| Exhibit 99.1

> News Release |

Newell Rubbermaid Reports Second Quarter 2010 Results

Normalized EPS of $0.51; Raising FY2010 Guidance

Gross Margin Expansion of 220 Basis Points

Strong Operating Cash Flow

ATLANTA, July 30, 2010– Newell Rubbermaid (NYSE: NWL) today announced second quarter 2010 financial results, including normalized earnings per share of $0.51, an 8.5 percent improvement over prior year results, and gross margin expansion of 220 basis points. The company also reported operating cash flow of $154.0 million, a 55.2 percent improvement over the prior year quarter.

“I am very pleased with the performance of our business,” said Mark Ketchum, President and Chief Executive Officer. “We delivered strong second quarter results across almost all metrics, including core sales growth of almost 4 percent, if adjusted for the customer orders shift from the second quarter to the first quarter in advance of an April SAP implementation. This growth was the result of a combination of market share gains and distribution wins as well as strong consumer demand in Latin American and developing markets in EMEA. We also generated significant improvement in gross margin this quarter driven by productivity gains and improved product mix. The solid progress we’ve made year to date despite a lackluster economy gives us increased confidence that our business model is working.”

Net sales in the second quarter were $1.50 billion, down 0.5 percent compared with the prior year. Core sales improved 1.5 percent. Core sales growth was 3.8 percent if adjusted for a timing shift in customer buying patterns from the second quarter to the first quarter in advance of an April SAP implementation at the Rubbermaid Consumer and Rubbermaid Commercial Products business units. The year over year impact of last year’s product line exits reduced net sales by 1.9 percent, and foreign currency translation had a nominal impact on sales.

Gross margin for the quarter was 39.3 percent, up 220 basis points from last year as productivity gains and improved product mix more than offset the impact of input cost inflation.

Operating income was $226.3 million, or 15.1 percent of sales, excluding $22.8 million of Project Acceleration restructuring costs and restructuring related costs incurred in connection with the European Transformation Plan. In 2009, operating income was $229.0 million, or 15.2 percent of sales, excluding Project Acceleration restructuring costs of $29.5 million.

Normalized earnings were $0.51 per diluted share, compared to prior year results of $0.47 per diluted share, driven primarily by improved gross margin and a lower tax rate resulting from the resolution of a tax examination. For the second quarter 2010, normalized diluted earnings per share exclude $0.06 per diluted share for restructuring and restructuring related costs, net of tax, $0.05 per diluted share of dilution related to the conversion feature of the convertible notes issued

3 Glenlake Parkway | Atlanta, GA 30328 | Phone +1 (770) 418-7000 | www.newellrubbermaid.com | NYSE: NWL

| > News Release |

in March 2009 and the impact of associated hedge transactions, and a benefit of $0.01 per diluted share related to the impact of hyperinflationary accounting for the company’s Venezuelan operations. For the second quarter 2009, normalized earnings per share exclude $0.08 per diluted share for Project Acceleration restructuring costs, net of tax, $0.01 per diluted share of dilution related to the conversion feature of the convertible notes issued in March 2009 and the impact of associated hedge transactions, and one-time costs of $0.01 per diluted share incurred for the early retirement of $325 million principal amount of medium-term notes. (A reconciliation of the “as reported” results to “normalized” results is included below.)

Net income, as reported, was $130.4 million, or $0.41 per diluted share, for the second quarter. This compares to $105.7 million, or $0.37 per diluted share, in the prior year.

The company generated operating cash flow of $154.0 million during the second quarter, compared to $99.2 million in the comparable period last year. The improvement was driven by increased earnings and working capital improvement. Capital expenditures were $37.8 million in the second quarter, compared to $38.3 million in the prior year.

A reconciliation of the second quarter 2010 and last year’s results is as follows:

| Q2 2010 | Q2 2009 | ||||||

Diluted earnings per share (as reported) | $ | 0.41 | $ | 0.37 | |||

Restructuring and restructuring related costs, net of tax | $ | 0.06 | $ | 0.08 | |||

Convertible notes dilution | $ | 0.05 | $ | 0.01 | |||

Other items, net of tax | ($ | 0.01 | ) | $ | 0.01 | ||

“Normalized” EPS | $ | 0.51 | $ | 0.47 | |||

Six Months Results

Net sales for the six months ended June 30, 2010 increased 3.5 percent to $2.80 billion, compared to $2.71 billion in the prior year. Core sales increased 4.1 percent for the six months. Foreign currency translation increased net sales by 1.0 percent, while the year over year impact of last year’s product line exits lowered net sales by 1.6 percent.

Gross margin was 37.8 percent, a 160 basis point improvement versus the prior year. Productivity gains and improved product mix more than offset the effect of input cost inflation.

3 Glenlake Parkway | Atlanta, GA 30328 | Phone +1 (770) 418-7000 | www.newellrubbermaid.com | NYSE: NWL

| > News Release |

Normalized earnings, which exclude the same items as those in the second quarter 2010, were $0.77 per diluted share, compared to $0.67 per diluted share in the prior year. (A reconciliation of the “as reported” results to “normalized” results is included below.)

Net income, as reported, was $188.8 million, or $0.61 per diluted share. This compares to $139.4 million, or $0.49 per diluted share, in the prior year.

The company generated operating cash flow of $183.4 million during the first six months of 2010, compared to $88.0 million in the prior year, driven by increased earnings and working capital improvement. Capital expenditures were $69.3 million, compared to $70.7 million in the prior year.

A reconciliation of the first six months 2010 and last year’s results is as follows:

| YTD Q2 2010 | YTD Q2 2009 | ||||

Diluted earnings per share (as reported) | $0.61 | $0.49 | |||

Restructuring and restructuring related costs, net of tax | $0.10 | $0.16 | |||

Convertible notes dilution | $0.07 | $0.01 | |||

Other items, net of tax | ($0.01 | ) | $0.01 | ||

“Normalized” EPS | $0.77 | $0.67 | |||

2010 Full Year Outlook

The company continues to expect 2010 net sales growth in the low to mid single digit range. However, the company is raising its expectations for core sales growth to mid single digits, as compared with low to mid single digits in its previous guidance. The impact of 2009 product exits is expected to be a negative one to two percent, and the impact from foreign currency is expected to be modestly negative.

The company still expects gross margin to improve 75 to 100 basis points with the combination of productivity, mix and pricing more than offsetting the impact of expected input cost inflation.

The company is raising its guidance for expected 2010 normalized earnings from its previously communicated range of $1.38 to $1.48 per diluted share to its new expectation of $1.40 to $1.50 per diluted share.

3 Glenlake Parkway | Atlanta, GA 30328 | Phone +1 (770) 418-7000 | www.newellrubbermaid.com | NYSE: NWL

| > News Release |

Operating cash flow is expected to exceed $500 million for the full year, including approximately $70 to $100 million in restructuring cash payments. The company expects capital expenditures of approximately $160 to $170 million.

A reconciliation of the 2010 earnings outlook is as follows:

| FY 2010 | ||||

Diluted earnings per share | $ | 1.16 to $1.26 | ||

Restructuring and restructuring related costs, net of tax | $ | 0.20 to $0.30 | ||

Other items, net of tax | ($0.01 | ) | ||

Convertible notes dilution | (A | ) | ||

“Normalized” EPS | $ | 1.40 to $1.50 | ||

| (A) | No provision is made in the 2010 outlook for potential dilution from the conversion feature of the convertible notes issued in March 2009 and associated hedge transactions, as the amount of full year 2010 dilution is dependent on the average stock price in each quarter of 2010. The conversion feature of the convertible notes and associated hedge transactions resulted in dilution of $0.07 per diluted share in the first six months of 2010 and $0.06 per diluted share for the full year 2009. |

Conference Call

The company’s second quarter 2010 earnings conference call is scheduled for today, July 30, 2010, at 9:00 am ET. To listen to the webcast, use the link provided under Events & Presentations in the Investor Relations section of Newell Rubbermaid’s Web site at www.newellrubbermaid.com. The webcast will be available for replay for two weeks. A brief supporting slide presentation will be available prior to the call under Quarterly Earnings in the Investor Relations section on the company’s Web site.

Non-GAAP Financial Measures

This release contains non-GAAP financial measures within the meaning of Regulation G promulgated by the Securities and Exchange Commission. Included in this release is a reconciliation of these non-GAAP financial measures to the most directly comparable financial measures calculated in accordance with GAAP.

About Newell Rubbermaid

Newell Rubbermaid Inc., an S&P 500 company, is a global marketer of consumer and commercial products with 2009 sales of approximately $5.6 billion and a strong portfolio of brands, including Rubbermaid®, Sharpie®, Graco®, Calphalon®, Irwin®, Lenox®, Levolor®, Paper Mate®, Dymo®, Waterman®, Parker®, Goody®, Technical ConceptsTM and Aprica®.

3 Glenlake Parkway | Atlanta, GA 30328 | Phone +1 (770) 418-7000 | www.newellrubbermaid.com | NYSE: NWL

| > News Release |

This press release and additional information about Newell Rubbermaid are available on the company’s Web site, www.newellrubbermaid.com.

Contacts:

Nancy O’Donnell Vice President, Investor Relations +1 (770) 418-7723 | David Doolittle Vice President, Corporate Communications +1 (770) 418-7519 |

Caution Concerning Forward-Looking Statements

Statements in this press release that are not historical in nature constitute forward-looking statements. These forward-looking statements relate to information or assumptions about the effects of sales, income/(loss), earnings per share, operating income or gross margin improvements or declines, Project Acceleration, the European Transformation Plan, capital and other expenditures, cash flow, dividends, restructuring costs, costs and cost savings, inflation or deflation, particularly with respect to commodities such as oil and resin, debt ratings, and management’s plans, projections and objectives for future operations and performance. These statements are accompanied by words such as “anticipate,” “expect,” “project,” “will,” “believe,” “estimate” and similar expressions. Actual results could differ materially from those expressed or implied in the forward-looking statements. Important factors that could cause actual results to differ materially from those suggested by the forward-looking statements include, but are not limited to, our dependence on the strength of retail, commercial and industrial sectors of the economy in light of the global economic slowdown; currency fluctuations; competition with other manufacturers and distributors of consumer products; major retailers’ strong bargaining power; changes in the prices of raw materials and sourced products and our ability to obtain raw materials and sourced products in a timely manner from suppliers; our ability to develop innovative new products and to develop, maintain and strengthen our end-user brands; our ability to expeditiously close facilities and move operations while managing foreign regulations and other impediments; our ability to implement successfully information technology solutions throughout our organization; our ability to improve productivity and streamline operations; our ability to refinance short-term debt on terms acceptable to us, particularly given the uncertainties in the global credit markets; changes to our credit ratings; significant increases in the funding obligations related to our pension plans due to declining asset values or otherwise; the imposition of tax liabilities greater than our provisions for such matters; the risks inherent in our foreign operations and those factors listed in the company’s latest quarterly report on Form 10-Q, and exhibit 99.1 thereto, filed with the Securities and Exchange Commission. Changes in such assumptions or factors could produce significantly different results. The information contained in this news release is as of the date indicated. The company assumes no obligation to update any forward-looking statements contained in this news release as a result of new information or future events or developments.

3 Glenlake Parkway | Atlanta, GA 30328 | Phone +1 (770) 418-7000 | www.newellrubbermaid.com | NYSE: NWL

Newell Rubbermaid Inc.

CONSOLIDATED STATEMENTS OF OPERATIONS (UNAUDITED)

(in millions, except per share data)

Reconciliation of “As Reported” Results to “Normalized” Results

| Three Months Ended June 30, | |||||||||||||||||||||||||||

| 2010 | 2009 | YOY % Change | |||||||||||||||||||||||||

| As Reported | Excluded Items (1) | Normalized | As Reported | Excluded Items (2) | Normalized | ||||||||||||||||||||||

Net sales | $ | 1,496.2 | $ | — | $ | 1,496.2 | $ | 1,504.3 | $ | — | $ | 1,504.3 | (0.5 | )% | |||||||||||||

Cost of products sold | 908.9 | — | 908.9 | 946.0 | — | 946.0 | |||||||||||||||||||||

GROSS MARGIN | 587.3 | — | 587.3 | 558.3 | — | 558.3 | 5.2 | % | |||||||||||||||||||

% of sales | 39.3 | % | 39.3 | % | 37.1 | % | 37.1 | % | |||||||||||||||||||

Selling, general & administrative expenses | 362.6 | (1.6 | ) | 361.0 | 329.3 | — | 329.3 | 9.6 | % | ||||||||||||||||||

% of sales | 24.2 | % | 24.1 | % | 21.9 | % | 21.9 | % | |||||||||||||||||||

Restructuring costs | 21.2 | (21.2 | ) | — | 29.5 | (29.5 | ) | — | |||||||||||||||||||

OPERATING INCOME | 203.5 | 22.8 | 226.3 | 199.5 | 29.5 | 229.0 | (1.2 | )% | |||||||||||||||||||

% of sales | 13.6 | % | 15.1 | % | 13.3 | % | 15.2 | % | |||||||||||||||||||

Nonoperating expenses: | |||||||||||||||||||||||||||

Interest expense, net | 33.2 | — | 33.2 | 40.3 | — | 40.3 | |||||||||||||||||||||

Other (income) expense, net | (5.9 | ) | 5.6 | (0.3 | ) | 1.2 | (4.7 | ) | (3.5 | ) | |||||||||||||||||

| 27.3 | 5.6 | 32.9 | 41.5 | (4.7 | ) | 36.8 | (10.6 | )% | |||||||||||||||||||

INCOME BEFORE INCOME TAXES | 176.2 | 17.2 | 193.4 | 158.0 | 34.2 | 192.2 | 0.6 | % | |||||||||||||||||||

% of sales | 11.8 | % | 12.9 | % | 10.5 | % | 12.8 | % | |||||||||||||||||||

Income taxes | 45.8 | 2.2 | 48.0 | 52.3 | 8.0 | 60.3 | (20.4 | )% | |||||||||||||||||||

Effective rate | 26.0 | % | 24.8 | % | 33.1 | % | 31.4 | % | |||||||||||||||||||

NET INCOME (3) | $ | 130.4 | $ | 15.0 | $ | 145.4 | $ | 105.7 | $ | 26.2 | $ | 131.9 | 10.2 | % | |||||||||||||

% of sales | 8.7 | % | 9.7 | % | 7.0 | % | 8.8 | % | |||||||||||||||||||

EARNINGS PER SHARE: | |||||||||||||||||||||||||||

Basic | $ | 0.46 | $ | 0.06 | $ | 0.52 | $ | 0.38 | $ | 0.09 | $ | 0.47 | |||||||||||||||

Diluted | $ | 0.41 | $ | 0.10 | $ | 0.51 | $ | 0.37 | $ | 0.10 | $ | 0.47 | |||||||||||||||

AVERAGE SHARES OUTSTANDING: |

| ||||||||||||||||||||||||||

Basic | 281.5 | 281.5 | 280.8 | 280.8 | |||||||||||||||||||||||

Diluted | 315.4 | 292.6 | 286.8 | 290.1 | |||||||||||||||||||||||

| (1) | Items excluded from “normalized” results for 2010 consist of $1.6 million of restructuring related costs incurred in connection with the European Transformation Plan, net of tax effects, $21.2 million of Project Acceleration restructuring costs, including asset impairment charges and employee termination and other costs, net of tax effects, the net of tax impact of a $5.6 million gain resulting from hyperinflationary accounting for the Company’s Venezuelan operations, as well as the dilutive impact of the conversion feature of the convertible notes issued in March 2009 and the associated hedge transactions. |

| (2) | Items excluded from “normalized” results for 2009 consist of $29.5 million of restructuring costs, including asset impairment charges and employee termination and other costs, and the associated tax effects, $4.7 million of debt extinguishment charges, net of tax effects, as well as the dilutive impact of the conversion feature of the convertible notes issued in March 2009 and the associated hedge transactions. |

| (3) | Net income attributable to noncontrolling interests was not material in either of the periods presented. |

Newell Rubbermaid Inc.

CONSOLIDATED STATEMENTS OF OPERATIONS (UNAUDITED)

(in millions, except per share data)

Reconciliation of “As Reported” Results to “Normalized” Results

| Six Months Ended June 30, | |||||||||||||||||||||||||||

| 2010 | 2009 | YOY % Change | |||||||||||||||||||||||||

| As Reported | Excluded Items (1) | Normalized | As Reported | Excluded Items (2) | Normalized | ||||||||||||||||||||||

Net sales | $ | 2,802.6 | $ | — | $ | 2,802.6 | $ | 2,708.2 | $ | — | $ | 2,708.2 | 3.5 | % | |||||||||||||

Cost of products sold | 1,743.6 | — | 1,743.6 | 1,727.1 | — | 1,727.1 | |||||||||||||||||||||

GROSS MARGIN | 1,059.0 | — | 1,059.0 | 981.1 | — | 981.1 | 7.9 | % | |||||||||||||||||||

% of sales | 37.8 | % | 37.8 | % | 36.2 | % | 36.2 | % | |||||||||||||||||||

Selling, general & administrative expenses | 688.2 | (1.6 | ) | 686.6 | 640.8 | — | 640.8 | 7.1 | % | ||||||||||||||||||

% of sales | 24.6 | % | 24.5 | % | 23.7 | % | 23.7 | % | |||||||||||||||||||

Restructuring costs | 37.2 | (37.2 | ) | — | 60.0 | (60.0 | ) | — | |||||||||||||||||||

OPERATING INCOME | 333.6 | 38.8 | 372.4 | 280.3 | 60.0 | 340.3 | 9.4 | % | |||||||||||||||||||

% of sales | 11.9 | % | 13.3 | % | 10.4 | % | 12.6 | % | |||||||||||||||||||

Nonoperating expenses: | |||||||||||||||||||||||||||

Interest expense, net | 65.2 | — | 65.2 | 70.9 | — | 70.9 | |||||||||||||||||||||

Other (income) expense, net | (6.2 | ) | 5.6 | (0.6 | ) | 1.9 | (4.7 | ) | (2.8 | ) | |||||||||||||||||

| 59.0 | 5.6 | 64.6 | 72.8 | (4.7 | ) | 68.1 | (5.1 | )% | |||||||||||||||||||

INCOME BEFORE INCOME TAXES | 274.6 | 33.2 | 307.8 | 207.5 | 64.7 | 272.2 | 13.1 | % | |||||||||||||||||||

% of sales | 9.8 | % | 11.0 | % | 7.7 | % | 10.1 | % | |||||||||||||||||||

Income taxes | 85.8 | 4.7 | 90.5 | 68.1 | 16.7 | 84.8 | 6.7 | % | |||||||||||||||||||

Effective rate | 31.2 | % | 29.4 | % | 32.8 | % | 31.2 | % | |||||||||||||||||||

NET INCOME (3) | $ | 188.8 | $ | 28.5 | $ | 217.3 | $ | 139.4 | $ | 48.0 | $ | 187.4 | 16.0 | % | |||||||||||||

% of sales | 6.7 | % | 7.8 | % | 5.1 | % | 6.9 | % | |||||||||||||||||||

EARNINGS PER SHARE: | |||||||||||||||||||||||||||

Basic | $ | 0.67 | $ | 0.10 | $ | 0.77 | $ | 0.50 | $ | 0.17 | $ | 0.67 | |||||||||||||||

Diluted | $ | 0.61 | $ | 0.16 | $ | 0.77 | $ | 0.49 | $ | 0.18 | $ | 0.67 | |||||||||||||||

AVERAGE SHARES OUTSTANDING: |

| ||||||||||||||||||||||||||

Basic | 281.3 | 281.3 | 280.7 | 280.7 | |||||||||||||||||||||||

Diluted | 311.6 | 283.6 | 283.7 | 281.2 | |||||||||||||||||||||||

| (1) | Items excluded from “normalized” results for 2010 consist of $1.6 million of restructuring related costs incurred in connection with the European Transformation Plan, net of tax effects, $37.2 million of Project Acceleration restructuring costs, including asset impairment charges and employee termination and other costs, net of tax effects, the net of tax impact of a $5.6 million gain resulting from hyperinflationary accounting for the Company’s Venezuelan operations, as well as the dilutive impact of the conversion feature of the convertible notes issued in March 2009 and the associated hedge transactions. |

| (2) | Items excluded from “normalized” results for 2009 consist of $60.0 million of restructuring costs, including asset impairment charges and employee termination and other costs, and the associated tax effects, $4.7 million of debt extinguishment charges, net of tax effects, as well as the dilutive impact of the conversion feature of the convertible notes issued in March 2009 and the associated hedge transactions. |

| (3) | Net income attributable to noncontrolling interests was not material in either of the periods presented. |

Newell Rubbermaid Inc.

CONSOLIDATED BALANCE SHEETS (UNAUDITED)

(in millions)

| June 30, 2010 | June 30, 2009 | |||||

Assets: | ||||||

Cash and cash equivalents | $ | 259.8 | $ | 418.1 | ||

Accounts receivable, net | 1,037.6 | 1,096.2 | ||||

Inventories, net | 802.4 | 848.4 | ||||

Deferred income taxes | 195.7 | 129.6 | ||||

Prepaid expenses and other | 105.3 | 110.5 | ||||

Total Current Assets | 2,400.8 | 2,602.8 | ||||

Property, plant and equipment, net | 536.3 | 603.1 | ||||

Goodwill | 2,701.7 | 2,722.0 | ||||

Other intangible assets, net | 636.6 | 645.6 | ||||

Other assets | 289.1 | 342.7 | ||||

Total Assets | $ | 6,564.5 | $ | 6,916.2 | ||

Liabilities and Stockholders’ Equity: | ||||||

Accounts payable | $ | 597.2 | $ | 460.8 | ||

Accrued compensation | 122.0 | 111.8 | ||||

Other accrued liabilities | 651.0 | 659.2 | ||||

Short-term debt | 1.0 | 7.1 | ||||

Current portion of long-term debt | 393.0 | 627.1 | ||||

Total Current Liabilities | 1,764.2 | 1,866.0 | ||||

Long-term debt | 2,049.3 | 2,393.5 | ||||

Deferred income taxes | 25.7 | — | ||||

Other non-current liabilities | 826.4 | 873.9 | ||||

Stockholders’ Equity—Parent | 1,895.4 | 1,779.2 | ||||

Stockholders’ Equity—Noncontrolling Interests | 3.5 | 3.6 | ||||

Total Stockholders’ Equity | 1,898.9 | 1,782.8 | ||||

Total Liabilities and Stockholders’ Equity | $ | 6,564.5 | $ | 6,916.2 | ||

Newell Rubbermaid Inc.

CONSOLIDATED STATEMENTS OF CASH FLOW (UNAUDITED)

(in millions)

| Six Months Ended June 30, | ||||||||

| 2010 | 2009 | |||||||

Operating Activities: | ||||||||

Net income | $ | 188.8 | $ | 139.4 | ||||

Adjustments to reconcile net income to net cash provided by operating activities: | ||||||||

Depreciation and amortization | 86.9 | 83.9 | ||||||

Deferred income taxes | 16.7 | 14.8 | ||||||

Non-cash restructuring costs | 1.9 | 13.3 | ||||||

Stock-based compensation expense | 18.8 | 16.6 | ||||||

Other | 12.7 | 12.9 | ||||||

Changes in operating assets and liabilities, excluding the effects of acquisitions: | ||||||||

Accounts receivable | (165.1 | ) | (115.3 | ) | ||||

Inventories | (131.8 | ) | 78.3 | |||||

Accounts payable | 172.4 | (77.8 | ) | |||||

Accrued liabilities and other | (17.9 | ) | (78.1 | ) | ||||

Net cash provided by operating activities | $ | 183.4 | $ | 88.0 | ||||

Investing Activities: | ||||||||

Acquisitions and acquisition related activity | $ | (1.5 | ) | $ | (12.1 | ) | ||

Capital expenditures | (69.3 | ) | (70.7 | ) | ||||

Proceeds from sales of non-current assets | 8.7 | 5.7 | ||||||

Other | (2.0 | ) | — | |||||

Net cash used in investing activities | $ | (64.1 | ) | $ | (77.1 | ) | ||

Financing Activities: | ||||||||

Proceeds from issuance of debt, net of debt issuance costs | $ | 2.4 | $ | 759.8 | ||||

Proceeds from issuance of warrants | — | 32.7 | ||||||

Purchase of call options | — | (69.0 | ) | |||||

Payments on notes payable and debt | (108.4 | ) | (517.2 | ) | ||||

Cash dividends | (28.0 | ) | (43.4 | ) | ||||

Purchase of noncontrolling interests in consolidated subsidiaries | — | (29.0 | ) | |||||

Other, net | (3.1 | ) | (4.1 | ) | ||||

Net cash (used in) provided by financing activities | $ | (137.1 | ) | $ | 129.8 | |||

Currency rate effect on cash and cash equivalents | $ | (0.7 | ) | $ | 2.0 | |||

(Decrease) increase in cash and cash equivalents | $ | (18.5 | ) | $ | 142.7 | |||

Cash and cash equivalents at beginning of period | 278.3 | 275.4 | ||||||

Cash and cash equivalents at end of period | $ | 259.8 | $ | 418.1 | ||||

Newell Rubbermaid Inc.

Financial Worksheet

(In Millions)

| 2010 | 2009 | Year-over-year changes | ||||||||||||||||||||||||||||||||||||||||||||||

| Reconciliation (1) | Reconciliation (1) | Net Sales | Normalized OI | |||||||||||||||||||||||||||||||||||||||||||||

| Net Sales | Reported OI | Excluded Items | Normalized OI | Operating Margin | Net Sales | Reported OI | Excluded Items | Normalized OI | Operating Margin | $ | % | $ | % | |||||||||||||||||||||||||||||||||||

Q1: | ||||||||||||||||||||||||||||||||||||||||||||||||

Home & Family | $ | 556.9 | $ | 68.8 | $ | — | $ | 68.8 | 12.4 | % | $ | 557.7 | $ | 60.3 | $ | — | $ | 60.3 | 10.8 | % | $ | (0.8 | ) | (0.1 | )% | $ | 8.5 | 14.1 | % | |||||||||||||||||||

Office Products | 351.6 | 47.3 | — | 47.3 | 13.5 | % | 318.2 | 31.1 | — | 31.1 | 9.8 | % | 33.4 | 10.5 | % | 16.2 | 52.1 | % | ||||||||||||||||||||||||||||||

Tools, Hardware & Commercial Products | 397.9 | 51.6 | — | 51.6 | 13.0 | % | 328.0 | 38.0 | — | 38.0 | 11.6 | % | 69.9 | 21.3 | % | 13.6 | 35.8 | % | ||||||||||||||||||||||||||||||

Restructuring Costs | — | (16.0 | ) | 16.0 | — | — | (30.5 | ) | 30.5 | — | ||||||||||||||||||||||||||||||||||||||

Corporate | — | (21.6 | ) | — | (21.6 | ) | — | (18.1 | ) | — | (18.1 | ) | (3.5 | ) | (19.3 | )% | ||||||||||||||||||||||||||||||||

Total | $ | 1,306.4 | $ | 130.1 | $ | 16.0 | $ | 146.1 | 11.2 | % | $ | 1,203.9 | $ | 80.8 | $ | 30.5 | $ | 111.3 | 9.2 | % | $ | 102.5 | 8.5 | % | $ | 34.8 | 31.3 | % | ||||||||||||||||||||

| 2010 | 2009 | Year-over-year changes | ||||||||||||||||||||||||||||||||||||||||||||||

| Reconciliation (2) | Reconciliation (1) | Net Sales | Normalized OI | |||||||||||||||||||||||||||||||||||||||||||||

| Net Sales | Reported OI | Excluded Items | Normalized OI | Operating Margin | Net Sales | Reported OI | Excluded Items | Normalized OI | Operating Margin | $ | % | $ | % | |||||||||||||||||||||||||||||||||||

Q2: | ||||||||||||||||||||||||||||||||||||||||||||||||

Home & Family | $ | 592.0 | $ | 75.6 | $ | — | $ | 75.6 | 12.8 | % | $ | 617.2 | $ | 80.4 | $ | — | $ | 80.4 | 13.0 | % | $ | (25.2 | ) | (4.1 | )% | $ | (4.8 | ) | (6.0 | )% | ||||||||||||||||||

Office Products | 483.5 | 99.4 | — | 99.4 | 20.6 | % | 496.9 | 99.2 | — | 99.2 | 20.0 | % | (13.4 | ) | (2.7 | )% | 0.2 | 0.2 | % | |||||||||||||||||||||||||||||

Tools, Hardware & Commercial Products | 420.7 | 70.1 | — | 70.1 | 16.7 | % | 390.2 | 67.6 | — | 67.6 | 17.3 | % | 30.5 | 7.8 | % | 2.5 | 3.7 | % | ||||||||||||||||||||||||||||||

Restructuring Costs | — | (21.2 | ) | 21.2 | — | — | (29.5 | ) | 29.5 | — | ||||||||||||||||||||||||||||||||||||||

Corporate | — | (20.4 | ) | 1.6 | (18.8 | ) | — | (18.2 | ) | — | (18.2 | ) | (0.6 | ) | (3.3 | )% | ||||||||||||||||||||||||||||||||

Total | $ | 1,496.2 | $ | 203.5 | $ | 22.8 | $ | 226.3 | 15.1 | % | $ | 1,504.3 | $ | 199.5 | $ | 29.5 | $ | 229.0 | 15.2 | % | $ | (8.1 | ) | (0.5 | )% | $ | (2.7 | ) | (1.2 | )% | ||||||||||||||||||

| 2010 | 2009 | Year-over-year changes | ||||||||||||||||||||||||||||||||||||||||||||||

| Reconciliation (2) | Reconciliation (1) | Net Sales | Normalized OI | |||||||||||||||||||||||||||||||||||||||||||||

| Net Sales | Reported OI | Excluded Items | Normalized OI | Operating Margin | Net Sales | Reported OI | Excluded Items | Normalized OI | Operating Margin | $ | % | $ | % | |||||||||||||||||||||||||||||||||||

YTD: | ||||||||||||||||||||||||||||||||||||||||||||||||

Home & Family | $ | 1,148.9 | $ | 144.4 | $ | — | $ | 144.4 | 12.6 | % | $ | 1,174.9 | $ | 140.7 | $ | — | $ | 140.7 | 12.0 | % | $ | (26.0 | ) | (2.2 | )% | $ | 3.7 | 2.6 | % | |||||||||||||||||||

Office Products | 835.1 | 146.7 | — | 146.7 | 17.6 | % | 815.1 | 130.3 | — | 130.3 | 16.0 | % | 20.0 | 2.5 | % | 16.4 | 12.6 | % | ||||||||||||||||||||||||||||||

Tools, Hardware & Commercial Products | 818.6 | 121.7 | — | 121.7 | 14.9 | % | 718.2 | 105.6 | — | 105.6 | 14.7 | % | 100.4 | 14.0 | % | 16.1 | 15.2 | % | ||||||||||||||||||||||||||||||

Restructuring Costs | — | (37.2 | ) | 37.2 | — | (60.0 | ) | 60.0 | — | |||||||||||||||||||||||||||||||||||||||

Corporate | — | (42.0 | ) | 1.6 | (40.4 | ) | (36.3 | ) | — | (36.3 | ) | (4.1 | ) | (11.3 | )% | |||||||||||||||||||||||||||||||||

Total | $ | 2,802.6 | $ | 333.6 | $ | 38.8 | $ | 372.4 | 13.3 | % | $ | 2,708.2 | $ | 280.3 | $ | 60.0 | $ | 340.3 | 12.6 | % | $ | 94.4 | 3.5 | % | $ | 32.1 | 9.4 | % | ||||||||||||||||||||

| (1) | Excluded items are related to Project Acceleration costs. |

| (2) | Excluded items are related to Project Acceleration costs and restructuring related costs incurred in connection with the European Transformation Plan. |

Newell Rubbermaid Inc.

Calculation of Free Cash Flow (1)

Three Months Ended June 30, | ||||||||

| 2010 | 2009 | |||||||

Free Cash Flow (in millions): | ||||||||

Net cash provided by operating activities | $ | 154.0 | $ | 99.2 | ||||

Capital expenditures | (37.8 | ) | (38.3 | ) | ||||

Free Cash Flow | $ | 116.2 | $ | 60.9 | ||||

Six Months Ended June 30, | ||||||||

| 2010 | 2009 | |||||||

Free Cash Flow (in millions): | ||||||||

Net cash provided by operating activities | $ | 183.4 | $ | 88.0 | ||||

Capital expenditures | (69.3 | ) | (70.7 | ) | ||||

Free Cash Flow | $ | 114.1 | $ | 17.3 | ||||

| (1) | Free Cash Flow is defined as cash flow provided by operating activities less capital expenditures. |

Newell Rubbermaid Inc.

Three Months Ended June 30, 2010

In Millions

Currency Analysis

| 2010 | 2009 | Year-Over-Year (Decrease) Increase | ||||||||||||||||||||

| Sales as Reported | Currency Impact | Adjusted Sales | Sales as Reported | Excluding Currency | Including Currency | Currency Impact | ||||||||||||||||

| By Segment | ||||||||||||||||||||||

Home & Family | $ | 592.0 | $ | (5.1 | ) | $ | 586.9 | $ | 617.2 | (4.9 | )% | (4.1 | )% | 0.8 | % | |||||||

Office Products | 483.5 | 13.8 | 497.3 | 496.9 | 0.1 | % | (2.7 | )% | (2.8 | )% | ||||||||||||

Tools, Hardware & Commercial Products | 420.7 | (6.5 | ) | 414.2 | 390.2 | 6.2 | % | 7.8 | % | 1.7 | % | |||||||||||

Total Company | $ | 1,496.2 | $ | 2.2 | $ | 1,498.4 | $ | 1,504.3 | (0.4 | )% | (0.5 | )% | (0.1 | )% | ||||||||

| By Geography | ||||||||||||||||||||||

United States | $ | 1,042.0 | $ | — | $ | 1,042.0 | $ | 1,071.7 | (2.8 | )% | (2.8 | )% | 0.0 | % | ||||||||

Canada | 88.0 | (10.6 | ) | 77.4 | 85.5 | (9.5 | )% | 2.9 | % | 12.4 | % | |||||||||||

Total North America | 1,130.0 | (10.6 | ) | 1,119.4 | 1,157.2 | (3.3 | )% | (2.4 | )% | 0.9 | % | |||||||||||

Europe, Middle East and Africa | 215.2 | 10.8 | 226.0 | 208.8 | 8.2 | % | 3.1 | % | (5.2 | )% | ||||||||||||

Latin America | 67.2 | 8.2 | 75.4 | 61.7 | 22.2 | % | 8.9 | % | (13.3 | )% | ||||||||||||

Asia Pacific | 83.8 | (6.2 | ) | 77.6 | 76.6 | 1.3 | % | 9.4 | % | 8.1 | % | |||||||||||

Total International | 366.2 | 12.8 | 379.0 | 347.1 | 9.2 | % | 5.5 | % | (3.7 | )% | ||||||||||||

Total Company | $ | 1,496.2 | $ | 2.2 | $ | 1,498.4 | $ | 1,504.3 | (0.4 | )% | (0.5 | )% | (0.1 | )% | ||||||||

Newell Rubbermaid Inc.

Six Months Ended June 30, 2010

In Millions

Currency Analysis

| 2010 | 2009 | Year-Over-Year (Decrease) Increase | ||||||||||||||||||||

| Sales as Reported | Currency Impact | Adjusted Sales | Sales as Reported | Excluding Currency | Including Currency | Currency Impact | ||||||||||||||||

| By Segment | ||||||||||||||||||||||

Home & Family | $ | 1,148.9 | $ | (15.9 | ) | $ | 1,133.0 | $ | 1,174.9 | (3.6 | )% | (2.2 | )% | 1.4 | % | |||||||

Office Products | 835.1 | 10.2 | 845.3 | 815.1 | 3.7 | % | 2.5 | % | (1.3 | )% | ||||||||||||

Tools, Hardware & Commercial Products | 818.6 | (21.7 | ) | 796.9 | 718.2 | 11.0 | % | 14.0 | % | 3.0 | % | |||||||||||

Total Company | $ | 2,802.6 | $ | (27.4 | ) | $ | 2,775.2 | $ | 2,708.2 | 2.5 | % | 3.5 | % | 1.0 | % | |||||||

| By Geography | ||||||||||||||||||||||

United States | $ | 1,946.6 | $ | — | $ | 1,946.6 | $ | 1,933.0 | 0.7 | % | 0.7 | % | 0.0 | % | ||||||||

Canada | 166.0 | (22.6 | ) | 143.4 | 147.0 | (2.4 | )% | 12.9 | % | 15.4 | % | |||||||||||

Total North America | 2,112.6 | (22.6 | ) | 2,090.0 | 2,080.0 | 0.5 | % | 1.6 | % | 1.1 | % | |||||||||||

Europe, Middle East, and Africa | 404.0 | (2.3 | ) | 401.7 | 368.4 | 9.0 | % | 9.7 | %�� | 0.6 | % | |||||||||||

Latin America | 122.9 | 12.2 | 135.1 | 115.4 | 17.1 | % | 6.5 | % | (10.6 | )% | ||||||||||||

Asia Pacific | 163.1 | (14.7 | ) | 148.4 | 144.4 | 2.8 | % | 13.0 | % | 10.2 | % | |||||||||||

Total International | 690.0 | (4.8 | ) | 685.2 | 628.2 | 9.1 | % | 9.8 | % | 0.8 | % | |||||||||||

Total Company | $ | 2,802.6 | $ | (27.4 | ) | $ | 2,775.2 | $ | 2,708.2 | 2.5 | % | 3.5 | % | 1.0 | % | |||||||

Q2 2010 Earnings Call Presentation July 30, 2010 |

2 Forward-Looking Statement 2 Statements in this presentation that are not historical in nature constitute forward-looking statements. These forward-looking statements relate to information or assumptions about the effects of sales, income/(loss), earnings per share, operating income or gross margin improvements or declines, Project Acceleration, the European Transformation Plan, capital and other expenditures, cash flow, dividends, restructuring costs, costs and cost savings, inflation or deflation, particularly with respect to commodities such as oil and resin, debt ratings, and management's plans, projections and objectives for future operations and performance. These statements are accompanied by words such as "anticipate," "expect," "project," "will," "believe," "estimate" and similar expressions. Actual results could differ materially from those expressed or implied in the forward-looking statements. Important factors that could cause actual results to differ materially from those suggested by the forward-looking statements include, but are not limited to, our dependence on the strength of retail, commercial and industrial sectors of the economy in light of the global economic slowdown; currency fluctuations; competition with other manufacturers and distributors of consumer products; major retailers' strong bargaining power; changes in the prices of raw materials and sourced products and our ability to obtain raw materials and sourced products in a timely manner from suppliers; our ability to develop innovative new products and to develop, maintain and strengthen our end-user brands; our ability to expeditiously close facilities and move operations while managing foreign regulations and other impediments; our ability to implement successfully information technology solutions throughout our organization; our ability to improve productivity and streamline operations; our ability to refinance short-term debt on terms acceptable to us, particularly given uncertainties in the global credit markets; changes to our credit ratings; significant increases in the funding obligations related to our pension plans due to declining asset values or otherwise; the imposition of tax liabilities greater than our provisions for such matters; the risks inherent in our foreign operations and those factors listed in the company’s latest quarterly report on Form 10-Q, and exhibit 99.1 thereto, filed with the Securities and Exchange Commission. Changes in such assumptions or factors could produce significantly different results. The information contained in this presentation is as of the date indicated. The company assumes no obligation to update any forward-looking statements contained in this presentation as a result of new information or future events or developments. |

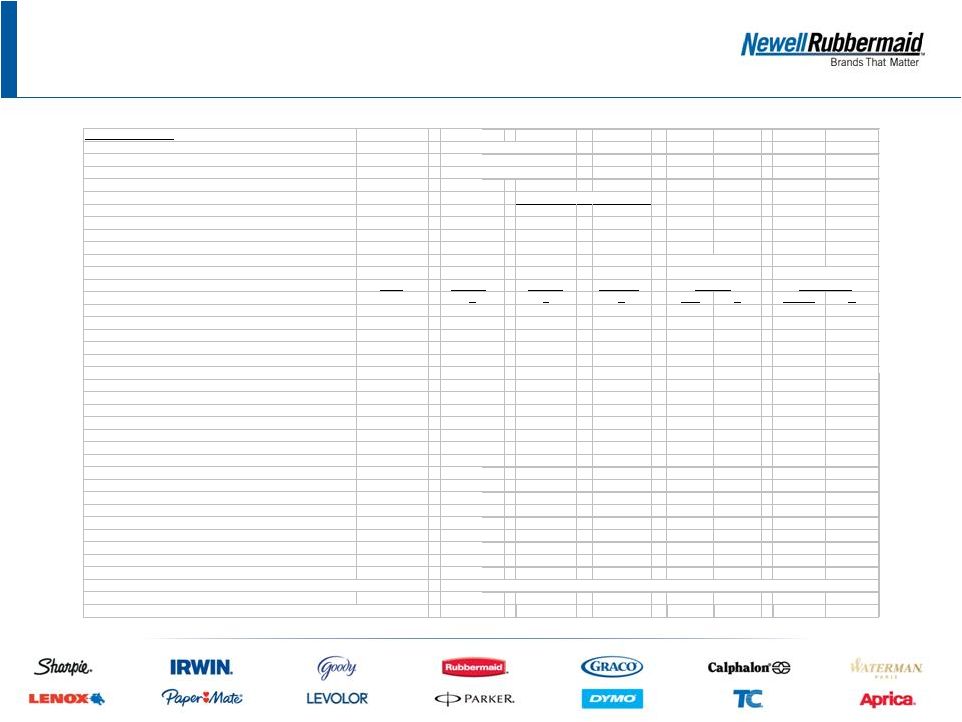

3 » Normalized EPS of $0.51; improvement versus prior year quarter normalized EPS of $0.47 primarily driven by expanded gross margins, offset by a return to more normal levels of brand building and other strategic spend, and a lower tax rate due to the favorable resolution of a tax examination » Net Sales of $1.5 billion, a slight decline versus the prior year, included a 1.5% increase in core sales offset by the impact of last year’s product line exits of (1.9%); foreign currency had a nominal impact for the quarter » Core Sales growth in the quarter of 3.8%, after adjusting for the first quarter pre-buying by certain customers in advance of SAP go-live » Gross Margin expansion of 220 basis points to 39.3% Year-over-year expansion fueled by productivity gains and improved product mix, which more than offset higher input costs » Operating Cash Flow of $154.0 million, compared to $99.2 million last year, driven by increased earnings and working capital improvement Q2 2010 Summary |

4 » Normalized EPS of $0.77; strong improvement versus prior year’s normalized EPS of $0.67 driven primarily by increases in core sales and expanded gross margins » Net Sales of $2.8 billion, a 3.5% increase over the prior year, consisted of a 4.1% increase in core sales and a 1.0% increase resulting from foreign currency, offset by the impact of last year’s product line exits of (1.6%) » Gross Margin expansion of 160 basis points to 37.8% Year-over-year expansion fueled by productivity gains and improved product mix, which more than offset the effect of input cost inflation » Operating Cash Flow of $183.4 million, compared to $88.0 million last year, driven by increased earnings and working capital improvement; capital expenditures were $69.3 million, compared to $70.7 million in the prior year YTD Q2 2010 Summary |

5 Q2 Sales: Percent Change by Segment H&F OP TH&C Total Core Sales (2.6) 3.1 6.1 1.5 Product Line Exits (2.3) (3.0) 0.0 (1.9) Currency Translation 0.8 (2.8) 1.7 (0.1) Total (4.1) (2.7) 7.8 (0.5) 5 |

6 YTD Q2 Sales: Percent Change by Segment H&F OP TH&C Total Core Sales (2.2) 7.0 11.0 4.1 Product Line Exits (1.4) (3.2) 0.0 (1.6) Currency Translation 1.4 (1.3) 3.0 1.0 Total (2.2) 2.5 14.0 3.5 6 |

7 Full Year 2010 Outlook 7 Outlook [ 1 ] Net Sales Growth Low to mid single digit growth Core Sales Mid single digit growth Product Line Exits -1% to -2% Currency Translation Modestly negative Gross Margin Expansion 75 to 100 basis points "Normalized" EPS [ 2 ] $1.40 to $1.50 Cash Flow from Operations > $500 million Capital Expenditures $160 to $170 million [ 1 ] Reflects outlook communicated in Q2 2010 Earnings Release and Earnings Call [ 2 ] See reconciliation included in the Appendix |

Appendix |

9 Reconciliation: Q2 2010 and Q2 2009 “Normalized” EPS Q2 2010 Q2 2009 Diluted earnings per share (as reported): $0.41 $0.37 Restructuring and restructuring related costs, net of tax [ 1 ] $0.06 $0.08 Convertible notes dilution $0.05 $0.01 Other items, net of tax [ 2 ] ($0.01) $0.01 "Normalized" EPS: $0.51 $0.47 [ 1 ] Restructuring and restructuring related costs include impairment charges, employee termination benefits and other costs associated with Project Acceleration as well as costs associated with the European Transformation Plan, and the related tax effects. [ 2 ] Other items in 2010 include a benefit related to the impact of hyperinflationary accounting for the Company's Venezuelan operations. Other items in 2009 include one-time costs for the early retirement of $325 million principal amount of medium-term notes. 9 |

10 Reconciliation: YTD Q2 2010 and YTD Q2 2009 “Normalized” EPS YTD Q2 2010 YTD Q2 2009 Diluted earnings per share (as reported): $0.61 $0.49 Restructuring and restructuring related costs, net of tax [ 1 ] $0.10 $0.16 Convertible notes dilution $0.07 $0.01 Other items, net of tax [ 2 ] ($0.01) $0.01 Normalized EPS: $0.77 $0.67 [ 1 ] Restructuring and restructuring related costs include impairment charges, employee termination benefits and other costs associated with Project Acceleration as well as costs associated with the European Transformation Plan, and the related tax effects. [ 2 ] Other items in 2010 include a benefit related to the impact of hyperinflationary accounting for the Company's Venezuelan operations. Other items in 2009 include one-time costs for the early retirement of $325 million principal amount of medium-term notes. 10 |

11 NWL Convertible Note Dilution and Warrant Model Including Reconciliation 11 Transaction Details Aggregate Principal Amount ($Millions) $345 Shares Underlying 40.088 Maturity March 15, 2014 Warrant Strike Price $11.59 Conversion Price $8.61 Beginning Shares Outstanding 280 Note: "In the money" warrants under the conversion feature of the convertible notes may be settled in cash, stock or a Shares Shares combination at NWL's election. The dilution impact Received Delivered on EPS in NWL's financial statements and in the from from table below reflects the settlement of the conversion Average Shares Purchased Sold feature as if shares were used. Share Noteholders Call Warrants Price Receive ¹ @ $8.61 @ $11.59 ² A B C A+C % A+B+C % Below Conversion Price Below $8.61 0 0 0 0 0 Between Conversion Price and Warrant Strike Price $8.61 0.00 0.00 0.00 0.0% 0.00 0.0% At maturity, under purchased call NWL receives from $9.00 1.75 (1.75) 1.75 0.6% 0.00 0.0% counterparties shares (or equivalent cash value) equal $10.00 5.59 (5.59) 5.59 2.0% 0.00 0.0% to amounts delivered to noteholders. $11.00 8.72 (8.72) 8.72 3.1% 0.00 0.0% $11.59 10.32 (10.32) 0.00 10.32 3.7% 0.00 0.0% Above Warrant Strike Price $12.00 11.34 (11.34) 1.37 12.71 4.5% 1.37 0.5% After maturity, NWL is responsible for delivering shares $13.00 13.55 (13.55) 4.35 17.90 6.4% 4.35 1.6% (or equivalent cash value) to counterparties for the value above $14.00 15.45 (15.45) 6.90 22.35 8.0% 6.90 2.5% the warrant strike price. $15.00 17.09 (17.09) 9.11 26.20 9.4% 9.11 3.3% $17.00 19.79 (19.79) 12.76 32.55 11.6% 12.76 4.6% $20.00 22.84 (22.84) 16.86 39.70 14.2% 16.86 6.0% $21.00 23.66 (23.66) 17.96 41.62 14.9% 17.96 6.4% $22.00 24.41 (24.41) 18.97 43.38 15.5% 18.97 6.8% $23.00 25.09 (25.09) 19.89 44.98 16.1% 19.89 7.1% $24.00 25.71 (25.71) 20.73 46.44 16.6% 20.73 7.4% All shares stated in Millions $25.00 26.29 (26.29) 21.50 47.79 17.1% 21.50 7.7% ¹ [(Share Price - Conversion Price) * Shares Underlying] / Share Price * Represents dilution incurred upon settlement of convertible notes, purchased call and warrant. ² [(Share Price - Warrant Strike Price) * Shares Underlying] / Share Price NWL Hedge GAAP Accounting "Economic" Dilution* Maturity (Non-GAAP) Dilution Before |

12 Reconciliation: Full Year 2010 Outlook for “Normalized” EPS FY 2010 Diluted earnings per share: $1.16 to $1.26 Restructuring and restructuring related costs, net of tax [ 1 ] $0.20 to $0.30 Other items, net of tax [ 2 ] ($0.01) Convertible notes dilution [ 3 ] TBD "Normalized" EPS: $1.40 to $1.50 [ 1 ] Restructuring and restructuring related costs include impairment charges, employee termination benefits and other costs associated with Project Acceleration as well as costs associated with the European Transformation Plan, and the related tax effects. [ 2 ] Other items include a benefit related to the impact of hyperinflationary accounting for the Company's Venezuelan operations. [ 3 ] No provision is made in the 2010 outlook for potential dilution from the conversion feature of the convertible notes issued in March 2009 and associated hedge transactions, as the amount of full year 2010 dilution is dependent on the average stock price in each quarter of 2010. The conversion feature of the convertible notes and associated hedge transactions resulted in dilution of $0.07 per diluted share in the first six months of 2010 and $0.06 per diluted share for the full year 2009. 12 |

13 Reconciliation: Q2 2010 and Q2 2009 Operating Income to Operating Income Excluding Charges Q2 2010 Q2 2009 Net Sales $1,496.2 $1,504.3 Operating Income (as reported) $203.5 $199.5 Restructuring and Restructuring Related Costs [ 1 ] $22.8 $29.5 Operating Income (excluding charges) $226.3 $229.0 Operating Income (excluding charges), as a Percent of Net Sales 15.1% 15.2% [ 1 ] Restructuring and restructuring related costs include impairment charges, employee termination benefits and other costs associated with Project Acceleration as well as costs associated with the European Transformation Plan, and the related tax effects. $ millions 13 |

14 Reconciliation: YTD Q2 2010 and YTD Q2 2009 Operating Income to Operating Income Excluding Charges YTD Q2 2010 YTD Q2 2009 Net Sales $2,802.6 $2,708.2 Operating Income (as reported) $333.6 $280.3 Restructuring and Restructuring Related Costs [ 1 ] $38.8 $60.0 Operating Income (excluding charges) $372.4 $340.3 Operating Income (excluding charges), as a Percent of Net Sales 13.3% 12.6% [ 1 ] Restructuring and restructuring related costs include impairment charges, employee termination benefits and other costs associated with Project Acceleration as well as costs associated with the European Transformation Plan, and the related tax effects. 14 |

15 Reconciliation: Q2 2010 and Q2 2009 Free Cash Flow Q2 2010 Q2 2009 Operating Cash Flow $154.0 $99.2 Capital Expenditures (37.8) (38.3) Free Cash Flow $116.2 $60.9 $ millions 15 |

16 Reconciliation: YTD Q2 2010 and YTD Q2 2009 Free Cash Flow YTD Q2 2010 YTD Q2 2009 Cash Flow From Operations $183.4 $88.0 Capital Expenditures (69.3) (70.7) Free Cash Flow $114.1 $17.3 $ millions 16 |