UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

SCHEDULE 14A

Proxy Statement Pursuant to Section 14(a) of the

Securities Exchange Act of 1934

(Amendment No. )

Filed by the Registrant x Filed by a Party other than the Registrant ¨

Check the appropriate box:

| ¨ | Preliminary Proxy Statement |

| ¨ | Confidential, for Use of the Commission Only (as permitted by Rule 14a-6(e)(2)) |

| ¨ | Definitive Proxy Statement |

| x | Definitive Additional Materials |

| ¨ | Soliciting Material Pursuant to §240.14a-12 |

Cedar Fair, L.P.

(Name of Registrant as Specified In Its Charter)

N/A

(Name of Person(s) Filing Proxy Statement, if other than the Registrant)

Payment of Filing Fee (Check the appropriate box):

| x | No fee required. |

| ¨ | Fee computed on table below per Exchange Act Rules 14a-6(i)(1) and 0-11. |

| (1) | Title of each class of securities to which transaction applies: |

| (2) | Aggregate number of securities to which transaction applies: |

| (3) | Per unit price or other underlying value of transaction computed pursuant to Exchange Act Rule 0-11 (set forth the amount on which the filing fee is calculated and state how it was determined): |

| (4) | Proposed maximum aggregate value of transaction: |

| (5) | Total fee paid: |

| ¨ | Fee paid previously with preliminary materials. |

| ¨ | Check box if any part of the fee is offset as provided by Exchange Act Rule 0-11(a)(2) and identify the filing for which the offsetting fee was paid previously. Identify the previous filing by registration statement number, or the Form or Schedule and the date of its filing. |

| (1) | Amount Previously Paid: |

| (2) | Form, Schedule or Registration Statement No.: |

| (3) | Filing Party: |

| (4) | Date Filed: |

On December 22, 2010, Cedar Fair made available the following presentation materials to be used by Cedar Fair at a meeting with Institutional Shareholder Services:

Presentation to ISS December 22, 2010 |

2 Forward-Looking Statements Some slides and comments included here, particularly related to estimates, comments on expectations about future performance or business conditions, may contain forward looking statements. These statements may involve risks and uncertainties that are difficult to predict, may be beyond our control and could cause actual results to differ materially from those described in such statements. Although we believe that the expectations reflected in such forward-looking statements are reasonable, we can give no assurance that such expectations will prove to be correct. Important factors, including those listed under Item 1A in the Partnership’s Form 10-K, could adversely affect our future financial performance and cause actual results to differ materially from our expectations. |

3 Additional Information About The Special Meeting Request This may be deemed to be solicitation material in respect of the Company's Special Meeting of Unitholders scheduled for January 11, 2011. On December 10, 2010, in connection with the Special Meeting, the Company filed a definitive proxy statement and a form of proxy with the SEC and the definitive proxy statement and a form of proxy has been mailed on or about December 13, 2010 to the Company’s unitholders of record as of December 9, 2010. In addition, the Company will file with, or furnish, to the SEC all additional relevant materials. BEFORE MAKING ANY VOTING DECISION, INVESTORS AND SECURITY HOLDERS OF THE COMPANY ARE URGED TO READ ALL RELEVANT DOCUMENTS FILED WITH OR FURNISHED TO THE SEC, INCLUDING THE COMPANY’S DEFINITIVE PROXY STATEMENT, BECAUSE THEY WILL CONTAIN IMPORTANT INFORMATION ABOUT THE SPECIAL MEETING. Investors and security holders will be able to obtain a copy of the definitive proxy statement and other documents filed by the Company free of charge from the SEC’s website, www.sec.gov. The Company’s Unitholders will also be able to obtain, without charge, a copy of the definitive proxy statement and other relevant documents by directing a request by mail or telephone to Investor Relations, Cedar Fair, L.P., One Cedar Point Dr., Sandusky, OH 44870, telephone: (419) 627- 2233, or from the Company’s website, www.cedarfair.com or by contacting Morrow & Co., LLC, at (203) 658-9400 or toll free at (800) 206-5879 The Company and its directors and executive officers and certain other members of its management and employees may be deemed to participate in the solicitation of proxies in respect of the Special Meeting of Unitholders. Additional information regarding the interests of such potential participants is included in the definitive proxy statement. |

4 Agenda I. Overview of Company and Corporate Growth Goals II. Summary of Our Brief History with Q Investments III. Review of Q Investments’ Proposals IV. Appendix A: Details on Long-term Strategy V. Appendix B: EBITDA Reconciliation |

5 Section I Company Overview |

6 FUN: Attractive Value Proposition for Long-Term Investors Recognized innovative leader in regional amusement parks, water parks, resorts and active entertainment Attractive park locations and diverse geographical footprint High-margin, seasonal industry niche Significant barriers to entry Strong and distinctive brands known for high-quality, pristine parks with cutting-edge attractions Consistently voted “Best in Class” Proven and stable business model that consistently generates a healthy revenue stream and strong cash flows A “Total Return” investment, not simply a “Yield MLP” Business strategy designed to increase revenues, adjusted EBITDA and cash flows to fund future growth, while increasing distributions and further reducing debt Goal of $1.25 to $1.75 per limited partner unit by 2015 Experienced and proven management team focused on sustainable long- term value creation for unitholders |

7 Growth Strategy in Place… Steadily grow attendance and revenues through continued investment in trend- setting new rides and attractions along with new targeted marketing programs Maintain strict controls over operating costs while maintaining “best-in-class” visitor experience Further reduce debt through the prudent use of excess cash flows Reduces risk to Cedar Fair – heavily levered capital structure increases sensitivity to macroeconomic downturns, bad weather and travel trends Provides balance sheet flexibility to take advantage of growth opportunities in the future |

8 … and Delivering Desired Results in 2010 Revenues expected between $965 million and $980 million Projected Adjusted EBITDA between $345 million and $355 million 2010 Projected Cash Flow (in millions) Adjusted EBITDA $345 - $355 Cash Interest Costs ~$130 Cash Taxes ~$19 Capital Expenditures ~$85 Cash Distributions ~$14 2010 Projected Cash Flow $97 - $107 |

9 Company on Strong Growth Trajectory – with Measurable Metrics in Place Grow revenues by 10% to 14% by 2015 (~2.3% CAGR) Grow adjusted EBITDA by 10% to 14% by 2015 (~2.3% CAGR) Achieve free cash flows of $120 million to $140 million on an annual basis during 2012 to 2015 Reduce Consolidated Leverage Ratio to 4.0x by 2013 Provide for a sustainable and growing distribution to unitholders Goal of $1.25 to $1.75 per limited partner unit by 2015; however, should cash flows exceed our expectations this distribution could be higher Represents a 10% to 14% annual yield based on today’s market price Our proven and stable business model should allow us to: |

10 Section II Brief History with Q Investments |

11 Brief History with Q Investments Q Investments has held FUN units for just one year Since that time… Its principal – Geoffrey Raynor – was offered a seat on the Board (he declined) It has stated in an SEC filing its interest in merging the company with Six Flags, a company that just emerged from bankruptcy It has flown the company’s former COO – who resigned from FUN – to its headquarters but has refused to meet with management It has actively participated in the selection of two new Board members It has threatened to “campaign vigorously” for the removal of the yet-to be named new CEO It has already sued FUN three times It has also seen the value of its units appreciate more than 20% |

12 Brief History with Q Investments Q Investments’ actions over the past 11 months suggest that the short-term interests of their hedge fund investors are not aligned with the best interests of all Cedar Fair unitholders The short-term focus of Q Investments is evident by the fact that, according to its 13F filing as of September 30, 2010, only one stock out of more than 30 in its portfolio had been held for more than two years We believe Q Investments’ true intentions are to get in, make a quick profit and get out – with no regard for what’s best for long-term investors |

13 Section III Review of Q Investments’ Proposals |

14 Summary – Overview Special Meeting of Unitholders: January 11, 2011 Proposal 1: to consider and vote upon a proposal from Q Investments to amend the Partnership Agreement to require the implementation of a policy providing that the Chairman of the Board of Directors of the General Partner be an independent director who has not previously served as an officer of the General Partner or its affiliates Proposal 2: to consider and vote upon a proposal from Q Investments to amend the Partnership Agreement to require the General Partner to make dividend distribution a higher priority than debt repayment and to take every action possible, including seeking necessary amendments to loan agreements, indentures and other documentation, to implement such distribution with the goal of returning to close to historical distribution levels based upon earnings Cedar Fair is asking unitholders to vote AGAINST both proposals |

15 Summary – Implications Proposal 1: Weakens Cedar Fair by requiring changes to the Company’s by- laws that puts unnecessary restrictions on the pool of qualified succession candidates going forward Proposal 2: Favors Q Investments’ short-term hedge funds investors over the Company’s long-term investors by preventing the Board from making prudent decisions with the Company’s capital |

16 Proposal 1: Succession Planning |

17 Proposal Would Restrict FUN’s Growth Potential by Unnecessarily Shrinking Pool of Qualified Candidates Implementing such a policy that so restricts who could be considered as a possible CEO successor will not result in strengthening the Company’s corporate governance or in creating – or enhancing – long-term value for unitholders As part of ongoing succession planning and corporate governance duties, the Board is open to considering and evaluating the concept of separating the roles of Chairman and Chief Executive Officer However, the proposal as structured would be highly disruptive to the Company’s ongoing succession-planning process that is well under way with Korn/Ferry International, a leading executive search firm Such a policy would limit the Board’s ability to determine the most capable candidate, including members of management, based on experience, abilities and business climate at any given time Attracting, retaining and grooming a deep and talented management team to run the diverse business portfolio has been – and will continue to be – a strategic imperative for the Company Proposal 1: Succession Planning |

18 While there is no set policy regarding Executive Chairman, the Board believes the most effective leadership model for the Company at this time is for Dick Kinzel to continue as Chairman and CEO through his contract term ending January 2, 2012 The Board regularly monitors its governance practices Proactively and voluntarily changed the Partnership Agreement in 2004 to enable unitholders to elect the Board of the General Partnership Recent appointment of two independent directors, both designated by Q Investments, further demonstrates the Company’s commitment to maintaining appropriate unitholder representation, open communications and effective corporate governance Active lead independent director in place along with annual board governance and individual director performance reviews FUN Has a Strong Track Record of Sound Corporate Governance Practices |

19 Lead independent director – Michael Kwiatkowski Seven of nine Board members meet NYSE independence requirements All members of Audit, Governance and Compensation committees are independent Two directors designated by Q Investments recently joined the Board: Eric Affeldt (Member of Audit and Compensation committees) John Scott (Member of Audit and Succession Planning committees) Both oppose Q Investments’ proposals Retained Korn/Ferry International to work with the special committee of independent directors of the Board to identify qualified candidate to succeed Dick Kinzel as CEO Company expects process to be completed by the end of the second quarter of 2011 Current Board and Committee Structure Ensures Independence |

20 Proposal 2: Use of Cash |

21 Proposal 2: Use of Cash In the first half of 2010, the Board carefully evaluated a wide range of financing options and use-of-cash scenarios – including input from Q Investments and other unitholders – with its independent advisors In July, debt refinancing was determined to be in the best long-term interest of the Company and its unitholders as it would allow for significantly enhanced financial flexibility and greater stability, among other things Company negotiated reinstatement of distributions into refinancing terms, beginning in 2010 Refinancing allowed the Company to resume its distributions to unitholders, which marked the 24 consecutive year of paying a unitholder distribution Prior to 2009, the Board had increased the distribution to unitholders in 22 of 23 consecutive years Q Investments’ request to mandate change in the Company’s proven fiscal policy is an apparent effort to create more short-term cash flow at the expense of long- term value creation and sustainable growth, which we believe is not in the best interests of all unitholders Q Investments’ proposal needlessly jeopardizes FUN’s financial flexibility by putting short-term gains ahead of the long-term health and total returns of the Company th |

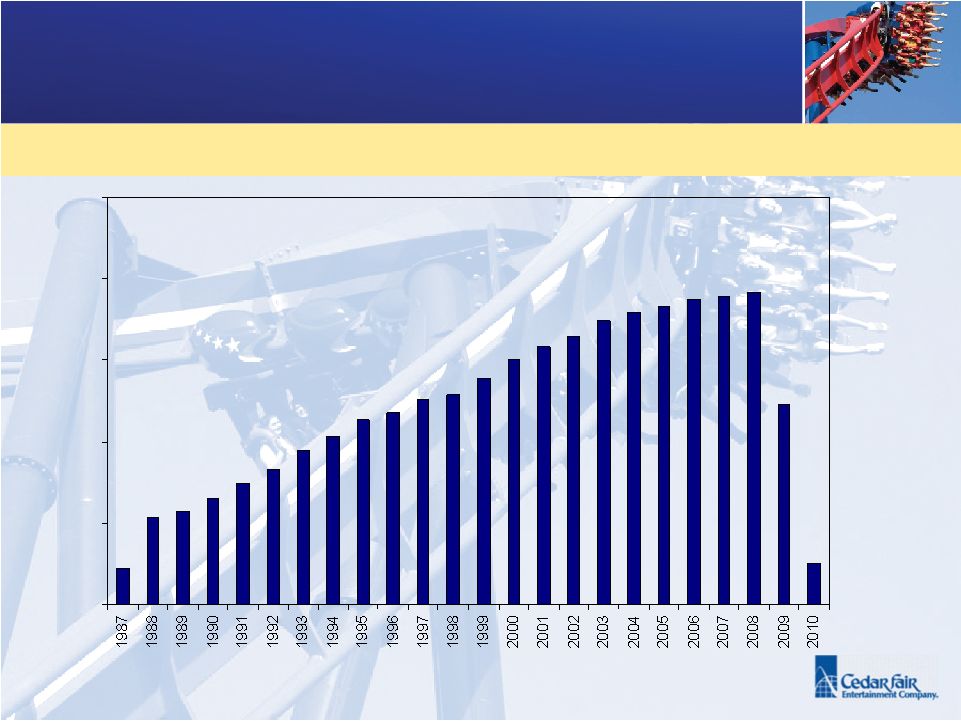

22 Commitment to Distributions Is Critical Piece of MLP Structure $0.22 $0.54 $0.57 $0.65 $0.74 $0.83 $0.94 $1.03 $1.13 $1.18 $1.26 $1.29 $1.39 $1.50 $1.58 $1.65 $1.74 $1.79 $1.83 $1.87 $1.90 $1.92 $1.23 $0.25 $0.00 $0.50 $1.00 $1.50 $2.00 $2.50 More than $1.4 billion paid in distributions since 1987 Dollars per unit FUN has demonstrated its commitment to distributions to unitholders over its history and has reconfirmed its commitment to growing distributions moving forward |

23 FUN Maintains an Unwavering Focus on Sustainable, Long-Term Value Creation for All Unitholders The Company’s long-term growth strategy is designed to provide unitholders with a strong and sustainable distribution and comprises: steady reinvestment in the parks and targeted marketing programs to generate continued organic growth strict controls over operating costs while maintaining “best-in-class” visitor experience prudent fiscal management that responsibly maintains an appropriate balance between distributions and a balance sheet, as well as an investment policy, that provides maximum long-term returns FUN has announced plans for increasing the distribution over the next five years and returning it to its historical rates in conjunction with a measured reduction in debt levels Management believes a policy limiting financial flexibility puts an unhealthy, short-term focus on use of cash with no regard for risk, changing business conditions and circumstances |

24 Debt Refinancing Critical Component of Prudent Fiscal Policy Cedar Fair is targeting a long-term capital structure that provides a low cost of capital, cushion against downside scenarios and ample liquidity to finance future growth and distributions Stronger credit ratings will provide lower cost of capital and enhance financial flexibility The absence of tax shield on debt reinforces the fortress balance sheet argument Challenging access to capital during downturns: Equity issuance: As a MLP, ability to raise equity is limited – cannot raise enough equity to make a material impact on debt or leverage Asset sales: In a downturn, selling theme park assets is challenging due to lack of strategic buyers and depressed valuations – even if possible, an asset sale would have an immaterial deleveraging impact Therefore, creating balance sheet strength is a critical component of a prudent financial policy Cedar Fair’s current dividend yield of 1.7% is in line with S&P 500 firms The Company plans to steadily increase its distributions towards the MLP average distributions (~6% yield) and its own historical distribution levels going forward |

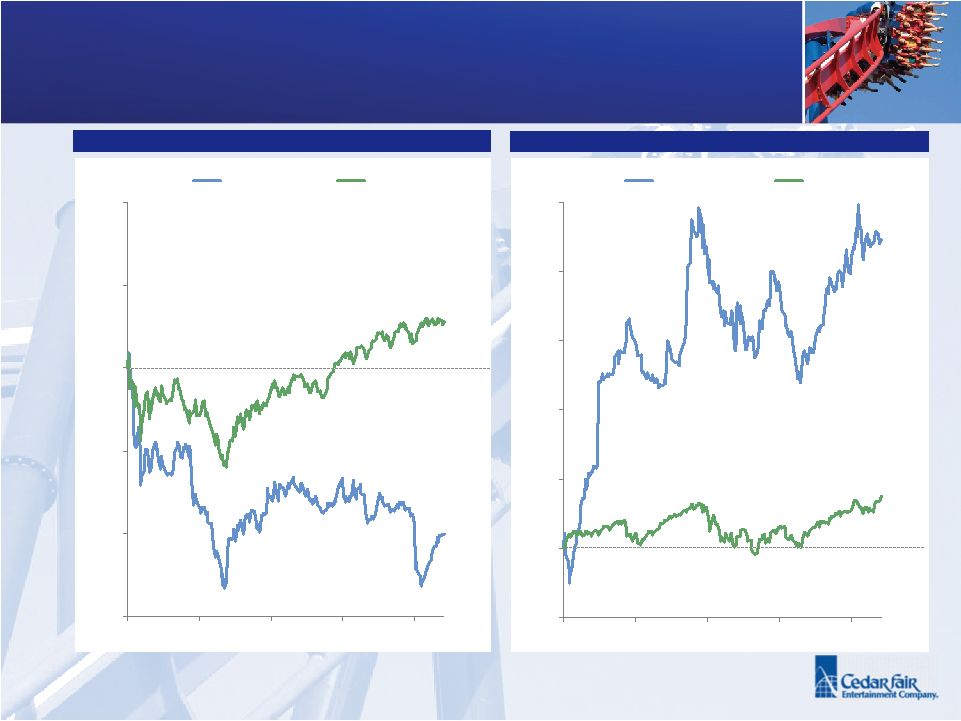

25 Unit price performance one year prior to distribution suspension Source: FactSet; market data as of 12/10/10 Since Our Focus Turned to Debt Reduction and Capital Structure, the Units have Recovered and Outperformed 25% 50% 75% 100% 125% 150% Nov-08 Feb-09 May-09 Aug-09 Nov-09 FUN S&P500 14% (50%) 75% 100% 125% 150% 175% 200% 225% Nov-09 Feb-10 May-10 Aug-10 Nov-10 FUN S&P500 19% 112% Unit price performance since distribution suspension |

26 Analysts Support Debt Refinancing Four out of five equity research analysts recommend FUN with a “buy” rating “We believe debt retirement is a more compelling use of cash flow in the near term and consider that to be the biggest key to improving unit holder value.” - Hilliard Lyons, June 2010 “Overall, the first half could not have gone better for FUN, as the company improved its park-level results, increased margins, and renegotiated its debt with expanded operating flexibility and extended maturities.” - Longbow, August 2010 “[Debt refinancing] will produce greater financial flexibility and capital structure certainty allowing for (1) future distribution reinstatement mid-late 2011, (2) debt reduction, and (3) growth of business.” - Wells Fargo, August 2010 “Further, while the less aggressive debt pay down is slightly disappointing, we recognize that there is a balance that must be struck between debt pay down and the payment of a distribution, and we believe the resumption and projected increase of the distribution will be viewed favorably by the market.” - KeyBanc, October 2010 “We believe Cedar Fair has addressed one of its primary risks with the July 2010 refinancing thereby extending maturities… which removed an overhang on the stock as investors were nervous about impending debt maturities.” - Merriman, November 2010 “We believe fears surrounding maturities and covenants on debt were the biggest overhang on FUN shares, and with these fears alleviated, we expect to see appreciation from here.” - Longbow, July 2010 |

27 Achieving Long-term Growth The Company’s long-term goals are obtainable because the Company refinanced its debt in July 2010 to provide the financial flexibility – and balance sheet strength – necessary to take full advantage of its long-term growth potential |

28 Cedar Fair’s Board Unanimously Recommend Unitholders Vote AGAINST the Proposals Submitted by Q Investments |

29 Section IV Appendix A: Details on Long- term Strategy |

30 Achieving Long-term Growth Create Value Trademark new rides and attractions Unique experience customer cannot recreate at home Increased focus on special events Create Urgency “Limited Time” offers Text message offers when inside park Goal: Grow revenues by 10% to 14% by 2015 (~2.3% CAGR) Create Buzz Media placement Online social networks (Facebook, Twitter) Digital marketing (blogs, text messaging) Extend Customers’ Stay Market competitive renovations to existing hotels Consideration of accommodations / resort development at other parks where appropriate |

31 Achieving Long-term Growth Revenue Growth Expanding market share and visitor spend Strict cost controls Proven history of controlling operating costs Low corporate overhead Remain focused on our four cornerstones: Safety, Cleanliness, Courtesy and Service – wrapped in Integrity Maintain operating margins between 34% and 36% Goal: Grow adjusted EBITDA by 10% to 14% by 2015 (~2.3% CAGR) |

32 Achieving Long-term Growth Adjusted EBITDA CAGR of ~2.3% to 2015 required to meet cash flow goals Cash FOR: Cash Interest Expense 2011 ~$160 million (due to “old” swaps which mature in 2011 and 2012) 2012 and beyond $110 million to $120 million Capital Expenditures 2011 expected to be approximately $75 million to $80 million Future average annual spend approximately $80 million to $90 million Cash Taxes Approximately $15 million to $20 million on an annual basis starting with 2011 Goal: Achieve free cash flows of $120 million to $140 million on an annual basis during 2012 to 2015 |

33 Achieving Long-term Growth We have stabilized our capital structure: Long-term debt includes: $1.175 billion senior secured term loan (matures Dec. 2016) $405 million senior unsecured notes (mature Dec. 2018) $260 million available through a senior secured revolving credit facility (matures July 2015) Reduce Leverage Ratios Reduce through growth in adjusted EBITDA and reduction of debt through the use of excess cash flow Senior secured leverage ratio to be reduced to sub-3.0x in 2013 (currently at 3.4x) Consolidated Leverage Ratio to be reduced to 4.0x in 2013 (currently at 4.5x) Interest Rates Guideline: ~60/40 fixed/variable Current swaps expire in Oct. 2011 ($1.0 billion) and Feb. 2012 ($268 million) Recently entered into $600 million of forward starting swaps Begin October 2011, mature in December 2015 LIBOR at an average rate of 2.6% Goal: Reduce Consolidated Leverage Ratio to 4.0x by 2013 |

34 Achieving Long-term Growth Excess Cash Flow distribution capacity per Credit Agreement 50% available senior secured leverage ratio is >3.25x 75% available senior secured leverage ratio is 2.75x to 3.25x 100% available senior secured leverage ratio is <2.75x Cedar Fair remains committed to issuing a distribution on a quarterly basis Provide for a sustainable and growing distribution to unitholders beginning today Represents a 10%-14% annual yield beginning 2015 based on current unit price Stabilizing the capital structure has put us in a position to reward unitholders as we execute our plan: |

35 Achieving Long-term Growth Declared 2010 distribution of $0.25 per unit Payable on December 15, 2010 to unitholders of record on December 3, 2010 24 consecutive year Cedar Fair has paid a distribution 2011 Distribution $20 million available for distributions under current senior secured credit agreement Board has announced it intends to pay full amount, or approximately $0.35 per unit Quarterly distributions would start at $0.08 per unit in March of 2011 Additional $20 million available for distributions if senior secured leverage ratio falls below 3.0x 2012 Distribution and Beyond Plan to steadily increase distribution on an annual basis Goal: $1.25 - $1.75 annual distribution per LP unit by 2015; however, should cash flows exceed our expectations this distribution could be higher th |

36 Section V Appendix B: EBITDA Reconciliation |

37 EBITDA Reconciliation EBITDA Adjustments ($ in thousands) LTM 9/26/2010 Net income $5,308 Interest expense 137,598 Interest (income) (1,076) Provision for taxes 4,093 Depreciation and amortization 130,675 EBITDA $276,688 Loss on early debt extinguishment 35,289 Net effect of swaps 19,001 Unrealized foreign exchange (gain) on Note (4,789) Equity-based compensation (687) Loss on impairment of goodwill and other Intangibles 5,890 Loss on impairment/retirement of fixed assets, net 345 Terminated merger costs 16,153 Class action settlement costs 276 Adj. EBITDA $348,166 |