UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

__________________________________

FORM 8-K

CURRENT REPORT

Pursuant to Section 13 OR 15(d) of the Securities Exchange Act of 1934

Date of Report (date of earliest event reported): November 29, 2006

REHABCARE GROUP, INC.

(Exact name of Company as specified in its charter)

| Delaware | 0-19294 | 51-0265872 | |

| (State or other jurisdiction | (Commission | (I.R.S. Employer | |

| of incorporation) | File Number) | Identification No.) |

| | | | | | | | | | | |

| 7733 Forsyth Boulevard | |

| Suite 2300 | |

| St. Louis, Missouri | 63105 | |

(Address of principal executive offices) | (Zip Code) |

| | | | | | | | |

(314) 863-7422

(Company's telephone number, including area code)

Not applicable

(Former name or former address if changed since last report)

Check the appropriate box below if the Form 8-K filing is intended to simultaneously satisfy the filing obligation of the Company under any of the following provisions:

o Written communications pursuant to Rule 425 under the Securities Act (17 CFR 230.425)

o Soliciting material pursuant to Rule 14a-12 under the Exchange Act (17 CFR 240.14a-12)

o Pre-commencement communications pursuant to Rule 14d-2(b) under the Exchange Act (17 CFR 240.14d-2(b))

o Pre-commencement communications pursuant to Rule 13e-4(c) under the Exchange Act (17 CFR 240.13e-4(c))

Item 7.01 | Regulation FD Disclosure |

Beginning on November 29, 2006, RehabCare executives will make presentations at investor conferences to analysts and in other forums using the slides as included in this Form 8-K as Exhibit 99. Presentations will be made using these slides, or modifications thereof, in connection with other presentations in the foreseeable future.

Information contained in this presentation is an overview and intended to be considered in the context of RehabCare's SEC filings and all other publicly disclosed information. We undertake no duty or obligation to update or revise this information. However, we may update the presentation periodically in a Form 8-K filing.

Forward-looking statements have been provided pursuant to the safe harbor provisions of the Private Securities Litigation Reform Act of 1995. Forward-looking statements involve known and unknown risks and uncertainties that may cause our actual results in future periods to differ materially from forecasted results. These risks and uncertainties may include but are not limited to, our ability to consummate acquisitions and other partnering relationships at reasonable valuations; our ability to integrate acquisitions and other partnering relationships within the expected timeframes and to achieve the revenue, cost savings and earnings levels from such acquisitions and relationships at or above the levels projected; our ability to comply with the terms of our borrowing agreements; changes in governmental reimbursement rates and other regulations or policies affecting reimbursement for the services provided by us to clients and/or patients; the operational, administrative and financial effect of our compliance with other governmental regulations and applicable licensing and certification requirements; our ability to attract new client relationships or to retain and grow existing client relationships through expansion of our service offerings and the development of alternative product offerings; the future financial results of any unconsolidated affiliates; the adequacy and effectiveness of our operating and administrative systems; our ability to attract and the additional costs of attracting and retaining administrative, operational and professional employees; shortages of qualified therapists and other healthcare personnel; significant increases in health, workers compensation and professional and general liability costs; litigation risks of our past and future business, including our ability to predict the ultimate costs and liabilities or the disruption of our operations; competitive and regulatory effects on pricing and margins; our ability to effectively respond to fluctuations in our census levels and number of patient visits; the proper functioning of our information systems; natural disasters and other unexpected events which could severely damage or interrupt our systems and operations; and general and economic conditions, including efforts by governmental reimbursement programs, insurers, healthcare providers and others to contain healthcare costs.

Item 9.01 | Financial Statements and Exhibits. |

| (d) | Exhibits - See exhibit index |

SIGNATURE

Pursuant to the requirements of the Securities Exchange Act of 1934, the company has duly caused this report to be signed on its behalf by the undersigned hereunto duly authorized.

Dated: November 29, 2006

By: /s/ Jay W. Shreiner

Name: Jay W. Shreiner

Title: Senior Vice President and

Chief Financial Officer

EXHIBIT INDEX

99 | Investor Relations Presentation in use beginning November 29, 2006. |

Exhibit 99

Investor Presentation

Third Quarter, 2006

0

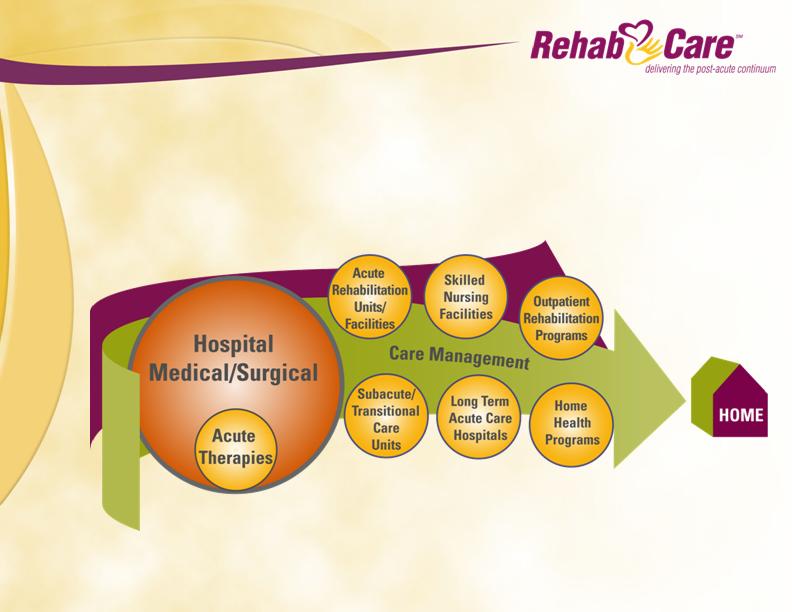

RehabCare aspires to be an integrated post acute rehabilitation services

company delivering rehabilitation care within strategic markets in the most

cost effective and appropriate care setting consistent with patients’ clinical

needs. We currently manage rehabilitation programs in host hospitals,

health systems and skilled nursing facilities and we own inpatient

rehabilitation facilities and long-term acute care hospitals.

Our Strategic Vision

1

Why We Believe In This Vision

Transforms disparate sites of rehabilitation into an

integrated delivery network enabling more:

Efficient deployment of therapists

Effective retention and recruitment of therapists

Focused allocation of corporate resources to strategic markets

Aligns with Medicare’s directional goals

Facilitates development of a common patient assessment tool to

channel patients to different clinical venues based on needs

Positions the Company for episodic post acute single payment

system

Leverages cost management and patient management across all

major rehabilitation settings

Diversifies operating portfolio across clinical settings,

customers and markets

Aligns with other healthcare services that are managed and

delivered on a local market basis

2

What We Do

Skilled Nursing Facility-Based Rehabilitation Programs

1,253 programs – 8 million patient visits annually

Hospital-Based Rehabilitation Programs – 173 Total Units

Acute Rehabilitation Units

117 programs –46,000 discharges annually

Subacute/Transitional Care Units

18 units –137,000 patient days annually

Outpatient Rehabilitation Programs

38 units –1.1 million visits annually

Freestanding Hospitals (8 solely and 1 jointly owned)

6 Inpatient Rehabilitation Hospitals

256 Beds – 2700 discharges annually

3 Long-Term Acute Care Hospitals

186 Beds – 1600 discharges annually

Other Healthcare Services

Phase 2 – consulting services for acute care hospitals

Polaris Group - consulting services for long-term care facilities

VTA Management Services – therapist staffing for SNFs and schools in

New York

3

Where We Are

Continuum Markets

Hospital-Based

Skilled-Nursing Based

Freestanding Hospitals

More than 1,400 locations treating 24,000 patients each day

4

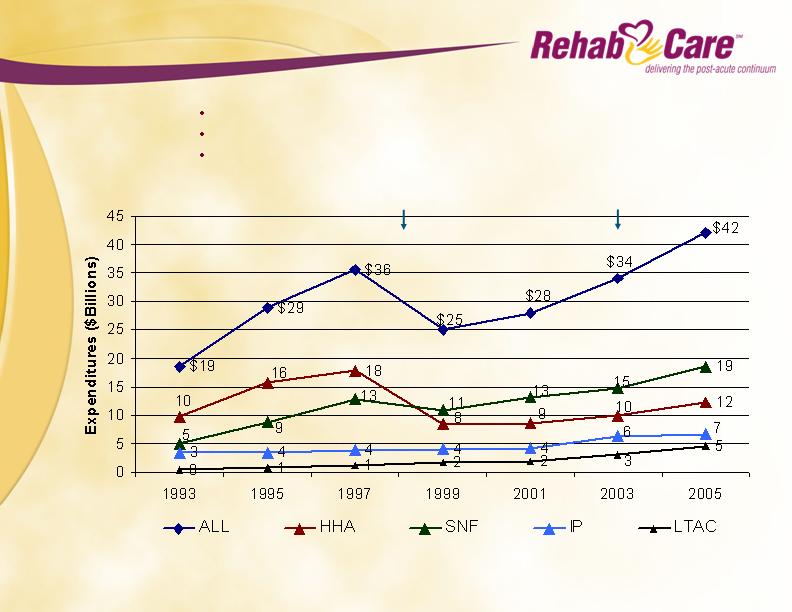

Medicare Reimbursement for

Post-Acute Services

Medicare reimbursement for post-acute services:

Totaled $42 billion in 2005, an increase of 68% since 1999

Projected $97 billion by 2014

Represents 13% of Medicare’s total spending

CMS contains costs by its PPS adjustments and regulations

HH & SNF PPS

IRF PPS

5

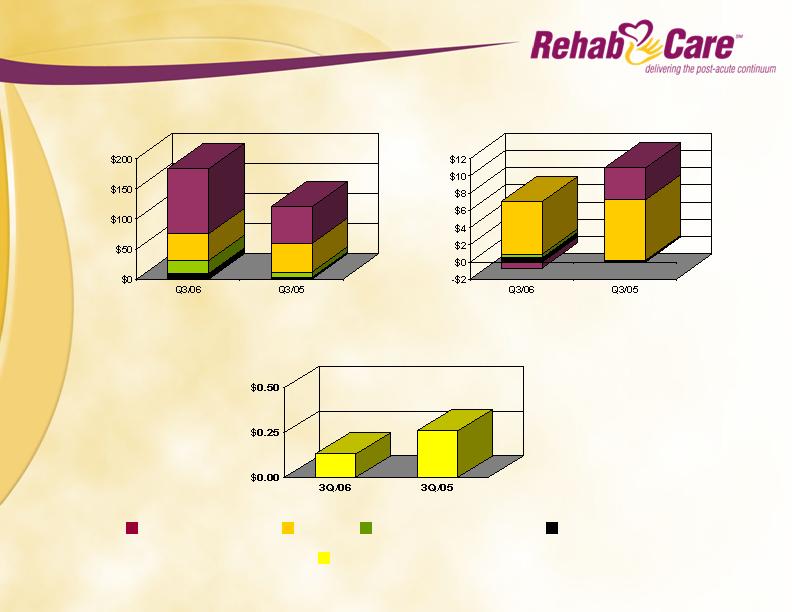

Hospital-Based

Rehabilitation Programs

(HRS Division)

$44.3M

SNF-Based

Rehabilitation Programs

(Contract Therapy Division)

$107.7M

Total Revenue $183.2 million

3Q/06

Other Healthcare

Services

$9.8M

5%

24%

59%

Freestanding

Hospitals

(IRFs and LTACHs)

$21.4M

12%

Our Revenue Trends

Hospital-Based

Rehabilitation Programs

(HRS Division)

$48.4M

SNF-Based

Rehabilitation Programs

(Contract Therapy Division)

$42.9M

Total Revenue $93.3 million

3Q/04

Other Healthcare

Services

$2.0M

2%

46%

52%

6

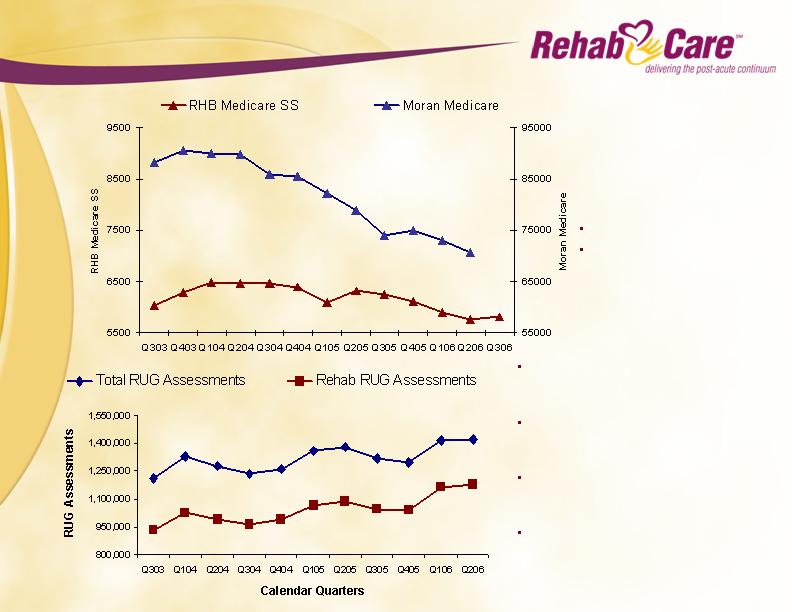

Our Revenues Follow Patient Care

Trends

In the time period studied by

Moran Report, September

2006:

Moran facilities declined 20%

RehabCare facilities

decreased 4%

Since Q3/03, RUG assessments

nationally increased 17% (208,000 days

per quarter)

Rehab RUG assessments in that period

increased 26% (243,000 days per

quarter)

During the same period, the number of

skilled facilities nationally remained

relatively stable

The number of rehabilitation

assessments outpaced the overall

increase in total assessments

7

Skilled Nursing Facility-Based

Rehabilitation

Largest Medicare post acute reimbursement setting

Growing care setting, in part due to 75% Rule

Lower operating margins require scale for better economies and

improve profitability

Acquisition of Symphony

Adds critical mass for selective markets; entry into other

markets

Adds significant therapist resources and client relationships

Provides $10-14 million projected annualized cost savings and

productivity improvements over 18 months

Continuum of Care Differentiation – Best Suited For Patients Who:

Have immediately preceding three-day hospital stay

Are unable to tolerate three hours of physical therapy daily

Have chronic complications and comorbidities

Average length of stay of about 30 days

8

Hospital-Based Rehabilitation

Provides 3-5 year contractual relationships with host hospitals

and health systems with existing market share and flow of

patients

Remains highest margin business with cash flows to fund other

businesses

Expect 3-5% historical growth to return after full implementation

of 75% Rule

Continuum of Care Differentiation – Best Suited For Patients Who:

Meet acute severity of illness, intensity of service and medical

stability criteria

Cannot be managed in less acute care settings

Qualify under one of 35 Case Mix Groups

Tolerate three hours of therapy daily for inpatient; ambulatory for

outpatient

Average length of stay of about 12 days

9

Freestanding Hospitals

Provides anchor operations in continuum markets

Continues strategy of working with host hospitals and health

systems with existing market share and flow of patients

Establishes ownership position and reduces risk of contract loss

Provides a vehicle for expansion of bed capacity

Enhances control over quality and competency in clinical and

medical matters

Continuum of Care Differentiation – Best Suited For Patients Who:

IRFs

Same differentiation as hospital-based rehabilitation; same

average length of stay

LTACHs

Complication and comorbidities requiring special treatment

such as ventilators or significant wound care

Average length of stay > 25 days

10

Freestanding Hospitals

Joint Venture Strategy

Definitive Agreement – Previously Announced

Austin -

Phase 1 - 20-bed IRF – open mid-2007

Phase 2 - replace 20-bed IRF with 36-bed IRF and

40-bed LTACH

North Kansas City – 35-bed LTACH – open early 2008

Other Development Projects

Chesterfield - 35-bed IRF – open late 2008 – certificate of

need filed Nov 2006

5 joint venture projects in various stages of development

Anticipate opening 2 to 3 facilities in 2007

11

3Q/06 Versus 3Q/05

$183.2

$120.0

Revenues (in millions)

Operating Earnings (in millions)

$6.3

$10.9

Consolidated Earnings Per Share

$0.13

$0.26*

Contract Therapy

HRS

Freestanding Hospitals

Other Healthcare Services

Consolidated

*Includes after tax losses on RehabCare’s equity investment in InteliStaf of $2.0 million.

12

Sources

Strong cash flows from operations - $22.4 million TTM

$121 million outstanding debt under $175 million

revolving credit facility (expandable to $225 million)

$8.3 million in subordinated debt related to acquisitions

at 9/30/06

Project $10–15 million debt paydown during Q4/06

Uses

Acquisitions of businesses - $135.9 million TTM

Investment in information technology – approaching $7.0

million TTM

Sources and Uses Of Capital

13

Improve margins in all businesses

Integration of Symphony and synergy realization

Roll out handheld technology and train new personnel

Grow freestanding hospital business

Joint ventures and acquisitions

Labor resources

Attract and deploy therapists

Expand staffing coordination

Grow campus recruiting

More fully develop continuum market strategy

Better manage scarce resources

Focus business development efforts

Client retention

Develop closer partnerships using technology and clinical resources

Impact of regulation

75% Rule, Part B Therapy Caps, Physician Fee Schedule, Fiscal

Intermediary activism

Current Key Initiatives

14

Medicare Reimbursement Initiatives

Impacting Rehabilitation Services

75% Rule

Limits the type and number of

rehabilitation patients that can be

cared for in an acute hospital

setting

Part B Therapy Caps

Limits the amount of therapy

services which can be provided to

Part B patients in skilled nursing

facilities

Physician Fee Schedule

Establishes amounts physicians

(including therapists) can be

reimbursed for Part B services.

Controlled annually by CMS,

MedPAC and Congress

Current operating at 64% compliance

in the 60% compliance requirement

Goes to 65% in 7/07 and 75% in 7/08

Recovered from therapy caps

initiated Jan 1, 2006

Caps return Jan 1, 2007 without

Congressional action

Published changes, including 5%

rate reduction, will be implemented

Jan 1, 2007 without Congressional

action

Part B revenues represent about 35%

of our skilled nursing revenues

15

Executing On Our Strategy – Key

Accomplishments

Strong revenue growth

Created a 9 facility IRF and LTACH hospital division through

acquisitions and de novo site developments

Acquired Symphony Health Services with 470 SNFs and

approximately $207 million in annual revenues

Profiled 87 markets where we have significant presence in

terms of clients, resources or a care continuum

47% of our units are located in these markets

Developed 15 practice guidelines to improve our

consistency of care in cases such as spinal cord injury and

cognitive and communication disorders

Developed a campus recruiting strategy to attract therapy

graduates to units in our markets

Formed the Allied Health Research Institute to support

allied health research, education and training

16

Safe Harbor

Forward-looking statements have been provided pursuant to the safe harbor provisions of the Private

Securities Litigation Reform Act of 1995. Forward-looking statements involve known and unknown

risks and uncertainties that may cause our actual results in future periods to differ materially from

forecasted results. These risks and uncertainties may include but are not limited to, our ability to

consummate acquisitions and other partnering relationships at reasonable valuations; our ability to

integrate acquisitions and other partnering relationships within the expected timeframes and to

achieve the revenue, cost savings and earnings levels from such acquisitions and relationships at or

above the levels projected; our ability to comply with the terms of our borrowing agreements; changes

in governmental reimbursement rates and other regulations or policies affecting reimbursement for

the services provided by us to clients and/or patients; the operational, administrative and financial

effect of our compliance with other governmental regulations and applicable licensing and

certification requirements; our ability to attract new client relationships or to retain and grow existing

client relationships through expansion of our service offerings and the development of alternative

product offerings; the future financial results of any unconsolidated affiliates; the adequacy and

effectiveness of our operating and administrative systems; our ability to attract and the additional

costs of attracting and retaining administrative, operational and professional employees; shortages of

qualified therapists and other healthcare personnel; significant increases in health, workers

compensation and professional and general liability costs; litigation risks of our past and future

business, including our ability to predict the ultimate costs and liabilities or the disruption of our

operations; competitive and regulatory effects on pricing and margins; our ability to effectively

respond to fluctuations in our census levels and number of patient visits; the proper functioning of

our information systems; natural disasters and other unexpected events which could severely damage

or interrupt our systems and operations; and general and economic conditions, including efforts by

governmental reimbursement programs, insurers, healthcare providers and others to contain

healthcare costs.

17

Investor Presentation

Third Quarter, 2006

18