January 2017 Bank Local. www.localfirstbank.com First Bank

_________________________________________________________________ www.localfirstbank.com FIRST BANCORP Important Information _________________________________________________________________ 2 Forward Looking Statements Information in this presentation contains forward - looking statements within the meaning of the Private Securities Litigation Reform Act of 1 995. These statements involve risks and uncertainties that could cause actual results to differ materially, including without limitation , reduced earnings due to larger than expected credit losses in the sectors of our loan portfolio secured by real estate due to economic factors, including declining real estate values, increasing interest rates. increasing unemployment, or changes in payment behavior or other factors; reduced earnings due to larger credit losses because our loans are concentrated by loan type, industry segment, borrower type, or location of the borrower or collateral; the rate of delinquencies and amount of loans charged - off; the adequacy of the l evel of our allowance for loan losses and the amount of loan loss provisions required in future periods, costs or difficulties related to the integration of the companies we acquired or may acquire may be greater than expected ; results of examinations by our regulatory authorities, including the possibility that the regulatory authorities may , among other things , require us to increase our allowance for loan losses or writedown assets; the amount of our loan portfolio collateralized by real estate, and the weakness in the commercial real estate market; our ability to maintain appropriate levels of capital; adverse changes in asset quality and resulting credit risk - related losses and expenses ; increased funding costs due to market illiquidity , increased competition for funding, and increased regulatory requirements with regard to funding; significant increases in competitive pressure in the banking and financial services industries; changes in political conditions or the legislative or regulatory environment, including the effect of recent financial reform legislation on the banking industry; general economic conditions, either nationally or regionally and especially in our primary service area, becoming less favorable than expected resulting in, among other things, a deterioration in credit quality; our ability to retain our existing customers, including our deposit relationships; changes occurring in business conditions and inflation; changes in monetary and tax policies; ability of borrowers to repay loans; risks associated with a failure in or breach of our operational or security systems or infrastructure, or those of our third party vendors and other service providers or other third parties, including as a result of cyber attacks, which could disrupt our businesses. result in the disclosure or misuse of confidential or proprietary information, damage our reputation, increase our costs and cause losses; changes in accounting principles, policies or guidelines; changes in the assessment of whether a deferred tax valuation allowance is necessary; our reliance on secondary sources such as FHLB advances, sales of securities and loans, federal funds lines of credit from correspondent banks and out - of - marker time deposits, to meet our liquidity needs; loss of consumer confidence and economic disruptions resulting from terrorist activities or other military actions ; and changes in the securities markets. Additional factors that could cause actual results to differ materially are discussed in the Company's filings with the Securities and Exchange Commission ("SEC"), including without limitation its Annual Report on Form 10 - K, its Quarterly Reports on Form 10 - Q, and its Current Reports Form 8 - K . The forward - looking statements in this presentation speak only as of the date of the presentation. and the Company does not assume any obligation to update such forward - looking statements. Non - GAAP Measures Statements included in this presentation include non - GAAP measures and should be read along with the earnings release and accompanying Financial Summary for the quarter and year ended December 31, 2016 which provide a reconciliation of non - GAAP measures to GAAP measures. Management believes that these non - GAAP measures provide additional useful information that allows readers to evaluate the ongoing performance of the Company. Non - GAAP measures should not be considered as an alternative to any measure of performance or financial condition as promulgated under GAAP, and investors should consider the Company's performance and financial condition as reported under GAAP and all other relevant information when assessing the performance or financial condition of the Company. Non - GAAP measures have limitations as analytical tools, and investors should not consider them in isolation or as a substitute for analysis of the Company's results or financial condition as reported under GAAP.

_________________________________________________________________ www.localfirstbank.com FIRST BANCORP 3 2016 Highlights _________________________________________________________________ Results / Strategic Initiatives Q4 2016 EPS of $0.40 - up 21.2% over Q4 2015 Loan Growth - 8.9% Q4 Annualized, 7.6% year - over - year Continued expansion into high growth markets – Charlotte, Raleigh, Greensboro Branch exchange Termination of all FDIC Loss Share Agreements • One time charge of $5.7 million • Indemnification asset expense eliminated for future periods Noninterest Income • Rollout of nationwide SBA lending platform - $1.4 million in Q3 & Q4 loan sale gains • SBA c onsulting firm a cquisition – Fees of $3.2 million for May - December 2016 • Insurance agency income – $1.9 million in 2016 - up 108% – 1/1/16 acquisition Carolina Bank integration planning

_________________________________________________________________ www.localfirstbank.com FIRST BANCORP Company Profile* _________________________________________________________________ 4 * All data as of 12/31/16; Market Capitalization as of 1/24/17 Bank Holding Company First Bancorp Subsidiary Bank First Bank Headquarters Southern Pines, North Carolina Established 1935 as Bank of Montgomery Assets $3.6 billion Loans $2.7 billion Deposits $2.9 billion Branches 89 in NC & SC Employees 833 full - time equivalent employees Ranking 7 th largest bank headquartered in NC Market Capitalization $595 million – Ticker FBNC Insider Ownership 5% Institutional Ownership 49% Member of Russell 2000 Yes

_________________________________________________________________ www.localfirstbank.com FIRST BANCORP 5 North Carolina’s Most Populous Markets Wilmington Asheville Charlotte Raleigh Winston - Salem Greensboro Fayetteville Greenville Less than 50 50 - 99 100 - 249 250 - 499 500 - 999 1,000 - 1,999 2,000 units or more Housing Units per Square Mile

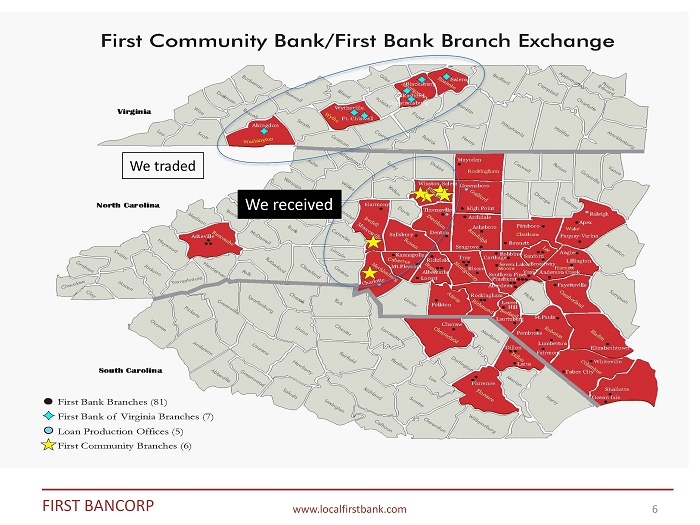

_________________________________________________________________ www.localfirstbank.com FIRST BANCORP 6 We traded We received

_________________________________________________________________ www.localfirstbank.com FIRST BANCORP 7 Branch Network Financial Highlights Company Overview Headquarters Greensboro, NC Year Established 1996 Balance Sheet Total Assets $706 Total Loans 491 Deposits 601 Loans / Deposits 81.7% % Core Deposits 87.1 LTM Profitability ROAA 0.75% ROATCE 8.67 Net Interest Margin 3.71 Efficiency Ratio 75.1 Noninterest Inc. / Avg. Assets 1.82 Noninterest Exp. / Avg. Assets 4.03 Asset Quality NPAs / Assets 2.86% NPAs (excl. TDRs) / Assets 1.15 Reserves / Loans 1.22 Capitalization Tang. Com. Equity / Assets 8.88% Leverage Ratio 9.74 CET1 Ratio 12.62 Total Capital Ratio 14.40 Carolina Bank Holdings, Inc. - Announced 6/22/16 (dollars in millions)

_________________________________________________________________ www.localfirstbank.com FIRST BANCORP 8

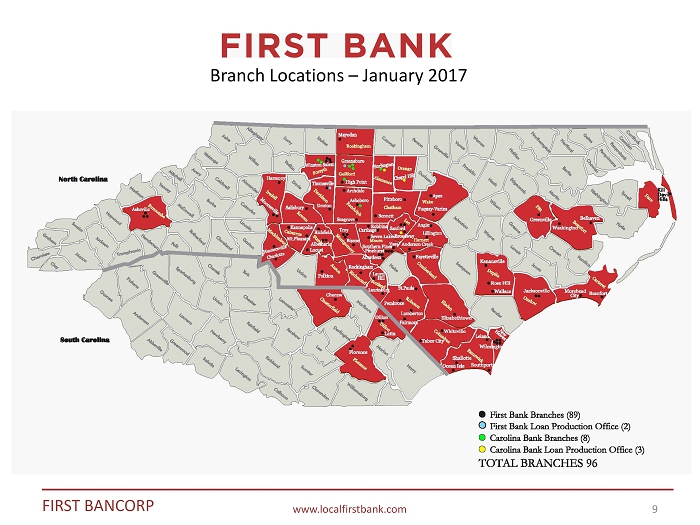

_________________________________________________________________ www.localfirstbank.com FIRST BANCORP 9 Branch Locations – January 2017

_________________________________________________________________ www.localfirstbank.com FIRST BANCORP Bank Consolidation in North Carolina Community Banks at 12/31/14 * Asset Size 1 Yadkin Bank $7.5 billion 2 Bank of North Carolina $5.7 billion 3 First Bancorp $3.5 billion 4 Square 1 Bank $3.1 billion 5 Park Sterling Bank $3.1 billion 6 Home Trust Bank $2.7 billion 7 NewBridge Bank $2.6 billion 8 CommunityOne Bank $2.4 billion 9 Southern Bank & Trust $2.4 billion 10 Fidelity Bank $1.8 billion 11 Paragon Commercial Bank $1.3 billion 12 Peoples Bank $1.1 billion 13 Macon Bank $1.1 billion 14 Piedmont Federal Savings Bank $0.9 billion 15 First South Bank $0.9 billion 16 High Point Bank & Trust $0.9 billion 10 * Banks with total assets less than $20 billion headquartered in North Carolina

_________________________________________________________________ www.localfirstbank.com FIRST BANCORP 11 Our Promise to Service Excellence “We help our customers realize their dreams by providing financial solutions and building trusted relationships.”

_________________________________________________________________ www.localfirstbank.com FIRST BANCORP 12 KNOWLEDGE & ACCURACY We employ the best associates and ensure all are well trained, establish quality standards, and hold each other accountable. COURTEOUS SERVICE We treat customers and fellow associates with respect, effectively communicate, and celebrate our unique contributions. CONVENIENCE & EASE Our customers choose when, where and how they do business with us. SAFETY & SOUNDNESS We ensure long term financial stability by enhancing trust and confidence and providing a safe environment. Service Excellence Principles

_________________________________________________________________ www.localfirstbank.com FIRST BANCORP 13 Percentages annualized where applicable Q4 2016 Q4 2015 Change Net income $8.4 million $6.8 million +23.6% EPS Common - Diluted $0.40 $0.33 +21.2% Return on Average Assets 0.94% 0.82% +12 bps Return on Avg. Common Equity 9.17% 7.96% +121 bps Loan s $2.7 billion $2.5 billion +7.6% Deposit s $2.9 billion $2.8 billion +4.8% Nonperforming Assets to Total Assets 1.64% 2.66% - 102 bps Net Interest Margin (2) 3.94% 4.05% - 11 bps Cost of Funds 0.25% 0.24% + 1 bp Noninterest Income (Core) (3) /Avg. Assets 1.10% 0.91% +19 bps Q4 2016 – Highlights (1) (1) All information at or for the periods ended December 31, 2016 is preliminary and based on Company information available at ti me of presentation. (2) Tax - equivalent net - interest income divided by average earning assets. (3) Excludes foreclosed property gains/losses, indemnification asset expense, other miscellaneous gains/losses.

_________________________________________________________________ www.localfirstbank.com FIRST BANCORP 14 2016 2015 Change Net income - common $27.3 million $26.4 million +3.4% EPS Common - Diluted $1.33 $1.30 +2.3% Nonperforming Assets $59.1 million $89.3 million - 33.8% Net Interest Margin (2) 4.03% 4.13% - 10 bps Cost of Funds 0.25% 0.24% +1 bp Tier I Leverage Ratio 10.09% 10.38% - 29 bps Total Risk Based Capital Ratio 13.33% 14.45% - 112 bps Tangible Book Value Per Share - Common $13.85 $13.56 +2.1% 2016 – Full Year Highlights (1) (1) All information at or for the periods ended December 31, 2016 is preliminary and based on Company information available at ti me of presentation. (2) Tax - equivalent net - interest income divided by average earning assets.

_________________________________________________________________ www.localfirstbank.com FIRST BANCORP Investment Thesis _________________________________________________________________ 15 ▪ Bank that offers many of the product capabilities found in larger regional banks but delivers those services with a local community bank focus ▪ Mobile Banking, Wealth Management, Trust Services, Credit Card, Treasury Services, Insurance, and Mortgage Banking ▪ Centered in one of the fastest - growing regions in the U.S . ▪ Focused on high growth markets ▪ Stable, low cost core deposit franchise ▪ Built over 80 years of serving our communities ▪ Strength of rural markets ▪ 2016 c ost of funds was 0.25% ▪ Strong and Improving Performance Metrics ▪ Conservative Balance Sheet ▪ Minimal credit risk in investment portfolio ▪ Core funded ▪ In market loan portfolio – almost no participations • Market disruptions provide opportunity

_________________________________________________________________ www.localfirstbank.com FIRST BANCORP 16 16 16 ▪ Closing stock price on January 25, 2017 = $29.06 ▪ Price to tangible book value – 2.10x ▪ Based on 12/31/16 tangible book value – common – $13.85 Valuation – Price to Tangible Common Book Value _________________________________________________________________ .95x 1.33x 1.71x 1.96x 1.97x 2.1x 2.18x 2.21x 2.24x 2.41x 2.46x 2.67x 2.97x 2.98x SBNC HTBI NKSH CBF AMNB FBNC PSTB FCBC UCBI UBSH CARO TOWN SSB BNCN Price / Tangible Common Book Value Median = 2.19x

_________________________________________________________________ www.localfirstbank.com FIRST BANCORP 17 17 • Price to trailing twelve month earnings – 21.8x • Based on trailing 12 month diluted common earnings per share of $1.33 and 1/25/17 share price of $29.06 • 2016 Full Year Negatively Impacted by Q3 FDIC Loss Share Agreement Termination • Based on EPS of $1.60 (Q4 2016 annualized), the price to earnings ratio is 18.2x Valuation – Price to Trailing 12 Month Earnings _________________________________________________________________ 14.1x 18.x 18.9x 20.1x 20.7x 21.3x 21.5x 21.6x 21.8x 26.3x 29.x 29.7x 31.4x 34.9x SBNC FCBC AMNB NKSH UCBI UBSH CARO SSB FBNC BNCN CBF TOWN PSTB HTBI Price / Trailing 12 Months Earnings Median = 21.5x