UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number | 811-05082 |

|

The Malaysia Fund, Inc. |

(Exact name of registrant as specified in charter) |

|

522 Fifth Avenue New York, NY | | 10036 |

(Address of principal executive offices) | | (Zip code) |

|

Ronald E. Robison

522 Fifth Avenue New York, New York 10036 |

(Name and address of agent for service) |

|

Registrant’s telephone number, including area code: | 1-800-221-6726 | |

|

Date of fiscal year end: | 12/31 | |

|

Date of reporting period: | 12/31/07 | |

| | | | | | | | |

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget (“OMB”) control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. Section 3507.

ITEM 1. REPORTS TO STOCKHOLDERS.

The Fund’s annual report transmitted to shareholders pursuant to Rule 30e-1 under the Investment Company Act of 1940 is as follows:

| 2007 Annual Report |

| |

| December 31, 2007 |

The Malaysia Fund, Inc.

Morgan Stanley

Investment Management Inc.

Investment Adviser

| The Malaysia Fund, Inc. |

| |

Letter to Stockholders | Overview (unaudited) |

Performance

For the year ended December 31, 2007, the Malaysia Fund, Inc. (the “Fund”) had total returns, based on net asset value and market price per share (including reinvestment of distributions), of 60.19%, net of fees and 55.48%, respectively, compared to its benchmark, the Kuala Lumpur Stock Exchange Composite (KLSE) Index (the “Index”) expressed in U.S. dollars which returned 40.63%. On December 31, 2007, the closing price of the Fund’s shares on the New York Stock Exchange was $10.85, representing a 10.6% discount to the Fund’s net asset value per share. Past performance is no guarantee of future results.

Factors Affecting Performance

• The Malaysian equity market started on a strong note in 2007, as the government continued to drum up interest in the 9th Malaysian Plan, a mid-term economic stimulus measure to boost the economy via infrastructure projects. The government also unveiled a series of 20-year plans for the various regions of the country over the year, which helped to shore up sentiment. However, interest began waning in the later part of 2007 as the government failed to provide follow-up details on these measures.

• The political situation took a turn for the worse as various groups took advantage of the coming elections to air their grievances. The minority Indian and Chinese communities took to the streets to demand better treatment and a review of the preferential rights of Malays. Several religious incidents further increased tensions among the populace.

• On the economic front, the economy continued to grow at a stable rate of 6.0% (based on consensus estimates), compared to a real gross domestic product growth of 5.2% in 2006. Despite the 7.0% appreciation of the Malaysian Ringgit, exports continued to do well. This was especially true for palm oil, which benefited from strong global demand for edible oils. In fact, at the end of the period the largest Malaysian stocks by capitalization were palm oil stocks, overtaking the banks.

Managment Strategies

• The Fund benefited from an overweight position in palm oil stocks, which did well due to strong earnings growth, as palm oil prices more than doubled during the period. Another positive contributor was the Fund’s underweight in government-linked companies, which continued to underperform owing to their disappointing results.

• Detractors from performance included the Fund’s overweight in a construction company, which underperformed as investor interest shifted from construction stocks with overseas exposure towards those with domestic businesses. However, we remain confident in the execution ability of the company’s management.

• The Fund seeks long-term capital appreciation and integrates top-down sector allocation and bottom-up stock selection with a growth bias. The team utilizes a rigorous fundamental research approach that considers dynamics, valuation, and sentiment and focuses on companies with strong management and solid earnings.

Sincerely,

| |

Ronald E. Robison | |

President and Principal Executive Officer | |

| |

| January 2008 |

2

| The Malaysia Fund, Inc. |

| |

Portfolio of Investments | December 31, 2007 |

| | | | Value | |

| | Shares | | (000) | |

COMMON STOCKS (98.6%) | | | | | |

(Unless Otherwise Noted) | | | | | |

Automobiles (1.2%) | | | | | |

Proton Holdings Bhd | | (a)512,000 | | $ | 567 | |

TAN Chong Motor Holdings Bhd | | 1,309,000 | | 820 | |

| | | | 1,387 | |

Commercial Banks (16.4%) | | | | | |

Bumiputra-Commerce Holdings Bhd | | 2,693,196 | | 8,873 | |

Malayan Banking Bhd | | 1,473,500 | | 5,095 | |

Public Bank Bhd | | 1,591,390 | | 5,283 | |

| | | | 19,251 | |

Construction & Engineering (5.5%) | | | | | |

Gamuda Bhd | | 882,200 | | 1,276 | |

IJM Corp. Bhd | | 1,985,500 | | 5,143 | |

| | | | 6,419 | |

Construction Materials (0.8%) | | | | | |

Lafarge Malayan Cement Bhd | | 548,100 | | 967 | |

Diversified Telecommunication Services (4.7%) | | | | | |

Telekom Malaysia Bhd | | 1,636,000 | | 5,513 | |

Electric Utilities (2.3%) | | | | | |

Tenaga Nasional Bhd | | 945,750 | | 2,736 | |

Food Products (24.8%) | | | | | |

IOI Corp. Bhd | | 5,296,250 | | 12,304 | |

Kuala Lumpur Kepong Bhd | | 1,225,500 | | 6,407 | |

Wilmar International Ltd. | | 2,794,500 | | 10,405 | |

| | | | 29,116 | |

Hotels, Restaurants & Leisure (6.9%) | | | | | |

Genting Bhd | | 2,019,000 | | 4,783 | |

Resorts World Bhd | | 2,793,500 | | 3,264 | |

| | | | 8,047 | |

Independent Power Producers & Energy Traders (1.5%) | | | | | |

Tanjong plc | | 314,000 | | 1,747 | |

Industrial Conglomerates (11.1%) | | | | | |

MMC Corp. Bhd | | 667,000 | | 1,860 | |

Sime Darby Bhd | | (a)3,092,910 | | 11,130 | |

| | | | 12,990 | |

Insurance (0.5%) | | | | | |

MAA Holdings Bhd | | 1,174,000 | | 592 | |

Marine (3.2%) | | | | | |

Malaysia International Shipping Corp. Bhd | | 1,271,000 | | 3,742 | |

Multi-Utilities (4.0%) | | | | | |

YTL Corp. Bhd | | 1,955,733 | | 4,659 | |

Real Estate (10.8%) | | | | | |

Bandar Raya Developments Bhd | | 1,050,000 | | $ | 1,004 | |

Glomac Bhd | | 1,763,000 | | 729 | |

IGB Corp. Bhd | | 3,024,000 | | 2,048 | |

IOI Properties Bhd | | 415,000 | | 1,633 | |

Naim Cendera Holdings Bhd | | 789,000 | | 1,130 | |

SP Setia Bhd | | 3,350,248 | | 5,027 | |

YNH Property Bhd | | 1,338,200 | | 1,089 | |

| | | | 12,660 | |

Wireless Telecommunication Services (4.9%) | | | | | |

Digi.Com Bhd | | 777,000 | | 5,806 | |

TOTAL COMMON STOCKS | | | | | |

(Cost $51,302) | | | | 115,632 | |

| | No. of | | | |

| | Rights | | | |

RIGHTS (0.1%) | | | | | |

Multi-Utilities (0.0%) | | | | | |

YTL Corp. Bhd,

expiring 1/7/08 | | (a)130,382 | | 58 | |

Real Estate (0.1%) | | | | | |

SP Setia Bhd,

expiring 1/14/08 | | (a)558,374 | | 71 | |

TOTAL RIGHTS (Cost $0) | | | | 129 | |

| | No. of | | | |

| | Warrants | | | |

WARRANTS (0.1%) | | | | | |

Construction & Engineering (0.1%) | | | | | |

IJM Corp. Bhd,

expiring 7/7/10 (Cost $2) | | (a)148,600 | | 167 | |

| | Shares | | | |

SHORT-TERM INVESTMENT (1.9%) | | | | | |

Investment Company (1.9%) | | | | | |

Morgan Stanley Institutional

Liquidity Money Market Portfolio —Institutional Class

(Cost $2,269) | | (b)2,268,942 | | 2,269 | |

TOTAL INVESTMENTS (100.7%)

(Cost $53,573) | | | | (c) 118,197 | |

LIABILITIES IN EXCESS OF OTHER ASSETS (-0.7%) | | | | (924) | |

NET ASSETS (100%) | | | | $ | 117,273 | |

(a) | Non-income producing security. |

(b) | See Note G within the Notes to Financial Statements regarding investment in Morgan Stanley Institutional Liquidity Money Market Portfolio — Institutional Class. |

| The accompanying notes are an integral part of the financial statements. | 3 |

| The Malaysia Fund, Inc. |

| |

Portfolio of Investments (cont’d) | December 31, 2007 |

(c) | The approximate market value and percentage of the investments, $115,761,000 and 97.9%, respectively, represent the securities that have been fair valued under the fair valuation policy for international investments as described in Note A within the Notes to Financial Statements. |

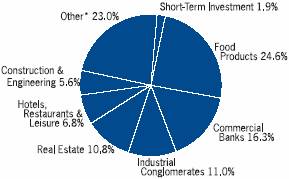

Graphic Presentation of Portfolio Holdings

The following graph depicts the Fund’s holdings by industry and/or security type, as a percentage of total investments.

* Industries which do not appear in the above graph, as well as those which represent less than 5% of total investments, if applicable, are included in the category labeled “Other”.

4 | The accompanying notes are an integral part of the financial statements. | |

| The Malaysia Fund, Inc. |

| |

| Financial Statements |

Statement of Assets and Liabilities | | December 31, 2007

(000) |

Assets: | | | |

Investments in Securities of Unaffiliated Issuers, at Value (Cost $51,304) | | $ | 115,928 | |

Investment in Security of Affiliated Issuer, at Value (Cost $2,269) | | 2,269 | |

Total Investments in Securities, at Value (Cost $53,573) | | 118,197 | |

Foreign Currency, at Value (Cost $846) | | 857 | |

Dividends Receivable | | 139 | |

Interest Receivable | | 8 | |

Receivable from Affiliate | | @— | |

Other Assets | | 2 | |

Total Assets | | 119,203 | |

Liabilities: | | | |

Payable For: | | | |

Dividends Declared | | 1,722 | |

U.S. Investment Advisory Fees | | 82 | |

Malaysian Investment Advisory Fees | | 54 | |

Custodian Fees | | 22 | |

Administration Fees | | 4 | |

Directors’ Fees and Expenses | | @— | |

Other Liabilities | | 46 | |

Total Liabilities | | 1,930 | |

Net Assets | | | |

Applicable to 9,662,129, Issued and Outstanding $0.01

Par Value Shares (20,000,000 Shares Authorized) | | $ | 117,273 | |

Net Asset Value Per Share | | $ | 12.14 | |

Net Assets Consist of: | | | |

Common Stock | | $ | 97 | |

Paid-in Capital | | 55,762 | |

Undistributed (Distributions in Excess of) Net Investment Income | | (6) | |

Accumulated Net Realized Gain (Loss) | | (3,215) | |

Unrealized Appreciation (Depreciation) on Investments and Foreign Currency Translations | | 64,635 | |

Net Assets | | $ | 117,273 | |

@ Amount is less than $500. | | | |

| The accompanying notes are an integral part of the financial statements. | 5 |

| The Malaysia Fund, Inc. |

| |

| Financial Statements |

Statement of Operations | | Year Ended

December 31, 2007

(000) | |

Investment Income | | | |

Dividends from Securities of Unaffiliated Issuers | | $ | 2,718 | |

Dividends from Security of Affiliated Issuer | | 44 | |

Interest from Securities of Unaffiliated Issuers | | 7 | |

Total Investment Income | | 2,769 | |

Expenses | | | |

U.S. Investment Advisory Fees (Note B) | | 790 | |

Malaysian Investment Advisory Fees (Note B) | | 198 | |

Administration Fees (Note C) | | 79 | |

Custodian Fees (Note D) | | 73 | |

Professional Fees | | 47 | |

Stockholder Reporting Expenses | | 22 | |

Stockholder Servicing Agent Fees | | 14 | |

Directors’ Fees and Expenses | | 2 | |

Other Expenses | | 34 | |

Total Expenses | | 1,259 | |

Waiver of Administration Fees (Note C) | | (31) | |

Rebate from Morgan Stanley Affiliated Cash Sweep (Note G) | | (1) | |

Expense Offset (Note D) | | @— | |

Net Expenses | | 1,227 | |

Net Investment Income (Loss) | | 1,542 | |

Net Realized Gain (Loss) on: | | | |

Investments | | 2,797 | |

Foreign Currency Transactions | | 138 | |

Net Realized Gain (Loss) | | 2,935 | |

Change in Unrealized Appreciation (Depreciation) on: | | | |

Investments | | 40,226 | |

Foreign Currency Translations | | 9 | |

Change in Unrealized Appreciation (Depreciation) | | 40,235 | |

Net Realized Gain (Loss) and Change in Unrealized Appreciation (Depreciation) | | 43,170 | |

Net Increase (Decrease) in Net Assets Resulting from Operations | | $ | 44,712 | |

@ Amount is less than $500. | | | |

6 | The accompanying notes are an integral part of the financial statements. | |

| The Malaysia Fund, Inc. |

| |

| Financial Statements |

Statements of Changes in Net Assets | | Year Ended

December 31, 2007

(000) | | Year Ended

December 31, 2006

(000) |

Increase (Decrease) in Net Assets | | | | | |

Operations: | | | | | |

Net Investment Income (Loss) | | $ | 1,542 | | $ | 653 | |

Net Realized Gain (Loss) | | 2,935 | | 2,710 | |

Change in Unrealized Appreciation (Depreciation) | | 40,235 | | 18,946 | |

Net Increase (Decrease) in Net Assets Resulting from Operations | | 44,712 | | 22,309 | |

Distributions from and/or in Excess of: | | | | | |

Net Investment Income | | (1,748 | ) | (796 | ) |

Capital Share Transactions: | | | | | |

Reinvestment of Distributions (2,592 shares in 2006) | | — | | 15 | |

Repurchase of Shares (23,828 and 3,870 shares, respectively) | | (237 | ) | (25 | ) |

Net Increase (Decrease) in Net Assets Resulting from Capital Share Transactions | | (237 | ) | (10 | ) |

Total Increase (Decrease) | | 42,727 | | 21,503 | |

Net Assets: | | | | | |

Beginning of Period | | 74,546 | | 53,043 | |

End of Period (Including Undistributed (Distributions in Excess of) Net Investment Income of $(6) and $21, respectively) | | $ | 117,273 | | $ | 74,546 | |

| The accompanying notes are an integral part of the financial statements. | 7 |

| The Malaysia Fund, Inc. |

| |

Selected Per Share Data and Ratios | Financial Highlights |

| | Year Ended December 31, | |

| | 2007 | | 2006 | | 2005 | | 2004 | | 2003 | |

Net Asset Value, Beginning of Period | | $ | 7.70 | | $ | 5.48 | | $ | 6.09 | | $ | 5.76 | | $ | 4.63 | |

Net Investment Income (Loss)† | | 0.16 | | 0.07 | | 0.11 | | 0.08 | | 0.06 | |

Net Realized and Unrealized Gain (Loss) on Investments | | 4.46 | | 2.23 | | (0.59 | ) | 0.31 | | 1.22 | |

Total from Investment Operations | | 4.62 | | 2.30 | | (0.48 | ) | 0.39 | | 1.28 | |

Distributions from and/or in Excess of:

Net Investment Income | | (0.18 | ) | (0.08 | ) | (0.13 | ) | (0.06 | ) | (0.15 | ) |

Anti-Dilutive Effect of Share Repurchase Program | | 0.00 | # | 0.00 | # | — | | — | | 0.00 | # |

Net Asset Value, End of Period | | $ | 12.14 | | $ | 7.70 | | $ | 5.48 | | $ | 6.09 | | $ | 5.76 | |

Per Share Market Value, End of Period | | $ | 10.85 | | $ | 7.09 | | $ | 5.18 | | $ | 6.21 | | $ | 6.01 | |

TOTAL INVESTMENT RETURN: | | | | | | | | | | | |

Market Value | | 55.48 | % | 38.41 | % | (14.60 | )% | 4.40 | % | 60.33 | % |

Net Asset Value (1) | | 60.19 | % | 42.09 | % | (7.87 | )% | 6.83 | % | 27.67 | % |

RATIOS, SUPPLEMENTAL DATA: | | | | | | | | | | | |

Net Assets, End of Period (Thousands) | | $ | 117,273 | | $ | 74,546 | | $ | 53,043 | | $ | 59,017 | | $ | 55,758 | |

Ratio of Expenses to Average Net Assets(2) | | 1.24 | %+ | 1.49 | % | 1.57 | % | 1.50 | % | 1.78 | % |

Ratio of Net Investment Income (Loss) to Average

Net Assets(2) | | 1.56 | %+ | 1.08 | % | 1.80 | % | 1.38 | % | 1.16 | % |

Portfolio Turnover Rate | | 7 | % | 28 | % | 25 | % | 24 | % | 29 | % |

(2) Supplemental Information on the Ratios to Average Net Assets: | | | | | | | | | | | |

Ratio Before Expenses Waived by Administrator:

Ratio of Expenses to Average Net Assets | | 1.27 | %+ | 1.51 | % | 1.58 | % | 1.50 | % | N/A | |

Ratio of Net Investment Income (Loss) to

Average Net Assets | | 1.53 | %+ | 1.06 | % | 1.79 | % | 1.38 | % | N/A | |

(1) | Total investment return based on net asset value per share reflects the effects of changes in net asset value on the performance of the Fund during each period, and assumes dividends and distributions, if any, were reinvested. This percentage is not an indication of the performance of a stockholder’s investment in the Fund based on market value due to differences between the market price of the stock and the net asset value per share of the Fund. |

† | Per share amounts are based on average shares outstanding. |

# | Amount is less than $0.005 per share. |

+ | Reflects rebate of certain Fund expenses in connection with the investments in Morgan Stanley Institutional Liquidity Money Market Portfolio — Institutional Class during the period. As a result of such rebate, the expenses as a percentage of its net assets were effected by less than 0.005%. |

8 | The accompanying notes are an integral part of the financial statements. | |

| The Malaysia Fund, Inc. |

| |

Notes to Financial Statements | December 31, 2007 |

The Malaysia Fund, Inc. (the “Fund”) was incorporated on March 12, 1987 and is registered as a diversified, closed-end management investment company under the Investment Company Act of 1940, as amended (the “1940 Act”). The Fund’s investment objective is long-term capital appreciation through investment in equity securities of Malaysian companies.

A. Accounting Policies: The following significant accounting policies are in conformity with U.S. generally accepted accounting principles. Such policies are consistently followed by the Fund in the preparation of its financial statements. U.S. generally accepted accounting principles may require management to make estimates and assumptions that affect the reported amounts and disclosures in the financial statements. Actual results may differ from those estimates.

1. Security Valuation: Securities listed on a foreign exchange are valued at their closing price. Unlisted securities and listed securities not traded on the valuation date for which market quotations are readily available are valued at the mean between the current bid and asked prices obtained from reputable brokers. Equity securities listed on a U.S. exchange are valued at the latest quoted sales price on the valuation date. Equity securities listed or traded on NASDAQ, for which market quotations are available, are valued at the NASDAQ Official Closing Price. Debt securities purchased with remaining maturities of 60 days or less are valued at amortized cost, if it approximates value.

All other securities and investments for which market values are not readily available, including restricted securities, and those securities for which it is inappropriate to determine prices in accordance with the aforementioned procedures, are valued at fair value as determined in good faith under procedures adopted by the Board of Directors (the “Directors”), although the actual calculations may be done by others. Factors considered in making this determination may include, but are not limited to, information obtained by contacting the issuer, analysts, or the appropriate stock exchange (for exchange-traded securities), analysis of the issuer’s financial statements or other available documents and, if necessary, available information concerning other securities in similar circumstances.

Most foreign markets close before the New York Stock Exchange (NYSE). Occasionally, developments that could affect the closing prices of securities and other assets may occur between the times at which valuations of such securities are determined (that is, close of the foreign market on which the securities trade) and the close of business on the NYSE. If these developments are expected to materially affect the value of the securities, the valuations may be adjusted to reflect the estimated fair value as of the close of the NYSE, as determined in good faith under procedures established by the Directors.

2. Repurchase Agreements: The Fund may enter into repurchase agreements under which the Fund lends excess cash and takes possession of securities with an agreement that the counterparty will repurchase such securities. In connection with transactions in repurchase agreements, a bank as custodian for the Fund takes possession of the underlying securities (collateral), with a market value at least equal to the amount of the repurchase transaction, including principal and accrued interest. To the extent that any repurchase transaction exceeds one business day, the value of the collateral is marked-to-market on a daily basis to determine the adequacy of the collateral. In the event of default on the obligation to repurchase, the Fund has the right to liquidate the collateral and apply the proceeds in satisfaction of the obligation. In the event of default or bankruptcy by the counterparty to the agreement, realization and/or retention of the collateral or proceeds may be subject to legal proceedings.

The Fund, along with other affiliated investment companies, may utilize a joint trading account for the purpose of entering into one or more repurchase agreements. At December 31, 2007, the Fund did not have any outstanding repurchase agreements.

3. Foreign Currency Translation: The books and records of the Fund are maintained in U.S. dollars. Foreign currency amounts are translated into U.S. dollars at the mean of the bid and asked prices of such currencies against U.S. dollars last quoted by a major bank as follows:

· investments, other assets and liabilities at the prevailing rates of exchange on the valuation date;

· investment transactions and investment income at the prevailing rate of exchange on the dates of such transactions.

Although the net assets of the Fund are presented at the foreign exchange rates and market values at the close of the period, the Fund does not isolate that portion of the results of operations arising as a result of changes in the foreign exchange rates from the fluctuations arising from changes in the market prices of the securities held at period

9

| The Malaysia Fund, Inc. |

| |

Notes to Financial Statements (cont’d) | December 31, 2007 |

end. Similarly, the Fund does not isolate the effect of changes in foreign exchange rates from the fluctuations arising from changes in the market prices of securities sold during the period. Accordingly, realized and unrealized foreign currency gains (losses) due to securities transactions are included in the reported net realized and unrealized gains (losses) on investment transactions and balances.

Net realized gains (losses) on foreign currency transactions represent net foreign exchange gains (losses) from sales and maturities of foreign currency exchange contracts, disposition of foreign currencies, currency gains or losses realized between the trade and settlement dates on securities transactions, and the difference between the amount of investment income and foreign withholding taxes recorded on the Fund’s books and the U.S. dollar equivalent amounts actually received or paid. Net unrealized currency gains (losses) from valuing foreign currency denominated assets and liabilities at period end exchange rates are reflected as a component of unrealized appreciation (depreciation) on investments and foreign currency translations in the Statement of Assets and Liabilities. The change in net unrealized currency gains (losses) on foreign currency translations for the period is reflected in the Statement of Operations.

A significant portion of the Fund’s net assets consist of Malaysian equity securities and foreign currency. Future economic and political developments in Malaysia could adversely affect the liquidity or value, or both, of securities in which the Fund is invested. Changes in currency exchange rates will affect the value of and investment income from such investments. Foreign securities may be subject to greater price volatility, lower liquidity and less diversity than equity securities of companies based in the United States. In addition, foreign securities may be subject to substantial governmental involvement in the economy and greater social, economic and political uncertainty.

4. Derivatives: The Fund may use derivatives to achieve its investment objectives. The Fund may engage in transactions in futures contracts on foreign currencies, stock indices, as well as in options, swaps and structured products. Consistent with the Fund’s investment objectives and policies, the Fund may use derivatives for non-hedging as well as hedging purposes.

Following is a description of derivative instruments that the Fund has utilized and their associated risks:

Foreign Currency Exchange Contracts: The Fund may enter into foreign currency exchange contracts generally to attempt to protect securities and related receivables and payables against changes in future foreign exchange rates and, in certain situations, to gain exposure to a foreign currency. A foreign currency exchange contract is an agreement between two parties to buy or sell currency at a set price on a future date. The market value of the contract will fluctuate with changes in currency exchange rates. The contract is marked-to-market daily and the change in market value is recorded by the Fund as unrealized gain or loss. The Fund records realized gains or losses when the contract is closed equal to the difference between the value of the contract at the time it was opened and the value at the time it was closed. Risk may arise upon entering into these contracts from the potential inability of counterparties to meet the terms of their contracts and is generally limited to the amount of unrealized gain on the contracts, if any, at the date of default. Risks may also arise from unanticipated movements in the value of a foreign currency relative to the U.S. dollar. At December 31, 2007, the Fund did not have any outstanding foreign currency exchange contracts.

5. New Accounting Pronouncement: In September 2006, Statement of Financial Accounting Standards No. 157, Fair Value Measurements (“SFAS 157”), was issued and is effective for fiscal years beginning after November 15, 2007. SFAS 157 defines fair value, establishes a framework for measuring fair value and expands disclosures about fair value measurements. As of December 31, 2007, the Adviser does not believe the adoption of SFAS 157 will impact the amounts reported in the financial statements, however, additional disclosures will be required about the inputs used to develop the measurements of fair value and the effect of certain measurements reported in the Statement of Operations for a fiscal period.

6. Other: Security transactions are accounted for on the date the securities are purchased or sold. Realized gains and losses on the sale of investment securities are determined on the specific identified cost basis. Interest income is recognized on the accrual basis. Dividend income and distributions are recorded on the ex-dividend date (except certain dividends which may be recorded as soon as the Fund is informed of such dividends) net of applicable withholding taxes.

10

| The Malaysia Fund, Inc. |

| |

Notes to Financial Statements (cont’d) | December 31, 2007 |

B. Investment Advisory Fees: Morgan Stanley Investment Management Inc. (the “U.S. Adviser” or “MS Investment Management”) provides investment advisory services to the Fund under the terms of an Investment Advisory Agreement (the “Agreement”). Under the Agreement, the U.S. Adviser is paid a fee computed weekly and payable monthly at an annual rate of 0.90% of the Fund’s first $50 million of average weekly net assets, 0.70% of the Fund’s next $50 million of average weekly net assets and 0.50% of the Fund’s average weekly net assets in excess of $100 million.

AMMB Consultant Sdn Bhd (the “Malaysian Adviser”) provides investment related research and assistance on behalf of the Fund to Morgan Stanley Investment Management Inc. under terms of a contract. Under the contract, the Malaysian Adviser is paid a fee computed weekly and payable monthly at an annual rate of 0.25% of the Fund’s first $50 million of average weekly net assets, 0.15% of the Fund’s next $50 million of average weekly net assets and 0.10% of the Fund’s average weekly net assets in excess of $100 million.

Effective January 31, 2008, the Adviser has terminated the agreement with the Malaysian Adviser.

C. Administration Fees: MS Investment Management also serves as Administrator to the Fund pursuant to an Administration Agreement. Effective July 1, 2007 the Administration Agreement has been amended to 0.08% of the Fund’s average weekly net assets. Prior to July 1, 2007, under the Administration Agreement, the administration fee was 0.08% of the Fund’s average daily net assets. MS Investment Management has agreed to limit the administration fee so that it will be no greater than the previous administration fee (prior to November 1, 2004) of 0.02435% of the Fund’s average weekly net assets plus $24,000 per annum. This waiver is voluntary and may be terminated at any time. For the year ended December 31, 2007, approximately $31,000 of administration fees were waived pursuant to this arrangement. Under a sub-administration agreement between the Administrator and JPMorgan Investor Services Co. (“JPMIS”), a corporate affiliate of JPMorgan Chase Bank, N.A., JPMIS provides certain administrative services to the Fund. For such services, the Administrator pays JPMIS a portion of the fee the Administrator receives from the Fund. Administration costs (including out-of-pocket expenses) incurred in the ordinary course of providing services under the agreement, except pricing services and extraordinary expenses, will be covered under the administration fee.

D. Custodian Fees: JPMorgan Chase Bank, N.A. (the “Custodian”) serves as Custodian for the Fund. The Custodian holds cash, securities, and other assets of the Fund as required by the 1940 Act. Custody fees are payable monthly based on assets held in custody, investment purchases and sales activity and account maintenance fees, plus reimbursement for certain out-of-pocket expenses.

The Fund has entered into an arrangement with its Custodian whereby credits realized on uninvested cash balances were used to offset a portion of the Fund’s expenses. These custodian credits are shown as “Expense Offset” on the Statement of Operations.

E. Federal Income Taxes: It is the Fund’s intention to continue to qualify as a regulated investment company and distribute all of its taxable income. Accordingly, no provision for Federal income taxes is required in the financial statements. The Fund files tax returns with the U.S. Internal Revenue Service and various states. Generally, the tax authorities can examine all tax returns filed for the last three years.

The Fund may be subject to taxes imposed by countries in which it invests. The Fund is currently not subject to Malaysian withholding taxes on dividends and/or capital gains.

The Fund adopted the provisions of the Financial Accounting Standards Board’s (“FASB”) Interpretation number 48 Accounting for Uncertainty in Income Taxes (the “Interpretation”), on June 30, 2007. The Interpretation is to be applied to all open tax years as of the date of effectiveness. As of December 31, 2007, this did not result in an impact to the Fund’s financial statements.

The tax character of distributions paid may differ from the character of distributions shown on the Statements of Changes in Net Assets due to short-term capital gains being treated as ordinary income for tax purposes. The tax character of distributions paid during 2007 and 2006 were as follows:

2007 Distributions

Paid From:

(000) | | 2006 Distributions

Paid From:

(000) |

Ordinary

Income | | Long-term

Capital

Gain | | Ordinary

Income | | Long-term

Capital

Gain |

$1,748 | | $ — | | $796 | | $ — |

The amount and character of income and capital gain distributions to be paid by the Fund are determined in accordance with Federal income tax regulations, which may differ from U.S. generally accepted accounting principles. These book/tax differences are considered either temporary or permanent in nature.

11

| The Malaysia Fund, Inc. |

| |

Notes to Financial Statements (cont’d) | December 31, 2007 |

Temporary differences are generally due to differing book and tax treatments for the timing of the recognition of gains (losses) on certain investment transactions and the timing of the deductibility of certain expenses.

Permanent differences, primarily due to differing treatments of gains (losses) related to foreign currency transactions, expired capital loss carryforward and excess distribution, resulted in the following reclassifications among the components of net assets at December 31, 2007:

Increase (Decrease) | |

Accumulated

Undistributed

(Distributions in

Excess of) Net

Investment

Income (Loss)

(000) | | Accumulated

Net Realized

Gain (Loss)

(000) | | Paid-in

Capital

(000) | |

$ 179 | | $ (43) | | $(136) | |

At December 31, 2007, the Fund had no distributable earnings on a tax basis.

At December 31, 2007, the U.S. Federal income tax cost basis of investments was $53,669,000 and, accordingly, net unrealized appreciation for U.S. Federal income tax purposes was $64,528,000, of which $65,671,000 related to appreciated securities and $1,143,000 related to depreciated securities.

At December 31, 2007, the Fund had a capital loss carryforward for U.S. Federal income tax purposes of approximately $3,119,000 available to offset future capital gains of which $2,005,000 will expire on December 31, 2009, and $1,114,000 will expire on December 31, 2013. At December 31, 2007, the Fund had expired capital loss carryforward for U.S. Federal income tax purposes of approximately $94,000. During the year ended December 31, 2007, the Fund utilized capital loss carryforwards for U.S. Federal income tax purposes of approximately $2,625,000.

To the extent that capital loss carryforwards are used to offset any future capital gains realized during the carryover period as provided by U.S. Federal income tax regulations, no capital gains tax liability will be incurred by the Fund for gains realized and not distributed. To the extent that capital gains are offset, such gains will not be distributed to the stockholders.

F. Contractual Obligations: The Fund enters into contracts that contain a variety of indemnifications. The Fund’s maximum exposure under these arrangements is unknown. However, the Fund has not had prior claims or losses pursuant to these contracts and expects the risk of loss to be remote.

G. Security Transactions and Transactions with Affiliates: The Fund invests in the Institutional Class of the Morgan Stanley Institutional Liquidity Money Market Portfolio, an open-end management investment company managed by the Adviser. Investment Advisory fees paid by the Fund are reduced by an amount equal to its pro-rata share of advisory and administration fees paid by the Morgan Stanley Institutional Liquidity Money Market Portfolio. For the year ended December 31, 2007, advisory fees paid were reduced by approximately $1,000 relating to the Fund’s investment in the Morgan Stanley Institutional Liquidity Money Market Portfolio.

A summary of the Fund’s transactions in shares of the affiliated issuer during the year ended December 31, 2007 is as follows:

Market Value

December 31,

2006

(000) | | Purchases

at Cost

(000) | | Sales

Proceeds

(000) | | Dividend

Income

(000) | | Market Value December 31,

2007

(000) | |

$— | | $3,109 | | $840 | | $44 | | $2,269 | |

During the year ended December 31, 2007, the Fund made purchases and sales totaling approximately $6,843,000 and $7,267,000, respectively, of investment securities other than long-term U.S. Government securities and short-term investments. There were no purchases or sales of long-term U.S. Government securities.

H. Other: On July 15, 2002, the Fund commenced a share repurchase program for purposes of enhancing stockholder value and reducing the discount at which the Fund’s shares traded from their net asset value. During the year ended December 31, 2007, the Fund repurchased 23,828 of its shares at an average discount of 11.42% from net asset value per share. Since the inception of the program, the Fund has repurchased 80,801 of its shares at an average discount of 13.80% from net asset value per share. The Fund expects to continue to repurchase its outstanding shares at such time and in such amounts as it believes will further the accomplishment of the foregoing objectives, subject to review by the Directors.

On July 1, 2007, the Stockholder Servicing Agent changed from American Stock Transfer & Trust Company to Computershare Trust Company, N.A. Requests for information or any correspondence concerning the Dividend Reinvestment and Cash Purchase Plan after July 1, 2007 should be directed to Computershare Trust Company, N.A., P.O. Box 43010, Providence, Rhode Island 02940-3010, 1 (800) 231-2608.

12

| The Malaysia Fund, Inc. |

| |

Notes to Financial Statements (cont’d) | December 31, 2007 |

On December 14, 2007, the Officers of the Fund, pursuant to authority granted by the Directors, declared a distribution of $0.1782 per share, derived from net investment income, payable on January 7, 2008, to stockholders of record on December 21, 2007.

I. Supplemental Proxy Information (unaudited): On June 19, 2007, an annual meeting of the Fund’s stockholders was held for the pupose of voting on the following matter, the result of which were as follows:

Election of Directors by all stockholders:

| | For | | Withhold | |

| | | | | |

Frank L. Bowman | | 5,680,401 | | 684,079 | |

James F. Higgins | | 5,686,451 | | 678,029 | |

Manuel H. Johnson | | 5,680,792 | | 683,688 | |

For More Information About Portfolio Holdings (unaudited)

The Fund provides a complete schedule of portfolio holdings in its semi-annual and annual reports within 60 days of the end of the Fund’s second and fourth fiscal quarters. The semi-annual reports and the annual reports are filed electronically with the Securities and Exchange Commission (SEC) on Form N-CSRS and Form N-CSR, respectively. Morgan Stanley also delivers the semi-annual and annual reports to Fund stockholders and makes these reports available on its public website, www.morganstanley.com/msim. Each Morgan Stanley fund also files a complete schedule of portfolio holdings with the SEC for the Fund’s first and third fiscal quarters on Form N-Q. Morgan Stanley does not deliver the reports for the first and third fiscal quarters to stockholders, nor are the reports posted to the Morgan Stanley public website. You may, however, obtain the Form N-Q filings (as well as the Form N-CSR and N-CSRS filings) by accessing the SEC’s website, http://www.sec.gov. You may also review and copy them at the SEC’s public reference room in Washington, DC. Information on the operation of the SEC’s Public Reference Room may be obtained by calling the SEC at 1(800) SEC-0330. You can also request copies of these materials, upon payment of a duplicating fee, by electronic request at the SEC’s e-mail address (publicinfo@sec.gov) or by writing the public reference section of the SEC, Washington, DC 20549-0102.

In addition to filing a complete schedule of portfolio holdings with the SEC each fiscal quarter, the Fund makes portfolio holdings information available by periodically providing the information on its public website, www.morganstanley.com/msim.

The Fund provides a complete schedule of portfolio holdings on the public website on a calendar-quarter basis approximately 31 calendar days after the close of the calendar quarter. The Fund also provides Top 10 holdings information on the public website approximately 15 business days following the end of each month. You may obtain copies of the Fund’s monthly or calendar-quarter website postings, by calling 1(800) 231-2608.

13

| The Malaysia Fund, Inc. |

| |

Notes to Financial Statements (cont’d) | December 31, 2007 |

Proxy Voting Policy and Procedures and Proxy Voting Record (unaudited)

A copy of (1) the Fund’s policies and procedures with respect to the voting of proxies relating to the Fund’s portfolio securities; and (2) how the Fund voted proxies relating to portfolio securities during the most recent twelve-month period ended June 30, is available without charge, upon request, by calling 1 (800) 548-7786 or by visiting our website at www.morganstanley.com/msim. This information is also available on the SEC’s web site at www.sec.gov.

14

| The Malaysia Fund, Inc. |

| |

Report of Independent Registered Public

Accounting Firm | December 31, 2007 |

To the Stockholders and Board of Directors of

The Malaysia Fund, Inc.

We have audited the accompanying statement of assets and liabilities of The Malaysia Fund, Inc. (the “Fund”), including the portfolio of investments, as of December 31, 2007, and the related statement of operations for the year then ended, the statements of changes in net assets for each of the two years in the period then ended, and the financial highlights for each of the five years in the period then ended. These financial statements and financial highlights are the responsibility of the Fund’s management. Our responsibility is to express an opinion on these financial statements and financial highlights based on our audits.

We conducted our audits in accordance with the standards of the Public Company Accounting Oversight Board (United States). Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements and financial highlights are free of material misstatement. We were not engaged to perform an audit of the Fund’s internal control over financial reporting. Our audits included consideration of internal control over financial reporting as a basis for designing audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the Fund’s internal control over financial reporting. Accordingly, we express no such opinion. An audit also includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements and financial highlights, assessing the accounting principles used and significant estimates made by management, and evaluating the overall financial statement presentation. Our procedures included confirmation of securities owned as of December 31, 2007, by correspondence with the custodian. We believe that our audits provide a reasonable basis for our opinion.

In our opinion, the financial statements and financial highlights referred to above present fairly, in all material respects, the financial position of The Malaysia Fund, Inc. at December 31, 2007, the results of its operations for the year then ended, the changes in its net assets for each of the two years in the period then ended, and the financial highlights for each of the five years in the period then ended, in conformity with U.S generally accepted accounting principles.

Boston, Massachusetts

February 19, 2008

15

| The Malaysia Fund, Inc. |

| |

Director and Officer Information (unaudited) | December 31, 2007 |

Independent Directors:

Name, Age and Address of

Independent Director | | Position(s)

Held with

Registrant | | Length of

Time

Served* | | Principal Occupation(s) During Past 5 Years | | Number of

Portfolios in

Fund

Complex

Overseen

by

Independent

Director** | | Other Directorships Held by

Independent Director |

Frank L. Bowman (63)

c/o Kramer Levin Naftalis &

Frankel LLP

Counsel to the Independent

Directors

1177 Avenue of the

Americas

New York, NY 10036 | | Director | | Since

August

2006 | | President and Chief Executive Officer, Nuclear Energy Institute (policy organization) (since February 2005); Director or Trustee of various Retail Funds and Institutional Funds (since August 2006); Chairperson of the Insurance Sub-Committee of the Insurance, Valuation and Compliance Committee (since February 2007); formerly, variously, Admiral in the U.S. Navy, Director of Naval Nuclear Propulsion Program and Deputy Administrator— Naval Reactors in the National Nuclear Security Administration at the U.S. Department of Energy (1996-2004). Honorary Knight Commander of the Most Excellent Order of the British Empire. | | 180 | | Director of the National Energy Foundation, the U.S. Energy Association, the American Council for Capital Formation and the Armed Services YMCA of the USA. |

| | | | | | | | | | |

Michael Bozic (66)

c/o Kramer Levin Naftalis &

Frankel LLP

Counsel to the Independent

Directors

1177 Avenue of the

Americas

New York, NY 10036 | | Director | | Since

April

2004 | | Private Investor; Chairperson of the Insurance, Valuation and Compliance Committee (since October 2006); Director or Trustee of the Retail Funds (since April 1994) and the Institutional Funds (since July 2003); formerly, Chairperson of the Insurance Committee (July 2006- September 2006), Vice Chairman of Kmart Corporation (December 1998-October 2000), Chairman and Chief Executive Officer of Levitz Furniture Corporation (November 1995-November 1998) and President and Chief Executive Officer of Hills Department Stores (May 1991-July 1995); variously Chairman, Chief Executive Officer, President and Chief Operating Officer (1987- 1991) of the Sears Merchandise Group of Sears, Roebuck & Co. | | 182 | | Director of various business organizations. |

| | | | | | | | | | |

Kathleen A. Dennis (54)

c/o Kramer Levin Naftalis &

Frankel LLP

Counsel to the Independent

Directors

1177 Avenue of the

Americas

New York, NY 10036 | | Director | | Since

August

2006 | | President, Cedarwood Associates (mutual fund and investment management) (since July 2006); Chairperson of the Money Market and Alternatives Sub-Committee of the Investment Committee (since October 2006) and Director or Trustee of various Retail Funds and Institutional Funds (since August 2006); formerly, Senior Managing Director of Victory Capital Management (1993-2006). | | 180 | | Director of various non-profit organizations. |

16

| The Malaysia Fund, Inc. |

| |

Director and Officer Information (cont’d) | December 31, 2007 |

Independent Directors (cont’d) :

Name, Age and Address of

Independent Director | | Position(s)

Held with

Registrant | | Length of

Time

Served* | | Principal Occupation(s) During Past 5 Years | | Number of

Portfolios in

Fund

Complex

Overseen

by

Independent

Director** | | Other Directorships Held by

Independent Director |

Dr. Manuel H. Johnson (58)

c/o Johnson Smick

Group, Inc.

888 16th Street, N.W.

Suite 740

Washington, D.C. 20006 | | Director | | Since

July

1991 | | Senior Partner, Johnson Smick International, Inc. (consulting firm); Chairperson of the Investment Committee (since October 2006) and Director or Trustee of the Retail Funds (since July 1991) and the Institutional Funds (since July 2003); Co-Chairman and a founder of the Group of Seven Council (G7C) international economic commission; formerly, Chairperson of the Audit Committee (July 1991- September 2006); Vice Chairman of the Board of Governors of the Federal Reserve System and Assistant Secretary of the U.S. Treasury. | | 182 | | Director of NVR, Inc. (home construction); Director of Evergreen Energy. |

| | | | | | | | | | |

Joseph J. Kearns (65)

c/o Kearns & Associates

LLC

PMB754

23852 Pacific Coast

Highway

Malibu, CA 90265 | | Director | | Since August

1994 | | President, Kearns & Associates LLC (investment consulting); Chairperson of the Audit Committee (since October 2006) and Director or Trustee of the Retail Funds (since July 2003) and the Institutional Funds (since August 1994); formerly Deputy Chairperson of the Audit Committee (July 2003-September 2006) and Chairperson of the Audit Committee of the Institutional Funds (October 2001- July 2003); CFO of the J. Paul Getty Trust. | | 183 | | Director of Electro Rent Corporation (equipment leasing) and The Ford Family Foundation. |

| | | | | | | | | | |

Michael F. Klein (49)

c/o Kramer Levin Naftalis &

Frankel LLP

Counsel to the

Independent Directors

1177 Avenue of the Americas

New York, NY 10036 | | Director | | Since

August

2006 | | Managing Director, Aetos Capital, LLC (since March 2000) and Co-President, Aetos Alternatives Management, LLC (since January 2004); Chairperson of the Fixed-Income Sub-Committee of the Investment Committee (since October 2006) and Director or Trustee of various Retail Funds and Institutional Funds (since August 2006); formerly, Managing Director, Morgan Stanley & Co., Inc. and Morgan Stanley Dean Witter Investment Management, President, Morgan Stanley Institutional Funds (June 1998-March 2000) and Principal, Morgan Stanley & Co., Inc. and Morgan Stanley Dean Witter Investment Management (August 1997-December 1999). | | 180 | | Director of certain investment funds managed or sponsored by Aetos Capital LLC; Director of Sanitized AG and Sanitized Marketing AG (specialty chemicals). |

| | | | | | | | | | |

Michael E. Nugent (71)

c/o Triumph Capital, L.P.

445 Park Avenue

New York, NY 10022 | | Chairman of the Board and Director | | Chairman

of the

Boards

since July

2006 and

Trustee

since July

1991 | | General Partner of Triumph Capital, L.P. (private investment partnership); Chairman of the Boards of the Retail Funds and Institutional Funds (since July 2006); Director or Trustee of the Retail Funds (since July 1991) and the Institutional Funds (since July 2001); formerly, Chairperson of the Insurance Committee (until July 2006). | | 182 | | None. |

17

| The Malaysia Fund, Inc. |

| |

Director and Officer Information (cont’d) | December 31, 2007 |

Independent Directors (cont’d) :

Name, Age and Address of

Independent Director | | Position(s)

Held with

Registrant | | Length of

Time

Served* | | Principal Occupation(s) During Past 5 Years | | Number of

Portfolios in

Fund

Complex

Overseen

by

Independent

Director** | | Other Directorships Held by

Independent Director |

W. Allen Reed (60)

c/o Kramer Levin Naftalis &

Frankel LLP

Counsel to the

Independent Directors

1177 Avenue of the

Americas

New York, NY 10036 | | Director | | Since

August

2006 | | Chairperson of the Equity Sub-Committee of the Investment Committee (since October 2006) and Director or Trustee of various Retail Funds and Institutional Funds (since August 2006); formerly, President and CEO of General Motors Asset Management; Chairman and Chief Executive Officer of the GM Trust Bank and Corporate Vice President of General Motors Corporation (July 1994-December 2005). | | 180 | | Director of Temple-Inland Industries (packaging and forest products); Director of Legg Mason and Director of the Auburn University Foundation. |

| | | | | | | | | | |

Fergus Reid (75)

c/o Lumelite Plastics

Corporation

85 Charles Coleman Blvd.

Pawling, NY 12564 | | Director | | Since

June

1992 | | Chairman of Lumelite Plastics Corporation; Chairperson of the Governance Committee and Director or Trustee of the Retail Funds (since July 2003) and the Institutional Funds (since June 1992). | | 183 | | Trustee and Director of certain investment companies in the JPMorgan Funds complex managed by JP Morgan Investment Management Inc. |

Interested Directors:

Name, Age and Address of

Interested Director | | Position(s)

Held with

Registrant | | Term of

Office and

Length of

Time

Served* | | Principal Occupation(s) During Past 5 Years | | Number of

Portfolios in

Fund

Complex

Overseen

by

Interested Director** | | Other Directorships Held by

Interested Director |

James F. Higgins (59)

c/o Morgan Stanley Trust

Harborside Financial Center

Plaza Two

Jersey City, NJ 07311 | | Director | | Since

June

2000 | | Director or Trustee of the Retail Funds (since June 2000) and the Institutional Funds (since July 2003); Senior Advisor of Morgan Stanley (since August 2000). | | 181 | | Director of AXA Financial, Inc. and The Equitable Life Assurance Society of the United States (financial services). |

* This is the earliest date the Director began serving the Retail Funds or Institutional Funds. Each Director serves an indefinite term, until his or her successor is elected.

** The Fund Complex includes all open-end and closed-end funds (including all of their portfolios) advised by the Adviser and any funds that have an investment adviser that is an affiliated person of the Adviser (including, but not limited to, Morgan Stanley Investment Management, Inc.).

18

| The Malaysia Fund, Inc. |

| |

Director and Officer Information (cont’d) | December 31, 2007 |

Executive Officers:

| | | | Term of Office | | |

| | Position(s) Held | | and Length of | | |

Name, Age and Address of Executive Officer | | with Registrant | | Time Served* | | Principal Occupation(s) During Past 5 Years |

Ronald E. Robison (67)

Morgan Stanley Investment Management Inc.

522 Fifth Avenue

New York, NY 10036 | | President and

Principal

Executive

Officer | | President since September 2005 and Principal Executive Officer since May 2003 | | President (since September 2005) and Principal Executive Officer (since May 2003) of funds in the Fund Complex; President (since September 2005) and Principal Executive Officer (since May 2003) of the Van Kampen Funds; Managing Director, Director and/or Officer of the Adviser and various entities affiliated with the Adviser; Director of Morgan Stanley SICAV (since May 2004). Formerly, Executive Vice President (July 2003 to September 2005) of funds in the Fund Complex and the Van Kampen Funds; President and Director of the Institutional Funds (March 2001 to July 2003); Chief Administrative Officer of Morgan Stanley Investment Advisors Inc.; Chief Administrative Officer of Morgan Stanley Services Company Inc. |

| | | | | | |

J. David Germany (53)

Morgan Stanley Investment Management Limited

20 Bank Street

Canary Wharf

London, England

E144AD | | Vice President | | Since

February 2006 | | Managing Director and (since December 2005) Chief Investment Officer— Global Fixed Income of Morgan Stanley Investment Management; Managing Director and Director of Morgan Stanley Investment Management Limited; Vice President of the Retail Funds and Institutional Funds (since February 2006). |

| | | | | | |

Dennis F. Shea (54)

Morgan Stanley Investment Management Inc.

522 Fifth Avenue

New York, NY 10036 | | Vice President | | Since

February 2006 | | Managing Director and (since February 2006) Chief Investment Officer— Global Equity of Morgan Stanley Investment Management; Vice President of the Retail Funds and Institutional Funds (since February 2006). Formerly, Managing Director and Director of Global Equity Research at Morgan Stanley. |

| | | | | | |

Amy R. Doberman (45)

Morgan Stanley Investment Management Inc.

522 Fifth Avenue

New York, NY 10036 | | Vice President | | Since

July 2004 | | Managing Director and General Counsel, U.S. Investment Management of Morgan Stanley Investment Management (since July 2004); Vice President of the Retail Funds and Institutional Funds (since July 2004); Vice President of the Van Kampen Funds (since August 2004); Secretary (since February 2006) and Managing Director (since July 2004) of the Adviser and various entities affiliated with the Adviser. Formerly, Managing Director and General Counsel — Americas, UBS Global Asset Management (July 2000-July 2004). |

| | | | | | |

Carsten Otto (44)

Morgan Stanley Investment Management Inc.

522 Fifth Avenue

New York, NY 10036 | | Chief

Compliance

Officer | | Since

October 2004 | | Managing Director and Global Head of Compliance for Morgan Stanley Investment Management (since April 2007); and Chief Compliance Officer of Morgan Stanley Retail Funds and Institutional Funds (since October 2004). Formerly, U.S. Director of Compliance (October 2004 - April 2007) and Assistant Secretary and Assistant General Counsel of the Retail Funds. |

| | | | | | |

Stefanie V. Chang Yu (41)

Morgan Stanley Investment Management Inc.

522 Fifth Avenue

New York, NY 10036 | | Vice President | | Since

December 1997 | | Managing Director of the Adviser and various entities affiliated with the Adviser; Vice President of the Retail Funds (since July 2002) and the Institutional Funds (since December 1997). Formerly, Secretary of various entities affiliated with the Adviser. |

19

| The Malaysia Fund, Inc. |

| |

Director and Officer Information (cont’d) | December 31, 2007 |

Executive Officers (cont’d):

| | | | Term of Office | | |

| | Position(s) Held | | and Length of | | |

Name, Age and Address of Executive Officer | | with Registrant | | Time Served* | | Principal Occupation(s) During Past 5 Years |

Mary E. Mullin (40)

Morgan Stanley Investment Management Inc.

522 Fifth Avenue

New York, NY 10036 | | Secretary | | Since

June 1999 | | Executive Director of the Adviser and various entities affiliated with the Adviser; Secretary of the Retail Funds (since July 2003) and the Institutional Funds (since June 1999). |

| | | | | | |

James W. Garrett (39)

Morgan Stanley Investment Management Inc.

522 Fifth Avenue

New York, NY 10036 | | Treasurer and

Chief Financial

Officer | | Treasurer since February 2002 and Chief Financial Officer since July 2003 | | Head of Global Fund Administration; Managing Director of the Adviser and various entities affiliated with the Adviser; Treasurer and Chief Financial Officer of the Institutional Funds. |

* This is the earliest date the Officer began serving the Retail Funds or Institutional Funds. Each Officer serves an indefinite term, until his or her successor is elected.

In accordance with Section 303A. 12(a) of the New York Stock Exchange Listed Company Manual, the Fund’s Annual CEO Certification certifying as to compliance with NYSE’s Corporate Governance Listing Standards was submitted to the Exchange on August 8, 2007.

The Fund’s Principal Executive Officer and Principal Financial Officer Certifications required by Section 302 of the Sarbanes-Oxley Act of 2002 were filed with the Fund’s N-CSR and are available on the Securities and Exchange Commission’s Website at http://www.sec.gov.

20

Dividend Reinvestment and Cash Purchase Plan

Pursuant to the Dividend Reinvestment and Cash Purchase Plan (the “Plan”), each stockholder will be deemed to have elected, unless Computershare Trust Company, N.A. (the “Plan Agent”) is otherwise instructed by the stockholder in writing, to have all distributions automatically reinvested in Fund shares. Participants in the Plan have the option of making additional voluntary cash payments to the Plan Agent, annually, in any amount from $100 to $3,000, for investment in Fund shares.

Dividend and capital gain distributions will be reinvested on the reinvestment date in full and fractional shares. If the market price per share equals or exceeds net asset value per share on the reinvestment date, the Fund will issue shares to participants at net asset value or, if net asset value is less than 95% of the market price on the reinvestment date, shares will be issued at 95% of the market price. If net asset value exceeds the market price on the reinvestment date, participants will receive shares valued at market price. The Fund may issue shares of its Common Stock in connection with dividend reinvestment requirements at the discretion of the Board of Directors. Should the Fund declare a dividend or capital gain distribution payable only in cash, the Plan Agent will purchase Fund shares for participants in the open market as agent for the participants.

The Plan Agent’s fees for the reinvestment of dividends and distributions will be paid by the Fund. However, each participant’s account will be charged a pro rata share of brokerage commissions incurred on any open market purchases effected on such participant’s behalf. A participant will also pay brokerage commissions incurred on purchases made by voluntary cash payments. Although stockholders in the Plan may receive no cash distributions, participation in the Plan will not relieve participants of any income tax which may be payable on such dividends or distributions.

In the case of stockholders, such as banks, brokers or nominees, that hold shares for others who are the beneficial owners, the Plan Agent will administer the Plan on the basis of the number of shares certified from time to time by the stockholder as representing the total amount registered in the stockholder’s name and held for the account of beneficial owners who are participating in the Plan.

Stockholders who do not wish to have distributions automatically reinvested should notify the Plan Agent in writing. There is no penalty for non-participation or withdrawal from the Plan, and stockholders who have previously withdrawn from the Plan may rejoin at any time. Requests for additional information or any correspondence concerning the Plan should be directed to the Plan Agent at:

The Malaysia Fund, Inc.

Computershare Trust Company, N.A.

P.O. Box 43078

Providence, Rhode Island 02940-3078

1(800) 231-2608

21

Morgan Stanley Institutional Closed-End Funds

An Important Notice Concerning Our

U.S. Privacy Policy (unaudited)

We are required by federal law to provide you with a copy of our Privacy Policy annually.

The following Policy applies to current and former individual investors in Morgan Stanley Institutional closed-end funds. This Policy is not applicable to partnerships, corporations, trusts or other non-individual clients or account holders. Please note that we may amend this Policy at any time, and will inform you of any changes to this Policy as required by law.

We Respect Your Privacy

We appreciate that you have provided us with your personal financial information. We strive to maintain the privacy of such information while we help you achieve your financial objectives. This Policy describes what non-public personal information we collect about you, why we collect it, and when we may share it with others. We hope this Policy will help you understand how we collect and share non-public personal information that we gather about you. Throughout this Policy, we refer to the non-public information that personally identifies you or your accounts as “personal information.”

1. What Personal Information Do We Collect About You?

To serve you better and manage our business, it is important that we collect and maintain accurate information about you. We may obtain this information from applications and other forms you submit to us, from your dealings with us, from consumer reporting agencies, from our Web sites and from third parties and other sources.

For example:

· We may collect information such as your name, address, e-mail address, telephone/fax numbers, assets, income and investment objectives through applications and other forms you submit to us.

· We may obtain information about account balances, your use of account(s) and the types of products and services you prefer to receive from us through your dealings and transactions with us and other sources.

· We may obtain information about your creditworthiness and credit history from consumer reporting agencies.

· We may collect background information from and through third-party vendors to verify representations you have made and to comply with various regulatory requirements.

· If you interact with us through our public and private Web sites, we may collect information that you provide directly through online communications (such as an e-mail address). We may also collect information about your Internet service provider, your domain name, your computer’s operating system and Web browser, your use of our Web sites and your product and service preferences, through the use of “cookies.” “Cookies” recognize your computer each time you return to one of our sites, and help to improve our sites’ content and personalize your experience on our sites by, for example, suggesting offerings that may interest you. Please consult the Terms of Use of these sites for more details on our use of cookies.

2. When Do We Disclose Personal Information We Collect About You?

To provide you with the products and services you request, to serve you better and to manage our business, we may disclose personal information we collect about you to our affiliated companies and to non-affiliated third parties as required or permitted by law.

A. Information We Disclose to Our Affiliated Companies. We do not disclose personal information that we collect about you to our affiliated companies except to enable them to provide services on our behalf or as otherwise required or permitted by law.

22

Morgan Stanley Institutional Closed-End Funds

An Important Notice Concerning Our

U.S. Privacy Policy (cont’d)

B. Information We Disclose to Third Parties. We do not disclose personal information that we collect about you to non-affiliated third parties except to enable them to provide services on our behalf, to perform joint marketing agreements with other financial institutions, or as otherwise required or permitted by law. For example, some instances where we may disclose information about you to nonaffiliated third parties include: for servicing and processing transactions, to offer our own products and services, to protect against fraud, for institutional risk control, to respond to judicial process or to perform services on our behalf. When we share personal information with these companies, they are required to limit their use of personal information to the particular purpose for which it was shared and they are not allowed to share personal information with others except to fulfill that limited purpose.

3. How Do We Protect the Security and Confidentiality of Personal Information We Collect About You?

We maintain physical, electronic and procedural security measures to help safeguard the personal information we collect about you. We have internal policies governing the proper handling of client information. Third parties that provide support or marketing services on our behalf may also receive personal information, and we require them to adhere to confidentiality standards with respect to such information.

23

The Malaysia Fund, Inc.

Directors | |

Michael E. Nugent | J. David Germany |

| Vice President |

Frank L. Bowman | |

| Dennis F. Shea |

Michael Bozic | Vice President |

| |

Kathleen A. Dennis | Amy R. Doberman |

| Vice President |

James F. Higgins | |

| Stefanie V. Chang Yu |

Dr. Manuel H. Johnson | Vice President |

| |

Joseph J. Kearns | James W. Garrett |

| Treasurer and Chief |

Michael F. Klein | Financial Officer |

| |

W. Allen Reed | Carsten Otto |

| Chief Compliance Officer |

Fergus Reid | |

| Mary E. Mullin |

Officers | Secretary |

Michael E. Nugent | |

Chairman of the Board and | |

Director | |

| |

Ronald E. Robison | |

President and Principal | |

Executive Officer | |

U.S. Investment Adviser and Administrator

Morgan Stanley Investment Management Inc.

522 Fifth Avenue

New York, New York 10036

Malaysian Investment Adviser

AMMB Consultant Sdn Bhd

9th Floor, Bangurian Arab-Malaysian

55 Jalan Raja Chulan, 50200

Kuala Lumpur, Malaysia

Custodian

JPMorgan Chase Bank, N.A.

270 Park Avenue

New York, New York 10017

Stockholder Servicing Agent

Computershare Trust Company, N.A.

250 Royall Street

Canton, Massachusetts 02021

Legal Counsel

Clifford Chance US LLP

31 West 52nd Street

New York, New York 10019-6131

Independent Registered Public Accounting Firm

Ernst & Young LLP

200 Clarendon Street

Boston, Massachusetts 02116

For additional Fund information, including the Fund’s net asset value per share and information regarding the investments comprising the Fund’s portfolio, please call 1(800) 231-2608 or visit our website at www.morganstanley.com/msim. All investments involve risks, including the possible loss of principal.

© 2008 Morgan Stanley

CEMFANN IU08-00734I-Y12/07

Item 2. Code of Ethics.

(a) The Fund has adopted a code of ethics (the “Code of Ethics”) that applies to its principal executive officer, principal financial officer, principal accounting officer or controller, or persons performing similar functions, regardless of whether these individuals are employed by the Fund or a third party.

(b) No information need be disclosed pursuant to this paragraph.

(c) Not applicable.

(d) Not applicable.

(e) Not applicable.

(f)

(1) The Fund’s Code of Ethics is attached hereto as Exhibit 12 A.

(2) Not applicable.

(3) Not applicable.

Item 3. Audit Committee Financial Expert.

The Fund’s Board of Trustees has determined that Joseph J. Kearns, an “independent” Trustee, is an “audit committee financial expert” serving on its audit committee. Under applicable securities laws, a person who is determined to be an audit committee financial expert will not be deemed an “expert” for any purpose, including without limitation for the purposes of Section 11 of the Securities Act of 1933, as a result of being designated or identified as an audit committee financial expert. The designation or identification of a person as an audit committee financial expert does not impose on such person any duties, obligations, or liabilities that are greater than the duties, obligations, and liabilities imposed on such person as a member of the audit committee and Board of Trustees in the absence of such designation or identification.

Item 4. Principal Accountant Fees and Services.

(a)(b)(c)(d) and (g). Based on fees billed for the periods shown:

2007

| | Registrant | | Covered Entities(1) | |

Audit Fees | | $ | 40,200 | | N/A | |

| | | | | |

Non-Audit Fees | | | | | |

Audit-Related Fees | | $ | | $ | 731,800 | (2) |

Tax Fees | | $ | 3,100 | (3) | $ | 104,020 | (4) |

All Other Fees | | $ | | $ | 166,270 | (5) |

Total Non-Audit Fees | | $ | 3,100 | | $ | 1,002,090 | |

| | | | | |

Total | | $ | 43,300 | | $ | 1,002,090 | |

2006

| | Registrant | | Covered Entities(1) | |

Audit Fees | | $ | 39,000 | | N/A | |

| | | | | |

Non-Audit Fees | | | | | |

Audit-Related Fees | | $ | | $ | 756,000 | (2) |

Tax Fees | | $ | 3,000 | (3) | $ | 79,422 | (6) |

All Other Fees | | $ | | $ | 531,708 | (7) |

Total Non-Audit Fees | | $ | 3,000 | | $ | 1,367,130 | |

| | | | | |

Total | | $ | 42,000 | | $ | 1,367,130 | |

N/A- Not applicable, as not required by Item 4.

(1) Covered Entities include the Adviser (excluding sub-advisors) and any entity controlling, controlled by or under common control with the Adviser that provides ongoing services to the Registrant.

(2) Audit-Related Fees represent assurance and related services provided that are reasonably related to the performance of the audit of the financial statements of the Covered Entities and funds advised by the Adviser or its affiliates, specifically attestation services provided in connection with a SAS 70 Report.

&nb sp;

(3) Tax Fees represent tax advice and compliance services provided in connection with the review of the Registrant’s tax returns.

(4) Tax Fees represent tax advice services provided to Covered Entities, including research and identification of PFIC Entities and consulting services for the Van Kampen Funds.

(5) All Other Fees represent attestation services provided in connection with performance presentation standards.

(6) Tax Fees represent tax advice services provided to Covered Entities, including research and identification of PFIC Entities.

(7) All Other Fees represent attestation services provided in

connection with performance presentation standards and a compliance review project performed.

(e)(1) The audit committee’s pre-approval policies and procedures are as follows:

APPENDIX A

AUDIT COMMITTEE

AUDIT AND NON-AUDIT SERVICES

PRE-APPROVAL POLICY AND PROCEDURES

OF THE

MORGAN STANLEY RETAIL AND INSTITUTIONAL FUNDS

AS ADOPTED AND AMENDED JULY 23, 2004,(1)

1. Statement of Principles

The Audit Committee of the Board is required to review and, in its sole discretion, pre-approve all Covered Services to be provided by the Independent Auditors to the Fund and Covered Entities in order to assure that services performed by the Independent Auditors do not impair the auditor’s independence from the Fund.

The SEC has issued rules specifying the types of services that an independent auditor may not provide to its audit client, as well as the audit committee’s administration of the engagement of the independent auditor. The SEC’s rules establish two different approaches to pre-approving services, which the SEC considers to be equally valid. Proposed services either: may be pre-approved without consideration of specific case-by-case services by the Audit Committee (“general pre-approval”); or require the specific pre-approval of the Audit Committee or its delegate (“specific pre-approval”). The Audit Committee believes that the combination of these two approaches in this Policy will result in an effective and efficient procedure to pre-approve services performed by the Independent Auditors. As set forth in this Policy, unless a type of service has received general pre-approval, it will require specific pre-approval by the Audit Committee (or by any member of the Audit Committee to which pre-approval authority has been delegated) if it is to be provided by the Independent Auditors. Any proposed services exceeding pre-approved cost levels or budgeted amounts will also require specific pre-approval by the Audit Committee.

The appendices to this Policy describe the Audit, Audit-related, Tax and All Other services that have the general pre-approval of the Audit Committee. The term of any general pre-approval is 12 months from the date of pre-approval, unless the Audit

(1) This Audit Committee Audit and Non-Audit Services Pre-Approval Policy and Procedures (the “Policy”), adopted as of the date above, supersedes and replaces all prior versions that may have been adopted from time to time.

Committee considers and provides a different period and states otherwise. The Audit Committee will annually review and pre-approve the services that may be provided by the Independent Auditors without obtaining specific pre-approval from the Audit Committee. The Audit Committee will add to or subtract from the list of general pre-approved services from time to time, based on subsequent determinations.

The purpose of this Policy is to set forth the policy and procedures by which the Audit Committee intends to fulfill its responsibilities. It does not delegate the Audit Committee’s responsibilities to pre-approve services performed by the Independent Auditors to management.

The Fund’s Independent Auditors have reviewed this Policy and believes that implementation of the Policy will not adversely affect the Independent Auditors’ independence.

2. Delegation

As provided in the Act and the SEC’s rules, the Audit Committee may delegate either type of pre-approval authority to one or more of its members. The member to whom such authority is delegated must report, for informational purposes only, any pre-approval decisions to the Audit Committee at its next scheduled meeting.

3. Audit Services