Investor Presentation

Fourth Quarter 2008

Exhibit 99

1

n $427 mm revenue - 57% of revenue

n 1,068 skilled nursing facility (SNF)

programs

n 39 states

n 7.6 million annual patient visits

Contract Therapy Division (CT)

Hospital Rehabilitation Services Division (HRS)

n $166 mm revenue - 22% of revenue

n 157 hospital-based programs

n 32 states

n 45,600 inpatient rehabilitation facility (IRF)

and skilled nursing unit discharges/year

and skilled nursing unit discharges/year

n 983,000 annual outpatient visits

Hospital Division (HD)

Other Healthcare Services Division

n $40 mm revenue - 6% of revenue

n Phase 2 Consulting - consulting and

care management for hospitals and

health systems

care management for hospitals and

health systems

n Polaris Group - consulting for long-term

care facilities

care facilities

n VTA Management Services - therapy

and nurse staffing for New York

and nurse staffing for New York

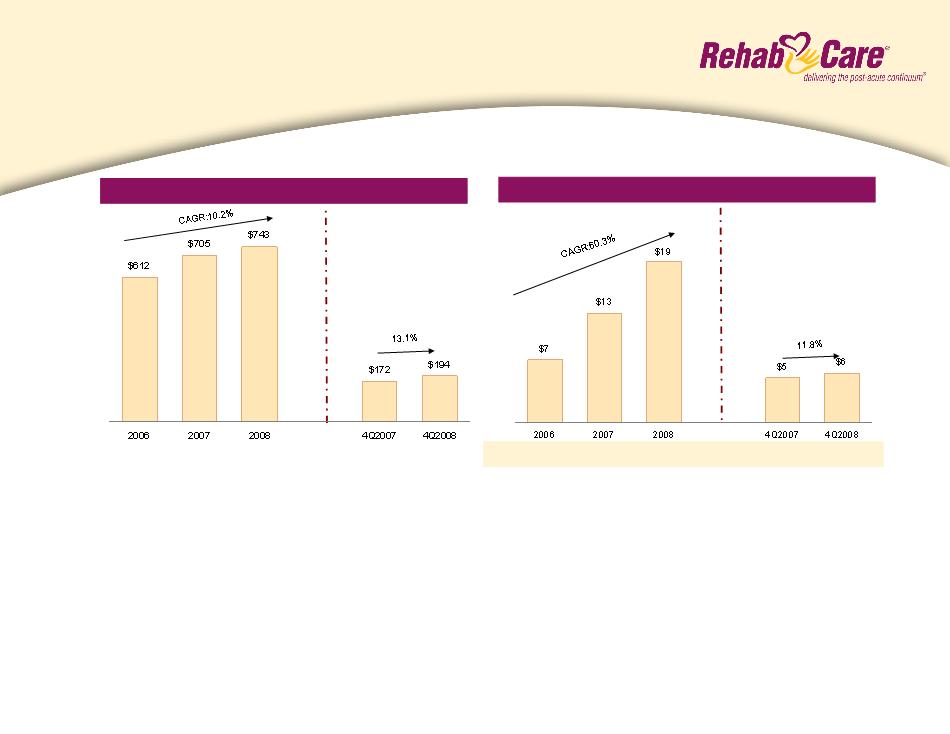

$743 mm consolidated revenues in 2008

Note: All statistics for the twelve months ended 12/31/08, divisional revenues include inter business unit revenues of $2mm

1 Not included in consolidated revenues

2 These statistics include the minority-owned rehab hospital

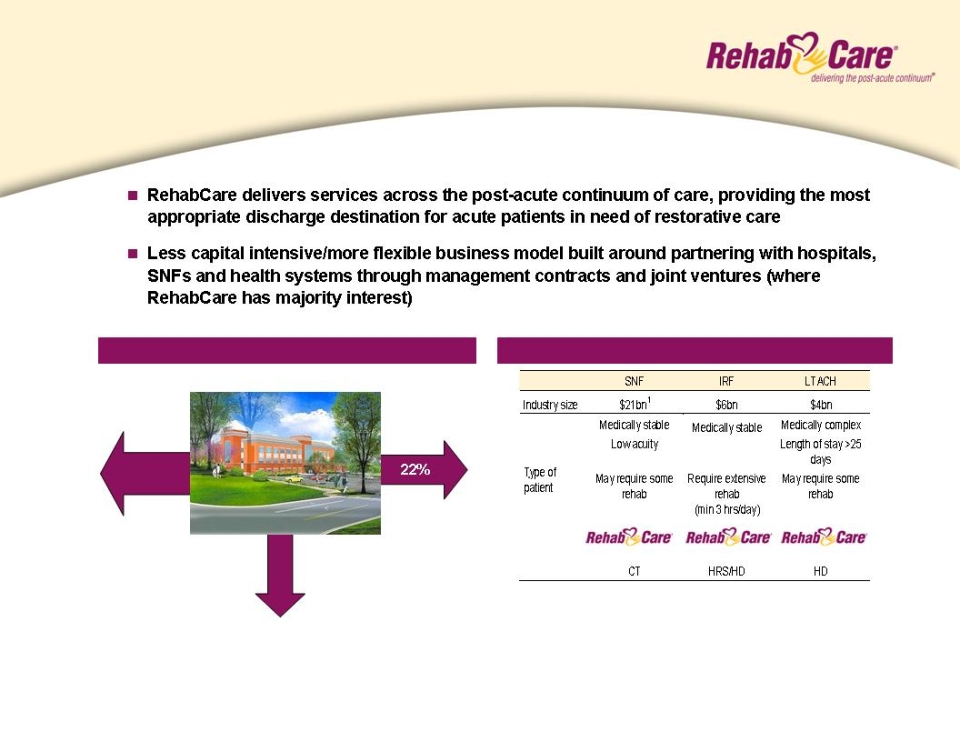

RehabCare at a glance

Operating divisions

Operating divisions

2

SNF/IRF/LTACH

No post

acute care

acute care

Hospice/Home Health

Source: MedPAC, equity research estimates

1 Of the $21bn SNF market size, $6bn is the market potential for Contract Therapy

Patient Discharge Destination

Overview of post-acute settings

65%

13%

Acute care hospital

RehabCare at a glance

The back door to acute care providers

The back door to acute care providers

3

n Manages rehab programs for SNFs

n Each Medicare certified SNF is required to provide physical, speech and occupational therapy, but many lack the

management know-how and/or scale to effectively manage a program

n RehabCare provides a compelling value proposition to our SNF partners

n Access to advanced technology platform that provides for more efficient utilization of therapists and management

resources, improved patient outcomes and increased SNF reimbursement

n Broader array of services

n Better access to scarce therapist labor pool

n Market size¹

n 15,800 Medicare certified skilled nursing facilities

Source: Information available from public filings or from company websites

¹ Source: MedPAC and Congressional Budget Office

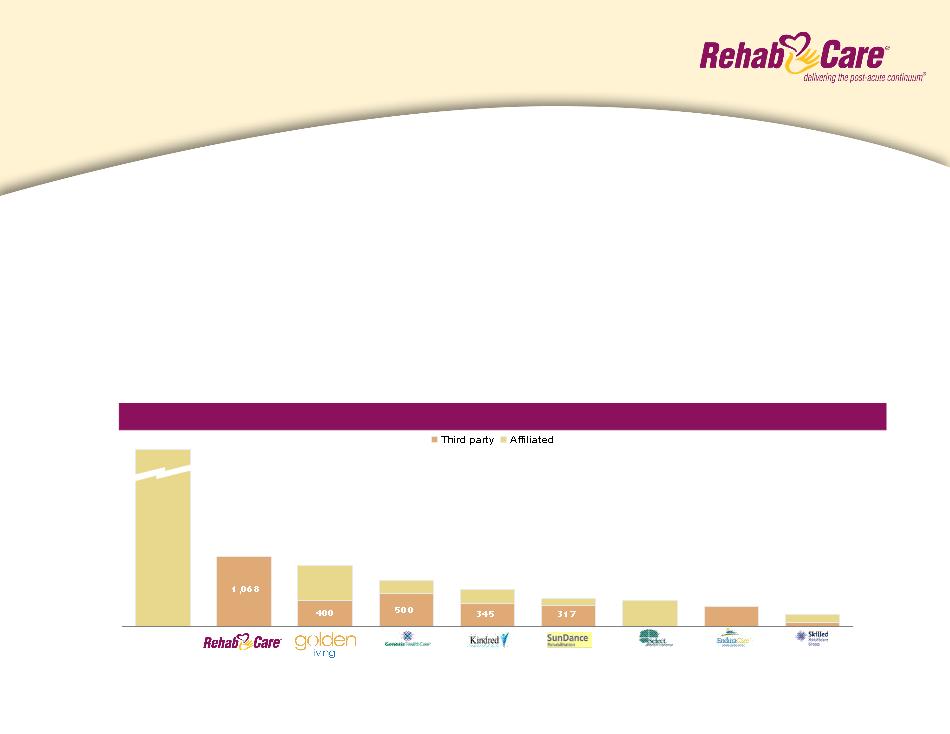

Competitive Landscape — # of facilities served

Self-

operated

11,000+

1,068

935

700

573

425

400

300

189

Contract Therapy

Division overview

Division overview

4

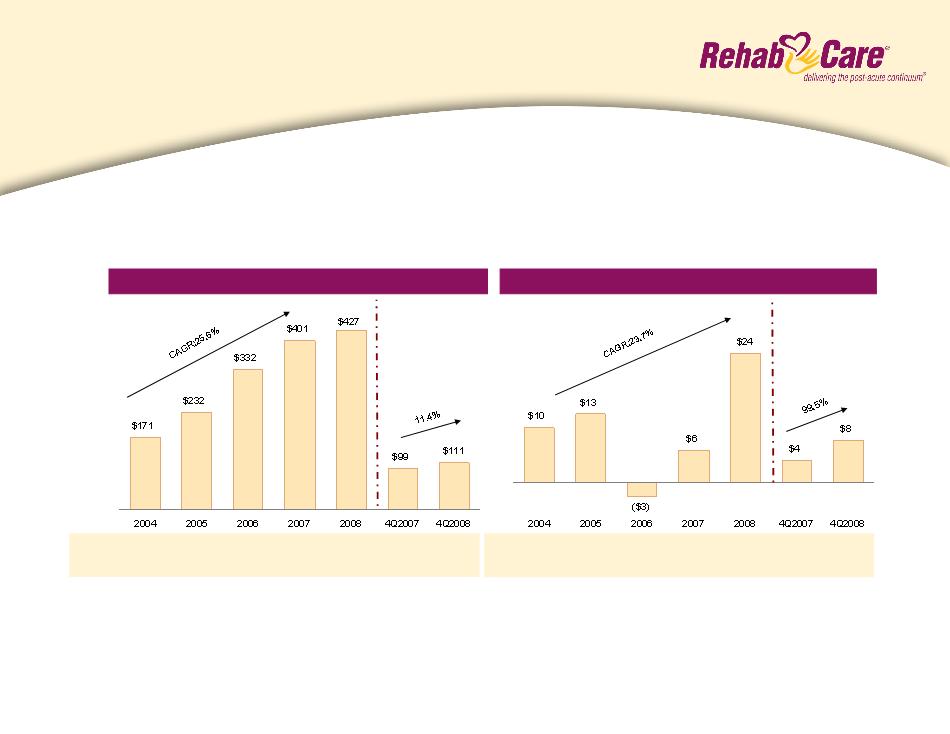

n Strong track record of profitable growth

n Operating earnings decline due to Symphony acquisition in 2006

n Margin recovery with completion of Symphony integration in 2007

Note: Includes Symphony acquisition as of July 1, 2006

¹Same store analysis does not include Symphony

n 5.5% to 6.5% operating earnings margin, driven by 4% to 6% year-over-year same store revenue growth and

assuming no market basket increase for FY 2010

n Stable to modest unit growth

2009 Outlook:

YOY growth: 30.9% 35.5% 42.8% 20.9% 6.5% (3.9%) 11.4%

Same store: 9.9% 8.4% 1.0%¹ 7.1%¹ 12.4% 9.1% 13.8%

Revenue ($mm)

% Margin: 6.0% 5.5% (0.8%) 1.5% 5.6% 4.0% 7.1%

Operating Earnings ($mm)

Contract Therapy

Performance

Performance

1,000 IRF's

5

n Manages hospital-based IRFs and outpatient therapy programs on a contract basis, providing our

partners with:

n Improved clinical outcomes

n Ability to attract ~30% admissions from external sources

n Broader clinical programming (brain, stroke, spinal dysfunction)

n Better access to scarce therapist labor pool

n Better compliance (60% rule, RAC, 3-hour rule)

— Enhanced denial management

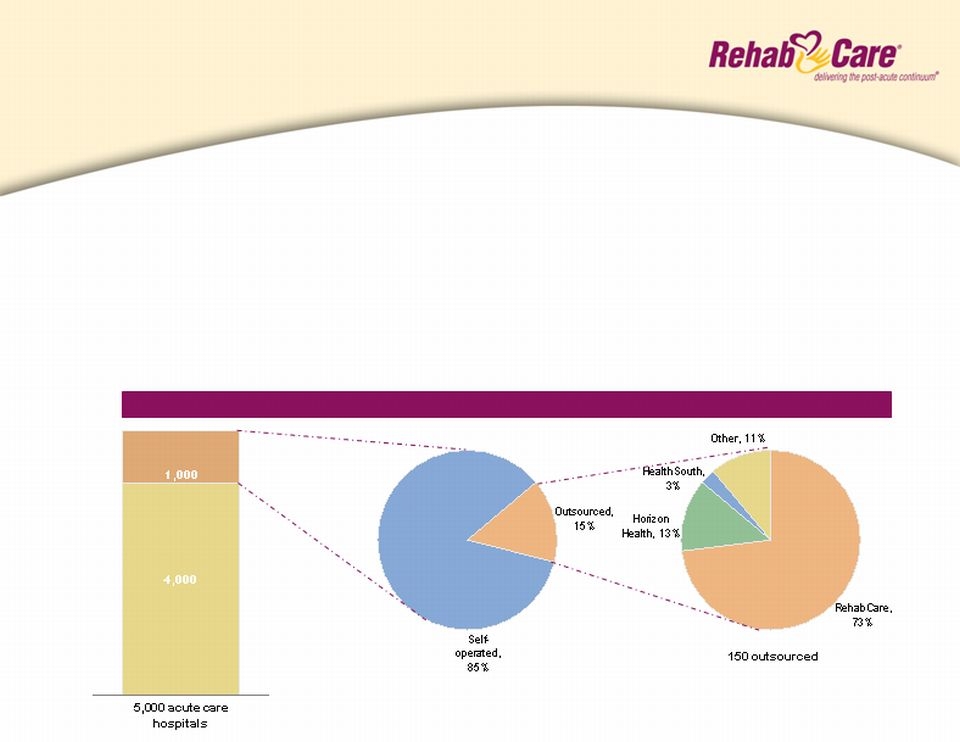

Source: Information available from public filings or from company websites

Competitive Landscape

Hospital Rehabilitation Services

Division overview

Division overview

6

n RehabCare offers acute care providers opportunity to

expand post-acute services and deliver a more

coordinated continuum of care for their patient

population

expand post-acute services and deliver a more

coordinated continuum of care for their patient

population

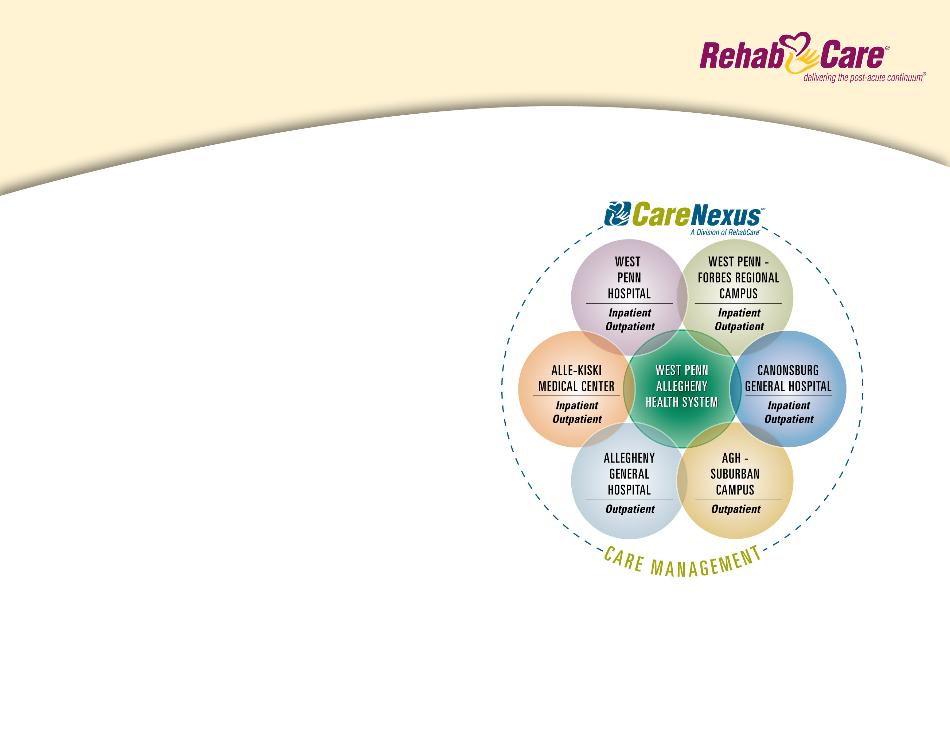

n Collaborative agreement with West Penn Allegheny

Health System (WPAHS) in October 2008 is an

example of this model

Health System (WPAHS) in October 2008 is an

example of this model

n Benefits for WPAHS:

n Enhanced clinical services for ever-growing post-acute

population

population

n Improved market share / decreased outmigration

n Improved patient outcomes / creation of “centers of excellence”

n Seamless integration of post-acute services and patient care

coordination through CareNexus

coordination through CareNexus

WPAHS agreement

A continuum of care model

A continuum of care model

7

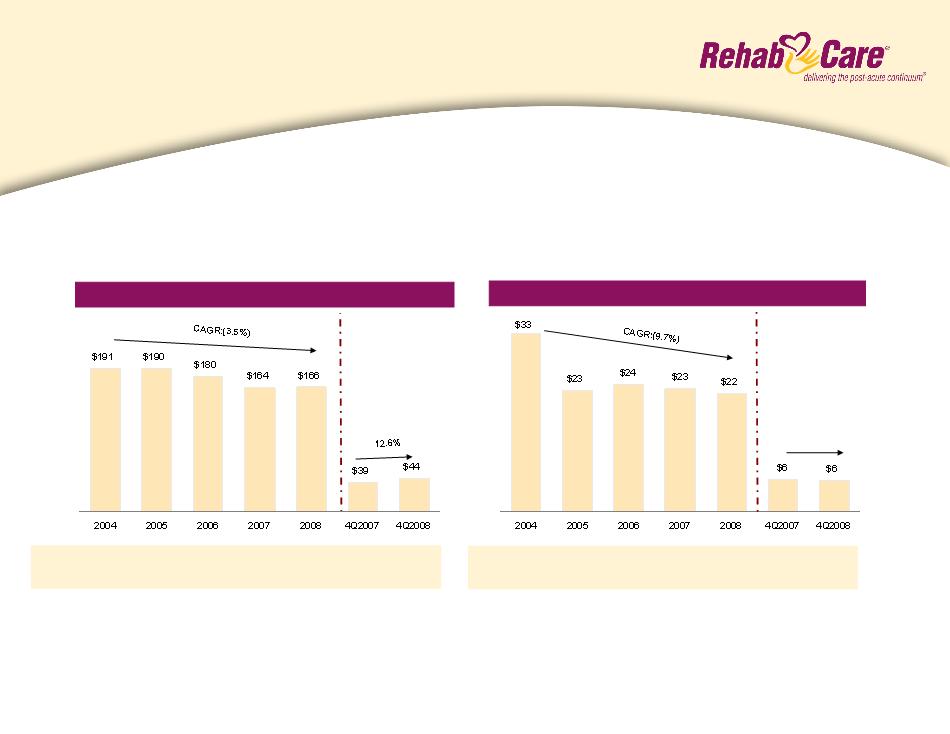

n Revenue and operating earnings declined due to implementation of the 75% Rule in 2004

n Clear runway to growth given freeze of 75% Rule at 60% starting January 2008

n Revenue and operating earnings rebounded during the second half of 2008 with further growth expected in 2009

YOY growth: 2.6% (0.5%) (5.3%) (8.7%) 0.9% (11.5%) 12.6%

IRFs: 113 120 115 107 113 107 113

Revenue ($mm)

¹includes $1.2 mm pretax charge from a bad debt write-down related to an outpatient

transaction

transaction

(2.9%)

Operating Earnings ($mm)

% Margin: 17.3% 11.9% 13.2% 14.0% 13.3% 15.5% 13.3%

¹

n 14% to 16% operating earnings margin, 3% to 5% year-over-year growth in same store IRF discharges and a modest

net increase in units

net increase in units

2009 Outlook:

Hospital Rehabilitation Services

Performance

Performance

8

n Market Size:

n 240+ IRFs

Freestanding IRFs

LTACHs

Competitive Landscape

n Market Size:

n 460+ LTACHs

Source: Information available from public filings or from company websites

¹ Includes St. Luke’s Rehabilitation Hospital (opened in November 2008) and minority-owned hospital

Centerre

Hospital Division

Market overview

Market overview

9

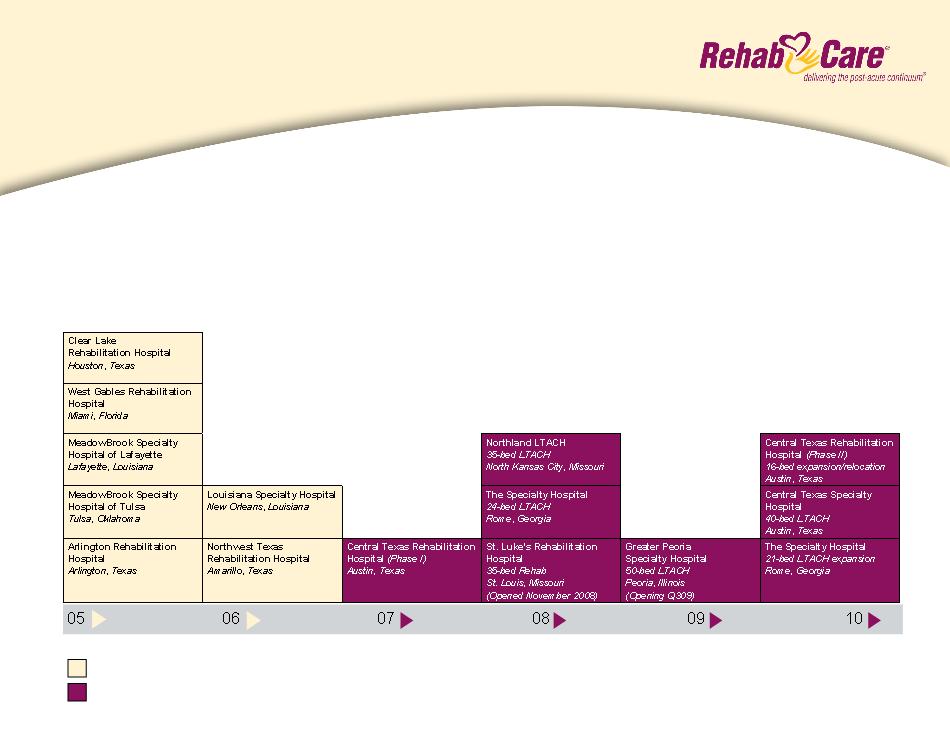

n 11 existing hospitals (St. Luke’s Rehabilitation Hospital opened November 2008), 2 in development,

2 expansions; one scheduled opening in 2009

n Strategy of partnering with real estate investors/joint venture partners to build hospitals in a capital-

efficient, high ROI fashion

efficient, high ROI fashion

Wholly Owned

Joint Venture

Growing portfolio of post-acute hospitals

10

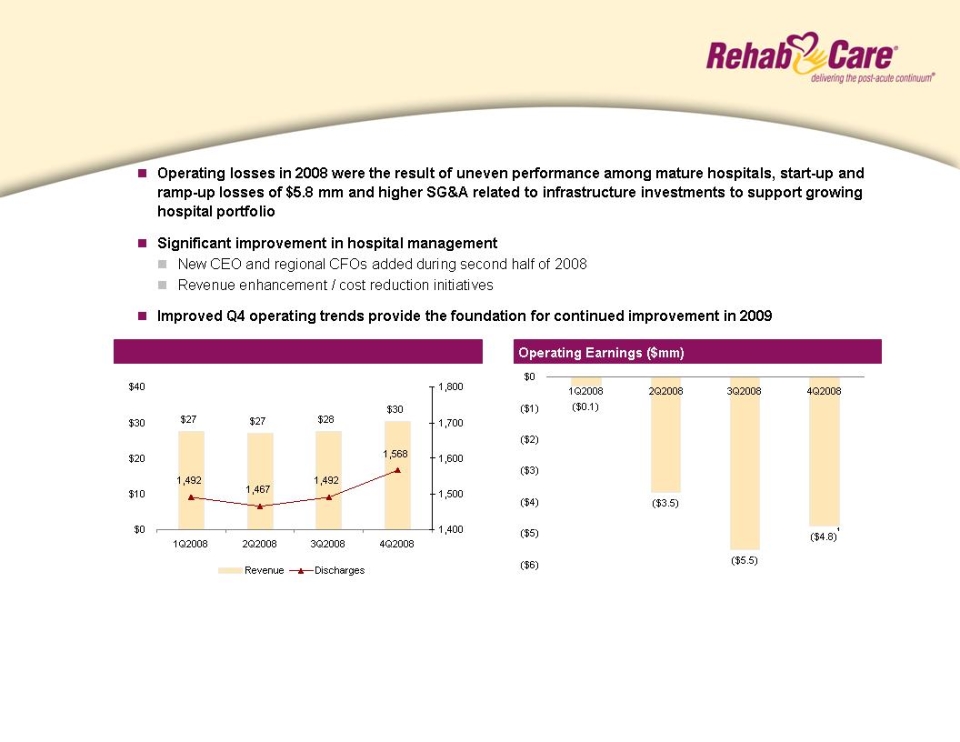

Revenue ($mm) and discharges

1Includes a $1.5 mm pretax charge related to the cancellation of a planned

acquisition and development project

acquisition and development project

n Sequential quarterly improvement in operating earnings performance with total year operating losses reduced by

$3 - - $4 mm compared to FY 2008

n $140-$150 mm in revenue, driven by strong growth in mature and de novo hospitals and assuming no market basket

increase for LTACHs or IRFs

increase for LTACHs or IRFs

2009 Outlook:

¹

Hospital Division

Performance

Performance

11

Net Earnings ($mm)

Revenue ($mm)

EPS: $0.42 $0.731 $1.052 $0.29 $0.322

n Strong consolidated revenue and net earnings growth for the full year

n Quarterly operating earnings will be impacted less by hospital start-up / ramp-up losses than in 2008

n Consistent with prior years, first quarter 2009 operating results will be impacted by the resumption of normalized

run rate costs, such as self insurance and employee benefit programs, along with fewer calendar days

n Effective tax rate of approximately 39% after consideration of minority interests and equity income

2009 Outlook:

¹includes a $0.17 per diluted share impairment charge on an intangible asset

²includes $0.09 per diluted share in charges related to a bad debt write-down of an

outpatient transaction and cancellation of a planned acquisition and development project

outpatient transaction and cancellation of a planned acquisition and development project

Consolidated financial summary

12

Cash and Cash Equivalents

Total Assets

Total Debt

Stockholders’ Equity

Percent of Debt to Total Capital

Percent of Net Debt to Total Capital

($mm)

$ 10.3

408.6

74.5

$ 244.0

23%

20%

$ 27.4

438.4

57.0

$267.8

18%

9%

12/31/07

12/31/08

n Cash flow from operations totaled $48.7 mm in FY 2008

n Days sales outstanding improved from 72 days at FYE 2007 to 66 days at FYE 2008

n Debt was reduced during FY 2008 by $17.5 mm with cash position increasing by $17.1 mm to

provide greater liquidity during credit crisis (net debt fell from $64mm at FYE 2007 to $30 mm at

FYE 2008)

provide greater liquidity during credit crisis (net debt fell from $64mm at FYE 2007 to $30 mm at

FYE 2008)

Consolidated balance sheet

13

LTACHs

IRFs

SNFs

n The Extension Act contained LTACH

-specific provisions through

December 31, 2010, including

stoppage of both the 25% rule and a

short-stay outlier payment provision.

It also instituted a moratorium on

development of new LTACHs.

-specific provisions through

December 31, 2010, including

stoppage of both the 25% rule and a

short-stay outlier payment provision.

It also instituted a moratorium on

development of new LTACHs.

n For FY2009, CMS implemented a

2.7% increase in rates

2.7% increase in rates

n MedPAC has recommended a net

1.6% rate increase in FY2010

1.6% rate increase in FY2010

n Prior legislation requires CMS to

report by June 2009 the results of an

LTACH study relating to such areas

as patient access and admission

criteria

report by June 2009 the results of an

LTACH study relating to such areas

as patient access and admission

criteria

n The SCHIP Extension Act of 2007,

which provided a permanent freeze

of the 75% Rule at 60%, effective

January 1, 2008, also eliminated a

market basket update through

FY2009

which provided a permanent freeze

of the 75% Rule at 60%, effective

January 1, 2008, also eliminated a

market basket update through

FY2009

n MedPAC has recommended that

payment rates not be increased in

FY2010

payment rates not be increased in

FY2010

n Prior legislation requires CMS to

report by June 2009 the results of an

IRF study relating to such areas as

patient access and admission criteria

report by June 2009 the results of an

IRF study relating to such areas as

patient access and admission criteria

n On July 15, 2008 Congress passed

MIPPA (Medicare Improvements for

Patients and Providers Act) that

extended the Part B therapy cap

exceptions process and provided a

1.1% increase in the physician fee

schedule through December 31,

2009

MIPPA (Medicare Improvements for

Patients and Providers Act) that

extended the Part B therapy cap

exceptions process and provided a

1.1% increase in the physician fee

schedule through December 31,

2009

n CMS issued a 3.4% industry rate

increase for FY2009, which became

effective on October 1, 2008

increase for FY2009, which became

effective on October 1, 2008

n MedPAC has recommended that

payment rates not be increased in

FY2010

payment rates not be increased in

FY2010

Current reimbursement environment

14

Summary

n On February 26, 2009, President Obama released his proposal to save nearly $18B over the

next 10 years, which included creating a site neutral, post-acute bundled payment

mechanism beginning in 2013

next 10 years, which included creating a site neutral, post-acute bundled payment

mechanism beginning in 2013

n Proposal creates a post-acute 30-day add-on to the acute DRG payment, likely controlled by

the acute care hospital, and institutes readmission penalties on acute care hospitals, which

should result in $8.4B in savings

the acute care hospital, and institutes readmission penalties on acute care hospitals, which

should result in $8.4B in savings

n Details of the proposal are pending and Congressional action is required to enact

n Combination of incentives and penalties will likely produce better patient outcomes

n Eliminates the need for arbitrary regulations such as the 60% Rule for IRFs, 25-day length-of

-stay requirement for LTACHs and the 3-day hospital admission requirement for SNFs

-stay requirement for LTACHs and the 3-day hospital admission requirement for SNFs

n Prompts acute care hospitals to have a post-acute care strategy, which may require a post-

acute partner

acute partner

n Creates opportunity for RehabCare, given our relationships and JV partnerships with acute

care providers, SNF footprint and the breadth of our capabilities across the post-acute

continuum

care providers, SNF footprint and the breadth of our capabilities across the post-acute

continuum

Potential Impact

Obama healthcare budget proposal

Impact on post-acute care

Impact on post-acute care

15

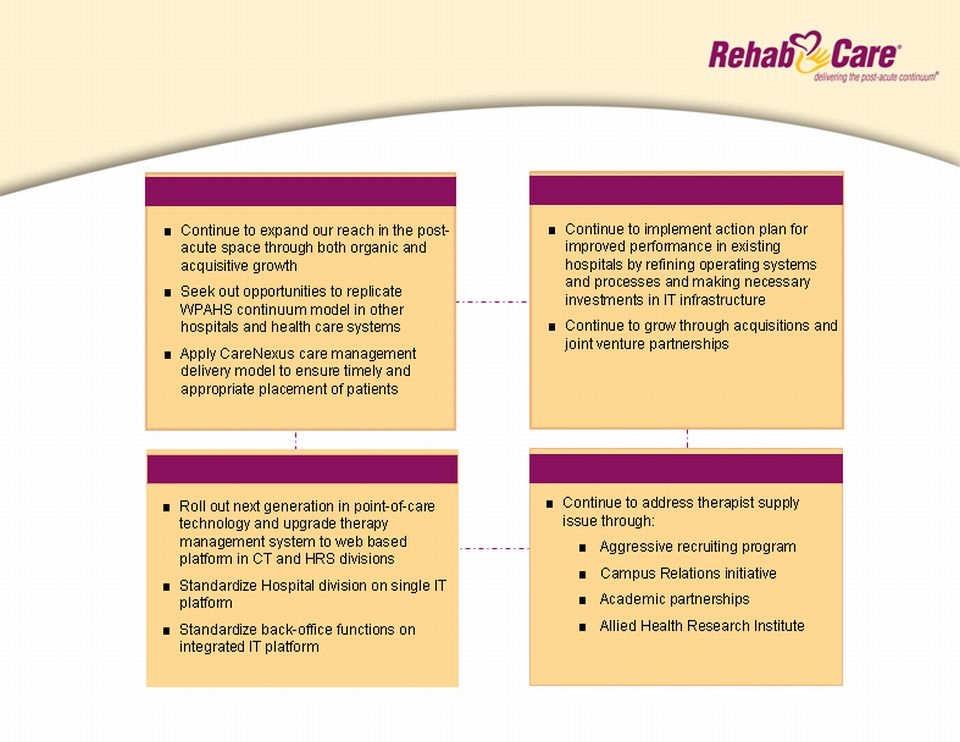

The Post-Acute Continuum

Hospital Division

IT Roadmap

Therapist Solutions

Long-term strategic plan

16

Why RehabCare?

One of the longest tenured post-acute providers (established in 1982)

n Increasing market demand

n Expenditures for post-acute services:

n Grew $20.4 billion from 2000-2007

n Projected to increase 150% by 2016

n Represents 15% of Medicare fee-for-service spending

n First wave of baby boomers enter Medicare in 2011

n Post-acute continuum capabilities

n Offers flexible solutions to clients and partners

n Gives us the ability to withstand market

pressures in any one segment

pressures in any one segment

n Positions us to capitalize on proposed bundled

or episodic payment system

or episodic payment system

17

Why RehabCare?

ü PPS

ü 75% Rule

2 Total debt less cash

ü Part B Therapy Caps

ü LTACH 25% rule

2006 | 2007 | 2008 | |

DSO | 78 | 72 | 66 |

CFFO | $19 | $52 | $49 |

Net Debt2 | $111 | $64 | $30 |

2006-08

10.2%

21.3%

¹

n Enhances competitive advantage in economic

downturns

downturns

n Greater flexibility with potential partners

searching for capital resources

searching for capital resources

n Allows continued evaluation of growth

opportunities

opportunities

Note: Includes Symphony acquisition as of July 1, 2006

¹ Includes $2.7mm in charges related to a bad debt write-down of an outpatient transaction and

cancellation of a planned acquisition and development project in FY2008

cancellation of a planned acquisition and development project in FY2008

■ Demonstrated ability to grow revenue and earnings organically and through acquisitions

■ Proven ability to adapt to market regulatory changes

■ Strong cash flows

18

Forward-looking statements have been provided pursuant to the safe harbor provisions of the Private Securities

Litigation Reform Act of 1995. Such statements are based on the Company’s current expectations and could be

affected by numerous factors, risks and uncertainties discussed in the Company’s filings with the Securities and

Exchange Commission, including the Company’s most recent annual report on Form 10-K, subsequent quarterly

reports on Form 10-Q and current reports on Form 8-K. Do not rely on forward looking statements as the

Company cannot predict or control many of the factors that ultimately may affect the Company’s ability to

achieve the results estimated. The Company makes no promise to update any forward looking statements

whether as a result of changes in underlying factors, new information, future events or otherwise.

Litigation Reform Act of 1995. Such statements are based on the Company’s current expectations and could be

affected by numerous factors, risks and uncertainties discussed in the Company’s filings with the Securities and

Exchange Commission, including the Company’s most recent annual report on Form 10-K, subsequent quarterly

reports on Form 10-Q and current reports on Form 8-K. Do not rely on forward looking statements as the

Company cannot predict or control many of the factors that ultimately may affect the Company’s ability to

achieve the results estimated. The Company makes no promise to update any forward looking statements

whether as a result of changes in underlying factors, new information, future events or otherwise.

Safe Harbor