UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-K

| x | | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

FOR THE FISCAL YEAR ENDED DECEMBER 31, 2005

OR

| ¨ | | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

FOR THE TRANSITION PERIOD FROM TO

COMMISSION FILE NUMBER

PATIENT SAFETY TECHNOLOGIES, INC.

(Exact name of registrant as specified in its charter)

Delaware | | 13-3419202 |

(State of Incorporation) | | (I.R.S. Employer Identification Number) |

| | | |

1800 Century Park East, Ste. 200, Los Angeles, CA 90067 |

(Address of principal executive offices) (Zip Code) |

Registrant’s telephone number, including area code: (310) 895-7750

Securities registered pursuant to Section 12(b) of the Act:

Title of each class Common Stock, par value $0.33 per share | Name of each exchange on which registered The American Stock Exchange |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

Yes ¨ No x.

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. ¨

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the past 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨.

Indicate by check mark, if disclosure of delinquent filers in response to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, or a non-accelerated filer. See definition of “accelerated filer and large accelerated filer” in Rule 12b-2 of the Exchange Act. (Check one):

Large accelerated filer ¨ | Accelerated filer ¨ | Non-accelerated filer x |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2) of the Act. Yes ¨ No x.

The aggregate market value of common stock held by non-affiliates of the Registrant on June 30, 2005, based on the closing price on that date of $3.68 on the American Stock Exchange, was $19,371,895. For the purposes of calculating this amount only, all directors and executive officers of the Registrant have been treated as affiliates.

There were 6,206,563 shares of the registrant's common stock outstanding as of March 27, 2006.

PATIENT SAFETY TECHNOLOGIES, INC.

FORM 10-K FOR THE FISCAL YEAR

ENDED DECEMBER 31, 2005

TABLE OF CONTENTS

| | | Page |

PART I |

| | | |

| Item 1. | Business | 1 |

| Item 1A. | Risk Factors | 11 |

| Item 1B. | Unresolved Staff Comments | 23 |

| Item 2. | Properties | 23 |

| Item 3. | Legal Proceedings | 24 |

| Item 4. | Submission of Matters to a Vote of Security Holders | 24 |

| | | |

PART II |

| | | |

| Item 5. | Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities | 26 |

| Item 6. | Selected Financial Data | 29 |

| Item 7. | Management’s Discussion and Analysis of Financial Condition and Results of Operations | 29 |

| Item 7A. | Quantitative and Qualitative Disclosures About Market Risk | 46 |

| Item 8. | Financial Statements and Supplementary Data | 47 |

| Item 9. | Changes In and Disagreements with Accountants on Accounting and Financial Disclosure | 80 |

| Item 9A. | Controls and Procedures | 80 |

| Item 9B. | Other Information | 80 |

| | | |

PART III |

| | | |

| Item 10. | Directors and Executive Officers of the Registrant | 80 |

| Item 11. | Executive Compensation | 84 |

| Item 12. | Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters | 92 |

| Item 13. | Certain Relationship and Related Transactions | 94 |

| Item 14. | Principal Accounting Fees and Services | 99 |

| | | |

PART IV |

| | | |

| Item 15. | Exhibits, Financial Statement Schedules | 99 |

| | | |

SIGNATURES | 105 |

"SAFE HARBOR" STATEMENT UNDER

THE PRIVATE SECURITIES LITIGATION REFORM ACT OF 1995

We believe that it is important to communicate our plans and expectations about the future to our stockholders and to the public. Some of the statements in this report are forward-looking statements about our plans and expectations of what may happen in the future, including in particular the statements about our plans and expectations under the headings “Item 1. Business” and “Item 7. Management's Discussion and Analysis of Financial Condition and Results of Operations.” Statements that are not historical facts are forward-looking statements. These forward-looking statements are made pursuant to the “safe-harbor” provisions of the Private Securities Litigation Reform Act of 1995. You can sometimes identify forward-looking statements by our use of forward-looking words like “may,” “should,” “expects,” “intends,” “plans,” “anticipates,” “believes,” “estimates,” “predicts,” “potential,” or “continue” or the negative of these terms and other similar expressions.

Although we believe that the plans and expectations reflected in or suggested by our forward-looking statements are reasonable, those statements are based only on the current beliefs and assumptions of our management and on information currently available to us and, therefore, they involve uncertainties and risks as to what may happen in the future. Accordingly, we cannot guarantee you that our plans and expectations will be achieved. Our actual results and stockholder values could be very different from and worse than those expressed in or implied by any forward-looking statement in this report as a result of many known and unknown factors, many of which are beyond our ability to predict or control. These factors include, but are not limited to, those contained in “Item 1A. Risk Factors” and elsewhere in this report. All written and oral forward-looking statements attributable to us are expressly qualified in their entirety by these cautionary statements.

Our forward-looking statements speak only as of the date they are made and should not be relied upon as representing our plans and expectations as of any subsequent date. Although we may elect to update or revise forward-looking statements at some time in the future, we specifically disclaim any obligation to do so, even if our plans and expectations change.

PART I

Item 1. Business.

Organizational History

Patient Safety Technologies, Inc. (referred to in this report as the “Company,” “we,” “us,” and “our”) was incorporated on March 31, 1987, under the laws of the state of Delaware. Beginning in July 1987 until March 31, 2005 we operated as an investment company registered pursuant to the Investment Company Act of 1940, as amended (the “1940 Act”). In or about August 1997 our Board of Directors determined it would be in the best interest of the Company and our stockholders to elect to become a registered business development company (a “BDC”) under the 1940 Act. On September 9, 1997 our shareholders approved the proposal to be regulated as a BDC and on November 18, 1997 we filed a notification of election to become a BDC with the Securities and Exchange Commission (“SEC”).

Through the first half of 2004 we focused our investment strategy on capital appreciation through long-term equity investments in start-up and early stage companies in the radio and telecommunications industries. Beginning in June 2004, we undertook a strategic restructuring and recapitalization plan which culminated in a change in control in our management and a shift in our business focus away from the radio and telecommunications industries toward the medical products, health care solutions, financial services and real estate industries. On March 30, 2005, our shareholders voted to withdraw our election to be treated as a BDC and on March 31, 2005 we filed an election to withdraw the election with the SEC. We are currently engaged in the acquisition of controlling interests in companies and research and development of products and services focused on the health care and medical products field, particularly the patient safety market. Although we still own certain real estate assets, we are no longer focusing on the financial services and real estate industries. As of March 29, 2006, our Board of Directors determined to focus our business exclusively on the patient safety medical products field.

On February 25, 2005, in furtherance of our restructuring plan, we purchased Surgicount Medical, Inc., a California corporation (“Surgicount”), from Brian Stewart and Dr. William Stewart, the former holders of 100% of the outstanding capital stock of Surgicount. Surgicount was not engaged in a business, but was used to hold certain assets. The assets acquired in connection with the Surgicount acquisition consist primarily of intellectual property rights, including one U.S. patent and one European patent, relating to Surgicount's Safety-Sponge™ System. The consideration paid to Brian Stewart and Dr. William Stewart in connection with the acquisition consisted of $340,000 in cash and 600,000 shares (post 3:1 forward split effective April 5, 2005) of common stock. In addition, in the event that prior to the fifth anniversary of the closing of the acquisition the cumulative gross revenues of Surgicount exceed $500,000, Brian Stewart and Dr. William Stewart are entitled to receive an additional 50,000 shares of common stock (for a total of 650,000 shares of common stock). In the event that prior to the fifth anniversary of the closing of the acquisition the cumulative gross revenues of Surgicount exceed $1,000,000, Brian Stewart and Dr. William Stewart will be entitled to receive an additional 50,000 shares of common stock (for a total of 700,000 shares of common stock).

Surgicount’s Safety-Sponge™ System helps reduce the number of retained sponges and towels in patients during surgical procedures and allows for faster and more accurate counting of surgical sponges. The Safety-Sponge™ System consists of a handheld scanner and bar-coded surgical dressings. By scanning the surgical dressings in at the beginning of a surgical procedure and then scanning them out at the end of the procedure, the sponges can be counted faster and more accurately than traditional methods which require two medical personnel manually counting the used and un-used sponges. Surgicount is the first acquisition in our plan to become a leader in the patient safety market.

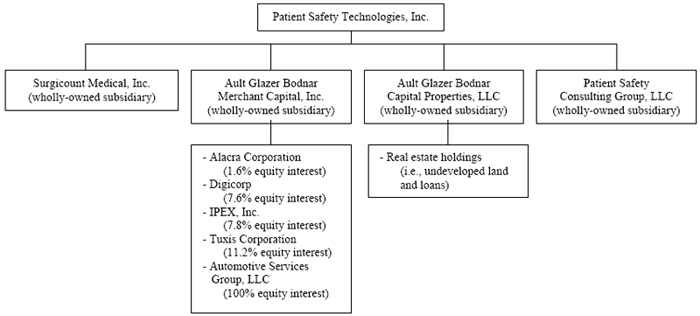

We currently have five wholly-owned operating subsidiaries: (1) Ault Glazer Bodnar Capital Properties, LLC (f/k/a Franklin Capital Properties, LLC), a Delaware limited liability company; (2) Patient Safety Consulting Group, LLC (f/k/a Franklin Medical Products, LLC), a Delaware limited liability company; (3) Surgicount Medical, Inc., a California corporation; (4) Ault Glazer Bodnar Merchant Capital, Inc., a Delaware corporation; and (5) Automotive Services Group, LLC, an Alabama limited liability company wholly owned by Ault Glazer Bodnar Merchant Capital, Inc. Ault Glazer Bodnar Capital Properties, LLC, a real estate development and management company, Patient Safety Consulting Group, LLC, a healthcare consulting services company, and Ault Glazer Bodnar Merchant Capital, Inc., a holding company formed to hold our non-patient safety related assets, all were created to augment our investments in the health care, medical products and financial services and real estate industries. Our prior focus on real estate properties led to the acquisition by Ault Glazer Bodnar Merchant Capital, Inc. of Automotive Services Group, LLC, a company formed to develop properties for the operation of automated car wash sites. We acquired Automotive Services Group, LLC in an effort to increase shareholder value through real estate development. Our corporate structure, including our subsidiaries and our interests in public and private companies that we have purchased, is set forth in the following diagram by reporting segment:

The Medical Products and Healthcare Solutions Industry

We believe that the healthcare delivery system is under tremendous pressure to identify and commercialize simple medical solutions quickly to lower costs, control infections, reduce liability and eliminate preventable errors. Increased litigation and a renewed focus on patient safety by regulators is spurring demand for new innovative medical devices. With the convergence of scientific, electronic and digital technologies, new breakthroughs in medical devices will play a critical role in solving problems in healthcare and enhancing patient safety in the future.

The medical community recognizes the importance of improving patient safety, not only to enhance the quality of care, but also to help manage medical costs and related litigation costs. We are confident the medical profession and healthcare professionals will rise to the occasion and help develop the medical solutions to revolutionize health care.

We are dedicated to leading this effort through the development and introduction of ground-breaking patient safety products such as our lead product, the patented Safety-SpongeTM System, which management believes will allow us to capture a significant portion of the United States and European surgical sponge sales. Based upon assumptions by our management that take into consideration factors such as the approximate number of hospitals and operating rooms in the United States and Europe, the approximate number of surgeries performed annually, and estimates for the average cost of surgical sponges per surgery, we believe that the existing market for surgical sponge sales in the United States and Europe represents a market opportunity equal to or in excess of $650 million in annual sales. Such estimate assumes approximately 61 million surgeries performed annually in the United States and Europe, and an average cost of surgical sponges of $10.60 per surgery. In addition, we believe that our Safety-Sponge™ System could save up to an estimated $1.0 billion annually in retained sponge litigation. The estimated size of the surgical sponge market and actual savings derived from utilizing the Safety-Sponge™ System from retained sponge litigation is based on management’s estimates and assumptions made by management. Although management took into consideration statistics from research and published articles by the American Hospital Association and New England Journal of Medicine, as well as various articles located through a search of retained sponge verdicts, the specific assumptions are management’s interpretation of multiple sources. Further, management believes that a large amount of the litigation relating to medical malpractice claims are settled under the terms of confidential agreements, thus the actual amount of many settlements are never disclosed and therefore subject to speculation.

We intend to target hospitals, physicians, nurses and clinics as our initial source of customers. In addition, we plan to develop strategic alliances with universities, medical facilities and notable medical researchers around the United States that will provide research, development and promotional support for our products and services.

Customers and Distribution

On April 5, 2005, we entered into a consulting agreement with Health West Marketing Incorporated, a California corporation (“Health West”), pursuant to which Health West agreed to help us establish a comprehensive manufacturing and distribution strategy for the Safety-Sponge™ System worldwide. The initial term of the agreement is for a period of two years. After the initial two-year term, the agreement will terminate unless extended by the parties for one or more additional one-year periods. In consideration for Health West’s services, we agreed to issue Health West 42,017 shares of common stock, to be issued as follows: (a) 10,505 shares were issued upon signing the agreement; (b) an additional 15,756 shares were issued as a result of Health West’s assistance in structuring a comprehensive manufacturing agreement with A Plus Manufacturing, which was entered into on August 17, 2005; and (c) if Health West helps us develop a regional distribution network to integrate the Safety-Sponge™ System into the existing acute care supply chain, then we will issue Health West the remaining 15,756 shares. As incentive for entering into the agreement, we issued Health West a callable warrant to purchase 150,000 shares of common stock with an exercise price of $5.95 per share, exercisable for five years. In addition, we agreed to issue a callable warrant to purchase 25,000 (post 3:1 forward stock split) shares of the common stock with an exercise price of $5.95 per share, exercisable upon assisting us to develop a global distribution strategy and identification of acquisition candidates. In the event of the death of Bill Adams, who is Health West’s Chief Executive Officer, the agreement will automatically terminate. We may terminate the agreement at any time upon delivery to Health West of notice of a good faith determination by our Board of Directors that the agreement should be terminated for cause or as a result of disability of Mr. Adams. Health West may voluntarily terminate the agreement only after expiration of the initial two-year term upon providing 30 days prior written notice to us.

Geographic Areas

We intend to market and sell our patient safety products and services in the United States and in Europe. However, the principal markets, products and methods of distribution will vary by country based on a number of factors, including healthcare regulations, insurance coverage and customer demographics. Business activities in some countries outside the United States are subject to higher risks than comparable U.S. activities because the business and commercial climate is influenced by restrictive economic policies and political uncertainties.

Product Development

Our Safety-SpongeTM System allows for faster and more accurate counting of surgical sponges. The Safety-SpongeTM System is a two-part system consisting of a handheld scanner/imager/computer and of Surgicount supplied surgical dressings. Our sponges are unique in that they are individually labeled with a “bar code” at the point of manufacture. The sponges are scanned in by a handheld scanner at the beginning of a surgical procedure, and then scanned out at the end of a procedure after their use. Each sponge, having a unique bar code, can accurately be accounted for at the end of the procedure. Without using our Safety-SpongeTM System, in a typical surgical procedure, a nurse and a scrub tech manually count all sponges used and un-used. The core of the Safety-SpongeTM System is the ability to uniquely identify an individual dressing.

Surgicount began developing the Safety-SpongeTM line of sponges in February 1994 and received confirmation from the U.S. Food and Drug Administration (“FDA”) that the product line was granted 510k exempt status on November 8, 1999. The Safety-SpongeTM line of sponges has passed required FDA biocompatibility tests including ISO sensitization, cytotoxicity and skin irritation tests. The Center for Devices and Radiological Health (“CDRH”) handles the premarket notification process for medical devices at the FDA. The CDRH requires the biological evaluation of medical devices to determine the potential toxicity resulting from contact of the component materials of the device with the human body. Evaluation of any new device intended for human use requires data from systemic testing to ensure that the benefits provided by the final product will exceed any potential risk produced by device materials. CDRH Blue Book Memo G95-1 provides guidance for required biocompatibility testing procedures for medical devices. Surgicount requested specific guidance from the CDRH as to the required biocompatibility tests for the Safety-SpongeTM line of products. The CDRH specifically guided Surgicount to three required biocompatibility tests for the Safety-SpongeTM line: Cytotoxicity, Sensitization and Irritation/Intracutaneous Reactivity. Surgicount has performed and in 2003 passed all three of these required biocompatibility tests. Cytotoxicity testing is conducted to determine whether or not the materials used in a medical device are harmfully reactive to certain biological elements on a cellular level. Sensitization or hypersensitivity reactions usually occur as a result of prolonged contact with a chemical substance that interacts with the body’s immune system. The tests are used to eliminate the possibility that patients will be exposed to strong sensitizing chemicals extracted from the medical device.

The tests were completed prior to our acquisition of Surgicount, which occurred in February 2005. At the time the acquisition was completed we focused on developing the product for commercialization. Although passing the three biocompatibility tests was necessary to satisfy any questions as to whether or not the product was safe for use in the body it was only a part of the process required to commercialize the product. In order to utilize the product as designed, investment in specialized software, hardware as well as modification of current operating room procedures was needed.

Software development, which was initially expected to take a few months, required approximately nine months for completion. Initially we expected that basic modification to existing software would be sufficient; however, based upon feedback from third party users and consultants we abandoned our plan to modify existing software currently in use and developed our own proprietary software for the system.

Finally, due to the nature of the medical products business any change in the procedures requires rigorous rounds of testing and review in every adopter. Demonstrations are given to relevant parties and small “in-service” (an in-hospital teaching of how to use the system to the relevant staff members) sessions are performed with the results evaluated. If the results are viewed positively a second larger in-service session is usually performed, which results are again reviewed. Assuming a positive outcome of the in-service sessions, the entire staff must then be trained to use the system prior to the placement of any order. In the event we are successful during the in-service sessions we expect to begin receiving orders for the Safety-SpongeTM System sometime in the first half of 2006.

The Safety-SpongeTM System is presently in the optimization and commercialization phase. Development of the Safety-SpongeTM System has been completed and the system is in final preparations to be rolled out into the market as a commercial product.

We intend to conduct further research and development to advance our products. However, we expect that any costs associated with R&D on our Safety-SpongeTM product will be insignificant and intend to outsource much of the R&D functions so that we may focus our direct efforts on optimizing the Safety-SpongeTM product and establishing distribution channels with strategic alliances with hospitals to deploy the product. We also seek qualified input from professionals in the healthcare profession as well as University hospitals such as Harvard and the University of California, San Francisco (“UCSF”). These physicians and researchers maintain medical practices primarily at University hospitals and are involved in various research and clinical development programs. We meet on an as needed basis to discuss medical, technology and development issues. Through direct contracts and sponsorship of studies, recommendations from these professionals have improved various aspects of the Safety-SpongeTM System. Examples where recommendations were utilized include: the ideal location for labels, label coarseness and thickness, improved operating room procedures, label structure and scanner function. In addition, we are developing relationships with Universities to co-develop and distribute patient safety continuing medical education (CME) products as well as University-developed patient safety products such as guides, specially designed notepads and bedside tools.

In the past we have relied on the professional advice of Dr. Jeffrey Pearl relating to operating room procedures and how to best adapt the Safety-SpongeTM for use in an operating room. Dr. Pearl is the Vice-chair of the Department of Surgery at UCSF, as well as the vice dean of the medical school and a highly respected medical researcher. In August of 2005, Dr. Pearl accepted a one-year consulting contract for continued services relating to operating room procedures and integration of the Safety-SpongeTM System. Integration of the Safety-SpongeTM System covers areas such as teaching nurses to use the system, optimum locations in the operating room, and optimum procedures for how to perform the count. The contract provides for a monthly cash payment of $2,000 and warrants to purchase 12,500 shares of our common stock.

We entered into a clinical trial agreement with Brigham and Women's Hospital, the teaching affiliate of Harvard Medical School, relating to Surgicount's Safety-Sponge TM System. The clinical trial is the result of an on-going collaboration between Harvard and Surgicount to refine the Safety-SpongeTM System in a clinical optimization study. Under terms of the agreement, Brigham and Women's Hospital will collect data on how the Safety-Sponge System saves time, reduces costs and increases patient safety in the operating room. The study will also continue to refine the system's technical processes in the operating room to provide clear guidance and instruction to hospitals, easily integrating the Safety-SpongeTM System into operating rooms. Brigham and Women's Hospital received a non-exclusive license to use the Safety-SpongeTM System, while we will own all technical innovations and other intellectual properties derived from the study. Unless the clinical trial agreement is terminated, we will provide a research grant to Brigham and Women’s Hospital over the course of the clinical trial in the aggregate amount of $430,513 of which $107,628 was paid in 2005. We expect the clinical trials will be completed around September 2006.

Manufacturing

While we have not yet begun commercial manufacturing of the Safety-SpongeTM System, we believe that the materials used in our products are readily available and can be purchased and/or produced by several different vendors and, therefore, we do not anticipate being dependent on any one vendor.

In order to meet the expected demand for bar-coded surgical dressings on August 17, 2005, Surgicount entered into an agreement for A Plus International Inc. (“A Plus”) to be the exclusive manufacturer and provider of the Safety-Sponge™ products, which includes bar coded gauze sponges, bar coded laparotomy sponges, bar coded O.R. towels and bar coded specialty sponges. Services to be provided by A Plus include manufacturing, packaging, sterilization, logistics and all related quality and regulatory compliance. During the term of the agreement, A Plus agreed not to manufacture, distribute or otherwise supply any bar coded gauze sponges, bar coded laparotomy sponges, bar coded O.R. towels or bar coded specialty sponges manufactured in China for any third party except for Surgicount. A Plus was founded in 1988 and is a global manufacturer of surgical dressings, patient drapes and surgical gowns. A Plus provides OEM support to the largest healthcare manufacturers and distributors in the world. A Plus employs over 6,000 people in seven factories throughout China and maintains over 200,000 sq. ft. of warehouse space in the United States. While we believe the manufacturing capacity of A Plus will be sufficient to meet our expected demand, in the event A Plus cannot meet our requirements the agreement allows us to retain additional providers of the Safety-Sponge™ products. The term of the agreement is for a period of five years and will automatically renew for successive three-year periods. Either party may terminate the agreement without cause at any time after eight years upon delivery of 90 days prior written notice.

Research and Development

Research and development activities are important to our business. However, at this time we do not have a research facility but rather focus our efforts on acquisitions of companies operating within our target industries that have demonstrated product viability through their own research and development activities. We intend to outsource much of the research and development activities related to improving our existing products or expanding our intellectual property to similar products or products that have similar characteristics in our target industries. We did not incur any costs during the fiscal years ended December 31, 2005 or 2004 relating to the development of new products, the improvement of existing products, technical support of products and compliance with governmental regulations for the protection of consumers. In the future, these costs will be charged directly to income in the year in which they are incurred.

Patents and Trademarks

We intend to make a practice of obtaining patent protection on our products and processes where possible. Our patents and trademarks are protected by registration in the United States and other countries where our products are marketed.

We currently own patents issued in the United States and Europe related to the Safety-SpongeTM System. This is covered by patent #5,931,824 registered with the United States Patent and Trademark Office and patent #1 032 911 B1 registered with the European Patent Office, which permits the holder to label or identify a dressing with a unique identifier. Patent #5,931,824 and #1 032 911 B1 will expire in August of 2019 and March of 2017, respectively. U.S Patent Number 5,931,824 is currently undergoing a reexamination proceeding in the U.S. Patent Office. We have also filed one provisional and one non-provisional patent application in the United States Patent Office covering improved methods and systems for the automated counting and tracking of surgical articles.

Sales of the Safety-SpongeTM System in the future are expected to contribute a significant part of our total revenue. We consider these patents and trademarks in the aggregate to be of material importance in the operation of our business. The loss or expiration of any product patent or trademark could result in a loss of market exclusivity and can result in a significant reduction in sales.

Competition

The medical products and healthcare solutions industry is highly competitive. We expect that if our business strategy proves to be successful, our current competitors in the medical products and healthcare solutions market may duplicate our strategy and new competitors may enter the market. We compete against other medical products and healthcare solutions companies, some of which are much larger and have significantly greater financial resources than we do. We also compete against large companies that seek to license medical products and healthcare solutions technologies for themselves. We cannot assure you that we will be able to successfully compete against these competitors in the acquisition, development, or commercialization of any medical products and healthcare solutions, funding of medical products and healthcare solutions companies or marketing of our products and solutions.

Competition in research, involving the development of new products and processes and the improvement of existing products and processes, is particularly significant and results from time to time in product and process obsolescence. The development of new and improved products is important to our success in all areas of our business. This competitive environment requires substantial investments in continuing research, multiple sales forces and strategic alliances. In addition, the winning and retention of customer acceptance of our patient safety products involves heavy expenditures for health care regulatory compliance, advertising, promotion and selling.

Because we have not begun selling and generating revenue from our patient safety products, our competitive position in the medical products and healthcare solutions industry cannot be determined.

Competitive Advantages

We believe that we are well positioned to provide financing and research and development resources to medical products and health care-related companies for the following reasons:

| | · | Focus on innovative technologies, products and services; |

| | · | Network of well respected industry affiliations and medical expertise; and |

| | · | Established deal sourcing network. |

Though by the nature of our patents, we can have no direct competition, there are several existing individuals/companies that are trying to address the same issues as Surgicount's Safety-Sponge System. Among these are a medical malpractice lawyer named Daniel Ballard and two radio frequency identification (“RFID”)-based companies, RF Surgical and ClearCount Medical.

Mr. Ballard’s invention and patent revolves around imbedding radio-opaque pellets (similar to BB’s) into the sponges. These would be read by placing the used sponges into a special machine after a surgery that would count the pellets, and thus the sponges placed in the machine.

The RFID companies both have similar approaches to solving retained sponges. Their approach is to “impregnate” sponges with RFID tags. RFID-reading wands would be held over the patients at the end of surgeries to ensure that no sponges are left behind. It is our understanding from limited discussions with the principals of RF Surgical and ClearCount Medical, and from discussions with sponge manufacturers, that the RFID companies are still in the development stage with their competing products. Surgicount has received FDA exemption for its Safety-Sponge System and its scanner is currently registered in the FDA’s database as non-interfering medical equipment. Since Surgicount’s Safety-Sponge System is fully developed and ready for manufacturing and distribution, we believe this provides an advantage over the above competing products.

Real Estate Industry and Express Car Wash Business

We had originally intended for our real estate operations to include a mixture of commercial properties, residential land development projects and other unimproved land, all in various stages of development and all available for sale. Performance of this type of real estate operations would largely have been dependent upon the performance of the operating properties, the current status of our development projects and non-recurring gains or losses recognized when and if real estate assets are sold. The results of operations for these types of real estate operations generally are unpredictable and we probably would have experienced significant year-over-year fluctuations from such operations. All of our real estate holdings are owned by our subsidiary Ault Glazer Bodnar Capital Properties, LLC (f/k/a Franklin Capital Properties, LLC) (“AGB Capital Properties”) except for our investment in Automotive Services Group, LLC (“ASG”), which is wholly owned by our subsidiary Ault Glazer Bodnar Merchant Capital, LLC (“AGB Merchant Capital”). During July 2005 we shifted the focus of our real estate operations to the identification of unimproved land for ASG to develop and operate automated car wash sites under the trade name “Bubba’s Express Wash.” ASG’s first express car wash site, developed in Birmingham, Alabama, had its grand opening on March 8, 2006. On July 18, 2005 our wholly owned subsidiary AGB Merchant Capital purchased 50% of the outstanding equity interests of ASG from West Highland, LLC, an unrelated third party, in exchange for $300,000. The remaining 50% interest in ASG was owned by Darrell W. Grimsley until March 15, 2006 when AGB Merchant Capital entered into a Unit Purchase Agreement to acquire the remaining 50% interest from Mr. Grimsley in exchange for agreeing to issue 200,000 shares of the Company’s common stock to Mr. Grimsley. We have consolidated ASG’s operations in our financial statements since we determined that we are the primary beneficiary of ASG, a variable interest entity as defined by FIN 46. Pursuant to ASG’s operating agreement, Mr. Grimsley had exclusive control over ASG’s operations from July 18, 2005 until AGB Merchant Capital purchased the remaining 50% interest on March 15, 2006. AGB Merchant Capital now owns 100% of the outstanding equity interests in ASG and has exclusive control over ASG as its sole managing member. We plan to change the name of AGB Merchant Capital to Automotive Services Group, Inc. to reflect the subsidiaries primary holding in ASG.

In addition to ASG, we had several real estate investments at December 31, 2005. These investments consisted of approximately 8.5 acres of undeveloped land in Heber Springs, Arkansas, 0.61 acres of undeveloped land in Springfield, Tennessee, and various loans secured by real estate in Heber Springs, Arkansas. Our real estate investments are held by our subsidiary AGB Capital Properties. As of March 29, 2006, we have determined to dispose of all our real estate holdings, including ASG, in order to focus exclusively on patient safety medical products. Our Board of Directors is currently evaluating the available alternatives to determine the most beneficial method to dispose of our real estate holdings. As of December 31, 2005, we had not generated any revenue, nor do we expect to generate any recurring revenue during 2006, on any of our real estate holdings. In the event that we liquidate some or all of our real estate holdings we expect that any gain or loss recognized on the liquidation would be insignificant to us primarily due to the short period of time that the properties were owned combined with the absence of any significant changes in property values in the real estate markets where the real estate holdings are located.

Express Car Wash Business

While we continue to own ASG, we consolidate the operations of its express car wash business with our business. An express car wash is a hybrid of full service conveyor (tunnel) and self-service car wash facilities. At an express wash, customers pay via cash or credit card at an automated kiosk (similar to a drive thru ATM) at the site entrance. The customers remain in their cars while being directed onto a high speed wash tunnel conveyor (2½ minutes +/- to wash completion in tunnel), and have the option of utilizing free vacuum facilities on site prior to exit. Facilities are located at highly visible locations in high automobile traffic locations. Typical sites for a Bubba’s Express Wash will require approximately one acre of land for construction of the tunnel and customer detail/vacuum areas. Facilities generally require two employees for operation. A fully staffed facility will typically require five employees (three full-time employees and two part-time employees).

As described above, as of the date of this report ASG presently has one operating Bubba’s Express Wash site which opened on March 8, 2006. As of March 29, 2006, our Board of Directors has determined to dispose of ASG along with all of our other non-patient safety related assets. Our Board of Directors is currently evaluating the available alternatives to determine the most beneficial method to dispose of ASG and its express car wash business.

Competition

We have concentrations of investments in Heber Springs, Arkansas and Springfield, Tennessee. We compete with a large number of real estate property owners and developers in those regions. Principal factors of competition are attractiveness of location, the quality of the property and breadth and quality of available uses for the property. Since we have not generated any revenue from our real estate holdings, the relative competitive position of the properties cannot be determined. The potential value that we could realize upon disposing of our real estate holdings depends upon, among other factors, trends of the national and local economies, taxes, governmental regulations, legislation and population trends.

ASG’s “express” car wash business competes with other car wash sites, which includes: (a) full service conveyor locations characterized by large numbers of employees required to deliver exterior and interior cleaning services; (b) in-bay automatic facilities (typically at gas stations or convenience stores); (c) self-serve locations (which in the past few years have begun to incorporate in-bay automatic facilities); and (d) full service detailing facilities. Prices generally correspond to the level of personnel required to deliver the service, with the highest prices at detail shops and full service conveyors, lower prices at in-bay facilities, and lowest prices at non-attended self-serve locations. ASG’s express car wash business also competes with the ability of automobile owners to wash their vehicles using their home facilities. ASG competes for car wash business by offering superior value delivered quickly, conveniently and inexpensively. ASG believes its “express” car wash facility provides comparable quality to a full service tunnel or a full service detail shop and at considerably less cost to customers comparable to in-bay automatic facilities and self service locations. The “express” car wash facility is also designed to require less time than any of the competing car wash methods. ASG estimates there are less than 150 “express” car wash sites nationwide in the United States, but that this number continues to grow at a considerable rate. This compares with ASG’s estimate that there are over 30,000 traditional car was facilities. ASG estimates that its express car wash business represents less than one percent of the car wash market in the United States.

Regulation of the Medical Products and Healthcare Industry

The healthcare industry is affected by extensive government regulation at the federal and state levels. In addition, our business may also be subject to varying degrees of governmental regulation in the countries in which operations are conducted, and the general trend is toward regulation of increasing stringency. In the United States, the drug, device, diagnostics and cosmetic industries have long been subject to regulation by various federal, state and local agencies, primarily as to product safety, efficacy, advertising and labeling. The exercise of broad regulatory powers by the Food and Drug Administration (“FDA”) continues to result in increases in the amounts of testing and documentation required for FDA clearance of new drugs and devices and a corresponding increase in the expense of product introduction. Similar trends toward product and process regulation are also evident in a number of major countries outside of the United States, especially in the European Community where efforts are continuing to harmonize the internal regulatory systems.

The FDA administers the Food, Drug and Cosmetics Act (the “FDC Act”). Under the FDC Act, most medical devices must receive FDA clearance through the Section 510(k) notification process (“510(k)”) or the more lengthy premarket approval (“PMA”) process before they can be sold in the United States. All of our products, currently consisting only of the Safety-Sponge™ System, must receive 510(k) clearance or PMA approval. The Center for Devices and Radiological Health (“CDRH”) handles the PMA approval process for medical devices at the FDA. The CDRH places medical devices into one of many predefined groups, then classifies each group into one of three classes (Class I, II or III) based on the level of controls necessary to assure the safety and effectiveness of the specific device group. Class I and II devices also have subsets of “exempt devices” which are exempt from the PMA approval requirement subject to certain limitations. 21 CFR 878.4450 (”Gauze/Sponge, Internal, X-Ray Detectable”) is the defined device group that the Safety-Sponge line of products falls into. This defined device group is specifically denoted as “exempt” from the premarket notification process. Surgicount submitted specific information on its Safety-Sponge product directly to the CDRH and received confirmation of the 501(k) exempt status of this line of products.

To obtain 510(k) marketing clearance, a company must show that a new product is “substantially equivalent” in terms of safety and effectiveness to a product already legally marketed and which does not require a PMA. Therefore, it is not always necessary to prove the actual safety and effectiveness of the new product in order to obtain 510(k) clearance for such product. To obtain a PMA, we must submit extensive data, including clinical trial data, to prove the safety, effectiveness and clinical utility of our products. FDA’s quality system regulations also require companies to adhere to certain good manufacturing practices requirements, which include testing, quality control, storage, and documentation procedures. Compliance with applicable regulatory requirements is monitored through periodic site inspections by the FDA. In addition, we are required to comply with FDA requirements for labeling and promotion. The Federal Trade Commission also regulates most device advertising.

The costs of human health care have been and continue to be a subject of study, investigation and regulation by governmental agencies and legislative bodies in the United States and other countries. In the United States, attention has been focused on drug prices and profits and programs that encourage doctors to write prescriptions for particular drugs or recommend particular medical devices. Managed care has become a more potent force in the market place and it is likely that increased attention will be paid to drug and medical device pricing, appropriate drug and medical device utilization and the quality of health care.

The regulatory agencies under whose purview we operate have administrative powers that may subject us to such actions as product recalls, seizure of products and other civil and criminal sanctions. In some cases we may deem it advisable to initiate product recalls voluntarily. We are also subject to the Safe Medical Devices Act of 1990, which imposes certain reporting requirements on distributors in the event of an incident involving serious illness, injury or death caused by a medical device.

In addition, sales and marketing practices in the health care industry have come under increased scrutiny by government agencies and state attorney generals and resulting investigations and prosecutions carry the risk of significant civil and criminal penalties.

Changes in regulations and healthcare policy occur frequently and may impact our results, growth potential and the profitability of products we sell. There can be no assurance that changes to governmental reimbursement programs will not have a material adverse effect on the Company and our operations.

Regulation of the Real Estate Industry

The real estate development industry is subject to substantial environmental, building, construction, zoning and real estate regulations that are imposed by various federal, state and local authorities. In order to develop our properties, we must obtain the approval of numerous governmental agencies regarding such matters as permitted land uses, density, the installation of utility services (such as water, sewer, gas, electric, telephone and cable television) and the dedication of acreage for various community purposes. Furthermore, changes in prevailing local circumstances or applicable laws may require additional approvals or modifications of approvals previously obtained. Delays in obtaining required approvals and authorizations could adversely affect the profitability of our projects.

Regulation of the Car Wash Industry

We are not aware of any existing or probable governmental regulations that may have a material effect on the normal operations of ASG’s express car wash business. We also are not aware of any relevant environmental laws that require compliance by ASG that may have a material effect on the normal operations of its express car wash business.

Code of Business Conduct and Ethics

Each executive officer and director as well as every employee of the Company is subject to the Company’s Code of Business Conduct and Ethics (the “Code of Ethics”) which was adopted by the Board of Directors on November 11, 2004 and is filed as Appendix D to the definitive proxy materials filed with the SEC on March 2, 2005. The Code of Ethics applies to all directors, officers and certain employees of the Company, including the chief executive officer, chief financial officer, principal accounting officer or controller, or persons performing similar functions. A copy of the Code of Ethics may be obtained, without charge, upon a written request mailed to: Patient Safety Technologies, Inc., c/o Corporate Secretary, 1800 Century Park East, Ste. 200, Los Angeles, California 90067. The Code of Ethics is also posted on our Internet website, which is located at www.patientsafetytechnologies.com.

Available Information

Copies of our quarterly reports on Form 10-Q, annual reports on Form 10-K and current reports on Form 8-K, and any amendments to the foregoing, will be provided without charge to any shareholder submitting a written request to the Corporate Secretary, Patient Safety Technologies, Inc., 1800 Century Park East, Ste. 200, Los Angeles, California 90067 or by calling (310) 895-7750. You may also obtain the documents filed by Patient Safety Technologies, Inc. with the SEC for free at the Internet website maintained by the SEC at www.sec.gov. The Company does not currently make these documents available on its website.

Item 1A. Risk Factors.

An investment in our securities involves a high degree of risk. Before you invest in our securities you should carefully consider the risks and uncertainties described below and the other information in this prospectus. Each of the following risks may materially and adversely affect our business, results of operations and financial condition. These risks may cause the market price of our common stock to decline, which may cause you to lose all or a part of the money you paid to buy our securities. We provide the following cautionary discussion of risks, uncertainties and possible inaccurate assumptions relevant to our business and our products. These are factors that we think could cause our actual results to differ materially from expected results.

RISKS RELATING TO OUR BUSINESS AND STRUCTURE

We have not made any sales or generated any revenue to date from our Safety-Sponge™ System and a substantial amount of our revenue during 2005 is from a related party. Because of this, you should not rely on our historical results of operations as an indication of our future performance.

We have not made any sales or generated any revenue to date from our Safety-Sponge™ System. Further, of our $562,374 of revenue during the fiscal year ended December 31, 2005, $552,375 was generated from a contract to provide management consulting services to one of our portfolio companies IPEX, Inc., which is considered a related party. Our future success is dependent on our ability to develop our patient-safety related assets into a successful business, which depends upon wide-spread acceptance of and commercializing our Safety-Sponge™ System. None of these factors is demonstrated by our historic performance to date and there is no assurance we will be able to accomplish them in order to sustain our operations. As a result, you should not rely on our historical results of operations as an indication of the future performance of our business.

We recently restructured our business strategy and objective and have limited operating history under our new structure. If we cannot successfully implement our new business structure the value of your investment in our business could decline.

Upon the change of control that occurred in October 2004, we restructured our business strategy and objective to focus on the medical products, healthcare solutions, financial services and real estate industries instead of the radio and telecommunications industries. Although we still own certain real estate assets, we are no longer focusing on the financial services and real estate industries. As of March 29, 2006, our Board of Directors determined to focus our business exclusively on the patient safety medical products field. We have a limited operating history under this new structure. Historically, we have not typically invested in these industries and therefore our historical results of operations should not be relied upon as an indication of our future financial performance. If we do not successfully implement our new business structure the value of your investment in our business could decline substantially.

Withdrawal of our election to be treated as a BDC may increase the risks to our shareholders since we are no longer subject the regulatory restrictions or financial reporting benefits of the 1940 Act.

Since we withdrew our election to be treated as a BDC, we are no longer subject to regulation under the 1940 Act, which is designed to protect the interests of investors in investment companies. As a non-BDC, we are no longer subject to many of the regulatory, financial reporting and other requirements and restrictions imposed by the 1940 Act including, but not limited to, limitations on the amounts, types and prices at which we may issue securities, participation in related party transactions, the payment of compensation to executives, and the scope of eligible investments.

The nature of our business has changed from investing in radio and telecommunications companies with the goal of achieving gains on appreciation and dividend income, to actively operating businesses in the medical products, health care solutions, financial services and real estate industries, with the goal of generating income from the operations of those businesses. No assurance can be given that our business strategy or investment objectives will be achieved by withdrawing our election to be treated as a BDC.

Further, our election to withdraw as a BDC under the 1940 Act has resulted in a significant change in our method of accounting. BDC financial statement presentation and accounting utilizes the value method of accounting used by investment companies, which allows BDCs to recognize income and value their investments at market value as opposed to historical cost. As an operating company, the required financial statement presentation and accounting for securities held is either fair value or historical cost methods of accounting, depending on the classification of the investment and our intent with respect to the period of time we intend to hold the investment.

A change in our method of accounting could reduce the market value of our investments in privately held companies by eliminating our ability to report an increase in the value of our holdings as they occur. Also, as an operating company, we have to consolidate our financial statements with subsidiaries, thus eliminating the portfolio company reporting benefits available to BDCs.

The Company and our subsidiaries may have to take actions that are disruptive to our business strategy to avoid registration under the 1940 Act.

The 1940 Act generally requires companies that are engaged primarily in the business of investing, reinvesting, owning, holding or trading in securities to register as investment companies. A company may be deemed to be an investment company if it owns “investment securities” with a value exceeding 40% of the value of its total assets (excluding government securities and cash items) on an unconsolidated basis, unless an exemption or exclusion applies. Securities issued by companies other than majority-owned subsidiaries are generally counted as investment securities for purposes of the 1940 Act. While on an unconsolidated basis, our subsidiaries’ assets which constitute investment securities have not approached 40%, as of December 31, 2005, 37.9% of our assets on a consolidated basis with subsidiaries were comprised of investment securities. If the Company or any of its subsidiaries were to own investment securities with a value exceeding 40% of its total assets it could require the subsidiary and/or the Company to register as an investment company. Registration as an investment company would subject us to restrictions that are inconsistent with our fundamental business strategy of equity growth through creating, building and operating companies in the medical products and healthcare services industries, particularly the patient safety field. Moreover, registration under the 1940 Act would subject us to increased regulatory and compliance costs, and other restrictions on the way we operate. We may also have to take actions, including buying, refraining from buying, selling or refraining from selling securities, when we would otherwise not choose to do so in order to continue to avoid registration under the 1940 Act.

We intend to undertake additional financings to meet our growth, operating and/or capital needs, which may result in dilution to your ownership and voting rights.

We anticipate that revenue from our operations for the foreseeable future will not be sufficient to meet our growth, operating and/or capital requirements. We believe that in order to have the financial resources to meet our operating requirements for the next twelve months we will need to undertake additional equity or debt financings to allow us to meet our future growth, operating and/or capital requirements. We currently have no commitments for any such financings. Any equity financing may be dilutive to our stockholders, and debt financing, if available, may involve restrictive covenants or other adverse terms with respect to raising future capital and other financial and operational matters. We may not be able to obtain additional financing in sufficient amounts or on acceptable terms when needed, which could adversely affect our operating results and prospects. If we fail to arrange for sufficient capital in the future, we may be required to reduce the scope of our business activities until we can obtain adequate financing.

We have received shareholder approval to sell up to $10 million of equity and/or debt securities to certain related parties which may result in dilution to your ownership and voting rights or may result in the incurrence of substantial debt.

We have received shareholder approval to sell equity and/or debt securities up to $10 million in any calendar year to Milton “Todd” Ault, III, Lynne Silverstein, Louis Glazer, M.D., Ph.G., and Melanie Glazer. Mr. Ault is our former Chairman and former Chief Executive Officer, Ms. Silverstein is our President and Secretary, Mr. Glazer is our present Chairman and Chief Executive Officer and the Chief Health and Science Officer of our subsidiary Patient Safety Consulting Group, LLC, and Ms. Glazer is the Manager of our subsidiary Ault Glazer Bodnar Capital Properties, LLC and also is Mr. Glazer’s spouse. If we propose to sell more than $10 million of securities in a calendar year to such persons additional shareholder approval would be required. Although we do not currently anticipate selling equity or debt securities to these persons if we do sell any such securities it will result in dilution to your ownership and voting rights and/or possibly result in our incurring substantial debt. Any such equity financing would result in dilution to existing stockholders and may involve securities that have rights, preferences, or privileges that are senior to our common stock. Any such debt financing may be convertible into common stock which would result in dilution to our stockholders and would have rights that are senior to our common stock. Further, any debt financing must be repaid regardless of whether or not we generate profits or cash flows from our business activities, which could strain our capital resources.

Should the value of our patents be less than their purchase price, we could incur significant impairment charges.

At December 31, 2005, patents received in the acquisition of Surgicount Medical, Inc., net of accumulated amortization, represented $4,413,791, or 27.5%, of our total assets. We perform an annual review in the fourth quarter of each year, or more frequently if indicators of potential impairment exist to determine if the recorded amount of our patents is impaired. This determination requires significant judgment and changes in our estimates and assumptions could materially affect the determination of fair value and/or impairment of patents. We may incur charges for the impairment of our patents in the future if sales of our patient safety products, in particular our Safety-Sponge™ System, fail to achieve our assumed revenue growth rates or assumed operating margin results.

We may not be able to effectively integrate our acquisition targets, which would be detrimental to our business.

On February 25, 2005, we purchased Surgicount Medical, Inc., a holding company for intellectual property rights relating to our Safety-Sponge™ System. We anticipate seeking other acquisitions in furtherance of our plan to acquire assets and businesses in the patient safety medical products industry. Acquisitions involve numerous risks, including potential difficulty in integrating operations, technologies, systems, and products and services of acquired companies, diversion of management’s attention and disruption of operations, increased expenses and working capital requirements and the potential loss of key employees and customers of acquired companies. In addition, acquisitions involve financial risks, such as the potential liabilities of the acquired businesses, the dilutive effect of the issuance of additional equity securities, the incurrence of additional debt, the financial impact of transaction expenses and the amortization of goodwill and other intangible assets involved in any transactions that are accounted for by using the purchase method of accounting, and possible adverse tax and accounting effects. Any of the foregoing could materially and adversely affect our business.

Failure to properly manage our potential growth would be detrimental to our business.

Any growth in our operations will place a significant strain on our resources and increase demands on our management and on our operational and administrative systems, controls and other resources. There can be no assurance that our existing personnel, systems, procedures or controls will be adequate to support our operations in the future or that we will be able to successfully implement appropriate measures consistent with our growth strategy. As part of this growth, we may have to implement new operational and financial systems, procedures and controls to expand, train and manage our employee base and maintain close coordination among our technical, accounting, finance, marketing, sales and editorial staffs. We cannot guarantee that we will be able to do so, or that if we are able to do so, we will be able to effectively integrate them into our existing staff and systems. We may fail to adequately manage our anticipated future growth. We will also need to continue to attract, retain and integrate personnel in all aspects of our operations. Failure to manage our growth effectively could hurt our business.

If the protection of our intellectual property rights is inadequate, our ability to compete successfully could be impaired.

In connection with our purchase of Surgicount Medical, Inc., we acquired one registered U.S. patent and one registered international patent of the Safety-Sponge™ System. We regard our patents, copyrights, trademarks, trade secrets and similar intellectual property as critical to our business. We rely on a combination of patent, trademark and copyright law and trade secret protection to protect our proprietary rights. Nevertheless, the steps we take to protect our proprietary rights may be inadequate. Detection and elimination of unauthorized use of our products is difficult. We may not have the means, financial or otherwise, to prosecute infringing uses of our intellectual property by third parties. Further, effective patent, trademark, service mark, copyright and trade secret protection may not be available in every country in which we will sell our products and offer our services. If we are unable to protect or preserve the value of our patents, trademarks, copyrights, trade secrets or other proprietary rights for any reason, our business, operating results and financial condition could be harmed.

Litigation may be necessary in the future to enforce our intellectual property rights, to protect our trade secrets, to determine the validity and scope of the proprietary rights of others, or to defend against claims that our products infringe upon the proprietary rights of others or that proprietary rights that we claim are invalid. Litigation could result in substantial costs and diversion of resources and could harm our business, operating results and financial condition regardless of the outcome of the litigation.

Other parties may assert infringement or unfair competition claims against us. We cannot predict whether third parties will assert claims of infringement against us, or whether any future claims will prevent us from operating our business as planned. If we are forced to defend against third-party infringement claims, whether they are with or without merit or are determined in our favor, we could face expensive and time-consuming litigation, which could distract technical and management personnel. If an infringement claim is determined against us, we may be required to pay monetary damages or ongoing royalties. Further, as a result of infringement claims, we may be required, or deem it advisable, to develop non-infringing intellectual property or enter into costly royalty or licensing agreements. Such royalty or licensing agreements, if required, may be unavailable on terms that are acceptable to us, or at all. If a third party successfully asserts an infringement claim against us and we are required to pay monetary damages or royalties or we are unable to develop suitable non-infringing alternatives or license the infringed or similar intellectual property on reasonable terms on a timely basis, it could significantly harm our business.

There are significant potential conflicts of interest with our officers, directors and our affiliated entities which could adversely affect our results from operations.

Certain of our officers, directors and/or their family members have existing responsibilities and, in the future, may have additional responsibilities, to act and/or provide services as executive officers, directors, owners and/or managers of Ault Glazer Bodnar & Company Investment Management LLC and/or some of the companies in which we invest. We currently share office space with Ault Glazer Bodnar & Company Investment Management LLC. William B. Horne, our Chief Financial Officer, and Melanie Glazer, Manager of our subsidiary Ault Glazer Bodnar Capital Properties, LLC, are principals of Ault Glazer Bodnar & Company Investment Management LLC. Mr. Horne devotes approximately 85% of his time to our business, based on a 60-hour, 6-day workweek. Mrs. Glazer works full time for Ault Glazer Bodnar Capital Properties, LLC. Mrs. Glazer is married to Louis Glazer, M.D., Ph.G., our current Chairman and Chief Executive Officer and Chief Health and Science Officer of Patient Safety Consulting Group, LLC. Our former Chairman and Chief Executive Officer, Milton “Todd” Ault, III, also is a principal of Ault Glazer Bodnar & Company Investment Management LLC. Accordingly, certain conflicts of interest may arise from time to time with our officers, directors and Ault Glazer Bodnar & Company Investment Management LLC.

Certain conflicts of interest may also arise from time to time with our officers, directors and the companies in which we invest. Of our $562,374 of revenue during the fiscal year ended December 31, 2005, $552,375 resulted from a contract to provide management consulting services to our portfolio company IPEX, Inc. Mr. Ault is currently a director of IPEX, Inc. and he served as interim Chief Executive Officer of IPEX, Inc. from May 26, 2005 until July 13, 2005. From May 28, 2005 until approximately December 14, 2005 Mr. Ault held an irrevocable proxy to vote 67% of the outstanding shares of IPEX, Inc. owned by the former Chief Executive Officer and a founder of IPEX, Inc. Darrell W. Grimsley, Jr., Chief Executive Officer of Automotive Services Group, LLC, a subsidiary which, as of March 14, 2006, is wholly owned by Ault Glazer Bodnar Merchant Capital, Inc., served as a director of IPEX, Inc. and a member of its Audit Committee from August 30, 2005 until January 30, 2006. Ms. Campbell served as a director of IPEX, Inc. and Chairman of its Audit Committee from June 23, 2005 until January 30, 2006. Mr. Horne is currently Chief Financial Officer and a director of our portfolio company Digicorp. From September 30, 2005 until December 29, 2005, Mr. Horne also served as Digicorp’s Chief Executive Officer and Chairman of Digicorp’s Board of Directors. One of our directors and Audit Committee Chairman, Alice Campbell, is currently a director of Digicorp. Mr. Ault served as Chief Executive Officer of Digicorp from April 26, 2005 until September 30, 2005 and Chairman of Digicorp’s Board of Directors from July 16, 2005 until September 30, 2005. Ms. Glazer served as a director of Digicorp from December 30, 2004 until December 29, 2005 and Chairman of Digicorp’s Board of Directors from December 30, 2004 until July 16, 2005. Ms. Silverstein served as Secretary of Digicorp from April 26, 2005 until December 29, 2005. Mr. Grimsley served as a director of Digicorp from July 16, 2005 until December 29, 2005.

Because of these possible conflicts of interest, such individuals may direct potential business and investment opportunities to other entities rather than to us, which may not be in the best interest of our stockholders. We will attempt to resolve any such conflicts of interest in our favor. Our Board of Directors does not believe that we have experienced any losses due to any conflicts of interest with the business of Ault Glazer Bodnar & Company Investment Management LLC, other than certain of our officers’ responsibility to devote their time to provide management and administrative services to Ault Glazer Bodnar & Company Investment Management LLC and its clients from time-to-time. Similarly, our Board of Directors does not believe that it has experienced any losses due to any conflicts of interest with the companies in which we hold investments other than certain of our officers’ and directors’ responsibility to devote their time to provide management services to some of such companies. However, subject to applicable law, we may engage in transactions with Ault Glazer Bodnar & Company Investment Management LLC and other related parties in the future. These related party transactions may raise conflicts of interest and, although we do not have a formal policy to address such conflicts of interest, our Audit Committee intends to evaluate relationships and transactions involving conflicts of interest on a case-by-case basis and the approval of our Audit Committee is required for all such transactions. The Audit Committee intends that any related party transactions will be on terms and conditions no less favorable to us than terms and conditions reasonably obtainable from third parties and in accordance with applicable law.

Our management has limited experience in managing and operating a public company. Any failure to comply or adequately comply with federal securities laws, rules or regulations could subject us to fines or regulatory actions, which may materially adversely affect our business, results of operations and financial condition.

Although our present Chairman and Chief Executive Officer, Louis Glazer, M.D., Ph.G., has extensive experience in the medical field, he has limited experience managing and operating a public company. In addition, prior to the change in control that occurred in October 2004, other members of our current senior management were primarily engaged in operating a private investment management firm. In this capacity they developed a general understanding of the administrative and regulatory environment in which public companies operate. However, our senior management lacks practical experience operating a public company and relies in many instances on the professional experience and advice of third parties including its consultants, attorneys and accountants. Failure to comply or adequately comply with any laws, rules, or regulations applicable to our business may result in fines or regulatory actions, which may materially adversely affect our business, results of operation, or financial condition.

We have experienced turnover in our Chief Executive Officer position in recent months and we are presently searching for a new Chief Executive Officer to replace Dr. Louis Glazer. If we are not able to retain a new Chief Executive Officer with significant professional experience in the patient safety or medical markets and pubic market experience, we may have difficulty implementing our business strategy.

Milton “Todd” Ault, III resigned as our Chairman and Chief Executive Officer on January 9, 2006. On January 7, 2006, our Board of Directors appointed Louis Glazer, M.D., Ph.G. as Chairman and Chief Executive Officer in anticipation of Mr. Ault’s resignation. During March 2005, Dr. Glazer has indicated his intent to resign as Chairman and Chief Executive Officer at such time that we retain a suitable candidate for the position of Chief Executive Officer. Our future success is dependent on our ability to attract and retain such a candidate. Although we do not believe we have experienced any losses or negative effects from Mr. Ault’s resignation and we do not expect any adverse consequences from the resignation of Dr. Glazer, if we are not able to retain a new Chief Executive Officer with significant professional experience in the patient safety or medical markets and public market experience, we may have difficulty implementing our business strategy.

Our former Chief Executive Officer controls a significant portion of our outstanding common stock and his ownership interest may conflict with our other stockholders who may be unable to influence management and exercise control over our business.

As of March 26, 2006, Milton “Todd” Ault, III, our former Chief Executive Officer and Chairman, beneficially owned approximately 26.6% of our common stock. As a result, Mr. Ault may be able to exert significant influence over our management and policies to:

| | · | elect or defeat the election of our directors; |

| | · | amend or prevent amendment of our certificate of incorporation or bylaws; |

| | · | effect or prevent a merger, sale of assets or other corporate transaction; and |

| | · | control the outcome of any other matter submitted to the shareholders for vote. |

Accordingly, our other stockholders may be unable to influence management and exercise control over our business.

RISKS RELATED TO OUR MEDICAL PRODUCTS AND HEALTHCARE-RELATED BUSINESS

We rely on a third party manufacturer and supplier to manufacture our Safety-Sponge™ System, the loss of which may interrupt our operations.

On August 17, 2005, Surgicount entered into an agreement for A Plus International Inc. to be the exclusive manufacturer and provider of Surgicount’s Safety-Sponge™ products. In the event A Plus International Inc. does not meet the requirements of the agreement, Surgicount may seek additional providers of the Safety-Sponge™ products. While our relationship with A Plus International Inc. is currently on good terms, we cannot assure you that we will be able to maintain our relationship with A Plus International Inc. or secure additional suppliers and manufacturers on favorable terms as needed. Although we believe the materials used in the manufacture of the Safety-Sponge™ System are readily available and can be purchased and/or produced by multiple vendors, the loss of our agreement with A Plus International Inc., the deterioration of our relationship with A Plus International Inc., changes in the specifications of components used in our products, or our failure to establish good relationships with major new suppliers or manufacturers as needed, could have a material adverse effect on our business, financial condition and results of operations.

The unpredictable product cycles of the medical device and healthcare-related industries and uncertain demand for products could cause our revenues to fluctuate.

Our target customer base includes hospitals, physicians, nurses and clinics. The medical device and healthcare-related industries are subject to rapid technological changes, short product life cycles, frequent new product introductions and evolving industry standards, as well as economic cycles. If the market for our products does not grow as rapidly as our management expects, our revenues could be less than expected. We also face the risk that changes in the medical device industry, for example, cost-cutting measures, changes to manufacturing techniques or production standards, could cause our manufacturing, design and engineering capabilities to lose widespread market acceptance. If our products do not gain market acceptance or suffer because of competing products, unfavorable regulatory actions, alternative treatment methods or cures, product recalls or liability claims, they will no longer have the need for our products and we may experience a decline in revenues. Adverse economic conditions affecting the medical device and healthcare-related industries, in general, or the market for our products in particular, could result in diminished sales, reduced profit margins and a disruption in our business.