Filed by: BHP Billiton Plc

and BHP Billiton Limited

Pursuant to Rule 425 under the Securities Act of 1933

Subject Company: Rio Tinto plc

Commission File No.: 001-10533

The following are slides comprising a presentation that was given by Don Argus, Chairman, BHP Billiton on November 11, 2008.

Resourcing the Future 11 November 2008 Don Argus Chairman SHANGHAI |

Slide 2 Disclaimer By reviewing/attending this presentation you agree to be bound by the following conditions. The directors of BHP Billiton Limited and BHP Billiton Plc (“BHP Billiton") accept responsibility for the information contained in this presentation. Having taken all reasonable care to ensure that such is the case, the information contained in this presentation is, to the best of the knowledge and belief of the directors of BHP Billiton, in accordance with the facts and contains no omission likely to affect its import. Subject to the above, neither BHP Billiton nor any of its directors, officers, employees or advisers nor any other person makes any representation or warranty, express or implied, as to, and accordingly no reliance should be placed on, the fairness, accuracy or completeness of the information contained in the presentation or of the views given or implied. To the extent permitted by law, neither BHP Billiton nor any of its directors, officers, employees or advisers nor any other person shall have any liability whatsoever for any errors or omissions or any loss howsoever arising, directly or indirectly, from any use of this information or its contents or otherwise arising in connection therewith. Information about Rio Tinto plc and Rio Tinto Limited ("Rio Tinto") is based on public information which has not been independently verified. This presentation is for information purposes only and does not constitute or form part of any offer for sale or issue of any securities or an offer or invitation to purchase or subscribe for any such securities, nor shall it or any part of it be relied on in connection with, any contract or investment decision, nor does it constitute a proposal to make a takeover bid or the solicitation of any vote or approval in any jurisdiction, nor shall there be any sale of securities in any jurisdiction in which such offer, solicitation or sale would be unlawful prior to registration or qualification under the securities laws of any such jurisdiction (or under an exemption from such requirements). No offering of securities shall be made into the United States except pursuant to registration under the US Securities Act of 1933, as amended, or an exemption therefrom. Neither this presentation nor any copy of it may be taken or transmitted or distributed or redistributed (directly or indirectly) in Japan or Malaysia. The distribution of this document in other jurisdictions may be restricted by law and persons into whose possession this document comes should inform themselves about, and observe, any such restrictions. This presentation is directed only at persons who (i) are persons falling within Article 49(2)(a) to (d) ("high net worth companies, unincorporated associations etc.") of the Financial Services and Markets Act 2000 (Financial Promotion) Order 2005 (as amended) (the "Order") or (ii) have professional experience in matters relating to investments falling within Article 19(5) of the Order or (iii) are outside the United Kingdom (all such persons being referred to as "relevant persons"). This presentation must not be acted on or relied on by persons who are not relevant persons. Certain statements in this presentation are forward-looking statements (including statements regarding contribution synergies, future cost savings, the cost and timing of development projects, future production volumes, increases in production and infrastructure capacity, the identification of additional mineral Reserves and Resources and project lives and, without limitation, other statements typically containing words such as "intends," "expects," "anticipates," "targets," plans," "estimates" and words of similar import.) These statements are based on current expectations and beliefs and numerous assumptions regarding BHP Billiton's present and future business strategies and the environments in which BHP Billiton and Rio Tinto will operate in the future and such assumptions, expectations and beliefs may or may not prove to be correct and by their nature, are subject to a number of known and unknown risks and uncertainties that could cause actual results, performance and achievements to differ materially. Factors that could cause actual results or performance to differ materially from those expressed or implied in the forward-looking statements include, but are not limited to, BHP Billiton's ability to successfully combine the businesses of BHP Billiton and Rio Tinto and to realise expected synergies from that combination, the presence of a competitive proposal in relation to Rio Tinto, satisfaction of any conditions to any proposed transaction, including the receipt of required regulatory and anti-trust approvals, Rio Tinto’s willingness to enter into any proposed transaction, the successful completion of any transaction, and the risk factors discussed in BHP Billiton's and Rio Tinto’s filings with the U.S. Securities and Exchange Commission ("SEC") (including in Annual Reports on Form 20-F for the most recent fiscal years) which are available at the SEC's website (http://www.sec.gov). Save as required by law or the rules of the UK Listing Authority and the London Stock Exchange, the UK Takeover Panel, or the listing rules of ASX Limited, BHP Billiton undertakes no duty to update any forward-looking statements in this presentation |

Slide 3 Disclaimer (continued) No statement concerning expected cost savings, revenue benefits (and resulting incremental EBITDA) and EPS accretion in this presentation should be interpreted to mean that the future earnings per share of the enlarged BHP Billiton group for current and future financial years will necessarily match or exceed the historical or published earnings per share of BHP Billiton, and the actual estimated cost savings and revenue benefits (and resulting EBITDA enhancement) may be materially greater or less than estimated. References in this presentation to “$” are to United States dollars unless otherwise specified. In connection with the offer and sale of securities BHP Billiton would issue to Rio Tinto plc US shareholders and Rio Tinto plc ADS holders, BHP Billiton has filed with the SEC a Registration Statement on Form F-4 ( the “Registration Statement”), which contains a preliminary prospectus ( the “Prospectus”), and will file additional relevant materials with the SEC. This communication is not a substitute for the Registration Statement or the Prospectus that BHP Billiton has filed, or any amendments or supplements to those documents BHP Billiton may file, with the SEC. U.S. INVESTORS AND U.S. HOLDERS OF RIO TINTO PLC SECURITIES AND ALL HOLDERS OF RIO TINTO PLC ADSs ARE URGED TO READ THE REGISTRATION STATEMENT, THE PROSPECTUS AND ANY OTHER DOCUMENTS MADE AVAILABLE TO THEM AND/OR FILED WITH THE SEC REGARDING THE POTENTIAL TRANSACTION, AS WELL AS ANY AMENDMENTS AND SUPPLEMENTS TO THOSE DOCUMENTS, WHEN THEY BECOME AVAILABLE BECAUSE THEY WILL CONTAIN IMPORTANT INFORMATION. Investors and security holders are able to obtain a free copy of the Registration Statement and the Prospectus as well as other relevant documents filed with the SEC at the SEC's website ( http://www.sec.gov). Copies of such documents may also be obtained from BHP Billiton without charge. BHP Billiton Limited is not required to, and does not plan to, prepare and file with the SEC a registration statement in respect of the Rio Tinto Limited Offer. Accordingly, Rio Tinto Limited shareholders should carefully consider the following: The Rio Tinto Limited Offer will be an exchange offer made for the securities of a foreign company. Such offer is subject to disclosure requirements of a foreign country that are different from those of the United States. Financial statements included in the document will be prepared in accordance with foreign accounting standards that may not be comparable to the financial statements of United States companies. It may be difficult for you to enforce your rights and any claim you may have arising under the U.S. federal securities laws, since the issuers are located in a foreign country, and some or all of their officers and directors may be residents of foreign countries. You may not be able to sue a foreign company or its officers or directors in a foreign court for violations of the U.S. securities laws. It may be difficult to compel a foreign company and its affiliates to subject themselves to a U.S. court's judgment. You should be aware that BHP Billiton may purchase securities of either Rio Tinto plc or Rio Tinto Limited otherwise than under the exchange offer, such as in open market or privately negotiated purchases. Information Relating to the US Offer for Rio Tinto plc Information for US Holders of Rio Tinto Limited Shares Information Relating to the US Offer for Rio Tinto plc and the Rio Tinto Limited Offer for Rio Tinto shareholders located in the US |

Slide 4 -2 0 2 4 6 8 10 12 14 Short-term global economic turmoil Source: IMF World Economic Indicators, October / November 2008 Gross domestic production (% growth, constant 2006 US$) Asian Banking Crisis Technology Correction Current Financial Crisis China Emerging and developing economies Advanced economies |

Slide 5 Housing Structural Reform High Value Manufacturing Urbanisation In the long-term China remains on the steep part of the development curve supported by six growth drivers Rising Incomes Rural Development |

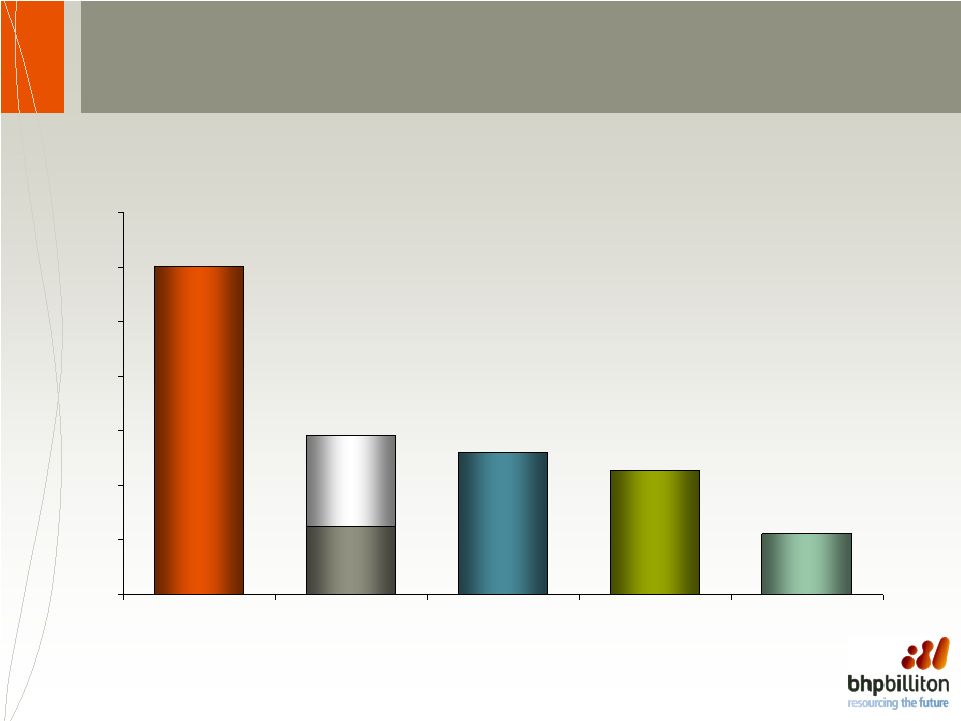

Slide 6 The significance of the resources sector to Australia GDP (Percent of GDP) Exports Percent (based on FOB value) 17% 83% 0% 20% 40% 60% 80% 100% 2006-07 46% 54% 0% 20% 40% 60% 80% 100% 2007 Total = A$168bn Total = A$998bn Other exports Mineral commodities** All other sectors Mining sector* * Direct and indirect contribution to GDP, contribution grew by 7.3% (absolute value) over this period, compared with 2.3% for all other sectors ** Defined as mineral fuels/lubricants (coal, petroleum products and gas) and metalliferous ores (iron ore, copper, nickel, bauxite/alumina, uranium, other base and precious metals) Source: Australian Bureau of Statistics 5204.0—Australian System of National Accounts, 2006–07, Table 9—Industry Gross Value Added (chain volume measures); Australian Bureau of Statistics 5209.0—Australian National Accounts Input-Output Tables 1998–99; Australian Bureau of Statistics, 5368.0 International Trade in Goods and Services, Table 12a,b |

Slide 7 Outstanding performance Neptune – Gulf of Mexico |

Slide 8 Our core strategy sets us apart in our industry • Focus on world-class assets that are large, low-cost and expandable • Focus on the extraction of upstream natural resources • Portfolio diversified by commodity, customer and geography reducing the volatility of cash flows • Maintenance of a deep diversified inventory of growth options • Focus on export orientated products • Overriding commitment to ethics, safety, environmental practice and community engagement • Employer of choice, and a preferred partner for countries and customers Simplicity Accountability Effectiveness |

Slide 9 0 100 200 300 400 500 600 700 BHP Billiton Rio Tinto(a) Vale Xstrata Anglo American Note: EBIT and Employees as per last published Annual Report, data does not include contractors. BHP Billiton as at 30-Jun-2008; Rio Tinto, Vale, Xstrata and Anglo American as at 31-Dec-2007. (a) Rio Tinto Post Alcan EBIT based on CY2007 full year proforma results. EBIT per employee (US$’000) Pre-Alcan Post-Alcan Despite our size, simplicity is a core element of this strategy |

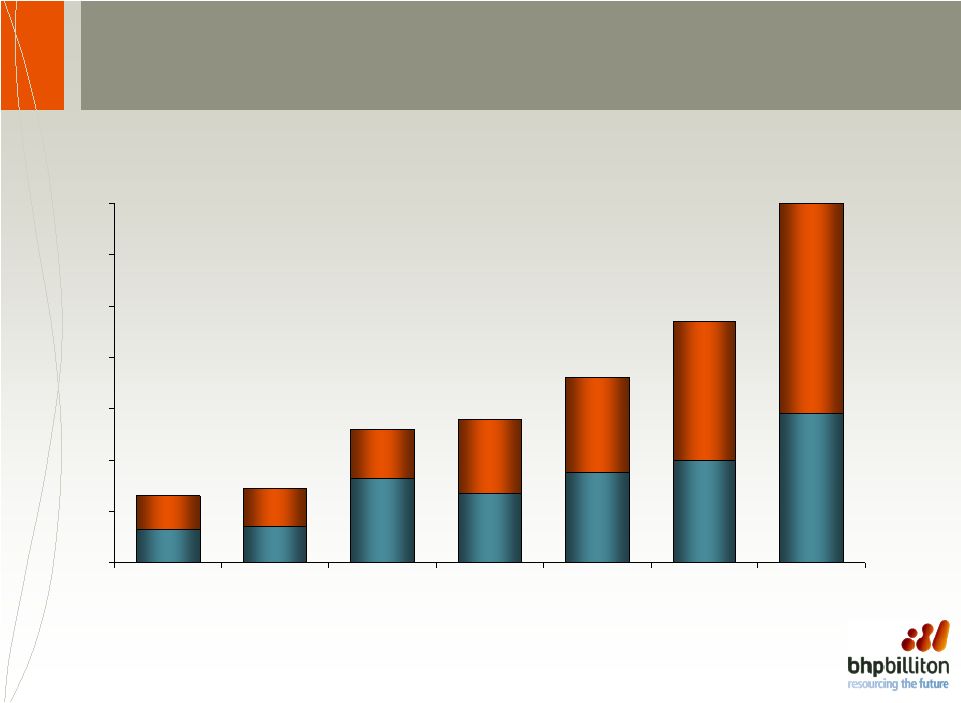

Slide 10 Outstanding results – delivering superior returns to shareholders Ordinary dividends per share (US cents per share) 13 15 26 28 36 47 70 0 10 20 30 40 50 60 70 FY2002 FY2003 FY2004 FY2005 FY2006 FY2007 FY2008 Note: Two interim dividends were paid in FY2004. H1 H2 |

Slide 11 Outstanding results – driven by strategy and execution • Achieved record profit for the 7 th consecutive year • Attributable profit up 12%, EPS up 18% • Dividend rebased upwards a signal of our outlook confidence • Full year dividend of 70 US cents per share, 49% increase • Production increases in 13 commodities, records in 7 • 10 major growth projects completed • A further 7 major projects sanctioned by the Board • Strong performance demonstrates the power of our diversified and high margin portfolio Underlying EBIT margin (a) (FY2008) 48% 67% 30% 31% 62% 51% 58% 24% 25% 20% Iron Ore Manganese Energy Coal Metallurgical Coal Diamonds and Specialty Products Base Metals Petroleum Stainless Steel Materials Aluminium Group Notes: (a) EBIT Margin excludes third party trading activities. |

Slide 12 Underlying EBIT margin (a) (%) The benefits of diversification across a high margin portfolio 0 10 20 30 40 50 60 70 80 H1 H2 H1 H2 H1 H2 H1 H2 H1 H2 H1 H2 H1 H2 Petroleum Aluminium Base Metals D&SP SSM Iron Ore Manganese Met Coal Energy Coal BHP Billiton FY2002 FY2003 FY2004 FY2005 FY2006 FY2007 FY2008 Notes: (a) FY2002 to FY2005 are calculated under UKGAAP. Subsequent periods are calculated under IFRS. All periods exclude third party trading activities. |

Slide 13 As at 14 August 2008 Proposed capital expenditure SSM Energy Coal D&SP Iron Ore Base Metals Petroleum Met Coal CSG Manganese Aluminium 2009 Execution 2013 Feasibility Future Options Maintenance of a deep diversified inventory of growth options Boffa/Santou Refinery Pyrenees Alumar Atlantis North Bakhuis Worsley E&G Douglas- Middelburg Newcastle Third Port WA Iron Ore Quantum 2 Potash - Jansen WA Iron Ore Quantum 1 Nimba Angola & DRC WA Iron Ore RGP 5 CW Africa Exploration Turrum NWS CWLH DRC Smelter NWS T5 NWS Nth Rankin B WA Iron Ore RGP 4 Kipper Olympic Dam Expansion 2 Browse LNG Olympic Dam Expansion 1 CMSA Heap Leach 2 Shenzi Nth Klipspruit NWS Angel Shenzi GEMCO Potash Olympic Dam Expansion 3 Thebe CMSA Pyro Expansion Wards Well Scarborough Caroona WA Iron Ore RGP 6 Eastern Indonesian Facility Escondida 3rd Conc RBM Puma Blackwater UG NWS WFGH MKO Talc Cannington Life Ext Corridor Sands Kennedy Gabon Saraji Exp Red Hill UG Resolution Neptune Nth GEMCO Exp Ekati Guinea Alumina Angostura Gas HPX3 Maruwai Stage 1 Knotty Head Samarco 4 Peak Downs Exp (Caval Ridge) Macedon CMSA Heap Leach 1 Antamina Exp Newcastle Third Port Exp Mad Dog West Mt Arthur Coal UG Cerrejon Opt Exp Daunia Maruwai Stage 2 Navajo Sth Perseverance Deeps Mt Arthur Coal OC (MAC20) Mt Arthur Coal (MACX) New Saraji Goonyella Expansions Escondida Moly $501m-$2bn $2bn+ $500m |

Slide 14 Focused on low risk volume growth from existing assets and in our own backyard By project type (b) 87% 13% Brownfield Greenfield By region (c) Existing New 3% 97% 63% Notes: a) Growth in production volumes on a copper equivalent units basis between CY2007 and CY2012 calculated using BHP Billiton estimates for BHP Billiton production. Production volumes exclude BHP Billiton’s Specialty Products operation and all bauxite production. All energy coal businesses are included. Alumina volumes reflect only tonnes available for external sale. Conversion of production forecasts to copper equivalent units completed using long term consensus price forecasts, plus BHP Billiton assumptions for diamonds, domestic coal and manganese. Prices as at July 2008. b) Brownfield includes growth from existing operations as at 31-Dec-2007, as well as expansions and additional developments of, or around those assets. c) Existing regions represents those countries in which BHP Billiton already has asset operating as at 31-Dec-2007. Expected production growth (a) (Copper equivalent tonnes, CY2007-CY2012) |

Slide 15 The Rio Tinto Offer |

Slide 16 Notes: a) Australian CGT rollover relief will be available for Australian resident shareholders accepting the Rio Tinto Ltd Offer if compulsory acquisition is reached in the Rio Tinto Ltd Offer. UK “rollover” provisions will apply to accepting Rio Tinto plc shareholders if there are at least 70 per cent acceptances under the Rio Tinto plc Offer. b) Estimated total incremental EBITDA (nominal) based on publicly available information. To be read in conjunction with the notes in Appendix IV of BHP Billiton’s announcement dated 6-Feb-2008. Full run rate synergies expected in the seventh full year following completion. c) Premium based on the combined volume-weighted market capitalisation of Rio Tinto based on the volume-weighted average closing share prices over the month ended 31-Oct-2007 of £43.09 and A$109.20 for Rio Tinto plc and Rio Tinto Ltd respectively and volume-weighted average closing share prices over the month ended 31-Oct-2007 of BHP Billiton Plc and BHP Billiton Ltd of £17.99 and A$45.77 respectively. Based on BHP Billiton and Rio Tinto issued ordinary shares outstanding (excluding Treasury shares and cross shareholdings eg. Rio Tinto plc’s shareholding in Rio Tinto Ltd) as at 9-Nov-2007 and exchange rates of 2.077 US$/£ and 0.927 US$/A$ as at 31-Oct-2007. NOTE: Consistent with the UK City Code on Takeovers and Mergers, the offer represents a 29% discount based on the combined market capitalisation of Rio Tinto based on the closing share prices of Rio Tinto plc of £43.50 on 7-Nov-2007 and Rio Tinto Ltd of A$113.40 on 8-Nov-2007 and closing share prices of BHP Billiton Plc and BHP Billiton Ltd of £11.40 and A$31.60 respectively on 5-Nov-2008. Based on BHP Billiton and Rio Tinto issued ordinary shares outstanding (excluding Treasury shares and cross shareholdings eg. Rio Tinto plc’s shareholding in Rio Tinto Ltd) as at 5-Nov-2008 and exchange rates of 1.615 US$/£ and 0.701 US$/A$ as at 5-Nov-2008. d) The offer is conditional on more than 50% acceptances of the publicly held shares in each of Rio Tinto plc and Rio Tinto Ltd. e) i.e. if BHP Billiton acquires 100% of the shares in Rio Tinto Limited and Rio Tinto plc on the 3.4:1 announced offer terms. • Pre-conditional offer, capable of acceptance by shareholders following completion of regulatory processes and posting of offer documents • Regulatory processes anticipated to be completed by early 2009 • Rio Tinto shareholders are being offered 3.4 BHP Billiton shares for every Rio Tinto share held • All share offer – No shareholder forced to exit – exchange shares into a stronger combined company – Ability to participate in the synergies as well as the premium – CGT rollover relief for eligible shareholders (a) • Unlocks US$3.7bn per annum of quantifiable synergies (b) • The offer represents a 45% premium to the undisturbed price (c) • 50% minimum acceptance condition (d) • Proposed share buyback of up to US$30bn following completion if the offer is successful (e) • BHP Billiton believes this offer is compelling for Rio Tinto shareholders, and value enhancing for BHP Billiton shareholders Overview of the offer for Rio Tinto |

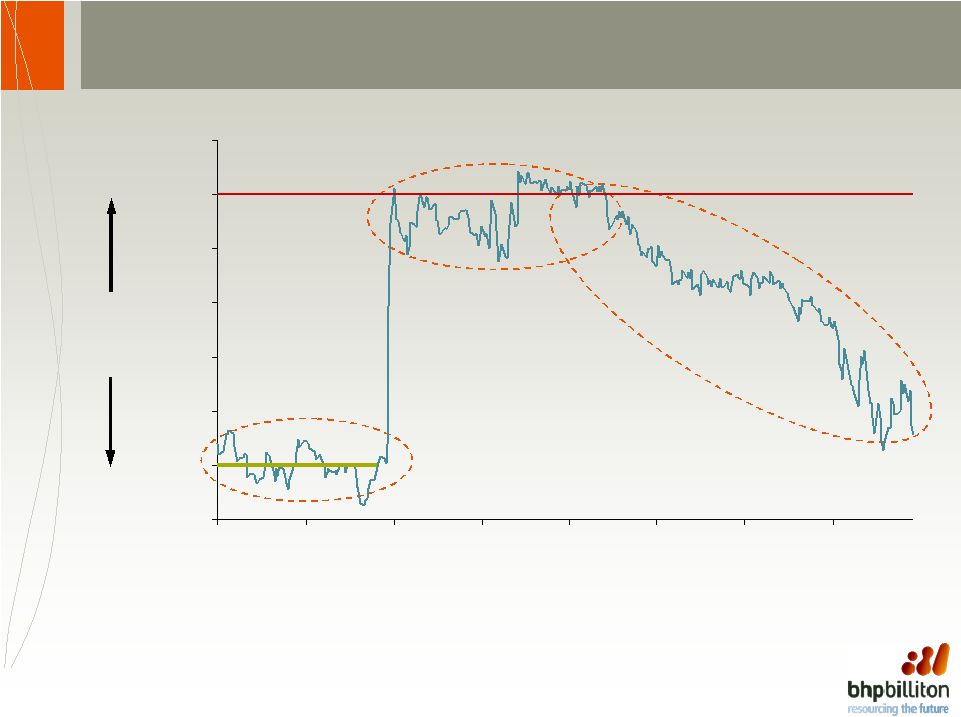

Slide 17 3.4 continues to be compelling value 45% premium (a) Ongoing regulatory clearance process Prior to BHP Billiton’s approach 1. 2. Initial period following announcement of proposal/offer 3. Historical share exchange ratio (b) 2.2 : 1 2.4 : 1 2.6 : 1 2.8 : 1 3.0 : 1 3.2 : 1 3.4 : 1 3.6 : 1 Jul-2007 Sep-2007 Nov-2007 Jan-2008 Mar-2008 May-2008 Jul-2008 Sep-2008 BHP Billiton's offer for Rio Tinto Source: Datastream (as at 5-Nov-2008). a) Premium based on the combined volume-weighted market capitalisation of Rio Tinto based on the volume-weighted average closing share prices over the month ended 31-Oct-2007 of £43.09 and A$109.20 for Rio Tinto plc and Rio Tinto Ltd respectively and volume-weighted average closing share prices over the month ended 31-Oct-2007 of BHP Billiton Plc an BHP Billiton Ltd of £17.99 and A$45.77 respectively. Based on BHP Billiton and Rio Tinto issued ordinary shares outstanding (excluding Treasury shares and cross shareholdings eg. Rio Tinto plc’s shareholding in Rio Tinto Ltd) as at 9-Nov-2007 and exchange rates of 2.077 US$/£ and 0.927 US$/A$ as at 31-Oct-2007. NOTE: Consistent with the UK City Code on Takeovers and Mergers, the offer represents a 29% discount based on the combined market capitalisation of Rio Tinto based on the closing share prices of Rio Tinto plc of £43.50 on 7-Nov-2007 and Rio Tinto Ltd of A$113.40 on 8-Nov-2007 and closing share prices of BHP Billiton Plc and BHP Billiton Ltd of £11.40 and A$31.60 respectively on 5-Nov-2008. Based on BHP Billiton and Rio Tinto issued ordinary shares outstanding (excluding Treasury shares and cross shareholdings eg. Rio Tinto plc’s shareholding in Rio Tinto Ltd) as at 5-Nov-2008 and exchange rates of 1.615 US$/£ and 0.701 US$/A$ as at 5-Nov-2008. b) Exchange ratio assumes 100% BHP Billiton Ltd shares for each Rio Tinto Ltd share and BHP Billiton shares for each Rio Tinto plc share consisting of 80% BHP Billiton Plc shares and 20% BHP Billiton Ltd shares. |

Slide 18 Shareholder questions – and a few answers • If satisfactory regulatory clearance is not achieved and/or the offer fails, what will happen to Rio Tinto’s relative share price? • What happens if regulatory clearance is achieved and Rio Tinto shareholders accept the offer? – Capture the 45% premium (a) – Exchange your Rio Tinto shares for a share in a stronger combined company: – With an unrivalled portfolio of long life, low cost assets – That unlocks substantial synergies not available to Rio Tinto any other way – That is more diversified, lower risk, has greater financial strength and is positioned to deliver superior returns, including higher dividends, through the cycle – That is better positioned to capture renewed growth in demand • And what is in it for BHP Billiton shareholders? – Earnings per share and cashflow per share accretive in the first full fiscal year following completion (b) – Become shareholders in the same stronger combined company which will unlock the substantial synergies that are also not available to BHP Billiton on its own Notes: a) Premium based on the combined volume-weighted market capitalisation of Rio Tinto based on the volume-weighted average closing share prices over the month ended 31-Oct-2007 of £43.09 and A$109.20 for Rio Tinto plc and Rio Tinto Ltd respectively and volume-weighted average closing share prices over the month ended 31-Oct-2007 of BHP Billiton Plc and BHP Billiton Ltd of £17.99 and A$45.77 respectively. Based on BHP Billiton and Rio Tinto issued ordinary shares outstanding (excluding Treasury shares and cross shareholdings eg. Rio Tinto plc’s shareholding in Rio Tinto Ltd) as at 9-Nov-2007 and exchange rates of 2.077 US$/£ and 0.927 US$/A$ as at 31-Oct-2007. NOTE: Consistent with the UK City Code on Takeovers and Mergers, the offer represents a 29% discount based on the combined market capitalisation of Rio Tinto based on the closing share prices of Rio Tinto plc of £43.50 on 7-Nov-2007 and Rio Tinto Ltd of A$113.40 on 8-Nov-2007 and closing share prices of BHP Billiton Plc and BHP Billiton Ltd of £11.40 and A$31.60 respectively on 5-Nov-2008. Based on BHP Billiton and Rio Tinto issued ordinary shares outstanding (excluding Treasury shares and cross shareholdings eg. Rio Tinto plc’s shareholding in Rio Tinto Ltd) as at 5-Nov-2008 and exchange rates of 1.615 US$/£ and 0.701 US$/A$ as at 5-Nov-2008. b) Earnings per share accretive after adjusting for the proposed share buyback and excluding depreciation on the write-up of Rio Tinto’s assets. Cash flow per share accretive after adjusting for the proposed share buyback. |

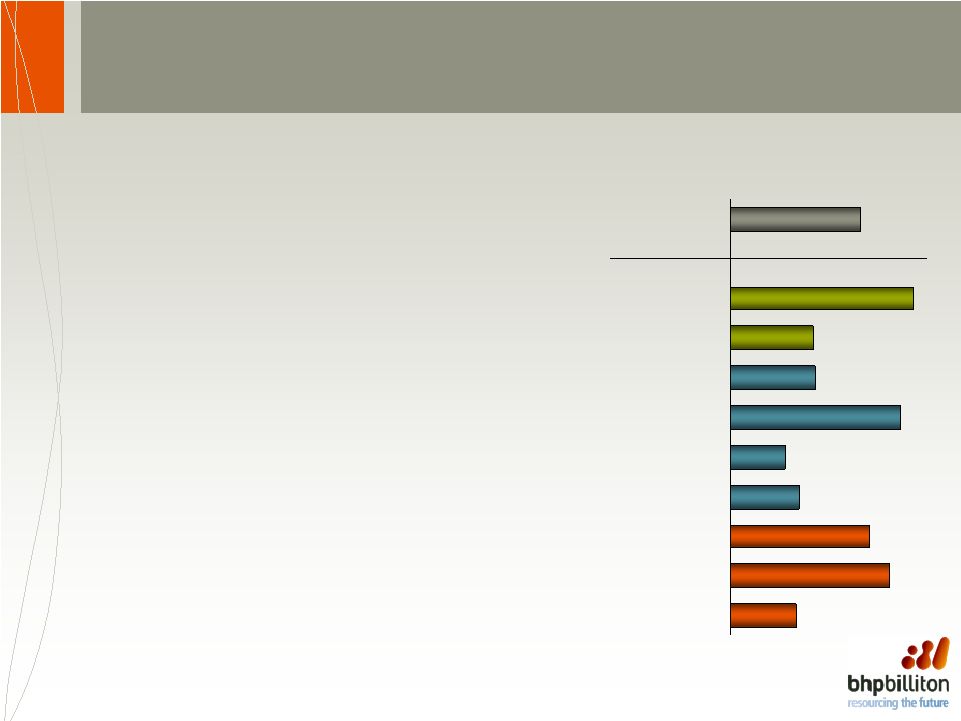

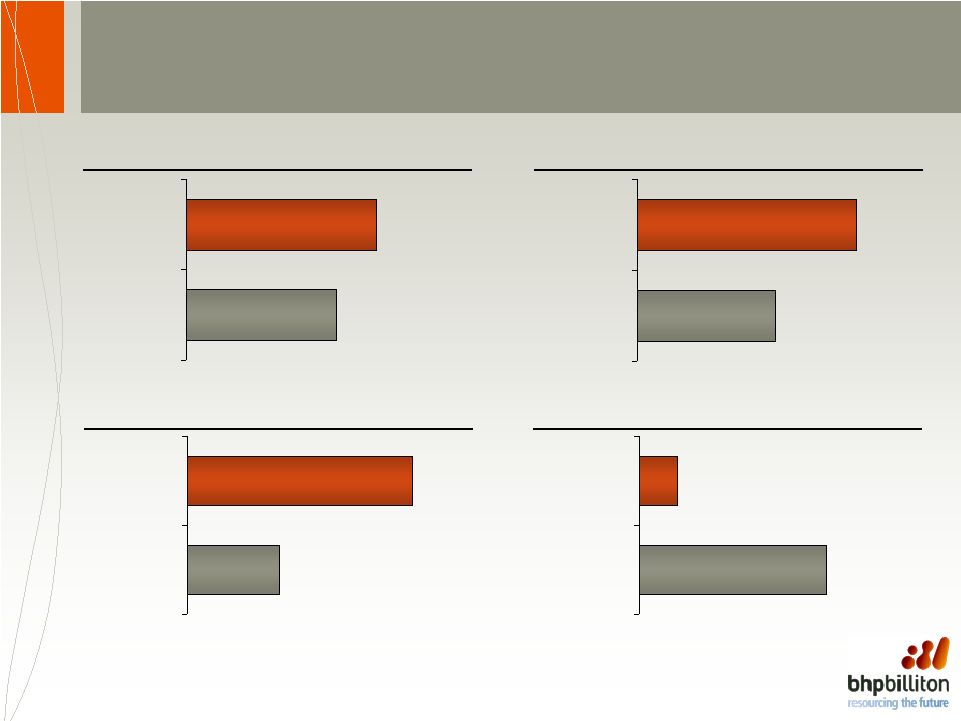

Slide 19 Comparative dividend per share FY2008 dividends per A$1,000 of shares (a) Net debt (c) Notes: a) Calculated based on Rio Tinto Ltd and BHP Billiton Ltd share prices as at 5-Nov-2008 and using the dividend for the respective periods as paid in A$ by BHP Billiton and Rio Tinto. b) Dividends per share on a US$ basis. Rio Tinto’s ordinary dividends per share restated to June year end. c) As at 30-Jun-2008. FY2007 to FY2008 DPS growth (b) FY2008 vs FY2002 DPS (b) 31% 49% Rio Tinto BHP Billiton Rio Tinto BHP Billiton A$24.95 (2.50% yield) A$19.67 (1.97% yield) 2.2 x 5.4 x Rio Tinto BHP Billiton Rio Tinto BHP Billiton US$8.5bn US$42.1bn |

Slide 20 Combination is about reducing risk, not increasing it • Increased size does not mean increased complexity – simplicity of the business model remains key • We believe operating as one company results in: – More diversified and higher quality asset portfolio, lower risk – An enhanced portfolio of growth opportunities – Greater ability to develop the next generation of large scale projects in new geographies – Operating and capital cost efficiencies – Quantifiable synergies of US$3.7bn per annum (a) – Other combination benefits • Key management positions will be filled by drawing on the best of both management teams • High share price correlation means similar portfolio concentration, whether the companies are combined or separate Notes: (a) Estimated incremental EBITDA (nominal) based on publicly available information. To be read in conjunction with the notes in Appendix IV of BHP Billiton’s announcement dated 6-Feb-2008. Full run rate synergies expected in the seventh full year following completion. |

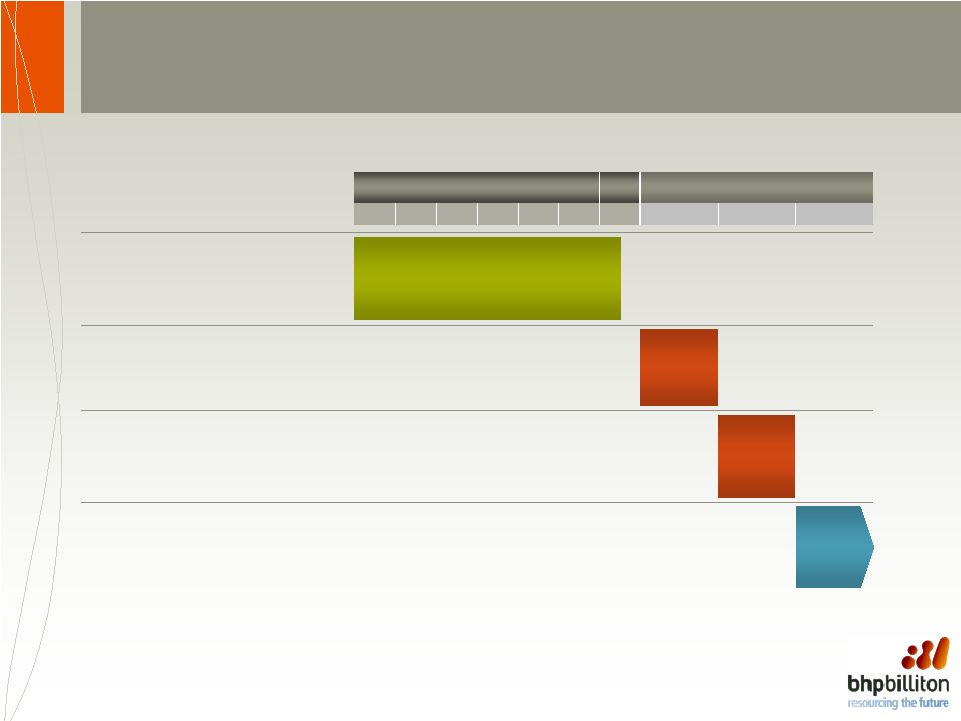

Slide 21 Indicative timetable for the offer Jan 2009 2008 Offer Period Event Jul Aug Sep Oct Nov Dec Day 0 (a) Day 60 Post Day 60 Regulatory Approvals Satisfaction of regulatory approval pre-conditions Offer Documentation Posting of offer documents for Rio Tinto plc offer and Rio Tinto Ltd offer to shareholders Offer Fulfilment Last date for fulfilment of greater than 50% minimum acceptance condition in both the Rio Tinto plc and Rio Tinto Ltd offers Post Day 60 Notes: a) Date for Day 0 may fall in 2008 or 2009. Timetable is indicative only. (within 28 days of the pre conditions being satisfied) If minimum acceptance conditions are met – offer continues. (i.e. in order to receive sufficient acceptances to enable compulsory acquisition) |

Slide 22 Summary • We expect financial market volatility and economic uncertainty to continue in the short-term • However, China, India and other developing economies are expected to continue to drive demand for commodities in the long-term • Our uniquely diversified portfolio of low cost and high quality assets places us at a competitive advantage in the current uncertain environment • Our strong cash flow and balance sheet allows us to re-invest throughout the cycle • Strong future production growth expected to be delivered from lower risk projects and high margin products • BHP Billiton is working towards completing the regulatory review process for the Rio Tinto offer by early 2009 • BHP Billiton believes this offer is compelling for Rio Tinto shareholders, and value enhancing for BHP Billiton shareholders Cannington |

Slide 23 Questions and Answers |

Slide 24 BHP Billitons’ senior management team Chairman and Chief Executive Officer Group Management Committee Don Argus Chairman • Chairman of BHP Billiton Group since June 2001 • Chairman of BHP Limited since April 1999 Marius Kloppers Chief Executive Officer • 15 years resources experience • 15 years at BHP Billiton Marcus Randolph Chief Executive Ferrous and Coal • 31 years resources experience • 9 years at BHP Billiton • Previously worked at Rio Tinto Alex Vanselow Chief Financial Officer • 19 years resources experience • 19 years at BHP Billiton Karen Wood Chief People Officer • 7 years resources experience • 7 years at BHP Billiton Michael Yeager Chief Executive Petroleum • 27 years resources experience • 2 years at BHP Billiton Alberto Calderon Chief Commercial Officer • 9 years resources experience • 2 years at BHP Billiton |

Slide 25 More information for shareholders Internet More information on BHP Billiton or BHP Billiton’s offer for Rio Tinto can be found at either of the following web pages: BHP Billiton: www.bhpbilliton.com BHP Billiton’s offer for Rio Tinto: www.bhpbilliton.com\RioTintoOffer Or Email: investor.relations@bhpbilliton.com BHP Billiton Shareholder Information Helpline If you have any additional questions you can contact the Shareholder Information Helpline on the following numbers: Australia toll free: 1300 766 363 New Zealand toll free: 0800 668 228 For other callers: +61 3 9415 4365 BHP Billiton Shareholder Services - Computershare For information about your shareholding contact: Within Australia: 1300 656 780 Outside Australia: +61 3 9415 4020 Fax: +61 3 9473 2460 |

|