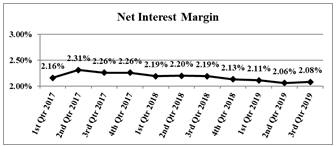

As illustrated in the table above, the main contributors to the increase in net interest income were from, securitiesheld-to-maturity, loans, securitiesavailable-for-sale, and interest-bearing deposits in other banks. Securitiesheld-to-maturity income increased primarily as a result of an increase in volume as well as rates. Loan income increased primarily from an increase in volume and an overall increase in rates. Securitiesavailable-for-sale income increased from an increase in rates paid on the portfolio. The Company has a sizable floating rateavailable-for-sale portfolio. These securities reprice as interest rates rise or fall. Interest-bearing deposits expense increased primarily from an increase in rates. The increase in interest income was partially offset by an increase in interest expense. This was mainly the result of increased rates paid on interest-bearing liabilities. The Company has modestly raised interest rates on these products to remain competitive.

Provision for Loan Losses

For the three months ended September 30, 2019, the loan loss provision was $75,000 compared to a provision of $0 for the same period last year. For the nine months ended September 30, 2019, the loan loss provision was $700,000 compared to a provision of $900,000 for the same period last year. The increase in the provision for the third quarter of 2019 was primarily the result of net loan recoveries during the third quarter of 2019. The decrease in the provision, for the nine month period ending, was primarily the result of improvements in historical loss factors. Further discussion relating to changes in portfolio composition is discussed in Note 4.

Non-Interest Income and Expense

Other operating income for the quarter ended September 30, 2019 increased by $117,000 from the same period last year to $4,286,000. This was mainly attributable to an increase in lockbox fees of $45,000 and an increase in service charges on deposit accounts of $173,000. This was offset, somewhat, by a decrease in net gains on sales of securities of $52,000 and a decrease in other income of $49,000. Lockbox income increased as a result of an increase in customer accounts. Service charges on deposit accounts increased primarily as a result of an increase in customer activity. Other income decreased mainly as a result of decreases in gains on insurance policies.

Other operating income for the nine months ended September 30, 2019 increased by $1,626,000 from the same period last year to $13,710,000. This was mainly attributable to an increase in lockbox fees of $714,000, an increase in other income of $466,000, an increase in service charges on deposit accounts of $533,000, and gains on sales of mortgage loans of $154,000 offset, somewhat, by a decrease of $241,000 from the sales of securities. Lockbox income increased as a result of an increase in customer accounts. Other income increase mainly as a result of proceeds from life insurance policies. Service charges on deposit accounts increased primarily as a result of an increase in customer activity.

For the quarter ended September 30, 2019, operating expenses increased by $114,000 or 0.7% to $17,462,000, from the same period last year. This was primarily attributable to an increase in salaries and employee benefits of $100,000 and an increase equipment expenses of $81,000. This was offset, somewhat, by a decrease of $49,000 in other expenses and a decrease of $18,000 in occupancy expenses. The increase in salaries and employee benefits was mainly attributable to merit increases. Equipment expense increased mainly from an increase in service contracts. Occupancy costs decreased primarily as a result of decreases in building maintenance. Other expenses decreased mainly as a result of FDIC assessment credits recognized during the quarter, offset, somewhat, by an increase in pension expense.

For the nine months ended September 30, 2019, operating expenses increased by $1,409,000 or 2.7% to $53,917,000, from the same period last year. This was primarily attributable to an increase in other expenses of $927,000, salaries and employee benefits of $290,000, and occupancy expenses of $107,000, and equipment expenses of $85,000. Other expenses increased primarily as a result of increases in pension and consulting expense offset, somewhat, by FDIC assessment credits recognized during the third quarter of 2019. Salaries and employee benefits increased mainly as a result of merit increases. Occupancy costs increased primarily as a result of increases in rent expense associated with a new operating facility and other annual rent increases. Equipment expenses increased mainly as a result of increases in service contracts.

Income Taxes

For the third quarter of 2019, the Company’s income tax expense totaled $435,000 on pretax income of $10,519,000 resulting in an effective tax rate of 4.1%. For last year’s corresponding quarter, the Company’s income tax expense totaled $444,000 on pretax income of $10,025,000 resulting in an effective tax rate of 4.4%. For the first nine months of 2019, the Company’s income tax expense totaled $584,000 on pretax income of $29,551,000 resulting in an effective tax rate of 2.0%. For the first nine months of 2018, the Company’s income tax expense totaled $1,259,000 on pretax income of $27,547,000 resulting in an effective tax rate of 4.6%. The decrease in the effective tax rate, for the nine month period, was primarily as a result of a reduction in tax accruals related to sequestration of the refundable portion of our alternative minimum tax (AMT) credit carryforward. On January 14, 2019, the IRS updated its announcement “Effect of Sequestration on the Alternative Minimum Tax Credit for Corporations” to clarify that refundable AMT credits under Section 53(e) of the Internal Revenue Code are not subject to sequestration for taxable years beginning after December 31, 2017. Therefore, the full amount of the AMT credit carryover will be refunded to the Company.

Page 45 of 48