Use these links to rapidly review the document

TABLE OF CONTENTS

ITEM 8. FINANCIAL STATEMENTS AND SUPPLEMENTARY DATA

PART IV

INDEX TO FINANCIAL STATEMENT SCHEDULE

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D. C. 20549

FORM 10-K

(Mark One) | ||

ý | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |

For the fiscal year ended December 31, 2013 | ||

or | ||

o | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |

Commission file number 1-9576

OWENS-ILLINOIS, INC.

(Exact name of registrant as specified in its charter)

| Delaware (State or other jurisdiction of incorporation or organization) | 22-2781933 (IRS Employer Identification No.) | |

One Michael Owens Way, Perrysburg, Ohio (Address of principal executive offices) | 43551 (Zip Code) |

Registrant's telephone number, including area code:(567) 336-5000

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Name of each exchange on which registered | |

|---|---|---|

| Common Stock, $.01 par value | New York Stock Exchange |

Securities registered pursuant to Section 12(g) of the Act:None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ý No o

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes o No ý

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports) and (2) has been subject to such filing requirements for the past 90 days. Yes ý No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ý No o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company. See the definitions of "large accelerated filer," "accelerated filer" and "smaller reporting company" in Rule 12b-2 of the Exchange Act.

| Large accelerated filerý | Accelerated filero | Non-accelerated filero (Do not check if a smaller reporting company) | Smaller reporting companyo |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes o No ý

The aggregate market value (based on the consolidated tape closing price on June 30, 2013) of the voting and non-voting common equity held by non-affiliates of Owens-Illinois, Inc. was approximately $4,901,946,000. For the sole purpose of making this calculation, the term "non-affiliate" has been interpreted to exclude directors and executive officers of the Company. Such interpretation is not intended to be, and should not be construed to be, an admission by Owens-Illinois, Inc. or such directors or executive officers of the Company that such directors and executive officers of the Company are "affiliates" of Owens-Illinois, Inc., as that term is defined under the Securities Act of 1934.

The number of shares of common stock, $.01 par value of Owens-Illinois, Inc. outstanding as of January 31, 2014 was 164,757,843.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the Owens-Illinois, Inc. Proxy Statement for The Annual Meeting of Share Owners To Be Held Thursday, May 15, 2014 ("Proxy Statement") are incorporated by reference into Part III hereof.

TABLE OF GUARANTORS

Exact Name of Registrant As Specified In Its Charter | State/Country of Incorporation or Organization | Primary Standard Industrial Classification Code Number | I.R.S Employee Identification Number | ||||||

|---|---|---|---|---|---|---|---|---|---|

Owens-Illinois Group, Inc | Delaware | 6719 | 34-1559348 | ||||||

Owens-Brockway Packaging, Inc | Delaware | 6719 | 34-1559346 | ||||||

The address, including zip code, and telephone number, of each additional registrant's principal executive office is One Michael Owens Way, Perrysburg, Ohio 43551; (567) 336-5000. These companies are listed as guarantors of the debt securities of the registrant. The consolidating condensed financial statements of the Company depicting separately its guarantor and non-guarantor subsidiaries are presented in the notes to the consolidated financial statements. All of the equity securities of each of the guarantors set forth in the table above are owned, either directly or indirectly, by Owens-Illinois, Inc.

PART I | 1 | |||||

ITEM 1. | BUSINESS | 1 | ||||

ITEM 1A. | RISK FACTORS | 8 | ||||

ITEM 1B. | UNRESOLVED STAFF COMMENTS | 16 | ||||

ITEM 2. | PROPERTIES | 17 | ||||

ITEM 3. | LEGAL PROCEEDINGS | 19 | ||||

ITEM 4. | MINE SAFETY DISCLOSURES | 19 | ||||

PART II | 20 | |||||

ITEM 5. | MARKET FOR REGISTRANT'S COMMON EQUITY, RELATED SHARE OWNER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES | 20 | ||||

ITEM 6. | SELECTED FINANCIAL DATA | 22 | ||||

ITEM 7. | MANAGEMENT'S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS | 26 | ||||

ITEM 7A. | QUALITATIVE AND QUANTITATIVE DISCLOSURES ABOUT MARKET RISK | 47 | ||||

ITEM 8. | FINANCIAL STATEMENTS AND SUPPLEMENTARY DATA | 50 | ||||

ITEM 9. | CHANGES IN AND DISAGREEMENTS WITH ACCOUNTANTS ON ACCOUNTING AND FINANCIAL DISCLOSURE | 106 | ||||

ITEM 9A. | CONTROLS AND PROCEDURES | 106 | ||||

ITEM 9B. | OTHER INFORMATION | 109 | ||||

PART III | 109 | |||||

ITEM 10. | DIRECTORS, EXECUTIVE OFFICERS AND CORPORATE GOVERNANCE | 109 | ||||

ITEM 11. | EXECUTIVE COMPENSATION | 109 | ||||

ITEM 12. | SECURITY OWNERSHIP OF CERTAIN BENEFICIAL OWNERS AND MANAGEMENT AND RELATED STOCKHOLDER MATTERS | 109 | ||||

ITEM 13. | CERTAIN RELATIONSHIPS AND RELATED TRANSACTIONS, AND DIRECTOR INDEPENDENCE | 110 | ||||

ITEM 14. | PRINCIPAL ACCOUNTANT FEES AND SERVICES | 110 | ||||

PART IV | 111 | |||||

ITEM 15. | EXHIBITS AND FINANCIAL STATEMENT SCHEDULES | 111 | ||||

SIGNATURES | 201 | |||||

EXHIBITS |

| |||||

General Development of Business

Owens-Illinois, Inc. (the "Company"), through its subsidiaries, is the successor to a business established in 1903. The Company is the largest manufacturer of glass containers in the world with 77 glass manufacturing plants in 21 countries. It competes in the glass container segment of the rigid packaging market and is the leading glass container manufacturer in most of the countries where it has manufacturing facilities.

Company Strategy

The Company's ambition is to be the world's leading maker of brand-building glass containers, delivering unmatched quality, innovation and service to its customers; generating strong financial results for its investors; and providing a safe, motivating and engaging work environment for its employees. To accomplish this ambition, the Company is focused on the following objectives:

- •

- Reduce structural costs through specific programs such as permanent footprint adjustments, asset optimization and global cost-cutting initiatives;

- •

- Grow selectively by taking advantage of the Company's position in emerging markets around the world and strengthening the Company's positions in Europe and North America;

- •

- Deliver brand-building product innovation to the Company's customers to help them build, develop and expand their brands; and

- •

- Invest strategically in process innovation and research and development to reduce manufacturing costs and improve efficiency, flexibility, reliability and sustainability.

Reportable Segments

The Company has four reportable segments based on its geographic locations: Europe, North America, South America and Asia Pacific. Information as to sales, earnings from continuing operations before interest income, interest expense, and provision for income taxes and excluding amounts related to certain items that management considers not representative of ongoing operations ("segment operating profit"), and total assets by reportable segment is included in Note 2 to the Consolidated Financial Statements.

Products and Services

The Company produces glass containers for alcoholic beverages, including beer, flavored malt beverages, spirits and wine. The Company also produces glass packaging for a variety of food items, soft drinks, teas, juices and pharmaceuticals. The Company manufactures glass containers in a wide range of sizes, shapes and colors and is active in new product development and glass container innovation.

Customers

In most of the countries where the Company competes, it has the leading position in the glass container segment of the rigid packaging market based on sales revenue. The Company's largest customers consist mainly of the leading food and beverage manufacturers in the world, including (in alphabetical order) Anheuser-Busch InBev, Brown Forman, Carlsberg, Coca-Cola, Constellation, Diageo, Heineken, Kirin, MillerCoors, Nestle, PepsiCo, Pernod Ricard, SABMiller, and Saxco International. No customer represents more than 10% of the Company's consolidated net sales.

1

The Company sells most of its glass container products directly to customers under annual or multi-year supply agreements. Multi-year contracts typically provide for price adjustments based on cost changes. The Company also sells some of its products through distributors. Many customers provide the Company with regular estimates of their product needs, which enables the Company to schedule glass container production to maintain reasonable levels of inventory. Due to the significance of transportation costs and the importance of timely delivery, glass container manufacturing facilities are generally located in close proximity to customers.

Markets and Competitive Conditions

The Company's principal markets for glass container products are in Europe, North America, South America and Asia Pacific.

Europe. The Company has a leading share of the glass container segment of the rigid packaging market in Europe, with 35 glass container manufacturing plants located in the Czech Republic, Estonia, France, Germany, Hungary, Italy, the Netherlands, Poland, Spain and the United Kingdom. The Company is also involved in two joint ventures that manufacture glass containers in Italy. These plants primarily produce glass containers for the beer, wine, champagne, spirits and food markets in these countries. Throughout Europe, the Company competes directly with a variety of glass container manufacturers including Verallia, Ardagh Group, Vetropak and Vidrala.

North America. The Company has 19 glass container manufacturing plants in the U.S. and Canada, and is also involved in a joint venture that manufactures glass containers in the U.S. The Company has the leading share of the glass container segment of the U.S. rigid packaging market, based on sales revenue by domestic producers. The principal glass container competitors in the U.S. are Verallia North America and Ardagh Group. Imports from Canada, China, Mexico, Taiwan and other countries also compete in U.S. glass container segments. Additionally, there are several major consumer packaged goods companies that self-manufacture glass containers.

South America. The Company has 13 glass manufacturing plants in South America, located in Argentina, Brazil, Colombia, Ecuador and Peru. In South America, the Company maintains a diversified portfolio serving several markets, including beer, non-alcoholic beverages, spirits, flavored malt beverages, wine, food and pharmaceuticals. The region also has a large infrastructure for returnable/refillable glass containers. The Company competes directly with Verallia in Brazil and Argentina, and does not believe that it competes with any other large, multinational glass container manufacturers in the rest of the region.

Asia Pacific. The Company has 10 glass container manufacturing plants in the Asia Pacific region, located in Australia, China, Indonesia and New Zealand. It is also involved in joint venture operations in China, Malaysia and Vietnam. In Asia Pacific, the Company primarily produces glass containers for the beer, wine, food and non-alcoholic beverage markets. The Company competes directly with Orora (formerly Amcor Limited) in Australia, and does not believe that it competes with any other large, multinational glass container manufacturers in the rest of the region. In China, the glass container segments of the packaging market are regional and highly fragmented with a large number of local competitors.

In addition to competing with other large and well-established manufacturers in the glass container segment, the Company competes in all regions with manufacturers of other forms of rigid packaging, principally aluminum cans and plastic containers. Competition is based on quality, price, service, innovation and the marketing attributes of the container. The principal competitors producing metal containers include Amcor, Ball Corporation, Crown Holdings, Inc., Rexam plc, and Silgan Holdings Inc. The principal competitors producing plastic containers include Amcor, Consolidated Container Holdings, LLC, Reynolds Group Holdings Limited, Plastipak Packaging, Inc. and

2

Silgan Holdings Inc. The Company also competes with manufacturers of non-rigid packaging alternatives, including flexible pouches, aseptic cartons and bag-in-box containers.

The Company seeks to provide products and services to customers ranging from large multinationals to small local breweries and wineries in a way that creates a competitive advantage for the Company. The Company believes that it is often the glass container partner of choice because of its innovation and branding capabilities, its global footprint and its expertise in manufacturing know-how and process technology.

Seasonality

Sales of many glass container products such as beer, beverages and food are seasonal. Shipments in the U.S. and Europe are typically greater in the second and third quarters of the year, while shipments in the Asia Pacific region are typically greater in the first and fourth quarters of the year, and shipments in South America are typically greater in the third and fourth quarters of the year.

Manufacturing

The Company has 77 glass manufacturing plants. It constantly seeks to improve the productivity of these operations through the systematic upgrading of production capabilities, sharing of best practices among plants and effective training of employees.

The Company operates machine shops that rebuild and repair high-productivity glass forming machines, as well as a mold shop that manufactures molds and related equipment. The Company also provides engineering support for its glass manufacturing operations through facilities located in the U.S., Australia, Poland and Peru.

Suppliers and Raw Materials

The primary raw materials used in the Company's glass container operations are sand, soda ash, limestone and recycled glass. Each of these materials, as well as the other raw materials used to manufacture glass containers, has historically been available in adequate supply from multiple sources. One of the sources is a soda ash mining operation in Wyoming in which the Company has a 25% interest.

Energy

The Company's glass container operations require a continuous supply of significant amounts of energy, principally natural gas, fuel oil and electrical power. Adequate supplies of energy are generally available at all of the Company's manufacturing locations. Energy costs typically account for 10-25% of the Company's total manufacturing costs, depending on the cost of energy, the type of energy available, the factory location and the particular energy requirements. The percentage of total cost related to energy can vary significantly because of volatility in market prices, particularly for natural gas and fuel oil in volatile markets such as North America and Europe.

In North America, approximately 90% of the sales volume is tied to customer contracts that contain provisions that pass the price of natural gas to the customer, effectively reducing the North America segment's exposure to changing natural gas market prices. Also, in order to limit the effects of fluctuations in market prices for natural gas, the Company uses commodity futures contracts related to its forecasted requirements in North America. The objective of these futures contracts is to reduce potential volatility in cash flows and expense due to changing market prices. The Company continually evaluates the energy markets with respect to its forecasted energy requirements to optimize its use of commodity futures contracts.

3

In Europe and Asia Pacific, the Company enters into fixed price contracts for a significant amount of its energy requirements. These contracts typically have terms of 12 months or less in Europe and one to three years in Asia Pacific. In South America, the Company enters into fixed price contracts for its energy requirements. These contracts typically have terms of two years, with annual price adjustments for inflation.

Technical Assistance License Agreements

The Company has agreements to license its proprietary glass container technology and to provide technical assistance to a limited number of companies around the world. These agreements cover areas related to manufacturing and engineering assistance. The worldwide licensee network provides a stream of revenue to help support the Company's development activities. In the years 2013, 2012 and 2011, the Company earned $16 million, $17 million and $16 million, respectively, in royalties and net technical assistance revenue.

Research, Development and Engineering

Research, development and engineering constitute important parts of the Company's technical activities. Expenditures for these activities were $62 million, $62 million and $71 million for 2013, 2012 and 2011, respectively. The Company primarily focuses on advancements in the areas of product innovation, manufacturing process control, melting technology, automatic inspection, light-weighting and further automation of manufacturing activities. The Company's research and development activities are conducted at its corporate facilities in Perrysburg, Ohio. During 2013, the Company completed the construction of a new research and development facility at this location. This new facility will enable the Company to expand its research and development capabilities.

The Company holds a large number of patents related to a wide variety of products and processes and has a substantial number of patent applications pending. While the aggregate of the Company's patents are of material importance to its businesses, the Company does not consider that any patent or group of patents relating to a particular product or process is of material importance when judged from the standpoint of any individual segment or its businesses as a whole.

Sustainability and the Environment

The Company is committed to reducing the impact its products and operations have on the environment. As part of this commitment, the Company has set targets for increasing the use of recycled glass in its manufacturing process, while reducing energy consumption and carbon dioxide equivalent ("CO2") emissions. Specific actions taken by the Company include working with governments and other organizations to establish and financially support recycling initiatives, partnering with other entities throughout the supply chain to improve the effectiveness of recycling efforts, reducing the weight of glass packaging and investing in research and development to reduce energy consumption in its manufacturing process.

The Company's worldwide operations, in addition to other companies within the industry, are subject to extensive laws, ordinances, regulations and other legal requirements relating to environmental protection, including legal requirements governing investigation and clean-up of contaminated properties as well as water discharges, air emissions, waste management and workplace health and safety. The Company strives to abide by and uphold such laws and regulations.

Glass Recycling and Bottle Deposits

The Company is an important contributor to recycling efforts worldwide and is among the largest users of recycled glass containers. If sufficient high-quality recycled glass were available on a consistent basis, the Company has the technology to make glass containers using 100% recycled glass. Using

4

recycled glass in the manufacturing process reduces energy costs and prolongs the operating life of the glass melting furnaces.

In the U.S., Canada, Europe and elsewhere, government authorities have adopted or are considering legal requirements that would mandate certain recycling rates, the use of recycled materials, or limitations on or preferences for certain types of packaging. The Company believes that governments worldwide will continue to develop and enact legal requirements around guiding customer and end-consumer packaging choices.

Sales of beverage containers are affected by governmental regulation of packaging, including deposit laws and extended producer responsibility regulations. As of December 31, 2013, there were a number of U.S. states, Canadian provinces and territories, European countries and Australian states with some form of incentive for consumer returns in their law. The structure and enforcement of such laws and regulations can impact the sales of beverage containers in a given jurisdiction. Such laws and regulations also impact the availability of post-consumer recycled glass for the Company to use in container production.

A number of U.S. states and Canadian provinces have recently considered or are now considering laws and regulations to encourage curbside, deposit and on-premise recycling. Although there is no clear trend in the direction of these state and provincial laws and regulations, the Company believes that U.S. states and Canadian provinces, as well as municipalities within those jurisdictions, will continue to adopt recycling laws, which will impact supplies of recycled glass. As a large user of recycled glass for making new glass containers, the Company has an interest in laws and regulations impacting supplies of such material in its markets.

Air Emissions

In Europe, the European Union Emissions Trading Scheme ("EUETS") is in effect to facilitate emissions reduction. The Company's manufacturing facilities which operate in EU countries must restrict the volume of their CO2 emissions to the level of their individually allocated emissions allowances as set by country regulators. If the actual level of emissions for any facility exceeds its allocated allowance, additional allowances can be bought to cover deficits; conversely, if the actual level of emissions for any facility is less than its allocation, the excess allowances can be sold. The EUETS has not had a material effect on the Company's results to date. However, should the regulators significantly restrict the number of emissions allowances available, it could have a material effect in the future.

In North America, the U.S. and Canada are engaged in significant legislative and regulatory activity relating to CO2 emissions, at the federal, state and provincial levels of government. The U.S. Environmental Protection Agency ("EPA") regulates emissions of hazardous air pollutants under the Clean Air Act, which grants the EPA authority to establish limits for certain air pollutants and to require compliance, levy penalties and bring civil judicial action against violators. The structure and scope of the EPA's CO2 regulations are currently the subject of litigation and are expected to be the subject of federal legislative activity. The EPA regulations, if preserved as proposed, could have a significant long-term impact on the Company's US operations. The EPA also implemented the Cross-State Air Pollution Rule, which set stringent emissions limits in many states starting in 2012. The state of California in the U.S and the province of Quebec in Canada adopted cap-and-trade legislation aimed at reducing greenhouse gas emissions starting in 2013.

In Asia Pacific, theNational Greenhouse and Energy Reporting Act 2007 commenced on July 1, 2008 in Australia. This act established a mandatory reporting system for corporate greenhouse gas emissions and energy production and consumption. In 2011, the Australian government adopted a carbon pricing mechanism that took effect in 2012, which requires certain manufacturers to pay a tax based on their

5

carbon-equivalent emissions. An emissions trading scheme has also been in effect in New Zealand since 2008.

In South America, the Brazilian government passed a law in 2009 requiring companies to reduce the level of greenhouse gas emissions by the year 2020. In the other South American countries, national and local governments are considering proposals that would impose regulations to reduce CO2 emissions, but no legislation has been implemented to date.

The Company is unable to predict what environmental legal requirements may be adopted in the future. However, the Company continually monitors its operations in relation to environmental impacts and invests in environmentally friendly and emissions-reducing projects. As such, the Company has made significant expenditures for environmental improvements at certain of its facilities over the last several years; however, these expenditures did not have a material adverse effect on the Company's results of operations or cash flows. The Company is unable to predict the impact of future environmental legal requirements on its results of operations or cash flows.

Employees

The Company's worldwide operations employed approximately 22,500 persons as of December 31, 2013. Approximately 79% of North American employees are hourly workers covered by collective bargaining agreements. The principal collective bargaining agreement, which at December 31, 2013, covered approximately 91% of the Company's union-affiliated employees in North America, will expire on March 31, 2016. Approximately 60% of employees in South America are unionized, although according to the labor legislation in each country, 100% of employees are covered by collective bargaining agreements. The majority of the hourly workers in Australia and New Zealand are also covered by collective bargaining agreements. The collective bargaining agreements in South America, Australia and New Zealand have varying terms and expiration dates. In Europe, a large number of the Company's employees are employed in countries in which employment laws provide greater bargaining or other rights to employees than the laws of the U.S. Such employment rights require the Company to work collaboratively with the legal representatives of the employees to effect any changes to labor arrangements. The Company considers its employee relations to be good and does not anticipate any material work stoppages in the near term.

Available Information

The Company's website is www.o-i.com. The Company's annual report on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, and amendments to those reports filed or furnished pursuant to Section 13(a) or 15(d) of the Securities Exchange Act of 1934 can be obtained from this site at no cost. The Company's SEC filings are also available for reading and copying at the SEC's Public Reference Room at 100 F Street, NE, Washington, D.C. 20549. Information on the operation of the Public Reference Room may be obtained by calling the SEC at 1-800-SEC-0330. The SEC also maintains a website at www.sec.gov that contains reports, proxy and information statements, and other information regarding issuers that file electronically with the SEC.

The Company's Corporate Governance Guidelines, Code of Business Conduct and Ethics and the charters of the Audit, Compensation, Nominating/Corporate Governance and Risk Oversight Committees are also available on the Investor Relations section of the Company's website. Copies of these documents are available in print to share owners upon request, addressed to the Corporate Secretary at the address above.

6

Executive Officers of the Registrant

Name and Age | Position | |

|---|---|---|

Albert P. L. Stroucken (66) | Chairman and Chief Executive Officer since 2006. Previously Chief Executive Officer of HB Fuller Company, a manufacturer of adhesives, sealants, coatings, paints and other specialty chemical products 1998-2006; Chairman of HB Fuller Company 1999-2006. | |

Stephen P. Bramlage, Jr. (43) | Chief Financial Officer and Senior Vice President since 2012; President of O-I Asia Pacific 2011-2012; General Manager of O-I New Zealand 2010-2011; Vice President of Finance 2008-2010; Vice President and Chief Financial Officer of O-I Europe 2008; Vice President and Treasurer 2006-2008. | |

James W. Baehren (63) | Senior Vice President and General Counsel since 2003; Senior Vice President Strategic Planning 2006-2012; Chief Administrative Officer 2004-2006; Corporate Secretary 1998-2010; Vice President and Director of Finance 2001-2003. | |

Paul A. Jarrell (51) | Senior Vice President since 2011; Chief Administrative Officer since 2013; Chief Human Resources Officer 2011-2012. Previously Executive Vice President and Chief Human Resources Officer for DSM, a life sciences and materials company based in The Netherlands 2009-2011; Vice President and Director of Human Resources for ITT, a fluid technologies and engineered products company 2006-2009. | |

Erik C. M. Bouts (52) | Vice President and President of O-I Europe since 2013. Previously Chief Executive Officer of the Glidden Company, part of AkzoNobel Architectural Paints Division in the U.S. 2007-2012; President and Chief Executive Officer of Philips Lighting Company North America, a division of Philips Electronics 2002-2006. | |

Arnaud N. J. M. de Weert (50) | Vice President and President of O-I North America since 2012. Previously Chief Operating Officer of Constellium, a manufacturer of aluminum products based in France 2011-2012; Operating Partner/Senior Advisor at Apollo Management, a U.S. private equity company 2009-2011; President Europe for Novelis AG, a manufacturer of rolled aluminum products 2006-2009. | |

Andres A. Lopez (51) | Vice President and President of O-I South America since 2009; Vice President of global manufacturing and engineering 2006-2009. | |

Sergio B. O. Galindo (46) | Vice President and President of O-I Asia Pacific since 2012; General Manager of O-I Colombia 2009-2012. |

Financial Information about Foreign and Domestic Operations

Information as to net sales, segment operating profit, and assets of the Company's reportable segments is included in Note 2 to the Consolidated Financial Statements.

7

Asbestos-Related Liability—The Company has made, and will continue to make, substantial payments to resolve claims of persons alleging exposure to asbestos-containing products and may need to record additional charges in the future for estimated asbestos-related costs. These substantial payments have affected and may continue to affect the Company's cost of borrowing and the ability to pursue acquisitions.

The Company is a defendant in numerous lawsuits alleging bodily injury and death as a result of exposure to asbestos dust. From 1948 to 1958, one of the Company's former business units commercially produced and sold approximately $40 million of a high-temperature, calcium-silicate based pipe and block insulation material containing asbestos. The Company exited the pipe and block insulation business in April 1958. The typical asbestos personal injury lawsuit alleges various theories of liability, including negligence, gross negligence and strict liability and seeks compensatory, and in some cases, punitive damages, in various amounts (herein referred to as "asbestos claims").

The Company believes that its ultimate asbestos-related liability (i.e., its indemnity payments or other claim disposition costs plus related legal fees) cannot reasonably be estimated. Beginning with the initial liability of $975 million established in 1993, the Company has accrued a total of approximately $4.3 billion through 2013, before insurance recoveries, for its asbestos-related liability. The Company's ability to reasonably estimate its liability has been significantly affected by, among other factors, the volatility of asbestos-related litigation in the United States, the significant number of co-defendants that have filed for bankruptcy, the magnitude and timing of co-defendant bankruptcy trust payments, the inherent uncertainty of future disease incidence and claiming patterns against the Company, and the success of efforts by co-defendants to restrict or eliminate their liability in the litigation.

The Company conducted a comprehensive review of its asbestos-related liabilities and costs in connection with finalizing and reporting its results of operations for the year ended December 31, 2013 and concluded that an increase in its accrual for future asbestos-related costs in the amount of $145 million (pretax and after tax) was required.

The ultimate amount of distributions that may be required to fund the Company's asbestos-related payments cannot reasonably be estimated. The Company's reported results of operations for 2013 were materially affected by the $145 million (pretax and after tax) fourth quarter charge and asbestos-related payments continue to be substantial. Any future additional charge may likewise materially affect the Company's results of operations for the period in which it is recorded. Also, the continued use of significant amounts of cash for asbestos-related costs has affected and may continue to affect the Company's cost of borrowing and its ability to pursue global or domestic acquisitions.

Substantial Leverage—The Company's indebtedness could adversely affect the Company's financial health.

The Company has a significant amount of debt. As of December 31, 2013, the Company had approximately $3.6 billion of total debt outstanding, a decrease from $3.8 billion at December 31, 2012.

The Company's indebtedness could result in the following consequences:

- •

- Increased vulnerability to general adverse economic and industry conditions;

- •

- Increased vulnerability to interest rate increases for the portion of the debt under the secured credit agreement;

- •

- Require the Company to dedicate a substantial portion of cash flow from operations to payments on indebtedness, thereby reducing the availability of cash flow to fund working capital, capital expenditures, acquisitions, development efforts and other general corporate purposes;

- •

- Limit flexibility in planning for, or reacting to, changes in the Company's business and the rigid packaging market;

8

- •

- Place the Company at a competitive disadvantage relative to its competitors that have less debt; and

- •

- Limit, along with the financial and other restrictive covenants in the documents governing indebtedness, among other things, the Company's ability to borrow additional funds.

Ability to Service Debt—To service its indebtedness, the Company will require a significant amount of cash. The Company's ability to generate cash depends on many factors beyond its control.

The Company's ability to make payments on and to refinance its indebtedness and to fund working capital, capital expenditures, acquisitions, development efforts and other general corporate purposes depends on its ability to generate cash in the future. The Company has no assurance that it will generate sufficient cash flow from operations, or that future borrowings will be available under the secured credit agreement, in an amount sufficient to enable the Company to pay its indebtedness, or to fund other liquidity needs. If short term interest rates increase, the Company's debt service cost will increase because some of its debt is subject to short term variable interest rates. At December 31, 2013, the Company's debt subject to variable interest rates represented approximately 25% of total debt.

The Company may need to refinance all or a portion of its indebtedness on or before maturity. If the Company is unable to generate sufficient cash flow and is unable to refinance or extend outstanding borrowings on commercially reasonable terms or at all, it may have to take one or more of the following actions:

- •

- Reduce or delay capital expenditures planned for replacements, improvements and expansions;

- •

- Sell assets;

- •

- Restructure debt; and/or

- •

- Obtain additional debt or equity financing.

The Company can provide no assurance that it could affect or implement any of these alternatives on satisfactory terms, if at all.

Debt Restrictions—The Company may not be able to finance future needs or adapt its business plans to changes because of restrictions placed on it by the secured credit agreement and the indentures and instruments governing other indebtedness.

The secured credit agreement, the indentures governing the senior debentures and notes, and certain of the agreements governing other indebtedness contain affirmative and negative covenants that limit the ability of the Company to take certain actions. For example, these indentures restrict, among other things, the ability of the Company and its restricted subsidiaries to borrow money, pay dividends on, or redeem or repurchase its stock, make investments, create liens, enter into certain transactions with affiliates and sell certain assets or merge with or into other companies. These restrictions could adversely affect the Company's ability to operate its businesses and may limit its ability to take advantage of potential business opportunities as they arise.

Failure to comply with these or other covenants and restrictions contained in the secured credit agreement, the indentures or agreements governing other indebtedness could result in a default under those agreements, and the debt under those agreements, together with accrued interest, could then be declared immediately due and payable. If a default occurs under the secured credit agreement, the Company could no longer request borrowings under the agreement, and the lenders could cause all of the outstanding debt obligations under such secured credit agreement to become due and payable, which would result in a default under a number of other outstanding debt securities and could lead to an acceleration of obligations related to these debt securities. A default under the secured credit

9

agreement, indentures or agreements governing other indebtedness could also lead to an acceleration of debt under other debt instruments that contain cross acceleration or cross-default provisions.

International Operations—The Company is subject to risks associated with operating in foreign countries.

The Company operates manufacturing and other facilities throughout the world. Net sales from international operations totaled approximately $5.2 billion, representing approximately 74% of the Company's net sales for the year ended December 31, 2013. As a result of its international operations, the Company is subject to risks associated with operating in foreign countries, including:

- •

- Political, social and economic instability;

- •

- War, civil disturbance or acts of terrorism;

- •

- Taking of property by nationalization or expropriation without fair compensation;

- •

- Changes in governmental policies and regulations;

- •

- Devaluations and fluctuations in currency exchange rates;

- •

- Imposition of limitations on conversions of foreign currencies into dollars or remittance of dividends and other payments by foreign subsidiaries;

- •

- Imposition or increase of withholding and other taxes on remittances and other payments by foreign subsidiaries;

- •

- Hyperinflation in certain foreign countries;

- •

- Impositions or increase of investment and other restrictions or requirements by foreign governments;

- •

- Loss or non-renewal of treaties or other agreements with foreign tax authorities;

- •

- Changes in tax laws, or the interpretation thereof, affecting foreign tax credits or tax deductions relating to our non-U.S. earnings or operations; and

- •

- Complying with the U.S. Foreign Corrupt Practices Act, which prohibits companies and their intermediaries from engaging in bribery or other prohibited payments to foreign officials for the purposes of obtaining or retaining business or gaining an unfair business advantage and requires companies to maintain accurate books and records and internal controls.

The risks associated with operating in foreign countries may have a material adverse effect on operations.

Foreign Currency Exchange Rates—The Company is subject to the effects of fluctuations in foreign currency exchange rates, which could adversely impact the Company's financial results.

The Company's reporting currency is the U.S. dollar. A significant portion of the Company's net sales, costs, assets and liabilities are denominated in currencies other than the U.S. dollar, primarily the Euro, Brazilian real, Colombian peso and Australian dollar. In its consolidated financial statements, the Company translates local currency financial results into U.S. dollars based on the exchange rates prevailing during the reporting period. During times of a strengthening U.S. dollar, the reported revenues and earnings of the Company's international operations will be reduced because the local currencies will translate into fewer U.S. dollars. This could have a material adverse effect on the Company's financial condition, results of operations and cash flows.

10

Competition—The Company faces intense competition from other glass container producers, as well as from makers of alternative forms of packaging. Competitive pressures could adversely affect the Company's financial health.

The Company is subject to significant competition from other glass container producers, as well as from makers of alternative forms of packaging, such as aluminum cans and plastic containers. The Company also competes with manufacturers of non-rigid packaging alternatives, including flexible pouches and aseptic cartons, in serving the packaging needs of certain end-use markets, including juice customers. The Company competes with each rigid packaging competitor on the basis of price, quality, service and the marketing and functional attributes of the container. Advantages or disadvantages in any of these competitive factors may be sufficient to cause the customer to consider changing suppliers and/or using an alternative form of packaging. The adverse effects of consumer purchasing decisions may be more significant in periods of economic downturn and may lead to longer term reductions in consumer spending on glass packaged products.

Pressures from competitors and producers of alternative forms of packaging have resulted in excess capacity in certain countries in the past and have led to capacity adjustments and significant pricing pressures in the rigid packaging market.

High Energy Costs—Higher energy costs worldwide and interrupted power supplies may have a material adverse effect on operations.

Electrical power, natural gas, and fuel oil are vital to the Company's operations as it relies on a continuous energy supply to conduct its business. Depending on the location and mix of energy sources, energy accounts for 10% to 25% of total production costs. Substantial increases and volatility in energy costs could cause the Company to experience a significant increase in operating costs, which may have a material adverse effect on operations.

Global Economic Environment—The global credit, financial and economic environment could have a material adverse effect on operations and financial condition.

The global credit, financial and economic environment could have a material adverse effect on operations, including the following:

- •

- Downturns in the business or financial condition of any of the Company's customers or suppliers could result in a loss of revenues or a disruption in the supply of raw materials;

- •

- Tightening of credit in financial markets could reduce the Company's ability, as well as the ability of the Company's customers and suppliers, to obtain future financing;

- •

- Volatile market performance could affect the fair value of the Company's pension assets and liabilities, potentially requiring the Company to make significant additional contributions to its pension plans to maintain prescribed funding levels;

- •

- The deterioration of any of the lending parties under the Company's revolving credit facility or the creditworthiness of the counterparties to the Company's derivative transactions could result in such parties' failure to satisfy their obligations under their arrangements with the Company; and

- •

- A significant weakening of the Company's financial position or results of operations could result in noncompliance with the covenants under the Company's indebtedness.

11

Business Integration Risks—The Company may not be able to effectively integrate additional businesses it acquires in the future.

The Company may consider strategic transactions, including acquisitions that will complement, strengthen and enhance growth in its worldwide glass operations. The Company evaluates opportunities on a preliminary basis from time to time, but these transactions may not advance beyond the preliminary stages or be completed. Such acquisitions are subject to various risks and uncertainties, including:

- •

- The inability to integrate effectively the operations, products, technologies and personnel of the acquired companies (some of which are located in diverse geographic regions) and achieve expected synergies;

- •

- The potential disruption of existing business and diversion of management's attention from day-to-day operations;

- •

- The inability to maintain uniform standards, controls, procedures and policies;

- •

- The need or obligation to divest portions of the acquired companies;

- •

- The potential impairment of relationships with customers;

- •

- The potential failure to identify material problems and liabilities during due diligence review of acquisition targets;

- •

- The potential failure to obtain sufficient indemnification rights to fully offset possible liabilities associated with acquired businesses; and

- •

- The challenges associated with operating in new geographic regions.

In addition, the Company cannot make assurances that the integration and consolidation of newly acquired businesses will achieve any anticipated cost savings and operating synergies.

Customer Consolidation—The continuing consolidation of the Company's customer base may intensify pricing pressures and have a material adverse effect on operations.

Many of the Company's largest customers have acquired companies with similar or complementary product lines. This consolidation has increased the concentration of the Company's business with its largest customers, the loss of which could have a material adverse effect on operations. In many cases, such consolidation has been accompanied by pressure from customers for lower prices, reflecting the increase in the total volume of products purchased or the elimination of a price differential between the acquiring customer and the company acquired. Increased pricing pressures from the Company's customers may have a material adverse effect on operations.

Seasonality—Profitability could be affected by varied seasonal demands.

Due principally to the seasonal nature of the consumption of beer and other beverages, for which demand is stronger during the summer months, sales of the Company's products have varied and are expected to vary by quarter. Shipments in the U.S. and Europe are typically greater in the second and third quarters of the year, while shipments in the Asia Pacific region are typically greater in the first and fourth quarters of the year, and shipments in South America are typically greater in the third and fourth quarters of the year. Unseasonably cool weather during peak demand periods can reduce demand for certain beverages packaged in the Company's containers.

12

Raw Materials—Profitability could be affected by the availability of raw materials.

The raw materials that the Company uses have historically been available in adequate supply from multiple sources. For certain raw materials, however, there may be temporary shortages due to weather or other factors, including disruptions in supply caused by raw material transportation or production delays. These shortages, as well as material volatility in the cost of any of the principal raw materials that the Company uses, may have a material adverse effect on operations.

Environmental Risks—The Company is subject to various environmental legal requirements and may be subject to new legal requirements in the future. These requirements may have a material adverse effect on operations.

The Company's operations and properties are subject to extensive laws, ordinances, regulations and other legal requirements relating to environmental protection, including legal requirements governing investigation and clean-up of contaminated properties as well as water discharges, air emissions, waste management and workplace health and safety. Such legal requirements frequently change and vary among jurisdictions. The Company's operations and properties must comply with these legal requirements. These requirements may have a material adverse effect on operations.

The Company has incurred, and expects to incur, costs for its operations to comply with environmental legal requirements, and these costs could increase in the future. Many environmental legal requirements provide for substantial fines, orders (including orders to cease operations), and criminal sanctions for violations. These legal requirements may apply to conditions at properties that the Company presently or formerly owned or operated, as well as at other properties for which the Company may be responsible, including those at which wastes attributable to the Company were disposed. A significant order or judgment against the Company, the loss of a significant permit or license or the imposition of a significant fine may have a material adverse effect on operations.

A number of governmental authorities have enacted, or are considering enacting, legal requirements that would mandate certain rates of recycling, the use of recycled materials and/or limitations on certain kinds of packaging materials. In addition, some companies with packaging needs have responded to such developments and/or perceived environmental concerns of consumers by using containers made in whole or in part of recycled materials. Such developments may reduce the demand for some of the Company's products and/or increase the Company's costs, which may have a material adverse effect on operations.

Taxes—Potential tax law changes could adversely affect net income and cash flow.

The Company is subject to income tax in the numerous jurisdictions in which it operates. Increases in income tax rates or other tax law changes could reduce the Company's net income and cash flow from affected jurisdictions. In particular, potential tax law changes in the U.S. regarding the treatment of the Company's unrepatriated non-U.S. earnings could have a material adverse effect on net income and cash flow. In addition, the Company's products are subject to import and excise duties and/or sales or value-added taxes in many jurisdictions in which it operates. Increases in these indirect taxes could affect the affordability of the Company's products and, therefore, reduce demand.

Labor Relations—Some of the Company's employees are unionized or represented by workers' councils.

The Company is party to a number of collective bargaining agreements with labor unions which at December 31, 2013, covered approximately 79% of the Company's employees in North America. Approximately 60% of employees in South America are unionized, although according to the labor legislation of each country, 100% of employees are covered by collective bargaining agreements. The agreement covering substantially all of the Company's union-affiliated employees in its U.S. glass container operations expires on March 31, 2016. The majority of the hourly workers in Australia and

13

New Zealand are also covered by collective bargaining agreements. The collective bargaining agreements in South America, Australia and New Zealand have varying terms and expiration dates. Upon the expiration of any collective bargaining agreement, if the Company is unable to negotiate acceptable contracts with labor unions, it could result in strikes by the affected workers and increased operating costs as a result of higher wages or benefits paid to union members. In Europe, a large number of the Company's employees are employed in countries in which employment laws provide greater bargaining or other rights to employees than the laws of the U.S. Such employment rights require the Company to work collaboratively with the legal representatives of the employees to effect any changes to labor arrangements. For example, most of the Company's employees in Europe are represented by workers' councils that must approve any changes in conditions of employment, including salaries and benefits and staff changes, and may impede efforts to restructure the Company's workforce. Although the Company believes that it has a good working relationship with its employees, if the Company's employees were to engage in a strike or other work stoppage, the Company could experience a significant disruption of operations and/or higher ongoing labor costs, which may have a material adverse effect on operations.

Key Management and Personnel Retention—Failure to retain key management and personnel could have a material adverse effect on operations.

The Company believes that its future success depends, in part, on its experienced management team and certain key personnel. The loss of certain key management and personnel could limit the Company's ability to implement its business plans and meet its objectives.

Joint Ventures—Failure by joint venture partners to observe their obligations could have a material adverse effect on operations.

A portion of the Company's operations is conducted through joint ventures, including joint ventures in the Europe, North America and Asia Pacific segments. If the Company's joint venture partners do not observe their obligations or are unable to commit additional capital to the joint ventures, it is possible that the affected joint venture would not be able to operate in accordance with its business plans, which could have a material adverse effect on the Company's financial condition and results of operations.

Information Technology—Failure or disruption of information technology could disrupt operations and adversely affect operations.

The Company relies on information technology to operate its plants, to communicate with its employees, customers and suppliers, and to report financial and operating results. As with all large systems, the Company's information technology systems could fail on their own accord or may be vulnerable to a variety of interruptions due to events, including, but not limited to, natural disasters, terrorist attacks, telecommunications failures, computer viruses, hackers or other security issues. While the Company has disaster recovery programs in place, failure or disruption of the Company's information technology systems could result in transaction errors, loss of customers, business disruptions, or loss of or damage to intellectual property, which could have a material adverse effect on operations.

The Company continues to undertake the phased implementation of an Enterprise Resource Planning ("ERP") software system. The implementation of a new ERP system poses several challenges related to, among other things, training of personnel, communication of new rules and procedures, migration of data and the potential instability of the system. While the Company has taken steps to mitigate these challenges, the unsuccessful implementation of the ERP system could have a material adverse effect on the Company's operations.

14

Intellectual Property—The loss of the Company's intellectual property rights may negatively impact its ability to compete.

If the Company is unable to maintain the proprietary nature of its technologies, its competitors may use its technologies to compete with it. The Company has a number of patents. The Company's patents may not withstand challenge in litigation, and patents do not ensure that competitors will not develop competing products or infringe upon the Company's patents. Additionally, the Company markets its products internationally and the patent laws of foreign countries may offer less protection than the patent laws in the U.S. The Company also relies on trade secrets, know-how and other unpatented technology, and others may independently develop the same or similar technology or otherwise obtain access to the Company's unpatented technology.

Accounting—The Company's financial results are based upon estimates and assumptions that may differ from actual results.

In preparing the Company's consolidated financial statements in accordance with U.S. generally accepted accounting principles, several estimates and assumptions are made that affect the accounting for and recognition of assets, liabilities, revenues and expenses. These estimates and assumptions must be made because certain information that is used in the preparation of the Company's financial statements is dependent on future events, cannot be calculated with a high degree of precision from data available or is not capable of being readily calculated based on generally accepted methodologies. In some cases, these estimates are particularly difficult to determine and the Company must exercise significant judgment. The Company believes that accounting for long-lived assets, pension benefit plans, contingencies and litigation, and income taxes involves the more significant judgments and estimates used in the preparation of its consolidated financial statements. Actual results for all estimates could differ materially from the estimates and assumptions that the Company uses, which could have a material adverse effect on the Company's financial condition and results of operations.

Accounting Standards—The adoption of new accounting standards or interpretations could adversely impact the Company's financial results.

The Company's implementation of and compliance with changes in accounting rules and interpretations could adversely affect its operating results or cause unanticipated fluctuations in its results in future periods. The accounting rules and regulations that the Company must comply with are complex and continually changing. Recent actions and public comments from the SEC have focused on the integrity of financial reporting generally. The Financial Accounting Standards Board has recently introduced several new or proposed accounting standards, or is developing new proposed standards, which would represent a significant change from current industry practices. In addition, many companies' accounting policies are being subjected to heightened scrutiny by regulators and the public. While the Company believes that its financial statements have been prepared in accordance with U.S. generally accepted accounting principles, the Company cannot predict the impact of future changes to accounting principles or its accounting policies on its financial statements going forward.

Goodwill—A significant write down of goodwill would have a material adverse effect on the Company's reported results of operations and net worth.

Goodwill at December 31, 2013 totaled $2.1 billion. The Company evaluates goodwill annually (or more frequently if impairment indicators arise) for impairment using the required business valuation methods. These methods include the use of a weighted average cost of capital to calculate the present value of the expected future cash flows of the Company's reporting units. Future changes in the cost of capital, expected cash flows, or other factors may cause the Company's goodwill to be impaired, resulting in a non-cash charge against results of operations to write down goodwill for the amount of

15

the impairment. If a significant write down is required, the charge would have a material adverse effect on the Company's reported results of operations and net worth.

Pension Funding—An increase in the underfunded status of the Company's pension plans could adversely impact the Company's operations, financial condition and liquidity.

The Company contributed $96 million, $219 million and $59 million to its defined benefit pension plans in 2013, 2012 and 2011, respectively. The amount the Company is required to contribute to these plans is determined by the laws and regulations governing each plan, and is generally related to the funded status of the plans. A deterioration in the value of the plans' investments or a decrease in the discount rate used to calculate plan liabilities generally would increase the underfunded status of the plans. An increase in the underfunded status of the plans could result in an increase in the Company's obligation to make contributions to the plans, thereby reducing the cash available for working capital and other corporate uses, and may have an adverse impact on the Company's operations, financial condition and liquidity.

ITEM 1B. UNRESOLVED STAFF COMMENTS

None.

16

The principal manufacturing facilities and other material important physical properties of the Company at December 31, 2013 are listed below. All properties are glass container plants and are owned in fee, except where otherwise noted.

| North American Operations | ||

United States | ||

Atlanta, GA | Portland, OR | |

Auburn, NY | Streator, IL | |

Brockway, PA | Toano, VA | |

Crenshaw, PA | Tracy, CA | |

Danville, VA | Waco, TX | |

Lapel, IN | Windsor, CO | |

Los Angeles, CA | Winston-Salem, NC | |

Muskogee, OK | Zanesville, OH | |

Oakland, CA | ||

Canada |

| |

Brampton, Ontario | Montreal, Quebec | |

Asia Pacific Operations | ||

Australia | ||

Adelaide | Melbourne | |

Brisbane | Sydney | |

China |

| |

Shanghai | Xianxian | |

Tianjin | Zhaoqing | |

Tianjin (mold shop) | ||

Indonesia |

| |

Jakarta | ||

New Zealand |

| |

Auckland | ||

European Operations | ||

Czech Republic | ||

Dubi | Nove Sedlo | |

Estonia |

| |

Jarvakandi | ||

France |

| |

Beziers | Vayres | |

Gironcourt | Veauche | |

Labegude | Vergeze | |

Puy-Guillaume | Wingles | |

Reims | ||

Germany |

| |

Bernsdorf | Rinteln | |

Holzminden |

17

Hungary |

| |

Oroshaza | ||

Italy |

| |

Asti | Origgio | |

Aprilia | Ottaviano | |

Bari | San Gemini | |

Marsala | San Polo | |

Mezzocorona | Villotta | |

The Netherlands |

| |

Leerdam | Schiedam | |

Maastricht | ||

Poland |

| |

Jaroslaw | Poznan | |

Spain |

| |

Barcelona | Sevilla | |

United Kingdom |

| |

Alloa | Harlow | |

South American Operations | ||

Argentina | ||

Rosario | ||

Brazil |

| |

Fortaleza | Sao Paulo | |

Recife | Vitoria de Santo Antao (glass container and | |

Rio de Janeiro (glass container and tableware) | tableware) | |

Colombia |

| |

Buga (tableware) | Soacha | |

Envigado | Zipaquira | |

Ecuador |

| |

Guayaquil | ||

Peru |

| |

Callao | Lurin(1) | |

Other Operations | ||

Machine Shops and Engineering Support Center | ||

Brockway, Pennsylvania | Jaroslaw, Poland | |

Cali, Colombia | Lurin, Peru | |

Hawthorn, Australia | Perrysburg, Ohio | |

Corporate Facilities | ||

Hawthorn, Australia(1) | Bussigny-Lausanne, Switzerland(1) | |

Perrysburg, Ohio(1) | ||

- (1)

- This facility is leased in whole or in part.

18

The Company believes that its facilities are well maintained and currently adequate for its planned production requirements over the next three to five years.

For further information on legal proceedings, see Note 13 to the Consolidated Financial Statements.

ITEM 4. MINE SAFETY DISCLOSURES

Not applicable

19

ITEM 5. MARKET FOR REGISTRANT'S COMMON STOCK AND RELATED SHARE OWNER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES

The price range for the Company's common stock on the New York Stock Exchange, as reported by the Financial Industry Regulatory Authority, Inc., was as follows:

| | 2013 | 2012 | |||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| | High | Low | High | Low | |||||||||

First Quarter | $ | 27.66 | $ | 21.82 | $ | 24.83 | $ | 20.24 | |||||

Second Quarter | 28.89 | 24.26 | 24.50 | 18.16 | |||||||||

Third Quarter | 31.27 | 27.74 | 20.05 | 17.07 | |||||||||

Fourth Quarter | 35.78 | 28.82 | 21.37 | 18.57 | |||||||||

The number of share owners of record on December 31, 2013 was 1,202. Approximately 91% of the outstanding shares were registered in the name of Depository Trust Company, or CEDE, which held such shares on behalf of a number of brokerage firms, banks, and other financial institutions. The shares attributed to these financial institutions, in turn, represented the interests of more than 34,000 unidentified beneficial owners. No dividends have been declared or paid since the Company's initial public offering in December 1991 and the Company does not anticipate paying any dividends in the near future. For restrictions on payment of dividends on the Company's common stock, see Management's Discussion and Analysis of Financial Condition and Results of Operations—Capital Resources and Liquidity—Current and Long-Term Debt and Note 12 to the Consolidated Financial Statements.

Information with respect to securities authorized for issuance under equity compensation plans is included herein under Item 12.

The Company purchased 407,000 shares of its common stock during the fourth quarter of 2013 (1.1 million shares for the year) pursuant to authorization by its Board of Directors in August 2012 to purchase up to $75 million of the Company's common stock until December 31, 2013. The following table provides information about the Company's purchases of its common stock during the fourth quarter of 2013:

Issuer Purchases of Equity Securities

Period | Total Number of Shares Purchased (in thousands) | Average Price Paid per Share | Total Number of Shares Purchased as Part of Publicly Announced Plan (in thousands) | Approximate Dollar Value of Shares that May Yet Be Purchased Under the Plan (in millions) | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

October 1 - October 31, 2013 | |||||||||||||

November 1 - November 30, 2013 | 407 | $ | 32.44 | ||||||||||

December 1 - December 31, 2013 | 2,491 | $ | 0 | ||||||||||

In December 2013, the Company's Board of Directors granted authorization to the Company to repurchase up to $100 million of its common stock through December 31, 2015.

20

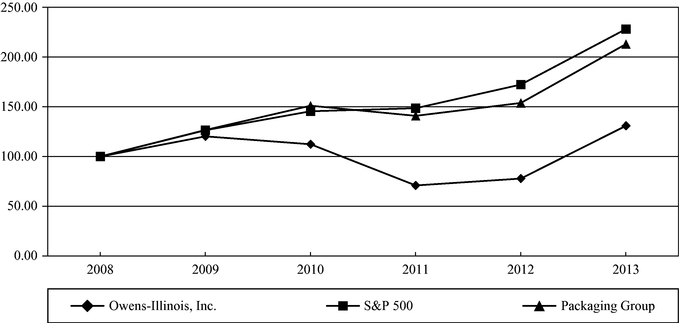

PERFORMANCE GRAPH

COMPARISON OF CUMULATIVE TOTAL RETURN

AMONG OWENS-ILLINOIS, INC., S&P 500, AND PACKAGING GROUP

| | Years Ending December 31, | ||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| | 2008 | 2009 | 2010 | 2011 | 2012 | 2013 | |||||||||||||

Owens-Illinois, Inc. | $ | 100.00 | $ | 120.27 | $ | 112.33 | $ | 70.91 | $ | 77.83 | $ | 130.92 | |||||||

S&P 500 | 100.00 | 126.46 | 145.51 | 148.59 | 172.37 | 228.19 | |||||||||||||

Packaging Group | 100.00 | 126.66 | 151.10 | 140.92 | 153.88 | 213.09 | |||||||||||||

The above graph compares the performance of the Company's Common Stock with that of a broad market index (the S&P 500 Composite Index) and a packaging group consisting of companies with lines of business or product end uses comparable to those of the Company for which market quotations are available.

The packaging group consists of: AptarGroup, Inc., Ball Corp., Bemis Company, Inc., Crown Holdings, Inc., Owens-Illinois, Inc., Sealed Air Corp., Silgan Holdings Inc., and Sonoco Products Co.

The comparison of total return on investment for each period is based on the investment of $100 on December 31, 2008 and the change in market value of the stock, including additional shares assumed purchased through reinvestment of dividends, if any.

21

ITEM 6. SELECTED FINANCIAL DATA

The selected consolidated financial data presented below relates to each of the five years in the period ended December 31, 2013. The financial data for each of the five years in the period ended December 31, 2013 was derived from the audited consolidated financial statements of the Company.

| | Years ended December 31, | |||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| | 2013 | 2012 | 2011 | 2010 | 2009 | |||||||||||

| | (Dollars in millions) | |||||||||||||||

Consolidated operating results(a): | ||||||||||||||||

Net sales | $ | 6,967 | $ | 7,000 | $ | 7,358 | $ | 6,633 | $ | 6,652 | ||||||

Cost of goods sold(b) | (5,636 | ) | (5,626 | ) | (5,969 | ) | (5,281 | ) | (5,316 | ) | ||||||

| | | | | | | | | | | | | | | | | |

Gross profit | 1,331 | 1,374 | 1,389 | 1,352 | 1,336 | |||||||||||

Selling and administrative, research, development and engineering | (568 | ) | (617 | ) | (627 | ) | (554 | ) | (551 | ) | ||||||

Other expense, net(c) | (189 | ) | (181 | ) | (844 | ) | (123 | ) | (347 | ) | ||||||

| | | | | | | | | | | | | | | | | |

Earnings (loss) before interest expense and items below | 574 | 576 | (82 | ) | 675 | 438 | ||||||||||

Interest expense(d) | (239 | ) | (248 | ) | (314 | ) | (249 | ) | (222 | ) | ||||||

| | | | | | | | | | | | | | | | | |

Earnings (loss) from continuing operations before income taxes | 335 | 328 | (396 | ) | 426 | 216 | ||||||||||

Provision for income taxes(e) | (120 | ) | (108 | ) | (85 | ) | (129 | ) | (83 | ) | ||||||

| | | | | | | | | | | | | | | | | |

Earnings (loss) from continuing operations | 215 | 220 | (481 | ) | 297 | 133 | ||||||||||

Earnings from discontinued operations | 31 | 66 | ||||||||||||||

Gain (loss) on disposal of discontinued operations | (18 | ) | (2 | ) | 1 | (331 | ) | |||||||||

| | | | | | | | | | | | | | | | | |

Net earnings (loss) | 197 | 218 | (480 | ) | (3 | ) | 199 | |||||||||

Net earnings attributable to noncontrolling interests | (13 | ) | (34 | ) | (20 | ) | (42 | ) | (36 | ) | ||||||

| | | | | | | | | | | | | | | | | |

Net earnings (loss) attributable to the Company | $ | 184 | $ | 184 | $ | (500 | ) | $ | (45 | ) | $ | 163 | ||||

| | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | |

22

| | Years ended December 31, | |||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| | 2013 | 2012 | 2011 | 2010 | 2009 | |||||||||||

Basic earnings (loss) per share of common stock: | ||||||||||||||||

Earnings (loss) from continuing operations | $ | 1.22 | $ | 1.13 | $ | (3.06 | ) | $ | 1.58 | $ | 0.66 | |||||

Earnings from discontinued operations | 0.14 | 0.31 | ||||||||||||||

Gain (loss) on disposal of discontinued operations | (0.11 | ) | (0.01 | ) | 0.01 | (2.00 | ) | |||||||||

| | | | | | | | | | | | | | | | | |

Net earnings (loss) | $ | 1.11 | $ | 1.12 | $ | (3.05 | ) | $ | (0.28 | ) | $ | 0.97 | ||||

| | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | |

Weighted average shares outstanding (in thousands) | 164,425 | 164,474 | 163,691 | 164,271 | 167,687 | |||||||||||

| | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | |

Diluted earnings (loss) per share of common stock: | ||||||||||||||||

Earnings (loss) from continuing operations | $ | 1.22 | $ | 1.12 | $ | (3.06 | ) | $ | 1.56 | $ | 0.65 | |||||

Earnings from discontinued operations | 0.14 | 0.30 | ||||||||||||||

Gain (loss) on disposal of discontinued operations | (0.11 | ) | (0.01 | ) | 0.01 | (1.97 | ) | |||||||||

| | | | | | | | | | | | | | | | | |

Net earnings (loss) | $ | 1.11 | $ | 1.11 | $ | (3.05 | ) | $ | (0.27 | ) | $ | 0.95 | ||||

| | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | |

Diluted average shares (in thousands) | 165,828 | 165,768 | 163,691 | 167,078 | 170,540 | |||||||||||

| | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | |

For the year ended December 31, 2011, diluted earnings per share of common stock was equal to basic earnings per share of common stock due to the loss from continuing operations.

| | Years ended December 31, | |||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| | 2013 | 2012 | 2011 | 2010 | 2009 | |||||||||||

| | (Dollars in millions) | |||||||||||||||

Other data: | ||||||||||||||||

The following are included in earnings from continuing operations: | ||||||||||||||||

Depreciation | $ | 350 | $ | 378 | $ | 405 | $ | 369 | $ | 364 | ||||||

Amortization of intangibles | 47 | 34 | 17 | 22 | 21 | |||||||||||

Amortization of deferred finance fees (included in interest expense) | 32 | 33 | 32 | 19 | 10 | |||||||||||

Balance sheet data (at end of period): | ||||||||||||||||

Working capital (current assets less current liabilities) | $ | 296 | $ | 486 | $ | 498 | $ | 698 | $ | 800 | ||||||

Total assets | 8,419 | 8,598 | 8,975 | 9,793 | 8,764 | |||||||||||

Total debt | 3,567 | 3,773 | 4,033 | 4,278 | 3,608 | |||||||||||

Share owners' equity | 1,603 | 1,055 | 1,041 | 2,065 | 1,773 | |||||||||||

Free cash flow(f) | $ | 339 | $ | 290 | $ | 220 | $ | 100 | $ | 322 | ||||||

Note that items (b) through (e) below relate to items management considers not representative of ongoing operations.

- (a)

- Amounts for 2009 - 2011 have been adjusted to reflect the retrospective application of a change in the method of valuing U.S. inventories to average cost from last-in, first-out.

Amounts related to the Company's Venezuelan operations have been reclassified to discontinued operations for 2009 - 2010 as a result of the expropriation of those operations in 2010.

23

- (b)

- Amount for 2010 includes charges of $12 million ($7 million after tax amount attributable to the Company) for acquisition-related fair value inventory adjustments.

- (c)

- Amount for 2013 includes charges of $145 million (pretax and after tax) to increase the accrual for estimated future asbestos-related costs and $119 million ($92 million after tax amount attributable to the Company) for restructuring, asset impairment and related charges.

Amount for 2012 includes charges of $155 million (pretax and after tax) to increase the accrual for estimated future asbestos-related costs, $168 million ($144 million after tax amount attributable to the Company) for restructuring, asset impairment and related charges, and a gain of $61 million ($33 million after tax amount attributable to the Company) related to cash received from the Chinese government as compensation for land in China that the Company was required to return to the government.

Amount for 2011 includes charges of $165 million (pretax and after tax) to increase the accrual for estimated future asbestos-related costs, $641 million ($640 million after tax amount attributable to the Company) to write down goodwill in the Asia Pacific segment and $112 million ($91 million after tax amount attributable to the Company) for restructuring, asset impairment and related charges.

Amount for 2010 includes charges of $170 million (pretax and after tax) to increase the accrual for estimated future asbestos-related costs, $13 million ($11 million after tax amount attributable to the Company) for restructuring, asset impairment and related charges, and $20 million (pretax and after tax amount attributable to the Company) for acquisition-related restructuring, transaction and financing costs.

Amount for 2009 includes charges of $180 million (pretax and after tax) to increase the accrual for estimated future asbestos-related costs, $207 million ($180 million after tax amount attributable to the Company) for restructuring, asset impairment and related charges, and $18 million ($17 million after tax amount attributable to the Company) for the remeasurement of certain bolivar-denominated assets and liabilities held outside of Venezuela.

- (d)

- Amount for 2013 includes charges of $9 million (pretax and after tax amount attributable to the Company) for note repurchase premiums.