UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-5066

Legg Mason Partners Arizona Municipals Fund, Inc.

(Exact name of registrant as specified in charter)

| 125 Broad Street, New York, NY | 10004 | |

| (Address of principal executive offices) | (Zip code) | |

Robert I. Frenkel, Esq.

Legg Mason & Co., LLC

300 First Stamford Place, 4th Fl.

Stamford, CT 06902

(Name and address of agent for service)

Registrant’s telephone number, including area code: (800) 451-2010

Date of fiscal year end: May 31,

Date of reporting period: May 31, 2006

| ITEM 1. | REPORT TO STOCKHOLDERS. |

The Annual Report to Stockholders is filed herewith.

ANNUAL REPORT

MAY 31, 2006

Legg Mason Partners

Arizona Municipals Fund, Inc.

INVESTMENT PRODUCTS: NOT FDIC INSURED Ÿ NO BANK GUARANTEE Ÿ MAY LOSE VALUE

Legg Mason Partners

Arizona Municipals Fund, Inc.

Annual Report • May 31, 2006

What’s

Inside

Fund Objective

The Fund seeks to provide Arizona investors with the maximum amount of income exempt from Federal and Arizona state income taxes* as is consistent with the preservation of capital.

| * | Certain investors may be subject to the Federal Alternative Minimum Tax and state and local taxes will apply. Capital gains, if any, are fully taxable. Please consult your personal tax adviser. |

| I | ||

| 1 | ||

| 5 | ||

| 6 | ||

| 8 | ||

| 9 | ||

| 10 | ||

| 15 | ||

| 16 | ||

| 17 | ||

| 18 | ||

| 21 | ||

| 31 | ||

| 32 | ||

| 36 | ||

“Smith Barney”, “Salomon Brothers” and “Citi” are service marks of Citigroup, licensed for use by Legg Mason as the names of funds and investment managers. Legg Mason and its affiliates, as well as the Fund’s investment manager, are not affiliated with Citigroup.

R. JAY GERKEN, CFA

Chairman, President and Chief Executive Officer

Dear Shareholder,

The U.S. economy was generally strong during the one-year reporting period. After expanding 3.3% in the second quarter of 2005, third quarter gross domestic product (“GDP”)i advanced 4.1%. GDP growth then slipped to 1.7% in the fourth quarter. This marked the first quarter in which GDP growth did not surpass 3.0% in nearly three years. However, as expected, the economy rebounded sharply in the first quarter of 2006. During this time, GDP rose 5.6%, its best showing since the third quarter of 2003. The economic turnaround was prompted by both strong consumer and business spending. In addition, the U.S. Labor Department reported that unemployment was 4.6% in May, its lowest rate since July 2001.

The Federal Reserve Board (“Fed”)ii continued to raise interest rates during the reporting period. Despite the “changing of the guard” from Fed Chairman Alan Greenspan to Ben Bernanke in early 2006, it was “business as usual” for the Fed, as it raised short-term interest rates eight times during the period. Since it began its tightening campaign in June 2004, the Fed has increased rates 16 consecutive times, bringing the federal funds rateiii from 1.00% to 5.00%. Coinciding with its latest rate hike in May 2006, the Fed said that the “extent and timing” of further increases would depend on future economic data. After the end of the Fund’s reporting period, at its June meeting, the Fed once again raised the federal funds rate by 0.25% to 5.25%.

Both short- and long-term yields rose over the reporting period. During the 12-months ended May 31, 2006, two-year Treasury yields increased from 3.60% to 5.04%. Over the same period, 10-year Treasury yields moved from 4.00% to 5.12%. Short-term rates rose in concert with the Fed’s repeated tightening, while long-term rates rose on fears of mounting inflationary pressures. Looking at the municipal market, yields of both two- and 10-year securities also rose over the reporting period.

Legg Mason Partners Arizona Municipals Fund, Inc. I

Please read on for a more detailed look at prevailing economic and market conditions during the Fund’s fiscal year and to learn how those conditions have affected Fund performance.

Information About Your Fund

As you may be aware, several issues in the mutual fund industry have come under the scrutiny of federal and state regulators. The Fund’s Manager and some of its affiliates have received requests for information from various government regulators regarding market timing, late trading, fees, and other mutual fund issues in connection with various investigations. The regulators appear to be examining, among other things, the Fund’s response to market timing and shareholder exchange activity, including compliance with prospectus disclosure related to these subjects. The Fund has been informed that the Manager and its affiliates are responding to those information requests, but are not in a position to predict the outcome of these requests and investigations.

Important information concerning the Fund and its Manager with regard to recent regulatory developments is contained in the Notes to Financial Statements included in this report.

As always, thank you for your confidence in our stewardship of your assets. We look forward to helping you continue to meet your financial goals.

Sincerely,

R. Jay Gerken, CFA

Chairman, President and Chief Executive Officer

July 14, 2006

II Legg Mason Partners Arizona Municipals Fund, Inc.

| i | Gross domestic product is a market value of goods and services produced by labor and property in a given country. |

| ii | The Federal Reserve Board is responsible for the formulation of a policy designed to promote economic growth, full employment, stable prices, and a sustainable pattern of international trade and payments. |

| iii | The federal funds rate is the interest rate that banks with excess reserves at a Federal Reserve district bank charge other banks that need overnight loans. |

Legg Mason Partners Arizona Municipals Fund, Inc. III

|  | JOSEPH P. DEANE (left) Vice President and DAVID T. FARE (right) Vice President and |

Special Shareholder Notices

Prior to April 7, 2006, the Fund operated under the name Smith Barney Arizona Municipals Fund Inc. The Fund’s investment strategy and objective have not changed.

As part of the continuing effort to integrate investment products managed by the advisers acquired with Citigroup’s asset management business, Legg Mason, Inc. (“Legg Mason”) has recommended various Fund actions in order to streamline product offerings, standardize share class pricing features, eliminate redundancies and improve efficiencies within the organization. At Board meetings held during June and July 2006, the Fund’s Board reviewed and approved these recommendations, and provided authorization to move ahead with proxy solicitations for those matters needing shareholder approval.

The Fund’s Board has approved the appointment of Legg Mason Partners Fund Advisor, LLC (“LMPFA”) as the Fund’s investment manager effective August 1, 2006. The Fund’s Board has also approved the appointment of Western Asset Management Company (“Western Asset”) as the Fund’s subadviser effective August 1, 2006. The portfolio managers who are responsible for the day-to-day management of the Fund remain the same immediately prior to and immediately after the date of these changes. LMPFA and Western Asset are wholly-owned subsidiaries of Legg Mason.

The Fund’s Board has also approved a reorganization pursuant to which the Fund’s assets would be acquired, and its liabilities assumed by Legg Mason Partners Managed Municipals Fund, Inc. (the “Acquiring Fund”), in exchange for shares of the Acquiring Fund. The Fund would then be liquidated, and shares of the Acquiring Fund would be distributed to Fund shareholders. Proxy materials describing the reorganization, and other initiatives requiring shareholder approval, are expected to be sent to shareholders later in 2006. If shareholder approval is obtained, Fund actions are generally expected to be implemented during the first quarter of 2007.

Effective as of the close of business on July 12, 2006, the Fund was closed to new purchases and exchanges, except for dividend reinvestments and other limited exceptions.

Q. What were the overall market conditions during the Fund’s reporting period?

A. Despite a variety of significant headwinds, the municipal bond market generated positive returns during the one-year period ended May 31, 2006 and outperformed the overall

Legg Mason Partners Arizona Municipals Fund, Inc. 2006 Annual Report 1

taxable bond market. Over that period, the Lehman Brothers Municipal Bond Indexi gained 1.89%, while the Lehman Brothers U.S. Aggregate Indexii returned –0.48%.

Over the last year, the bond market has been impacted by a strong economy, numerous inflationary pressures, and continued rate hikes by the Federal Reserve Board (“Fed”)iii. To gain some perspective on how far we’ve come in terms of interest rates, consider the following; In May 2004, the federal funds rateiv, a barometer of short-term interest rates, was a mere 1.00%, its lowest level in more than 40 years. This was due, in part, to the Fed’s attempt to stimulate the economy in the aftermath of September 11th.

Then, in June 2004, the economy appeared to be on solid footing and the Fed officially ended its accommodative monetary policy by instituting its first rate hike in four years, bringing the federal funds rate from 1.00% to 1.25%. At that time, the Fed telegraphed what it had in mind for short-term rates as it said, “policy accommodation can be removed at a pace that is likely to be measured.” The Fed certainly has been true to its word, as it has now instituted 16 straight 0.25% rate hikes through the end of May 2006, bringing the federal funds rate to 5.00% at the end of the reporting period. After the end of the Fund’s reporting period, at its June meeting, the Fed once again raised the federal funds rate by 0.25% to 5.25%.

Given the solid economy and rising rate environment, both short- and long-term Treasury yields rose over the reporting period. For the 12-months ended May 31, 2006, two-year Treasury yields increased from 3.60% to 5.04%. Over the same period, 10-year Treasury yields moved from 4.00% to 5.12%. During the reporting period, both short- and longer-term municipal yields also rose, albeit to a lesser extent than equal durationv Treasuries. This, coupled with improving balance sheets in many states, in our opinion, helped municipal securities to outperform taxable bonds over the last year.

Performance Review

For the 12 months ended May 31, 2006, Class A shares of the Legg Mason Partners Arizona Municipals Fund, Inc., excluding sales charges, returned 4.72%. These shares outperformed the Lipper Arizona Municipal Debt Funds Category Average,1 which increased 1.42%. The Fund’s unmanaged benchmark, the Lehman Brothers Municipal Bond Index, returned 1.89% for the same period.

Certain investors may be subject to the Federal Alternative Minimum Tax, and state and local taxes may apply. Capital gains, if any, are fully taxable. Please consult your personal tax or legal adviser.

| 1 | Lipper, Inc. is a major independent mutual-fund tracking organization. Returns are based on the 12-month period ended May 31, 2006, including the reinvestment of all distributions, including returns of capital, if any, calculated among the 32 funds in the Fund’s Lipper category and excluding sales charges. |

2 Legg Mason Partners Arizona Municipals Fund, Inc. 2006 Annual Report

| Performance Snapshot as of May 31, 2006 (excluding sales charges) (unaudited) | ||||

| 6 months | 12 months | |||

Arizona Municipals Fund — Class A Shares | 2.44% | 4.72% | ||

Lehman Brothers Municipal Bond Index | 1.52% | 1.89% | ||

Lipper Arizona Municipal Debt Funds Category Average | 1.37% | 1.42% | ||

| The performance shown represents past performance. Past performance is no guarantee of future results and current performance may be higher or lower than the performance shown above. Principal value, investment returns and yields will fluctuate and investors’ shares, when redeemed, may be worth more or less than their original cost. Current reimbursements and/or fee waivers are voluntary, and may be reduced or terminated at any time. Absent these reimbursements or waivers, performance would have been lower. To obtain performance data current to the most recent month-end, please visit our website at www.leggmason.com/InvestorServices. | ||||

| Excluding sales charges, Class B shares returned 2.14% and Class C shares returned 2.28% over the six months ended May 31, 2006. Excluding sales charges, Class B shares returned 4.08% and Class C shares returned 4.12% over the twelve months ended May 31, 2006. All share class returns assume the reinvestment of all distributions, including returns of capital, if any, at net asset value and the deduction of all Fund expenses. Returns have not been adjusted to include sales charges that may apply when shares are purchased or the deduction of taxes that a shareholder would pay on Fund distributions. | ||||

| The 30-Day SEC Yield for Class A, Class B and Class C shares was 4.13%, 3.73% and 3.86%, respectively. Absent reimbursements or fee waivers, the 30-Day SEC Yield for Class A, Class B and Class C shares would have been 3.84%, 3.43% and 3.56%, respectively. | ||||

| The 30-Day SEC Yield is the average annualized net investment income per share for the 30 days ended May 31, 2006 and is subject to change. | ||||

| Lipper, Inc. is a major independent mutual-fund tracking organization. Returns are based on the period ended May 31, 2006, including the reinvestment of all distributions, including returns of capital, if any, calculated among the 32 funds for the six-month period and among the 32 funds for the 12-month period in the Fund’s Lipper category and excluding sales charges. | ||||

Q. What were the most significant factors affecting Fund performance?

What were the leading contributors to performance?

A. Given the rising interest rate environment and expectations for further Fed tightening, we maintained a defensive approach in terms of the Fund’s maturity. As such, the Fund’s duration was generally shorter than its benchmark index. This proved to be beneficial, as bond prices generally fall when interest rates rise. In addition, we were able to use the proceeds from our cash flows and coupons and reinvest that money into municipal bonds offering higher coupons.

Throughout the reporting period, we also emphasized a well-diversified portfolio, with holdings from a diverse array of market segments that we believed had favorable risk/reward characteristics.

Legg Mason Partners Arizona Municipals Fund, Inc. 2006 Annual Report 3

What were the leading detractors from performance?

A. During the reporting period, we continued to maintain a high quality portfolio. This had a somewhat negative effect on returns, as lower-rated, more speculative municipals generated better results over the period. However, given the prevailing market environment and the Fund’s investment objective, we believed a higher quality approach was appropriate.

Q. Were there any significant changes to the Fund during the reporting period?

A. There were no significant changes during the reporting period, as we maintained a high quality portfolio and were defensively positioned.

Thank you for your investment in the Legg Mason Partners Arizona Municipals Fund, Inc. As ever, we appreciate that you have chosen us to manage your assets and we remain focused on achieving the Fund’s investment goals.

Sincerely,

Joseph P. Deane Vice President and Investment Officer |

David T. Fare, CFA Vice President and Investment Officer |

July 14, 2006

The information provided is not intended to be a forecast of future events, a guarantee of future results or investment advice. Views expressed may differ from those of the firm as a whole.

Risks: Keep in mind, the Fund’s investments are subject to interest rate and credit risks. As interest rates rise, bond prices fall, reducing the value of the Fund’s share price. Portfolio holdings may include lower-rated securities (commonly known as “junk bonds”) that present greater risk of loss of principal than higher rated securities. The Fund may use derivatives, such as options and futures, which can be illiquid, may disproportionately increase losses, and have a potentially large impact on Fund performance. Please see the Fund’s prospectus for information on these and other risks.

All index performance reflects no deduction for fees, expenses or taxes. Please note an investor cannot invest directly in an index.

| i | The Lehman Brothers Municipal Bond Index is a broad measure of the municipal bond market with maturities of at least one year. |

| ii | The Lehman Brothers U.S. Aggregate Index is a broad-based bond index comprised of government, corporate, mortgage and asset-backed issues, rated investment grade or higher, and having at least one year to maturity. |

| iii | The Federal Reserve Board is responsible for the formulation of a policy designed to promote economic growth, full employment, stable prices, and a sustainable pattern of international trade and payments. |

| iv | The federal funds rate is the interest rate that banks with excess reserves at a Federal Reserve district bank charge other banks that need overnight loans. |

| v | Duration is a common gauge of the price sensitivity of a fixed income asset or portfolio to a change in interest rates. |

4 Legg Mason Partners Arizona Municipals Fund, Inc. 2006 Annual Report

Legg Mason Partners Arizona Municipals Fund, Inc. 2006 Annual Report 5

Example

As a shareholder of the Fund, you may incur two types of costs: (1) transaction costs, including front-end and back-end sales charges (loads) on purchase payments and (2) ongoing costs, including management fees; distribution and/or service (12b-1) fees; and other Fund expenses. This example is intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds.

This example is based on an investment of $1,000 invested on December 1, 2005 and held for the six months ended May 31, 2006.

Actual Expenses

The table below titled “Based on Actual Total Return” provides information about actual account values and actual expenses. You may use the information provided in this table, together with the amount you invested, to estimate the expenses that you paid over the period. To estimate the expenses you paid on your account, divide your ending account value by $1,000 (for example, an $8,600 ending account value divided by $1,000 = 8.6), then multiply the result by the number under the heading entitled “Expenses Paid During the Period”.

| Based on Actual Total Return(1) | |||||||||||||||

| Actual Total Return Without Sales Charges(2) | Beginning Account Value | Ending Account Value | Annualized Expense Ratio | Expenses Paid During the Period(3) | |||||||||||

Class A | 2.44 | % | $ | 1,000.00 | $ | 1,024.40 | 0.74 | % | $ | 3.73 | |||||

Class B | 2.14 | 1,000.00 | 1,021.40 | 1.34 | 6.75 | ||||||||||

Class C | 2.28 | 1,000.00 | 1,022.80 | 1.27 | 6.40 | ||||||||||

| (1) | For the six months ended May 31, 2006. |

| (2) | Assumes reinvestment of all distributions, including returns of capital, if any, at net asset value and does not reflect the deduction of the applicable sales charge with respect to Class A shares or the applicable contingent deferred sales charges (“CDSC”) with respect to Class B and C shares. Total return is not annualized, as it may not be representative of the total return for the year. Performance figures may reflect voluntary fee waivers and/or expense reimbursements. Past performance is no guarantee of future results. In the absence of voluntary fee waivers and/or expense reimbursements, the total return would have been lower. |

| (3) | Expenses (net of voluntary fee waivers and/or expense reimbursements) are equal to each class’ respective annualized expense ratio multiplied by the average account value over the period, multiplied by the number of days in the most recent fiscal half-year, then divided by 365. |

6 Legg Mason Partners Arizona Municipals Fund, Inc. 2006 Annual Report

Fund Expenses (unaudited) (continued)

Hypothetical Example for Comparison Purposes

The table below titled “Based on Hypothetical Total Return” provides information about hypothetical account values and hypothetical expenses based on the actual expense ratio and an assumed rate of return of 5.00% per year before expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use the information provided in this table to compare the ongoing costs of investing in the Fund and other funds. To do so, compare the 5.00% hypothetical example relating to the Fund with the 5.00% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the table below are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as front-end or back-end sales charges (loads). Therefore, the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transaction costs were included, your costs would have been higher.

| Based on Hypothetical Total Return(1) | |||||||||||||||

| Hypothetical Annualized Total Return | Beginning Account Value | Ending Account Value | Annualized Expense Ratio | Expenses Paid During the Period(2) | |||||||||||

Class A | 5.00 | % | $ | 1,000.00 | $ | 1,021.24 | 0.74 | % | $ | 3.73 | |||||

Class B | 5.00 | 1,000.00 | 1,018.25 | 1.34 | 6.74 | ||||||||||

Class C | 5.00 | 1,000.00 | 1,018.60 | 1.27 | 6.39 | ||||||||||

| (1) | For the six months ended May 31, 2006. |

| (2) | Expenses (net of voluntary fee waivers and/or expense reimbursements) are equal to each class’ respective annualized expense ratio multiplied by the average account value over the period, multiplied by the number of days in the most recent fiscal half-year, then divided by 365. |

Legg Mason Partners Arizona Municipals Fund, Inc. 2006 Annual Report 7

| Average Annual Total Returns(1) (unaudited) | |||||||||

| Without Sales Charges(2) | |||||||||

| Class A | Class B | Class C | |||||||

Twelve Months Ended 5/31/06 | 4.72 | % | 4.08 | % | 4.12 | % | |||

Five Years Ended 5/31/06 | 3.34 | 2.75 | 2.74 | ||||||

Ten Years Ended 5/31/06 | 4.44 | 3.86 | 3.84 | ||||||

Inception* through 5/31/06 | 5.84 | 4.40 | 4.66 | ||||||

| With Sales Charges(3) | |||||||||

| Class A | Class B | Class C | |||||||

Twelve Months Ended 5/31/06 | 0.55 | % | (0.42 | )% | 3.12 | % | |||

Five Years Ended 5/31/06 | 2.49 | 2.58 | 2.74 | ||||||

Ten Years Ended 5/31/06 | 4.01 | 3.86 | 3.84 | ||||||

Inception* through 5/31/06 | 5.62 | 4.40 | 4.66 | ||||||

| Cumulative Total Returns(1) (unaudited) | |||||||

| Without Sales Charges(2) | |||||||

Class A (5/31/96 through 5/31/06) | 54.34 | % | |||||

Class B (5/31/96 through 5/31/06) | 46.07 | ||||||

Class C (5/31/96 through 5/31/06) | 45.70 | ||||||

| (1) | All figures represent past performance and are not a guarantee of future results. Investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. The returns shown do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. Performance figures may reflect voluntary fee waivers and/or expense reimbursements. In the absence of voluntary fee waivers and/or expense reimbursements, the total return would have been lower. |

| (2) | Assumes reinvestment of all distributions, including returns of capital, if any, at net asset value and does not reflect the deduction of the applicable sales charge with respect to Class A shares or the applicable contingent deferred sales charges (“CDSC”) with respect to Class B and C shares. |

| (3) | Assumes reinvestment of all distributions, including returns of capital, if any, at net asset value. In addition, Class A shares reflect the deduction of the maximum initial sales charge of 4.00%. Class B shares reflect the deduction of a 4.50% CDSC, which applies if shares are redeemed within one year from purchase payment. This CDSC declines by 0.50% the first year after purchase and thereafter by 1.00% per year until no CDSC is incurred. Class C shares reflect the deduction of a 1.00% CDSC, which applies if shares are redeemed within one year from purchase payment. |

| * | Inception dates for Class A, B and C shares are June 1, 1987, November 6, 1992 and December 8, 1994, respectively. |

8 Legg Mason Partners Arizona Municipals Fund, Inc. 2006 Annual Report

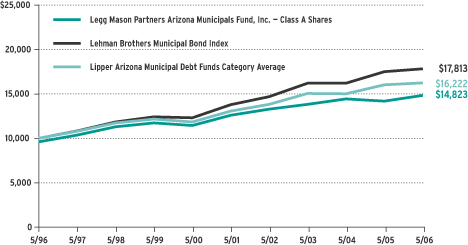

Historical Performance (unaudited)

Value of $10,000 Invested in Class A Shares of Legg Mason Partners Arizona Municipals Fund, Inc. vs. Lehman Brothers Municipal Bond Index and Lipper Arizona Municipal Debt Funds Category Average† (May 1996 — May 2006)

| † | Hypothetical illustration of $10,000 invested in Class A shares on May 31, 1996, assuming deduction of the maximum 4.00% sales charge at the time of investment and reinvestment of all distributions, including returns of capital, if any, at net asset value through May 31, 2006. The Lehman Brothers Municipal Bond Index is a broad based, total return index comprised of investment-grade, fixed rate municipal bonds selected from issues larger than $50 million issued since January 1991. The Index is unmanaged and is not subject to the same management and trading expenses as a mutual fund. Please note that an investor cannot invest directly in an index. The Lipper Arizona Municipal Debt Funds Category Average is composed of the Fund’s peer group of mutual funds (32 funds as of May 31, 2006). The performance of the Fund’s other classes may be greater or less than the Class A shares’ performance indicated on this chart, depending on whether higher or lower sales charges and fees were incurred by shareholders investing in the other classes. |

All figures represent past performance and are not a guarantee of future results. Investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. The returns shown do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. Performance figures may reflect voluntary fee waivers and/or expense reimbursements. In the absence of voluntary fee waivers and/or expense reimbursements, the total return would have been lower.

Legg Mason Partners Arizona Municipals Fund, Inc. 2006 Annual Report 9

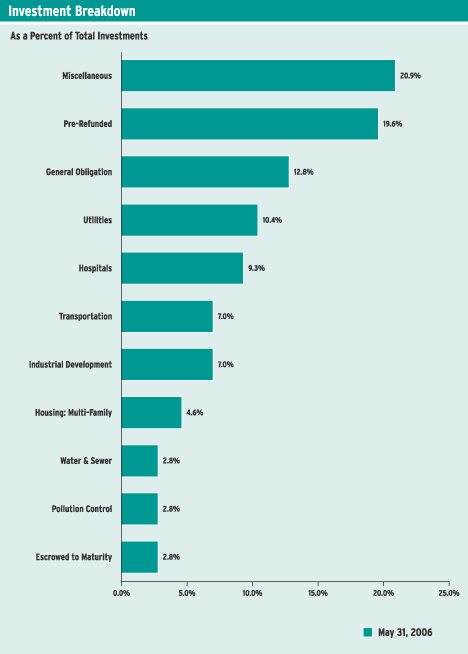

Schedule of Investments (May 31, 2006)

LEGG MASON PARTNERS ARIZONA MUNICIPALS FUND, INC.

| Face Amount | Rating‡ | Security | Value | ||||||

| MUNICIPAL BONDS — 98.0% | |||||||||

| Escrowed to Maturity (a) — 2.7% | |||||||||

| $ | 90,000 | AAA | Arizona State Municipal Financing Program, COP, Series 20, | $ | 90,569 | ||||

Maricopa County, AZ: | |||||||||

| 295,000 | AAA | GO, Elementary School District No. 14, Creighton School Improvement Project of 1990, Series C, FGIC-Insured, | 311,682 | ||||||

| 500,000 | AAA | IDA, Hospital Facilities Revenue, Samaritan Health Services, Series A, MBIA-Insured, 7.000% due 12/1/16 (b) | 605,280 | ||||||

Total Escrowed to Maturity | 1,007,531 | ||||||||

| General Obligation — 12.7% | |||||||||

Maricopa County, AZ, GO, Elementary School District: | |||||||||

| 1,000,000 | A | No. 08, Osborne Elementary School District, 7.500% due 7/1/09 | 1,099,290 | ||||||

| 355,000 | AAA | No. 14, Creighton School Improvement Project of 1990, Series C, FGIC-Insured, 6.500% due 7/1/08 | 374,788 | ||||||

Phoenix, AZ, GO: | |||||||||

| 1,400,000 | AA+ | Series A, 6.250% due 7/1/17 | 1,654,716 | ||||||

| 400,000 | AA+ | Series B, 5.000% due 7/1/22 | 416,548 | ||||||

| 1,000,000 | AAA | Pima County, AZ, Unified School District No. 1, Tucson, | 1,138,740 | ||||||

Total General Obligation | 4,684,082 | ||||||||

| Hospitals — 9.2% | |||||||||

| 1,500,000 | Baa3(c) | Arizona Health Facilities Authority, Hospital Systems Revenue, Phoenix Children’s Hospital, Series A, 6.125% due 11/15/22 | 1,563,525 | ||||||

Maricopa County, AZ, Hospital Revenue, Sun Health Corp.: | |||||||||

| 1,500,000 | BBB | 5.900% due 4/1/09 | 1,549,905 | ||||||

| 285,000 | BBB | Unrefunded Balance, 6.125% due 4/1/18 | 295,679 | ||||||

Total Hospitals | 3,409,109 | ||||||||

| Housing: Multi-Family — 4.5% | |||||||||

| 500,000 | AAA | Maricopa County, AZ, IDA, MFH Revenue, Metro Gardens, Mesa Ridge Project, Series A, MBIA-Insured, 5.650% due 7/1/19 | 502,380 | ||||||

Phoenix, AZ, IDA, MFH Revenue, Ventana Palms Apartments Project, Series A, MBIA-Insured: | |||||||||

| 150,000 | Aaa(c) | 6.100% due 10/1/19 | 159,139 | ||||||

| 950,000 | Aaa(c) | 6.150% due 10/1/29 | 1,008,425 | ||||||

Total Housing: Multi-Family | 1,669,944 | ||||||||

| Industrial Development — 6.3% | |||||||||

| 2,125,000 | NR | Maricopa County, AZ, IDA, MFH Revenue, Stanford Court Apartments, Series B, 6.250% due 7/1/18 (d)(e) | 212,500 | ||||||

| 750,000 | NR | Navajo County, AZ, IDA Revenue, Stone Container Corp. Project, 7.400% due 4/1/26 (f) | 769,155 | ||||||

See Notes to Financial Statements.

10 Legg Mason Partners Arizona Municipals Fund, Inc. 2006 Annual Report

Schedule of Investments (May 31, 2006) (continued)

| Face Amount | Rating‡ | Security | Value | ||||||

| Industrial Development — 6.3% (continued) | |||||||||

| $ | 320,000 | AAA | Pima County, AZ, IDA, Industrial Revenue Refunding, FSA-Insured, 7.250% due 7/15/10 | $ | 323,795 | ||||

| 1,000,000 | AAA | Tucson, AZ, IDA, Lease Revenue, University of Arizona/Marshall Foundation, Series A, AMBAC-Insured, 5.000% due 7/15/22 | 1,032,880 | ||||||

Total Industrial Development | 2,338,330 | ||||||||

| Miscellaneous — 20.6% | |||||||||

| 1,500,000 | AAA | Downtown Phoenix Hotel Corp., Subordinated Series B, FGIC-Insured, 5.000% due 7/1/36 | 1,541,310 | ||||||

Phoenix, AZ, Civic Improvement Corp., Excise Tax Revenue, Senior Lien: | |||||||||

| 2,630,000 | AAA | Adams Street Garage Project B, 5.375% due 7/1/29 (g) | 2,760,658 | ||||||

| 2,350,000 | AAA | Municipal Courthouse Project A, 5.375% due 7/1/29 (g) | 2,466,748 | ||||||

Sierra Vista, AZ, Municipal Property Corp., Municipal Facilities Revenue, AMBAC-Insured: | |||||||||

| 355,000 | AAA | 6.000% due 1/1/11 | 357,400 | ||||||

| 500,000 | AAA | 6.150% due 1/1/15 | 503,435 | ||||||

Total Miscellaneous | 7,629,551 | ||||||||

| Pollution Control — 2.8% | |||||||||

| 1,000,000 | B- | Coconino County, AZ, Pollution Control Corp. Revenue, Nevada Power Co. Project, 6.375% due 10/1/36 (f) | 1,018,730 | ||||||

| Pre-Refunded (h) — 19.3% | |||||||||

| 1,000,000 | Aaa(c) | Arizona Water Infrastructure Finance Authority, Water Quality Revenue, Series A, Call 10/1/11 @ 100, 5.000% due 10/1/19 | 1,058,760 | ||||||

Maricopa County, AZ, GO: | |||||||||

| 600,000 | AAA | Elementary School District, No. 08, Osborne Elementary School District, Series A, FGIC-Insured, Call 7/1/06 @ 101, | 606,996 | ||||||

| 1,000,000 | AA | Unified High School District No. 210, Phoenix Project of 1995, | 1,011,300 | ||||||

| 715,000 | BBB | Maricopa County, AZ, Hospital Revenue, Sun Health Corp., | 742,921 | ||||||

| 3,000,000 | AAA | Mesa, AZ, IDA Revenue, Discovery Health Systems, Series A, | 3,214,680 | ||||||

| 500,000 | AAA | Pinal County, AZ, Unified School District No. 43, Apache Junction, | 505,820 | ||||||

Total Pre-Refunded | 7,140,477 | ||||||||

| Transportation — 6.9% | |||||||||

Phoenix, AZ, Civic Improvement Corp., Airport Revenue: | |||||||||

| 1,000,000 | AAA | Junior Lien, FGIC-Insured, 5.375% due 7/1/29 (f) | 1,010,490 | ||||||

| 1,500,000 | AAA | Senior Lien, Series A, FSA-Insured, 5.000% due 7/1/25 | 1,531,290 | ||||||

Total Transportation | 2,541,780 | ||||||||

| Utilities — 10.2% | |||||||||

| 1,000,000 | AA | Arizona Agricultural Improvement & Power District, Electric System Revenue, Salt River Project, Refunding, Series A, 5.000% due 1/1/23 | 1,036,200 | ||||||

See Notes to Financial Statements.

Legg Mason Partners Arizona Municipals Fund, Inc. 2006 Annual Report 11

Schedule of Investments (May 31, 2006) (continued)

| Face Amount | Rating‡ | Security | Value | ||||||

| Utilities — 10.2% (continued) | |||||||||

Arizona Water Infrastructure Finance Authority Revenue, Water Quality, Series A: | |||||||||

| $ | 1,000,000 | AAA | 5.000% due 10/1/21 | $ | 1,057,800 | ||||

| 500,000 | AAA | 5.000% due 10/1/22 | 527,620 | ||||||

| 145,000 | BBB | Prescott Valley, AZ, Improvement District, Special Assessment, | 148,215 | ||||||

| 1,000,000 | BB+ | Yavapai County, AZ, IDA Revenue, Citizens Utilities Co. Project, | 1,015,450 | ||||||

Total Utilities | 3,785,285 | ||||||||

| Water & Sewer — 2.8% | |||||||||

| 1,000,000 | AAA | Phoenix, AZ, Civic Improvement Corp., Wastewater System Revenue, FGIC-Insured, 5.000% due 7/1/24 | 1,029,730 | ||||||

| TOTAL INVESTMENTS BEFORE SHORT-TERM INVESTMENT (Cost — $36,621,600) | 36,254,549 | ||||||||

| SHORT-TERM INVESTMENT — 0.5% | |||||||||

| Industrial Development — 0.5% | |||||||||

| 200,000 | A-1+ | Phoenix, AZ, IDA, Revenue, Valley of the Sun YMCA Project, LOC-Bank of America, 3.580%, 6/1/06 (i) (Cost — $200,000) | 200,000 | ||||||

| TOTAL INVESTMENTS — 98.5% (Cost — $36,821,600#) | 36,454,549 | ||||||||

Other Assets in Excess of Liabilities — 1.5% | 558,590 | ||||||||

| TOTAL NET ASSETS — 100.0% | $ | 37,013,139 | |||||||

| ‡ | All ratings are by Standard & Poor’s Ratings Service, unless otherwise noted. All ratings are unaudited. |

| (a) | Bonds are escrowed to maturity by government securities and/or U.S. government agency securities and are considered by the Manager to be triple-A rated even if issuer has not applied for new ratings. |

| (b) | All or a portion of this security is held at the broker as collateral for open futures contracts. |

| (c) | Rating by Moody’s Investors Service. All ratings are unaudited. |

| (d) | Security is currently in default. |

| (e) | Security is valued in good faith at fair value by or under the direction of the Board of Directors (See Note 1). |

| (f) | Income from this issue is considered a preference item for purposes of calculating the alternative minimum tax (“AMT”). |

| (g) | All or a portion of this security is segregated for open futures contracts. |

| (h) | Pre-Refunded bonds are escrowed with government obligations and/or government agency securities and are considered by the Manager to be triple-A rated even if issuer has not applied for new ratings. |

| (i) | Variable rate demand obligations have a demand feature under which the Fund can tender them back to the issuer on no more than 7 days notice. Date shown is the date of the next interest rate change. |

| # | Aggregate cost for federal income tax purposes is $36,812,757. |

See pages 13 and 14 for definitions of ratings.

Abbreviations used in this schedule: | ||

| AMBAC | — Ambac Assurance Corporation | |

| BIG | — Bond Investors Guaranty | |

| COP | — Certificate of Participation | |

| FGIC | — Financial Guaranty Insurance Company | |

| FSA | — Financial Security Assurance | |

| GO | — General Obligation | |

| IDA | — Industrial Development Authority | |

| LOC | — Letter of Credit | |

| MBIA | — Municipal Bond Investors Assurance Corporation | |

| MFH | — Multi-Family Housing | |

See Notes to Financial Statements.

12 Legg Mason Partners Arizona Municipals Fund, Inc. 2006 Annual Report

Bond Ratings (unaudited)

The definitions of the applicable rating symbols are set forth below:

Standard & Poor’s Ratings Service (“Standard & Poor’s’’) — Ratings from “AA’’ to “CCC’’ may be modified by the addition of a plus (+) or minus (-) sign to show relative standings within the major rating categories.

AAA | — Bonds rated “AAA’’ have the highest rating assigned by Standard & Poor’s. Capacity to pay interest and repay principal is extremely strong. |

AA | — Bonds rated “AA’’ have a very strong capacity to pay interest and repay principal and differ from the highest rated issue only in a small degree. |

A | — Bonds rated “A’’ have a strong capacity to pay interest and repay principal although they are somewhat more susceptible to the adverse effects of changes in circumstances and economic conditions than debt in higher rated categories. |

BBB | — Bonds rated “BBB’’ are regarded as having an adequate capacity to pay interest and repay principal. Whereas they normally exhibit adequate protection parameters, adverse economic conditions or changing circumstances are more likely to lead to a weakened capacity to pay interest and repay principal for bonds in this category than in higher rated categories. |

BB, B, CCC, CC and C | — Bonds rated “BB’’, “B”, “CCC”, “CC” and “C” are regarded, on balance, as predominantly speculative with respect to capacity to pay interest and repay principal in accordance with the terms of the obligation. “BB” represents the lowest degree of speculation and “C” the highest degree of speculation. While such bonds will likely have some quality and protective characteristics, these are outweighed by large uncertainties or major risk exposures to adverse conditions. |

D | — Bonds rated “D” are in default and payment of interest and/or repayment of principal is in arrears. |

Moody’s Investors Service (“Moody’s’’) — Numerical modifiers 1, 2 and 3 may be applied to each generic rating from “Aa’’ to “Caa,’’ where 1 is the highest and 3 the lowest ranking within its generic category.

Aaa | — Bonds rated “Aaa’’ are judged to be of the best quality. They carry the smallest degree of investment risk and are generally referred to as “gilt edge.’’ Interest payments are protected by a large or by an exceptionally stable margin and principal is secure. While the various protective elements are likely to change, such changes as can be visualized are most unlikely to impair the fundamentally strong position of such issues. |

Aa | — Bonds rated “Aa’’ are judged to be of high quality by all standards. Together with the “Aaa’’ group they comprise what are generally known as high grade bonds. They are rated lower than the best bonds because margins of protection may not be as large as in “Aaa” securities or fluctuation of protective elements may be of greater amplitude or there may be other elements present which make the long-term risks appear somewhat larger than in “Aaa” securities. |

A | — Bonds rated “A’’ possess many favorable investment attributes and are to be considered as upper medium grade obligations. Factors giving security to principal and interest are considered adequate but elements may be present which suggest a susceptibility to impairment some time in the future. |

Baa | — Bonds rated “Baa’’ are considered as medium grade obligations, i.e., they are neither highly protected nor poorly secured. Interest payments and principal security appear adequate for the present but certain protective elements may be lacking or may be characteristically unreliable over any great length of time. Such bonds lack outstanding investment characteristics and in fact have speculative characteristics as well. |

Ba | — Bonds rated “Ba” are judged to have speculative elements; their future cannot be considered as well assured. Often the protection of interest and principal payments may be very moderate and therefore not well safeguarded during both good and bad times over the future. Uncertainty of position characterizes bonds in this class. |

B | — Bonds rated “B” generally lack characteristics of desirable investments. Assurance of interest and principal payments or of maintenance of other terms of the contract over any long period of time may be small. |

Caa | — Bonds rated “Caa” are of poor standing. These may be in default, or present elements of danger may exist with respect to principal or interest. |

Ca | — Bonds rated “Ca” represent obligations which are speculative in a high degree. Such issues are often in default or have other marked short-comings. |

C | — Bonds rated “C” are the lowest class of bonds and issues so rated can be regarded as having extremely poor prospects of ever attaining any real investment standing. |

NR | — Indicates that the bond is not rated by Standard & Poor’s or Moody’s or Fitch Ratings Service. |

Legg Mason Partners Arizona Municipals Fund, Inc. 2006 Annual Report 13

Short-Term Security Ratings (unaudited)

SP-1 | — Standard & Poor’s highest rating indicating very strong or strong capacity to pay principal and interest; those issues determined to possess overwhelming safety characteristics are denoted with a plus (+) sign. |

A-1 | — Standard & Poor’s highest commercial paper and variable-rate demand obligation (VRDO) rating indicating that the degree of safety regarding timely payment is either overwhelming or very strong; those issues determined to possess overwhelming safety characteristics are denoted with a plus (+) sign. |

VMIG 1 | — Moody’s highest rating for issues having a demand feature — VRDO. |

MIGI | — Moody’s highest rating for short-term municipal obligations. |

P-1 | — Moody’s highest rating for commercial paper and for VRDO prior to the advent of the VMIG 1 rating. |

14 Legg Mason Partners Arizona Municipals Fund, Inc. 2006 Annual Report

Statement of Assets and Liabilities (May 31, 2006)

| ASSETS: | ||||

Investments, at value (Cost — $36,821,600) | $ | 36,454,549 | ||

Interest receivable | 678,505 | |||

Receivable from broker — variation margin on open futures contracts | 21,875 | |||

Receivable for Fund shares sold | 77 | |||

Prepaid expenses | 7,901 | |||

Total Assets | 37,162,907 | |||

| LIABILITIES: | ||||

Distributions payable | 59,219 | |||

Due to custodian | 41,551 | |||

Investment management fee payable | 6,432 | |||

Deferred compensation payable | 4,321 | |||

Distribution fees payable | 3,249 | |||

Payable for Fund shares repurchased | 2,710 | |||

Accrued expenses | 32,286 | |||

Total Liabilities | 149,768 | |||

Total Net Assets | $ | 37,013,139 | ||

| NET ASSETS: | ||||

Par value (Note 6) | $ | 3,915 | ||

Paid-in capital in excess of par value | 39,882,863 | |||

Undistributed net investment income | 108,840 | |||

Accumulated net realized loss on investments and futures contracts | (2,674,000 | ) | ||

Net unrealized depreciation on investments and futures contracts | (308,479 | ) | ||

Total Net Assets | $ | 37,013,139 | ||

Shares Outstanding: | ||||

Class A | 3,191,058 | |||

Class B | 411,858 | |||

Class C | 312,043 | |||

Net Asset Value: | ||||

Class A (and redemption price) | $9.45 | |||

Class B * | $9.45 | |||

Class C * | $9.45 | |||

Maximum Public Offering Price Per Share: | ||||

Class A (based on maximum sales charge of 4.00%) | $9.84 | |||

| * | Redemption price is NAV of Class B and C shares reduced by a 4.50% and 1.00% CDSC, respectively, if shares are redeemed within one year from purchase payment (See Note 2). |

See Notes to Financial Statements.

Legg Mason Partners Arizona Municipals Fund, Inc. 2006 Annual Report 15

Statement of Operations (For the year ended May 31, 2006)

| INVESTMENT INCOME: | ||||

Interest | $ | 2,067,870 | ||

| EXPENSES: | ||||

Investment management fee (Note 2) | 157,926 | |||

Distribution fees (Notes 2 and 4) | 99,292 | |||

Shareholder reports (Note 4) | 56,714 | |||

Legal fees | 52,830 | |||

Administration fees (Note 2) | 42,917 | |||

Audit and tax | 19,610 | |||

Registration fees | 16,711 | |||

Custody fees | 14,021 | |||

Transfer agent fees (Notes 2 and 4) | 11,188 | |||

Directors’ fees (Note 2) | 2,424 | |||

Insurance | 994 | |||

Miscellaneous expenses | 3,949 | |||

Total Expenses | 478,576 | |||

Less: Fee waivers and/or expense reimbursements (Notes 2 and 8) | (104,995 | ) | ||

Net Expenses | 373,581 | |||

Net Investment Income | 1,694,289 | |||

REALIZED AND UNREALIZED GAIN (LOSS) ON INVESTMENTS AND FUTURES CONTRACTS (NOTES 1 AND 3): | ||||

Net Realized Gain From: | ||||

Investment transactions | 170,787 | |||

Futures contracts | 826,875 | |||

Net Realized Gain | 997,662 | |||

Change in Net Unrealized Appreciation/Depreciation From: | ||||

Investments | (1,109,076 | ) | ||

Futures contracts | 221,697 | |||

Change in Net Unrealized Appreciation/Depreciation | (887,379 | ) | ||

Net Gain on Investments and Futures Contracts | 110,283 | |||

Increase in Net Assets From Operations | $ | 1,804,572 | ||

See Notes to Financial Statements.

16 Legg Mason Partners Arizona Municipals Fund, Inc. 2006 Annual Report

Statements of Changes in Net Assets (For the years ended May 31,)

| 2006 | 2005 | |||||||

| OPERATIONS: | ||||||||

Net investment income | $ | 1,694,289 | $ | 1,964,349 | ||||

Net realized gain (loss) | 997,662 | (1,259,851 | ) | |||||

Change in net unrealized appreciation/depreciation | (887,379 | ) | (1,606,695 | ) | ||||

Increase (Decrease) in Net Assets From Operations | 1,804,572 | (902,197 | ) | |||||

| DISTRIBUTIONS TO SHAREHOLDERS FROM (NOTES 1 AND 5): | ||||||||

Net investment income | (1,619,707 | ) | (1,956,140 | ) | ||||

Decrease in Net Assets From Distributions to Shareholders | (1,619,707 | ) | (1,956,140 | ) | ||||

| FUND SHARE TRANSACTIONS (NOTE 6): | ||||||||

Net proceeds from sale of shares | 5,581,439 | 4,495,825 | ||||||

Reinvestment of distributions | 828,981 | 895,269 | ||||||

Cost of shares repurchased | (15,017,143 | ) | (9,296,041 | ) | ||||

Decrease in Net Assets From Fund Share Transactions | (8,606,723 | ) | (3,904,947 | ) | ||||

Decrease in Net Assets | (8,421,858 | ) | (6,763,284 | ) | ||||

| NET ASSETS: | ||||||||

Beginning of year | 45,434,997 | 52,198,281 | ||||||

End of year* | $ | 37,013,139 | $ | 45,434,997 | ||||

* Includes undistributed net investment income of: | $108,840 | $36,236 | ||||||

See Notes to Financial Statements.

Legg Mason Partners Arizona Municipals Fund, Inc. 2006 Annual Report 17

For a share of each class of capital stock outstanding throughout each year ended May 31:

| Class A Shares(1) | 2006 | 2005 | 2004 | 2003 | 2002 | |||||||||||||||

Net Asset Value, Beginning of Year | $ | 9.41 | $ | 9.98 | $ | 9.98 | $ | 10.04 | $ | 10.00 | ||||||||||

Income (Loss) From Operations: | ||||||||||||||||||||

Net investment income | 0.41 | 0.40 | 0.44 | 0.45 | 0.48 | |||||||||||||||

Net realized and unrealized gain (loss) | 0.02 | (0.57 | ) | — | (0.05 | ) | 0.05 | |||||||||||||

Total Income (Loss) From Operations | 0.43 | (0.17 | ) | 0.44 | 0.40 | 0.53 | ||||||||||||||

Less Distributions From: | ||||||||||||||||||||

Net investment income | (0.39 | ) | (0.40 | ) | (0.44 | ) | (0.46 | ) | (0.49 | ) | ||||||||||

Total Distributions | (0.39 | ) | (0.40 | ) | (0.44 | ) | (0.46 | ) | (0.49 | ) | ||||||||||

Net Asset Value, End of Year | $ | 9.45 | $ | 9.41 | $ | 9.98 | $9.98 | $ | 10.04 | |||||||||||

Total Return(2) | 4.72 | % | (1.77 | )% | 4.45 | % | 4.07 | % | 5.40 | % | ||||||||||

Net Assets, End of Year (000s) | $30,171 | $36,960 | $41,220 | $40,319 | $41,824 | |||||||||||||||

Ratios to Average Net Assets: | ||||||||||||||||||||

Gross expenses | 1.08 | % | 1.00 | % | 0.92 | % | 1.00 | % | 0.91 | % | ||||||||||

Net expenses | 0.82 | (3)(4) | 0.99 | (3) | 0.92 | 1.00 | 0.91 | |||||||||||||

Net investment income | 4.33 | 4.10 | 4.39 | 4.48 | 4.80 | |||||||||||||||

Portfolio Turnover Rate | 11 | % | 0 | % | 9 | % | 11 | % | 11 | % | ||||||||||

| (1) | Per share amounts have been calculated using the average shares method. |

| (2) | Performance figures may reflect voluntary fee waivers and/or expense reimbursements. Past performance is no guarantee of future results. In the absence of voluntary fee waivers and/or expense reimbursements, the total return would have been lower. |

| (3) | The investment manager voluntarily waived a portion of its fees and/or reimbursed expenses. |

| (4) | Effective August 1, 2005, the Manager is waiving management fees and/or reimbursing expenses at the rate necessary to limit total annual operating expenses for Class A shares to 0.75% of average net assets. The Manager is waiving management fees and/or reimbursing expenses for Class B and Class C shares at the same rate as it waives fees and/or reimburses expenses for Class A. |

See Notes to Financial Statements.

18 Legg Mason Partners Arizona Municipals Fund, Inc. 2006 Annual Report

Financial Highlights (continued)

For a share of each class of capital stock outstanding throughout each year ended May 31:

| Class B Shares(1) | 2006 | 2005 | 2004 | 2003 | 2002 | |||||||||||||||

Net Asset Value, Beginning of Year | $ | 9.41 | $ | 9.99 | $ | 9.98 | $ | 10.05 | $ | 10.00 | ||||||||||

Income (Loss) From Operations: | ||||||||||||||||||||

Net investment income | 0.35 | 0.34 | 0.39 | 0.40 | 0.42 | |||||||||||||||

Net realized and unrealized gain (loss) | 0.03 | (0.58 | ) | 0.01 | (0.06 | ) | 0.07 | |||||||||||||

Total Income (Loss) From Operations | 0.38 | (0.24 | ) | 0.40 | 0.34 | 0.49 | ||||||||||||||

Less Distributions From: | ||||||||||||||||||||

Net investment income | (0.34 | ) | (0.34 | ) | (0.39 | ) | (0.41 | ) | (0.44 | ) | ||||||||||

Total Distributions | (0.34 | ) | (0.34 | ) | (0.39 | ) | (0.41 | ) | (0.44 | ) | ||||||||||

Net Asset Value, End of Year | $ | 9.45 | $ | 9.41 | $ | 9.99 | $9.98 | $ | 10.05 | |||||||||||

Total Return(2) | 4.08 | % | (2.45 | )% | 4.00 | % | 3.38 | % | 4.92 | % | ||||||||||

Net Assets, End of Year (000s) | $3,894 | $5,389 | $7,571 | $9,694 | $9,746 | |||||||||||||||

Ratios to Average Net Assets: | ||||||||||||||||||||

Gross expenses | 1.70 | % | 1.60 | % | 1.47 | % | 1.54 | % | 1.41 | % | ||||||||||

Net expenses | 1.44 | (3)(4) | 1.59 | (3) | 1.47 | 1.54 | 1.41 | |||||||||||||

Net investment income | 3.71 | 3.49 | 3.84 | 3.94 | 4.20 | |||||||||||||||

Portfolio Turnover Rate | 11 | % | 0 | % | 9 | % | 11 | % | 11 | % | ||||||||||

| (1) | Per share amounts have been calculated using the average shares method. |

| (2) | Performance figures may reflect voluntary fee waivers and/or expense reimbursements. Past performance is no guarantee of future results. In the absence of voluntary fee waivers and/or expense reimbursements, the total return would have been lower. |

| (3) | The investment manager voluntarily waived a portion of its fees and/or reimbursed expenses. |

| (4) | Effective August 1, 2005, the Manager is waiving management fees and/or reimbursing expenses at the rate necessary to limit total annual operating expenses for Class A shares to 0.75% of average net assets. The Manager is waiving management fees and/or reimbursing expenses for Class B and Class C shares at the same rate as it waives fees and/or reimburses expenses for Class A. |

See Notes to Financial Statements.

Legg Mason Partners Arizona Municipals Fund, Inc. 2006 Annual Report 19

Financial Highlights (continued)

For a share of each class of capital stock outstanding throughout each year ended May 31:

| Class C Shares(1) | 2006 | 2005 | 2004 | 2003 | 2002 | |||||||||||||||

Net Asset Value, Beginning of Year | $ | 9.41 | $ | 9.98 | $ | 9.97 | $ | 10.04 | $ | 10.00 | ||||||||||

Income (Loss) From Operations: | ||||||||||||||||||||

Net investment income | 0.35 | 0.34 | 0.38 | 0.40 | 0.42 | |||||||||||||||

Net realized and unrealized gain (loss) | 0.03 | (0.57 | ) | 0.01 | (0.07 | ) | 0.05 | |||||||||||||

Total Income (Loss) From Operations | 0.38 | (0.23 | ) | 0.39 | 0.33 | 0.47 | ||||||||||||||

Less Distributions From: | ||||||||||||||||||||

Net investment income | (0.34 | ) | (0.34 | ) | (0.38 | ) | (0.40 | ) | (0.43 | ) | ||||||||||

Total Distributions | (0.34 | ) | (0.34 | ) | (0.38 | ) | (0.40 | ) | (0.43 | ) | ||||||||||

Net Asset Value, End of Year | $ | 9.45 | $ | 9.41 | $ | 9.98 | $ | 9.97 | $ | 10.04 | ||||||||||

Total Return(2) | 4.12 | % | (2.35 | )% | 3.97 | % | 3.35 | % | 4.78 | % | ||||||||||

Net Assets, End of Year (000s) | $2,948 | $3,086 | $3,407 | $3,494 | $3,091 | |||||||||||||||

Ratios to Average Net Assets: | ||||||||||||||||||||

Gross expenses | 1.65 | % | 1.60 | % | 1.50 | % | 1.57 | % | 1.51 | % | ||||||||||

Net expenses | 1.39 | (3)(4) | 1.59 | (3) | 1.50 | 1.57 | 1.51 | |||||||||||||

Net investment income | 3.77 | 3.49 | 3.81 | 3.91 | 4.18 | |||||||||||||||

Portfolio Turnover Rate | 11 | % | 0 | % | 9 | % | 11 | % | 11 | % | ||||||||||

| (1) | Per share amounts have been calculated using the average shares method. |

| (2) | Performance figures may reflect voluntary fee waivers and/or expense reimbursements. Past performance is no guarantee of future results. In the absence of voluntary fee waivers and/or expense reimbursements, the total return would have been lower. |

| (3) | The investment manager voluntarily waived a portion of its fees and/or reimbursed expenses. |

| (4) | Effective August 1, 2005, the Manager is waiving management fees and/or reimbursing expenses at the rate necessary to limit total annual operating expenses for Class A shares to 0.75% of average net assets. The Manager is waiving management fees and/or reimbursing expenses for Class B and Class C shares at the same rate as it waives fees and/or reimburses expenses for Class A. |

See Notes to Financial Statements.

20 Legg Mason Partners Arizona Municipals Fund, Inc. 2006 Annual Report

| 1. | Organization and Significant Accounting Policies |

Legg Mason Partners Arizona Municipals Fund, Inc. (formerly known as Smith Barney Arizona Municipals Fund Inc.) (the “Fund”), a Maryland corporation, is registered under the Investment Company Act of 1940, as amended (the “1940 Act”), as a diversified, open-end management investment company.

The following are significant accounting policies consistently followed by the Fund and are in conformity with U.S. generally accepted accounting principles (“GAAP”). Estimates and assumptions are required to be made regarding assets, liabilities and changes in net assets resulting from operations when financial statements are prepared. Changes in the economic environment, financial markets and any other parameters used in determining these estimates could cause actual results to differ.

(a) Investment Valuation. Securities are valued at the mean between the bid and asked prices provided by an independent pricing service that are based on transactions in municipal obligations, quotations from municipal bond dealers, market transactions in comparable securities and various other relationships between securities. Securities for which market quotations are not readily available or are determined not to reflect fair value, will be valued in good faith by or under the direction of the Fund’s Board of Directors. Short-term obligations with maturities of 60 days or less are valued at amortized cost, which approximates value.

(b) Financial Futures Contracts. The Fund may enter into financial futures contracts typically to hedge a portion of the portfolio. Upon entering into a financial futures contract, the Fund is required to deposit cash or securities as initial margin. Additional securities are also segregated up to the current market value of the financial futures contracts. Subsequent payments, known as variation margin, are made or received by the Fund each day, depending on the daily fluctuation in the value of the underlying financial instruments. The Fund recognizes an unrealized gain or loss equal to the daily variation margin. When the financial futures contracts are closed, a realized gain or loss is recognized equal to the difference between the proceeds from (or cost of) the closing transactions and the Fund’s basis in the contracts.

The risks associated with entering into financial futures contracts include the possibility that a change in the value of the contract may not correlate with the changes in the value of the underlying instruments. In addition, investing in financial futures contracts involves the risk that the Fund could lose more than the original margin deposit and subsequent payments required for a futures transaction. Risks may also arise upon entering into these contracts from the potential inability of the counterparties to meet the terms of their contracts.

(c) Fund Concentration. Since the Fund invests primarily in obligations of issuers within Arizona, it is subject to possible concentration risks associated with economic, political, or legal developments or industrial or regional matters specifically affecting Arizona.

(d) Security Transactions and Investment Income. Security transactions are accounted for on a trade date basis. Interest income, adjusted for amortization of premium and accretion of discount, is recorded on the accrual basis. The cost of investments sold is determined by use of the specific identification method. To the extent any issuer defaults on an expected interest payment, the Fund’s policy is to generally halt any additional interest income accruals and consider the realizability of interest accrued up to the date of default.

Legg Mason Partners Arizona Municipals Fund, Inc. 2006 Annual Report 21

Notes to Financial Statements (continued)

(e) Distributions to Shareholders. Distributions from net investment income on the shares of the Fund are declared each business day to shareholders of record, and are paid monthly. The Fund intends to satisfy conditions that will enable interest from municipal securities, which is exempt from federal and certain state income taxes, to retain such tax-exempt status when distributed to the shareholders of the Fund. Distributions of net realized gains, if any, are taxable and are declared at least annually. Distributions are recorded on the ex-dividend date and are determined in accordance with income tax regulations, which may differ from GAAP.

(f) Class Accounting. Investment income, common expenses and realized/unrealized gain (loss) on investments are allocated to the various classes of the Fund on the basis of daily net assets of each class. Fees relating to a specific class are charged directly to that class.

(g) Federal and Other Taxes. It is the Fund’s policy to comply with the federal income and excise tax requirements of the Internal Revenue Code of 1986, as amended, applicable to regulated investment companies. Accordingly, the Fund intends to distribute substantially all of its income and net realized gains on investments, if any, to shareholders each year. Therefore, no federal income tax provision is required in the Fund’s financial statements.

(h) Reclassification. GAAP requires that certain components of net assets be adjusted to reflect permanent differences between financial and tax reporting. These reclassifications have no effect on net assets or net asset values per share. During the year ended May 31, 2006, the following reclassifications have been made:

| Undistributed Net Investment Income | Accumulated Net Realized Loss | ||||||

(a) | $ | (1,978 | ) | $ | 1,978 | ||

| (a) | Reclassifications are primarily due to differences between book and tax accretion of market discount on fixed income securities. |

| 2. | Investment Management Agreement and Other Transactions with Affiliates |

On December 1, 2005, Citigroup Inc. (“Citigroup”) completed the sale of substantially all of its asset management business to Legg Mason, Inc. (“Legg Mason”). As a result, the Fund’s investment manager, Smith Barney Fund Management LLC (“SBFM” or the “Manager”), previously an indirect wholly-owned subsidiary of Citigroup, became a wholly-owned subsidiary of Legg Mason. Completion of the sale caused the Fund’s then existing investment advisory and administration contracts to terminate. The Fund’s shareholders approved a new investment management contract between the Fund and the Manager, which became effective on December 1, 2005.

Legg Mason, whose principal executive offices are in Baltimore, Maryland, is a financial services holding company.

Prior to the Legg Mason transaction, the Fund paid the Manager an advisory fee calculated at an annual rate of 0.30% of the Fund’s average daily net assets and an administration fee calculated at an annual rate of 0.20% of the Fund’s average daily net assets up to $500 million and 0.18% of the Fund’s average daily net assets in excess of $500 million. These fees were calculated daily and paid monthly.

22 Legg Mason Partners Arizona Municipals Fund, Inc. 2006 Annual Report

Notes to Financial Statements (continued)

Effective December 1, 2005, as a result of the termination of the administration contract, the separate administration fee is no longer applicable.

Under the new investment management agreement effective December 1, 2005, the Fund pays the Manager a management fee calculated at an annual rate of 0.50% of the Fund’s average daily net assets up to $500 million and 0.48% of the Fund’s average daily net assets in excess of $500 million. This fee is calculated daily and paid monthly.

Effective August 1, 2005, the Manager has waived investment management fees and/or reimbursed expenses at the rate necessary to limit total annual operating expenses for Class A shares to 0.75% of average net assets. The Manager has waived investment management fees and/or reimbursed expenses for Class B and Class C shares at the same rate as it waived fees and/or reimbursed expenses for Class A. The Manager may change or eliminate the voluntary expense limitation at any time.

During the year ended May 31, 2006, the Manager waived a portion of its investment management fee and/or reimbursed expenses amounting to $104,995. Such waivers and/or expense reimbursements are voluntary and may be reduced or terminated at any time.

The Fund’s Board has approved PFPC Inc. (“PFPC”) to serve as transfer agent for the Fund, effective January 1, 2006. The principal business office of PFPC is located at 4400 Computer Drive, Westborough, MA 01581. Prior to January 1, 2006, Citicorp Trust Bank, fsb. (“CTB”), a subsidiary of Citigroup, acted as the Fund’s transfer agent. Also, prior to January 1, 2006, PFPC acted as the Fund’s sub-transfer agent. CTB received account fees and asset-based fees that varied according to the size and type of account. PFPC was responsible for shareholder recordkeeping and financial processing for all shareholder accounts and was paid by CTB. For the period ended May 31, 2006, the Fund paid transfer agent fees of $6,663 to CTB.

The Fund’s Board has appointed the Fund’s current distributor, Citigroup Global Markets Inc. (“CGM”), and Legg Mason Investor Services, LLC (“LMIS”), a wholly-owned broker-dealer subsidiary of Legg Mason, as co-distributors of the Fund. The Fund’s Board has also approved an amended and restated Rule 12b-1 Plan. CGM and other broker-dealers, financial intermediaries and financial institutions (each called a “Service Agent”) that currently offer Fund shares will continue to make the Fund’s shares available to their clients. Additional Service Agents may offer Fund shares in the future.

There is a maximum initial sales charge of 4.00% for Class A shares. There is a contingent deferred sales charge (“CDSC”) of 4.50% on Class B shares, which applies if redemption occurs within one year from purchase payment. This CDSC declines by 0.50% the first year after purchase payment and thereafter by 1.00% per year until no CDSC is incurred. Class C shares have a 1.00% CDSC, which applies if redemption occurs within one year from purchase payment. In certain cases, Class A shares have a 1.00% CDSC, which applies if redemption occurs within one year from purchase payment. This CDSC only applies to those purchases of Class A shares, which, when combined with current holdings of Class A shares, equal or exceed $500,000 in the aggregate. These purchases do not incur an initial sales charge.

Legg Mason Partners Arizona Municipals Fund, Inc. 2006 Annual Report 23

Notes to Financial Statements (continued)

For the period ended May 31, 2006, LMIS, and CGM and its affiliates received sales charges of approximately $4,500 on sales of the Fund’s Class A shares. In addition, for the period ended May 31, 2006, CDSCs paid to LMIS, and CGM and its affiliates were approximately:

| Class A | Class B | ||||||

CDSCs | $ | 0 | * | $ | 2,000 | ||

| * | Amount represent less than $1,000. |

The Fund has adopted an unfunded, non-qualified deferred compensation plan (the “Plan”) which allows non-interested directors (“Directors”) to defer the receipt of all or a portion of the directors’ fees earned until a later date specified by the Directors. The deferred fees earn a return based on notional investments selected by the Directors. The balance of the deferred fees payable may change depending upon the investment performance. Any gains or losses incurred in the deferred balances are reported in the Statement of Operations under Directors’ fees. Under the Plan, deferred fees are considered a general obligation of the Fund and any payments made pursuant to the Plan will be made from the Fund’s general assets. The Board of Directors voted to discontinue offering the Plan to its members, effective January 1, 2007. This change will have no effect on fees previously deferred. As of May 31, 2006, the Fund had accrued $4,321 as deferred compensation under the Plan.

Certain officers and one Director of the Fund are employees of Legg Mason or its affiliates and do not receive compensation from the Fund.

| 3. | Investments |

During the year ended May 31, 2006, the aggregate cost of purchases and proceeds from sales of investments (excluding short-term investments) were as follows:

Purchases | $ | 4,165,440 | |

Sales | 6,848,765 | ||

At May 31, 2006, the aggregate gross unrealized appreciation and depreciation of investments for federal income tax purposes were as follows:

Gross unrealized appreciation | $ | 1,595,533 | ||

Gross unrealized depreciation | (1,962,584 | ) | ||

Net unrealized depreciation | $ | (367,051 | ) | |

At May 31, 2006, the Fund had the following open futures contracts:

| Contracts to Sell: | Number of Contracts | Expiration Date | Basis Value | Market Value | Unrealized Gain | ||||||||

U.S. Treasury Bonds | 70 | 9/06 | $ | 7,493,884 | $ | 7,435,312 | $ | 58,572 | |||||

24 Legg Mason Partners Arizona Municipals Fund, Inc. 2006 Annual Report

Notes to Financial Statements (continued)

| 4. | Class Specific Expenses |

The Fund has adopted a Rule 12b-1 distribution plan and under that plan, the Fund pays a service fee with respect to its Class A, B and C shares calculated at the annual rate of 0.15% of the average daily net assets of each respective class. The Fund also pays a distribution fee with respect to its Class B and C shares calculated at the annual rate of 0.50% and 0.55% of the average daily net assets of each class, respectively. Distribution fees are accrued daily and paid monthly.

For the year ended May 31, 2006, class specific expenses were as follows:

| Distribution Fees | Transfer Agent Fees | Shareholder Reports Expenses | |||||||

Class A | $ | 48,971 | $ | 7,898 | $ | 42,008 | |||

Class B | 30,244 | 2,106 | 10,842 | ||||||

Class C | 20,077 | 1,184 | 3,864 | ||||||

Total | $ | 99,292 | $ | 11,188 | $ | 56,714 | |||

| 5. | Distributions to Shareholders by Class |

| Year Ended May 31, 2006 | Year Ended May 31, 2005 | |||||

Net Investment Income: | ||||||

Class A | $ | 1,351,569 | $ | 1,617,904 | ||

Class B | 164,893 | 222,245 | ||||

Class C | 103,245 | 115,991 | ||||

Total | $ | 1,619,707 | $ | 1,956,140 | ||

| 6. | Capital Shares |

At May 31, 2006, the Fund had 500 million shares of capital stock authorized with a par value of $0.001 per share. The Fund has the ability to issue multiple classes of shares. Each share of a class represents an identical interest in the Fund and has the same rights, except that each class bears certain direct expenses, including those specifically related to the distribution of its shares.

Transactions in shares of each class were as follows:

| Year Ended May 31, 2006 | Year Ended May 31, 2005 | |||||||||||||

| Shares | Amount | Shares | Amount | |||||||||||

Class A | ||||||||||||||

Shares sold | 574,879 | $ | 5,398,508 | 423,888 | $ | 4,175,594 | ||||||||

Shares issued on reinvestment | 73,043 | 687,461 | 74,534 | 729,568 | ||||||||||

Shares repurchased | (1,383,518 | ) | (13,030,519 | ) | (700,140 | ) | (6,852,155 | ) | ||||||

Net Decrease | (735,596 | ) | $ | (6,944,550 | ) | (201,718 | ) | $ | (1,946,993 | ) | ||||

Legg Mason Partners Arizona Municipals Fund, Inc. 2006 Annual Report 25

Notes to Financial Statements (continued)

| Year Ended May 31, 2006 | Year Ended May 31, 2005 | |||||||||||||

| Shares | Amount | Shares | Amount | |||||||||||

Class B | ||||||||||||||

Shares sold | 996 | $ | 9,373 | 14,662 | $ | 144,995 | ||||||||

Shares issued on reinvestment | 7,206 | 67,812 | 8,557 | 83,957 | ||||||||||

Shares repurchased | (168,824 | ) | (1,589,710 | ) | (208,578 | ) | (2,056,776 | ) | ||||||

Net Decrease | (160,622 | ) | $ | (1,512,525 | ) | (185,359 | ) | $ | (1,827,824 | ) | ||||

Class C | ||||||||||||||

Shares sold | 18,433 | $ | 173,558 | 17,929 | $ | 175,236 | ||||||||

Shares issued on reinvestment | 7,834 | 73,708 | 8,350 | 81,744 | ||||||||||

Shares repurchased | (42,229 | ) | (396,914 | ) | (39,740 | ) | (387,110 | ) | ||||||

Net Decrease | (15,962 | ) | $ | (149,648 | ) | (13,461 | ) | $ | (130,130 | ) | ||||

| 7. | Income Tax Information and Distributions to Shareholders |

Subsequent to the fiscal year end, the Fund made the following distributions:

| Record Date Payable Date | Class A | Class B | Class C | ||||||

Daily | |||||||||

6/30/06 | $ | 0.037031 | $ | 0.032117 | $ | 0.033384 | |||

The tax character of distributions paid during the fiscal years ended May 31, was as follows:

| 2006 | 2005 | |||||

Distributions paid from: | ||||||

Tax-Exempt Income | $ | 1,619,707 | $ | 1,956,140 | ||

As of May 31, 2006, the components of accumulated earnings on a tax basis were as follows:

Undistributed tax-exempt income — net | $ | 113,161 | ||

Capital loss carryforward* | (2,624,271 | ) | ||

Other book/tax temporary differences (a) | (62,893 | ) | ||

Unrealized appreciation/(depreciation) (b) | (299,636 | ) | ||

Total accumulated earnings/(losses) — net | $ | (2,873,639 | ) | |

| (*) | During the taxable year ended May 31, 2006, the Fund utilized $447,944 of its capital loss carryover available from prior years. As of May 31, 2006, the Fund had the following net capital loss carryforwards remaining: |

Year of Expiration | Amount | |||

5/31/2009 | $ | (637,666 | ) | |

5/31/2010 | (60,095 | ) | ||

5/31/2012 | (230,432 | ) | ||

5/31/2013 | (1,696,078 | ) | ||

| $ | (2,624,271 | ) | ||

26 Legg Mason Partners Arizona Municipals Fund, Inc. 2006 Annual Report

Notes to Financial Statements (continued)

These amounts will be available to offset any future taxable capital gains.

| (a) | Other book/tax temporary differences are attributable primarily to the realization for tax purposes of unrealized gains on certain futures contracts and differences in the book/tax treatment of various items. |

| (b) | The difference between book-basis and tax-basis unrealized appreciation/(depreciation) is attributable primarily to the difference between book & tax accretion methods for market discount on fixed income securities. |

8. Regulatory Matters

On May 31, 2005, the U.S. Securities and Exchange Commission (“SEC”) issued an order in connection with the settlement of an administrative proceeding against SBFM and CGM relating to the appointment of an affiliated transfer agent for the Smith Barney family of mutual funds (the “Funds”).

The SEC order finds that SBFM and CGM willfully violated Section 206(1) of the Investment Advisers Act of 1940 (“Advisers Act”). Specifically, the order finds that SBFM and CGM knowingly or recklessly failed to disclose to the boards of the Funds in 1999 when proposing a new transfer agent arrangement with an affiliated transfer agent that: First Data Investors Services Group (“First Data”), the Funds’ then-existing transfer agent, had offered to continue as transfer agent and do the same work for substantially less money than before; and that Citigroup Asset Management (“CAM”), the Citigroup business unit that, at the time, included the Fund’s investment manager and other investment advisory companies, had entered into a side letter with First Data under which CAM agreed to recommend the appointment of First Data as sub-transfer agent to the affiliated transfer agent in exchange for, among other things, a guarantee by First Data of specified amounts of asset management and investment banking fees to CAM and CGM. The order also finds that SBFM and CGM willfully violated Section 206(2) of the Advisers Act by virtue of the omissions discussed above and other misrepresentations and omissions in the materials provided to the Funds’ boards, including the failure to make clear that the affiliated transfer agent would earn a high profit for performing limited functions while First Data continued to perform almost all of the transfer agent functions, and the suggestion that the proposed arrangement was in the Funds’ best interests and that no viable alternatives existed. SBFM and CGM do not admit or deny any wrongdoing or liability. The settlement does not establish wrongdoing or liability for purposes of any other proceeding.

The SEC censured SBFM and CGM and ordered them to cease and desist from violations of Sections 206(1) and 206(2) of the Advisers Act. The order requires Citigroup to pay $208.1 million, including $109 million in disgorgement of profits, $19.1 million in interest, and a civil money penalty of $80 million. Approximately $24.4 million has already been paid to the Funds, primarily through fee waivers. The remaining $183.7 million, including the penalty, has been paid to the U.S. Treasury and will be distributed pursuant to a plan submitted for the approval of the SEC. At this time, there is no certainty as to how the above-described proceeds of the settlement will be distributed, to whom such distributions will be made, the methodology by which such distributions will be allocated, and when such distributions will be made. The order also required that transfer agency fees received from the Funds since December 1, 2004, less certain expenses, be placed in escrow and provided that a portion of such fees might be subsequently distributed in accordance with the terms of the order. On April 3, 2006, an aggregate amount of approximately $9 million was distributed to the affected Funds.

Legg Mason Partners Arizona Municipals Fund, Inc. 2006 Annual Report 27

Notes to Financial Statements (continued)

The order required SBFM to recommend a new transfer agent contract to the Fund boards within 180 days of the entry of the order; if a Citigroup affiliate submitted a proposal to serve as transfer agent or sub-transfer agent, SBFM and CGM would have been required, at their expense, to engage an independent monitor to oversee a competitive bidding process. On November 21, 2005, and within the specified timeframe, the Fund’s Board selected a new transfer agent for the Fund. No Citigroup affiliate submitted a proposal to serve as transfer agent. Under the order, SBFM also must comply with an amended version of a vendor policy that Citigroup instituted in August 2004.

Although there can be no assurance, SBFM does not believe that this matter will have a material adverse effect on the Funds.

On December 1, 2005, Citigroup completed the sale of substantially all of its global asset management business, including SBFM, to Legg Mason.

| 9. | Legal Matters |

Beginning in August 2005, five class action lawsuits alleging violations of federal securities laws and state law were filed against CGM and SBFM, (collectively, the “Defendants”) based on the May 31, 2005 settlement order issued against the Defendants by the SEC as described in Note 8. The complaints seek injunctive relief and compensatory and punitive damages, removal of SBFM as the advisor for the Smith Barney family of funds, rescission of the Funds’ management and other contracts with SBFM, recovery of all fees paid to SBFM pursuant to such contracts, and an award of attorneys’ fees and litigation expenses.