As filed with the Securities and Exchange Commission on July 23, 2012

File No. 333-

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-14

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

¨ Pre-Effective Amendment No.

¨ Post-Effective Amendment No.

NUVEEN INVESTMENT FUNDS, INC.

(Exact Name of Registrant as Specified in Charter)

333 West Wacker Drive

Chicago, Illinois 60606

(Address of Principal Executive Offices, Zip Code)

Registrant’s Telephone Number, including Area Code (312) 917-7700

Kevin J. McCarthy

Vice President and Secretary

333 West Wacker Drive

Chicago, Illinois 60606

(Name and Address of Agent for Service)

Copy to:

| | |

Deborah Bielicke Eades Vedder Price P.C. 222 North LaSalle Street Chicago, Illinois 60601 | | Eric F. Fess Chapman and Cutler LLP 111 West Monroe Street Chicago, Illinois 60603 |

Approximate date of proposed public offering: As soon as practicable after the effective date of this Registration Statement.

TITLE OF SECURITIES BEING REGISTERED: Shares of Common Stock (par value $0.0001 per share) of the Registrant.

No filing fee is required because of reliance on Section 24(f) and an indefinite number of shares have previously been registered pursuant to Rule 24f-2 under the Investment Company Act of 1940.

It is proposed that this filing will become effective on August 22, 2012 pursuant to Rule 488 under the Securities Act of 1933.

Important Information for

Nuveen Large Cap Value Fund Shareholders

At a special meeting of shareholders of Nuveen Large Cap Value Fund (the “Acquired Fund”), a series of Nuveen Investment Funds, Inc. (the “Corporation”), you will be asked to vote upon an important change affecting your fund. The purpose of the special meeting is to allow you to vote on a reorganization of your fund into Nuveen Dividend Value Fund (the “Acquiring Fund”), another series of the Corporation. If the reorganization is approved and completed, you will become a shareholder of the Acquiring Fund. The Acquired Fund and the Acquiring Fund are collectively referred to herein as the “Funds.”

Although we recommend that you read the complete Proxy Statement/Prospectus, for your convenience, we have provided the following brief overview of the issue to be voted on.

| Q. | Why am I receiving this Proxy Statement/Prospectus? |

| A. | Nuveen Fund Advisors, Inc. (“Nuveen Fund Advisors”), each Fund’s investment adviser, has proposed the reorganization of the Acquired Fund into the Acquiring Fund as part of an initiative to eliminate certain redundancies among the products it offers and in an effort to achieve certain operating efficiencies. |

| Q. | What advantages will the reorganization produce for Acquired Fund shareholders? |

| A. | Nuveen Fund Advisors and the Board of Directors of the Corporation (the “Board”) believe that shareholders of the Acquired Fund will benefit from operational efficiencies and economies of scale that are expected to arise as a result of the larger net asset size of the Acquiring Fund following the reorganization. These operational efficiencies and economies of scale are expected to result in lower gross and net expenses for shareholders of the Acquired Fund. |

| Q. | What are the similarities between the investment policies of the Funds? |

| A. | The investment objective of the Acquired Fund is capital appreciation, with current income as the Fund’s secondary objective. The investment objective of the Acquiring Fund is long-term growth of capital and income. Although the investment objectives of the Funds are not the same, they are similar and the Funds employ similar investment strategies to achieve their investment objectives. The Acquired Fund invests, under normal market conditions, at least 80% of its net assets, plus the amount of any borrowings for investment purposes, in common stocks of large-capitalization companies, defined as companies that have market capitalizations of $5 billion or greater at the time of purchase. The Acquiring Fund invests, under normal market conditions, at least 80% of its net assets, plus the amount of any borrowings for investment purposes, in equity securities of companies which in the opinion of the Fund’s sub-adviser have the ability to pay above average dividends and finance expected growth, have strong management and are trading at attractive valuations. The Acquiring Fund has no restrictions on the capitalization levels of the companies in which it invests, but all of the Acquiring Fund’s equity securities must provide current income at the time of purchase. A more detailed comparison of the investment objectives, policies and risks of the Funds is contained in the Proxy Statement/Prospectus. |

| Q. | What will happen if shareholders do not approve the reorganization? |

| A. | If the reorganization is not approved by shareholders, the Board will take such actions as it deems to be in the best interests of the Acquired Fund, which may include additional solicitation, continuing to operate the Fund as a stand-alone fund, or liquidating the Fund. |

| Q. | Will Acquired Fund shareholders receive new shares in exchange for their current shares? |

| A. | Yes. If shareholders approve the reorganization and it is completed, each Acquired Fund shareholder will receive shares of the Acquiring Fund in an amount equal in total value to the total value of the Acquired Fund shares surrendered by such shareholder. |

| Q. | Will this reorganization create a taxable event for me? |

| A. | No. The reorganization is intended to qualify as a tax-free reorganization for federal income tax purposes. It is expected that you will recognize no gain or loss for federal income tax purposes as a direct result of the reorganization. Prior to the closing of the reorganization, the Acquired Fund expects to distribute all of its net investment income and net capital gains, if any. Such a distribution may be taxable to the Acquired Fund’s shareholders for federal income tax purposes. Due to the Acquired Fund’s capital loss carryforwards, a net capital gain distribution is not expected. However, in light of realized capital gains in the Acquiring Fund’s portfolio that may not be distributed prior to the reorganization, and in light of unrealized capital gains currently in the acquiring Fund’s portfolio, you may be subject to higher capital gain distributions in the future than you would have been absent the reorganization. |

| Q. | How do total operating expenses compare between the two Funds? |

| A. | The total operating expenses of the Acquiring Fund immediately following the reorganization are expected to be lower than the total operating expenses of the Acquired Fund for all share classes. |

| Q. | Who will bear the costs of the reorganization? |

| A. | The reorganization is expected to result in cost savings for each Fund. The Acquired Fund’s projected cost savings are expected due to the operational efficiencies and economies of scale that the larger combined fund should experience. The Acquiring Fund’s projected cost savings consist of management fees expected to be reimbursed pursuant to the proposed management fee reimbursement arrangement that will be implemented if shareholders approve the reorganization and it is completed. In light of these anticipated cost savings, the costs of the reorganization will be allocated between the Funds ratably up to each Fund’s projected cost savings during the first year following the reorganization. Nuveen Fund Advisors estimates that the costs of the reorganization will be approximately $154,000 and that the cost savings during the first year following the reorganization will be approximately $232,000 for the Acquired Fund and $234,000 for the Acquiring Fund. As a result, each of the Acquired Fund and the Acquiring Fund are expected to be charged approximately $77,000. To the extent that such reorganization expenses otherwise exceed the projected cost savings for the Funds during the first year following the reorganization, Nuveen Fund Advisors or its affiliates (“Nuveen”) will pay such expenses. In addition, to the extent that the payment of these expenses would cause a Fund’s expenses to exceed its expense cap for all share classes in effect through December 31, 2012, Nuveen will reimburse such expenses to the extent necessary to operate within the cap. Based on current expense levels it is anticipated that the Acquired Fund’s expenses will exceed its expense cap and that Nuveen will reimburse approximately $12,000 of reorganization expenses charged to the |

| | Acquired Fund. The Funds are expected to recover their costs of the reorganization within the first year following the reorganization assuming that annual cost savings occur at the level shown above. If the reorganization is not approved or completed, Nuveen will pay all such reorganization expenses. |

| Q. | What is the timetable for the reorganization? |

| A. | If approved by shareholders on , 2012, the reorganization is expected to occur at the close of business on , 2012. |

| Q. | Whom do I call if I have questions? |

| A. | If you need any assistance, or have any questions regarding the proposal or how to vote your shares, please call Computershare Fund Services, your proxy solicitor, at (866) 905-8160 from 8 a.m. to 10 p.m. Central time on Monday through Friday or 11 a.m. to 5 p.m. Central time on Saturday. Please have your proxy materials available when you call. |

| Q. | How do I vote my shares? |

| A. | You may vote by mail, telephone or over the Internet: |

| | • | | To vote by mail, please mark, sign, date and mail the enclosed proxy card. No postage is required if mailed in the United States. |

| | • | | To vote by telephone, please call the toll-free number located on your proxy card and follow the recorded instructions, using your proxy card as a guide. |

| | • | | To vote over the Internet, go to the Internet address provided on your proxy card and follow the instructions, using your proxy card as a guide. |

| Q. | Will Nuveen contact me? |

| A. | You may receive a call from representatives of Computershare Fund Services, the proxy solicitation firm retained by Nuveen, to verify that you received your proxy materials and to answer any questions you may have about the reorganization. |

| Q. | How does the Board suggest that I vote? |

| A. | After careful consideration, the Board has agreed unanimously that the reorganization is in the best interests of your Fund and recommends that you vote “FOR” the reorganization. |

, 2012

Dear Shareholders:

We are pleased to invite you to the special meeting of shareholders of Nuveen Large Cap Value Fund (the “Special Meeting”). The Special Meeting is scheduled for , 2012, at [ : ] p.m., Central time, at the offices of Nuveen Investments, Inc., 333 West Wacker Drive, Chicago, Illinois 60606.

At the Special Meeting, you will be asked to consider and approve a very important proposal. Subject to shareholder approval, Nuveen Dividend Value Fund (the “Acquiring Fund”) will acquire all the assets and liabilities of Nuveen Large Cap Value Fund (the “Acquired Fund” and together with the Acquiring Fund, the “Funds” and each a “Fund”) in exchange solely for shares of the Acquiring Fund, which will be distributed in complete liquidation of the Acquired Fund to the shareholders of the Acquired Fund (the “Reorganization”).

Nuveen Fund Advisors, Inc. (“Nuveen Fund Advisors”), each Fund’s investment adviser, has proposed the Reorganization involving the Acquired Fund, as well as a number of other reorganizations involving other funds advised by Nuveen Fund Advisors, to eliminate certain redundancies among the products it offers and in an effort to achieve certain operating efficiencies.

The Reorganization is being proposed because Nuveen Fund Advisors and the Board of Directors of Nuveen Investment Funds, Inc. (the “Board”) believe that the shareholders of the Acquired Fund will benefit from potential operating efficiencies and economies of scale that may be achieved by combining the Funds pursuant to the Reorganization. Following the Reorganization, the Acquiring Fund is expected to have lower gross and net total operating expenses than the Acquired Fund had prior to the Reorganization. The Board believes the Reorganization is in the best interests of the Acquired Fund and recommends that you vote “For” the proposed Reorganization.

The attached Proxy Statement/Prospectus has been prepared to give you information about this proposal.

All shareholders are cordially invited to attend the Special Meeting. In order to avoid delay and additional expense, and to assure that your shares are represented, please vote as promptly as possible, whether or not you plan to attend the Special Meeting. You may vote by mail, telephone or over the Internet.

| | • | | To vote by mail, please mark, sign, date and mail the enclosed proxy card. No postage is required if mailed in the United States. |

| | • | | To vote by telephone, please call the toll-free number located on your proxy card and follow the recorded instructions, using your proxy card as a guide. |

| | • | | To vote over the Internet, go to the Internet address provided on your proxy card and follow the instructions, using your proxy card as a guide. |

We appreciate your continued support and confidence in Nuveen and our family of funds.

|

| Very truly yours, |

|

Kevin J. McCarthy Vice President and Secretary |

, 2012

NUVEEN Large Cap Value Fund

NOTICE OF SPECIAL MEETING OF SHAREHOLDERS

TO BE HELD ON , 2012

To the Shareholders:

Notice is hereby given that a special meeting of shareholders of Nuveen Large Cap Value Fund (the “Acquired Fund”), a series of Nuveen Investment Funds, Inc. (the “Corporation”), a Maryland corporation, will be held at the offices of Nuveen Investments, Inc., 333 West Wacker Drive, Chicago, Illinois 60606, on , 2012 at [ : p.m.], Central time (the “Special Meeting”), for the following purposes:

1. To approve an Agreement and Plan of Reorganization (and the related transactions) which provides for (i) the transfer of all the assets of the Acquired Fund to Nuveen Dividend Value Fund (the “Acquiring Fund”) in exchange solely for voting shares of common stock of the Acquiring Fund and the assumption by the Acquiring Fund of all the liabilities of the Acquired Fund; and (ii) the distribution by the Acquired Fund of Class A, Class C, Class R3 and Class I shares of the Acquiring Fund to the shareholders of Class A, Class C, Class R3 and Class I shares, respectively, of the Acquired Fund in complete liquidation and termination of the Acquired Fund (the “Reorganization”). A vote in favor of the Reorganization will be considered a vote in favor of an amendment to the Corporation’s Articles of Incorporation effecting the Reorganization.

2. To transact such other business as may properly come before the Special Meeting.

Only shareholders of record as of the close of business on , 2012 are entitled to vote at the Special Meeting or any adjournments or postponements thereof.

All shareholders are cordially invited to attend the Special Meeting. In order to avoid delay and additional expense, and to assure that your shares are represented, please vote as promptly as possible, whether or not you plan to attend the Special Meeting. You may vote by mail, telephone or over the Internet.

| | • | | To vote by mail, please mark, sign, date and mail the enclosed proxy card. No postage is required if mailed in the United States. |

| | • | | To vote by telephone, please call the toll-free number located on your proxy card and follow the recorded instructions, using your proxy card as a guide. |

| | • | | To vote over the Internet, go to the Internet address provided on your proxy card and follow the instructions, using your proxy card as a guide. |

|

Kevin J. McCarthy

Vice President and Secretary |

Proxy Statement/Prospectus

Dated , 2012

Relating to the Acquisition of the Assets and Liabilities of NUVEEN LARGE CAP VALUE FUND by NUVEEN DIVIDEND VALUE FUND (formerly Nuveen Equity Income Fund)

This Proxy Statement/Prospectus is being furnished to shareholders of Nuveen Large Cap Value Fund (the “Acquired Fund”), a series of Nuveen Investment Funds, Inc. (the “Corporation”), a Maryland corporation and an open-end investment company registered under the Investment Company Act of 1940, as amended (the “1940 Act”), and relates to the special meeting of shareholders of the Acquired Fund to be held at the offices of Nuveen Investments, Inc., 333 West Wacker Drive, Chicago, Illinois 60606, on , 2012 at [ : p.m.], Central time and at any and all adjournments and postponements thereof (the “Special Meeting”). This Proxy Statement/Prospectus is provided in connection with the solicitation by the Board of Directors of the Corporation (the “Board”) of proxies to be voted at the Special Meeting, and any and all adjournments or postponements thereof. The purpose of the Special Meeting is to consider the proposed reorganization (the “Reorganization”) of the Acquired Fund into Nuveen Dividend Value Fund (formerly Nuveen Equity Income Fund) (the “Acquiring Fund”), a series the Corporation. The Acquired Fund and the Acquiring Fund are referred to herein collectively as the “Funds” and individually as a “Fund.” If shareholders approve the Reorganization and it is completed, shareholders of the Acquired Fund will receive shares of the corresponding class of the Acquiring Fund with the same total value as the total value of the Acquired Fund shares surrendered by such shareholders. The Board has determined that the Reorganization is in the best interests of the Acquired Fund. The address, principal executive office and telephone number of the Funds and the Corporation is 333 West Wacker Drive, Chicago, Illinois 60606, (800) 257-8787.

A vote in favor of the Reorganization will be considered a vote in favor of an amendment to the Corporation’s Articles of Incorporation effecting the Reorganization.

The enclosed proxy and this Proxy Statement/Prospectus are first being sent to shareholders of the Acquired Fund on or about , 2012. Shareholders of record as of the close of business on , 2012 are entitled to vote at the Special Meeting and any adjournments or postponements thereof.

The Securities and Exchange Commission has not approved or disapproved these securities or determined whether the information in this Proxy Statement/Prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

This Proxy Statement/Prospectus concisely sets forth the information shareholders of the Acquired Fund should know before voting on the Reorganization (in effect, investing in Class A, Class C, Class R3 and Class I shares of the Acquiring Fund) and constitutes an offering of Class A, Class C, Class R3 and Class I shares of common stock, par value $0.0001 per share, of the Acquiring Fund. Please read it carefully and retain it for future reference.

The following documents have been filed with the Securities and Exchange Commission (“SEC”) and are incorporated into this Proxy Statement/Prospectus by reference and also accompany this Proxy Statement/Prospectus:

| | (i) | the Corporation’s prospectus dated February 29, 2012, as supplemented through the date of this Proxy Statement/Prospectus, relating to the Funds; and |

| | (ii) | the unaudited financial statements contained in the Corporation’s Semi-Annual Report relating to each Fund for the six-month period ended April 30, 2012. |

The following documents contain additional information about the Funds, have been filed with the SEC and are incorporated into this Proxy Statement/Prospectus by reference:

| | (i) | the Statement of Additional Information relating to the proposed Reorganization, dated , 2012 (the “Reorganization SAI”); |

| | (ii) | the Corporation’s statement of additional information dated February 29, 2012, as supplemented through the date of this Proxy Statement/Prospectus, relating to the Funds; and |

| | (iii) | the audited financial statements contained in the Corporation’s Annual Report relating to each Fund for the fiscal year ended October 31, 2011. |

No other parts of the documents referenced above are incorporated by reference herein.

Copies of the foregoing may be obtained without charge by calling or writing the Funds at the telephone number or address shown above. If you wish to request the Reorganization SAI, please ask for the “Reorganization SAI.” In addition, the Acquiring Fund will furnish, without charge, a copy of its most recent annual report and semi-annual report to a shareholder upon request. Any such request should be directed to the Acquiring Fund by calling (800) 257-8787 or by writing the Acquiring Fund at 333 West Wacker Drive, Chicago, Illinois 60606.

The Corporation is subject to the informational requirements of the Securities Exchange Act of 1934, as amended, and the 1940 Act, and in accordance therewith files reports and other information with the SEC. Reports, proxy statements, registration statements and other information filed by the Corporation (including the registration statement relating to the Acquiring Fund on Form N-14 of which this Proxy Statement/Prospectus is a part) may be inspected without charge and copied (for a duplication fee at prescribed rates) at the SEC’s Public Reference Room at 100 F Street, N.E., Washington, D.C. 20549 or at the SEC’s Northeast Regional Office (3 World Financial Center, New York, New York 10281) or Midwest Regional Office (175 W. Jackson Boulevard, Suite 900, Chicago, Illinois 60604). You may call the SEC at (202) 551-8090 for information about the operation of the Public Reference Room. You may obtain copies of this information, with payment of a duplication fee, by electronic request at the following e-mail address: publicinfo@sec.gov, or by writing the SEC’s Public Reference Branch, Office of Consumer Affairs and Information Services, Securities and Exchange Commission, Washington, D.C. 20549. You may also access reports and other information about the Funds on the EDGAR database on the SEC’s Internet site at http://www.sec.gov.

TABLE OF CONTENTS

i

TABLE OF CONTENTS

(continued)

ii

SUMMARY

The following is a summary of, and is qualified by reference to, the more complete information contained in this Proxy Statement/Prospectus and the information attached hereto or incorporated herein by reference, including the Agreement and Plan of Reorganization. As discussed more fully below and elsewhere in this Proxy Statement/Prospectus, the Board believes the proposed Reorganization is in the best interests of each Fund and that the interests of each Fund’s existing shareholders would not be diluted as a result of the Reorganization. If the Reorganization is approved and completed, shareholders of the Acquired Fund will become shareholders of the Acquiring Fund and will cease to be shareholders of the Acquired Fund.

Shareholders should read the entire Proxy Statement/Prospectus carefully together with the Acquiring Fund’s Prospectus that accompanies this Proxy Statement/Prospectus, which is incorporated herein by reference. This Proxy Statement/Prospectus constitutes an offering of Class A, Class C, Class R3 and Class I shares of the Acquiring Fund only.

Background

Nuveen Fund Advisors, Inc. (“Nuveen Fund Advisors” or the “Adviser”), each Fund’s investment adviser, has proposed the reorganization of the Acquired Fund into the Acquiring Fund, as well as a number of other fund reorganizations between funds with similar investment objectives and policies, as part of an initiative to eliminate certain redundancies among the products it offers and in an effort to achieve certain operating efficiencies.

The Reorganization

This Proxy Statement/Prospectus is being furnished to shareholders of the Acquired Fund in connection with the proposed combination of the Acquired Fund with and into the Acquiring Fund pursuant to the terms and conditions of the Agreement and Plan of Reorganization dated , 2012 by the Corporation, on behalf of the Acquired Fund and the Acquiring Fund, and Nuveen Fund Advisors (the “Agreement”). The Agreement provides for (i) the transfer of all the assets of the Acquired Fund to the Acquiring Fund in exchange solely for Class A, Class C, Class R3 and Class I voting shares of common stock, par value $0.0001 per share, of the Acquiring Fund and the assumption by the Acquiring Fund of all the liabilities of the Acquired Fund; and (ii) the distribution by the Acquired Fund of Class A, Class C, Class R3 and Class I shares of the Acquiring Fund to the shareholders of the corresponding class of the Acquired Fund in complete liquidation and termination of the Acquired Fund as soon as practicable following the Closing Date (as defined herein).

If shareholders approve the Reorganization and it is completed, Acquired Fund shareholders will become shareholders of the Acquiring Fund. The Board has determined that the Reorganization is in the best interests of the Acquired Fund and that the interests of existing shareholders will not be diluted as a result of the Reorganization. The Board unanimously approved the Reorganization and the Agreement at a meeting held on May 21-23, 2012. The Board recommends a vote “FOR” the Reorganization.

If shareholders approve the Reorganization, the Reorganization is expected to result in cost savings for each Fund. The Acquired Fund’s projected cost savings are expected due to the operational efficiencies and economies of scale that the larger combined fund should experience. The Acquiring Fund’s projected cost savings consist of management fees expected to be reimbursed pursuant to the proposed management fee reimbursement arrangement that will be implemented if shareholders

approve the Reorganization and it is completed. This arrangement is intended to maintain the Acquiring Fund’s operating expenses at levels experienced during the fiscal year ended October 31, 2011. For the twelve-month period ended April 30, 2012, the Acquiring Fund experienced gross total operating expenses of 1.16%, 1.91%, 1.41% and 0.91% for Class A, Class C, Class R3 and Class I shares, respectively, which are higher than those experienced during the fiscal year ended October 31, 2011 as shown in the “Annual Fund Operating Expenses” table. Accordingly, the proposed management fee reimbursement arrangement is projected to benefit the Acquiring Fund. In light of the anticipated cost savings, the costs of the Reorganization will be allocated between the Funds ratably up to each Fund’s projected cost savings during the first year following the Reorganization. Nuveen Fund Advisors estimates that the costs of the Reorganization will be approximately $154,000 and that the cost savings during the first year following the Reorganization will be approximately $232,000 for the Acquired Fund and $234,000 for the Acquiring Fund. As a result, each of the Acquired Fund and the Acquiring Fund are expected to be charged approximately $77,000. To the extent that such Reorganization expenses otherwise exceed the projected cost savings for the Funds during the first year following the Reorganization, Nuveen Fund Advisors or its affiliates (“Nuveen”) will pay such expenses. In addition, to the extent that the payment of these expenses would cause a Fund’s expenses to exceed its expense cap for all share classes in effect through December 31, 2012, Nuveen will reimburse such expenses to the extent necessary to operate within the cap. Based on current expense levels it is anticipated that the Acquired Fund’s expenses will exceed its expense cap and that Nuveen will reimburse approximately $12,000 of Reorganization expenses charged to the Acquired Fund. The Funds are expected to recover their costs of the Reorganization within the first year following the Reorganization assuming that annual cost savings occur at the level shown above. If the Reorganization is not approved or completed, Nuveen will pay all such Reorganization expenses.

The Board is asking shareholders of the Acquired Fund to approve the Reorganization at the Special Meeting to be held on , 2012. Approval of the Reorganization requires the affirmative vote of the holders of a majority of the total number of shares outstanding and entitled to vote. See “Voting Information and Requirements” below.

If shareholders of the Acquired Fund approve the Reorganization, it is expected that the Reorganization will occur at the close of business on , 2012 (the “Closing Date”), but it may be at a different time as described herein. If the Reorganization is not approved, the Board will take such action as it deems to be in the best interests of the Acquired Fund. The Closing Date may be delayed and the Reorganization may be abandoned at any time by the mutual agreement of the parties. In addition, either Fund may at its option terminate the Agreement at or before the Closing Date due to (i) a breach by any other party of any representation, warranty, or agreement contained in the Agreement to be performed at or before the Closing Date, if not cured within 30 days, (ii) a condition precedent to the obligations of the terminating party that has not been met and it reasonably appears that it will not or cannot be met, or (iii) a determination by the Board that the consummation of the transactions contemplated by the Agreement is not in the best interests of a Fund.

Reasons for the Proposed Reorganization

The Board believes that the proposed Reorganization would be in the best interests of each Fund. In approving the Reorganization, the Board considered a number of principal factors in reaching its determination, including the following:

| | • | | the similarities and differences in the Funds’ investment objectives and principal investment strategies; |

2

| | • | | the Funds’ relative risks; |

| | • | | the Funds’ relative sizes; |

| | • | | the relative investment performance of the Funds and portfolio managers; |

| | • | | the relative fees and expense ratios of the Funds, including caps on the Funds’ expenses agreed to by the Adviser; |

| | • | | the anticipated tax-free nature of the Reorganization; |

| | • | | the expected costs of the Reorganization and the extent to which the Funds would bear any such costs; |

| | • | | the terms of the Reorganization and whether the Reorganization would dilute the interests of shareholders of the Funds; |

| | • | | the effect of the Reorganization on shareholder services and shareholder rights; |

| | • | | alternatives to the Reorganization; and |

| | • | | any potential benefits of the Reorganization to the Adviser and its affiliates as a result of the Reorganization. |

For a more detailed discussion of the Board’s considerations regarding the approval of the Reorganization, see “The Board’s Approval of the Reorganization.”

Distribution, Purchase, Redemption, Exchange of Shares and Dividends

The Funds have identical procedures for purchasing, exchanging and redeeming shares. The Acquired Fund offers four classes of shares: Class A, Class C, Class R3 and Class I Shares. The Acquiring Fund offers five classes of shares: Class A, Class B, Class C, Class R3 and Class I Shares. The corresponding classes of each Fund have the same investment eligibility criteria. The Acquiring Fund normally declares and pays dividends from net investment income quarterly. The Acquired Fund’s dividends from net investment income, if any, are normally declared and paid annually. Each Fund declares and pays any taxable capital gains or other taxable distributions once a year at year end. See “Comparison of the Funds—Distribution, Purchase, Redemption, Exchange of Shares and Dividends” below for a more detailed discussion.

Material Federal Income Tax Consequences of the Reorganization

As a condition to closing, the Funds will receive an opinion from Vedder Price P.C. (which will be based on certain factual representations and certain customary assumptions and exclusions) substantially to the effect that the Reorganization will qualify as a tax-free reorganization under Section 368(a) of the Internal Revenue Code of 1986, as amended (the “Code”). Accordingly, it is expected that neither Fund will recognize gain or loss for federal income tax purposes as a direct result of the Reorganization. In connection with the Reorganization, a portion of the Acquired Fund’s portfolio assets may be sold prior to the Reorganization, which could result in the Acquired Fund declaring taxable distributions to its shareholders on or prior to the Closing Date. However, it is not

3

expected that any material portfolio sales (i.e., more than 5% of the Acquired Fund assets) will occur solely in connection with the Reorganization. In addition, the Acquired Fund recently experienced a change in its portfolio management team, and, as a result, the Acquired Fund may have material portfolio sales prior to the Reorganization. For a more detailed discussion of the federal income tax consequences of the Reorganization, please see “The Proposed Reorganization—Material Federal Income Tax Consequences” below.

COMPARISON OF THE FUNDS

Investment Objectives

The Funds have similar investment objectives. The Acquired Fund’s investment objective is capital appreciation. The Acquired Fund’s secondary objective is current income. The Acquiring Fund’s investment objective is long-term growth of capital and income. The investment objective of each Fund may be changed without shareholder approval upon providing notice at least 60 days in advance.

Investment Strategies

The Acquired Fund and the Acquiring Fund also have similar principal investment strategies and risks. The similarities and differences of the principal investment strategies of the Funds are:

| | |

| Acquired Fund | | Acquiring Fund |

| |

• Under normal market conditions, the Fund invests at least 80% of net assets, plus the amount of any borrowings for investment purposes, in common stocks of large-capitalization companies, defined as companies that have market capitalizations of $5 billion or greater at the time of purchase. | | • Under normal market conditions, the Fund invests at least 80% of its net assets, plus the amount of any borrowings for investment purposes, in equity securities of companies that, in the opinion of the Fund’s sub-adviser, have the ability to pay above average dividends and finance expected growth, have strong management, and are trading at attractive valuations. |

| |

• In selecting stocks, the Fund’s sub-adviser invests in companies that it believes are undervalued relative to other companies in the same industry or market, exhibit good or improving fundamentals, and exhibit an identifiable catalyst that could close the gap between market value and fair value over the next one to two years. | | |

4

| | |

| Acquired Fund | | Acquiring Fund |

| |

| | • The Fund will attempt to maintain a dividend that will grow over time. As a result, higher-yielding equity securities will generally represent the core holdings of the Fund. However, the Fund also may invest in lower-yielding, higher-growth equity securities if the sub-adviser believes they will help balance the portfolio. |

| |

| | • The Fund’s equity securities include common stocks, convertible preferred stocks, and corporate debt securities that are convertible into common stocks. All such equity securities will provide current income at the time of purchase. |

| |

| | • The Fund may invest in convertible debt securities without regard to their ratings, and therefore may hold convertible debt securities which are rated lower than investment grade. |

| |

• The Fund may invest up to 15% of its total assets in non-dollar denominated equity securities of non-U.S. issuers. | | • The Fund may invest up to 15% of its total assets in non-dollar denominated equity securities of non-U.S. issuers. |

| |

• The Fund may invest up to 25% of its assets, collectively, in non-dollar denominated equity securities of non-U.S. issuers and in dollar-denominated equity securities of non-U.S. issuers that are either listed on a U.S. stock exchange or represented by depositary receipts that may or may not be sponsored by a domestic bank. | | • The Fund may invest up to 25% of its assets, collectively, in non-dollar denominated equity securities of non-U.S. issuers and in dollar-denominated equity securities of non-U.S. issuers that are either listed on a U.S. stock exchange or represented by depositary receipts that may or may not be sponsored by a domestic bank. |

| |

• Up to 15% of the Fund’s total assets may be invested in equity securities of emerging market issuers. A country is considered to be an “emerging market” if it is defined as such by Morgan Stanley Capital International Inc. | | • Up to 15% of the Fund’s total assets may be invested in equity securities of emerging market issuers. A country is considered to be an “emerging market” if it is defined as such by Morgan Stanley Capital International Inc. |

5

| | |

| Acquired Fund | | Acquiring Fund |

| |

• The Fund may utilize options, futures contracts, options on futures contracts, and forward foreign currency exchange contracts (“derivatives”). The Fund may use these derivatives to manage market or business risk, enhance the Fund’s return, or hedge against adverse movements in currency exchange rates. | | • The Fund may utilize options, futures contracts, options on futures contracts, and forward foreign currency exchange contracts (“derivatives”). The Fund may use these derivatives to manage market or business risk, enhance the Fund’s return, or hedge against adverse movements in currency exchange rates. |

Comparison of Principal Investment Strategies

Although the investment objectives of the Funds are not the same, they are similar and the Funds employ similar investment strategies to achieve their investment objectives. Under normal market conditions, the Acquired Fund invests at least 80% of its net assets, plus the amount of any borrowings for investment purposes, in common stocks of large-capitalization companies, defined as companies that have market capitalizations of $5 billion or greater at the time of purchase. Under normal market conditions, the Acquiring Fund invests at least 80% of its net assets, plus the amount of any borrowings for investment purposes, in equity securities which in the opinion of the Fund’s sub-adviser have the ability to pay above average dividends and finance expected growth, have strong management and are trading at attractive valuations. The Acquiring Fund has no restrictions on the capitalization levels of the companies in which it invests, but all of the Fund’s equity securities must provide current income at the time of purchase.

The Acquiring Fund invests in equity securities, which may include common stocks, convertible preferred stocks and corporate debt securities that are convertible into common stocks. The Acquired Fund invests in common stocks, but it does not invest in convertible preferred stocks or convertible debt securities as a principal strategy.

Both Funds have the same principal investment strategies regarding investment in foreign securities, emerging market securities and derivatives.

In evaluating the Reorganization, each Acquired Fund shareholder should consider the risks of investing in the Acquiring Fund. The principal risks of investing in the Acquiring Fund are described in the section below entitled “Risk Factors.”

The Reorganization may result in one-time brokerage costs for the Acquired Fund to the extent it is necessary for the Acquired Fund to sell holdings prior to the Reorganization so that the Acquiring Fund’s portfolio immediately following the Reorganization remains in compliance with its investment policies and restrictions. If the Reorganization had occurred as of April 30, 2012, the Acquired Fund would not have been required to dispose of its securities in order to comply with the Acquiring Fund’s investment policies and restrictions, and would not have sold any material portion (i.e., more than 5% of its assets) of the securities in its portfolio solely as a result of the Reorganization.

Fees and Expenses

The tables below provide information about the fees and expenses attributable to each class of shares of the Funds, and the pro forma fees and expenses of the combined fund. You may qualify for

6

sales charge discounts on purchases of Class A shares if you and your family invest, or agree to invest in the future, at least $50,000 in a Fund or other Nuveen mutual funds. Shareholder fees reflect the fees currently in effect for each Fund as of their fiscal year ended October 31, 2011. The pro forma fees and expenses are based on the amounts shown in the table for each Fund, assuming the Reorganization occurred as of October 31, 2011.

Shareholder Fees

(paid directly from your investment)

| | | | | | |

| | | Acquired

Fund | | Acquiring

Fund | | Combined

Fund Pro

Forma |

Maximum Sales Charge (Load) Imposed on Purchases (as a percentage of offering price) | | | | | | |

Class A | | 5.75% | | 5.75% | | 5.75% |

Class C | | None | | None | | None |

Class R3 | | None | | None | | None |

Class I | | None | | None | | None |

Maximum Deferred Sales Charge (Load) (as a percentage of the lesser of purchase price or redemption proceeds) | | | | | | |

Class A | | None | | None | | None |

Class C1 | | 1.00% | | 1.00% | | 1.00% |

Class R3 | | None | | None | | None |

Class I | | None | | None | | None |

Maximum Sales Charge (Load) Imposed on Reinvested Dividends | | | | | | |

Class A | | None | | None | | None |

Class C | | None | | None | | None |

Class R3 | | None | | None | | None |

Class I | | None | | None | | None |

Exchange Fees | | | | | | |

Class A | | None | | None | | None |

Class C | | None | | None | | None |

Class R3 | | None | | None | | None |

Class I | | None | | None | | None |

Annual Low Balance Account fee (for accounts under $1,000)2 | | | | | | |

Class A | | $15 | | $15 | | $15 |

Class C | | $15 | | $15 | | $15 |

Class R3 | | None | | None | | None |

Class I | | $15 | | $15 | | $15 |

| 1 | The CDSC on Class C shares applies only to redemptions within 12 months of purchase. |

| 2 | Fee applies to the following types of accounts under $1,000 held directly with the Fund: individual retirement accounts (IRAs), Coverdell Education Savings Accounts and accounts established pursuant to the Uniform Transfers to Minors Act (UTMA) or Uniform Gifts to Minors Act (UGMA). |

7

Annual Fund Operating Expenses

(expenses that you pay each year as a percentage of the value of your investment)

| | | | | | |

| | | Acquired

Fund | | Acquiring

Fund | | Combined

Fund Pro

Forma1 |

Management Fees | | | | | | |

Class A | | 0.75% | | 0.77% | | 0.77% |

Class C | | 0.75% | | 0.77% | | 0.77% |

Class R3 | | 0.75% | | 0.77% | | 0.77% |

Class I | | 0.75% | | 0.77% | | 0.77% |

Distribution and Service (12b-1) Fees | | | | | | |

Class A | | 0.25% | | 0.25% | | 0.25% |

Class C | | 1.00% | | 1.00% | | 1.00% |

Class R3 | | 0.50% | | 0.50% | | 0.50% |

Class I | | 0.00% | | 0.00% | | 0.00% |

Other Expenses | | | | | | |

Class A | | 0.19% | | 0.12% | | 0.13% |

Class C | | 0.19% | | 0.12% | | 0.13% |

Class R3 | | 0.19% | | 0.12% | | 0.13% |

Class I | | 0.19% | | 0.12% | | 0.13% |

Total Annual Fund Operating Expenses2 | | | | | | |

Class A | | 1.19% | | 1.14% | | 1.15% |

Class C | | 1.94% | | 1.89% | | 1.90% |

Class R3 | | 1.44% | | 1.39% | | 1.40% |

Class I | | 0.94% | | 0.89% | | 0.90% |

Fee Waivers and/or Expense Reimbursements | | | | | | |

Class A | | 0.00% | | 0.00% | | (0.01%)3 |

Class C | | 0.00% | | 0.00% | | (0.01%)3 |

Class R3 | | 0.00% | | 0.00% | | (0.01%)3 |

Class I | | 0.00% | | 0.00% | | (0.01%)3 |

Total Annual Fund Operating Expenses–After Fee Waivers and/or Expense Reimbursements | | | | | | |

Class A | | 1.19% | | 1.14% | | 1.14% |

Class C | | 1.94% | | 1.89% | | 1.89% |

Class R3 | | 1.44% | | 1.39% | | 1.39% |

Class I | | 0.94% | | 0.89% | | 0.89% |

| 1 | Pro forma expenses do not include the expenses to be charged to the Funds in connection with the Reorganization. See “The Proposed Reorganization—Reorganization Expenses” for additional information about these expenses. |

| 2 | Expenses have been restated to reflect current contractual fees and estimated other expenses. |

| 3 | If the Reorganization is approved by shareholders and completed, Nuveen Fund Advisors has agreed to waive fees and/or reimburse expenses through October 31, 2013 so that Total Annual Fund Operating Expenses (excluding 12b-1 distribution and/or service fees, interest expenses, taxes, fees incurred in acquiring and disposing of portfolio securities and extraordinary expenses) do not exceed 1.14%, 1.89%, 1.39% and 0.89% for Class A, Class C, Class R3 and Class I, respectively, of average daily net assets. The expense limitation will not be terminated or modified prior to that date without the approval of the Board. |

Example

The example below is intended to help you compare the cost of investing in each Fund and the pro forma cost of investing in the combined fund. The example assumes you invest $10,000 in a Fund for the time periods indicated (based on information in the tables above) and then either redeem or do not

8

redeem your shares at the end of a period. The example assumes that your investment has a 5% return each year and that a Fund’s expenses remain at the level shown in the table above. Expense caps are taken into account for the periods stated in the table above. Although your actual costs may be higher or lower, based on these assumptions your costs would be:

| | | | | | |

| | | Acquired

Fund | | Acquiring

Fund | | Combined

Fund Pro

Forma |

1 Year | | | | | | |

Assuming you sold your shares at the end of each period | | | | | | |

Class A | | $ 689 | | $ 685 | | $ 685 |

Class C | | $ 197 | | $ 192 | | $ 192 |

Class R3 | | $ 147 | | $ 142 | | $ 142 |

Class I | | $ 96 | | $ 91 | | $ 91 |

Assuming you kept your shares | | | | | | |

Class A | | $ 689 | | $ 685 | | $ 685 |

Class C | | $ 197 | | $ 192 | | $ 192 |

Class R3 | | $ 147 | | $ 142 | | $ 142 |

Class I | | $ 96 | | $ 91 | | $ 91 |

| | | |

3 Years | | | | | | |

Assuming you sold your shares at the end of each period | | | | | | |

Class A | | $ 931 | | $ 916 | | $ 918 |

Class C | | $ 609 | | $ 594 | | $ 596 |

Class R3 | | $ 456 | | $ 440 | | $ 442 |

Class I | | $ 300 | | $ 284 | | $ 286 |

Assuming you kept your shares | | | | | | |

Class A | | $ 931 | | $ 916 | | $ 918 |

Class C | | $ 609 | | $ 594 | | $ 596 |

Class R3 | | $ 456 | | $ 440 | | $ 442 |

Class I | | $ 300 | | $ 284 | | $ 286 |

| | | |

5 Years | | | | | | |

Assuming you sold your shares at the end of each period | | | | | | |

Class A | | $1,192 | | $1,167 | | $1,171 |

Class C | | $1,047 | | $1,021 | | $1,025 |

Class R3 | | $ 787 | | $ 761 | | $ 765 |

Class I | | $ 520 | | $ 493 | | $ 497 |

Assuming you kept your shares | | | | | | |

Class A | | $1,192 | | $1,167 | | $1,171 |

Class C | | $1,047 | | $1,021 | | $1,025 |

Class R3 | | $ 787 | | $ 761 | | $ 765 |

Class I | | $ 520 | | $ 493 | | $ 497 |

9

| | | | | | |

| | | Acquired

Fund | | Acquiring

Fund | | Combined

Fund Pro

Forma |

| | | |

10 Years | | | | | | |

Assuming you sold your shares at the end of each period | | | | | | |

Class A | | $1,935 | | $1,881 | | $1,891 |

Class C | | $2,264 | | $2,212 | | $2,221 |

Class R3 | | $1,724 | | $1,669 | | $1,679 |

Class I | | $1,155 | | $1,096 | | $1,107 |

Assuming you kept your shares | | | | | | |

Class A | | $1,935 | | $1,881 | | $1,891 |

Class C | | $2,264 | | $2,212 | | $2,221 |

Class R3 | | $1,724 | | $1,669 | | $1,679 |

Class I | | $1,155 | | $1,096 | | $1,107 |

Portfolio Turnover

Each Fund pays transaction costs, such as commissions, when it buys and sells securities (or “turns over” its portfolio). A higher portfolio turnover rate may indicate higher transaction costs and may result in higher taxes when Fund shares are held in a taxable account. These costs, which are not reflected in annual fund operating expenses or in the example, affect each Fund’s performance. During their most recent fiscal periods for which financial statements are available, the Funds had the following portfolio turnover rates:

| | | | | | | | |

Fund | | Fiscal Year Ended | | Rate | | Semi-Annual Period Ended | | Rate |

Acquired Fund | | 10/31/11 | | 114% | | 4/30/12 | | 47% |

Acquiring Fund | | 10/31/11 | | 33% | | 4/30/12 | | 11% |

After the Reorganization is completed, the portfolio managers of the Acquiring Fund may, in their discretion, sell securities acquired from the Acquired Fund. To the extent that the portfolio managers choose to sell a significant percentage of such securities, the Acquiring Fund’s portfolio turnover rate and brokerage costs may be higher than they otherwise would have been.

Risk Factors

In evaluating the Reorganization, you should consider carefully the risks of the Acquiring Fund to which you will be subject if the Reorganization is approved and completed. Investing in a mutual fund involves risk, including the risk that you may receive little or no return on your investment or even that you may lose part or all of your investment. Because of these and other risks, you should consider an investment in the Acquiring Fund to be a long-term investment. An investment in the Acquiring Fund may not be appropriate for all shareholders. For a complete description of the risks of an investment in the Acquiring Fund, see the section in the Acquiring Fund’s Prospectus entitled “Principal Risks.”

Because the Funds have similar investment strategies, the principal risks of each Fund are similar. The principal risks of investing in the Acquiring Fund are described below. An investment in the Acquired Fund is also subject to certain of these risks; however, it is not subject to credit risk, high yield securities risk or interest rate risk as principal risks. In addition, the principal risks of the

10

Acquired Fund include investment focus risk, because of the Fund’s focus on investments in large-cap stocks and its emphasis on value style investing.

Credit Risk. Credit risk is the risk that an issuer of a debt security may be unable or unwilling to make interest and principal payments when due and the related risk that the value of a debt security may decline because of concerns about the issuer’s ability or willingness to make such payments. In addition, parties to other financial contracts with the Fund could default on their obligations.

Derivatives Risk. The use of derivatives involves additional risks and transaction costs which could leave the Fund in a worse position than if it had not used these instruments. Derivatives may entail investment exposures that are greater than their cost would suggest. As a result, a small investment in derivatives could have a large impact on performance.

Equity Securities Risk. Equity securities may decline significantly in price over short or extended periods of time, and such declines may occur in the equity market as a whole, or they may occur in only a particular country, company, industry, or sector of the market.

High Yield Securities Risk. High yield securities generally are less liquid, have more volatile prices, and have greater credit risk than investment grade securities.

Interest Rate Risk. Interest rate risk is the risk that the value of the Fund’s portfolio will decline because of rising interest rates.

Non-U.S./Emerging Markets Risk. Non-U.S. issuers or U.S. issuers with significant non-U.S. operations may be subject to risks in addition to those of issuers located in or that principally operate in the United States as a result of, among other things, political, social and economic developments abroad and different legal, regulatory and tax environments. These additional risks may be heightened for securities of issuers located in, or with significant operations in, emerging market countries. Also, changes in currency exchange rates may affect the Fund’s net asset value, the value of dividends and interest earned, and gains and losses realized on the sale of securities.

Fundamental Investment Restrictions

The Funds have identical fundamental investment restrictions that cannot be changed without shareholder approval. In addition, each Fund is a diversified fund. As diversified funds, each Fund, with respect to 75% of its assets, may not invest more than 5% of its total assets in the securities of any one issuer (other than securities issued by other investment companies or by the U.S. government, its agencies, instrumentalities or authorities) and may not purchase more than 10% of the outstanding voting securities of any one issuer.

Performance Information

The total returns of the Funds for the periods ended December 31, 2011, based on historical fees and expenses for each period, are set forth in the bar charts and tables below.

The following bar charts and tables provide some indication of the potential risks of investing in each Fund. Each Fund’s past performance (before and after taxes) is not necessarily an indication of how the Fund will perform in the future. Updated performance information is available at www.nuveen.com/MF/products/performancesummary.aspx or by calling (800) 257-8787.

11

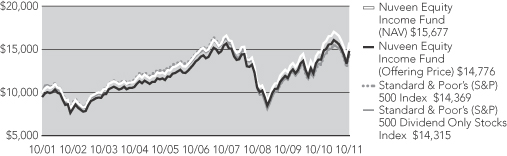

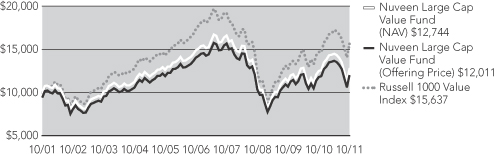

The bar charts below show the annual calendar year returns for each Fund’s Class A shares. The performance of the other share classes will differ due to their different expense structures. The bar charts and highest/lowest quarterly and year-to-date returns that follow do not reflect sales charges, and if these charges were reflected, the returns would be less than those shown. The tables below show the average annual returns for the periods ended December 31, 2011 for each Fund. The tables also show how each Fund’s performance compares with the returns of a broad measure of market performance and an index of funds with similar investment objectives. In addition, the Acquiring Fund’s performance is compared to the Standard & Poor’s 500® Index and Standard & Poor’s 500® Dividend Only Stocks as these were the Fund’s previous benchmarks. Going forward, the Acquiring Fund’s performance will be compared to the Russell 1000® Value Index because it more closely reflects the Fund’s investment universe. This information is intended to help you assess the variability of Fund returns (and consequently, the potential risks of a Fund investment).

All after-tax returns are calculated using the historical highest individual federal marginal income tax rates and do not reflect the impact of state and local taxes. After-tax returns are shown for Class A shares only; after-tax returns for Class C, Class R3 and Class I shares will vary. Your own actual after-tax returns will depend on your specific tax situation and may differ from what is shown here. After-tax returns are not relevant to investors who hold fund shares in tax-deferred accounts such as IRAs or employer-sponsored retirement plans.

Both the bar charts and the tables assume that all distributions have been reinvested. Performance reflects fee waivers, if any, in effect during the periods presented. If any such waivers were not in place, performance would be reduced.

Prior to July 1, 2004, Class R3 shares were designated Class S shares, which had lower fees and expenses. The performance information in the table prior to July 1, 2004 is based on the performance of the Class S shares. If current fees and expenses had been in effect, performance would have been lower.

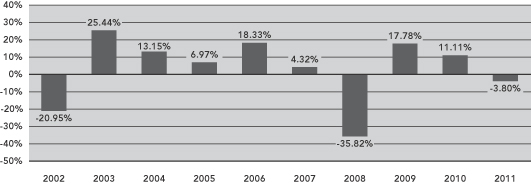

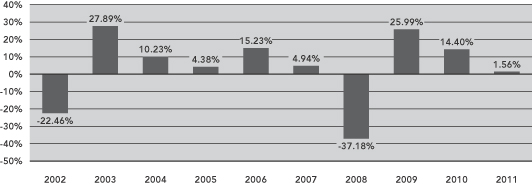

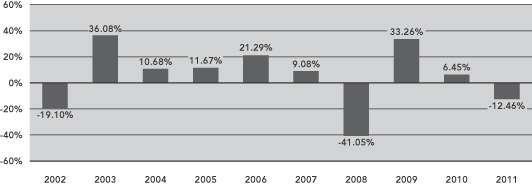

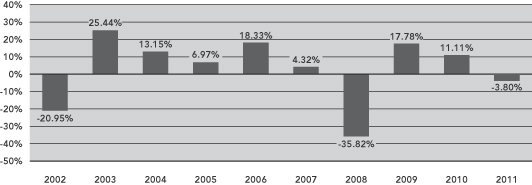

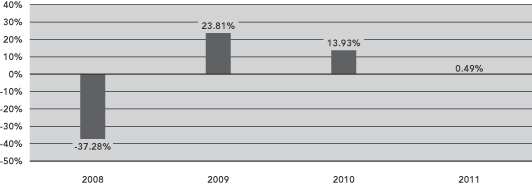

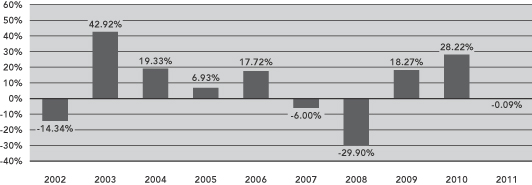

Acquired Fund – Class A Annual Total Return

During the periods shown in the bar chart, the Acquired Fund’s Class A highest and lowest calendar quarter returns were 15.62% and -19.74%, respectively, for the quarters ended September 30, 2009 and December 31, 2008. The Acquired Fund’s Class A year-to-date return through June 30, 2012 was 5.81%.

12

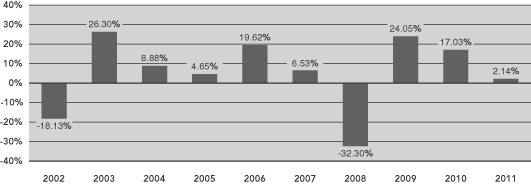

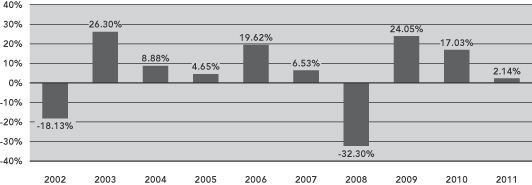

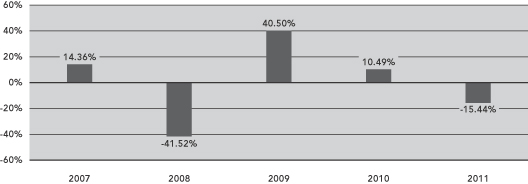

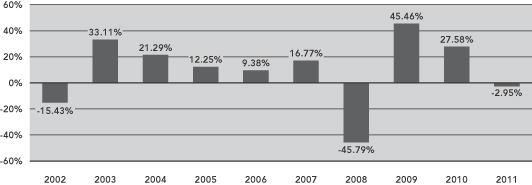

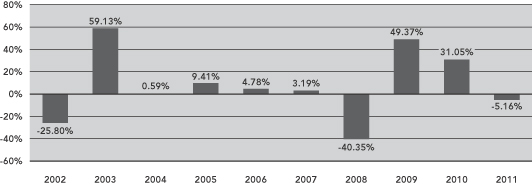

Acquiring Fund – Class A Total Return

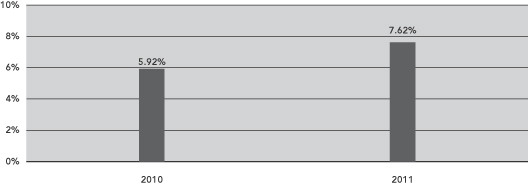

During the periods shown in the bar chart, the Acquiring Fund’s Class A highest and lowest calendar quarter returns were 16.68% and -17.11%, respectively, for the quarters ended June 30, 2003 and December 31, 2008. The Acquiring Fund’s Class A year-to-date return through June 30, 2012 was 7.04%.

| | | | | | |

| | | Average Annual Total Returns for the

Periods Ended December 31, 2011 |

Acquired Fund | | 1 Year | | 5 Years | | 10 Years |

Class A (return before taxes) | | (9.32)% | | (4.50)% | | 1.21% |

Class A (return after taxes on distributions) | | (9.38)% | | (5.16)% | | 0.55% |

Class A (return after taxes on distributions and sale of fund shares) | | (5.99)% | | (3.83)% | | 0.94% |

Class C (return before taxes) | | (4.53)% | | (4.09)% | | 1.04% |

Class R3 (return before taxes) | | (4.06)% | | (3.61)% | | 1.61% |

Class I (return before taxes) | | (3.60)% | | (3.13)% | | 2.07% |

Russell 1000® Value Index (reflects no deduction for fees, expenses or taxes) | | 0.39% | | (2.64)% | | 3.89% |

Lipper Large-Cap Value Classification Average (reflects no deduction for taxes or certain expenses) | | (2.15)% | | (2.67)% | | 2.87% |

| |

| | | Average Annual Total Returns for the

Periods Ended December 31, 2011 |

Acquiring Fund | | 1 Year | | 5 Years | | 10 Years |

Class A (return before taxes) | | (3.76)% | | 0.16% | | 3.57% |

Class A (return after taxes on distributions) | | (4.06)% | | (0.45)% | | 2.94% |

Class A (return after taxes on distributions and sale of fund shares) | | (2.04)% | | 0.07% | | 2.97% |

Class C (return before taxes) | | 1.37% | | 0.60% | | 3.41% |

Class R3 (return before taxes) | | 1.96% | | 1.08% | | 3.98% |

Class I (return before taxes) | | 2.39% | | 1.61% | | 4.45% |

Russell 1000® Value Index (reflects no deduction for fees, expenses or taxes) | | 0.39% | | (2.64)% | | 3.89% |

Standard & Poor’s 500® Index (reflects no deduction for fees, expenses or taxes) | | 2.11% | | (0.25)% | | 2.92% |

Standard & Poor’s 500® Dividend Only Stocks (reflects no deduction for fees, expenses or taxes) | | 1.68% | | (0.56)% | | 2.61% |

Lipper Equity Income Classification Average (reflects no deduction for taxes or certain expenses) | | 3.07% | | 0.44% | | 4.42% |

13

Investment Adviser and Sub-Adviser

Both Funds are managed by Nuveen Fund Advisors, which offers advisory and investment management services to a broad range of mutual fund clients. Nuveen Fund Advisors has overall responsibility for management of the Funds, oversees the management of the Funds’ portfolios, manages the Funds’ business affairs and provides certain clerical, bookkeeping and other administrative services. Nuveen Fund Advisors is located at 333 West Wacker Drive, Chicago, Illinois 60606. Nuveen Fund Advisors is a subsidiary of Nuveen Investments, Inc. (“Nuveen Investments”). On November 13, 2007, Nuveen Investments was acquired by investors led by Madison Dearborn Partners, LLC, which is a private equity investment firm based in Chicago, Illinois. The Nuveen family of advisers has been providing advice to investment companies since 1976.

Nuveen Fund Advisors has selected its affiliate, Nuveen Asset Management, LLC (“Nuveen Asset Management”), located at 333 West Wacker Drive, Chicago, Illinois 60606, to serve as a sub-adviser to each of the Funds. Nuveen Asset Management manages the investment of the Funds’ assets on a discretionary basis, subject to the supervision of Nuveen Fund Advisors.

The Funds are managed by the same portfolio managers. Cori B. Johnson, CFA, has managed the Acquiring Fund since August 1994 and the Acquired Fund since April 2012. Ms. Johnson entered the financial services industry in 1981 and joined FAF Advisors, Inc. (“FAF”) in 1985. She joined Nuveen Asset Management on January 1, 2011 in connection with its acquisition of a portion of FAF’s asset management business.

Gerald C. Bren, CFA, has managed the Acquiring Fund since August 1994 and the Acquired Fund since April 2012. Mr. Bren entered the financial services industry when he joined FAF in 1972. He joined Nuveen Asset Management on January 1, 2011 in connection with its acquisition of a portion of FAF’s asset management business. Mr. Bren has announced that he will retire from Nuveen Asset Management on December 31, 2012. He will continue to act as a portfolio manager for the Funds until that time.

Derek M. Sadowsky has managed the Acquiring Fund since February 2012 and the Acquired Fund since April 2012. He entered the financial services industry in 1998 and joined Nuveen Asset Management on January 1, 2011 in connection with its acquisition of a portion of FAF’s asset management business. Prior to joining FAF in 2010, Mr. Sadowsky was an analyst at State Street Global Advisors in charge of the global basic materials sector. Previously, he was an associate at Putnam Investments where he worked on the global basic materials team, and served as an associate at Citigroup covering the domestic chemical sector.

For a complete description of the advisory services provided to the Acquiring Fund, see the section of the Fund’s Prospectus entitled “Who Manages the Funds” and the sections of the Fund’s Statement of Additional Information entitled “Investment Adviser” and “Sub-Adviser.” Additional information about the portfolio manager compensation structure, other accounts managed by the portfolio managers and the portfolio managers’ ownership of securities in the Funds is provided in the Funds’ Statement of Additional Information.

14

Advisory and Other Fees

Pursuant to investment management agreements between Nuveen Fund Advisors and the Corporation, on behalf of the Funds, each Fund pays Nuveen Fund Advisors fund-level fees, payable monthly, at the annual rates set forth below:

| | | | | | |

Acquired Fund - Management Fee | | Acquiring Fund - Management Fee |

Average Daily Net Assets | | Fee Rate | | Average Daily Net Assets | | Fee Rate |

| | | |

For the first $125 million | | 0.5500% | | For the first $125 million | | 0.6000% |

For the next $125 million | | 0.5375% | | For the next $125 million | | 0.5875% |

For the next $250 million | | 0.5250% | | For the next $250 million | | 0.5750% |

For the next $500 million | | 0.5125% | | For the next $500 million | | 0.5625% |

For the next $1 billion | | 0.5000% | | For the next $1 billion | | 0.5500% |

For net assets over $2 billion | | 0.4750% | | For net assets over $2 billion | | 0.5250% |

In addition to the fund-level fee, each Fund pays a complex-level fee. The maximum complex-level fee is 0.20% of the Fund’s average daily net assets, based upon complex-level “eligible assets” of $55 billion. Therefore, the maximum management fee rate for each Fund is the fund-level fee rate plus 0.20%. As complex-level eligible assets increase, the complex-level fee rate decreases pursuant to a breakpoint schedule. Each Fund’s individual complex-level fee rate is determined by taking the current overall complex-level fee rate, which is based on the aggregate amount of the “eligible assets” of all Nuveen funds, and making an upward adjustment to that rate (subject to the maximum 0.20% rate noted above) based upon the percentage of the Fund’s assets, if any, that are not “eligible assets.” For each Nuveen Fund that was formerly a First American Fund, including both of the Funds, the portion of the Fund’s assets classified as “eligible assets” excludes some or all of the Fund’s assets, based on the Fund’s size relative to its size at the time Nuveen Fund Advisors became the Fund’s investment adviser. The Acquired Fund has experienced net redemptions subsequent to that time, and its complex-level fee rate therefore is slightly higher than the complex-level fee rate for the Acquiring Fund. As of April 30, 2012, the complex-level fee rate applicable to the Acquiring Fund was 0.1922%, and the rate applicable to the Acquired Fund was 0.1998%. Currently, none of the Acquired Fund’s assets are eligible assets, and the Acquired Fund’s assets will retain their status as ineligible assets after the Reorganization for purposes of calculating the combined fund’s complex-level fee. As a result, the combined fund will have a slightly higher complex-level fee rate than the Acquiring Fund. Information regarding the Board’s approval of the investment management agreements for the Funds is currently available in the Funds’ annual reports to shareholders for the fiscal year ended October 31, 2011.

If the Reorganization is approved by shareholders and completed, Nuveen Fund Advisors has agreed to waive fees and/or reimburse expenses for the combined fund so that total annual fund operating expenses, excluding 12b-1 distribution and/or service fees, interest expenses, taxes, fees incurred in acquiring and disposing of portfolio securities and extraordinary expenses, after fee waivers and/or expense reimbursements do not exceed 1.14%, 1.89%, 1.39% and 0.89% of the average daily net assets of Class A, Class C, Class R3 and Class I, respectively. The fee waiver and expense reimbursement will not be terminated prior to October 31, 2013 without approval of the Board.

In addition, Nuveen Fund Advisors has agreed to reimburse management fees across all share classes of both Funds through December 31, 2012 to the extent necessary so that total annual fund operating expenses, excluding 12b-1 distribution and service fees, interest expenses, taxes, fees incurred in acquiring and disposing of portfolio securities, acquired fund fees and expenses and

15

extraordinary expenses, do not exceed 0.95% for the Acquiring Fund and 1.06% for the Acquired Fund, provided that in no event will Nuveen Fund Advisors be required to make any reimbursements that would result in an annualized net management fee of less than 0.78% for the Acquiring Fund and 0.74% for the Acquired Fund. This management fee reimbursement arrangement will not be terminated prior to that time without approval of the Board. However, the total operating expenses of each Fund currently are below these expense limits.

For the Funds’ fiscal year ended October 31, 2011, each Fund paid its investment adviser (Nuveen Fund Advisors beginning on January 1, 2011 and FAF prior to January 1, 2011) the following management fees (net of any fee waivers and expense reimbursements) as a percentage of average net assets:

| | |

| | | Management Fee Rate |

Acquired Fund | | 0.72% |

Acquiring Fund | | 0.75% |

Each Fund has adopted a distribution and service plan (the “Plan”) pursuant to Rule 12b-1 under the 1940 Act. Under the Plans, Class C shares and Class R3 shares are subject to a distribution fee, and Class A shares, Class C and Class R3 shares are subject to a service fee. Class I shares are not subject to either distribution or service fees.

Under the Plan, for each Fund (a) Class A shares are subject to an annual service fee of 0.25% of the average daily net assets of Class A shares, (b) Class C shares are subject to (i) an annual distribution fee of 0.75% of the average daily net assets of Class C shares and (ii) an annual service fee of 0.25% of the average daily net assets of Class C shares, and (c) Class R3 shares are subject to (i) an annual distribution fee of 0.25% of the average daily net assets of Class R3 shares and (ii) an annual service fee of 0.25% of the average daily net assets of Class R3 shares. For a complete description of these arrangements for the Acquiring Fund, see the section of the Fund’s Prospectus entitled “What Share Classes We Offer” and the section of the Fund’s Statement of Additional Information entitled “Distributor.”

Board Members and Officers

Both Funds are series of the Corporation and, as a result, have the same Board and the same officers. The management of each Fund, including general oversight of the duties performed by Nuveen Fund Advisors under the Investment Management Agreement for each Fund, is the responsibility of the Board. There are currently ten members of the Board, one of whom is an “interested person” (as defined in the 1940 Act) and nine of whom are not interested persons (the “independent board members”). The names and business addresses of the board members and officers of the Acquiring Fund and their principal occupations and other affiliations during the past five years are set forth under “Management” in the Statement of Additional Information for the Acquiring Fund and are incorporated herein by reference.

Distribution, Purchase, Redemption, Exchange of Shares and Dividends

The Acquired Fund offers four classes of shares: Class A, Class C, Class R3 and Class I shares. The Acquiring Fund offers five classes of shares: Class A, Class B, Class C, Class R3 and Class I shares. You may purchase, redeem or exchange shares of the Funds on any business day, which is any

16

day the New York Stock Exchange is open for business. You may purchase, redeem or exchange shares of each Fund through a financial advisor or other financial intermediary or directly from such Fund. No initial sales charge or contingent deferred sales charges will be imposed on shares of the Acquiring Fund received or shares of the Acquired Fund exchanged in connection with the Reorganization. Any purchases of any class of shares made after the Reorganization will be subject to the standard fee structure applicable to such class. Class B shares of the Acquiring Fund are available only through exchanges and dividend reinvestments by current Class B shareholders and are not offered through this Proxy Statement/Prospectus. The Acquiring Fund’s initial and subsequent investment minimums generally are set forth in the following table, although the Fund may reduce or waive the minimums in some cases. The Acquired Fund’s investment minimums for Class A, Class C, Class R3 and Class I shares are identical to the Acquiring Fund’s investment minimums for Class A, Class C, Class R3 and Class I shares, respectively.

| | | | | | |

| | | Class A and Class C | | Class R3 | | Class I |

| | | |

| Eligibility and Minimum Initial Investment | | $3,000 for all accounts except: • $2,500 for Traditional/Roth IRA accounts. • $2,000 for Coverdell Education Savings Accounts. • $250 for accounts opened through fee-based programs. • No minimum for retirement plans. | | Available only through certain retirement plans. No minimum. | | Available only through fee-based programs and to other limited categories of investors as described in the prospectus. $100,000 for all accounts except: • $250 for clients of financial intermediaries and family offices that have accounts holding Class I shares with an aggregate value of at least $100,000 (or that are expected to reach this level). • No minimum for certain other categories of eligible investors as described in the prospectus. |

| Minimum Additional Investment | | $100 | | No minimum. | | No minimum. |

For a complete description of purchase, redemption and exchange options, see the section of the Acquiring Fund’s Prospectus entitled “How You Can Buy and Sell Shares,” and “General Information,” and the section of the Acquiring Fund’s Statement of Additional Information entitled “Purchase and Redemption of Fund Shares.”

The Acquiring Fund normally declares and pays dividends from net investment income quarterly. The Acquired Fund’s dividends from net investment income, if any, are normally declared and paid annually. Each Fund declares and pays any taxable capital gains or other taxable distributions once a year at year end. If the Reorganization is approved by the shareholders of the Acquired Fund, the Acquired Fund intends to distribute to its shareholders, prior to the closing of the Reorganization, all its net investment income and net capital gains, if any, for the period ending on the Closing Date. Due to the Acquired Fund’s capital loss carryforwards, a net capital gain distribution is not expected. However, in light of realized capital gains in the Acquiring Fund’s portfolio that may not be distributed prior to the Reorganization, and in light of unrealized capital gains currently in the Acquiring Fund’s portfolio, Acquired Fund shareholders may be subject to higher capital gain distributions in the future than they would have been absent the Reorganization. See “Material Federal Income Tax Consequences” below.

17

Tax Information

The Funds’ distributions are taxable and will generally be taxed as ordinary income or capital gains.

Payments to Broker-Dealers and Other Financial Intermediaries

If you purchase shares of a Fund through a broker-dealer or other financial intermediary (such as a bank or financial advisor), the Fund, its distributor or its investment adviser may pay the intermediary for the sale of Fund shares and related services. These payments may create a conflict of interest by influencing the broker-dealer or other financial intermediary and your salesperson to recommend the Fund over another investment. Ask your financial advisor or visit your financial intermediary’s website for more information.

Further Information

Additional information concerning the Acquiring Fund and Acquired Fund is contained in this Proxy Statement/Prospectus and additional information regarding the Acquiring Fund is contained in the accompanying Acquiring Fund prospectus. The cover page of this Proxy Statement/Prospectus describes how you may obtain further information.

THE PROPOSED REORGANIZATION

The proposed Reorganization will be governed by the Agreement, a form of which is attached as Appendix I. The Agreement provides that the Acquired Fund will transfer all its assets to the Acquiring Fund solely in exchange for the issuance of full and fractional voting shares of the Acquiring Fund and the assumption by the Acquiring Fund of all the liabilities of the Acquired Fund. The closing of the Reorganization will take place at the close of business on the Closing Date. The following discussion of the Agreement is qualified in its entirety by the full text of the Agreement.

The Acquired Fund will transfer all its assets to the Acquiring Fund, and in exchange, the Acquiring Fund will assume all the liabilities of the Acquired Fund and deliver to the Acquired Fund a number of full and fractional shares of the Acquiring Fund having a net asset value equal to the value of the assets of the Acquired Fund less the liabilities of the Acquired Fund assumed by the Acquiring Fund. At the designated time on the Closing Date as set forth in the Agreement, the Acquired Fund will distribute in complete liquidation of the Acquired Fund, pro rata to its shareholders of record, all Acquiring Fund shares received by the Acquired Fund. This distribution will be accomplished by the transfer of the Acquiring Fund shares credited to the account of the Acquired Fund on the books of the Acquiring Fund to open accounts on the share records of the Acquiring Fund in the name of the Acquired Fund shareholders, and representing the respective pro rata number of Acquiring Fund shares due such shareholders. All issued and outstanding shares of the Acquired Fund will simultaneously be canceled on the books of the Acquired Fund. As a result of the proposed Reorganization, each Acquired Fund Class A, Class C, Class R3 and Class I shareholder will receive a number of Acquiring Fund Class A, Class C, Class R3 and Class I shares, respectively, equal in value, as of the close of regular trading on the New York Stock Exchange on the Closing Date, to the value of the Acquired Fund Class A, Class C, Class R3 and Class I shares surrendered by such shareholder.

18

The Board has determined that the proposed Reorganization is in the best interests of each Fund and that the interests of existing shareholders will not be diluted as a result of the transactions contemplated by the Agreement.

The consummation of the Reorganization is subject to the terms and conditions of, and the representations and warranties being true as set forth in, the Agreement. The Agreement may be terminated by mutual agreement of the Funds. In addition, either Fund may at its option terminate the Agreement at or before the Closing Date due to (i) a breach by any other party of any representation, warranty, or agreement to be performed at or before the Closing Date, if not cured within 30 days, (ii) a condition precedent to the obligations of the terminating party that has not been met and it reasonably appears that it will not or cannot be met, or (iii) a determination by the Board that the consummation of the transactions contemplated by the Agreement is not in the best interests of a Fund.