UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-K

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d)

OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 2006

Commission File Number 0-15572

| | FIRST BANCORP | |

| | (Exact Name of Registrant as Specified in its Charter) | |

| North Carolina | | 56-1421916 |

| (State of Incorporation) | | (I.R.S. Employer Identification Number) |

| | | |

| 341 North Main Street, Troy, North Carolina | | 27371-0508 |

| (Address of Principal Executive Offices) | | (Zip Code) |

| | | |

| Registrant’s telephone number, including area code: | | (910) 576-6171 |

Securities Registered Pursuant to Section 12(b) of the Act: None

Securities Registered Pursuant to Section 12(g) of the Act:

COMMON STOCK, NO PAR VALUE

(Title of each class)

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act of 1933. ¨ YES ý NO

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Securities Exchange Act of 1934. ¨ YES ý NO

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Exchange Act during the preceding twelve months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. ý YES ¨ NO

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of the registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of the Form 10-K or any amendment to the Form 10-K. ý

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, or a non-accelerated filer. ¨ Large Accelerated Filer ý Accelerated Filer ¨ Non-Accelerated Filer

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). ¨ YES ý NO

The aggregate market value of the Common Stock, no par value, held by non-affiliates of the registrant, based on the closing price of the Common Stock as of June 30, 2006 as reported by The NASDAQ Global Select Market, was approximately $248,390,000.

The number of shares of the registrant’s Common Stock outstanding on February 26, 2007 was 14,362,672.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the Registrant’s Proxy Statement to be filed pursuant to Regulation 14A are incorporated herein by reference into Part III.

| | | Begins on |

| | | Page (s) |

| | | |

| | |

| Business | 4 |

| Risk Factors | 13 |

| Unresolved Staff Comments | 15 |

| Properties | 15 |

| Legal Proceedings | 15 |

| Submission of Matters to a Vote of Shareholders | 15 |

| | | |

| | |

| Market for the Registrant’s Common Stock, Related Shareholder Matters, and Issuer Purchases of Equity Securities | 16 |

| Selected Consolidated Financial Data | 18, 49 |

| Management’s Discussion and Analysis of Financial Condition and Results of Operations | 18 |

| | Critical Accounting Policies | 18 |

| | Merger and Acquisition Activity | 21 |

| | Overview Comparison of 2006 to 2005 | 22 |

| | Overview Comparison of 2005 to 2004 | 24 |

| | Statistical Information | |

| | Net Interest Income | 26, 50 |

| | Provision for Loan Losses | 28, 56 |

| | Noninterest Income | 28, 51 |

| | Noninterest Expenses | 30, 51 |

| | Income Taxes | 31, 52 |

| | Stock-Based Compensation | 31 |

| | Distribution of Assets and Liabilities | 34, 52 |

| | Securities | 35, 52 |

| | Loans | 36, 54 |

| | Nonperforming Assets | 37, 55 |

| | Allowance for Loan Losses and Loan Loss Experience | 39, 55 |

| | Deposits and Securities Sold Under Agreements to Repurchase | 40, 56 |

| | Borrowings | 41 |

| | Liquidity, Commitments, and Contingencies | 42, 58 |

| | Off-Balance Sheet Arrangements and Derivative Financial Instruments | 43 |

| | Interest Rate Risk (Including Quantitative and Qualitative Disclosures About Market Risk) | 44, 59 |

| | Return on Assets and Equity | 46, 59 |

| | Capital Resources and Shareholders’ Equity | 46, 60 |

| | Inflation | 47 |

| | Current Accounting and Regulatory Matters | 48 |

| Quantitative and Qualitative Disclosures About Market Risk | 48 |

| 48 |

| Financial Statements and Supplementary Data: | |

| | Consolidated Balance Sheets as of December 31, 2006 and 2005 | 62 |

| | Consolidated Statements of Income for each of the years in the three-year period ended December 31, 2006 | 63 |

| | | |

| | | Begins on |

| | | Page (s) |

| | Consolidated Statements of Comprehensive Income for each of the years in the three-year period ended December 31, 2006 | 64 |

| | Consolidated Statements of Shareholders’ Equity for each of the years in the three-year period ended December 31, 2006 | 65 |

| | Consolidated Statements of Cash Flows for each of the years in the three-year period ended December 31, 2006 | 66 |

| | Notes to Consolidated Financial Statements | 67 |

| | Report of Independent Registered Public Accounting Firm (Current Firm) | 102 |

| | Report of Independent Registered Public Accounting Firm (Predecessor Firm) | 104 |

| | Selected Consolidated Financial Data | 49 |

| | Quarterly Financial Summary | 61 |

| | | |

| Changes in and Disagreements with Accountants on Accounting and Financial Disclosures | 105 |

| Controls and Procedures | 105 |

| Other Information | 106 |

| | | |

| | |

| Directors, Executive Officers and Corporate Governance | 107* |

| Executive Compensation | 107* |

| Security Ownership of Certain Beneficial Owners and Management and Related Shareholder Matters | 107* |

| Certain Relationships and Related Transactions, and Director Independence | 108* |

| Principal Accountant Fees and Services | 108* |

| | | |

| | |

| Exhibits and Financial Statement Schedules | 108 |

| | | |

| | 111 |

| | | |

| * | Information called for by Part III (Items 10 through 14) is incorporated herein by reference to the Registrant’s definitive Proxy Statement for the 2007 Annual Meeting of Shareholders to be filed with the Securities and Exchange Commission. |

General Description

The Company

First Bancorp (the “Company”) is a bank holding company. The principal activity of the Company is the ownership and operation of First Bank (the “Bank”), a state-chartered bank with its main office in Troy, North Carolina. The Company also owns and operates two nonbank subsidiaries: Montgomery Data Services, Inc. (“Montgomery Data”), a data processing company, and First Bancorp Financial Services, Inc. (“First Bancorp Financial”), which owns and operates various real estate. Each of these subsidiaries is fully consolidated for financial reporting purposes. The Company is also the parent to four statutory business trusts created under the laws of the State of Delaware, which have issued a total of $67.0 million in trust preferred debt securities. Under current accounting requirements, these four statutory business trusts are not consolidated for financial reporting purposes - see discussion of FIN 46 in Note 1(t) to the consolidated financial statements under Item 8 below.

The Company was incorporated in North Carolina on December 8, 1983, as Montgomery Bancorp, for the purpose of acquiring 100% of the outstanding common stock of the Bank through a stock-for-stock exchange. On December 31, 1986, the Company changed its name to First Bancorp to conform its name to the name of the Bank, which had changed its name from Bank of Montgomery to First Bank in 1985.

The Bank was organized in 1934 and began banking operations in 1935 as the Bank of Montgomery, named for the county in which it operated. As of December 31, 2006, the Bank operated in a 26-county area centered in Troy, North Carolina. Troy, population 3,500, is located in the center of Montgomery County, approximately 60 miles east of Charlotte, 50 miles south of Greensboro, and 80 miles southwest of Raleigh. The Bank conducts business from 68 branches located within a 120-mile radius of Troy, covering principally a geographical area from Latta, South Carolina to the southeast, to Wilmington, North Carolina to the east, to Radford, Virginia to the north, to Wytheville, Virginia to the northwest, and to Harmony, North Carolina to the west. The Bank also has a loan production office in Blacksburg, which is located in southwestern Virginia and represents the Bank’s furthest location to the north of Troy. Of the Bank’s 68 branches, 61 are in North Carolina, with three branches in South Carolina and four braches in Virginia (where the Bank operates under the name “First Bank of Virginia”). Ranked by assets, the Bank was the 7th largest bank headquartered in North Carolina as of December 31, 2006.

As of December 31, 2006, the Bank had one wholly owned subsidiary, First Bank Insurance Services, Inc. (“First Bank Insurance”). First Bank Insurance was acquired as an active insurance agency in 1994 in connection with the Company’s acquisition of a bank that had an insurance subsidiary. On December 29, 1995, the insurance agency operations of First Bank Insurance were divested. From December 1995 until October 1999, First Bank Insurance was inactive. In October 1999, First Bank Insurance began operations again as a provider of non-FDIC insured investments and insurance products. Currently, First Bank Insurance’s primary business activity is the placement of property and casualty insurance coverage.

The Company’s principal executive offices are located at 341 North Main Street, Troy, North Carolina 27371-0508, and its telephone number is (910) 576-6171. Unless the context requires otherwise, references to the “Company” in this annual report on Form 10-K shall mean collectively First Bancorp and its consolidated subsidiaries.

General Business

The Bank engages in a full range of banking activities, providing such services as checking, savings, NOW and

money market accounts and other time deposits of various types including certificates of deposits (CDs) and individual retirement accounts (IRAs); loans for business, agriculture, real estate, personal uses, home improvement and automobiles; credit cards; debit cards; letters of credit; safe deposit box rentals; bank money orders; and electronic funds transfer services, including wire transfers, automated teller machines, and bank-by-phone capabilities. In December 2004, the Bank also began offering its internet banking product, with on-line bill pay and cash management features. In 2005, the Bank began offering repurchase agreements (also called securities sold under agreement to repurchase), which are similar to interest-bearing deposits and allows the Bank to pay interest to business customers without statutory limitations on the number of withdrawals that these customers can make. Because the majority of the Bank’s customers are individuals and small to medium-sized businesses located in the counties it serves, management does not believe that the loss of a single customer or group of customers would have a material adverse impact on the Bank. There are no seasonal factors that tend to have any material effect on the Bank’s business, and the Bank does not rely on foreign sources of funds or income. Because the Bank operates primarily within the central Piedmont region of North Carolina, the economic conditions within that area could have a material impact on the Company. See additional discussion below in the section entitled “Territory Served and Competition.”

Beginning in 1999, First Bank Insurance began offering non-FDIC insured investment and insurance products, including mutual funds, annuities, long-term care insurance, life insurance, and company retirement plans, as well as financial planning services (the “investments division”). In May 2001, First Bank Insurance added to its product line when it acquired two insurance agencies that specialized in the placement of property and casualty insurance. In October 2003, the “investments division” of First Bank Insurance became a part the Bank. The primary activity of First Bank Insurance is now the placement of property and casualty insurance products.

Montgomery Data’s primary business is to provide electronic data processing services for the Bank. Ownership and operation of Montgomery Data allows the Company to do all of its electronic data processing without paying fees for such services to an independent provider. Maintaining its own data processing system also allows the Company to adapt the system to its individual needs and to the services and products it offers. Although not a significant source of income, Montgomery Data has historically made its excess data processing capabilities available to area financial institutions for a fee. For the years ended December 31, 2006, 2005 and 2004, external customers provided gross revenues of $162,000, $279,000 and $416,000, respectively. During 2005, two of the five customers terminated their services with Montgomery Data and switched to another provider. During 2006, one other customer terminated its service, which left Montgomery Data with two outside customers as of December 31, 2006. Montgomery Data intends to continue to market its services to area banks, but does not currently have any near-term prospects for additional business.

First Bancorp Financial was organized under the name of First Recovery in September of 1988 for the purpose of providing a back-up data processing site for Montgomery Data and other financial and non-financial clients. First Recovery’s back-up data processing operations were divested in 1994. First Bancorp Financial now periodically purchases parcels of real estate from the Bank that were acquired through foreclosure or from branch closings. First Bancorp Financial actively pursues the sale of these properties.

First Bancorp Capital Trust I was organized in October 2002 for the purpose of issuing $20.6 million in debt securities. These borrowings are due on November 7, 2032 and are structured as trust preferred capital securities, which qualify as capital for regulatory capital adequacy requirements. These debt securities are callable by the Company at par on any quarterly interest payment date beginning on November 7, 2007. The interest rate on these debt securities adjusts on a quarterly basis at a rate of three-month LIBOR plus 3.45%. This rate may not exceed 12.50% through November 2007.

First Bancorp Capital Trust II and First Bancorp Capital Trust III were organized in December 2003 for the purpose of issuing $20.6 million in debt securities ($10.3 million were issued from each trust). These borrowings are due on December 19, 2033 and are also structured as trust preferred capital securities in order to qualify as

regulatory capital. These debt securities are callable by the Company at par on any quarterly interest payment date beginning on January 23, 2009. The interest rate on these debt securities adjusts on a quarterly basis at a weighted average rate of three-month LIBOR plus 2.70%.

First Bancorp Capital Trust IV was organized in April 2006 for the purpose of issuing $25.8 million in debt securities. These borrowings are due on June 15, 2036 and are structured as trust preferred capital securities, which qualify as capital for regulatory capital adequacy requirements. These debt securities are callable by the Company at par on any quarterly interest payment date beginning on June 15, 2011. The interest rate on these debt securities adjusts on a quarterly basis at a rate of three-month LIBOR plus 1.39%.

Territory Served and Competition

The Company’s headquarters are located in Troy, Montgomery County, North Carolina. The Company serves primarily the south central area of the Piedmont region of North Carolina. The following table presents, for each county where the Company operates, the number of bank branches operated by the Company within the county at December 31, 2006, the approximate amount of deposits with the Company in the county as of December 31, 2006, the Company’s approximate market share at June 30, 2006, and the number of bank competitors located in the county at June 30, 2006.

County | | No. of Branches | | Deposits (in millions) | | Market Share | | Number of Competitors |

| Anson, NC | | 1 | | $ | 12 | | | | 4.5 | % | | | 4 | |

| Brunswick, NC | | 2 | | | 4 | | | | - | | | | 10 | |

| Cabarrus, NC | | 2 | | | 31 | | | | 1.9 | % | | | 11 | |

| Chatham, NC | | 2 | | | 48 | | | | 9.7 | % | | | 9 | |

| Davidson, NC | | 3 | | | 115 | | | | 6.2 | % | | | 10 | |

| Dillon, SC | | 3 | | | 68 | | | | 25.5 | % | | | 2 | |

| Duplin, NC | | 3 | | | 64 | | | | 11.8 | % | | | 7 | |

| Guilford, NC | | 1 | | | 47 | | | | 0.4 | % | | | 25 | |

| Harnett, NC | | 3 | | | 110 | | | | 11.8 | % | | | 7 | |

| Iredell, NC | | 2 | | | 27 | | | | 1.1 | % | | | 16 | |

| Lee, NC | | 4 | | | 171 | | | | 21.4 | % | | | 7 | |

| Montgomery, NC | | 5 | | | 92 | | | | 36.0 | % | | | 4 | |

| Montgomery, VA | | 1 | | | 12 | | | | 0.9 | % | | | 10 | |

| Moore, NC | | 11 | | | 344 | | | | 25.0 | % | | | 10 | |

| New Hanover, NC | | 2 | | | 5 | | | | - | | | | 16 | |

| Pulaski, VA | | 1 | | | 19 | | | | - | | | | 7 | |

| Randolph, NC | | 4 | | | 58 | | | | 3.6 | % | | | 15 | |

| Richmond, NC | | 1 | | | 30 | | | | 7.5 | % | | | 6 | |

| Robeson, NC | | 5 | | | 143 | | | | 15.0 | % | | | 10 | |

| Rockingham, NC | | 1 | | | 20 | | | | 1.6 | % | | | 10 | |

| Rowan, NC | | 2 | | | 46 | | | | 3.1 | % | | | 12 | |

| Scotland, NC | | 2 | | | 47 | | | | 15.5 | % | | | 5 | |

| Stanly, NC | | 4 | | | 92 | | | | 10.3 | % | | | 6 | |

| Wake, NC | | 1 | | | 15 | | | | 0.1 | % | | | 26 | |

| Washington, VA | | 1 | | | 35 | | | | 2.8 | % | | | 13 | |

| Wythe, VA | | 1 | | | 41 | | | | 8.1 | % | | | 9 | |

| Total | | 68 | | $ | 1,696 | | | | | | | | | |

| | | | | | | | | | | | | | | | |

The Company’s 68 branches and facilities are primarily located in small communities whose economies are based primarily on services, manufacturing and light industry. Although the Company’s market is predominantly small communities and rural areas, the market area is not dependent on agriculture. Textiles, furniture, mobile homes, electronics, plastic and metal fabrication, forest products, food products, chicken hatcheries, and cigarettes are among the leading manufacturing industries in the trade area. Leading producers of lumber, socks, hosiery and area rugs are located in Montgomery County. The Pinehurst area within Moore County is a widely known golf resort and retirement area. The High Point area is widely known for its furniture market. New

Hanover and Brunswick Counties are in the southeastern coastal region of North Carolina, which are popular with tourists and have significant retirement populations. Additionally, several of the communities served by the Company are “bedroom” communities of large cities like Charlotte, Raleigh and Greensboro, while several branches are located in medium-sized cities such as Albemarle, Asheboro, High Point, Southern Pines and Sanford. The Company also has branches in small communities such as Bennett, Polkton, Vass, and Harmony.

Approximately 20% of the Company’s deposit base is in Moore County, and approximately 10% is in Lee County, and, accordingly, material changes in competition, the economy or population of Moore or Lee counties could materially impact the Company. No other county comprises more than 10% of the Company’s deposit base.

The Company competes in its various market areas with, among others, several large interstate bank holding companies that are headquartered in North Carolina. These large competitors have substantially greater resources than the Company, including broader geographic markets, higher lending limits and the ability to make greater use of large-scale advertising and promotions. A significant number of interstate banking acquisitions have taken place in the past decade, thus further increasing the size and financial resources of some of the Company’s competitors, three of which are among the largest bank holding companies in the nation. In many of the Company’s markets, the Company also competes against banks that have been organized within the past ten years. These new banks often focus on loan and deposit balance sheet growth, and not necessarily on earnings profitability. This strategy often allows them to offer more attractive terms on loans and deposits than the Company is able to offer because the Company must achieve an acceptable level of profitability. Moore County, which as noted above comprises a disproportionate share of the Company’s deposits, is a particularly competitive market, with at least ten other financial institutions having a physical presence. See “Supervision and Regulation” below for a further discussion of regulations in the Company’s industry that affect competition.

The Company competes not only against banking organizations, but also against a wide range of financial service providers, including federally and state-chartered savings and loan institutions, credit unions, investment and brokerage firms and small-loan or consumer finance companies. One of the credit unions in the Company’s market area is among the largest in the nation. Competition among financial institutions of all types is virtually unlimited with respect to legal ability and authority to provide most financial services. The Company also experiences competition from internet banks, particularly in the area of time deposits.

However, the Company believes it has certain advantages over its competition in the areas it serves. The Company seeks to maintain a distinct local identity in each of the communities it serves and actively sponsors and participates in local civic affairs. Most lending and other customer-related business decisions can be made without delays often associated with larger systems. Additionally, employment of local managers and personnel in various offices and low turnover of personnel enable the Company to establish and maintain long-term relationships with individual and corporate customers.

Lending Policy and Procedures

Conservative lending policies and procedures and appropriate underwriting standards are high priorities of the Bank. Loans are approved under the Bank’s written loan policy, which provides that lending officers, principally branch managers, have authority to approve loans of various amounts up to $250,000. Each of the Bank’s regional senior lending officers has discretion to approve secured loans in principal amounts up to $350,000 and together can approve loans up to $3,000,000. Lending limits may vary depending upon whether the loan is secured or unsecured.

The Bank’s board of directors reviews and approves loans that exceed management’s lending authority, loans to executive officers, directors, and their affiliates and, in certain instances, other types of loans. New credit extensions are reviewed daily by the Bank’s senior management and at least monthly by its board of directors.

The Bank continually monitors its loan portfolio to identify areas of concern and to enable management to take corrective action. Lending officers and the board of directors meet periodically to review past due loans and portfolio quality, while assuring that the Bank is appropriately meeting the credit needs of the communities it serves. Individual lending officers are responsible for pursuing collection of past-due amounts and monitoring any changes in the financial status of borrowers.

The Bank also contracts with an independent consulting firm to review new loan originations meeting certain criteria, as well as to assign risk grades to existing credits meeting certain thresholds. The consulting firm’s observations, comments, and risk grades, including variances with the Bank’s risk grades, are shared with the audit committee of the Company’s board of directors, and are considered by management in setting Bank policy, as well as in evaluating the adequacy of the allowance for loan losses. The consulting firm also provides training on a periodic basis to the Company’s loan officers to keep them updated on current developments in the marketplace. For additional information, see “Allowance for Loan Losses and Loan Loss Experience” under Item 7 below.

Investment Policy and Procedures

The Company has adopted an investment policy designed to optimize the Company’s income from funds not needed to meet loan demand in a manner consistent with appropriate liquidity and risk objectives. Pursuant to this policy, the Company may invest in federal, state and municipal obligations, federal agency obligations, public housing authority bonds, industrial development revenue bonds, the Federal Home Loan Bank, Fannie Mae, Government National Mortgage Association, Freddie Mac, Student Loan Marketing Association securities, and, to a limited extent, corporate bonds. Except for corporate bonds, the Company’s investments must be rated at least Baa by Moody’s or BBB by Standard and Poor’s. Securities rated below A are periodically reviewed for creditworthiness. The Company may purchase non-rated municipal bonds only if such bonds are in the Company’s general market area and determined by the Company to have a credit risk no greater than the minimum ratings referred to above. Industrial development authority bonds, which normally are not rated, are purchased only if they are judged to possess a high degree of credit soundness to assure reasonably prompt sale at a fair value. The Company is also authorized by its board of directors to invest a portion of its security portfolio in high quality corporate bonds, with the amount of bonds related to any one issuer not to exceed the Company’s legal lending limit. Prior to purchasing a corporate bond, the Company’s management performs due diligence on the issuer of the bond, and the purchase is not made unless the Company believes that the purchase of the bond bears no more risk to the Company than would an unsecured loan to the same company.

The Company’s investment officer implements the investment policy, monitors the investment portfolio, recommends portfolio strategies and reports to the Company’s investment committee. Reports of all purchases, sales, issuer calls, net profits or losses and market appreciation or depreciation of the bond portfolio are reviewed by the Company’s board of directors each month. Once a quarter, the Company’s interest rate risk exposure is evaluated by its board of directors. Once a year, the written investment policy is reviewed by the board of directors, and the Company’s portfolio is compared with the portfolios of other companies of comparable size.

Mergers and Acquisitions

As part of its operations, the Company has pursued an acquisition strategy over the years to augment its internal growth. The Company regularly evaluates the potential acquisition of or merger with various financial institutions. The Company’s acquisitions to date have generally fallen into one of three categories - 1) an acquisition of a financial institution or branch thereof within a market in which the Company operates, 2) an acquisition of a financial institution or branch thereof in a market contiguous or nearly contiguous to a market in which the Company operates, or 3) an acquisition of a company that has products or services that the Company does not currently offer.

The Company believes that it can enhance its earnings by pursuing these types of acquisition opportunities through any combination or all of the following: 1) achieving cost efficiencies, 2) enhancing the acquiree’s earnings or gaining new customers by introducing a more successful banking model with more products and services to the acquiree’s market base, 3) increasing customer satisfaction or gaining new customers by providing more locations for the convenience of customers, and 4) leveraging the Company’s customer base by offering new products and services.

Since 2000, the Company has completed acquisitions in all three categories described above. During that time, the Company has 1) completed three whole-bank acquisitions, with one being in the existing market area and the other two being in contiguous markets, with assets totaling approximately $500 million, 2) purchased ten bank branches from other banks (both in the existing market area and in contiguous/nearly contiguous markets) with total assets of approximately $250 million, and 3) acquired two insurance agencies, which provided the Company with the ability to offer property and casualty insurance coverage.

There are many factors that the Company considers when evaluating how much to offer for potential acquisition candidates - in the form of a purchase price comprised of cash and/or stock for a whole company purchase or a deposit premium in a branch purchase. Most significantly, the Company compares expectations of future earnings per share on a stand-alone basis with projected future earnings per share assuming completion of the acquisition under various pricing scenarios. Significant assumptions that affect this analysis include the estimated future earnings stream of the acquisition candidate, the amount of cost efficiencies that can be realized, and the interest rate earned/lost on the cash received/paid. In addition to the earnings per share comparison, the Company also considers other factors including (but not limited to): marketplace acquisition statistics, location of the candidate in relation to the Company’s expansion strategy, market growth potential, management of the candidate, potential integration issues (including corporate culture), and the size of the acquisition candidate.

The Company plans to continue to evaluate acquisition opportunities that could potentially benefit the Company and its shareholders. These opportunities may include acquisitions that do not fit the categories discussed above.

For a further discussion of recent acquisition activity, see “Merger and Acquisition Activity” under Item 7 below.

Employees

As of December 31, 2006, the Company had 579 full-time and 82 part-time employees. The Company is not a party to any collective bargaining agreements and considers its employee relations to be good.

Supervision and Regulation

As a bank holding company, the Company is subject to supervision, examination and regulation by the Board of Governors of the Federal Reserve System (the “Federal Reserve Board”) and the North Carolina Office of the Commissioner of Banks (the “Commissioner”). The Bank is subject to supervision and examination by the Federal Deposit Insurance Corporation (the “FDIC”) and the Commissioner. For additional information, see also Note 15 to the consolidated financial statements.

Supervision and Regulation of the Company

The Company is a bank holding company within the meaning of the Bank Holding Company Act of 1956, as amended. The Company is also regulated by the Commissioner under the Bank Holding Company Act of 1984.

A bank holding company is required to file quarterly reports and other information regarding its business operations and those of its subsidiaries with the Federal Reserve Board. It is also subject to examination by the Federal Reserve Board and is required to obtain Federal Reserve Board approval prior to making certain

acquisitions of other institutions or voting securities. The Commissioner is empowered to regulate certain acquisitions of North Carolina banks and bank holding companies, issue cease and desist orders for violations of North Carolina banking laws, and promulgate rules necessary to effectuate the purposes of the North Carolina Bank Holding Company Act of 1984.

Regulatory authorities have cease and desist powers over bank holding companies and their nonbank subsidiaries where their actions would constitute a serious threat to the safety, soundness or stability of a subsidiary bank. Those authorities may compel holding companies to invest additional capital into banking subsidiaries upon acquisitions or in the event of significant loan losses or rapid growth of loans or deposits.

National and state banks are also authorized by the Act to engage, through “financial subsidiaries,” in any activity that is permissible for a financial holding company (as described below) and any activity that the Secretary of the Treasury, in consultation with the Federal Reserve Board, determines is financial in nature or incidental to any such financial activity, except (i) insurance underwriting, (ii) real estate development or real estate investment activities (unless otherwise permitted by law), (iii) insurance company portfolio investments and (iv) merchant banking. The authority of a national or state bank to invest in a financial subsidiary is subject to a number of conditions, including, among other things, requirements that the bank be well-managed and well-capitalized (after deducting from the bank’s capital outstanding investments in financial subsidiaries).

The United States Congress and the North Carolina General Assembly have periodically considered and adopted legislation that has resulted in, and could result in further, deregulation of both banks and other financial institutions. Such legislation could modify or eliminate geographic restrictions on banks and bank holding companies and current restrictions on the ability of banks to engage in certain nonbanking activities. For example, in 1999, the U.S. enacted legislation that allowed bank holding companies to engage in a wider range of non-banking activities, including greater authority to engage in securities and insurance activities. Under the Gramm-Leach-Bliley Act (the “Act”), a bank holding company that elects to become a financial holding company may engage in any activity that the Federal Reserve Board, in consultation with the Secretary of the Treasury, determines by regulation or order is (i) financial in nature, (ii) incidental to any such financial activity, or (iii) complementary to any such financial activity and does not pose a substantial risk to the safety or soundness of depository institutions or the financial system generally. The Act made significant changes in U.S. banking law, principally by repealing certain restrictive provisions of the 1933 Glass-Steagall Act. The Act lists certain activities that are deemed to be financial in nature, including lending, exchanging, transferring, investing for others, or safeguarding money or securities; underwriting and selling insurance; providing financial, investment, or economic advisory services; underwriting, dealing in or making a market in, securities; and any activity currently permitted for bank holding companies by the Federal Reserve Board under Section 4(c)(8) of the Bank Holding Company Act. The Act does not authorize banks or their affiliates to engage in commercial activities that are not financial in nature. A bank holding company may elect to be treated as a financial holding company only if all depository institution subsidiaries of the holding company are well-capitalized, well-managed and have at least a satisfactory rating under the Community Reinvestment Act. At the present time, the Company does not anticipate applying for status as a financial holding company under the Act. This and other legislative and regulatory changes have increased the ability of financial institutions to expand the scope of their operations, both in terms of services offered and geographic coverage. Such legislative changes have placed the Company in more direct competition with other financial institutions, including mutual funds, securities brokerage firms, insurance companies, investment banking firms, and internet banks. The Company cannot predict what other legislation might be enacted or what other regulations might be adopted or, if enacted or adopted, the effect thereof on the Company’s business.

After the September 11, 2001 terrorist attacks in New York and Washington, D.C., the United States government acted in several ways to tighten control on activities perceived to be connected to money laundering and terrorist funding. A series of orders were issued that identify terrorists and terrorist organizations and require the blocking of property and assets of, as well as prohibiting all transactions or dealings with, such terrorists, terrorist organizations and those that assist or sponsor them. The USA Patriot Act substantially broadened

existing anti-money laundering legislation and the extraterritorial jurisdiction of the United States, imposed new compliance and due diligence obligations, created new crimes and penalties, compelled the production of documents located both inside and outside the United States, including those of foreign institutions that have a correspondent relationship in the United States, and clarified the safe harbor from civil liability to customers. In addition, the United States Treasury Department issued regulations in cooperation with the federal banking agencies, the Securities and Exchange Commission, the Commodity Futures Trading Commission and the Department of Justice to require customer identification and verification, expand the money-laundering program requirement to the major financial services sectors, including insurance and unregistered investment companies, such as hedge funds, and facilitate and permit the sharing of information between law enforcement and financial institutions, as well as among financial institutions themselves. The United States Treasury Department also has created the Treasury USA Patriot Act Task Force to work with other financial regulators, the regulated community, law enforcement and consumers to continually improve the regulations. The Company has established policies and procedures to ensure compliance with the USA Patriot Act.

In 2002, the Sarbanes-Oxley Act was signed into law. The Sarbanes-Oxley Act represents a comprehensive revision of laws affecting corporate governance, accounting obligations and corporate reporting. The Sarbanes-Oxley Act is applicable to all companies with equity or debt securities registered under the Securities Exchange Act of 1934, as amended. In particular, the Sarbanes-Oxley Act established: (i) new requirements for audit committees, including independence, expertise, and responsibilities; (ii) additional responsibilities regarding financial statements for the Chief Executive Officer and Chief Financial Officer of the reporting company; (iii) new standards for auditors and regulation of audits; (iv) increased disclosure and reporting obligations for the reporting company and their directors and executive officers; and (v) new and increased civil and criminal penalties for violation of the securities laws. The most significant expense associated with compliance with the Sarbanes-Oxley Act has been the internal control documentation and attestation requirements of Section 404 of the Act. The Company’s incremental external costs associated with complying with Section 404 of the Sarbanes-Oxley Act amounted to approximately $305,000, $832,000 and $193,000, for the years ended December 31, 2006, 2005, and 2004 respectively. The incremental costs relate to higher external audit fees and outside consultant fees. These amounts do not include the value of the significant internal resources devoted to compliance.

Supervision and Regulation of the Bank

Federal banking regulations applicable to all depository financial institutions, among other things: (i) provide federal bank regulatory agencies with powers to prevent unsafe and unsound banking practices; (ii) restrict preferential loans by banks to “insiders” of banks; (iii) require banks to keep information on loans to major shareholders and executive officers and (iv) bar certain director and officer interlocks between financial institutions.

As a state-chartered bank, the Bank is subject to the provisions of the North Carolina banking statutes and to regulation by the Commissioner. The Commissioner has a wide range of regulatory authority over the activities and operations of the Bank, and the Commissioner’s staff conducts periodic examinations of the Bank and its affiliates to ensure compliance with state banking regulations. Among other things, the Commissioner regulates the merger and consolidation of state-chartered banks, the payment of dividends, loans to officers and directors, recordkeeping, types and amounts of loans and investments, and the establishment of branches. The Commissioner also has cease and desist powers over state-chartered banks for violations of state banking laws or regulations and for unsafe or unsound conduct that is likely to jeopardize the interest of depositors.

The dividends that may be paid by the Bank to the Company are subject to legal limitations under North Carolina law. In addition, regulatory authorities may restrict dividends that may be paid by the Bank or the Company’s other subsidiaries. The ability of the Company to pay dividends to its shareholders is largely dependent on the dividends paid to the Company by its subsidiaries.

The Bank is a member of the FDIC, which currently insures the deposits of member banks. For this protection, each member bank pays a quarterly statutory assessment, based on its level of deposits, and is subject to the rules and regulations of the FDIC. For each of the past three years, due to the funded status of the insurance fund, the FDIC has not assessed the Bank any insurance premiums. However, in late 2006 the FDIC adopted new regulations that will result in all financial institutions, including the Bank, being assessed deposit insurance premiums ranging from 5 cents to 43 cents per $100 of assessable deposits beginning in 2007. The amount of the assessment within that range will be based on risk factors that have been established by the FDIC. Based on the specified risk factors, the Bank believes its assessment rate for 2007 will be between 5 cents and 7 cents per $100 of assessable deposits, which will result in annual insurance premium expense to the Bank of approximately $800,000 to $1.1 million based on its current deposit base. However, as part of the 2006 legislation that created the new assessment schedule, the rules provide credits to certain institutions that paid deposit insurance premiums in years prior to 1996. As a result, the Bank has received a one-time credit of $833,000 that can be used to offset FDIC insurance premiums beginning in 2007. Accordingly, the Company expects that this one-time credit will substantially offset its FDIC insurance premiums in 2007, but that there will be little, or no, remaining credit in 2008. Thus, the Company expects that its deposit insurance premium expense will increase significantly in 2008.

In addition to deposit insurance assessments, the FDIC is authorized to collect assessments against insured deposits to be paid to the Finance Corporation (FICO) to service FICO debt incurred in connection with the resolution of the thrift industry crisis the 1980s. The FICO assessment rate is adjusted quarterly. The average annual assessment rate in 2006 was 1.28 cents per $100 for insured deposits, which resulted in approximately $200,000 in expense for the Bank for 2006. For the first quarter of 2007, the FICO assessment rate for such deposits will decrease to 1.22 cents per $100 of assessable deposits.

The FDIC also is authorized to approve conversions, mergers, consolidations and assumptions of deposit liability transactions between insured banks and uninsured banks or institutions, and to prevent capital or surplus diminution in such transactions where the resulting, continuing, or assumed bank is an insured nonmember bank. In addition, the FDIC monitors the Bank’s compliance with several banking statutes, such as the Depository Institution Management Interlocks Act and the Community Reinvestment Act of 1977. The FDIC also conducts periodic examinations of the Bank to assess its compliance with banking laws and regulations, and it has the power to implement changes in or restrictions on a bank’s operations if it finds that a violation is occurring or is threatened.

Neither the Company nor the Bank can predict what other legislation might be enacted or what other regulations might be adopted, or if enacted or adopted, the effect thereof on the Bank’s operations.

See “Capital Resources and Shareholders’ Equity” under Item 7 below for a discussion of regulatory capital requirements.

Available Information

The Company maintains a corporate Internet site at www.firstbancorp.com, which contains a link within the “Investor Relations” section of the site to each of its filings with the Securities and Exchange Commission, including its annual reports on Form 10-K, its quarterly reports on Form 10-Q, its current reports on Form 8-K, and amendments to those reports filed or furnished pursuant to Section 13(a) or 15(d) of the Securities Exchange Act of 1934. These filings are available, free of charge, as soon as reasonably practicable after the Company electronically files such material with, or furnishes it to, the Securities and Exchange Commission. These filings can also be accessed at the Securities and Exchange Commission’s website located at www.sec.gov. Information included on the Company’s Internet site is not incorporated by reference into this annual report.

We are subject to interest rate risk, which could negatively impact earnings.

Net interest income is our most significant component of earnings. Our net interest income results from the difference between the yields we earn on our interest-earning assets, primarily loans and investments, and the rates that we pay on our interest-bearing liabilities, primarily deposits and borrowings. When interest rates change, the yields we earn on our interest-earning assets and the rates we pay on our interest-bearing liabilities do not necessarily move in tandem with each other because of the difference between their maturities and repricing characteristics. This mismatch can negatively impact net interest income if the margin between yields earned and rates paid narrows, as described below. Interest rate environment changes can occur at any time and are affected by many factors that are outside our control, including inflation, recession, unemployment trends, the Federal Reserve’s monetary policy, domestic and international disorder and instability in domestic and foreign financial markets.

Since mid-2004, the interest rate environment has generally been one in which short-term interest rates have risen faster than long-term interest rates. In 2006, this continued disparity resulted in short-term interest rates reaching the same level as long-term interest rates, which is referred to as a “flat yield curve.” A flat yield curve is unfavorable for us and many other financial institutions because our funding costs are generally tied to short-term interest rates, while our investment rates, in the form of securities and loans, are more closely correlated to long-term interest rates prevailing in the marketplace. The flat yield curve negatively impacted our net interest margin in 2006. However, strong growth that we achieved in loans and deposits in 2006 more than offset its negative impact, resulting in an increase in net interest income in 2006 compared to 2005. Many economists are predicting a continued flat interest rate environment in 2007, or one in which short-term interest rates rise higher than long-term interest rates. If that happens, our net interest margin will continue to experience negative pressure relative to prior periods when short-term interest rates were lower than long-term interest rates.

We face strong competition, which could hurt our business.

Our business operations are centered primarily in North Carolina, southwestern Virginia and northeastern South Carolina. Increased competition within this region may result in reduced loan originations and deposits. Ultimately, we may not be able to compete successfully against current and future competitors. Many competitors offer the types of loans and banking services that we offer. These competitors include savings associations, national banks, regional banks and other community banks. We also face competition from many other types of financial institutions, including finance companies, internet banks, brokerage firms, insurance companies, credit unions, mortgage banks and other financial intermediaries.

We compete in our market areas with several large interstate bank holding companies, including three of the largest in the nation, which are headquartered in North Carolina. These large competitors have substantially greater resources than we have, including broader geographic markets, more banking locations, higher lending limits and the ability to make greater use of large-scale advertising and promotions. Also, these institutions, particularly to the extent they are more diversified than we are, may be able to offer the same products and services that we offer at more competitive rates and prices.

We also compete in some of our market areas with many banks that have been organized within the past ten years. These new banks often focus on loan and deposit balance sheet growth, and not necessarily on earnings profitability. This strategy often allows them to offer more attractive terms on loans and deposits than we are able to offer because we must achieve an acceptable level of profitability.

Moore County, which comprises a disproportionate share of our deposits, is a particularly competitive market, with at least ten other financial institutions having a physical presence, including both large interstate

bank holding companies and recently organized banks.

Our allowance for loan losses may not be adequate to cover actual losses.

Like all financial institutions, we maintain an allowance for loan losses to provide for probable losses caused by customer loan defaults. The allowance for loan losses may not be adequate to cover actual loan losses, and in this case additional and larger provisions for loan losses would be required to replenish the allowance. Provisions for loan losses are a direct charge against income.

We establish the amount of the allowance for loan losses based on historical loss rates, as well as estimates and assumptions about future events. Because of the extensive use of estimates and assumptions, our actual loan losses could differ, possibly significantly, from our estimate. We believes that our allowance for loan losses is adequate to provide for probable losses, but it is possible that the allowance for loan losses will need to be increased for credit reasons or that regulators will require us to increase this allowance. Either of these occurrences could materially and adversely affect our earnings and profitability.

We are vulnerable to the economic conditions within the fairly small geographic region in which we operate.

Like many businesses, our overall success is partially dependent on the economic conditions in the marketplace where we operate. Our marketplace is predominately concentrated in the central Piedmont region of North Carolina. An economic downturn in this fairly small geographic region that negatively impacted our customers would likely also have an adverse impact on us. For example, an economic downturn could result in higher loan default rates and reduce the value of real estate securing those loans, which would likely increase our loan losses. At December 31, 2006, approximately 86% of our loans were secured by real estate collateral, and thus a decrease in real estate values could have an adverse impact on our operations.

We are subject to extensive regulation, which could have an adverse effect on our operations.

We are subject to extensive regulation and supervision from the North Carolina Commissioner of Banks, the FDIC, and the Federal Reserve Board. This regulation and supervision is intended primarily for the protection of the FDIC insurance fund and our depositors and borrowers, rather than for holders of our common stock. Regulatory authorities have extensive discretion in their supervisory and enforcement activities, including the imposition of restrictions on operations, the classification of our assets and determination of the level of the allowance for loan losses. Changes in the regulations that apply to us, or changes in our compliance with regulations, could have a material impact on our operations.

In the normal course of business, we process large volumes of transactions involving millions of dollars. If internal controls fail to work as expected, if systems are used in an unauthorized manner, or if employees subvert our internal controls, we could experience significant losses.

We process large volumes of transactions on a daily basis and are exposed to numerous types of operational risk. Operational risk includes the risk of fraud by persons inside or outside the company, the execution of unauthorized transactions by employees, errors relating to transaction processing and systems and breaches of the internal control system and compliance requirements. This risk of loss also includes potential legal actions that could arise as a result of an operational deficiency or as a result of noncompliance with applicable regulatory standards.

We establish and maintain systems of internal operational controls that provide us with timely and accurate information about our level of operational risk. Although not foolproof, these systems have been designed to manage operational risk at appropriate, cost-effective levels. Procedures exist that are designed to ensure that policies relating to conduct, ethics, and business practices are followed. From time to time, losses from

operational risk may occur, including the effects of operational errors. We continually monitor and improve our internal controls, data processing systems, and corporate-wide processes and procedures, but there can be no assurance that future losses will not occur.

We have a risk of loss related to our merchant credit card activities.

We process credit card transactions for approximately 575 commercial merchant clients. As these clients present us with credit card transactions authorized by their customers, we deposit funds in their checking accounts and collect the corresponding amounts due from the credit card issuer. In the event that the customer disputes the charge, we are contractually liable for any amounts legally due to the customer in the event our merchant clients do not make payment. We experienced a $1.9 million loss in 2006 as a result of this contingent liability. Although we subsequently reviewed the rest of our merchant relationships, we cannot guarantee that a similar loss will not occur again in the future.

None

The main offices of the Company, the Bank and First Bancorp Financial are owned by the Bank and are located in a three-story building in the central business district of Troy, North Carolina. The building houses administrative and bank teller facilities. The Bank’s Operations Division, including customer accounting functions, offices and operations of Montgomery Data, and offices for loan operations, are housed in two one-story steel frame buildings approximately one-half mile west of the main office. Both of these buildings are owned by the Bank. The Company operates 68 bank branches. The Company owns all its bank branch premises except 10 branch offices for which the land and buildings are leased and two branch offices for which the land is leased but the building is owned. In addition, the Company leases one loan production office. There are no options to purchase or lease additional properties. The Company considers its facilities adequate to meet current needs and believes that lease renewals or replacement properties can be acquired as necessary to meet future needs.

Item 3. Legal Proceedings

Various legal proceedings may arise in the ordinary course of business and may be pending or threatened against the Company and/or its subsidiaries. However, neither the Company nor any of its subsidiaries is involved in any pending legal proceedings that management believes could have a material effect on the consolidated financial position of the Company.

There were no tax shelter penalties assessed by the Internal Revenue Service against the Company during the year ended December 31, 2006.

Item 4. Submission of Matters to a Vote of Shareholders

No matters were submitted to a vote of shareholders during the fourth quarter of 2006.

Item 5. Market for the Registrant’s Common Stock, Related Shareholder Matters, and Issuer Purchases of Equity Securities

The Company’s common stock trades on The NASDAQ Global Select Market under the symbol FBNC. Table 22, included in “Management’s Discussion and Analysis” below, set forth the high and low market prices of the Company’s common stock as traded by the brokerage firms that maintain a market in the Company’s common stock and the dividends declared for the periods indicated. It is the Company’s current intention to continue to pay cash dividends in the future comparable to those in the recent past. See “Business - Supervision and Regulation” above and Note 15 to the consolidated financial statements for a discussion of regulatory restrictions on the Company’s payment of dividends. As of December 31, 2006, there were approximately 2,650 shareholders of record and another 3,600 shareholders whose stock is held in “street name.” There were no sales of unregistered securities during the year ended December 31, 2006.

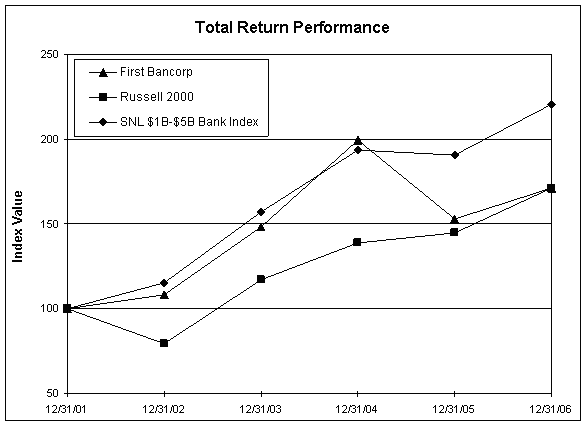

Performance Graph

The performance graph shown below compares the Company’s cumulative total return to shareholders for the five-year period commencing December 31, 2001 and ending December 31, 2006, with the cumulative total return of the Russell 2000 Index (reflecting overall stock market performance of small-capitalization companies), and an index of banks with between $1 billion and $5 billion in assets, as constructed by SNL Securities, LP (reflecting changes in banking industry stocks). The graph and table assume that $100 was invested on December 31, 2001 in each of the Company’s common stock, the Russell 2000 Index, and the SNL Bank Index, and that all dividends were reinvested.

First Bancorp

Comparison of Five-Year Total Return Performances (1)

Five Years Ending December 31, 2006

| | | Total Return Index Values (1) December 31, | |

| | | 2001 | | 2002 | | 2003 | | 2004 | | 2005 | | 2006 | |

| First Bancorp | | $ | 100.00 | | | 108.14 | | | 148.42 | | | 199.43 | | | 152.93 | | | 171.43 | |

| Russell 2000 | | | 100.00 | | | 79.52 | | | 117.09 | | | 138.55 | | | 144.86 | | | 171.47 | |

| SNL Index-Banks between $1 billion and $5 billion | | | 100.00 | | | 115.44 | | | 156.98 | | | 190.74 | | | 190.43 | | | 220.36 | |

Notes:

| (1) | Total return indices were provided from an independent source, SNL Securities LP, Charlottesville, Virginia, and assume initial investment of $100 on December 31, 2001, reinvestment of dividends, and changes in market values. Total return index numerical values used in this example are for illustrative purposes only. |

Issuer Purchases of Equity Securities

Pursuant to authorizations by the Company’s board of directors, the Company has from time to time repurchased shares of common stock in private transactions and in open-market purchases. The most recent board authorization was announced on July 30, 2004 and authorized the repurchase of 375,000 shares of the Company’s stock. During 2006, the Company repurchased a total of 53,000 shares of its own stock at an average price of $20.97 per share. As shown below, the Company did not repurchase any shares of its common stock during the three months ended December 31, 2006.

| Issuer Purchases of Equity Securities | |

Period | | Total Number of Shares Purchased (2) | | Average Price Paid per Share | | Total Number of Shares Purchased as Part of Publicly Announced Plans or Programs (1) | | Maximum Number of Shares that May Yet Be Purchased Under the Plans or Programs (1) | |

| Month #1 (October 1, 2006 to October 31, 2006) | | | – | | | | | | | | | 262,015 | |

| Month #2 (November 1, 2006 to November 30, 2006) | | | | | | | | | | | | 262,015 | |

| Month #3 (December 1, 2006 to December 31, 2006) | | | | | | | | | | | | 262,015 | |

| Total | | | | | | | | | | | | 262,015 | |

Footnotes to the Above Table

(1) Any shares repurchased would be pursuant to publicly announced share repurchase authorizations. On July 30, 2004, the Company announced that its Board of Directors had approved the repurchase of 375,000 shares of the Company’s common stock. The repurchase authorization does not have an expiration date. There are no plans or programs the issuer has determined to terminate prior to expiration, or under which the issuer does not intend to make further purchases.

(2) The table above does not include shares that were used by option holders to satisfy the exercise price of the Company’s call options issued by the Company to its employees and directors pursuant to the Company’s stock option plans. In November 2006, a total of 2,091 shares of the Company’s common stock, with a weighted average market price of $22.35 per share, were used to satisfy an exercise of options.

Item 6. Selected Consolidated Financial Data

Table 1 sets forth selected consolidated financial data for the Company.

Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations

Management’s Discussion and Analysis is intended to assist readers in understanding the Company’s results of operations and changes in financial position for the past three years. This review should be read in conjunction with the consolidated financial statements and accompanying notes beginning on page 62 of this report and the supplemental financial data contained in Tables 1 through 22 included with this discussion and analysis. All share data for periods prior to November 15, 2004 has been adjusted from originally reported amounts to reflect the 3-for-2 stock split paid on November 15, 2004.

CRITICAL ACCOUNTING POLICIES

The accounting principles followed by the Company and the methods of applying these principles conform with accounting principles generally accepted in the United States of America and with general practices followed by the banking industry. Certain of these principles involve a significant amount of judgment and/or

use of estimates based on the Company’s best assumptions at the time of the estimation. The Company has identified three policies as being more sensitive in terms of judgments and estimates, taking into account their overall potential impact to the Company’s consolidated financial statements - 1) the allowance for loan losses, 2) tax uncertainties, and 3) intangible assets.

Allowance for Loan Losses

Due to the estimation process and the potential materiality of the amounts involved, the Company has identified the accounting for the allowance for loan losses and the related provision for loan losses as an accounting policy critical to the Company’s consolidated financial statements. The provision for loan losses charged to operations is an amount sufficient to bring the allowance for loan losses to an estimated balance considered adequate to absorb losses inherent in the portfolio.

Management’s determination of the adequacy of the allowance is based primarily on a mathematical model that estimates the appropriate allowance for loan losses. This model has two components. The first component involves the estimation of losses on loans defined as “impaired loans.” A loan is considered to be impaired when, based on current information and events, it is probable the Company will be unable to collect all amounts due according to the contractual terms of the loan agreement. The estimated valuation allowance is the difference, if any, between the loan balance outstanding and the value of the impaired loan as determined by either 1) an estimate of the cash flows that the Company expects to receive from the borrower discounted at the loan’s effective rate, or 2) in the case of a collateral-dependent loan, the fair value of the collateral.

The second component of the allowance model is to estimate losses for all loans not considered to be impaired loans. First, loans that have been risk graded by the Company as having more than “standard” risk but are not considered to be impaired are assigned estimated loss percentages generally accepted in the banking industry. Loans that are classified by the Company as having normal credit risk are segregated by loan type, and estimated loss percentages are assigned to each loan type, based on the historical losses, current economic conditions, and operational conditions specific to each loan type.

The reserve estimated for impaired loans is then added to the reserve estimated for all other loans. This becomes the Company’s “allocated allowance.” In addition to the allocated allowance derived from the model, management also evaluates other data such as the ratio of the allowance for loan losses to total loans, net loan growth information, nonperforming asset levels and trends in such data. Based on this additional analysis, the Company may determine that an additional amount of allowance for loan losses is necessary to reserve for probable losses. This additional amount, if any, is the Company’s “unallocated allowance.” The sum of the allocated allowance and the unallocated allowance is compared to the actual allowance for loan losses recorded on the books of the Company and any adjustment necessary for the recorded allowance to equal the computed allowance is recorded as a provision for loan losses. The provision for loan losses is a direct charge to earnings in the period recorded.

Although management uses the best information available to make evaluations, future adjustments may be necessary if economic, operational, or other conditions change. In addition, various regulatory agencies, as an integral part of their examination process, periodically review the Company’s allowance for loan losses. Such agencies may require the Company to recognize additions to the allowance based on the examiners’ judgment about information available to them at the time of their examinations.

For further discussion, see “Nonperforming Assets” and “Allowance for Loan Losses and Loan Loss Experience” below.

Tax Uncertainties

The Company reserves for tax uncertainties in instances when it has taken a position on a tax return that may differ from the opinion of the applicable taxing authority. In accounting for tax contingencies, the Company assesses the relative merits and risks of certain tax transactions, taking into account statutory, judicial and regulatory guidance in the context of the Company's tax position. For those matters where it is probable that the Company will have to pay additional taxes, interest or penalties and a loss or range of losses can be reasonably estimated, the Company records reserves in the consolidated financial statements. For those matters where it is reasonably possible but not probable that the Company will have to pay additional taxes, interest or penalties and the loss or range of losses can be reasonably estimated, the Company only makes disclosures in the notes and does not record reserves in the consolidated financial statements. The process of concluding that a loss is reasonably possible or probable and estimating the amount of loss or range of losses and related tax reserves is inherently subjective and future changes to the reserve may be necessary based on changes in management's intent, tax law or related interpretations, or other functions.

The section below entitled “Income Taxes” and Note 12 to the consolidated financial statements include information related to a tax loss contingency accrual that was recorded in 2005. For 2004, the Company had determined that this same tax uncertainty required disclosure, but not loss accrual.

Intangible Assets

Due to the estimation process and the potential materiality of the amounts involved, the Company has also identified the accounting for intangible assets as an accounting policy critical to the Company’s consolidated financial statements.

When the Company completes an acquisition transaction, the excess of the purchase price over the amount by which the fair market value of assets acquired exceeds the fair market value of liabilities assumed represents an intangible asset. The Company must then determine the identifiable portions of the intangible asset, with any remaining amount classified as goodwill. Identifiable intangible assets associated with these acquisitions are generally amortized over the estimated life of the related asset, whereas goodwill is tested annually for impairment, but not systematically amortized. Assuming no goodwill impairment, it is beneficial to the Company’s future earnings to have a lower amount assigned to identifiable intangible assets and higher amount of goodwill as opposed to having a higher amount considered to be identifiable intangible assets and a lower amount classified as goodwill.

For the Company, the primary identifiable intangible asset typically recorded in connection with a whole bank or bank branch acquisition is the value of the core deposit intangible, whereas when the Company acquires an insurance agency, the primary identifiable intangible asset is the value of the acquired customer list. Determining the amount of identifiable intangible assets and their average lives involves multiple assumptions and estimates and is typically determined by performing a discounted cash flow analysis, which involves a combination of any or all of the following assumptions: customer attrition/runoff, alternative funding costs, deposit servicing costs, and discount rates. The Company typically engages a third party consultant to assist in each analysis. For the whole bank and bank branch transactions recorded to date, the core deposit intangibles have generally been estimated to have a life ranging from seven to ten years, with an accelerated rate of amortization. For insurance agency acquisitions, the identifiable intangible assets related to the customer lists were determined to have a life of ten to fifteen years, with amortization occurring on a straight-line basis.

Subsequent to the initial recording of the identifiable intangible assets and goodwill, the Company amortizes the identifiable intangible assets over their estimated average lives, as discussed above. In addition, on at least an annual basis, goodwill is evaluated for impairment by comparing the fair value of the Company’s reporting units to their related carrying value, including goodwill (the Company’s community banking operation is its only

material reporting unit). At its last evaluation, the fair value of the Company’s community banking operation exceeded its carrying value, including goodwill. If the carrying value of a reporting unit were ever to exceed its fair value, the Company would determine whether the implied fair value of the goodwill, using a discounted cash flow analysis, exceeded the carrying value of the goodwill. If the carrying value of the goodwill exceeded the implied fair value of the goodwill, an impairment loss would be recorded in an amount equal to that excess. Performing such a discounted cash flow analysis would involve the significant use of estimates and assumptions.

The Company reviews identifiable intangible assets for impairment whenever events or changes in circumstances indicate that the carrying value may not be recoverable. The Company’s policy is that an impairment loss is recognized, equal to the difference between the asset’s carrying amount and its fair value, if the sum of the expected undiscounted future cash flows is less than the carrying amount of the asset. Estimating future cash flows involves the use of multiple estimates and assumptions, such as those listed above.

MERGER AND ACQUISITION ACTIVITY

The Company did not complete any acquisitions in 2004 or 2005. The Company completed two branch purchases in 2006, as follows:

(a) On July 7, 2006, the Company completed the purchase of a branch of First Citizens Bank located in Dublin, Virginia. The Company assumed the branch’s $21 million in deposits and did not purchase any loans in this transaction. The primary reason for this acquisition was to increase the Company’s presence in southwestern Virginia, a market in which the Company already had three branches with a large customer base. The Company paid a deposit premium for the branch of approximately $994,000, all of which is deductible for tax purposes. The identifiable intangible asset associated with the fair value of the core deposit base, as determined by an independent consulting firm, was determined to be $269,000 and is being amortized as expense on an accelerated basis over an eight year period based on an amortization schedule provided by the consulting firm. The weighted-average amortization period is approximately 2.2 years. The remaining intangible asset of $725,000 has been classified as goodwill, and thus is not being systematically amortized, but rather is subject to an annual impairment test. The primary factor that contributed to a purchase price that resulted in recognition of goodwill was the Company��s desire to expand its presence in southwestern Virginia with facilities, operations and experienced staff in place. This branch’s operations are included in the accompanying Consolidated Statements of Income beginning on the acquisition date of July 7, 2006. Historical pro forma information is not presented due to the immateriality of this transaction to the overall consolidated financial statements of the Company.

(b) On September 1, 2006, the Company completed the purchase of a branch of Bank of the Carolinas in Carthage, North Carolina. The Company assumed the branch’s $24 million in deposits and $6 million in loans. The primary reason for this acquisition was to increase the Company’s presence in Moore County, a market in which the Company already had ten branches with a large customer base. The Company paid a deposit premium for the branch of approximately $1,768,000, all of which is deductible for tax purposes. The identifiable intangible asset associated with the fair value of the core deposit base, as determined by an independent consulting firm, was determined to be approximately $235,000 and is being amortized as expense on an accelerated basis over a thirteen year period based on an amortization schedule provided by the consulting firm. The weighted-average amortization period is approximately 3.2 years. The remaining intangible asset of $1,533,000 has been classified as goodwill, and thus is not being systematically amortized, but rather is subject to an annual impairment test. The primary factor that contributed to a purchase price that resulted in recognition of goodwill was the Company’s desire to expand in an existing high-growth market with facilities, operations and experienced staff in place. This branch’s operations are included in the accompanying Consolidated Statements of Income beginning on the acquisition date of September 1, 2006. Historical pro forma information is not presented due to the immateriality of this transaction to the overall consolidated financial statements of the Company.

See Note 2 and Note 6 to the consolidated financial statements for additional information regarding intangible assets.

ANALYSIS OF RESULTS OF OPERATIONS

Net interest income, the “spread” between earnings on interest-earning assets and the interest paid on interest-bearing liabilities, constitutes the largest source of the Company’s earnings. Other factors that significantly affect operating results are the provision for loan losses, noninterest income such as service fees and noninterest expenses such as salaries, occupancy expense, equipment expense and other overhead costs, as well as the effects of income taxes.

2006 Compared to 2005

Overview - Net income was 20.0% higher in 2006 than in 2005. Both years had unusual items of expense that negatively impacted earnings. In 2006, a merchant credit card loss totaling $1.9 million, or $0.08 per diluted share (after-tax) negatively impacted earnings, while in 2005, the Company recorded a tax loss related to an unfavorable state tax audit amounting to $4.3 million, or $0.30 per diluted share. Excluding those items, net income would have been essentially unchanged in 2006 compared to 2005. The positive impact on earnings of high growth in loans and deposits during 2006 was offset by a lower net interest margin and higher expenses that were associated with the Company’s growth.

| Financial Highlights | | | | | | | |

| ($ in thousands except per share data) | | 2006 | | 2005 | | Change |

| | | | | | | | |

| Earnings | | | | | | | | | | |

| Net interest income | | $ | 74,536 | | | 68,591 | | | 8.7 | % |

| Provision for loan losses | | | 4,923 | | | 3,040 | | | 61.9 | % |

| Noninterest income | | | 14,310 | | | 15,004 | | | -4.6 | % |

| Noninterest expenses | | | 53,198 | | | 47,636 | | | 11.7 | % |

| Income before income taxes | | | 30,725 | | | 32,919 | | | -6.7 | % |

| Income tax expense | | | 11,423 | | | 16,829 | | | -32.1 | % |

| Net income | | $ | 19,302 | | | 16,090 | | | 20.0 | % |

| | | | | | | | | | | |

| Net income per share | | | | | | | | | | |

| Basic | | $ | 1.35 | | | 1.14 | | | 18.4 | % |

| Diluted | | | 1.34 | | | 1.12 | | | 19.6 | % |

| | | | | | | | | | | |

| At Year End | | | | | | | | | | |

| Assets | | $ | 2,136,624 | | | 1,801,050 | | | 18.6 | % |

| Loans | | | 1,740,396 | | | 1,482,611 | | | 17.4 | % |

| Deposits | | | 1,695,679 | | | 1,494,577 | | | 13.5 | % |

| | | | | | | | | | | |

| Ratios | | | | | | | | | | |

| Return on average assets | | | 1.00 | % | | 0.94 | % | | | |

| Return on average equity | | | 11.83 | % | | 10.39 | % | | | |