Filed by Ares Capital Corporation

pursuant to Rule 425 under the Securities Act of 1933

and deemed filed under Rule 14a-12 of the Securities Exchange Act of 1934

Subject Company: American Capital, Ltd.

Commission File No. 814-00149

Ares Capital Corporation Strategic Acquisition of American Capital Investor Presentation November 22, 2016

Disclaimer The following slides contain “forward-looking” statements as that term is defined in Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended by the Private Securities Litigation Reform Act of 1995, including statements regarding the proposed transaction between American Capital Ltd. (“ACAS”) and Ares Capital Corporation (“ARCC”) pursuant to a merger between ACAS and ARCC. All statements, other than historical facts, including statements regarding the expected timing of the closing of the proposed transaction; the ability of the parties to complete the proposed transaction considering the various closing conditions; the expected benefits of the proposed transaction such as improved operations, enhanced revenues and cash flow, growth potential, market profile and financial strength; the competitive ability and position of the combined company following completion of the proposed transaction; and any assumptions underlying any of the foregoing, are forward-looking statements. Forward-looking statements concern future circumstances and results and other statements that are not historical facts and are sometimes identified by the words “may,” “will,” “should,” “potential,” “intend,” “expect,” “endeavor,” “seek,” “anticipate,” “estimate,” “overestimate,” “underestimate,” “believe,” “could,” “project,” “predict,” “continue,” “target” or other similar words or expressions. Forward-looking statements are based upon current plans, estimates and expectations that are subject to risks, uncertainties and assumptions. Should one or more of these risks or uncertainties materialize, or should underlying assumptions prove incorrect, actual results may vary materially from those indicated or anticipated by such forward-looking statements. The inclusion of such statements should not be regarded as a representation that such plans, estimates or expectations will be achieved. Important factors that could cause actual results to differ materially from such plans, estimates or expectations include, among others, (1) that one or more closing conditions to the transaction may not be satisfied or waived, on a timely basis or otherwise, including that a governmental entity may prohibit, delay or refuse to grant approval for the consummation of the proposed transaction, may require conditions, limitations or restrictions in connection with such approvals or that the required approval by the stockholders of each of ACAS and ARCC may not be obtained; (2) the risk that the mergers or other transactions contemplated by the ARCC/ACAS merger agreement may not be completed in the time frame expected by ACAS and ARCC, or at all; (3) unexpected costs, charges or expenses resulting from the proposed transaction; (4) uncertainty of the expected financial performance of the combined company following completion of the proposed transaction; (5) failure to realize the anticipated benefits of the proposed transaction, including as a result of delay in completing the proposed transaction or integrating the businesses of ACAS and ARCC; (6) the ability of the combined company to implement its business strategy; (7) difficulties and delays in achieving synergies and cost savings of the combined company; (8) inability to retain and hire key personnel; (9) the occurrence of any event that could give rise to termination of the ARCC/ACAS merger agreement; (10) the risk that stockholder litigation in connection with the proposed transaction may affect the timing or occurrence of the contemplated merger or result in significant costs of defense, indemnification and liability; (11) evolving legal, regulatory and tax regimes; (12) changes in laws or regulations or interpretations of current laws and regulations that would impact ARCC’s classification as a business development company; (13) changes in general economic and/or industry specific conditions; and (14) other risk factors as detailed from time to time in ACAS and ARCC’s reports filed with the SEC, including ACAS and ARCC’s respective annual reports on Form 10-K for the year ended December 31, 2015, periodic quarterly reports on Form 10-Q, periodic current reports on Form 8-K, the Joint Proxy Statement (as defined below), the Registration Statement (as defined below) and other documents filed with the SEC. Any forward-looking statements speak only as of the date of this communication. Neither ACAS nor ARCC undertakes any obligation to update any forward-looking statements, whether as a result of new information or development, future events or otherwise, except as required by law. Readers are cautioned not to place undue reliance on any of these forward-looking statements. The following slides contain summaries of certain financial and statistical information about ARCC and ACAS. The information contained in this presentation is summary information that is intended to be considered in the context of ARCC’s and ACAS SEC filings and other public announcements that ARCC may make, by press release or otherwise, from time to time. These materials contain information about ARCC and ACAS, information about their respective historical performance and general information about the market. In addition, information related to past performance, while helpful as an evaluation tool, is not necessarily indicative of future results and you should not view information related to the past performance of ARCC and ACAS or information about the market, as indicative of ARCC’s or ACAS future results or the potential future results of the combined company following the consummation of the Transaction. Further, performance information respecting investment returns on portfolio transactions is not directly equivalent to returns on an investment in ARCC’s common stock.

Disclaimer The following slides contain information in respect of each of ARCC and ACAS. Neither ARCC nor ACAS makes any representation or warranty, express or implied, with respect to the information contained herein (including, without limitation, information obtained from third parties) or the accuracy or completeness thereof, and expressly disclaim any and all liability based on or relating to the information contained in, or errors or omissions from, these materials; or based on or relating to the recipient’s use (or the use by any of its affiliates or representatives or any other person) of these materials; or based on any other written or oral communications transmitted to the recipient or any of its affiliates or representatives in the course of its evaluation of ARCC. ARCC undertakes no duty or obligation to update or revise the information contained in these materials. Although the companies signed a merger agreement as previously reported and filed with the SEC, the companies remain independent as of the date hereof. Certain information set forth herein includes preliminary estimates, projections and targets based on current assumptions and involves significant elements of subjective judgment and analysis. Such assumptions, estimates, projections and targets may change materially or may not be realized, and are not intended to be complete or constitute all of the information necessary to adequately evaluate ARCC or ACAS. NO OFFER OR SOLICITATION These materials are for informational purposes only and shall not constitute an offer to sell or the solicitation of an offer to sell or the solicitation of an offer to buy any securities or the solicitation of any vote or approval in any jurisdiction pursuant to or in connection with the proposed transaction or otherwise, nor shall there be any sale, issuance or transfer of securities in any jurisdiction in contravention of applicable law. No offer of securities shall be made except by means of a prospectus meeting the requirements of Section 10 of the Securities Act of 1933, as amended. ADDITIONAL INFORMATION AND WHERE TO FIND IT In connection with the proposed transaction, ARCC has filed with the Securities and Exchange Commission (the “SEC”) a registration statement on Form N-14 (the “Registration Statement”) that includes a joint proxy statement of ARCC and ACAS (the “Joint Proxy Statement”) and that constitutes a prospectus of ARCC. The Joint Proxy Statement and Registration Statement, as applicable, have been mailed or otherwise delivered to stockholders as required by applicable law. INVESTORS AND SECURITY HOLDERS ARE URGED TO READ THE JOINT PROXY STATEMENT AND THE REGISTRATION STATEMENT, AS WELL AS ANY AMENDMENTS OR SUPPLEMENTS TO THESE DOCUMENTS, CAREFULLY AND IN THEIR ENTIRETY BECAUSE THEY CONTAIN IMPORTANT INFORMATION ABOUT AMERICAN CAPITAL, ARES CAPITAL, THE PROPOSED TRANSACTION AND RELATED MATTERS. Investors and security holders may obtain the Joint Proxy Statement, the Registration Statement and other documents filed with the SEC by ACAS and ARCC, free of charge, from the SEC’s website at www.sec.gov and from either ACAS or ARCC’s websites at www.americancapital.com or at www.arescapitalcorp.com. Investors and security holders may also obtain free copies of the Joint Proxy Statement, the Registration Statement and other documents filed with the SEC from ACAS by contacting ACAS Investor Relations Department at 1-301-951-5917 or from ARCC by contacting ARCC’s Investor Relations Department at 1-888-818-5298. PARTICIPANTS IN THE SOLICITATION ACAS, ARCC and their respective directors, executive officers, other members of their management and employees may be deemed to be participants in the solicitation of proxies in connection with the proposed transaction. Information regarding the persons who may, under the rules of the SEC, be considered participants in the solicitation of the ARCC and ACAS stockholders in connection with the proposed transaction, and their direct or indirect interests, by security holdings or otherwise, is set forth in the Joint Proxy Statement and Registration Statement filed with the SEC. These documents may be obtained free of charge from the sources indicated above.

Investment Thesis for Transaction We believe this strategic acquisition will enhance ARCC’s position as the largest business development company(1) in the United States and a leading direct lender to U.S. middle market companies We believe that this acquisition will generate value for our stockholders Enhances Stockholder Value in Accretive Transaction: ARCC anticipates that the acquisition will be accretive to core earnings per share with the potential for increased dividends over time Improves Value Proposition to Our Clients: The combined company will offer an enhanced value proposition to financial sponsors and borrowers with the ability to originate and hold larger transactions Accelerates Growth of Potentially High Returning Lending Program: The combination may allow ARCC to accelerate the growth of its currently high yielding investment in the Senior Direct Lending Program and increase the target size of the investments made by the program Further Diversifies Our Portfolio: The acquisition will result in a more diversified portfolio across issuers and industries Improves Access to Capital Markets: With greater scale and diversification, we anticipate increased access to banks and capital market participants Creates Greater Fee Income Opportunities: The acquisition increases our balance sheet scale and potential for increased fee income from greater underwriting and distribution capabilities Significant Support from our External Advisor: In addition to the approximately $275 million in cash consideration at closing, Ares Capital Management LLC, the external manager of ARCC, is waiving up to $100 million in potential income-based fees for the ten calendar quarters beginning in the first full quarter after the acquisition Measured using total assets and market capitalization as of 9/30/16.

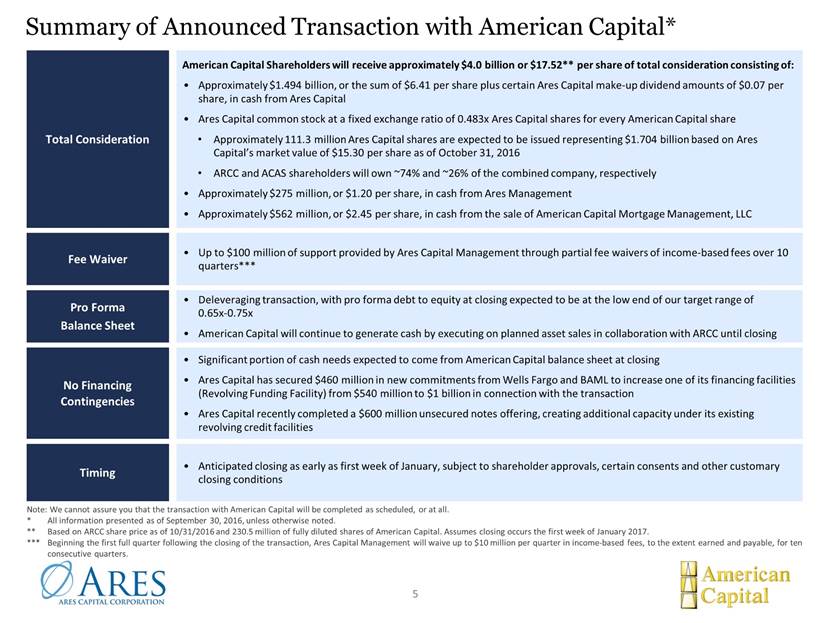

American Capital Shareholders will receive approximately $4.0 billion or $17.52** per share of total consideration consisting of: Approximately $1.494 billion, or the sum of $6.41 per share plus certain Ares Capital make-up dividend amounts of $0.07 per share, in cash from Ares Capital Ares Capital common stock at a fixed exchange ratio of 0.483x Ares Capital shares for every American Capital share Approximately 111.3 million Ares Capital shares are expected to be issued representing $1.704 billion based on Ares Capital’s market value of $15.30 per share as of October 31, 2016 ARCC and ACAS shareholders will own ~74% and ~26% of the combined company, respectively Approximately $275 million, or $1.20 per share, in cash from Ares Management Approximately $562 million, or $2.45 per share, in cash from the sale of American Capital Mortgage Management, LLC Total Consideration Up to $100 million of support provided by Ares Capital Management through partial fee waivers of income-based fees over 10 quarters*** Fee Waiver Deleveraging transaction, with pro forma debt to equity at closing expected to be at the low end of our target range of 0.65x-0.75x American Capital will continue to generate cash by executing on planned asset sales in collaboration with ARCC until closing Pro Forma Balance Sheet Significant portion of cash needs expected to come from American Capital balance sheet at closing Ares Capital has secured $460 million in new commitments from Wells Fargo and BAML to increase one of its financing facilities (Revolving Funding Facility) from $540 million to $1 billion in connection with the transaction Ares Capital recently completed a $600 million unsecured notes offering, creating additional capacity under its existing revolving credit facilities No Financing Contingencies Anticipated closing as early as first week of January, subject to shareholder approvals, certain consents and other customary closing conditions Timing Note: We cannot assure you that the transaction with American Capital will be completed as scheduled, or at all. * All information presented as of September 30, 2016, unless otherwise noted. ** Based on ARCC share price as of 10/31/2016 and 230.5 million of fully diluted shares of American Capital. Assumes closing occurs as early as the first week of January 2017. *** Beginning the first full quarter following the closing of the transaction, Ares Capital Management will waive up to $10 million per quarter in income-based fees, to the extent earned and payable, for ten consecutive quarters. Summary of Announced Transaction with American Capital*

Based on ARCC’s stock price of $15.30 per share as of 10/31/2016 at a fixed exchange ratio of 0.483x. $1.478 billion of cash from ARCC, excluding $16 million make-up dividend. Includes certain Ares Capital make-up dividend amounts of $16 million, assuming closing occurs the first week of January 2017. Approximately $275 million of cash from a subsidiary of Ares Management, L.P. Approximately $562 million in proceeds from the sale of American Capital Mortgage Manager. Calculated based on 230.5 million of fully diluted shares. Price at announcement represents ACAS share price of $15.62 as of close on 5/20/2016. Unaffected ACAS share price is based on the 11/13/2015 price of $14.31 prior to the Elliott Management shareholder proposal filed with SEC. Other factors may have contributed to the increase in share price since that time. Total Consideration Paid to ACAS Shareholders ACAS shareholders are currently expected to receive a premium to the price at announcement of the transaction and the unaffected share price 12.2% Premium to Price at Announcement (7) ACAS shareholders will also benefit from certain fee waivers provided by Ares Management 22.4% Premium to Unaffected Price (8) $13.87 per share from ARCC (6) (1) (2) (4) (5) Make-up Dividend from ARCC(3) $0.07 Offer per Share ACAS Share Price at 5/20/2016 Unaffected ACAS Share Price at 11/13/2015 $17.52 $15.62 $14.31 ARCC Stock $7.39 ARCC Cash $6.41 ARES Cash $1.20 Cash from ACMM $2.45

Transaction Updates Significant Progress Made with Asset Monetizations and Realizations and Junior Capital Reduced ACAS Balance Sheet Composition has De-risked with NAV Growth, All Debt Repaid and Cash Increased Significant Progress Toward Closing with Few Remaining Open Items As of 9/30/16. Assumes no changes to 9/30/16 fair value of investments for ARCC or ACAS, but includes ARCC’s estimated fair value adjustments for ACAS as shown on slide 15. From March 31, 2016 through September 30, 2016, ACAS has received cash proceeds from realizations and repayments of portfolio investments of ~$1.8 billion, with the proceeds used to reduce debt or build cash balances Includes the sale of American Capital Mortgage Manager for $562 million, with proceeds of $2.45 per share to be paid to ACAS shareholders at closing Over $600 million of these asset sales related to control equity positions excluding American Capital Mortgage Manager ACAS net asset value per share has increased by 6.3% since March 31, 2016(1) Balance sheet comprised of approximately $1.1 billion of cash with no debt(1) Pro forma debt to equity ratio of 0.70x,(1) with closing leverage expected to be at the low end of our target range of 0.65x-0.75x Stockholder approval at respective shareholder meetings (Meetings scheduled on December 15, 2016) Consents from certain investment funds managed by American Capital Asset Management and its subsidiaries representing at least 75% of aggregate AUM of all such funds Registration Statement and Joint Proxy Statement on Form N-14 declared effective Expiration of the waiting period under the Hart-Scott-Rodino Antitrust Act Sale of American Capital Mortgage Manager Approval from the Financial Conduct Authority in the United Kingdom and the Guernsey Financial Services Commission in Guernsey 9/30/16 Pro Forma Net Asset Value Significantly Improved and Further Progress Expected on Closing Net Asset Value The September 30, 2016 pro forma impact of the transaction to ARCC stand alone net asset value has significantly improved since the March 31, 2016 pro forma financials On a pro forma combined basis as of September 30, 2016, ARCC would have had a net asset value per share of $16.49 versus stand alone net asset value per share of $16.59, a difference of only 0.6%, and we believe that further progress is possible as ACAS continues to build retained earnings prior to closing(2) We continue to believe the transaction will ultimately be accretive to net asset value per share over time(2)

Update on ARCC’s Performance and Strategy Since transaction announcement, ARCC has continued to perform well and execute on its strategy in the following ways: 1 Generated strong Q2 and Q3 core EPS of $0.39 per share and $0.43 per share, respectively, both in excess of the $0.38 per share quarterly dividend 2 Successfully launched Senior Direct Lending Program with ~$3 billion of investment capacity(1) 3 Issued $600 million of investment grade notes at lowest coupon for such capital in ARCC and BDC history 4 Continued to originate attractive investment opportunities with more than $2 billion(2) of new commitments in the aggregate during Q2 and Q3, generating meaningful fee income 5 Substantial progress working with ACAS team to begin execution of portfolio rotation strategy The SDLP is capitalized as transactions are completed and all portfolio decisions and generally all other decisions in respect of the SDLP must be approved by an investment committee of the SDLP consisting of representatives of ARCC and Varagon (with approval from a representative of each required). Includes $0.2 billion investment as part of the initial funding of the subordinated certificates of the Senior Direct Lending Program in Q3-16.

Opportunities for Value Creation Total Investments: $8.8 billion (1) $11.8 billion $3.0 billion (2) We believe that the pro forma portfolio has multiple drivers of potential ROE expansion As of 9/30/2016. As of 9/30/2016, adjusted for actual exits/repayments of ACAS investments between 10/1/2016 and 10/31/2016 of $57 million at fair value, investments expected to be sold pursuant to contractual agreements as of 10/31/2016 of $74 million at fair value, as well as a reduction in fair value from purchase accounting adjustments of $167 million of ARCC’s estimates of fair value. As of 9/30/2016, the weighted average effective interest rate disclosed by ACAS on ACAS interest bearing investments was 9.6%. Please note that the ACAS yield calculation methodology may differ from ARCC. Pro forma combined portfolio includes $1.5 billion of portfolio rotation opportunity from legacy ACAS structured products, subordinated debt and equity portfolio 57.2% 48.4% 55.0% 2.2% 1.6% 21.6% 16.1% 8.2% 9.4% 8.5% 12.4% 3.2% 3.9% 3.7% 3.8% 6.9% 26.1% 11.8% 0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100% ARCC Adj. ACAS Pro Forma Senior Secured Debt SDLP SSLP Senior Subordinated Debt Structured Products Preferred Equity Other Equity

Pro Forma Company Benefits Enhanced Size and Liquidity Diversified Portfolio Potential Catalyst for Dividend Growth Total Equity ($B) Investment Portfolio ($B) (1) ARCC pro-forma shows opportunity for improvement in a number of key areas 215 Portfolio Companies 314 Portfolio Companies Key Drivers of Potential ROE Expansion(3) Increased Fee Income Increased Portfolio Yield Accelerated SDLP growth Near term fee waiver Cost savings opportunities Total pro forma investments as of 9/30/2016, adjusted for actual exits and repayments of ACAS investments between 10/1/2016 and 10/31/2016 of $57 million at fair value, investments expected to be sold pursuant to contractual agreements as of 10/31/2016 of $74 million at fair value, as well as a reduction in fair value from purchase accounting adjustments of $167 million of ARCC’s estimates of fair value. Core Earnings over the last twelve months over the average stockholders’ equity for the same period; Core Earnings is a non-GAAP financial measure which is the net increase in stockholders’ equity resulting from operations less professional fees and other costs related to the proposed acquisition of American Capital, realized & unrealized gains and losses, any capital gains incentive fees attributable to such net realized and unrealized gains and losses and any income taxes related to such realized gains and losses. There can be no assurance that any or all of these possibilities will be achieved. Return on Equity (2) Pro Forma Combined Company Pro Forma Combined Company 9.6% LTM 9/30 ARCC $8.8 $11.8 9/30 ARCC Pro Forma ARCC $5.2 $7.0 9/30 ARCC Pro Forma ARCC

Conclusion Since the transaction announcement, ACAS has made significant progress with portfolio monetizations and realizations while increasing its net asset value We expect to meet all closing conditions, subject to ARCC and ACAS stockholder approvals The difference between ARCC stand alone and pro forma net asset values has continued to improve since March 31, 2016(1) and we believe that further progress is possible as ACAS continues to build retained earnings prior to closing(2) We continue to expect the transaction to be accretive to core earnings per share as we reposition the ACAS portfolio, with the potential for increased dividends over time The ACAS balance sheet has been de-risked with no debt and approximately $1.1 billion of cash(1) As of 9/30/16. Assumes no changes to 9/30/16 fair value of investments for ARCC or ACAS, but includes ARCC’s estimated fair value adjustments for ACAS as shown on slide 15.

Appendix

Pro Forma Combined Balance Sheet – 9/30/2016 13 ($ in millions, except per share amounts) Actual Ares Capital Adjusted American Capital (A)* Pro Forma Adjustments Ares Capital Pro Forma Combined Assets and Liabilities Data: Investments, at fair value $ 8,805 $ 3,163 $ (167) [B] $ 11,801 Cash and cash equivalents 125 1,191 (679) [B] 204 (1,494) [C] 1,061 [D] Other assets 206 349 (267) [B] 297 9 [D] Total assets $ 9,136 $ 4,703 $ (1,537) $ 12,302 Debt $ 3,721 $ - $ 1,100 [D] $ 4,821 Other liabilities 206 124 112 [B] 467 (6) [D] 31 [E] Total liabilities $ 3,927 $ 124 $ 1,237 $ 5,288 Stockholders' equity 5,209 4,579 (1,225) [B] 7,014 (1,494) [C] (24) [D] (31) [E] Total liabilities and stockholders' equity $ 9,136 $ 4,703 $ (1,537) $ 12,302 Total shares outstanding 314.0 213.9 111.3 425.3 Net assets per share $ 16.59 $ 21.40 $ 16.49 Principal Debt / Equity (1) 0.73x 0.70x (1) Principal debt is $3,801 million for ARCC and $4,901 million for ARCC Pro Forma Combined as of 9/30/2016. * Please see endnotes to pro forma condensed consolidated financial statements

Endnotes ($ in millions, except per share amounts) To reflect American Capital’s balance sheet as of September 30, 2016, updated for estimated changes subsequent to September 30, 2016: Includes actual exits and repayments of investments occurring between October 1, 2016 and October 31, 2016 of $57 at fair value (total proceeds of $58). Also includes investments expected to be sold pursuant to contractual agreements as of October 31, 2016 of $74 at fair value (total proceeds of $75). Ares Capital and American Capital cannot assure you that American Capital will sell all or any portion of these investments. Includes proceeds received from 0.1 million stock options exercised from October 1, 2016 through October 31, 2016, totaling $1. Actual American Capital September 30, 2016 Pro Forma Adjustments Adjusted American Capital September 30, 2016 Investments, at fair value $3,294 ($131) (1) $3,163 Cash and cash equivalents 1,057 134 (1)(2) 1,191 Other assets 349 - 349 Total assets $4,700 $3 $4,703 Debt $- $- $- Other liabilities 124 - 124 Total liabilities $124 $0 $124 Net assets 4,576 3 (1)(2) 4,579 Total liabilities and net assets $4,700 $3 $4,703

Endnotes ($ in millions, except per share amounts) To reflect the acquisition of American Capital by the issuance of approximately 111.3 million shares of Ares Capital common stock. The table below reflects the allocation of the purchase price on the basis of Ares Capital’s estimate of the fair value of assets acquired and liabilities assumed: Primarily to reflect the allocation of the purchase price to American Capital’s assets and liabilities based on Ares Capital’s estimates of fair value. There is no single approach for determining fair value in good faith. As a result, determining fair value requires that judgment be applied to the specific facts and circumstances of each portfolio investment while employing a consistently applied valuation process. The adjustment to other liabilities includes an adjustment to record a liability for the estimated loss on future lease payments of $40. In addition to the net effect of the fair value adjustments to American Capital’s assets and liabilities, the net assets of American Capital were decreased for various transaction costs expected to be incurred by American Capital of approximately $185, including $68 of other liabilities expected to be paid within the 36 months following the completion of the mergers. Pursuant to the merger agreement, in connection with the Mortgage Manager Sale, American Capital stockholders will receive a distribution equal to approximately $562. Based on ARCC share price as of 10/31/16 and 230.5 million of fully diluted shares of American Capital. Includes $16 related to certain make-up dividend amounts paid by Ares Capital pursuant to the merger agreement. ($ in millions, except per share amounts) Adjusted American Capital September 30, 2016 Pro Forma Adjustments Pro Forma September 30, 2016 Common stock issued $1,704 Cash consideration paid 1,494 Deemed contribution from Ares Capital Management 156 Total purchase price $3,354 Assets acquired: Investments, at fair value $3,163 ($167) (1) $2,996 Cash and cash equivalents 1,191 (679) (2)(3) 512 Deferred tax asset 256 (256) (1) — Other assets 93 (11) (1) 82 Total assets acquired $4,703 ($1,113) $3,590 Other liabilities assumed (124) (112) (1)(2) (236) Net assets acquired $4,579 ($1,225) $3,354 (4) (5)

Endnotes ($ in millions, except per share amounts) The net assets of the pro forma combined company were decreased for the cash consideration paid by Ares Capital to American Capital stockholders of approximately $6.41 per fully diluted share plus certain Ares Capital dividend makeup amounts of $0.07 per share, or approximately $1,494. The pro forma adjustment to cash and cash equivalents primarily reflects draws under Ares Capital’s revolving credit facilities with the cash proceeds used to fund the various net cash requirements of Ares Capital related to the mergers, including certain costs expected to be incurred by Ares Capital related to the mergers. For the purposes of these unaudited pro forma condensed consolidated financial statements, it is assumed that Ares Capital’s Revolving Funding Facility is amended and upsized from its current committed amount of $540 to $1,000 as contemplated by the Debt Commitment Letter (as defined in the merger agreement). The net assets of the pro forma combined company were decreased by $24 to reflect various other costs expected to be incurred by Ares Capital in connection with the mergers. U.S. generally accepted accounting principles (“GAAP”) require that Ares Capital consider the cumulative aggregate unrealized appreciation in determining the capital gains incentive fee accrued under GAAP, as a capital gains incentive fee would be payable if such unrealized capital appreciation were realized, even though such unrealized capital appreciation is not permitted to be considered in calculating the fee actually payable under the investment advisory and management agreement. Ares Capital is also required by GAAP to record an investment at its fair value as of the time of acquisition instead of at the actual amount paid for such investment by Ares Capital (including, for example, as a result of the application of the acquisition method of accounting). As a result, solely for the purposes of calculating the capital gains incentive fee, the “accreted or amortized cost basis” of an investment shall be an amount (the “Contractual Cost Basis”) equal to (1)(x) the actual amount paid by Ares Capital for such investment plus (y) any amounts recorded in Ares Capital’s financial statements as required by GAAP that are attributable to the accretion of such investment plus (z) any other adjustments made to the cost basis included in Ares Capital’s financial statements, including PIK interest or additional amounts funded (net of repayments) minus (2) any amounts recorded in Ares Capital’s financial statements as required by GAAP that are attributable to the amortization of such investment, whether such calculated Contractual Cost Basis is higher or lower than the fair value of such investment (as determined in accordance with GAAP) at the time of acquisition. In accordance with the above, the pro forma adjustments as of September 30, 2016 include $31 for the capital gains incentive fees accrued in accordance with GAAP but do not reflect amounts that would actually be payable under the investment advisory and management agreement as such amounts would only be included in the contractual calculation when such related investments are ultimately realized.