Table of Contents

☐ | REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR 12(g) OF THE SECURITIES EXCHANGE ACT OF 1934 |

☒ | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

☐ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

☐ | SHELL COMPANY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

Commission File No.: 001-09526 |

BHP GROUP LIMITED |

(ABN 49 004 028 077) |

(Exact name of Registrant as specified in its charter) |

N/A |

(Translation of Registrant’s name into English) |

VICTORIA, AUSTRALIA |

(Jurisdiction of incorporation or organization) |

171 COLLINS STREET MELBOURNE, VICTORIA 3000 AUSTRALIA (Address of principal executive offices) |

STEFANIE WILKINSON BHP GROUP LIMITED 171 COLLINS STREET MELBOURNE VIC 3000 AUSTRALIA TELEPHONE AUSTRALIA 1300 55 47 57 TELEPHONE INTERNATIONAL +61 3 9609 3333 FACSIMILE +61 3 9609 3015 (Name, telephone, e-mail and/or facsimile number and address of company contact person) |

Title of each class | Trading symbol | Name of each exchange on which registered | ||

American Depositary Shares* | BHP | New York Stock Exchange | ||

Ordinary Shares** | BHP | New York Stock Exchange | ||

| * | Evidenced by American Depositary Receipts. Each American Depositary Receipt represents two ordinary shares of BHP Group Limited. |

| ** | Not for trading, but only in connection with the listing of the American Depositary Shares. |

BHP Group Limited | ||

Ordinary Shares | 5,071,530,817 |

| Large accelerated filer | ☒ | Accelerated filer | ☐ | |||

| Non-accelerated filer | ☐ | Emerging growth company | ☐ | |||

U.S. GAAP ☐ | International Financial Reporting Standards as issued by the International Accounting Standards Board ☒ | Other ☐ |

Table of Contents

Company details

BHP Group Limited’s registered office and global headquarters are at 171 Collins Street, Melbourne, Victoria 3000, Australia.

‘BHP’, the ‘Company’, the ‘Group’, ‘BHP Group’, ‘our business’, ‘organisation’, ‘we’, ‘us’, ‘our’ and ‘ourselves’ refer to BHP Group Limited, and except where the context otherwise requires, our subsidiaries.

Refer to Financial Statements note 30 ‘Subsidiaries’ for a list of our significant subsidiaries and to Exhibit 8.1 – List of Subsidiaries for a list of our subsidiaries. Those terms do not include non-operated assets.

This Report covers functions and assets (including those under exploration, projects in development or execution phases, sites and operations that are closed or in the closure phase) that have been wholly owned and operated by BHP or that have been owned as a joint venture(1) operated by BHP (referred to in this Report as ‘operated assets’ or ‘operations’) from 1 July 2023 to 30 June 2024, unless otherwise stated. Certain sections of this Report include data in relation to the Daunia and Blackwater mines, which were divested during the year. Data in relation to the Daunia and Blackwater mines is shown for the period up to completion on 2 April 2024, unless stated otherwise. Some of the land and tenements related to the Daunia and Blackwater mines are pending transfer following completion, however given that the assets are no longer under BMA’s control or operated for BMA’s benefit (except for periods prior to completion or where specifically stated) data related to the land and tenements has been excluded from this Report.

BHP also holds interests in assets that are owned as a joint venture but not operated by BHP (referred to in this Report as ‘non-operated joint ventures’ or ‘non-operated assets’). Notwithstanding that this Report may include production, financial and other information from non-operated assets, non-operated assets are not included in the BHP Group and, as a result, statements regarding our operations, assets and values apply only to our operated assets unless stated otherwise.

BHP Group Limited has a primary listing on the Australian Securities Exchange. BHP holds an international secondary listing on the London Stock Exchange, a secondary listing on the Johannesburg Stock Exchange and an ADR program listed on the New York Stock Exchange.

Introduction

This document is our annual report on Form 20-F for the year ended 30 June 2024 (this “Annual Report”). Reference is made to our Australian Annual Report for the year ended 30 June 2024, which has been furnished to the U.S. Securities and Exchange Commission (the “SEC”) on a Report on Form 6-K on 27 August 2024, which includes information that has been omitted from this Form 20-F. Only information that is included in, or expressly incorporated by reference into, this Form 20-F shall be deemed to form a part of this Annual Report.

The SEC maintains an Internet website that contains reports and other information regarding issuers that file electronically with the SEC. Our filings with the SEC are available to the public through the SEC’s website at http://www.sec.gov.

Materiality, as used in the context of climate and sustainability-related disclosures, may differ from the materiality standards applied by other reporting regimes, including as defined for SEC reporting purposes. Any issues identified as material for purposes of sustainability in this document are therefore not necessarily material for SEC reporting purposes.

All references to websites in this Annual Report are intended to be inactive textual references for information only and any information contained in or accessible through any such website does not form a part of this Annual Report.

Forward-looking statements

This Report contains forward-looking statements, which involve risks and uncertainties. Forward-looking statements include all statements, other than statements of historical or present facts, including: statements regarding trends in commodity prices and currency exchange rates; demand for commodities; global market conditions, reserves and resources estimates; development and production forecasts; guidance; expectations, plans, strategies and objectives of management; climate scenarios; approval of projects and consummation of transactions; closure, divestment, acquisition or integration of certain assets, operations or facilities (including associated costs or benefits); anticipated production or construction commencement dates; capital costs and scheduling; operating costs and availability of materials and skilled employees; anticipated productive lives of projects, mines and facilities; the availability, implementation and adoption of new technologies, including artificial intelligence; provisions and contingent liabilities; and tax, legal and other regulatory developments.

Forward-looking statements may be identified by the use of terminology, including, but not limited to, ‘aim’, ‘ambition’, ‘anticipate’, ‘aspiration’, ‘believe’, ‘commit’, ‘continue’, ‘could’, ‘ensure’, ‘estimate’, ‘expect’, ‘forecast’, ‘goal’, ‘guidance’, ‘intend’, ‘likely’, ‘may’, ‘milestone’, ‘must’, ‘need’, ‘objective’, ‘outlook’, ‘pathways’, ‘plan’, ‘project’, ‘schedule’, ‘seek’, ‘should’, ‘target’, ‘trend’, ‘will’, ‘would’, or similar words. These statements discuss future expectations or performance, or provide other forward-looking information.

| (1) | References in this Annual Report to a ‘joint venture’ are used for convenience to collectively describe assets that are not wholly owned by BHP. Such references are not intended to characterise the legal relationship between the owners of the asset. |

i

Table of Contents

Examples of forward-looking statements contained in this Report include, without limitation, statements describing (i) our strategy, our values and how we define our success; (ii) our expectations regarding future demand for certain commodities, in particular copper, nickel, iron ore, steelmaking coal, potash and steel, and our intentions, commitments or expectations with respect to our supply of certain commodities, including copper, nickel, iron ore, potash, uranium and gold; (iii) our future exploration and partnership plans and perceived benefits and opportunities, including our focus to grow our copper and potash assets; (iv) our business outlook, including our outlook for long-term economic growth and other macroeconomic and industry trends; (vi) our projected and expected production and performance levels and development projects; (vii) our expectations regarding our investments, including in potential growth options and technology and innovation, and perceived benefits and opportunities; (viii) our reserves and resources estimates; (ix) our plans for our major projects and related budget and capital allocations; (x) our expectations, commitments and objectives with respect to sustainability, decarbonisation, natural resource management, climate change and portfolio resilience and timelines and plans to seek to achieve or implement such objectives, including our approach to equitable change and transitions, our Climate Transition Action Plan, climate change adaptation strategy and goals, targets, pathways and strategies to seek to reduce or support the reduction of greenhouse gas emissions, and related perceived costs, benefits and opportunities for BHP; (xi) the assumptions, beliefs and conclusions in our climate change related statements and strategies, including in our Climate Change Report 2020, for example, in respect of future temperatures, energy consumption and greenhouse gas emissions, and climate-related impacts; (xii) our commitment to social value; (xiii) our commitments to sustainability reporting, frameworks, standards and initiatives; (xiv) our commitments to improve or maintain safe tailings storage management; (xv) our commitments to achieve certain inclusion and diversity targets, aspirations and outcomes; (xvi) our commitments to achieve certain targets and outcomes with respect to Indigenous peoples and the communities where we operate; and (xvii) our commitments to achieve certain health and safety targets and outcomes.

Forward-looking statements are based on management’s expectations and reflect judgements, assumptions, estimates and other information available, as at the date of this Report. These statements do not represent guarantees or predictions of future financial or operational performance and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control and which may cause actual results to differ materially from those expressed in the statements contained in this Report. BHP cautions against reliance on any forward-looking statements.

For example, our future revenues from our assets, projects or mines described in this Report will be based, in part, on the market price of the commodities produced, which may vary significantly from current levels or those reflected in our reserves and resources estimates. These variations, if materially adverse, may affect the timing or the feasibility of the development of a particular project, the expansion of certain facilities or mines, or the continuation of existing assets.

Other factors that may affect our future operations and performance, including the actual construction or production commencement dates, revenues, costs or production output and anticipated lives of assets, mines or facilities include: (i) our ability to profitably produce and deliver the products extracted to applicable markets; (ii) the impact of economic and geopolitical factors, including foreign currency exchange rates on the market prices of the commodities we produce and competition in the markets in which we operate; (iii) activities of government authorities in the countries where we sell our products and in the countries where we are exploring or developing projects, facilities or mines, including increases in taxes and royalties or implementation of trade or export restrictions; (iv) changes in environmental and other regulations; (v) political or geopolitical uncertainty; (vi) labour unrest; (vii) weather, climate variability or other manifestations of climate change; and (viii) other factors identified in the risk factors set out in OFR 8.1.

In addition, there are limitations with respect to scenario analysis, including any climate-related scenario analysis, and it is difficult to predict which, if any, of the scenarios might eventuate. Scenario analysis is not an indication of probable outcomes and relies on assumptions that may or may not prove to be correct or eventuate.

Except as required by applicable regulations or by law, BHP does not undertake to publicly update or review any forward-looking statements, whether as a result of new information or future events.

Past performance cannot be relied on as a guide to future performance.

Emissions and energy consumption data

Due to the inherent uncertainty and limitations in measuring GHG emissions and operational energy consumption under the calculation methodologies used in the preparation of such data, all GHG emissions and operational energy consumption data or references to GHG emissions and operational energy consumption volumes (including ratios or percentages) in this Report are estimates. There may also be differences in the manner that third parties calculate or report GHG emissions or operational energy consumption data compared to BHP, which means third-party data may not be comparable to our data. For information on how we calculate our GHG emissions and operational energy consumption, refer to the BHP GHG Emissions Calculation Methodology 2024, available at bhp.com/climate

ii

Table of Contents

Form 20-F Cross Reference Table

Item Number | Description | Report section reference | ||||

1. | Identity of Directors, Senior Management and Advisors | Not applicable | ||||

2. | Offer Statistics and Expected Timetable | Not applicable | ||||

3. | Key Information | |||||

| A | [Reserved] | Not applicable | ||||

| B | Capitalization and indebtedness | Not applicable | ||||

| C | Reasons for the offer and use of proceeds | Not applicable | ||||

| D | Risk factors | 8.1 | ||||

4. | Information on the Company | |||||

| A | History and development of the company | Cover page, Company details, Chair’s review, Chief Executive Officer’s review, Operating and Financial Review 1 to 9, Additional information 1, 2, 4 to 9.4 | ||||

| B | Business overview | Operating and Financial Review 1 to 5, 9, Additional information 1, 4 to 8, 9.3, 9.9 and Note 1 to the Financial Statements | ||||

| C | Organizational structure | Additional information 9.3 and Note 30 to the Financial Statements | ||||

| D | Property, plants and equipment | Operating and Financial Review 3, 5.1, 5.2, 5.3, 6 to 9, Additional information 1, 4 to 6 and Notes 11, 15 and 22 to the Financial Statements | ||||

4A. | Unresolved Staff Comments | None | ||||

5. | Operating and Financial Review and Prospects | |||||

| A | Operating results | Operating and Financial Review 4, 5, 9, Additional information 2 to 4 | ||||

| B | Liquidity and capital resources | Operating and Financial Review 4, Financial Statements 1.4, Notes 11 and 21 to 24 to the Financial Statements | ||||

| C | Research and development, patents and licenses, etc. | Operating and Financial Review 3, 5, 8 and 9, Directors’ Report 10, Additional information 1, 5, 6 and Notes 11 and 15 to the Financial Statements | ||||

| D | Trend information | Chair’s review, Chief Executive Officer’s review, Operating and Financial Review 1 to 6, 8, 9, Additional information 1 to 7 | ||||

| E | Critical Accounting Estimates | IFRS is applied in the Financial Statements as issued by the IASB | ||||

6. | Directors, Senior Management and Employees | |||||

| A | Directors and senior management | Corporate Governance Statement 4.1, 6.1, Directors’ Report 2 | ||||

| B | Compensation | Remuneration Report | ||||

| C | Board practices | Corporate Governance Statement 4.1, 4.7, 5.2, 5.4, Remuneration Report | ||||

| D | Employees | Operating and Financial Review 6.6, Additional information 7 | ||||

| E | Share ownership | Remuneration Report, Directors’ Report 3, 4 and Notes 17, 18, 25 and 26 to the Financial Statements | ||||

| F | Erroneously Awarded Compensation | Not applicable | ||||

7. | Major Shareholders and Related Party Transactions | |||||

| A | Major shareholders | Additional information 9.5 | ||||

| B | Related party transactions | Remuneration Report and Notes 25 and 33 to the Financial Statements | ||||

| C | Interests of experts and counsel | Not applicable | ||||

8. | Financial Information | |||||

iii

Table of Contents

| A | Consolidated Statements and Other Financial Information | Operating and Financial Review 7, Additional information 8, 9.6, Financial Statements beginning on page F-1 in this Annual Report and Financial Statements 1A | ||||

| B | Significant Changes | Note 35 to the Financial Statements | ||||

9. | The Offer and Listing | |||||

| A | Offer and listing details | Additional information 9.2 | ||||

| B | Plan of distribution | Not applicable | ||||

| C | Markets | Additional information 9.2 | ||||

| D | Selling shareholders | Not applicable | ||||

| E | Dilution | Not applicable | ||||

| F | Expenses of the issue | Not applicable | ||||

10. | Additional Information | |||||

| A | Share capital | Not applicable | ||||

| B | Memorandum and articles of association | Additional information 9.3, 9.4 | ||||

| C | Material contracts | Additional Information 8 (regarding the Framework Agreement) | ||||

| D | Exchange controls | Additional information 9.9 | ||||

| E | Taxation | Additional information 9.10 | ||||

| F | Dividends and paying agents | Not applicable | ||||

| G | Statement by experts | Not applicable | ||||

| H | Documents on display | Additional information 9.4 | ||||

| I | Subsidiary information | Note 30 to the Financial Statements and Exhibit 8.1 | ||||

| J | Annual Report to Security Holders | Not applicable | ||||

11. | Quantitative and Qualitative Disclosures About Market Risk | Note 24 to the Financial Statements | ||||

12. | Description of Securities Other than Equity Securities | |||||

| A | Debt Securities | Not applicable | ||||

| B | Warrants and Rights | Not applicable | ||||

| C | Other Securities | Not applicable | ||||

| D | American Depositary Shares | Additional information 9.7 and Exhibit 2.1 | ||||

13. | Defaults, Dividend Arrearages and Delinquencies | Not applicable | ||||

14. | Material Modifications to the Rights of Security Holders and Use of Proceeds | Not applicable | ||||

15. | Controls and Procedures | Corporate Governance Statement 9.2 and Financial Statements 1A | ||||

16A. | Audit committee financial expert | Corporate Governance Statement 5.2 | ||||

16B. | Code of Ethics | Corporate Governance Statement 8 | ||||

16C. | Principal Accountant Fees and Services | Corporate Governance Statement 9.2 and Note 36 to the Financial Statements | ||||

16D. | Exemptions from the Listing Standards for Audit Committees | Not applicable | ||||

16E. | Purchases of Equity Securities by the Issuer and Affiliated Purchasers | Directors’ Report 4 | ||||

16F. | Change in Registrant’s Certifying Accountant | Not applicable | ||||

16G. | Corporate Governance | Corporate Governance Statement | ||||

16H. | Mine Safety Disclosure | Not applicable | ||||

16I. | Disclosure Regarding Foreign Jurisdictions that Prevent Inspections | Not applicable | ||||

16J. | Insider Trading Policies | Exhibit 11.1 | ||||

16K. | Cybersecurity | Operating and Financial Review 8.1, Additional information 9.8 | ||||

17. | Financial Statements | Not applicable | ||||

18. | Financial Statements | Financial Statements begin on page F-1 in this Annual Report | ||||

19. | Exhibits | Exhibits |

iv

Table of Contents

Bringing people and resources together to build a better world.

“A resource mix for today. Critical for the future. Our project pipeline and focus on continuous improvement in existing operations leave us well poised for growth across our four commodity pillars of copper, potash, iron ore and steelmaking coal in the decades ahead.”

Mike Henry

Chief Executive Officer

v

Table of Contents

Contents

| 1 | ||||||

| 3 | ||||||

Operating and Financial Review | ||||||

| 1 | Why BHP | 5 | ||||

| 1.1 | Where we operate | 7 | ||||

| 1.2 | Our portfolio | 8 | ||||

| 2 | What differentiates us | 10 | ||||

| 3 | Positioning for growth | 15 | ||||

| 4 | Financial review | 18 | ||||

| 4.1 | 18 | |||||

| 4.2 | Key performance indicators | 18 | ||||

| 4.3 | Financial results | 20 | ||||

| 4.4 | Debt and sources of liquidity | 22 | ||||

| 5 | Our assets | 25 | ||||

| 5.1 | Minerals Australia | 25 | ||||

| 5.2 | Copper South Australia | 28 | ||||

| 5.3 | Minerals Americas | 29 | ||||

| 5.4 | Commercial | 32 | ||||

| 6 | Sustainability | 34 | ||||

| 6.1 | Safety | 34 | ||||

| 6.2 | Our sustainability approach | 37 | ||||

| 6.3 | Sustainability governance | 37 | ||||

| 6.4 | Material sustainability topics for reporting | 38 | ||||

| 6.5 | 2030 goals | 40 | ||||

| 6.6 | People | 43 | ||||

| 6.7 | Health | 50 | ||||

| 6.8 | Ethics and business conduct | 53 | ||||

| 6.9 | Climate change | 55 | ||||

| 6.10 | Environment and nature | 70 | ||||

| 6.11 | Community | 77 | ||||

| 6.12 | Indigenous peoples | 79 | ||||

| 6.13 | Independent limited assurance report | 83 | ||||

| 7 | Samarco | 84 | ||||

| 8 | How we manage risk | 85 | ||||

| 8.1 | Risk factors | 87 | ||||

| 8.2 | Management of risks | 92 | ||||

| 9 | Performance by commodity | 99 | ||||

vi

Table of Contents

vii

Table of Contents

| 147 | ||||||

People and Remuneration Committee Chair letter to shareholders | 148 | |||||

| 1 | Remuneration governance | 151 | ||||

| 2 | Executive KMP remuneration framework | 152 | ||||

| 3 | Remuneration for the CEO and other Executive KMP | 155 | ||||

| 4 | Remuneration for Non-executive Directors | 162 | ||||

| 5 | Statutory KMP remuneration and other disclosures | 164 | ||||

| 171 | ||||||

Additional information | ||||||

| 1 | Information on mining operations | 172 | ||||

| 2 | Financial information summary | 195 | ||||

| 3 | Financial information by commodity | 196 | ||||

| 4 | Production | 198 | ||||

| 5 | Major projects | 201 | ||||

| 6 | Mineral resources and mineral reserves | 202 | ||||

| 7 | People - performance data | 225 | ||||

| 8 | Legal proceedings | 227 | ||||

| 9 | Shareholder information | 231 | ||||

| 9.1 | History and development | 231 | ||||

| 9.2 | Markets | 231 | ||||

| 9.3 | Organisational structure | 232 | ||||

| 9.4 | Constitution | 232 | ||||

| 9.5 | Share ownership | 235 | ||||

| 9.6 | Dividends | 238 | ||||

| 9.7 | American Depositary Receipts fees and charges | 238 | ||||

| 9.8 | Supplemental cybersecurity disclosures for US reporting | 239 | ||||

| 9.9 | Government regulations | 240 | ||||

| 9.10 | Taxation | 243 | ||||

| 10 | Glossary | 247 | ||||

| 263 | ||||||

viii

Table of Contents

ix

Table of Contents

x

Table of Contents

Chair’s review

Dear Shareholders,

I am pleased to provide BHP’s Annual Report for FY2024.

Our operational and financial performance was strong in FY2024, and we made solid progress against our social value and sustainability commitments. It is more than four years since we began the strategic transformation of BHP’s portfolio towards future-facing commodities and the world has changed markedly in that time. Thank you for the trust you have given us through this period.

Today, BHP has a portfolio of world-class assets focused on products that are critical to the future. A portfolio positioned for growth, yet resilient and able to withstand volatility. A product mix that can continue to deliver financial and social value over the long term.

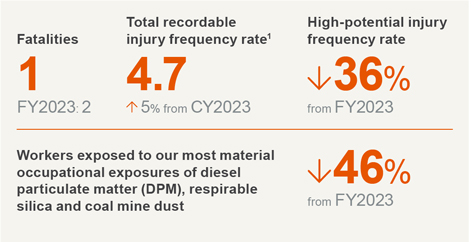

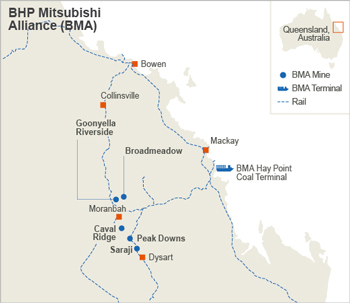

However, FY2024 was overshadowed by a fatality. We are deeply saddened that Luke O’Brien, a team member working with one of our contracting partners at BHP Mitsubishi Alliance (BMA), was fatally injured in January in a vehicle incident at the Saraji mine in Queensland. Our heartfelt thoughts and condolences go to Luke’s family and friends. Safety is our top priority and our commitment to zero fatalities and serious injuries at BHP is unwavering.

Our strategic priorities

During FY2024 I had the pleasure of meeting with our people, Indigenous partners, suppliers and other stakeholders at our global sites and offices. These discussions reinforced that our ongoing commitment to the priorities of safety, culture and capability, capital discipline, the continued development of our world-class portfolio and social value continue to be the right focus areas for BHP.

Safe, inclusive and productive workplaces

Our commitment to safety includes eliminating sexual harassment, racism and bullying in our workplaces. We are determined to eliminate these unequivocally unacceptable behaviours.

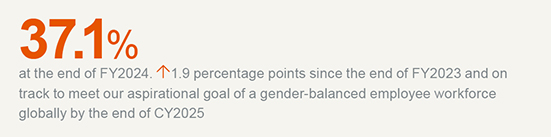

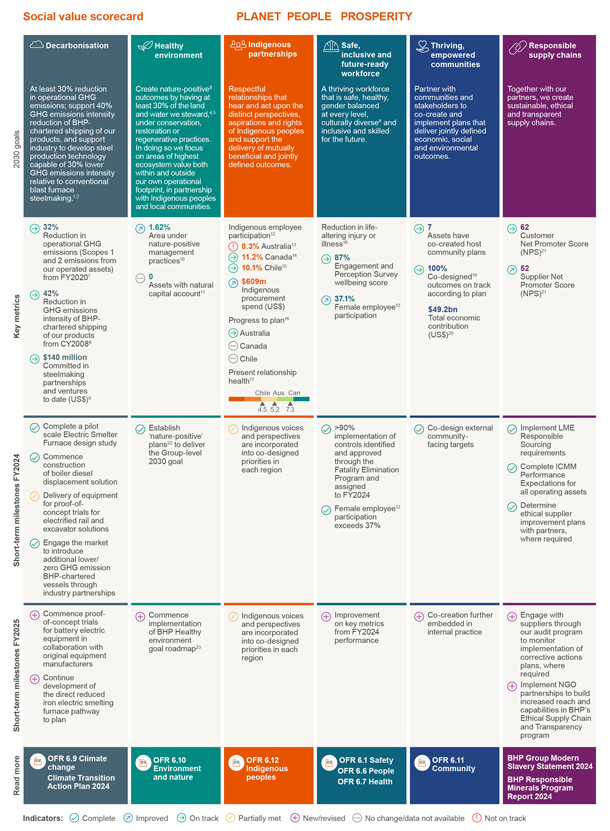

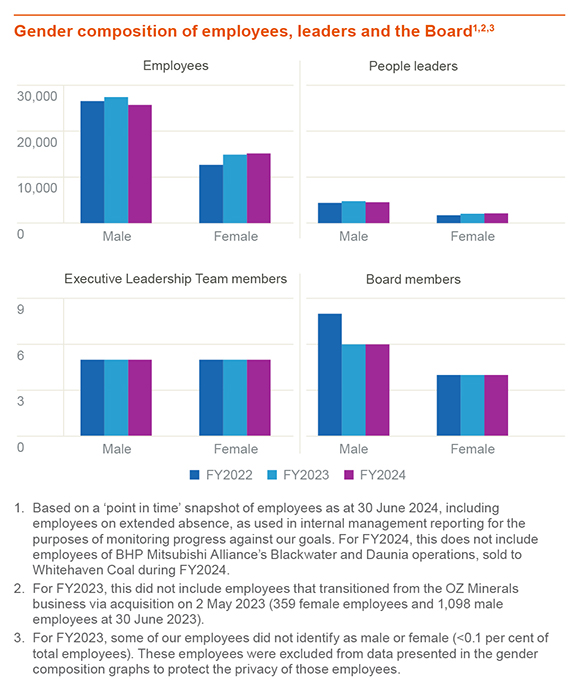

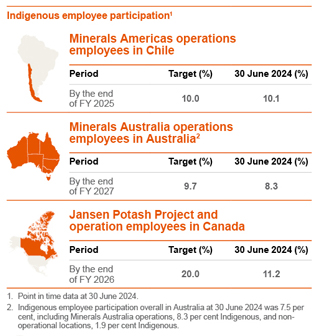

We know diverse and inclusive teams are safer and more productive. We achieved a 1.9 percentage point year-on-year increase in female employee participation in FY2024 to 37.1 per cent by year end. We also made progress towards our Indigenous employment targets, including Indigenous employee participation reaching 10.1 per cent in Chile and 11.2 per cent in Canada by year end. We have more work to do, but we are making progress on our commitment to provide a safe and inclusive workplace culture.

Positioned for success

BHP, and mining, have a clear and undeniable role to provide the metals and minerals the world needs for more sustainable development.

The global trends shaping our future are interconnected, unstoppable and bring with them new challenges and opportunities for our sector. A growing and increasingly urbanised population seeking a higher standard of living will require vast amounts of metals and minerals. That demand will only be amplified by the energy transition.

We are continuing to position our portfolio to align with these trends. Iron ore for steel to build cities and renewables infrastructure, steelmaking coal for the blast furnace process for making steel, copper for electrification, nickel for electric vehicle batteries and potash for food security and more sustainable land.

Delivering value

BHP’s strong operational performance and disciplined approach to capital allocation has seen the Board determine dividends totaling US$7.4 billion to shareholders for the year. This will take the total amount of cash dividends returned to you since 1 July 2021 to over US$42 billion including the FY2024 final dividend.

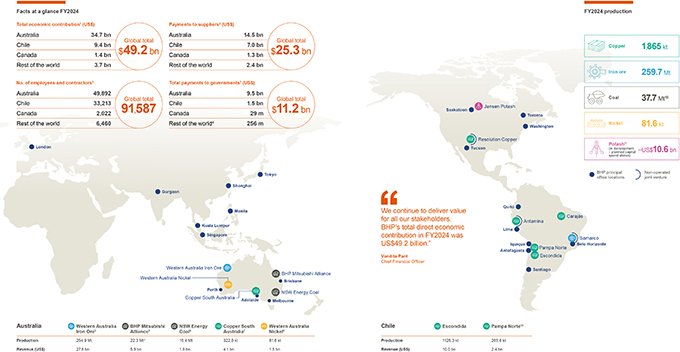

We continued to make significant contributions to the communities where we operate through employment, community partnerships, payments to local suppliers, and taxes and royalties paid to governments. Our total global economic contribution was US$49.2 billion in FY2024.

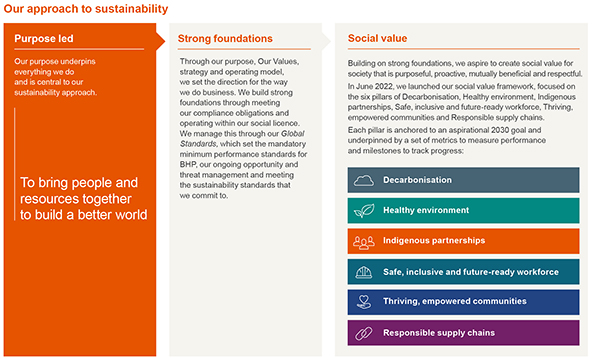

Creating social value is vital to our business and goes hand in hand with long-term sustainable shareholder value. In FY2024, we delivered tangible progress in each of the six pillars of our social framework which are focused on decarbonisation, the environment, Indigenous partnerships, workforce, communities, and supply chains. Social value is interwoven into our strategic decision-making through our social value framework, which helps us to meet the world’s demand for resources more sustainably, with more renewable energy, less fresh water use and less disruption.

Our social value highlights in FY2024 included the completion of all our FY2024 Australian Reconciliation Action Plan targets and reforms, US$137 million in voluntary social investment including community and environmental initiatives and continued progress towards reducing our operational greenhouse gas emissions.

1

Table of Contents

Our Climate Transition Action Plan 2024 provides an update on our climate change strategy and our progress and plans in relation to our greenhouse gas emissions goals and targets. Our plan shows we are serious about addressing the impacts of climate change from our business while continuing to provide strong shareholder returns. At the Annual General Meeting this year there will be a ‘Say on climate’ vote and I recommend you vote in favour of our Climate Transition Action Plan 2024.

Board updates

Our structured Board renewal process continued in FY2024. Ross McEwan joined the Board as a Non-executive Director on 3 April 2024. Ross has significant experience in the financial services industry with deep expertise in capital allocation, risk management and value creation in complex regulatory environments. Don Lindsay also joined the Board as a Non-executive Director on 1 May 2024 and brings over 40 years of global experience in the resources sector and investment banking, including in mining and resource development, financial markets, growth and value creation. In April 2024, Ian Cockerill retired from the Board and in October 2023, Terry Bowen also retired from the Board. We benefited greatly from Ian’s and Terry’s extensive experience and I would like to thank them for their contribution and commitment to BHP during their time with us.

Outlook

In recent decades, we have seen global economies and supply chains come together and support sustained economic development. Today, we are seeing more turbulence, tension and polarisation in the geopolitical landscape. We expect economic conditions to remain challenging in FY2025 as geopolitical issues continue to create volatility and impact global markets, security and trade.

Despite these challenges, I am optimistic about our future.

We have a world-class portfolio of large, long-life and high-quality assets which stands to benefit from the global changes shaping our world. We have a clear focus on being the best operator in the resources sector, being disciplined in capital management through our Capital Allocation Framework and having a differentiated approach to creating social value. We have a culture that is committed to safety, productivity and continuous improvement and we are working to make our workforce more inclusive and diverse.

I am confident BHP is well positioned to continue to create sustainable long-term value for shareholders and for our partners and stakeholders in the year ahead.

Thank you for your continued support.

/s/ Ken MacKenzie

Ken MacKenzie

Chair

2

Table of Contents

Chief Executive Officer’s review

Dear Shareholders,

At BHP, we work to bring people and resources together to build a better world, and we continued to make solid progress on this in FY2024.

The tragic loss of a coworker at Saraji in January in a light vehicle incident underscored why safety must remain our first priority. Following an investigation, we have identified improvement areas for Saraji and BMA and work is underway to implement these. We must eliminate fatalities and serious injuries at our operations.

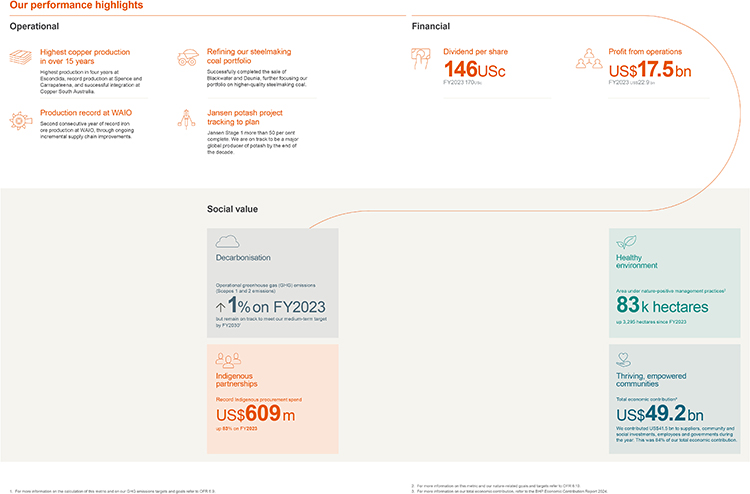

It was a year of strong overall business performance at BHP. By executing our strategy, we outperformed our competitors in key areas. We achieved an annual production record at Western Australia Iron Ore (WAIO), where we also widened our lead as the world’s lowest-cost iron ore producer. We delivered record production at copper assets Spence and Carrapateena, and the highest copper production in four years at Escondida – the world’s largest copper mine. We will distribute dividends totaling 146 US cents per share for the year.

Poised for growth

We continued to advance growth options in the commodities the world needs to meet the demands of the energy transition and population growth. We believe we have the balance sheet, technical and operational capability that will be needed to unlock new supply for the decades to come.

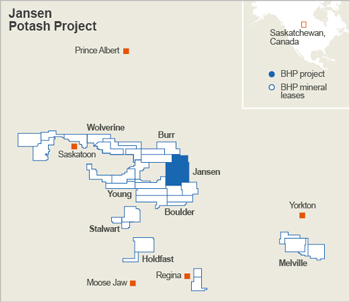

Construction of our Jansen potash project in Canada is ahead of the original schedule and first production is expected in just over two years. We have approved Jansen Stage 2, which will make BHP one of the leading players in the global potash industry by the end of the decade.

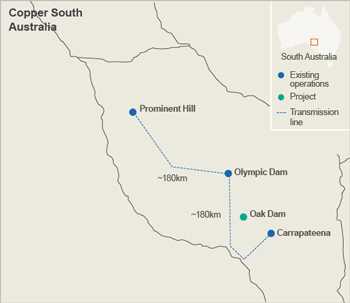

We have strengthened our position in copper. The integration of Prominent Hill and Carrapateena with Olympic Dam has delivered greater-than-expected synergies. We are exploring options to grow Copper South Australia’s production beyond 500 kilotonnes per annum (ktpa) of copper, with further potential up to 650 ktpa. In July 2024, we increased our early-stage copper options by agreeing to acquire a 50 per cent interest in the Filo del Sol and Josemaria projects with Lundin Mining in Argentina and Chile. If approved, this will give us the opportunity to advance one of the most significant copper discoveries globally in recent decades.

Our project pipeline and focus on continuous improvement in existing operations leave us well poised for growth across our four commodity pillars of copper, potash, iron ore and steelmaking coal in the decades ahead.

Winning strategy

Our actions in FY2024 are consistent with our winning strategy, founded on the three strategic pillars of safety and sustainability, exceptional performance and winning portfolio. In a cyclical industry, the stability of our operations and financial performance reflects the resilience and durability of our business.

The creation of social value is integral to our strategy and the delivery of long-term shareholder value. When we create social value, we build our case as the preferred partner for communities, we gain access to more opportunities, and we attract the best talent.

In the financial year, we increased Indigenous employment globally and boosted supplier spend with Indigenous businesses by 83 per cent to more than US$600 million. This was part of a broader 9 per cent increase to US$3.3 billion in supplier spend by BHP-operated businesses to more than 2,600 small, local and Indigenous businesses. This not only benefits our operations, but provides crucial support for jobs, businesses and families in regional communities surrounding them.

We made further progress on our operational decarbonisation plans and remain on track to meet our operational GHG emissions target of at least a 30 per cent reduction by FY2030 against an FY2020 baseline.

Refining our portfolio

We continue to focus on building a portfolio of world-class assets in attractive commodities in stable jurisdictions.

We refined our steelmaking coal portfolio in Queensland with the sale of the Daunia and Blackwater mines by our joint venture BMA. This strategic shift positions BMA well for the forecasted strong demand for higher-quality steelmaking coal. Following the transaction, around 90 per cent of our steelmaking coals are high-grade products attracting premium pricing.

In July 2024, we made the difficult but necessary decision to transition Western Australia Nickel into a period of temporary suspension. This reflected significant global oversupply of nickel, which we expect will continue until the end of the decade. We have offered redeployment to all frontline workers in other parts of BHP and will continue to support impacted host communities in a range of ways, including through our A$20 million Community Fund. We will continue to invest approximately US$300 million per annum in our Western Australia Nickel facilities to enable a potential re-start if the global nickel market outlook improves. We will review the decision by February 2027.

Our people and culture differentiate us

Our strong performance in FY2024 is a testament to our more than 90,000 employees and contractors who work hard to build a better BHP every day. They are empowered to do so by the BHP Operating System and we continue to build an inclusive and diverse culture with a performance edge.

3

Table of Contents

During the year we refreshed Our Values, which set the tone for our culture. Our Values comprise three simple statements. First and foremost, we must always ‘Do what’s right’ – operating safely and with integrity are non-negotiable. We also need to constantly ‘Seek better ways’ – listening to others, seeking out new ideas, and improving on today. And finally, we must always strive to ‘Make a difference’, which applies not only to the company and the team, but also to the individual. Every day we have the opportunity to have a positive impact on performance, those around us, and the world. Our Values help guide everything we do at BHP. They reflect both what we stand for and who we aspire to be.

Innovation and technology

BHP is well placed to capitalise on the opportunities afforded by artificial intelligence (AI) and advanced data analytics given our large-scale, repeatable operations and processes, and vast amounts of data. We are already starting to see benefits. The application of AI at our Escondida processing plants has helped save more than three gigalitres of water – and 118-gigawatt hours of energy – since FY2022. Machine learning has assisted in the discovery of new copper deposits in Australia and the United States.

Through our Xplor and BHP Ventures programs we continue to seek new partnerships and access to game-changing technologies and insight to help drive sustainable growth for the decades ahead.

In great shape

BHP finished FY2024 in an excellent position. We are well placed to benefit from the significant global changes happening around us. We have strategic clarity and exposure to the right commodities. We continue to build on our excellence in operations and discipline in our capital allocation.

We hold resilient, long-term assets with substantial optionality. This allows us to make smart choices about how and where we use our balance sheet to fund growth and generate value.

As we look to FY2025, we will continue to execute our strategy to create value for our shareholders, community partners and stakeholders, now and into the future.

Thank you for your continued support.

/s/ Mike Henry

Mike Henry

Chief Executive Officer

4

Table of Contents

1 Why BHP

Our strategy

We will responsibly manage the most resilient long-term portfolio of assets, in highly attractive commodities, and will grow value through being excellent at operations, discovering and developing resources, acquiring the right assets and options, and capital allocation.

Through our differentiated approach to social value, we will be a trusted partner who creates value for all stakeholders.

The world needs essential metals and minerals to be produced by companies who set and uphold high ESG standards, who run their operations safely and efficiently, and who allocate capital in a consistent and disciplined way. These are the companies that will succeed. This is BHP.

Our capabilities, track record, scale and the unique way we work through the BHP Operating System enable a culture of continuous improvement.

We aim to grow value for our shareholders, partners and stakeholders through our portfolio of large long-life quality assets in attractive commodities and through our focus on social value, which is integral to how we operate.

BHP is positioned to benefit from the changes shaping our planet now and for decades to come as demand for our commodities grows.

Our products are vital

Population growth, urbanisation and improving living standards are global trends that underpin strong demand for the commodities we produce.

Demand for essential commodities is expected to increase as the world seeks to decarbonise.

Iron ore is needed for making steel to build cities and renewables infrastructure. Steelmaking coal is needed for the blast furnace process for making steel. Copper is vital for electrification. Nickel can be used in electric vehicle batteries. Potash can help with food security and more sustainable land use.

Scale is important

As new large low-cost ore bodies become harder to find and develop, the scale and quality of our assets set us apart. We have some of the largest resources and lowest-cost assets in the world.

One of our biggest growth levers is productivity and unlocking more value from our existing assets. We seek to improve productivity through the capabilities of our people and culture of continuous improvement driven through the BHP Operating System, and the use of technology and innovation to extract more from what we do every day and more from our resources.

5

Table of Contents

The scale of our assets provides multiple growth options. We are seeking to produce more iron ore in Western Australia. We are working to improve productivity at our steelmaking coal operations in Queensland. We are advancing multiple growth options in copper in Chile and our recently established copper province in South Australia. We have sanctioned the second stage of our Jansen potash project in Canada, which will eventually double its expected annual production.

>For more information refer to OFR 5

Social value is embedded in everything we do

We are committed to social value: our positive contribution to society. It is vital for our future and a consideration in the strategic decisions we make.

Social value underpins stable operations, reduces risk and opens doors to opportunities, partnerships, talent and capital. Delivering social value will help us to continue to generate long-term value for all partners and stakeholders, including shareholders.

>For more information refer to OFR 6.2 to 6.5

We do what we say

BHP has a track record of doing what we say we will do. We continue to plan strategically, responsibly, consistently, with a clear focus on being the best operator, being disciplined in capital allocation and continuing to generate value and returns for stakeholders.

We have generated net operating cash flows of over US$15 billion for all but one of the past 15 years. This stability is our hallmark – achieved through robust capital management and consistent operational performance.

Including the final dividend for FY2024 declared, we will have distributed more than US$42 billion in total in cash dividends to shareholders since 1 July 2021. This includes US$7.4 billion in cash dividends for FY2024.

Our total economic contribution in FY2024 was US$49.2 billion. This includes contributions to suppliers, wages and benefits for more than 90,000 employees and contractors, dividends, taxes and royalties, and voluntary investment in projects in the communities where we operate.

>For more information refer to OFR 4 and the BHP Economic Contribution Report 2024 available at bhp.com/ECR2024

The future is clear

Key commodities we produce or are positioning to produce are vital for a better world and can help address global challenges, such as climate change and food security.

We are continuing to build an inclusive and diverse workforce of talented people. We have a strong balance sheet and industry-leading operational capability underpinned by the BHP Operating System and our technical Centres of Excellence.

Our track record, long-term stability and commitment to social value and sustainability set us apart.

This combination will help us achieve our aim of growing value more consistently for our partners and stakeholders and drive attractive returns and long-term value for our shareholders.

6

Table of Contents

1.1 Where we operate

Footnotes

| 1. | This includes contribution to suppliers, wages and benefits for employees and contractors, dividends, taxes and royalties, and voluntary social investment. For more information refer to the Economic Contribution Report 2024. |

| 2. | For more information refer to the Economic Contribution Report 2024. |

| 3. | Based on a ‘point-in-time’ snapshot of employees as at 30 June 2024, including employees on extended absence. Contractor data is collected from internal organisation systems and averaged for a 10-month period, July 2023 to April 2024. Figures reported do not include employees and contractors of BHP Mitsubishi Alliance Blackwater and Daunia operations, sold to Whitehaven Coal during FY2024, and employees and contractors of the operations in Brazil that were acquired as part of the OZ Minerals acquisition completed during FY2023. |

| 4. | Rest of the world includes consolidation adjustments related to intra-group transactions. |

| 5. | Shown on a BHP share basis. |

| 6. | Includes Newcastle Coal Infrastructure Group (NCIG), which is an equity accounted investment and its financial information presented above, with the exception of net operating assets, reflects BHP Group’s share. Total Coal statutory result excludes contribution related to NCIG until future profits exceed accumulated losses. |

| 7. | Includes Olympic Dam, Prominent Hill and Carrapateena. |

| 8. | Includes Nickel West and West Musgrave project. |

| 9. | Reflects the contribution of the Blackwater and Daunia mines to 2 April 2024, the date on which BMA’s owners completed its divestment. |

| 10. | BHP’s attributable coal production for the year, being 50 per cent of BMA’s steelmaking coal production (22.3 Mt) and 100 per cent of New South Wales Energy Coal production (15.4 Mt). |

| 11. | In October 2023, BHP approved US$4.9 billion in capital expenditure for Jansen Stage 2. First potash production from Jansen Stage 1, which has approved capital expenditure of US$5.7 billion, is expected in late CY2026. |

| 12. | Includes Spence and Cerro Colorado. |

7

Table of Contents

1.2 Our portfolio

A resource mix for today – and for the future

We have copper, which is used in electrification. Iron ore, which is essential for making steel needed for construction, including renewables infrastructure. Our higher-quality steelmaking coal is used in the blast furnace process for making steel. Nickel can be used in electric vehicle batteries. We are on track to be a major global producer of potash by the end of the decade. Potash is used in fertilisers to assist with food security for a growing population and more sustainable land use. Among our by-products, we are a major producer of uranium and gold.

Copper

Highest production in over 15 years

1.86 Mt

^9% on FY2023

We hold the world’s largest copper mineral resources.1 We are using technical innovation, such as new flotation technology, to help lower energy costs and unlock value. We continue to pursue our strategy to increase our exposure to future-facing commodities, including copper, through exploration, acquisition and early-stage options. Our copper production rose 9 per cent in FY2024 to the highest in more than 15 years.

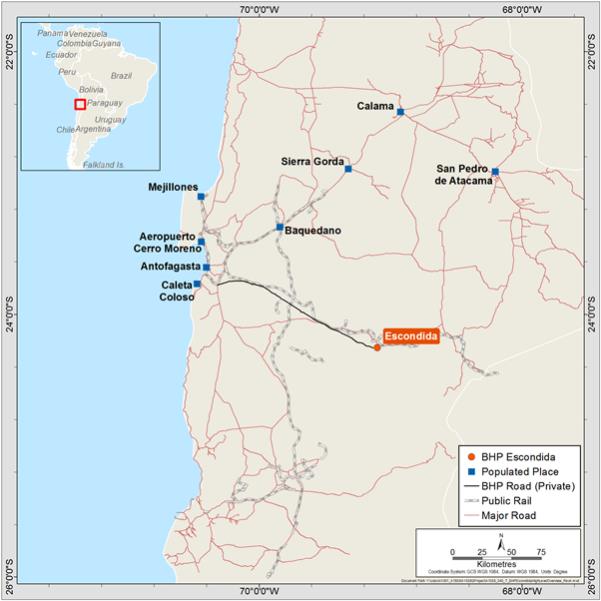

Escondida in Chile is the world’s largest copper mine. It increased production by 7 per cent in FY2024 compared to FY2023, to 1.12 million tonnes (Mt) (100 per cent basis). This was primarily due to a higher concentrator feed grade as mining progressed into areas of higher-grade ore as planned following the implementation of measures to manage geotechnical events in FY2023. Spence in Chile delivered another year of record production, up 6 per cent to 255 kilotonnes (kt). We are exploring a range of growth options across our Chilean copper assets, including a potential new concentrator at Escondida and the application of leaching technologies at Spence and Cerro Colorado.

We have established a significant resource base at Copper South Australia by adding Olympic Dam with Carrapateena and Prominent Hill from our OZ Minerals acquisition in FY2023. The successful integration of the former OZ Minerals assets has delivered increased production and exceeded our annualised synergies planned at the time of the acquisition of OZ Minerals. This has been through actions such as the processing of Prominent Hill and Carrapateena concentrate at Olympic Dam into higher-margin cathode and refined gold, resulting in annual records for cathode and gold production at Olympic Dam. Copper South Australia production was 322 kt in FY2024, including record production at Carrapateena. We’re progressing growth options at Copper South Australia, where our aspiration is to grow copper production to beyond 500 kt per year. Given the gold, silver and uranium co-products, this would be equivalent to over 700 kt per annum copper equivalent. We had exploration success in South Australia in FY2024 with OD Deeps, delivering greater than two kilometres in strike and more than one kilometre in depth at over 1 per cent copper grade and an Inferred Mineral Resource declaration at Oak Dam.

In July 2024, we agreed to acquire a 50 per cent interest in the Filo del Sol and Josemaria copper projects in Argentina and Chile with Lundin Mining. If approved, this will give us the opportunity to jointly advance an emerging copper district with world-class potential.

>For more information refer to OFR 5.2 and 5.3

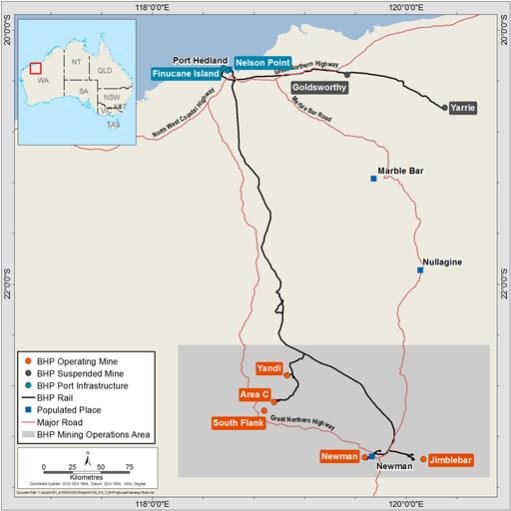

Iron ore

Second-consecutive full-year production record

260 Mt

^1% on FY2023

Western Australia Iron Ore (WAIO) is the lowest-cost major iron ore producer globally2 and has one of the lowest greenhouse gas (GHG) emission production intensities of benchmarked iron ore operations.3

WAIO delivered a second-consecutive full-year production record of 287 Mt (255 Mt BHP share), reflecting strong supply chain performance with increased capacity unlocked by the Port Debottlenecking Project 1 and increased production from South Flank, our newest and most technologically advanced mine. These more than offset the impacts of the continued tie-in activity for the Rail Technology Programme 1. South Flank ramped up to full production capacity of 80 million tonnes per annum (Mtpa) (100 per cent basis) on schedule during FY2024.

8

Table of Contents

We continue to invest in improvements in our rail and port operations and are assessing options to grow our WAIO production up to 330 Mtpa if market conditions warrant. These options include optimal mine and infrastructure configurations and potentially increased ore beneficiation. We expect to complete these studies in CY2025.

>For more information refer to OFR 5.1

Steelmaking coal

Focusing on higher-quality product

22.3 Mt

i 23% on FY2023

We continue to focus our steelmaking coal operations in Queensland on higher-quality product and have one of the lowest GHG emission production intensities of benchmarked export steelmaking coal mines.3 In a challenging year for BMA, production decreased from the prior year as a result of increased stripping to improve supply chain stability and restore depleted inventory positions, which arose from extended weather impacts and labour constraints over recent years, and the divestment of Blackwater and Daunia on 2 April 2024.

We believe a wholesale shift away from the blast furnace process for steelmaking is decades in the future. We also believe higher-quality steelmaking coals have potential for greater upside for quality premiums. This is because we believe steelmakers will seek to operate their blast furnaces with stronger, higher-performance steelmaking coal to lower overall coal consumption and, over time, to improve blast furnace process performance when implementing future GHG emission reduction technologies.

On 2 April 2024, BHP and its joint venture partner, Mitsubishi Development Pty Ltd, completed the sale of the Blackwater and Daunia mines to Whitehaven Coal for up to US$4.1 billion (100 per cent basis). Following the sale, around 90 per cent of BMA’s products will be sold by reference to the Platts PLV HCC FOB Qld index, the highest quality steelmaking coal index, up from 64 per cent prior to the transaction.

>For more information refer to OFR 5.1

Nickel

Temporary suspension announced

81.6 kt

^2% on FY2023

Nickel West production in FY2024 was in line with the prior year.

On 11 July 2024, we announced Western Australia Nickel, comprising the Nickel West operations and West Musgrave project, would be temporarily suspended from October 2024. We intend to review this decision by February 2027.

The decision to temporarily suspend Western Australia Nickel reflects oversupply in the global nickel market. Forward consensus nickel prices over the next half of the decade have fallen sharply reflecting strong growth of alternative low-cost nickel supply.

During the temporary suspension, BHP will continue to support our workforce and local communities. BHP will invest approximately US$300 million per annum following completion of a transition period to support a potential re-start of Western Australia Nickel. The transition period commenced in July 2024. Operations will be suspended in October 2024 and handover activities for temporary suspension are expected to be completed by December 2024.

>For more information refer to OFR 5.1

9

Table of Contents

Potash

Major global producer by the end of the decade

US$10.6bn

Total approved capital expenditure through Jansen Stage 1 and Jansen Stage 2

We are developing one of the world’s largest potash mines in Canada. The Jansen potash project will increase our product diversification, customer base and operating footprint, and expand our business into a future growth market.

The US$5.7 billion Jansen Stage 1 project is ahead of the original schedule and was over 50 per cent complete by the end of FY2024. First production from Jansen Stage 1 is expected in late CY2026, followed by a two-year ramp-up period. In October 2023, we announced an additional investment of US$4.9 billion for Jansen Stage 2, which will increase Jansen’s total planned potash production capacity to ~8.5 Mtpa. We have commenced execution of Jansen Stage 2.

Transitioning directly from Jansen Stage 1 to Jansen Stage 2 during the construction period will bring operational benefits, including leveraging the experience of our integrated project team and continued use of our existing suppliers and contractors.

We are on track to be a major global producer of potash by the end of the decade. Longer term, Jansen has the potential for two additional expansions to reach an ultimate production capacity of 16 to 17 Mtpa (subject to studies and approvals).

>For more information refer to OFR 5.3

Footnotes

| 1. | Largest copper mineral resources on a contained metal basis, equity share. Peers include: Anglo American, Antofagasta, Codelco, First Quantum Minerals, Freeport, Glencore, Rio Tinto, Southern Copper and Teck. Source peers: Wood Mackenzie Ltd, Q2 2023. Source BHP data: BHP Annual Report 2024. |

| 2. | Based on published unit costs of major iron ore producers as reported at 30 June 2024. There may be differences in the manner that third parties calculate or report unit costs data compared to BHP, which means third-party data may not be comparable with our data. |

| 3. | For CY2023, the GHG emissions intensity of our production of our commodities is estimated to rank in the first quartile for our iron ore, copper and steelmaking coal mines, and the second quartile for our nickel operations (ahead of all Indonesian-based operations) of global mining operations analysed by CRU. This analysis is based on CY2023 data from CRU (as CRU data is prepared on a calendar year basis), and includes CRU’s assumptions and estimates of BHP’s operations. We transitioned to using CRU (rather than Skarn Associates) for this analysis in FY2024 as part of an annual vendor assessment and selection process. For more information on how the GHG emission intensity for our iron ore and steelmaking coal mines has been calculated and compared refer to the BHP ESG Standards and Databook 2024 available at bhp.com/climate. |

2 What differentiates us

BHP’s ability to deliver differentiates us from our competitors. We do what we say we will do. This has created stability in our historical performance that has been a hallmark of BHP for more than a decade.

There are many factors that underpin this historic stability, each of which is vital. It’s the unique combination of these factors that sets us apart.

Our people

We have more than 90,000 employees and contractors globally. We strive to offer an engaging and supportive workplace, which empowers our people to find safer and more productive ways of working. We do this by providing the tools and opportunities in our working environment to allow our people to perform at their best. Our people are empowered daily in their work by the BHP Operating System.

10

Table of Contents

Our Values

Our Values set the tone for our culture, a unique part of our competitive advantage. They are a declaration of what we stand for. They guide our decision-making, reinforce our culture and ensure all our people are steering in the same direction, delivering on our purpose.

In FY2024, Our Values were refreshed to:

Do what’s right – A sustainable future starts with safety and integrity, building trust with those around us

Seek better ways – Listening to learn and inspiring challenge is how we drive progress

Make a difference – The accountability to act, create value and have impact is on each of us, every day

Our Values help our people move quickly and deliberately when we encounter challenges and opportunities.

Health and safety

>For more information refer to OFR 6.1 and 6.8

Female employee participation

Indigenous employee participation2

Footnotes

| 1. | Combined employee and contractor frequency per 1 million hours worked. |

| 2. | Point in time data at 30 June 2024. |

| 3. | Participation in Minerals Australia operations in Australia. FY2023 figure does not include OZ Minerals. |

| 4. | Participation in Minerals Americas operations in Chile. |

| 5. | Participation in Jansen potash project and operation employees in Canada. |

11

Table of Contents

BHP Operating System

The BHP Operating System (BOS) is our unique overarching management system that enables the right culture, routines, behaviours and leadership to deliver stable operating excellence and leading safety performance. It provides us with a competitive edge.

BOS drives continuous improvement through the application of BOS tools and practices. It makes improvement central to everyone’s role, allowing people to work on the system, not just in it.

BOS helps us continuously focus on leadership development, capability and engagement, and creates better-planned, more stable work processes.

Aligning around our strategy, operating philosophy and principles for decision-making will make us an even better company – one that focuses on safety, leads the sector, generates strong returns for our shareholders, and meets the expectations of our partners, communities and other stakeholders.

We have deployed BOS across our business.

How BOS works

Three principles underpin BOS and guide how we think and behave at BHP

Exceptional performance

Operating and financial strength

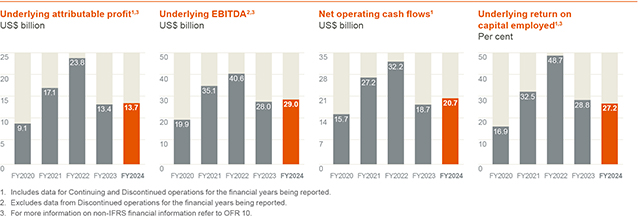

The strength of our portfolio, our operating excellence and financial rigour from our disciplined application of the Capital Allocation Framework (CAF) enables us to deliver strong and consistent returns. We achieved net operating cash flow of US$20.7 billion in FY2024. Our net operating cash flow has been more than US$15 billion for all but one of the past 15 years.

In FY2024, through our CAF, we kept our balance sheet strong, delivered growth and returns for our shareholders, made progress towards our social value and GHG emission reduction objectives and prioritised capital to maintain reliable operations.

Operational excellence

Our strong results in FY2024 were driven by performance and discipline at our operations, which overall performed well. We achieved production guidance across all commodities in FY2024, with steelmaking coal achieving the upper end of its revised production guidance. This included record annual production at WAIO, Spence and Carrapateena, record cathode and gold production at Olympic Dam, and the highest production in four years at Escondida.

Our focus on cost discipline helped us manage inflationary pressures effectively. We experienced a global inflation rate of around 4 per cent, particularly in relation to labour. Our cost discipline allowed us to mitigate these ongoing cost pressures with unit costs around 2.9 per cent higher across our major assets. We met unit cost guidance at Escondida, WAIO and Spence, and revised unit cost guidance at BMA. WAIO extended its lead over competitors as the lowest cost major iron ore producer globally.

For mining companies, cost differentiation is becoming even more pronounced. General inflation and labour are expected to continue to put upwards pressure on costs. The costs of decarbonisation are also expected to be inflationary and will disproportionately impact companies with higher GHG emissions intensity. As such, while the marginal cost of mining production is clearly higher than in the past; in the medium term there are signs it could go higher.

12

Table of Contents

Technology and innovation

The use of technology and our focus on innovation, together with BOS, have helped accelerate continuous improvement – from the introduction of advanced technologies designed to improve safety and increase productivity of our operated assets, to reducing water and energy consumption.

Technology is a key lever for BHP and has been used to:

| • | support the maintenance of safe, predictable and productive operations |

| • | drive productivity improvements, with an emphasis on automation and real-time, data-driven insights and decision-making |

| • | unlock the next stage of value growth potential, such as by realising greater margins at our existing operations and enabling the discovery of new assets |

| • | improve sustainability outcomes through innovation |

| • | help drive inclusion and diversity, such as remote operations and decision support tools that make roles more accessible to a wider range of people |

The advanced use of next generation technologies, such as artificial intelligence (AI) and cloud and data analytics, are supporting quicker and more efficient resource recovery, more safely and more sustainably. They are also helping lift performance through operational improvements.

Examples of how BHP used AI in FY2024 include:

| • | A digital tool at Escondida used AI to increase revenue by US$18.9 million in FY2024 by enabling drill and blast teams to select a more optimal blasting pattern design. The technology also helps to mitigate coarse ore restrictions at Escondida’s semi-autogenous grinding (SAG) mills by improving post-blasting fragmentation. We will use this tool at Spence to assist with stabilising its SAG mill performance and increase its productivity. |

| • | Next generation improvements to the Process Area Set Point Optimisation (PASPO) were rolled out across BMA sites in FY2024 to increase production of on-specification steelmaking coal, increasing revenue by US$15.5 million. For example, the Caval Ridge team identified an opportunity to increase yield by reducing density variation while keeping train product ash on specification. |

We upgraded our global technology system 1SAP ERP to S/4HANA in FY2024. The modernisation of this core global platform is critical to our operations, as it is used to:

| • | pay our people and suppliers |

| • | sell and deliver our products |

| • | better maintain our equipment |

| • | accurately report our financial results to the market |

| • | above all, enable us to operate more safely, efficiently and reliably |

Social value

We are committed to social value and sustainability and are making progress in more responsibly providing commodities the world needs to develop and decarbonise. We believe this commitment can help us become a partner of choice with communities, governments, suppliers and our customers. We seek to be a valued partner with the communities where we operate and the Indigenous peoples we interact with.

In FY2024, we continued to refine our approach to social value. We have provided progress on our 2030 goals through our 2030 social value scorecard.

>For more information on our 2030 social value scorecard refer to OFR 6.5

Through our commitment to sustainability, we seek to reduce the impact of our operational activities. We have set a long-term goal to achieve net zero operational GHG emissions (Scopes 1 and 2 emissions from our operated assets) by CY2050. We also have a long-term goal of net zero Scope 3 GHG emissions by CY2050. Achievement of this Scope 3 goal is uncertain, particularly given the challenges of a net zero pathway for our customers in steelmaking, and we cannot ensure the outcome alone.

We manage our operational decarbonisation projects across our operated assets through our CAF to help us use our capital effectively.

13

Table of Contents

We are also working with our suppliers and customers to support their efforts to reduce GHG emissions. For example, during FY2024 we signed a framework agreement with Rio Tinto and BlueScope to investigate the development of an ironmaking electric smelting furnace pilot plant using Pilbara iron ores that have been pre-processed into direct reduced iron. This process route could open a pathway to an alternative to the conventional blast furnace method of steelmaking with the potential to reduce GHG emissions intensity by 85 per cent and meet near zero emission steelmaking benchmarks.1

For more information on our GHG emission goals and targets refer to OFR 6.9

We have set goals in areas such as environment and water stewardship. To meet the FY2024 short-term milestone for the Healthy environment pillar of our social value scorecard, we have developed a Group-level framework for nature-positive plans to achieve our 2030 Healthy environment goal (BHP Healthy environment goal roadmap).2 Our 2030 Healthy environment goal is to create nature-positive3 outcomes by having at least 30 per cent of the land and water we steward4 at the end of FY2030 under conservation, restoration or regenerative practices.

At 30 June 2024, we had 83,012 hectares or 1.62 per cent5 of the land and water we steward4,6 under nature-positive management practices.7

>For more information refer to OFR 6.5

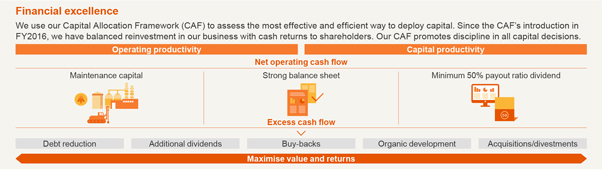

Financial excellence

We use our Capital Allocation Framework (CAF) to assess the most effective and efficient way to deploy capital. Since the CAF’s introduction in FY2016, we have balanced reinvestment in our business with cash returns to shareholders.

Our CAF promotes discipline in all capital decisions.

Footnotes

| 1. | Based on direct reduced iron electric smelting furnace route (using renewable or other low to zero GHG emissions power). Estimated reduction in GHG emissions intensity is calculated relative to a baseline reference of 2.2 tonnes of CO2-e per tonne of crude steel, as sourced from IEA Iron and Steel Technology Roadmap (October 2020). For more information refer to our Value chain GHG emissions – Hydrogen reduction and electric smelting of BHP ores case study on page 26 of our Climate Transition Action Plan 2024, available at bhp.com/CTAP2024. |

| 2. | The BHP Healthy environment goal roadmap is intended to apply to our operated assets in Australia, Chile and Canada. Due to the acquisition of OZ Minerals and prioritisation of activities based on risks and impacts, Carrapateena, Prominent Hill, West Musgrave and legacy assets are currently out of scope for the roadmap; with the exception of West Musgrave, these assets are planned to be incorporated into the roadmap in FY2025. Incorporation of West Musgrave into the BHP Healthy environment goal roadmap will be reviewed following the decision to temporarily suspend the Western Australia Nickel operations. |

| 3. | Nature-positive is defined by the TNFD Glossary version 1.0 as ‘A high-level goal and concept describing a future state of nature (e.g. biodiversity, ecosystem services and natural capital), which is greater than the current state’. We understand it includes land and water management practices that halt and reverse nature loss – that is, supporting healthy, functioning ecosystems. BHP intends to review this definition in FY2025, in light of the recently revised TNFD Glossary version 2.0 (June 2024) definition of nature-positive. |

| 4. | This excludes areas we hold under greenfield exploration licences (or equivalent tenements), which are outside the area of influence of our existing mine operations. 30 per cent will be calculated based on the areas of land and water that we steward at the end of FY2030. |

| 5. | 1.62 per cent is calculated based on the areas of land and water that we stewarded (excluding areas we hold under greenfield exploration licences (or equivalent tenements) and subject to footnote 6) at 30 June 2024 – which was approximately 5,125,935 hectares; an increase of approximately 18,750 hectares compared to approximately 5,107,185 hectares at 30 June 2023. For more information on the restatement of FY023 figures refer to OFR 6.10. |

| 6. | While some of the land related to the Daunia and Blackwater mines is pending transfer following BMA’s divestment of these mines on 2 April 2024, these areas are no longer under BMA’s control or operated for BMA’s benefit so have been excluded from the areas of land and water we stewarded at 30 June 2024. |

| 7. | Nature-positive management practices refer to an area under stewardship that has a formal management plan that includes conservation, restoration or regenerative practices. For more information refer to the BHP ESG Standards and Databook 2024, available at bhp.com/ESGStandards2024. |

14

Table of Contents

3 Positioning for growth

With our clear strategy and our laser-like focus on creating and sustaining the right portfolio of the best assets in attractive commodities with enhanced growth optionality, BHP is well placed to capitalise on the changes shaping our world. As the global population grows and urbanises and the world pursues decarbonisation and electrification, we are positioning our portfolio and pursuing multiple growth options to increase our exposure to these megatrends.

Unlocking growth at our assets

One of our biggest near-term growth levers is from improving productivity at our existing assets and unlocking more of their potential.

WAIO was designed with an initial capacity of 240 Mtpa. In FY2024, it produced a record 287 Mt (100 per cent basis). We are implementing initiatives to grow WAIO production to more than 305 Mtpa over the medium term. This is expected to be through South Flank, which reached full production capacity in FY2024, the continued debottlenecking of our port and rail systems, the rollout of autonomous haulage trucks, and ongoing productivity enhancements. We are studying options to further grow annual production up to 330 Mt over the medium to long term, with these studies expected to be completed in CY2025.

Escondida has significant resource potential and we are progressing a range of studies, including potentially replacing the original Los Colorados concentrator. We are also looking at different leaching technologies that could help us extract more copper while potentially using less energy and water, reduce or eliminate the need for tailings dams, and enable production of cathode-finished product that does not require smelting.

Growing our position in potash

Potash is a fertiliser and enables more efficient and sustainable farming. With the world’s population continuing to grow and rising concerns around food security and land use, potash is a future-facing commodity that presents opportunities for growth.

At the end of FY2024, Jansen Stage 1 was tracking ahead of the original schedule and more than 50 per cent complete. Production is expected to commence in late CY2026, followed by a two-year ramp-up period. When Jansen Stage 1 reaches full production, planned production will be approximately 4.15 Mtpa.

During FY2024, BHP approved Jansen Stage 2, which will double planned production to around 8.5 Mtpa at full capacity. Jansen Stage 2 is an important milestone that underscores our confidence in potash and marks the next phase of BHP’s growth in Canada. We believe Jansen will deliver long-term value for shareholders and the local community, and will position BHP as one of the leaders in the global potash industry. We have commenced execution of Jansen Stage 2, with first production expected in FY2029.

Copper South Australia: Consolidating a significant resource base

We have established a significant resource base at Copper South Australia by combining OZ Minerals’ two South Australian mines, Prominent Hill and Carrapateena, with Olympic Dam and the Oak Dam deposit.

With Copper South Australia, we are focused on developing an asset with greater scale and simplicity. Copper South Australia produced 322 kt of copper in FY2024 and we are pursuing potential pathways to expand this to more than 500 kilotonnes per annum (ktpa) through increases in mine production rates and improved mining methods, the expansion of smelting and refining capacity, the application of BOS, the development of exploration assets and greater by-product production.

Exploration efforts progressed at the Oak Dam copper deposit located 65 kilometres southeast of Olympic Dam and at OD Deeps, which is below Olympic Dam. The Copper South Australia province is expected to produce copper, gold and uranium oxide for decades to come.

>For more information refer to OFR 5.2

Creating and accelerating longer-term options

BHP Ventures

BHP Ventures is our dedicated venture capital unit. It looks for game-changing technologies via emerging companies to help drive ongoing and more sustainable growth within BHP and provides us with a portfolio of new growth options for the decades ahead.

BHP Ventures complements the innovation already underway within BHP by forging new partnerships and creating fresh opportunities to strengthen our portfolio and support the decarbonisation of our operated assets and decarbonisation opportunities in our value chain. For our partners, BHP Ventures provides an opportunity to collaborate with us.

New investments in FY2024 included SiTration, which is developing a silicon membrane-based technology for metal extraction, and ZwitterCo, which is developing membrane solutions for the treatment of water. BHP continued to support existing portfolio companies Boston Metal and Electra through technical knowledge exchanges and the supply of iron ores for testing in relation to technologies that have potential to contribute to our Scope 3 emissions medium-term goal for steelmaking and our long-term net zero goal. BHP also continued to test early-stage leaching technologies from Jetti Resources and Ceibo as part of broader copper leaching studies.

Think & Act Differently

Think & Act Differently is BHP’s internal team set up to find and accelerate the best mining technology solutions to support our ambitions to deliver commodities the world needs in new ways. It is focused on opening new and accelerated pathways to market through partnerships, rapid experimentation and systems thinking. It aims to de-risk a portfolio of over 100 initiatives, from small scale experiments to on-site demonstrations.

15

Table of Contents

We are seeking to advance technologies that can unlock resource growth, particularly relating to copper, and build capability across the mining value chain to find new ways to understand ore bodies and responsibly extract and process resources. Current areas of work include leaching, ore body knowledge and accelerated minerals recovery.

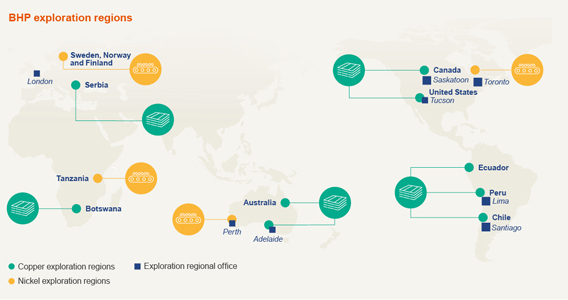

BHP Exploration

During FY2024, we advanced our global programs focusing on early-stage exploration opportunities in Australia, Canada, Chile, Peru, Sweden, Serbia and the United States. This effort involved concept evaluation work through prospect testing.

We fully integrated the OZ Minerals exploration portfolio, significantly expanding our land holdings and enabling us to develop an important province in South Australia with significant copper potential.

In Canada, we continued our partnership with Midland Exploration Inc. through our prospect generation exploration alliance.

In the United States, we entered an alliance with Ivanhoe Electric Inc., with BHP to provide initial funding of US$15 million over three years to explore for copper and other critical minerals across areas of interest in Arizona, New Mexico and Utah.

In Australia, we commenced a partnership with Red Ox Copper Pty Ltd, exploring for copper in Northern Queensland.

In Europe, we acquired Ragnar Metals Sweden AB for A$9.8 million, gaining ownership of the Tullsta nickel project. Similarly, we entered into early-stage exploration alliances with Kingsrose Mining Ltd across areas of interest in Finland and Norway, and with Tutume Metals in Botswana.

Aso in FY2024, we withdrew from the Elliott Farm-in and joint venture agreement with Encounter Resources Limited in Australia.

Growth through exploration, focused on copper and nickel

BHP Xplor

BHP Xplor, launched in FY2023, is a global accelerator program designed to support early-stage mineral exploration companies in finding critical resources needed for the energy transition. Its aim is to identify and nurture the next generation of explorers, empowering them to fast track their geologic concepts for potential long-term partnership. The program supports technical, business and operational facets to equip participant companies with the necessary tools and guidance to become investment ready.