Exhibit 99.1

|

Second Quarter 2016 Results & Outlook July 28, 2016

Jackson Generating Station Ludington Pumped Storage Cross Winds âEnergy Park

Among lowest acquisition cost ever Fourth largest in the world #2 in renewable sales in the Great Lakes area

|

This presentation is made as of the date hereof and contains “forward-looking statements” as defined in Rule 3b-6 of the

Securities Exchange Act of 1934, Rule 175 of the Securities Act of 1933, and relevant legal decisions. The forward-looking statements are subject to risks and uncertainties. All forward-looking statements should be considered in the context of the risk and other factors detailed from time to time in CMS Energy’s and Consumers Energy’s Securities and Exchange Commission filings. Forward-looking statements should be read in conjunction with “FORWARD-LOOKING STATEMENTS AND

INFORMATION” and “RISK FACTORS” sections of CMS Energy’s and Consumers Energy’s Form 10-K for the year ended

December 31, 2015 and as updated in subsequent 10-Qs. CMS Energy’s and Consumers Energy’s “FORWARD-LOOKING

STATEMENTS AND INFORMATION” and “RISK FACTORS” sections are incorporated herein by reference and discuss important factors that could cause CMS Energy’s and Consumers Energy’s results to differ materially from those anticipated in such statements. CMS Energy and Consumers Energy undertake no obligation to update any of the information presented herein to reflect facts, events or circumstances after the date hereof.

The presentation also includes non-GAAP measures when describing CMS Energy’s results of operations and financial performance. A reconciliation of each of these measures to the most directly comparable GAAP measure is included in the appendix and posted on our website at www.cmsenergy.com.

CMS Energy provides historical financial results on both a reported (GAAP) and adjusted (non-GAAP) basis and provides forward-looking guidance on an adjusted basis. Adjustments could include items such as, discontinued operations, asset sales, impairments, restructuring costs, regulatory items from prior years, or other items. Management views adjusted earnings as a key measure of the company’s present operating financial performance and uses adjusted earnings for external communications with analysts and investors. Internally, the company uses adjusted earnings to measure and assess performance. Because the company is not able to estimate the impact of specific line items, which have the potential to significantly impact, favorably or unfavorably, the company’s reported earnings in future periods, the company is not providing reported earnings guidance nor is it providing a reconciliation for the comparable future period earnings. The adjusted earnings should be considered supplemental information to assist in fully understanding our business results, rather than as a substitute for the reported earnings.

Investors and others should note that CMS Energy routinely posts important information on its website and considers the Investor Relations section, www.cmsenergy.com/investor-relations, a channel of distribution.

1 |

|

|

Overview

Second Quarter Results

First Half Checklist Consumers Energy Way

Financial Results & Outlook

Second Quarter; Full Year

Unique Model Brexit Impact

Patti Poppe President & CEO

Tom Webb

Executive VP & CFO

2 |

|

|

a

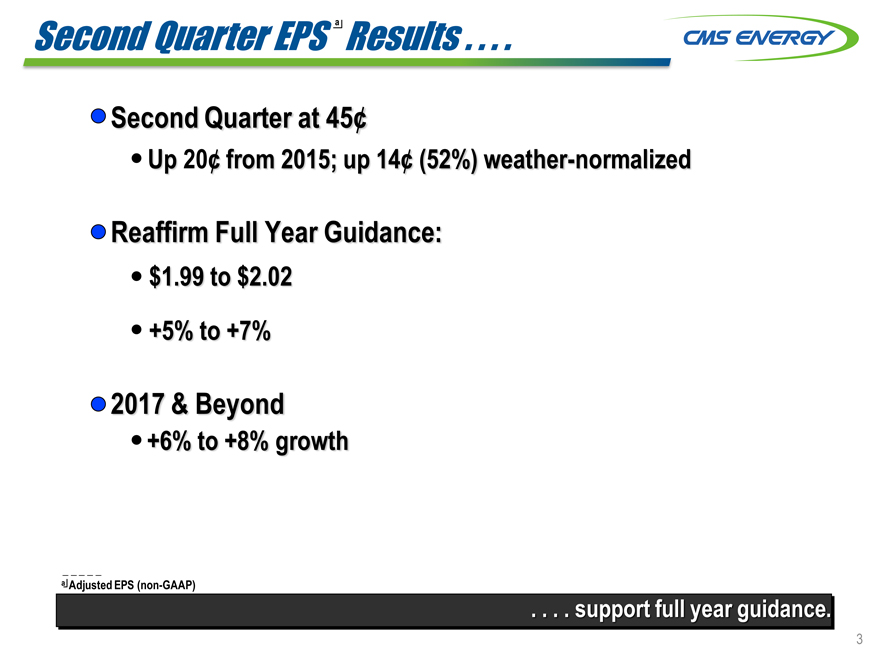

Second Quarter EPS Results . . . .

Second Quarter at 45¢

Up 20¢ from 2015; up 14¢ (52%) weather-normalized

Reaffirm Full Year Guidance:

$1.99 to $2.02 +5% to +7%

2017 & Beyond

+6% to +8% growth

a Adjusted EPS (non-GAAP)

. . . . support full year guidance.

3 |

|

|

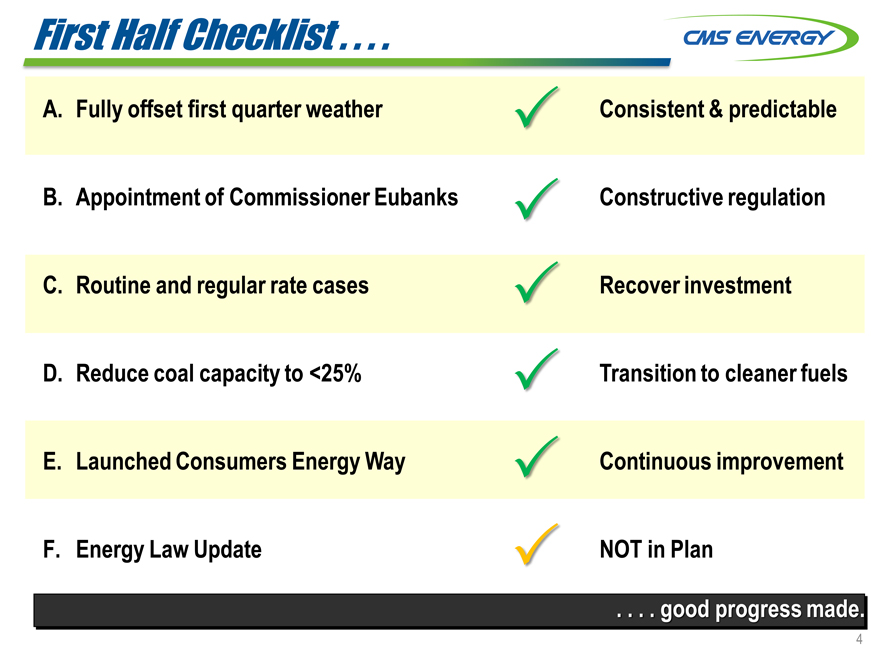

First Half Checklist . . . .

A. Fully offset first quarter weather

B. Appointment of Commissioner Eubanks C. Routine and regular rate cases D. Reduce coal capacity to <25% E. Launched Consumers Energy Way F. Energy Law Update

consistent & predictable constructive regulation recover investment transition to cleaner fuels continuous improvement NOT in Plan

. . .. good progress made.

4 |

|

|

Constructive Regulation . . . .

Commission

Sally Talberg (I) Chairman

Term Ends: July 2, 2019

Norm Saari (R)

Term Ends: July 2, 2021

Rachael Eubanks (I) Term Ends: July 2, 2017

Newly appointed!

Tier 1 State Ranking

Michigan

1 |

| 2 3 4 5 6 9 18 9 6 Barclays Research, 2016 state rankings |

. . . . is supported by a quality Commission and a strong existing Law.

5 |

|

|

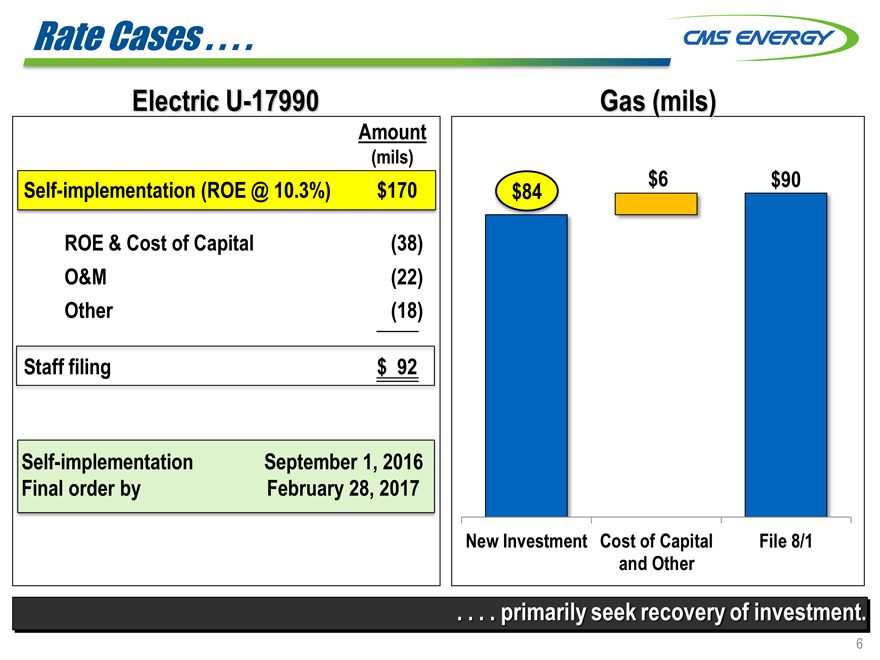

Rate Cases . . . .

Electric U-17990

Amount

(mils)

Self-implementation (ROE @ 10.3%) $170

ROE & Cost of Capital(38)

O&M(22)

Other(18)

Self-implementation September 1, 2016

Final order by February 28, 2017

Staff filing $92

Gas (mils)

$6 $90 $84 New Investment Cost of Capital File 8/1 and Other

. . . . primarily seek recovery of investment.

6 |

|

|

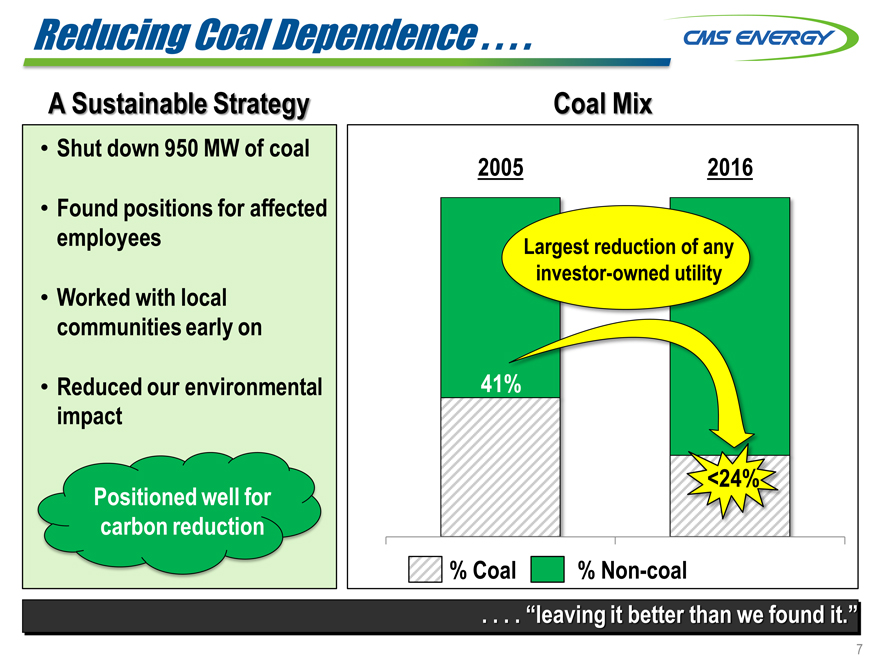

Reducing Coal Dependence . . . .

A Sustainable Strategy

Shut down 950 MW of coal

Found positions for affected employees

Worked with local communities early on

Reduced our environmental impact

Positioned well for carbon reduction

Coal Mix

2005 2016

Largest reduction of any investor-owned utility

41%

<24%

% Coal % Non-coal

. . . . “leaving it better than we found it.”

7 |

|

|

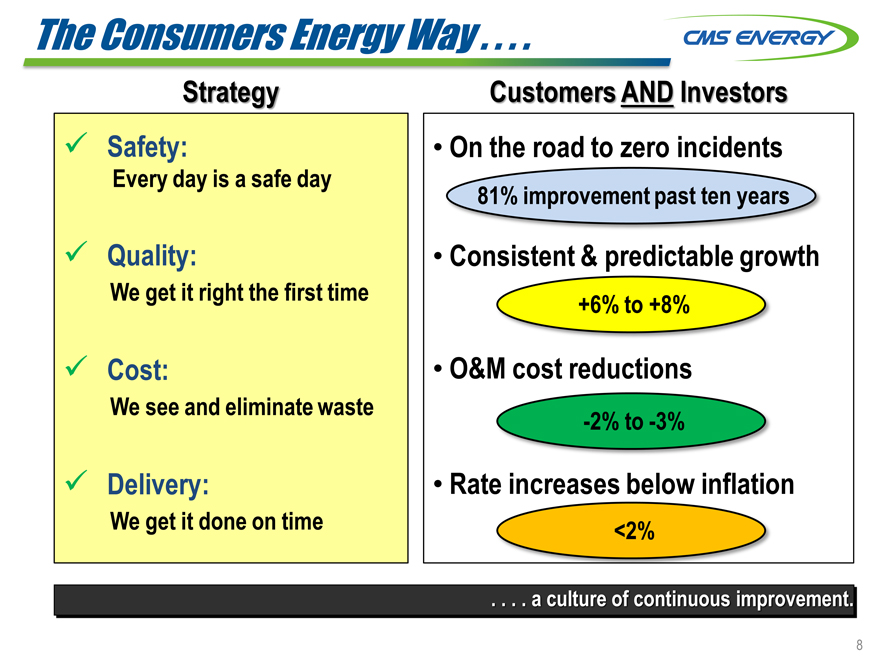

The Consumers Energy Way . . . .

Strategy Safety:

Every day is a safe day

Quality:

We get it right the first time

Cost:

We see and eliminate waste

Delivery:

We get it done on time

Customers AND Investors

On the road to zero incidents

81% improvement past ten years

Consistent & predictable growth

+6% to +8%

O&M cost reductions

-2% to -3%

Rate increases below inflation

<2%

. . . . a culture of continuous improvement.

8 |

|

|

O&M Cost Performance . . . .

Room to Improve

(Electric Distribution Cost Per Customer)

2014 2015

$30 mil to go until st Quartile 1st Quartile

2nd Quartile

Co ers

($97) Consumers

($100)

3rd Quartile Source: SNL, Form 1, Electric Non-fuel O&M, 2014 DCO normalized for Polar Vortex

Here’s How

Build the job as designed

Accurately schedule the job

“Field services” project

. . . . opportunities to improve even more.

9

|

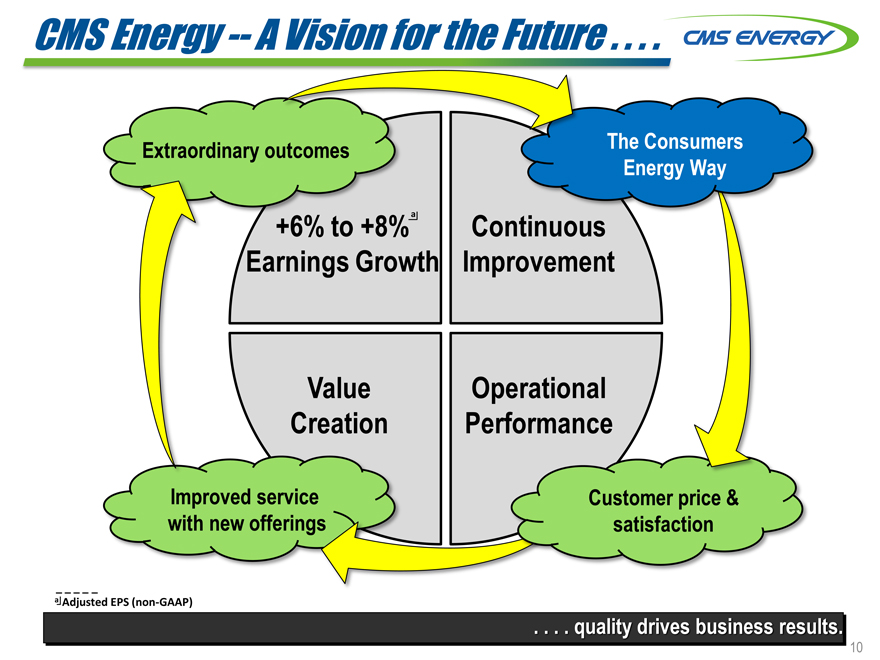

CMS Energy — A Vision for the Future . . . .

Extraordinary outcomes The Consumers Energy Way

a

+6% to +8% Continuous

Earnings Growth Improvement

Value Operational

Creation Performance

Improved service Customer price & with new offerings satisfaction

a Adjusted EPS (non-GAAP)

. . . . quality drives business results.

4th Quartile

10

|

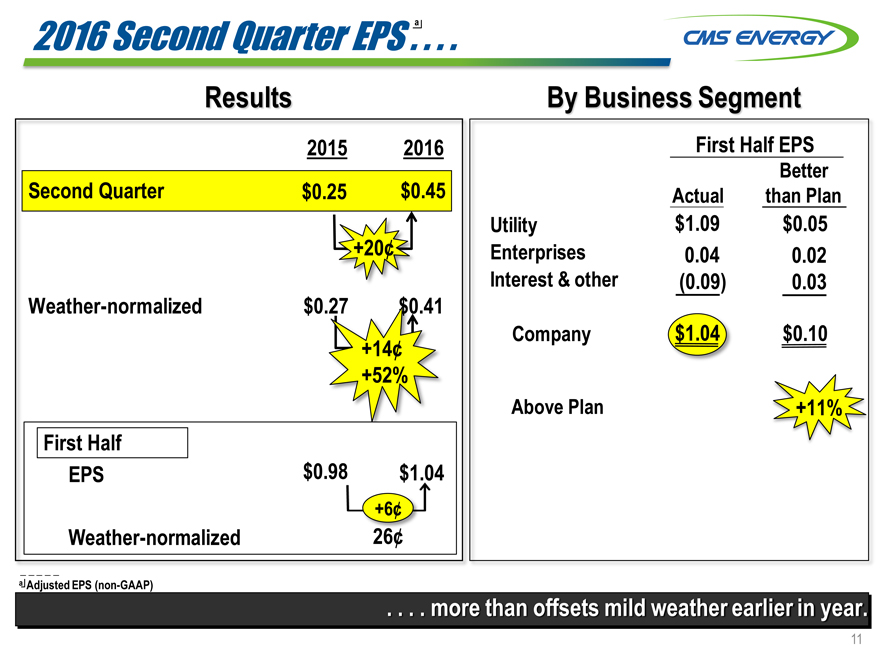

a

2016 Second Quarter EPS

Results

2015 2016

Second Quarter $0.25 $0.45

+20¢

$0.27

+14¢

$0.41 |

| +52% |

First Half

EPS $0.98 $1.04

+6¢

Weather-normalized 26¢

a Adjusted EPS (non-GAAP)

By Business Segment

First Half EPS

Better

Actual than Plan

Utility $1.09 $ 0.05

Enterprises 0.04 0.02

Interest & other(0.09) 0.03

Company $1.04 $ 0.10

Above Plan +11%

. . . . more than offsets mild weather earlier in year.

11

|

a

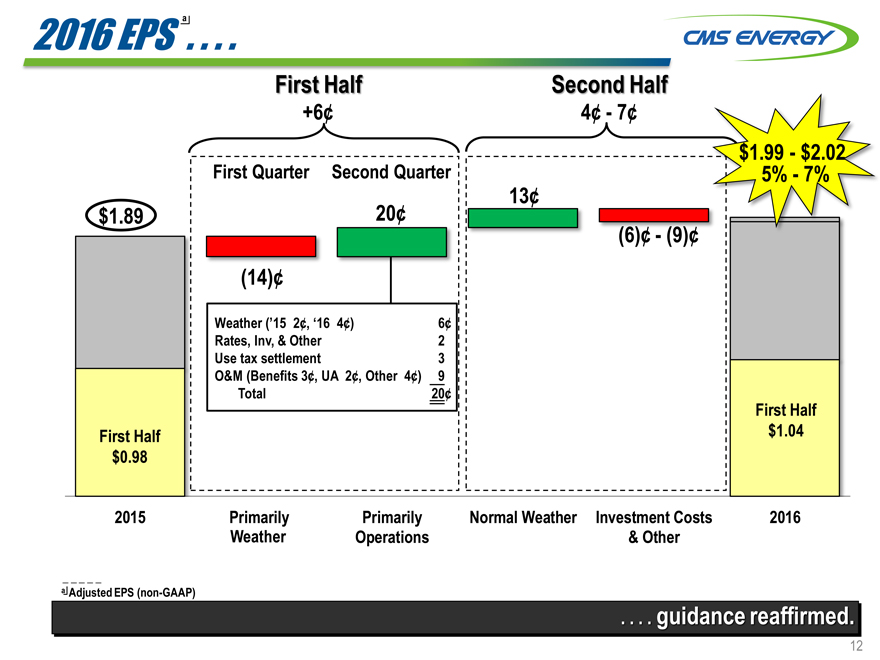

2016 EPS . . . .

First Half Second Half

+6¢ 4¢—7¢

$1.99—$2.02 |

|

First Quarter Second Quarter 5%—7%

13¢ |

|

$1.89 |

| 20¢ |

(6)¢—(9)¢ |

|

(14)¢ |

|

Weather (’15 2¢, ‘16 4¢) 6¢

Rates, Inv, & Other 2

Use tax settlement 3

O&M (Benefits 3¢, UA 2¢, Other 4¢) 9

Total 20¢

First Half

First Half $1.04

$0.98

2015 Primarily Primarily Normal Weather Investment Costs 2016

Weather Operations & Other

a Adjusted EPS (non-GAAP)

. . . . guidance reaffirmed.

12

|

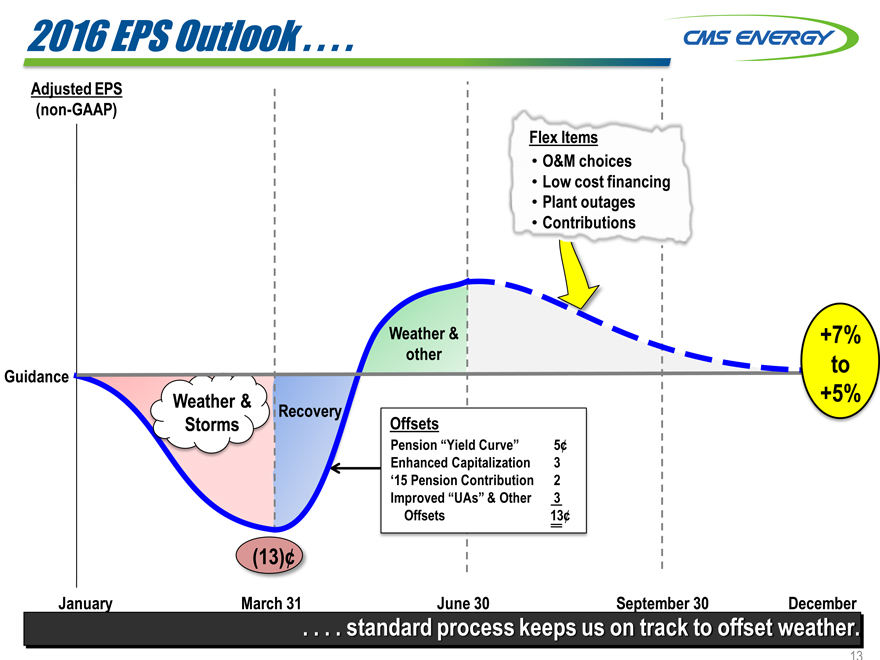

2016 EPS Outlook . . . .

Adjusted EPS

(non-GAAP)

Flex Items

O&M choices

Low cost financing

Plant outages

Contributions

Weather & +7%

other to

Guidance

Weather & +5%

Recovery

Storms Offsets

Pension “Yield Curve” 5¢

Enhanced Capitalization 3

‘15 Pension Contribution 2

Improved “UAs” & Other 3

Offsets 13¢

(13)¢ |

|

January March 31 June 30 September 30 December

. . . . standard process keeps us on track to offset weather.

13

|

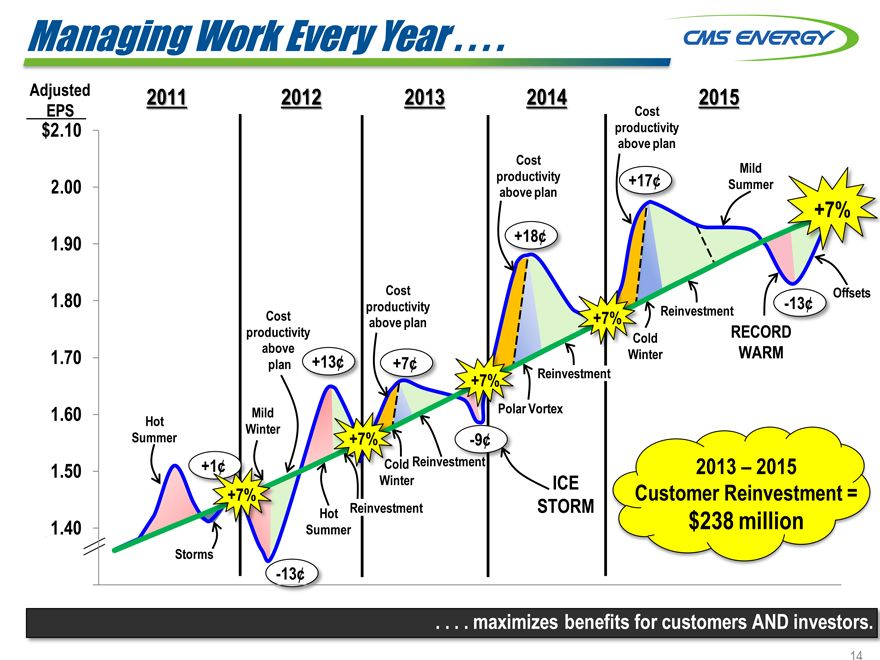

Managing Work Every Year . . . .

Adjusted 2011 2012 2013 2014 2015

EPS Cost

$2.10 |

| productivity |

above plan

Cost Mild

2.00 |

| productivity above plan +17¢ Summer |

+7%

1.90 |

| +18¢ |

1.80 |

| Cost -13¢ Offsets |

productivity Reinvestment

Cost above plan +7%

productivity ld RECORD

1.70 |

| above plan +13¢ +7¢ Winter WARM |

+7% Reinvestment

1.60 |

| Hot Mild r Vortex |

Winter

Summer +7% -9¢

1.50 |

| +1¢ ld Reinves 2013 – 2015 |

+7% Winter ICE Customer Reinvestment =

Reinvestment STORM

1.40 |

| Summer Hot $238 million |

Storms

-13¢

. . . . maximizes benefits for customers AND investors.

14

|

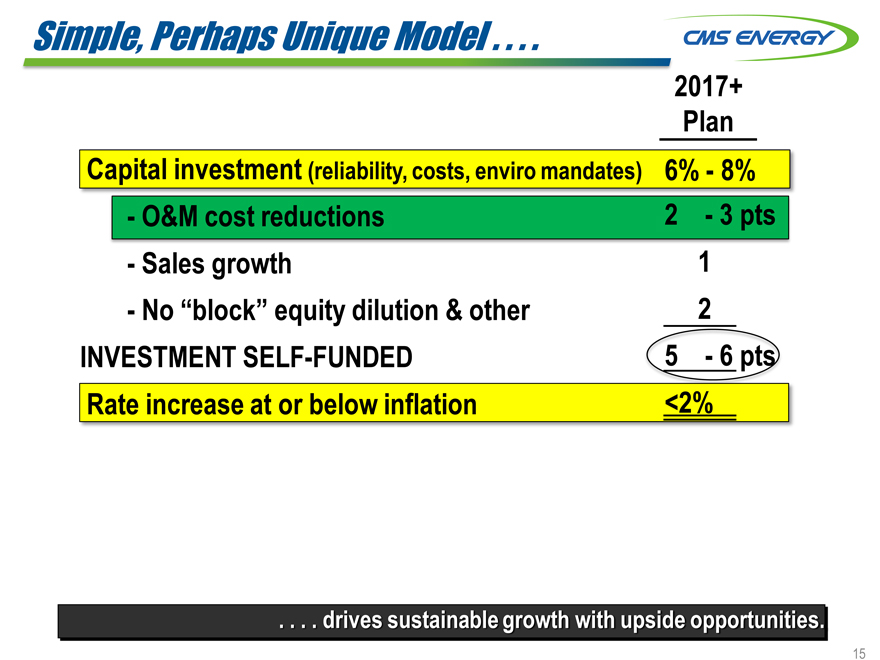

Simple, Perhaps Unique Model . . . .

2017+

Plan

Capital investment (reliability, costs, enviro mandates) 6%—8%

- O&M cost reductions 2—3 pts

- Sales growth 1

- No “block” equity dilution & other 2

INVESTMENT SELF-FUNDED 5—6 pts

Rate increase at or below inflation <2%

. . . .. drives sustainable growth with upside opportunities.

15

|

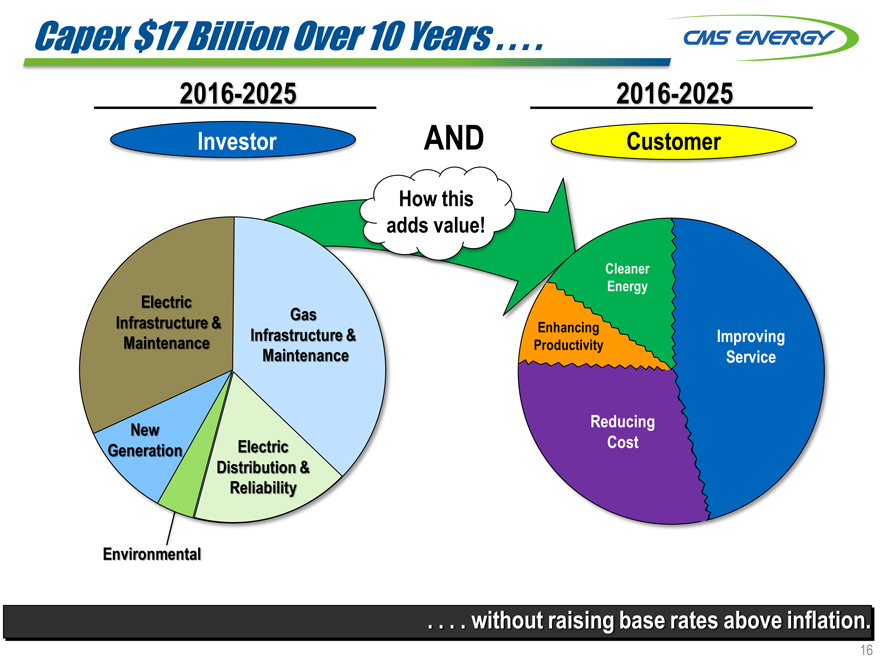

Capex $17 Billion Over 10 Years . . . .

2016-2025 2016-2025

Investor AND Customer

How this

adds value!

Cleaner

Energy

Electric

Gas

Infrastructure & Enhancing

Maintenance Infrastructure & Productivity Improving

Maintenance Service

New Reducing

Generation Electric Cost

Distribution &

Reliability

Environmental

. . . . without raising base rates above inflation.

16

|

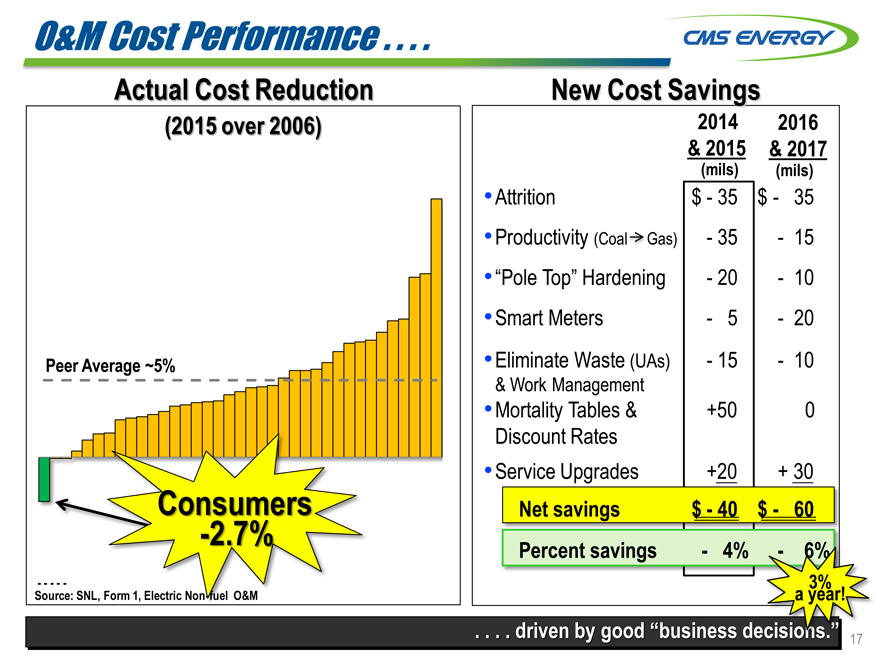

O&M Cost Performance . . . .

Actual Cost Reduction

(2015 over 2006)

Peer Average ~5%

Consumers -2.7%

Source: SNL, Form 1, Electric Non-fuel O&M

New Cost Savings

2014 2016

& 2015 & 2017

(mils)(mils)

Attrition $—35 $—35

Productivity (Coal Gas)—35—15

“Pole Top” Hardening—20—10

Smart Meters—5—20

Eliminate Waste (UAs)—15—10

& Work Management

Mortality Tables & +50 0

Discount Rates

Service Upgrades +20 + 30

Net savings $—40 $—60

Percent savings—4%

3%

a year!

. . . . driven by good “business decision.”

17

|

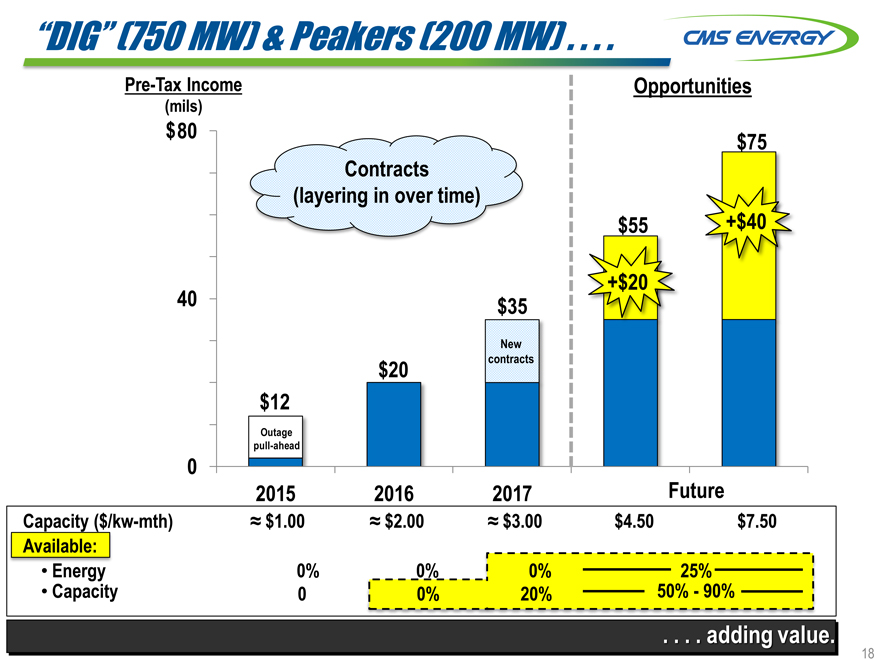

“DIG” (750 MW) & Peakers (200 MW) . . . .

Pre-Tax Income Opportunities

(mils)

$ 80 $75

Contracts

(layering in over time)

$55 +$40

+$20

40 |

| $35 |

New

$20 contracts

$12

Outage

pull-ahead

0

2015 2016 2017 Future

Capacity ($/kw-mth) ? $1.00 ? $2.00 ? $3.00 $4.50 $ 7.50

Available:

Energy 0% 0% 0% 25%

Capacity 0 0% 20% 50%—90%

. . . . adding value.

18

|

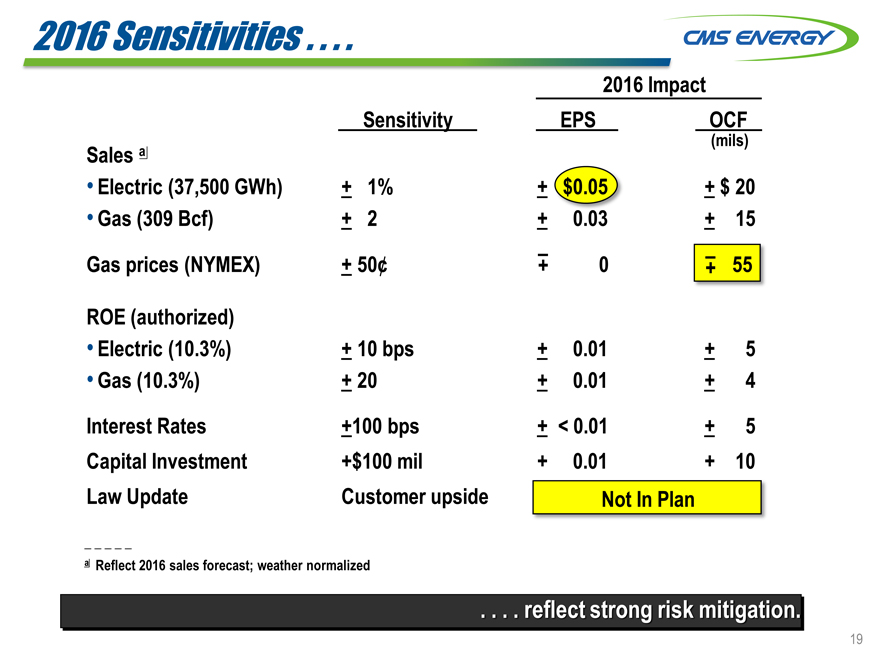

2016 Sensitivities . . . .

2016 Impact

Sensitivity EPS OCF

(mils)

Sales a

Electric (37,500 GWh) + 1% + $0.05 + $ 20

Gas (309 Bcf) + 2 + 0.03 + 15

Gas prices (NYMEX) + 50¢ + – 0 + – 55

ROE (authorized)

Electric (10.3%) + 10 bps + 0.01 + 5

Gas (10.3%) + 20 + 0.01 + 4

Interest Rates +100 bps + < 0.01 + 5

Capital Investment +$100 mil + 0.01 + 10

_ Law Update Customer upside Not In Plan

a Reflect 2016 sales forecast; weather normalized

. . . . reflect strong risk mitigation.

19

|

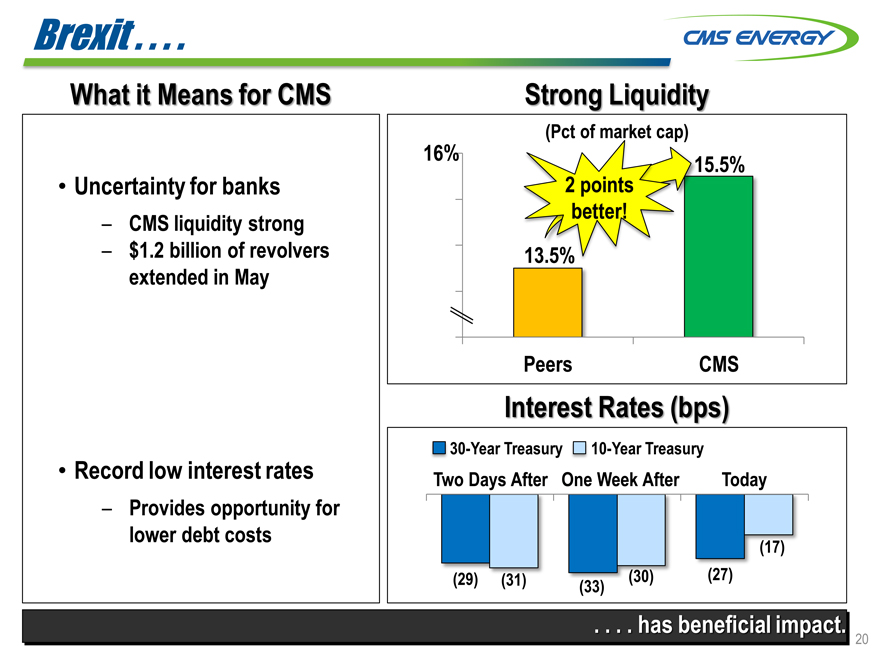

Brexit . . . .

What it Means for CMS

Uncertainty for banks

– CMS liquidity strong

– $1.2 billion of revolvers extended in May

Record low interest rates

– Provides opportunity for lower debt costs

Strong Liquidity

(Pct of market cap)

16% 5.5%

2 |

| points |

better!

Peers CMS

Interest Rates (bps)

30-Year Treasury 10-Year Treasury

Two Days After One Week After Today

(17) |

|

(29)(31)(33)(30)(27)

. . . . has beneficial impact.

20

|

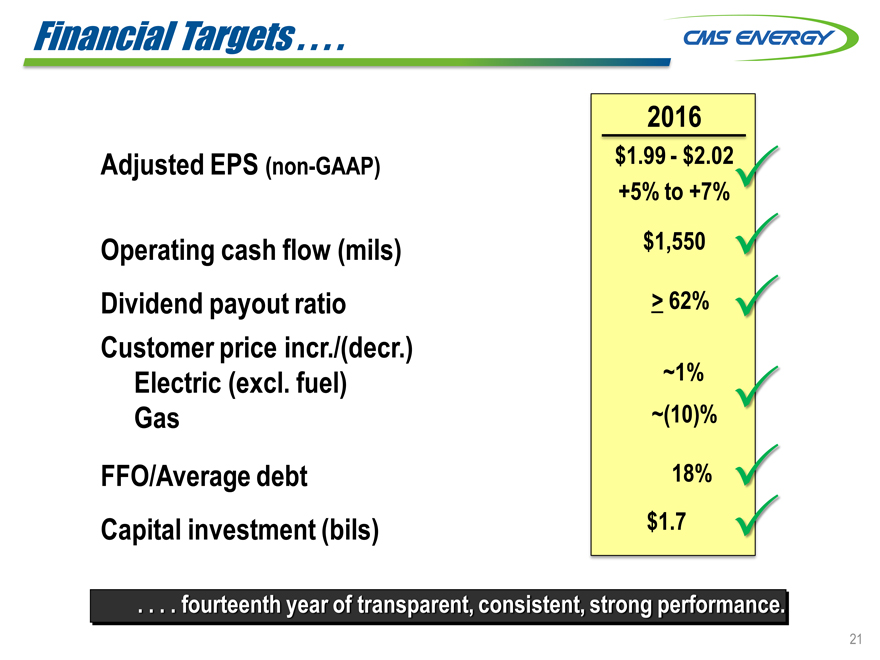

Financial Targets . . . .

Adjusted EPS (non-GAAP)

Operating cash flow (mils)

Dividend payout ratio Customer price incr./(decr.) Electric (excl. fuel) Gas

FFO/Average debt

Capital investment (bils)

2016

$1.99—$2.02

+5% to $1,550

> 62%

~1%

~(10)%

18%

$1.7

. . . . fourteenth year of transparent, consistent, strong performance.

21

|

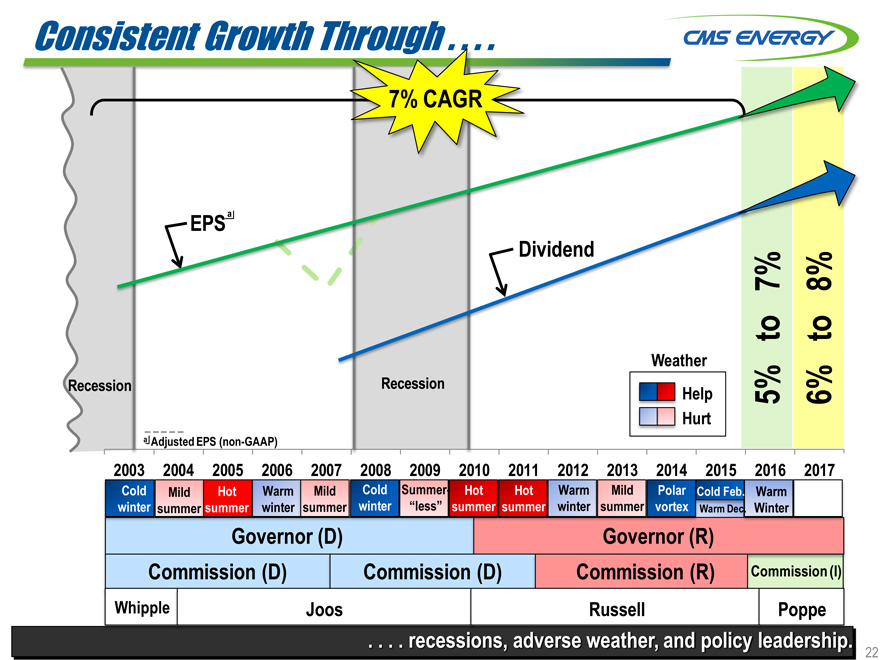

Consistent Growth Through

7% CAGR

7% 8%

to to

Weather

Recession Recession Help 5% 6%

Hurt

a Adjusted EPS (non-GAAP)

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 Cold Feb

Cold Mild Hot Warm Mild Cold Summer- Hot Hot Warm Mild Polar Cold Feb. Warm

winter summe summer winter summer winter “less” summer summer winter summer vortex Warm Dec. Winter

Governor (D) Governor (R)

Commission(D) Commission (D) Commission (R) Commission (I)

Whipple Joos Russell Poppe

. . . . recessions, adverse weather, and policy leadership.

22

|

Q & A

|

Appendix

|

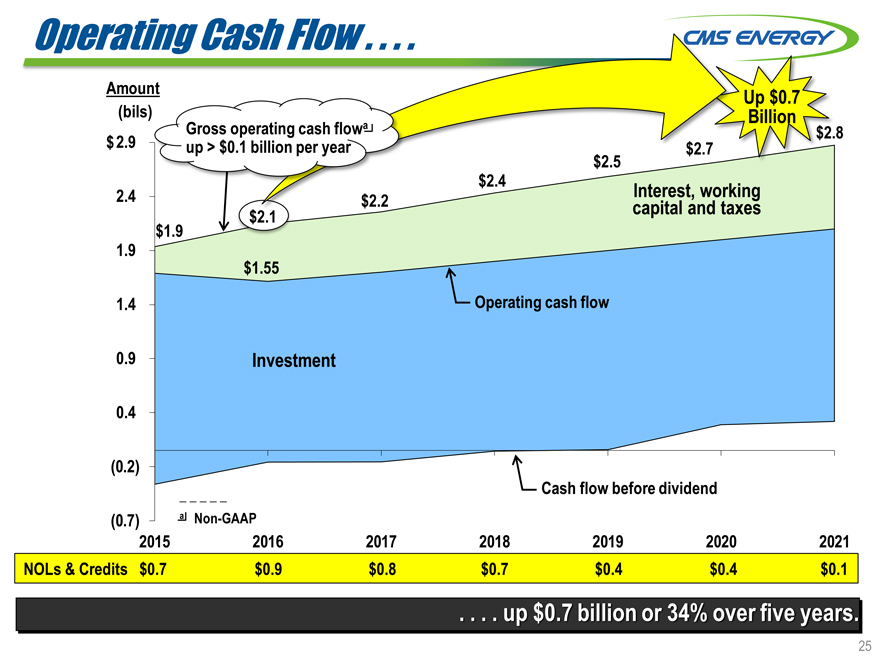

Operating Cash Flow

Amount Up $0.7

(bils) Billion

Gross operating cash flowa 8

$ 2.9 up > $0.1 billion per year

2.4

$2.1 |

| taxes |

$1.9

1.9

$1.55

1.4 |

| Operating cash flow |

0.9 |

| Investment |

0.4

(0.2)

Cash flow before dividend

(0.7) |

| a Non-GAAP |

2015 2016 2017 2018 2019 2020 2021

NOLs & Credits $0.7 $0.9 $0.8 $0.7 $0.4 $0.4 $0.1

up $0.7 billion or 34% over five years.

25

|

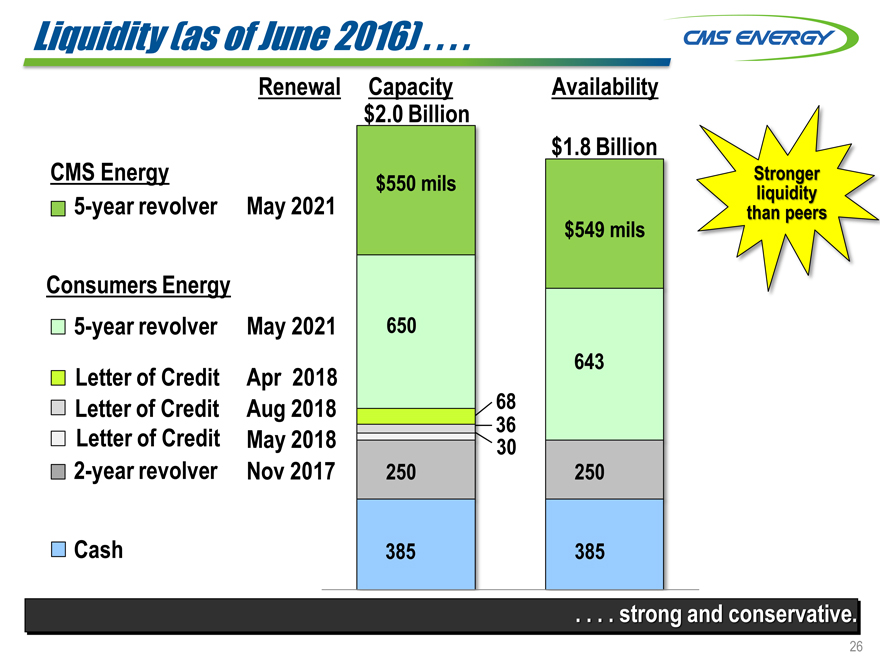

Liquidity (as of June 2016)

Renewal Capacity Availability

$2.0 |

| Billion |

$1.8 |

| Billion |

CMS Energy $550 mils

5-year revolver May 2021

$549 mils

Consumers Energy

5-year revolver May 2021 650

Letter of Credit Apr 2018 643

Letter of Credit Aug 2018 68

36 |

|

Letter of Credit May 2018 30

2-year revolver Nov 2017 250 250

Cash 385 385

. . . . strong and conservative.

26

|

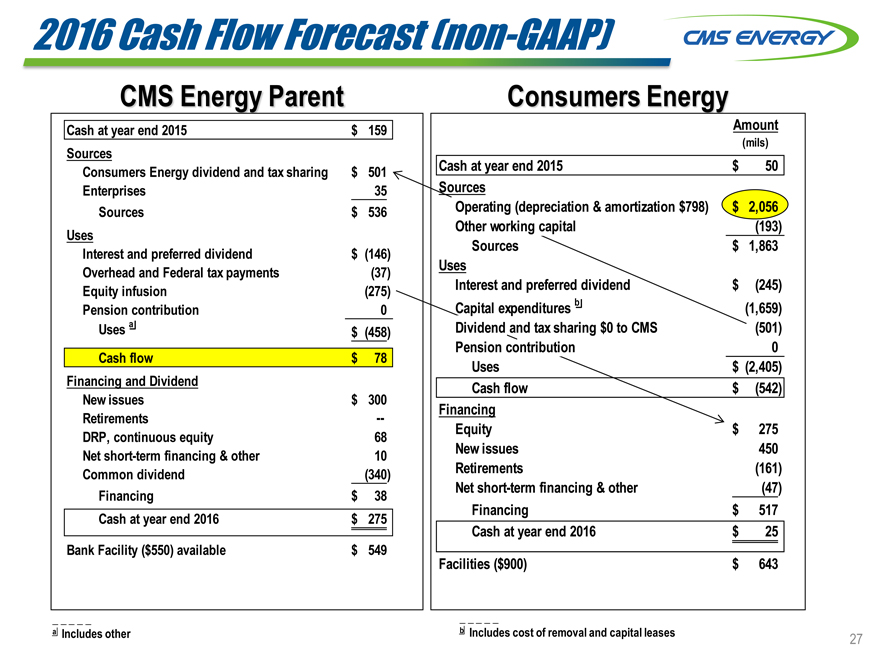

2016 Cash Flow Forecast (non-GAAP)

CMS Energy Parent Consumers Energy

Cash at year end 2015 $ 159 Amount

(mils)

Sources

Consumers Energy dividend and tax sharing $ 501 Cash at year end 2015 $ 50

Enterprises 35 Sources

Sources $ 536 Operating (depreciation & amortization $798) $ 2,056

Uses Other working capital(193)

Interest and preferred dividend $ (146) Sources $ 1,863

Overhead and Federal tax payments(37) Uses

Equity infusion(275) Interest and preferred dividend $ (245)

Pension contribution 0 Capital expenditures b(1,659)

Uses a $ (458) Dividend and tax sharing $0 to CMS(501)

Pension contribution 0

Cash flow $ 78 Uses $ (2,405)

Financing and Dividend Cash flow $ (542)

New issues $ 300

Retirements — Financing

DRP, continuous equity 68 Equity $ 275

Net short-term financing & other 10 New issues 450

Common dividend(340) Retirements(161)

Financing $ 38 Net short-term financing & other(47)

Cash at year end 2016 $ 275 Financing $ 517

Cash at year end 2016 $ 25

Bank Facility ($550) available $ 549

Facilities ($900) $ 643

a Includes other b Includes cost of removal and capital leases

27

|

GAAP Reconciliation

|

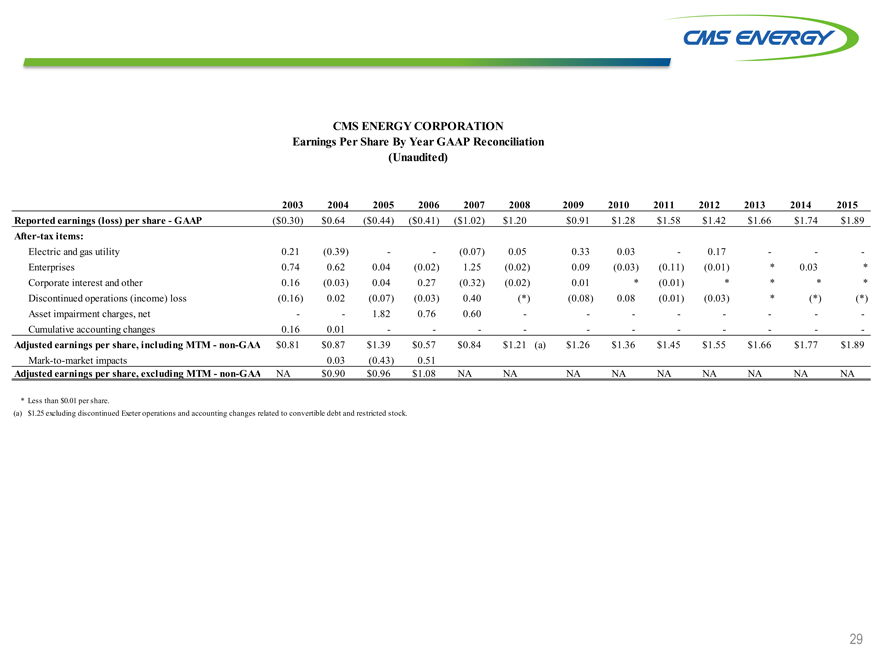

CMS ENERGY CORPORATION

Earnings Per Share By Year GAAP Reconciliation

(Unaudited)

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Reported earnings (loss) per share - GAAP ($0.30) $0.64 ($0.44) ($0.41) ($1.02) $1.20 $0.91 $1.28 $1.58 $1.42 $ 1.66 $ 1.74 $ 1.89

After-tax items:

Electric and gas utility 0.21 (0.39) - - (0.07) 0.05 0.33 0.03 - 0.17 - - -

Enterprises 0.74 0.62 0.04 (0.02) 1.25 (0.02) 0.09 (0.03) (0.11) (0.01) * 0.03 *

Corporate interest and other 0.16 (0.03) 0.04 0.27 (0.32) (0.02) 0.01 * (0.01) * * * *

Discontinued operations (income) loss (0.16) 0.02 (0.07) (0.03) 0.40 (*) (0.08) 0.08 (0.01) (0.03) * (*) (*)

Asset impairment charges, net - - 1.82 0.76 0.60 - - - - - - - -

Cumulative accounting changes 0.16 0.01 - - - - - - - - - - -

Adjusted earnings per share, including MTM - non-GAA $0.81 $0.87 $1.39 $0.57 $0.84 $1.21 (a) $1.26 $1.36 $1.45 $1.55 $ 1.66 $ 1.77 $ 1.89

Mark-to-market impacts 0.03 (0.43) 0.51

Adjusted earnings per share, excluding MTM - non-GAA NA $0.90 $0.96 $1.08 NA NA NA NA NA NA NA NA NA

* Less than $0.01 per share.

(a) $1.25 excluding discontinued Exeter operations and accounting changes related to convertible debt and restricted stock.

29

|

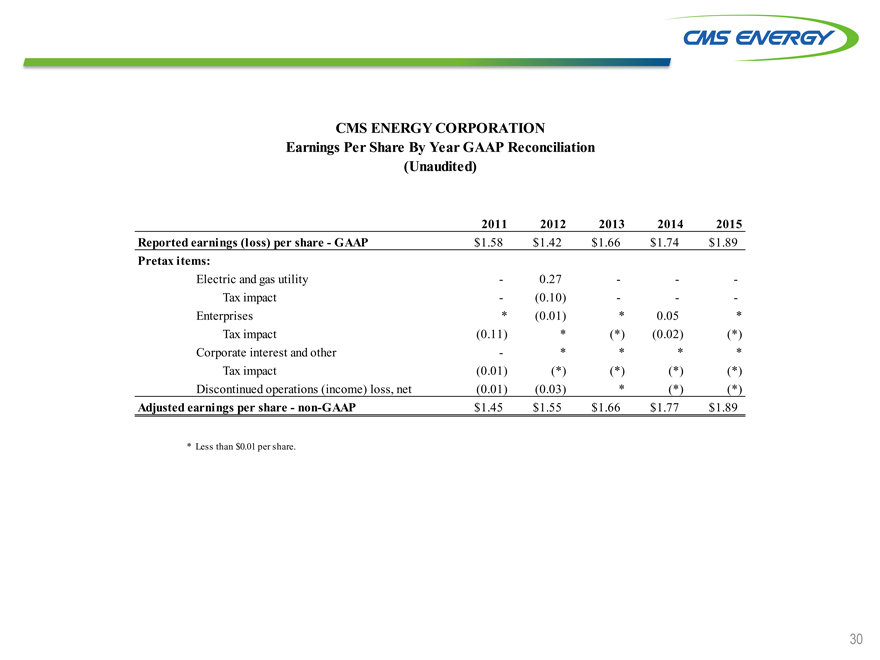

CMS ENERGY CORPORATION

Earnings Per Share By Year GAAP Reconciliation

(Unaudited)

2011 2012 2013 2014 2015

Reported earnings (loss) per share - GAAP $1.58 $1.42 $ 1.66 $1.74 $ 1.89

Pretax items:

Electric and gas utility - 0.27 - - -

Tax impact - (0.10) - - -

Enterprises * (0.01) * 0.05 *

Tax impact (0.11) * (*) (0.02) (*)

Corporate interest and other - * * * *

Tax impact (0.01) (*) (*) (*) (*)

Discontinued operations (income) loss, net (0.01) (0.03) * (*) (*)

Adjusted earnings per share - non-GAAP $1.45 $1.55 $ 1.66 $1.77 $ 1.89

* Less than $0.01 per share.

30

|

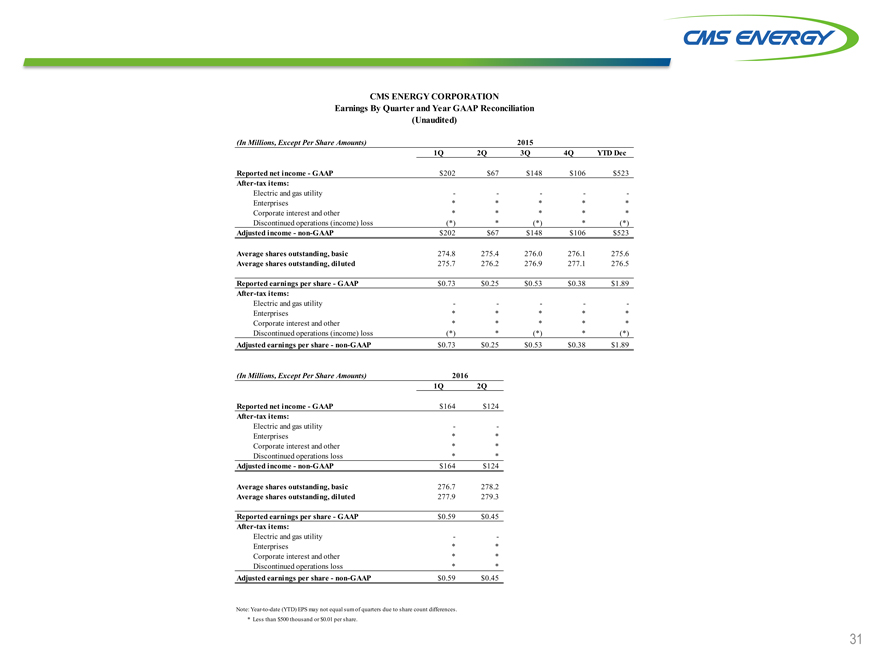

CMS ENERGY CORPORATION

Earnings By Quarter and Year GAAP Reconciliation

(Unaudited)

(In Millions, Except Per Share Amounts) 2015

1Q 2Q 3Q 4Q YTD Dec

Reported net income—GAAP $202 $67 $148 $106 $523

After-tax items:

Electric and gas utility — — -

Enterprises*****

Corporate interest and other*****

Discontinued operations (income) loss(*)*(*)*(*)

Adjusted income—non-GAAP $202 $67 $148 $106 $523

Average shares outstanding, basic 274.8 275.4 276.0 276.1 275.6

Average shares outstanding, diluted 275.7 276.2 276.9 277.1 276.5

Reported earnings per share—GAAP $0.73 $0.25 $0.53 $0.38 $1.89

After-tax items:

Electric and gas utility — — -

Enterprises*****

Corporate interest and other*****

Discontinued operations (income) loss(*)*(*)*(*)

Adjusted earnings per share—non-GAAP $0.73 $0.25 $0.53 $0.38 $1.89

(In Millions, Except Per Share Amounts) 2016

1Q 2Q

Reported net income—GAAP $164 $124

After-tax items:

Electric and gas utility —

Enterprises**

Corporate interest and other**

Discontinued operations loss**

Adjusted income—non-GAAP $164 $124

Average shares outstanding, basic 276.7 278.2

Average shares outstanding, diluted 277.9 279.3

Reported earnings per share—GAAP $0.59 $0.45

After-tax items:

Electric and gas utility —

Enterprises**

Corporate interest and other**

Discontinued operations loss**

Adjusted earnings per share—non-GAAP $0.59 $0.45

Note: Year-to-date (YTD) EPS may not equal sum of quarters due to share count differences.

* |

| Less than $500 thousand or $0.01 per share. |

31

|

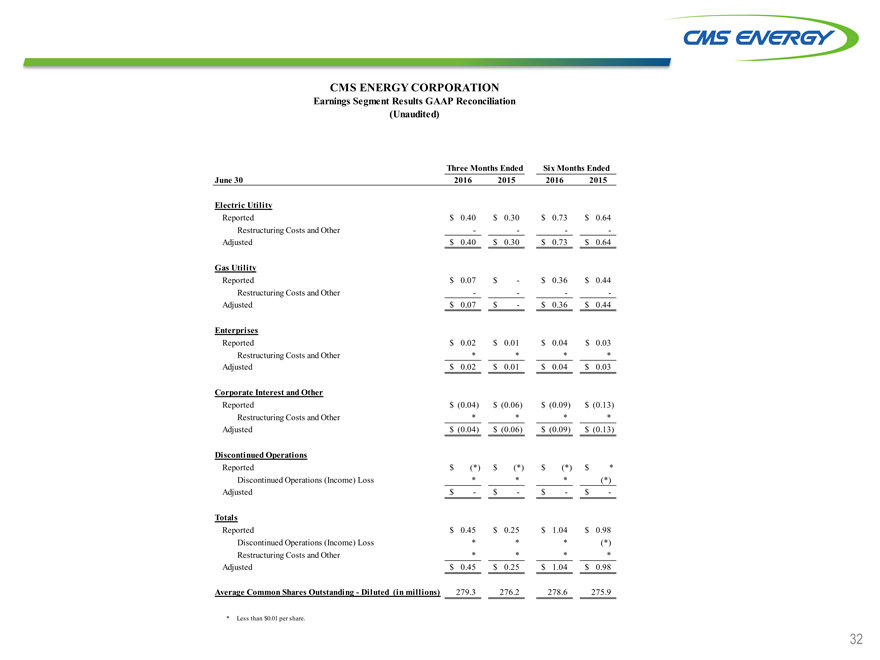

CMS ENERGY CORPORATION

Earnings Segment Results GAAP Reconciliation

(Unaudited)

Three Months Ended Six Months Ended

June 30 2016 2015 2016 2015

Electric Utility

Reported $ 0.40 $ 0.30 $ 0.73 $ 0.64

Restructuring Costs and Other — —

Adjusted $ 0.40 $ 0.30 $ 0.73 $ 0.64

Gas Utility

Reported $ 0.07 $—$ 0.36 $ 0.44

Restructuring Costs and Other — —

Adjusted $ 0.07 $—$ 0.36 $ 0.44

Enterprises

Reported $ 0.02 $ 0.01 $ 0.04 $ 0.03

Restructuring Costs and Other****

Adjusted $ 0.02 $ 0.01 $ 0.04 $ 0.03

Corporate Interest and Other

Reported $(0.04) $(0.06) $(0.09) $(0.13)

Restructuring Costs and Other****

Adjusted $(0.04) $(0.06) $(0.09) $(0.13)

Discontinued Operations

Reported $(*) $(*) $(*) $*

Discontinued Operations (Income) Loss***(*)

Adjusted $—$—$—$ -

Totals

Reported $ 0.45 $ 0.25 $ 1.04 $ 0.98

Discontinued Operations (Income) Loss***(*)

Restructuring Costs and Other****

Adjusted $ 0.45 $ 0.25 $ 1.04 $ 0.98

Average Common Shares Outstanding—Diluted (in millions) 279.3 276.2 278.6 275.9

* |

| Less than $0.01 per share. |

32

|

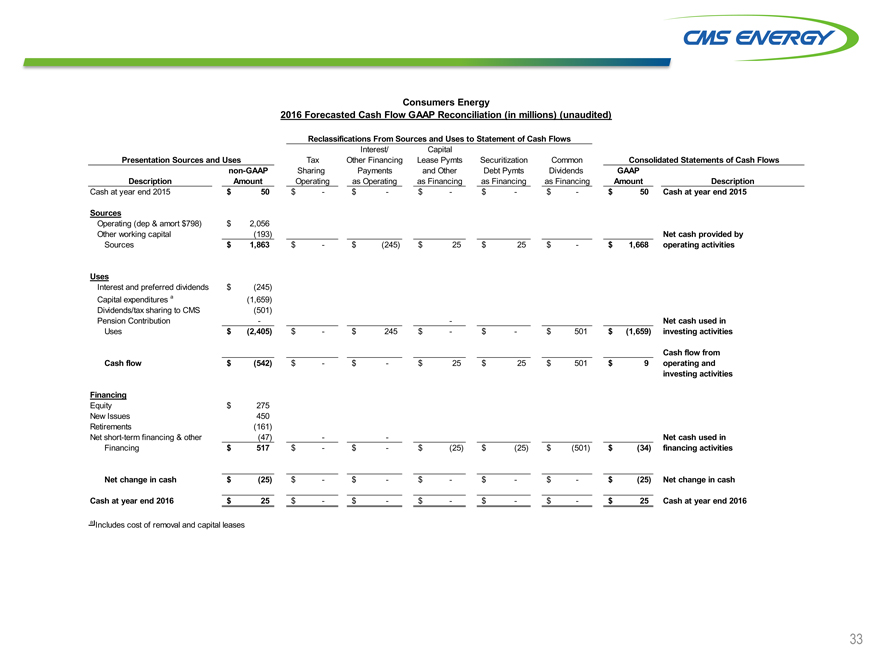

Consumers Energy

2016 Forecasted Cash Flow GAAP Reconciliation (in millions) (unaudited)

Reclassifications From Sources and Uses to Statement of Cash Flows

Interest/ Capital

Presentation Sources and Uses Tax Other Financing Lease Pymts Securitization Common Consolidated Statements of Cash Flows

non-GAAP Sharing Payments and Other Debt Pymts Dividends GAAP

Description Amount Operating as Operating as Financing as Financing as Financing Amount Description

Cash at year end 2015 $ 50 $—$—$—$—$—$ 50 Cash at year end 2015

Sources

Operating (dep & amort $798) $ 2,056

Other working capital(193) Net cash provided by

Sources $ 1,863 $—$(245) $ 25 $ 25 $—$ 1,668 operating activities

Uses

Interest and preferred dividends $(245)

Capital expenditures a(1,659)

Dividends/tax sharing to CMS(501)

Pension Contribution — Net cash used in

Uses $(2,405) $—$ 245 $—$—$ 501 $(1,659) investing activities

Cash flow from

Cash flow $(542) $—$—$ 25 $ 25 $ 501 $ 9 operating and

investing activities

Financing

Equity $ 275

New Issues 450

Retirements(161)

Net short-term financing & other(47) — Net cash used in

Financing $ 517 $—$—$(25) $(25) $(501) $(34) financing activities

Net change in cash $(25) $—$—$—$—$—$(25) Net change in cash

Cash at year end 2016 $ 25 $—$—$—$—$—$ 25 Cash at year end 2016

a Includes cost of removal and capital leases

33

|

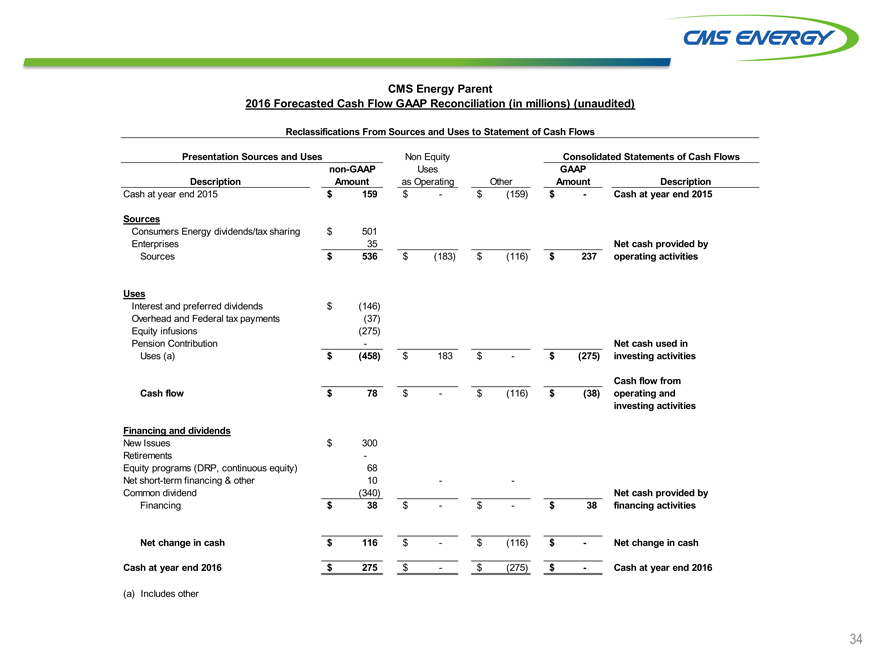

CMS Energy Parent

2016 Forecasted Cash Flow GAAP Reconciliation (in millions) (unaudited)

Reclassifications From Sources and Uses to Statement of Cash Flows

Presentation Sources and Uses Non Equity Consolidated Statements of Cash Flows

non-GAAP Uses GAAP

Description Amount as Operating Other Amount Description

Cash at year end 2015 $ 159 $—$(159) $—Cash at year end 2015

Sources

Consumers Energy dividends/tax sharing $ 501

Enterprises 35 Net cash provided by

Sources $ 536 $(183) $(116) $ 237 operating activities

Uses

Interest and preferred dividends $(146)

Overhead and Federal tax payments(37)

Equity infusions(275)

Pension Contribution—Net cash used in

Uses (a) $(458) $ 183 $—$(275) investing activities

Cash flow from

Cash flow $ 78 $—$(116) $(38) operating and

investing activities

Financing and dividends

New Issues $ 300

Retirements -

Equity programs (DRP, continuous equity) 68

Net short-term financing & other 10 —

Common dividend(340) Net cash provided by

Financing $ 38 $—$—$ 38 financing activities

Net change in cash $ 116 $—$(116) $—Net change in cash

Cash at year end 2016 $ 275 $—$(275) $—Cash at year end 2016

(a) |

| Includes other |

34

|

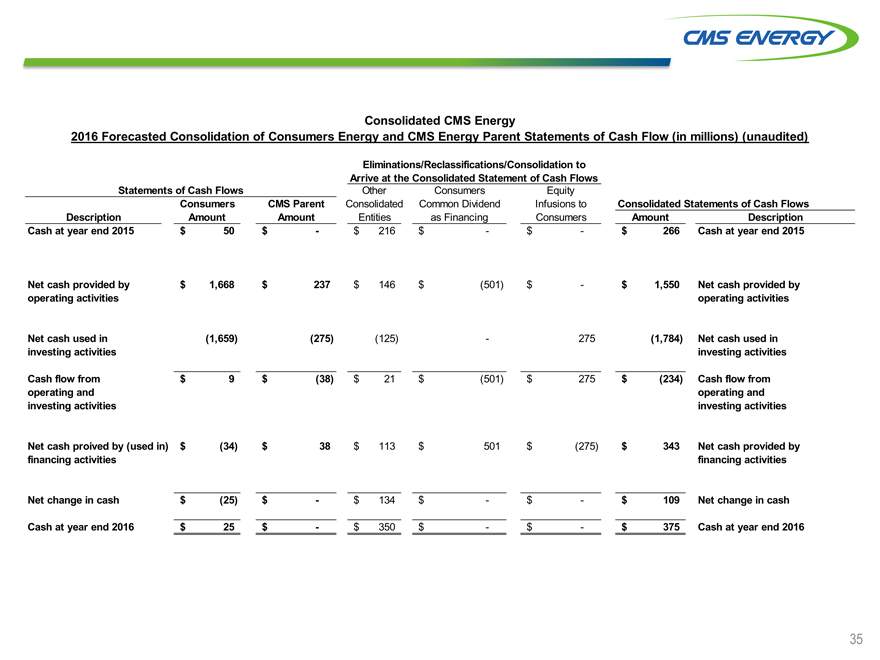

Consolidated CMS Energy

2016 Forecasted Consolidation of Consumers Energy and CMS Energy Parent Statements of Cash Flow (in millions) (unaudited)

Eliminations/Reclassifications/Consolidation to

Arrive at the Consolidated Statement of Cash Flows

Statements of Cash Flows Other Consumers Equity

Consumers CMS Parent Consolidated Common Dividend Infusions to Consolidated Statements of Cash Flows

Description Amount Amount Entities as Financing Consumers Amount Description

Cash at year end 2015 $ 50 $—$ 216 $—$—$ 266 Cash at year end 2015

Net cash provided by $ 1,668 $ 237 $ 146 $(501) $—$ 1,550 Net cash provided by

operating activities operating activities

Net cash used in(1,659)(275)(125)—275(1,784) Net cash used in

investing activities investing activities

Cash flow from $ 9 $(38) $ 21 $(501) $ 275 $(234) Cash flow from

operating and operating and

investing activities investing activities

Net cash proived by (used in) $(34) $ 38 $ 113 $ 501 $(275) $ 343 Net cash provided by

financing activities financing activities

Net change in cash $(25) $—$ 134 $—$—$ 109 Net change in cash

Cash at year end 2016 $ 25 $—$ 350 $—$—$ 375 Cash at year end 2016

35

|

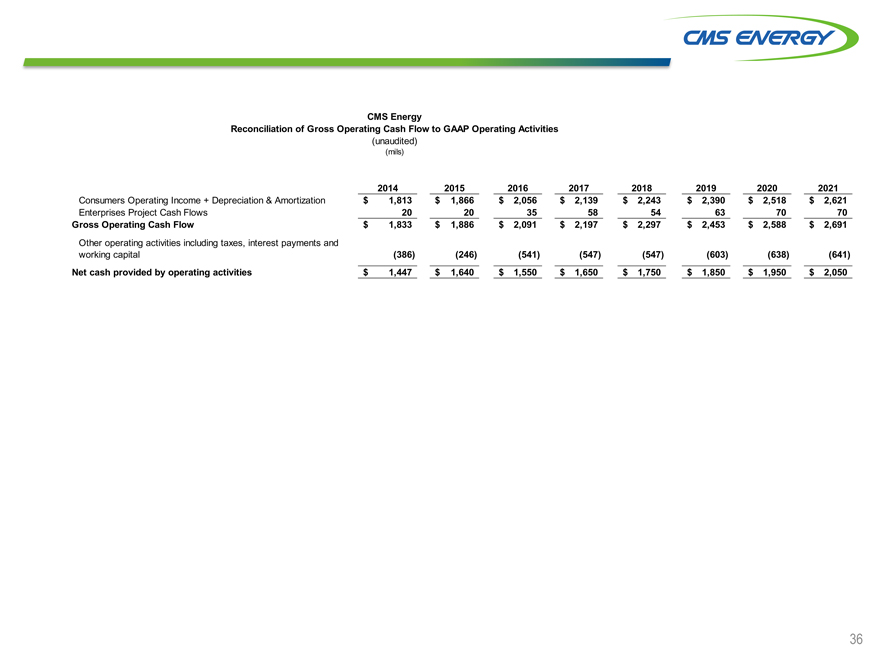

CMS Energy

Reconciliation of Gross Operating Cash Flow to GAAP Operating Activities

(unaudited)

(mils)

2014 2015 2016 2017 2018 2019 2020 2021

Consumers Operating Income + Depreciation & Amortization $ 1,813 $ 1,866 $ 2,056 $ 2,139 $ 2,243 $ 2,390 $ 2,518 $ 2,621

Enterprises Project Cash Flows 20 20 35 58 54 63 70 70

Gross Operating Cash Flow $ 1,833 $ 1,886 $ 2,091 $ 2,197 $ 2,297 $ 2,453 $ 2,588 $ 2,691

Other operating activities including taxes, interest payments and

working capital(386)(246)(541)(547)(547)(603)(638)(641)

Net cash provided by operating activities $ 1,447 $ 1,640 $ 1,550 $ 1,650 $ 1,750 $ 1,850 $ 1,950 $ 2,050

36