UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

Certified Shareholder Report of

Registered Management Investment Companies

Investment Company Act File Number: 811-05085

Capital Income Builder

(Exact Name of Registrant as Specified in Charter)

333 South Hope Street, 55th Floor

Los Angeles, California 90071

(Address of Principal Executive Offices)

Registrant's telephone number, including area code: (949) 975-5000

Date of fiscal year end: October 31

Date of reporting period: October 31, 2022

Gregory F. Niland

Capital Income Builder

5300 Robin Hood Road

Norfolk, Virginia 23513

(Name and Address of Agent for Service)

ITEM 1 – Reports to Stockholders

Capital Income Builder® Annual report

for the year ended

October 31, 2022 |  |

| | |

Seeking

income growth

opportunities from

around the world

Capital Income Builder seeks to provide you with a level of current income that exceeds the average yield on U.S. stocks generally and to provide you with a growing stream of income over the years. The fund’s secondary objective is to provide you with growth of capital.

This fund is one of more than 40 offered by Capital Group, home of American Funds, one of the nation’s largest mutual fund families. For over 90 years, Capital Group has invested with a long-term focus based on thorough research and attention to risk.

Fund results shown in this report, unless otherwise indicated, are for Class F-2 and Class A shares at net asset value. If a sales charge (maximum 5.75% for Class A shares) had been deducted, the results would have been lower. Results are for past periods and are not predictive of results for future periods. Current and future results may be lower or higher than those shown. Prices and returns will vary, so investors may lose money. Investing for short periods makes losses more likely. For current information and month-end results, visit capitalgroup.com.

Here are the average annual total returns on a $1,000 investment for periods ended September 30, 2022 (the most recent calendar quarter-end):

| | | 1 year | | 5 years | | 10 years |

| | | | | | | |

| Class F-2 shares | | | –10.85 | % | | | 2.28 | % | | | 4.96 | % |

| Class A shares (reflecting 5.75% maximum sales charge) | | | –16.15 | | | | 0.86 | | | | 4.13 | |

For other share class results, visit capitalgroup.com and americanfundsretirement.com.

The total annual fund operating expense ratios are 0.36% for Class F-2 shares and 0.59% for Class A shares as of the prospectus dated January 1, 2023 (unaudited). The expense ratios are restated to reflect current fees.

Investment results assume all distributions are reinvested and reflect applicable fees and expenses. When applicable, results reflect fee waivers and/or expense reimbursements, without which they would have been lower. Visit capitalgroup.com for more information.

The fund’s 30-day yield as of October 31, 2022, was 2.63% for Class F-2 shares and 2.29% for Class A shares, calculated in accordance with the U.S. Securities and Exchange Commission (SEC) formula. The fund’s 12-month distribution rate as of that date was 3.99% for Class F-2 shares and 3.53% for Class A shares. The Class A share results reflect the 5.75% maximum sales charge. The SEC yield reflects the rate at which the fund is earning income on its current portfolio of securities, while the distribution rate reflects the fund’s past dividends paid to shareholders. Accordingly, the fund’s SEC yield and distribution rate may differ.

The return of principal for bond funds and for funds with significant underlying bond holdings is not guaranteed. Fund shares are subject to the same interest rate, inflation and credit risks associated with the underlying bond holdings. Investing outside the United States may be subject to additional risks, such as currency fluctuations, periods of illiquidity and price volatility. These risks may be heightened in connection with investments in developing countries. Refer to the fund prospectus and the Risk Factors section of this report for more information on these and other risks associated with investing in the fund.

Investments are not FDIC-insured, nor are they deposits of or guaranteed by a bank or any other entity, so they may lose value.

Contents

| 1 | | Letter to investors |

| | | |

| 4 | | The value of a long-term perspective |

| | | |

| 6 | | Investment portfolio |

| | | |

| 35 | | Financial statements |

| | | |

| 67 | | Board of trustees and other officers |

| | | |

Fellow investors:

Global markets retreated from last year’s strong gains amid heightened geopolitical risk, persistent inflationary pressures and aggressive monetary tightening. For the 12 months ended October 31, 2022, Capital Income Builder fell 9.21%, with all dividends reinvested, faring better than the 18.50% loss of the 70%/30% MSCI All Country World Index (ACWI)/Bloomberg U.S. Aggregate Index. The blended index, which measures returns for global stock markets and U.S. fixed income, is the fund’s primary benchmark as of January 1, 2021.

Dividend income

Capital Income Builder’s primary objective is to provide shareholders a level of current income that exceeds the average yield on U.S. stocks in general as well as a growing stream of income over the years. The secondary goal is to grow capital. In pursuit of its income objective, the fund recorded a 12-month yield of 3.99% for its F-2 share class, greater than the corresponding yield for the MSCI ACWI (2.33%). The 12-month yield for the Bloomberg U.S. Aggregate Index was 5.01% as of October 31, 2022, versus 1.66% in October 2021.

The fund’s F-2 shares paid dividends of approximately $1.04 a share, including a special dividend of about 61 cents per share, in December 2021. The fund also went on to pay regular dividends of approximately 46 cents a share in March and June 2022 and about 45 cents in September. The fund strives to grow its quarterly distribution rate over time.

Results at a glance

For periods ended October 31, 2022, with all distributions reinvested

| | | Cumulative

total returns | | Average annual total returns |

| | | 1 year | | 5 years | | 10 years | | Lifetime

(since Class A

inception on

7/30/87) |

| | | | | | | | | |

| Capital Income Builder (Class F-2 shares)1 | | | –9.21 | % | | | 3.33 | % | | | 5.53 | % | | | 8.60 | % |

| Capital Income Builder (Class A shares) | | | –9.42 | | | | 3.11 | | | | 5.32 | | | | 8.41 | |

| 70%/30% MSCI ACWI/Bloomberg Index2,3,4 | | | –18.50 | | | | 3.76 | | | | 5.97 | | | | 6.71 | |

| MSCI ACWI (All Country World Index)2,3,5 | | | –19.96 | | | | 5.24 | | | | 7.98 | | | | 6.83 | |

| Bloomberg U.S. Aggregate Index3,6 | | | –15.68 | | | | –0.54 | | | | 0.74 | | | | 5.39 | |

| | | | | | | | | | | | | | | | | |

| 1 | Class F-2 shares were first offered on August 1, 2008. Class F-2 share results prior to the date of first sale are hypothetical based on the results of the original share class of the fund without a sales charge, adjusted for typical estimated expenses. Visit capitalgroup.com for more information on specific expense adjustments and the actual dates of first sale. |

| 2 | From July 30, 1987, through December 31, 1987, the MSCI World Index was used because the MSCI ACWI did not exist. MSCI World Index results reflect dividends net of withholding taxes, and MSCI ACWI results reflect dividends gross of withholding taxes through December 31, 2000, and dividends net of withholding taxes thereafter. |

| 3 | The market indexes are unmanaged and, therefore, have no expenses. Investors cannot invest directly in an index. There have been periods when the fund has lagged the index. Sources: MSCI, Bloomberg Index Services Ltd. |

| 4 | The 70%/30% MSCI ACWI/Bloomberg Index blends the MSCI ACWI with the Bloomberg U.S. Aggregate Index by weighting their total returns at 70% and 30%, respectively. Results assume the blend is rebalanced monthly. As of January 1, 2021, the fund’s primary benchmark is the 70%/30% MSCI ACWI/Bloomberg U.S. Aggregate Index. |

| 5 | The MSCI All Country World Index is a free float-adjusted, market capitalization-weighted index that measures equity results in global developed and emerging markets. It consists of more than 40 developed and emerging market country indexes. |

| 6 | The Bloomberg U.S. Aggregate Index represents the U.S. investment-grade, fixed-rate bond market. |

| | |

Global markets struggled

While Capital Income Builder ended the fiscal year in negative territory, it held up notably well in the face of major stock and bond market declines as investors absorbed the implications of Russia’s February invasion of Ukraine, the challenge of balancing persistent inflationary pressures with a potential recession, and the U.S. Federal Reserve’s firm commitment to tighter monetary policy. In 2022, the Fed raised interest rates five times by the end of October, including three 75-basis-point increases, to combat rising inflation in the most aggressive rate hiking in decades. Europe grappled with significant political upheaval and economic challenges coupled with monetary tightening; the European Central Bank (ECB) raised interest rates to the highest level since 2009. Among other major markets, China faced slowing economic growth and the implications of COVID-19-induced lockdowns.

Against this backdrop, the MSCI ACWI fell 19.96% for the fiscal year, versus a 14.61% drop for the S&P 500 Index.1 All MSCI ACWI sectors declined, except for energy, which rose 28.95% as oil and natural gas prices soared. Communication services, consumer discretionary and information technology fell the most, with communication services sliding 39.56%. Value stocks fared better than growth equities in a significant reversal from previous years; the MSCI ACWI Value Index2 lost 10.29%, versus a 29.25% decline for the MSCI ACWI Growth Index.3 Bond markets sank as central banks aggressively raised interest rates to fight high inflation. The Bloomberg U.S. Aggregate Index dropped 15.68%, while the Bloomberg Corporate Investment Grade Index fell 19.57%.

Inside the portfolio

Capital Income Builder’s holdings are focused on companies that we believe will provide current and growing dividend income and capital appreciation through a challenging market environment.

VICI Properties — which makes up 1.7% of fund assets — was a major contributor. Shares of the real estate investment trust, which owns portfolios for Caesars Palace Las Vegas, MGM Grand and the Venetian Resort Las Vegas, rose 9.10%; VICI posted strong 2021 profits and robust quarterly earnings throughout 2022 following its acquisition of MGM Growth Properties and expanded partnership with Great Wolf Resorts. Real estate firms in general compose a notable portion of the fund, at 6.0% of assets.

Shares of Canadian Natural Resources rose 41.12% for the fiscal year, amid higher energy prices and tighter supply in the face of ongoing conflict in Ukraine. In general, Capital Income Builder invests in select low-cost energy providers and sound capital allocators that focus on shareholder returns. We believe that many of these companies are likely to continue participating in the major long-term energy transition happening across the globe. This includes Europe’s shift from Russian gas and increased demand for renewables amid pressure for reduced carbon emissions. Despite potential challenges, we believe this longer-term global energy shift will offer significant opportunities related to new pipelines and demand for liquified natural gas and renewable energy sources.

Investments in the consumer staples sector — which make up 10.3% of the portfolio — further supported fund results and are likely to remain resilient in a slowing economy. Shares of General Mills rose 32.01%; the food giant had a dividend yield of 2.57% at the end of the fiscal year. British American Tobacco (BAT) and Phillip Morris International, which respectively make up 1.7% and 2.2% of fund assets, also helped relative results. Both firms remain committed to developing reduced-risk, next-generation products and have managed to sustain pricing power in an inflationary environment.

In general, health care tends to hold up well during cyclical downturns, and the sector appears to be more resistant to current inflationary pressures than other areas of the market, such as food and energy. Select health care companies offer attractive valuations, along with the potential for improving fundamentals and long-term product pipeline opportunities driven by innovative research. AbbVie was one of the largest contributors to the portfolio for the fiscal year; the pharmaceutical firm is the second-largest fund holding, making up 2.3% of assets. AbbVie offered a 3.85% dividend yield as of October 31. Shares of Amgen also rose sharply, and shares of Gilead Sciences climbed, bolstered by sales of its cancer and HIV drugs in the first three quarters of 2022.

In the industrials sector, aerospace and defense companies have benefited from post-COVID-19 reopenings and higher defense budgets in the face of rising geopolitical tensions. Shares of Raytheon Technologies gained amid strong profits throughout the fiscal year, driven by recovering demand for commercial aerospace and expectations for increased military spending.

Shares of Comcast fell sharply. The telecommunications giant reported strong results for its theme park business in the first three quarters of 2022, but grappled with slower revenue from its Sky business, which operates across Europe. Comcast offered a dividend yield of 3.34% as of October 31.

Shares of energy company Gazprom declined amid Russian sanctions and the implications of European efforts to reduce dependence on Russian gas following the invasion of Ukraine. Shares of the Moscow Exchange Micex also fell sharply. The energy crisis stemming from the Russia-Ukraine conflict also hurt European

| 1 | The S&P 500 Index is a market capitalization-weighted index that represents approximately 500 widely held common stocks. |

| 2 | The MSCI ACWI Value Index captures large- and mid-cap securities exhibiting overall value style characteristics across 23 developed market and 24 emerging market countries. Value style characteristics are defined using three variables: book value to price, 12-month forward earnings to price and dividend yield. |

| 3 | The MSCI ACWI Growth Index captures large- and mid-cap securities exhibiting overall growth style characteristics across 23 developed market and 24 emerging market countries. Growth style characteristics are defined using five variables: short- and long-term forward EPS growth rates, current internal growth rate, long-term historical EPS growth trend and long-term historical sales per share growth trend. |

| | |

utilities firms, with shares of Italian utilities provider Enel affected by adverse economic and geopolitical pressures, including worries about exposure to Russian gas, Italian political uncertainty and the risk of a European recession.

In the technology sector, several semiconductor stocks declined in the face of supply chain issues and fears about the potential impact of a global economic slowdown. Shares of GlobalWafers, Taiwan Semiconductor Manufacturing Company and Vanguard International all fell. GlobalWafers was also weighed down by issues related to its failed takeover of Germany-based silicon wafer maker Siltronic.

Bond allocations

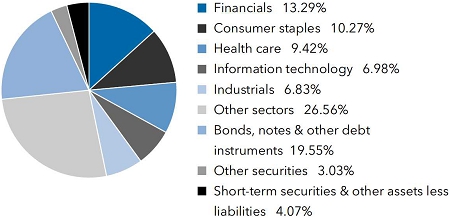

Capital Income Builder’s bond allocations aim to complement its global equity investments in both higher-yielding stocks with lower-dividend growth potential and stocks with lower current yields and prospects for faster dividend growth. Fixed income investments tend to include well-diversified, higher-quality securities, with the goal of providing income and cushioning equity volatility. U.S. bonds declined over the fiscal year, but still held up better than global stocks, with the Bloomberg U.S. Aggregate Index falling 15.68% versus a 19.96% decline for the MSCI ACWI Index. Bond allocations now offer more income opportunities than a year ago, in the view of managers; exposure to bonds has notably increased to 19.6% of total assets from 15.3% as of October 31, 2021. The fund remains focused on high-quality, lower-risk bonds as a source of steady income. As bond valuations have become more attractive, the fund has seen increased exposure to select mortgage-backed securities.

Moving forward

The world is currently facing a variety of economic, geopolitical and market-based crosscurrents. Inflation appears likely to persist, concerns about recession loom and higher interest rates have become a reality across key developed markets. More broadly, current circumstances appear to reflect longer-term shifts from deflation to inflation and lower to higher interest rates, heightened geopolitical risk, the redistribution of global supply chains, and a multiyear global energy transition.

Against this backdrop, dividend-paying stocks have garnered investor attention after a decade-long period of growth-oriented stocks dominating markets. In a rising and more normalized interest rate environment, total return is likely to be driven by a combination of capital appreciation and dividend returns. For more historical context, dividend returns represented more than one-third of total S&P 500 returns from January 1926 to September 2022, with capital appreciation making up the rest of the return. (By contrast, dividends constituted more than 70% of S&P 500 returns in the 1970s, when inflation was rampant.*) Capital Income Builder was created in 1987 after a period of high inflation to help provide a stream of dividends in an attempt to counter inflation. Dividend payers tend to hold up well in inflationary environments.

We recognize the immediate challenges and opportunities across a range of possible economic scenarios, while staying firmly grounded in Capital Income Builder’s key driving philosophy of finding higher-yielding stocks with predictable growth. The fund continues to focus on companies with sound, improving capital allocation that we believe are poised to maintain healthy balance sheets and pay sustainable dividends. This includes convictions in companies with low starting yields that we believe can grow dividends reliably over time, bond proxies that are typically higher yielding but have lower growth, and cyclical companies with significant cash flow in areas such as aerospace and energy. We continue to find attractive dividend opportunities across the globe. In our view, many non-U.S. companies offer relatively appealing valuations, strong dividend culture and potential currency-related benefits, especially if dollar strength starts to wane.

Given the scope of many different economic and market-related crosscurrents, we believe Capital Income Builder’s focus on income has the potential to benefit investors, especially in light of its emphasis on companies that can adapt and continue to provide sustainable dividend growth in an uncertain environment. We expect that the fund’s focus on high-quality, lower-risk bonds should also offer further stability through volatile periods.

We would like to thank you for your continued support and look forward to reporting to you again in six months.

Sincerely,

David A. Hoag

Co-President

Winnie Kwan

Co-President

Steven T. Watson

Co-President

December 8, 2022

For current information about the fund, visit capitalgroup.com.

| * | Source: Capital/S&P Dow Jones indexes. Dividends constituted 4.2% of the S&P 500’s total return from January 1, 1970, to December 31, 1979, while capital appreciation made up 1.7%. From January 1, 1926, to September 30, 2022, dividends constituted 3.8% of the S&P 500’s total return, while capital appreciation made up 6.2%. |

| | |

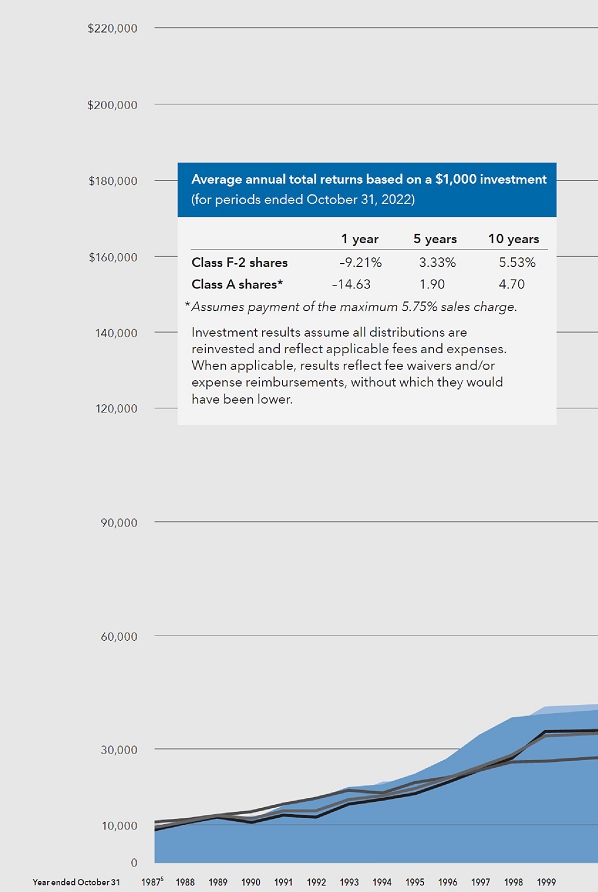

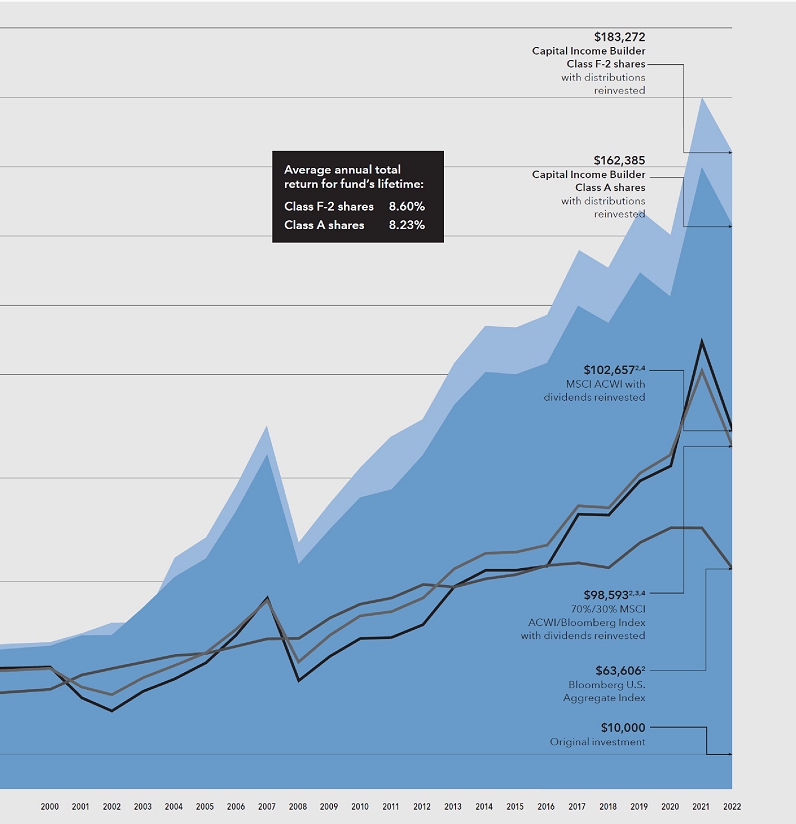

The value of a long-term perspective

Fund results shown are for Class F-2 and Class A shares. Class A share results reflect deduction of the maximum sales charge of 5.75% on the $10,000 investment1; thus, the net amount invested was $9,425. Results are for past periods and are not predictive of results for future periods. Prices and returns will vary, so investors may lose money. For current information and month-end results, visit capitalgroup.com.

The results shown are before taxes on fund distributions and sale of fund shares. Class F-2 shares were first offered on August 1, 2008. Class F-2 share results prior to the date of first sale are hypothetical based on the results of the original share class of the fund without a sales charge, adjusted for typical estimated expenses. Visit capitalgroup.com for more information on specific expense adjustments and the actual dates of first sale.

| 1 | As outlined in the prospectus, the sales charge is reduced for accounts (and aggregated investments) of $25,000 or more and is eliminated for purchases of $1 million or more. There is no sales charge on dividends or capital gain distributions that are reinvested in additional shares. |

| 2 | The market index is unmanaged and, therefore, has no expenses. Investors cannot invest directly in an index. There have been periods when the fund has lagged the index. |

| 3 | The 70%/30% MSCI ACWI/Bloomberg Index blends the MSCI ACWI (All Country World Index) with the Bloomberg U.S. Aggregate Index by weighting their total returns at 70% and 30%, respectively. Results assume the blend is rebalanced monthly. |

| 4 | From July 30, 1987, through December 31, 1987, the MSCI World Index was used because the MSCI ACWI did not exist. MSCI World Index results reflect dividends net of withholding taxes, and MSCI ACWI results reflect dividends gross of withholding taxes through December 31, 2000, and dividends net of withholding taxes thereafter. |

| 5 | For the period July 30, 1987, commencement of operations, through October 31, 1987. |

How a hypothetical $10,000 investment has grown

There have always been reasons not to invest. If you look beyond the negative headlines, however, you will find that despite occasional stumbles, financial markets have tended to reward investors over the long term. As the chart below shows, over its lifetime Capital Income Builder has done demonstrably better than its primary benchmark. Dividends, particularly when reinvested, have accounted for a large portion of the fund’s overall results.

Investment portfolio October 31, 2022

| Sector diversification | Percent of net assets |

| Country diversification by domicile | | Percent of

net assets |

| United States | | | 66.30 | % |

| Eurozone* | | | 6.14 | |

| United Kingdom | | | 6.07 | |

| Canada | | | 4.01 | |

| Switzerland | | | 3.55 | |

| India | | | 1.30 | |

| Brazil | | | 1.10 | |

| Singapore | | | 1.06 | |

| Hong Kong | | | .98 | |

| Other countries | | | 5.42 | |

| Short-term securities & other assets less liabilities | | | 4.07 | |

| * | Countries using the euro as a common currency; those represented in the fund’s portfolio are Belgium, Finland, France, Germany, Greece, Ireland, Italy, Luxembourg, the Netherlands, Portugal and Spain. |

| Common stocks 73.35% | | Shares | | | Value

(000) | |

| Financials 13.29% | | | | | | | | |

| Zurich Insurance Group AG | | | 3,525,191 | | | $ | 1,504,283 | |

| Toronto-Dominion Bank (CAD denominated) | | | 14,222,612 | | | | 910,243 | |

| JPMorgan Chase & Co. | | | 6,041,003 | | | | 760,441 | |

| PNC Financial Services Group, Inc. | | | 4,332,697 | | | | 701,160 | |

| CME Group, Inc., Class A | | | 4,003,180 | | | | 693,751 | |

| DBS Group Holdings, Ltd. | | | 26,771,329 | | | | 646,778 | |

| Morgan Stanley | | | 7,838,387 | | | | 644,080 | |

| Münchener Rückversicherungs-Gesellschaft AG | | | 2,121,470 | | | | 560,615 | |

| DNB Bank ASA | | | 26,715,932 | | | | 472,842 | |

| Power Corporation of Canada, subordinate voting shares | | | 16,459,500 | | | | 408,724 | |

| BlackRock, Inc. | | | 564,743 | | | | 364,773 | |

| Principal Financial Group, Inc. | | | 3,792,800 | | | | 334,259 | |

| Webster Financial Corp. | | | 5,822,182 | | | | 315,912 | |

| American International Group, Inc. | | | 4,926,520 | | | | 280,812 | |

| B3 SA-Brasil, Bolsa, Balcao | | | 94,751,330 | | | | 275,880 | |

| Blackstone, Inc., nonvoting shares | | | 2,966,119 | | | | 270,332 | |

| Tryg A/S | | | 12,163,039 | | | | 263,221 | |

| East West Bancorp, Inc. | | | 2,668,647 | | | | 190,995 | |

| Travelers Companies, Inc. | | | 1,001,700 | | | | 184,774 | |

| Ping An Insurance (Group) Company of China, Ltd., Class H | | | 40,046,667 | | | | 160,194 | |

| Ping An Insurance (Group) Company of China, Ltd., Class A | | | 2,804,884 | | | | 13,892 | |

| AIA Group, Ltd. | | | 22,469,800 | | | | 170,177 | |

| State Street Corp. | | | 2,268,303 | | | | 167,854 | |

| Kaspi.kz JSC1 | | | 2,447,140 | | | | 160,288 | |

| KBC Groep NV | | | 2,979,119 | | | | 149,267 | |

| Citizens Financial Group, Inc. | | | 3,587,962 | | | | 146,748 | |

| National Bank of Canada | | | 2,053,000 | | | | 139,785 | |

| OneMain Holdings, Inc. | | | 3,542,856 | | | | 136,612 | |

| ING Groep NV | | | 13,717,920 | | | | 134,944 | |

| Wells Fargo & Company | | | 2,556,514 | | | | 117,574 | |

| Swedbank AB, Class A | | | 7,814,300 | | | | 116,529 | |

| KeyCorp | | | 6,498,537 | | | | 116,129 | |

| China Pacific Insurance (Group) Co., Ltd., Class H | | | 69,619,612 | | | | 112,283 | |

| Corebridge Financial, Inc.2 | | | 4,000,000 | | | | 90,680 | |

| Truist Financial Corp. | | | 2,020,500 | | | | 90,498 | |

| Franklin Resources, Inc. | | | 3,799,500 | | | | 89,098 | |

| EFG International AG | | | 10,030,543 | | | | 82,140 | |

| BNP Paribas SA | | | 1,607,000 | | | | 75,428 | |

| TPG, Inc., Class A2 | | | 2,401,693 | | | | 73,852 | |

| Bank Central Asia Tbk PT | | | 128,165,200 | | | | 72,310 | |

| Great-West Lifeco, Inc.2 | | | 3,060,000 | | | | 70,843 | |

| Citigroup, Inc. | | | 1,460,000 | | | | 66,956 | |

| Hang Seng Bank, Ltd. | | | 4,630,800 | | | | 65,188 | |

| Common stocks (continued) | | Shares | | | Value

(000) | |

| Financials (continued) | | | | | | | | |

| Euronext NV | | | 999,658 | | | $ | 63,523 | |

| Patria Investments, Ltd., Class A3 | | | 4,432,700 | | | | 63,033 | |

| Banco Santander, SA | | | 18,170,300 | | | | 47,083 | |

| Cullen/Frost Bankers, Inc. | | | 297,924 | | | | 46,193 | |

| Hong Kong Exchanges and Clearing, Ltd. | | | 1,619,200 | | | | 43,112 | |

| Vontobel Holding AG | | | 722,067 | | | | 40,670 | |

| Macquarie Group, Ltd. | | | 349,591 | | | | 37,903 | |

| China Merchants Bank Co., Ltd., Class H | | | 8,228,000 | | | | 27,044 | |

| SouthState Corp. | | | 214,206 | | | | 19,371 | |

| IIFL Wealth Management, Ltd. | | | 760,130 | | | | 16,266 | |

| UniCredit SpA | | | 1,105,058 | | | | 13,703 | |

| Jonah Energy Parent, LLC4 | | | 1,631 | | | | 81 | |

| Moscow Exchange MICEX-RTS PJSC4,5 | | | 85,235,374 | | | | — | 6 |

| Sberbank of Russia PJSC4,5,7 | | | 19,327,472 | | | | — | 6 |

| | | | | | | | 12,821,126 | |

| | | | | | | | | |

| Consumer staples 10.27% | | | | | | | | |

| Philip Morris International, Inc. | | | 23,047,508 | | | | 2,116,914 | |

| British American Tobacco PLC | | | 36,080,352 | | | | 1,420,678 | |

| British American Tobacco PLC (ADR) | | | 5,339,964 | | | | 211,569 | |

| Nestlé SA | | | 7,926,274 | | | | 863,116 | |

| PepsiCo, Inc. | | | 4,360,157 | | | | 791,717 | |

| General Mills, Inc. | | | 9,602,257 | | | | 783,352 | |

| Altria Group, Inc. | | | 16,618,974 | | | | 768,960 | |

| Imperial Brands PLC | | | 18,410,813 | | | | 448,451 | |

| Kimberly-Clark Corp. | | | 3,457,945 | | | | 430,376 | |

| ITC, Ltd. | | | 100,224,616 | | | | 422,196 | |

| Unilever PLC (GBP denominated) | | | 5,086,840 | | | | 231,856 | |

| Carlsberg A/S, Class B | | | 1,849,873 | | | | 218,028 | |

| Danone SA | | | 4,292,863 | | | | 213,564 | |

| Keurig Dr Pepper, Inc. | | | 5,079,438 | | | | 197,285 | |

| Anheuser-Busch InBev SA/NV | | | 3,286,679 | | | | 164,352 | |

| Kraft Heinz Company | | | 2,880,637 | | | | 110,818 | |

| Procter & Gamble Company | | | 671,222 | | | | 90,393 | |

| Mondelez International, Inc. | | | 1,289,056 | | | | 79,251 | |

| Vector Group, Ltd. | | | 6,328,252 | | | | 67,206 | |

| Seven & i Holdings Co., Ltd. | | | 1,730,200 | | | | 64,626 | |

| Viscofan, SA, non-registered shares | | | 779,691 | | | | 46,424 | |

| Reckitt Benckiser Group PLC | | | 602,632 | | | | 39,946 | |

| Scandinavian Tobacco Group A/S | | | 2,058,240 | | | | 34,503 | |

| Wuliangye Yibin Co., Ltd., Class A | | | 1,569,956 | | | | 28,716 | |

| Hilton Food Group PLC | | | 2,800,821 | | | | 19,593 | |

| Kimberly-Clark de México, SAB de CV, ordinary participation certificates, Class A | | 12,310,685 | | | | 19,423 | |

| Coca-Cola HBC AG (CDI) | | | 636,500 | | | | 13,887 | |

| Haleon PLC5 | | | 3,284,000 | | | | 10,093 | |

| | | | | | | | 9,907,293 | |

| | | | | | | | | |

| Health care 9.42% | | | | | | | | |

| AbbVie, Inc. | | | 15,298,693 | | | | 2,239,729 | |

| Amgen, Inc. | | | 4,741,895 | | | | 1,281,971 | |

| Gilead Sciences, Inc. | | | 13,892,977 | | | | 1,090,043 | |

| Medtronic PLC | | | 7,216,561 | | | | 630,294 | |

| AstraZeneca PLC | | | 5,314,855 | | | | 624,989 | |

| Abbott Laboratories | | | 5,862,665 | | | | 580,052 | |

| Novartis AG | | | 6,628,923 | | | | 535,557 | |

| Bristol-Myers Squibb Company | | | 6,563,686 | | | | 508,489 | |

| Pfizer, Inc. | | | 7,911,544 | | | | 368,282 | |

| UnitedHealth Group, Inc. | | | 614,542 | | | | 341,163 | |

| Roche Holding AG, nonvoting non-registered shares | | | 888,794 | | | | 295,170 | |

| GSK PLC | | | 11,330,890 | | | | 185,662 | |

| Royalty Pharma PLC, Class A | | | 3,759,287 | | | | 159,093 | |

| Merck & Co., Inc. | | | 702,500 | | | | 71,093 | |

| CVS Health Corp. | | | 669,922 | | | | 63,442 | |

| EBOS Group, Ltd. | | | 2,658,446 | | | | 57,961 | |

| Bayer AG | | | 1,072,107 | | | | 56,387 | |

| Koninklijke Philips NV (EUR denominated) | | | 310,789 | | | | 3,937 | |

| Organon & Co. | | | 70,250 | | | | 1,839 | |

| | | | | | | | 9,095,153 | |

| Common stocks (continued) | | Shares | | | Value

(000) | |

| Information technology 6.98% | | | | | | | | |

| Broadcom, Inc. | | | 5,841,109 | | | $ | 2,746,023 | |

| Microsoft Corp. | | | 6,287,744 | | | | 1,459,574 | |

| Taiwan Semiconductor Manufacturing Company, Ltd. | | | 51,783,456 | | | | 626,753 | |

| Automatic Data Processing, Inc. | | | 883,400 | | | | 213,518 | |

| Texas Instruments, Inc. | | | 1,198,011 | | | | 192,437 | |

| Paychex, Inc. | | | 1,520,436 | | | | 179,883 | |

| Apple, Inc. | | | 1,163,450 | | | | 178,403 | |

| KLA Corp. | | | 430,103 | | | | 136,106 | |

| NetApp, Inc. | | | 1,815,150 | | | | 125,736 | |

| QUALCOMM, Inc. | | | 1,015,727 | | | | 119,510 | |

| Vanguard International Semiconductor Corp. | | | 54,804,249 | | | | 112,934 | |

| SAP SE | | | 880,449 | | | | 84,983 | |

| Tokyo Electron, Ltd. | | | 314,000 | | | | 83,391 | |

| GlobalWafers Co., Ltd. | | | 7,363,753 | | | | 81,927 | |

| Western Union Company | | | 6,010,700 | | | | 81,205 | |

| Analog Devices, Inc. | | | 418,785 | | | | 59,727 | |

| MediaTek, Inc. | | | 2,989,467 | | | | 54,738 | |

| Intel Corp. | | | 1,604,123 | | | | 45,605 | |

| Fidelity National Information Services, Inc. | | | 529,032 | | | | 43,904 | |

| Tripod Technology Corp. | | | 12,630,424 | | | | 34,964 | |

| International Business Machines Corp. | | | 227,619 | | | | 31,477 | |

| SINBON Electronics Co., Ltd. | | | 3,987,072 | | | | 30,996 | |

| BE Semiconductor Industries NV | | | 326,200 | | | | 16,673 | |

| | | | | | | | 6,740,467 | |

| | | | | | | | | |

| Industrials 6.83% | | | | | | | | |

| Raytheon Technologies Corp. | | | 20,758,595 | | | | 1,968,330 | |

| Lockheed Martin Corp. | | | 1,167,324 | | | | 568,113 | |

| BAE Systems PLC | | | 48,702,793 | | | | 454,862 | |

| Honeywell International, Inc. | | | 2,195,550 | | | | 447,936 | |

| RELX PLC | | | 11,642,336 | | | | 312,557 | |

| RELX PLC (ADR) | | | 759,134 | | | | 20,466 | |

| L3Harris Technologies, Inc. | | | 1,233,957 | | | | 304,133 | |

| Siemens AG | | | 2,500,430 | | | | 273,397 | |

| Kone OYJ, Class B | | | 6,371,100 | | | | 260,979 | |

| Trinity Industries, Inc.3 | | | 7,712,016 | | | | 220,024 | |

| Deutsche Post AG | | | 5,658,237 | | | | 200,800 | |

| VINCI SA | | | 2,097,947 | | | | 193,190 | |

| Singapore Technologies Engineering, Ltd. | | | 74,142,756 | | | | 172,839 | |

| Illinois Tool Works, Inc. | | | 650,000 | | | | 138,794 | |

| BOC Aviation, Ltd. | | | 16,978,156 | | | | 113,661 | |

| Grupo Aeroportuario del Pacífico, SAB de CV, Class B | | | 6,602,714 | | | | 102,275 | |

| Trelleborg AB, Class B | | | 4,230,000 | | | | 93,211 | |

| Ventia Services Group Pty, Ltd.3 | | | 48,847,735 | | | | 86,550 | |

| Norfolk Southern Corp. | | | 342,215 | | | | 78,049 | |

| LIXIL Corp. | | | 4,771,900 | | | | 72,239 | |

| United Parcel Service, Inc., Class B | | | 396,000 | | | | 66,437 | |

| Compañia de Distribución Integral Logista Holdings, SA, non-registered shares | | | 3,048,755 | | | | 63,091 | |

| Waste Management, Inc. | | | 382,611 | | | | 60,594 | |

| General Dynamics Corp. | | | 224,400 | | | | 56,055 | |

| ITOCHU Corp. | | | 1,951,900 | | | | 50,525 | |

| Marubeni Corp. | | | 5,050,000 | | | | 44,253 | |

| Carrier Global Corp. | | | 1,081,344 | | | | 42,994 | |

| CCR SA, ordinary nominative shares | | | 14,116,678 | | | | 35,418 | |

| Airbus SE, non-registered shares | | | 319,385 | | | | 34,587 | |

| AB Volvo, Class B | | | 1,935,186 | | | | 31,689 | |

| Sulzer AG | | | 374,355 | | | | 24,955 | |

| | | | | | | | 6,593,003 | |

| | | | | | | | | |

| Utilities 6.34% | | | | | | | | |

| Dominion Energy, Inc. | | | 11,728,074 | | | | 820,613 | |

| DTE Energy Company | | | 4,849,200 | | | | 543,644 | |

| Power Grid Corporation of India, Ltd. | | | 179,406,466 | | | | 494,477 | |

| National Grid PLC | | | 41,878,261 | | | | 455,479 | |

| Iberdrola, SA, non-registered shares | | | 41,961,778 | | | | 426,091 | |

| E.ON SE | | | 47,693,266 | | | | 399,498 | |

| The Southern Co. | | | 5,832,500 | | | | 381,912 | |

| Engie SA | | | 22,511,806 | | | | 292,641 | |

| Common stocks (continued) | | Shares | | | Value

(000) | |

| Utilities (continued) | | | | | | | | |

| ENGIE SA, bonus dividend | | | 3,818,624 | | | $ | 49,640 | |

| Edison International | | | 5,359,531 | | | | 321,786 | |

| AES Corp. | | | 9,541,613 | | | | 249,609 | |

| Entergy Corp. | | | 2,209,425 | | | | 236,718 | |

| Evergy, Inc. | | | 3,750,568 | | | | 229,272 | |

| Duke Energy Corp. | | | 2,412,000 | | | | 224,750 | |

| Public Service Enterprise Group, Inc. | | | 2,527,930 | | | | 141,741 | |

| Sempra Energy | | | 875,819 | | | | 132,196 | |

| CenterPoint Energy, Inc. | | | 4,465,549 | | | | 127,759 | |

| Exelon Corp. | | | 3,270,868 | | | | 126,223 | |

| Enel SpA | | | 27,463,619 | | | | 122,650 | |

| SSE PLC | | | 6,716,533 | | | | 119,851 | |

| NextEra Energy, Inc. | | | 1,226,469 | | | | 95,051 | |

| ENN Energy Holdings, Ltd. | | | 5,081,900 | | | | 50,530 | |

| Power Assets Holdings, Ltd. | | | 9,434,000 | | | | 45,129 | |

| CMS Energy Corp. | | | 352,820 | | | | 20,129 | |

| American Electric Power Company, Inc. | | | 120,522 | | | | 10,596 | |

| | | | | | | | 6,117,985 | |

| | | | | | | | | |

| Energy 6.32% | | | | | | | | |

| Canadian Natural Resources, Ltd. (CAD denominated)2 | | | 15,064,682 | | | | 903,538 | |

| TC Energy Corp. (CAD denominated) | | | 16,592,645 | | | | 728,817 | |

| TC Energy Corp. | | | 1,387,400 | | | | 60,935 | |

| Chevron Corp. | | | 4,200,335 | | | | 759,841 | |

| Exxon Mobil Corp. | | | 5,570,288 | | | | 617,244 | |

| TotalEnergies SE | | | 7,980,721 | | | | 434,571 | |

| EOG Resources, Inc. | | | 3,127,408 | | | | 426,954 | |

| BP PLC | | | 70,864,879 | | | | 389,923 | |

| Shell PLC (GBP denominated) | | | 10,113,335 | | | | 278,815 | |

| Shell PLC (ADR) | | | 738,100 | | | | 41,061 | |

| ConocoPhillips | | | 2,289,004 | | | | 288,620 | |

| Pioneer Natural Resources Company | | | 909,940 | | | | 233,318 | |

| Woodside Energy Group, Ltd. | | | 7,591,011 | | | | 174,704 | |

| Woodside Energy Group, Ltd. (CDI) | | | 2,125,736 | | | | 49,146 | |

| Enbridge, Inc. (CAD denominated)2 | | | 4,457,700 | | | | 173,681 | |

| Schlumberger, Ltd. | | | 3,258,133 | | | | 169,521 | |

| Equitrans Midstream Corp. | | | 18,872,981 | | | | 158,910 | |

| Baker Hughes Co., Class A | | | 4,650,800 | | | | 128,641 | |

| DT Midstream, Inc. | | | 1,195,562 | | | | 71,375 | |

| Galp Energia, SGPS, SA, Class B | | | 1,006,588 | | | | 10,221 | |

| Constellation Oil Services Holding SA, Class B-14,5 | | | 282,550 | | | | — | 6 |

| Gazprom PJSC4,7 | | | 84,735,990 | | | | — | 6 |

| | | | | | | | 6,099,836 | |

| | | | | | | | | |

| Real estate 6.01% | | | | | | | | |

| VICI Properties, Inc. REIT3 | | | 52,658,330 | | | | 1,686,120 | |

| Crown Castle, Inc. REIT | | | 11,951,934 | | | | 1,592,715 | |

| Equinix, Inc. REIT | | | 823,841 | | | | 466,656 | |

| Gaming and Leisure Properties, Inc. REIT | | | 8,273,693 | | | | 414,677 | |

| Federal Realty Investment Trust REIT | | | 2,500,000 | | | | 247,450 | |

| Link REIT | | | 32,738,146 | | | | 193,518 | |

| American Tower Corp. REIT | | | 869,676 | | | | 180,188 | |

| CK Asset Holdings, Ltd. | | | 28,272,934 | | | | 156,318 | |

| Charter Hall Group REIT | | | 13,076,087 | | | | 108,232 | |

| POWERGRID Infrastructure Investment Trust3 | | | 59,148,100 | | | | 98,707 | |

| Mindspace Business Parks REIT | | | 21,491,600 | | | | 92,242 | |

| Extra Space Storage, Inc. REIT | | | 513,464 | | | | 91,109 | |

| Embassy Office Parks REIT | | | 21,328,000 | | | | 88,731 | |

| Americold Realty Trust, Inc. REIT | | | 2,701,312 | | | | 65,507 | |

| CTP NV | | | 6,006,045 | | | | 62,322 | |

| Digital Realty Trust, Inc. REIT | | | 610,751 | | | | 61,228 | |

| Kimco Realty Corp. REIT | | | 2,819,000 | | | | 60,270 | |

| Sun Hung Kai Properties, Ltd. | | | 5,568,353 | | | | 59,907 | |

| Longfor Group Holdings, Ltd. | | | 25,875,500 | | | | 32,964 | |

| CubeSmart REIT | | | 727,081 | | | | 30,443 | |

| Douglas Elliman, Inc. | | | 2,245,900 | | | | 10,376 | |

| TAG Immobilien AG | | | 658,445 | | | | 4,129 | |

| | | | | | | | 5,803,809 | |

| Common stocks (continued) | | Shares | | | Value

(000) | |

| Consumer discretionary 2.71% | | | | | | | | |

| McDonald’s Corp. | | | 1,815,766 | | | $ | 495,087 | |

| Home Depot, Inc. | | | 1,138,335 | | | | 337,095 | |

| Starbucks Corp. | | | 3,619,300 | | | | 313,395 | |

| Industria de Diseño Textil, SA | | | 13,201,427 | | | | 299,282 | |

| Kering SA | | | 495,863 | | | | 227,230 | |

| Midea Group Co., Ltd., Class A | | | 35,149,235 | | | | 193,502 | |

| LVMH Moët Hennessy-Louis Vuitton SE | | | 251,902 | | | | 159,074 | |

| YUM! Brands, Inc. | | | 902,600 | | | | 106,733 | |

| Darden Restaurants, Inc. | | | 623,503 | | | | 89,248 | |

| Restaurant Brands International, Inc. | | | 1,393,243 | | | | 82,731 | |

| Galaxy Entertainment Group, Ltd. | | | 17,447,000 | | | | 79,682 | |

| Cie. Financière Richemont SA, Class A | | | 687,066 | | | | 67,201 | |

| Hasbro, Inc. | | | 663,260 | | | | 43,278 | |

| OPAP SA | | | 2,405,363 | | | | 29,476 | |

| Mercedes-Benz Group AG | | | 494,395 | | | | 28,631 | |

| Inchcape PLC | | | 2,546,035 | | | | 21,723 | |

| Kindred Group PLC (SDR) | | | 1,933,000 | | | | 16,807 | |

| Thule Group AB | | | 828,459 | | | | 16,327 | |

| VF Corp. | | | 397,691 | | | | 11,235 | |

| | | | | | | | 2,617,737 | |

| | | | | | | | | |

| Communication services 2.71% | | | | | | | | |

| Comcast Corp., Class A | | | 19,657,649 | | | | 623,934 | |

| Verizon Communications, Inc. | | | 10,020,406 | | | | 374,463 | |

| SoftBank Corp. | | | 33,512,558 | | | | 330,291 | |

| BCE, Inc. | | | 5,561,882 | | | | 250,874 | |

| Koninklijke KPN NV | | | 81,065,231 | | | | 226,799 | |

| Singapore Telecommunications, Ltd. | | | 117,092,300 | | | | 206,789 | |

| Nippon Telegraph and Telephone Corp. | | | 6,654,900 | | | | 183,228 | |

| HKT Trust and HKT, Ltd., units | | | 100,055,060 | | | | 113,061 | |

| Warner Music Group Corp., Class A | | | 2,928,864 | | | | 76,209 | |

| Omnicom Group, Inc. | | | 931,500 | | | | 67,767 | |

| WPP PLC | | | 7,309,271 | | | | 64,208 | |

| Indus Towers, Ltd. | | | 18,916,173 | | | | 42,390 | |

| Pearson PLC | | | 2,478,885 | | | | 27,302 | |

| ProSiebenSat.1 Media SE | | | 3,562,000 | | | | 24,219 | |

| | | | | | | | 2,611,534 | |

| | | | | | | | | |

| Materials 2.47% | | | | | | | | |

| Vale SA (ADR), ordinary nominative shares | | | 30,925,978 | | | | 400,182 | |

| Vale SA, ordinary nominative shares | | | 19,740,969 | | | | 256,551 | |

| Rio Tinto PLC | | | 7,048,863 | | | | 366,755 | |

| Linde PLC | | | 781,484 | | | | 232,374 | |

| Air Products and Chemicals, Inc. | | | 855,988 | | | | 214,339 | |

| BHP Group, Ltd. (CDI) | | | 7,292,000 | | | | 173,647 | |

| International Flavors & Fragrances, Inc. | | | 1,645,521 | | | | 160,619 | |

| LyondellBasell Industries NV | | | 1,630,155 | | | | 124,625 | |

| Evonik Industries AG | | | 4,821,154 | | | | 88,882 | |

| Sociedad Química y Minera de Chile SA, Class B (ADR) | | | 936,668 | | | | 87,747 | |

| BASF SE | | | 1,925,521 | | | | 86,458 | |

| UPM-Kymmene OYJ | | | 1,677,885 | | | | 56,229 | |

| Asahi Kasei Corp. | | | 8,589,800 | | | | 55,140 | |

| Nexa Resources SA | | | 4,624,901 | | | | 23,217 | |

| WestRock Co. | | | 662,600 | | | | 22,568 | |

| Shin-Etsu Chemical Co., Ltd. | | | 178,600 | | | | 18,665 | |

| Fortescue Metals Group, Ltd. | | | 1,982,847 | | | | 18,644 | |

| | | | | | | | 2,386,642 | |

| | | | | | | | | |

| Total common stocks (cost: $58,698,846,000) | | | | | | | 70,794,585 | |

| | | | | | | | | |

| Preferred securities 0.06% | | | | | | | | |

| Information technology 0.05% | | | | | | | | |

| Samsung Electronics Co., Ltd., nonvoting preferred shares | | | 1,163,110 | | | | 43,521 | |

| Preferred securities (continued) | | Shares | | | Value

(000) | |

| Financials 0.01% | | | | | | | | |

| CoBank, ACB, Class E, 5.006% noncumulative preferred shares1,8 | | | 13,000 | | | $ | 10,368 | |

| | | | | | | | | |

| Total preferred securities (cost: $50,246,000) | | | | | | | 53,889 | |

| | | | | | | | | |

| Rights & warrants 0.00% | | | | | | | | |

| Consumer discretionary 0.00% | | | | | | | | |

| Compagnie Financière Richemont SA, Class A, warrants, expire 11/22/20235 | | | 684,470 | | | | 335 | |

| | | | | | | | | |

| Total rights & warrants (cost: $0) | | | | | | | 335 | |

| | | | | | | | | |

| Convertible stocks 0.48% | | | | | | | | |

| Utilities 0.30% | | | | | | | | |

| NextEra Energy, Inc., noncumulative convertible preferred units, 6.926% 9/1/2025 | | | 3,206,400 | | | | 149,098 | |

| AES Corp., convertible preferred units, 6.875% 2/15/2024 | | | 913,000 | | | | 89,940 | |

| American Electric Power Company, Inc., convertible preferred units, 6.125% 8/15/20232 | | | 938,000 | | | | 46,637 | |

| | | | | | | | 285,675 | |

| | | | | | | | | |

| Health care 0.11% | | | | | | | | |

| Danaher Corp., Series B, cumulative convertible preferred shares, 5.00% 4/15/20232 | | | 84,600 | | | | 110,696 | |

| | | | | | | | | |

| Consumer discretionary 0.07% | | | | | | | | |

| Aptiv PLC, Series A, convertible preferred shares, 5.50% 6/15/2023 | | | 623,573 | | | | 66,647 | |

| | | | | | | | | |

| Total convertible stocks (cost: $445,466,000) | | | | | | | 463,018 | |

| | | | | | | | | |

| Investment funds 2.49% | | | | | | | | |

| Capital Group Central Corporate Bond Fund3 | | | 305,300,361 | | | | 2,402,714 | |

| | | | | | | | | |

| Total investment funds (cost: $3,076,443,000) | | | | | | | 2,402,714 | |

| | | | | | | | | |

| Bonds, notes & other debt instruments 19.55% | | Principal amount

(000) | | | | | |

| U.S. Treasury bonds & notes 8.87% | | | | | | | | |

| U.S. Treasury 5.90% | | | | | | | | |

| U.S. Treasury 7.625% 11/15/2022 | | USD | 39,700 | | | | 39,764 | |

| U.S. Treasury 7.125% 2/15/2023 | | | 299,800 | | | | 302,333 | |

| U.S. Treasury 6.25% 8/15/2023 | | | 350,000 | | | | 354,607 | |

| U.S. Treasury 2.25% 3/31/2024 | | | 300,000 | | | | 290,227 | |

| U.S. Treasury 3.25% 8/31/2024 | | | 49,842 | | | | 48,717 | |

| U.S. Treasury 4.25% 9/30/2024 | | | 858 | | | | 854 | |

| U.S. Treasury 7.50% 11/15/20249 | | | 331,275 | | | | 350,374 | |

| U.S. Treasury 7.625% 2/15/2025 | | | 250,000 | | | | 266,697 | |

| U.S. Treasury 2.875% 7/31/2025 | | | 100,000 | | | | 95,995 | |

| U.S. Treasury 6.875% 8/15/2025 | | | 145,145 | | | | 154,148 | |

| U.S. Treasury 6.00% 2/15/2026 | | | 206,000 | | | | 215,431 | |

| U.S. Treasury 6.75% 8/15/2026 | | | 35,000 | | | | 37,914 | |

| U.S. Treasury 6.50% 11/15/2026 | | | 178,000 | | | | 192,091 | |

| U.S. Treasury 2.25% 2/15/2027 | | | 75 | | | | 69 | |

| U.S. Treasury 6.625% 2/15/2027 | | | 65,000 | | | | 70,712 | |

| U.S. Treasury 2.50% 3/31/2027 | | | 136,000 | | | | 126,259 | |

| U.S. Treasury 2.75% 7/31/2027 | | | 475,000 | | | | 444,292 | |

| U.S. Treasury 6.375% 8/15/2027 | | | 85,000 | | | | 92,476 | |

| U.S. Treasury 4.125% 10/31/2027 | | | 952 | | | | 948 | |

| U.S. Treasury 6.125% 11/15/20279 | | | 499,614 | | | | 540,324 | |

| U.S. Treasury 2.875% 8/15/2028 | | | 160,000 | | | | 148,740 | |

| U.S. Treasury 5.50% 8/15/2028 | | | 140,000 | | | | 148,628 | |

| U.S. Treasury 5.25% 11/15/2028 | | | 89,000 | | | | 93,414 | |

| U.S. Treasury 5.25% 2/15/2029 | | | 25,000 | | | | 26,306 | |

| U.S. Treasury 6.125% 8/15/2029 | | | 30,000 | | | | 33,333 | |

| U.S. Treasury 6.25% 5/15/2030 | | | 274,563 | | | | 310,970 | |

| U.S. Treasury 1.875% 2/15/2032 | | | 195,000 | | | | 162,394 | |

| U.S. Treasury 2.875% 5/15/2032 | | | 300,000 | | | | 272,203 | |

| U.S. Treasury 2.75% 8/15/2032 | | | 1,151 | | | | 1,031 | |

| Bonds, notes & other debt instruments (continued) | | Principal amount

(000) | | | Value

(000) | |

| U.S. Treasury bonds & notes (continued) | | | | | | | | |

| U.S. Treasury (continued) | | | | | | | | |

| U.S. Treasury 1.125% 5/15/20409 | | USD | 228,288 | | | $ | 136,871 | |

| U.S. Treasury 2.50% 2/15/2046 | | | 29,300 | | | | 21,056 | |

| U.S. Treasury 2.875% 11/15/2046 | | | 20,300 | | | | 15,692 | |

| U.S. Treasury 3.00% 5/15/2047 | | | 116,000 | | | | 91,746 | |

| U.S. Treasury 3.00% 2/15/20499 | | | 228,388 | | | | 183,256 | |

| U.S. Treasury 2.875% 5/15/2049 | | | 41,800 | | | | 32,717 | |

| U.S. Treasury 1.375% 8/15/2050 | | | 40,000 | | | | 21,439 | |

| U.S. Treasury 2.00% 8/15/2051 | | | 40,000 | | | | 25,330 | |

| U.S. Treasury 1.875% 11/15/2051 | | | 58,498 | | | | 35,815 | |

| U.S. Treasury 2.25% 2/15/20529 | | | 220,000 | | | | 148,257 | |

| U.S. Treasury 2.875% 5/15/2052 | | | 2,249 | | | | 1,753 | |

| U.S. Treasury 3.00% 8/15/20529 | | | 200,000 | | | | 160,787 | |

| | | | | | | | 5,695,970 | |

| | | | | | | | | |

| U.S. Treasury inflation-protected securities 2.97% | | | | | | | | |

| U.S. Treasury Inflation-Protected Security 0.125% 1/15/202310 | | | 275,640 | | | | 275,023 | |

| U.S. Treasury Inflation-Protected Security 0.625% 4/15/202310 | | | 319,953 | | | | 317,904 | |

| U.S. Treasury Inflation-Protected Security 0.375% 7/15/202310 | | | 239,587 | | | | 237,632 | |

| U.S. Treasury Inflation-Protected Security 0.625% 1/15/202410 | | | 306,081 | | | | 301,297 | |

| U.S. Treasury Inflation-Protected Security 0.50% 4/15/202410 | | | 149,188 | | | | 146,156 | |

| U.S. Treasury Inflation-Protected Security 0.125% 7/15/202410 | | | 602,434 | | | | 587,393 | |

| U.S. Treasury Inflation-Protected Security 0.125% 10/15/202410 | | | 247,702 | | | | 240,540 | |

| U.S. Treasury Inflation-Protected Security 0.25% 1/15/202510 | | | 52,589 | | | | 50,816 | |

| U.S. Treasury Inflation-Protected Security 0.125% 4/15/202610 | | | 225,759 | | | | 213,189 | |

| U.S. Treasury Inflation-Protected Security 0.50% 1/15/202810 | | | 150,089 | | | | 141,442 | |

| U.S. Treasury Inflation-Protected Security 0.125% 1/15/203110 | | | 199,106 | | | | 176,542 | |

| U.S. Treasury Inflation-Protected Security 2.125% 2/15/204110 | | | 1,001 | | | | 1,051 | |

| U.S. Treasury Inflation-Protected Security 1.00% 2/15/20499,10 | | | 158,542 | | | | 131,682 | |

| U.S. Treasury Inflation-Protected Security 0.25% 2/15/205010 | | | 3,341 | | | | 2,244 | |

| U.S. Treasury Inflation-Protected Security 0.125% 2/15/205110 | | | 59,496 | | | | 38,372 | |

| | | | | | | | 2,861,283 | |

| | | | | | | | | |

| Total U.S. Treasury bonds & notes | | | | | | | 8,557,253 | |

| | | | | | | | | |

| Mortgage-backed obligations 7.15% | | | | | | | | |

| Federal agency mortgage-backed obligations 6.41% | | | | | | | | |

| BX Trust, Series 2021-ACNT, Class D, (1-month USD-LIBOR + 1.85%) 5.262% 11/15/20381,8,11 | | | 1,121 | | | | 1,056 | |

| Fannie Mae Pool #930337 6.00% 1/1/202411 | | | 1 | | | | 1 | |

| Fannie Mae Pool #AA8755 4.50% 7/1/202411 | | | 569 | | | | 565 | |

| Fannie Mae Pool #AA8211 4.50% 8/1/202411 | | | 84 | | | | 83 | |

| Fannie Mae Pool #AX9959 3.50% 12/1/202911 | | | 219 | | | | 209 | |

| Fannie Mae Pool #BA2999 3.50% 11/1/203011 | | | 247 | | | | 237 | |

| Fannie Mae Pool #683351 5.50% 2/1/203311 | | | 82 | | | | 83 | |

| Fannie Mae Pool #CA1299 3.50% 3/1/203311 | | | 101 | | | | 97 | |

| Fannie Mae Pool #MA3438 3.50% 8/1/203311 | | | 275 | | | | 261 | |

| Fannie Mae Pool #MA3658 3.50% 5/1/203411 | | | 381 | | | | 361 | |

| Fannie Mae Pool #CA4490 3.50% 8/1/203411 | | | 532 | | | | 504 | |

| Fannie Mae Pool #887695 6.00% 6/1/203611 | | | 1,122 | | | | 1,161 | |

| Fannie Mae Pool #894308 6.00% 10/1/203611 | | | 168 | | | | 170 | |

| Fannie Mae Pool #902164 6.00% 11/1/203611 | | | 1,016 | | | | 1,049 | |

| Fannie Mae Pool #902503 6.00% 11/1/203611 | | | 808 | | | | 837 | |

| Fannie Mae Pool #903076 6.00% 12/1/203611 | | | 1,405 | | | | 1,456 | |

| Fannie Mae Pool #AD0249 5.50% 4/1/203711 | | | 110 | | | | 112 | |

| Fannie Mae Pool #AS9772 3.50% 6/1/203711 | | | 35 | | | | 33 | |

| Fannie Mae Pool #966172 7.00% 7/1/203711 | | | 131 | | | | 132 | |

| Fannie Mae Pool #256845 6.50% 8/1/203711 | | | 69 | | | | 72 | |

| Fannie Mae Pool #256960 6.50% 11/1/203711 | | | 381 | | | | 402 | |

| Fannie Mae Pool #257137 7.00% 3/1/203811 | | | 23 | | | | 25 | |

| Fannie Mae Pool #963269 5.50% 5/1/203811 | | | 1,190 | | | | 1,222 | |

| Fannie Mae Pool #963341 5.50% 5/1/203811 | | | 272 | | | | 279 | |

| Fannie Mae Pool #963454 5.50% 6/1/203811 | | | 989 | | | | 1,015 | |

| Fannie Mae Pool #963796 5.50% 6/1/203811 | | | 333 | | | | 339 | |

| Fannie Mae Pool #929964 6.00% 9/1/203811 | | | 506 | | | | 523 | |

| Fannie Mae Pool #970772 5.50% 11/1/203811 | | | 48 | | | | 48 | |

| Fannie Mae Pool #AE0392 5.50% 12/1/203911 | | | 66 | | | | 67 | |

| Fannie Mae Pool #AL0152 6.00% 6/1/204011 | | | 3,625 | | | | 3,736 | |

| Fannie Mae Pool #AE8073 4.00% 12/1/204011 | | | 213 | | | | 200 | |

| Bonds, notes & other debt instruments (continued) | | Principal amount

(000) | | | Value

(000) | |

| Mortgage-backed obligations (continued) | | | | | | | | |

| Federal agency mortgage-backed obligations (continued) | | | | | | | | |

| Fannie Mae Pool #AL1571 5.00% 6/1/204111 | | USD | 3,124 | | | $ | 3,130 | |

| Fannie Mae Pool #AL0913 6.00% 7/1/204111 | | | 2,563 | | | | 2,648 | |

| Fannie Mae Pool #AJ0257 4.00% 9/1/204111 | | | 76 | | | | 71 | |

| Fannie Mae Pool #AJ4154 4.00% 11/1/204111 | | | 210 | | | | 198 | |

| Fannie Mae Pool #AB4050 4.00% 12/1/204111 | | | 410 | | | | 385 | |

| Fannie Mae Pool #AJ4189 4.00% 12/1/204111 | | | 238 | | | | 224 | |

| Fannie Mae Pool #AJ9165 4.00% 1/1/204211 | | | 5,565 | | | | 5,228 | |

| Fannie Mae Pool #890407 4.00% 2/1/204211 | | | 557 | | | | 523 | |

| Fannie Mae Pool #AL2745 4.00% 3/1/204211 | | | 1,689 | | | | 1,586 | |

| Fannie Mae Pool #AO6721 4.00% 6/1/204211 | | | 10,749 | | | | 10,097 | |

| Fannie Mae Pool #AO1820 4.00% 6/1/204211 | | | 903 | | | | 848 | |

| Fannie Mae Pool #890445 4.00% 7/1/204211 | | | 1,271 | | | | 1,194 | |

| Fannie Mae Pool #AS0831 4.50% 10/1/204311 | | | 585 | | | | 558 | |

| Fannie Mae Pool #AW4156 4.00% 5/1/204411 | | | 2,159 | | | | 2,023 | |

| Fannie Mae Pool #AW4026 4.00% 6/1/204411 | | | 2,645 | | | | 2,478 | |

| Fannie Mae Pool #AX2782 4.00% 9/1/204411 | | | 2,704 | | | | 2,530 | |

| Fannie Mae Pool #AY1313 4.00% 3/1/204511 | | | 5,096 | | | | 4,748 | |

| Fannie Mae Pool #AS6840 4.00% 3/1/204611 | | | 6,107 | | | | 5,721 | |

| Fannie Mae Pool #AL8522 3.50% 5/1/204611 | | | 944 | | | | 850 | |

| Fannie Mae Pool #BC8719 4.00% 6/1/204611 | | | 2,458 | | | | 2,301 | |

| Fannie Mae Pool #BC8720 4.00% 6/1/204611 | | | 1,779 | | | | 1,666 | |

| Fannie Mae Pool #AS7598 4.00% 7/1/204611 | | | 5,672 | | | | 5,309 | |

| Fannie Mae Pool #BD1967 4.00% 7/1/204611 | | | 1,808 | | | | 1,691 | |

| Fannie Mae Pool #BD5477 4.00% 7/1/204611 | | | 38 | | | | 36 | |

| Fannie Mae Pool #MA2691 4.50% 7/1/204611 | | | 1,084 | | | | 1,041 | |

| Fannie Mae Pool #AS7759 4.00% 8/1/204611 | | | 13,369 | | | | 12,516 | |

| Fannie Mae Pool #AS7760 4.00% 8/1/204611 | | | 5,784 | | | | 5,414 | |

| Fannie Mae Pool #AS7939 4.00% 9/1/204611 | | | 9,136 | | | | 8,552 | |

| Fannie Mae Pool #AL9190 4.00% 9/1/204611 | | | 1,497 | | | | 1,401 | |

| Fannie Mae Pool #BC4712 4.00% 10/1/204611 | | | 5,044 | | | | 4,697 | |

| Fannie Mae Pool #BC4801 4.00% 11/1/204611 | | | 3,401 | | | | 3,166 | |

| Fannie Mae Pool #MA2907 4.00% 2/1/204711 | | | 28 | | | | 27 | |

| Fannie Mae Pool #AS9313 4.00% 3/1/204711 | | | 4,688 | | | | 4,388 | |

| Fannie Mae Pool #BE3229 4.00% 3/1/204711 | | | 1,718 | | | | 1,599 | |

| Fannie Mae Pool #BD7165 4.00% 4/1/204711 | | | 28 | | | | 26 | |

| Fannie Mae Pool #AS9454 4.00% 4/1/204711 | | | 18 | | | | 17 | |

| Fannie Mae Pool #BM4187 4.50% 5/1/204711 | | | 16,386 | | | | 15,873 | |

| Fannie Mae Pool #BH2491 4.00% 6/1/204711 | | | 2,532 | | | | 2,367 | |

| Fannie Mae Pool #MA3058 4.00% 7/1/204711 | | | 3,044 | | | | 2,840 | |

| Fannie Mae Pool #CA0243 4.50% 8/1/204711 | | | 15,382 | | | | 14,714 | |

| Fannie Mae Pool #BJ1668 4.00% 12/1/204711 | | | 2,933 | | | | 2,744 | |

| Fannie Mae Pool #MA3211 4.00% 12/1/204711 | | | 555 | | | | 517 | |

| Fannie Mae Pool #BJ2751 4.50% 5/1/204811 | | | 7,997 | | | | 7,644 | |

| Fannie Mae Pool #CA2033 4.00% 7/1/204811 | | | 10,346 | | | | 9,584 | |

| Fannie Mae Pool #CA2157 4.00% 8/1/204811 | | | 21,531 | | | | 19,945 | |

| Fannie Mae Pool #BF0320 5.50% 1/1/204911 | | | 13,514 | | | | 13,954 | |

| Fannie Mae Pool #BF0572 5.50% 4/1/204911 | | | 29,819 | | | | 29,686 | |

| Fannie Mae Pool #FM2675 4.00% 6/1/204911 | | | 6,322 | | | | 5,862 | |

| Fannie Mae Pool #FM1262 4.00% 7/1/204911 | | | 18,165 | | | | 16,827 | |

| Fannie Mae Pool #BO2264 3.00% 10/1/204911 | | | 11,069 | | | | 9,493 | |

| Fannie Mae Pool #CA4819 4.00% 12/1/204911 | | | 9,057 | | | | 8,343 | |

| Fannie Mae Pool #BO6274 3.00% 1/1/205011 | | | 16,925 | | | | 14,522 | |

| Fannie Mae Pool #FM2872 3.00% 2/1/205011 | | | 38,978 | | | | 33,429 | |

| Fannie Mae Pool #CA5216 3.00% 2/1/205011 | | | 16,680 | | | | 14,363 | |

| Fannie Mae Pool #CA5226 3.00% 2/1/205011 | | | 7,089 | | | | 6,105 | |

| Fannie Mae Pool #FM2676 4.00% 3/1/205011 | | | 5,885 | | | | 5,415 | |

| Fannie Mae Pool #CA6309 3.00% 7/1/205011 | | | 34,692 | | | | 30,194 | |

| Fannie Mae Pool #FM4897 3.00% 11/1/205011 | | | 6,823 | | | | 5,929 | |

| Fannie Mae Pool #CA8046 3.00% 12/1/205011 | | | 27,283 | | | | 23,628 | |

| Fannie Mae Pool #FM9632 3.00% 11/1/205111 | | | 45,436 | | | | 38,945 | |

| Fannie Mae Pool #FM9631 3.00% 11/1/205111 | | | 19,253 | | | | 16,492 | |

| Fannie Mae Pool #CB2414 3.00% 12/1/205111 | | | 22,258 | | | | 19,172 | |

| Fannie Mae Pool #FS0972 3.50% 1/1/205211 | | | 23,335 | | | | 20,795 | |

| Fannie Mae Pool #FS0647 3.00% 2/1/205211 | | | 14,733 | | | | 12,744 | |

| Fannie Mae Pool #BF0142 5.50% 8/1/205611 | | | 38,808 | | | | 39,601 | |

| Fannie Mae Pool #BF0145 3.50% 3/1/205711 | | | 32,100 | | | | 28,681 | |

| Fannie Mae Pool #BF0339 5.00% 1/1/205911 | | | 36,985 | | | | 37,297 | |

| Bonds, notes & other debt instruments (continued) | | Principal amount

(000) | | | Value

(000) | |

| Mortgage-backed obligations (continued) | | | | | | | | |

| Federal agency mortgage-backed obligations (continued) | | | | | | | | |

| Fannie Mae Pool #BF0342 5.50% 1/1/205911 | | USD | 26,412 | | | $ | 26,755 | |

| Fannie Mae Pool #BF0379 3.50% 4/1/205911 | | | 78,726 | | | | 70,340 | |

| Fannie Mae Pool #BF0497 3.00% 7/1/206011 | | | 27,354 | | | | 23,225 | |

| Fannie Mae Pool #BF0548 3.00% 7/1/206111 | | | 21,243 | | | | 17,969 | |

| Fannie Mae, Series 2001-25, Class ZA, 6.50% 6/25/203111 | | | 190 | | | | 192 | |

| Fannie Mae, Series 2006-65, Class PF, (1-month USD-LIBOR + 0.28%) 3.866% 7/25/20368,11 | | | 572 | | | | 562 | |

| Fannie Mae, Series 2001-50, Class BA, 7.00% 10/25/204111 | | | 28 | | | | 29 | |

| Fannie Mae, Series 2002-W3, Class A5, 7.50% 11/25/204111 | | | 39 | | | | 42 | |

| Fannie Mae, Series 2017-M7, Class A2, Multi Family, 2.961% 2/25/20278,11 | | | 2,640 | | | | 2,462 | |

| Fannie Mae, Series 2006-51, Class PO, principal only, 0% 3/25/203611 | | | 301 | | | | 270 | |

| Fannie Mae, Series 2006-32, Class OA, principal only, 0% 5/25/203611 | | | 585 | | | | 476 | |

| Fannie Mae, Series 2006-56, Class OG, principal only, 0% 7/25/203611 | | | 74 | | | | 61 | |

| Fannie Mae, Series 2006-96, Class OP, principal only, 0% 10/25/203611 | | | 133 | | | | 113 | |

| Freddie Mac Pool #G13173 5.50% 5/1/202311 | | | 4 | | | | 4 | |

| Freddie Mac Pool #ZK3460 3.50% 8/1/202611 | | | 26 | | | | 25 | |

| Freddie Mac Pool #RD5008 3.50% 9/1/202911 | | | 171 | | | | 162 | |

| Freddie Mac Pool #ZS7148 3.50% 4/1/203011 | | | 9 | | | | 9 | |

| Freddie Mac Pool #V62089 3.50% 6/1/203311 | | | 285 | | | | 270 | |

| Freddie Mac Pool #ZS8716 3.50% 9/1/203311 | | | 230 | | | | 217 | |

| Freddie Mac Pool #G18723 3.50% 2/1/203411 | | | 3,715 | | | | 3,520 | |

| Freddie Mac Pool #ZT1799 3.50% 3/1/203411 | | | 535 | | | | 506 | |

| Freddie Mac Pool #QN3000 1.50% 8/1/203511 | | | 210 | | | | 179 | |

| Freddie Mac Pool #ZA2505 3.50% 5/1/203811 | | | 315 | | | | 286 | |

| Freddie Mac Pool #A76884 5.00% 5/1/203811 | | | 249 | | | | 242 | |

| Freddie Mac Pool #G04697 5.50% 9/1/203811 | | | 880 | | | | 904 | |

| Freddie Mac Pool #A87873 5.00% 8/1/203911 | | | 3,329 | | | | 3,316 | |

| Freddie Mac Pool #G06789 6.00% 5/1/204011 | | | 38 | | | | 39 | |

| Freddie Mac Pool #G06061 4.00% 10/1/204011 | | | 537 | | | | 505 | |

| Freddie Mac Pool #Q00232 4.50% 4/1/204111 | | | 4,892 | | | | 4,745 | |

| Freddie Mac Pool #Q00850 4.50% 5/1/204111 | | | 160 | | | | 155 | |

| Freddie Mac Pool #G06841 5.50% 6/1/204111 | | | 1,730 | | | | 1,778 | |

| Freddie Mac Pool #G08456 5.00% 7/1/204111 | | | 99 | | | | 96 | |

| Freddie Mac Pool #G60546 4.00% 12/1/204211 | | | 4,054 | | | | 3,814 | |

| Freddie Mac Pool #Q21442 4.50% 8/1/204311 | | | 315 | | | | 300 | |

| Freddie Mac Pool #760014 2.745% 8/1/20458,11 | | | 589 | | | | 571 | |

| Freddie Mac Pool #G60138 3.50% 8/1/204511 | | | 15,667 | | | | 14,159 | |

| Freddie Mac Pool #G60279 4.00% 10/1/204511 | | | 4,404 | | | | 4,134 | |

| Freddie Mac Pool #Q41088 4.00% 6/1/204611 | | | 10,400 | | | | 9,696 | |

| Freddie Mac Pool #Q41905 4.00% 7/1/204611 | | | 3,872 | | | | 3,609 | |

| Freddie Mac Pool #Q42626 4.00% 8/1/204611 | | | 3,896 | | | | 3,633 | |

| Freddie Mac Pool #T65389 3.50% 9/1/204611 | | | 58 | | | | 51 | |

| Freddie Mac Pool #Q44227 4.00% 9/1/204611 | | | 944 | | | | 885 | |

| Freddie Mac Pool #Q49716 4.50% 8/1/204711 | | | 350 | | | | 332 | |

| Freddie Mac Pool #ZS4735 3.50% 9/1/204711 | | | 2,866 | | | | 2,577 | |

| Freddie Mac Pool #K39018 6.50% 10/1/204711 | | | 49 | | | | 49 | |

| Freddie Mac Pool #G08793 4.00% 12/1/204711 | | | 17,669 | | | | 16,429 | |

| Freddie Mac Pool #Q52596 4.50% 12/1/204711 | | | 371 | | | | 356 | |

| Freddie Mac Pool #SI2002 4.00% 3/1/204811 | | | 900 | | | | 836 | |

| Freddie Mac Pool #Q55986 4.50% 5/1/204811 | | | 7,897 | | | | 7,532 | |

| Freddie Mac Pool #ZT1704 4.50% 1/1/204911 | | | 156,223 | | | | 149,717 | |

| Freddie Mac Pool #SD0214 3.00% 11/1/204911 | | | 40,605 | | | | 34,818 | |

| Freddie Mac Pool #QA5741 3.00% 12/1/204911 | | | 4,557 | | | | 3,916 | |

| Freddie Mac Pool #QA5125 3.50% 12/1/204911 | | | 1,445 | | | | 1,294 | |

| Freddie Mac Pool #SD7551 3.00% 1/1/205211 | | | 75,421 | | | | 64,614 | |

| Freddie Mac Pool #RA7556 4.50% 6/1/205211 | | | 83,287 | | | | 78,378 | |

| Freddie Mac Pool #SD1584 4.50% 9/1/205211 | | | 18,699 | | | | 17,777 | |

| Freddie Mac Pool #RA7938 5.00% 9/1/205211 | | | 3,461 | | | | 3,347 | |

| Freddie Mac, Series 2122, Class QM, 6.25% 2/15/202911 | | | 503 | | | | 507 | |

| Freddie Mac, Series KS01, Class A2, Multi Family, 2.522% 1/25/202311 | | | 303 | | | | 302 | |

| Freddie Mac, Series K030, Class A2, Multi Family, 3.25% 4/25/202311 | | | 8,427 | | | | 8,374 | |

| Freddie Mac, Series K036, Class A2, Multi Family, 3.527% 10/25/202311 | | | 10,000 | | | | 9,853 | |

| Freddie Mac, Series K050, Class A2, Multi Family, 3.334% 8/25/202511 | | | 11,250 | | | | 10,795 | |

| Freddie Mac, Series K055, Class A2, Multi Family, 2.673% 3/25/202611 | | | 3,500 | | | | 3,266 | |

| Freddie Mac, Series K064, Class A2, Multi Family, 3.224% 3/25/20278,11 | | | 4,390 | | | | 4,121 | |

| Freddie Mac, Series K066, Class A2, Multi Family, 3.117% 6/25/202711 | | | 4,360 | | | | 4,064 | |

| Freddie Mac, Series K067, Class A2, Multi Family, 3.194% 7/25/202711 | | | 4,810 | | | | 4,489 | |

| Bonds, notes & other debt instruments (continued) | | Principal amount

(000) | | | Value

(000) | |

| Mortgage-backed obligations (continued) | | | | | | | | |

| Federal agency mortgage-backed obligations (continued) | | | | | | | | |

| Freddie Mac, Series K068, Class A2, Multi Family, 3.244% 8/25/202711 | | USD | 2,350 | | | $ | 2,196 | |

| Freddie Mac, Series K069, Class A2, Multi Family, 3.187% 9/25/20278,11 | | | 8,906 | | | | 8,295 | |

| Freddie Mac, Series 3135, Class OP, principal only, 0% 4/15/202611 | | | 102 | | | | 95 | |

| Freddie Mac, Series 3117, Class OG, principal only, 0% 2/15/203611 | | | 71 | | | | 60 | |

| Freddie Mac, Series 3136, Class OP, principal only, 0% 4/15/203611 | | | 715 | | | | 602 | |

| Freddie Mac, Series 3147, Class OD, principal only, 0% 4/15/203611 | | | 269 | | | | 228 | |

| Freddie Mac, Series 3155, Class FO, principal only, 0% 5/15/203611 | | | 482 | | | | 406 | |

| Freddie Mac, Series 3149, Class MO, principal only, 0% 5/15/203611 | | | 137 | | | | 116 | |

| Freddie Mac, Series 3149, Class AO, principal only, 0% 5/15/203611 | | | 117 | | | | 100 | |

| Freddie Mac Seasoned Credit Risk Transfer Trust, Series 2017-3, Class MT, 3.00% 7/25/205611 | | | 8,686 | | | | 7,615 | |

| Freddie Mac Seasoned Credit Risk Transfer Trust, Series 2017-3, Class HT, 3.25% 7/25/205611 | | | 1,750 | | | | 1,561 | |

| Freddie Mac Seasoned Credit Risk Transfer Trust, Series 2017-2, Class MA, 3.00% 8/25/205611 | | | 9,088 | | | | 8,470 | |

| Freddie Mac Seasoned Credit Risk Transfer Trust, Series 2017-2, Class HA, 3.00% 8/25/20568,11 | | | 8,984 | | | | 8,385 | |

| Freddie Mac Seasoned Credit Risk Transfer Trust, Series 2018-1, Class HT, 3.00% 5/25/205711 | | | 9,323 | | | | 8,101 | |

| Freddie Mac Seasoned Credit Risk Transfer Trust, Series 2017-4, Class HT, 3.25% 6/25/20578,11 | | | 13,988 | | | | 12,632 | |

| Freddie Mac Seasoned Credit Risk Transfer Trust, Series 2017-4, Class MT, 3.50% 6/25/205711 | | | 7,871 | | | | 7,090 | |

| Freddie Mac Seasoned Credit Risk Transfer Trust, Series 2017-4, Class M45T, 4.50% 6/25/205711 | | | 14,615 | | | | 14,153 | |

| Freddie Mac Seasoned Credit Risk Transfer Trust, Series 2018-3, Class MA, 3.50% 8/25/205711 | | | 13,397 | | | | 12,722 | |

| Freddie Mac Seasoned Credit Risk Transfer Trust, Series 2018-2, Class MT, 3.50% 11/25/205711 | | | 9,780 | | | | 8,780 | |

| Freddie Mac Seasoned Credit Risk Transfer Trust, Series 2019-1, Class MT, 3.50% 7/25/205811 | | | 4,585 | | | | 4,112 | |

| Freddie Mac Seasoned Credit Risk Transfer Trust, Series 2019-1, Class MA, 3.50% 7/25/205811 | | | 1,472 | | | | 1,395 | |

| Freddie Mac Seasoned Credit Risk Transfer Trust, Series 2019-2, Class MT, 3.50% 8/26/205811 | | | 3,854 | | | | 3,458 | |

| Freddie Mac Seasoned Credit Risk Transfer Trust, Series 2019-3, Class MT, 3.50% 10/25/205811 | | | 2,387 | | | | 2,144 | |

| Freddie Mac Seasoned Credit Risk Transfer Trust, Series 2019-4, Class MA, 3.00% 2/25/205911 | | | 31,780 | | | | 29,479 | |

| Freddie Mac Seasoned Loan Structured Transaction Trust, Series 2018-1, Class A1, 3.50% 6/25/202811 | | | 702 | | | | 666 | |

| Freddie Mac Seasoned Loan Structured Transaction Trust, Series 2019-3, Class A1C, 2.75% 11/25/202911 | | | 40,722 | | | | 37,096 | |

| Government National Mortgage Assn. 4.00% 11/1/205211,12 | | | 582,342 | | | | 536,747 | |

| Government National Mortgage Assn. 4.50% 11/1/205211,12 | | | 154,223 | | | | 146,198 | |

| Government National Mortgage Assn. 5.00% 11/1/205211,12 | | | 740,308 | | | | 720,325 | |

| Government National Mortgage Assn. 5.50% 11/1/205211,12 | | | 89,955 | | | | 89,526 | |

| Government National Mortgage Assn. Pool #736682 4.50% 12/15/203711 | | | 645 | | | | 625 | |

| Government National Mortgage Assn. Pool #738938 6.50% 2/20/203911 | | | 84 | | | | 86 | |

| Government National Mortgage Assn. Pool #783690 6.00% 9/20/203911 | | | 840 | | | | 884 | |

| Government National Mortgage Assn. Pool #783689 5.50% 2/20/204011 | | | 1,162 | | | | 1,222 | |

| Government National Mortgage Assn. Pool #783539 5.00% 10/20/204011 | | | 935 | | | | 916 | |

| Government National Mortgage Assn. Pool #751708 3.50% 12/15/204011 | | | 78 | | | | 71 | |

| Government National Mortgage Assn. Pool #783688 5.00% 6/20/204111 | | | 1,071 | | | | 1,081 | |

| Government National Mortgage Assn. Pool #005198 6.50% 9/20/204111 | | | 356 | | | | 370 | |

| Government National Mortgage Assn. Pool #783687 4.50% 12/20/204111 | | | 1,056 | | | | 1,019 | |

| Government National Mortgage Assn. Pool #MA2894 4.50% 6/20/204511 | | | 1,151 | | | | 1,124 | |

| Government National Mortgage Assn. Pool #MA3246 4.50% 11/20/204511 | | | 1,519 | | | | 1,492 | |

| Government National Mortgage Assn. Pool #MA5077 3.50% 3/20/204811 | | | 4,476 | | | | 4,072 | |

| Government National Mortgage Assn. Pool #MA5468 5.00% 9/20/204811 | | | 442 | | | | 434 | |

| Government National Mortgage Assn. Pool #MA5530 5.00% 10/20/204811 | | | 105 | | | | 103 | |

| Government National Mortgage Assn. Pool #MA5652 4.50% 12/20/204811 | | | 592 | | | | 570 | |

| Government National Mortgage Assn. Pool #MA5711 4.50% 1/20/204911 | | | 982 | | | | 944 | |

| Government National Mortgage Assn. Pool #MA5712 5.00% 1/20/204911 | | | 1,236 | | | | 1,213 | |

| Government National Mortgage Assn. Pool #MA5764 4.50% 2/20/204911 | | | 2,130 | | | | 2,053 | |

| Government National Mortgage Assn. Pool #MA5878 5.00% 4/20/204911 | | | 12,530 | | | | 12,286 | |

| Government National Mortgage Assn. Pool #MA6042 5.00% 7/20/204911 | | | 7,793 | | | | 7,710 | |

| Bonds, notes & other debt instruments (continued) | | Principal amount

(000) | | | Value

(000) | |

| Mortgage-backed obligations (continued) | | | | | | | | |

| Federal agency mortgage-backed obligations (continued) | | | | | | | | |

| Government National Mortgage Assn. Pool #773426 4.70% 9/20/206111 | | USD | 9 | | | $ | 9 | |

| Government National Mortgage Assn. Pool #795485 4.677% 7/20/206211 | | | 16 | | | | 16 | |

| Government National Mortgage Assn. Pool #AG8088 4.95% 3/20/206411 | | | 2 | | | | 2 | |

| Government National Mortgage Assn. Pool #AG8117 4.886% 4/20/206411 | | | 2 | | | | 2 | |

| Government National Mortgage Assn. Pool #AG8193 4.947% 9/20/206411 | | | 2 | | | | 2 | |

| Government National Mortgage Assn. Pool #AG8207 4.946% 11/20/206411 | | | 2 | | | | 2 | |

| Government National Mortgage Assn. Pool #AG8244 4.945% 1/20/206511 | | | 2 | | | | 2 | |

| Government National Mortgage Assn., Series 2005-7, Class AO, principal only, 0% 2/16/203511 | | | 496 | | | | 421 | |

| Government National Mortgage Assn., Series 2007-8, Class LO, principal only, 0% 3/20/203711 | | | 394 | | | | 316 | |

| Uniform Mortgage-Backed Security 2.50% 11/1/203711,12 | | | 50,000 | | | | 45,059 | |

| Uniform Mortgage-Backed Security 2.50% 12/1/203711,12 | | | 100,000 | | | | 89,992 | |

| Uniform Mortgage-Backed Security 3.00% 11/1/205211,12 | | | 10,770 | | | | 9,157 | |

| Uniform Mortgage-Backed Security 4.00% 11/1/205211,12 | | | 42,182 | | | | 38,352 | |

| Uniform Mortgage-Backed Security 4.50% 11/1/205211,12 | | | 170,910 | | | | 160,362 | |

| Uniform Mortgage-Backed Security 5.00% 11/1/205211,12 | | | 308,088 | | | | 297,172 | |

| Uniform Mortgage-Backed Security 5.50% 11/1/205211,12 | | | 900 | | | | 888 | |

| Uniform Mortgage-Backed Security 6.00% 11/1/205211,12 | | | 864 | | | | 868 | |

| Uniform Mortgage-Backed Security 3.00% 12/1/205211,12 | | | 256,650 | | | | 218,192 | |

| Uniform Mortgage-Backed Security 4.00% 12/1/205211,12 | | | 4,004 | | | | 3,639 | |

| Uniform Mortgage-Backed Security 4.50% 12/1/205211,12 | | | 784,836 | | | | 735,845 | |

| Uniform Mortgage-Backed Security 5.00% 12/1/205211,12 | | | 500,000 | | | | 481,797 | |

| Uniform Mortgage-Backed Security 5.50% 12/1/205211,12 | | | 1,136,525 | | | | 1,119,160 | |

| Uniform Mortgage-Backed Security 6.00% 12/1/205211,12 | | | 25,756 | | | | 25,791 | |

| | | | | | | | 6,189,050 | |

| | | | | | | | | |

| Collateralized mortgage-backed obligations (privately originated) 0.37% | | | | | | | | |

| Arroyo Mortgage Trust, Series 2021-1R, Class A1, 1.175% 10/25/20481,8,11 | | | 14,702 | | | | 12,525 | |

| Bear Stearns ARM Trust, Series 2003-8, Class IIIA, 2.795% 1/25/20348,11 | | | 305 | | | | 239 | |

| BRAVO Residential Funding Trust, Series 2022-R1, Class A, 3.125% 1/29/2070 (6.125% on 1/29/2025)1,11,13 | | | 3,150 | | | | 2,750 | |

| Cascade Funding Mortgage Trust, Series 2020-HB4, Class A, 0.946% 12/26/20301,8,11 | | | 5,836 | | | | 5,651 | |

| Cascade Funding Mortgage Trust, Series 2021-HB7, Class A, 1.151% 10/27/20311,8,11 | | | 14,286 | | | | 13,394 | |

| Cascade Funding Mortgage Trust, Series 2021-HB7, Class M1, 2.125% 10/27/20311,8,11 | | | 1,296 | | | | 1,183 | |

| Cascade Funding Mortgage Trust, Series 2021-HB6, Class A, 0.898% 6/25/20361,8,11 | | | 10,909 | | | | 10,324 | |

| CIM Trust, Series 2022-R2, Class A1, 3.75% 12/25/20611,8,11 | | | 17,648 | | | | 16,509 | |

| CS First Boston Mortgage Securities Corp., Series 2002-30, Class IA1, 7.50% 11/25/203211 | | | 116 | | | | 113 | |

| CS First Boston Mortgage Securities Corp., Series 2002-34, Class IA1, 7.50% 12/25/203211 | | | 78 | | | | 78 | |

| CS First Boston Mortgage Securities Corp., Series 2003-21, Class VA1, 6.50% 7/25/203311 | | | 95 | | | | 88 | |

| Finance of America Structured Securities Trust, Series 2019-JR1, Class A, 2.00% 3/25/20691,11 | | | 8,250 | | | | 8,732 | |

| Flagstar Mortgage Trust, Series 2021-10INV, Class A3, 2.50% 10/25/20511,8,11 | | | 26,847 | | | | 20,764 | |

| Freddie Mac Structured Agency Credit Risk Debt Notes, Series 2021-DNA6, Class M2, (30-day Average USD-SOFR + 1.50%) 4.497% 10/25/20411,8,11 | | | 815 | | | | 750 | |

| Freddie Mac Structured Agency Credit Risk Debt Notes, Series 2022-DNA3, Class M1A, (30-day Average USD-SOFR + 2.00%) 4.997% 4/25/20421,8,11 | | | 8,041 | | | | 7,886 | |

| Freddie Mac Structured Agency Credit Risk Debt Notes, Series 2022-DNA6, Class M1A, (30-day Average USD-SOFR + 2.15%) 5.147% 9/25/20421,8,11 | | | 3,087 | | | | 3,061 | |

| Freddie Mac Structured Agency Credit Risk Debt Notes, Series 2022-DNA6, Class M1B, (30-day Average USD-SOFR + 3.70%) 6.697% 9/25/20421,8,11 | | | 5,838 | | | | 5,807 | |

| GS Mortgage-Backed Securities Trust, Series 2022-PJ5, Class A4, 2.50% 10/25/20521,8,11 | | | 62,494 | | | | 48,384 | |

| Home Partners of America Trust, Series 2022-1, Class A, 3.93% 4/17/20391,11 | | | 18,702 | | | | 17,417 | |

| Legacy Mortgage Asset Trust, Series 2022-GS1, Class A1, 4.00% 2/25/2061 (7.00% on 4/25/2025)1,11,13 | | | 18,711 | | | | 17,749 | |

| Legacy Mortgage Asset Trust, Series 2021-GS2, Class A1, 1.75% 4/25/20611,8,11 | | | 2,175 | | | | 2,021 | |

| Legacy Mortgage Asset Trust, Series 2021-GS5, Class A1, 2.25% 7/25/2067 (5.25% on 11/25/2024)1,11,13 | | | 8,933 | | | | 8,170 | |

| Mello Warehouse Securitization Trust, Series 2021-3, Class A, (1-month USD-LIBOR + 0.85%) 4.436% 11/25/20551,8,11 | | | 24,241 | | | | 23,395 | |

| Mill City Mortgage Trust, Series 2018-1, Class A1, 3.25% 5/25/20621,8,11 | | | 161 | | | | 155 | |

| NewRez Warehouse Securitization Trust, Series 2021-1, Class A, (1-month USD-LIBOR + 0.75%) 4.336% 5/25/20551,8,11 | | | 25,007 | | | | 24,526 | |

| Bonds, notes & other debt instruments (continued) | | Principal amount

(000) | | | Value

(000) | |

| Mortgage-backed obligations (continued) | | | | | | | | |

| Collateralized mortgage-backed obligations (privately originated) (continued) | | | | | |

| Onslow Bay Financial Mortgage Loan Trust, Series 2022-J1, Class A2, 2.50% 2/25/20521,8,11 | | USD | 11,202 | | | $ | 8,608 | |

| Reverse Mortgage Investment Trust, Series 2021-HB1, Class A, 1.259% 11/25/20311,8,11 | | | 7,154 | | | | 6,797 | |

| Towd Point Mortgage Trust, Series 2016-5, Class A1, 2.50% 10/25/20561,8,11 | | | 2,492 | | | | 2,458 | |

| Towd Point Mortgage Trust, Series 2017-5, Class A1, 4.186% 2/25/20571,8,11 | | | 688 | | | | 678 | |

| Towd Point Mortgage Trust, Series 2017-4, Class A1, 2.75% 6/25/20571,8,11 | | | 653 | | | | 620 | |

| Towd Point Mortgage Trust, Series 2017-3, Class A1, 2.75% 7/25/20571,8,11 | | | 346 | | | | 339 | |

| Towd Point Mortgage Trust, Series 2017-6, Class A1, 2.75% 10/25/20571,8,11 | | | 981 | | | | 937 | |

| Towd Point Mortgage Trust, Series 2018-2, Class A1, 3.25% 3/25/20581,8,11 | | | 1,270 | | | | 1,213 | |

| Towd Point Mortgage Trust, Series 2018-5, Class A1A, 3.25% 7/25/20581,8,11 | | | 314 | | | | 300 | |

| Towd Point Mortgage Trust, Series 2020-4, Class A1, 1.75% 10/25/20601,11 | | | 72,185 | | | | 64,214 | |

| Treehouse Park Improvement Association No.1 - Anleihen 9.75% 12/1/20331,4 | | | 6,473 | | | | 5,446 | |

| Tricon Residential Trust, Series 2021-SFR1, Class A, 1.943% 7/17/20381,11 | | | 19,525 | | | | 16,943 | |

| | | | | | | | 360,224 | |

| | | | | | | | | |

| Commercial mortgage-backed securities 0.37% | | | | | | | | |

| Barclays Commercial Mortgage Securities, LLC, Series 2017-DELC, Class A, 4.387% 8/15/20361,8,11 | | | 14,672 | | | | 14,319 | |

| Barclays Commercial Mortgage Securities, LLC, Series 2022-C17, Class A5, 4.441% 9/15/205511 | | | 8,633 | | | | 7,873 | |

| Boca Commercial Mortgage Trust, Series 2022-BOCA, Class A, (1-month USD CME Term SOFR + 1.7696%) 5.145% 5/15/20391,8,11 | | | 10,389 | | | | 10,135 | |

| BPR Trust, Series 2022-OANA, Class A, (1-month USD CME Term SOFR + 1.898%) 5.274% 4/15/20371,8,11 | | | 31,327 | | | | 30,430 | |

| BX Trust, Series 2022-CSMO, Class A, (1-month USD CME Term SOFR + 2.115%) 5.49% 6/15/20271,8,11 | | | 31,020 | | | | 30,668 | |