Exhibit 99

Investor Presentation

Third Quarter 2008

1

$721 million consolidated

revenues(1)

revenues(1)

Hospital Rehabilitation Services Division

$161 million revenue - 22% of revenue (1)

• 156 hospital-based programs

• 31 states

• 44,500 inpatient and skilled nursing unit discharges/year (1)

• 950,000 annual outpatient visits (1)

$106 million revenue - 15% of revenue (1)

Hospital Division

• 5 LTACHs, 5 rehabilitation hospitals

• 1 rehabilitation hospital minority owned (2)

• 7 states (3)

• 483 beds (3)

• 6,500 annual patient discharges (1) (3)

Other Healthcare Services Division

$38 million revenue - 5% of revenue (1)

• Phase 2 Consulting - - consulting and care management for hospitals and health systems

• Polaris Group - consulting for long-term care facilities

• VTA Management Services - therapy and nurse staffing for New York

(1) For twelve months ended 9/30/08

(2) Not included in consolidated

revenues

revenues

(3) These statistics include the

minority-owned rehab hospital

minority-owned rehab hospital

$416 million revenue - 58% of revenue (1)

Contract Therapy Division

• 1,075 skilled nursing facility programs

• 40 states

• 7.5 million annual patient visits (1)

Service Lines

2

The Contract Therapy division manages skilled nursing facility (SNF) rehab programs that are

designed to provide therapy intervention to both short-stay patients and long-term residents with a

wide range of conditions, including neurological, orthopedic and other conditions common to the

geriatric patient.

designed to provide therapy intervention to both short-stay patients and long-term residents with a

wide range of conditions, including neurological, orthopedic and other conditions common to the

geriatric patient.

Competitive Landscape

Company

• Self-Operation

• RehabCare

• Aegis Therapies

• Genesis

• Kindred - Peoplefirst

• Sundance

• Select Medical

• EnduraCare

• Skilled Healthcare

Owned

>12,000

0

N/A

~200

228

108

0

0

75

Source: Information available from public filings or from company websites

Managed

0

1,075

N/A

~500

345

317

~400

~300

114

Total

>12,000

1,075

>1,000

~700

573

425

~400

~300

189

Contract Therapy (CT)

Market Overview

Market Overview

Market Size

• 17,000 Medicare certified skilled nursing facilities

3

Part B Therapy Caps & Physician Fee Schedule (PFS)

On July 15, 2008, Congress overrode a Presidential veto to pass the

Medicare Improvements for Patients and Providers Act of 2008. This law:

Medicare Improvements for Patients and Providers Act of 2008. This law:

• Reinstates the therapy cap exceptions process for Part B patients

through December 31, 2009, which had expired June 30, 2008

through December 31, 2009, which had expired June 30, 2008

• Continues 0.5% physician increase for 2008 and provides an additional

1.1% increase for physicians in 2009, in lieu of a scheduled 10.6%

reduction

1.1% increase for physicians in 2009, in lieu of a scheduled 10.6%

reduction

We are pressing our trade groups toward finalizing an alternative to the therapy

cap exception process.

cap exception process.

2009 Final Rule

On July 31, 2008, CMS issued its final rule for SNFs, which went into effect

October 1. The final rule delays implementation of a recalibration of RUG

(Resource Utilization Group) categories and includes a market basket increase of

3.4% for FY09.

October 1. The final rule delays implementation of a recalibration of RUG

(Resource Utilization Group) categories and includes a market basket increase of

3.4% for FY09.

Contract Therapy

Legislative/Regulatory Environment

Legislative/Regulatory Environment

4

Contract Therapy

Performance

Performance

Dollars in millions | Q3 08 | Q2 08 | Q1 08 | Q4 07 |

Operating Revenues | $105.6 | $106.3 | $104.3 | $99.4 |

Operating Earnings | $6.6 | $5.6 | $3.8 | $4.0 |

Number of Locations End of Period | 1,075 | 1,053 | 1,038 | 1,064 |

Outlook

• Raising operating earnings margin target to a range of 5.5% to 6.5% for the

fourth quarter

fourth quarter

• Modest net increase in locations for the remainder of 2008

• Overall strong operating performance

• Operating earnings margin improved from 3.2% in Q3 07 to 6.2% in Q3

08, which exceeded guidance range of 4.5% to 5.5%

08, which exceeded guidance range of 4.5% to 5.5%

• Same store revenue increased $10.0 million or 11.8% in Q3 08 compared

to year ago period

to year ago period

• Net gain in operating units for two consecutive quarters

5

Acute care hospital-based inpatient rehabilitation facilities (IRFs) in RehabCare’s Hospital

Rehabilitation Services (HRS) division are for patients who require early, intensive therapies (at

least 3 hours/day 5 days/week) for recovery from stroke, brain injury, neurological disorders,

amputation and other disabling injuries and illnesses. Outpatient therapy programs provide

proactive, exercise-oriented therapy with hands-on treatment for individuals of all ages.

Rehabilitation Services (HRS) division are for patients who require early, intensive therapies (at

least 3 hours/day 5 days/week) for recovery from stroke, brain injury, neurological disorders,

amputation and other disabling injuries and illnesses. Outpatient therapy programs provide

proactive, exercise-oriented therapy with hands-on treatment for individuals of all ages.

Competitive Landscape (Acute care hospital-based IRFs)

• Self-Operation

• RehabCare (110)

• Horizon Health (Physical Rehab Services) (>20)

• HealthSouth (11)

• Milestone(1)

• TherEx (formerly National Rehab Partners)(1)

(1) Private company or a subsidiary of a public company; number of locations is not available

Source: Information available from public filings or from company websites

Hospital Rehabilitation Services (HRS)

Market Overview

Market Overview

Market Size

• 5,000 acute care hospitals (approximately 1,000 hospital-based IRFs)

6

Hospital Rehab Services

Performance

Performance

Dollars in millions | Q3 08 | Q2 08 | Q1 08 | Q4 07 |

Operating Revenues | $41.6 | $40.2 | $40.2 | $38.8 |

Operating Earnings | $6.2 | $5.3 | $4.6 | $6.0 |

Number of Locations End of Period | 156 | 154 | 153 | 154 |

IRF Discharges | 10,569 | 10,309 | 10,276 | 10,190 |

Outlook

• Raised operating earnings margin target to range of 13% to 16% for the fourth quarter

• Modest increase in IRF units

• 3% - 5% growth in same store discharges YOY in the fourth quarter

• Operating earnings margin reached 15.0% in Q3 08, which was the upper end of

guidance range of 12% - 15%

guidance range of 12% - 15%

• Unit and revenue growth are returning to HRS following legislatively enacted freeze

of CMS 13 Rule at 60% in December 2007

of CMS 13 Rule at 60% in December 2007

• Same store IRF discharges increase by 3.7% in Q3 08 compared to year ago

same period

same period

• Unit count in Q3 08 increased for the second consecutive quarter

• Five signed but unopened IRF contracts with three scheduled to open in Q4 08

7

Inpatient rehabilitation facilities (IRFs) are equipped to treat patients with a wide range of

debilitating injuries and illnesses, offering inpatient and outpatient services in a home-like

environment. Long-term acute care hospitals (LTACHs) are specialty care hospitals designed

for extended stay patients with complex and chronic conditions.

debilitating injuries and illnesses, offering inpatient and outpatient services in a home-like

environment. Long-term acute care hospitals (LTACHs) are specialty care hospitals designed

for extended stay patients with complex and chronic conditions.

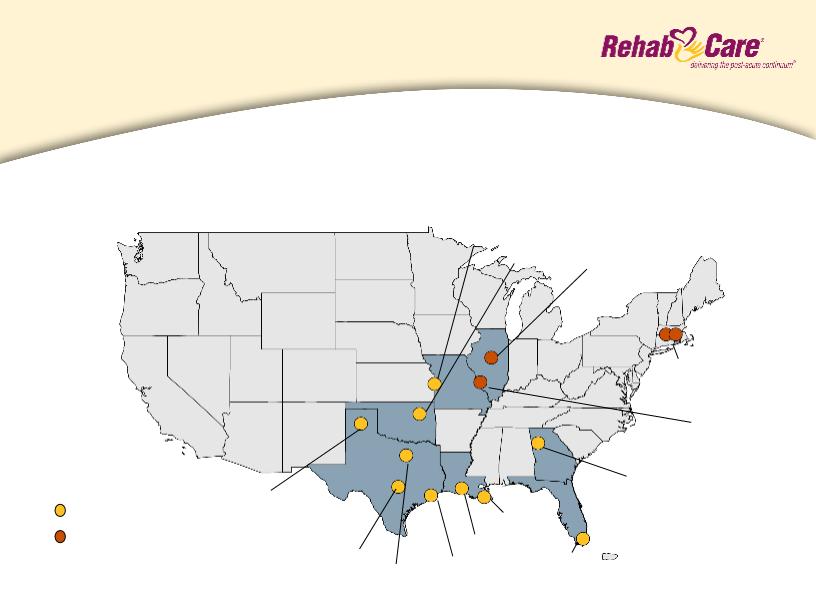

Hospital Division

Description and Locations

Description and Locations

Arlington, TX

Providence, RI

St. Louis, MO

N. Kansas City, MO

Tulsa, OK

Miami, FL

Houston, TX

New Orleans, LA

Amarillo, TX

Austin, TX

Rome, GA

Lafayette, LA

Peoria, IL

Current locations

Future locations

8

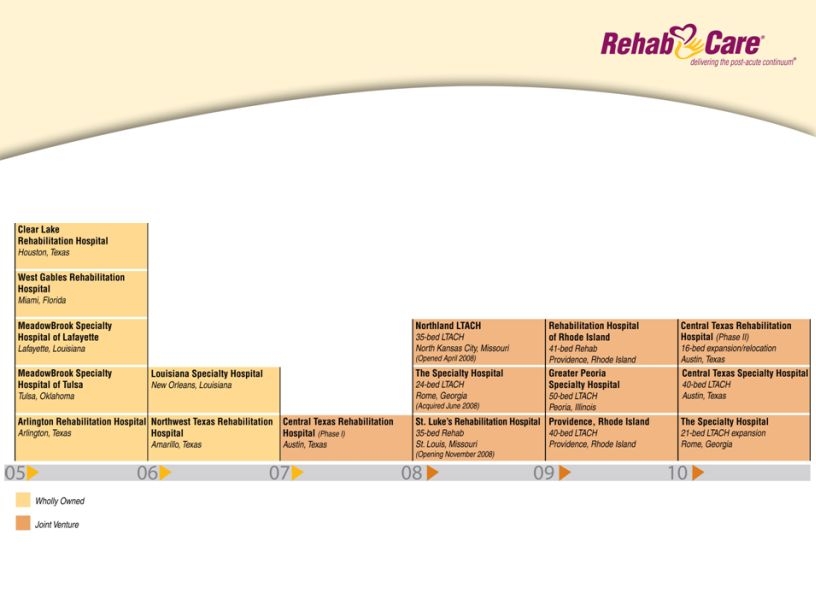

Hospital Division

Development Timeline

Development Timeline

• 10 existing hospitals, 4 in development including 1 awaiting

State Attorney General approval, 2 expansions

State Attorney General approval, 2 expansions

• Two development projects (Kokomo, IN and Reading, PA

LTACHs) canceled in third quarter

LTACHs) canceled in third quarter

9

Market Size:

• 240+ IRFs

Competitive Landscape

• Select Medical (88)

• Kindred (83)

• Regency Hospital (23)

• Triumph Healthcare (20)

• LifeCare (20)

• Vibra Healthcare (12)

• Cornerstone Healthcare (9)

• Ernest Health (8)

• HealthSouth (6)

• RehabCare (5)

Market Size:

• 460+ LTACHs

Freestanding IRFs

LTACHs

(1)Includes minority-owned hospital

Source: Information available from public filings or from company websites

Hospital Division

Market Overview

Market Overview

Competitive Landscape

• HealthSouth (93)

• RehabCare (6)(1)

• Ernest Health (6)

• Select Medical (4)

• Vibra Healthcare (4)

• Centerre (4)

10

Hospital Division

Performance

Dollars in millions | Q3 08 | Q2 08 | Q1 08 | Q4 07 |

Operating Revenues | $27.5 | $27.2 | $27.5 | $23.8 |

Operating Earnings (loss) | $(5.5) | $(3.5) | $(0.1) | $(0.7) |

Number of IRFs End of Period | 5 | 5 | 5 | 5 |

IRF Patient Discharges | 994 | 1,045 | 1,076 | 962 |

60% Compliance Level (Avg) | 59.4% | 58.5% | 59.7% | 63.6% |

Number of LTACHs End of Period | 5 | 5 | 3 | 3 |

LTACH Patient Discharges | 498 | 422 | 416 | 407 |

Outlook

• Expect operating loss of $3.7 to $4.7 million, which includes start-up and ramp-

up losses associated with Northland LTAC and St. Luke’s Rehabilitation

Hospitals, in the fourth quarter

up losses associated with Northland LTAC and St. Luke’s Rehabilitation

Hospitals, in the fourth quarter

• Operating losses have been the result of:

• Uneven operating performance among mature hospitals

• Start-up/ramp-up losses from new hospitals (aggregate $5.0 million over the past 4

quarters)

quarters)

• Higher SG&A related to infrastructure investments to support growing portfolio of hospitals

11

(dollars in millions except per share) | 3Q 08 | 2Q 08 | 1Q 08 | 4Q 07 |

Operating Revenues | $182.6 | $183.9 | $182.4 | $171.8 |

Operating Earnings | $7.0 | $7.7(1) | $8.6 | $9.1 |

Net Earnings | $4.0 | $4.5(1) | $4.5 | $5.1 |

Diluted Earnings Per Share | $0.22 | $0.25(1) | $0.25 | $0.29 |

(1) Includes a favorable pretax net settlement on a non-compete agreement of $0.6 million, or $0.4

million after tax and $0.02 per diluted share.

million after tax and $0.02 per diluted share.

• Improved operating earnings performance in CT and HRS

divisions has been masked by operating losses in the Hospital

division

divisions has been masked by operating losses in the Hospital

division

Consolidated Financial Summary

12

(Dollars in thousands)

Cash and Cash Equivalents

Total Assets

Total Debt

Stockholders’ Equity

Percent of Debt to Total Capital

6/30/08

9/30/08

$ 14,345

426,704

71,000

$255,903

22%

$ 12,405

415,953

52,000

$261,371

17%

• Cash flow from operations totaled $32.0 million for nine months

ended September 30, 2008. Debt was reduced by $19.0 million

in the third quarter

ended September 30, 2008. Debt was reduced by $19.0 million

in the third quarter

Consolidated Balance Sheet

13

• Continue to implement action plan for turning around Hospital

division, which includes strengthening field management,

centralizing business functions, trimming overhead, ramping

up market development efforts and reevaluating the

development pipeline

division, which includes strengthening field management,

centralizing business functions, trimming overhead, ramping

up market development efforts and reevaluating the

development pipeline

• Maintain targeted margins in operating divisions

• Grow operating revenues sequentially through

− same store growth

− net increases in units for all divisions

• Address therapist supply issue through academic

partnerships, campus relations/recruiting and innovative

initiatives like the Allied Health Research Institute

partnerships, campus relations/recruiting and innovative

initiatives like the Allied Health Research Institute

Primary Objectives

14

Investment Considerations

Why RehabCare?

Why RehabCare?

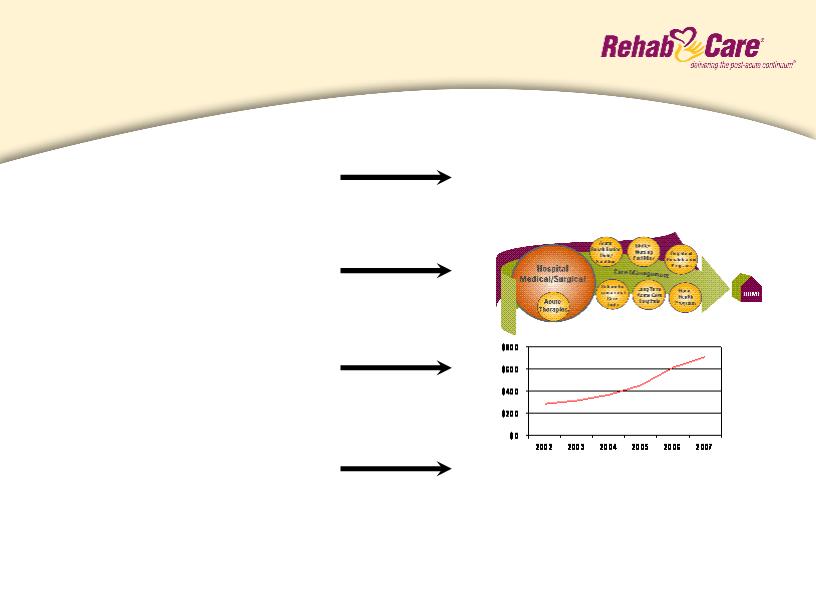

Increasing market demand

Unique continuum of care model

Demonstrated ability to grow revenue

organically and through acquisitions

organically and through acquisitions

Proven ability to adapt to market

and regulatory changes

Expenditures for post-acute services:

ü Grew $20.4 billion from 2000-2007

ü Projected increase of 150% by 2016

ü Represents 15% of Medicare fee-for-

service spending

service spending

ü PPS

ü 75% rule

ü Part B therapy caps

ü LTACH 25% rule

One of the longest tenured post-acute providers (established in 1982)

Revenues1

1 excludes StarMed

15

Forward-looking statements have been provided pursuant to the safe harbor provisions of the

Private Securities Litigation Reform Act of 1995. Such statements are based on the Company’s

current expectations and could be affected by numerous factors, risks and uncertainties discussed in

the Company’s filings with the Securities and Exchange Commission, including the Company’s most

recent annual report on Form 10-K, subsequent quarterly reports on Form 10-Q and current reports

on Form 8-K. Do not rely on forward looking statements as the Company cannot predict or control

many of the factors that ultimately may affect the Company’s ability to achieve the results estimated.

The Company makes no promise to update any forward looking statements whether as a result of

changes in underlying factors, new information, future events or otherwise.

Private Securities Litigation Reform Act of 1995. Such statements are based on the Company’s

current expectations and could be affected by numerous factors, risks and uncertainties discussed in

the Company’s filings with the Securities and Exchange Commission, including the Company’s most

recent annual report on Form 10-K, subsequent quarterly reports on Form 10-Q and current reports

on Form 8-K. Do not rely on forward looking statements as the Company cannot predict or control

many of the factors that ultimately may affect the Company’s ability to achieve the results estimated.

The Company makes no promise to update any forward looking statements whether as a result of

changes in underlying factors, new information, future events or otherwise.

Safe Harbor