UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2011

OR

¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission file number 0-16633

THE JONES FINANCIAL COMPANIES, L.L.L.P.

(Exact name of registrant as specified in its charter)

| | |

| MISSOURI | | 43-1450818 |

(State or other jurisdiction of incorporation or organization) | | (IRS Employer Identification No.) |

| |

12555 Manchester Road Des Peres, Missouri | | 63131 |

| (Address of principal executive offices) | | (Zip Code) |

(314) 515-2000

Registrant’s telephone number, including area code

Securities registered pursuant to Section 12(b) of the Act:

| | |

| Title of each class | | Name of each exchange on which registered |

| NONE | | NONE |

Securities registered pursuant to Section 12(g) of the Act:

Limited Partnership Interests

(Title of Class)

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. YES ¨ NO x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. YES ¨ NO x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. YES x NO ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). YES x NO ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulations S-K (§229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. x

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

| | | | | | |

Large accelerated filer | | ¨ | | Accelerated filer | | ¨ |

| | | |

Non-accelerated filer | | x (Do not check if a smaller reporting company) | | Smaller reporting company | | ¨ |

Indicated by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ¨ No x

As of February 24, 2012, 660,508 units of limited partnership interests, each representing $1,000 of limited partner capital, are outstanding (“Units”). There is no public or private market for such Units.

DOCUMENTS INCORPORATED BY REFERENCE

None

THE JONES FINANCIAL COMPANIES, L.L.L.P.

TABLE OF CONTENTS

| | | | | | |

| | | | | Page | |

PART I | | | | | | |

Item 1 | | Business | | | 4 | |

Item 1A | | Risk Factors | | | 16 | |

Item 1B | | Unresolved Staff Comments | | | 30 | |

Item 2 | | Properties | | | 30 | |

Item 3 | | Legal Proceedings | | | 31 | |

Item 4 | | Mine Safety Disclosures | | | 33 | |

| | |

PART II | | | | | | |

| | |

Item 5 | | Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities | | | 34 | |

Item 6 | | Selected Financial Data | | | 34 | |

Item 7 | | Management’s Discussion and Analysis of Financial Condition and Results of Operations | | | 36 | |

Item 7A | | Quantitative and Qualitative Disclosures about Market Risk | | | 60 | |

Item 8 | | Financial Statements and Supplementary Data | | | 61 | |

Item 9 | | Changes in and Disagreements with Accountants on Accounting and Financial Disclosure | | | 94 | |

Item 9A | | Controls and Procedures | | | 94 | |

Item 9B | | Other Information | | | 94 | |

| | |

PART III | | | | | | |

| | |

Item 10 | | Directors, Executive Officers and Corporate Governance | | | 95 | |

Item 11 | | Executive Compensation | | | 102 | |

Item 12 | | Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters | | | 105 | |

Item 13 | | Certain Relationships and Related Transactions, and Director Independence | | | 105 | |

Item 14 | | Principal Accounting Fees and Services | | | 106 | |

| | |

PART IV | | | | | | |

| | |

Item 15 | | Exhibits and Financial Statement Schedules | | | 107 | |

| | Signatures | | | 108 | |

3

PART I

The Jones Financial Companies, L.L.L.P. (“JFC”) is a registered limited liability limited partnership organized under the Uniform Limited Partnership Law of the State of Missouri Revised Statutes. Unless expressly stated, or the context otherwise requires, the terms “Registrant” and “Partnership” refer to JFC and all of its consolidated subsidiaries. The Partnership’s principal operating subsidiary, Edward D. Jones & Co., L.P. (“Edward Jones”), was organized on February 20, 1941 and reorganized as a limited partnership on May 23, 1969. JFC was organized on June 5, 1987 and, along with Edward Jones, was reorganized on August 28, 1987.

As of December 31, 2011, the Partnership operates in two geographic operating segments, the United States of America (“U.S.”) and Canada. Edward Jones is comprised of a U.S. registered broker-dealer and (through a subsidiary) a Canadian registered broker-dealer and primarily serves individual investors. As the ultimate parent company of Edward Jones, JFC is a holding company. Edward Jones primarily derives its revenue from the retail brokerage business through the sale of listed and unlisted securities and insurance products, investment banking, principal transactions, distribution of mutual fund shares, and through fees related to assets held by, and account services provided to, its clients. Edward Jones primarily conducts business with its clients, various brokers, dealers, clearing organizations, depositories and banks in the U.S. and in Canada. For financial information related to these two operating segments for the years ended December 31, 2011, 2010 and 2009, see Item 7 – Management’s Discussion and Analysis of Financial Condition and Results of Operations and Note 17 to the Consolidated Financial Statements.

4

PART I

Item | 1. Business, continued |

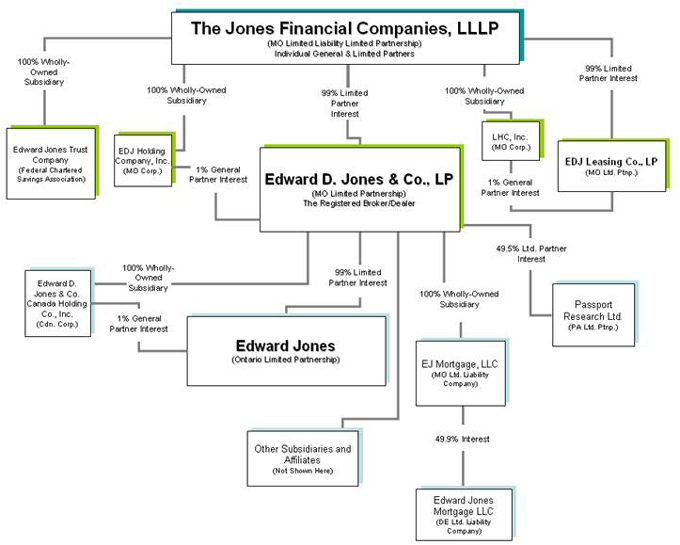

ORGANIZATIONAL STRUCTURE

At December 31, 2011, the Partnership was organized as follows:

For additional information about the Partnership’s other subsidiaries and affiliates, see Exhibit 21.

During 2009, Edward Jones sold 100% of the issued and outstanding shares of its subsidiary, Edward Jones Limited (“EDJ Limited”), a United Kingdom (“U.K.”) private limited company engaged in the retail financial services business in the U.K.

5

PART I

Item | 1. Business, continued |

Branch Office Network. The Partnership primarily serves individual long-term investors in small to medium-size towns and metropolitan suburbs through its extensive network of branch offices. The Partnership operated 11,390 branch offices as of February 24, 2012, primarily staffed by a single financial advisor and a branch office administrator. Of this total, the Partnership operated 10,841 offices in the U.S. (located in all 50 states, predominantly in communities with populations of under 50,000 and metropolitan suburbs) and 549 offices in Canada.

Governance.Unlike a corporation, the Partnership is not governed by a board of directors and has no individuals who are designated as directors. Moreover, none of its securities are listed on a securities exchange and therefore the governance requirements that apply to many U.S. Securities and Exchange Commission (“SEC”) reporting companies do not apply to it. Under the terms of the Partnership’s Eighteenth Amended and Restated Partnership Agreement (“the Partnership Agreement”), the Managing Partner has primary responsibility for administering the Partnership’s business, determining its policies and controlling the management and conduct of the Partnership’s business, and has the power to admit and dismiss general partners of JFC and to adjust the proportion of their respective interests in JFC. As of February 24, 2012, JFC was composed of 362 general partners, 14,416 limited partners and 280 subordinated limited partners. See Item 10 – Directors, Executive Officers and Corporate Governance for a description of the governance structure of the Partnership.

Revenues by Source. The following table sets forth on a continuing operations basis, for the past three years, the sources of the Partnership’s revenues. Due to the interdependence of the activities and departments of the Partnership’s investment business and the arbitrary assumptions required to allocate overhead, it is impractical to identify and specify expenses applicable to each aspect of the Partnership’s operations. Further information on revenue related to the Partnership’s reportable segments is provided in Note 17 to the Consolidated Financial Statements and Item 7 – Management’s Discussion and Analysis of Financial Condition and Results of Operations.

| | | | | | | | | | | | | | | | | | | | | | | | |

(Dollars in thousands) | | 2011 | | | 2010 | | | 2009 | |

Asset-based fees | | $ | 1,776,883 | | | | 39 | % | | $ | 1,397,333 | | | | 33 | % | | $ | 967,386 | | | | 28 | % |

Commissions | | | | | | | | | | | | | | | | | | | | | | | | |

Mutual funds | | | 866,005 | | | | 19 | % | | | 856,020 | | | | 21 | % | | | 766,192 | | | | 21 | % |

Listed securities | | | 392,743 | | | | 9 | % | | | 338,605 | | | | 8 | % | | | 281,549 | | | | 8 | % |

Insurance | | | 385,184 | | | | 8 | % | | | 326,698 | | | | 8 | % | | | 271,605 | | | | 8 | % |

Over-the-counter securities | | | 54,755 | | | | 1 | % | | | 54,529 | | | | 1 | % | | | 41,581 | | | | 1 | % |

| | | | | | | | | | | | | | | | | | | | | | | | |

Total commissions | | | 1,698,687 | | | | 37 | % | | | 1,575,852 | | | | 38 | % | | | 1,360,927 | | | | 38 | % |

Account and activity fees | | | 522,898 | | | | 11 | % | | | 503,264 | | | | 12 | % | | | 489,605 | | | | 14 | % |

Principal transactions | | | 284,231 | | | | 6 | % | | | 320,777 | | | | 8 | % | | | 398,108 | | | | 11 | % |

Investment banking | | | 153,100 | | | | 3 | % | | | 208,615 | | | | 5 | % | | | 183,797 | | | | 5 | % |

Interest and dividends | | | 130,150 | | | | 3 | % | | | 126,769 | | | | 3 | % | | | 112,637 | | | | 3 | % |

Other revenue | | | 11,553 | | | | 1 | % | | | 30,489 | | | | 1 | % | | | 35,558 | | | | 1 | % |

| | | | | | | | | | | | | | | | | | | | | | | | |

Total revenue | | $ | 4,577,502 | | | | 100 | % | | $ | 4,163,099 | | | | 100 | % | | $ | 3,548,018 | | | | 100 | % |

| | | | | | | | | | | | | | | | | | | | | | | | |

Asset-based Fees

The Partnership earns fees from investment advisory services offered through Edward Jones Advisory Solutions (“Advisory Solutions”), Edward Jones Managed Account Program (“MAP”) and, in Canada, Edward Jones Portfolio Program (“Portfolio Program”). Advisory Solutions and MAP are both registered as an investment advisory program with the SEC under the Investment Advisers Act of 1940.

6

PART I

Item | 1. Business, continued |

Portfolio Program is not required to be registered under this act as services from this program are only offered in Canada. Advisory Solutions provides investment advisory services to its clients for a monthly fee based upon the average value of their assets in the program, and consists of a Partnership managed account invested in mutual funds, exchange-traded funds (ETFs) and money market funds. For this program, the client must elect either a research or a custom type account model. If the client elects a research type model, the Partnership assumes full investment discretion on the accounts, which will be one of 60 different research models (including Unified Managed Accounts) developed and managed by Edward Jones’ Mutual Fund Research department. If the client elects to build a custom type model, the Partnership assumes limited investment discretion on the accounts developed by the client and his or her financial advisor.

MAP and Portfolio Program offer investment advisory services to clients, for a monthly fee based upon the average value of assets in the program, by using independent investment managers rather than Edward Jones’ Mutual Fund Research department.

In addition to the advisory programs mentioned above, the Partnership also earns asset-based fees from the trust and investment management services offered to its clients through Edward Jones Trust Company (“EJTC”).

The Partnership also earns service fees on most of its clients’ assets which are held by mutual fund companies and insurance companies. The fees generally range from 15 to 25 basis points (0.15% to 0.25%) of the value of the client assets so held.

In addition, the Partnership earns revenue sharing from certain mutual fund and insurance vendors. In most cases, this is additional compensation paid by investment advisers or distributors based on a percentage of average vendor assets held by the Partnership’s clients, on those products covered under the revenue sharing agreements. Revenue sharing agreements that provide for a fixed annual payment are also included in asset-based fees.

The Partnership does not manage any mutual funds, although it is a 49.5% limited partner of Passport Research, Ltd., the investment adviser to certain money market funds made available to the Partnership’s clients. Revenue from this source is primarily based on client assets in the funds. However, due to the current low interest rate environment, the investment adviser voluntarily chose (beginning in March 2009) to reduce certain fees charged to the funds to a level that will maintain a positive client yield on funds. For further information on this reduction of fees, see Item 7 – Management’s Discussion and Analysis of Financial Condition and Results of Operations.

Commissions

Commissions revenue is primarily comprised of charges to clients for the purchase or sale of securities, mutual fund shares and insurance products. The following briefly describes the Partnership’s sources of commissions revenue.

Mutual Funds. The Partnership distributes mutual fund shares in continuous offerings and new underwritings. As a dealer in mutual fund shares, the Partnership receives a dealer’s discount which generally ranges from 1% to 5% of the purchase price of the shares, depending on the terms of each fund’s prospectus and the amount of the purchase.

7

PART I

Item | 1. Business, continued |

Listed Securities Transactions. The Partnership receives a commission when it acts as an agent for a client in the purchase or sale of listed securities. These securities include common and preferred stocks and debt securities traded on and off the securities exchanges. The commission is based on the value of the securities purchased or sold.

Insurance.The Partnership sells life insurance, long-term care insurance, disability insurance, fixed and variable annuities and other types of insurance products of unaffiliated insurance companies to its clients through its financial advisors who hold insurance sales licenses. As an agent for the insurance companies, the Partnership receives commissions on the premiums paid for the policies.

Over-the-Counter Securities Transactions. Partnership activities in unlisted (over-the-counter) securities transactions are similar to its activities as a broker in listed securities. In connection with client orders to buy or sell securities, the Partnership charges a commission for agency transactions.

Account and Activity Fees

Revenue sources include sub-transfer agent accounting services fees, Individual Retirement Account (“IRA”) custodial services fees, and other product fees.

The Partnership charges fees to certain mutual funds for sub-transfer agent accounting services, including maintaining client account information and providing other administrative services for the mutual funds. Also, the Partnership acts as the custodian for clients’ IRA accounts and the clients are charged an annual fee for this service. Account and activity fees also include sales based revenue sharing fees pursuant to arrangements with certain mutual fund and insurance vendors where the vendors pay additional compensation to the Partnership based on a percentage of current year sales by the Partnership of products supplied by these vendors. The Partnership receives revenue from offering mortgage loans to its clients through a joint venture and through a co-branded credit card with a major credit card company. In addition, the Partnership earns transaction fee revenue relating to client purchases and sales of securities.

Principal Transactions

The Partnership makes a market in over-the-counter corporate securities, municipal obligations, government obligations, unit investment trusts, mortgage-backed securities and certificates of deposit. The Partnership’s market-making activities are conducted with other dealers in the “wholesale” and “retail” markets where the Partnership acts as a dealer buying from and selling to its clients. In making markets in securities, the Partnership exposes its capital to the risk of fluctuation in the fair value of its security positions. The Partnership maintains securities positions in inventory solely to support its business of buying securities from and selling securities to its retail clients and does not seek to profit by engaging in proprietary trading for its own account.

Investment Banking

Investment banking revenue is primarily derived from the Partnership’s distribution of U.S. government obligations and unit investment trusts on behalf of issuers, as well as underwriting of corporate securities and municipal obligations. The Partnership’s investment banking activities are performed primarily by its Syndicate and Investment Banking departments. The principal service which the Partnership renders as an investment banker is the underwriting and distribution of securities, either in a primary distribution on behalf of the issuer of such securities or in a secondary distribution on behalf of a holder of such securities.

8

PART I

Item | 1. Business, continued |

The distributions of corporate and municipal securities are, in most cases, underwritten by a group or syndicate of underwriters. Each underwriter has a participation in the offering.

Unlike many larger firms against which the Partnership competes, the Partnership historically has not, and does not presently engage in other investment banking activities, such as assisting in mergers and acquisitions, arranging private placement of securities issues with institutions, or providing consulting and financial advisory services to entities.

In the case of an underwritten offering managed by the Partnership, the Syndicate and Investment Banking departments may form underwriting syndicates and work with the branch office network for sales of the Partnership’s own participation and with other members of the syndicate in the pricing and negotiation of other terms. In offerings managed by others in which the Partnership participates as a syndicate member, these departments serve as active coordinators between the managing underwriter and the Partnership’s branch office network.

The underwriting activity of the Partnership involves substantial risks. An underwriter may incur losses if it is unable to resell the securities it is committed to purchase or if it is forced to liquidate all or part of its commitment at less than the agreed upon purchase price. Furthermore, the commitment of capital to an underwriting may adversely affect the Partnership’s capital position and, as such, its participation in an underwriting may be limited by the requirement that it must at all times be in compliance with the SEC’s uniform net capital requirements (the “Uniform Net Capital Rule”).

Interest and Dividends

Interest and dividends revenue is earned on margin account balances, cash and cash equivalents, cash and investments segregated under federal regulations, securities purchased under agreements to resell, partnership loans for general partnership interests, inventory securities and investment securities. Loans secured by securities held in client margin accounts provide a source of income to the Partnership. The Partnership is permitted to use securities owned by margin clients having an aggregate market value generally up to 140% of the debit balance in margin accounts as collateral for the borrowings. The Partnership may also use funds provided by free credit balances in client accounts to finance client margin account borrowings.

The Partnership is exposed to market risk for changes in interest rates and market prices on its inventory and investment securities. The Partnership’s interest income is impacted by the level of interest rates it charges its clients, the interest rate earned on overnight investments and the level of clients’ loan balances and credit balances.

9

PART I

Item | 1. Business, continued |

Significant Revenue Source

As of December 31, 2011, the Partnership distributed mutual funds for approximately 75 mutual fund sponsors, including American Funds Distributors, Inc. which represents 19% of the Partnership’s total revenue for the year ended December 31, 2011. This revenue consisted of commissions, asset-based fees and account and activity fees, which are described above. All of the revenue generated from this vendor relates to business conducted with the Partnership’s U.S. segment.

BUSINESS OPERATIONS

Research Department.The Partnership maintains a Research department to provide specific investment recommendations and market information for clients. The department supplements its own research with the services of an independent research service. In addition, the Research department provides recommendations for asset allocation, portfolio rebalancing and investment selections for Advisory Solutions client accounts.

Client Account Administration and Operations.Employees in the Operations division are responsible for activities relating to client securities and the processing of transactions with other broker-dealers, exchanges and clearing organizations. These activities include receipt, identification, and delivery of funds and securities, internal financial controls, accounting and personnel functions, office services, custody of client securities and the handling of margin accounts. The Partnership processes substantially all of its own transactions.

To expedite the processing of orders, the Partnership’s branch office system is linked to the home office through an extensive communications network. Orders for securities are generally captured at the branch electronically, routed to the home office and forwarded to the appropriate market for execution. The Partnership’s processing of paperwork following the execution of a security transaction is generally automated.

There is considerable fluctuation during any one year and from year to year in the volume of transactions the Partnership processes. The Partnership records transactions and posts its books on a daily basis. The Partnership has a computerized branch office communication system which is principally utilized for entry of security orders, quotations, messages between offices, research of various client account information, and cash and security receipts functions. Home office personnel, including operations and compliance personnel, monitor day-to-day operations to determine compliance with applicable laws, rules and regulations. Failure to keep current and accurate books and records can render the Partnership liable to disciplinary action by governmental and self-regulatory organizations (“SROs”).

The Partnership clears and settles virtually all of its listed and over-the-counter equities, municipal bond, corporate bond, mutual fund and annuity transactions for its U.S. broker-dealer through the National Securities Clearing Corporation (“NSCC”), Fixed Income Clearing Corporation (“FICC”) and Depository Trust Company (“DTC”), which are all subsidiaries of the Depository Trust and Clearing Corporation located in New York, New York.

In conjunction with clearing and settling transactions with NSCC, the Partnership holds client securities on deposit with DTC in lieu of maintaining physical custody of the certificates. The Partnership also uses a major bank for custody and settlement of treasury securities and Government National Mortgage Association (“GNMA”), Federal National Mortgage Association (“FNMA”) and Federal Home Loan Mortgage Corporation (“FHLMC”) issues.

10

PART I

Item | 1. Business, continued |

The Partnership is substantially dependent upon the operational capacity and ability of NSCC, DTC, FICC, and Canadian Depository of Securities (“CDS”). Any serious delays in the processing of securities transactions encountered by these clearing and depository companies may result in delays of delivery of cash or securities to the Partnership’s clients.

Broadridge Financial Solutions, Inc. (“Broadridge”), along with its U.S. business, Securities Processing Solutions, U.S., and its international business, Securities Processing Solutions, International, provide automated data processing services for client account activity and related records for the Partnership in the U.S. and Canada, respectively. The Partnership does not employ its own floor brokers for transactions on exchanges. The Partnership has arrangements with other brokers to execute the Partnership’s transactions in return for a commission based on the size and type of trade. If, for any reason, any of the Partnership’s clearing, settling or executing agents were to fail, the Partnership and its clients would be subject to possible loss. To the extent that the Partnership would not be able to meet the obligations to the clients, such clients might experience delays in obtaining the protections afforded them.

The Canadian broker-dealer has an agreement with Broadridge to provide the securities processing systems, as well as an agreement with Computershare Trust Company of Canada to act as trustee for cash balances held by clients in their retirement accounts. The Canadian broker-dealer is the custodian for client securities and manages all related securities and cash processing, such as trades, dividends, corporate actions, client cash receipts and disbursements, client tax reporting and statements.

The Canadian broker-dealer handles the routing and settlement of client transactions. In addition, the Canadian broker-dealer is a member of CDS and FundServ for clearing and settlement of transactions. CDS effects clearing of securities on the Canadian National Stock Exchange (“CNQ”), Toronto Stock Exchange (“TSX”) and TSX Venture Exchange (“CDNX”). Client securities on deposit are also held with CDS and National Bank Correspondent Network (“NBCN”).

The Partnership believes that its internal controls and safeguards concerning the risks of securities thefts are adequate. The possibility of securities thefts is an industry-wide risk. The Partnership has not had, to date, significant problems with such thefts. The Partnership maintains fidelity bonding insurance which, in the opinion of management, provides adequate coverage.

Employees. In contrast to some other broker-dealers, the Partnership’s financial advisors are employees (or general partners of the Partnership) and are not independent contractors. As of February 24, 2012, the Partnership had approximately 37,000 full and part-time employees, including its 12,169 financial advisors. The Partnership’s financial advisors are generally compensated on a commission basis and may, in addition, be entitled to bonus compensation based on their respective branch office profitability and the profitability of the Partnership. The Partnership has in the past paid bonuses to its non-financial advisor employees pursuant to a discretionary formula established by management.

U.S. employees of the Partnership are bonded under a blanket policy as required by New York Stock Exchange (“NYSE”) rules. The per occurrence coverage limit for U.S. employees is $5.0 million, subject to a $2.0 million deductible provision. In addition, there is excess coverage with an annual aggregate amount of $45.0 million. Canadian employees of the Partnership are bonded under a blanket policy as required by the Investment Industry Regulation Organization of Canada (“IIROC”). The annual aggregate amount of coverage for Canadian employees is CAD $25.0 million, subject to a CAD $0.05 million deductible provision per occurrence.

11

PART I

Item | 1. Business, continued |

The Partnership maintains an initial training program for prospective financial advisors that spans nearly four months which includes preparation for regulatory exams, concentrated instruction in the classroom and on-the-job training in a branch office. During the first phase, U.S. trainees spend nearly two months studying Series 7 and Series 66 examination materials and taking the examinations. In Canada, financial advisors have the requisite examinations completed prior to being hired. After passing the requisite examinations, trainees spend one week in a comprehensive training program in one of the Partnership’s home office training facilities, followed by seven weeks of on-the-job training in their market and in a nearby branch location. This training includes reviewing investments, compliance requirements, office procedures, and understanding client needs, as well as establishing a base of potential clients. One final week is then spent in a home office training facility to complete the initial training program. Five months later, the financial advisor attends an additional training class in a home office location, and subsequently, the Partnership offers periodic continuing training to its experienced financial advisors for the entirety of their career. Training programs for the more experienced financial advisors focus on meeting client needs and effective management of the branch office.

The Partnership considers its employee relations to be good and believes that its compensation and employee benefits, which include medical, life and disability insurance plans and profit sharing and deferred compensation retirement plans, are competitive with those offered by other firms principally engaged in the securities business.

Competition.The Partnership is subject to intense competition in all phases of its business from other securities firms, many of which are substantially larger than the Partnership in terms of capital, brokerage volume and underwriting activities. In addition, the Partnership encounters competition from other organizations such as banks, insurance companies, and others offering financial services and advice. The Partnership also competes with a number of firms offering discount brokerage services, usually with lower levels of personalized service to individual clients. With minor exceptions, clients are free to transfer their business to competing organizations at any time, although a fee may be charged to do so. There is intense competition among firms for financial advisors. The Partnership experiences continued efforts by competing firms to hire away its financial advisors, although the Partnership believes that its rate of turnover of financial advisors is not higher than that of other comparable firms.

REGULATION

Broker-Dealer and Investment Adviser Regulation

Broker-dealers are subject to regulations which cover all aspects of the securities business, including sales methods, trade practices among broker-dealers, use and safekeeping of client funds and securities, client payment and margin requirements, capital structure of securities firms, record-keeping and the conduct of directors, officers and employees.

The SEC is the federal agency responsible for the administration of the U.S. securities laws. Its mission is to protect investors, maintain fair, orderly and efficient markets and facilitate capital formation. Edward Jones is registered as a broker-dealer and investment adviser with the SEC. Much of the regulation of broker-dealers has been delegated to SROs, principally the Financial Industry Regulation Authority, Inc. (“FINRA”). FINRA adopts rules (which are subject to approval by the SEC) that govern the broker-dealer industry and conducts periodic examinations of Edward Jones’ operations.

12

PART I

Item | 1. Business, continued |

Securities firms are also subject to regulation by state securities commissions in those states in which they conduct business. Edward Jones is registered as a broker-dealer in all 50 states, the District of Columbia, Puerto Rico and the U.S. Virgin Islands.

The SEC, SROs and state securities commissions may conduct administrative proceedings which can result in censure, fine, suspension or expulsion of a broker-dealer, its officers or employees. Edward Jones has in the past been, and may in the future be, the subject of regulatory actions by various agencies that have the authority to regulate its activities (see Item 3 – Legal Proceedings for more information).

As an investment dealer in all provinces and territories of Canada, the Canadian broker-dealer is subject to provincial, territorial and federal laws. All provinces and territorial jurisdictions have established securities administrators to fulfill the administration of securities laws. The Canadian broker-dealer is also subject to the regulation of the Canadian SRO, IIROC, which oversees the business conduct and financial affairs of its member firms, as well as all trading activity on debt and equity marketplaces in Canada. IIROC fulfills its regulatory obligations by implementing and enforcing rules regarding the proficiency, business and financial conduct of member firms and their registered employees, and marketplace integrity rules regarding trading activity on Canadian debt and equity marketplaces.

Pursuant to U.S. federal law, Edward Jones belongs to the Securities Investors Protection Corporation (“SIPC”). For clients in the U.S., SIPC provides $500,000 of coverage for missing securities, including a maximum of $250,000 for cash claims. Pursuant to IIROC requirements, the Canadian broker-dealer belongs to the Canadian Investor Protection Fund (“CIPF”), a non-profit organization that provides investor protection for investment dealer insolvency. For clients in Canada, CIPF limits coverage to CAD $1,000,000 in total, which can be any combination of securities and cash.

The Partnership currently maintains additional protection for U.S. clients provided by Underwriters at Lloyd’s. The additional protection contract provided by Underwriters at Lloyd’s protects clients’ accounts in excess of the SIPC coverage subject to specified limits. This policy covers theft, misplacement, destruction, burglary, embezzlement or abstraction of client securities up to an aggregate limit of $900 million for covered claims of all U.S. clients of Edward Jones. Market losses are not covered by SIPC or the additional protection.

In addition, Edward Jones is subject to the rules and regulations of the Investment Advisers Act of 1940, which require investment advisers to register with the SEC. The Investment Advisers Act’s rules and regulations govern all aspects of the investment advisory business, including registration, trading practices, custody of client funds and securities, record-keeping, advertising and business conduct.

Additional legislation, changes in rules promulgated by the SEC, the Department of Labor and SROs, and/or changes in the interpretation or enforcement of existing laws and rules, may directly affect the operations and profitability of broker-dealers and investment advisers. With the passage of the Dodd-Frank Wall Street Reform and Consumer Protection Act (“Dodd-Frank Act”), the SEC has been directed to study existing practices in the industry, and granted discretionary rulemaking authority to establish, among other things, comparable standards of conduct for broker-dealers and investment advisers when providing personalized investment

13

PART I

Item | 1. Business, continued |

advice about securities to retail clients and such other clients as the SEC provides by rule. The SEC may engage in rulemaking or issue interpretive guidance concerning the standard of conduct for broker-dealers and investment advisers. FINRA or other regulatory authorities may also issue rules related to the Dodd–Frank Act, but it is unclear at this time what impact such rulemaking activities will have on the Partnership or its operations.

Trust Regulation of EJTC and Regulation of JFC as EJTC’s Parent

Pursuant to the Dodd-Frank Act, effective July 21, 2011 authority for the supervision and regulation of EJTC was transferred from the Office of Thrift Supervision (“OTS”) to the Office of the Comptroller of the Currency (“OCC”). As of the same date, responsibility for the supervision and regulation of JFC, based on its status as a savings and loan holding company (“SLHC”) (which such status is the result of its 100% ownership of EJTC), was transferred from the OTS to the Board of Governors of the Federal Reserve System (“FRB”). The Dodd-Frank Act, however, allows entities controlling a savings association that functions solely in a trust or fiduciary capacity to cease to be a SLHC. On July 25, 2011, the Partnership requested that the FRB deregister it as a SLHC. A permanent decision from the FRB is still pending, but, by letter dated March 15, 2012, the FRB: (a) granted JFC a temporary exemption from submitting the FRB regulatory reports beginning with the March 31, 2012 reporting period; (b) determined that JFC should submit certain informational filings to the FRB during the temporary exemption period; and (c) informed JFC that, if it does not receive a permanent exemption by December 31, 2012, it will be required to begin submitting the FRB’s regulatory reports by March 31, 2013.

Uniform Net Capital Rule

As a result of its activities as a broker-dealer and a member firm of FINRA, Edward Jones is subject to the Uniform Net Capital Rule which is designed to measure the general financial integrity and liquidity of a broker-dealer and the minimum net capital deemed necessary to meet the broker-dealer’s continuing commitments to its clients. The Uniform Net Capital Rule provides for two methods of computing net capital and Edward Jones has adopted what is generally referred to as the alternative method. Minimum required net capital under the alternative method is equal to the greater of $0.25 million or 2% of the aggregate debit items, as defined. The Uniform Net Capital Rule prohibits withdrawal of equity capital whether by payment of dividends, repurchase of stock or other means, if net capital would thereafter be less than minimum requirements. Additionally, certain withdrawals require the approval of the SEC to the extent they exceed defined levels even though such withdrawals would not cause net capital to be less than 5% of aggregate debit items. In computing net capital, various adjustments are made to exclude assets which are not readily convertible into cash and to provide a conservative valuation of other assets, such as a company’s securities owned. Failure to maintain the required net capital may subject Edward Jones to suspension or expulsion by FINRA, the SEC and other regulatory bodies and/or exchanges and may ultimately require liquidation. Edward Jones has, at all times, been in compliance with the Uniform Net Capital Rule.

The Canadian broker-dealer and EJTC are also required to maintain specified levels of regulatory capital. Each subsidiary has, at all times, been in compliance with the applicable capital requirements in the jurisdictions in which it operates.

14

PART I

Item | 1. Business, continued |

FORWARD-LOOKING STATEMENTS

This report on Form 10-K, and in particular Management’s Discussion and Analysis of Financial Condition and Results of Operations, contains forward-looking statements within the meaning of U.S. securities laws. You can identify forward-looking statements by the use of the words “believe,” “expect,” “anticipate,” “intend,” “estimate,” “project,” “will,” “should,” and other expressions which predict or indicate future events and trends and which do not relate to historical matters. You should not rely on forward-looking statements, because they involve known and unknown risks, uncertainties and other factors, some of which are beyond the control of the Partnership. These risks, uncertainties and other factors may cause the actual results, performance or achievements of the Partnership to be materially different from the anticipated future results, performance or achievements expressed or implied by the forward-looking statements.

Some of the factors that might cause differences between forward-looking statements and actual events include, but are not limited to, the following: (1) general economic conditions; (2) regulatory actions; (3) changes in legislation or regulation, including new regulations under the Dodd-Frank Act; (4) actions of competitors; (5) litigation; (6) the ability of clients, other broker-dealers, banks, depositories and clearing organizations to fulfill contractual obligations; (7) changes in interest rates; (8) changes in technology; and (9) a fluctuation or decline in the fair value of securities. These forward-looking statements were based on information, plans, and estimates at the date of this report, and the Partnership does not undertake to update any forward-looking statements to reflect changes in underlying assumptions or factors, new information, future events or other changes.

15

PART I

The Partnership is subject to a number of risks potentially impacting its business, financial condition, results of operations and cash flows. In addition to the risks and uncertainties discussed elsewhere in this Annual Report on Form 10-K, or in the Partnership’s other filings with the SEC, the following are some important factors that could cause the Partnership’s actual results to differ materially from results experienced in the past or those projected in any forward-looking statement. The risks and uncertainties described below are not the only ones facing the Partnership. Additional risks and uncertainties not presently known to the Partnership or that the Partnership currently deems immaterial could also have a material adverse effect on the Partnership’s business and operations. If any of the matters included in the following risks were to occur, the Partnership’s business, financial condition, results of operations and cash flows could be materially adversely affected.

RISK RELATED TO THE PARTNERSHIP’S BUSINESS

MARKET CONDITIONS —As a part of the securities industry, a downturn in the U.S. and/or global securities markets has in the past had, and could in the future have, a significant negative effect on revenues and could significantly reduce or eliminate profitability of the Partnership.

General political and economic conditions and events such as economic recession, natural disasters, terrorist attacks, war, changes in local economic and political conditions, regulatory changes or changes in the law, or interest rate or currency rate fluctuations could create a downturn in the U.S and/or global securities markets. The securities industry, and therefore the Partnership, is highly dependent upon market prices and volumes which are highly unpredictable and volatile in nature. Events such as global recession, frozen credit markets, institutional failures, and government-sponsored bailouts of a number of large financial services companies, as well as debt ceiling debates, and sovereign credit downgrades, could make the capital markets increasingly volatile. Weakened global economic conditions and an unsettled nature of financial markets, among other things, could cause significant declines in the Partnership’s net revenues which will adversely impact its overall financial results.

With the Partnership’s composition of net revenue now more heavily weighted towards asset-based fee revenue than trade revenue as in the past, a decrease in the market value of assets due to market declines can cause much more negative impact on the Partnership’s financial results than experienced in prior years, due to the fact that asset-based fees are earned on the value of the underlying assets. Conversely, in times of improved market conditions the Partnership’s asset-based fee revenue should be positively impacted due to the increase in the market value of assets on which fees are earned.

In addition, the Partnership could experience a material reduction in volume and lower securities prices in times of unfavorable economic conditions, which would result in lower commission revenue and losses in dealer inventory accounts and syndicate positions. This would have a material adverse impact on the profitability of the Partnership’s operations.

While the Partnership’s results have improved in 2010 and 2011, financial markets continue to experience extreme volatility and the risks to sustained global economic growth remain high. Furthermore, the Partnership would be subject to increased risk of its clients being unable to meet their commitments such as margin obligations if there was an economic recession. If clients are unable to meet their margin obligations, the Partnership has an increased risk of losing money on margin transactions and incurring additional expenses defending or pursuing claims. Developments such as lower revenues and declining profit margins could reduce or eliminate the Partnership’s profitability.

16

PART I

Item | 1A. Risk Factors, continued |

LEGISLATIVEAND REGULATORY INITIATIVES —Newly adopted federal legislation and pending regulatory proposals intended to reform the financial services industry could significantly impact the regulation and operation of the Partnership and its subsidiaries, its revenue and its profitability. In addition, such laws and regulations may significantly alter or restrict the Partnership’s historic business practices, which could negatively affect its operating results.

The Partnership is subject to extensive regulation by federal and state regulatory agencies and by SROs, within the industry. The Partnership operates in a regulatory environment that is subject to ongoing change and has seen significantly increased regulation in recent years. The Partnership may be adversely affected as a result of new or revised legislation or regulations, changes in federal, state or foreign tax laws and regulations, or by changes in the interpretation or enforcement of existing laws and regulations.

The Dodd-Frank Act. The Dodd-Frank Act, passed by the U.S. Congress and signed by the President July 21, 2010, includes provisions that could potentially impact the Partnership’s operations. Since the passage of the Dodd-Frank Act, the Partnership has not been required to enact material changes to its operations. However, the Partnership continues to review and evaluate the provisions of the Dodd-Frank Act and the impending rules to determine what impact or potential impact it may have on the financial services industry, the Partnership and its operations. Among the numerous potentially impactful provisions in the Dodd-Frank Act are: (i) pursuant to Section 913 of the Dodd-Frank Act, the SEC staff issued a study recommending a universal fiduciary standard of care applicable to both broker-dealers and investment advisers when providing personalized investment advice about securities to retail clients, and such other clients as the SEC provides by rule. When proposed, the uniform standard of care for personalized investment advice is expected to require the broker-dealer and investment adviser to act in the best interest of the client; and (ii) pursuant to Section 914 of the Dodd-Frank Act, a new SRO may be proposed to regulate investment advisers. In addition, the Dodd-Frank Act contains new or enhanced regulations that could impact specific securities products offered by the Partnership to investors and specific securities transactions. Proposed rules related to these provisions are anticipated in 2012. It is unclear what impact any such rules, if adopted, would have on the Partnership.

Additionally, the Partnership continues to monitor several other proposed regulations and rules that do not presently appear as though they will have a material impact on the Partnership, such as Title X of the Dodd-Frank Act, which established the Bureau of Consumer Financial Protection with broad authority to issue new regulations, and proposed rules related to Section 956 of the Dodd-Frank Act, which would prohibit certain types of incentive-based compensation arrangements. In their present form, the Partnership does not believe these regulations and rules will have a material impact on the Partnership, but if revised the impact on the Partnership could be material.

It is expected that FINRA or other regulatory authorities will continue to issue rules related to the Dodd-Frank Act in the future and the Partnership will continue to monitor and review any such rules.

17

PART I

Item | 1A. Risk Factors, continued |

Department of Labor. In October 2010, the Department of Labor (the “DOL”) proposed a modification to a rule that would have impacted the Employee Retirement Income Security Act’s definition of “fiduciary” and potentially limited certain of Edward Jones’ business practices. In September 2011, the DOL announced that it was withdrawing the proposed rule and stated its intention to re-propose the rule in early 2012 with significant modifications. The DOL has indicated that the re-proposed rule will impact IRAs and has indicated an intention to address what has been generally described as “third party payments,” such as revenue sharing. The Partnership cannot predict what the re-proposed rule will say, what its scope will be, when or if it will be re-proposed or adopted, or what the impact will be on the Partnership. However, any such rule could impact the operations of Edward Jones and the profitability of the Partnership.

Trust Reform and the Volcker Rule. The Partnership has requested that the FRB deregister it as a SLHC and has received a temporary exemption from the FRB from submitting the FRB regulatory reports. The Partnership anticipates that this request will be approved and is preparing for supervision and regulation of the Partnership as a holding company by the OCC. If the request is not approved, however, the Partnership could become subject to what is commonly referred to as the “Volcker Rule”, which was jointly proposed in October 2011 by the SEC, the Federal Deposit Insurance Corporation, the FRB, and the OCC. The proposed Volcker Rule has the stated purpose of generally prohibiting certain banking entities from engaging in proprietary trading or sponsoring or investing in a hedge fund or private equity fund. At this time, it is unclear what impact the proposed Volcker Rule would have on the financial services industry, the Partnership and its operations if adopted and applicable to the Partnership. However, the Partnership continues to review and evaluate the proposed Volcker Rule to determine what impact or potential impact it may have.

International Financial Reporting Standards. The International Accounting Standards Board (“IASB”) developed a core set of accounting standards to act as a framework for financial reporting known as the International Financial Reporting Standards (“IFRS”). By 2007, the majority of listed European Union companies, including banks and insurance companies, began using IFRS to prepare financial statements. In contrast, the majority of public companies in the U.S. prepare financial statements under accounting principles generally accepted in the U.S. (“GAAP”).

The SEC is evaluating adoption of IFRS in the U.S. It is unclear at this time whether the SEC will propose mandatory adoption of IFRS or some other form of GAAP and IFRS harmonization. The Canadian Accounting Standards Board began requiring use of IFRS in Canada in 2011 for publically accountable profit-oriented enterprises. This change did not impact the Partnership’s Consolidated Financial Statements.

The Partnership is currently waiting on further guidance from the SEC to determine what impact, if any, the adoption of IFRS in the U.S. could have on its financial position or results of operations. If adopted, IFRS could significantly impact the way the Partnership determines income before allocations to partners, allocations to partners, or returns on partnership capital. In addition, switching to IFRS would be a complex endeavor for the Partnership. The Partnership may need to develop new systems and controls around the principles of IFRS and the specific costs associated with this conversion are uncertain.

Rule 12b-1 Fees. The Partnership receives various payments in connection with the purchase, sale and holding of mutual fund shares by its clients. Those payments include Rule 12b-1 fees (i.e., service fees) and expense reimbursements. Rule 12b-1, under the Investment Company Act of 1940 (“ICA”), allows a mutual fund to pay distribution and marketing expenses out of the fund’s assets. The SEC currently does not limit the size of Rule 12b-1 fees that funds may pay.

18

PART I

Item | 1A. Risk Factors, continued |

FINRA does impose such limitations. However, on July 21, 2010 the SEC proposed reform of Rule 12b-1. The proposal called for the rescission of Rule 12b-1 and a proposed new Rule 12b-2 which would allow funds to deduct a fee on an annual basis of up to 25 basis points to pay for distribution expenses without a cumulative cap on this fee. Additionally, the proposal includes other amendments that would permit funds to deduct an asset-based distribution fee in which the fund may deduct ongoing sales charges with no annual limit, but cumulatively the asset-based distribution fee could not exceed the amount of the highest front-end load for a particular fund. The proposed rule also allows funds to create and distribute a class of shares at net asset value and dealers could establish their own fee schedule. The proposal includes additional requirements for disclosure on trade confirmations and in fund documents. These proposed rules have not been enacted and the Partnership cannot predict with any certainty whether or which of these proposals will be enacted in their current form, revised form or enacted at all. In addition, the Partnership is not yet able to determine the potential financial impact on its operating results related to this proposed reform of Rule 12b-1. For further information on the amount of Rule 12b-1 fees earned by the Partnership, see Item 7 – Management’s Discussion and Analysis of Financial Condition and Results of Operations.

Health Care Reform.The Patient Protection and Affordable Care Act (“PPACA”) was signed into law on March 23, 2010. PPACA requires employers to provide affordable coverage with a minimum essential benefit to full-time employees or pay a financial penalty. The bill contains provisions that go into effect over the next several years that expand employee eligibility for the Partnership’s medical plan and places limits on plan design. Regulatory guidance required to fully assess the impact of this law is still forthcoming. Accordingly, the Partnership is not yet able to determine the full potential financial impact on its operating results in future years.

Federal “Do Not Call” Regulations.The Partnership is also subject to federal and state regulations like other businesses and must evaluate and adapt to new regulations as they are adopted. In particular, the Partnership believes the federal “do not call” regulations enacted in recent years have affected the manner in which many of its financial advisors conduct their businesses. While the Partnership believes it is in compliance with these regulations, these regulations could impact the Partnership’s future revenues or results of operations.

Any of the foregoing regulatory initiatives could adversely affect the Partnership’s business operations, business model, and profitability. The Partnership cannot predict with any certainty whether or which of the regulatory proposals that have not yet been adopted will be adopted, and if so whether they will be adopted in their current form or adopted subject to further revisions. If adopted, some of these initiatives could significantly and adversely impact the Partnership’s operating costs, its structure, its ability to generate revenue, and its overall profitability.

COMPETITION —The Partnership is subject to intense competition for clients and personnel, and many of its competitors have greater resources.

All aspects of the Partnership’s business are highly competitive. The Partnership competes for clients and personnel directly with other securities firms and increasingly with other types of organizations and other businesses offering financial services, such as banks and insurance companies. Many of these organizations have substantially greater capital and additional resources, and some entities offer a wider range of financial services. Over the past several years, there has been significant consolidation of firms in the financial services industry, forcing the Partnership to compete with larger firms with greater capital and resources, brokerage volume and underwriting activities, and more competitive pricing. Also, the Partnership continues to compete with a number of firms offering discount brokerage services, usually with lower levels of personalized service to individual clients. With minor exceptions, clients are free to transfer their business to competing organizations at any time, although there may be a fee to do so.

19

PART I

Item | 1A. Risk Factors, continued |

Competition among financial services firms also exists for financial advisors and other personnel. The Partnership’s continued ability to expand its business and to compete effectively depends on the Partnership’s ability to attract qualified employees and to retain and motivate current employees. If the Partnership’s profitability decreases, then bonuses paid to financial advisors and other personnel, along with profit-sharing contributions, may be decreased or eliminated, increasing the risk that personnel could be hired away by competitors. In addition, the Partnership has recently faced increased competition from larger firms in its non-urban markets, and from a broad range of firms in the urban and suburban markets in which the Partnership competes.

The competitive pressure the Partnership experiences could have an adverse effect on its business, results of operations, financial condition and cash flow. For additional information, see Item 1—Business Operations—Competition.

BRANCH OFFICE SYSTEM —The Partnership’s system of maintaining branch offices primarily staffed by one financial advisor may expose the Partnership to risk of loss or liability from the activities of the financial advisors and to increases in rent related to increased real property values.

Most of the Partnership’s branch offices are staffed by a single financial advisor and a branch office administrator without an onsite supervisor as would be found at broker-dealers with multi-broker branches. The Partnership’s primary supervisory activity is conducted from its home offices. Although this method of supervision is designed to comply with all applicable industry and regulatory requirements, it is possible that the Partnership is exposed to a risk of loss arising from alleged imprudent or illegal actions of its financial advisors. Furthermore, the Partnership may be exposed to further losses if additional time elapses before its supervisory personnel detect problem activity.

The Partnership maintains personal financial and account information and other documents and instruments for its clients at its branch offices, both physically and in electronic format. Despite reasonable precautions, because the branch offices are relatively small and some are in remote locations, the security systems at these branch offices may not prevent theft of such information. If security of a branch is breached and personal financial and account information is stolen, the Partnership’s clients may suffer financial harm and the Partnership could suffer financial harm, reputational damage and regulatory issues.

In addition, the Partnership leases its branch office spaces and a material increase in the value of real property may increase the amount of rent paid, which will negatively impact the Partnership’s profitability.

20

PART I

Item | 1A. Risk Factors, continued |

INABILITYTO ACHIEVE OUR GROWTH RATE —If the Partnership is unable to fully achieve its goals for hiring financial advisors or the attrition rate of its financial advisors is higher than its expectations, the Partnership may not be able to meet its planned growth rates or maintain its current number of financial advisors.

It is more difficult for the Partnership to attract qualified applicants for financial advisor positions during market downturns. In addition, the Partnership relies heavily on referrals from its current financial advisors in recruiting new financial advisors. During an economic downturn, current financial advisors can be less effective in recruiting potential new financial advisors through referrals.

Regardless of the presence of a market downturn, the Partnership may not be able to meet its hiring objectives. For instance, the Partnership has been below its hiring objectives in 2010 and 2011 and did not achieve its hiring objectives in seven out of the past nine years. There can be no assurance that the Partnership will be able to hire at desired rates in future periods to achieve its planned growth. In addition, the Partnership may not be able to hire at levels to maintain its current number of financial advisors.

A significant number of the Partnership’s financial advisors have been licensed as brokers for less than three years. As a result of their relative inexperience, many of these financial advisors have encountered or may encounter difficulties developing or expanding their businesses. Consequently, the Partnership has periodically experienced higher rates of attrition, particularly with respect to the less experienced financial advisors and especially during market downturns. The Partnership generally loses more than half of its financial advisors who have been licensed for less than three years. In the past, the Partnership also has experienced increased financial advisor attrition due to increased competition from other financial services companies and efforts by those firms to recruit its financial advisors. There can be no assurance that the attrition rates the Partnership has experienced in the past will not continue or increase in the future. In addition, the Partnership raised the performance standards for its financial advisors in 2011, which may attribute to higher attrition for financial advisors unable to meet these performance standards.

Either the failure to achieve hiring goals or an attrition rate higher than anticipated may result in a decline in the revenue the Partnership receives from commissions and other securities related revenues. As a result, the Partnership may not be able to either maintain its current number of financial advisors or achieve the level of net growth upon which its business model is based and its revenues and results of operations may be adversely impacted.

In order to attract candidates to become financial advisors, in 2011 the Partnership increased the compensation paid to new financial advisors during the first three years as a financial advisor. The intent is to attract a greater number of high quality recruits with an enhanced level of compensation in order to meet the Partnership’s growth objectives. If the Partnership increases new financial advisor compensation and does not comparatively increase the level of productivity and retention rate of these financial advisors, then the additional compensation could negatively impact the Partnership’s financial performance in future periods.

21

PART I

Item | 1A. Risk Factors, continued |

LITIGATIONAND REGULATORY INVESTIGATIONSAND PROCEEDINGS —As a securities firm, the Partnership is subject to litigation involving civil plaintiffs seeking substantial damages and regulatory investigations and proceedings, which have increased over time and are expected to continue to increase even as global market conditions improve.

Many aspects of the Partnership’s business involve substantial litigation and regulatory risks. The Partnership is, from time to time, subject to examinations and informal inquiries by regulatory and other governmental agencies.

Such matters have in the past, and could in the future, lead to formal actions, which may impact the Partnership’s business. In the ordinary course of business, the Partnership also is subject to arbitration claims, lawsuits and other significant litigation such as class action suits. Over time, there has been increasing litigation involving the securities industry in general, including class action suits that generally seek substantial damages.

The Partnership has incurred significant expenses to defend and/or settle claims in the past. In view of the inherent difficulty of predicting the outcome of such matters, particularly in cases in which claimants seek substantial or indeterminate damages or in actions which are at very preliminary stages, the Partnership cannot predict with certainty the eventual loss or range of loss related to such matters. Due to the uncertainty related to litigation and regulatory investigations and proceedings, the Partnership cannot determine if future litigation will have a material adverse effect on its consolidated financial condition. Such legal actions may be material to future operating results for a particular period or periods. See Item 3 – Legal Proceedings for more information regarding unresolved claims.

RELIANCEON ORGANIZATIONS —The Partnership’s dependence on third-party organizations exposes the Partnership to disruption if its products and services are no longer offered, supported or develop defects.

The Partnership incurs obligations to its clients which are supported by obligations from firms within the industry, especially those firms with which the Partnership maintains relationships by which securities transactions are executed. The inability of an organization with which the Partnership does a large volume of business to promptly meet its obligations could result in substantial losses to the Partnership.

The Partnership is particularly dependent on Broadridge, which acts as the Partnership’s primary vendor for providing accounting and record-keeping for client accounts in both the U.S. and Canada. The Partnership’s communications and information systems are integrated with the information systems of Broadridge. There are relatively few alternative providers to Broadridge and although the Partnership has analyzed the feasibility of performing Broadridge’s functions internally, the Partnership may not be able to do it in a cost-effective manner or otherwise. Consequently, any new computer systems or software packages implemented by Broadridge which are not compatible with the Partnership’s systems, or any other interruption or the cessation of service by Broadridge as a result of systems limitations or failures, could cause unanticipated disruptions in the Partnership’s business which may result in financial losses and/or disciplinary action by governmental agencies and/or SROs.

22

PART I

Item | 1A. Risk Factors, continued |

CANADIAN OPERATIONS — The Partnership is focusing heavily on efforts, and intends to continue to make substantial investments to support the potential profitability of its Canadian operations, which have not yet achieved profitability.

The Partnership commenced operations in Canada in 1994 and plans to continue to expand its branch system in Canada. Despite recent improvements in Canadian financial performance, the Canadian operations have operated at a substantial deficit from inception. The Partnership plans to make additional investments in its Canadian operations, which may be substantial. However, the number of Canadian financial advisors employed by the Partnership has declined since 2009. This decline could affect the ability of the Partnership to reach its profitability goals for the Canadian segment.

In addition, Gary Reamey has decided to retire at the end of 2012 and therefore has stepped down as country leader for Canada effective January 1, 2012, and David Lane has assumed those responsibilities. The Canadian operations could be adversely impacted during this transitional period.

There is no assurance the Canadian operations will ultimately become profitable. For further information on the Canadian operations, see Note 17 to the Consolidated Financial Statements.

CAPITAL LIMITATIONS; UNIFORM NET CAPITAL RULE —The SEC’s Uniform Net Capital Rule imposes minimum net capital requirements and could limit the Partnership’s ability to engage in certain activities which are crucial to its business.

Adequacy of capital is vitally important to broker-dealers, and lack of sufficient capital may limit the Partnership’s ability to compete effectively. In particular, lack of sufficient capital or compliance with the Uniform Net Capital Rule may limit Edward Jones’ ability to commit to certain securities activities such as underwriting and trading, which require significant amounts of capital, its ability to expand margin account balances, as well as its commitment to new activities requiring an investment of capital. FINRA regulations and the Uniform Net Capital Rule may restrict Edward Jones’ ability to expand its business operations, including opening new branch offices or hiring additional financial advisors. Consequently, a significant operating loss or an extraordinary charge against net capital could adversely affect Edward Jones’ ability to expand or even maintain its present levels of business.

In addition to the regulatory requirements applicable to Edward Jones, EJTC and the Canadian broker-dealer are subject to regulatory capital requirements in the U.S. and in Canada. Failure by the Partnership to maintain the required net capital for any of its subsidiaries may subject it to disciplinary actions by the SEC, FINRA, IIROC, OCC or other regulatory bodies, which could ultimately require its liquidation. In the U.S., Edward Jones may be unable to expand its business and may be required to restrict its withdrawal of subordinated debt and partnership capital in order to meet the net capital requirements.

LIQUIDITY —The Partnership’s business in the securities industry requires that sufficient liquidity be available to maintain its business activities, and it may not always have access to sufficient funds.

Liquidity, or ready access to funds, is essential to the Partnership’s business. The current tight credit market environment could have a negative impact on its ability to maintain sufficient liquidity to meet its working capital needs. Short term and long term financing are two sources of liquidity that could be affected by the current tight credit market. As a result of the concerns about the stability of the markets in general, some lenders have reduced their lending to borrowers, including the Partnership.

23

PART I

Item | 1A. Risk Factors, continued |

There is no assurance that financing will be available at attractive terms, or at all, in the future. A significant decrease in the Partnership’s access to funds could negatively affect its business and financial management in addition to its reputation in the industry.

Many limited partners, subordinated limited partners and general partners have financed the initial and subsequent purchases of their Partnership interest by obtaining personal bank loans. Any such bank agreement is and will be between the partner and the bank. The Partnership does not guarantee the bank loans, nor can partners pledge their Partnership interest as collateral for the bank loan. Partners who finance all or a portion of their Partnership interest with bank financing or financing from the Partnership may be more likely to request the withdrawal of capital to repay such obligations should the Partnership experience a period of reduced earnings. As a partnership, any withdrawals by general partners, subordinated limited partners or limited partners are subject to the terms of the Partnership Agreement and would reduce the Partnership’s available liquidity and capital.

In 2011, the Partnership began making loans available to general partners (other than those who are members of the Partnership’s Executive Committee) that require financing for some or all of their individual partner capital contributions. Loans made by the Partnership to general partners are generally for a period of one year and bear interest at a rate defined in the loan documents. The Partnership recognizes interest income for the interest paid by general partners in connection with such loans. General partners borrowing from the Partnership are required to repay such loans by applying the majority of earnings received from the Partnership to such loans. As a result, there is no assurance that general partner’s will be able to repay the interest and/or the principal amount of their loans at or prior to its maturity.

UPGRADEOF TECHNOLOGICAL SYSTEMS —The Partnership may engage in significant technology initiatives in the future which may be costly and could lead to disruptions.

From time to time, the Partnership has engaged in significant technology initiatives and expects to continue to do so in the future. Such initiatives are not only necessary to better meet the needs of the Partnership’s clients, but also to satisfy new industry standards and practices and better secure the transmission of clients’ information on the Partnership’s systems. With any major system replacement, there will be a period of education and adjustment for the branch and home office employees utilizing the system. Following any upgrade or replacement, if the Partnership’s systems or equipment does not operate properly, is disabled or fails to perform due to increased demand (which might occur during market upswings or downturns), or if a new system or system upgrade contains a major problem, the Partnership could experience unanticipated disruptions in service, including interrupted trading, slower response times, decreased client service and client satisfaction and delays in the introduction of new products and services, any of which could result in financial losses, liability to clients, regulatory intervention or reputational damage. Further, the inability of the Partnership’s systems to accommodate a significant increase in volume of transactions also could constrain its ability to expand its business.

24

PART I

Item | 1A. Risk Factors, continued |

INTEREST RATE ENVIRONMENT —The Partnership’s profitability is impacted by the low interest rate environment.

The current low interest rate environment adversely impacts the interest income the Partnership earns from clients’ margin loans, the investment of excess funds, and securities the Partnership owns, as well as the fees earned by the Partnership through its minority ownership in the investment adviser to the Edward Jones money market funds. And, while the low interest rate environment positively impacts the Partnership’s expenses related to liabilities that finance certain assets, such as amounts payable to clients and other interest-bearing liabilities, its interest bearing liabilities are less impacted by short-term interest rates compared to its interest earning assets, resulting in interest income being more sensitive to the current low interest rate environment than interest expense.

CREDIT RISK —The Partnership is subject to credit risk due to the nature of the transactions it processes for its clients.

The Partnership is exposed to the risk that third parties who owe it money, securities or other assets will not meet their obligations. Many of the transactions in which the Partnership engages expose it to credit risk in the event of default by its counterparty or client, such as cash balances held at various major U.S. financial institutions, which typically exceed Federal Deposit Insurance Corporation insurance coverage limits. In addition, the Partnership’s credit risk may be increased when the collateral it holds cannot be realized or is liquidated at prices insufficient to recover the full amount of the obligation due to the Partnership. See Item 7 – Management’s Discussion and Analysis of Financial Condition and Results of Operations, for more information about the Partnership’s credit risk.

LACKOF CAPITAL PERMANENCY — Because the Partnership’s capital is subject to mandatory liquidation either upon the death or withdrawal request of a partner, the capital is not permanent and a significant mandatory liquidation could lead to a substantial reduction in the Partnership’s capital, which could, in turn, have a material adverse effect on the Partnership’s business.