Exhibit 99.1

CMS ENERGY

Midwest Utilities Seminar

April 10, 2013

Cross Winds® Energy Park

Gas Combined Cycle Plant

Consumers Smart Energy Program

CMS ENERGY

This presentation is made as of the date hereof and contains “forward-looking statements” as defined in Rule 3b-6 of the

Securities Exchange Act of 1934, as amended, Rule 175 of the Securities Act of 1933, as amended, and relevant legal decisions. The forward-looking statements are subject to risks and uncertainties. They should be read in conjunction with “FORWARD-LOOKING STATEMENTS AND INFORMATION” and “RISK FACTORS” sections of CMS Energy’s and Consumers Energy’s Form 10-K for the year ended December 31 and as updated in subsequent 10-Qs. CMS Energy’s and Consumers Energy’s “FORWARD-LOOKING STATEMENTS AND INFORMATION” and “RISK FACTORS” sections are incorporated herein by reference and discuss important factors that could cause CMS Energy’s and Consumers Energy’s results to differ materially from those anticipated in such statements. CMS Energy and Consumers Energy undertake no obligation to update any of the information presented herein to reflect facts, events or circumstances after the date hereof.

The presentation also includes non-GAAP measures when describing CMS Energy’s results of operations and financial performance. A reconciliation of each of these measures to the most directly comparable GAAP measure is included in the appendix and posted on our website at www.cmsenergy.com.

CMS Energy provides financial results on both a reported (Generally Accepted Accounting Principles) and adjusted (non-GAAP) basis. Management views adjusted earnings as a key measure of the company’s present operating financial performance, unaffected by discontinued operations, asset sales, impairments, regulatory items from prior years, or other items. Certain of these items have the potential to impact, favorably or unfavorably, the company’s reported earnings in 2013. The company is not able to estimate the impact of these matters and is not providing reported earnings guidance.

1

CMS ENERGY

Model Delivers. . . .

Above Average Return

Future

Return

Attractive dividend yield 4%

62% payout ratio

EPS growth rate

5%-7%

Driven by $7 billion investment in regulated Utility over next five years

Shareowner return 9%-11%

EPSa Growth vs Peers

7% 5%-7% 6%

5% 4% 4%

CMS

Peers

CMS

Peers

Ten-Year Growth

Future

a Adjusted EPS (non-GAAP)

. . . . good, future return opportunity.

2

CMS ENERGY

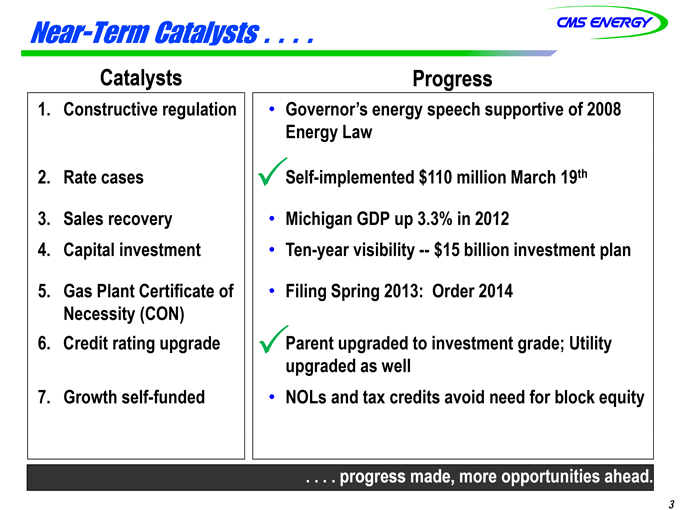

Near-Term Catalysts….

Catalysts

1. Constructive regulation

2. Rate cases

3. Sales recovery

4. Capital investment

5. Gas Plant Certificate of Necessity (CON)

6. Credit rating upgrade

7. Growth self-funded

Progress

• Governor’s energy speech supportive of 2008 Energy Law

Self-implemented $110 million March 19th

• Michigan GDP up 3.3% in 2012

• Ten-year visibility — $15 billion investment plan

• Filing Spring 2013: Order 2014

Parent upgraded to investment grade; Utility upgraded as well

• NOLs and tax credits avoid need for block equity

. . . . progress made, more opportunities ahead.

3

CMS ENERGY

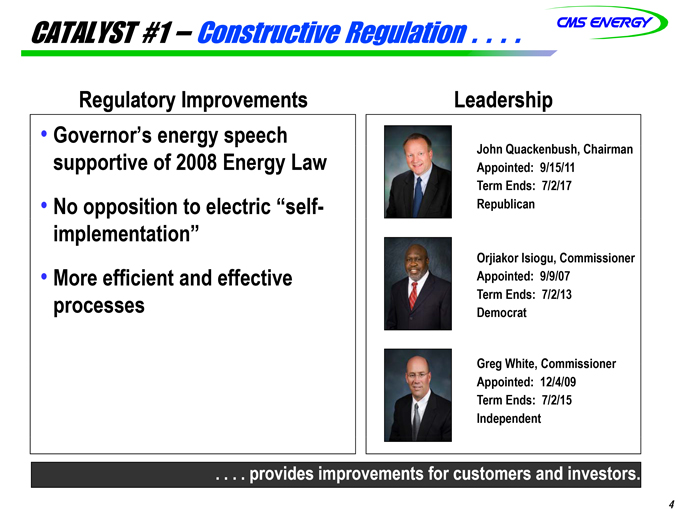

CATALYST #1 – Constructive Regulation . . . .

Regulatory Improvements

• Governor’s energy speech supportive of 2008 Energy Law

• No opposition to electric “self-implementation”

• More efficient and effective processes

Leadership

John Quackenbush, Chairman

Appointed: 9/15/11

Term Ends: 7/2/17

Republican

Orjiakor Isiogu, Commissioner

Appointed: 9/9/07

Term Ends: 7/2/13

Democrat

Greg White, Commissioner

Appointed: 12/4/09

Term Ends: 7/2/15

Independent

. . . . provides improvements for customers and investors.

4

CMS ENERGY

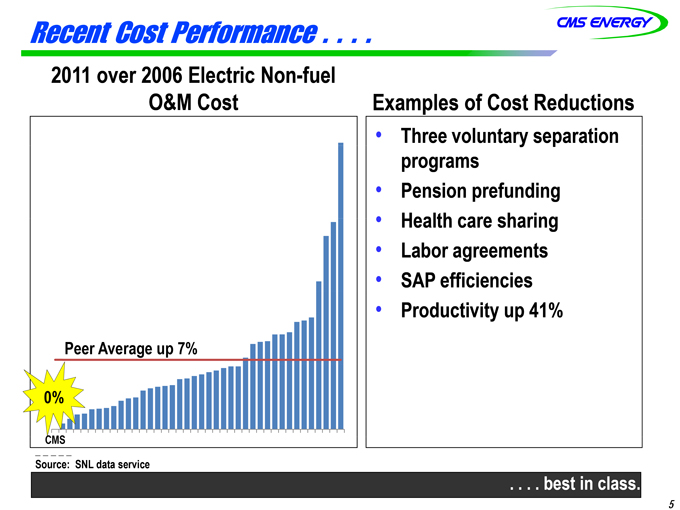

Recent Cost Performance . . . .

2011 over 2006 Electric Non-fuel O&M Cost

Peer Average up 7%

0%

CMS

Examples of Cost Reductions

• Three voluntary separation programs

• Pension prefunding

• Health care sharing

• Labor agreements

• SAP efficiencies

• Productivity up 41%

Source: SNL data service

. . . . best in class.

5

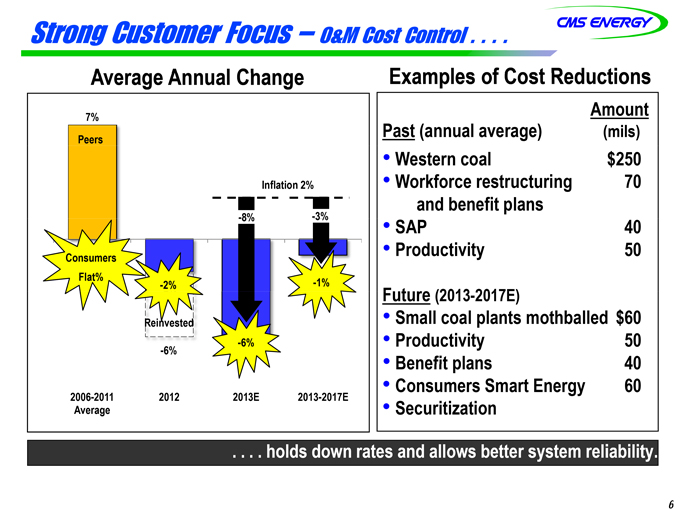

CMS ENERGY

Strong Customer Focus – O&M Cost Control . . . .

Average Annual Change

7%

Peers

Inflation 2%

-8%

-3%

Consumers

Flat%

-2%

-1%

Reinvested

-6%

-6%

2006-2011

2012

2013E

2013-2017E

Average

Examples of Cost Reductions

Amount

Past (annual average)

(mils)

Western coal

$250

Workforce restructuring and benefit plans

70

SAP

40

Productivity

50

Future (2013-2017E)

Small coal plants mothballed $60

Productivity

50

Benefit plans

40

Consumers Smart Energy

60

Securitization

. . . . holds down rates and allows better system reliability.

6

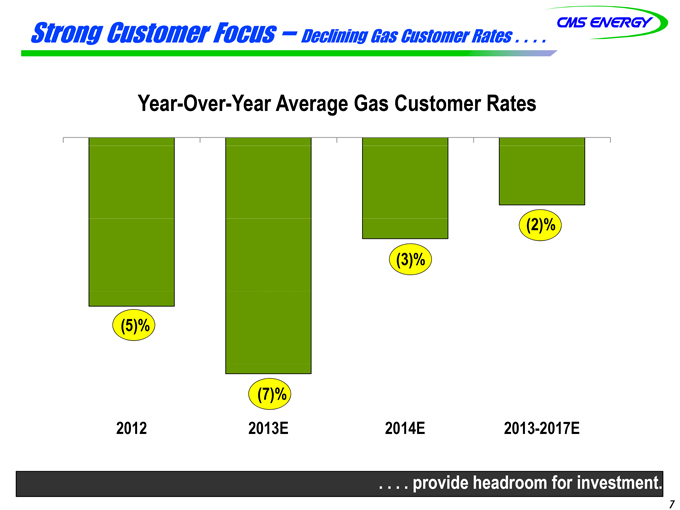

CMS ENERGY

Strong Customer Focus — Declining Gas Customer Rates . . . .

Year-Over-Year Average Gas Customer Rates

(2)%

(3)%

(5)%

(7)%

2012

2013E

2014E

2013-2017E

. . . . provide headroom for investment.

7

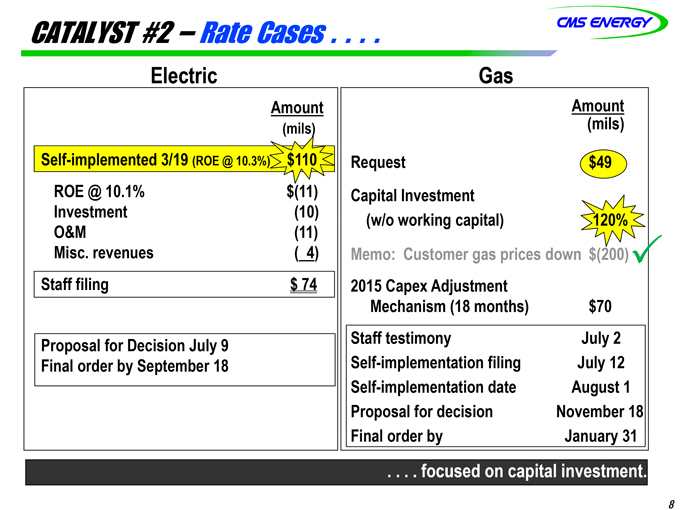

CMS ENERGY

CATALYST #2 – Rate Cases . . . .

Electric

Amount

(mils)

Self-implemented 3/19 (ROE @ 10.3%)

$110

ROE @ 10.1%

$(11)

Investment

(10)

O&M

(11)

Misc. revenues

( 4)

Staff filing

$ 74

Proposal for Decision July 9

Final order by September 18

Gas

Amount

(mils)

Request $49

Capital Investment (w/o working capital) 120%

Memo: Customer gas prices down $(200)

2015 Capex Adjustment Mechanism (18 months) $70

Staff testimony July 2

Self-implementation filing July 12

Self-implementation date August 1

Proposal for decision November 18

Final order by January 31

. . . . focused on capital investment.

8

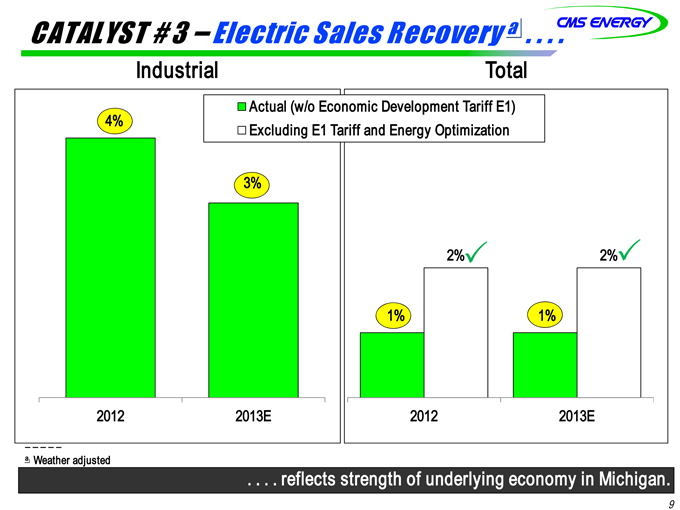

CMS ENERGY

CATALYST #3 – Electric Sales Recovery a . . . .

Industrial

Total

Actual (w/o Economic Development Tariff E1)

4%

Excluding E1 Tariff and Energy Optimization

3%

2%

2%

1%

1%

2012

2013E

2012

2013E

_ _ _ _ _

a Weather adjusted

. . . . reflects strength of underlying economy in Michigan.

9

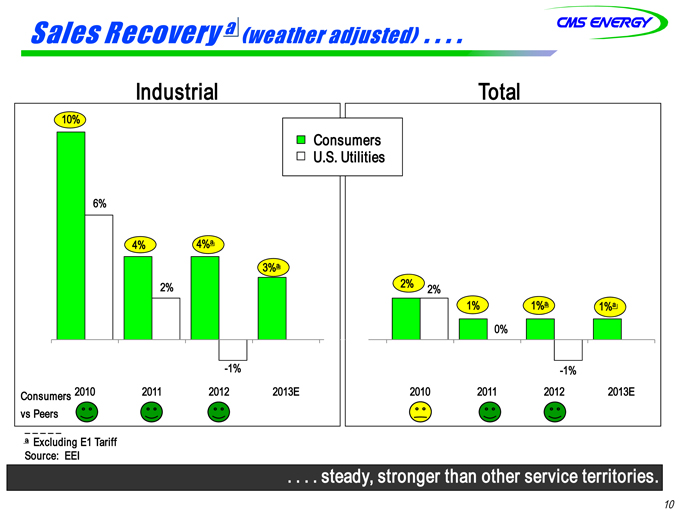

CMS ENERGY

Sales Recovery a

(weather adjusted) . . . .

Industrial

Total

10%

Consumers

U.S. Utilities

6%

4%

4%a

3%a

2%

2%

2%

1%

1%a

1%a

0%

-1%

-1%

Consumers 2010

2011

2012

2013E

2010

2011

2012

2013E

vs Peers

_ _ _ _ _

a Excluding E1 Tariff Source: EEI

. . . . steady, stronger than other service territories.

10

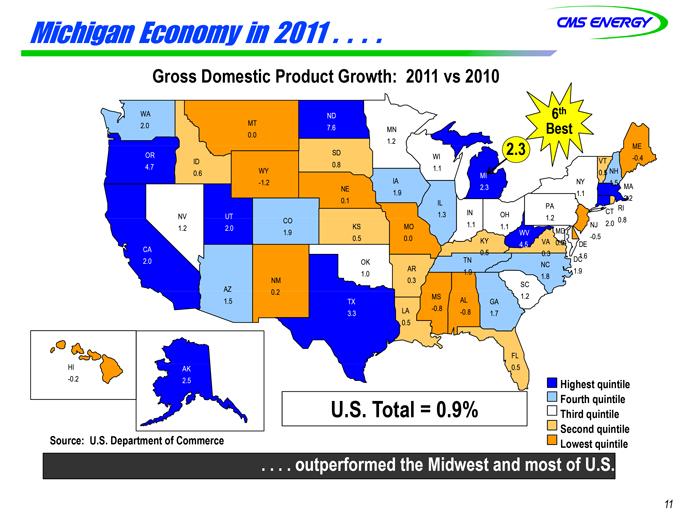

CMS ENERGY

Michigan Economy in 2011 . . . .

Gross Domestic Product Growth: 2011 vs 2010

WA

MT ND

2.0 7.6

MN

6th Best

0.0

1.2

SD 2.3 ME

WI -0.4

ID VT

0.8

WY 1.1 NH

0.6 MI 0.5

-1.2 IA NY 1.5

NE 2.3 MA

1.9 1.1

0.1 2.2

IL PA

RI

1.3 IN OH CT

NV UT 1.2 0.8

CO 2.0

KS MO 1.1 1.1 NJ

1.2 2.0 MD

1.9 WV

0.5 0.0 -0.5

KY VA 0.9 DE

4.5

0.5

0.3 1.6

OK TN DC

NC

AR 1.9 1.9

1.0 1.8

NM 0.3

SC

AZ 0.2 MS 1.2

1.5 TX AL GA

LA -0.8 -0.8

3.3 1.7

0.5

FL

HI AK 0.5

OR 4.7 CA 2.0

-0.2 2.5 Highest quintile

U.S. Total = 0.9% Fourth quintile

Third quintile

Second quintile

Source: U.S. Department of Commerce Lowest quintile

. . . . outperformed the Midwest and most of U.S.

11

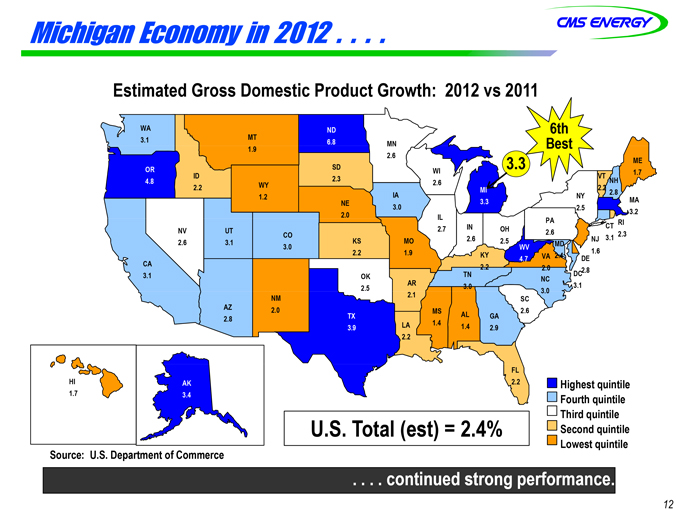

CMS ENERGY

Michigan Economy in 2012 . . . .

Estimated Gross Domestic Product Growth: 2012 vs 2011

WA ND 6th 3.1 MT

1.9 6.8 MN Best 2.6

SD 3.3 ME OR WI 1.7 ID 2.3 VT

4.8 2.6 NH 2.2 WY 2.2 MI 2.8 1.2 IA NY

NE 3.0 3.3 MA 2.5 2.0 3.2 IL PA

RI 2.7 IN OH CT

NV UT 2.6 2.3 CO 3.1 KS MO 2.6 2.5 NJ

2.6 3.1 MD 3.0 WV

2.2 1.9 1.6 KY VA 2.4 DE

4.7 CA 2.2

2.0 2.8 3.1 OK TN DC

NC

AR 3.0 3.1 2.5 2.1 3.0

NM SC AZ 2.0 2.6 MS AL

2.8 TX 1.4 GA 3.9 LA 1.4 2.9 2.2

FL

HI AK 2.2 Highest quintile

1.7 3.4

Fourth quintile Third quintile

U.S. Total (est) = 2.4% Second quintile

Source: U.S. Department of Commerce Lowest quintile

. . . . continued strong performance.

12

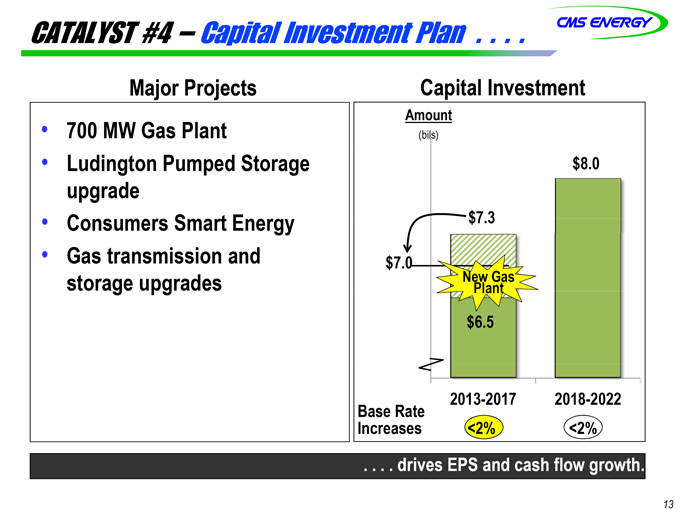

CMS ENERGY

CATALYST #4 – Capital Investment Plan . . . .

Major Projects

• 700 MW Gas Plant

• Ludington Pumped Storage upgrade

• Consumers Smart Energy

• Gas transmission and storage upgrades

Capital Investment

Amount

(bils)

$8.0

$7.3

$7.0

New Gas

Plant

$6.5

2013-2017

2018-2022

Base Rate

Increases

<2%

<2%

. . . . drives EPS and cash flow growth.

13

CMS ENERGY

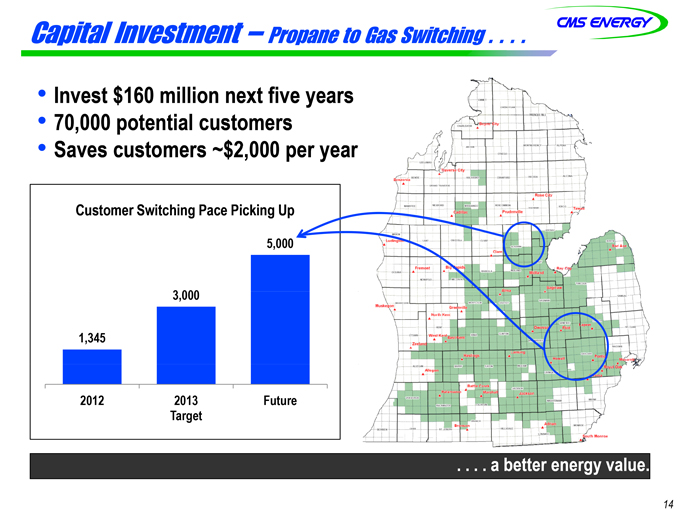

Capital Investment – Propane to Gas Switching . . . .

• Invest $160 million next five years

• 70,000 potential customers

• Saves customers ~$2,000 per year

Customer Switching Pace Picking Up

5,000 3,000 1,345

2012 2013 Future Target

. . . . a better energy value.

14

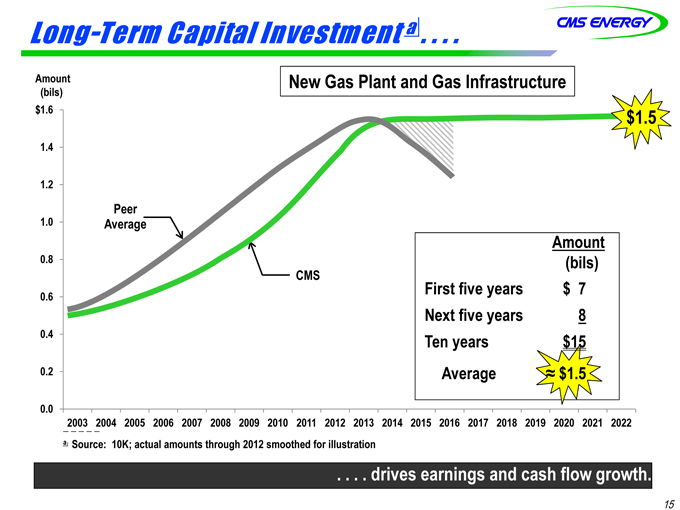

CMS ENERGY

Long-Term Capital Investment a . . . .

Amount New Gas Plant and Gas Infrastructure

(bils) $1.6 $1.5 1.4

1.2

Peer 1.0 Average

Amount 0.8 (bils)

CMS

First five years $ 7

0.6

Next five years 8 0.4 Ten years $15 0.2 Average ≈$1.5

0.0

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022

a Source: 10K; actual amounts through 2012 smoothed for illustration

. . . . drives earnings and cash flow growth.

15

CMS ENERGY

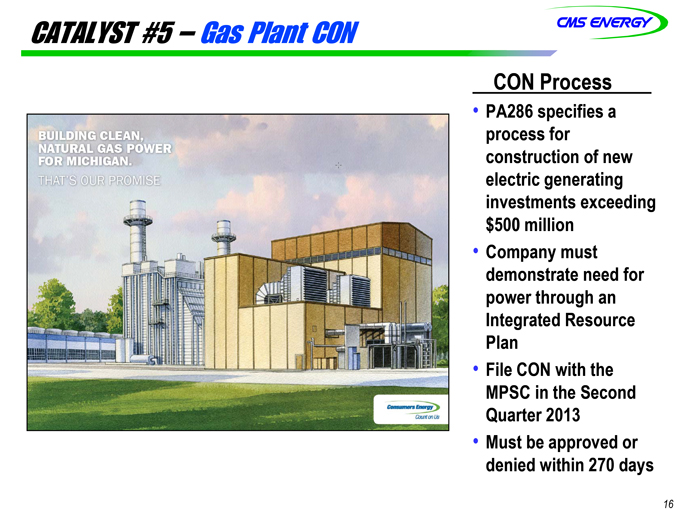

CATALYST #5 – Gas Plant CON

BUILDING CLEAN, NATURAL GAS POWER FOR MICHIGAN.

THAT’S OUR PROMISE

CON Process

• PA286 specifies a process for construction of new electric generating investments exceeding $500 million

• Company must demonstrate need for power through an Integrated Resource Plan

• File CON with the MPSC in the Second Quarter 2013

• Must be approved or denied within 270 days

16

CMS ENERGY

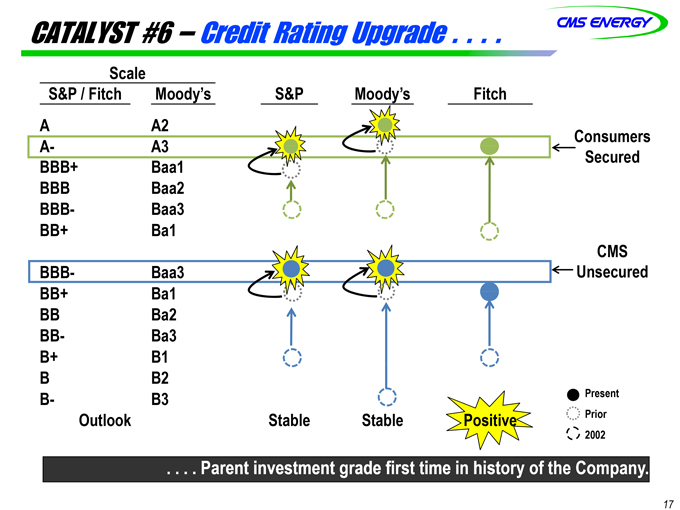

CATALYST #6 – Credit Rating Upgrade . . . .

Scale

S&P / Fitch

Moody’s

S&P

Moody’s

Fitch

A

A2

A-

A3

Consumers

BBB+

Baa1

Secured

BBB

Baa2

BBB-

Baa3

BB+

Ba1

CMS

BBB-

Baa3

Unsecured

BB+

Ba1

BB

Ba2

BB-

Ba3

B+

B1

B

B2

B-

B3

Present

Outlook

Stable

Stable

Positive

Prior

2002

. . . . Parent investment grade first time in history of the Company.

17

CMS ENERGY

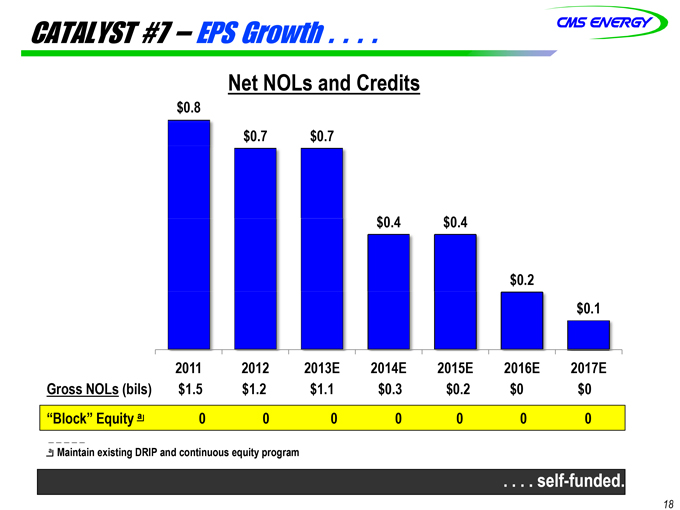

CATALYST #7 – EPS Growth . . . .

Net NOLs and

Credits

$0.8

$0.7

$0.7

$0.4

$0.4

$0.2

$0.1

2011

2012

2013E

2014E

2015E

2016E

2017E

Gross NOLs (bils)

$1.5

$1.2

$1.1

$0.3

$0.2

$0

$0

“Block” Equity a

0

0

0

0

0

0

0

a Maintain existing DRIP and continuous equity program

. . . . self-funded.

18

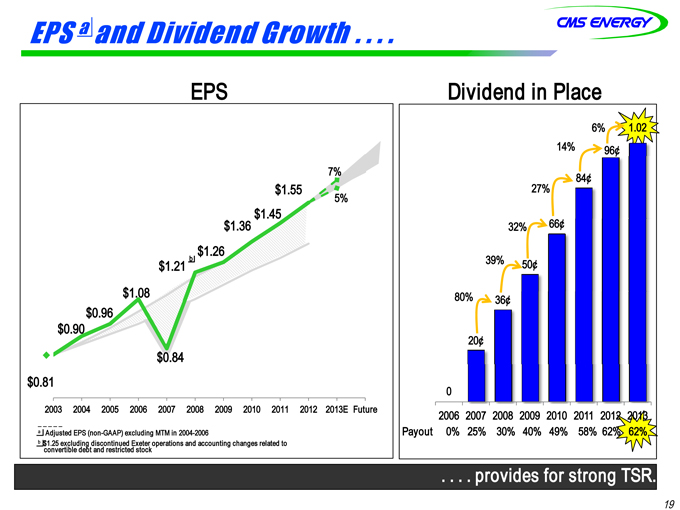

CMS ENERGY

EPS a and Dividend Growth . . . .

EPS

Dividend in Place

6%

1.02

14%

96¢

7%

84¢

$1.55

27%

5%

$1.45

$1.36

32%

66¢

$1.26

$1.21 b

39%

50¢

$1.08

80%

36¢

$0.96

$0.90

20¢

$0.84

$0.81

0

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013E Future

2006

2007

2008

2009

2010

2011

2012

2013

a Adjusted EPS (non-GAAP) excluding MTM in 2004-2006

Payout

0%

25%

30%

40%

49%

58%

62%

62%

b $1.25 excluding discontinued Exeter operations and accounting changes related to convertible debt and restricted stock

. . . . provides for strong TSR.

19

CMS ENERGY

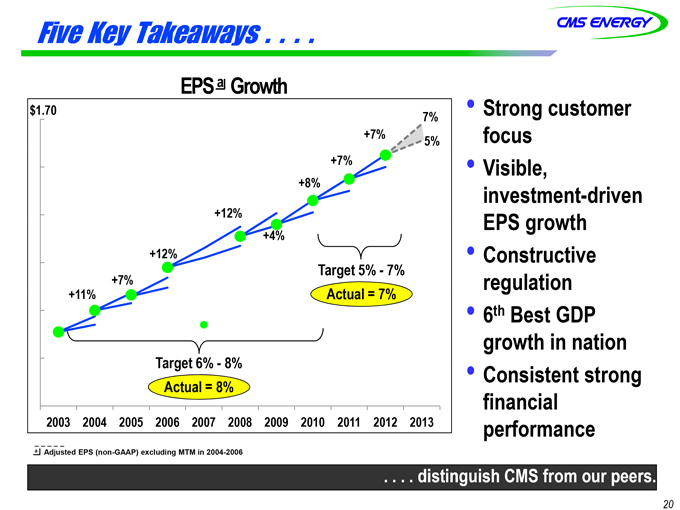

Five Key Takeaways . . . .

EPS a Growth

$1.70

Strong customer

7%

+7%

5%

focus

+7%

Visible,

+8%

investment-driven

+12%

EPS growth

+4%

+12%

Constructive

Target 5% - 7%

+7%

regulation

+11%

Actual = 7%

6th Best GDP

growth in nation

Target 6% - 8%

Consistent strong

Actual = 8%

financial

2003 2004

2005

2006 2007 2008 2009

2010

2011 2012

2013

performance

a Adjusted EPS (non-GAAP) excluding MTM in 2004-2006

. . . . distinguish CMS from our peers.

20

APPENDIX

CMS ENERGY

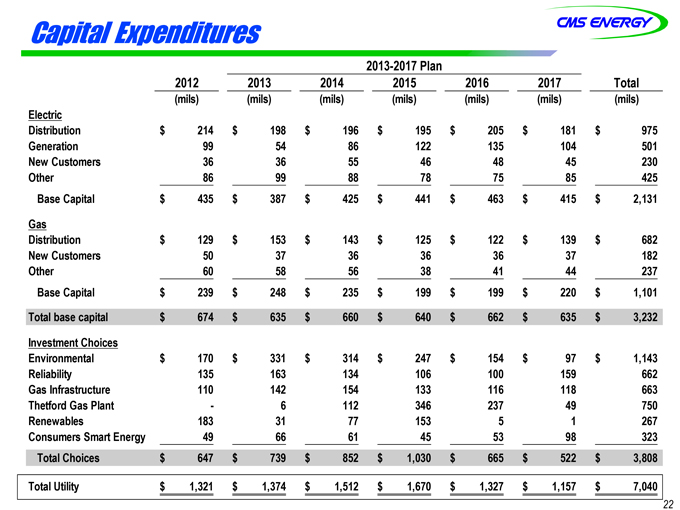

Capital Expenditures

2013-2017 Plan

2012

2013

2014

2015

2016

2017

Total

(mils)

(mils)

(mils)

(mils)

(mils)

(mils)

(mils)

Electric

Distribution

$214

$198

$196

$195

$205

$181

$975

Generation

99

54

86

122

135

104

501

New Customers

36

36

55

46

48

45

230

Other

86

99

88

78

75

85

425

Base Capital

$435

$387

$425

$441

$463

$415

$2,131

Gas

Distribution

$129

$153

$143

$125

$122

$139

$682

New Customers

50

37

36

36

36

37

182

Other

60

58

56

38

41

44

237

Base Capital

$239

$248

$235

$199

$199

$220

$1,101

Total base capital

$674

$635

$660

$640

$662

$635

$3,232

Investment Choices

Environmental

$170

$331

$314

$247

$154

$97

$1,143

Reliability

135

163

134

106

100

159

662

Gas Infrastructure

110

142

154

133

116

118

663

Thetford Gas Plant

-

6

112

346

237

49

750

Renewables

183

31

77

153

5

1

267

Consumers Smart Energy

49

66

61

45

53

98

323

Total Choices

$647

$739

$852

$1,030

$665

$522

$3,808

Total Utility

$1,321

$1,374

$1,512

$1,670

$1,327

$1,157

$7,040

22

CMS ENERGY

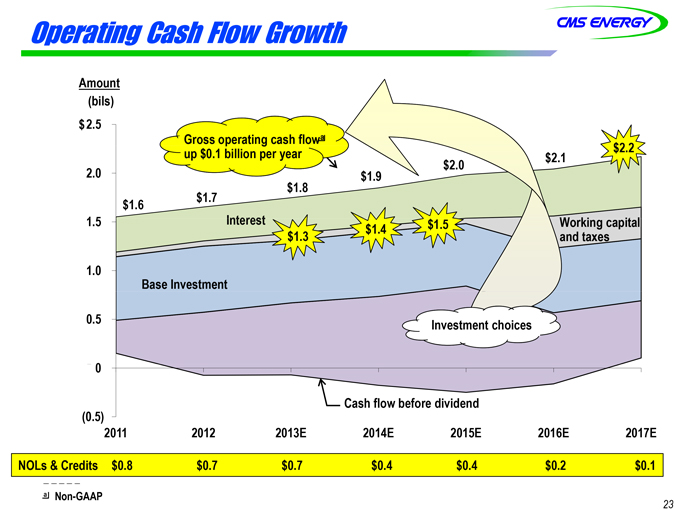

Operating Cash Flow Growth

Amount

(bils)

$2.5

Gross operating cash flow a

up $0.1 billion per year

$2.2

$2.1

2.0

$2.0

$1.9

$1.8

$1.6

$1.7

1.5

Interest

$1.4

$1.5

Working capital and

$1.3

taxes

1.0

Base Investment

0.5

Investment choices

0

Cash flow before dividend

(0.5)

2011

2012

2013E

2014E

2015E

2016E

2017E

NOLs & Credits

$0.8

$0.7

$0.7

$0.4

$0.4

$0.2

$0.1

a Non-GAAP

23

CMS ENERGY

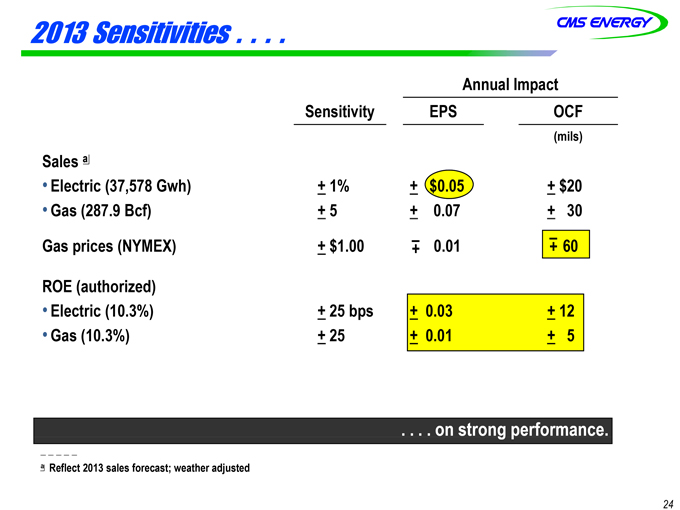

2013 Sensitivities . . . .

Annual Impact

Sensitivity EPS OCF (mils)

Sales a

• Electric (37,578 Gwh) ± 1% ± $0.05 ± $20

• Gas (287.9 Bcf) ± 5 ± 0.07 ± 30

Gas prices (NYMEX) ± $1.00 -+ 0.01 -+ 60

ROE (authorized)

• Electric (10.3%) ± 25 bps ± 0.03 ± 12

• Gas (10.3%) ± 25 ± 0.01 ± 5

. . . . on strong performance.

_ _ _ _ _

a Reflect 2013 sales forecast; weather adjusted

24

GAAP Reconciliation

CMS ENERGY CORPORATION

Earnings Per Share By Year GAAP Reconciliation

(Unaudited)

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | 2003

| | | 2004

| | | 2005

| | | 2006

| | | 2007

| | | 2008

| | | 2009

| | | 2010

| | | 2011

| | | 2012

| |

Reported earnings (loss) per share - GAAP | | ($ | 0.30 | ) | | $ | 0.64 | | | ($ | 0.44 | ) | | ($ | 0.41 | ) | | ($ | 1.02 | ) | | $ | 1.20 | | | $ | 0.91 | | | $ | 1.28 | | | $ | 1.58 | | | $ | 1.42 | |

| | |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

|

After-tax items: | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Electric and gas utility | | | 0.21 | | | | (0.39 | ) | | | — | | | | — | | | | (0.07 | ) | | | 0.05 | | | | 0.33 | | | | 0.03 | | | | 0.00 | | | | 0.17 | |

Enterprises | | | 0.74 | | | | 0.62 | | | | 0.04 | | | | (0.02 | ) | | | 1.25 | | | | (0.02 | ) | | | 0.09 | | | | (0.03 | ) | | | (0.11 | ) | | | (0.01 | ) |

Corporate interest and other | | | 0.16 | | | | (0.03 | ) | | | 0.04 | | | | 0.27 | | | | (0.32 | ) | | | (0.02 | ) | | | 0.01 | | | | * | | | | (0.01 | ) | | | * | |

Discontinued operations (income) loss | | | (0.16 | ) | | | 0.02 | | | | (0.07 | ) | | | (0.03 | ) | | | 0.40 | | | | ( | *) | | | (0.08 | ) | | | 0.08 | | | | (0.01 | ) | | | (0.03 | ) |

Asset impairment charges, net | | | — | | | | — | | | | 1.82 | | | | 0.76 | | | | 0.60 | | | | — | | | | — | | | | — | | | | — | | | | — | |

Cumulative accounting changes | | | 0.16 | | | | 0.01 | | | | — | | | | — | | | | — | | | | — | | | | — | | | | — | | | | — | | | | — | |

| | |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

|

Adjusted earnings per share, including MTM - non-GAAP | | $ | 0.81 | | | $ | 0.87 | | | $ | 1.39 | | | $ | 0.57 | | | $ | 0.84 | | | $ | 1.21 | (a) | | $ | 1.26 | | | $ | 1.36 | | | $ | 1.45 | | | $ | 1.55 | |

Mark-to-market impacts | | | | | | | 0.03 | | | | (0.43 | ) | | | 0.51 | | | | | | | | | | | | | | | | | | | | | | | | | |

| | |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

|

Adjusted earnings per share, excluding MTM - non-GAAP | | | NA | | | $ | 0.90 | | | $ | 0.96 | | | $ | 1.08 | | | | NA | | | | NA | | | | NA | | | | NA | | | | NA | | | | NA | |

| | |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

|

| * | | Less than $500 thousand or $0.01 per share. |

| (a) | | $1.25 excluding discontinued Exeter operations and accounting changes related to convertible debt and restricted stock. |

2003-12 EPS

CMS Energy

Reconciliation of Gross Operating Cash Flow to GAAP Operating Activities

(unaudited)

(mils)

| | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | 2011

| | | 2012

| | | 2013

| | | 2014

| | | 2015

| | | 2016

| | | 2017

| |

Consumers Operating Income + Depreciation & Amortization | | $ | 1,527 | | | $ | 1,635 | | | $ | 1,735 | | | $ | 1,821 | | | $ | 1,948 | | | $ | 2,011 | | | $ | 2,113 | |

Enterprises Project Cash Flows | | | 24 | | | | 17 | | | | 20 | | | | 29 | | | | 37 | | | | 44 | | | | 56 | |

| | |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

|

Gross Operating Cash Flow | | $ | 1,551 | | | $ | 1,652 | | | $ | 1,755 | | | $ | 1,850 | | | $ | 1,985 | | | $ | 2,055 | | | $ | 2,169 | |

Other operating activities including taxes, interest payments and working capital | | | (382 | ) | | | (411 | ) | | | (405 | ) | | | (400 | ) | | | (435 | ) | | | (805 | ) | | | (819 | ) |

| | |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

|

Net cash provided by operating activities | | $ | 1,169 | | | $ | 1,241 | | | $ | 1,350 | | | $ | 1,450 | | | $ | 1,550 | | | $ | 1,250 | | | $ | 1,350 | |

| | |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

|

2011-17 OCF

CMS Energy

2012 Reconciliation of Gross Operating Cash Flow to GAAP Operating Activities

(unaudited)

(mils)

| | | | |

| | | 2012

| |

Consumers Operating Income + Depreciation & Amortization | | $ | 1,635 | (a) |

Enterprises Project Cash Flows | | | 17 | |

| | |

|

|

|

Gross Operating Cash Flow | | $ | 1,652 | |

Other operating activities including taxes, interest payments and working capital | | | (411 | ) |

| | |

|

|

|

Net cash provided by operating activities | | $ | 1,241 | |

| | |

|

|

|

| (a) | | Excludes impact of $59 million electric decoupling write off |

2012 OCF