Exhibit 13

Annual Report to Stockholders

| At Or For The Year Ended March 31, | ||||||||||

| 2010 | 2009 | 2008 | 2007 | 2006 | ||||||

| Balance Sheet Data | (Dollars In Thousands, Except Per Share Data) | |||||||||

| Total Assets | $ | 956,002 | $ | 984,662 | $ | 840,030 | $ | 738,110 | $ | 658,678 |

| Cash And Cash Equivalents | 8,805 | 6,562 | 10,539 | 13,438 | 14,351 | |||||

| Investment And Mortgage-Backed Securities | 311,046 | 314,099 | 264,312 | 249,905 | 238,433 | |||||

Total Loans Receivable, Net (1) | 568,399 | 611,090 | 517,932 | 436,038 | 375,109 | |||||

| Deposits | 694,252 | 661,714 | 590,850 | 523,738 | 479,229 | |||||

| Advances From Federal Home Loan Bank | 164,004 | 218,998 | 178,234 | 153,049 | 131,363 | |||||

| Total Shareholders' Equity | 67,861 | 67,092 | 47,496 | 42,693 | 37,602 | |||||

| Income Data | ||||||||||

| Total Interest Income | 47,507 | 48,867 | 49,632 | 42,098 | 32,617 | |||||

| Total Interest Expense | 20,136 | 26,321 | 29,544 | 23,933 | 15,969 | |||||

| Net Interest Income | 27,371 | 22,546 | 20,088 | 18,165 | 16,648 | |||||

| Provision For Loan Losses | 8,155 | 2,825 | 895 | 600 | 660 | |||||

| Net Interest Income After Provision For Loan Losses | 19,216 | 19,721 | 19,193 | 17,565 | 15,988 | |||||

| Non-Interest Income | 6,071 | 4,496 | 4,489 | 3,861 | 2,630 | |||||

| General And Administrative Expense | 22,622 | 20,499 | 17,322 | 15,157 | 13,027 | |||||

| Income Taxes | 1,060 | 1,265 | 2,080 | 2,142 | 1,778 | |||||

| Net Income | 1,605 | 2,453 | 4,280 | 4,127 | 3,813 | |||||

| Preferred Stock Dividends | 900 | 252 | - | - | - | |||||

| Accretion Of Preferred Stock To Redemption Value | 73 | 20 | - | - | - | |||||

| Net Income Available to Common Shareholders | $ | 632 | $ | 2,181 | $ | 4,280 | $ | 4,127 | $ | 3,813 |

| Per Common Share Data | ||||||||||

| Net Income Per Common Share (Basic) | $ | 0.26 | $ | 0.87 | $ | 1.66 | $ | 1.59 | $ | 1.51 |

| Cash Dividends Declared | $ | 0.32 | $ | 0.32 | $ | 0.28 | $ | 0.24 | $ | 0.16 |

| Other Data | ||||||||||

| Interest Rate Spread Information: | ||||||||||

| Average During Period | 2.83% | 2.45% | 2.44% | 2.47% | 2.52% | |||||

| End Of Period | 3.21% | 2.58% | 2.14% | 2.51% | 2.59% | |||||

Net Interest Margin (Net Interest Income/Average Earning Assets) | 2.98% | 2.63% | 2.69% | 2.76% | 2.79% | |||||

Average Interest-Earning Assets To Average Interest- Bearing Liabilities | 106.64% | 105.80% | 106.30% | 108.00% | 110.25% | |||||

| Common Equity To Total Assets | 5.21% | 4.98% | 5.65% | 5.78% | 5.71% | |||||

Non-Performing Assets To Total Assets (2) | 4.39% | 1.51% | 0.81% | 0.15% | 0.20% | |||||

Return On Assets (Ratio Of Net Income To Average Total Assets) | 0.06% | 0.24% | 0.54% | 0.59% | 0.62% | |||||

Return On Common Equity (Ratio Of Net Income To Average Common Equity) | 1.27% | 4.72% | 9.54% | 10.24% | 10.27% | |||||

Common Equity To Assets Ratio (Ratio Of Average Common Equity To Average Total Assets) | 5.09% | 5.10% | 5.66% | 5.78% | 6.03% | |||||

Dividend Pay-Out Ratio On Common Shares(3) | 124.56% | 36.59% | 16.90% | 15.11% | 10.67% | |||||

| Number Of Full-Service Offices | 13 | 13 | 13 | 11 | 11 | |||||

| (1) | INCLUDES LOANS HELD FOR SALE. |

| (2) | NON-PERFORMING ASSETS CONSIST OF NON-ACCRUAL LOANS AND REPOSSESSED ASSETS. |

| (3) | RATIO OF DIVIDENDS PAID ON COMMON SHARES TO NET INCOME AVAILABLE TO COMMON SHAREHOLDERS |

7

SECURITY FEDERAL CORPORATION AND SUBSIDIARIES

Management’s Discussion and Analysis of Financial Condition and Results of Operations

General

The following discussion is presented to provide the reader with an understanding of the financial condition and the results of operations of Security Federal Corporation and its subsidiaries. The investment and other activities of the parent company, Security Federal Corporation (the “Company”), have had no significant impact on the results of operations for the periods presented in the financial statements. The information presented in the following discussion of financial results is indicative of the activities of Security Federal Bank (“Bank”), a wholly owned subsidiary of the Company. The Bank is a federally chartered stock savings bank that was founded in 1922. The Bank also has two wholly owned subsidiaries: Security Federal Insurance Inc. (“SFINS”) and Security Financial Services Corporation (“SFSC”). SFINS was formed in the fiscal year ended March 31, 2002 and began operating during the December 2001 quarter. SFINS is an insurance agency offering auto, business, health, and home insurance. SFINS has a wholly owned subsidiary, Collier Jennings Financial Corporation (“Collier Jennings”), which has three wholly owned subsidiaries Security Federal Auto Insurance, The Auto Insurance Store Inc., and Security Federal Premium Pay Plans Inc. SFSC was formed in 1975 and is currently inactive. In addition to the Bank, Security Federal Corporation has another wholly owned subsidiary, Security Federal Statutory Trust (the “Trust”), which issued and sold fixed and floating rate capital securities of the Trust. Under current accounting guidance, however, the Trust is not consolidated in the Company’s financial statements. Unless the context indicates otherwise, references to the Company shall include the Bank and its subsidiaries.

Prior to April 1, 2009, the Bank had two additional subsidiaries: Security Federal Investments, Inc. (“SFINV”) and Security Federal Trust Inc. (“SFT”). SFINV provided primarily investment brokerage services. SFT offered trust, financial planning and financial management services. On April 1, 2009, the assets and operations of SFINV and SFT were dissolved into the Bank. The services of these two entities are now offered through the trust and investment divisions of the Bank.

The principal business of the Bank is accepting deposits from the general public and originating consumer and commercial business loans as well as mortgage loans that enable borrowers to purchase or refinance one-to-four family residential real estate. The Bank also originates construction loans on single-family residences, multi-family dwellings and projects, and commercial real estate, as well as loans for the acquisition, development and construction of residential subdivisions, and commercial projects.

The Bank's net income is dependent on its interest rate spread which is the difference between the average yield earned on its loan and investment portfolios and the average rate paid on its deposits and borrowings. The Bank’s interest spread is influenced by interest rates, deposit flows, and loan demands. Levels of non-interest income and operating expense are also significant factors in earnings.

Forward-Looking Statements

This document, including information included or incorporated by reference, contents, and future filings by the Company on Form 10-K, Form 10-Q, and Form 8-K, and future oral and written statements by the Company and its management may contain forward-looking statements about the Company and its subsidiaries which we believe are within the meaning of the Private Securities Litigation Reform Act of 1995. Forward-looking statements often include the words “believes,” “expects,” “anticipates,” “estimates,” “forecasts,” “intends,” “plans,” “targets,” “potentially,” “probably,” “projects,” “outlook” or similar expressions or future or conditional verbs such as “may,” “will,” “should,” “would” and “could.” These forward-looking statements are subject to known and unknown risks, uncertainties and other factors that could cause actual results to differ materially from the results anticipated, including, but not limited to:

| · | the credit risks of lending activities, including changes in the level and trend of loan delinquencies and write-offs and changes in our allowance for loan losses and provision for loan losses that may be impacted by deterioration in the housing and commercial real estate markets; |

| · | changes in general economic conditions, either nationally or in our market areas; |

| · | changes in the levels of general interest rates, and the relative differences between short and long term interest rates, deposit interest rates, our net interest margin and funding sources; |

| · | fluctuations in the demand for loans, the number of unsold homes, land and other properties and fluctuations in real |

| · | estate values in our market areas; |

8

SECURITY FEDERAL CORPORATION AND SUBSIDIARIES

Management’s Discussion and Analysis of Financial Condition and Results of Operations

Forward-Looking Statements, Continued

| · | results of examinations of us by the Office of Thrift Supervision (the “OTS”) or the FDIC or other regulatory authorities, including the possibility that any such regulatory authority may, among other things, require us to increase our reserve for loan losses, write-down assets, change our regulatory capital position or affect our ability to borrow funds or maintain or increase deposits, which could adversely affect our liquidity and earnings; |

| · | legislative or regulatory changes that adversely affect our business including changes in regulatory policies and principles, or the interpretation of regulatory capital or other rules; |

| · | further increases in premiums for deposit insurance; |

| · | our ability to control operating costs and expenses; |

| · | the use of estimates in determining fair value of certain of our assets, which estimates may prove to be incorrect and result in significant declines in valuation; |

| · | difficulties in reducing risk associated with the loans on our balance sheet; |

| · | staffing fluctuations in response to product demand or the implementation of corporate strategies that affect our workforce and potential associated charges; |

| · | computer systems on which we depend could fail or experience a security breach; |

| · | our ability to retain key members of our senior management team; |

| · | costs and effects of litigation, including settlements and judgments; |

| · | our ability to implement our branch expansion strategy; |

| · | our ability to successfully integrate any assets, liabilities, customers, systems, and management personnel we have acquired or may in the future acquire into our operations and our ability to realize related revenue synergies and cost savings within expected time frames and any goodwill charges related thereto; |

| · | changes in premiums or claims that adversely affect our insurance segment; |

| · | increased competitive pressures among financial services companies; |

| · | changes in consumer spending, borrowing and savings habits; |

| · | the availability of resources to address changes in laws, rules, or regulations or to respond to regulatory actions; |

| · | our ability to pay dividends on our common stock; |

| · | adverse changes in the securities markets; |

| · | inability of key third-party providers to perform their obligations to us; |

| · | changes in accounting policies and practices, as may be adopted by the financial institution regulatory agencies or the Financial Accounting Standards Board, including additional guidance and interpretation on accounting issues and details of the implementation of new accounting methods; |

| · | future legislative changes in the TARP Capital Purchase Program; and |

| · | other economic, competitive, governmental, regulatory, and technological factors affecting our operations, pricing, products and services and the other risks described elsewhere in this document. |

9

SECURITY FEDERAL CORPORATION AND SUBSIDIARIES

Management’s Discussion and Analysis of Financial Condition and Results of Operations

Forward-Looking Statements, Contined

Some of these and other factors are discussed in our Annual Report on Form 10-K for the year ended March 31, 2010 under the Item 1A, “Risk Factors.” Such developments could have an adverse impact on our financial position and our results of operations.

Any forward-looking statements are based upon management’s beliefs and assumptions at the time they are made. We undertake no obligation to publicly update or revise any forward-looking statements included or incorporated by reference in this document or to update the reasons why actual results could differ from those contained in such statements, whether as a result of new information, future events or otherwise. In light of these risks, uncertainties and assumptions, the forward-looking statements discussed in this document might not occur, and you should not put undue reliance on any forward-looking statements.

Critical Accounting Policies

The Company has adopted various accounting policies which govern the application of accounting principles generally accepted in the United States in the preparation of the Company’s financial statements. The significant accounting policies of the Company are described in Note 1 of the Notes to the Consolidated Financial Statements included herein.

Certain accounting policies involve significant judgments and assumptions by management, which have a material impact on the carrying value of certain assets and liabilities; management considers these accounting policies to be critical accounting policies. The judgments and assumptions used by management are based on historical experience and other factors, which are believed to be reasonable under the circumstances. Because of the nature of the judgments and assumptions made by management, actual results could differ from these judgments and estimates, which could have a material impact on the carrying values of assets and liabilities and the results of operations of the Company.

Of these significant accounting policies, the Company considers its policies regarding the allowance for loan losses to be its most critical accounting policy because of the significant degree of management judgment involved in determining the amount of allowance for loan losses. The Company has developed policies and procedures for assessing the adequacy of the allowance for loan losses, and recognizes that this process requires a number of assumptions and estimates with respect to its loan portfolio. The Company’s assessments may be impacted in future periods by changes in economic conditions, the impact of regulatory examinations, and the discovery of information with respect to borrowers, which is not known to management at the time of the issuance of the consolidated financial statements. For a further discussion of the Company’s estimation process and methodology related to the allowance for loan losses, see the discussion under the section entitled “Comparison of the Years Ended March 31, 2010 and 2009 - Financial Condition” and “-Provision for Loan Losses” and “Comparison of the Years Ended March 31, 2009 and 2008- Financial Condition– Financial Condition” and “-Provision for Loan Losses” included herein.

Asset and Liability Management

The Bank’s program of asset and liability management seeks to limit the Bank’s vulnerability to material and prolonged increases or decreases in interest rates, or "interest rate risk." The principal determinant of the exposure of the Bank's earnings to interest rate risk is the timing difference (“gap”) between the repricing or maturity of the Bank's interest-earning assets and the repricing or maturity of its interest-bearing liabilities. If the maturities of the Bank's assets and liabilities were perfectly matched and the interest rates borne by its assets and liabilities were equally flexible and moved concurrently (neither of which is the case), the impact on net interest income of any material and prolonged changes in interest rates would be minimal.

A positive gap position generally has an adverse effect on net interest income during periods of falling interest rates. A positive one-year gap position occurs when the dollar amount of rate sensitive assets maturing or repricing within one year exceeds the dollar amount of rate sensitive liabilities maturing or repricing during that same one-year period. As a result, in a period of falling interest rates, the interest received on interest-earning assets will increase slower than the interest paid on interest-bearing liabilities, causing a decrease in net interest income. During periods of rising interest rates, the interest received on interest-earning assets will increase faster than interest paid on interest-bearing liabilities, thus increasing net interest income.

A negative gap position generally has an adverse effect on net interest income during periods of rising interest rates. A negative one-year gap position occurs when the dollar amount of rate sensitive liabilities maturing or repricing within one year exceeds the dollar amount of rate sensitive assets maturing or repricing during that same period. As a result, during periods of rising interest rates, the interest paid on interest-bearing liabilities will increase faster than interest received from interest-earning assets, thus reducing net interest income. The reverse is true in periods of declining interest rates, as discussed above, which generally results in an increase in net interest income.

10

SECURITY FEDERAL CORPORATION AND SUBSIDIARIES

Management’s Discussion and Analysis of Financial Condition and Results of Operations

Asset and Liability Management, Continued

The Bank’s Board of Directors reviews the Interest Rate Exposure Report generated for the Bank by the Office of Thrift Supervision (“OTS”). This report measures the interest rate sensitivity of the Bank’s net portfolio value (“NPV”) on a quarterly basis under different interest rate scenarios. The Bank’s sensitivity measure is well within the Bank’s policy on changes in NPV. The Bank's asset and liability policies are directed toward maximizing long-term profitability while managing acceptable interest rate risk within the Bank’s policies.

At March 31, 2010, the negative mismatch of interest-earning assets repricing or maturing within one year with interest-bearing liabilities repricing or maturing within one year was ($7.4) million or (0.8)% of total assets compared to ($9.5) million or (1.0)% at March 31, 2009. For more information on the Bank’s repricing position at March 31, 2010, see the tables on pages 11 and 12.

During the year ended March 31, 2010, the Bank originated, for investment purposes, $27.6 million in adjustable rate residential real estate loans (“ARM’s”), which are held for investment and are not sold. The Bank’s loan portfolio included $264.1 million of adjustable rate consumer loans, commercial loans, and mortgage loans or, 45.0% of total gross loans at March 31, 2010. During fiscal 2010, the Bank originated $308.7 million in consumer and commercial loans, which are usually short term in nature. The Bank's portfolio of consumer and commercial loans was $465.1 million at March 31, 2010, $494.5 million at March 31, 2009, and $400.2 million at March 31, 2008. Consumer and commercial loans combined were 79.3% of total loans at March 31, 2010, 78.8% of total loans at March 31, 2009, and 74.9% at March 31, 2008.

At March 31, 2010, the Bank held approximately $6.6 million in longer term fixed rate residential mortgage loans. These loans, which amounted to 1.2% of the total loan portfolio, had converted from ARM loans to fixed rate loans during the previous 60 months. These fixed rate loans have remaining maturities ranging from 10 to 30 years. As of March 31, 2010, the Bank no longer had any ARM loans that have conversion features to fixed rate loans. On new originations, the Bank sells virtually all of its 15 and 30 year fixed rate mortgage loans at origination. Fixed rate residential loans sold to Freddie Mac and other institutional investors, on a service-released basis totaled $67.8 million in fiscal 2010, $45.3 million in fiscal 2009, and $38.9 million in fiscal 2008. The Bank sells all its fixed rate mortgage loans on a service-release basis.

Certificates of deposit of $100,000 or more, referred to as “Jumbo Certificates,” are normally considered to be interest rate sensitive because of their relatively short maturities. At March 31, 2010, the Bank had $195.9 million outstanding in Jumbo Certificates compared to $192.8 million at March 31, 2009. Brokered deposits totaled $34.4 million at March 31, 2010 compared to $25.4 million at March 31, 2009. The majority of the Bank’s deposits are originated within the Bank’s immediate market area.

The following table sets forth the maturity schedule of certificates of deposit with balances of $100,000 or greater at March 31, 2010:

| At March 31, 2010 | ||||

| (In Thousands) | ||||

| Within 3 Months | $ | 34,335 | ||

| After 3 Months, Within 6 Months | 54,773 | |||

| After 6 Months, Within 12 Months | 54,758 | |||

| After 12 Months | 51,994 | |||

| $ | 195,860 | |||

11

SECURITY FEDERAL CORPORATION AND SUBSIDIARIES

Management’s Discussion and Analysis of Financial Condition and Results of Operations

Asset and Liability Management, Continued

The following table sets forth the Bank’s interest-bearing liabilities and interest-earning assets repricing or maturing within one year. The table on the following page presents the Bank's entire interest-bearing liabilities and interest-earning assets into repricing or maturity time periods. Both tables present adjustable rate loans in the periods they are scheduled to reprice and fixed rate loans are shown in the time frame of corresponding principal amortization schedules. Adjustable and fixed rate loans are also adjusted for the Company’s estimates of pre-payments. Mortgage-backed securities are shown at repricing dates, but also include prepayment estimates. Both tables also assume investments reprice at the earlier of maturity; the likely call date, if any, based on current interest rates; or the next scheduled interest rate change, if any. NOW accounts are assumed to have a decay rate of 20% the first year, money market accounts to have a decay rate of 65% the first year, and statement savings accounts to have a decay rate of 20% the first year. The balance, for all three products, is deemed to reprice in the one to three year category. Callable fixed rate Federal Home Loan Bank (“FHLB”) advances are included in borrowings, and are deemed to mature at the expected call date or maturity, based on the stated interest rate of the advance and current market rates. Junior subordinated debentures are shown at their repricing date or call date.

| At March 31 | ||||

| 2010 | 2009 | |||

| (Dollars In Thousands) | ||||

Loans (1) | $ | 402,832 | $ | 408,858 |

| Mortgage-Backed Securities: | ||||

| Held To Maturity | 871 | 7,200 | ||

| Available For Sale | 36,890 | 134,792 | ||

| Investment Securities: | ||||

| Held To Maturity | 3,117 | 4,965 | ||

| Available For Sale | 21,339 | 12,373 | ||

| Other Interest-Earning Assets And FHLB Stock | 12,791 | 12,791 | ||

| Total Interest Rate Sensitive Assets Repricing Within 1 Year | $ | 477,840 | $ | 580,979 |

| Deposits | $ | 439,474 | $ | 470,784 |

| FHLB Advances And Other Borrowed Money | 45,738 | 119,713 | ||

| Total Interest Rate Sensitive Liabilities Repricing Within 1 Year | $ | 485,212 | $ | 590,497 |

| Gap | $ | (7,372) | $ | (9,518) |

| Interest Rate Sensitive Assets/Interest Rate Sensitive Liabilities | 98.48% | 98.39% | ||

| Gap As A Percent Of Total Assets | (0.8)% | (1.0)% | ||

| (1) | LOANS ARE NET OF UNDISBURSED FUNDS AND LOANS IN PROCESS. |

12

SECURITY FEDERAL CORPORATION AND SUBSIDIARIES

Management’s Discussion and Analysis of Financial Condition and Results of Operations

Asset and Liability Management, Continued

The following table sets forth the interest rate sensitivity of the Bank's assets and liabilities at March 31, 2010, on the basis of the factors and assumptions set forth in the table on the previous page.

Less Than Three Months | Over 3 –12 Months | Over 1 – 3 Years | Over 3 – 5 Years | Over 5 – 10 Years | Over 10 Years | Total | ||||||||

| (Dollars In Thousands) | ||||||||||||||

| Interest-Earnings Assets | ||||||||||||||

Loans (1) | $ | 250,391 | $ | 152,441 | $ | 115,368 | $ | 52,177 | $ | 8,420 | $ | 2,060 | $ | 580,857 |

| Mortgage-Backed Securities: | ||||||||||||||

| Held To Maturity, At Cost | 147 | 724 | 2,066 | 3,012 | 3,564 | 636 | 10,149 | |||||||

Available For Sale, At Fair Value | 9,278 | 27,612 | 110,430 | 53,911 | 29,237 | 1,767 | 232,235 | |||||||

Investment Securities: (2) | ||||||||||||||

| Held To Maturity, At Cost | 1,078 | 2,039 | 2,566 | 2,020 | 774 | 159 | 8,636 | |||||||

Available For Sale, At Fair Value | 7,071 | 14,268 | 15,736 | 12,910 | 7,872 | 2,169 | 60,026 | |||||||

| FHLB Stock, At Cost | - | 12,624 | - | - | - | - | 12,624 | |||||||

| Other Interest-Earning Assets | 167 | - | - | - | - | - | 167 | |||||||

| Total Interest-Earning Assets | $ | 268,132 | $ | 209,708 | $ | 246,166 | $ | 124,030 | $ | 49,867 | $ | 6,791 | $ | 904,694 |

| Interest-Bearing Liabilities | ||||||||||||||

| Deposits: | ||||||||||||||

| Certificate Accounts | $ | 72,908 | $ | 236,405 | $ | 66,418 | $ | 16,539 | $ | - | $ | - | $ | 392,270 |

| NOW Accounts | 3,331 | 9,993 | 53,298 | - | - | - | 66,622 | |||||||

| Money Market Accounts | 27,825 | 85,213 | 60,867 | - | - | - | 173,905 | |||||||

| Statement Savings Account | 950 | 2,849 | 15,193 | - | - | - | 18,992 | |||||||

Borrowings (2) | 30,738 | 15,000 | 47,277 | 35,304 | 52,900 | 6,084 | 187,303 | |||||||

Total Interest-Bearing Liabilities | $ | 135,752 | $ | 349,460 | $ | 243,053 | $ | 51,843 | $ | 52,900 | $ | 6,084 | $ | 839,092 |

| Current Period Gap | $ | 132,380 | $ | (139,752) | $ | 3,113 | $ | 72,187 | $ | (3,033) | $ | 707 | $ | 65,602 |

| Cumulative Gap | $ | 132,380 | $ | (7,372) | $ | (4,259) | $ | 67,928 | $ | 64,895 | $ | 65,602 | $ | 65,602 |

| Cumulative Gap As A Percent Of Total Assets | 13.8% | (0.8)% | (0.5)% | 7.1% | 6.8% | 6.9% | 6.9% | ||||||||

| (1) | LOANS ARE NET OF UNDISBURSED FUNDS AND LOANS IN PROCESS. |

| (2) | CALLABLE SECURITIES AND FHLB ADVANCES ARE SHOWN AT THEIR LIKELY CALL DATES BASED ON MANAGEMENT’S ESTIMATES AT MARCH 31, 2010. |

In evaluating the Bank's exposure to interest rate risk, certain shortcomings inherent in the method of analysis presented in the foregoing tables must be considered. For example, although certain assets and liabilities may have similar maturities or periods of repricing, they may react in different degrees to changes in market interest rates. Additionally, the interest rates of certain types of assets and liabilities may fluctuate in advance of changes in market interest rates. Loan repayment rates and withdrawals of deposits will likely differ substantially from the assumed rates previously set forth in the event of significant changes in interest rates due to the option of borrowers to prepay their loans and the ability of depositors to withdraw funds prior to maturity. Further, certain assets, such as ARMs, have features that restrict changes in interest rates on a short-term basis as well as over the life of the asset.

Financial Condition

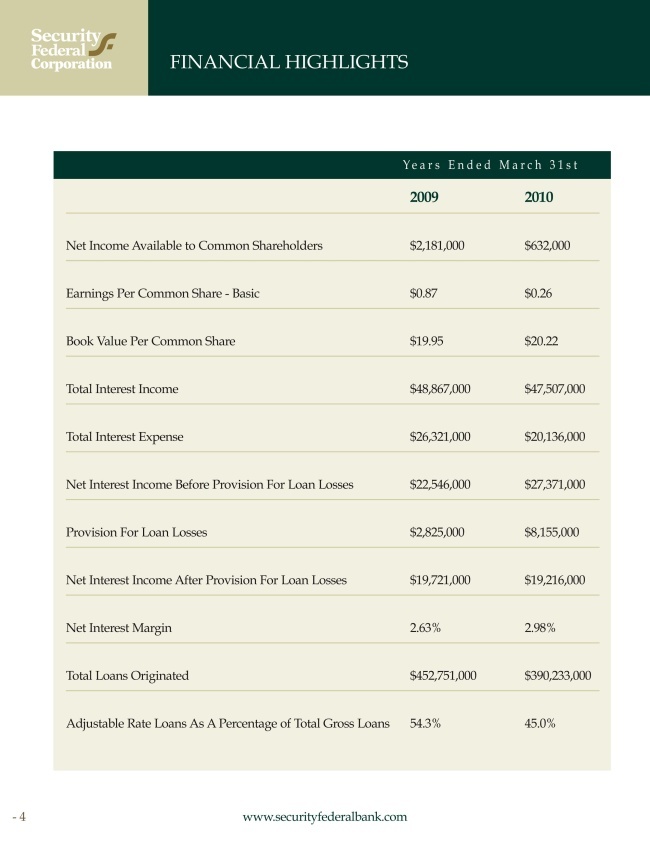

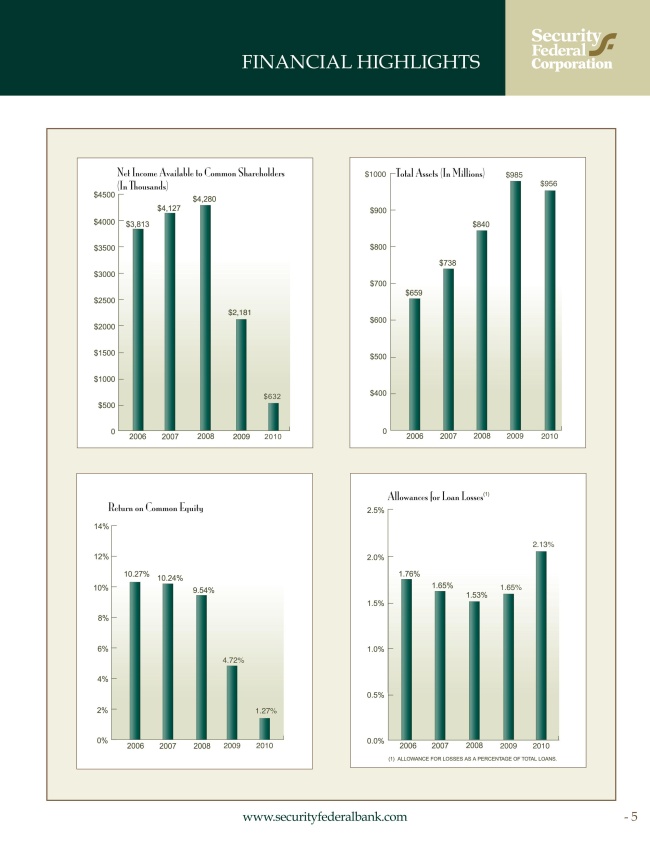

Total assets at March 31, 2010 were $956.0 million, a decrease of $28.7 million or 2.9% from $984.7 million at March 31, 2009. This decrease was primarily the result of a decrease in net loans receivable and a decrease in held to maturity securities.

13

SECURITY FEDERAL CORPORATION AND SUBSIDIARIES

Management’s Discussion and Analysis of Financial Condition and Results of Operations

Financial Condition, Continued

Total net loans receivable were $568.4 million at March 31, 2010, a decrease of $42.7 million or 7.0% from $611.1 million at March 31, 2009. Residential real estate loans held for investment decreased $8.7 million or 6.9% to $118.3 million at March 31, 2010. Typically, long term, newly originated fixed rate mortgage loans are not retained in the portfolio but are sold immediately. ARMs are typically retained in the portfolio. At March 31, 2010, the Bank held 90.5% of its residential mortgage loans in ARMs, while it had 9.5% in fixed rate mortgages. Consumer loans decreased $499,000 or 0.7% while commercial business and commercial real estate loans decreased $28.9 million or 6.8% to $396.5 million at fiscal year end March 31, 2010 from $425.4 million at March 31, 2009. Loans held for sale, which were $3.2 million at March 31, 2010, decreased $2.6 million from $5.7 million from the previous fiscal year end. The decrease in loans is the result of increased interest rates, tightened underwriting standards and a general decrease in loan demand. Total investments and mortgage-backed securities decreased $3.1 million or 1.0% to $311.0 million at March 31, 2010. Cash and cash equivalents were $8.8 million at March 31, 2010 compared to $6.6 million at March 31, 2009. Premises and equipment decreased $955,000 or 4.4% to $20.7 million in fiscal 2010 as a result of normal annual depreciation of premises and equipment. The Bank did not undergo any significant construction or renovation projects during the year ended March 31, 2010. The cash value of Bank Owned Life Insurance (“BOLI”) was $10.0 million at March 31, 2010 compared to $9.6 million at March 31, 2009 reflecting a $360,000 increase as a result of accumulated BOLI earnings. There were no additional BOLI purchases during the fiscal year ended March 31, 2010. BOLI, which earns tax-free yields, is utilized to partially offset the cost of the Company’s employee benefits programs and provide key person insurance on certain officers of the Company.

The Company’s non-performing assets increased $27.1 million to $42.0 million at March 31, 2010 from $14.9 million at March 31, 2009. The increase was primarily concentrated in non-performing commercial real estate loans which increased $17.4 million to $25.5 million at March 31, 2010 from $8.0 million at March 31, 2009. The balance in non-performing commercial real estate loans consisted of 58 loans to 29 borrowers with an average loan balance of $439,000. The following table sets forth detailed information concerning our non-performing assets for the periods indicated:

| At March 31, 2010 | At March 31, 2009 | $ Increase | % Increase | |||||||||||||||||||||

| Amount | Percent (1) | Amount | Percent (1) | (Decrease) | (Decrease) | |||||||||||||||||||

| Loans 90 days or more past due or non-accrual loans: | ||||||||||||||||||||||||

Residential real estate | $ | 4,344,060 | 0.8 | % | $ | 1,112,023 | 0.2 | % | $ | 3,232,037 | 290.6 | |||||||||||||

| Commercial business | 699,182 | 0.1 | 2,808,080 | 0.5 | (2,108,898 | ) | (75.1 | ) | ||||||||||||||||

| Commercial real estate | 25,479,420 | 4.4 | 8,044,372 | 1.3 | 17,435,048 | 216.7 | ||||||||||||||||||

| Consumer | 703,288 | 0.1 | 955,683 | 0.1 | (252,395 | ) | (26.4 | ) | ||||||||||||||||

Total non-performing loans | 31,225,950 | 5.4 | 12,920,158 | 2.1 | 18,305,792 | 141.7 | ||||||||||||||||||

| Other non-performing assets | ||||||||||||||||||||||||

Repossessed assets | 43,106 | 0.0 | 61,126 | 0.0 | (18,020 | ) | (29.5 | ) | ||||||||||||||||

Real estate owned | 10,729,944 | 1.9 | 1,924,046 | 0.3 | 8,805,898 | 457.7 | ||||||||||||||||||

Total other non-performing assets | 10,773,050 | 1.9 | 1,985,172 | 0.3 | 8,787,878 | 442.7 | ||||||||||||||||||

| Total non-performing assets | $ | 41,999,000 | 7.3 | % | $ | 14,905,330 | 2.4 | % | $ | 27,093,670 | 181.8 | % | ||||||||||||

| Total non-performing assets as a percentage of total assets | 4.4 | % | 1.5 | % | ||||||||||||||||||||

(1) Percent of gross loans receivable, net of deferred fees and loans in process and loans held for sale

A majority of the non-performing commercial real estate category, or $11.4 million consisted of 15 loans secured by commercial buildings to 12 separate borrowers. Of this amount, eight loans totaling $4.0 million were secured by buildings located in the Midlands area of South Carolina; three loans totaling $356,000 were secured by buildings located in Aiken, South Carolina; one loan for $5.5 million was secured by a building located in Charleston, South Carolina; one loan for $622,000 was secured by a building in Florida; one loan for $938,000 was secured by a building in Hardeeville, South Carolina; and one loan for $11,000 was secured by a building in North Augusta, South Carolina.

Of the remaining commercial real estate category $9.3 million was concentrated in construction loans and land acquisition and development type loans (“A&D loans”).

14

SECURITY FEDERAL CORPORATION AND SUBSIDIARIES

Management’s Discussion and Analysis of Financial Condition and Results of Operations

Financial Condition, Continued

The balance consisted of $6.3 million in A&D loans to three separate borrowers for the development of residential subdivisions in the Midlands area of South Carolina and $3.0 million in loans to 14 separate borrowers secured by builder lots or speculative houses in varying degrees of completion throughout South Carolina. The remaining loans in the commercial real estate category were secured by first mortgages on principal residences or raw land.

The Company also experienced an increase in non-performing one- to four- family real estate loans which increased $3.2 million to $4.3 million at March 31, 2010 from $1.1 million at March 31, 2009. At March 31, 2010, this balance was comprised of 16 loans with an average balance of $272,000. The increase in non-performing one- to four- family real estate loans is a result of the general deteriorating conditions in the local economy including rising unemployment rates and declining housing prices.

Repossessed assets acquired in settlement of loans increased $8.8 million to $10.8 million at March 31, 2010 from $2.0 million at March 31, 2009. The Company foreclosed on 25 real estate properties during the year ended March 31, 2010 and sold 10 properties. At March 31, 2010, the balance consisted of the following 29 real estate properties: 13 single-family residences located throughout our market area in South Carolina and Georgia; three lots within two subdivisions of Aiken, South Carolina and approximately 17 acres of land in Aiken, South Carolina; one mobile home including small acreage in Lexington County, South Carolina and five mobile homes and small acreage in Aiken, South Carolina; one commercial building in Aiken, South Carolina and two commercial buildings in Augusta, Georgia; a condominium development in Atlanta, Georgia that was originally acquired as a participation loan from another financial institution; a 55 lot subdivision development and adjacent 17 acres of land in Columbia, South Carolina; and 34.8 acres of land in Blufton, South Carolina also originally acquired as a participation loan from another financial institution. In addition to the properties listed above, the balance also included $43,000 in various other repossessed assets that were not real estate.

The Bank reviews its loan portfolio and allowance for loan losses on a monthly basis. Future additions to the Bank's allowance for loan losses are dependent on, among other things, the performance of the Bank's loan portfolio, the economy, changes in real estate values, and interest rates. There can be no assurance that additions to the allowance will not be required in future periods. The determination of the appropriate level of the allowance for loan losses inherently involves a high degree of subjectivity and requires us to make significant estimates of current credit risks and future trends, all of which may undergo material changes. Continuing deterioration in economic conditions affecting borrowers, new information regarding existing loans, identification of additional problem loans and other factors, both within and outside of our control, may require an increase in the allowance for loan losses. In addition, bank regulatory agencies periodically review our allowance for loan losses and may require an increase in the provision for possible loan losses or the recognition of further loan charge-offs, based on judgments different than those of management. In addition, if charge-offs in future periods exceed the allowance for loan losses, we will need additional provisions to increase the allowance for loan losses. Any increases in the allowance for loan losses will result in a decrease in net income and, possibly, capital, and may have a material adverse effect on our financial condition and results of operations. Management continually monitors its loan portfolio for the impact of local economic changes. The ratio of allowance for loan losses to total loans was 2.13% at March 31, 2010 compared to 1.65% at March 31, 2009. The Bank continues to practice conservative lending and past due loans are monitored closely.

The cumulative interest not accrued during the year ended March 31, 2010 relating to all non-performing loans totaled $665,000. Our strategy is to work with our borrowers to reach acceptable payment plans while protecting our interests in the existing collateral. In the event an acceptable arrangement cannot be reached, we may have to acquire these properties through foreclosure or other means and subsequently sell, develop, or liquidate them.

The balance of loans in troubled debt restructurings decreased during the year ended March 31, 2010. The Bank had five loans that were troubled debt restructurings totaling $336,000 at March 31, 2010 compared to seven loans totaling $652,000 at March 31, 2009. The five troubled debt restructurings consisted of four consumer loans secured by first mortgages on residential dwellings totaling $163,000, and one commercial loan secured by a first mortgage on land totaling $174,000. None of the troubled debt restructurings were delinquent at March 31, 2010. All troubled debt restructurings are reviewed for impairment. At March 31, 2010, the Bank held $35.3 million in impaired loans compared to $27.7 million at March 31, 2009. The Bank had specific reserves totaling $2.0 million related to $10.9 million in impaired loans at March 31, 2010 compared to $1.9 million in specific reserves related to $6.0 million in impaired loans at March 31, 2009.

In July 2006, the Company acquired Collier Jennings Financial Corporation, an insurance agency specializing in consumer automobile insurance and premium financing.

15

SECURITY FEDERAL CORPORATION AND SUBSIDIARIES

Management’s Discussion and Analysis of Financial Condition and Results of Operations

Financial Condition, Continued

The resulting goodwill and other intangibles were $1.2 million and $250,000, respectively at March 31, 2010; and $1.4 million and $353,000 at March 31, 2009, respectively. Collier Jennings is now a subsidiary of Security Federal Insurance Inc.

Deposits at the Bank increased $32.5 million or 4.9% to $694.3 million at March 31, 2010 from $661.7 million at March 31, 2009. The Bank had brokered time deposits of $34.4 million at March 31, 2010 compared to $25.4 million at March 31, 2009. Brokered time deposit were appealing because rates paid on these deposits were typically significantly lower than rates paid on time deposits obtained in the Bank’s primary market areas. Total deposits, excluding brokered time deposits, increased $23.5 million or 3.7%. Brokered time deposits were 5.0% of total deposits at March 31, 2010 and 3.8% of total deposits at March 31, 2009.

Advances from the FHLB decreased $55.5 million or 25.1% to $164.0 million at March 31, 2010 from $219.0 million a year earlier. Other borrowed money, which consists of retail repurchase agreements, term auction facility borrowings from the Federal Reserve Bank, and a line of credit with another financial institution, decreased $14.0 million or 53.7% to $12.1 million at March 31, 2010 from $26.1 million at March 31, 2009. The Company issued its first trust preferred security issuance in September 2006. Gross proceeds of the issuance were $5.2 million and are classified as junior subordinated debentures on the Consolidated Balance Sheet included in the Consolidated Financial Statements contained herein. In December 2009, the Company issued $6.1 million in convertible senior debentures. The debentures will mature on December 1, 2029 and accrue interest at the rate of 8.0% per annum until maturity or earlier redemption or repayment. The debentures are convertible into the Company’s common stock at a conversion price of $20 per share at the option of the holder at any time prior to maturity.

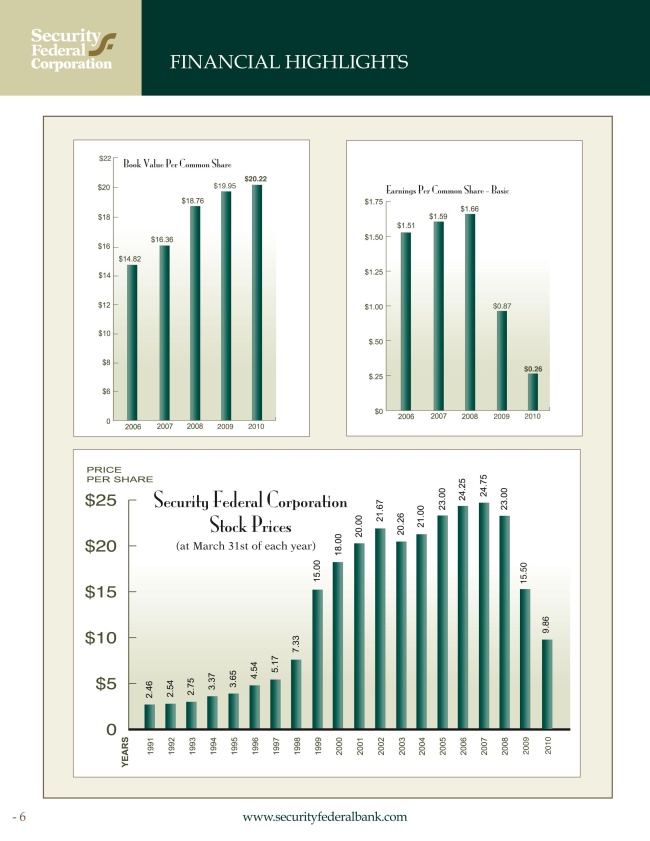

Total shareholders' equity was $67.9 million at March 31, 2010, an increase of $768,000 or 1.2% from $67.1 million a year earlier. The Company’s net income for the year was $1.6 million. Preferred stock dividends were $900,000 and accretion of preferred stock to its redemption value was $73,000 for the year resulting in net income available to common shareholders of $632,000. Other changes in shareholders’ equity were: proceeds from employee stock purchase plan purchases of $20,000, stock compensation expense of $33,000, and a net increase in other comprehensive income of $798,000, offset partially by $788,000 in dividends paid to common shareholders.

16

SECURITY FEDERAL CORPORATION AND SUBSIDIARIES

Management’s Discussion and Analysis of Financial Condition and Results of Operations

Results of Operations

The following table presents the dollar amount of changes in interest income and interest expense for major components of interest-earning assets and interest-bearing liabilities. The table also distinguishes between the changes related to higher or lower outstanding balances and the changes related to the volatility of interest rates. For each category of interest-earning assets and interest-bearing liabilities, information is provided on changes attributable to: (1) changes in rate (changes in rate multiplied by prior year volume); (2) changes in volume (changes in volume multiplied by prior year rate); and (3) net change (the sum of the prior columns). For purposes of this table, changes attributable to both rate and volume, which cannot be segregated, have been allocated proportionately to the change attributable to volume and the change attributable to rate.

| Fiscal Year 2010 Compared To 2009 | Fiscal Year 2009 Compared To 2008 | |||||||||||

| Volume | Rate | Net | Volume | Rate | Net | |||||||

| (In Thousands) | ||||||||||||

| Interest-Earning Assets: | ||||||||||||

Loans: (1) | ||||||||||||

| Mortgage Loans | $ | (340) | $ | (556) | $ | (896) | $ | 204 | $ | (390) | $ | (186) |

| Other Loans | 1,985 | (2,180) | (195) | 6,204 | (7,161) | (957) | ||||||

| Total Loans | 1,645 | (2,736) | (1,091) | 6,408 | (7,551) | (1,143) | ||||||

Mortgage-Backed Securities (2) | 1,239 | (1,074) | 165 | 3,538 | 87 | 3,625 | ||||||

Investments (2) | 348 | (773) | (425) | (2,481) | (716) | (3,197) | ||||||

| Other Interest-Earning Assets | (3) | (6) | (9) | 20 | (70) | (50) | ||||||

| Total Interest-Earning Assets | $ | 3,229 | $ | (4,589) | $ | (1,360) | $ | 7,485 | $ | (8,250) | $ | (765) |

| Interest-Bearing Liabilities: | ||||||||||||

| Deposits: | ||||||||||||

| Certificate Accounts | $ | 1,295 | $ | (4,883) | $ | (3,588) | $ | 2,431 | $ | (3,074) | $ | (643) |

| NOW Accounts | 16 | (132) | (116) | (8) | (532) | (540) | ||||||

| Money Market Accounts | 392 | (1,479) | (1,087) | (22) | (1,954) | (1,976) | ||||||

| Savings Accounts | 9 | (46) | (37) | (1) | (45) | (46) | ||||||

| Total Deposits | 1,712 | (6,540) | (4,828) | 2,400 | (5,605) | (3,205) | ||||||

| Borrowings | (225) | (1,132) | (1,357) | 2,150 | (2,168) | (18) | ||||||

| Total Interest-Bearing Liabilities | 1,487 | (7,672) | (6,185) | 4,550 | (7,773) | (3,223) | ||||||

| Effect On Net Income | $ | 1,742 | $ | 3,083 | $ | 4,825 | $ | 2,935 | $ | (477) | $ | 2,458 |

| (1) | INTEREST ON NON-ACCRUAL LOANS IS NOT INCLUDED IN INCOME, ALTHOUGH THEIR LOAN BALANCES ARE INCLUDED IN AVERAGE LOANS OUTSTANDING. |

| (2) | SECURITIES AVAILABLE FOR SALE ARE COMPUTED USING THEIR HISTORICAL COST. |

17

SECURITY FEDERAL CORPORATION AND SUBSIDIARIES

Management’s Discussion and Analysis of Financial Condition and Results of Operations

Results of Operations, Continued

The following table presents the total dollar amount of interest income from average interest-earning assets for the periods indicated and the resultant yields, as well as the interest expense on average interest-bearing liabilities expressed both in dollars and rates. No tax equivalent adjustments were made.

Yield/ Rate At March 31, 2010 | Averages For Fiscal Years Ended March 31, | ||||||||||||||||||

| 2010 | 2009 | 2008 | |||||||||||||||||

| Average Balance | Interest | Yield/ Rate | Average Balance | Interest | Yield/ Rate | Average Balance | Interest | Yield/ Rate | |||||||||||

| (Dollars In Thousands) | |||||||||||||||||||

| Interest-Earning Assets: | |||||||||||||||||||

| Mortgage Loans | 5.57% | $ | 121,311 | $ | 6,675 | 5.50% | $ | 127,205 | $ | 7,571 | 5.95% | $ | 123,893 | $ | 7,757 | 6.26% | |||

| Other Loans | 6.19% | 476,667 | 27,725 | 5.82% | 443,589 | 27,920 | 6.29% | 356,994 | 28,877 | 8.09% | |||||||||

Total Loans (1) | 6.06% | 597,978 | 34,400 | 5.75% | 570,794 | 35,491 | 6.22% | 480,887 | 36,634 | 7.62% | |||||||||

Mortgage-Backed Securities (2) | 4.14% | 245,173 | 10,603 | 4.32% | 217,989 | 10,438 | 4.79% | 144,041 | 6,813 | 4.73% | |||||||||

Investments (2) | 3.51% | 74,845 | 2,503 | 3.34% | 66,280 | 2,928 | 4.42% | 120,544 | 6,125 | 5.08% | |||||||||

Other Interest- Earning Assets | 0.01% | 1,261 | 1 | 0.07% | 2,378 | 10 | 0.42% | 1,619 | 60 | 3.71% | |||||||||

Total Interest-Earning Assets | 5.32% | $ | 919,257 | $ | 47,507 | 5.17% | $ | 857,441 | $ | 48,867 | 5.70% | $ | 747,091 | $ | 49,632 | 6.64% | |||

| Interest-Bearing Liabilities: | |||||||||||||||||||

| Certificate Accounts | 2.15% | $ | 383,769 | $ | 10,537 | 2.75% | $ | 349,161 | $ | 14,125 | 4.05% | $ | 295,424 | $ | 14,768 | 5.00% | |||

| NOW Accounts | 0.20% | 64,722 | 158 | 0.24% | 60,930 | 274 | 0.45% | 61,534 | 814 | 1.32% | |||||||||

Money Market Accounts | 1.28% | 161,663 | 2,429 | 1.50% | 143,110 | 3,516 | 2.46% | 143,695 | 5,492 | 3.82% | |||||||||

| Savings Accounts | 0.39% | 17,440 | 76 | 0.44% | 16,107 | 113 | 0.70% | 16,195 | 159 | 0.98% | |||||||||

Total Interest-Bearing Accounts | 1.67% | 627,594 | 13,200 | 2.10% | 569,308 | 18,028 | 3.17% | 516,848 | 21,233 | 4.11% | |||||||||

| Other Borrowings | 0.80% | 41,749 | 249 | 0.60% | 14,758 | 387 | 2.62% | 10,171 | 334 | 3.29% | |||||||||

| Jr. Subordinated Debt | 4.42% | 5,155 | 239 | 4.64% | 5,155 | 290 | 5.64% | 5,155 | 362 | 7.03% | |||||||||

| Sr. Convertible Debt | 8.00% | 2,017 | 162 | 8.03% | - | - | - | - | - | - | |||||||||

| FHLB Advances | 3.71% | 185,499 | 6,286 | 3.39% | 221,204 | 7,616 | 3.44% | 170,606 | 7,615 | 4.46% | |||||||||

Total Interest-Bearing Liabilities | 2.11% | $ | 862,014 | $ | 20,136 | 2.34% | $ | 810,425 | $ | 26,321 | 3.25% | $ | 702,780 | $ | 29,544 | 4.20% | |||

| Net Interest Income | $ | 27,371 | $ | 22,546 | $ | 20,088 | |||||||||||||

| Interest Rate Spread | 3.21% | 2.83% | 2.45% | 2.44% | |||||||||||||||

Net Yield On Earning Assets | 2.98% | 2.63% | 2.69% | ||||||||||||||||

| (1) | INTEREST ON NON-ACCRUAL LOANS IS NOT INCLUDED IN INCOME, ALTHOUGH THEIR LOAN BALANCES ARE INCLUDED IN AVERAGE LOANS OUTSTANDING. |

| (2) | SECURITIES AVAILABLE FOR SALE ARE COMPUTED USING THEIR HISTORICAL COST. |

18

SECURITY FEDERAL CORPORATION AND SUBSIDIARIES

Management’s Discussion and Analysis of Financial Condition and Results of Operations

Comparison of the Years Ended March 31, 2010 and 2009

General

The Company’s earnings available to common shareholders were $632,000 for the year ended March 31, 2010, compared to $2.2 million for the year ended March 31, 2009. The $1.5 million or 71.0% decrease in earnings was attributable primarily to the increase in the allowance for loan losses through additional charges to the provision for loan losses coupled with an increase in general and administrative expenses attributable to increased FDIC insurance premiums. These factors were offset by an increase in the Company’s net interest margin.

Net Interest Income

Net interest margin for the year ended March 31, 2010 increased 35 basis points to 2.98% up from 2.63% in the previous year. As a result, net interest income increased $4.8 million or 21.4% to $27.4 million for the year ended March 31, 2010 compared to $22.6 million for the previous year. The increase was attributable to a decrease in interest expense offset in part by a decrease in interest income. Average interest-earning assets increased $61.8 million to $919.3 million while average interest-bearing liabilities increased $51.6 million to $862.0 million. The interest rate spread was 2.83% for the year ended March 31, 2010 compared to 2.45% for the year ended March 31, 2009.

Interest income on loans decreased $1.1 million to $34.4 million during the year ended March 31, 2010 from $35.5 million during fiscal 2009. The decrease was attributable to a 47 basis point decrease in the yield earned on the Bank’s loans during fiscal 2010 offset in part by an increase in average total loans outstanding of $27.2 million. Interest income on investment securities, mortgage-backed securities, and other investments decreased $269,000 as a result of an increase in the aggregate average balance in the overall investment portfolio, including mortgage-backed securities, investments, and other interest-earning assets of $34.6 million offset by a decrease in the yield.

Interest expense on deposits decreased $4.8 million or 26.8% to $13.2 million during the year ended March 31, 2010. Average interest bearing deposits increased $58.3 million while the average cost of those deposits decreased 107 basis points during the year ended March 31, 2010. Interest expense on FHLB advances and other borrowings decreased $1.5 million or 18.4% to $6.5 million during fiscal 2010. The decrease was a result of a decrease in average FHLB advances and other borrowings outstanding during fiscal 2010 of $8.7 million while the average costs of those borrowings decreased 51 basis points to 2.88% in fiscal 2010 compared to 3.39% in fiscal 2009. Interest expense on junior subordinated debentures was $239,000 for fiscal 2010 compared to $290,000 during fiscal 2009. The average outstanding balance on these debentures remained constant at $5.2 million during both periods while the average cost decreased 100 basis points to 4.64% in fiscal 2010 compared to 5.64% in fiscal 2009. Interest expense on senior convertible debentures was $162,000 and the average balance was $2.0 million. The senior convertible debentures were issued during fiscal 2010.

Provision for Loan Losses

The Company’s provision for loan losses increased $5.3 million to $8.2 million during the year ended March 31, 2010 from $2.8 million in fiscal 2009. The increase in the provision for loan losses reflected the Company’s concern for the condition of the local and national economy coupled with an increase in non-performing assets. Non-accrual loans, which are loans delinquent 90 days or more, were $31.2 million at March 31, 2010 compared to $12.9 million at March 31, 2009. Non-performing assets, which include non-accrual loans and repossessed assets, increased $27.1 million to $42.0 million at March 31, 2010 from $14.9 million at March 31, 2009. Non-performing assets were 4.4% of total assets at March 31, 2010 and 1.5% of total assets at March 31, 2009. Net charge-offs were $6.0 million or 1.04% of gross loans in fiscal 2010 compared to $710,000 or 0.11% of gross loans in fiscal 2009. Management of the Bank continues to be concerned about current market conditions and closely monitors the loan portfolio on an on-going basis to proactively identify any potential problem loans.

The amount of the provision is determined by management’s on-going monthly analysis of the loan portfolio. Management uses multiple methods to measure the estimate of the adequacy of the allowance for loan losses. These methods incorporate the percentage of classified loans, averages of historical loan losses in each loan category and current economic trends, and the assignment of percentage targets of reserves in each loan category. The Company considers subjective factors such as changes in local and national economic conditions, industry trends, the composition and volume of the loan portfolio, credit concentrations, lending policies, and the experience and ability of the staff, management, and the Board of Directors.

19

SECURITY FEDERAL CORPORATION AND SUBSIDIARIES

Management’s Discussion and Analysis of Financial Condition and Results of Operations

Provision for Loan Losses, Continued

Management believes the allowance for loan losses is adequate based on its best estimates of the losses inherent in the loan portfolio, although there can be no guarantee as to these estimates. In addition, bank regulatory agencies may require additional provisions to the allowance for loan losses based on their judgments and estimates as part of their examination process. Because the allowance for loan losses is an estimate, there can be no guarantee that actual loan losses would not exceed the allowance for loan losses, or that additional increases in the allowance for loan losses will not be required in the future.

Non-Interest Income

Non-interest income increased $1.6 million to $6.1 million during fiscal 2010. Gain on sale of investments increased $1.1 million to $1.2 million during fiscal 2010 from $127,000 during fiscal 2009. Gain on sale of loans increased $412,000 to $1.0 million during fiscal 2010 compared to $628,000 during fiscal 2009 as a result of an increase in the origination and sale of fixed rate residential mortgage loans. Service fees on deposit accounts increased $88,000 or 7.7% to $1.2 million during fiscal 2010.

Income from insurance agency commissions was $457,000 during fiscal 2010 compared to $625,000 during fiscal 2009. Other agency income from Collier Jennings increased $138,000 to $472,000 during fiscal 2010 from $334,000 during fiscal 2009 as a result of growth and expansion of the Bank’s insurance subsidiary. Trust income increased $24,000 or 5.6% to $455,000 during fiscal 2010. Income from BOLI increased $2,000 or 0.4% to $360,000 during fiscal year 2010. Other miscellaneous income including annuity and investment brokerage commissions, Bank credit life insurance on loans, and other miscellaneous income decreased $7,000 or 0.8% to $843,000 during fiscal 2010. In 2010 SFINS incurred a $401,000 loss compared to a $281,000 loss in 2009. These losses are partially as a result of the continued integration of Collier Jennings. In addition, the Company sold the South Augusta office of its insurance subsidiary during the first quarter of the 2010 fiscal year. This resulted in the loss of premium income associated with this location when compared to the prior year.

General and Administrative Expenses

General and administrative expenses increased $2.1 million or 10.4% to $22.6 million during the year ended March 31, 2010 compared to $20.5 million during the same period one year earlier. The increase is primarily the result of an increase in FDIC insurance premiums incurred during the period. For the year ended March 31, 2010, the Company expensed $1.8 million in FDIC insurance premiums, an increase of $1.1 million or 153.8% from $724,000 for the prior year. The majority of the increase was the result of a one time special assessment and additional provisions imposed by the FDIC on all FDIC insured deposit institutions to help replenish the government’s Deposit Insurance Fund.

Compensation and employee benefits increased $166,000 or 1.4% to $11.8 million as the result of annual cost of living salary adjustments offset by a decrease in the number of employees employed by the Company. Occupancy expense increased $15,000 or 0.8% to $2.0 million. Depreciation and maintenance of equipment expense increased $151,000 or 9.3% to $1.8 million. Advertising expense decreased $138,000 or 25.4% from $542,000 to $404,000 as a result of the Company’s efforts to reduce expenses during the year.

Mandatorily redeemable financial instrument valuation expense was $63,000 for the year ended March 31, 2010 compared to $183,000 for the same period one year earlier. Based on its terms, the mandatorily redeemable financial instrument is redeemable at the greater of $26 per share or one and a half times the book value per common share of the Company which equated to $30.33 at March 31, 2010. The Company recorded a valuation expense to properly reflect the fair value of the instrument at March 31, 2010 based on the book value.

Other miscellaneous expenses, which encompasses repossessed assets expense, legal, professional, and consulting expenses, stationery and office supplies, and other expenses increased $935,000 or 28.5% during fiscal 2010. This increase is a result of fees associated with the Company’s senior convertible debt offering combined with costs required to insure compliance with increased regulation and legislation that is present in the current environment. Other expenses also include increased real estate owned expenses and increased expenses associated with loan collection and workout efforts.

Income Taxes

The provision for income taxes decreased $204,000 or 16.2% to $1.1 million during the year ended March 31, 2010 compared to $1.3 million for the year ended March 31, 2009. The effective tax rate was 39.8% for fiscal 2010 and 34.0% for fiscal 2009.

20

SECURITY FEDERAL CORPORATION AND SUBSIDIARIES

Management’s Discussion and Analysis of Financial Condition and Results of Operations

Comparison of the Years Ended March 31, 2009 and 2008

General

The Company’s earnings available to common shareholders were $2.2 million for the year ended March 31, 2009, compared to $4.3 million for the year ended March 31, 2008. The $2.1 million or 49.0% decrease in earnings was attributable primarily to compression of the net interest margin along with the Company’s decision to increase the provision for loan losses as a result of the weakening economy and increases in non-performing assets. These factors, in addition to an increase in general and administrative expenses attributable to costs associated with the Company’s recent expansion into two new market areas, were offset slightly by an increase in non-interest income.

Net Interest Income

The decline in interest rates during the year negatively impacted the Company’s net interest margin during the year ended March 31, 2009. This decrease combined with the Bank’s efforts to maintain competitive deposit rates within its primary market areas resulted in a six basis point decrease in net interest margin to 2.63% for the year ended March 31, 2009 compared to 2.69% in the previous year.

Despite the compression in the Company’s margin, net interest income increased $2.5 million or 12.2% to $22.6 million in fiscal 2009 from $20.1 million in fiscal 2008. The increase was attributable to a decrease in interest expense offset in part by a decrease in interest income. Average interest-earning assets increased $110.4 million to $857.4 million while average interest-bearing liabilities increased $107.6 million to $810.4 million. The interest rate spread was 2.45% for the year ended March 31, 2009.

Interest income on loans decreased $1.1 million to $35.5 million during the year ended March 31, 2009 from $36.6 million during fiscal 2008. The decrease was attributable to a 140 basis point decrease in the yield earned on the Bank’s loans during fiscal 2009 offset in part by an increase in average total loans outstanding of $89.9 million. Interest income on investment securities, mortgage-backed securities, and other investments increased $378,000 as a result of an increase in the aggregate average balance in the overall investment portfolio, including mortgage-backed securities, investments, and other interest-earning assets of $20.4 million offset by a decrease in the yield of 22 basis points.

Interest expense on deposits decreased $3.2 million or 15.1% to $18.0 million during the year ended March 31, 2009. Average interest bearing deposits increased $52.5 million while the average cost of those deposits decreased 94 basis points during the year. Interest expense on FHLB advances and other borrowings increased $55,000 or 0.7% to $8.0 million during fiscal 2009. The increase was a result of an increase in average FHLB advances and other borrowings outstanding during the year of $55.2 million while the average costs of those borrowings decreased 101 basis points to 3.39% in fiscal 2009 compared to 4.40% in fiscal 2008. Interest expense on junior subordinated debentures was $290,000 for fiscal 2009 compared to $362,000 during fiscal 2008. The average outstanding balance on these debentures remained constant at $5.2 million during both periods while the average cost decreased 139 basis points to 5.64% in fiscal 2009 compared to 7.03% in fiscal 2008.

Provision for Loan Losses

The Company’s provision for loan losses increased $1.9 million to $2.8 million during the year ended March 31, 2009 from $895,000 in fiscal 2008. The increase in the provision for loan losses reflected the Company’s concern for the condition of the local and national economy coupled with overall growth in its loan portfolio and an increase in non-performing assets. Non-accrual loans, which are loans delinquent 90 days or more, were $12.9 million at March 31, 2009 compared to $6.0 million at March 31, 2008. Non-performing assets, which include non-accrual loans and repossessed assets, increased $8.1 million to $14.9 million at March 31, 2009 from $6.8 million at March 31, 2008. Despite this increase, non-performing assets comprise less than 2% of total assets at March 31, 2009 and 2008. The Company also maintained relatively low and stable trends related to net charge-offs. Net charge-offs were $710,000 or 0.11% of gross loans in fiscal 2009 compared to $125,000 or 0.02% of gross loans in fiscal 2008. Management of the Bank continues to be concerned about current market conditions and closely monitors the loan portfolio on an on-going basis to proactively identify any potential problem loans.

Non-Interest Income

Non-interest income increased $7,000 to $4.5 million during fiscal 2009. Gain on sale of investments decreased $141,000 to $127,000 during fiscal 2009 from $268,000 during fiscal 2008. Gain on sale of loans increased $14,000 to $628,000 during fiscal 2009 compared to $613,000 during fiscal 2008 as a result of an increase in the origination and sale of fixed rate residential mortgage loans. Service fees on deposit accounts decreased $90,000 or 7.3% to $1.1 million during fiscal 2009.

21

SECURITY FEDERAL CORPORATION AND SUBSIDIARIES

Management’s Discussion and Analysis of Financial Condition and Results of Operations

Non-Interest Income, Continued

Income from insurance agency commissions was $625,000 during fiscal 2009 compared to $665,000 during fiscal 2008. Other agency income from Collier Jennings increased $236,000 to $334,000 during fiscal 2009 from $98,000 during fiscal 2008 as a result of growth and expansion of the Bank’s insurance subsidiary. Trust income decreased $12,000 or 2.6% to $431,000 during fiscal 2009 as a result of a decrease in the market value of the underlying trust accounts. The Bank earns trust fees as a percentage of the market value of each trust account.

Income from BOLI increased $31,000 or 9.6% to $358,000 during fiscal year 2009 as a result of an additional purchase of life insurance. Other miscellaneous income including annuity and investment brokerage commissions, Bank credit life insurance on loans, and other miscellaneous income increased $8,000 or 1.0% to $850,000 during fiscal 2009.

The Bank’s three financial subsidiaries, SFINS, SFINV, and SFT began operating in the third quarter of the fiscal year ended March 31, 2002. SFINS is an insurance agency handling property and casualty insurance and health insurance. In 2009 SFINS incurred a $281,000 loss compared to a $266,000 loss in 2008. These losses are partially as a result of the continued integration of Collier Jennings. In addition, changes in South Carolina insurance laws enacted during fiscal 2008 negatively impacted revenue in conjunction with a decrease in the commissions percentages earned from the insurance companies resulting from current market conditions and increased competition. SFINV markets mutual funds, discount brokerage, and annuities. SFT is a full-service trust company. SFINV and SFT had losses of $32,000 and $10,000, respectively, in fiscal 2009 and $18,000 and $77,000, respectively in 2008.

General and Administrative Expenses

General and administrative expenses increased $3.2 million or 18.3% to $20.5 million during the year ended March 31, 2009 compared to $17.3 million during the same period one year earlier. The largest increase was compensation and employee benefits which increased $1.4 million or 13.5% to $11.7 million. Occupancy expense increased $204,000 or 11.4% to $2.0 million. The majority of the increases in salary and employee benefits and occupancy are the result of hiring additional staff to handle the Company’s growth including expansion into the two new market areas of Richland County, South Carolina and Columbia County, Georgia. Annual cost of living salary adjustments contributed slightly to the increase in compensation and employee benefits as well. Depreciation and maintenance of equipment expense increased $280,000 or 20.7% to $1.6 million primarily as a result of the Company’s continued expansion and additional locations.

Advertising expense increased $162,000 or 42.7% from $380,000 to $542,000 as a result of the Company using more print media advertising to attract deposits specifically in its new market areas and to promote the Bank’s insurance subsidiary. FDIC insurance premiums increased $663,000 to $724,000 for fiscal 2009 from $62,000 in fiscal 2008. Previously, the Bank was benefiting from a one-time credit assessment made available by the Federal Deposit Insurance Reform Act of 2005. The credit assessment amount was applied to reduce the Bank’s quarterly deposit insurance assessments. The Bank exhausted this credit during the quarter ended June 30, 2008.

Mandatorily redeemable financial instrument valuation expense was $183,000 for the year ended March 31, 2009 compared to no expense for the same period one year earlier. Based on its terms, the mandatorily redeemable financial instrument is redeemable at the greater of $26 per share or one and a half times the book value per common share of the Company which equated to $29.35 at March 31, 2009. The Company recorded a valuation expense to properly reflect the fair value of the instrument at March 31, 2009 based on the book value.

Other miscellaneous expenses, which encompasses repossessed assets expense, legal, professional, and consulting expenses, stationery and office supplies, and other expenses increased $294,000 or 8.7% during fiscal 2009. This increase is attributable to general growth including maintaining additional employees and locations.

Income Taxes

The provision for income taxes decreased $815,000 or 39.2% to $1.3 million during the year ended March 31, 2009 compared to $2.1 million for the year ended March 31, 2008. The effective tax rate was 34.0% for fiscal 2009 and 32.7% for fiscal 2008.

22

SECURITY FEDERAL CORPORATION AND SUBSIDIARIES

Management’s Discussion and Analysis of Financial Condition and Results of Operations

Regulatory Capital

The following table reconciles the Bank's shareholders' equity to its various regulatory capital positions:

| At March 31, | ||||

| 2010 | 2009 | |||

| (In Thousands) | ||||

Bank’s Shareholders’ Equity (1) | $ | 71,729 | $ | 69,724 |

| Reduction For Goodwill And Other Intangibles | 1,449 | 1,774 | ||

| Tangible Capital | 70,280 | 67,950 | ||

| Core Capital | 70,280 | 67,950 | ||

| Supplemental Capital | 7,296 | 7,770 | ||

| Less Assets Required To Be Deducted | - | - | ||

| Total Risk-Based Capital | $ | 77,576 | $ | 75,720 |

| (1) | FOR FISCAL 2010 AND 2009, EXCLUDES UNREALIZED GAIN OF $4.6 MILLION and $3.8 MILLION RESPECTIVELY ON AVAILABLE FOR SALE SECURITIES. |

The following table compares the Bank's capital levels relative to regulatory requirements at March 31, 2010:

Amount Required | Percent Required | Actual Amount | Actual Percent | Excess Amount | Excess Percent | |||||||

| (Dollars In Thousands) | ||||||||||||

| Tangible Capital | $ | 18,993 | 2.0% | $ | 70,280 | 7.4% | $ | 51,287 | 5.4% | |||

| Tier 1 Leverage (Core) Capital | 37,987 | 4.0% | 70,280 | 7.4% | 32,293 | 3.4% | ||||||

| Tier 1 Risk-Based (Core) Capital | 23,274 | 4.0% | 70,280 | 12.1% | 47,006 | 8.1% | ||||||

| Total Risk-Based Capital | 46,548 | 8.0% | 77,576 | 13.3% | 31,028 | 5.3% | ||||||

23

SECURITY FEDERAL CORPORATION AND SUBSIDIARIES

Management’s Discussion and Analysis of Financial Condition and Results of Operations

Liquidity and Capital Resources

Liquidity refers to the ability to generate sufficient cash flows to fund current loan demand, repay maturing borrowings, fund maturing deposit withdrawals, and meet operating expenses. The Bank's primary sources of funds include loan repayments, loan sales, increased deposits, advances from the FHLB, and cash flow generated from operations. The need for funds varies among periods depending on funding needs as well as the rate of amortization and prepayment on loans. The use of FHLB and other advances varies depending on loan demand, deposit inflows, and the use of investment leverage strategies to increase net interest income.

The principal use of the Bank's funds is the origination of mortgages and other loans and the purchase of investments and mortgage-backed securities. Loan originations on loans held for investment were $336.4 million in fiscal 2010 compared to $415.3 million in fiscal 2009 and $390.9 million in fiscal 2008. The decrease in originations in fiscal 2010 was primarily the result of a decrease in commercial loan originations, which decreased $61.3 million. In fiscal 2009 and 2008 loan originations increased $38.7 million, and $28.1 million, respectively. Purchases of investments and mortgage-backed securities were $150.2 million in fiscal 2010 compared to $144.3 million in fiscal 2009 and $142.8 million in fiscal 2008. Other uses of the Bank’s funds included paying down debt including a line of credit and FHLB Advances.

Unused lines of credit on home equity loans, credit cards, and commercial loans amounted to $55.8 million at March 31, 2010. Home equity loans are made on a floating rate basis with final maturities of 10 to 15 years. Credit cards are generally made on a floating rate basis, and are renewed annually or every other year. In addition to the above commitments, the Bank has undisbursed loans-in-process of $3.2 million at March 31, 2010, which will disburse over an average of 90 days. These commitments to originate loans and future advances of lines of credit are expected to be funded from loan amortizations and prepayments, deposit inflows, maturing investments, and short-term borrowing capacity.

The following table sets forth the length of time until maturity for unused commitments to extend credit and standby letters of credit at March 31, 2010:

(In Thousands) | Within One Month | After One Through Three Months | After Three Through Twelve Months | Within One Year | One Year Or Greater | Total | ||||||||||||||||||

| Unused Lines Of Credit | $ | 2,205 | $ | 4,721 | $ | 16,667 | $ | 23,593 | $ | 32,204 | $ | 55,797 | ||||||||||||

| Standby Letters Of Credit | 20 | - | 529 | 549 | 100 | 649 | ||||||||||||||||||

| Total | $ | 2,225 | $ | 4,721 | $ | 17,196 | $ | 24,142 | $ | 32,304 | $ | 56,446 | ||||||||||||

Management believes that future liquidity can be met through the Bank's deposit base, which increased $32.5 million during fiscal 2010, and from maturing investments. In addition, at March 31, 2010 the Bank had another $124.1 million in unused borrowing capacity at the FHLB at March 31, 2010.

Historically the Bank’s cash flow from operating activities has been relatively stable. The cash flows from investing activities vary with the need to invest excess funds or utilize leverage strategies with the purchase of mortgage-backed and investment securities. The cash flows from financing activities vary depending on the need for FHLB and other advances. During the 2010 fiscal year, the Company received $6.1 million through the issuance of senior convertible debentures. See "Consolidated Statements of Cash Flows" in the Consolidated Financial Statements contained herein.

24

SECURITY FEDERAL CORPORATION AND SUBSIDIARIES

Management’s Discussion and Analysis of Financial Condition and Results of Operations

Contractual Obligations

In the normal course of business, the Company enters into contractual obligations that meet various business needs. These contractual obligations include time deposits to customers, borrowings from the FHLB of Atlanta, other borrowings, junior subordinated debentures, senior convertible debentures and lease obligations for facilities. See Notes 5, 8, 9, 10 and 12 of the Notes to the Consolidated Financial Statements included herein for additional information. The following table summarizes the Company’s long-term contractual obligations at March 31, 2010. Contractual repayments may differ from actual because some of the obligations may be subject to calls.

Less than One Year | Over One to Three Years | Over Three to Five Years | Thereafter | Total | ||||||||||||||||

| (In Thousands) | ||||||||||||||||||||

| Time deposits | $ | 309,313 | $ | 66,418 | $ | 16,539 | $ | - | $ | 392,270 | ||||||||||

| FHLB Advances | 31,100 | 44,700 | 35,304 | 52,900 | 164,004 | |||||||||||||||

| Other Borrowings | 12,060 | - | - | - | 12,060 | |||||||||||||||

| Jr. Sub. Debentures | - | - | - | 5,155 | 5,155 | |||||||||||||||

| Sr. Conv. Debentures | - | - | - | 6,084 | 6,084 | |||||||||||||||

Operating Lease Obligations | 434 | 809 | 823 | 1,888 | 3,954 | |||||||||||||||

| Total | $ | 352,907 | $ | 111,927 | $ | 52,666 | $ | 66,027 | $ | 583,527 | ||||||||||

Off-Balance Sheet Arrangements

In the normal course of business, the Company makes off-balance sheet arrangements, including credit commitments to its customers to meet their financial needs. These arrangements involve, to varying degrees, elements of credit and interest rate risk not recognized in the consolidated statement of financial condition. The Bank makes personal, commercial, and real estate lines of credit available to customers and does issue standby letters of credit.

Commitments to extend credit to customers are subject to the Bank’s normal credit policies and are essentially the same as those involved in extending loans to customers. See Note 17 of the Notes to the Consolidated Financial Statements included herein for additional information.

Impact of Inflation and Changing Prices

The Consolidated Financial Statements, related notes, and other financial information presented herein have been prepared in accordance with Generally Accepted Accounting Principles (“GAAP”) that require the measurement of financial position and operating results in terms of historical dollars without considering changes in relative purchasing power over time due to inflation. Unlike most industrial companies, substantially all of the assets and liabilities of a financial institution are monetary in nature. As a result, interest rates generally have a more significant impact on a financial institution's performance than does the effect of inflation.

25

[ELLIOTT DAVIS LLC LETTERHEAD]

REPORT OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM

Shareholders and Board of Directors

Security Federal Corporation and Subsidiaries

Aiken, South Carolina

We have audited the accompanying consolidated balance sheets of Security Federal Corporation and Subsidiaries (the “Company”) as of March 31, 2010 and 2009, and the related consolidated statements of income, changes in shareholders' equity and comprehensive income and cash flows for each of the three years in the period ended March 31, 2010. These consolidated financial statements are the responsibility of the Company's management. Our responsibility is to express an opinion on these consolidated financial statements based on our audits.

We conducted our audits in accordance with the standards of the Public Company Accounting Oversight Board (United States). Those standards require that we plan and perform the audits to obtain reasonable assurance about whether the financial statements are free of material misstatement. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements. An audit also includes assessing the accounting principles used and significant estimates made by management, as well as evaluating the overall financial statement presentation. We believe that our audits provide a reasonable basis for our opinion.

In our opinion, the consolidated financial statements referred to above present fairly, in all material respects, the financial position of Security Federal Corporation and Subsidiaries as of March 31, 2010 and 2009, and the results of their operations and their cash flows for each of the three years in the period ended March 31, 2010, in conformity with accounting principles generally accepted in the United States.

Columbia, South Carolina

June 18, 2010

26

SECURITY FEDERAL CORPORATION AND SUBSIDIARIES

Consolidated Balance Sheets

| March 31, | ||||||||

| 2010 | 2009 | |||||||

| ASSETS: | ||||||||