the Alberta Fund is different from the second quarter forecast surplus of $4.6 billion.

Cash adjustments to the surplus / deficit, such as differences between accrued revenue and expense, SUCH sector and entity net income included in the bottom line but retained by various entities, and transfers not reported on the income statement are necessary to determine the cash balance available for allocation.

In 2024-25, the opening cash balance was $3.7 billion from the 2023-24 final results. Of this, $2 billion was allocated to the Heritage Fund.

After cash adjustments totaling $3.4 billion, there is $2.9 billion in surplus cash available for allocation to debt repayment or the Alberta Fund in 2024-25. Details of the various cash adjustments are included below.

| • | Retained income of funds and agencies. Funds and agencies are forecast to retain $2.2 billion of the reported surplus, as this cash belongs to the funds and agencies and not the General Revenue Fund (GRF). |

| - | This includes: $2.7 billion in income from Heritage Fund and endowment funds, ATB Financial, Agricutlure Financial Services Corporation, TIER, other government business enterprises, and entities. |

| - | The net loss of $590 million reported by APMC, in contrast, is the responsibility of APMC and GRF cash is not required. |

| • | Capital cash adjustments. A negative $2.4 billion cash adjustment mainly reflects non-SUCH capital investment cash requirements of $4.2 billion not reported in the surplus, less non-SUCH non-cash amortization expense of $1.4 billion that is included in expense and the surplus. |

| • | Other cash adjustments. $1.1 billion are forecast mainly in differences between accrued and cash revenue and expense and cash needed for student and other loans, and other changes in financial assets and liabilities. |

| - | The differences between energy royalties, PIT, and CIT revenue and cash received are among the most significant and volatile cash adjustments. |

| - | Cash received from energy royalties is forecast to track higher than projected revenues for the second quarter as forecasted oil prices trend lower for the rest of the fiscal year. |

This plan for using cash from the Alberta Fund and debt repayment is preliminary and will continue to be evaluated as the fiscal year unfolds.

Cash Available for Allocation / Debt Maturities

(billions of dollars)

Cash available for allocation: | ||||

From 2023-24 results | 3.7 | |||

Allocation to Heritage Fund | (2.0 | ) | ||

2024-25 surplus | 4.6 | |||

less entity retained income | (2.1 | ) | ||

less capital plan requirements | (2.4 | ) | ||

plus net other cash adjustments | 1.1 | |||

plus ATB Financial dividend | 0.1 | |||

Total cash available | 2.9 | |||

Allocation: | ||||

2024-25 taxpayer-supported debt | 1.44 | |||

Alberta Fund | 1.44 | |||

Total allocation | 2.9 | |||

Debt maturities | ||||

2024-25 maturities | 6.0 | |||

2025-26 maturities | 13.2 | |||

2026-27 maturities | 5.8 | |||

| 2024-25 Second Quarter Fiscal Update and Economic Statement | 7 | |

Risks to the forecast

The fiscal framework was developed to help manage Alberta’s unique economic and revenue volatility in both good times and bad. The government’s revenue is highly sensitive to global economic conditions and energy prices in particular, and these sensitivities continue to grow over time. Government revenues are as volatile today as they have ever been in Alberta. A US$1 per barrel (/bbl) change in the West Texas Intermediate (WTI) oil price has a $630 million impact to the government’s revenue. In recent months, oil prices have been volatile, with WTI fluctuating below US$70/bbl since September. Budget 2024 included balanced budgets in each of the next three years based on a WTI forecast of US$74/bbl.

Low scenario

While the fiscal situation has improved in 2024-25 since budget, uncertainty around global economic conditions, including a potential drop in oil prices present risks to the forecast for Budget 2025.

If oil prices remain under US$70/bbl, government revenue could drop by over $2.5 billion. Coupled with the pressure unprecedented population growth has put on government programs, services and infrastructure, compensation negotiations and delivering on important government commitments such as the implementation of a new personal income tax bracket, the government could be in a deficit position as early as 2025-26.

The unprecedented population growth Alberta has experienced will have an impact on programs and services for years to come. For example, in September 2024, the government announced the School Construction Accelerator Program to build new schools, modernize existing schools, expanding the modular classroom and create more charter school spaces to address growing enrolment pressures. The program will have impacts to the fiscal plan for at least the next seven years as the government works to add 200,000 new and modernized student spaces.

The fiscal framework includes allowable exceptions to balancing the budget. One exception that allows government to report a deficit is a significant drop in revenue from the previous year’s third quarter forecast. The framework also requires the government to return to balance within three years of reporting a deficit.

High scenario

Alberta’s fiscal framework is also designed to guide decision-making when the government experiences higher revenue. The framework limits year-over-year growth in operating expense to population growth plus inflation as well as limits in-year expense growth to a budgeted, voted contingency. In Budget 2024, the contingency was set at $2 billion. In addition to these spending limitations, available surplus cash at the end of the year must be used to improve the government’s net financial position or be allocated to the Alberta Fund.

The fiscal rules are in place to help avoid increasing spending to levels that may not be sustainable and could result in deficits in the future given Alberta’s revenue volatility.

Budget 2024 Sensitivities to Fiscal Year Assumptions, 2024-25a

(millions of dollars)

| Change | Net Impact | |||||

Oil price (WTI US$/bbl) | -$1 | -630 | ||||

Light-heavy oil price differential (US$/bbl) | +$1 | -600 | ||||

Natural gas price (Cdn$/GJ) | -10¢ | -10 | ||||

Exchange rate (US¢/Cdn$) | + 1¢ | -490 | ||||

Interest rates | +1% | -229 | ||||

Primary household income | -1% | -180 | ||||

| a | Sensitivities are based on current assumptions of prices and rates and show the effect for a full 12 month period. Sensitivities can vary significantly at different price and rate levels. The energy price sensitivities do not include the potential impact of price changes on the revenue from land lease sales. |

| 8 | 2024-25 Second Quarter Fiscal Update and Economic Statement | |

Assets and Liabilities

Financial assets of $94.1 billion are forecast for March 31, 2025, an increase of $7.2 billion from March 31, 2024.

| • | Assets of the Heritage, endowment and other funds, and the Alberta Enterprise Corporation (AEC) are forecast to grow $4.3 billion. The Heritage Fund 2024-25 net income is fully retained in the fund. The forecast also includes the $2 billion allocated from surplus cash in Budget 2024. The net assets of the endowment funds and the AEC have increased a net $0.4 billion, mainly due to increased income. |

| • | Financial assets from self-supporting lending activity and Agriculture Financial Services Corporation (AFSC) are increasing by $1.1 billion from 2023-24, as a result of the Alberta Crop Insurance Fund being replenished. |

| • | Commercial enterprise equity is a net of $232 million lower than at March 31, 2024. This change is mainly due to a forecast operating loss at APMC’s Sturgeon Refinery, partially offset by a positive net income from ATB Financial and other enterprises. |

| • | At March 31, 2025 $2.9 billion surplus cash is forecast to be available for allocation to debt repayment and the Alberta Fund. |

| • | In advance of the large upcoming debt maturities in 2025-26, additional borrowing is being undertaken to achieve efficiencies and the lowest cost possible in repaying the maturing bonds. The funds raised in advance are held in a designated debt retirement account. At March 31, 2025, the debt retirement account is forecast to hold $10 billion, an increase of $4.9 billion from the prior year. |

| • | Other financial assets are forecast to be $1.2 billion more than March 31, 2024. These include financial assets of school boards, universities and colleges, the health authority, student loans, accounts and interest receivables, natural gas royalty deposits, cash associated with future liabilities such as corporate income tax refunds, the cash reserve, and derivative financial instruments. |

Liabilities are forecast at $132.2 billion, $3.9 billion higher than at March 31, 2024.

Taxpayer-supported debt is estimated at $84 billion on March 31, 2025, $2.2 billion more than 2024.

| • | Liabilities for capital projects are up $10 million from March 31, 2024 and down $2.4 billion from budget as a result of the higher 2024-25 surplus. |

| • | Fiscal Plan debt is forecast at $36 billion, up $2.3 billion from the prior year as a result of the pre-funding plan. Additional borrowing of $1.8 billion is required for the pre-funding of debt maturities coming due in 2025-26. |

| • | Debt issued to finance loans to local authorities and for AFSC is increasing by $143 million from the prior year. |

| • | Government obligations for pension plan liabilities have decreased by $0.4 billion, mainly from improved valuations for the pre-1992 Teacher’s Pension. |

| • | Asset retirement obligations are $2.4 billion. The government’s adoption of the Asset Retirement Obligation standard requires recognition of future disposal costs of certain capital assets that need remediation or decommissioning work. |

| • | Other liabilities are $2 billion higher than the prior year. These include liabilities of the Schools, Universities, Colleges and Health sector, natural gas royalty and security deposits, unearned revenue, estimated corporate income tax refunds, trade payables, other liabilities of AFSC, coal phase-out liabilities, and derivative financial instruments. |

Net financial debt (financial assets less liabilities) as at March 31, 2025, is estimated at $38.1 billion, $3.3 billion less than on March 31, 2024, essentially reflecting the planned repayment of taxpayer-supported debt. The increase in borrowing in advance of large, upcoming debt maturities is offset by corresponding assets in the debt retirement account. Net debt to GDP is estimated at 8.2 per cent at March 31, 2025.

Capital and other non-financial assets, of $62.9 billion are forecast for March 31, 2025, a $1.3 billion net increase from March 31, 2024, mainly displaying the difference between capital asset acquisition (capital investment less a contingenc) and amortization expense. Deferred capital contribution liabilities remained largely unchanged at $4 billion.

Net assets - operating of $17.2 billion are forecast for March 31, 2025, an improvement of $4.6 billion from March 31, 2024 mainly as a result of the forecast surplus.

Net assets of $20.8 billion are forecast for March 31, 2025, consisting of net assets - operating and $3.6 billion in accumulated remeasurement gains and losses.

| 2024-25 Second Quarter Fiscal Update and Economic Statement | 9 | |

Summary Statement of Financial Position

(millions of dollars)

| At March 31 | Change

from

2024 | |||||||||||||||

| 2024 | 2025 | |||||||||||||||

| Actual | Budget | Forecast | ||||||||||||||

Financial Assets | ||||||||||||||||

Alberta Heritage Savings Trust Fund accumulated operating surplus | 20,872 | 23,779 | 24,856 | 3,984 | ||||||||||||

Endowment fund accumulated operating surpluses: | ||||||||||||||||

Alberta Heritage Foundation for Medical Research | 2,202 | 2,321 | 2,362 | 160 | ||||||||||||

Alberta Heritage Science and Engineering Research | 1,288 | 1,350 | 1,385 | 97 | ||||||||||||

Alberta Heritage Scholarship | 1,459 | 1,531 | 1,566 | 107 | ||||||||||||

Alberta Enterprise Corporation | 337 | 333 | 333 | (4 | ) | |||||||||||

General Revenue Fund - surplus cash | 1,984 | - | - | (1,984 | ) | |||||||||||

General Revenue Fund - debt retirement | 5,035 | 10,702 | 9,982 | 4,947 | ||||||||||||

Alberta Fund | 3,667 | - | 1,435 | (2,232 | ) | |||||||||||

Self-supporting lending activity: | ||||||||||||||||

Loans to local authorities (including SUCH sector) | 14,590 | 14,579 | 14,671 | 81 | ||||||||||||

Agriculture Financial Services Corporation | 2,966 | 4,017 | 4,017 | 1,051 | ||||||||||||

Equity in commercial enterprises: ATB / AGLC / APMC / CUDGCo / Bal. Pool / PSIs | 862 | 584 | 630 | (232 | ) | |||||||||||

Student loans | 4,640 | 5,246 | 5,246 | 606 | ||||||||||||

Technology Innovation and Emissions Reduction Fund | 1,017 | 1,033 | 919 | (98 | ) | |||||||||||

Other financial assets (including SUCH sector / Alberta Innovates Corp.) | 25,970 | 26,738 | 26,732 | 762 | ||||||||||||

Total Financial Assets | 86,889 | 92,213 | 94,134 | 7,245 | ||||||||||||

Liabilities | ||||||||||||||||

Taxpayer-supported debt: | ||||||||||||||||

Direct borrowing for the Capital Plan | 44,957 | 47,360 | 44,967 | 10 | ||||||||||||

Alternative financing (P3s - public-private partnerships - Capital Plan) | 2,637 | 2,540 | 2,539 | (98 | ) | |||||||||||

Debt issued to reduce pre-1992 Teachers’ Pension Plan unfunded liability | 478 | 478 | 478 | - | ||||||||||||

Direct borrowing for the Fiscal Plan | 33,763 | 37,452 | 36,013 | 2,250 | ||||||||||||

Total taxpayer-supported debt | 81,835 | 87,830 | 83,997 | 2,162 | ||||||||||||

Self-supporting lending organization / activity debt: | ||||||||||||||||

Debt for local authority loans | 14,590 | 14,579 | 14,671 | 81 | ||||||||||||

Agriculture Financial Services Corporation | 3,125 | 3,187 | 3,187 | 62 | ||||||||||||

Total taxpayer and self-supported debt | 99,550 | 105,596 | 101,855 | 2,305 | ||||||||||||

Coal phase-out liabilities | 609 | 530 | 530 | (79 | ) | |||||||||||

Pension liabilities | 7,904 | 7,540 | 7,540 | (364 | ) | |||||||||||

Asset retirement obligations | 2,391 | 2,402 | 2,402 | 11 | ||||||||||||

Other liabilities (including SUCH sector / Alberta Innovates Corp.) | 17,799 | 18,242 | 19,868 | 2,069 | ||||||||||||

Total Liabilities | 128,253 | 134,310 | 132,195 | 3,943 | ||||||||||||

Net Financial Assets / (Debt) | (41,364 | ) | (42,097 | ) | (38,061 | ) | 3,302 | |||||||||

Capital / Other Non-financial Assets | 61,515 | 62,617 | 62,842 | 1,328 | ||||||||||||

Spent deferred capital contributions | (3,964 | ) | (3,982 | ) | (4,031 | ) | (67 | ) | ||||||||

Net Assets | 16,187 | 16,538 | 20,750 | 4,564 | ||||||||||||

Net assets / (liabilities) - statement of operations | 12,649 | 13,000 | 17,212 | 4,563 | ||||||||||||

Accumulated remeasurement gains | 3,538 | 3,538 | 3,538 | - | ||||||||||||

Change in Net Assets - statement of operations (before adjustments) | 4,149 | 351 | 4,563 | 414 | ||||||||||||

Net financial debt / GDP (calendar year, nominal) | -9.4% | -9.2% | -8.2% | |||||||||||||

| 10 | 2024-25 Second Quarter Fiscal Update and Economic Statement | |

Capital Plan Highlights

The 2024-25 Capital Plan is forecast at $8.3 billion, down $34 million from Budget 2024. This reflects a decrease of $88 million in capital investment, offset by an increase of $54 million in capital grants. Compared to the first quarter forecast, the plan has decreased by $246 million, primarily due to the re-profiling of capital investments to future years.

The net $88 million decrease in capital investment includes a $107 million net decrease resulting from the re-profiling of cash flows to future years primarily for Health and Mental Health and Addictions projects. This adjustment aligns funding with project progress. Additionally, $50 million in savings are anticipated as various government facilities, school facilities,

and health infrastructure projects are expected to be completed under budget as they approach completion. Finally, these decreases are partially offset by $69 million in new funding, which consists of $50 million in fiscal 2024-25 for the construction of 250 modular housing units to support Jasper residents displaced by this summer’s wildfire, as part of the $112 million total commitment for interim housing, and $19 million for compassionate intervention facilities planning.

The Alberta government has launched the School Construction Accelerator Program to expedite the construction of new and modernized schools and increase student capacity across the province. Further updates will be provided in Budget 2025.

The $54 million increase in capital grants primarily relates to re-profiling of unspent funds from the prior year for affordable housing projects, federally-funded infrastructure projects, and recovery community projects managed by third parties.

The Capital Plan is financed from a variety of sources, including the federal contributions; donations; funding from school boards, post-secondary institutions, the health authority, and other funds and agencies; public-private partnerships; as well as general revenue fund or borrowed cash. More details can be found in the table on page 25.

Capital Plan Summary by Ministrya

(millions of dollars)

| Fiscal Year | Change

from

Budget | |||||||||||||||

| 2023-24 | 2024-25 | |||||||||||||||

| Actual | Budget | Forecast | ||||||||||||||

Advanced Education | 575 | 437 | 444 | 7 | ||||||||||||

Affordability and Utilities | 8 | 7 | 7 | - | ||||||||||||

Agriculture and Irrigation | 31 | 97 | 109 | 12 | ||||||||||||

Arts, Culture and Status of Women | 124 | 98 | 102 | 4 | ||||||||||||

Children and Family Services | 7 | 3 | 4 | 1 | ||||||||||||

Education | 773 | 946 | 925 | (21 | ) | |||||||||||

Energy and Minerals | 144 | 228 | 236 | 8 | ||||||||||||

Environment and Protected Areas | 104 | 107 | 113 | 6 | ||||||||||||

Forestry and Parks | 75 | 140 | 151 | 11 | ||||||||||||

Health | 735 | 1,443 | 1,273 | (170 | ) | |||||||||||

Indigenous Relations | 11 | 10 | 18 | 8 | ||||||||||||

Infrastructure | 351 | 385 | 323 | (62 | ) | |||||||||||

Jobs, Economy and Trade | 14 | 25 | 26 | 1 | ||||||||||||

Justice | 23 | 14 | 14 | - | ||||||||||||

Mental Health and Addiction | 26 | 140 | 162 | 22 | ||||||||||||

Municipal Affairs | 765 | 1,050 | 1,067 | 17 | ||||||||||||

Public Safety and Emergency Services | 7 | 12 | 17 | 5 | ||||||||||||

Seniors, Community and Social Services | 136 | 202 | 281 | 79 | ||||||||||||

Service Alberta and Red Tape Reduction | 34 | 64 | 64 | - | ||||||||||||

Technology and Innovation | 128 | 233 | 263 | 30 | ||||||||||||

Tourism and Sport | - | 10 | 10 | - | ||||||||||||

Transportation and Economic Corridors | 2,211 | 2,629 | 2,637 | 8 | ||||||||||||

Treasury Board and Finance | 18 | 18 | 17 | (1 | ) | |||||||||||

Legislative Assembly | 1 | 2 | 2 | - | ||||||||||||

Total Capital Plan | 6,300 | 8,299 | 8,265 | (34 | ) | |||||||||||

| a | The Capital Plan comprises capital grants included in expense plus capital investment in government-owned assets not included in expense. Capital investment adds to government capital assets, and those assets are depreciated over time through amortization expense included in total expense. |

| 2024-25 Second Quarter Fiscal Update and Economic Statement | 11 | |

Fiscal Update and

Economic Statement

2024-25 Second Quarter

| 12 | 2024-25 Second Quarter Fiscal Update and Economic Statement | |

Economic Update

Overview

Alberta’s economic outlook remains solid, although risks are rising. The energy sector continues to drive growth in business activity and output on the back of increased pipeline capacity. Alberta’s exceptionally strong population growth is also boosting residential construction activity, while easing price pressures and falling interest rates are providing some relief to households. However, demand concerns are weighing on global oil prices. Rising protectionism and geopolitical tensions heighten risks to the global economy.

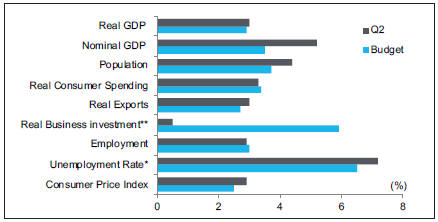

After moderating to 2.3 per cent in 2023, growth in Alberta’s real gross domestic product (GDP) is expected to accelerate to 3.0 per cent this year. This is 0.3 percentage points (ppts) lower than the first quarter but still slightly higher than budget (Chart 1). The downward revision from the first quarter reflects weaker-than-expected business investment in industries outside the oil & gas sector and more cautious consumer spending. Despite solid headline growth, real GDP per capita is forecast to decline this year before improving in 2025.

Alberta’s labour market continues to struggle with the rapid increase in the population. While employment is expected to grow at a solid pace of 2.9 per cent this year, it will trail behind the expansion in the labour force. As a result, the unemployment rate is forecast to average 7.2 per cent this year, higher than first quarter and budget expectations.

Next year, real GDP growth is forecast to moderate but remain solid at 2.7 per cent. Population growth is set to slow to 2.5 per cent in the 2025 census year, reflecting the impact of the federal government’s targets on immigration and non-permanent residents (Chart 2). While lower population growth will be drag on consumer spending, it should provide some relief to Alberta’s tight housing market and help dampen shelter inflation. However, the labour market will take some time to adjust to the slower population growth. With job growth slowing to 2.1 per cent next year, the unemployment rate is expected to rise to 7.4 per cent.

Global growth holding up but risks rising

The outlook for the global economy remains constructive, underpinned by moderating inflation and falling interest rates, but risks are on the rise. The International Monetary Fund (IMF) still anticipates global growth at 3.2 per cent in 2024 and 2025, unchanged from April. The U.S. economy is expected to outperform developed countries, with the IMF increasing its real GDP growth forecast to 2.8 and 2.2 per cent for 2024 and 2025, respectively. Growth in the Euro Area is expected to pick up to around 1.2 per cent over the forecast horizon but remains soft, weighed down by weakness in manufacturing activity. However, the

ongoing slump in the property sector and weakness in consumer spending are anticipated to keep China’s growth subdued below 5 per cent. In the U.S., there are concerns that rising fiscal deficits, higher tariffs and restrictive immigration policies could stoke inflationary pressures and weigh on broader global economic activity.

Uncertainties related to more protectionist trade policies and escalating geopolitical tensions are increasing and pose significant risks to the outlook.

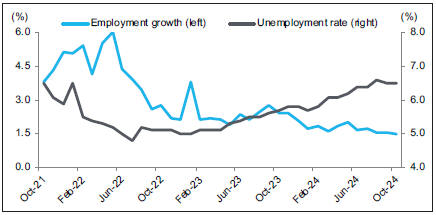

Canadian economy losing momentum

The Canadian economy is shifting into a lower gear. While real GDP growth held

Chart 1: Alberta’s economic expansion on track

Year-over-year growth in key economic indicators, 2024

| Source: | Alberta Treasury Board and Finance; *Unemployment rate is forecasted level, |

**Investment in Plant & Equipment. |

Chart 2: Alberta’s population will grow next year, but at a slower pace

Annual change in population by census year, historical and forecast

| Sources: | Statistics Canada, Haver Analytics and Alberta Treasury Board and Finance |

| 2024–25 Second Quarter Fiscal Update and Economic Statement | 13 | |

up better than expected in the first half of the year, recent indicators point to slower momentum for the rest of 2024. Job gains have also softened, with year-over-year (y/y) employment growth declining to 1.5 per cent in October – the slowest rate post-COVID (Chart 3). Canadian real GDP growth is now expected to decelerate to 1.1 per cent this year before rising to 1.7 per cent in 2025. The federal government is projecting that the 2025-2027 Immigration Levels Plan targets will result in a population decline of 0.2 per cent in 2025 and 2026 calendar years. This poses downside risks to Canada’s real GDP growth next year.

With inflation back to the two per cent target and economic activity softening, the Bank of Canada (BoC) has accelerated the pace of interest rate cuts. The BoC lowered its policy rate by an outsized 0.5 percentage points in October – the

fourth consecutive reduction since June – which brings the policy rate to 3.75 per cent. Diverging interest rates between Canada and the U.S., along with slower Canadian economic growth relative to the U.S., has weighed on the Loonie. It is now forecast to average US¢73.30/Cdn$ in 2024-25, lower than expected in the first quarter and budget.

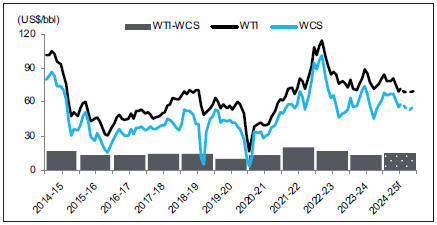

Oil price volatility continues

Oil prices have fluctuated considerably since the first quarter update. Despite a tight supply-demand balance, the West Texas Intermediate (WTI) oil price has oscillated below US$70 per barrel (/bbl) since September on concerns over Chinese demand and increased risks to the global economy (Chart 4). A recent decision by OPEC+ to delay plans to increase output has helped to allay fears

Chart 3: Canada’s labour market is softening

Year-over-year growth in Canadian employment and the unemployment rate*

| Sources: | Statistics Canada and Haver Analytics; *seasonally adjusted |

Chart 4: Demand concerns to weigh on near-term outlook for WTI

Oil prices

| Sources: | Alberta Energy and Alberta Treasury Board and Finance; f-forecast |

of oversupply. However, geopolitical risks, including the potential escalation of the conflict in the Middle East that could reduce supply in the near term, are adding to the volatility in prices. WTI is now forecast to average US$74.00/bbl in 2024-25, same as budget but US$2.50/ bbl lower than the first quarter.

Additional egress capacity from the Trans Mountain Pipeline Expansion (TMX) is helping to strengthen and stabilize Alberta’s heavy oil prices, particularly during periods when the differential typically widens. Higher demand for heavier crude grades has also contributed to a narrower light-heavy differential so far this year. The light-heavy differential is expected to average US$14.00/bbl 2024-25, US$0.40 and US$2.00 narrower than the first quarter and budget forecasts, respectively. This, along with a weaker Canadian dollar, has helped to offset the impact of lower WTI prices. As a result, Western Canadian Select (WCS) price is expected to be higher. It is forecast to average Cdn$81.80/bbl in 2024-25, Cdn$5.00 higher than budget.

Natural gas prices subdued

Natural gas prices in Western Canada remain under pressure. AECO, the Western Canadian natural gas price benchmark, has held mostly below Cdn$1 per gigajoule (/GJ) since the spring. Robust production, coupled with weaker demand, has led to a build-up in storage inventories. The Alberta Reference Price (ARP) is now forecast to average Cdn$1.20/GJ in 2024-25, down from Cdn$1.80/GJ in the first quarter and $2.90/GJ in budget. Looking ahead, the completion of LNG Canada’s Phase 1 in 2025 is anticipated to improve market access for Western Canadian natural gas, providing an outlet for production in the region and potentially supporting price stability over the long term. This expanded export capacity will enable Western Canadian producers to access new international markets, particularly in Asia, where demand for LNG is expected to remain strong.

Oil a key driver of output and investment

Despite the recent volatility in oil prices, Alberta’s energy sector continues to drive growth in business activity and output. Rigs drilling held up throughout the spring break period and advanced 8.9 per cent y/y in October to a five-year seasonal high. Although oil

| 14 | 2024–25 Second Quarter Fiscal Update and Economic Statement | |

production dipped temporarily due in part to maintenance activities, it has risen 4.5 per cent year-to-date (YTD). The completion of TMX in early May has boosted Alberta’s takeaway capacity and improved access to the U.S. West Coast and Asian markets for Alberta’s crude. Strong production levels and inventory drawdowns are expected to lift oil export volumes by 5.0 per cent this year, exceeding the first quarter and budget forecasts of 4.5 and 3.0 per cent, respectively. Growth is projected to ease to 2.7 per cent next year, in line with a more moderate increase in Alberta’s oil production, which is forecast to surpass 4.0 million barrels per day (bpd) in 2025.

Natural gas, however, remains a weak spot. Some producers have deferred activity or shut in production in response to low prices, which is weighing on natural gas output. Next year, natural gas production is expected to bounce back as prices partially recover.

Investment in the oil and gas extraction sector is forecast to rise 9.2 per cent in 2024 and 6.4 per cent in 2025, on the back of expanded pipeline capacity. Growing bitumen production is expected to lift sustaining capital in the non-conventional sector, while strategic spending remains focused on small-scale expansions and optimization projects.

Non-energy output slow to pick up

Weakness in agriculture and manufacturing products continues to weigh on business output. The value of non-energy goods exports has pulled back sharply from its recent high and

is down 3.1 per cent YTD through September. While the decline so far this year has been largely driven by farm, fishing & intermediate food products, other categories such as chemicals and industrial machinery & equipment have also contributed to the weakness. Similarly, manufacturing sales have fallen to its lowest level since August 2023 and are down 2.3 per cent YTD, reflecting declines in both durable and non-durable goods. These have been partly offset by higher shipments of food manufacturing and wood products, which continue to benefit from Alberta’s rapid population growth and booming residential construction activity.

Given the YTD weakness, growth in overall real manufacturing exports has been revised down to 0.5 per cent this year before rebounding to 2.4 per cent next year. Meanwhile, growth in services exports is expected to remain solid in 2024 and 2025 on the back of expanded pipeline capacity and strong demand for Alberta’s crude oil.

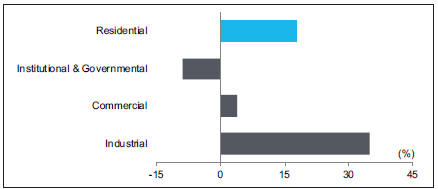

Industrial sector propping up investment

Non-residential investment in Alberta’s private sector is being driven by strong activity in industrial building construction. Spending on industrial building has ramped up to its highest level since 2016 and is up 35 per cent YTD (Chart 5). While some of this momentum reflects higher prices, activity is also underway or ramping up in a number of major projects, such as the DOW Path2Zero project.

Chart 5: Industrial sector leads growth in investment

Year-to-date growth in building construction investment

Sources: Statistics Canada and Haver Analytics

In contrast, other categories have been slow to gain momentum this year. Some major projects have either delayed or pushed back construction timelines. While business investment in machinery and equipment bounced back in the second quarter, it remains only 0.2 per cent higher YTD. Engineering construction spending has also eased from last year’s high levels, due in part to many large-scale pipeline and power projects wrapping up. Commercial building investment continues to decline, as ongoing weakness in retail buildings and warehouses outweighing a pickup in office investment.

With the other categories lagging, investment outside oil and gas extraction has been revised downward and is expected to remain flat this year before rebounding by 8.8 per cent in 2025. The stronger growth next year partly reflects the impact of falling interest rates, as well as certain projects delaying construction. Investment will also get an additional boost from $3.4 billion worth of new projects that have been announced since the first quarter update, with most of the investment occurring in 2025.

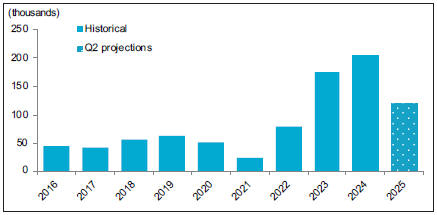

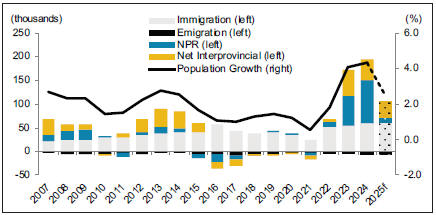

Population growth decelerating

Following two years of exceptional population gains, Alberta is expected to see population growth slow significantly in 2025. The federal government’s immigration plan targets large net outflows of non-permanent residents (NPRs) and slower immigration. While Alberta is expected to be less impacted than other regions of the country, it will not be immune to this policy. The province’s population is forecast to grow at 2.5 per cent in the 2025 census year, much slower than the 4.4 per cent in 2024. However, uncertainty remains regarding the implementation of the policy.

Although moderating from the exceptional highs of the last few years, population growth will continue to be supported by natural increase and migration. Net international migration in 2025 is expected to be about half of the preceding year, a result of the lower federal targets. Similarly, NPRs are expected to pull back. Alberta is forecast to see a slight net positive gain of NPRs in the 2025 census year (Chart 6) and outflows starting in 2026. Net interprovincial migration is forecast to soften from last year’s record level but

| 2024–25 Second Quarter Fiscal Update and Economic Statement | 15 | |

remain historically strong due to Alberta’s continued affordability advantage. Overall, the province is forecast to add nearly 120,000 new residents in the 2025 census year.

Employment gains slowing

Momentum in Alberta’s labour market is shifting down after strong gains earlier in the year. The province has added more than 40,000 jobs since December 2023, but y/y growth eased to 2.4 per cent in the third quarter. This is the slowest pace post-COVID. The deceleration was widespread, with annual gains slowing in both the goods and service sectors and predominantly in full-time positions. Employment in retail & wholesale trade and professional, scientific & technical services fell y/y, while hiring in some industries was tepid. At the same time, the job finding rate has slowed and job vacancies continue to decline, although they are still above pre-COVID levels. Employment is now forecast to rise 2.9 per cent this year, slightly lower than the first quarter and budget forecast of 3.0 per cent. Despite the slowdown, employment remains solid, outpacing the national average.

The province is expected to continue adding jobs next year, although at a much slower pace. Weaker gains in the fourth quarter, coupled with downward revisions to consumer spending and non-residential business investment in 2025, suggest that employment growth will decelerate further next year. Employment is forecast to rise 2.1 per cent in 2025, down 1.0 percentage point from the first quarter and budget.

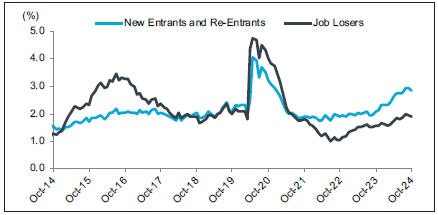

Unemployment to stay high

Cooling labour demand and the surging population over the last few years is keeping unemployment elevated in the province. The increase in unemployment over the past year has been particularly notable among youth and less-experienced workers, although all cohorts have experienced higher unemployment rates. The rise, however, has not been driven by layoffs, but rather by more people entering the labour force who are unable to find work (Chart 7). While the unemployment rate dipped for the second consecutive month to 7.3 per cent in October, it remains high. It is now projected to average 7.2 per cent this year, up 0.2 and 0.7 percentage points from the first quarter and budget forecast, respectively.

Even with the slower population growth next year, the unemployment rate in the province is expected to rise further as the labour market takes some time to adjust. It is forecast to average 7.4 per cent in 2025, higher than the first quarter and budget. Job gains are expected to lag behind, but a decline in the labour force participation rate will take some pressure off the unemployment rate.

The high unemployment in the province is masking some of the imbalances in the labour market. Despite elevated unemployment, wages in the province continue to post strong gains. So far this year, average hourly wages are up 4.2 per cent, driven by the oil & gas, construction, professional & scientific services, and the finance/real estate sector. As investment ramps up in the province, demand for skilled workers is expected to keep wage growth strong next year.

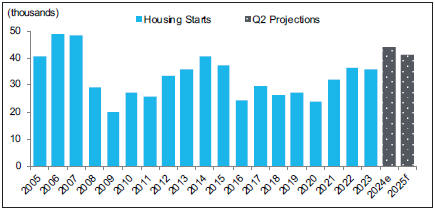

Residential construction holding strong

Activity in Alberta’s residential construction sector remains robust. Although housing starts have eased from their recent peak, they remain elevated and averaged nearly 49,000 units in the third quarter of 2024, the highest quarterly level since 2007. The increase has been supported by a ramp-up in hiring, with payroll employment in the residential building construction sector up more than 8.5 per cent through August. Given the YTD strength, housing starts in the province are now expected to average 44,000 units this year, exceeding the first quarter and budget expectations. This is expected to boost real residential construction investment, which is forecast to rise 12 per cent in 2024.

Chart 6: Sharp pullback in NPRs a drag on population growth in 2025

Annual change in the Alberta population by migration component by census year

Sources: Statistics Canada, Haver Analytics and Alberta Treasury Board and Finance; e-estimate,

f-forecast

Chart 7: Unemployment rate rising with new entrants

Contribution to Alberta’s unemployment rate

Sources: Statistics Canada and Alberta Treasury Board and Finance calculations

| 16 | 2024–25 Second Quarter Fiscal Update and Economic Statement | |

Resale activity is cooling down from last year’s blistering pace but remains strong. This reflects the supply of new homes coming online and a rotation in sales from Calgary to Edmonton. Home sales in Calgary are down slightly YTD, with higher house prices and limited inventory of lower priced homes constraining activity. In contrast, better affordability has fueled double-digit sales growth in Edmonton so far this year. With the strong gains in Edmonton and moderation in Calgary, the sales-to-new-listings ratio in Edmonton surpassed that of Calgary for the first time since March 2022, signaling tighter housing market conditions.

Next year, housing starts are forecast to continue at a robust pace of about 41,000 units as supply continues to catch up with the increase in demand from Alberta’s population boom over the past few years (Chart 8). Falling interest rates are also expected to encourage homebuyers to move off the sidelines, supporting both resale and construction activity. This, combined with strong momentum in residential construction during the latter half of this year, should lift real investment to grow 4.8 per cent in 2025. Additionally, renovation spending is projected to rebound next year, fueled by lower interest rates and improving sentiment.

Broader price pressures easing

Alberta’s consumer inflation continues to drift lower as price pressures moderate across many categories. With prices declining in the last two months, inflation fell below two per cent y/y in September, the slowest pace since June 2023. Energy prices plunged in the month and were down almost 11 per cent from a year ago, led by a sharp decline in gasoline prices which was partly driven by weaker oil prices. Electricity prices have also come down from last year’s heightened levels. Sluggish demand is weighing on prices for durables and semi-durables, which are both lower compared to a year ago. Meanwhile, food inflation has slowed in recent months but continues to outpace headline inflation.

Inflation is now expected to average 2.9 per cent in 2024, down slightly from the first quarter update but 0.4 percentage points higher than budget. Shelter cost remain the biggest driver of inflationary pressure this year, fueled by strong growth in rent and home ownership cost. Both

Chart 8: Housing starts to hold above 40,000 units next year

Alberta housing starts

Sources: Canada Mortgage and Housing Corporation, Haver Analytics and Alberta Treasury Board and

Finance; f-forecast

were up 12 per cent and 7.0 per cent y/y in September, respectively, although they have eased from their recent peaks. Shelter inflation is expected to moderate further next year as more housing supply comes into the market and lower interest rates weigh on mortgage interest cost. This, combined with lower oil prices, should dampen inflation to 2.0 per cent in 2025.

Some relief for consumers

While households continue to hold back on spending, moderating inflation and interest rate cuts are starting to provide some much-needed relief. Growth in consumer insolvencies is easing compared to the elevated pace seen earlier this year, while mortgage arrears in Alberta are down 10 per cent y/y compared with a 28 per cent increase in Canada.

There are early signs that improving confidence and past interest rate cuts are having an impact on spending. Retail sales at motor vehicles and gasoline stations still remain down, partly reflecting lower prices, but core retail sales (which exclude motor vehicles and gasoline station) appear to have bottomed out in June. They are up 2.4 per cent YTD and overall retail sales have been up on a y/y basis in four of the last five months.

Real consumer spending is now forecast to rise 3.3 per cent in 2024, down slightly from the first quarter and budget. A deceleration in population and household income growth in 2025 is expected to weigh on growth in real consumer spending, which is forecast to slow to 2.6 per cent.

The impact of interest rate cuts will take time to permeate through the economy. On a per capita basis, real consumer spending is expected to decline this year before improving in 2025. As interest rates decline further further and sentiment improves, households are expected to feel the benefits more noticeably in the latter half of next year.

| 2024–25 Second Quarter Fiscal Update and Economic Statement | 17 | |

Key Energy and Economic Assumptions

| 2024-25 | 2024-25 Fiscal Year | |||||||||||||||||||

Fiscal Year Assumptions | 2023-24 Actual | 6 Months Actual | Budget | 2nd Quarter | ||||||||||||||||

Prices | ||||||||||||||||||||

Crude Oil Price | ||||||||||||||||||||

WTI (US$/bbl) | 77.83 | 78.00 | 74.00 | 74.00 | ||||||||||||||||

Light-Heavy Differential (US$/bbl) | 17.29 | 13.50 | 16.00 | 14.00 | ||||||||||||||||

WCS @ Hardisty (Cdn$/bbl) | 81.67 | 87.90 | 76.80 | 81.80 | ||||||||||||||||

Natural Gas Price | ||||||||||||||||||||

Alberta Reference Price (Cdn$/GJ) | 2.07 | 0.77 | 2.90 | 1.20 | ||||||||||||||||

Production | ||||||||||||||||||||

Conventional Crude Oil (000s barrels/day) | 511 | 521 | 507 | 519 | ||||||||||||||||

Raw Bitumen (000s barrels/day) | 3,332 | 3,326 | 3,429 | 3,451 | ||||||||||||||||

Natural Gas (billions of cubic feet) | 4,267 | 2,120 | 4,291 | 4,308 | ||||||||||||||||

Interest rates | ||||||||||||||||||||

3-month Canada Treasury Bills (per cent) | 4.88 | 4.60 | 4.10 | 4.00 | ||||||||||||||||

10-year Canada Bonds (per cent) | 3.46 | 3.40 | 3.70 | 3.30 | ||||||||||||||||

Exchange Rate (US¢/Cdn$) | 74.2 | 73.2 | 75.9 | 73.3 | ||||||||||||||||

| 2023 Calendar Year | 2024 Calendar Year | 2025 Calendar Year | ||||||||||||||||||||||

Calendar Year Assumptionsa | Budget | Actual | Budget | 2nd Quarter | Budget | 2nd Quarter | ||||||||||||||||||

Gross Domestic Product | ||||||||||||||||||||||||

Nominal (millions of dollars) | 440,632 | 452,410 | 456,081 | 464,927 | 483,902 | 487,617 | ||||||||||||||||||

per cent change | -4.1 | -4.3 | 3.5 | 5.2 | 6.1 | 4.9 | ||||||||||||||||||

Real (millions of 2017 dollars) | 351,903 | 356,761 | 362,093 | 362,706 | 374,055 | 372,505 | ||||||||||||||||||

per cent change | 2.5 | 2.3 | 2.9 | 3 | 3.3 | 2.7 | ||||||||||||||||||

Other Indicators | ||||||||||||||||||||||||

Employment (thousands) | 2,461 | 2,461 | 2,535 | 2,534 | 2,614 | 2,588 | ||||||||||||||||||

per cent change | 3.6 | 3.6 | 3.0 | 2.9 | 3.1 | 2.1 | ||||||||||||||||||

Unemployment Rate (per cent) | 5.9 | 5.9 | 6.5 | 7.2 | 6.0 | 7.4 | ||||||||||||||||||

Average Weekly Earnings | 2.4 | 2.1 | 3.8 | 3.3 | 3.6 | 3.4 | ||||||||||||||||||

(per cent change) | ||||||||||||||||||||||||

Primary Household Income | 7.7 | 5.7 | 6.7 | 7.1 | 5.6 | 5.5 | ||||||||||||||||||

(per cent change) | ||||||||||||||||||||||||

Net Corporate Operating Surplus | -14.5 | -26.9 | 0.0 | 3.5 | 4.9 | 4.4 | ||||||||||||||||||

(per cent change) | ||||||||||||||||||||||||

Housing Starts (thousands of units) | 36.0 | 36.0 | 38.8 | 44.0 | 39.9 | 41.0 | ||||||||||||||||||

Alberta Consumer Price Index | 3.3 | 3.3 | 2.5 | 2.9 | 2.2 | 2.0 | ||||||||||||||||||

(per cent change) | ||||||||||||||||||||||||

Population (July 1st, thousands) | 4,695 | 4,685 | 4,870 | 4,889 | b | 4,982 | 5,009 | |||||||||||||||||

per cent change | 4.1 | 3.9 | 3.7 | 4.4 | 2.3 | 2.5 | ||||||||||||||||||

| a | Forecast was finalized on November 5, 2024 prior to the release of the 2023 Provincial Economic Accounts. |

| b | Estimate |

| 18 | 2024–25 Second Quarter Fiscal Update and Economic Statement | |

2024-25 Second Quarter

Fiscal Update Tables

| 2024–25 Second Quarter Fiscal Update and Economic Statement | 19 | |

Table of Contents

Tables

Consolidated Fiscal Summary | 21 | |||

Operating Expense by Ministry | 22 | |||

Disaster and Emergency Assistance Expense | 22 | |||

Capital Amortization Expense | 23 | |||

Inventory Consumption Expense | 23 | |||

Inventory Acquisition | 23 | |||

Debt Servicing Costs | 24 | |||

Capital Grants | 24 | |||

Capital Investment | 25 | |||

Capital Plan Funding Sources | 25 | |||

Cash Adjustments / GRF Cash and Allocation | 26 | |||

| 20 | 2024-25 Second Quarter Fiscal Update and Economic Statement | |

Consolidated Fiscal Summary

(millions of dollars)

| Fiscal Year | Change

from

Budget | |||||||||||||||||

| 2023-24 | 2024-25 | |||||||||||||||||

| Actual | Budget | Forecast | ||||||||||||||||

| 1 | Total Revenue | 74,732 | 73,537 | 77,887 | 4,350 | |||||||||||||

Expense | ||||||||||||||||||

| 2 | Operating expense | 58,143 | 60,124 | 61,292 | 1,168 | |||||||||||||

| 3 | % change from prior year | 6.2 | 3.4 | 5.4 | - | |||||||||||||

| 4 | Capital grants | 2,103 | 3,469 | 3,523 | 54 | |||||||||||||

| 5 | Amortization / inventory consumption / loss on disposals | 4,399 | 4,564 | 4,574 | 10 | |||||||||||||

| 6 | Taxpayer-supported debt servicing costs | 2,250 | 2,608 | 2,406 | (202 | ) | ||||||||||||

| 7 | Self-supported debt servicing costs | 899 | 781 | 767 | (14 | ) | ||||||||||||

| 8 | Pension provisions | (372 | ) | (364 | ) | (364 | ) | - | ||||||||||

| 9 | Disaster and emergency assistance | 3,025 | - | 847 | 847 | |||||||||||||

| 10 | Expense before contingency | 70,447 | 71,182 | 73,045 | 1,863 | |||||||||||||

| 11 | Contingency (forecast un-allocated) | - | 2,000 | 279 | (1,721 | ) | ||||||||||||

| 12 | Total Expense | 70,447 | 73,182 | 73,324 | 143 | |||||||||||||

| 13 | Surplus / Deficit | 4,285 | 355 | 4,563 | 4,208 | |||||||||||||

| Capital Plan | ||||||||||||||||||

| 14 | Capital grants | 2,103 | 3,469 | 3,523 | 54 | |||||||||||||

| 15 | Capital investment | 4,197 | 4,830 | 4,742 | (88 | ) | ||||||||||||

| 16 | Total Capital Plan | 6,300 | 8,299 | 8,265 | (34 | ) | ||||||||||||

| Cash Adjustments / Borrowing Requirements | (at March 31) | |||||||||||||||||

| 17 | Cash at start of year / Alberta Fund | 5,136 | 3,218 | 3,667 | 449 | |||||||||||||

| 18 | Alberta Fund allocation - Heritage Fund | - | (2,000 | ) | (2,000 | ) | ||||||||||||

| 19 | Surplus / (deficit) | 4,285 | 355 | 4,563 | 4,208 | |||||||||||||

Cash adjustments | ||||||||||||||||||

| 20 | Retained income of funds and agencies | (972 | ) | (2,099 | ) | (2,157 | ) | (58 | ) | |||||||||

| 21 | Other cash adjustments | 1,280 | 279 | 1,123 | 844 | |||||||||||||

| 22 | Capital cash adjustments | (2,397 | ) | (2,257 | ) | (2,425 | ) | (168 | ) | |||||||||

| 23 | ATB Financial dividend | - | 100 | 100 | - | |||||||||||||

| 24 | Surplus cash (cash at start of year + surplus +/- net cash adjustments) | 7,333 | (2,404 | ) | 2,871 | 5,275 | ||||||||||||

| 25 | Less: Taxpayer-supported debt repayment | (3,666 | ) | - | (1,435 | ) | (1,435 | ) | ||||||||||

| 26 | Less: Allocation to Alberta Fund | (3,666 | ) | - | (1,435 | ) | (1,435 | ) | ||||||||||

| 27 | Direct borrowing required | - | 2,404 | - | (2,404 | ) | ||||||||||||

| 28 | Cash at end of year | - | - | - | - | |||||||||||||

| 2024-25 Second Quarter Fiscal Update and Economic Statement | 21 | |

Operating Expense by Ministry

(millions of dollars)

| Fiscal Year | Change

from

Budget | |||||||||||||||

| 2023-24 | 2024-25 | |||||||||||||||

| Actual | Budget | Forecast | ||||||||||||||

Advanced Education | 6,233 | 6,305 | 6,323 | 18 | ||||||||||||

Affordability and Utilities | 119 | 84 | 85 | 1 | ||||||||||||

Agriculture and Irrigation | 743 | 870 | 874 | 4 | ||||||||||||

Arts, Culture and Status of Women | 132 | 157 | 157 | - | ||||||||||||

Children and Family Services | 1,603 | 1,498 | 1,498 | - | ||||||||||||

Education | 8,878 | 9,252 | 9,377 | 125 | ||||||||||||

Energy and Minerals b | 822 | 816 | 851 | 34 | ||||||||||||

Environment and Protected Areas | 377 | 512 | 432 | (80 | ) | |||||||||||

Executive Council b | 47 | 63 | 63 | - | ||||||||||||

Forestry and Parks | 285 | 351 | 355 | 4 | ||||||||||||

Health a | 24,053 | 24,830 | 25,546 | 716 | ||||||||||||

Immigration and Multiculturalism | 39 | 42 | 42 | - | ||||||||||||

Indigenous Relations | 214 | 210 | 217 | 7 | ||||||||||||

Infrastructure | 462 | 488 | 488 | - | ||||||||||||

Jobs, Economy and Trade | 1,557 | 1,849 | 1,835 | (14 | ) | |||||||||||

Justice | 652 | 681 | 681 | - | ||||||||||||

Mental Health and Addiction a | 1,263 | 1,548 | 1,564 | 16 | ||||||||||||

Municipal Affairs | 220 | 235 | 235 | - | ||||||||||||

Public Safety and Emergency Services | 1,205 | 1,249 | 1,250 | 1 | ||||||||||||

Seniors, Community and Social Services | 5,284 | 5,229 | 5,469 | 240 | ||||||||||||

Service Alberta and Red Tape Reduction | 159 | 180 | 185 | 6 | ||||||||||||

Technology and Innovation | 723 | 759 | 759 | - | ||||||||||||

Tourism and Sport | 112 | 126 | 126 | - | ||||||||||||

Transportation and Economic Corridors | 564 | 549 | 547 | (2 | ) | |||||||||||

Treasury Board and Finance | 2,237 | 2,086 | 2,177 | 91 | ||||||||||||

Legislative Assembly | 160 | 156 | 156 | - | ||||||||||||

Total Operating Expense | 58,143 | 60,124 | 61,292 | 1,168 | ||||||||||||

a 2023-24 Actuals and 2024-25 Budget numbers restated to reflect Recovery Alberta transfer from Health to Mental Health and Addiction. b 2024-25 Budget numbers restated to reflect a portion of Industry Advocacy program transfer from Energy and Minerals to Executive Council.

Disaster and Emergency Assistance Expense

(millions of dollars) |

| |||||||||||||||

| Fiscal Year | Change

from

Budget | |||||||||||||||

| 2023-24 | 2024-25 | |||||||||||||||

| Actual | Budget | Forecast | ||||||||||||||

Agriculture and Irrigation – agriculture support | 1,856 | - | - | - | ||||||||||||

Forestry and Parks – wildfire fighting | 851 | - | 647 | 647 | ||||||||||||

Health - wildfire supports | 4 | - | - | - | ||||||||||||

Public Safety and Emergency Services – wildfire / flood support | 260 | - | 163 | 163 | ||||||||||||

Municipal Affairs - wildfire support | - | - | 17 | 17 | ||||||||||||

Seniors, Community and Social Services - wildfire support | 54 | - | 20 | 20 | ||||||||||||

Total Disaster and Emergency Assistance Expense | 3,025 | - | 847 | 847 | ||||||||||||

| 22 | 2024-25 Second Quarter Fiscal Update and Economic Statement | |

Capital Amortization Expense

(millions of dollars)

| 2023-24 | 2024-25 | from | ||||||||||||||

| Actual | Budget | Forecast |

Budget | |||||||||||||

Advanced Education | 526 | 548 | 548 | - | ||||||||||||

Affordability and Utilities | 1 | 2 | 2 | - | ||||||||||||

Agriculture and Irrigation | 30 | 37 | 37 | - | ||||||||||||

Arts, Culture and Status of Women | 7 | 7 | 7 | - | ||||||||||||

Education | 475 | 481 | 481 | - | ||||||||||||

Energy and Minerals | 13 | 13 | 13 | - | ||||||||||||

Environment and Protected Areas | 4 | 4 | 4 | - | ||||||||||||

Forestry and Parks | 28 | 46 | 46 | - | ||||||||||||

Health | 562 | 580 | 580 | - | ||||||||||||

Infrastructure | 149 | 160 | 160 | - | ||||||||||||

Jobs, Economy and Trade | 1 | 2 | 2 | - | ||||||||||||

Justice | 1 | 4 | 4 | - | ||||||||||||

Municipal Affairs | 1 | 4 | 1 | (3 | ) | |||||||||||

Public Safety and Emergency Services | 29 | 29 | 29 | - | ||||||||||||

Seniors, Community and Social Services | 52 | 52 | 52 | - | ||||||||||||

Service Alberta and Red Tape Reduction | 16 | 18 | 18 | - | ||||||||||||

Technology and Innovation | 57 | 80 | 80 | - | ||||||||||||

Transportation and Economic Corridors | 788 | 853 | 853 | - | ||||||||||||

Treasury Board and Finance | 23 | 22 | 22 | - | ||||||||||||

Legislative Assembly | 2 | 2 | 2 | - | ||||||||||||

Total Amortization Expense a | 2,764 | 2,943 | 2,940 | (3 | ) | |||||||||||

a 2024-25 Budget numbers restated for the adoption of the Public Private partnership standard, which reflects decreases in amortization expense of $6 million for Education and $18 million for Transportation and Economic Corridors.

Inventory Consumption Expense

(millions of dollars) |

| |||||||||||||||

| Fiscal Year | Change

from

Budget | |||||||||||||||

| 2023-24 | 2024-25 | |||||||||||||||

| Actual | Budget | Forecast | ||||||||||||||

Advanced Education | 54 | 196 | 196 | - | ||||||||||||

Arts, Culture and Status of Women | 1 | 1 | 1 | - | ||||||||||||

Education | 22 | - | - | - | ||||||||||||

Forestry and Parks | 1 | 1 | 1 | - | ||||||||||||

Health a | 1,467 | 1,328 | 1,328 | - | ||||||||||||

Infrastructure | 1 | 2 | 2 | - | ||||||||||||

Mental Health and Addiction a | 14 | 16 | 16 | - | ||||||||||||

Public Safety and Emergency Services | 1 | 1 | 1 | - | ||||||||||||

Service Alberta and Red Tape Reduction | 4 | 6 | 6 | - | ||||||||||||