Exhibit 99.1

Exhibit 99.1

Morgan Stanley Conference

March 7, 2013

Cross Winds Energy Park

Gas Combined Cycle Plant

Consumers Smart Energy Program

This presentation is made as of the date hereof and contains “forward-looking statements” as defined in Rule 3b-6 of the Securities Exchange Act of 1934, as amended, Rule 175 of the Securities Act of 1933, as amended, and relevant legal decisions. The forward-looking statements are subject to risks and uncertainties. They should be read in conjunction with “FORWARD-LOOKING STATEMENTS AND INFORMATION” and “RISK FACTORS” sections of CMS Energy’s and Consumers Energy’s Form 10-K for the year ended December 31 and as updated in subsequent 10-Qs. CMS Energy’s and Consumers Energy’s “FORWARD-LOOKING STATEMENTS AND INFORMATION” and “RISK FACTORS” sections are incorporated herein by reference and discuss important factors that could cause CMS Energy’s and Consumers Energy’s results to differ materially from those anticipated in such statements. CMS Energy and Consumers Energy undertake no obligation to update any of the information presented herein to reflect facts, events or circumstances after the date hereof.

The presentation also includes non-GAAP measures when describing CMS Energy’s results of operations and financial performance. A reconciliation of each of these measures to the most directly comparable GAAP measure is included in the appendix and posted on our website at www.cmsenergy.com.

CMS Energy provides financial results on both a reported (Generally Accepted Accounting Principles) and adjusted (non-GAAP) basis. Management views adjusted earnings as a key measure of the company’s present operating financial performance, unaffected by discontinued operations, asset sales, impairments, regulatory items from prior years, or other items. Certain of these items have the potential to impact, favorably or unfavorably, the company’s reported earnings in 2013. The company is not able to estimate the impact of these matters and is not providing reported earnings guidance.

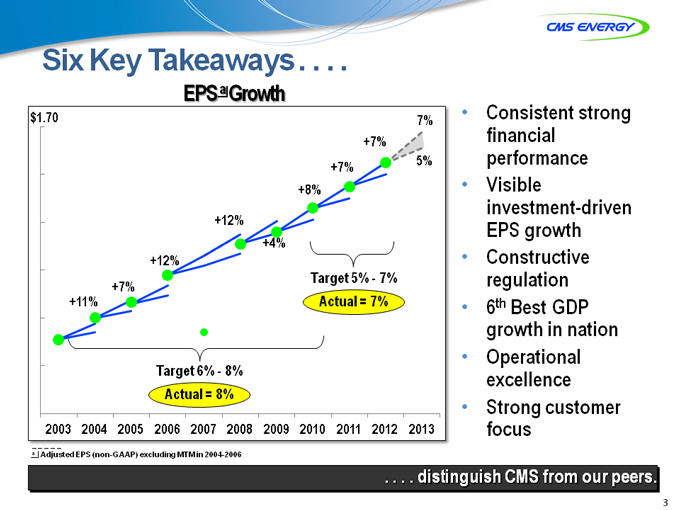

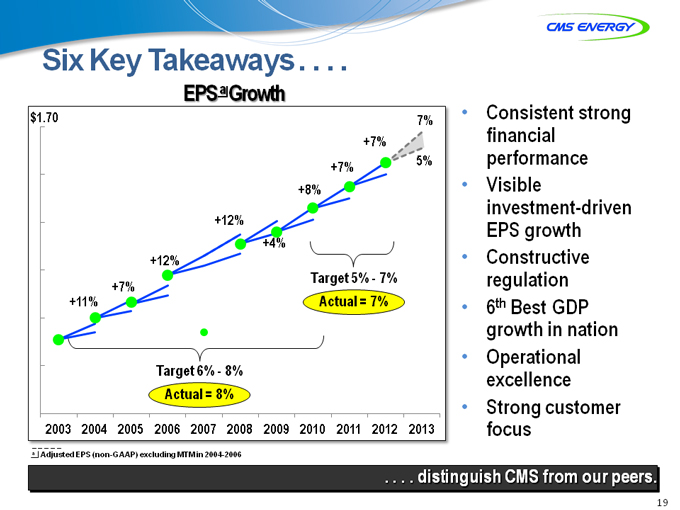

Six Key Takeaways . . . .

EPS a Growth

$1.70 7%

+7%

+7% 5%

+8%

+12%

+4%

+12%

+7% Target 5%—7%

+11% Actual = 7%

Target 6%—8%

Actual = 8%

2003 _ 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

a Adjusted EPS (non-GAAP) excluding MTM in 2004-2006

Consistent strong financial performance Visible investment-driven EPS growth Constructive regulation 6th Best GDP growth in nation Operational excellence Strong customer focus

. . . . distinguish CMS from our peers.

3

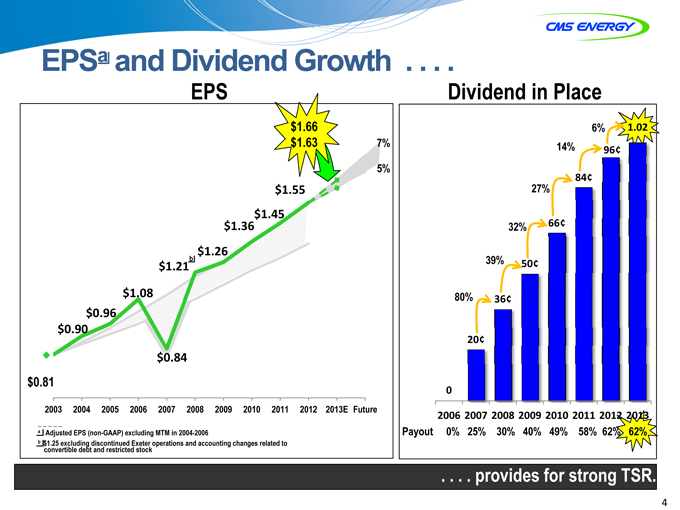

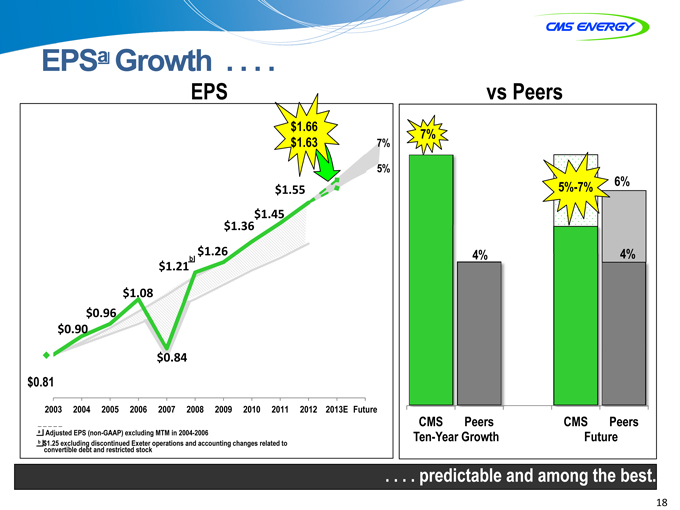

EPSa and Dividend Growth . . . .

EPS

$1 66.

$1.63 7%

5%

$1.55

$1.45

$1.36

$1.26

$1.21b

$1.08

$0.96

$0.90

$0.84

$0 81.

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013E Future

a Adjusted EPS (non-GAAP) excluding MTM in 2004-2006

b $1.25 excluding discontinued Exeter operations and accounting changes related to

convertible debt and restricted stock

Dividend in Place

6% 102.

14% 96¢

84¢

27%

32% 66¢

39% 50¢

80% 36¢

20¢

0

2006 2007 2008 2009 2010 2011 2012 2013

Payout 0% 25% 30% 40% 49% 58% 62% 62%

. . . . provides for strong trong TSR.

4

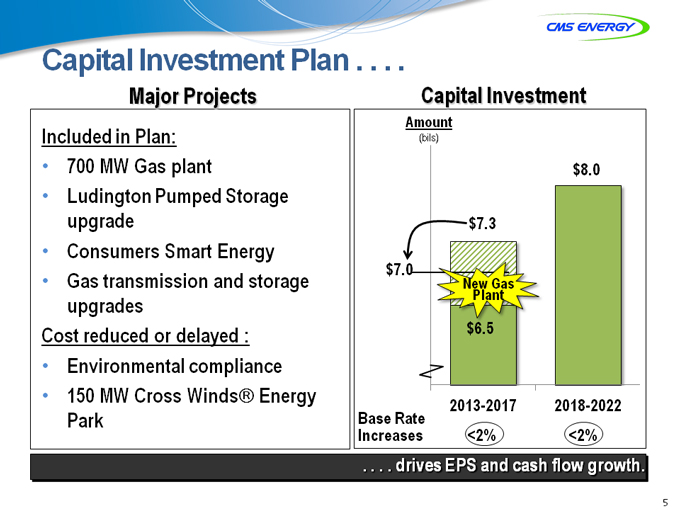

Capital Investment Plan . . . .

Major Projects

Included in Plan:

• 700 MW Gas plant

• Ludington Pumped Storage upgrade

• Consumers Smart Energy

• Gas transmission and storage upgrades Cost reduced or delayed :

• Environmental compliance

• 150 MW Cross Winds Energy Park

Capital Investment

Amount

(bils)

$8.0

$7.3

$7.0

New Gas

Plant

$6.5

2013-2017 2018-2022

Base Rate

Increases <2% <2%

. . . . drivesrives EPS and cash flow growth.

5

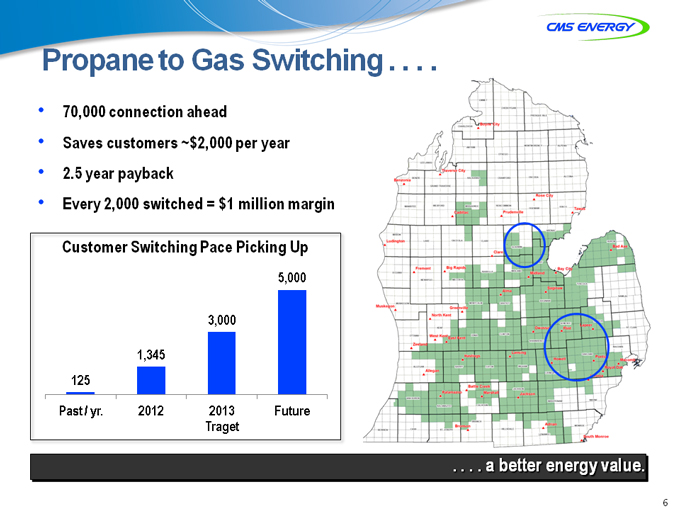

Propane to Gas Switching . . . .

70,000 connection onnection ahead head

Saves customers ~$2,000 per year 2.5 year payback Every 2,000 switched = $1 million margin

Customer Switching Pace Picking Up

5,000

3,000

1,345

125

Past / yr. 2012 2013 Future

Traget

. . . . a better etter energy value.

6

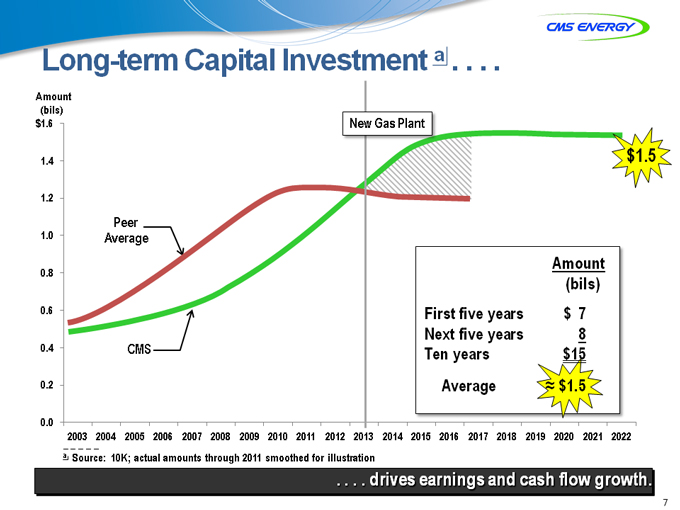

Long-term Capital Investment a . . . .

Amount

(bils)

$1.6 New Gas Plant

1.4 $1.5

1.2

Peer

10. Average

Amount

08.(bils)

06. First five years $ 7

Next five years 8

0.4 CMS Ten years $15

0.2 Average $1.5

0.0

_ 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022

a Source: 10K; actual amounts through 2011 smoothed for illustration

. . . . drives earnings and cash flow growth.

7

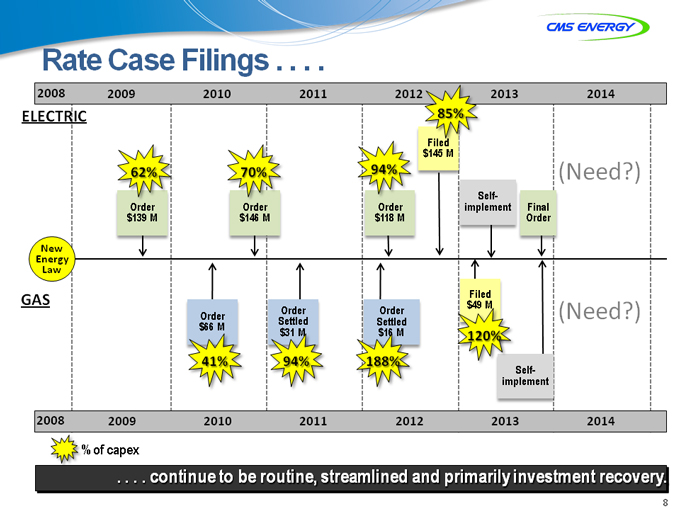

Rate Case Filings . . . .

2008 2009 2010 2011 2012 2013 2014

ELECTRIC 85%

Filed

$145 M

62% 70% 94%94%(Need )

Self-

Order Order Order implement Final

$139 M $146 M $118 M Order

New

Energy

Law

Filed

GAS Order Order Order $49 M(Need )

$66 M Settled Settled

$31 M $16 M 120%

41% 94% 188% Self-

implement

2008 2009 2010 2011 2012 2013 2014

% of capex

. . . . continue to be routine, streamlined and primarily investment recovery.

8

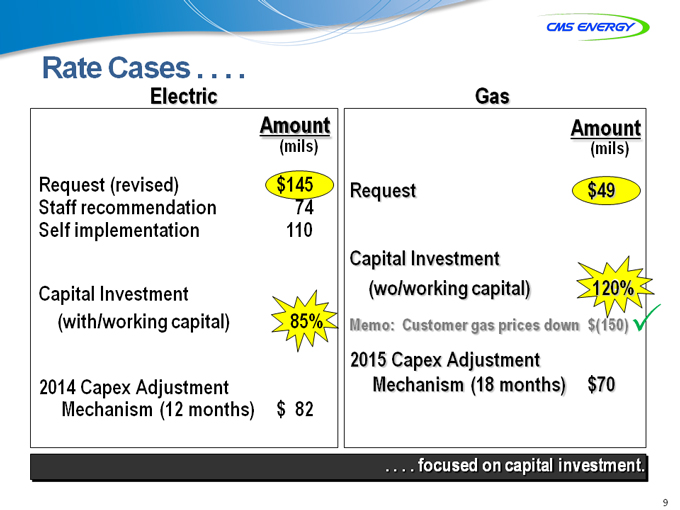

Rate Cases .. . . .

Electric

Amount

(mils)

Request (revised) $ 145

Staff recommendation 74

Self implementation 110

Capital Investment

(with/working capital) 85%

2014 Capex Adjustment

Mechanism (12 months) $ 82

Gas

Amount

(mils)

Request $49

Capital Investment

(wo/working capital) 120%

Memo: Customer gas prices down $(150)

2015 Capex Adjustment

Mechanism (18 months) $70

. . . . focused on capital investment.

9

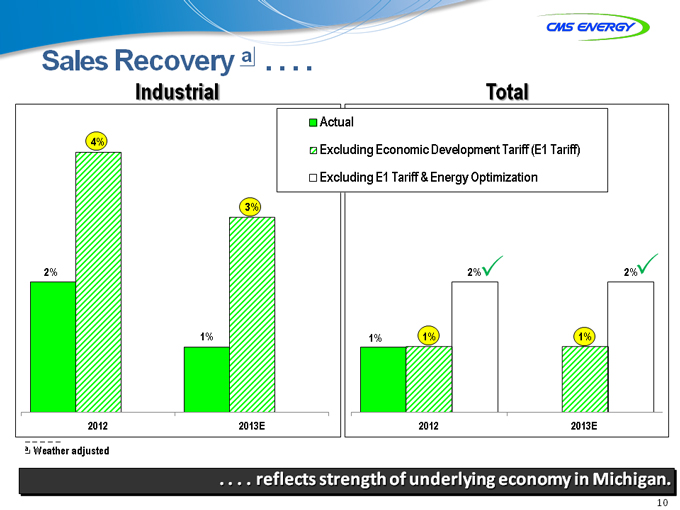

Sales Recovery a . . . .

Actual

Excluding Economic Development Tariff (E1 Tariff) Excluding E1 Tariff & Energy Optimization

Industrial

4%

3%

2%

1%

2012 2013E

a Weather adjusted

Total

2% 2%

1% 1% 1%

2012 2013E

. . . . reeflects strength of underlying economy in Michigan.

10

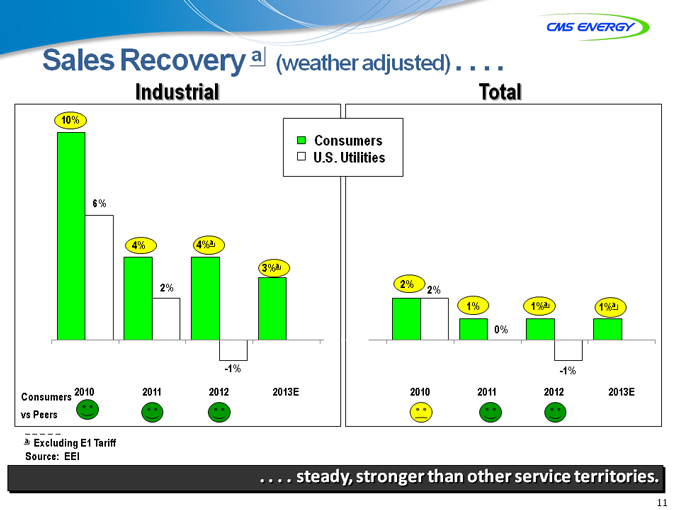

Sales Recovery a (weather adjusted) . . . .

Industrial

10%

6%

4% 4%a

3%a

2%

-1%

Consumers 2010 2011 2012 2013E

vs _ Peers

a Excluding E1 Tariff

Source: EEI

Consumers U.S. Utilities

Total

2% 2%

1% 1%a 1%a

0%

-1%

2010 2011 2012 2013E

. . . . steady, stronger than other service territories.

11

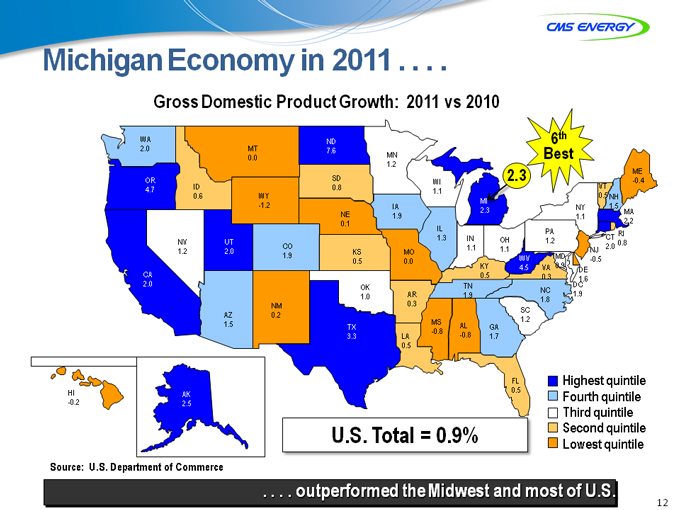

Michigan Economy in 2011 . . . .

Gross Domestic Product Growth: 2011 vs 2010

WA ND 6th

2.0 MT 7.6 MN Best

0.0

12.

2.3 ME

OR SD WI -04.

4.7 ID 0.8 1.1 VT

0.6 WY 0.5 NH

MI

-1.2 IA NY 1.5

NE 1.9 2.3 1.1 MA

0.1 2.2

IL PA RI

NV UT 1.3 IN OH 1.2 CT 0.8

1.2 2.0 CO KS MO 1.1 1.1 NJ 2.0

19. 0.5 0.0 WV MD -0.5

KY 4.5 VA 0.9 DE

CA 0.5 0.3 1.6

2.0 OK TN DC

1.0 AR 1.9 NC 1.9

1.8

NM 0.3 SC

AZ 0.2

1.5 TX MS AL GA 1.2

3.3 LA -0.8 -0.8 1.7

05.

FL Highest quintile

HI AK 0.5 Fourth quintile

-0.2 2.5

Third quintile

US Total=09%. Lowest Second quintile quintile

Source: U.S. Department of Commerce

. . . . outperformed the Midwest and most of US . .

12

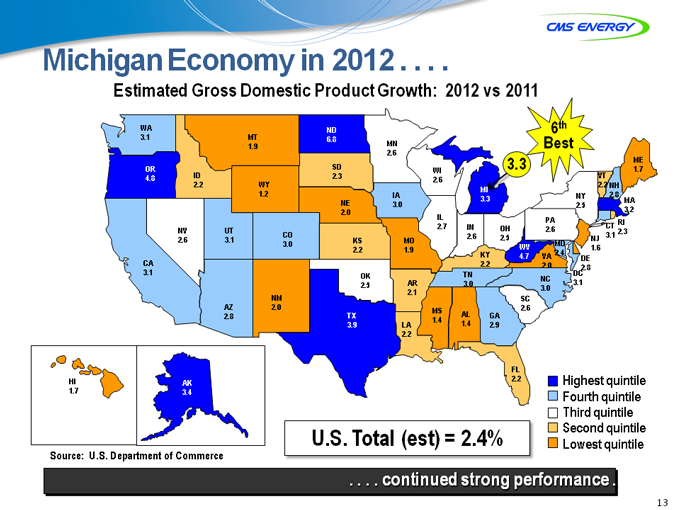

Michigan Economy in 2012 . . . .

Estimated Gross Domestic Product Growth: 2012 vs 2011

WA ND 6th

3.1 MT 6.8 MN Best

19.

2.6

3.3 ME

OR SD WI 1.7

4.8 ID 2.3 2.6 VT

2.2 WY 2.2 NH

MI

1.2 IA NY 2.8

NE 3.0 33. 2.5 MA

2.0 3.2

IL PA RI

NV UT 2.7 IN OH 2.6 CT 2.3

2.6 3.1 CO KS MO 26. 2.5 NJ 3.1

3.0 WV MD

2.2 1.9 1.6

KY 4.7 VA 2.4 DE

CA 2.2 2.0 2.8

31. OK TN DC

2.5 AR 3.0 NC 3.1

2.1 3.0

NM SC

AZ 2.0 MS 26.

2.8 TX AL GA

3.9 LA 1.4 1.4 2.9

2.2

FL

HI AK 2.2 Highest quintile

1.7 3.4 Fourth quintile

Third quintile

US Total(est)=24%. Lowest Second quintile quintile

Source: U.S. Department of Commerce

. . . . continued strong performance .

13

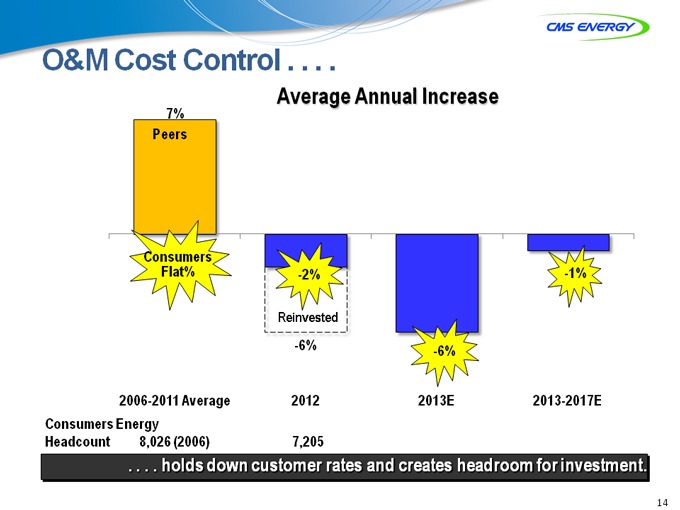

O&M Cost Control . . . .

Average Annual Increase

7%

Peers

Consumers

Flat% -2% -1%

-2%

Reinvested

-6% -6%

2006-2011 Average 2012 2013E 2013-2017E

Consumers Energy

Headcount 8,026 (2006) 7,205

. . . . holdsolds down customer rates and creates headroom for investment.

14

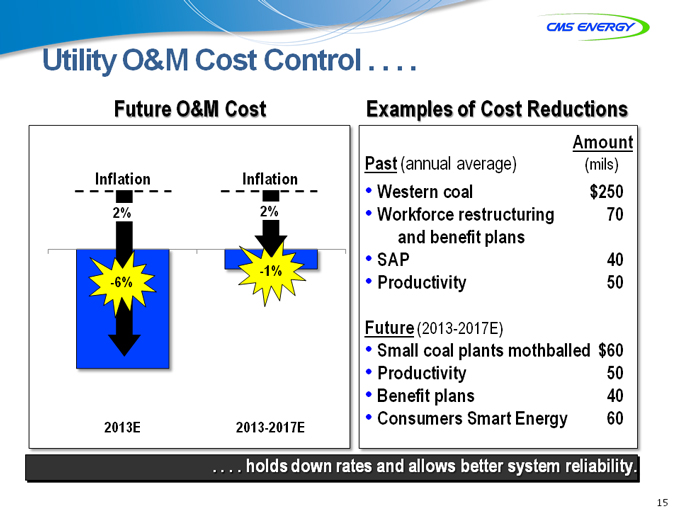

Utility O&M Cost Control . . . .

Future O&M Cost

Inflation Inflation

2% 2%

-1%

-6%

2013E 2013-2017E

Examples of Cost Reductions

Amount

Past (annual average)(mils)

• Western coal $250

• Workforce restructuring 70

and benefit plans

• SAP 40

• Productivity 50

Future (2013-2017E)

• Small coal plants mothballed $60

• Productivity 50

• Benefit plans 40

• Consumers Smart Energy 60

. . . . holds down rates and allows better system reliability

15

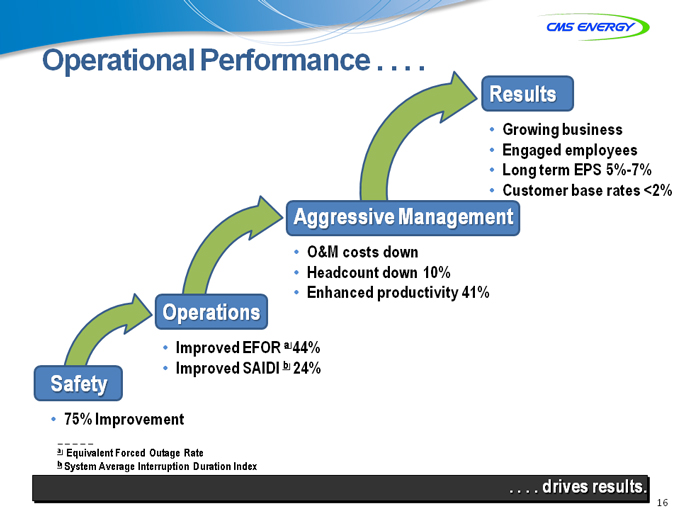

Operational Performance . . . .

Results

• Growing business

• Engaged employees

• Long term EPS 5%-7%

• Customer base rates <2%

Aggressive Management

• O&M costs down

• Headcount down 10%

• Enhanced productivity 41%

Operations

• Improved EFOR a 44%

• Improved SAIDI b 24%

Safety

• _ 75% Improvement

a Equivalent Forced Outage Rate

b System Average Interruption Duration Index

. drives results.

16

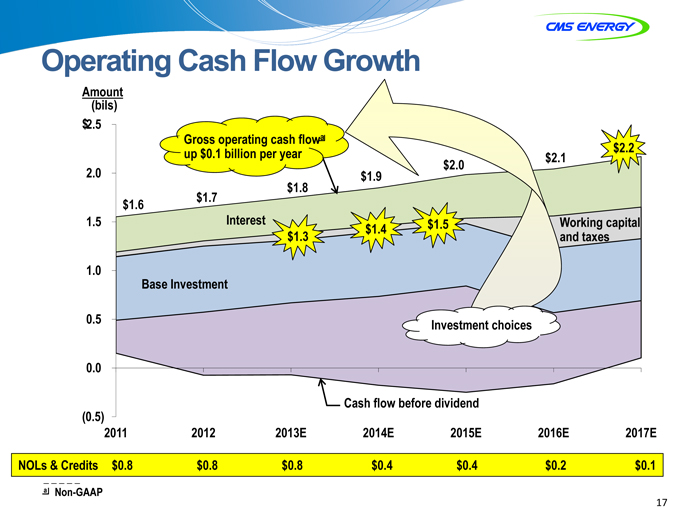

Operating Cash Flow Growth

Amount

(bils)

$2.5

Gross operating cash flowa

up $0.1 billion per year $2.2

2.0 .

$ 1.8

$1.6 $1.7

1.5 Interest $1.4 $1.5 king capital

$1.3 taxes

1 0.

Base Investment

0.5 Investment choices

0

Cash flow before dividend

(0.5)

2011 2012 2013E 2014E 2015E 2016E 2017E

NOLs & Credits $0.8 $0.8 $0.8 $0.4 $0.4 $0.2 $0.1

a Non-GAAP

17

EPSa Growth . . . .

EPS

$1 66.

$1.63 7%

5%

$1.55

$1.45

$1.36

$1.26

$1.21b

$1.08

$0.96

$0.90

$0.84

$0 81.

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013E Future

a Adjusted EPS (non-GAAP) excluding MTM in 2004-2006

b $1.25 excluding discontinued Exeter operations and accounting changes related to

convertible debt and restricted stock

vs Peers

7%

5%-7% 6%

5%

4% 4%

CMS Peers CMS Peers

Ten-Year Growth Future

. . . . predictable and among mong the best est.

18

Six Key Takeaways . . . .

EPS Growth

$1.70 7%

+7%

+7% 5%

+8%

+12%

+4%

+12%

+7% Target 5%—7%

+11% Actual = 7%

Target 6%—8%

Actual = 8%

2003 _ 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

a Adjusted EPS (non-GAAP) excluding MTM in 2004-2006

Consistent strong financial performance Visible investment-driven EPS growth Constructive regulation 6th Best GDP growth in nation Operational excellence Strong customer focus

. . . . distinguish CMS from our peers.

19

Appendix

20

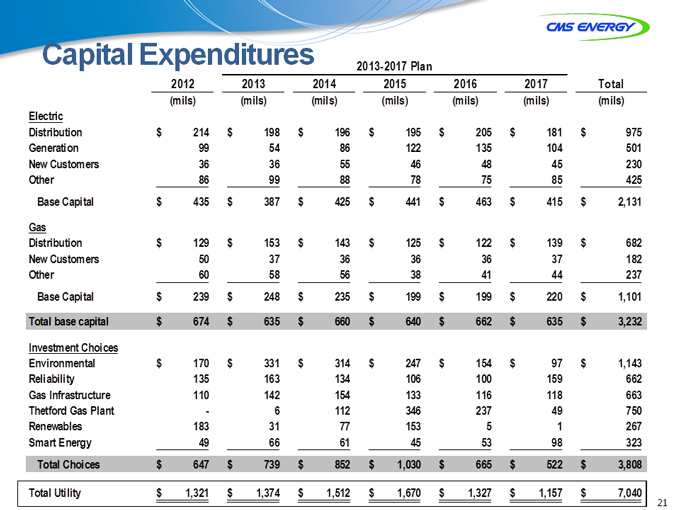

Capital Expenditures

2013-2017 Plan

2012 2013 2014 2015 2016 2017 Total

(mils)(mils)(mils)(mils)(mils)(mils)(mils)

Electric

Distribution $ 214 $ 198 $ 196 $ 195 $ 205 $ 181 $ 975

Generation 99 54 86 122 135 104 501

New Customers 36 36 55 46 48 45 230

Other 86 99 88 78 75 85 425

Base Capital $ 435 $ 387 $ 425 $ 441 $ 463 $ 415 $ 2,131

Gas

Distribution $ 129 $ 153 $ 143 $ 125 $ 122 $ 139 $ 682

New Customers 50 37 36 36 36 37 182

Other 60 58 56 38 41 44 237

Base Capital $ 239 $ 248 $ 235 $ 199 $ 199 $ 220 $ 1,101

Total base capital $ 674 $ 635 $ 660 $ 640 $ 662 $ 635 $ 3,232

Investment Choices

Environmental $ 170 $ 331 $ 314 $ 247 $ 154 $ 97 $ 1,143

Reliability 135 163 134 106 100 159 662

Gas Infrastructure 110 142 154 133 116 118 663

Thetford Gas Plant—6 112 346 237 49 750

Renewables 183 31 77 153 5 1 267

Smart Energy 49 66 61 45 53 98 323

Total Choices $ 647 $ 739 $ 852 $ 1,030 $ 665 $ 522 $ 3,808

Total Utility $ 1,321 $ 1,374 $ 1,512 $ 1,670 $ 1,327 $ 1,157 $ 7,040

21

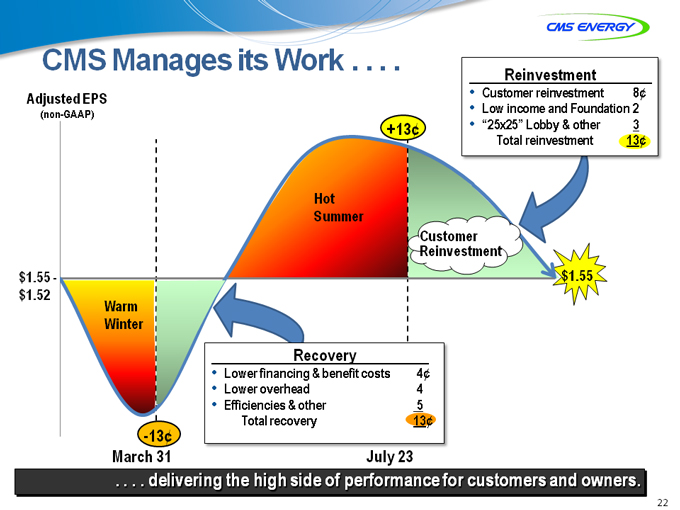

CMS Manages its Work . . . .

Adjusted EPS • Customer reinvestment 8¢

(non-GAAP) • Low income and Foundation 2

+13¢ • “25x25” Lobby & other 3

Total reinvestment 13¢

Hot

Summer

Customer

Reinvestment

$ 1.55—$ 1.55

$ 1.52

Warm

Winter

Recovery

• Lower financing & benefit costs 4¢

• Lower overhead 4

• Efficiencies & other 5

Total recovery 13¢

-13¢

March 31 July 23

Reinvestment

. . . . delivering the high side of performance for customers and owners.

22

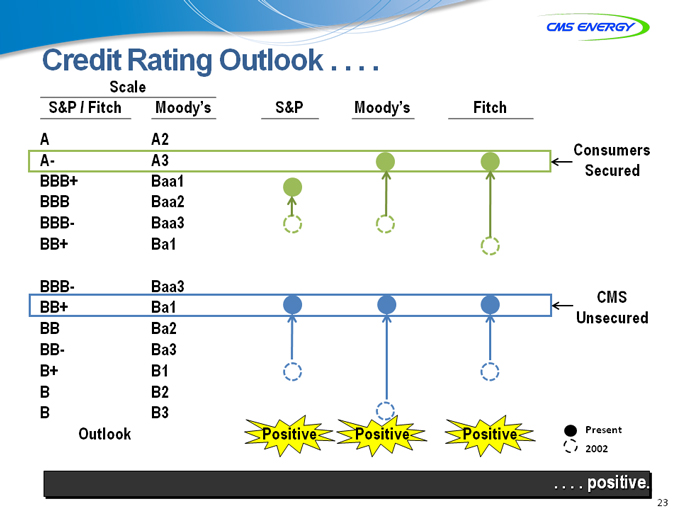

Credit Rating Outlook . . . .

Scale

S&P / Fitch Moody’s S&P Moody’s Fitch

A A2

A- A3 Consumers

BBB+ Baa1 Secured

BBB Baa2

BBB- Baa3

BB+ Ba1

BBB- Baa3

BB+ Ba1 CMS

BB Ba2 Unsecured

BB- Ba3

B+ B1

B B2

B B3

Outlook Positive Positive Positive Present

2002

. . . . positive.

23

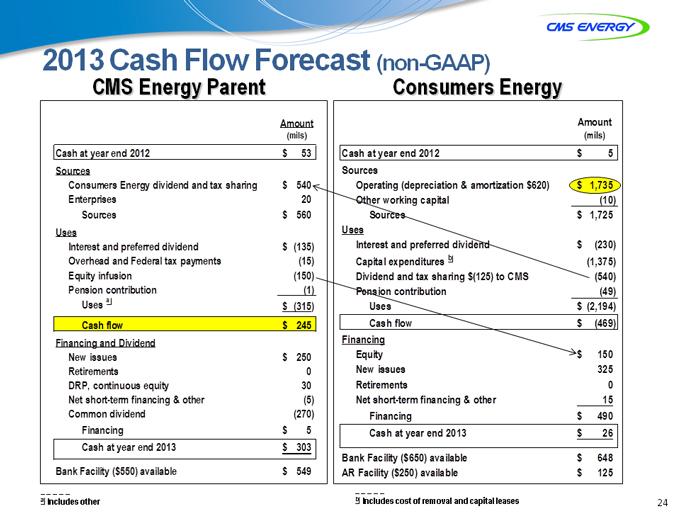

2013 Cash Flow Forecast (non-GAAP)

CMS Energy Parent Consumers Energy

Amount Amount

(mils)(mils)

Cash at year end 2012 $ 53 Cash at year end 2012 $ 5

Sources Sources

Consumers Energy dividend and tax sharing $ 540 Operating (depreciation & amortization $620) $ 1,735

Enterprises 20 Other working capital(10)

Sources $ 560 Sources $ 1,725

Uses Uses

Interest and preferred dividend $(135) Interest and preferred dividend $ (230)

Overhead and Federal tax payments(15) Capital expenditures b(1,375)

Equity infusionsion(150) Dividend and tax sharing $(125) to CMS(540)

Pension contribution(1) Pension contribution(49)

Uses a $(315) Uses $ (2,194)

Cash flow $ 245 Cash flow $ (469)

Financing and Dividend Financing

New issues $ 250 Equity $ 150

Retirements 0 New issues 325

DRP, continuous equity 30 Retirements 0

Net short-term financing & other(5) Net short-term financing & other 15

Common dividend(270) Financing $ 490

Financing $ 5 Cash at year end 2013 $ 26

Cash at year end 2013 $ 303

Bank Facility ($650) available $ 648

Bank _ Facility ($550) available $ 549 AR _ Facility ($250) available $ 125

a Includes other b Includes cost of removal and capital leases

24

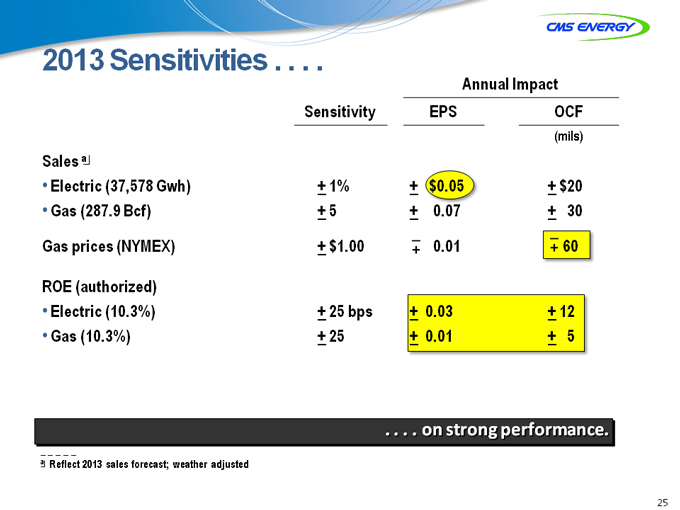

2013 Sensitivities . . . .

Annual Impact

Sensitivity EPS OCF

(mils)

Sales a

• Electric (37,578 Gwh) + 1% + $0.05 + $20

• Gas (287.9 Bcf) + 5 + 0.07 + 30

Gas prices (NYMEX) + $1.00 –+ 0.01 –+ 60

ROE (authorized)

• Electric (10.3%) + 25 bps + 0.03 + 12

• Gas (10.3%) + 25 + 0.01 + 5

. . . . onn strong performance.

a Reflect 2013 sales forecast; weather adjusted

25

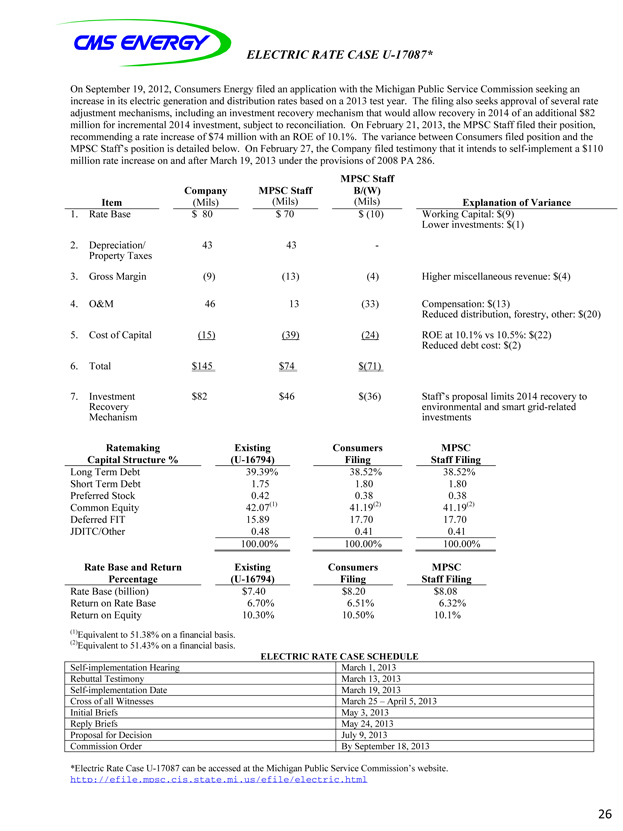

ELECTRIC RATE CASE U-17087*

On September 19, 2012, Consumers Energy filed an application with the Michigan Public Service Commission seeking an increase in its electric generation and distribution rates based on a 2013 test year. The filing also seeks approval of several rate adjustment mechanisms, including an investment recovery mechanism that would allow recovery in 2014 of an additional $82 million for incremental 2014 investment, subject to reconciliation. On February 21, 2013, the MPSC Staff filed their position, recommending a rate increase of $74 million with an ROE of 10.1%. The variance between Consumers filed position and the MPSC Staff’s position is detailed below. On February 27, the Company filed testimony that it intends to self-implement a $110 million rate increase on and after March 19, 2013 under the provisions of 2008 PA 286.

MPSC Staff

Company MPSC Staff B/(W)

Item(Mils)(Mils)(Mils) Explanation of Variance

1. Rate Base $ 80 $ 70 $ (10) Working Capital: $(9)

Lower investments: $(1)

2. Depreciation/ 43 43 -

Property Taxes

3. Gross Margin(9)(13)(4) Higher miscellaneous revenue: $(4)

4. O&M 46 13(33) Compensation: $(13)

Reduced distribution, forestry, other: $(20)

5. Cost of Capital(15)(39)(24) ROE at 10.1% vs 10.5%: $(22)

Reduced debt cost: $(2)

6. Total $ 145 $74 $(71)

7. Investment $ 82 $46 $(36) Staff’s proposal limits 2014 recovery to

Recovery environmental and smart grid-related

Mechanism investments

Ratemaking Existing Consumers MPSC

Capital Structure %(U-16794) Filing Staff Filing

Long Term Debt 39.39% 38.52% 38.52%

Short Term Debt 1.75 1.80 1.80

Preferred Stock 0.42 0.38 0.38

Common Equity 42.07(1) 41.19(22) 41.19(2)

Deferred FIT 15.89 17.70 17.70

JDITC/Other 0.48 0.41 0.41

100.00% 100.00% 100.00%

Rate Base and Return Existing Consumers MPSC

Percentage(U-16794) Filing Staff Filing

Rate Base (billion) $7.40 $8.20 $8.08

Return on Rate Base 6.70% 6.51% 6.32%

Return on Equity 10.30% 10.50% 10.1%

(1)Equivalent to 51.38% on a financial basis.

(2)Equivalent to 51.43% on a financial basis.

ELECTRIC RATE CASE SCHEDULE

Self-implementation Hearing March 1, 2013

Rebuttal Testimony March 13, 2013

Self-implementation Date March 19, 2013

Cross of all Witnesses March 25 – April 5, 2013

Initial Briefs May 3, 2013

Reply Briefs May 24, 2013

Proposal for Decision July 9, 2013

Commission Order By September 18, 2013

*Electric Rate Case U-17087 can be accessed at the Michigan Public Service Commission’s website.

http://eefile.mpssc.cis.state.mi.us/efile/electric.html

26

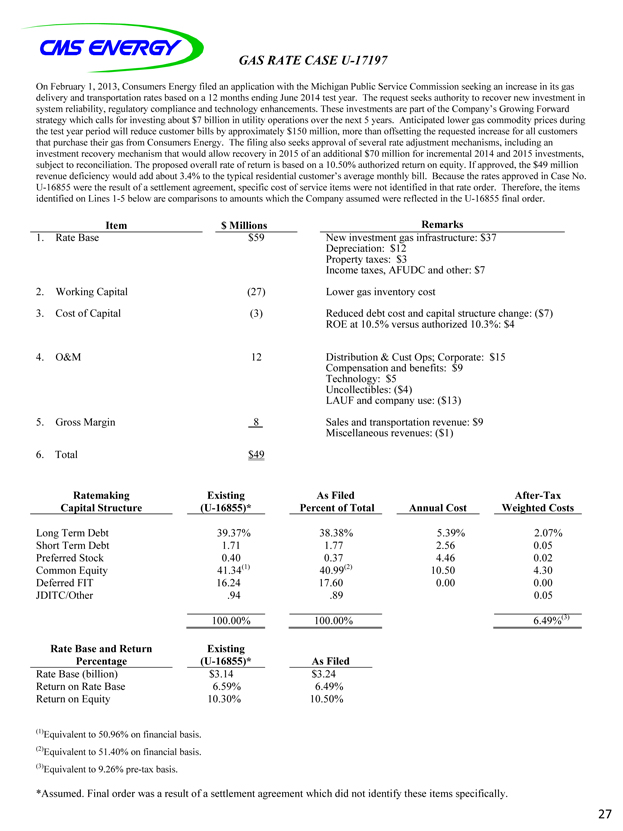

GAS RATE CASE U-17197

On February 1, 2013, Consumers Energy filed an application with the Michigan Public Service Commission seeking an increase in its gas delivery and transportation rates based on a 12 months ending June 2014 test year. The request seeks authority to recover new investment in system reliability, regulatory compliance and technology enhancements. These investments are part of the Company’s Growing Forward strategy which calls for investing about $7 billion in utility operations over the next 5 years. Anticipated lower gas commodity prices during the test year period will reduce customer bills by approximately $150 million, more than offsetting the requested increase for all customers that purchase their gas from Consumers Energy. The filing also seeks approval of several rate adjustment mechanisms, including an investment recovery mechanism that would allow recovery in 2015 of an additional $70 million for incremental 2014 and 2015 investments, subject to reconciliation. The proposed overall rate of return is based on a 10.50% authorized return on equity. If approved, the $49 million revenue deficiency would add about 3.4% to the typical residential customer’s average monthly bill. Because the rates approved in Case No. U-16855 were the result of a settlement agreement, specific cost of service items were not identified in that rate order. Therefore, the items identified on Lines 1-5 be elow are comparisons to amounts which the Company assumed were reflected in the U-16855 final order.

Item $ Millions Remarks

1. Rate Base $59 New investment gas infrastructure: $37

Depreciation: $12

Property taxes: $3

Income taxes, AFUDC and other: $7

2. Working Capital(27) Lower gas inventory cost

3. Cost of Capital(3) Reduced debt cost and capital structure change: ($7)

ROE at 10.5% versus authorized 10.3%: $4

4. O&M 12 Distribution & Cust Ops; Corporate: $15

Compensation and benefits: $9

Technology: $5

Uncollectibles: ($4)

LAUF and compaany use: ($13)

5. Gross Margin 8 Sales and transportation revenue: $9

Miscellaneous revenues: ($1)

6. Total $49

Ratemaking Existing As Filed After-Tax

Capital Structure(U-16855)* Percent of Total Annual Cost Weighted Costs

Long Term Debt 39.37% 38.38% 5.39% 2.07%

Short Term Debt 1.71 1.77 2.56 0.05

Preferred Stock 0.40 0.37 4.46 0.02

Common Equity 41.34(1) 40.99(2) 10.50 4.30

Deferred FIT 16.24 17.60 0.00 0.00

JDITC/Other .94 .89 0.05

100.00% 100.00% 6.49%(3)

Rate Base and Return Existing

Percentage(U-16855)* As Filed

Rate Base (billion) $3.14 $3.24

Return on Rate Base 6.59% 6.49%

Return on Equity 10.30% 10.50%

(1)Equivalent to 50.96% on financial basis. (2)Equivalent to 51.40% on financial basis.

(3)

Equivalent to 9.26% pre-tax basis.

*Assumed. Final order was a result of a settlement agreement which did not identify these items specifically.

27

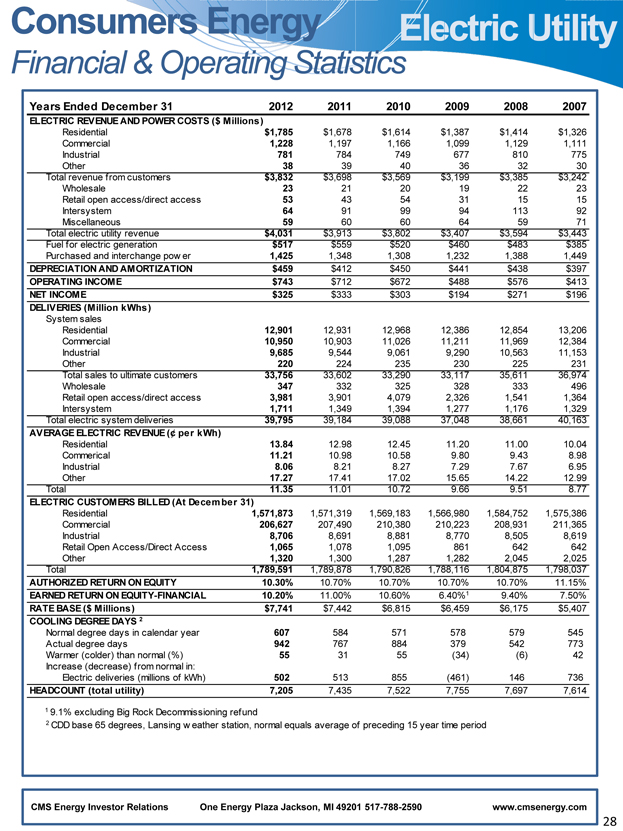

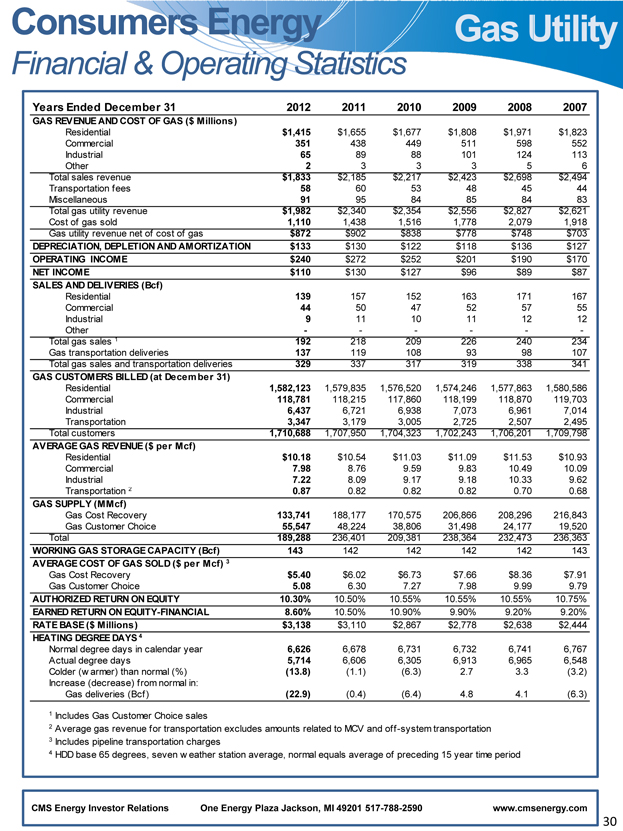

Financial & Operating Statistics

Years Ended December 31 2012 2011 2010 2009 2008 2007

ELECTRIC REVENUE AND POWER COSTS ($ Millions)

Residential $1,785 $1,678 $1,614 $1,38 $1,414 $1,326

Commercial 1,228 1,197 1,166 1,09 1,129 1,111

I dustrial 781 784 749 67 810 775

Other 38 39 40 3 32 30

Total revenue from customers $3,832 $3,698 $3,569 $3,19 $3,385 $3,242

holesale 23 21 20 1 22 23

Retail open access/direct a cess 53 43 54 3 15 15

I tersystem 64 91 99 9 113 92

Miscellaneous 59 60 60 6 59 71

Total electric utility revenue $4,031 $3,913 $3,802 $3,40 $3,594 $3,443

Fuel for electric generation $517 $559 $520 $46 $483 $385

Purchased and interchange pow er 1,425 1,348 1,308 1,23 1,388 1,449

DEPRECIATION AND AM ORTIZATION $459 $412 $450 $441 $438 $397

OPERATING INCOME $743 $712 $672 $488 $576 $413

NET INCOME $325 $333 $303 $194 $271 $196

DELIVERIES (Million kWhs)

System sales

Residential 12,901 12,931 12,968 12,38 12,854 13,206

Commercial 10,950 10,903 11,026 11,21 11,969 12,384

I dustrial 9,685 9,544 9,061 9,29 10,563 11,153

Other 220 224 235 23 225 231

Total sales to ultimate customers 33,756 33,602 33,290 33,11 35,611 36,974

holesale 347 332 325 32 333 496

Retail open access/direct a cess 3,981 3,901 4,079 2,32 1,541 1,364

I tersystem 1,711 1,349 1,394 1,27 1,176 1,329

Total electric system deliv ries 39,795 39,184 39,088 37,04 38,661 40,163

AVERAGE ELECTRIC REVENUE (¢ per k Wh)

Residential 13.84 12.98 12.45 11.2 11.00 10.04

Commerical 11.21 10.98 10.58 9.8 9.43 8.98

I dustrial 8.06 8.21 8.27 7.2 7.67 6.95

Other 17.27 17.41 17.02 15.6 14.22 12.99

Total 11.35 11.01 10.72 9.6 9.51 8.77

ELECTRIC CUSTOMERS BILLED (At De cem ber 31)

Residential 1,571,873 1,571,319 1,569,183 1,566,98 ,584,752 1, 75,386

Commercial 206,627 207,490 210,380 210,22 208,931 11,365

I dustrial 8,706 8,691 8,881 8,77 8,505 8,619

Retail Open Access/Direct ccess 1,065 1,078 1,095 86 642 642

Other 1,320 1,300 1,287 1,28 2,045 2,025

Total 1,789,591 1,789,878 1,790,826 1,788,11 ,804,875 1, 98,037

AUTHORIZED RETURN ON EQUITY 10.30% 10.70% 10.70% 10.70% 10.70% 11.15%

EARNED RETURN ON EQUITY-FINANCIAL 10.20% 11.00% 10.60% 6.40%1 9.40% 7.50%

RATE BASE ($ Millions) $7,741 $7,442 $6,815 $6,459 $6,175 $5,407

COOLING DEGREE DAYS 2

Normal degree days in calendar year 607 584 571 578 579 545

Actual degree days 942 767 884 379 542 773

War er (colder) than normal (%) 55 31 55(34)(6) 42

Increase (decrease) from normal in:

Electric deli eries (millions of kWh) 502 513 855(461) 146 736

HEADCOUNT (total utility) 7,205 7,435 7,522 7,755 7,697 7,614

1 9.1% excluding Big Rock Decommissioning ref und

2 CDD base 65 degrees, Lansing w eather station, normal equals average of preceding 15 year time period

CMS Energy Investor Relations One Energy Plaza Jackson, MI 49201 517-788-2590 www.cmsenergy.com

28

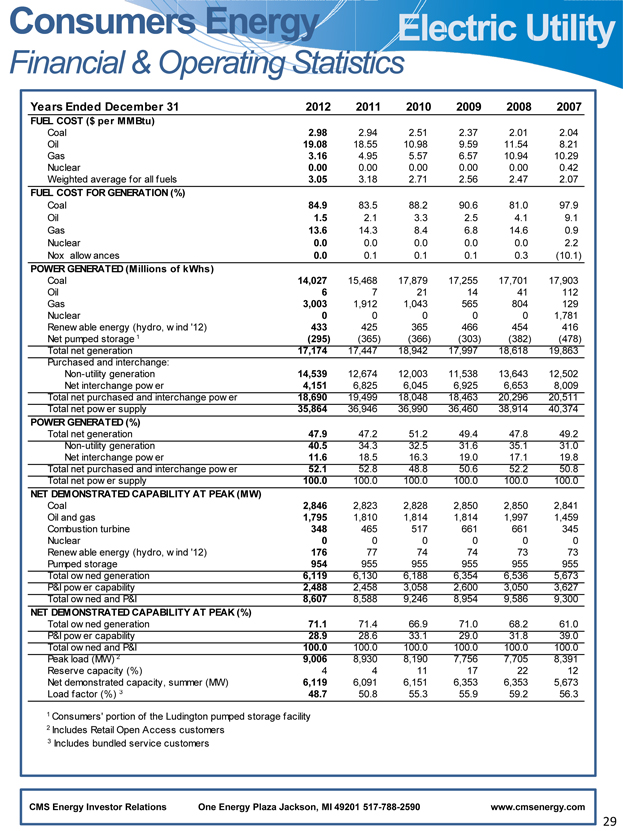

Financial & Operating Statistics

Years Ended Decembe r 31 2012 2011 2010 2009 2008 2007

FUEL COST ($ pe r MM Btu)

Coal .98 2.94 2.51 2.37 2.01 2.04

Oil 1 .08 18.55 10.98 9.59 11.54 8.21

Gas .16 4.95 5.57 6.57 10.94 10.29

Nuclear .00 0.00 0.00 0.00 0.00 0.42

Weighted average f or all fuels .05 3.18 2.71 2.56 2.47 2.07

FUEL COST FOR GENERATION (%)

Coal 84.9 83.5 88.2 90.6 81.0 97.9

Oil 1.5 2.1 3.3 2.5 4.1 9.1

Gas 13.6 14.3 8.4 6.8 14.6 0.9

Nuclear 0.0 0.0 0.0 0.0 0.0 2.2

Nox allow ances 0.0 0.1 0.1 0.1 0.3(10.1)

POWER GENERATED (Millions of kWhs)

Coal 14,027 15,468 17,879 17,255 17,701 17,903

Oil 6 7 21 14 41 112

Gas 3,003 1,912 1,043 565 804 129

Nuclear 0 0 0 0 0 1,781

Renew able energy (hydro, w ind ‘12) 433 425 365 466 454 416

Net pumped storage 1(295)(365)(366)(303)(382)(478)

Total net generation 17,174 17,447 18,942 17,997 18,618 19,863

Purchased and interchange:

Non-utility generation 14,539 12,674 12,003 11,538 13,643 12,502

Net interchange pow er 4,151 6,825 6,045 6,925 6,653 8,009

Total net purchased and interchange pow er 18,690 19,499 18,048 18,463 20,296 20,511

Total net pow er supply 35,864 36,946 36,990 36,460 38,914 40,374

POWER GENERATED (%)

Total net generation 7.9 47.2 51.2 49.4 47.8 49.2

Non-utility generation 0.5 34.3 32.5 31.6 35.1 31.0

Net interchange pow er 1.6 18.5 16.3 19.0 17.1 19.8

Total net purchased and interchange pow er 2.1 52.8 48.8 50.6 52.2 50.8

Total net pow er supply 1 0.0 100.0 100.0 100.0 100.0 100.0

NET DEMONSTRATED CAPABILITY AT PEAK (MW)

Coal 2,846 2,823 2,828 2,850 2,850 2,841

Oil and gas 1,795 1,810 1,814 1,814 1,997 1,459

Combustion turbine 348 465 517 661 661 345

Nuclear 0 0 0 0 0 0

Renew able energy (hydro, w ind ‘12) 176 77 74 74 73 73

Pumped storage 954 955 955 955 955 955

Total ow ned generation 6,119 6,130 6,188 6,354 6,536 5,673

P&I pow er capability 2,488 2,458 3,058 2,600 3,050 3,627

Total ow ned and P&I 8,607 8,588 9,246 8,954 9,586 9,300

NET DEMONSTRATED CAPABILITY AT PEAK (%)

Total ow ned generation 1.1 71.4 66.9 71.0 68.2 61.0

P&I pow er capability 8.9 28.6 33.1 29.0 31.8 39.0

Total ow ned and P&I 1 0.0 100.0 100.0 100.0 100.0 100.0

Peak load (MW) 2 9,006 8,930 8,190 7,756 7,705 8,391

Reserve capacity (%) 4 4 11 17 22 12

Net demonstrated capacity, summer (MW) 6,119 6,091 6,151 6,353 6,353 5,673

Load factor (%) 3 8.7 50.8 55.3 55.9 59.2 56.3

1 Consumers’ portion of the Ludington pumped storage f acility

2 Includes Retail Open Access customers

3 Includes bundled service customers

CMS Energy Investor Relations One Energy Plaza Jackson, MI 49201 517-788-2590 www.cmsenergy.com

29

Financial & Operating Statistics

Years Ended December 31 2012 2011 2010 2009 2008 2007

GAS REVENUE AND COST OF GAS ($ Millions)

Residential $1,415 $1,655 $1,677 $1,808 $ ,971 $1,823

Commercial 351 438 449 511 598 552

Industrial 65 89 88 101 124 113

Other 2 3 3 3 5 6

Total sales revenue $1,833 $2,185 $2,217 $2,423 $ ,698 $2,494

Transportation fees 58 60 53 48 45 44

Miscellaneous 91 95 84 85 84 83

Total gas utility revenue $1,982 $2,340 $2,354 $2,556 $ ,827 $2,621

Cost of gas sold 1,110 1,438 1,516 1,778 ,079 1,918

Gas utility revenue net of cost of gas $872 $902 $838 $778 $748 $703

DEPRECIATION, DEPLETION AND AMORTIZATION $133 $130 $122 $118 $136 $127

OPERATING INCOME $240 $272 $252 $201 $190 $170

NET INCOME $110 $130 $127 $96 $89 $87

SALES AND DELIVERIES (Bcf)

Residential 139 157 152 163 171 167

Commercial 44 50 47 52 57 55

Industrial 9 11 10 11 12 12

Other — — —

Total gas sales 1 192 218 209 226 240 234

Gas transportation deliveries 137 119 108 93 98 107

Total gas sales and transportation deliveries 329 337 317 319 338 341

GAS CUSTOMERS BILLED (at De cem ber 31)

Residential 1,582,123 1,579,835 1,576,520 1,574,246 1,57 ,863 1,580,586

Commercial 118,781 118,215 117,860 118,199 11 ,870 119,703

Industrial 6,437 6,721 6,938 7,073 ,961 7,014

Transportation 3,347 3,179 3,005 2,725 ,507 2,495

Total customers 1,710,688 1,707,950 1,704,323 1,702,243 1,70 ,201 1,709,798

AVERAGE GAS REVENUE ($ per Mcf)

Residential $10.18 $10.54 $11.03 $11.09 $ 1.53 $10.93

Commercial 7.98 8.76 9.59 9.83 0.49 10.09

Industrial 7.22 8.09 9.17 9.18 0.33 9.62

Transportation 2 0.87 0.82 0.82 0.82 0.70 0.68

GAS SUPPLY (MM cf)

Gas Cost Recovery 133,741 188,177 170,575 206,866 20 ,296 216,843

Gas Customer Choice 55,547 48,224 38,806 31,498 2 ,177 19,520

Total 189,288 236,401 209,381 238,364 23 ,473 236,363

WORKING GAS STORAGE CAPACITY (Bcf) 143 142 142 142 142 143

AVERAGE COST OF GAS SOLD ($ per Mcf) 3

Gas Cost Recovery $5.40 $6.02 $6.73 $7.66 8.36 $7.91

Gas Customer Choice 5.08 6.30 7.27 7.98 9.99 9.79

AUTHORIZED RETURN ON EQUITY 10.30% 10.50% 10.55% 10.55% 10.55% 10.75%

EARNED RETURN ON EQUITY-FINANCIAL 8.60% 10.50% 10.90% 9.90% 9.20% 9.20%

RATE BASE ($ Millions ) $3,138 $3,110 $2,867 $2,778 $2,638 $2,444

HEATING DEGREE DAYS 4

Normal degree days in calendar year 6,626 6,678 6,731 6,732 ,741 6,767

Actual degree days 5,714 6,606 6,305 6,913 ,965 6,548

Colder (w armer) than normal (%)(13.8)(1.1)(6.3) 2.7 3.3(3.2)

Increase (decrease) from normal in:

Gas deliveries (Bcf)(22.9)(0.4)(6.4) 4.8 4.1(6.3)

1 Includes Gas Customer Choice sales

2 Average gas revenue for transportation excludes amounts related to MCV and off-system transportation

3 Includes pipeline transportation charges

4 HDD base 65 degrees, seven w eather station average, normal equals average of preceding 15 year time period

CMS Energy Investor Relations One Energy Plaza Jackson, MI 49201 517-788-2590 www.cmsenergy.com

30

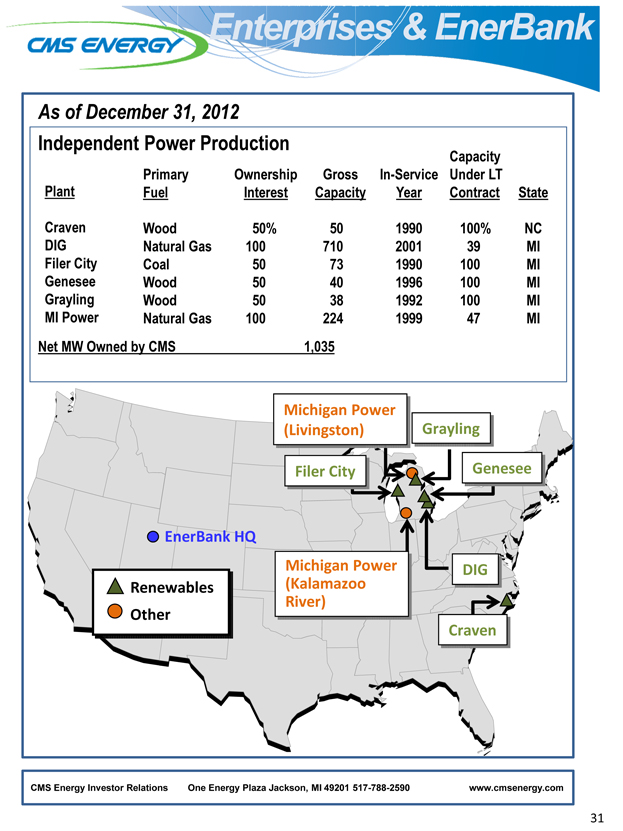

As of December 31, 2012

Independent Power Production

Capacity

Primary Ownership Gross In-Service Under LT

Plant Fuel Interest Capacity Year Contract State

Craven Wood 50% 50 1990 100% NC

DIG Natural Gas 100 710 2001 39 MI

Filer City Coal 50 73 1990 100 MI

Genesee Wood 50 40 1996 100 MI

Grayling Wood 50 38 1992 100 MI

MI Power Natural Gas 100 224 1999 47 MI

Net MW Owned by CMS 1,035

Michigan Power

(Livingston) Grayling

Filer City Genesee

EnerBank HQ

Michigan Power DIG

Renewables(Kalamazoo

River)

Other

Craven

CMS Energy Investor Relations One Energy Plaza Jackson, MI 49201 517-788-2590 www.cmsenergy.com

31

GAAP Reconciliation

32

CMS ENERGY CORPORATION

Earnings Per Share By Year GAAP Reconciliation

(Unaudited)

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | 2003

| | | 2004

| | | 2005

| | | 2006

| | | 2007

| | | 2008

| | | 2009

| | | 2010

| | | 2011

| | | 2012

| |

Reported earnings (loss) per share - GAAP | | ($ | 0.30 | ) | | $ | 0.64 | | | ($ | 0.44 | ) | | ($ | 0.41 | ) | | ($ | 1.02 | ) | | $ | 1.20 | | | $ | 0.91 | | | $ | 1.28 | | | $ | 1.58 | | | $ | 1.42 | |

| | |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

|

After-tax items: | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Electric and gas utility | | | 0.21 | | | | (0.39 | ) | | | — | | | | — | | | | (0.07 | ) | | | 0.05 | | | | 0.33 | | | | 0.03 | | | | 0.00 | | | | 0.17 | |

Enterprises | | | 0.74 | | | | 0.62 | | | | 0.04 | | | | (0.02 | ) | | | 1.25 | | | | (0.02 | ) | | | 0.09 | | | | (0.03 | ) | | | (0.11 | ) | | | (0.01 | ) |

Corporate interest and other | | | 0.16 | | | | (0.03 | ) | | | 0.04 | | | | 0.27 | | | | (0.32 | ) | | | (0.02 | ) | | | 0.01 | | | | * | | | | (0.01 | ) | | | * | |

Discontinued operations (income) loss | | | (0.16 | ) | | | 0.02 | | | | (0.07 | ) | | | (0.03 | ) | | | 0.40 | | | | (*) | | | | (0.08 | ) | | | 0.08 | | | | (0.01 | ) | | | (0.03 | ) |

Asset impairment charges, net | | | — | | | | — | | | | 1.82 | | | | 0.76 | | | | 0.60 | | | | — | | | | — | | | | — | | | | — | | | | — | |

Cumulative accounting changes | | | 0.16 | | | | 0.01 | | | | — | | | | — | | | | — | | | | — | | | | — | | | | — | | | | — | | | | — | |

| | |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

|

Adjusted earnings per share, including MTM - non-GAAP | | $ | 0.81 | | | $ | 0.87 | | | $ | 1.39 | | | $ | 0.57 | | | $ | 0.84 | | | | $1.21 | (a) | | $ | 1.26 | | | $ | 1.36 | | | $ | 1.45 | | | $ | 1.55 | |

Mark-to-market impacts | | | | | | | 0.03 | | | | (0.43 | ) | | | 0.51 | | | | | | | | | | | | | | | | | | | | | | | | | |

| | |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

|

Adjusted earnings per share, excluding MTM - non-GAAP | | | NA | | | $ | 0.90 | | | $ | 0.96 | | | $ | 1.08 | | | | NA | | | | NA | | | | NA | | | | NA | | | | NA | | | | NA | |

| | |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

|

| * | | Less than $500 thousand or $0.01 per share. |

| (a) | | $1.25 excluding discontinued Exeter operations and accounting changes related to convertible debt and restricted stock. |

2003-12 EPS

CMS Energy

Reconciliation of Gross Operating Cash Flow to GAAP Operating Activities

(unaudited)

(mils)

| | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | 2011

| | | 2012

| | | 2013

| | | 2014

| | | 2015

| | | 2016

| | | 2017

| |

Consumers Operating Income + Depreciation & Amortization | | $ | 1,527 | | | $ | 1,635 | | | $ | 1,735 | | | $ | 1,821 | | | $ | 1,948 | | | $ | 2,011 | | | $ | 2,113 | |

Enterprises Project Cash Flows | | | 24 | | | | 17 | | | | 20 | | | | 29 | | | | 37 | | | | 44 | | | | 56 | |

| | |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

|

Gross Operating Cash Flow | | $ | 1,551 | | | $ | 1,652 | | | $ | 1,755 | | | $ | 1,850 | | | $ | 1,985 | | | $ | 2,055 | | | $ | 2,169 | |

Other operating activities including taxes, interest payments and working capital | | | (382 | ) | | | (411 | ) | | | (405 | ) | | | (400 | ) | | | (435 | ) | | | (805 | ) | | | (819 | ) |

| | |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

|

Net cash provided by operating activities | | $ | 1,169 | | | $ | 1,241 | | | $ | 1,350 | | | $ | 1,450 | | | $ | 1,550 | | | $ | 1,250 | | | $ | 1,350 | |

| | |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

|

2011-17 OCF

CMS Energy

2012 Reconciliation of Gross Operating Cash Flow to GAAP Operating Activities

(unaudited)

(mils)

| | | | |

| | | 2012

| |

Consumers Operating Income + Depreciation & Amortization | | $ | 1,635 | (a) |

Enterprises Project Cash Flows | | | 17 | |

| | |

|

|

|

Gross Operating Cash Flow | | $ | 1,652 | |

Other operating activities including taxes, interest payments and working capital | | | (411 | ) |

| | |

|

|

|

Net cash provided by operating activities | | $ | 1,241 | |

| | |

|

|

|

| (a) | | Excludes impact of $59 million electric decoupling write off |

2012 OCF

Consumers Energy

2013 Forecasted Cash Flow GAAP Reconciliation (in millions) (unaudited)

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | Reclassifications From Sources and Uses to Statement of Cash Flows

| | | |

Presentation Sources and Uses

| | | Tax

Sharing

Operating

| | | Interest

Payments

as

Operating

| | | Other

Working

Capital

as

Investing

| | | Capital

Lease

Pymts as

Financing

| | | Securitization

Debt Pymts

as

Financing

| | | Preferred

Dividends

as

Financing

| | | Common

Dividends

as

Financing

| | | Consolidated Statements of

Cash Flows

|

Description

| | non-GAAP

Amount

| | | | | | | | | | GAAP

Amount

| | | Description

|

Cash at year end 2012 | | $ | 5 | | | $ | — | | | $ | — | | | $ | — | | | $ | — | | | $ | — | | | $ | — | | | $ | — | | | $ | 5 | | | Cash at year end 2012 |

| | | | | | | | | | |

Sources | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Operating (dep & amort $620) | | $ | 1,735 | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Other working capital | | | (10) | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| | |

Sources | | $ | 1,725 | | | $ | (125 | ) | | $ | (228 | ) | | $ | (101 | ) | | $ | 28 | | | $ | 41 | | | $ | — | | | $ | — | | | $ | 1,340 | | | Net cash provided by operating activities |

| | | | | | | | | | |

Uses | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Interest and preferred dividends | | $ | (230) | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Pension Contribution | | | (49) | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Capital expendituresa | | | (1,375) | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Dividends/tax sharing to CMS | | | (540) | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| | |

Uses | | $ | (2,194) | | | $ | 125 | | | $ | 228 | | | $ | 101 | | | $ | — | | | $ | — | | | $ | 2 | | | $ | 415 | | | $ | (1,323 | ) | | Net cash provided by investing activities |

| | |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| | |

Cash flow | | $ | (469 | ) | | $ | — | | | $ | — | | | $ | — | | | $ | 28 | | | $ | 41 | | | $ | 2 | | | $ | 415 | | | $ | 17 | | | Cash flow from operating and investing activities |

| | | | | | | | | | |

Financing | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Equity | | $ | 150 | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

New Issues | | | 325 | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Retirements | | | — | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Net short-term financing & other | | | 15 | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| | |

Financing | | $ | 490 | | | $ | — | | | $ | — | | | $ | — | | | $ | (28 | ) | | $ | (41 | ) | | $ | (2 | ) | | $ | (415 | ) | | $ | 4 | | | Net cash provided by financing activities |

| | |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| | |

Net change in cash | | $ | 21 | | | $ | — | | | $ | — | | | $ | — | | | $ | — | | | $ | — | | | $ | — | | | $ | — | | | $ | 21 | | | Net change in cash |

| | |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| | |

Cash at year end 2013 | | $ | 26 | | | $ | — | | | $ | — | | | $ | — | | | $ | — | | | $ | — | | | $ | — | | | $ | — | | | $ | 26 | | | Cash at year end 2013 |

| | |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| | |

| a | | Includes cost of removal and capital leases |

2013 B-1

CMS Energy Parent

2013 Forecasted Cash Flow GAAP Reconciliation

(in millions) (unaudited)

| | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | Reclassifications From Sources and Uses to Statement of Cash Flows

| | | | | | |

Presentation Sources and Uses

| | | Interest | | | Overheads & | | | Other | | | Cash From | | | Consolidated Statements of

Cash Flows

|

Description

| | non-GAAP

Amount

| | | Payments

as Operating

| | | Tax Payments

as Operating

| | | Uses (a)

as Operating

| | | Consolidated

Companies

| | | GAAP

Amount

| | | Description

|

Cash at year end 2012 | | $ | 53 | | | $ | — | | | $ | — | | | $ | — | | | $ | 35 | | | $ | 88 | | | Cash at year end 2012 |

Sources | | | | | | | | | | | | | | | | | | | | | | | | | | |

Consumers Energy dividends/tax sharing | | $ | 540 | | | | | | | | | | | | | | | | | | | | | | | |

Enterprises | | | 20 | | | | | | | | | | | | | | | | | | | | | | | |

| | |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

Sources | | $ | 560 | | | $ | (135 | ) | | $ | (15 | ) | | $ | (6 | ) | | $ | 23 | | | $ | 427 | | | Net cash provided by operating activities |

Uses | | | | | | | | | | | | | | | | | | | | | | | | | | |

Interest and preferred dividends | | $ | (135 | ) | | | | | | | | | | | | | | | | | | | | | | |

Overhead and Federal tax payments | | | (15 | ) | | | | | | | | | | | | | | | | | | | | | | |

Equity infusions | | | (150 | ) | | | | | | | | | | | | | | | | | | | | | | |

Pension Contribution | | | (1 | ) | | | | | | | | | | | | | | | | | | | | | | |

| | |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| | |

Uses(a) | | $ | (315 | ) | | $ | 135 | | | $ | 15 | | | $ | 6 | | | $ | (86 | ) | | $ | (245 | ) | | Net cash provided by investing activities |

| | |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| | |

Cash flow | | $ | 245 | | | $ | — | | | $ | — | | | $ | — | | | $ | (63 | ) | | $ | 182 | | | Cash flow from operating and investing activities |

Financing and dividends | | | | | | | | | | | | | | | | | | | | | | | | | | |

New Issues | | $ | 250 | | | | | | | | | | | | | | | | | | | | | | | |

Retirements | | | — | | | | | | | | | | | | | | | | | | | | | | | |

Equity programs (DRP, continuous equity) | | | 30 | | | | | | | | | | | | | | | | | | | | | | | |

Net short-term financing & other | | | (5 | ) | | | | | | | | | | | | | | | | | | | | | | |

Common dividend | | | (270 | ) | | | | | | | | | | | | | | | | | | | | | | |

| | |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| | |

Financing | | $ | 5 | | | $ | — | | | $ | — | | | $ | — | | | $ | 72 | | | $ | 77 | | | Net cash provided by financing activities |

| | |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| | |

Net change in cash | | $ | 250 | | | $ | — | | | $ | — | | | $ | — | | | $ | 9 | | | $ | 259 | | | Net change in cash |

| | |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| | |

Cash at year end 2013 | | $ | 303 | | | $ | — | | | $ | — | | | $ | — | | | $ | 44 | | | $ | 347 | | | Cash at year end 2013 |

| | |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| | |

2013 B-2

Consolidated CMS Energy

2013 Forecasted Consolidation of Consumers Energy and CMS Energy Parent Statements of Cash Flow

(in millions) (unaudited)

| | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | Eliminations/Reclassifications to Arrive at the

Consolidated Statement of Cash Flows

| | | | | | |

Statements of Cash Flows

| | | Consumers | | | Consumers | | | Equity | | | Consolidated Statements of

Cash Flows

|

Description

| | Consumers

Amount

| | | CMS Parent

Amount

| | | Common Dividend

as Financing

| | | Preferred Dividend

as Operating

| | | Infusions to

Consumers

| | | Amount

| | | Description

|

Cash at year end 2012 | | $ | 5 | | | $ | 88 | | | $ | — | | | $ | — | | | $ | — | | | $ | 93 | | | Cash at year end 2012 |

Net cash provided by operating activities | | $ | 1,340 | | | $ | 427 | | | $ | (415 | ) | | $ | (2 | ) | | $ | — | | | $ | 1,350 | | | Net cash provided by operating activities |

Net cash provided by investing activities | | | (1,323 | ) | | | (245 | ) | | | — | | | | — | | | | 150 | | | | (1,418 | ) | | Net cash provided by investing activities |

| | |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| | |

Cash flow from operating and investing activities | | $ | 17 | | | $ | 182 | | | $ | (415 | ) | | $ | (2 | ) | | $ | 150 | | | $ | (68 | ) | | Cash flow from operating and investing activities |

Net cash provided by financing activities | | $ | 4 | | | $ | 77 | | | $ | 415 | | | $ | 2 | | | $ | (150 | ) | | $ | 348 | | | Net cash provided by financing activities |

| | |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| | |

Net change in cash | | $ | 21 | | | $ | 259 | | | $ | — | | | $ | — | | | $ | — | | | $ | 280 | | | Net change in cash |

| | |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| | |

Cash at year end 2013 | | $ | 26 | | | $ | 347 | | | $ | — | | | $ | — | | | $ | — | | | $ | 373 | | | Cash at year end 2013 |

| | |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| | |

2013 B-3