MTI & AMCOL Creating a Global Leader in Minerals Exhibit 99.1 |

IMPORTANT INFORMATION The tender offer referred to in this presentation has not yet commenced. This presentation is for informational purposes only and it is neither an offer to purchase nor a solicitation of an offer to sell shares of AMCOL’s common stock. At the time any such tender offer is commenced, MTI will file a Tender Offer Statement on Schedule TO, containing an offer to purchase, a form of letter of transmittal and other related tender offer documents with the SEC, and AMCOL will file a Solicitation/Recommendation Statement relating to such tender offer with the SEC. AMCOL’s stockholders are strongly advised to read these tender offer materials carefully and in their entirety when they become available, as they may be amended from time to time, because they will contain important information about such tender offer that AMCOL’s stockholders should consider prior to making any decisions with respect to such tender offer. Once filed, stockholders of AMCOL will be able to obtain a free copy of these documents at the website maintained by the SEC at www.sec.gov. Disclaimer 2 FORWARD-LOOKING STATEMENTS This presentation may contain “forward-looking statements,” which describe or are based on current expectations; in particular within the meaning of the federal securities laws, statements of anticipated changes in the business environment in which the company operates, the expected timing and benefits of the proposed acquisition of Amcol and in the company’s future operating results. Actual results may differ materially from these expectations. In addition, any statements that are not historical fact (including statements containing the words “believes,” “plans,” “anticipates,” “expects,” “estimates,” and similar expressions) should also be considered to be forward-looking statements. The company undertakes no obligation to publicly update any forward-looking statement, whether as a result of new information, future events, or otherwise. Forward-looking statements in this document should be evaluated together with the many uncertainties that affect our businesses, particularly those mentioned in the risk factors and other cautionary statements in our 2013 Annual Report on Form 10-K and in our other reports filed with the Securities and Exchange Commission (the “SEC”). |

MTI’s acquisition of AMCOL accelerates growth and creates shareholder value • Portfolio of market leader positions • Broad portfolio of complementary products • World class innovators in mineralogy, fine particle technology and polymer chemistry • Diversification into energy, environmental and consumer products • Geographic expansion • Continued innovation • Historical growth and geographic expansion • High-performance operating company • Continuous improvement • Strong cash flow • Immediately accretive excluding transaction costs • Rapid deleveraging expected Combines global leaders in PCC and Bentonite Platform for accelerated growth MTI’s performance track record Long-term growth in shareholder value 3 |

Is entirely consistent with MTI’s M&A strategy 4 Source: Company presentations. • Minerals-Based Companies with Technological Differentiation • Additional Growth Venues – Environment, Energy, Consumer • More Balanced, Less Cyclical Portfolio • Industries of Focus – Alternative Energy – Food – Oil/Gas – Recycling – Environment – Beverages – Pharmaceuticals Transaction Scorecard |

• Implied enterprise value to 2013A EBITDA of 11.1x without synergies and 8.4x with $50 million near-term synergies • 33% premium over AMCOL’s 30-day moving average • Immediately accretive to MTI’s earnings before expected synergies • MTI to acquire 100% of outstanding AMCOL shares in tender offer/merger • $45.75 per AMCOL share in cash • $1.7B transaction value including assumption of AMCOL’s debt • Committed debt financing of $1.56 billion supplemented with MTI cash • Transaction subject to customary conditions, including regulatory approvals • Closing expected prior to May 2014 Offers superior value to AMCOL shareholders 5 NOTE: EBITDA multiples based on $150m AMCOL adjusted 2013 EBITDA TIMING KEY METRICS OFFER SUMMARY |

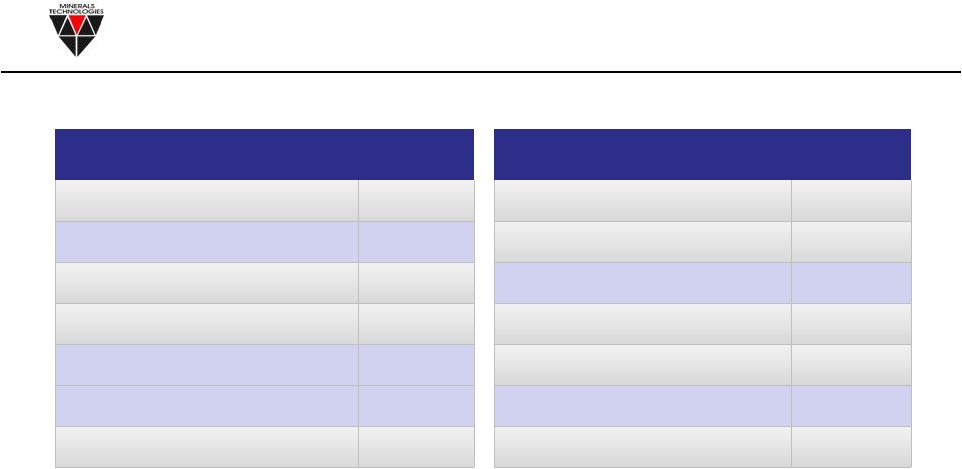

SOURCES ($ in millions) MTI Cash $394 MTI New Debt Financing $1,560 Term Loan B Total Sources $1,954 USES ($ in millions) Purchase of Equity $1,520 Debt Refinanced $371 Transaction Costs $38 Make Whole / Swap Unwind $25 Total Uses $1,954 Transaction sources and uses 6 Source: Company filings, MTI management projections. |

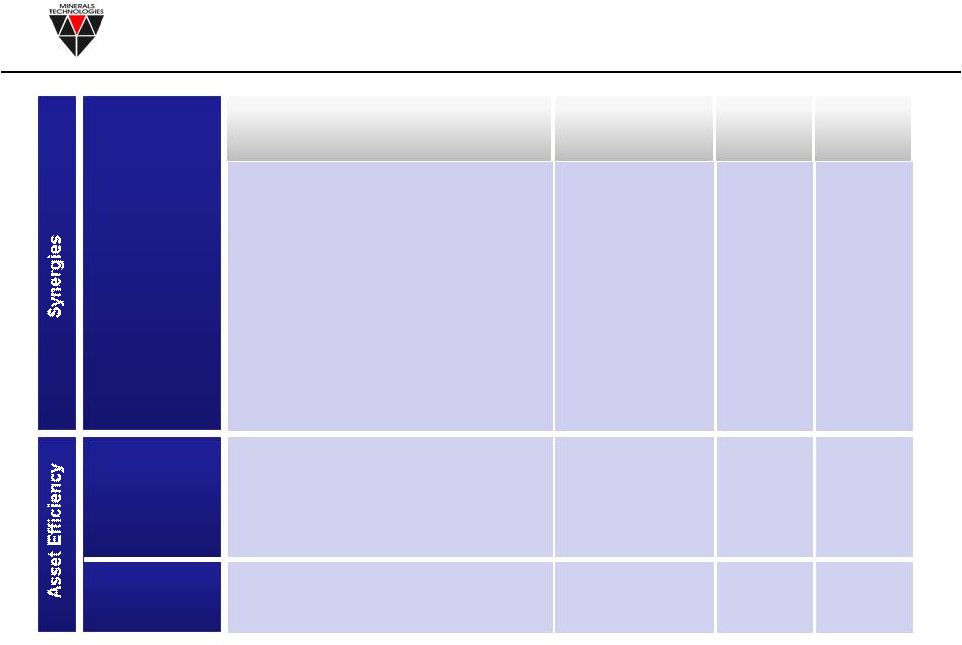

Unlocks more than $50 million of cost synergies and releases more than $100 million cash 7 DESCRIPTION RUN RATE ANNUAL SYNERGIES (Run Rate Year) AS % of AMCOL SALES AS % of Combined EBITDA GROWTH & OPERATIONAL EXCELLENCE • Acceleration of geographic expansion and new product development • Rapid deployment of MTI shared service business model • Productivity improvement throughout AMCOL operations • Corporate and overhead expense reduction • ERP integration $50m in 2-3 years Up to $70m in 5 years 5-7% ~16-21% NET WORKING CAPITAL IMPROVEMENTS • Reduction of Net Working Capital days outstanding Up to $100m (2014-2017) ASSET TURNOVER • Improvement in asset utilization and capital deployment Up to $50m (2014-2019) |

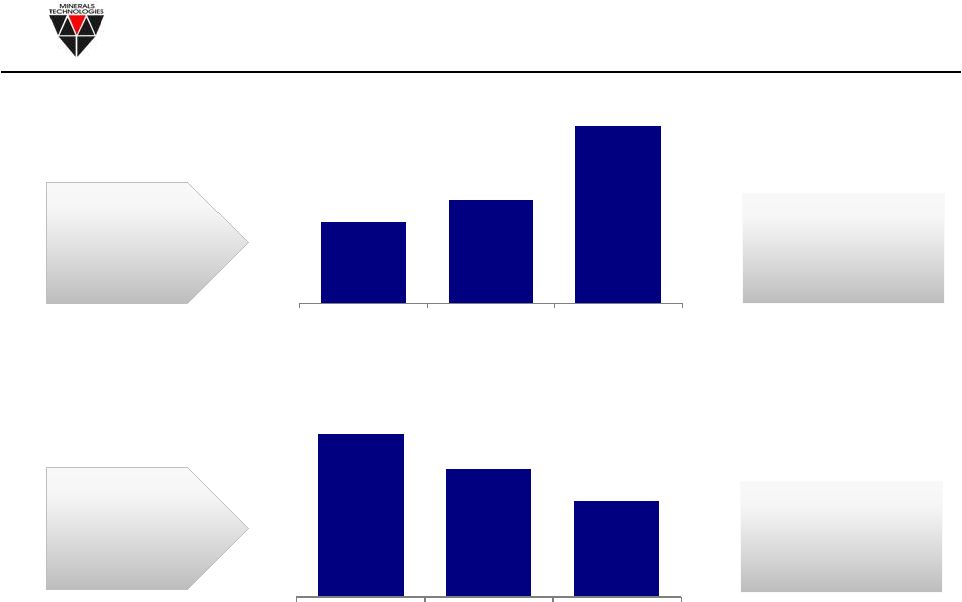

Transaction will be highly accretive to earnings 8 Source: Company filings, MTI management projections. NOTE: accretion excludes transaction costs PRO FORMA EPS ACCRETION vs MTI 2013 of $2.42 / share EOY 39% 50% 55% Year 1 Year 2 Year 3 94% 71% Without Synergies $50m Synergies |

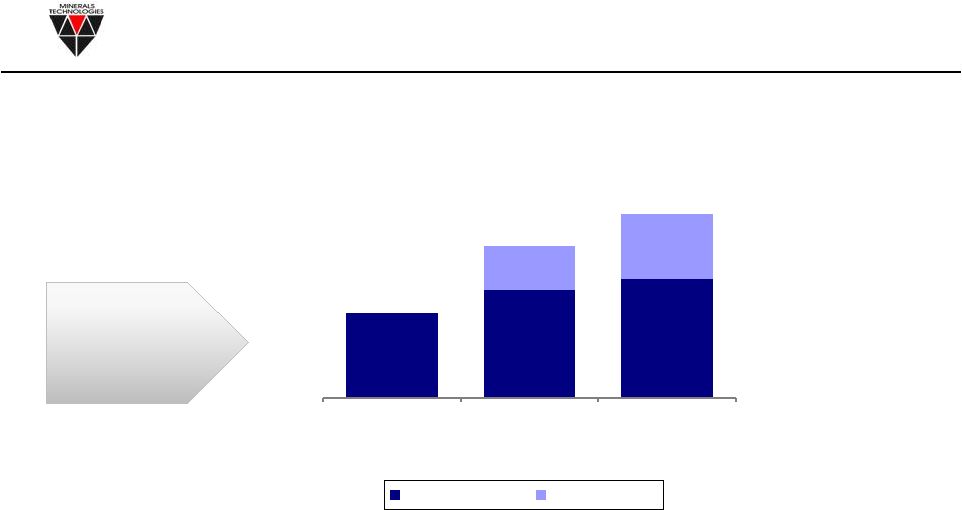

Generates significant cash and results in rapid deleveraging 9 Source: Company filings, MTI management projections. More than $265 million per year PRO FORMA CASH FROM OPERATIONS 3.8x 3.0x 2.2x Year 1 Year 2 Year 3 Committed to rapid deleveraging PRO FORMA NET LEVERAGE 4.4x At Close EOY EOY EOY $265 $283 $343 Year 1 Year 2 Year 3 $MM |

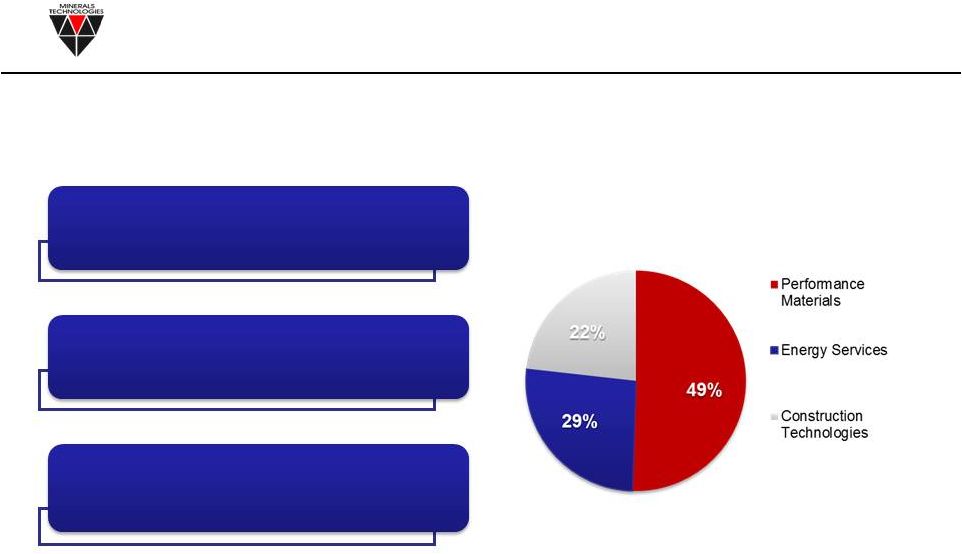

AMCOL: Broad and diversified product offering across segments 10 Product Offerings Sales Concentration Key drivers of profit include growth in core markets, growth in geographies such as China, India and Brazil, margin expansion and optimization of business/product portfolio. Performance Materials Includes: Metalcasting, drilling fluids, pet products, bioAg Energy Services Includes: Includes: Water treatment, well testing, coil tubing Construction Technologies Includes: Building materials, drilling products, environmental lining technologies, mercury removal |

MTI to further deploy strong culture of operational excellence, productivity improvement and employee engagement MTI management has proven ability to effectively manage SG&A, capex and NWC $50m of cost synergies, maybe as much as $70m in the next five years Combines two global #1 industrial minerals platforms: PCC (MTI) and bentonite (AMCOL) Less cyclical with increased relevance and visibility to investors Creates a leading US-based industrial minerals company with over $2bn in sales MTI and AMCOL are both US-based, global, industrial minerals companies with “mine-to-market” business models Both deliver value via differentiated mineral and processing technology and innovation Complementary end markets and geographic presence Expands MTI participation into energy, environmental and consumer products Shared end markets including: adhesives and sealants, fillers and extenders for paper, steel and metal, health and beauty, animal feed and pet waste absorbents Combined $300m of current sales in high-growth Asian markets More than $1bn of identified innovation and geographic growth opportunities in five to ten years MTI has consistently demonstrated commitment to a conservative capital structure Both MTI and AMCOL have strong cash flows - Long-term contracts for MTI PCC; diversified end markets for AMCOL bentonite - Combined entity would have been free cash flow positive during the recent financial crisis Net leverage projected to decline below 2.2x by end of third year after closing Provides a superior growth outlook, healthy operating margins and strong cash flows 11 Complementary Business Models &Technologies Superior Growth Outlook Compelling Synergies Strong Cash Flows Enhanced Scale & Diversification |

• 2013 sales: $1.0bn • Mineralogy • Fine particle and surface treatment • End-use application knowledge Leverages complementary fit based on similar geographies and differentiated product and process technologies 12 Size Revenue Geographic Breakdown Technology And Process Know-how Strong Market Positions End Markets Service Focus Investment Focus Investor Group MTI • Paint and coatings • Glass and ceramics • Steel • Paper • Building materials • Automotive • ~$340m steel mill services • Global PCC • North America Specialty PCC • Monolithic BOF • Talc AMCOL • 2013 sales: $1.0bn • Clay mineralogy • Polymer science • End-use application knowledge • North America bentonite • Auto foundry castings • Environmental lining • Water treatment • Automotive • Building materials • Oil and gas • Infrastructure • ~$300m energy services - China, India, Brazil and Middle East - Focused investments with expected long-term returns ~40-50% of each company owned by common shareholders (as of 12/31) |

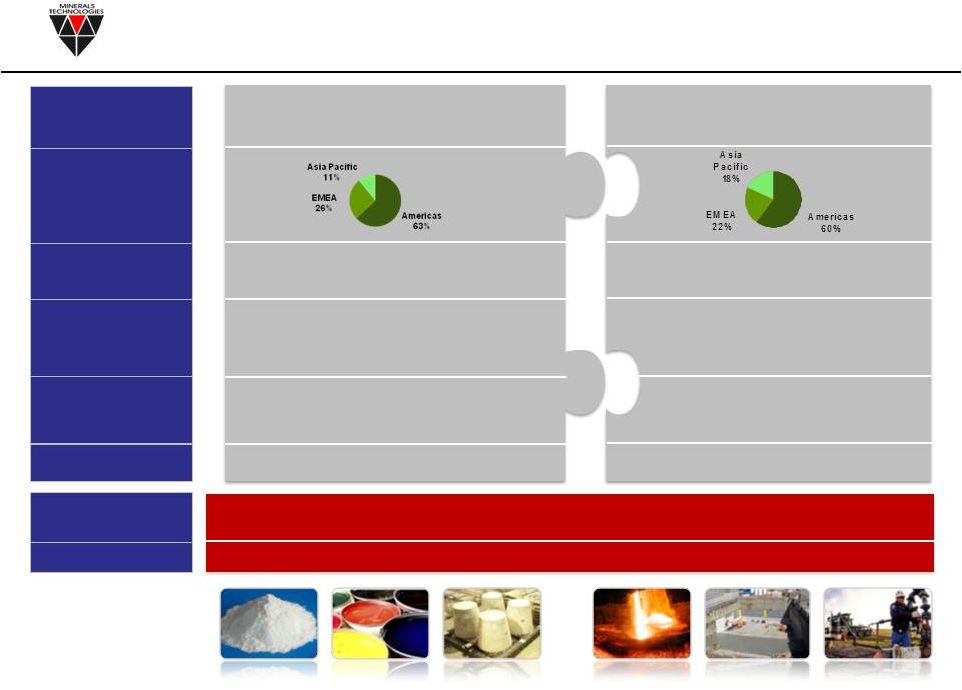

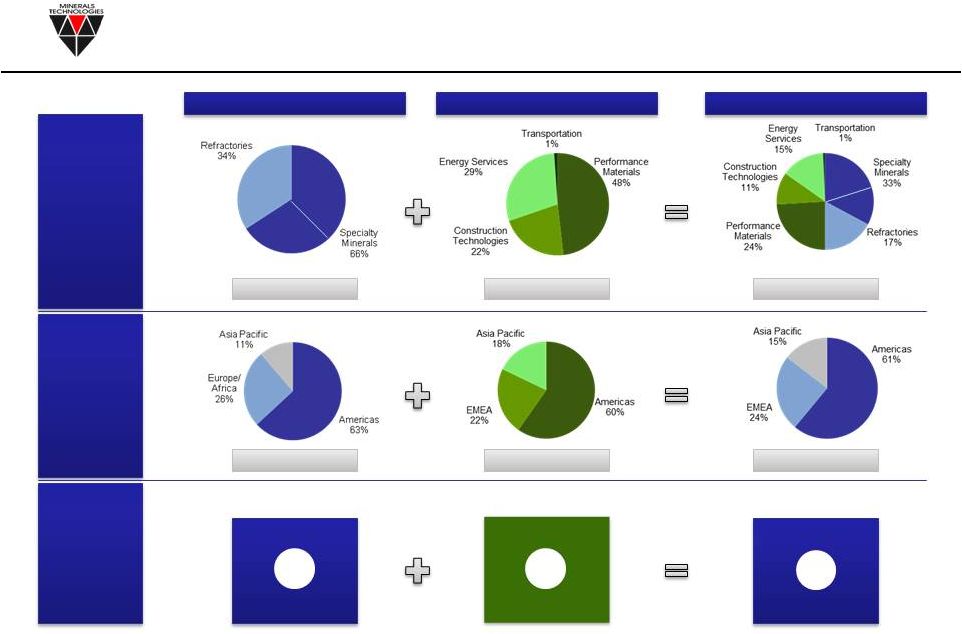

Perf Min Paper PCC Paper PCC Perf Min 2013A REVENUE BY SEGMENT ($ in bn) 2013A REVENUE BY SEGMENT ($ in bn) 2013A REVENUE BY GEOGRAPHY ($ in bn) 2013A REVENUE BY GEOGRAPHY ($ in bn) PRO FORMA (a) PRO FORMA (a) $2.0bn $2.0bn Source: MTI Management, Wall Street research. (a) Does not include potential synergies. MTI MTI $1.0bn $1.0bn AMCOL AMCOL $1.0bn $1.0bn 2013A EBITDA AND MARGIN ($ in m) 2013A EBITDA AND MARGIN ($ in m) 13 Pro forma business mix 17% 15% 16% $174 $150 $324 |

Results in strong #1 leadership positions across multiple industries 14 # 1 Global and North American Bentonite #1 US Bulk Clumping Cat Litter # 1 US Metalcasting Binders for Auto & Heavy Equipment AMCOL Leadership Positions # 1 Quality Assured Waterproof Concrete Structures MTI Leadership Positions #1 Global PCC #1 North American Monolithic Refractories #1 North America and Europe Solid Core Calcium Wire #1 Global Refractory Laser Measurement Systems # 1 North American Specialty PCC #1 US & Brazil Off-shore Water Treatment |

• Adhesives and sealants • Functional fillers and extenders • Consumer products • Animal feed • Pet waste absorbents • Agricultural products Creates a portfolio of $1 billion growth opportunities 15 AMCOL Growth • Continued penetration of PCC for Paper in Asia’s growing market • Further commercialization of FulFill® high filler technology • Commercialization of Paper PCC innovation pipeline • Further growth of full-service refractories business model • Continued growth of metallurgical wire business • Expansion of new MTI EAF refractory products • Customization and globalization of Performance Minerals MTI Growth New Growth Opportunities • Global expansion of water treatment technologies for oil-field applications • Further success with new Amcol lining technologies • Introduction of new mercury sorbent technologies for coal-fired power plants • Expansion of Enersol TM into bio/ag industry |

• MTI and AMCOL are starting to work together to affect a smooth transition • Integration plan is focused on: • Employees • Customers • Suppliers • Business segment strategies • Achievement of targeted synergies • Assuring stability and continuity of: • Business processes • All operations • Key relationships • Investments Focused on integration 16 |

Customer focused employees Strong cash flows Superior performance and operational excellence A $2bn minerals-based company with global reach based on: • Mine-to-market value chain management • Demonstrated process technology and innovation leadership • Broad and deep talent pool • Deeper geographic footprint • Significant end market overlap Allowing reinvestment in: • Further market penetration and geographic expansion, especially in Asia • Innovating customized technologies to satisfy future customer needs • Organic growth across all business segments …creating superior return for shareholders Minerals Technologies’ vision for the future 17 |